CJSC Moscow Efes Brewery - data.cbonds.info

113

October 2007 CJSC "Moscow Efes Brewery" Placement price: at par (RUR1,000) RUR 6 bln series 01 coupon bonds with a tenor of 3 years Issued by Closed Joint Stock Company "Moscow Efes Brewery", Guaranteed by Opened Joint Stock Company "Brewery Union "Krasny Vostok Solodovpivo" Information Memorandum LEAD MANAGERS CJSC "Moscow Efes Brewery", established in accordance with Russian law (hereafter the "Issuer") is to place 6 mln coupon, nonconvertible series 01 doc umentary bearer bonds with required centralized storage with par values of RUR1,000 each, with six coupon payments and maturity on the 1,092nd day after the start of placement date, with the par value of RUR6 bln and cumulative coupon payments on the bonds with a surety by OJSC "Brewery Union "Krasny Vostok Solodovpivo" (hereafter the "Surety") (hereafter the "Bonds") in accordance with the Decision of issuance and the Prospectus on securities regis tered with the Federal Financial Markets Service (hereafter the "FFMS") on July 5th, 2007 (hereafter the "Decision of Issue" and "Securities Prospectus", respectively) with state registration number 40100217H. The interest rate for the first coupon is to be set at auction (hereafter the "Auction") in an annual percentage on the date of the start of placement, to be conducted on MICEX (hereafter the "Exchange", "MICEX"). The auction is to take place in accordance with the regulations and terms of the Exchange, which are in force on the date of the Bond placement. The rate for the first coupon is to be fixed until the first put option or until maturity of the Bonds, depending on the decision to use a put option, about which the Issuer will provide information on the day of the announcement of the placement date. The funds raised from the Bonds placement are to be used for investment purposes and to finance working capital (see "Use of Proceeds"). Issuance is made with a single certificate (hereafter the "Certificate"), which is required to be stored at National Depositary Center (here after the "Depositary"). Additional certificates are not to be given to bondholders. Bondholders do not have the right to demand to be given the certificates. The list and attestation of rights to the Bonds, and the list and attestation of transfer of the Bonds, including encumbrance of the Bonds, are carried out by the Depositary during its fulfillment of its functions as a Depositary, and by depositaries that are deponents of the Depositary (hereafter collectively "Depositaries"). Rights of ownership of the Bonds are to be confirmed with written notices given by the Depositary and the Depositaries to the Bondholders.

Transcript of CJSC Moscow Efes Brewery - data.cbonds.info

October 2007

CJSC "Moscow Efes Brewery"

Placement price: at par (RUR1,000)

RUR 6 bln series 01 coupon bonds with a tenor of 3 years

Issued by Closed Joint Stock Company "Moscow Efes Brewery",Guaranteed by Opened Joint Stock Company "Brewery Union "Krasny Vostok � Solodovpivo"

I n f o r m a t i o n M e m o r a n d u m

L E A D M A N A G E R S

CJSC "Moscow Efes Brewery", established in accordance with Russian law (hereafter the "Issuer") is to place 6 mln coupon, non�convertible series 01 doc�umentary bearer bonds with required centralized storage with par values of RUR1,000 each, with six coupon payments and maturity on the 1,092nd day afterthe start of placement date, with the par value of RUR6 bln and cumulative coupon payments on the bonds with a surety by OJSC "Brewery Union "KrasnyVostok � Solodovpivo" (hereafter the "Surety") (hereafter the "Bonds") in accordance with the Decision of issuance and the Prospectus on securities regis�tered with the Federal Financial Markets Service (hereafter the "FFMS") on July 5th, 2007 (hereafter the "Decision of Issue" and "Securities Prospectus",respectively) with state registration number 4�01�00217�H. The interest rate for the first coupon is to be set at auction (hereafter the "Auction") in an annualpercentage on the date of the start of placement, to be conducted on MICEX (hereafter the "Exchange", "MICEX"). The auction is to take place in accordancewith the regulations and terms of the Exchange, which are in force on the date of the Bond placement. The rate for the first coupon is to be fixed until the firstput option or until maturity of the Bonds, depending on the decision to use a put option, about which the Issuer will provide information on the day of theannouncement of the placement date. The funds raised from the Bonds placement are to be used for investment purposes and to finance working capital (see"Use of Proceeds"). Issuance is made with a single certificate (hereafter the "Certificate"), which is required to be stored at National Depositary Center (here�after the "Depositary"). Additional certificates are not to be given to bondholders. Bondholders do not have the right to demand to be given the certificates.The list and attestation of rights to the Bonds, and the list and attestation of transfer of the Bonds, including encumbrance of the Bonds, are carried out by theDepositary during its fulfillment of its functions as a Depositary, and by depositaries that are deponents of the Depositary (hereafter collectively"Depositaries"). Rights of ownership of the Bonds are to be confirmed with written notices given by the Depositary and the Depositaries to the Bondholders.

CJSC "Moscow Efes Brewery" Information Memorandum

1October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

2

Disclaimer

THE INFORMATION CONTAINED IN THE MEMORANDUM GIVES A SHORT DESCRIPTION OF THE BASIC TERMS

AND CONDITIONS OF THE BOND ISSUE ("BASIC ISSUE TERMS"). THE BASIC TERMS ARE ENTIRELY CONTAINED IN

THE ISSUE PROSPECTUS, WHICH IS REGISTERED BY THE FEDERAL FINANCIAL MARKETS SERVICE. INVESTORS ARE

STRONGLY RECOMMENDED TO CONSIDER INFORMATION GIVEN IN THE PROSPECTUS WHILE MAKING DECISION

TO INVEST IN THE BONDS.

THE INFORMATION CONTAINED IN THE MEMORANDUM WAS PROVIDED BY CJSC "MOSCOW EFES BREWERY"

(HEREAFTER THE "ISSUER"). THE LEAD MANAGER, REPRESENTATIVES THEREOF, OR COMPANIES AFFILIATED

WITH THE LEAD MANAGERS AND/OR WITH COMPANY THAT HAVE PROVIDED INFORMATION, HAVE NOT

UNDERTAKEN A CHECK OF THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED IN THE

MEMORANDUM. THE LEAD MANAGERS DO NOT BEAR RESPONSIBILITY FOR THE COMPLETENESS OR ACCURA�

CY OF THE INFORMATION PROVIDED BY CJSC "MOSCOW EFES BREWERY". THIS MATERIAL AND THE INFORMA�

TION CONTAINED THEREIN ARE PURELY INFORMATIONAL AND CANNOT BE TREATED AS AN OFFER.

THE INFORMATION CONTAINED IN THE INFORMATIONAL MEMORANDUM IS NOT EXHAUSTIVE. ANY PARTY

CONSIDERING PURCHASING THE BONDS MUST UNDERTAKE ITS OWN ANALYSIS OF THE FINANCIAL CONDITION

OF THE ISSUER AND SURETY, AND OF THE BASIC CONDITIONS ON THE BASIS OF INFORMATION CONTAINED IN

THE ISSUE PROSPECTUS, PUBLISHED ON THE ISSUER'S SITE WWW.EFES.COM.RU.

ALL FORWARD LOOKING STATEMENTS REGARDING FUTURE EVENTS AND/OR ACTIONS, AND PROSPECTS OF

ECONOMIC ENVIRONMENT WHERE THE ISSUER OPERATES, INCLUDING FUTURE PLANS AND THE CERTAINTY OF

SPECIFIC EVENTS OCCURRING, EXPRESS OUR OPINION ON THE DAY OF PUBLICATION AND ARE SUBJECT TO

CHANGE WITHOUT PRIOR NOTICE.

THE LEAD MANAGERS DO NOT BEAR RESPONSIBILITY FOR ANALYSIS OF THE FINANCIAL AND/OR OTHER

INFORMATION ABOUT THE ISSUER AND SURETY, NOR FOR THE PROVISION OF ADDITIONAL INFORMATION.

EMPLOYEES OF THE LEAD MANAGER ARE NOT AUTHORIZED TO PROVIDE INFORMATION REGARDING THE

ISSUER AND/OR THE BONDS NOT CONTAINED IN THE MEMORANDUM.

THE DATE SHOWN ON THE FIRST PAGE OF THE MEMORANDUM DOES NOT INDICATE THAT INFORMATION CON�

TAINED IN THE MEMORANDUM IS COMPLETE AND/OR ACCURATE ON THAT DATE. NIETHER LEAD MANAGER

NOR ISSUER ARE RESPONSIBLE FOR UPDATING THE INFORMATION CONTAINED IN THE MEMORANDUM.

THIS MEMORANDUM IS NOT INTENDED FOR DISTRIBUTION IN THE US, UK, CANADA, AUSTRALIA AND

JAPAN.

THIS MEMORANDUM IS NOT AN OFFER OF SECURITIES FOR SALE IN THE ABOVEMENTIONED COUNTRIES. THE

BONDS CANNOT BE PLACED OR SOLD IN THE US WITHOUT REGISTRATION AND CANNOT BE EXEMPT FROM REG�

ISTRATION IN ACCORDANCE WITH THE US SECURITY ACT OF 1933 (WITH AMENDMENTS). THE ISSUER HAS NO

INTENTION TO REGISTER ANY PART OF THIS PLACEMENT OR TO OFFER ANY PUBLIC PLACEMENT IN THE US.

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

Table of contents

EXECUTIVE SUMMARY ..........................................................................................................5Issuer and surety.................................................................................................................5Strategy...............................................................................................................................5Market share.......................................................................................................................6Selected financials ..............................................................................................................6Investment highlights..........................................................................................................7

TERMS AND CONDITIONS OF BOND ISSUE .......................................................................8USE OF PROCEEDS ..............................................................................................................10LEGAL STRUCTURE ..............................................................................................................11STRATEGY ............................................................................................................................14COMPETITIVE ENVIRONMENT............................................................................................15

Global industry overview .................................................................................................15Russian beer market .........................................................................................................16Major competitors ............................................................................................................19Competitive advantages....................................................................................................20

SALES, MARKETING AND DISTRIBUTION..........................................................................22Marketing .........................................................................................................................22Sales..................................................................................................................................23Distribution ......................................................................................................................24Customers .........................................................................................................................25

MANAGEMENT AND EMPLOYEES.......................................................................................26OPERATIONS .......................................................................................................................30

History..............................................................................................................................30Production facilities..........................................................................................................30The brewing process .........................................................................................................31Raw materials procurement..............................................................................................32Research and development...............................................................................................33Intellectual property rights ...............................................................................................33Legal matters ....................................................................................................................33

CAPITAL EXPENDITURES .....................................................................................................34SELECTED COMBINED FINANCIAL DATA ..........................................................................35

Profit and loss statement ..................................................................................................35Balance sheet....................................................................................................................38

RISK FACTORS......................................................................................................................41Country risks.....................................................................................................................41Industry risks ....................................................................................................................43Issuer's risks......................................................................................................................44

BOND DESCRIPTION...........................................................................................................47TAX CONSIDERATIONS.......................................................................................................53APPENDIX 1: AUDITED CONSOLIDATED FINANCIAL STATEMENTS OF MOSCOW

EFES BREWERY FOR THE YEAR ENDED 31st OF DECEMBER, 2005 AND 2006 PREPARED IN ACCORDANCE WITH IFRS ..................................58

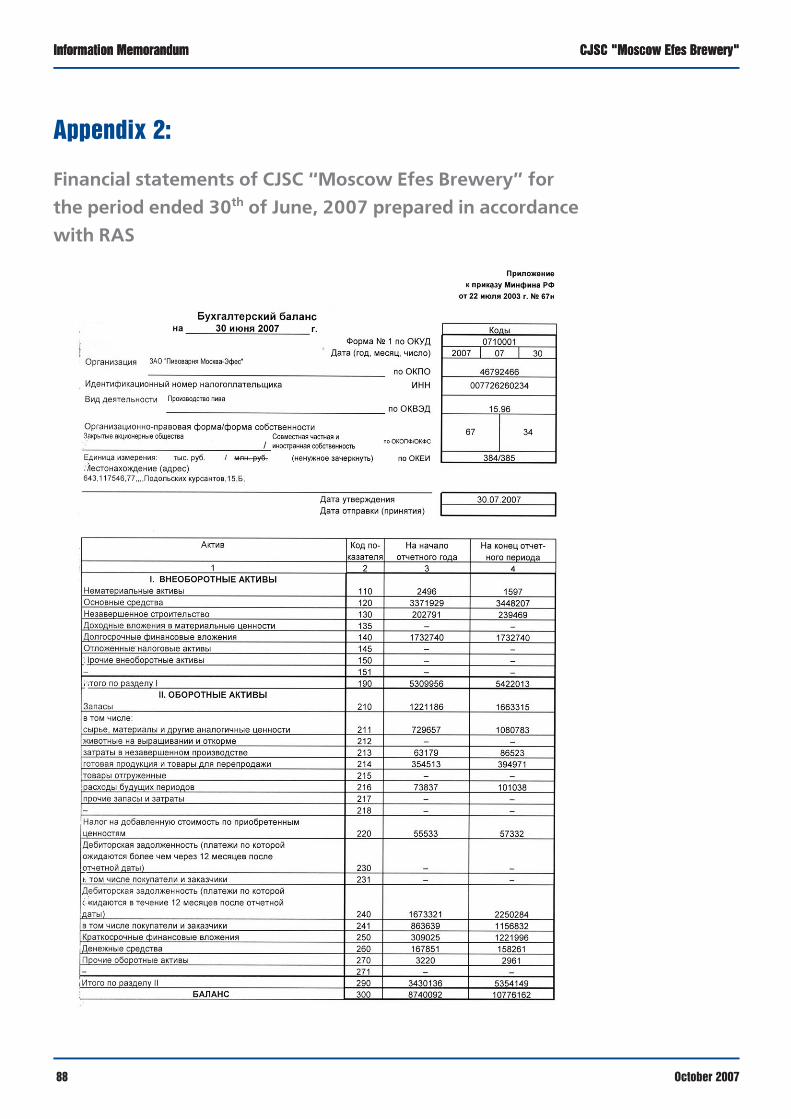

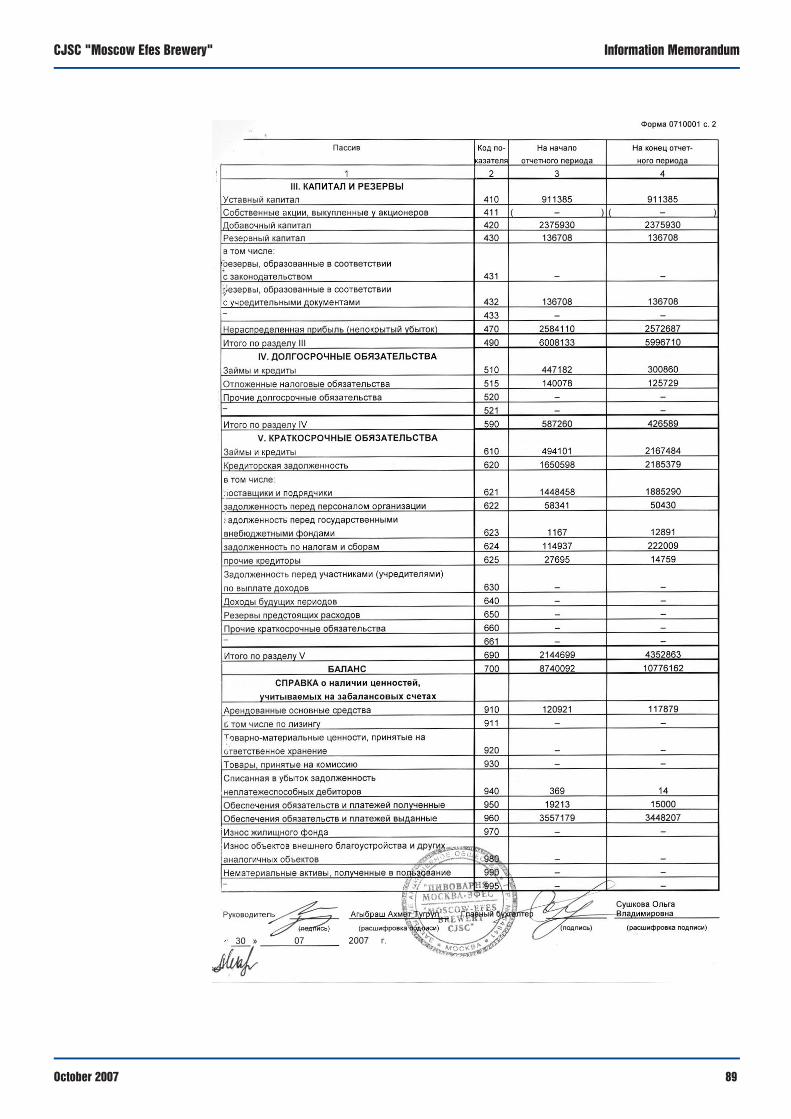

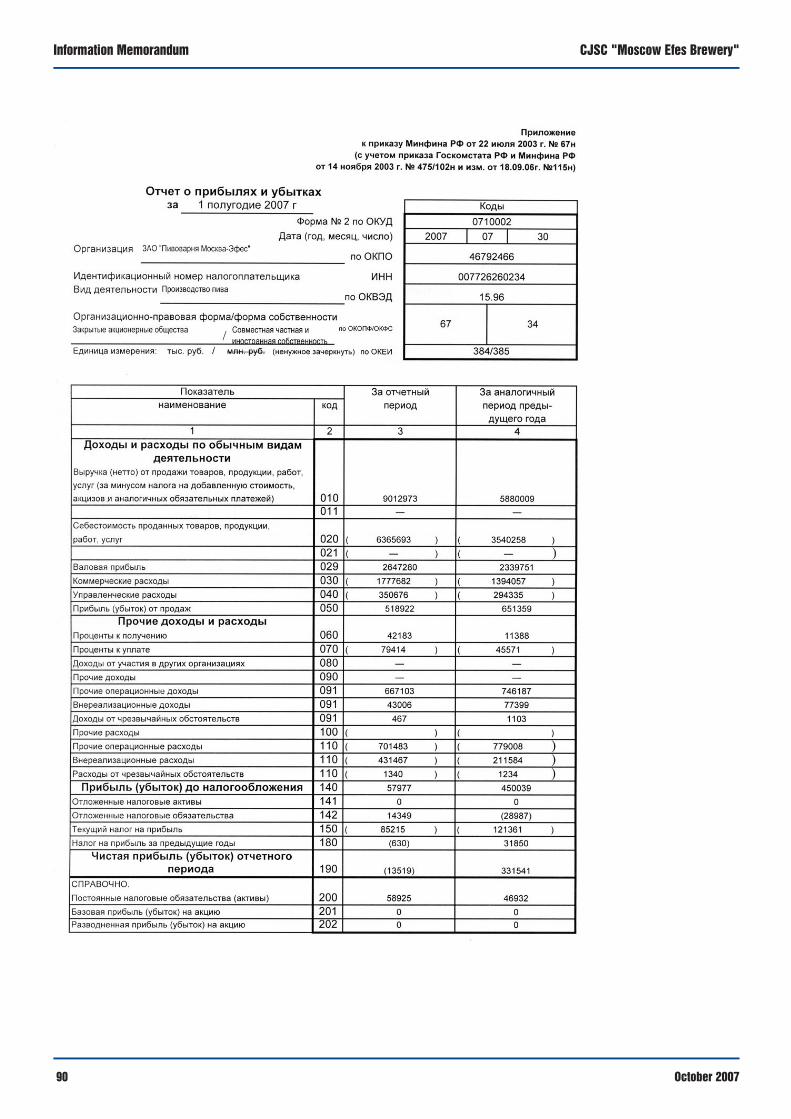

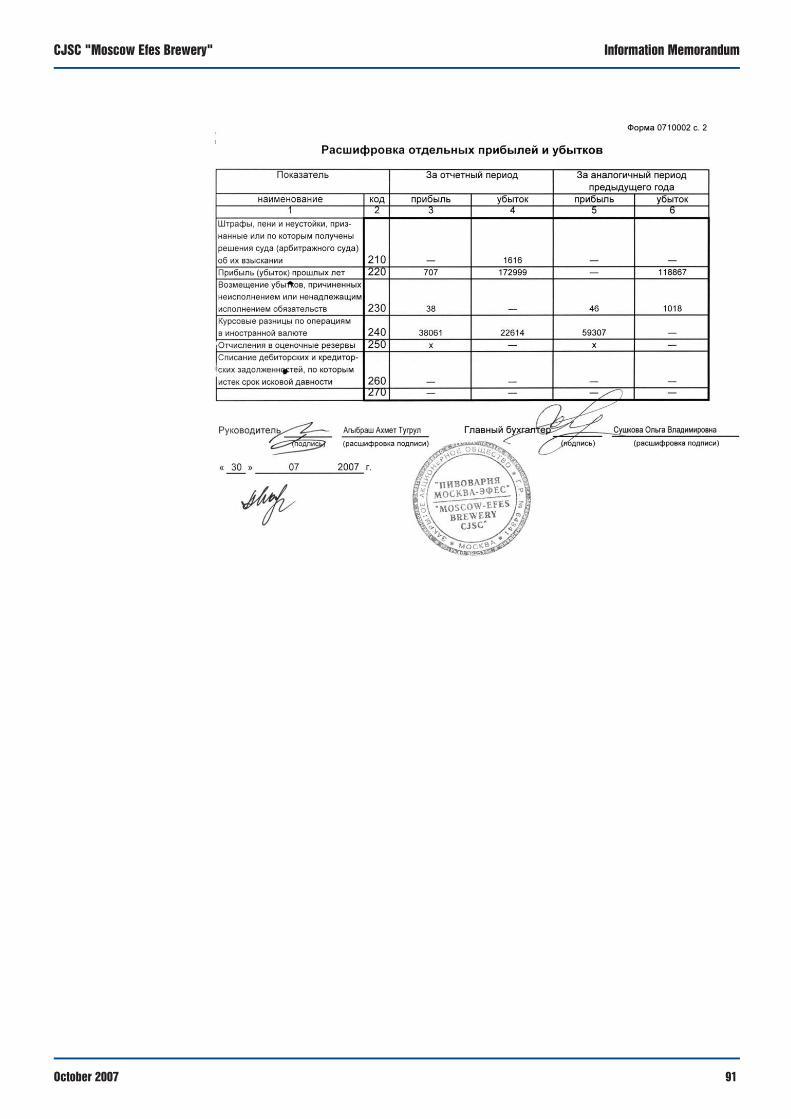

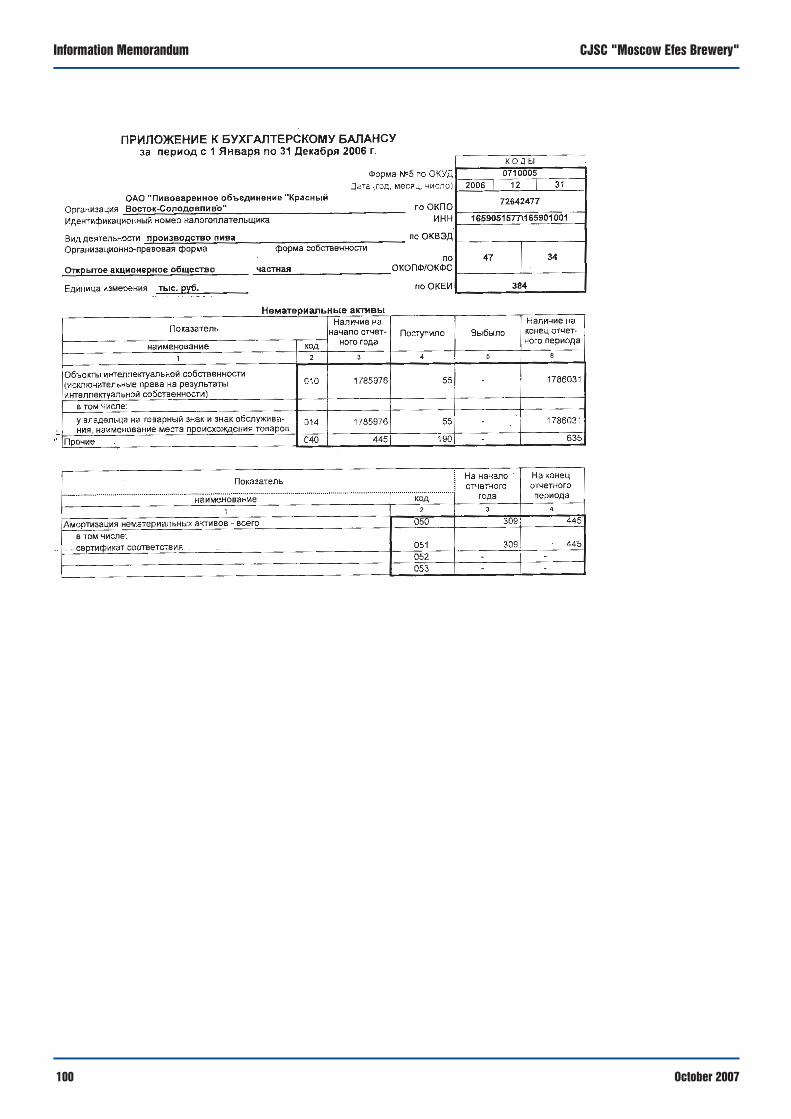

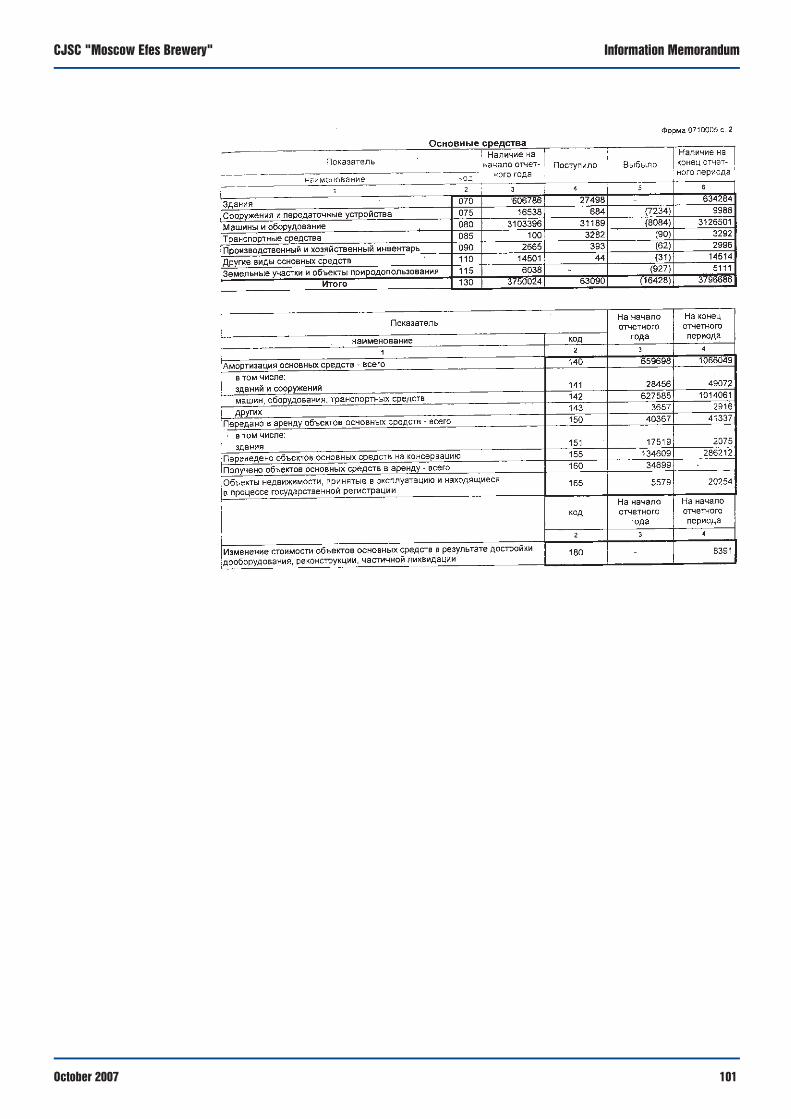

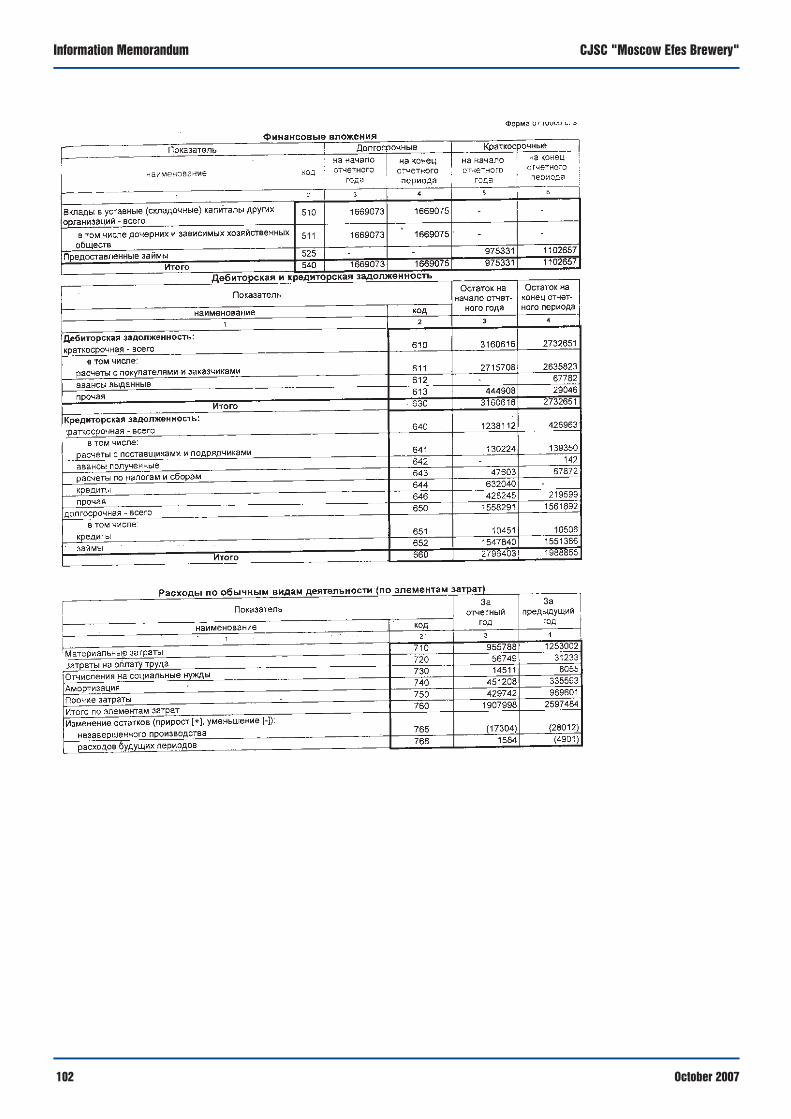

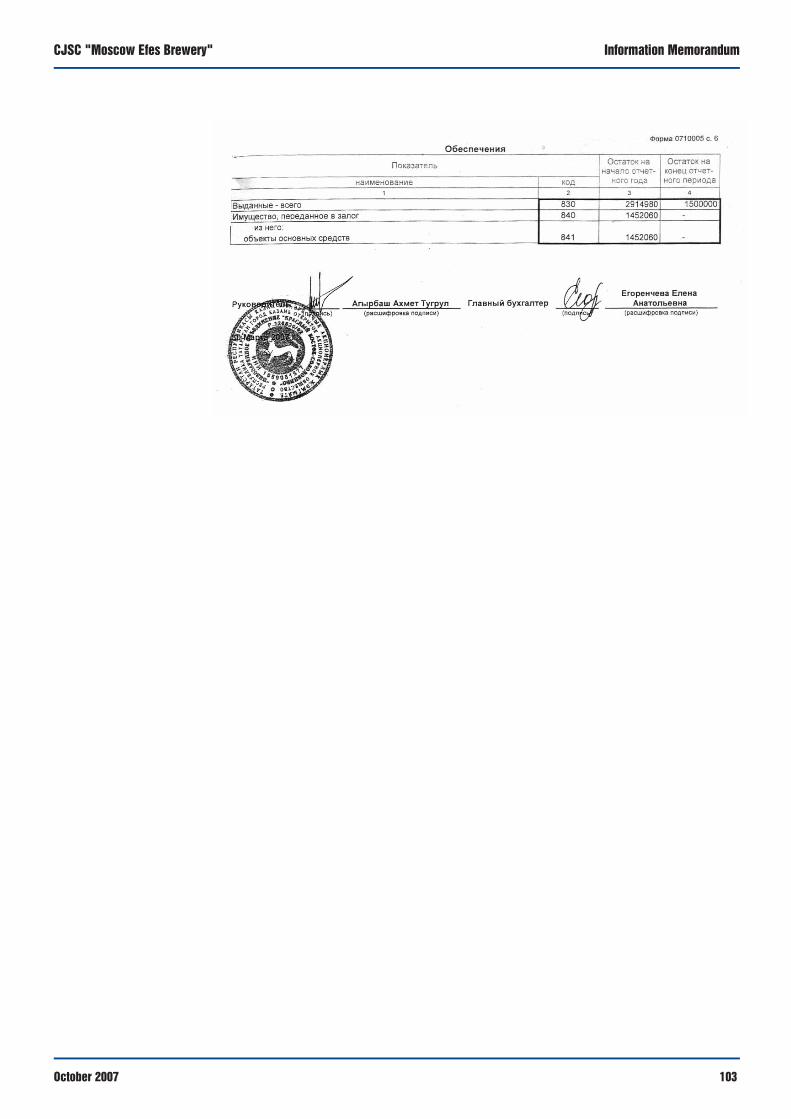

APPENDIX 2: FINANCIAL STATEMENTS OF CJSC ìMOSCOW EFES BREWERYî FOR THE PERIOD ENDED 30th OF JUNE, 2007 PREPARED IN ACCORDANCEWITH RAS ......................................................................................................88

3October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

4

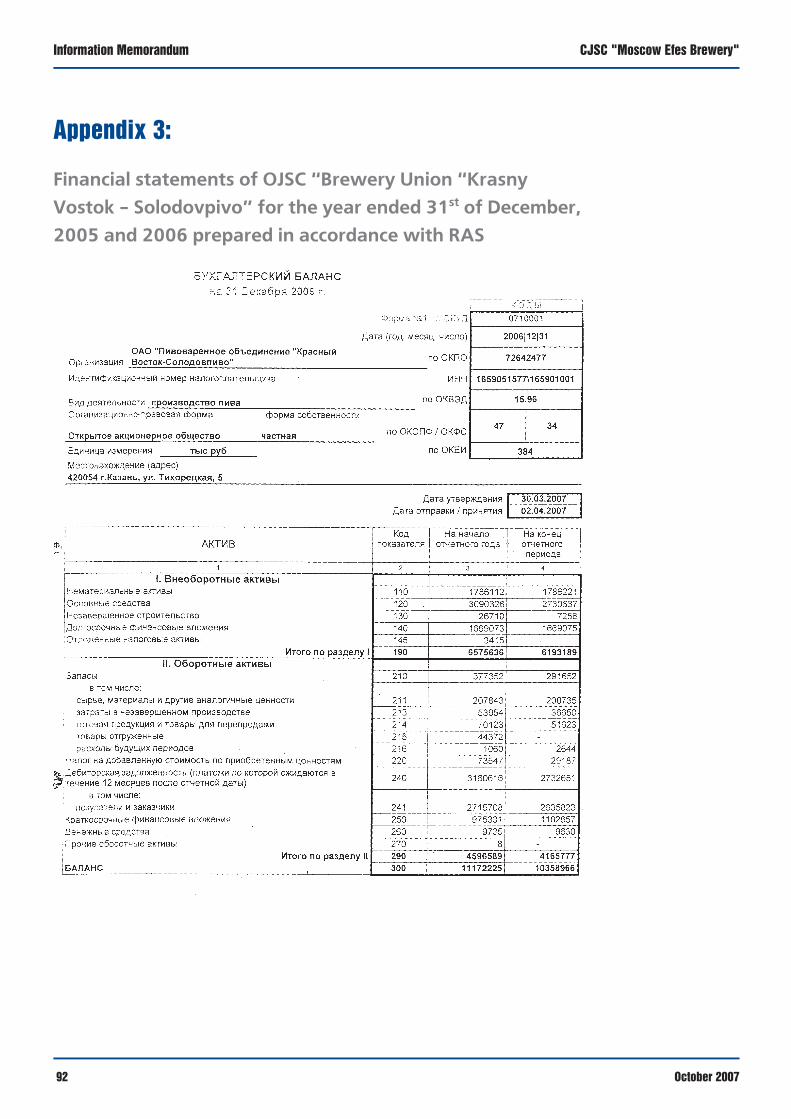

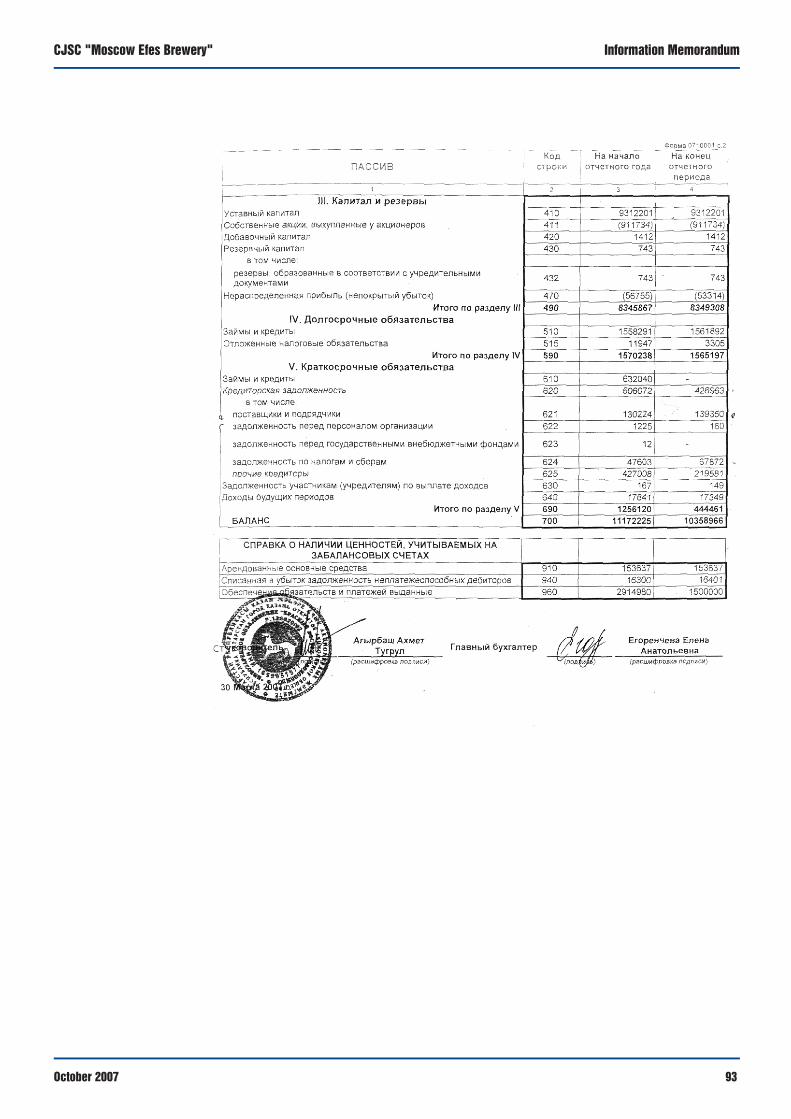

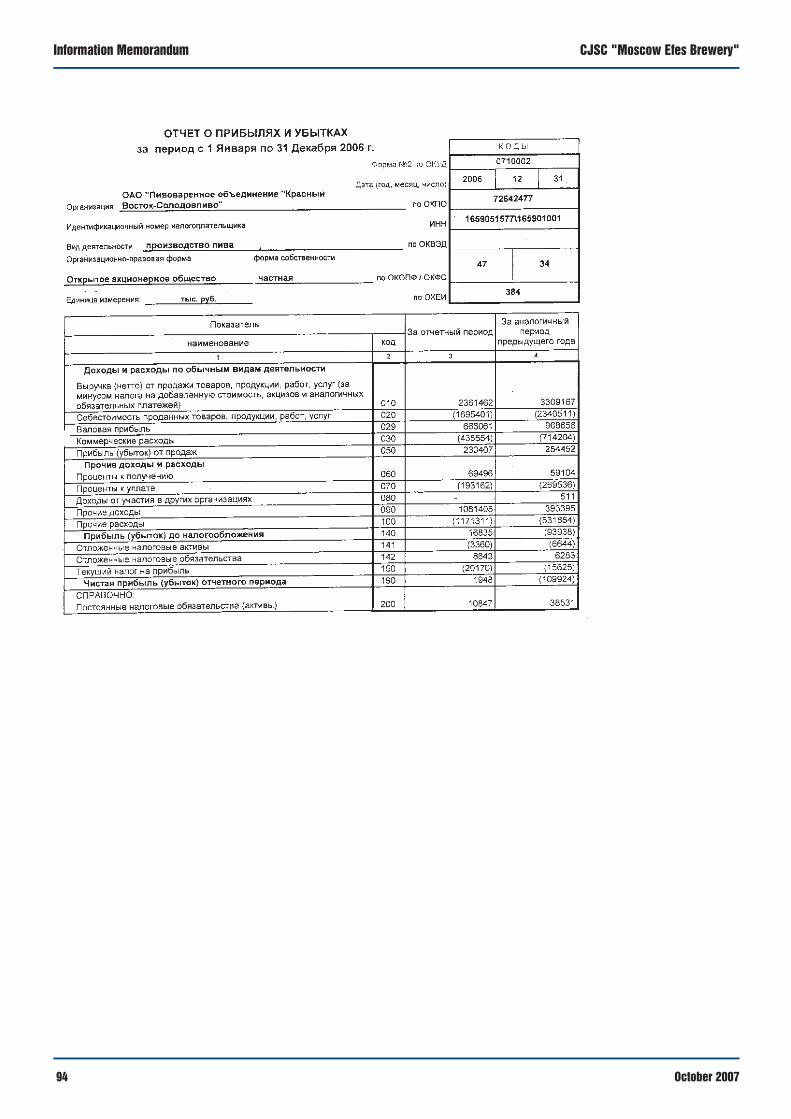

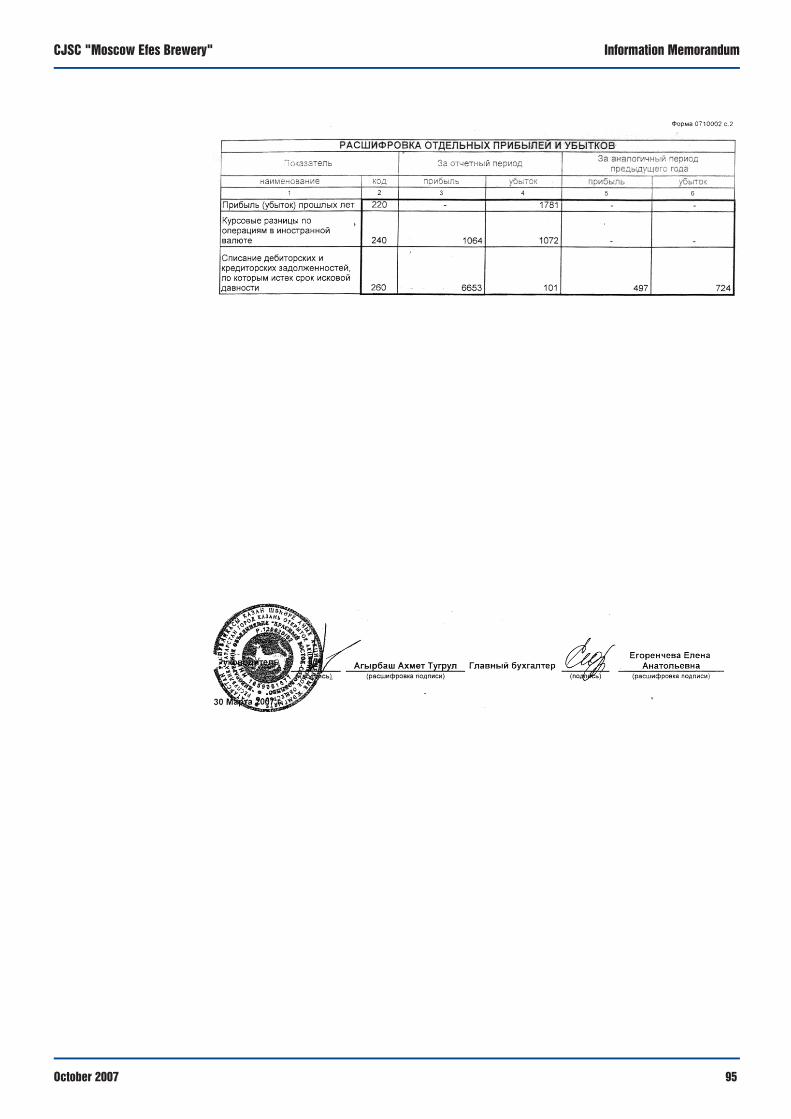

APPENDIX 3: FINANCIAL STATEMENTS OF OJSC "BREWERY UNION � KRASNYVOSTOK � SOLODOVPIVO" FOR THE YEAR ENDED 31st OF DECEMBER, 2005 AND 2006 PREPARED IN ACCORDANCE WITH RAS..................................92

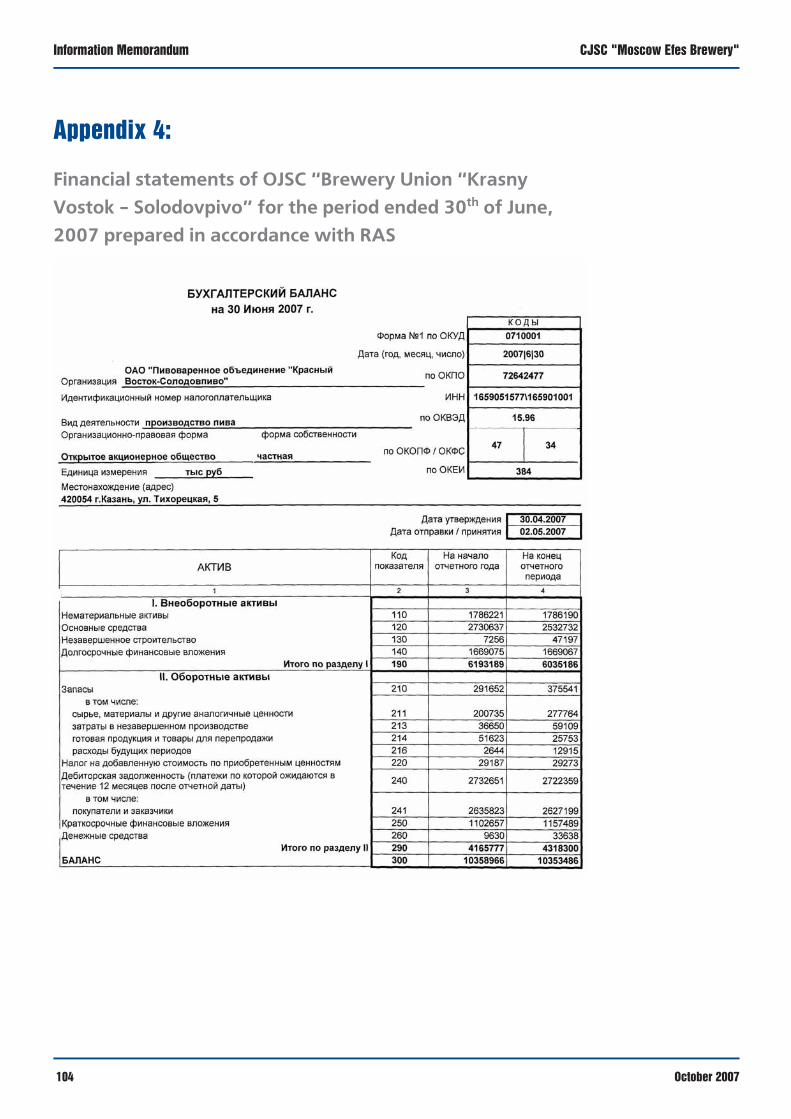

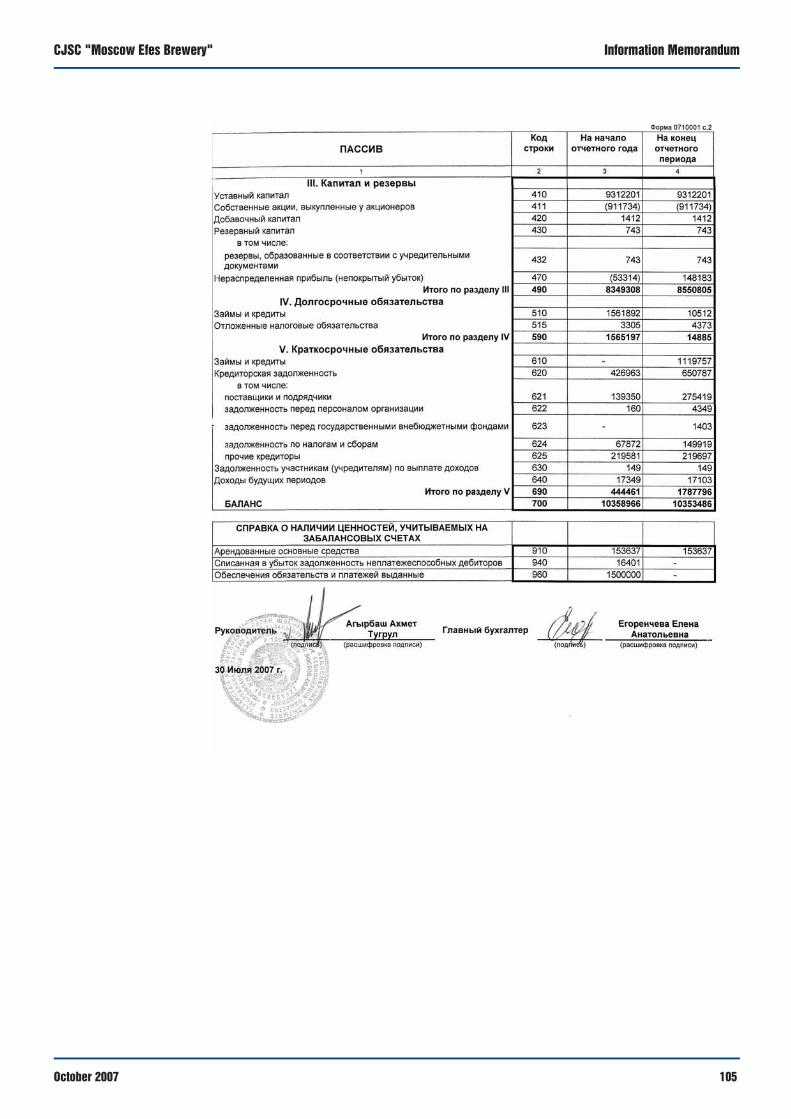

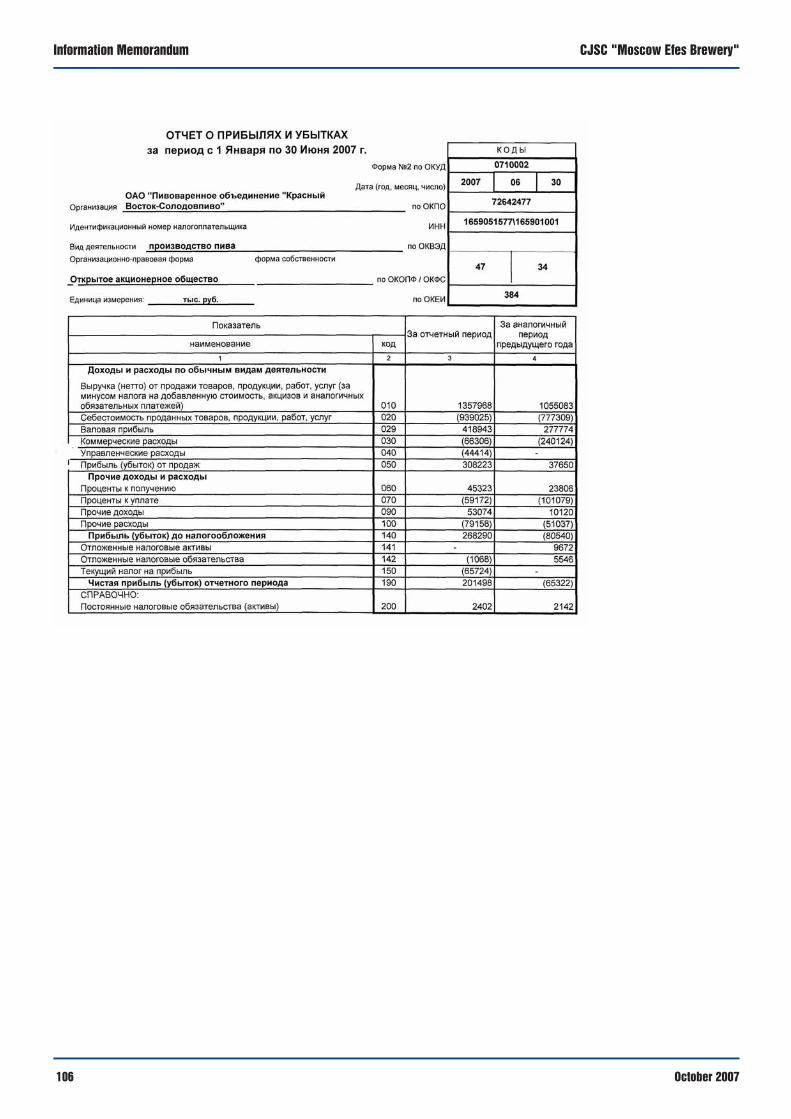

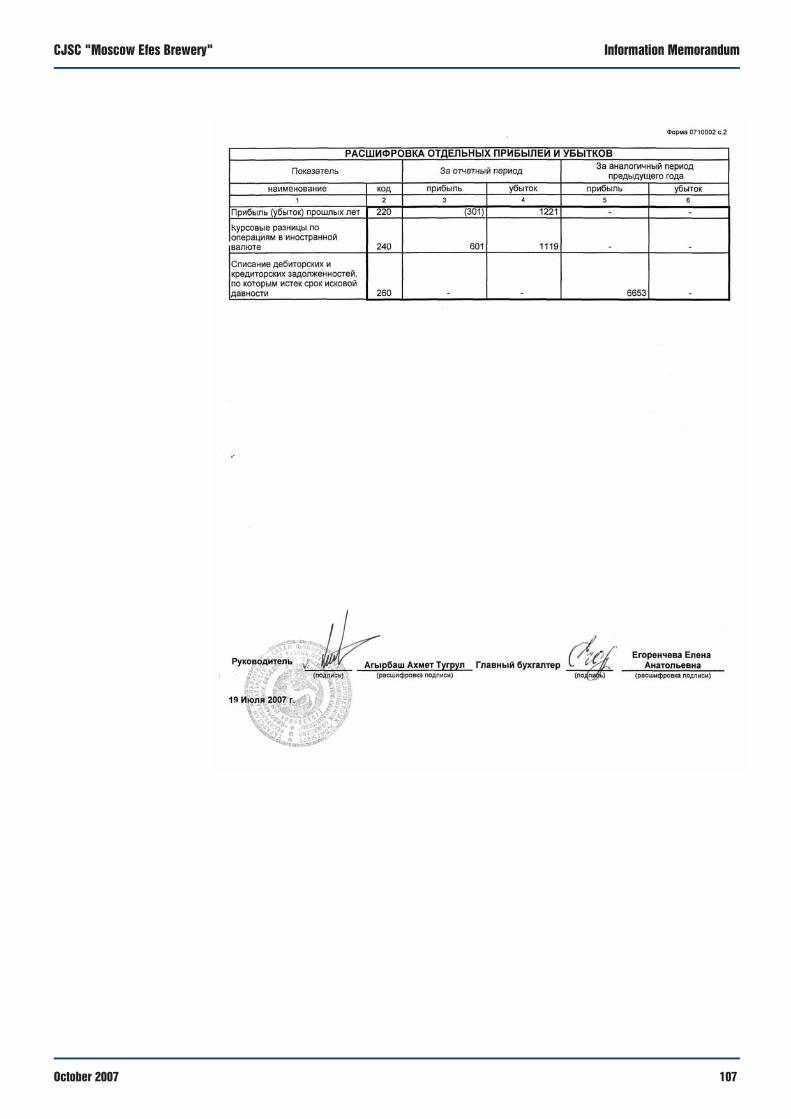

APPENDIX 4: FINANCIAL STATEMENTS OF OJSC "BREWERY UNION � KRASNY VOSTOK � SOLODOVPIVO" FOR THE PERIOD ENDED 30th OF JUNE, 2007 PREPARED IN ACCORDANCE WITH RAS..................104

APPENDIX 5: SURETYSHIP AGREEMENT...........................................................................108

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

Executive summary

Issuer and Surety

CJSC "Moscow Efes Brewery" and its subsidiaries ("Efes Moscow") and OJSC "Brewing Union"Krasny Vostok � Solodovpivo" and its subsidiaries ("Krasny Vostok Goup", "KV Group") jointlyconstitute Efes Russia, i.e. business division of Efes Breweries International N.V. ("EBI"), engagedin production and sales of beer products in Russia. Together with Efes Russia EBI controls oper�ations of brewery facilities in Kazakhstan, Moldova and Serbia.

EBI is a majority�owned subsidiary of Anadolu Efes Biraclllk ve Malt Sanayii A.S. ("AnadoluEfes"), which controls 70.2 per cent of EBI, while the remaining 29.8 per cent is publicly held(traded on the London Stock Exchange). Anadolu Efes together with its subsidiaries and affili�ates produces and markets beer, malt and soft drinks across a geography including Turkey,Russia, other CIS countries, South�Eastern Europe and the Middle East. Anadolu Efes' beer andsoft drink interests include 15 breweries, six malteries and 12 Coca�Cola bottling facilities in 12 countries. Anadolu Efes's current annual brewing capacity is approximately 33.7 mln hec�tolitres, its malting capacity is approximately 236,500 tonnes and its Coca�Cola bottling capac�ity is approximately 573 mln unit cases. Anadolu Efes generated net sales on a combined basisof US$1.2 bln and US$1.8 bln in 2005 and 2006, respectively.

As of the year ended 31st of December, 2006 Efes Russia accounted for 79 per cent of EBI'ssales and 28 per cent of Anadolu Efes sales on a consolidated basis. Efes Russia's beer interestsinclude five breweries and four malteries with annual brewing capacity of approximately 20.2 mlnhectolitres and malting capacity of approximately 139,000 tonnes. Efes Russia generated netsales on a combined basis of US$369 mln, US$514 mln and US$308 mln in 2005, 2006 and1H2007, respectively.

Strategy

Efes Russia intends to pursue a strategy aimed at increasing revenue and profits, including:

1. Capitalize on the growth of the beer market in Russia. Viewing Russian beer market as oneof the most prospective for the development of beverage operations, Efes Russia intends tomaintain its position among the leading brewers in Russia and support demand for its productsby:

■ increasing the production capacity of its existing brewing facilities through the installation ofadditional production lines to continue serving areas with demonstrated growth potential;

■ establishing additional brewing facilities in Russia, through strategic acquisitions or green�field projects;

■ expanding Efes Russia's distribution system through a combination of direct order�taking inhigh density population areas and fostering preferential relationships with authorized deal�ers in other geographic areas.

2. Focus on high margin or growing segments. Efes Russia's product strategy is to focus on themost profitable, largest segments and/or those segments with the highest growth potential in theRussian beer market. To this end, Efes Russia seeks to have a brand portfolio that comprehen�sively covers all abovementioned beer segments.

5October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

6

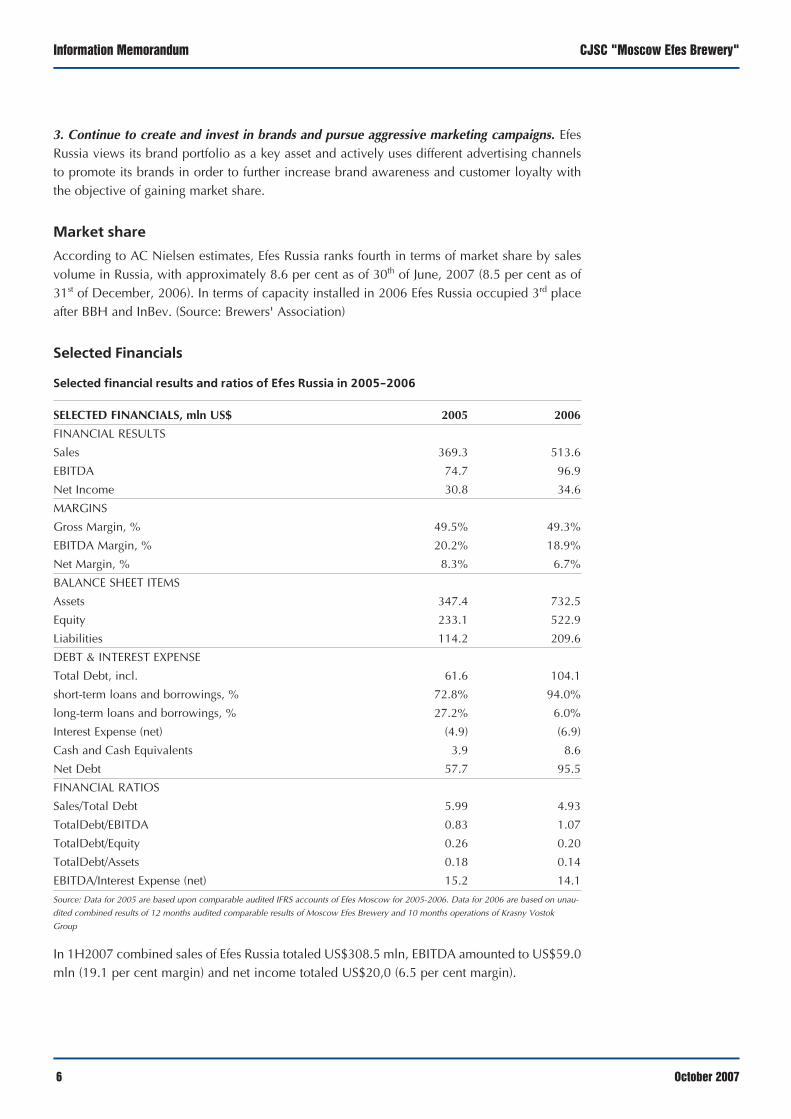

3. Continue to create and invest in brands and pursue aggressive marketing campaigns. EfesRussia views its brand portfolio as a key asset and actively uses different advertising channelsto promote its brands in order to further increase brand awareness and customer loyalty withthe objective of gaining market share.

Market share

According to AC Nielsen estimates, Efes Russia ranks fourth in terms of market share by salesvolume in Russia, with approximately 8.6 per cent as of 30th of June, 2007 (8.5 per cent as of31st of December, 2006). In terms of capacity installed in 2006 Efes Russia occupied 3rd placeafter BBH and InBev. (Source: Brewers' Association)

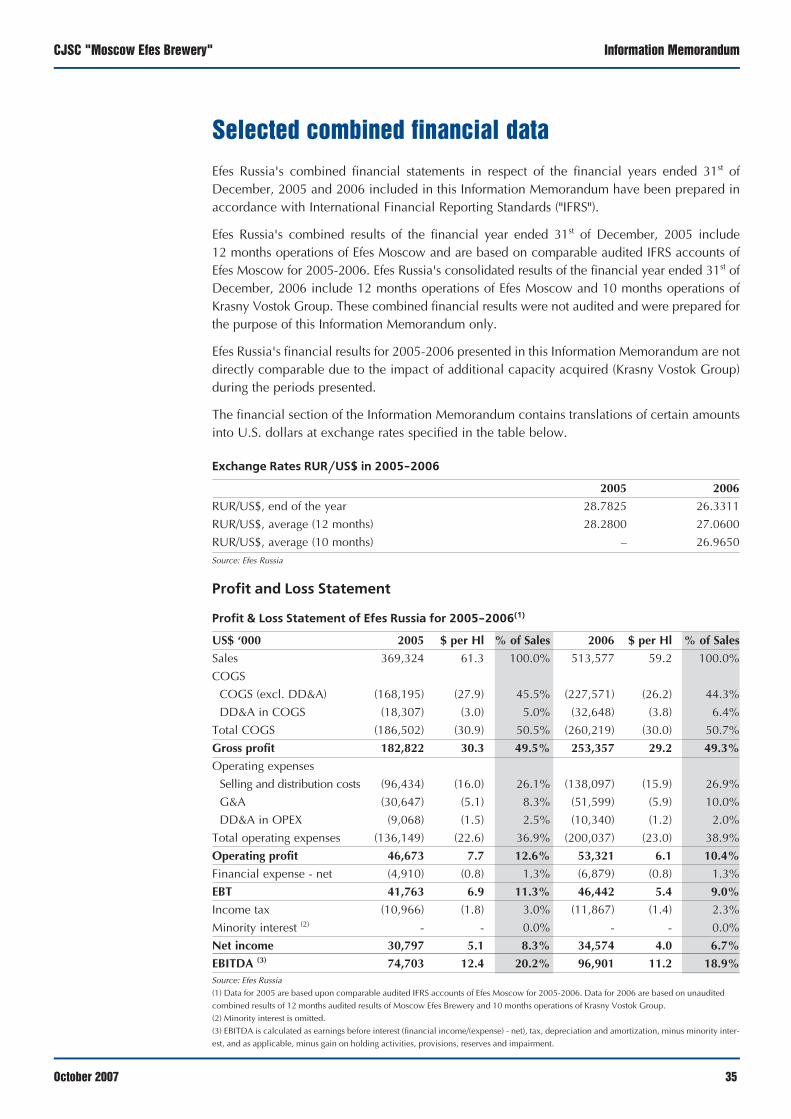

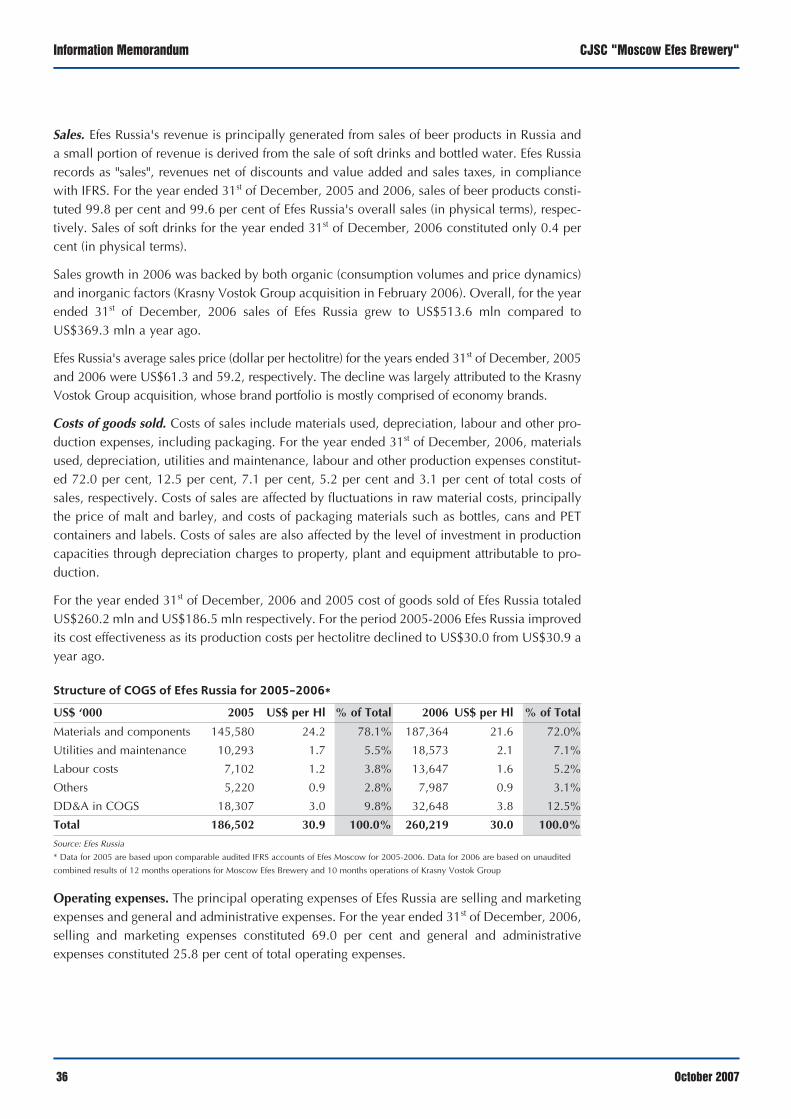

Selected Financials

Selected financial results and ratios of Efes Russia in 2005�2006

SELECTED FINANCIALS, mln US$ 2005 2006

FINANCIAL RESULTS

Sales 369.3 513.6

EBITDA 74.7 96.9

Net Income 30.8 34.6

MARGINS

Gross Margin, % 49.5% 49.3%

EBITDA Margin, % 20.2% 18.9%

Net Margin, % 8.3% 6.7%

BALANCE SHEET ITEMS

Assets 347.4 732.5

Equity 233.1 522.9

Liabilities 114.2 209.6

DEBT & INTEREST EXPENSE

Total Debt, incl. 61.6 104.1

short�term loans and borrowings, % 72.8% 94.0%

long�term loans and borrowings, % 27.2% 6.0%

Interest Expense (net) (4.9) (6.9)

Cash and Cash Equivalents 3.9 8.6

Net Debt 57.7 95.5

FINANCIAL RATIOS

Sales/Total Debt 5.99 4.93

TotalDebt/EBITDA 0.83 1.07

TotalDebt/Equity 0.26 0.20

TotalDebt/Assets 0.18 0.14

EBITDA/Interest Expense (net) 15.2 14.1

Source: Data for 2005 are based upon comparable audited IFRS accounts of Efes Moscow for 2005�2006. Data for 2006 are based on unau�

dited combined results of 12 months audited comparable results of Moscow Efes Brewery and 10 months operations of Krasny Vostok

Group

In 1H2007 combined sales of Efes Russia totaled US$308.5 mln, EBITDA amounted to US$59.0mln (19.1 per cent margin) and net income totaled US$20,0 (6.5 per cent margin).

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

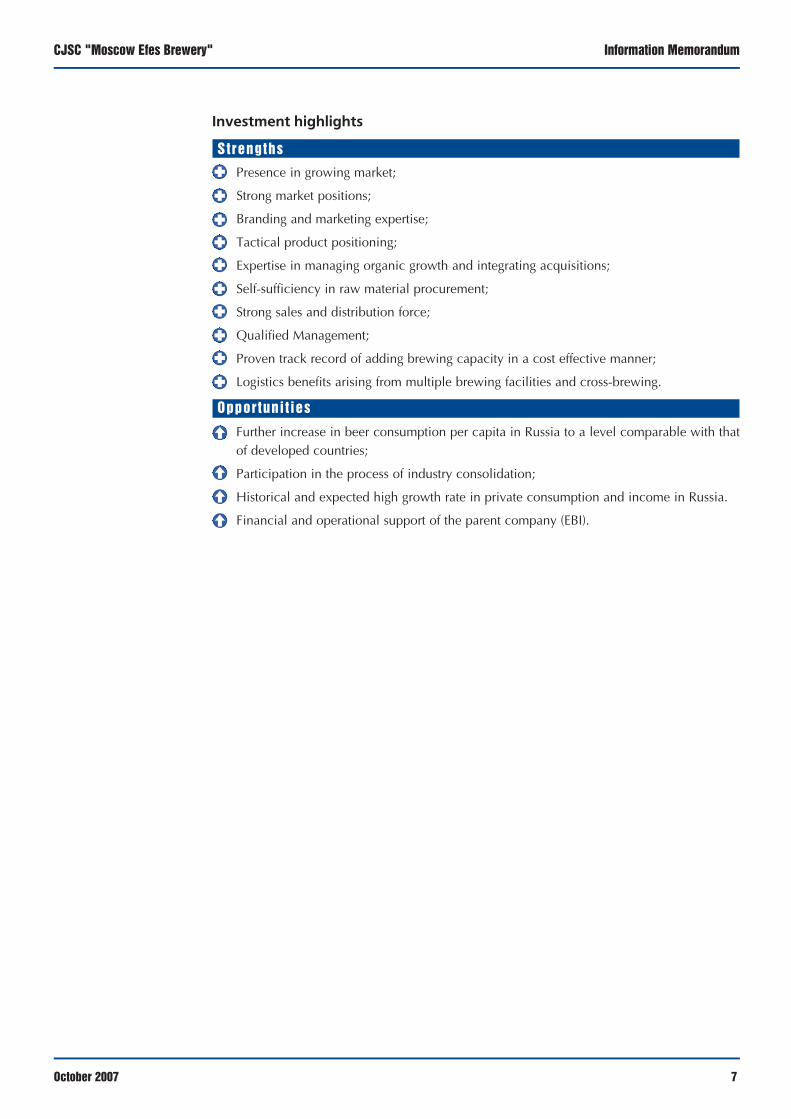

Investment highlights

Strengths

Presence in growing market;

Strong market positions;

Branding and marketing expertise;

Tactical product positioning;

Expertise in managing organic growth and integrating acquisitions;

Self�sufficiency in raw material procurement;

Strong sales and distribution force;

Qualified Management;

Proven track record of adding brewing capacity in a cost effective manner;

Logistics benefits arising from multiple brewing facilities and cross�brewing.

Opportuni t ies

Further increase in beer consumption per capita in Russia to a level comparable with thatof developed countries;

Participation in the process of industry consolidation;

Historical and expected high growth rate in private consumption and income in Russia.

Financial and operational support of the parent company (EBI).

7October 2007

Terms and conditions

Information Memorandum CJSC "Moscow Efes Brewery"

8 October 2007

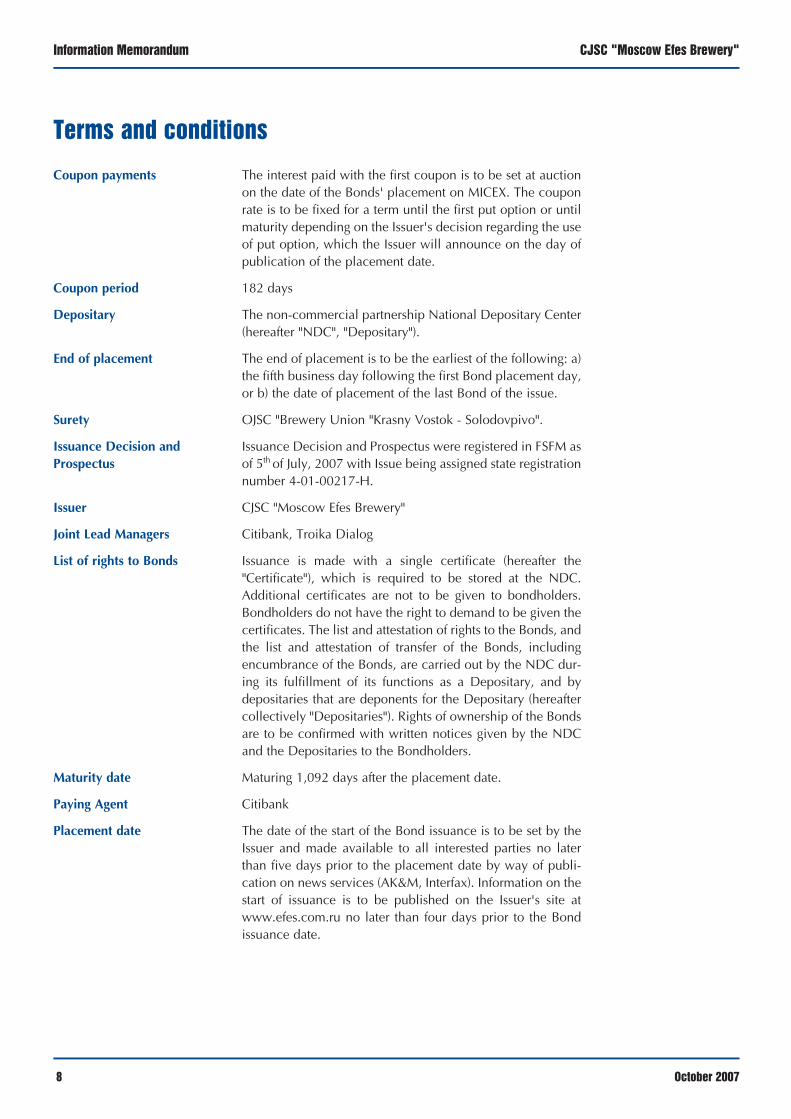

The interest paid with the first coupon is to be set at auctionon the date of the Bonds' placement on MICEX. The couponrate is to be fixed for a term until the first put option or untilmaturity depending on the Issuer's decision regarding the useof put option, which the Issuer will announce on the day ofpublication of the placement date.

182 days

The non�commercial partnership National Depositary Center(hereafter "NDC", "Depositary").

The end of placement is to be the earliest of the following: a)the fifth business day following the first Bond placement day,or b) the date of placement of the last Bond of the issue.

OJSC "Brewery Union "Krasny Vostok � Solodovpivo".

Issuance Decision and Prospectus were registered in FSFM asof 5th of July, 2007 with Issue being assigned state registrationnumber 4�01�00217�H.

CJSC "Moscow Efes Brewery"

Citibank, Troika Dialog

Issuance is made with a single certificate (hereafter the"Certificate"), which is required to be stored at the NDC.Additional certificates are not to be given to bondholders.Bondholders do not have the right to demand to be given thecertificates. The list and attestation of rights to the Bonds, andthe list and attestation of transfer of the Bonds, includingencumbrance of the Bonds, are carried out by the NDC dur�ing its fulfillment of its functions as a Depositary, and bydepositaries that are deponents for the Depositary (hereaftercollectively "Depositaries"). Rights of ownership of the Bondsare to be confirmed with written notices given by the NDCand the Depositaries to the Bondholders.

Maturing 1,092 days after the placement date.

Citibank

The date of the start of the Bond issuance is to be set by theIssuer and made available to all interested parties no laterthan five days prior to the placement date by way of publi�cation on news services (AK&M, Interfax). Information on thestart of issuance is to be published on the Issuer's site atwww.efes.com.ru no later than four days prior to the Bondissuance date.

Coupon payments

Coupon period

Depositary

End of placement

Surety

Issuance Decision andProspectus

Issuer

Joint Lead Managers

List of rights to Bonds

Maturity date

Paying Agent

Placement date

CJSC "Moscow Efes Brewery" Information Memorandum

9October 2007

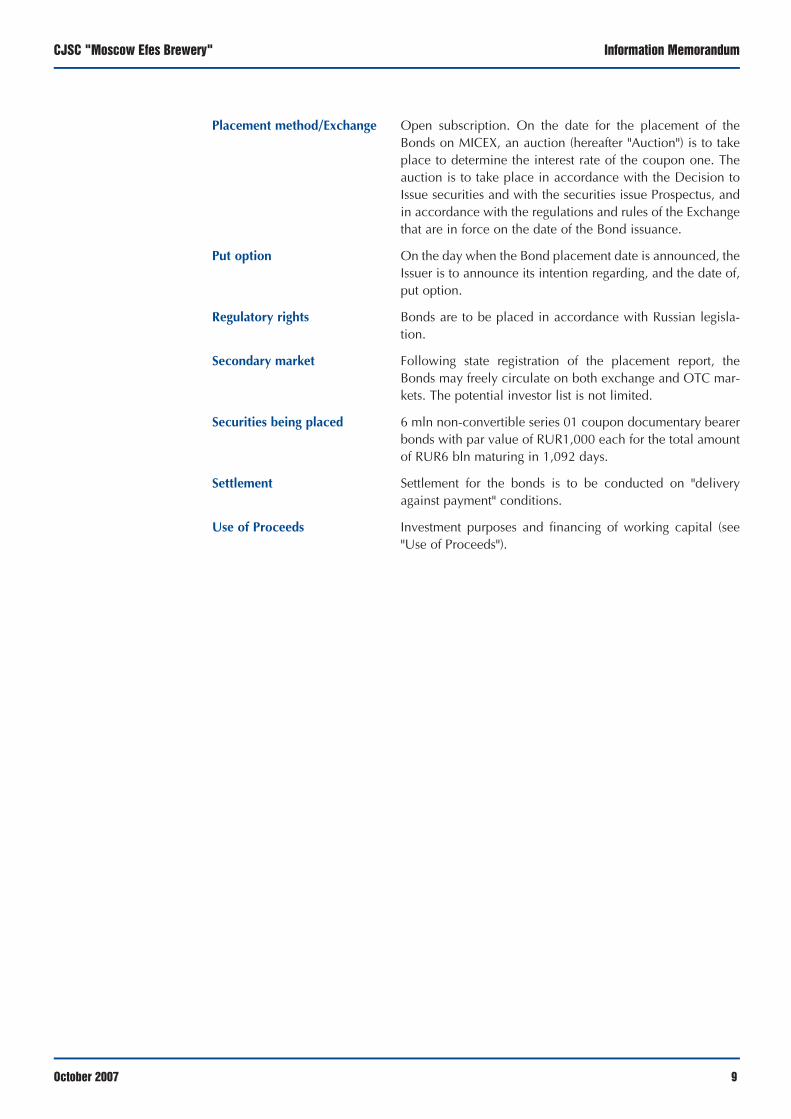

Open subscription. On the date for the placement of theBonds on MICEX, an auction (hereafter "Auction") is to takeplace to determine the interest rate of the coupon one. Theauction is to take place in accordance with the Decision toIssue securities and with the securities issue Prospectus, andin accordance with the regulations and rules of the Exchangethat are in force on the date of the Bond issuance.

On the day when the Bond placement date is announced, theIssuer is to announce its intention regarding, and the date of,put option.

Bonds are to be placed in accordance with Russian legisla�tion.

Following state registration of the placement report, theBonds may freely circulate on both exchange and OTC mar�kets. The potential investor list is not limited.

6 mln non�convertible series 01 coupon documentary bearerbonds with par value of RUR1,000 each for the total amountof RUR6 bln maturing in 1,092 days.

Settlement for the bonds is to be conducted on "deliveryagainst payment" conditions.

Investment purposes and financing of working capital (see"Use of Proceeds").

Placement method/Exchange

Put option

Regulatory rights

Secondary market

Securities being placed

Settlement

Use of Proceeds

Information Memorandum CJSC "Moscow Efes Brewery"

10 October 2007

Use of proceeds

Up to 75 per cent of amounts, received from the Bond issue will be used to finance purchaseof 92.9 per cent voting shares of OJSC "Brewing Union Krasny Vostok � Solodovpivo".

Up to 25 per cent of amounts received from the Bond issue will be used to refinance existingdebt.

CJSC "Moscow Efes Brewery" Information Memorandum

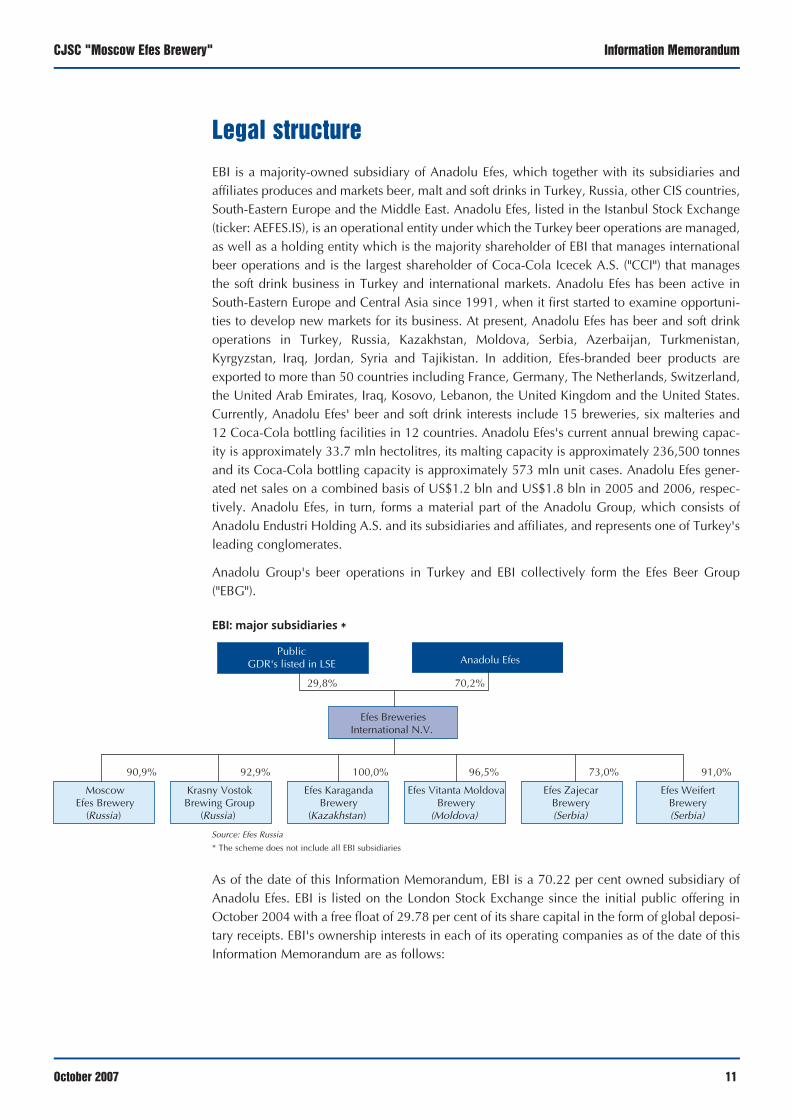

Legal structure

EBI is a majority�owned subsidiary of Anadolu Efes, which together with its subsidiaries andaffiliates produces and markets beer, malt and soft drinks in Turkey, Russia, other CIS countries,South�Eastern Europe and the Middle East. Anadolu Efes, listed in the Istanbul Stock Exchange(ticker: AEFES.IS), is an operational entity under which the Turkey beer operations are managed,as well as a holding entity which is the majority shareholder of EBI that manages internationalbeer operations and is the largest shareholder of Coca�Cola Icecek A.S. ("CCI") that managesthe soft drink business in Turkey and international markets. Anadolu Efes has been active inSouth�Eastern Europe and Central Asia since 1991, when it first started to examine opportuni�ties to develop new markets for its business. At present, Anadolu Efes has beer and soft drinkoperations in Turkey, Russia, Kazakhstan, Moldova, Serbia, Azerbaijan, Turkmenistan,Kyrgyzstan, Iraq, Jordan, Syria and Tajikistan. In addition, Efes�branded beer products areexported to more than 50 countries including France, Germany, The Netherlands, Switzerland,the United Arab Emirates, Iraq, Kosovo, Lebanon, the United Kingdom and the United States.Currently, Anadolu Efes' beer and soft drink interests include 15 breweries, six malteries and12 Coca�Cola bottling facilities in 12 countries. Anadolu Efes's current annual brewing capac�ity is approximately 33.7 mln hectolitres, its malting capacity is approximately 236,500 tonnesand its Coca�Cola bottling capacity is approximately 573 mln unit cases. Anadolu Efes gener�ated net sales on a combined basis of US$1.2 bln and US$1.8 bln in 2005 and 2006, respec�tively. Anadolu Efes, in turn, forms a material part of the Anadolu Group, which consists ofAnadolu Endustri Holding A.S. and its subsidiaries and affiliates, and represents one of Turkey'sleading conglomerates.

Anadolu Group's beer operations in Turkey and EBI collectively form the Efes Beer Group("EBG").

EBI: major subsidiaries *

Source: Efes Russia

* The scheme does not include all EBI subsidiaries

As of the date of this Information Memorandum, EBI is a 70.22 per cent owned subsidiary ofAnadolu Efes. EBI is listed on the London Stock Exchange since the initial public offering inOctober 2004 with a free float of 29.78 per cent of its share capital in the form of global deposi�tary receipts. EBI's ownership interests in each of its operating companies as of the date of thisInformation Memorandum are as follows:

11October 2007

Anadolu Efes

Efes BreweriesInternational N.V.

70,2%

MoscowEfes Brewery

(Russia)

90,9%

Efes KaragandaBrewery

(Kazakhstan)

100,0%

Efes ZajecarBrewery(Serbia)

73,0%

Efes WeifertBrewery(Serbia)

96,5%

PublicGDR's listed in LSE

29,8%

Krasny VostokBrewing Group

(Russia)

92,9% 91,0%

Efes Vitanta MoldovaBrewery

(Moldova)

Information Memorandum CJSC "Moscow Efes Brewery"

12

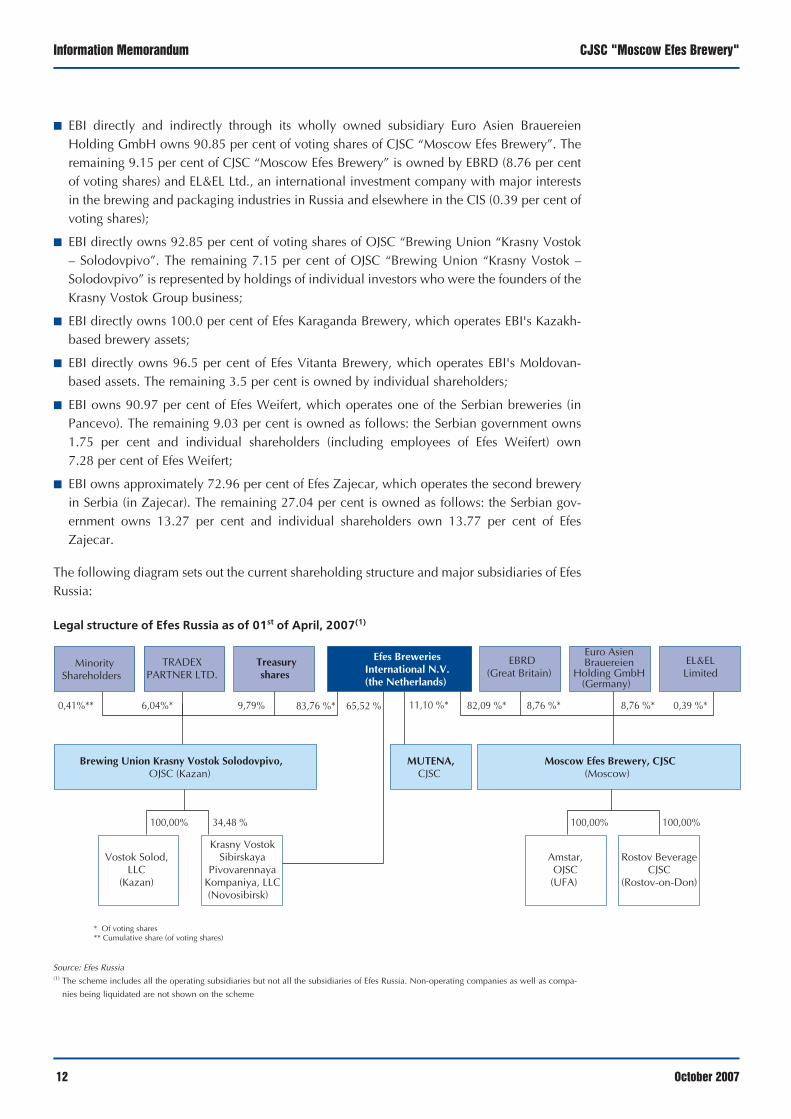

■ EBI directly and indirectly through its wholly owned subsidiary Euro Asien BrauereienHolding GmbH owns 90.85 per cent of voting shares of CJSC ìMoscow Efes Breweryî. Theremaining 9.15 per cent of CJSC ìMoscow Efes Breweryî is owned by EBRD (8.76 per centof voting shares) and EL&EL Ltd., an international investment company with major interestsin the brewing and packaging industries in Russia and elsewhere in the CIS (0.39 per cent ofvoting shares);

■ EBI directly owns 92.85 per cent of voting shares of OJSC ìBrewing Union ìKrasny Vostokñ Solodovpivoî. The remaining 7.15 per cent of OJSC ìBrewing Union ìKrasny Vostok ñSolodovpivoî is represented by holdings of individual investors who were the founders of theKrasny Vostok Group business;

■ EBI directly owns 100.0 per cent of Efes Karaganda Brewery, which operates EBI's Kazakh�based brewery assets;

■ EBI directly owns 96.5 per cent of Efes Vitanta Brewery, which operates EBI's Moldovan�based assets. The remaining 3.5 per cent is owned by individual shareholders;

■ EBI owns 90.97 per cent of Efes Weifert, which operates one of the Serbian breweries (inPancevo). The remaining 9.03 per cent is owned as follows: the Serbian government owns1.75 per cent and individual shareholders (including employees of Efes Weifert) own 7.28 per cent of Efes Weifert;

■ EBI owns approximately 72.96 per cent of Efes Zajecar, which operates the second breweryin Serbia (in Zajecar). The remaining 27.04 per cent is owned as follows: the Serbian gov�ernment owns 13.27 per cent and individual shareholders own 13.77 per cent of EfesZajecar.

The following diagram sets out the current shareholding structure and major subsidiaries of EfesRussia:

Legal structure of Efes Russia as of 01st of April, 2007(1)

Source: Efes Russia (1) The scheme includes all the operating subsidiaries but not all the subsidiaries of Efes Russia. Non�operating companies as well as compa�

nies being liquidated are not shown on the scheme

October 2007

Efes BreweriesInternational N.V.(the Netherlands)

Brewing Union Krasny Vostok Solodovpivo,OJSC (Kazan)

83,76 %*

* Of voting shares ** Cumulative share (of voting shares)

TRADEXPARTNER LTD.

6,04%*

MinorityShareholders

0,41%** 9,79%

Krasny VostokSibirskaya

PivovarennayaKompaniya, LLC(Novosibirsk)

Vostok Solod,LLC

(Kazan)

100,00% 100,00% 100,00%34,48 %

65,52 %

Moscow Efes Brewery, CJSC(Moscow)

Amstar,OJSC(UFA)

Rostov BeverageCJSC

(Rostov�on�Don)

EBRD(Great Britain)

EL&ELLimited

Euro AsienBrauereien

Holding GmbH(Germany)

82,09 %* 8,76 %* 8,76 %* 0,39 %*

Treasuryshares

MUTENA,CJSC

11,10 %*

CJSC "Moscow Efes Brewery" Information Memorandum

A put option has been granted to the EBRD by EBI that may be exercisable between the 7th andthe 10th anniversary (2008 and 2011) of the date of EBRD's first subscription in the share capi�tal of CJSC ìMoscow Efes Breweryî. By such put option, EBRD will be entitled to sell its stakein CJSC ìMoscow Efes Breweryî to EBI at an option price determined by an independent valu�ation.

EBI includes it as liability in the consolidated financial statements at fair value. The liability forthe put option has been measured by applying a weighting of different valuation techniquesand US$103,400 (YTL 145.294) was presented in "other non�current liabilities" as "liability forput option" in the EBI's consolidated balance sheet.

13October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

14

Strategy

Efes Russia represents the largest branch of EBI and intends to pursue a strategy aimed atincreasing revenue and profits, including:

1) Capitalize on the growth of the beer market in Russia. Russia is currently the 3rd largest beermarket in the world (source: Canadean). Efes Russia believes that Russian market possessessignificant potential for future growth due to improving macroeconomic trends, and conse�quently higher purchasing power alongside a low base of per capita beer consumption com�pared to that of Western European countries. Efes Russia will continue to pursue a strategyaimed at growing organically and inorganically faster than the competition in Russia in orderto capitalize on such growth potential and intends to support demand for its products by:

■ increasing the capacity of its overall production platform through:

(i) the installation of additional production lines to continue serving areas with demon�strated growth potential, such as the capacity increase in Efes Russia's brewery in Ufa,whereby the capacity increased from 2.0 mln hl (1.2 mln hl in 2004) to 4.1 mln hl inJuly 2006;

(ii) establishing of additional brewing facilities in Russia, such as the completed acquisi�tion of a brewery in Ufa, establishment of greenfield brewery in Rostov in 2003, andthe acquisition of Krasny Vostok Group in February 2006;

■ expanding Efes Russia's distribution system through a combination of direct order�takingin high density population areas and fostering preferential relationships with authorizeddealers in other geographic areas.

For example, through the restructuring of its distribution system in Russia to increase theamount of sales effected through direct order�taking with retail outlets, Efes Russia increased thenumber of outlets served through direct order�taking in Moscow from approximately 2,500 in2004 to approximately 7,000 in 2005 and to approximately 11,500 in 2006. In areas, whereEfes Russia does not have direct order�taking it places significant emphasis on its relationshipwith authorized dealers, thereby seeking to minimize logistical complexity.

2) Focus on high margin or growing segments. Efes Russia's principal beer segments includepremium, mainstream and economy beers. Efes Russia's product strategy is to focus on themost profitable, largest segments and/or those segments with the highest growth potential inthe Russian beer market. To this end, Efes Russia seeks to have a brand portfolio that com�prehensively covers the principal beer segments in which it operates and that allows it tobenefit from key market trends including the increase in consumption of premium beers.

3) Continue to create and invest in brands and pursue aggressive marketing campaigns. EfesRussia views its brand portfolio as a key asset, due to the fact that brand perception is a crit�ical factor in a consumer's choice of beer in Russia. As such, Efes Russia makes extensiveuse of advertising, using appropriate media channels, and sponsoring sports, including foot�ball (soccer) and cultural events such as music concerts. Efes Russia intends to continue topromote its brands extensively in order to further increase brand awareness and customerloyalty with the objective of growing faster than the competition.

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

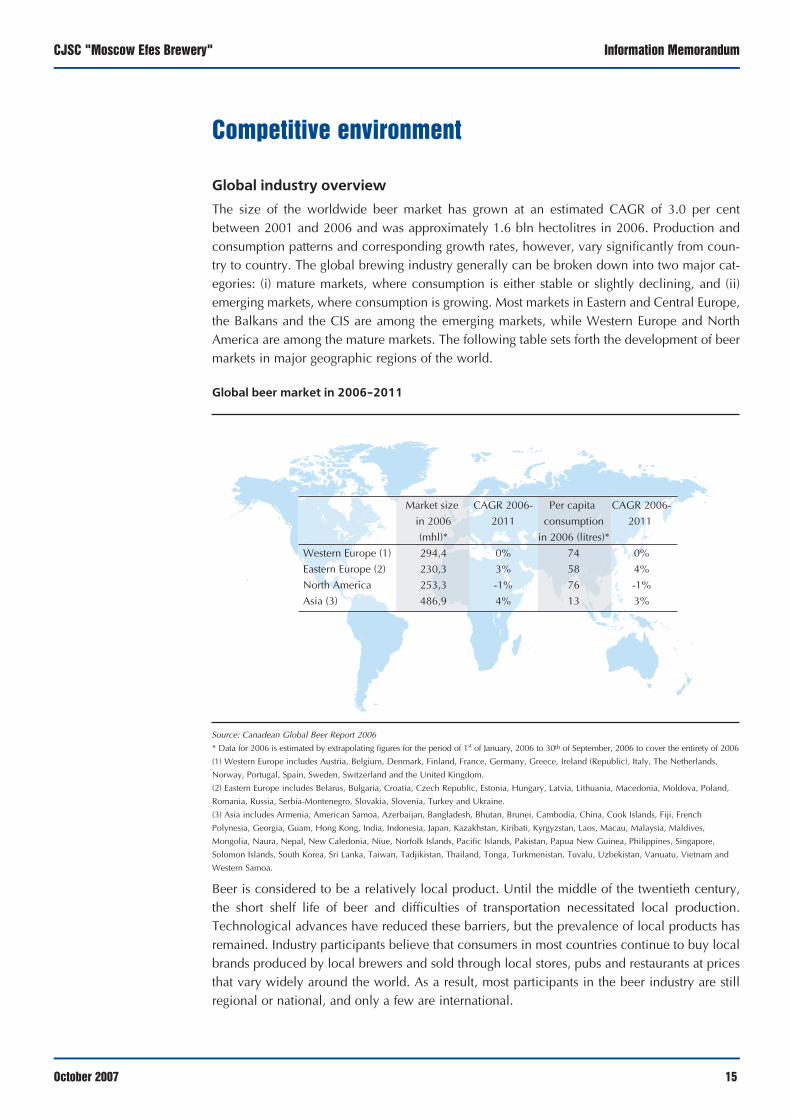

Сompetitive environment

Global industry overview

The size of the worldwide beer market has grown at an estimated CAGR of 3.0 per centbetween 2001 and 2006 and was approximately 1.6 bln hectolitres in 2006. Production andconsumption patterns and corresponding growth rates, however, vary significantly from coun�try to country. The global brewing industry generally can be broken down into two major cat�egories: (i) mature markets, where consumption is either stable or slightly declining, and (ii)emerging markets, where consumption is growing. Most markets in Eastern and Central Europe,the Balkans and the CIS are among the emerging markets, while Western Europe and NorthAmerica are among the mature markets. The following table sets forth the development of beermarkets in major geographic regions of the world.

Global beer market in 2006�2011

Source: Canadean Global Beer Report 2006

* Data for 2006 is estimated by extrapolating figures for the period of 1st of January, 2006 to 30th of September, 2006 to cover the entirety of 2006

(1) Western Europe includes Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland (Republic), Italy, The Netherlands,

Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

(2) Eastern Europe includes Belarus, Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Macedonia, Moldova, Poland,

Romania, Russia, Serbia�Montenegro, Slovakia, Slovenia, Turkey and Ukraine.

(3) Asia includes Armenia, American Samoa, Azerbaijan, Bangladesh, Bhutan, Brunei, Cambodia, China, Cook Islands, Fiji, French

Polynesia, Georgia, Guam, Hong Kong, India, Indonesia, Japan, Kazakhstan, Kiribati, Kyrgyzstan, Laos, Macau, Malaysia, Maldives,

Mongolia, Naura, Nepal, New Caledonia, Niue, Norfolk Islands, Pacific Islands, Pakistan, Papua New Guinea, Philippines, Singapore,

Solomon Islands, South Korea, Sri Lanka, Taiwan, Tadjikistan, Thailand, Tonga, Turkmenistan, Tuvalu, Uzbekistan, Vanuatu, Vietnam and

Western Samoa.

Beer is considered to be a relatively local product. Until the middle of the twentieth century,the short shelf life of beer and difficulties of transportation necessitated local production.Technological advances have reduced these barriers, but the prevalence of local products hasremained. Industry participants believe that consumers in most countries continue to buy localbrands produced by local brewers and sold through local stores, pubs and restaurants at pricesthat vary widely around the world. As a result, most participants in the beer industry are stillregional or national, and only a few are international.

15October 2007

Market size CAGR 2006� Per capita CAGR 2006�

in 2006 2011 consumption 2011

(mhl)* in 2006 (litres)*

Western Europe (1) 294,4 0% 74 0%

Eastern Europe (2) 230,3 3% 58 4%

North America 253,3 �1% 76 �1%

Asia (3) 486,9 4% 13 3%

Information Memorandum CJSC "Moscow Efes Brewery"

16

The general trend in the brewing industry is toward consolidation at the national and, to someextent, international levels. In many mature markets, the top two or three brewing companiesaccount jointly for a market share by sales volume of over 50.0 per cent. For example, the topthree brewing companies in each of France, Italy and the United Kingdom accounted forapproximately 81 per cent, 60 per cent and 68 per cent, respectively, of sales volume in therespective countries for 2006. On a worldwide level, consolidation is occurring, although it isnot as pronounced as in many mature markets. For example, whereas in 1999, the top 20 inter�national brewing companies accounted for approximately 37.7 per cent of sales volume world�wide, in 2004 they accounted for 65.4 per cent (source: Canadean).

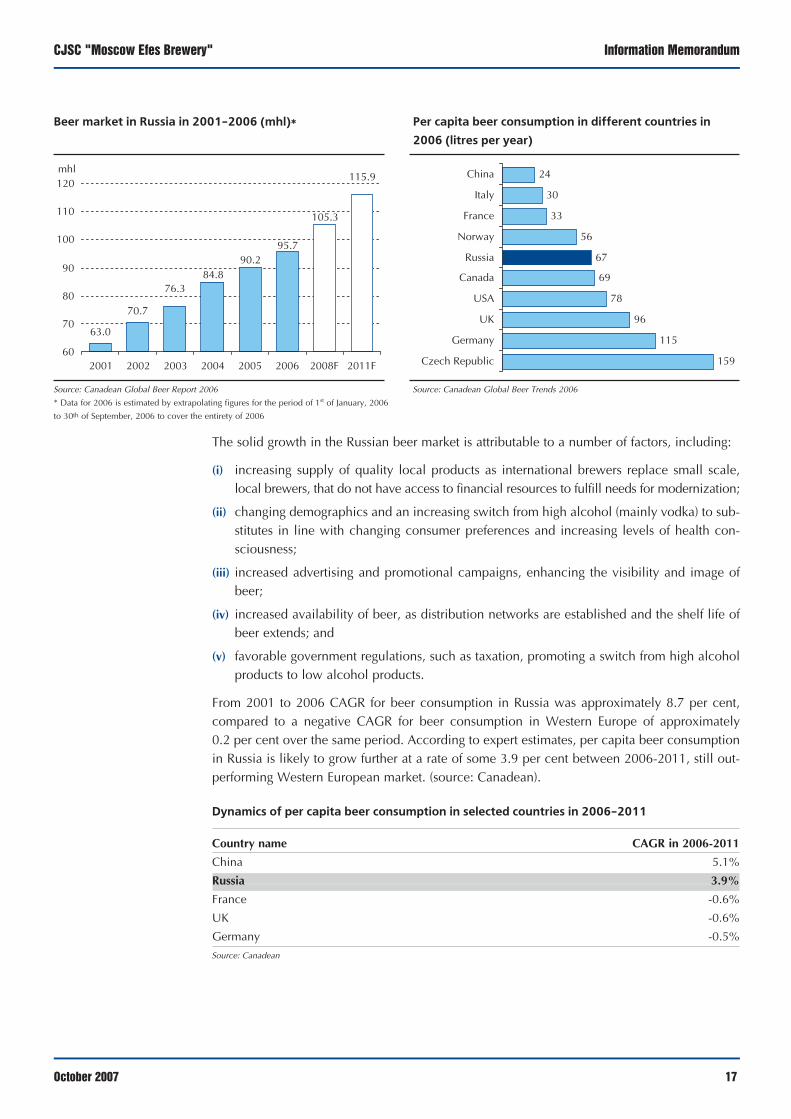

Russian beer market

The Russian beer market is one of the most dynamic and highest volume growth markets inEurope, with both domestic and foreign producers trying to increase their market share in therapidly growing industry.

Largest beer markets in the world in 2006

Source: Canadean Global Beer Trends 2006

The market size has grown significantly, from approximately 63.0 mln hectolitres in 2001, toan estimated 95.7 mln hectolitres in 2006, constituting a CAGR of approximately 8.7 per cent(source: Canadean). In spite of regulatory changes, including federal restrictions imposed onproduction and distribution of alcohol drinks in Russia in 2006 (e. g., introduction of UnifiedState Automated Information System ("EGAIS system")) the Russian beer market is expected togrow further albeit at a slower rate.

In spite of the strong historical increase in beer consumption, estimated per capita beer con�sumption of approximately 67 litres remains relatively low when compared to mature markets.With a population of approximately 142.2 mln, Russia is among the most attractive beer mar�kets in the world, and, according to Canadean research, beer consumption in Russia is expect�ed to grow at a CAGR of approximately 3.9 per cent in the period from 2006 to 2011.

October 2007

330

231

96 94 9463 59 58

0

50

100

150

200

250

300

350mhl

China USA Russia Brazil Germany Japan Mexico UK

CJSC "Moscow Efes Brewery" Information Memorandum

The solid growth in the Russian beer market is attributable to a number of factors, including:

(i) increasing supply of quality local products as international brewers replace small scale,local brewers, that do not have access to financial resources to fulfill needs for modernization;

(ii) changing demographics and an increasing switch from high alcohol (mainly vodka) to sub�stitutes in line with changing consumer preferences and increasing levels of health con�sciousness;

(iii) increased advertising and promotional campaigns, enhancing the visibility and image ofbeer;

(iv) increased availability of beer, as distribution networks are established and the shelf life ofbeer extends; and

(v) favorable government regulations, such as taxation, promoting a switch from high alcoholproducts to low alcohol products.

From 2001 to 2006 CAGR for beer consumption in Russia was approximately 8.7 per cent,compared to a negative CAGR for beer consumption in Western Europe of approximately 0.2 per cent over the same period. According to expert estimates, per capita beer consumptionin Russia is likely to grow further at a rate of some 3.9 per cent between 2006�2011, still out�performing Western European market. (source: Canadean).

Dynamics of per capita beer consumption in selected countries in 2006�2011

Country name CAGR in 2006�2011

China 5.1%

Russia 3.9%

France �0.6%

UK �0.6%

Germany �0.5%

Source: Canadean

17October 2007

Beer market in Russia in 2001�2006 (mhl)* Per capita beer consumption in different countries in 2006 (litres per year)

Source: Canadean Global Beer Report 2006 Source: Canadean Global Beer Trends 2006

* Data for 2006 is estimated by extrapolating figures for the period of 1st of January, 2006

to 30th of September, 2006 to cover the entirety of 2006

63.0

70.7

76.384.8

90.295.7

105.3

115.9

60

70

80

90

100

110

120

2001 2002 2003 2004 2005 2006 2008F 2011F

mhl

159

115

96

78

69

67

56

33

30

24

Czech Republic

Germany

UK

USA

Canada

Russia

Norway

France

Italy

China

Information Memorandum CJSC "Moscow Efes Brewery"

18

The beer market in Russia can be split in five segments based primarily on average price. Theseare:

(i) Super premium segment brands: this category consists of all imported beer brands (outsideof CIS origin), licensed brands and ultra premium Russian brands. The brands in this seg�ment are priced at 64 Rubles per litre or higher.

(ii) Premium segment brands: this category consists of some licensed brands and some premi�um brands from CIS. The brands in this segment are priced between 40�60 Rubles per litre.

(iii) Upper mainstream brands: this category consists of national brands and are pricedbetween 38�43 Rubles per litre.

(iv) Lower mainstream brands: the brands in this category consist of national brands which arepriced between 29�38 Rubles per litre.

(v) Economy segment brands: this category consists of all brands that are priced below 29Rubles per litre.

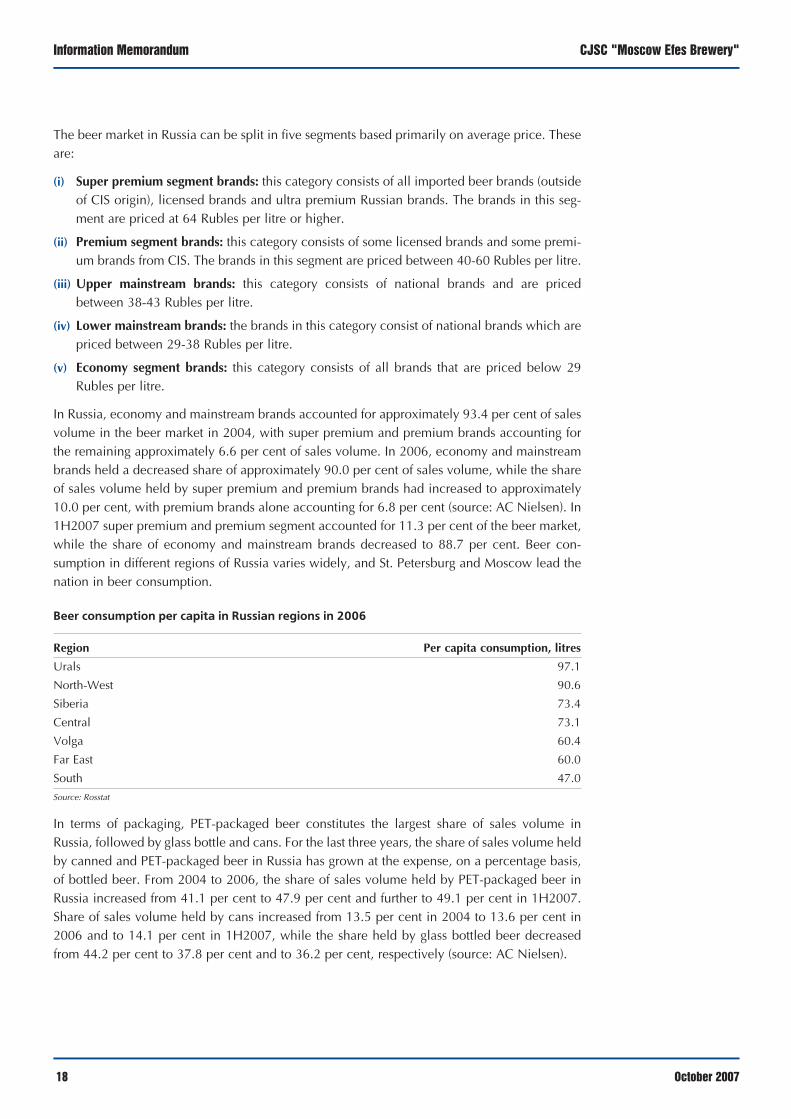

In Russia, economy and mainstream brands accounted for approximately 93.4 per cent of salesvolume in the beer market in 2004, with super premium and premium brands accounting forthe remaining approximately 6.6 per cent of sales volume. In 2006, economy and mainstreambrands held a decreased share of approximately 90.0 per cent of sales volume, while the shareof sales volume held by super premium and premium brands had increased to approximately10.0 per cent, with premium brands alone accounting for 6.8 per cent (source: AC Nielsen). In1H2007 super premium and premium segment accounted for 11.3 per cent of the beer market,while the share of economy and mainstream brands decreased to 88.7 per cent. Beer con�sumption in different regions of Russia varies widely, and St. Petersburg and Moscow lead thenation in beer consumption.

Beer consumption per capita in Russian regions in 2006

Region Per capita consumption, litres

Urals 97.1

North�West 90.6

Siberia 73.4

Central 73.1

Volga 60.4

Far East 60.0

South 47.0

Source: Rosstat

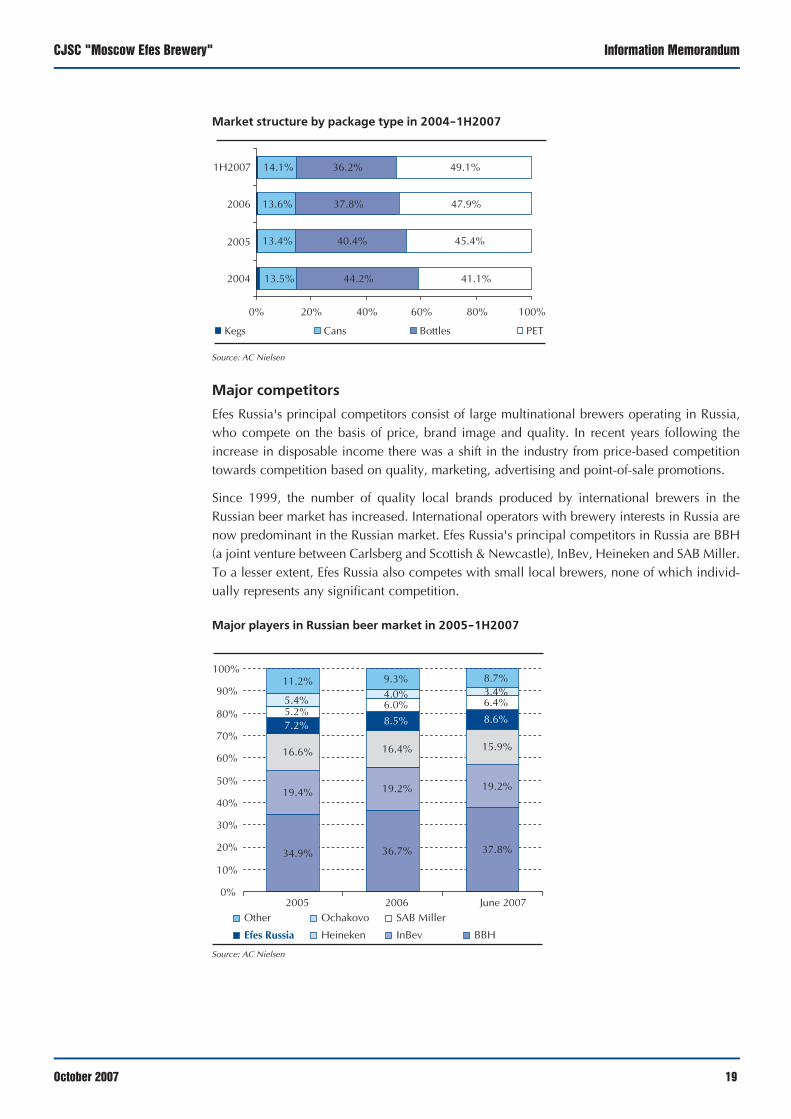

In terms of packaging, PET�packaged beer constitutes the largest share of sales volume inRussia, followed by glass bottle and cans. For the last three years, the share of sales volume heldby canned and PET�packaged beer in Russia has grown at the expense, on a percentage basis,of bottled beer. From 2004 to 2006, the share of sales volume held by PET�packaged beer inRussia increased from 41.1 per cent to 47.9 per cent and further to 49.1 per cent in 1H2007.Share of sales volume held by cans increased from 13.5 per cent in 2004 to 13.6 per cent in2006 and to 14.1 per cent in 1H2007, while the share held by glass bottled beer decreasedfrom 44.2 per cent to 37.8 per cent and to 36.2 per cent, respectively (source: AC Nielsen).

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

Market structure by package type in 2004�1H2007

Source: AC Nielsen

Major competitors

Efes Russia's principal competitors consist of large multinational brewers operating in Russia,who compete on the basis of price, brand image and quality. In recent years following theincrease in disposable income there was a shift in the industry from price�based competitiontowards competition based on quality, marketing, advertising and point�of�sale promotions.

Since 1999, the number of quality local brands produced by international brewers in theRussian beer market has increased. International operators with brewery interests in Russia arenow predominant in the Russian market. Efes Russia's principal competitors in Russia are BBH(a joint venture between Carlsberg and Scottish & Newcastle), InBev, Heineken and SAB Miller.To a lesser extent, Efes Russia also competes with small local brewers, none of which individ�ually represents any significant competition.

Major players in Russian beer market in 2005�1H2007

Source: AC Nielsen

19October 2007

13.5%

13.4%

13.6%

14.1%

44.2%

40.4%

37.8%

36.2%

41.1%

45.4%

47.9%

49.1%

0% 20% 40% 60% 80% 100%

2004

2005

2006

1H2007

Kegs Cans Bottles PET

Other Ochakovo SAB Miller

Efes Russia Heineken InBev BBH

34.9% 36.7% 37.8%

19.4% 19.2% 19.2%

16.6% 16.4% 15.9%

7.2% 8.5% 8.6%5.2%

6.0% 6.4%5.4% 4.0% 3.4%11.2% 9.3% 8.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 June 2007

Information Memorandum CJSC "Moscow Efes Brewery"

20

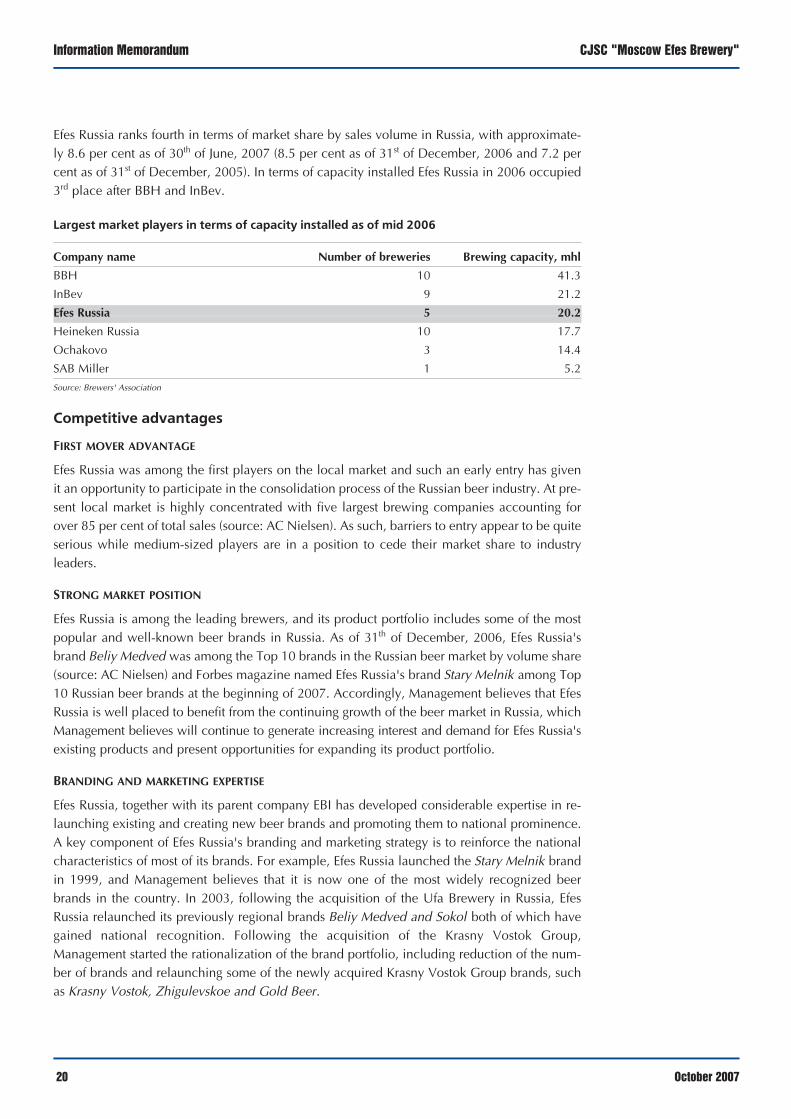

Efes Russia ranks fourth in terms of market share by sales volume in Russia, with approximate�ly 8.6 per cent as of 30th of June, 2007 (8.5 per cent as of 31st of December, 2006 and 7.2 percent as of 31st of December, 2005). In terms of capacity installed Efes Russia in 2006 occupied3rd place after BBH and InBev.

Largest market players in terms of capacity installed as of mid 2006

Company name Number of breweries Brewing capacity, mhl

BBH 10 41.3

InBev 9 21.2

Efes Russia 5 20.2

Heineken Russia 10 17.7

Ochakovo 3 14.4

SAB Miller 1 5.2

Source: Brewers' Association

Competitive advantages

FIRST MOVER ADVANTAGE

Efes Russia was among the first players on the local market and such an early entry has givenit an opportunity to participate in the consolidation process of the Russian beer industry. At pre�sent local market is highly concentrated with five largest brewing companies accounting forover 85 per cent of total sales (source: AC Nielsen). As such, barriers to entry appear to be quiteserious while medium�sized players are in a position to cede their market share to industryleaders.

STRONG MARKET POSITION

Efes Russia is among the leading brewers, and its product portfolio includes some of the mostpopular and well�known beer brands in Russia. As of 31th of December, 2006, Efes Russia'sbrand Beliy Medved was among the Top 10 brands in the Russian beer market by volume share(source: AC Nielsen) and Forbes magazine named Efes Russia's brand Stary Melnik among Top10 Russian beer brands at the beginning of 2007. Accordingly, Management believes that EfesRussia is well placed to benefit from the continuing growth of the beer market in Russia, whichManagement believes will continue to generate increasing interest and demand for Efes Russia'sexisting products and present opportunities for expanding its product portfolio.

BRANDING AND MARKETING EXPERTISE

Efes Russia, together with its parent company EBI has developed considerable expertise in re�launching existing and creating new beer brands and promoting them to national prominence.A key component of Efes Russia's branding and marketing strategy is to reinforce the nationalcharacteristics of most of its brands. For example, Efes Russia launched the Stary Melnik brandin 1999, and Management believes that it is now one of the most widely recognized beerbrands in the country. In 2003, following the acquisition of the Ufa Brewery in Russia, EfesRussia relaunched its previously regional brands Beliy Medved and Sokol both of which havegained national recognition. Following the acquisition of the Krasny Vostok Group,Management started the rationalization of the brand portfolio, including reduction of the num�ber of brands and relaunching some of the newly acquired Krasny Vostok Group brands, suchas Krasny Vostok, Zhigulevskoe and Gold Beer.

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

TACTICAL PRODUCT POSITIONING

Management believes that it has a strong expertise of tactical product positioning. This assumestimely shifts to more popular beer segments, such as growing premium segment in Russia, aswell as catching new trends in beverage packaging. For example, Efes Russia benefited from anincrease of demand for PET�packaged beer products by introducing economy segment brandBeliy Medved in 2003, Krasny Vostok, Gold Beer and Zhigulevskoe in 2006 whose aggregatePET sales volume was approximately 55 per cent of Efes Russia's total sales volume in 2006. Atpresent Efes Russia has a technological capability to produce high quality beer in all packagetypes, which makes it more flexible to any shifts in market demand.

EXPERTISE IN MANAGING ORGANIC GROWTH AND INTEGRATING ACQUISITIONS

Efes Russia has a proven track record of successfully managing rapid organic growth and inte�grating new acquisitions into its production through adding brewing capacity in a cost effectivemanner: it has grown through a combination of strategic acquisitions, greenfield developmentsand modular expansion of its brewing facilities, demonstrating its ability to apply the know�howwithin its parent EBI, while developing its own experience and expertise in managing growth.

QUALITY AND EXPERIENCE OF MANAGEMENT

Management believes that it has a distinct advantage over competitors because of its accumu�lated experience in Russia, and the length of time that many members of Management teamhave worked together. Efes Russia actively recruits from leading international companies andplaces special emphasis on in�house training of new team members.

NATIONWIDE STRONG SALES AND DISTRIBUTION FORCE

Management believes that it has a competitive advantage because of its strong sales and distri�bution force covering all Russian high�density population areas through a network of sales rep�resentatives (direct order�taking) and authorized dealers. Alongside a growth in disposableincome in Russia there was a shift within the national beverage industry from price�based com�petition towards aggressive promotion campaigns, stressing quality of the product and con�tributing to the brand awareness. In such conditions, nationwide sales force becomes a neces�sary prerequisite for support and further increase in market share.

LOGISTICS BENEFIT ARISING FROM MULTI�PLANTS AND CROSS�BREWING

Following the acquisition of the Krasny Vostok Group, all of Efes Moscow's products (exceptfor the licenced ones) started being produced in all the breweries of the Krasny Vostok Groupas well. This cross�brewing has brought significant advantages, as it enables effective cateringof high consumption growth regions of Russia including Eastern Regions of Russia through EfesRussia's products from the brewery in Novosibirsk.

SELF�SUFFICIENCY IN RAW MATERIAL PROCUREMENT

Efes Russia is able to supply a majority of its malt and pre�form requirement through its fourmalt production facilities (139 000 tonnes annual capacity) and pre�form production line (1.3 mln units/day). As such, possibility to generate a constant supply of malt provides a distinct competitive advantage over some local producers.

Efes Russia has an advantage of having good relationship with the suppliers, and the contractsare renewed on annual basis.

21October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

22

Sales, marketing and distribution

Marketing

Efes Russia views its brand portfolio as a key asset, as the Management believes that the imageof a brand and its message are essential elements in consumer's choice of beer. Efes Russiaseeks to have a brand portfolio that comprehensively covers the principal beer segments inwhich it operates, principally the premium, mainstream and economy segments. Managementbelieves that local positioning of its brands is a key element in facilitating better understandingof, and responses to, the needs of local consumers.

Efes Russia markets its brands through a broad range of marketing channels, including, amongothers, TV, billboard and radio advertising and consumer promotions (Above The Line ("ATL")and Below The Line ("BTL") activities). Television advertising is a part of Efes Russia's overallmarketing strategy as it allows Efes Russia to promote its brands at a national level. The empha�sis on a national brand promotes customer loyalty and latent demand for Efes Russia's productsand facilitates future growth by providing a solid consumer base in different regions.

Efes Russia also sponsors high profile sports, music festivals and other special events, therebygiving broad exposure to the local brands and to the Efes brand. Sponsorships include thebiggest Rock event in Russia "Krylia" sponsored by Stary Melnik, Stary Melnik sponsorship ofthe Russian National Football Team and the Efes International Blues Festival, among others.

As for BTL activities in 2006, more than 1,200,000 prizes were distributed trough in�store pro�motions in 82 different locations, which help to support the brand image in the field.

Efes Russia's marketing is principally aimed at the population aged between 18 and 40. EfesRussia focuses on this particular demographic because people within this age consume morebeer per capita than other age groups (which is consistent with per capita consumption patternsin Western economies) and are more likely to remain loyal to a brand if they form that loyaltyat a young age. Efes Russia's management believes that beer brands have longer product lifecycles than brands in many other consumer product sectors and that the strength of a beerbrand tends to endure over a long period of time once brand loyalty is established.

Management believes that Russian law, which restricts beer advertising and the advertising ofalcoholic beverages will primarily affect potential market entrants, acting as a barrier to entryby preventing the use of an important method for increasing brand awareness. Managementalso believes that these restrictions could, to some extent, represent an obstacle for incumbentparticipants to launch new products. However, Management believes that these new restric�tions are unlikely to significantly affect brand recognition of existing brands of incumbent par�ticipants such as Efes Russia. In any event, Management believes that Efes Russia benefits fromthe Anadolu Efes' extensive experience of operations in markets with similar restrictions.

The combined marketing and advertising expenditures of Efes Russia as a percentage of saleswere approximately 11.1 per cent in 2006 (11.4 per cent in 2005).

The following table sets out Efes Russia's brands in each segment.

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

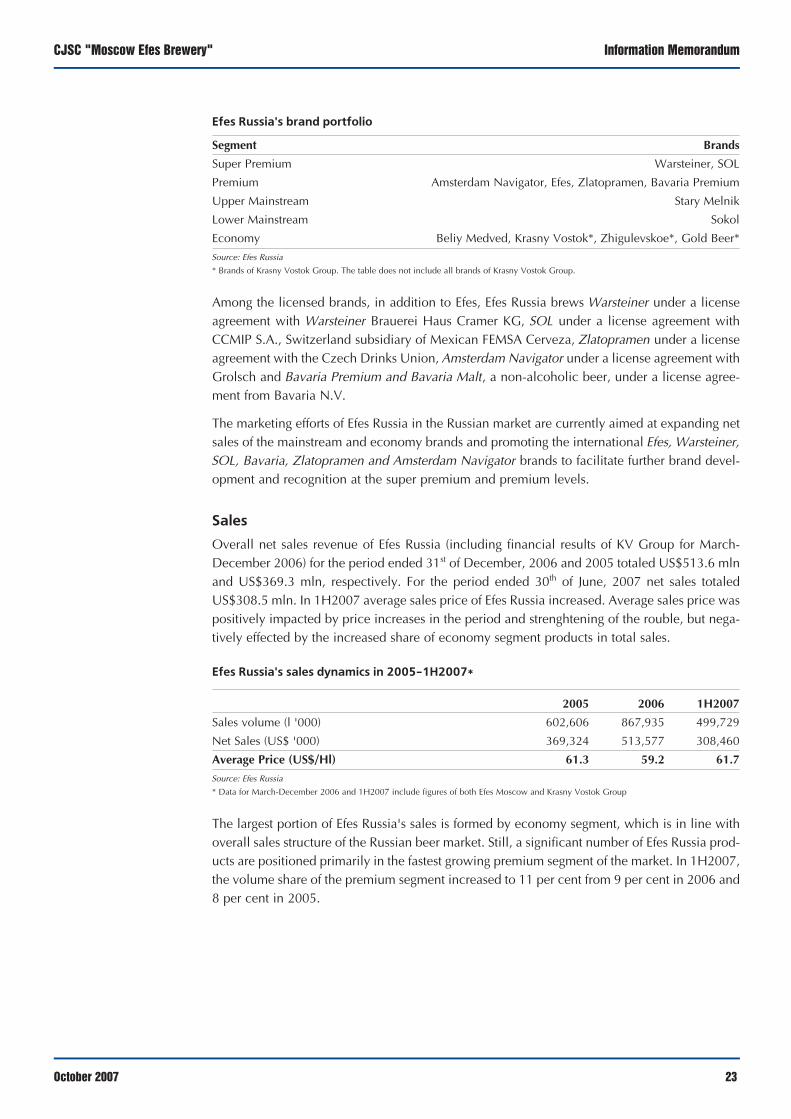

Efes Russia's brand portfolio

Segment Brands

Super Premium Warsteiner, SOL

Premium Amsterdam Navigator, Efes, Zlatopramen, Bavaria Premium

Upper Mainstream Stary Melnik

Lower Mainstream Sokol

Economy Beliy Medved, Krasny Vostok*, Zhigulevskoe*, Gold Beer*

Source: Efes Russia

* Brands of Krasny Vostok Group. The table does not include all brands of Krasny Vostok Group.

Among the licensed brands, in addition to Efes, Efes Russia brews Warsteiner under a licenseagreement with Warsteiner Brauerei Haus Cramer KG, SOL under a license agreement withCCMIP S.A., Switzerland subsidiary of Mexican FEMSA Cerveza, Zlatopramen under a licenseagreement with the Czech Drinks Union, Amsterdam Navigator under a license agreement withGrolsch and Bavaria Premium and Bavaria Malt, a non�alcoholic beer, under a license agree�ment from Bavaria N.V.

The marketing efforts of Efes Russia in the Russian market are currently aimed at expanding netsales of the mainstream and economy brands and promoting the international Efes, Warsteiner,SOL, Bavaria, Zlatopramen and Amsterdam Navigator brands to facilitate further brand devel�opment and recognition at the super premium and premium levels.

Sales

Overall net sales revenue of Efes Russia (including financial results of KV Group for March�December 2006) for the period ended 31st of December, 2006 and 2005 totaled US$513.6 mlnand US$369.3 mln, respectively. For the period ended 30th of June, 2007 net sales totaledUS$308.5 mln. In 1H2007 average sales price of Efes Russia increased. Average sales price waspositively impacted by price increases in the period and strenghtening of the rouble, but nega�tively effected by the increased share of economy segment products in total sales.

Efes Russia's sales dynamics in 2005�1H2007*

2005 2006 1H2007

Sales volume (l '000) 602,606 867,935 499,729

Net Sales (US$ '000) 369,324 513,577 308,460

Average Price (US$/Hl) 61.3 59.2 61.7

Source: Efes Russia

* Data for March�December 2006 and 1H2007 include figures of both Efes Moscow and Krasny Vostok Group

The largest portion of Efes Russia's sales is formed by economy segment, which is in line withoverall sales structure of the Russian beer market. Still, a significant number of Efes Russia prod�ucts are positioned primarily in the fastest growing premium segment of the market. In 1H2007,the volume share of the premium segment increased to 11 per cent from 9 per cent in 2006 and8 per cent in 2005.

23October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

24

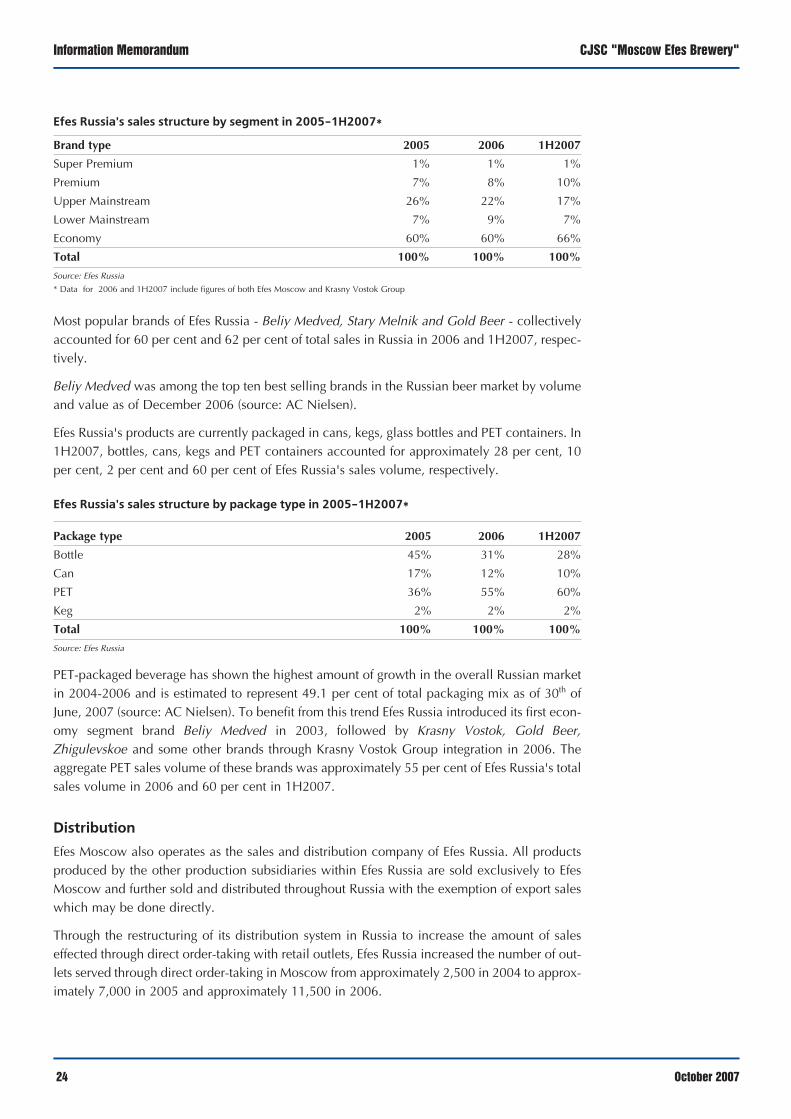

Efes Russia's sales structure by segment in 2005�1H2007*

Brand type 2005 2006 1H2007

Super Premium 1% 1% 1%

Premium 7% 8% 10%

Upper Mainstream 26% 22% 17%

Lower Mainstream 7% 9% 7%

Economy 60% 60% 66%

Total 100% 100% 100%

Source: Efes Russia

* Data for 2006 and 1H2007 include figures of both Efes Moscow and Krasny Vostok Group

Most popular brands of Efes Russia � Beliy Medved, Stary Melnik and Gold Beer � collectivelyaccounted for 60 per cent and 62 per cent of total sales in Russia in 2006 and 1H2007, respec�tively.

Beliy Medved was among the top ten best selling brands in the Russian beer market by volumeand value as of December 2006 (source: AC Nielsen).

Efes Russia's products are currently packaged in cans, kegs, glass bottles and PET containers. In1H2007, bottles, cans, kegs and PET containers accounted for approximately 28 per cent, 10per cent, 2 per cent and 60 per cent of Efes Russia's sales volume, respectively.

Efes Russia's sales structure by package type in 2005�1H2007*

Package type 2005 2006 1H2007

Bottle 45% 31% 28%

Can 17% 12% 10%

PET 36% 55% 60%

Keg 2% 2% 2%

Total 100% 100% 100%

Source: Efes Russia

PET�packaged beverage has shown the highest amount of growth in the overall Russian marketin 2004�2006 and is estimated to represent 49.1 per cent of total packaging mix as of 30th ofJune, 2007 (source: AC Nielsen). To benefit from this trend Efes Russia introduced its first econ�omy segment brand Beliy Medved in 2003, followed by Krasny Vostok, Gold Beer,Zhigulevskoe and some other brands through Krasny Vostok Group integration in 2006. Theaggregate PET sales volume of these brands was approximately 55 per cent of Efes Russia's totalsales volume in 2006 and 60 per cent in 1H2007.

Distribution

Efes Moscow also operates as the sales and distribution company of Efes Russia. All productsproduced by the other production subsidiaries within Efes Russia are sold exclusively to EfesMoscow and further sold and distributed throughout Russia with the exemption of export saleswhich may be done directly.

Through the restructuring of its distribution system in Russia to increase the amount of saleseffected through direct order�taking with retail outlets, Efes Russia increased the number of out�lets served through direct order�taking in Moscow from approximately 2,500 in 2004 to approx�imately 7,000 in 2005 and approximately 11,500 in 2006.

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

Efes Russia also has exclusive sales teams in more than 135 cities and towns in Russia, includ�ing Rostov�on�Don, Ufa, Ekaterinburg, Samara, Novosibirsk and St. Petersburg. These exclusivesales teams covered approximately 29,500 and 63,000 retail outlets outside of Moscowthroughout Russia in 2005 and 2006, respectively. As of 31st of December, 2006, the total salesforce of Efes Russia consisted of 626 people, including 176 sales representatives in Moscow.About 86 per cent of Efes Russia's sales as of 31st of December, 2006 were sales to authorizeddealers pursuant to a standard dealership agreement. Efes Russia currently has approximately175 authorized dealers.

Customers

Russian off�trade retail outlets that sell beer can be broadly classified under six categories:

(i) supermarkets with a selling area of at least 300 square metres, more than two check�outsand self�service;

(ii) mini markets with a selling area of under 300 square metres and usually one or two check�outs;

(iii) food stores which stock a wide range of foods;

(iv) "kiosks", selling items such as cigarettes, beer, soft drinks, and snacks, where customers areserved through a glass window with a selling area of under 12 square metres;

(v) "pavilions", which are relatively larger kiosks in which customers can be served through thecounter; and

(vi) open markets, which are groups of kiosks or pavilions.

The majority of off�trade sales points consist of smaller retail points, with food stores constitut�ing 57.6 per cent of all off�trade retail outlets in Russia and accounting for 50.9 per cent of beersales (source: AC Nielsen). Kiosks, pavilions and open markets collectively accounted for 31.4per cent of off�trade retail outlets and 30.7 per cent of beer sales as of December 2006 (source:AC Nielsen). Supermarkets and minimarkets accounted for 11.0 per cent of off�trade retail out�lets and 18.4 per cent of beer sales as of December 2006 (source: AC Nielsen).

In 2006 top 10 customers constituted 29 per cent share in overall sales volume of Efes Russiain value terms, while LLC ìSovet Plusî, LLC ìAlitaî, LLC ìAtlasî, LLC ìRikomî, and OJSC ìMarko Poloî were listed as the main customers.

25October 2007

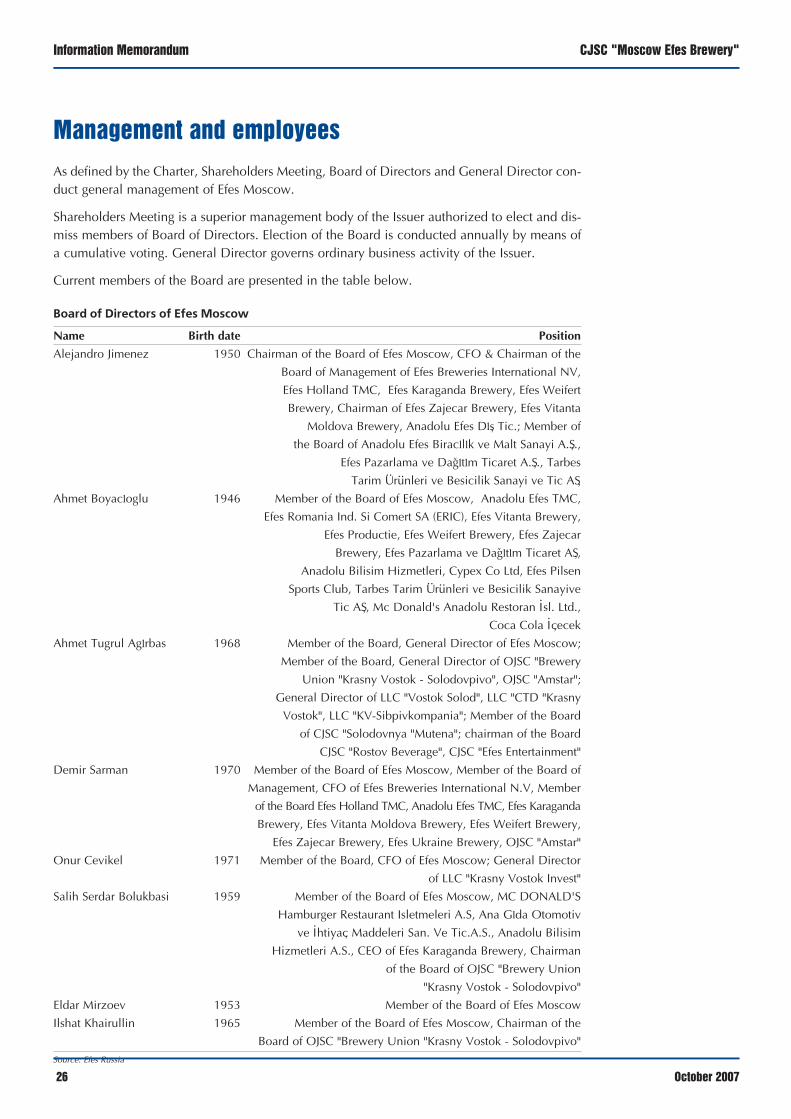

Board of Directors of Efes Moscow

Name Birth date Position

Alejandro Jimenez 1950 Chairman of the Board of Efes Moscow, CFO & Chairman of the

Board of Management of Efes Breweries International NV,

Efes Holland TMC, Efes Karaganda Brewery, Efes Weifert

Brewery, Chairman of Efes Zajecar Brewery, Efes Vitanta

Moldova Brewery, Anadolu Efes Dls, Tic.; Member of

the Board of Anadolu Efes Biraclllk ve Malt Sanayi A.S,.,

Efes Pazarlama ve Dagltlm Ticaret A.S,., Tarbes

Tarim U..

ru..nleri ve Besicilik Sanayi ve Tic AS,

Ahmet Boyacloglu 1946 Member of the Board of Efes Moscow, Anadolu Efes TMC,

Efes Romania Ind. Si Comert SA (ERIC), Efes Vitanta Brewery,

Efes Productie, Efes Weifert Brewery, Efes Zajecar

Brewery, Efes Pazarlama ve Dagltlm Ticaret AS,,

Anadolu Bilisim Hizmetleri, Cypex Co Ltd, Efes Pilsen

Sports Club, Tarbes Tarim U..

ru..nleri ve Besicilik Sanayive

Tic AS,, Mc Donald's Anadolu Restoran I.sl. Ltd.,

Coca Cola I.c,ecek

Ahmet Tugrul Aglrbas 1968 Member of the Board, General Director of Efes Moscow;

Member of the Board, General Director of OJSC "Brewery

Union "Krasny Vostok � Solodovpivo", OJSC "Amstar";

General Director of LLC "Vostok Solod", LLC "CTD "Krasny

Vostok", LLC "KV�Sibpivkompania"; Member of the Board

of CJSC "Solodovnya "Mutena"; chairman of the Board

CJSC "Rostov Beverage", CJSC "Efes Entertainment"

Demir Sarman 1970 Member of the Board of Efes Moscow, Member of the Board of

Management, CFO of Efes Breweries International N.V, Member

of the Board Efes Holland TMC, Anadolu Efes TMC, Efes Karaganda

Brewery, Efes Vitanta Moldova Brewery, Efes Weifert Brewery,

Efes Zajecar Brewery, Efes Ukraine Brewery, OJSC "Amstar"

Onur Cevikel 1971 Member of the Board, CFO of Efes Moscow; General Director

of LLC "Krasny Vostok Invest"

Salih Serdar Bolukbasi 1959 Member of the Board of Efes Moscow, MC DONALD'S

Hamburger Restaurant Isletmeleri A.S, Ana Glda Otomotiv

ve I.htiyac, Maddeleri San. Ve Tic.A.S., Anadolu Bilisim

Hizmetleri A.S., CEO of Efes Karaganda Brewery, Chairman

of the Board of OJSC "Brewery Union

"Krasny Vostok � Solodovpivo"

Eldar Mirzoev 1953 Member of the Board of Efes Moscow

Ilshat Khairullin 1965 Member of the Board of Efes Moscow, Chairman of the

Board of OJSC "Brewery Union "Krasny Vostok � Solodovpivo"Source: Efes Russia

Information Memorandum CJSC "Moscow Efes Brewery"

26

Management and employees

As defined by the Charter, Shareholders Meeting, Board of Directors and General Director con�duct general management of Efes Moscow.

Shareholders Meeting is a superior management body of the Issuer authorized to elect and dis�miss members of Board of Directors. Election of the Board is conducted annually by means ofa cumulative voting. General Director governs ordinary business activity of the Issuer.

Current members of the Board are presented in the table below.

October 2007

^

^

CJSC "Moscow Efes Brewery" Information Memorandum

Current role of each Member of the Board of Directors of Efes Moscow is as follows:

Alejandro Jimenez

■ 2007� till present � President of Efes Beer Group & Chairman of the Board of Managementand CEO of EBI

■ 2001�2007 � Managing Director, Partner of Dinesa Corp. (Mexico)

■ 1994�2001� Chief Operating Officer and Member of the Board of Directors of PanamcoMexico

■ Date of Affiliation: 30th of April, 2007

■ Date of the latest election: 29th of June, 2007 � Chairman of the Board of Efes Moscow

■ Graduated from University of Texas with a Bachelor of Science degree in ChemicalEngineering

Ahmet Boyacioglu

■ 2001� till present � Member of the Board of EFES PAZARLAMA VE DAGITIM TICARET A.S. (Istanbul)

■ 2005�2007 � President of Efes Beer Group & Chairman of the Board of Management andCEO of EBI

■ Date of Affiliation: 30th of April, 1998

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Middle East Technical University with a Bachelor's degree in BusinessManagement

Ahmet Tugrul Agirbas

■ 2001� 2005 � Marketing Director of Efes Russia

■ 2005� till present � General Director of Efes Russia

■ Date of Affiliation: 11th of October 2005

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Istanbul University with a Bachelor of Arts degree in Management

Demir Sarman

■ 2001� till present �CFO of EBI and Member of the Board of Management

■ Date of Affiliation: 28th of July, 2003

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Middle East Technical University with Bachelor of Science degree in Economics

Onur Cevikel

■ 2002� till present �CFO of Efes Moscow

■ Date of Affiliation: 26th of April, 2001

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Istanbul University with a Bachelor of Arts degree in Management

Salih Serdar Bolukbasi

■ 2007 � till present � COO of Efes Beer Group, International Beer operations

■ Date of Affiliation: 1st of October, 2007

■ 2005 � 2007 � COO of Efes Beer Group, Russia & CIS Operations

■ 2001� 2005 � General Director of Anadolu Efes Turkey Beer Operations

27October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

28

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Middle East Technical University with a Bachelor of Science degree inEconomics

Eldar Mirzoev

■ 2001� till present � Projects Manager in Efes Moscow

■ 2004 � till present � Member of the Board of OJSC "Pokrovsky Stekolny Zavod"

■ 2006 � till present � Head of representative office of Anadolu Cam Sanayi AS

■ Date of Affiliation: 30th of April, 2007

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from Azerbaijanian University of National Economy

Ilshat Khairullin

■ 2007 � till present � Chairman of the Board of OJSC "Edelveis Group"

■ 2004 � 2006� Chairman of the Board of OJSC "Brewing Union "Krasny Vostok � Solodovpivo"

■ 2006 � 2007� Chairman of the Board of OJSC "Hiring Group"

■ 1999� 2004 � General Director of OJSC "Edelveis Group"

■ Date of Affiliation: 23th of June, 2006

■ Date of the latest election: 29th of June, 2007 � Member of the Board of Efes Moscow

■ Graduated from State Agricultural University of Kazan

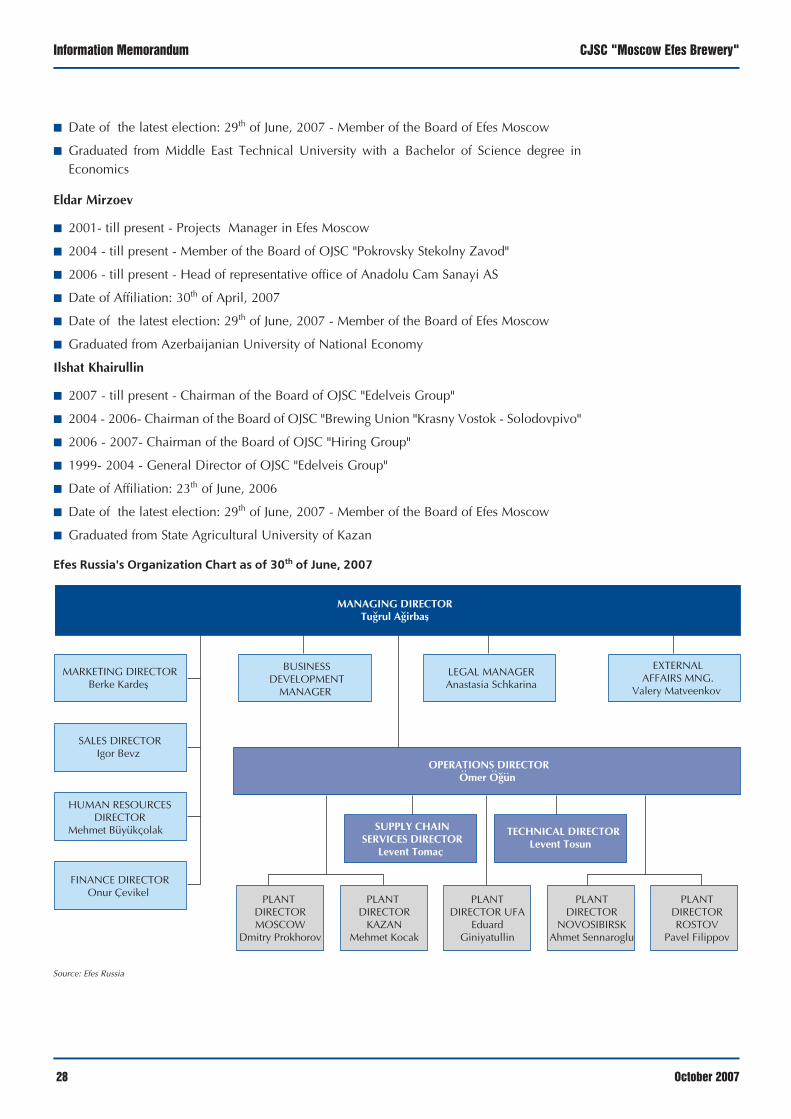

Efes Russia's Organization Chart as of 30th of June, 2007

Source: Efes Russia

October 2007

MANAGING DIRECTORTugrul Agirbas

OPERATIONS DIRECTOROmer Ogun

LEGAL MANAGERAnastasia Schkarina

BUSINESSDEVELOPMENT

MANAGER

TECHNICAL DIRECTORLevent Tosun

SUPPLY CHAINSERVICES DIRECTOR

Levent Tomac

EXTERNALAFFAIRS MNG.

Valery Matveenkov

PLANT DIRECTOR

KAZANMehmet Kocak

PLANTDIRECTOR UFA

EduardGiniyatullin

PLANTDIRECTOR

NOVOSIBIRSKAhmet Sennaroglu

PLANTDIRECTORROSTOV

Pavel Filippov

PLANT DIRECTORMOSCOW

Dmitry Prokhorov

FINANCE DIRECTOROnur Cevikel

HUMAN RESOURCESDIRECTOR

Mehmet Buyukcolak

SALES DIRECTORIgor Bevz

MARKETING DIRECTORBerke Kardes

..

.. .. ..

..

CJSC "Moscow Efes Brewery" Information Memorandum

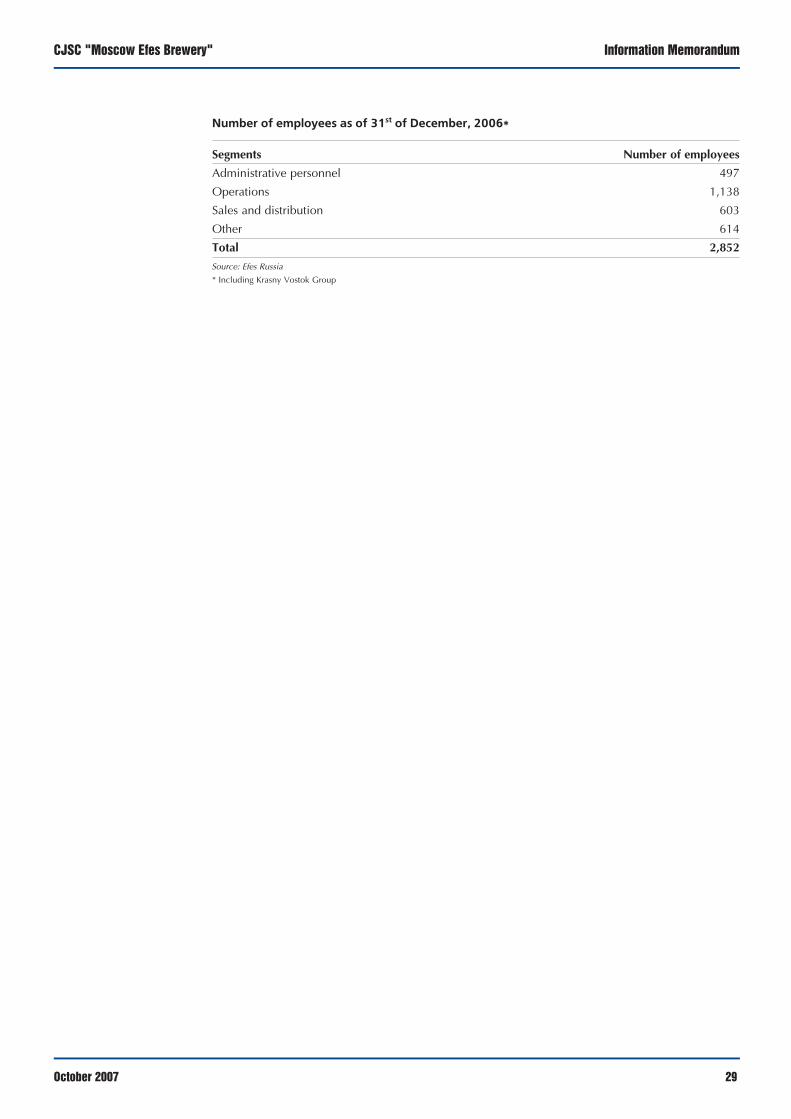

Number of employees as of 31st of December, 2006*

Segments Number of employees

Administrative personnel 497

Operations 1,138

Sales and distribution 603

Other 614

Total 2,852

Source: Efes Russia

* Including Krasny Vostok Group

29October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

30

Operations

History

Efes Moscow was incorporated by EBI in March 1997 with the participation of Knyaz Rurik JSC("Knyaz Rurik"), a closed joint stock company established by the government of the City ofMoscow, to develop a maltery and brewery complex in Moscow. Efes Moscow was establishedto build a brewery and malting complex in Moscow and undertake the production, marketingand sale of beer and malt. Construction of the Moscow brewery started in January 1998 andcommercial production commenced in May 1999. In November 2001, Efes Moscow com�menced the construction of a new state�of�the�art brewery in Rostov�on�Don, where commer�cial production began in June 2003. In May 2003 Efes Moscow acquired 100 per cent of theshare capital of OJSC Amstar ("Amstar"), whose principal asset was a brewery in Ufa, througha combination of cash and shares in Efes Moscow. In February 2006, EBI expanded its Russianoperations through the KV Group acquisition, which added two breweries in Kazan andNovosibirsk, and three malteries in Kazan.

Production facilities

Efes Russia operates breweries in each of the cities of Moscow, Rostov, Ufa, Kazan andNovosibirsk, whose annual capacity is presented in the table below. Average annual capacityutilization of Efes Russia in 2005 and 2006 was 75 per cent and 49 per cent, respectively.

Efes Russia's production capacity as of 1st of January, 2007

Site Capacity, mhl

Kazan brewery 7.0

Moscow brewery 4.6

Ufa brewery 4.1

Novosibirsk brewery 3.0

Rostov brewery 1.5

Total 20.2

Source: Efes Russia

Kazan Brewery, in the city of Kazan, the capital city of the Federal Republic of Tatarstan, is oneof the two breweries acquired through the KV Group acquisition. The establishment of theKazan brewery in its earliest form dates back to 1872, when it was founded and built in thecentre of Kazan. Most of the brewery's modernization and enlargement took place in the lastseven years, with the brewery's annual brewing capacity reaching approximately to its currentlevel of 7.0 mln hectolitres, which can be expanded up to approximately 10.0 mln hectolitresper annum within the brewery's existing infrastructure. The brewery has three adjacent malter�ies that are situated on the same area. The Kazan facility employed 669 people as of December2006. Currently, the Kazan brewery produces Beliy Medved, Krasny Vostok, Solodov,Zhigulevskoe, Gold Beer and other beer products.

Since the beginning of the construction of the Moscow brewery in 1998, Efes Moscow hasmade substantial investments to increase its capacity. The initial layout and modular infras�tructure of the brewery provided a combined platform to expand the capacity rapidly and at alower cost relative to the initial capital outlay for construction. Following the commencement

October 2007

CJSC "Moscow Efes Brewery" Information Memorandum

of its operations in 1999 with an annual capacity of 1.5 mln hectolitres, the annual capacity ofthe brewery was increased to approximately 2.2 mln hectolitres during 2001 and to approxi�mately 3.0 mln hectolitres in 2002 and then to its current annual capacity of approximately 4.6mln hectolitres in 2004. Currently, the Moscow brewery produces Beliy Medved, Stary Melnik,Sokol, Warsteiner, Zlatopramen, SOL, Bavaria and Efes beer products. The plant occupies atotal area of approximately 130,372 square meters, including a closed production area ofapproximately 20,000 square meters and a warehousing area of approximately 25,568 squaremeters. As of December 2006 Moscow facility employed 1,132 people.

Efes Moscow acquired the brewery in Ufa in August 2003. Currently, the Ufa brewery producesBeliy Medved, Stary Melnik, Sokol, Efes and Amsterdam Navigator beer products. In July 2006,the capacity of the brewery in Ufa was increased by 2.0 mln hectolitres, resulting in currentinstalled capacity of 4.1 mln hectolitres. The plant occupies a total area of 130,791 squaremeters, including a closed production area of approximately 21,204 square meters and a ware�housing area of approximately 14,296 square meters. As of December 2006 Ufa facilityemployed 435 people.

The Novosibirsk brewery, which is the second brewery acquired by the Krasny Vostok Groupacquisition, is located in Western Siberia near the cities of Tomsk, Barnaul, Kemerovo,Krasnoyarsk and Omsk. The Novosibirsk brewery was built as a greenfield project in 2002 andcontains modern infrastructure. The brewery is built on 14.2 hectares of land. Its existing brew�ing capacity is approximately 3.0 mln hectolitres per annum. As of December 2006Novosibirsk facility employed 331 people. Currently, the Novosibirsk brewery produces EfesPilsener, Stary Melnik, Sokol, Beliy Medved, Krasny Vostok, Zhigulevskoe, Gold Beer Greenbeer products.

The facility in Rostov was converted between November 2001 and June 2003 from a Coca�Cola bottling plant, which was previously operated by Anadolu Efes' soft drink business, into abrewery with an annual capacity of 1.5 mln hectolitres. The plant occupies a total area ofapproximately 67,845 square meters, including a closed production area of 13,029 squaremeters and a warehousing area of 13,992 square meters. Currently, the Rostov�on�Don brew�ery produces Beliy Medved, Sokol, Efes and Stary Melnik beer products. As of December 2006,Rostov facility employed 285 people.

The brewing process

The brewing process begins with barley, which is the fundamental ingredient of beer. Barley ismalted and combined with other ingredients such as sugar, rice, corn or wheat, which areadded to produce different beer flavours. The proportion of ancillary ingredients used in brew�ing varies according to local taste preferences and type of beer.

Malted barley is being lightly crushed into a coarse powder called grist. At this stage, the othercereals can be introduced, if required by the brewer's recipe, to produce particular character�istics of flavour or colour or appearance. The grist is transferred to a large vessel called a mashtun, where it is mashed with hot water. The natural components within malt dissolve in thewater (brewers term this water liquor), and eventually a sweet yellow liquid is run off. The wort,as it is called, is then boiled with hops in large vessels, known as coppers.

The next stage is fermentation, the most critical process of all. The hopped wort is cooled andrun into fermentation vessels. Air is dosed and yeast is added, and it begins to convert the nat�

31October 2007

Information Memorandum CJSC "Moscow Efes Brewery"

32