C.J. Jepma Foundation JIN Meerkoetlaan 30a 9765 TD Paterswolde tel.: +31(0) 50 309 68 15 e-mail:...

23

C.J. Jepma Foundation JIN Meerkoetlaan 30a 9765 TD Paterswolde tel.: +31(0) 50 309 68 15 e-mail: [email protected] the Future of the Market for Natural Gas four storylines to 2040

-

Upload

brian-barber -

Category

Documents

-

view

219 -

download

0

Transcript of C.J. Jepma Foundation JIN Meerkoetlaan 30a 9765 TD Paterswolde tel.: +31(0) 50 309 68 15 e-mail:...

C.J. Jepma

Foundation JINMeerkoetlaan 30a9765 TD Paterswolde

tel.: +31(0) 50 309 68 15e-mail: [email protected]

the Future of the Market for Natural Gas

four storylines to 2040

Goal of the study

The ultimate goal of the study is to assess what strategic action may be required from international gas market players in order to optimally address the various developments foreseen in the structure, size, and position of the international gas market as a result of the present and possibly changing trend towards more sustainable energy production, use and implementation.

New challenges to the gas industry

Can natural gas play an important role as transition fuel towards a carbon free energy system, and how will this work out in the future role of gas on the energy market?

Will security of supply of energy issues increasingly dominate public concern, and how may this affect the gas market conditions?

New challenges to the gas industry

To what extent may climate change and other environmental and safety concerns affect the trends in fossil fuel and renewable fuel use, and how will this affect the gas market share?

Will internationalisation and liberalisation of the gas market lead to more flexible but less predictable gas flows, and to what extent can flexibility in demand be matched by flexibility of supply?

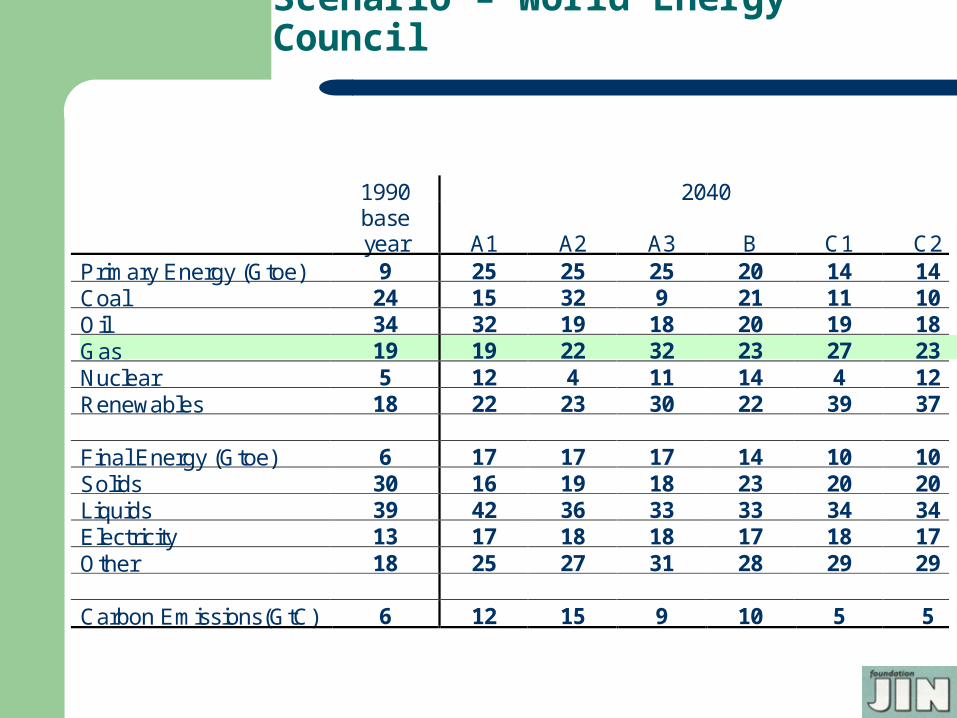

Scenario – World Energy Council

1990 2040

base year A1 A2 A3 B C1 C2

Primary Energy (Gtoe) 9 25 25 25 20 14 14 Coal 24 15 32 9 21 11 10 Oil 34 32 19 18 20 19 18 Gas 19 19 22 32 23 27 23 Nuclear 5 12 4 11 14 4 12 Renewables 18 22 23 30 22 39 37 Final Energy (Gtoe) 6 17 17 17 14 10 10 Solids 30 16 19 18 23 20 20 Liquids 39 42 36 33 33 34 34 Electricity 13 17 18 18 17 18 17 Other 18 25 27 31 28 29 29 Carbon Emissions(GtC) 6 12 15 9 10 5 5

Scenario – World Energy Council

Share of gas in primary energy is scheduled to increase from 19% in 1990 to levels ranging from 22-32% in 2040.

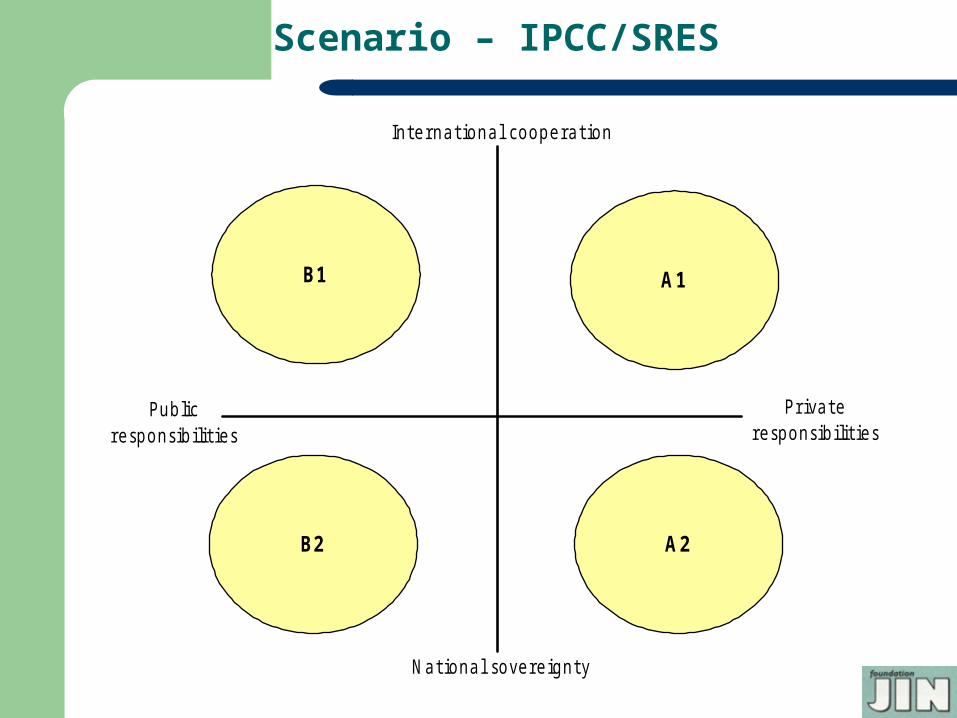

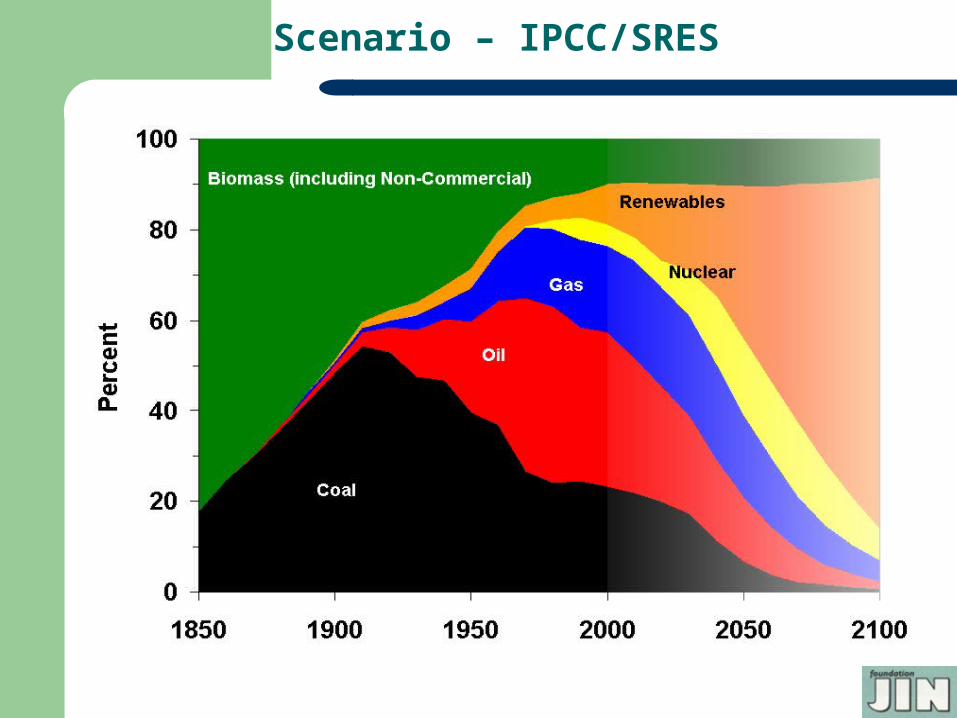

Scenario – IPCC/SRES

Envisage a number of possible developments: diffusion of existing technologies and knowledge

from the present industrialised countries to the rest of the world, slow technological development

industrialised countries strongly shift away from their traditional economic development path: emergence of ‘knowledge’ economies

world will follow a new Kondratieff wave leading to enhanced economic growth with new high-technology industries and with opportunities for developing to catch up their development

Scenario – IPCC/SRES

B1 A1

B2 A2

Nat ional sovereignty

Privateresponsibilit ies

Publicresponsibilit ies

Internat ional cooperat ion

Scenario – IPCC/SRES

Scenario – IEA

1978 2002 2010 2020 2030 2002-2030*

Coal 1407 2389 2763 3193 3601 1.5%

Oil 2413 3676 4308 5074 5766 1.6%

Gas 892 2190 2703 3451 4130 2.3%

Nuclear 29 692 778 776 764 0.4%

Hydro 104 224 276 321 365 1.8%

Biomass and waste 687 1119 1264 1428 1605 1.3%

of which traditional 490 763 828 888 920 0.7%

renewables 4 55 101 162 256 5.7%

Total 5536 10345 12194 14404 16487 1.7%

Scenario – IEA

7000

6000

5000

4000

3000

2000

1000

01970 1980 1990 2000 2010 2020 2030

Coal Oil Gas Nuclear Hydro Other

World primary energy demand by fuel (in Mtoe)

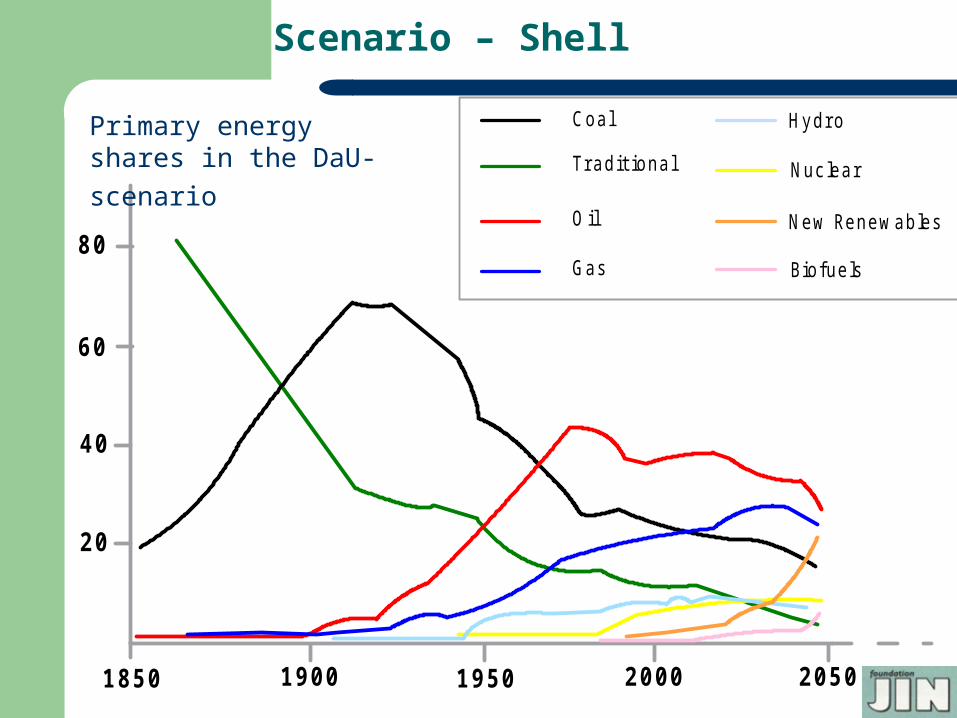

Scenario – Shell

80

60

40

20

2000 2050195019001850

Tr adit ional

Coal

O il

Gas

New Renewables

Biofuels

Hydr o

Nuc lear

Primary energy shares in the DaU-scenario

Scenario – Shell (DaU)

Dynamics as Usual 1975 2000 2025 2050 Oil 2740 3724 4918 5363 Coal 1639 2178 2998 2763 Coal CH4/H2 94 375 Gas 1101 2178 3911 4145 Nuclear 94 679 820 749 Hydro 398 703 960 913 Biofuels 117 1218 Other renewables 94 1171 4473 Total 5972 9555 14988 20000

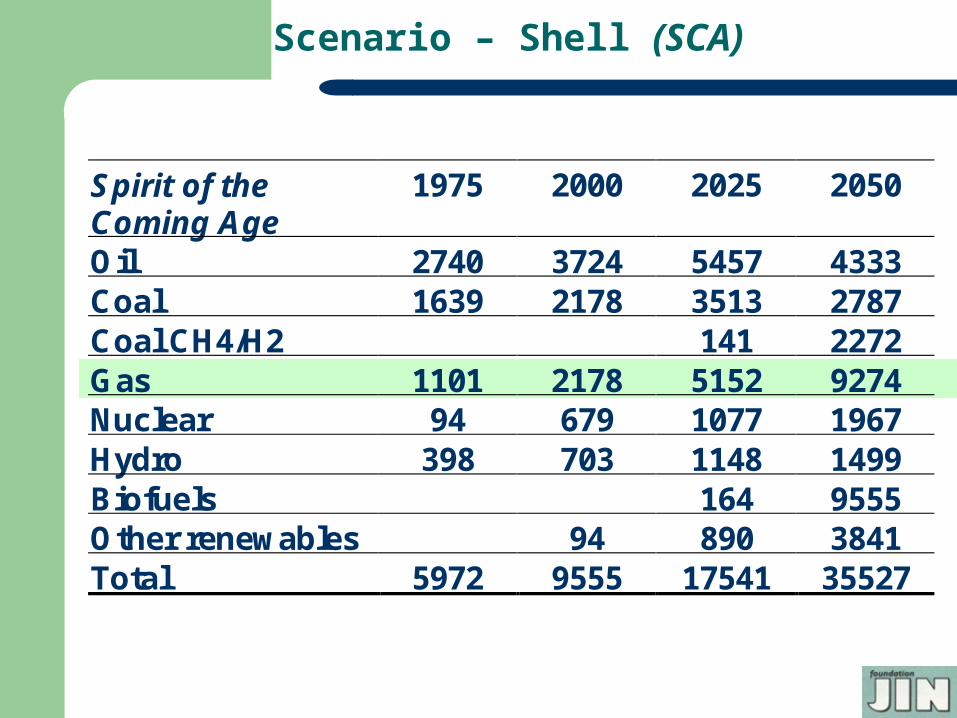

Scenario – Shell (SCA)

Spirit of the Coming Age

1975 2000 2025 2050

Oil 2740 3724 5457 4333 Coal 1639 2178 3513 2787 Coal CH4/H2 141 2272 Gas 1101 2178 5152 9274 Nuclear 94 679 1077 1967 Hydro 398 703 1148 1499 Biofuels 164 9555 Other renewables 94 890 3841 Total 5972 9555 17541 35527

Four non-traditional storylines

the role of gas as a transition fuel in a rapidly greening world

security of supply in a world with increasing gas supply - infrastructure constraints

other fuels, both traditional (incl. nuclear) and renewable ones, are increasingly successful in increasing their share in overall energy supply

the flexibility to generate sufficient swing to serve increasingly volatile demand patterns in a decentralising energy supply world.

Transition storyline

Assumptions increasing awareness of climate change risks fast and massive introduction of

commercially viable applications of renewable energy

the use of green gas (= biomass-based) is strongly promoted

decentralized energy systems based on micro CHP, small-scale renewables, and green gas become increasingly popular

large-scale biomass plantations are set up, especially in the tropics

Transition storyline

Rationale Russian Kyoto ratification, EU ETS starts‘05 potentially catastrophic unstable regime of

intermittent abrupt climate change negotiations on the post-Kyoto period regime trade policy measures are increasingly

accepted domestic power production based on coal is

already being phased out market share of CHP has already increased

fairly rapidly in industrialised countries

Security of Supply storyline

Assumptions growing concern about the availability of energy oil reserves are depleted the share of renewables remains low, nuclear

option under debate, coal is phased out for environmental reasons – gas is strategic option

Europe, NAFTA, Japan, China and India increasingly compete for the available gas resources

concerns about terrorist attacks regions increasingly try to become less

dependent on imports

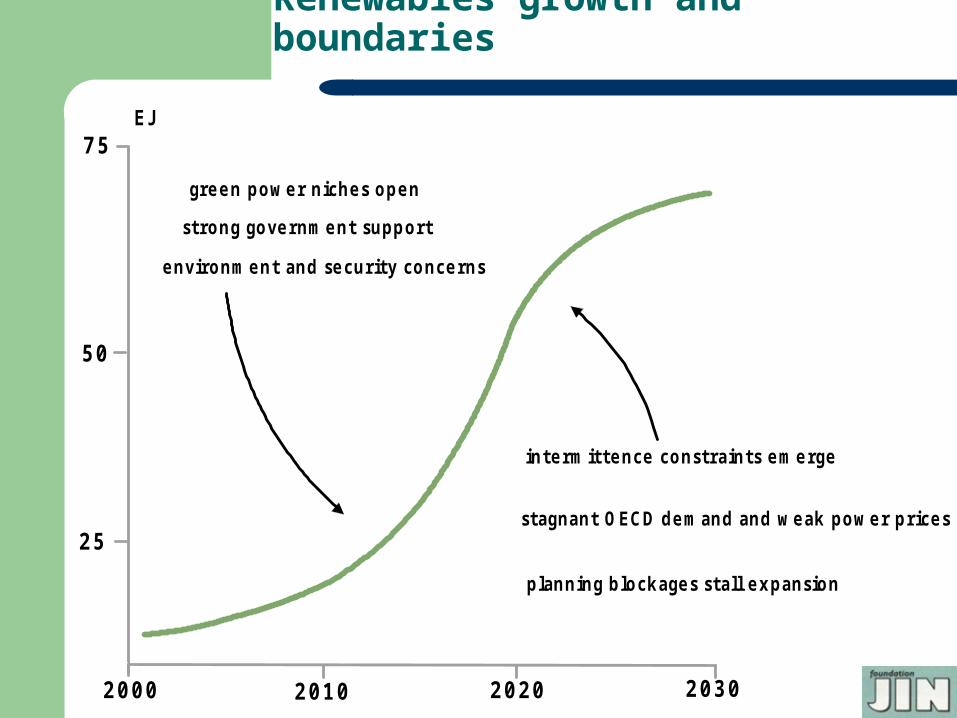

Renewables growth and boundaries

2020

75

50

25

2000 2010 2030

environment and security concerns

green pow er niches open

strong government support

intermittence constraints emerge

stagnant OECD demand and w eak power prices

planning blockages stall expansion

EJ

Gas Imports as a % of total energy consumption

20

15

10

5

2000 2010 20201970 1980 1990

J apan

Europe

North East Asia

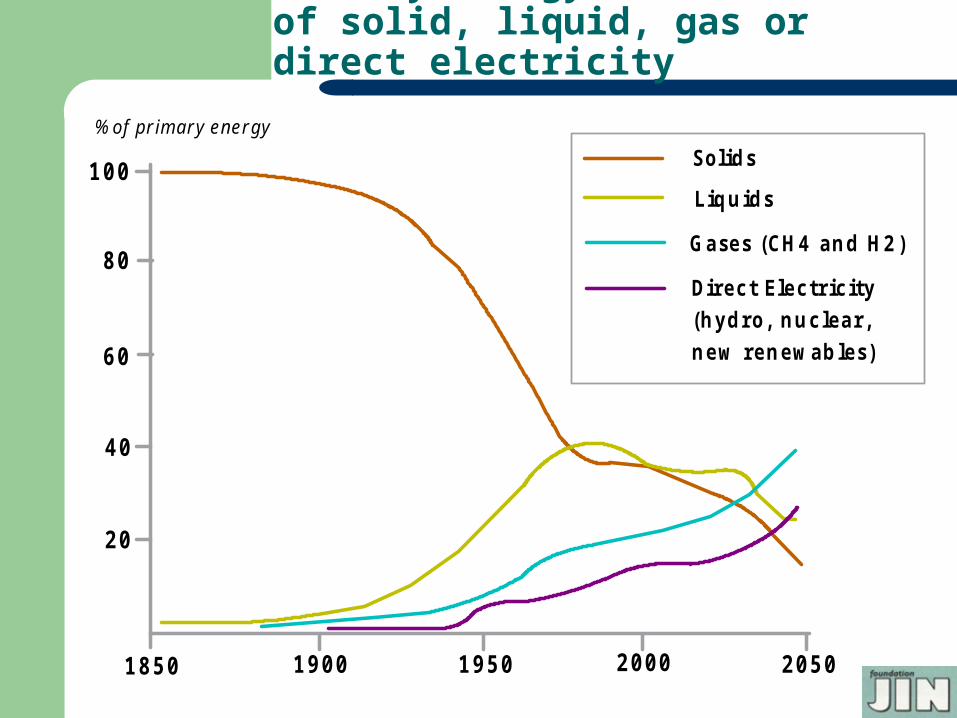

Primary energy demand in terms of solid, liquid, gas or direct electricity

80

% of pr imar y ener gy

100

60

40

20

2000 2050195019001850

Solids

Liquids

Gases (CH4 and H2)

Direct Electr ic ity(hydro, nuc lear ,new renewables)

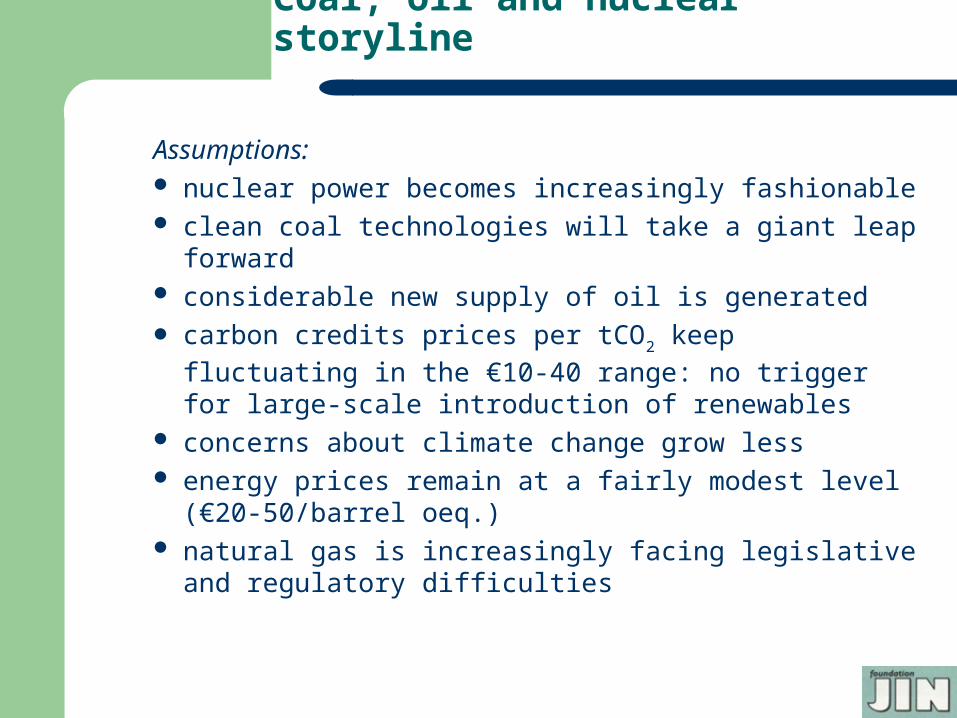

Coal, oil and nuclear storyline

Assumptions: nuclear power becomes increasingly fashionable clean coal technologies will take a giant leap

forward considerable new supply of oil is generated carbon credits prices per tCO2 keep fluctuating in

the €10-40 range: no trigger for large-scale introduction of renewables

concerns about climate change grow less energy prices remain at a fairly modest level

(€20-50/barrel oeq.) natural gas is increasingly facing legislative and

regulatory difficulties

Flexibility storyline

Assumptions: flexibility by production is increasingly taken

over by flexibility in storage and import through LNG

politics and policy driven regulatory regimes lead to underinvestment or at least suboptimal investment in gasinfrastructure

gas is seen as providing the flexibility needed gas production flexibility is less and less

available international conflicts and interventions lead to

increasing tensions and regionalised international gas markets.

![-+,+ I`r =``og` I`r =``og` >jiq`mod]g`assets.cobaltnitra.com/teams/repository/export/488/e55c0...I`r =``og` >jiq`mod]g`Ê,1 H\gdI`r =``og` >jiq`mod]g`Ê,2 Q`mnpn](https://static.fdocuments.in/doc/165x107/5fa938d4f006652a014f30a5/-ir-og-ir-og-jiqmodg-ir-og-jiqmodg1-hgdir.jpg)