CII BCG Growth Index August 2016 - CII Naoroji Godrej ... · Monthly Report August 2016...

16

Monthly Report August 2016 [email protected] it d @ ii i [email protected] dh t di@ ii i Monthly Report – August 2016 sangita.das@cii.in sandhya.satwadi@cii.in

Transcript of CII BCG Growth Index August 2016 - CII Naoroji Godrej ... · Monthly Report August 2016...

Monthly Report August [email protected]

it d @ ii [email protected]

dh t di@ ii iMonthly Report – August 2016 [email protected] [email protected]

Draft – For discussion only

Summary growth trends: August 2016Summary growth trends: August 2016

Overall, August registered a stronger growth of ~9% for the Indian industry compared to July that witnessed growth of 6%; latest IIP data also indicated a weak performance for July

Growth was relatively high across different regions with South witnessing the highest growth of ~11% for the 5th consecutive month; West saw a growth of ~9% each, while East showed an improvement clocking growth of 7%; North witnessed the lowest growth of ~6%

All

right

s re

serv

ed.

Inflation seemed to be ~1% year-on-year – similar to previous months in 2016; South saw above average price increments as indicated by an inflation of ~3%

onsu

lting

Gro

up, I

nc. A

2-wheelers (~26%), Passenger vehicles (~17%), Material Handling sector (12%) emerged as winners in August; Engineering sector (10%) and Building Materials (7%) showed healthy

2016

by

The

Bos

ton

Cog ; g g ( ) g ( ) y

growth, while Auto Components (~6%) showed modest growth and Commercial vehicles (~1.5%) witnessed relatively weak growth

1

Cop

yrig

ht ©

2

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Inflation reported above is the value over volume growth based on the survey results.Source: CII BCG Growth Index Survey; Industry association data on automotive sales

Draft – For discussion only

Survey results: August 2016 performanceSurvey results: August 2016 performance

Y Y th %

Summary – all respondents Regional growth – All respondents1

4

8

12

YoY growth %

9% 8%

4%6%6%

9% 8%7%5%

3%

VolumeValue

0

Jul’16 Aug ’16Jun’16May’16Apr’16

Industry growthPeer growth

North:6% (6%)

East

All

right

s re

serv

ed.

Industry growth comparison

Peer growth comparison

6080

Volume growth (%)

2530 2 wheelers

PV

West:9% (8%)

East:7% (7%)

Volume growth (%)

onsu

lting

Gro

up, I

nc. A60

-20-40

200

-60

40

-80 505

101520

Build. materCV

MHEOthers

PVAuto comp

Engg prod.& serv.

South:11%(8%)

Region

xx:xx% (yy%)

2016

by

The

Bos

ton

Co

Value growth (%)

-80-60 -20-80 20-40 40 80600

Value growth (%)

-5-5 0 5 10 15 20 25 30

All industry average All industry average

Valuegrowth yoy

Volume growth yoy

2

Cop

yrig

ht ©

21. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basisNote: Building materials (BM) industry refers to cement, cementitious products, paints, tiles, roofing, scaffolding. Industry average is displayed only when there are 3+ responses per industry. Other industries where responses were received include: consumer durables, Steel, chemicals, plastics, logistics, packaging, Consulting services, Financial services. Regional averages may not fully align with national average because of different regional exposures of respondent industries. All averages are 'simple averages' (i.e. not weighted by size of company). CV – Commercial vehicles, PV –Passenger vehicles, Auto Comp – Auto Components, Engg prod & services – Engineering products and services, Build. mater. – Building Materials, MHE – Material Handling EquipmentSource: CII BCG Growth Index Survey; Industry association data on automotive sales

Draft – For discussion only

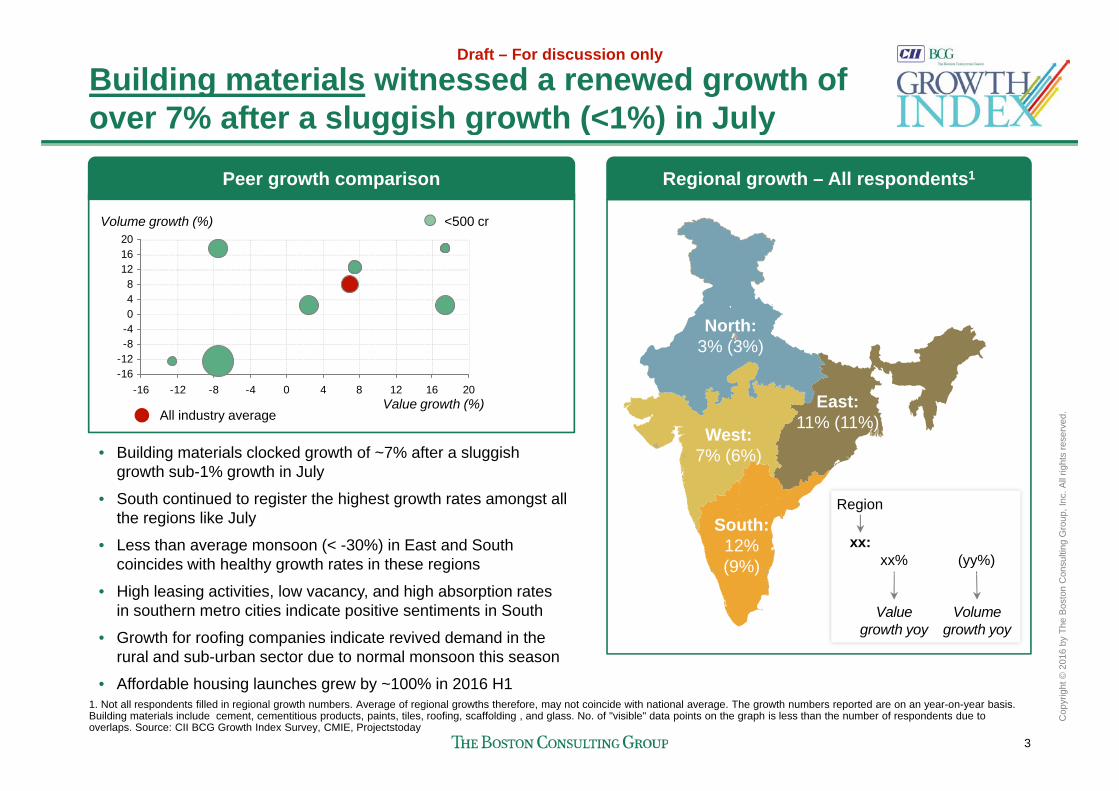

Building materials witnessed a renewed growth of over 7% after a sluggish growth (<1%) in Julyover 7% after a sluggish growth ( 1%) in July

Peer growth comparison Regional growth – All respondents1

48

121620

Volume growth (%) <500 cr

-16-12-8-40

-16 -12 -8 -4 0 4 8 12 16 20

North:3% (3%)

E t

All

right

s re

serv

ed.Value growth (%)

All industry average

• Building materials clocked growth of ~7% after a sluggish growth sub-1% growth in July

West:7% (6%)

East:11% (11%)

onsu

lting

Gro

up, I

nc. A• South continued to register the highest growth rates amongst all

the regions like July

• Less than average monsoon (< -30%) in East and South coincides with healthy growth rates in these regions

South:12%(9%)

Region

xx:xx% (yy%)

2016

by

The

Bos

ton

Co

• High leasing activities, low vacancy, and high absorption rates in southern metro cities indicate positive sentiments in South

• Growth for roofing companies indicate revived demand in the rural and sub-urban sector due to normal monsoon this season

( )

Valuegrowth yoy

Volume growth yoy

3

Cop

yrig

ht ©

2

• Affordable housing launches grew by ~100% in 2016 H11. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Building materials include cement, cementitious products, paints, tiles, roofing, scaffolding , and glass. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. Source: CII BCG Growth Index Survey, CMIE, Projectstoday

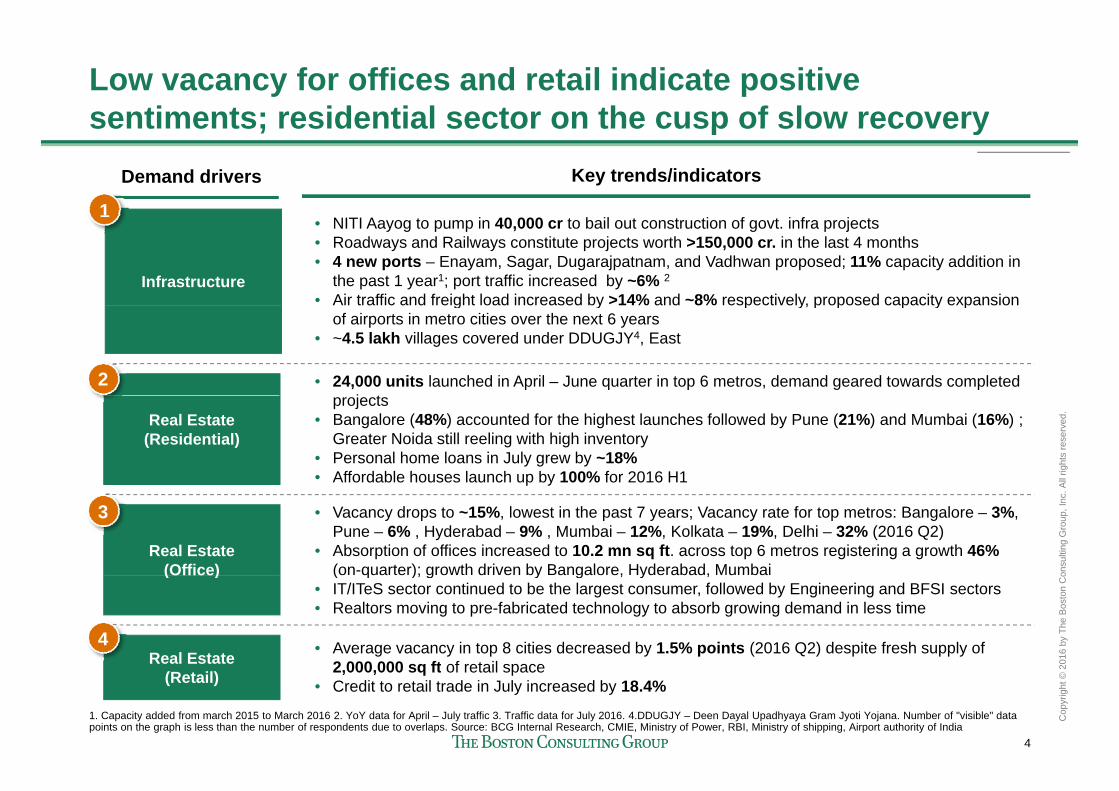

Low vacancy for offices and retail indicate positive sentiments; residential sector on the cusp of slow recoverysentiments; residential sector on the cusp of slow recovery

Demand drivers Key trends/indicators

1

Infrastructure

• NITI Aayog to pump in 40,000 cr to bail out construction of govt. infra projects• Roadways and Railways constitute projects worth >150,000 cr. in the last 4 months• 4 new ports – Enayam, Sagar, Dugarajpatnam, and Vadhwan proposed; 11% capacity addition in

the past 1 year1; port traffic increased by ~6% 2

• Air traffic and freight load increased by >14% and ~8% respectively, proposed capacity expansion

1

g y p y, p p p y pof airports in metro cities over the next 6 years

• ~4.5 lakh villages covered under DDUGJY4, East

• 24,000 units launched in April – June quarter in top 6 metros, demand geared towards completed j t

2

All

right

s re

serv

ed.

Real Estate (Residential)

projects • Bangalore (48%) accounted for the highest launches followed by Pune (21%) and Mumbai (16%) ;

Greater Noida still reeling with high inventory• Personal home loans in July grew by ~18% • Affordable houses launch up by 100% for 2016 H1

onsu

lting

Gro

up, I

nc. A

Real Estate (Office)

p y

• Vacancy drops to ~15%, lowest in the past 7 years; Vacancy rate for top metros: Bangalore – 3%, Pune – 6% , Hyderabad – 9% , Mumbai – 12%, Kolkata – 19%, Delhi – 32% (2016 Q2)

• Absorption of offices increased to 10.2 mn sq ft. across top 6 metros registering a growth 46% (on-quarter); growth driven by Bangalore, Hyderabad, Mumbai

3

2016

by

The

Bos

ton

Co(Office) (o qua e ); g o d e by a ga o e, yde abad, u ba

• IT/ITeS sector continued to be the largest consumer, followed by Engineering and BFSI sectors• Realtors moving to pre-fabricated technology to absorb growing demand in less time

Real Estate • Average vacancy in top 8 cities decreased by 1.5% points (2016 Q2) despite fresh supply of 2 000 000 sq ft of retail space

4

4

Cop

yrig

ht ©

2

1. Capacity added from march 2015 to March 2016 2. YoY data for April – July traffic 3. Traffic data for July 2016. 4.DDUGJY – Deen Dayal Upadhyaya Gram Jyoti Yojana. Number of "visible" data points on the graph is less than the number of respondents due to overlaps. Source: BCG Internal Research, CMIE, Ministry of Power, RBI, Ministry of shipping, Airport authority of India

(Retail) 2,000,000 sq ft of retail space • Credit to retail trade in July increased by 18.4%

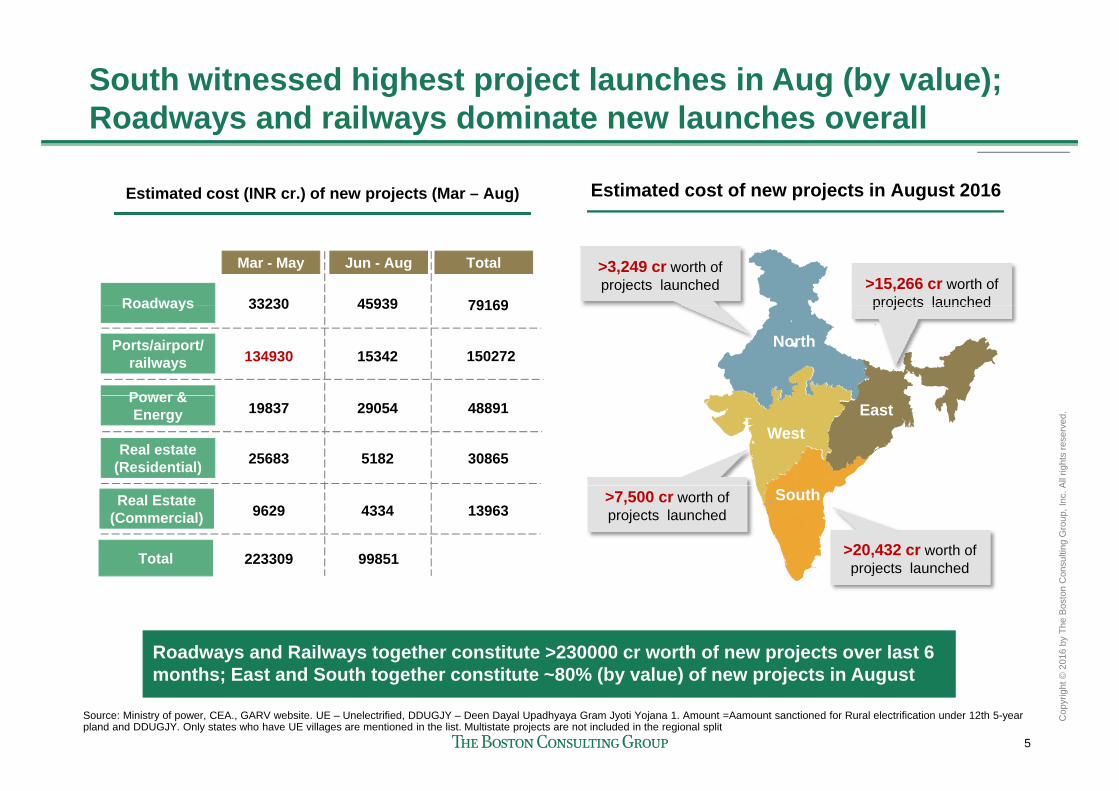

South witnessed highest project launches in Aug (by value); Roadways and railways dominate new launches overallRoadways and railways dominate new launches overall

Estimated cost of new projects in August 2016Estimated cost (INR cr.) of new projects (Mar – Aug)

>3,249 cr worth of projects launched >15,266 cr worth of

projects launchedRoadways

Mar - May

33230 45939 79169

Jun - Aug Total

North

projects launchedRoadways

Ports/airport/ railways

Power &

33230 45939

134930 15342

79169

150272

All

right

s re

serv

ed.

WestEast

Power & Energy

Real estate (Residential)

19837 29054

25683 5182

48891

30865

onsu

lting

Gro

up, I

nc. ASouth>7,500 cr worth of

projects launched

>20,432 cr worth of projects launched

Real Estate(Commercial) 9629 4334 13963

Total 223309 99851

2016

by

The

Bos

ton

Co

Roadways and Railways together constitute >230000 cr worth of new projects over last 6

p j

5

Cop

yrig

ht ©

2months; East and South together constitute ~80% (by value) of new projects in August

Source: Ministry of power, CEA., GARV website. UE – Unelectrified, DDUGJY – Deen Dayal Upadhyaya Gram Jyoti Yojana 1. Amount =Aamount sanctioned for Rural electrification under 12th 5-year pland and DDUGJY. Only states who have UE villages are mentioned in the list. Multistate projects are not included in the regional split

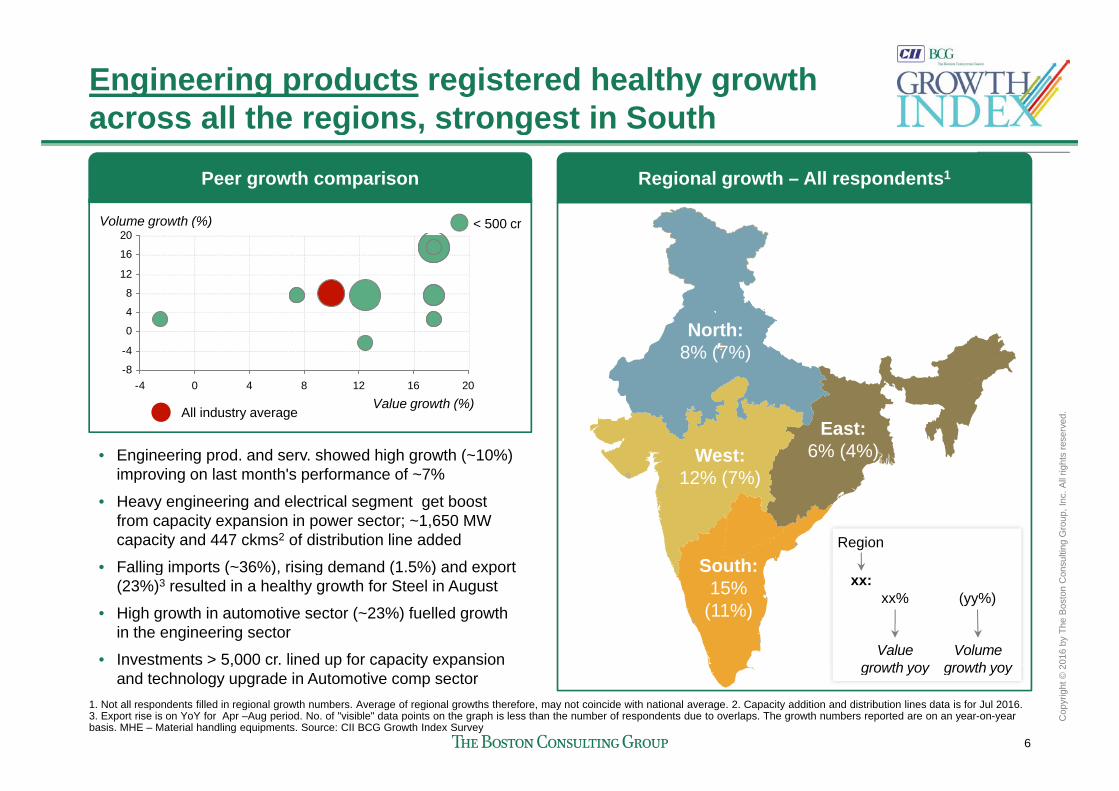

Engineering products registered healthy growth across all the regions, strongest in Southacross all the regions, strongest in South

Regional growth – All respondents1Peer growth comparison

V l h (%)

8

12

16

20Volume growth (%) < 500 cr

North:8% (7%)

-8

-4

0

4

-4 0 4 8 12 16 20

All

right

s re

serv

ed.

West:12% (7%)

East:6% (4%)

Value growth (%)All industry average

• Engineering prod. and serv. showed high growth (~10%) improving on last month's performance of ~7%

onsu

lting

Gro

up, I

nc. A

( )

South:

• Heavy engineering and electrical segment get boost from capacity expansion in power sector; ~1,650 MW capacity and 447 ckms2 of distribution line added

• Falling imports (~36%), rising demand (1.5%) and export Region

2016

by

The

Bos

ton

Co

15%(11%)

g p ( ) g ( ) p(23%)3 resulted in a healthy growth for Steel in August

• High growth in automotive sector (~23%) fuelled growth in the engineering sector

• Investments > 5,000 cr. lined up for capacity expansion Valuegro th o

Volume gro th o

xx:xx% (yy%)

6

Cop

yrig

ht ©

2

es e s 5,000 c ed up o capac y e pa s oand technology upgrade in Automotive comp sector

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. 2. Capacity addition and distribution lines data is for Jul 2016. 3. Export rise is on YoY for Apr –Aug period. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. The growth numbers reported are on an year-on-year basis. MHE – Material handling equipments. Source: CII BCG Growth Index Survey

growth yoy growth yoy

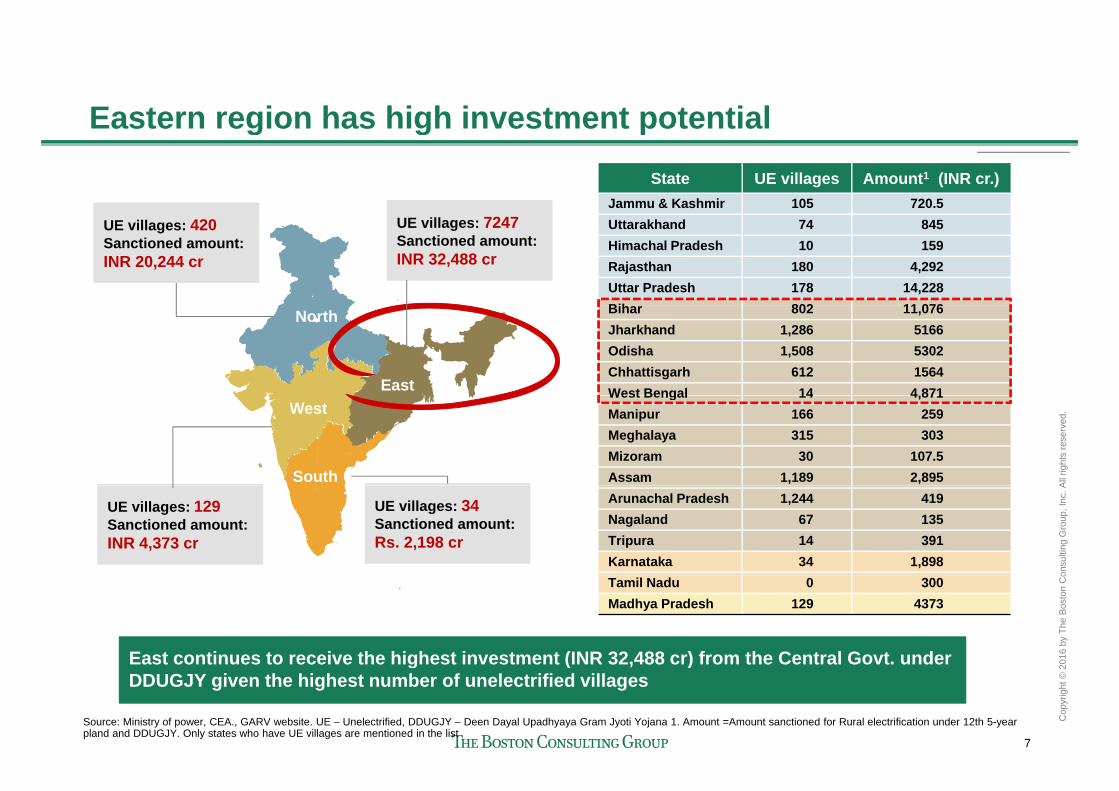

Eastern region has high investment potentialEastern region has high investment potentialState UE villages Amount1 (INR cr.)

Jammu & Kashmir 105 720.5Uttarakhand 74 845Himachal Pradesh 10 159Rajasthan 180 4,292Uttar Pradesh 178 14,228Bih 802 11 076

UE villages: 420Sanctioned amount:INR 20,244 cr

UE villages: 7247Sanctioned amount:INR 32,488 cr

Bihar 802 11,076Jharkhand 1,286 5166Odisha 1,508 5302Chhattisgarh 612 1564West Bengal 14 4 871

North

East

All

right

s re

serv

ed.

West Bengal 14 4,871Manipur 166 259Meghalaya 315 303Mizoram 30 107.5Assam 1,189 2,895

West

South

onsu

lting

Gro

up, I

nc. A

Arunachal Pradesh 1,244 419Nagaland 67 135Tripura 14 391Karnataka 34 1,898

UE villages: 129Sanctioned amount:INR 4,373 cr

UE villages: 34Sanctioned amount:Rs. 2,198 cr

2016

by

The

Bos

ton

Co

Tamil Nadu 0 300Madhya Pradesh 129 4373

East continues to receive the highest investment (INR 32,488 cr) from the Central Govt. under

7

Cop

yrig

ht ©

2

g ( , )DDUGJY given the highest number of unelectrified villages

Source: Ministry of power, CEA., GARV website. UE – Unelectrified, DDUGJY – Deen Dayal Upadhyaya Gram Jyoti Yojana 1. Amount =Amount sanctioned for Rural electrification under 12th 5-year pland and DDUGJY. Only states who have UE villages are mentioned in the list

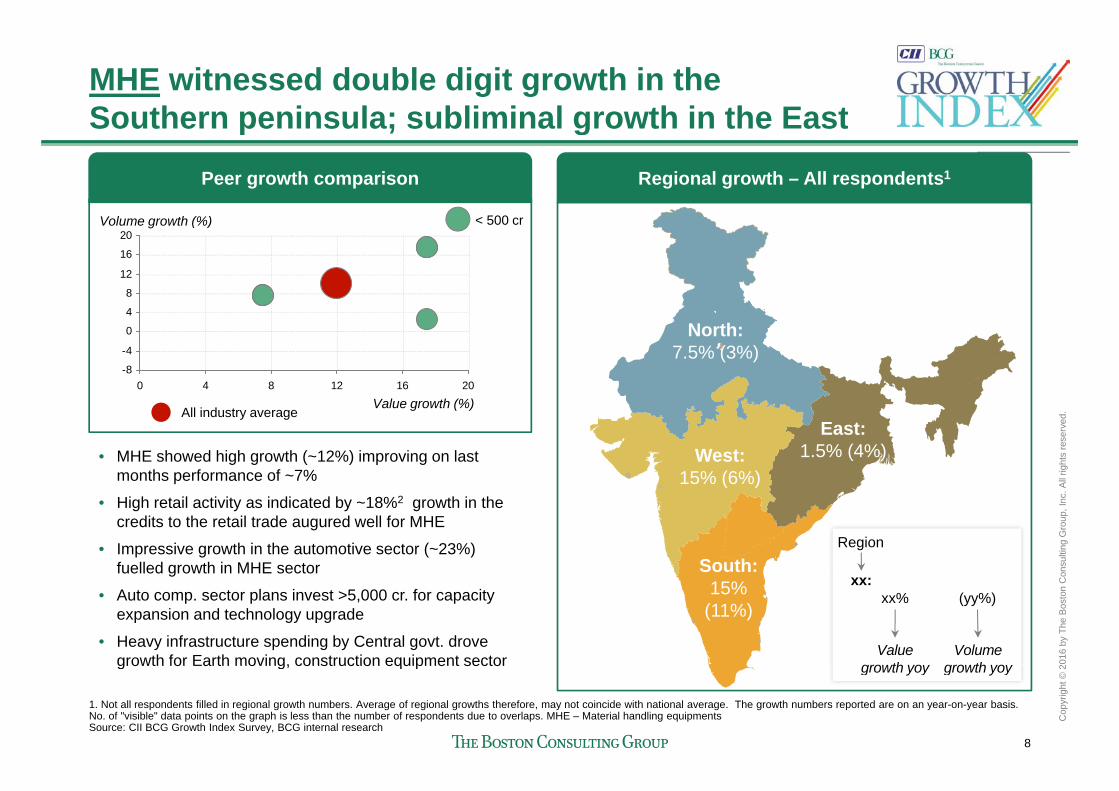

MHE witnessed double digit growth in the Southern peninsula; subliminal growth in the EastSouthern peninsula; subliminal growth in the East

Regional growth – All respondents1Peer growth comparison

V l h (%) 500

8

12

16

20Volume growth (%) < 500 cr

North:7.5% (3%)

-8

-4

0

4

0 4 8 12 16 20

All

right

s re

serv

ed.

West:15% (6%)

East:1.5% (4%)

Value growth (%)All industry average

• MHE showed high growth (~12%) improving on last months performance of ~7%

onsu

lting

Gro

up, I

nc. A

( )

South:

• High retail activity as indicated by ~18%2 growth in the credits to the retail trade augured well for MHE

• Impressive growth in the automotive sector (~23%) fuelled growth in MHE sector

Region

2016

by

The

Bos

ton

Co

15%(11%)

g

• Auto comp. sector plans invest >5,000 cr. for capacity expansion and technology upgrade

• Heavy infrastructure spending by Central govt. drove growth for Earth moving, construction equipment sector

Valuegro th o

Volume gro th o

xx:xx% (yy%)

8

Cop

yrig

ht ©

2

growth for Earth moving, construction equipment sector

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. MHE – Material handling equipmentsSource: CII BCG Growth Index Survey, BCG internal research

growth yoy growth yoy

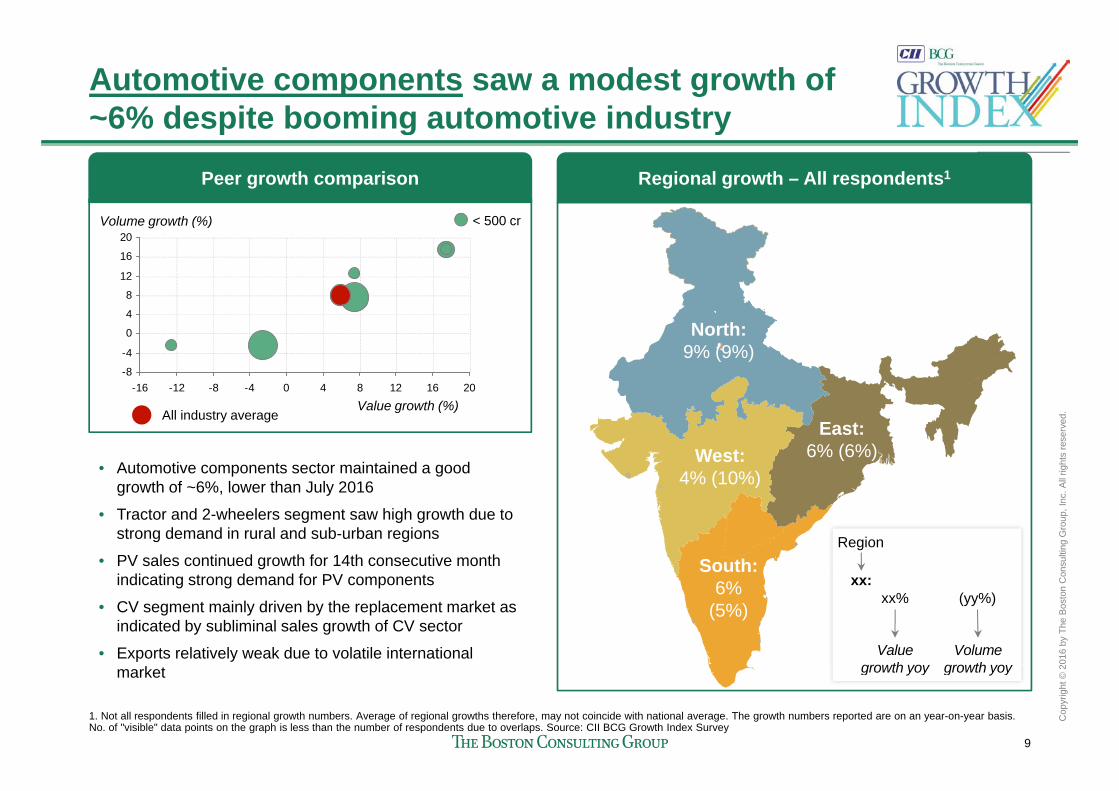

Automotive components saw a modest growth of ~6% despite booming automotive industry6% despite booming automotive industry

Regional growth – All respondents1

V l h (%) 500

Peer growth comparison

8

12

16

20Volume growth (%) < 500 cr

North:9% (9%)

-8

-4

0

4

-16 -12 -8 -4 0 4 8 12 16 20

All

right

s re

serv

ed.

West:4% (10%)

East:6% (6%)

Value growth (%)All industry average

• Automotive components sector maintained a good growth of 6% lower than July 2016

onsu

lting

Gro

up, I

nc. A

( )

South:

growth of ~6%, lower than July 2016

• Tractor and 2-wheelers segment saw high growth due to strong demand in rural and sub-urban regions

• PV sales continued growth for 14th consecutive month i di ti t d d f PV t

Region

2016

by

The

Bos

ton

Co

6%(5%)

indicating strong demand for PV components

• CV segment mainly driven by the replacement market as indicated by subliminal sales growth of CV sector

• Exports relatively weak due to volatile international Valuegro th o

Volume gro th o

xx:xx% (yy%)

9

Cop

yrig

ht ©

2market

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. Source: CII BCG Growth Index Survey

growth yoy growth yoy

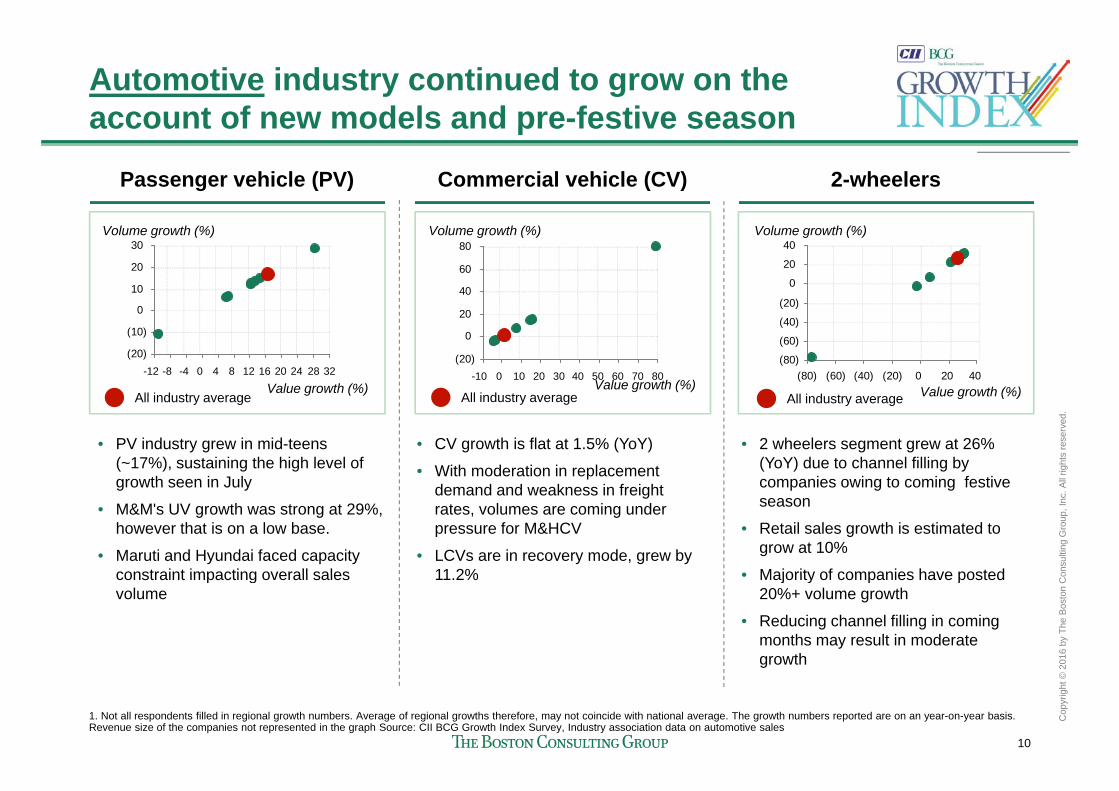

Automotive industry continued to grow on the account of new models and pre-festive seasonaccount of new models and pre festive season

Passenger vehicle (PV) Commercial vehicle (CV) 2-wheelers

0

10

20

30Volume growth (%)

40

60

80Volume growth (%)

(20)

0

20

40Volume growth (%)

Value growth (%)All industry average

(20)

(10)

0

20 24 28 3216124-12 -8 -4 80Value growth (%)

All industry average

(20)

0

20

70 806050402010 300-10Value growth (%)All i d t

(80)

(60)

(40)

(20)

(80) (60) (40) (20) 0 20 40

All

right

s re

serv

ed.

• PV industry grew in mid-teens (~17%), sustaining the high level of growth seen in July

• CV growth is flat at 1.5% (YoY)

• With moderation in replacement d d d k i f i ht

g ( )All industry average All industry average Value growth (%)All industry average

• 2 wheelers segment grew at 26% (YoY) due to channel filling by companies owing to coming festive

onsu

lting

Gro

up, I

nc. Agrowth seen in July

• M&M's UV growth was strong at 29%, however that is on a low base.

• Maruti and Hyundai faced capacity constraint impacting overall sales

demand and weakness in freight rates, volumes are coming under pressure for M&HCV

• LCVs are in recovery mode, grew by 11 2%

companies owing to coming festive season

• Retail sales growth is estimated to grow at 10%

• Majority of companies have posted

2016

by

The

Bos

ton

Coconstraint impacting overall sales

volume11.2% • Majority of companies have posted

20%+ volume growth

• Reducing channel filling in coming months may result in moderate growth

10

Cop

yrig

ht ©

2

g

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Revenue size of the companies not represented in the graph Source: CII BCG Growth Index Survey, Industry association data on automotive sales

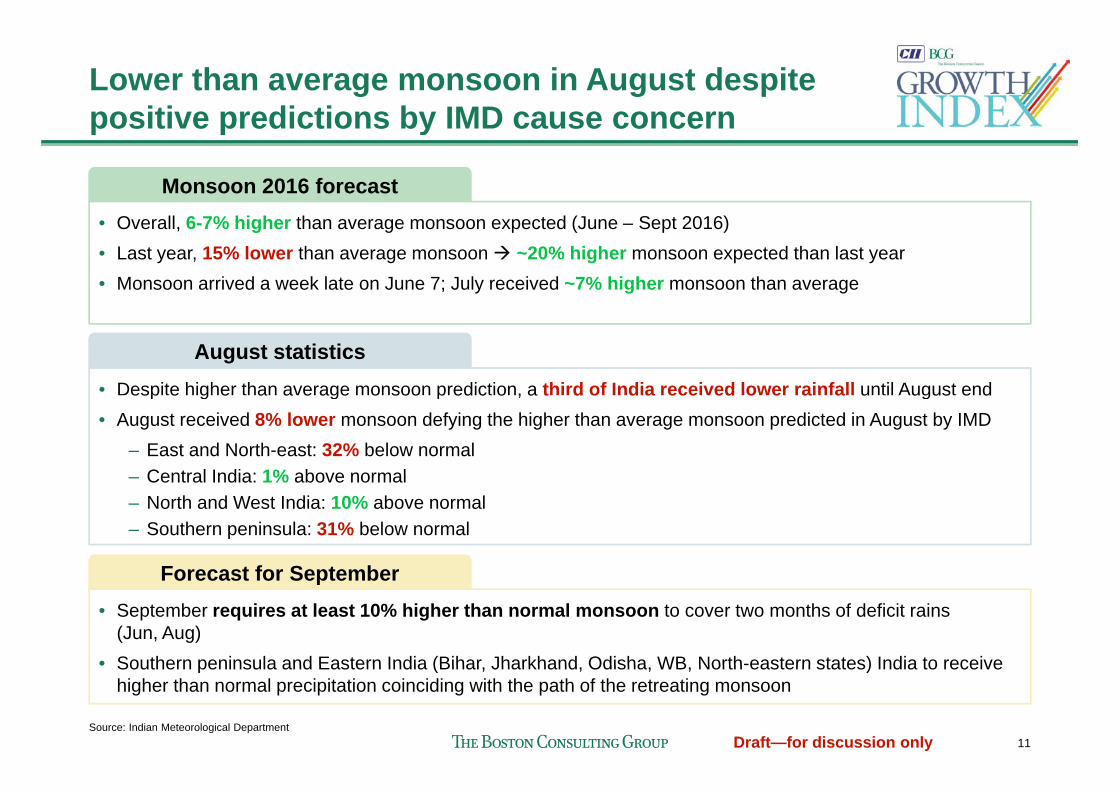

Lower than average monsoon in August despite positive predictions by IMD cause concernpositive predictions by IMD cause concern

Monsoon 2016 forecastO ll 6 7% hi h th t d (J S t 2016)• Overall, 6-7% higher than average monsoon expected (June – Sept 2016)

• Last year, 15% lower than average monsoon ~20% higher monsoon expected than last year• Monsoon arrived a week late on June 7; July received ~7% higher monsoon than average

August statistics• Despite higher than average monsoon prediction, a third of India received lower rainfall until August endesp e g e a a e age o soo p ed c o , a t d o d a ece ed o e a a u ugus e d• August received 8% lower monsoon defying the higher than average monsoon predicted in August by IMD

– East and North-east: 32% below normal– Central India: 1% above normal– North and West India: 10% above normal– Southern peninsula: 31% below normal

Forecast for SeptemberForecast for September• September requires at least 10% higher than normal monsoon to cover two months of deficit rains

(Jun, Aug) • Southern peninsula and Eastern India (Bihar Jharkhand Odisha WB North-eastern states) India to receive

11Draft—for discussion only

• Southern peninsula and Eastern India (Bihar, Jharkhand, Odisha, WB, North-eastern states) India to receive higher than normal precipitation coinciding with the path of the retreating monsoon

Source: Indian Meteorological Department

IIP index drops to -2.4% registering the sharpest fall of the year; Manufacturing sector de-grows at -3.4%of the year; Manufacturing sector de grows at 3.4%

YoY growth (%) in July 2016 Growth trends of various sectors

15

Growth (YoY)%• IIP general index plummeted to an year-low of -

2.4%• Manufacturing sectors registered a sharp decline

10

g g pde-growing at -3.4%

• Growth rates declined for both Mining and Electricity sectors at 0.8% and 1.6%,respectively

0

5

respectively• 12 out of the 22 industry groups in the

manufacturing sector saw negative growth• Losers: Electrical machinery & apparatus (-

-5

01616’1

616161616’16151515151515

Losers: Electrical machinery & apparatus (59.2%), Apparel (-16.2%), leather products (-10.1%), Wooden products (-7.9%)

• Winners: Tobacco products (22.3%), coke and refined petroleum products (12 3%) Chemicals

Aug

’

Jul’

Jun’

May

’

Apr

’

Mar

’

Feb’

Jan’

Dec

’

Nov

’

Oct

’

Sep

’

Aug

’

Jul’

GeneralElect.

Manf.Mining

refined petroleum products (12.3%), Chemicals (5.4%), Machinery equipments (8.8%)

• Consumer goods saw a marginal growth of 1.3%on the account of good performance of consumer Aug data not yet

released by the Govt

12Draft—for discussion only

durables (5.9%)

Source: CSO, Analyst Report. Note: list of "winners" and "losers" is not exhaustive

released by the Govt.

IIP indicated a slower growth for 5 out of 8 core sectors in July 2016sectors in July 2016

% weight in IIPCore Sectors Monthly growth rates (YoY) for core sectors

Coal 4.379

in IIP

512

5-124

9636200

6

y g ( )

Crude Oil

Natural Gas

5.216

1.708

-2-4-3-2-51

-5-4-3-200

3-4-7-7-10

1-15

-6-4-214-4

Petroleum Refinery 5.93914

4118

118523-4063

10158231613131618139Fertilizers

Steel

1.254

6.684

310158166131316139

-123630-3-4-8-1-2-6-1

Cement 2.406

Electricity Generation 10 316

110

2412149

3-212

-251

285

1511963091164

13Draft—for discussion only

Electricity Generation 10.316 2304

Jul-15 Oct-15 Jan-16 Apr-16 Jul-16

Source: CSO, Analyst Report.

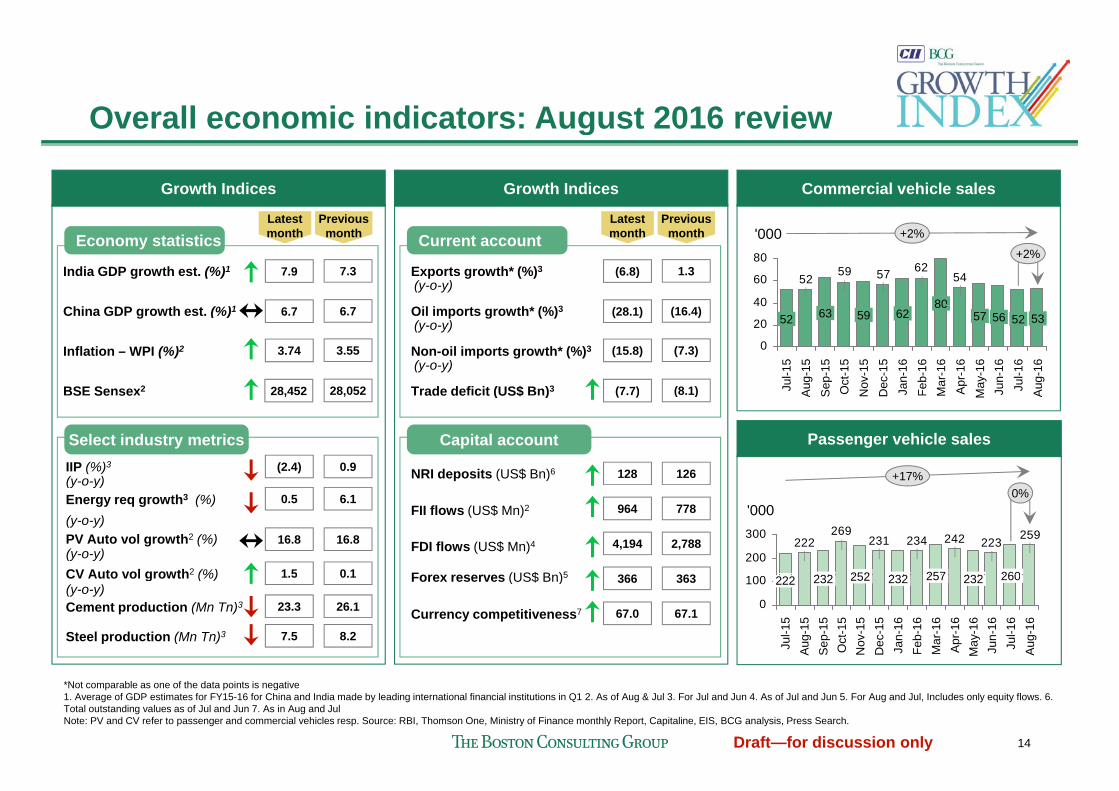

Overall economic indicators: August 2016 review

Commercial vehicle sales

Overall economic indicators: August 2016 review

L t t P i

Growth Indices Growth Indices

L t t P iLatest month

Previous month

India GDP growth est. (%)1

1

7.9 7.3

Latest month

Previous month

Exports growth* (%)3

3

(6.8) 1.3

Economy statistics Current account

(y-o-y) 54625759

52

40

60

80 +2%

+2%'000

80China GDP growth est. (%)1

Inflation – WPI (%)2

BSE Sensex2

3.74

6.7

3.55

28,052

6.7 Oil imports growth* (%)3

Non-oil imports growth* (%)3

Trade deficit (US$ Bn)3

(15.8)

(7.7)

(28.1)

(7.3)

(8.1)

(16.4)(y-o-y)

(y-o-y)0

20

40

May

-16

52

Jun-

16

53

Jul-1

6A

ug-1

6

62

Dec

-15

Nov

-15

Jan-

16

80

Feb-

16M

ar-1

6

57

Apr

-16

56

Jul-1

5

52

Aug

-15

Sep

-15

63

Oct

-15

59

28,452S Se se ,

(y-o-y)IIP (%)3 (2.4) 0.9

ade de c t (US$ ) ( ) ( )

NRI deposits (US$ Bn)6 128 126

Select industry metrics Capital account Passenger vehicle sales

M ADN MA S

+17%

,

(y-o-y)

(y o y)

(y-o-y)

CV Auto vol growth2 (%)

Energy req growth3 (%)

PV Auto vol growth2 (%)

0.5

1 5

16.8

6.1

0 1

16.8

Forex reserves (US$ Bn)5

FII flows (US$ Mn)2

FDI flows (US$ Mn)4

964

366

4,194

778

363

2,788259

223242234231269

222200

300

232

'000

260232257232252

0%

Steel production (Mn Tn)3

CV Auto vol growth (%)

Cement production (Mn Tn)3(y-o-y)

23.3

1.5

7.5

26.1

0.1

8.2

Forex reserves (US$ Bn)5

Currency competitiveness7 67.0

366

67.1

363

0

100

Oct

-15

232

Nov

-15

Dec

-15

Aug-

15

Aug-

16Ju

l-16

260

Jun-

16M

ay-1

6

232

Apr

-16

257

Mar

-16

Feb-

16

Jul-1

5

222

Jan-

16

Sep-

15

232252

14Draft—for discussion only

*Not comparable as one of the data points is negative1. Average of GDP estimates for FY15-16 for China and India made by leading international financial institutions in Q1 2. As of Aug & Jul 3. For Jul and Jun 4. As of Jul and Jun 5. For Aug and Jul, Includes only equity flows. 6. Total outstanding values as of Jul and Jun 7. As in Aug and JulNote: PV and CV refer to passenger and commercial vehicles resp. Source: RBI, Thomson One, Ministry of Finance monthly Report, Capitaline, EIS, BCG analysis, Press Search.

Thank you

bcg.com | bcgperspectives.com