CIECH - Financial results for 1Q2016

26

Financial results for 1Q16 Warsaw, 21 May 2016

-

Upload

ciech-group-ir -

Category

Investor Relations

-

view

445 -

download

0

Transcript of CIECH - Financial results for 1Q2016

Financial results for 1Q16

Warsaw, 21 May 2016

2

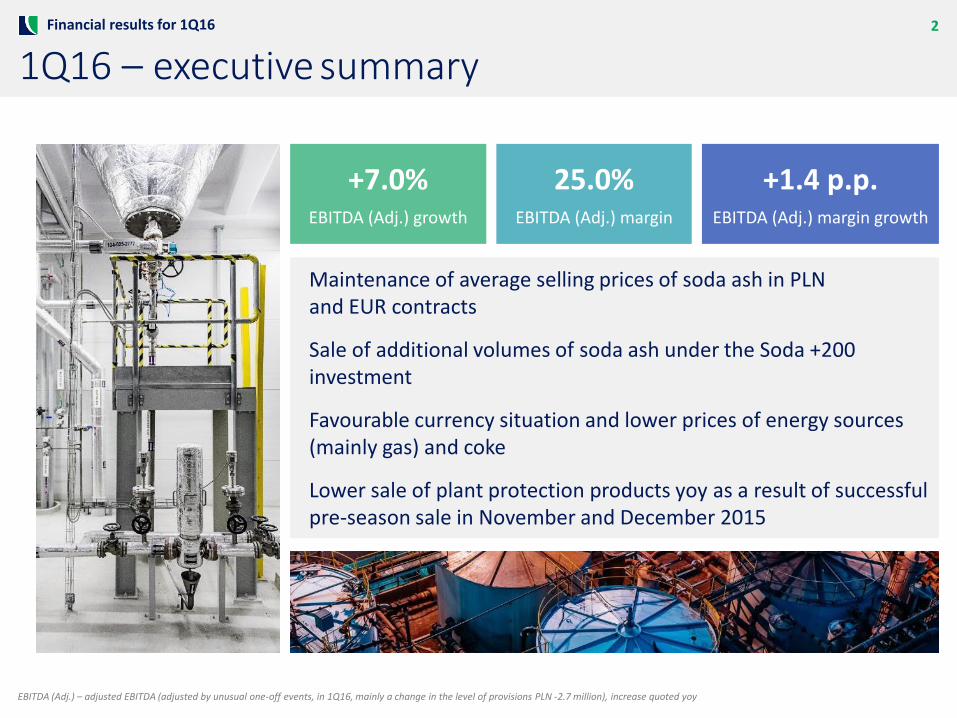

1Q16 – executive summaryFinancial results for 1Q16

+7.0%EBITDA (Adj.) growth

Maintenance of average selling prices of soda ash in PLN and EUR contracts

Sale of additional volumes of soda ash under the Soda +200 investment

Favourable currency situation and lower prices of energy sources (mainly gas) and coke

Lower sale of plant protection products yoy as a result of successful pre-season sale in November and December 2015

25.0%EBITDA (Adj.) margin

+1.4 p.p.EBITDA (Adj.) margin growth

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q16, mainly a change in the level of provisions PLN -2.7 million), increase quoted yoy

1. Market situation and major events

2. Financial results for 1Q16

3. Outlook for next quarters

4

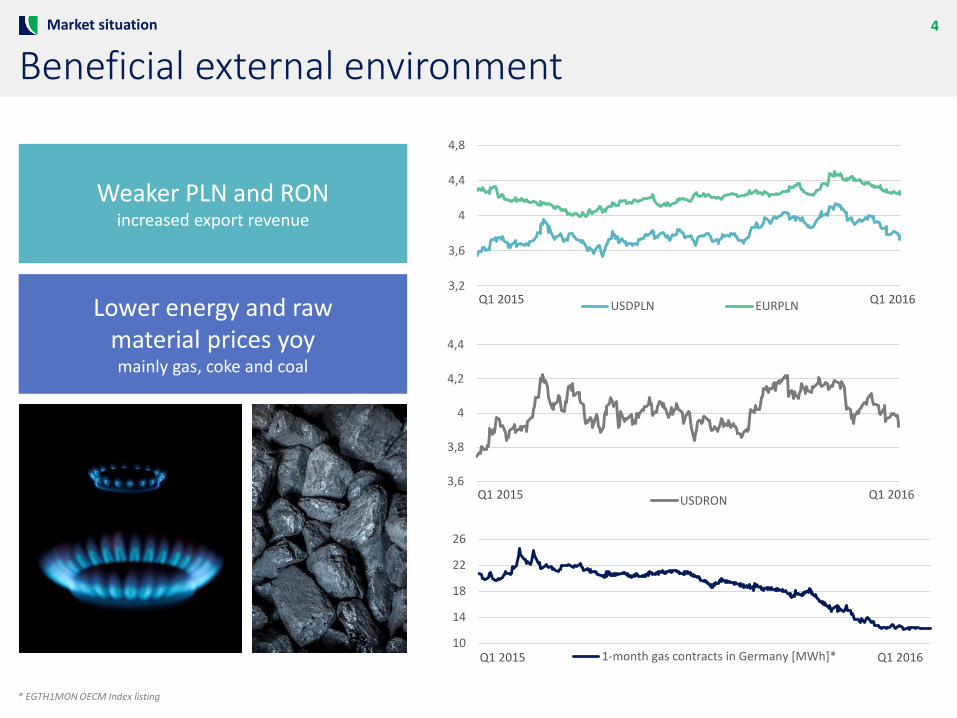

Beneficial external environmentMarket situation

Weaker PLN and RON increased export revenue

Lower energy and rawmaterial prices yoymainly gas, coke and coal

10

14

18

22

26

1-month gas contracts in Germany [MWh]*Q1 2015 Q1 2016

3,2

3,6

4

4,4

4,8

USDPLN EURPLNQ1 2015 Q1 2016

3,6

3,8

4

4,2

4,4

USDRONQ1 2015 Q1 2016

* EGTH1MON OECM Index listing

5

Market environmentMarket situation

The global and European soda ash market continues to be balanced*

*Source: IHS reports

Noticeable pressure soda

prices in overseas markets*

inflow of Chinese soda

Transfer of settlements of EU subsidies for farmers

Freezing of a large part of rapeseed and wheat crops

a necessity of re-sowing

6

The most important events of 1Q16The most important events

Launch of the second stage of the Soda +200 project and sale of additional

volumes of soda ash(in 1Q mainly light and dense compacted)

Maintenance of attractive soda ash prices (average rollover)

Contracts in PLN and EUR – a slight growth of pricesContracts in USD – drop of prices

Marketing of a new ZIEMOVIT brand

in the Home and Garden segment

Continuation of extension of the furnace for sodium silicate production

Lower costs of debt by approx. PLN 16 million in 1Q16

Lower sale of plant protection products yoy as a result of successful pre-season sale in November and December 2015

1. Market situation and major events

2. Financial results for 1Q16

3. Outlook for next quarters

8

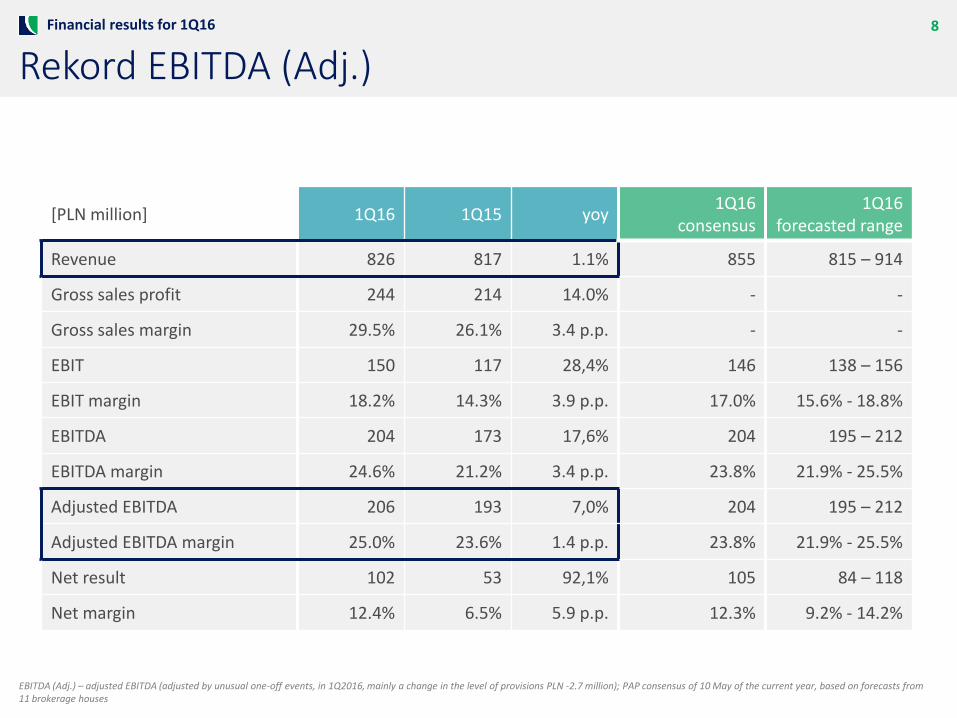

Rekord EBITDA (Adj.)

[PLN million] 1Q16 1Q15 yoy1Q16

consensus1Q16

forecasted range

Revenue 826 817 1.1% 855 815 – 914

Gross sales profit 244 214 14.0% - -

Gross sales margin 29.5% 26.1% 3.4 p.p. - -

EBIT 150 117 28,4% 146 138 – 156

EBIT margin 18.2% 14.3% 3.9 p.p. 17.0% 15.6% - 18.8%

EBITDA 204 173 17,6% 204 195 – 212

EBITDA margin 24.6% 21.2% 3.4 p.p. 23.8% 21.9% - 25.5%

Adjusted EBITDA 206 193 7,0% 204 195 – 212

Adjusted EBITDA margin 25.0% 23.6% 1.4 p.p. 23.8% 21.9% - 25.5%

Net result 102 53 92,1% 105 84 – 118

Net margin 12.4% 6.5% 5.9 p.p. 12.3% 9.2% - 14.2%

Financial results for 1Q16

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million); PAP consensus of 10 May of the current year, based on forecasts from 11 brokerage houses

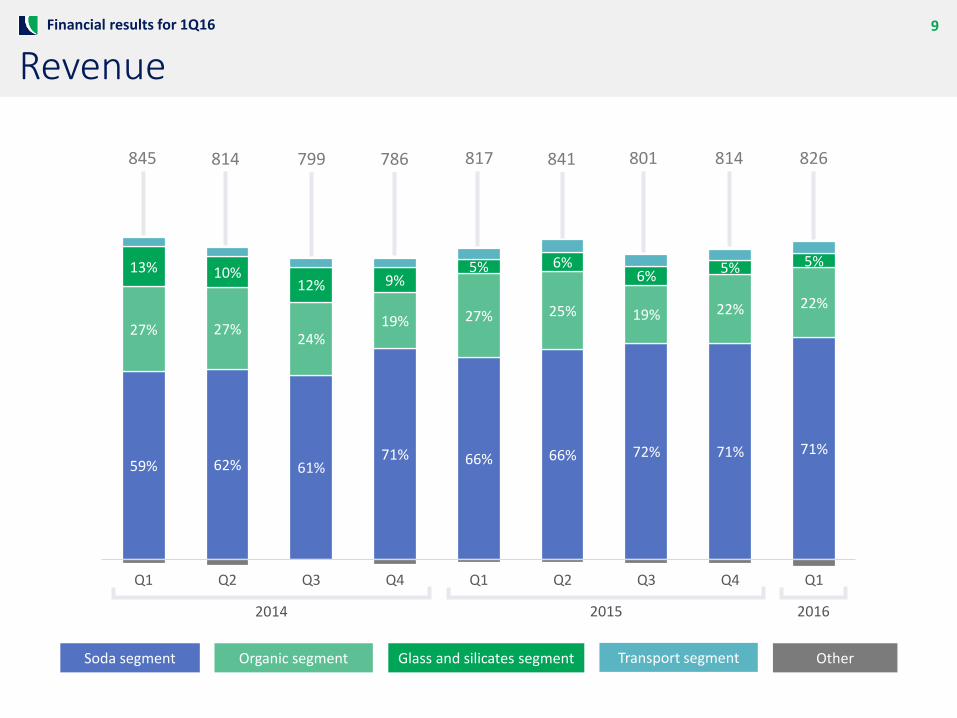

59% 62% 61%71% 66% 66% 72% 71% 71%

27% 27%24%

19% 27% 25% 19% 22% 22%

13% 10%12% 9%

5% 6%6%

5% 5%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

9

Revenue

2014

845 814 799 786 817 841 801 814 826

2015 2016

Financial results for 1Q16

Organic segment Glass and silicates segment Transport segment OtherSoda segment

10

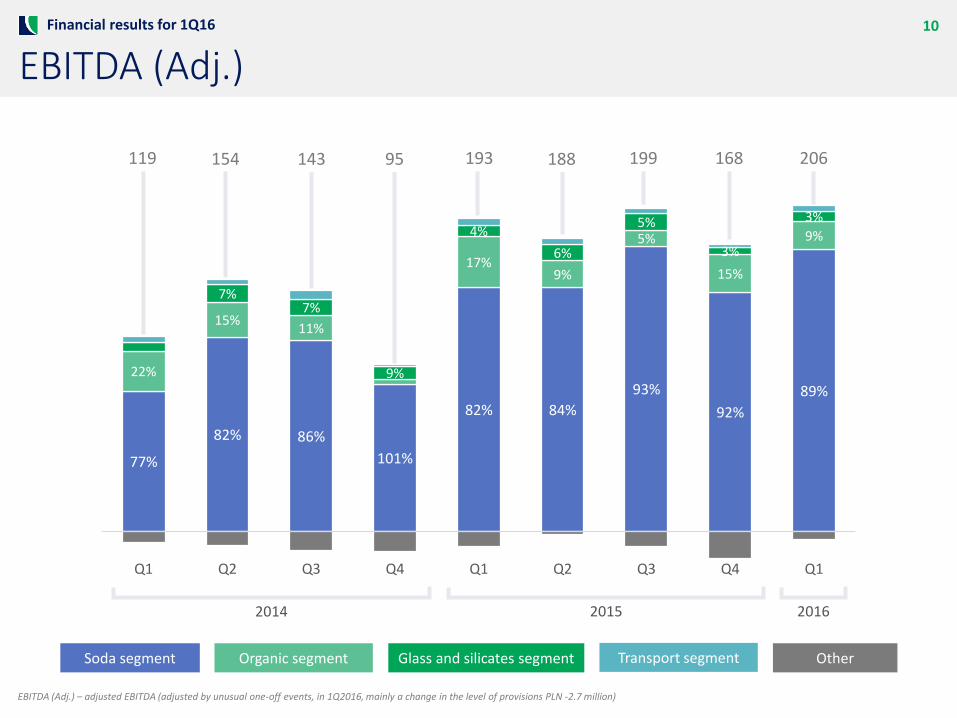

EBITDA (Adj.)

77%

82% 86%

101%

82% 84%

93%

92%

89%

22%

15%11%

17%9%

5%

15%

9%

7%7%

9%

4%

6%

5%

3%

3%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million)

2014 2015 2016

119 154 143 95 193 188 199 168 206

Financial results for 1Q16

Organic segment Glass and silicates segment Transport segment OtherSoda segment

11

Soda segmentFinancial results for 1Q16

Q1 Q2 Q3 Q4

536 590

557

574

574

2 241

2015 2016

158 183

158

185

155

656

2015 2016

In plus:

Higher production volumes

Favourable market situation – balancing of the European soda ash market with a trend for growth in demand

An insignificant selling prices growth of soda of Polish and German origin (in connection with the market situation and effective sales negotiations)

Lower prices of furnace fuel (coke) and power sources (coal, gas)

Favourable currency situation – weakening of PLN and RON

Growth of the volume of sale of dry salt and maintenance of prices

Continued increase of effectiveness of soda production process

In minus:

Drop in soda sale prices in Romania with regard to overseas export, as a result of pressure on the part of Chinese producers

Sale of additional volumes of light and compacted soda at lower prices (in connection with the launch of dense soda production –the Soda +200 project)

Partial use of more expensive coal from other suppliers (fulfilment of earlier obligations)

+10.1% +15.4%

Revenue [PLN million] EBITDA (Adj.) [PLN million]

Share in total revenue (main products)

Dense soda ash 42%

Light soda ash 12%

Salt 5%

Sodium bicarbonate 5%

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million), yoy comparison

12

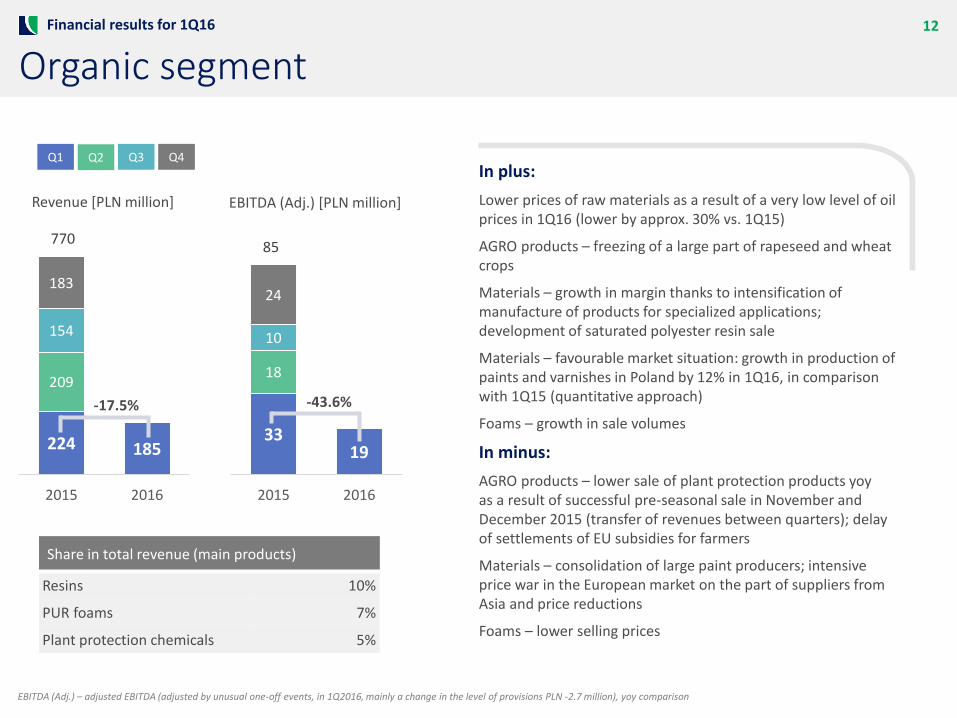

Organic segment

224 185

209

154

183

770

2015 2016

3319

18

10

24

85

2015 2016

In plus:

Lower prices of raw materials as a result of a very low level of oil prices in 1Q16 (lower by approx. 30% vs. 1Q15)

AGRO products – freezing of a large part of rapeseed and wheat crops

Materials – growth in margin thanks to intensification of manufacture of products for specialized applications; development of saturated polyester resin sale

Materials – favourable market situation: growth in production of paints and varnishes in Poland by 12% in 1Q16, in comparison with 1Q15 (quantitative approach)

Foams – growth in sale volumes

In minus:

AGRO products – lower sale of plant protection products yoy as a result of successful pre-seasonal sale in November and December 2015 (transfer of revenues between quarters); delayof settlements of EU subsidies for farmers

Materials – consolidation of large paint producers; intensive price war in the European market on the part of suppliers from Asia and price reductions

Foams – lower selling prices

Financial results for 1Q16

-17.5% -43.6%

Q1 Q2 Q3 Q4

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million), yoy comparison

Revenue [PLN million] EBITDA (Adj.) [PLN million]

Share in total revenue (main products)

Resins 10%

PUR foams 7%

Plant protection chemicals 5%

13

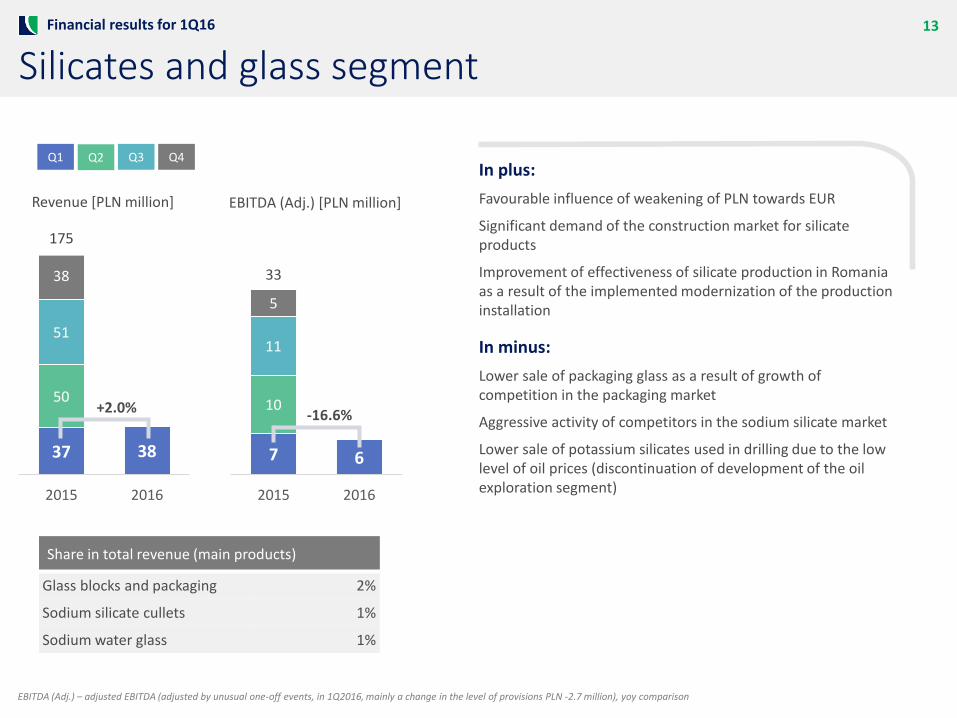

Silicates and glass segment

37 38

50

51

38

175

2015 2016

7 6

10

11

5

33

2015 2016

In plus:

Favourable influence of weakening of PLN towards EUR

Significant demand of the construction market for silicate products

Improvement of effectiveness of silicate production in Romania as a result of the implemented modernization of the production installation

In minus:

Lower sale of packaging glass as a result of growth of competition in the packaging market

Aggressive activity of competitors in the sodium silicate market

Lower sale of potassium silicates used in drilling due to the low level of oil prices (discontinuation of development of the oil exploration segment)

Financial results for 1Q16

+2.0% -16.6%

Q1 Q2 Q3 Q4

Revenue [PLN million] EBITDA (Adj.) [PLN million]

Share in total revenue (main products)

Glass blocks and packaging 2%

Sodium silicate cullets 1%

Sodium water glass 1%

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million), yoy comparison

14

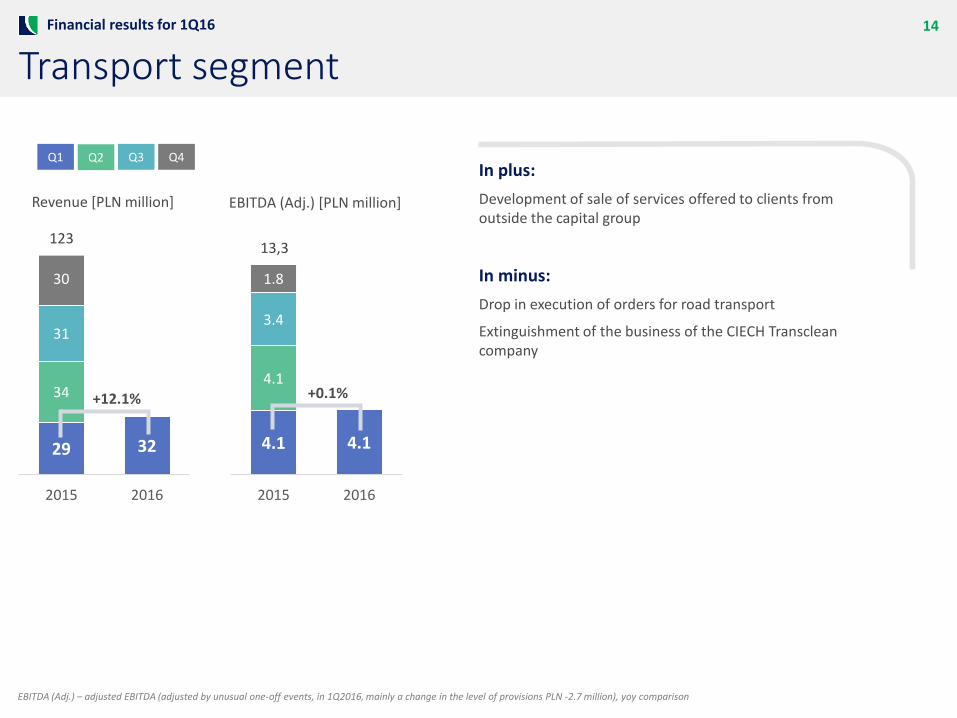

Transport segment

29 32

34

31

30

123

2015 2016

4.1 4.1

4.1

3.4

1.8

13,3

2015 2016

In plus:

Development of sale of services offered to clients from outside the capital group

In minus:

Drop in execution of orders for road transport

Extinguishment of the business of the CIECH Transclean company

Financial results for 1Q16

+12.1% +0.1%

Q1 Q2 Q3 Q4

Revenue [PLN million] EBITDA (Adj.) [PLN million]

EBITDA (Adj.) – adjusted EBITDA (adjusted by unusual one-off events, in 1Q2016, mainly a change in the level of provisions PLN -2.7 million), yoy comparison

15

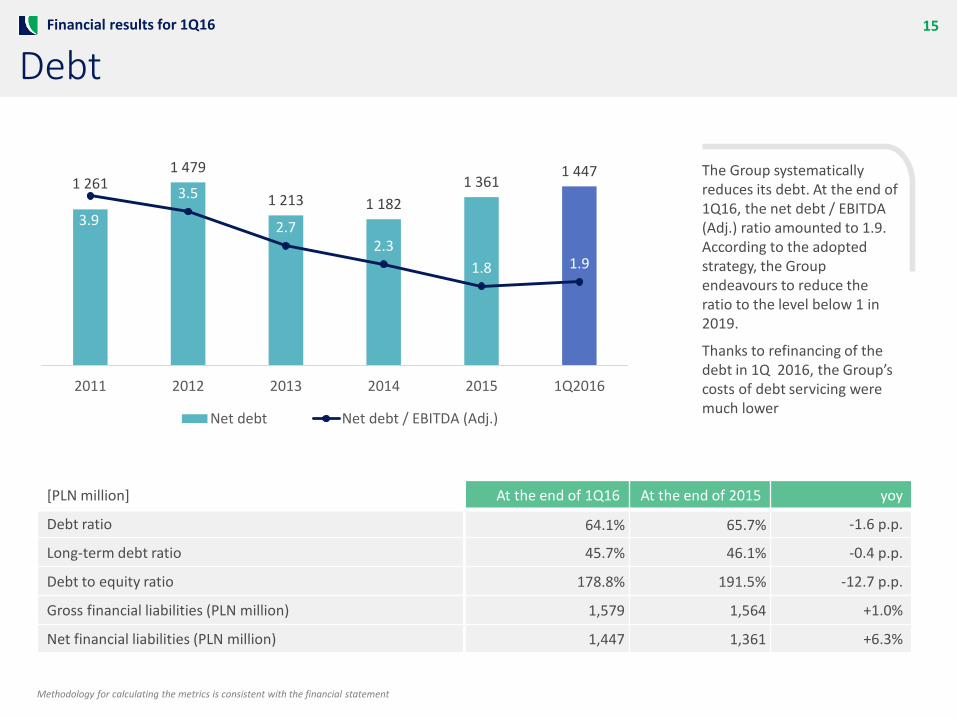

Debt

1 2611 479

1 213 1 182

1 3611 447

3.9

3.5

2.72.3

1.8 1.9

2011 2012 2013 2014 2015 1Q2016

Net debt Net debt / EBITDA (Adj.)

[PLN million] At the end of 1Q16 At the end of 2015 yoy

Debt ratio 64.1% 65.7% -1.6 p.p.

Long-term debt ratio 45.7% 46.1% -0.4 p.p.

Debt to equity ratio 178.8% 191.5% -12.7 p.p.

Gross financial liabilities (PLN million) 1,579 1,564 +1.0%

Net financial liabilities (PLN million) 1,447 1,361 +6.3%

The Group systematically reduces its debt. At the end of 1Q16, the net debt / EBITDA (Adj.) ratio amounted to 1.9. According to the adopted strategy, the Group endeavours to reduce the ratio to the level below 1 in 2019.

Thanks to refinancing of the debt in 1Q 2016, the Group’s costs of debt servicing were much lower

Financial results for 1Q16

Methodology for calculating the metrics is consistent with the financial statement

16

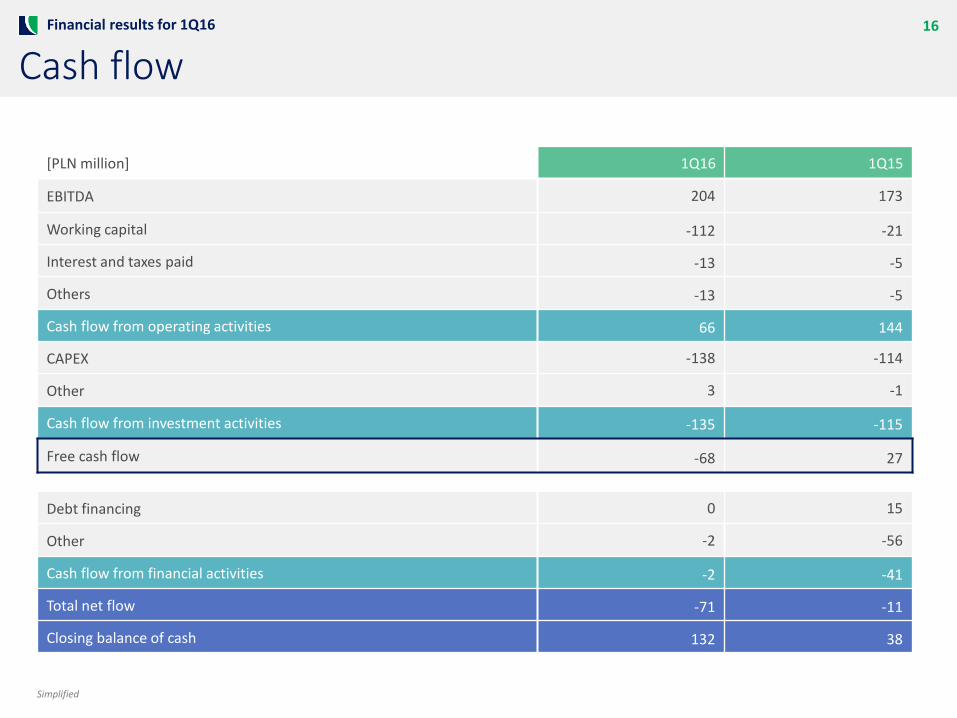

Cash flow

[PLN million] 1Q16 1Q15

EBITDA 204 173

Working capital -112 -21

Interest and taxes paid -13 -5

Others -13 -5

Cash flow from operating activities 66 144

CAPEX -138 -114

Other 3 -1

Cash flow from investment activities -135 -115

Free cash flow -68 27

Debt financing 0 15

Other -2 -56

Cash flow from financial activities -2 -41

Total net flow -71 -11

Closing balance of cash 132 38

Financial results for 1Q16

Simplified

1. Market situation and major events

2. Financial results for 1Q16

3. Outlook for next quarters

18

Challenges connected with the market environment2016 Outlook

Soda market – supply and prices

Macroeconomic situation, including the economic situation in China

Prices of energy sources, in

particular gas

Prices of oil and oil-derivative raw materials Supply of technological steam to CSR

19

High CAPEX connected with continuation of large projects2016 Outlook

Modernization and extension of the furnace

for sodium silicate production

Continuation of construction of the installation for treatment of

nitrogen and sulphur oxide fumes

Final stage of the SODA +200 project

+ approx. 1,000 other projects

=CAPEX: PLN 623 million (2016)

20

Pillars of continued development – soda and organic segments2016 Outlook

Soda segment Organic segment

Soda ash, baking soda, salt Plant protection products, materials, foams

Sale of additional volumes of soda originating from new

production capacity Development of the product portfolio in the

area of plant protection products, including the

ZIEMOVIT product lineOptimization of the salt product portfolio

Growth of product quality and concentration on more

processed products

Growth of effectiveness of the AGRO area in

CIECH Sarzyna

Increase of the share of dry salt in revenues, reduction of

exposure to weather conditions

Extension of the product portfolio of foams

with high-margin products

Expansion to foreign markets

Growth of innovativeness thanks to new initiatives in the R&D area

Glass and Silicates Segment Implementation of the contract with Solvay for supply of sodium silicate

Use of new silicate applicationsSodium silicates, potassium silicates

Appendices

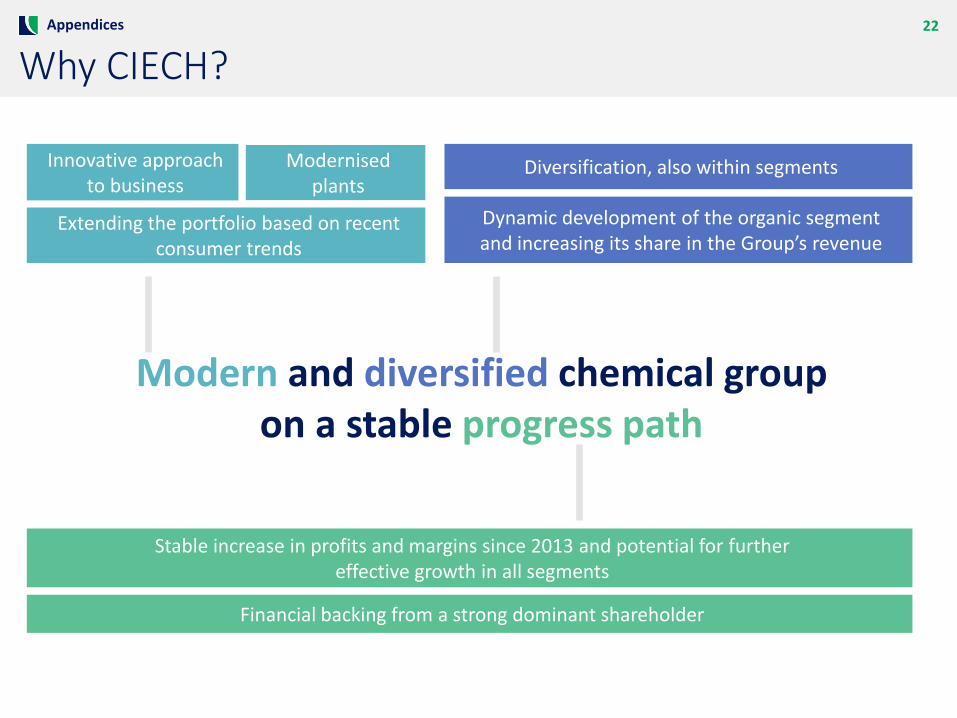

22

Why CIECH?

Modern and diversified chemical groupon a stable progress path

Innovative approach to business

Diversification, also within segments

Stable increase in profits and margins since 2013 and potential for furthereffective growth in all segments

Financial backing from a strong dominant shareholder

Dynamic development of the organic segmentand increasing its share in the Group’s revenue

Extending the portfolio based on recent consumer trends

Modernised plants

Appendices

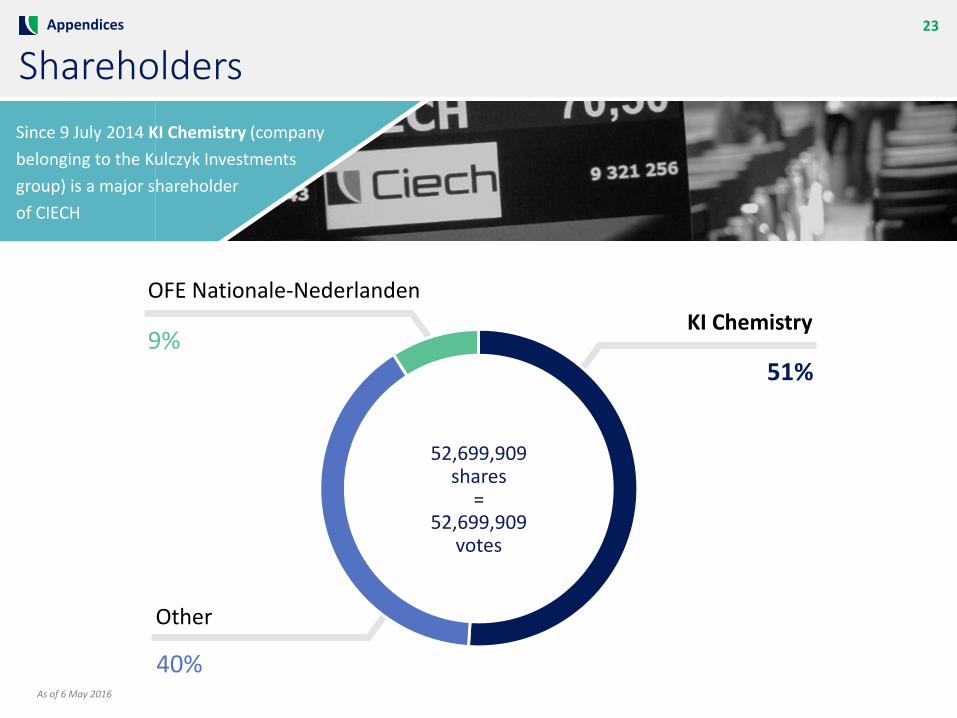

23

ShareholdersAppendices

KI Chemistry

OFE Nationale-Nederlanden

Other

52,699,909shares

=52,699,909

votes

Since 9 July 2014 KI Chemistry (company

belonging to the Kulczyk Investments

group) is a major shareholder

of CIECH

9%51%

40%As of 6 May 2016

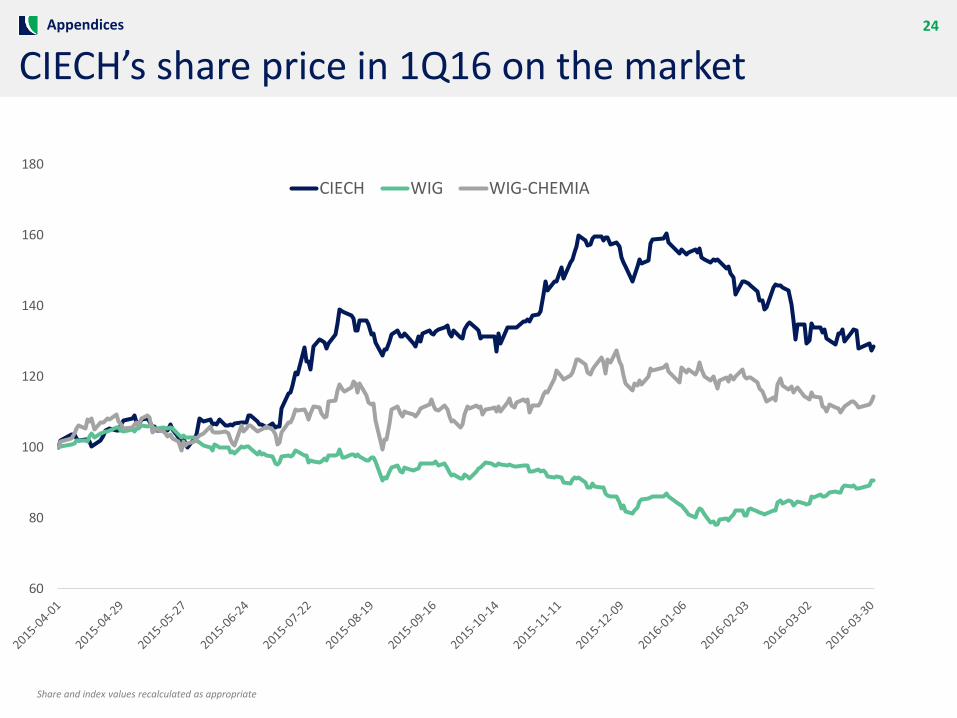

24

CIECH’s share price in 1Q16 on the market

60

80

100

120

140

160

180

CIECH WIG WIG-CHEMIA

Appendices

Share and index values recalculated as appropriate

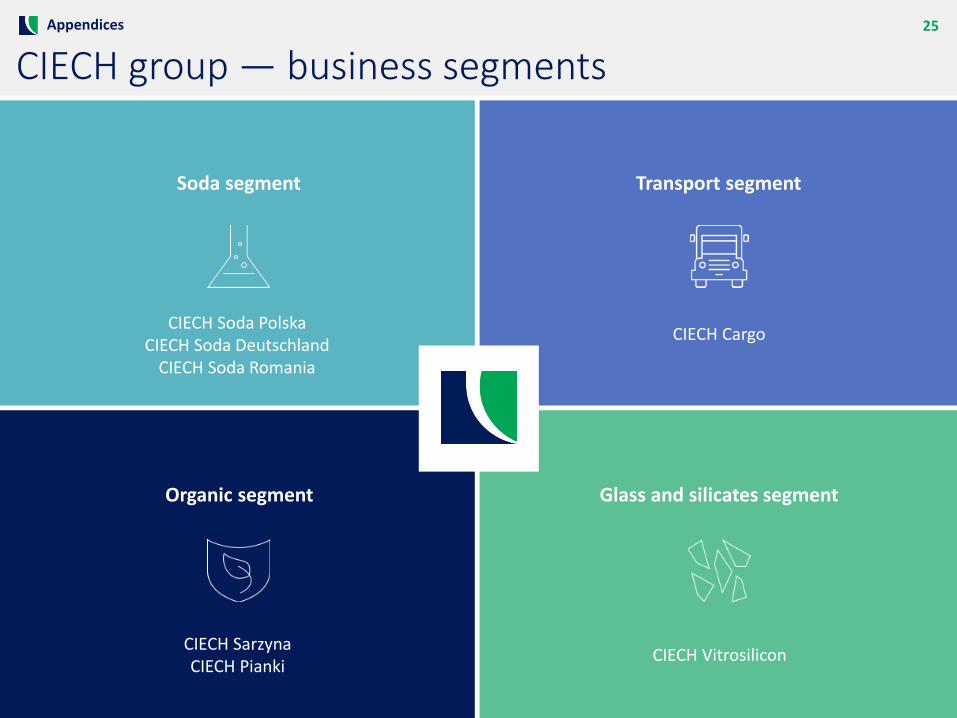

Segment

25

CIECH group — business segments

Soda segment

Salt

Organic segment

Transport segment

Glass and silicates segment

CIECH Soda PolskaCIECH Soda Deutschland

CIECH Soda Romania

CIECH Cargo

CIECH SarzynaCIECH Pianki

CIECH Vitrosilicon

Appendices

This document has been prepared solely for informational purposes. It includes only summary information, is not exhaustive, and may not be used as a sole basis for any assessment or analysis. CIECH S.A. makes no guarantees (explicit or implicit) regarding information presented herein and such information, including forecasts, estimates and opinions, should not be unduly relied upon. CIECH S.A. does not accept any responsibility for possible mistakes, omissions or irregularities found herein. The document is based on sources of information which CIECH S.A. deems to be reliable and accurate, however, it does not guarantee them to be exhaustive nor to fully reflect the actual situation. This document does not constitute an advertisement or a public offer of securities. It may include forward-looking statements that involve investment risks or uncertainties and may significantly differ from actual results. CIECH S.A does not accept any responsibility for consequences of decisions made based on this document. The responsibility lies exclusively with the party using the document. This document is protected by the Copyright and Related Rights Act. Copying, publishing or distributing it requires prior written consent of CIECH S.A.

CONTACT FOR INVESTORS:Joanna Siedlaczek - Investor Relations Expert+48 669 600 567, [email protected]

Modern and diversified chemical groupon a stable progress path