Chapter Planning

40

CHAPTER 1 --------------------------------------------------------------------------------------------------------------- - 1.1 INTRODUCTION : Deriv at ives are on e of the most complex instruments. Th e wo rd derivative comes from the word ‘to derive’. It indicates that it has no independent value. A derivative is a contract whose value is derived from the value of another asset, known as the underlying asset, which could e a share, a stock market index, an interest rate, a commodity, or a currency. The underlying is the identification tag for a derivative contract. !hen the price of the underlying changes, the value of the derivative also changes. !ithout an underlying asset, derivatives do not have any meaning. "or example, the value of a gold futures contract derives from the value of the underlying asset i.e., gold. The prices in the derivatives market are driven y the spot or cash market price of the underlying asset, which is gold in this example. Derivatives are very similar to insurance. Insurance protects against specific risks, such as fire, floods, theft and so on. Derivatives on the other hand, take care of market risks # volatility in interest rates, currency rates, commodity prices, and share prices. Derivatives offer a sound mechanism for insuring against va rio us ki nds of ri sks ar ising in the wo rld of fi nance. They of fer a range of mec hanisms to improve redistri ution of risk, which can e ext end ed to every product existing, from coffee to cotton and live cattle to det instruments. In this era of gloalisation, the world is a riskier place and exposure to risk is growing. $isk cannot e avoided or ignored. %an, howev er is risk averse. The risk averse characteristic of human eings has rought aout growth in derivatives. Derivatives help the risk averse individuals y offering a mechanism for hedging risks. Derivative pro duc ts, several centuries ago , emerged as hedgin g devices against fluctuations in commodity prices. &ommodity futures and options 1

-

Upload

delson-bhatkhande -

Category

Documents

-

view

218 -

download

0

Transcript of Chapter Planning

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 1/40

CHAPTER 1---------------------------------------------------------------------------------------------------------------

-

1.1 INTRODUCTION :

Derivatives are one of the most complex instruments. The word

derivative comes from the word ‘to derive’. It indicates that it has no independent

value. A derivative is a contract whose value is derived from the value of another

asset, known as the underlying asset, which could e a share, a stock market index,

an interest rate, a commodity, or a currency. The underlying is the identification tag

for a derivative contract. !hen the price of the underlying changes, the value of the

derivative also changes. !ithout an underlying asset, derivatives do not have any

meaning. "or example, the value of a gold futures contract derives from the value of

the underlying asset i.e., gold. The prices in the derivatives market are driven y the

spot or cash market price of the underlying asset, which is gold in this example.

Derivatives are very similar to insurance. Insurance protects againstspecific risks, such as fire, floods, theft and so on. Derivatives on the other hand,

take care of market risks # volatility in interest rates, currency rates, commodity

prices, and share prices. Derivatives offer a sound mechanism for insuring against

various kinds of risks arising in the world of finance. They offer a range of

mechanisms to improve redistriution of risk, which can e extended to every

product existing, from coffee to cotton and live cattle to det instruments.

In this era of gloalisation, the world is a riskier place and exposure to

risk is growing. $isk cannot e avoided or ignored. %an, however is risk averse. The

risk averse characteristic of human eings has rought aout growth in derivatives.

Derivatives help the risk averse individuals y offering a mechanism for hedging

risks.

Derivative products, several centuries ago, emerged as hedging

devices against fluctuations in commodity prices. &ommodity futures and options

1

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 2/40

have had a lively existence for several centuries. "inancial derivatives came into the

limelight in the post#'()* period+ today they account for ) percent of the financial

market activity in -urope, orth America, and -ast Asia. The asic difference

etween commodity and financial derivatives lies in the nature of the underlyinginstrument. In commodity derivatives, the underlying asset is a commodity+ it may e

wheat, cotton, pepper, turmeric, corn, orange, oats, /oya eans, rice, crude oil,

natural gas, gold, silver, and so on. In financial derivatives, the underlying includes

treasuries, onds, stocks, stock index, foreign exchange, and -uro dollar deposits.

The market for financial derivatives has grown tremendously oth in terms of variety

of instruments and turnover.

0resently, most ma1or institutional orrowers and investors use

derivatives. /imilarly, many act as intermediaries dealing in derivative transactions.

Derivatives are responsile for not only increasing the range of financial products

availale ut also fostering more precise ways of understanding, 2uantifying and

managing financial risk.

Derivatives contracts are used to counter the price risks involved in

assets and liailities. Derivatives do not eliminate risks. They divert risks from

investors who are risk averse to those who are risk neutral. The use of derivatives

instruments is the part of the growing trend among financial intermediaries like

anks to sustitute off#alance sheet activity for traditional lines of usiness. The

exposure to derivatives y anks have implications not only from the point of capital

ade2uacy, ut also from the point of view of estalishing trading norms, usiness

rules and settlement process. Trading in derivatives differ from that in e2uities as

most of the derivatives are market to the market.

2

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 3/40

1.2 DEFINITION OF DERIVATIVES :

Derivative is a product whose value is derived from the value of one or

more asic variales, called ases 3underlying asset, index, or reference rate4, in a

contractual manner. The underlying asset can e e2uity, forex, commodity or any

other asset.

According to Securities Contracts (Reu!ation" Act# 1$%& 'SC(R"A,

derivatives is

A security derived from a det instrument, share, loan, whether secured or

unsecured, risk instrument or contract for differences or any other form of

security.

A contract which derives its value from the prices, or index of prices, of

underlying securities.

Derivatives are securities under the /ecurities &ontract 3$egulation4

Act and hence the trading of derivatives is governed y the regulatory framework

under the /ecurities &ontract 3$egulation4 Act.

3

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 4/40

1.) HISTOR* OF DERIVATIVES :

The history of derivatives is 2uite colourful and surprisingly a lot longer

than most people think. "orward delivery contracts, stating what is to e delivered

for a fixed price at a specified place on a specified date, existed in ancient 5reece

and $ome. $oman emperors entered forward contracts to provide the masses with

their supply of -gyptian grain. These contracts were also undertaken etween

farmers and merchants to eliminate risk arising out of uncertain future prices of

grains. Thus, forward contracts have existed for centuries for hedging price risk.

The first organi6ed commodity exchange came into existence in the

early ')**’s in 7apan. The first formal commodities exchange, the C+icao ,oar-

o Tra-e (C,OT", was formed in '898 in the :/ to deal with the prolem of ‘credit

risk’ and to provide centralised location to negotiate forward contracts. "rom

‘forward’ trading in commodities emerged the commodity ‘futures’. The first type of

futures contract was called ‘to arrive at’. Trading in futures egan on the &;<T in

the '8=*’s. In '8=, &;<T listed the first ‘exchange traded’ derivatives contract,

known as the futures contracts. "utures trading grew out of the need for hedging the

price risk involved in many commercial operations. The C+icao /ercanti!e

E0c+ane (C/E", a spin#off of &;<T, was formed in '('(, though it did exist

efore in '8)9 under the names of C+icao Pro-uce E0c+ane (CPE" and

C+icao E an- ,utter ,oar- (CE,,". The first financial futures to emerge

were the currency in '()> in the :/. The first foreign currency futures were tradedon %ay '=, '()>, on Internationa! /onetar3 /ar4et (I//"# a division of &%-. The

currency futures traded on the I%% are the ;ritish 0ound, the &anadian Dollar, the

7apanese ?en, the /wiss "ranc, the 5erman %ark, the Australian Dollar, and the

-uro dollar. &urrency futures were followed soon y interest rate futures. Interest

rate futures contracts were traded for the first time on the &;<T on <ctoer >*,

'(). /tock index futures and options emerged in '(8>. The first stock index futures

contracts were traded on @ansas &ity ;oard of Trade on "eruary >9, '(8>.

4

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 5/40

The first of the several networks, which offered a trading link etween

two exchanges, was formed etween the Sina5ore Internationa! /onetar3

E0c+ane (SI/E6" and the &%- on /eptemer ), '(89.

<ptions are as old as futures. Their history also dates ack to ancient

5reece and $ome. <ptions are very popular with speculators in the tulip cra6e of

seventeenth century olland. Tulips, the rightly coloured flowers, were a symol of

affluence+ owing to a high demand, tulip ul prices shot up. Dutch growers and

dealers traded in tulip ul options. There was so much speculation that people

even mortgaged their homes and usinesses. These speculators were wiped out

when the tulip cra6e collapsed in '=B) as there was no mechanism to guarantee the

performance of the option terms.

The first call and put options were invented y an American financier,

$ussell /age, in '8)>. These options were traded over the counter. Agricultural

commodities options were traded in the nineteenth century in -ngland and the :/.

<ptions on shares were availale in the :/ on the over the counter 3<T&4 market

only until '()B without much knowledge of valuation. A group of firms known as 0ut

and &all rokers and Dealer’s Association was set up in early '(**’s to provide a

mechanism for ringing uyers and sellers together.

<n April >=, '()B, the &hicago ;oard options -xchange 3&;<-4 was

set up at &;<T for the purpose of trading stock options. It was in '()B again that

lack, %erton, and /choles invented the famous ,!ac47Sc+o!es O5tion For8u!a.

This model helped in assessing the fair price of an option which led to an increased

interest in trading of options. !ith the options markets ecoming increasingly

popular, the American /tock -xchange 3A%-C4 and the 0hiladelphia /tock

-xchange 30C4 egan trading in options in '().

The market for futures and options grew at a rapid pace in the eighties

and nineties. The collapse of the ;retton !oods regime of fixed parties and the

introduction of floating rates for currencies in the international financial markets

5

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 6/40

paved the way for development of a numer of financial derivatives which served as

effective risk management tools to cope with market uncertainties.

The &;<T and the &%- are two largest financial exchanges in theworld on which futures contracts are traded. The &;<T now offers 98 futures and

option contracts 3with the annual volume at more than >'' million in >**'4.The

&;<- is the largest exchange for trading stock options. The &;<- trades options

on the /E0 '** and the /E0 ** stock indices. The 0hiladelphia /tock -xchange

is the premier exchange for trading foreign options.

The most traded stock indices include /E0 **, the Dow 7ones

Industrial Average, the asda2 '**, and the ikkei >>. The :/ indices and the

ikkei >> trade almost round the clock. The >> is also traded on the &hicago

%ercantile -xchange.

6

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 7/40

CHAPTER 2---------------------------------------------------------------------------------------------------------------

-

2.1 DERIVATIVES IN INDIA :

India has started the innovations in financial markets very late. /ome

of the recent developments initiated y the regulatory authorities are very important

in this respect. "utures trading have een permitted in certain commodity

exchanges. %umai /tock -xchange has started futures trading in cottonseed and

cotton under the ;<<- and under the -ast India &otton Association. ecessary

infrastructure has een created y the Nationa! Stoc4 E0c+ane (NSE" and the

,o89a3 Stoc4 E0c+ane (,SE" for trading in stock index futures and the

commencement of operations in selected scripts. ieralised exchange rate

management system has een introduced in the year '((> for regulating the flow of

foreign exchange. A committee headed y /./.Tarapore was constituted to go into

the merits of full convertiility on capital accounts. $;I has initiated measures for

freeing the interest rate structure. It has also envisioned /u89ai Inter ,an4 Oer

Rate (/I,OR" on the line of on-on Inter ,an4 Oer Rate (I,OR" as a step

towards introducing "utures trading in Interest $ates and "orex. ;adla transactions

have een anned in all >B stock exchanges from 7uly >**'. /- has started

trading in index options ased on the I"T? and certain /tocks.

A. E;UIT* DERIVATIVES IN INDIA <

In the decade of '((*’s revolutionary changes took place in the

institutional infrastructure in India’s e2uity market. It has led to wholly new ideas in

market design that has come to dominate the market. These new institutional

arrangements, coupled with the widespread knowledge and orientation towards

e2uity investment and speculation, have comined to provide an environment where

7

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 8/40

the e2uity spot market is now India’s most sophisticated financial market. <ne

aspect of the sophistication of the e2uity market is seen in the levels of market

li2uidity that are now visile. The market impact cost of doing program trades of

$s. million at the I"T? index is around *.>F. This state of li2uidity on the e2uityspot market does well for the market efficiency, which will e oserved if the index

futures market when trading commences. India’s e2uity spot market is dominated y

a new practice called ‘"utures G /tyle settlement’ or account period settlement. In its

present scene, trades on the largest stock exchange 3/-4 are netted from

!ednesday morning till Tuesday evening, and only the net open position as of

Tuesday evening is settled. The future style settlement has proved to e an ideal

launching pad for the skills that are re2uired for futures trading.

/tock trading is widely prevalent in India, hence it seems easy to think

that derivatives ased on individual securities could e very important. The index is

the counter piece of portfolio analysis in modern financial economies. Index

fluctuations affect all portfolios. The index is much harder to manipulate. This is

particularly important given the weaknesses of aw -nforcement in India, which

have made numerous manipulative episodes possile. The market capitalisation of

the /-#* index is $s.>.= trillion. This is six times larger than the market

capitalisation of the largest stock and ** times larger than stocks such as /terlite,

;0 and Hideocon. If market manipulation is used to artificially otain '*F move in

the price of a stock with a '*F weight in the I"T?, this yields a 'F in the I"T?.

&ash settlements, which is universally used with index derivatives, also helps in

terms of reducing the vulneraility to market manipulation, in so far as the ‘short#

s2uee6e’ is not a prolem. Thus, index derivatives are inherently less vulnerale to

market manipulation.

,. CO//ODIT* DERIVATIVES TRADIN= IN INDIA <

In India, the futures market for commodities evolved y the setting up of the

;omay &otton Trade Association td.J, in '8). A separate association y the

name K;omay &otton -xchange tdJ was estalished following widespread

discontent amongst leading cotton mill owners and merchants over the functioning

8

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 9/40

of the ;omay &otton Trade Association. !ith the setting up of the ‘5u1arati Hyapari

%andaliJ in '(**, the futures trading in oilseed egan. &ommodities like groundnut,

castor seed and cotton etc egan to e exchanged.

$aw 1ute and 1ute goods egan to e traded in &alcutta with the

estalishment of the &alcutta essian -xchange td.J in '('(. The most notale

centres for existence of futures market for wheat were the &hamer of &ommerce at

apur, which was estalished in '('B. <ther markets were located at Amritsar,

%oga, udhiana, 7alandhar, "a6ilka, Dhuri, ;arnala and ;hatinda in 0un1a and

%u6affarnagar, &handausi, %eerut, /aharanpur, athras, 5a6iaad, /ikenderaad

and ;arielly in :.0. The ;ullion "utures market egan in ;omay in '((*. After the

economic reforms in '((' and the trade lierali6ation, the 5ovt. of India appointed

in 7une '((B one more committee on "orward %arkets under &hairmanship of 0rof.

@.. @ara. The &ommittee recommended that futures trading e introduced in

asmati rice, cotton, raw 1ute and 1ute goods, groundnut, rapeseedLmustard seed,

cottonseed, sesame seed, sunflower seed, safflower seed, copra and soyean, and

oils and oilcakes of all of them, rice ran oil, castor oil and its oilcake, linseed, silver

and onions. All over the world commodity trade forms the ma1or ackone of the

economy. In India, trading volumes in the commodity market have also seen a

steady rise # to $s ,)',*** crore in "?* from $s ',>(,*** crore in "?*9. In the

current fiscal year, trading volumes in the commodity market have already crossed

$s B,*,*** crore in the first four months of trading. /ome of the commodities

traded in India include Agricultural &ommodities like $ice !heat, /oya, 5roundnut,

Tea, &offee, 7ute, $uer, /pices, &otton, 0recious %etals like 5old E /ilver, ;ase

%etals like Iron <re, Aluminium, ickel, ead, Minc and -nergy &ommodities like

crude oil, coal. &ommodities form around *F of the Indian 5D0. Though there are

no institutions or anks in commodity exchanges, as yet, the market for

commodities is igger than the market for securities. &ommodities market is

estimated to e around $s 99,**,*** &rores in future. Assuming a future trading

multiple is aout 9 times the physical market, in many countries it is much higher at

around '* times.

9

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 10/40

2.2 T*PES OF DERIVATIVES :

There are mainly four types of derivatives i.e. "orwards, "utures,

<ptions and swaps.

Derivatives

Forwards Futures Options Swaps

1. FOR>ARDS 7

A contract that oligates one counter party to uy and the other to sell

a specific underlying asset at a specific price, amount and date in the future is

known as a forward contract. "orward contracts are the important type of forward#

ased derivatives. They are the simplest derivatives. There is a separate forward

market for multitude of underlyings, including the traditional agricultural or physical

10

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 11/40

commodities, as well as currencies and interest rates. The change in the value of a

forward contract is roughly proportional to the change in the value of its underlying

asset. These contracts create credit exposures. As the value of the contract is

conveyed only at the maturity, the parties are exposed to the risk of default duringthe life of the contract. "orward contracts are customised with the terms and

conditions tailored to fit the particular usiness, financial or risk management

o1ectives of the counter parties. egotiations often take place with respect to

contract si6e, delivery grade, delivery locations, delivery dates and credit terms.

2. FUTURES 7

A future contract is an agreement etween two parties to uy or sell an

asset at a certain time the future at the certain price. "utures contracts are the

special types of forward contracts in the sense that are standardi6ed exchange#

traded contracts.

-2uities, onds, hyrid securities and currencies are the commodities

of the investment usiness. They are traded on organised exchanges in which a

clearing house interposes itself etween uyer and seller and guarantees all

transactions, so that the identity of the uyer or the seller is a matter of indifference

to the opposite party. "utures contract protect those who use these commodities in

their usiness.

"utures trading are to enter into contracts to uy or sell financial

instruments, dealing in commodities or other financial instruments for forward

delivery or settlement on standardised terms. The futures market facilitates stock

holding and shifting of risk. They act as a mechanism for collection and distriution

of information and then perform a forward pricing function. The futures trading can

e performed when there is variation in the price of the actual commodity and there

exists economic agents with commitments in the actual market. There must e a

possiility to specify a standard grade of the commodity and to measure deviations

from this grade. A futures market is estalished specifically to meet purely

speculative demands is possile ut is not known. &onditions which are thought ofnecessary for the estalishment of futures trading are the presence of speculative

11

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 12/40

capital and financial facilities for payment of margins and contract settlement. In

addition, a strong infrastructure is re2uired, including financial, legal and

communication systems.

). OPTIONS 7

A derivative transaction that gives the option holder the right ut not

the oligation to uy or sell the underlying asset at a price, called the strike price,

during a period or on a specific date in exchange for payment of a premium is

known as o5tion. :nderlying asset refers to any asset that is traded. The price at

which the underlying is traded is called the stri4e 5rice.

There are two types of options i.e., CA OPTION AND PUT

OPTION.

a. CA OPTION :

A contract that gives its owner the right ut not the oligation

to uy an underlying asset#stock or any financial asset, at a specified

price on or efore a specified date is known as a Ca!! o5tion. The owner

makes a profit provided he sells at a higher current price and uys at a

lower future price.

9. PUT OPTION :

A contract that gives its owner the right ut not the oligation

to sell an underlying asset#stock or any financial asset, at a specified price

on or efore a specified date is known as a ‘Put o5tion. The owner

makes a profit provided he uys at a lower current price and sells at a

higher future price. ence, no option will e exercised if the future price

does not increase.

12

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 13/40

0ut and calls are almost always written on e2uities, although

occasionally preference shares, onds and warrants ecome the su1ect of options.

?. S>APS 7

/waps are transactions which oligates the two parties to the contract

to exchange a series of cash flows at specified intervals known as payment or

settlement dates. They can e regarded as portfolios of forwardNs contracts. A

contract wherey two parties agree to exchange 3swap4 payments, ased on some

notional principle amount is called as a S>AP. In case of swap, only the payment

flows are exchanged and not the principle amount. The two commonly used swaps

areO

a. INTEREST RATE S>APS :

Interest rate swaps is an arrangement y which one party

agrees to exchange his series of fixed rate interest payments to a party in

exchange for his variale rate interest payments. The fixed rate payer

takes a short position in the forward contract whereas, the floating rate

payer takes a long position in the forward contract.

9. CURRENC* S>APS :

&urrency swaps is an arrangement in which oth the principle

amount and the interest on loan in one currency are swapped for the

principle and the interest payments on loan in another currency. The

parties to the swap contract of currency generally hail from two different

countries. This arrangement allows the counter parties to orrow easily

13

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 14/40

and cheaply in their home currencies. :nder a currency swap, cash flows

to e exchanged are determined at the spot rate at a time when swap is

done. /uch cash flows are supposed to remain unaffected y suse2uent

changes in the exchange rates.

c. FINANCIA S>AP :

"inancial swaps constitute a funding techni2ue which permit a

orrower to access one market and then exchange the liaility for another

type of liaility. It also allows the investors to exchange one type of asset

for another type of asset with a preferred income stream.

T+e ot+er 4in- o -eri@ati@es# +ic+ are not# 8uc+ 5o5u!ar are as

o!!os :

%. ,ASBETS 7

;askets options are option on portfolio of underlying asset. -2uity Index

<ptions are most popular form of askets.

&. EAPS 7

ormally option contracts are for a period of ' to '> months. owever,

exchange may introduce option contracts with a maturity period of >#B years. These

long#term option contracts are popularly known as eaps or ong term -2uity

Anticipation /ecurities.

. >ARRANTS 7

14

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 15/40

<ptions generally have lives of up to one year, the ma1ority of options traded

on options exchanges having a maximum maturity of nine months. onger#dated

options are called warrants and are generally traded over#the#counter.

. S>APTIONS 7

/waptions are options to uy or sell a swap that will ecome operative at the

expiry of the options. Thus a swaption is an option on a forward swap. $ather than

have calls and puts, the swaptions market has receiver swaptions and payer

swaptions. A receiver swaption is an option to receive fixed and pay floating. A

payer swaption is an option to pay fixed and receive floating.

15

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 16/40

2.) FUTURES VS. FOR>ARD /ARBET :

16

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 17/40

/ettlements are made daily through /ettlement occurs on date agreed

17

F u t u r e s M a r k e t F o r w a r d M a r k e t

%argin deposits are to e re2uired

of all participants.

Typically, no money changes hands

until delivery, although a small

margin deposit might e re2uired of

non#dealer customers on certain

occasions.

&ontract terms are standardised

with all uyers and sellers

negotiating only with respect to

price.

All contract terms are negotiated

privately y the parties.

on#memer participants deal

through rokers 3exchange

memers who represent them on

the exchange floor4

0articipants deal typically on a

principal#to#principal asis.

0articipants include anks,

corporations, financial institutions,

individual investors, and

speculators.

0articipants are primarily institutions

dealing with one other and other

interested parties dealing through

one or more dealers.The clearing house of the exchange

ecomes the opposite side to each

cleared transactions+ therefore, the

credit risk for a futures market

participant is always the same and

there is no need to analyse the

credit of other market participants.

A participant must examine the

credit risk and estalish credit limits

for each opposite party.

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 18/40

the exchange clearing house. 5ains

on open positions may e

withdrawn and losses are collected

daily.

upon etween the parties to each

transaction.

ong and short positions are usually

li2uidated easily.

"orward positions are not as easily

offset or transferred to the other

participants.

/ettlements are normally made in

cash, with only a small percentage

of all contracts resulting actual

delivery.

%ost transactions result in delivery.

A single, round trip 3in and out ofthe market4 commission is charged.

It is negotiated etween roker and

customer and is relatively small in

relation to the value of the contract.

o commission is typically chargedif the transaction is made directly

with another dealer. A commission

is charged to orn uyer and seller,

however, if transacted through a

roker.

Trading is regulated. Trading is mostly unregulated.

The delivery price is the spot price. The delivery price is the forward

price.

2.? PARTICIPANTS IN THE DERIVATIVES /ARBET :

The participants in the derivatives market are as followsO

18

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 19/40

A. TRADIN= PARTICIPANTS :

1. HED=ERS <

The process of managing the risk or risk management is called as

hedging. edgers are those individuals or firms who manage their risk with the help

of derivative products. edging does not mean maximising of return. The main

purpose for hedging is to reduce the volatility of a portfolio y reducing the risk.

2. SPECUATORS <

/peculators do not have any position on which they enter into futures

and options %arket i.e., they take the positions in the futures market without having

position in the underlying cash market. They only have a particular view aout future

price of a commodity, shares, stock index, interest rates or currency. They consider

various factors like demand and supply, market positions, open interests, economic

fundamentals, international events, etc. to make predictions. They take risk in turn

from high returns. /peculators are essential in all markets G commodities, e2uity,

interest rates and currency. They help in providing the market the much desired

volume and li2uidity.

). AR,ITRA=EURS <

Aritrage is the simultaneous purchase and sale of the same

underlying in two different markets in an attempt to make profit from price

discrepancies etween the two markets. Aritrage involves activity on several

different instruments or assets simultaneously to take advantage of price distortions

1udged to e only temporary.

Aritrage occupies a prominent position in the futures world. It is the

mechanism that keeps prices of futures contracts aligned properly with prices of

underlying assets. The o1ective is simply to make profits without risk, ut the

complexity of aritrage activity is such that it is reserved to particularly well#informed

19

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 20/40

and experienced professional traders, e2uipped with powerful calculating and data

processing tools. Aritrage may not e as easy and costless as presumed.

,. INTER/EDIAR* PARTICIPANTS :

?. ,ROBERS <

"or any purchase and sale, rokers perform an important function of

ringing uyers and sellers together. As a memer in any futures exchanges, may

e any commodity or finance, one need not e a speculator, aritrageur or hedger.

;y virtue of a memer of a commodity or financial futures exchange one get a rightto transact with other memers of the same exchange. This transaction can e in

the pit of the trading hall or on online computer terminal. All persons hedging their

transaction exposures or speculating on price movement, need not e and for that

matter cannot e memers of futures or options exchange. A non#memer has to

deal in futures exchange through memer only. This provides a memer the role of

a roker. is existence as a roker takes the enefits of the futures and options

exchange to the entire economy all transactions are done in the name of the

memer who is also responsile for final settlement and delivery. This activity of a

memer is price risk free ecause he is not taking any position in his account, ut

his other risk is clients default risk. e cannot default in his oligation to the clearing

house, even if client defaults. /o, this risk premium is also inuilt in rokerage

recharges. %ore and more involvement of non#memers in hedging and speculation

in futures and options market will increase rokerage usiness for memer and

more volume in turn reduces the rokerage. Thus more and more participation of

traders other than memers gives li2uidity and depth to the futures and options

market. %emers can attract involvement of other y providing efficient services at a

reasonale cost. In the asence of well functioning roking houses, the futures

exchange can only function as a clu.

%. /ARBET /ABERS AND O,,ERS <

20

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 21/40

-ven in organised futures exchange, every deal cannot get the

counter party immediately. It is here the 1oer or market maker plays his role. They

are the memers of the exchange who takes the purchase or sale y other

memers in their ooks and then s2uare off on the same day or the next day. They2uote their id#ask rate regularly. The difference etween id and ask is known as

id#ask spread. !hen volatility in price is more, the spread increases since 1oers

price risk increases. In less volatile market, it is less. 5enerally, 1oers carry limited

risk. -ven y incurring loss, they s2uare off their position as early as possile. /ince

they decide the market price considering the demand and supply of the commodity

or asset, they are also known as market makers. Their role is more important in the

exchange where outcry system of trading is present. A uyer or seller of a particular

futures or option contract can approach that particular 1oing counter and 2uotes

for executing deals. In automated screen ased trading est uy and sell rates are

displayed on screen, so the role of 1oer to some extent. In any case, 1oers

provide li2uidity and volume to any futures and option market.

C. INSTITUTIONA FRA/E>ORB :

&. E6CHAN=E <

-xchange provides uyers and sellers of futures and option contract

necessary infrastructure to trade. In outcry system, exchange has trading pit where

memers and their representatives assemle during a fixed trading period and

execute transactions. In online trading system, exchange provide access to

memers and make availale real time information online and also allow them to

execute their orders. "or derivative market to e successful exchange plays a very

important role, there may e separate exchange for financial instruments and

commodities or common exchange for oth commodities and financial assets.

. CEARIN= HOUSE <

A clearing house performs clearing of transactions executed in futures

and option exchanges. &learing house may e a separate company or it can e a

21

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 22/40

division of exchange. It guarantees the performance of the contracts and for this

purpose clearing house ecomes counter party to each contract. Transactions are

etween memers and clearing house. &learing house ensures solvency of the

memers y putting various limits on him. "urther, clearing house devises a goodmanaging system to ensure performance of contract even in volatile market. This

provides confidence of people in futures and option exchange. Therefore, it is an

important institution for futures and option market.

. CUSTODIAN G >ARE HOUSE <

"utures and options contracts do not generally result into delivery ut

there has to e smooth and standard delivery mechanism to ensure proper

functioning of market. In stock index futures and options which are cash settled

contracts, the issue of delivery may not arise, ut it would e there in stock futures

or options, commodity futures and options and interest rates futures. In the asence

of proper custodian or warehouse mechanism, delivery of financial assets and

commodities will e a cumersome task and futures prices will not reflect the

e2uilirium price for convergence of cash price and futures price on maturity,

custodian and warehouse are very relevant.

$. ,ANB FOR FUND /OVE/ENTS <

"utures and options contracts are daily settled for which large fund

movement from memers to clearing house and ack is necessary. This can e

smoothly handled if a ank works in association with a clearing house. ;ank can

make daily accounting entries in the accounts of memers and facilitate daily

settlement a routine affair. This also reduces a possiility of any fraud or

misappropriation of fund y any market intermediary.

1. RE=UATOR* FRA/E>ORB <

A regulator creates confidence in the market esides providing evel

playing field to all concerned, for foreign exchange and money market, $;I is the

22

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 23/40

regulatory authority so it can take initiative in starting futures and options trade in

currency and interest rates. "or capital market, /-;I is playing a lead role, along

with physical market in stocks, it will also regulate the stock index futures to e

started very soon in India. The approach and outlook of regulator directly affects thestrength and volume in the market. "or commodities, "orward %arket &ommission

is working for settling up national ational &ommodity -xchange.

2.% ROE OF DERIVATIVES :

Derivative markets help investors in many different ways O

23

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 24/40

1. RISB /ANA=E/ENT <

"utures and options contract can e used for altering the risk ofinvesting in spot market. "or instance, consider an investor who owns an asset. e

will always e worried that the price may fall efore he can sell the asset. e can

protect himself y selling a futures contract, or y uying a 0ut option. If the spot

price falls, the short hedgers will gain in the futures market, as you will see later.

This will help offset their losses in the spot market. /imilarly, if the spot price falls

elow the exercise price, the put option can always e exercised.

Derivatives markets help to reallocate risk among investors. A person

who wants to reduce risk, can transfer some of that risk to a person who wants to

take more risk. &onsider a risk#averse individual. e can oviously reduce risk y

hedging. !hen he does so, the opposite position in the market may e taken y a

speculator who wishes to take more risk. /ince people can alter their risk exposure

using futures and options, derivatives markets help in the raising of capital. As an

investor, you can always invest in an asset and then change its risk to a level that is

more acceptale to you y using derivatives.

2. PRICE DISCOVER* <

0rice discovery refers to the markets aility to determine true

e2uilirium prices. "utures prices are elieved to contain information aout future

spot prices and help in disseminating such information. As we have seen, futures

markets provide a low cost trading mechanism. Thus information pertaining to

supply and demand easily percolates into such markets. Accurate prices are

essential for ensuring the correct allocation of resources in a free market economy.

<ptions markets provide information aout the volatility or risk of the underlying

asset.

). OPERATIONA ADVANTA=ES <

24

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 25/40

As opposed to spot markets, derivatives markets involve lower

transaction costs. /econdly, they offer greater li2uidity. arge spot transactions can

often lead to significant price changes. owever, futures markets tend to e more

li2uid than spot markets, ecause herein you can take large positions y depositingrelatively small margins. &onse2uently, a large position in derivatives markets is

relatively easier to take and has less of a price impact as opposed to a transaction

of the same magnitude in the spot market. "inally, it is easier to take a short position

in derivatives markets than it is to sell short in spot markets.

?. /ARBET EFFICIENC* <

The availaility of derivatives makes markets more efficient+ spot,

futures and options markets are inextricaly linked. /ince it is easier and cheaper to

trade in derivatives, it is possile to exploit aritrage opportunities 2uickly and to

keep prices in alignment. ence these markets help to ensure that prices reflect true

values.

%. EASE OF SPECUATION <

Derivative markets provide speculators with a cheaper alternative to

engaging in spot transactions. Also, the amount of capital re2uired to take a

comparale position is less in this case. This is important ecause facilitation of

speculation is critical for ensuring free and fair markets. /peculators always take

calculated risks. A speculator will accept a level of risk only if he is convinced that

the associated expected return, is commensurate with the risk that he is taking.

CHAPTER )

25

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 26/40

---------------------------------------------------------------------------------------------------------------

-

HO> ,ANBS USE DERIVATIVES :

ASSET IA,IIT* /ANA=E/ENT 7

;anks have traditionally taken deposits from their customers and put those

deposits to work as loans. ;ecause the deposits and the loans are dominated in the

same currency, this activity has no associated foreign exchange risk. ;ut it does

limit anks to lending to customers which need to orrow in the currencies which the

anks have availale on deposits.

If a ank is asked to lend to a customer in a currency other than one of those

it has on deposits it creates a currency exposure for the ank. /uppose a customer

wants to orrow -:$</ from a :/ ;ank for years and that the :/ ank has no

natural source of -:$</. It is possile for the anks to cover this exposure in the

forward market y selling -:$</ forwards and uying :/ dollars. The transaction

costs associated with this, in particular the id L offer spread in the medium term

foreign exchange forward market, would make the resultant cost of the loan

prohiitively expensive for the orrower.

&urrency swaps provide an economic alternative to this prolem for anks. In

order to cover the exposure created y a loan to a customer in -:$</ funded y a

ank’s deposit in :/ dollar, a ank could receive fixed rate :/ dollars in a currency

swap and pay fixed rate -:$</.

<ne of the conse2uences of the development of the currency swap market is

that anks now often make much more competitive medium term forward foreign

exchange prices than they used to. %ost anks 2uote forward foreign exchange and

currency swap prices from the same desk and increases li2uidity in the latter has

improved li2uidity in the former. ;anks therefore, need no longer restrict theirlending activities to the currencies in which they have natural deposits. They are

26

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 27/40

free to fund themselves in the most competitively priced currency and to lend to their

customers in the currency of the customer’s preference, using a currency swap as

an asset and liaility matching tool

The ormal yield curveJ, reflects that it is much easier for anks to orrow at

the short end of the curve than the long end. This means that anks can fund

themselves much more effectively in the inter ank market in maturities such as the

overnight, tom L next 3overnight from tomorrow, or tomorrow to the next day4, spot L

next, one week, one month, three months and six months than they can in

maturities such as five years or >* years.

!ith the development of the swaps market it is possile for anks to satisfy their

customers demands for fixed rate funding while ensuring that the anks assets and

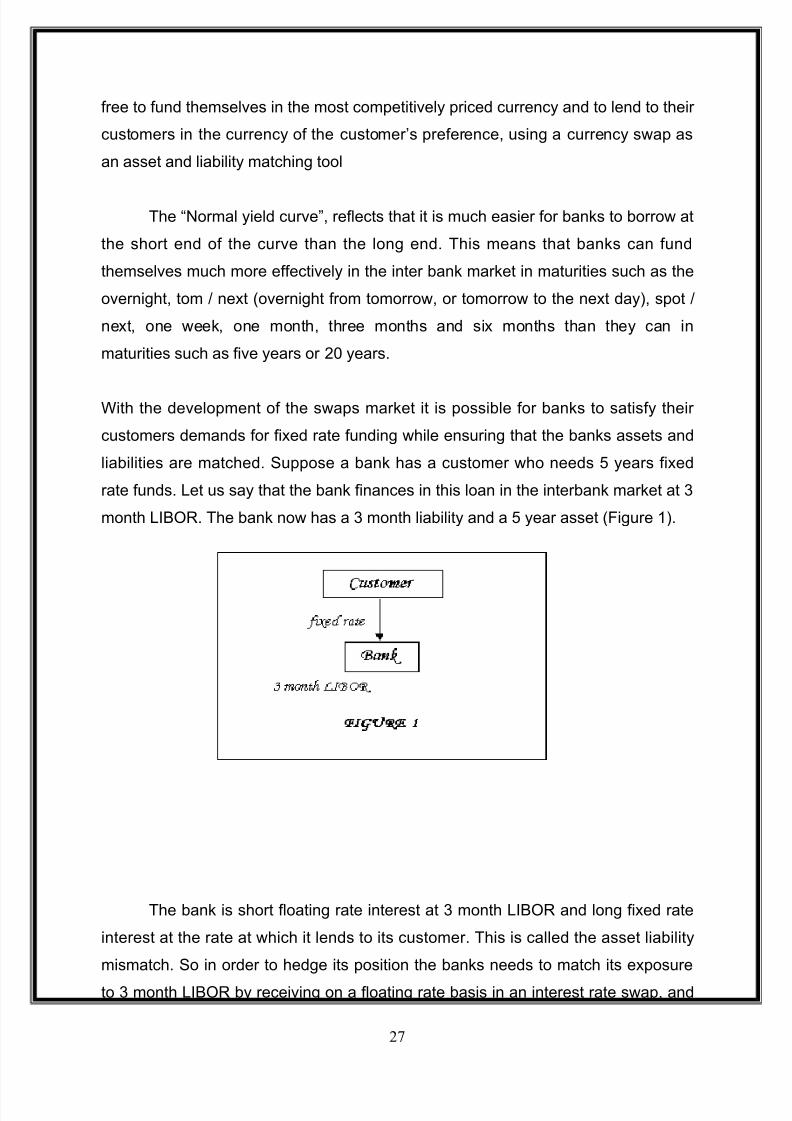

liailities are matched. /uppose a ank has a customer who needs years fixed

rate funds. et us say that the ank finances in this loan in the interank market at B

month I;<$. The ank now has a B month liaility and a year asset 3"igure '4.

The ank is short floating rate interest at B month I;<$ and long fixed rate

interest at the rate at which it lends to its customer. This is called the asset liaility

mismatch. /o in order to hedge its position the anks needs to match its exposure

to B month I;<$ y receiving on a floating rate asis in an interest rate swap, and

27

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 28/40

match its exposure on a fixed rate asis y paying a fixed rate in a interest rate

swap. This is a hedge which is ideally suited to an interest rate swap which the ank

receives a floating rare of interest and pays a fixed rare 3"igure >4.

This structure has the enefit for the ank that it eliminates the ank’s

exposure to interest rate risk. The ank can no longer profit from a fall in interest

rates ut it cannot lose money on its asset and liaility mismatch as a result of an

increase in rates. The ank will make or lose money ased on its pricing of the

credit risk in the transaction and its overall loan exposure rather than on its aility to

forecast interest rates. ence the interest rate swaps provide anks with an

opportunity to change their risks from interest rate to credit.

28

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 29/40

CHAPTER ?

---------------------------------------------------------------------------------------------------------------

-

O,ECTIVE OF THE STUD* :

The main objectives behind the study of deivatives ae!

To understand the scope and growth of derivatives in India.

To understand how the derivatives are used y anks.

To understand how derivatives can e used to hedge risk.

H*POTHESIS :

Derivative market in India is undeveloped.

;anks are successful in using derivatives to hedge the risk.

29

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 30/40

CHAPTER %

---------------------------------------------------------------------------------------------------------------

-

ANA*SIS :

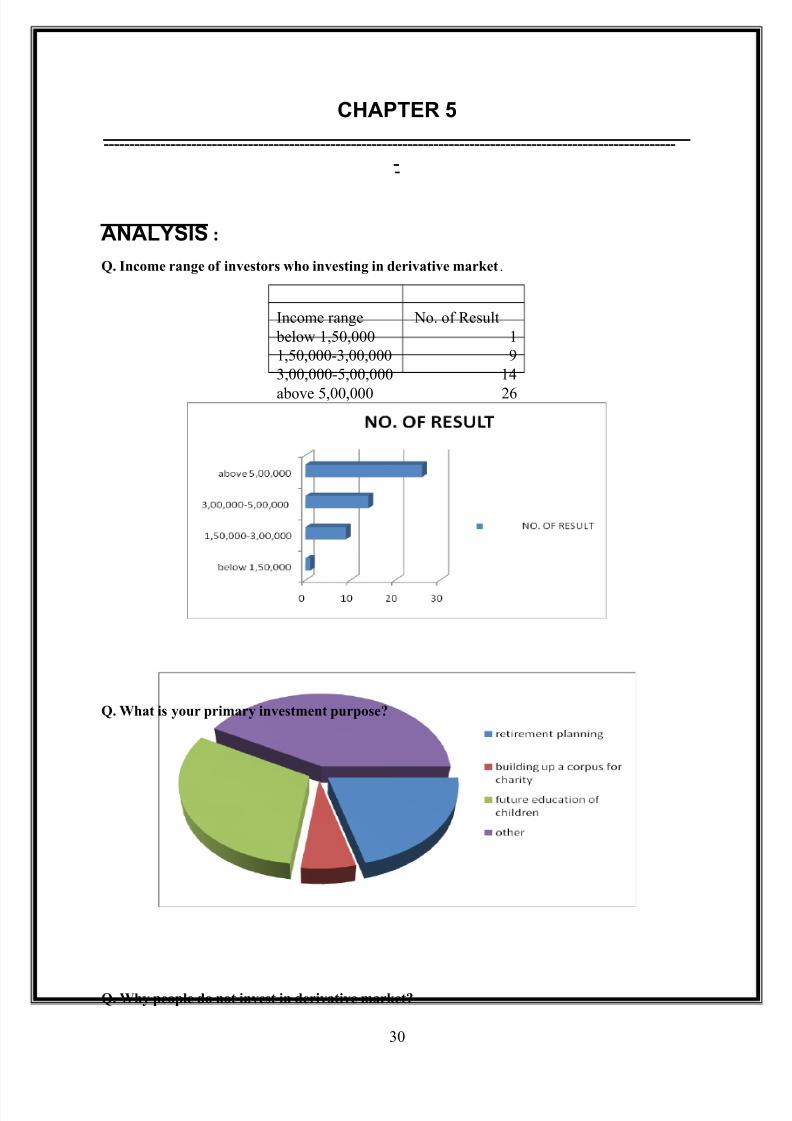

Q. Income range of investors who investing in derivative market.

"ncome an#e $o. of %esu&t

be&o' 1(50(000 1

1(50(000-3(00(000 9

3(00(000-5(00(000 14

above 5(00(000 26

Q. What is your primary investment purpose?

Q. Why people do not invest in derivative market?

30

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 31/40

Reasons No.of result

)ac* of *no'&ed#e + undestandin# 27

"ncease s,ecu&ation 2

%is*y + hi#h&y &evea#ed 17

ounte ,aty is* 4

Q. What is the purpose of investing in derivative market?

urpose of investment No. of Result

ed#e thei fund 27

%is* conto& 9/oe stab&e 1

iect investment 'ithout buyin# + ho&din# assets 13

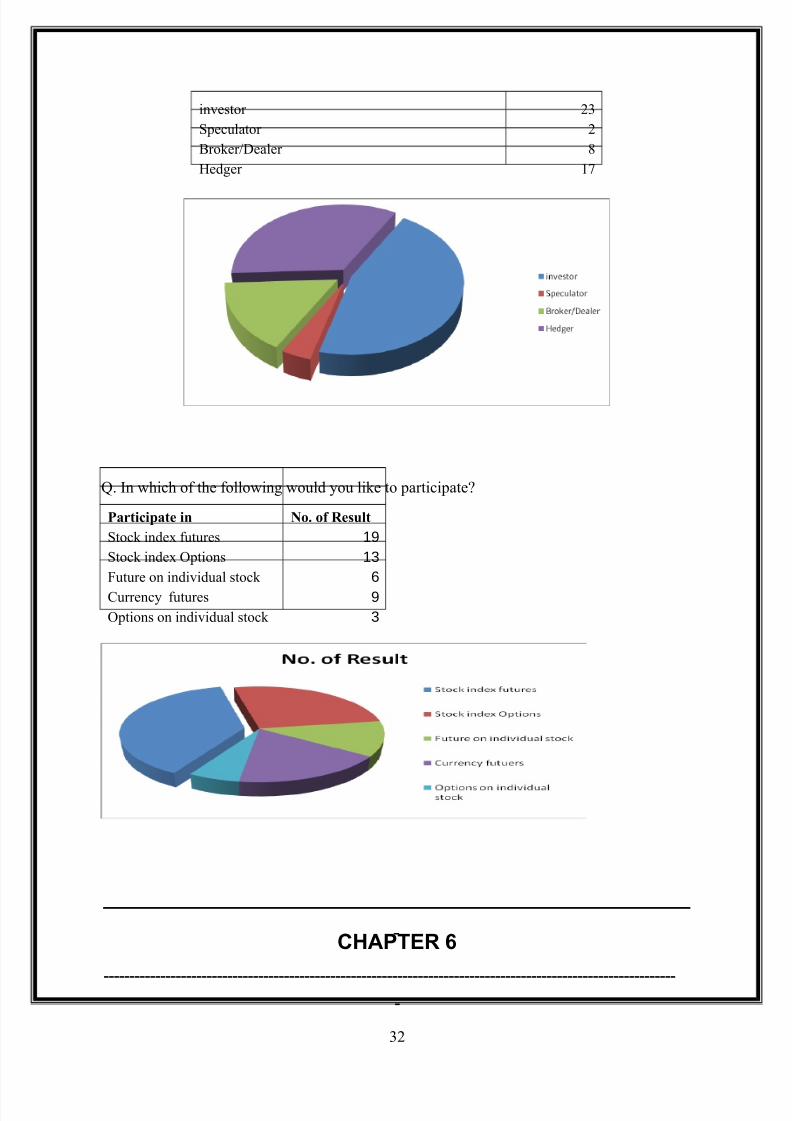

. ou ,atici,ate in deivative ma*et as

articipation as No. of Result

31

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 32/40

investo 23

,ecu&ato 2

o*eea&e 8

ed#e 17

. "n 'hich of the fo&&o'in# 'ou&d you &i*e to ,atici,ate

articipate in No. of Result

toc* inde futues 19

toc* inde ,tions 13

utue on individua& stoc* 6

uency futues 9

,tions on individua& stoc* 3

CHAPTER &

----------------------------------------------------------------------------------------------------------------

32

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 33/40

RECO//ENDATIONS

$;I should play a greater role in supporting derivatives.

Derivatives market should e developed in order to keep it at par with

other derivative markets in the world.

/peculation should e discouraged.

There must e more derivative instruments aimed at individual

investors.

/-;I should conduct seminars regarding the use of derivatives to

educate individual investors.

33

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 34/40

!I"I#$I#%N& %' &#()*

+. !I"I#,) #I",:

The time avai&ab&e to conduct the study 'as on&y ha&f months. "t bein# a 'ide to,ic( had

a &imited time..

. !I"I#,) R,&%(R,&:

)imited esouces ae avai&ab&e to co&&ect the infomation about the commodity tadin#

/. 0%!$#$!I#*:

hae ma*et is so much vo&ati&e and it is difficu&t to foecast anythin# about it 'hethe

you tade thou#h on&ine o off&ine

1. $&,#& %0,R$2,:

ome of the as,ects may not be coveed in my study.

34

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 35/40

CONCUSION

Derivative securities markets play an important role y allowing

investors who do not want the risks associated with holding an asset to

transfer it to those who do. owever, ecause they are markets for risk

as opposed to physical assets, derivatives markets can e very

dangerous places for unsophisticated investors. 0eople who reduce

their risk y entering a derivative market are called hedgers, and those

who increase their risk are called speculators.

The derivative securities markets play a vital role in the modern financial

systems, and without them many common usiness transactions would

e rendered much riskier or practically impossile.

Derivatives were utili6ed in the financial markets around the world

from 2uite a long time whose origin can e traced ack to =th century

;.&. !ith the passage of time, the need of these instruments increased

among various sections of the society for hedging purposes. ater, the

speculative motive of the investors also surfaced and led to its

popularity.

35

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 36/40

,I,IO=RAPH* :

,OOBS

"utures markets G /unil. @. 0arameswaran

:nderstanding futures market G $oert. !. @lo

Derivatives %arket in India G /usan Thomas

"inancial Derivatives G H. @. ;halla

"inancial /ervices and %arkets G Dr. /. 5uruswamy

"utures and <ptions G D. &. 5ardner

INTERNET

www.cxotoday.com

www.indiainfoline.com

www.indiamart.com

36

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 37/40

;UESTIONNAIRE

SURVE* ;UESTIONNAIRE OF INVESTORS FOR PERCEPTION

TO>ARDS INVEST/ENT IN DERIVATIVE /ARBET

1. :ducationa& ua&ification

;"$<=T T<:>? %@" A /@%=TT$ T/)iect =nde#aduate

;"$<=T T<:>? %@" A /@%=TT$ T/)iect Baduate

;"$<=T T<:>? %@" A /@%=TT$ T/)iect <ost Baduate

;"$<=T T<:>? %@" A /@%=TT$ T/)iect <ofessiona& e#ee o&de

2. "ncome %an#e!

;"$<=T T<:>? %@" A /@%=TT$ T/)iect e&o' 1(50(000

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 1(50(000 C 3(00(000

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 3(00(000 C 5(00(000

;"$<=T T<:>? %@" A /@%=TT$ T/)iect @bove 5(00(000

3. $oma&&y 'hat ,ecenta#e of you month&y househo&d income cou&d be avai&ab&e fo

investment

;"$<=T T<:>? %@" A /@%=TT$ T/)iect et'een 5D to 10D

;"$<=T T<:>? %@" A /@%=TT$ T/)iect et'een 11D to 15D

;"$<=T T<:>? %@" A /@%=TT$ T/)iect et'een 16D to 20D

;"$<=T T<:>? %@" A /@%=TT$ T/)iect et'een 21D to 25D

;"$<=T T<:>? %@" A /@%=TT$ T/)iect /oe than 25D

4. Ehat is you ,imay investment ,u,ose

;"$<=T T<:>? %@" A /@%=TT$ T/)iect %etiement <&annin#

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ui&din# u, a co,us fo

chaity donations

;"$<=T T<:>? %@" A /@%=TT$ T/)iect u,,otin# futue education

of you chi&den

37

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 38/40

;"$<=T T<:>? %@" A /@%=TT$ T/)iect the F,ecifyG

HHHHHHHHHHHHHHHHHHHHH

5. Ehat *ind of is* do you ,eceive 'hi&e investin# in the stoc* ma*et

;"$<=T T<:>? %@" A /@%=TT$ T/)iect =ncetainty of etuns

;"$<=T T<:>? %@" A /@%=TT$ T/)iect &um, in stoc* ma*et

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ea of bein# 'indu, of

com,any ;"$<=T T<:>? %@" A /@%=TT$ T/)iect the

F,ecifyG HHHHHHHHHHHHHHHHH

6. Ehy ,eo,&e do not invest in deivative ma*et F%an* you ,efeence 1-4G

;"$<=T T<:>? %@" A /@%=TT$ T/)iect )ac* of *no'&ed#e and

difficu&ty in undestandin#

;"$<=T T<:>? %@" A /@%=TT$ T/)iect "ncease s,ecu&ation

;"$<=T T<:>? %@" A /@%=TT$ T/)iect Iey is*y and hi#h&y

&evea#ed instument

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ounte ,aty is*

7. Ehat is the ,u,ose of investin# in deivative ma*et

;"$<=T T<:>? %@" A /@%=TT$ T/)iect To hed#e thei fund

;"$<=T T<:>? %@" A /@%=TT$ T/)iect %is* conto&

;"$<=T T<:>? %@" A /@%=TT$ T/)iect /oe stab&e

;"$<=T T<:>? %@" A /@%=TT$ T/)iect iect investment 'ithout

buyin# and ho&din# assets

8. ou ,atici,ate in deivative ma*et as!

;"$<=T T<:>? %@" A /@%=TT$ T/)iect "nvesto

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ,ecu&ato

;"$<=T T<:>? %@" A /@%=TT$ T/)iect o*eea&e

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ed#e

9. om 'hee you ,efe to ta*e advice befoe investin# in deivative ma*et

;"$<=T T<:>? %@" A /@%=TT$ T/)iect o*ea#e houses;"$<=T T<:>? %@" A /@%=TT$ T/)iect %eseach ana&yst

38

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 39/40

;"$<=T T<:>? %@" A /@%=TT$ T/)iect Eebsites

;"$<=T T<:>? %@" A /@%=TT$ T/)iect $e's $et'o*s

10. "n 'hich of the fo&&o'in# 'ou&d you &i*e to ,atici,ate;"$<=T T<:>? %@" A /@%=TT$ T/)iect toc* "nde utues

;"$<=T T<:>? %@" A /@%=TT$ T/)iect toc* "nde ,tions

;"$<=T T<:>? %@" A /@%=TT$ T/)iect utue on individua& stoc*

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ,tions on individua& stoc*

;"$<=T T<:>? %@" A /@%=TT$ T/)iect uency futues

11. Ehat contact matuity ,eiod 'ou&d inteest you fo tadin# in

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 1 month

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 2 month

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 3 month

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 6 month

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 9 month

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 12 month

12. o' often do you invest in deivative ma*et

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 1-10 times in a yea

;"$<=T T<:>? %@" A /@%=TT$ T/)iect 11-50 times

;"$<=T T<:>? %@" A /@%=TT$ T/)iect /oe than 50 times

;"$<=T T<:>? %@" A /@%=TT$ T/)iect %e#u&a&y

13. Ehich of the fo&&o'in# statements best descibes you ovea&& a,,oach to invest as a

mean of achievin# you #oa&s

;"$<=T T<:>? %@" A /@%=TT$ T/)iect avin# a e&ative &eve& of

stabi&ity in my ovea&& investment ,otfo&io.

;"$<=T T<:>? %@" A /@%=TT$ T/)iect /odeate&y inceasin# my

investment va&ue 'hi&e minimiJin# ,otentia& fo &oss of

,inci,a&.

;"$<=T T<:>? %@" A /@%=TT$ T/)iect <usue investment #o'th(

acce,tin# modeate to hi#h &eve&s of is* and ,inci,a& f&uctuation.

39

8/12/2019 Chapter Planning

http://slidepdf.com/reader/full/chapter-planning 40/40

;"$<=T T<:>? %@" A /@%=TT$ T/)iect ee* maimum &on#-tem

etuns( acce,tin# maimum is* 'ith ,inci,a&

f&uctuation.

14. Ehat 'as the esu&t of you investment

;"$<=T T<:>? %@" A /@%=TT$ T/)iect Beat esu&ts

;"$<=T T<:>? %@" A /@%=TT$ T/)iect /odeate but acce,tab&e

;"$<=T T<:>? %@" A /@%=TT$ T/)iect isa,,ointed