Chapter 9 Plant Assets, Natural Resources, and Intangibles

48

8/28/2019 1 Chapter 9 Plant Assets, Natural Resources, and Intangibles Chapter 9 Learning Objectives 1. Measure the cost of property, plant, and equipment 2. Account for depreciation using the straight-line, units-of-production, and double-declining-balance methods 3. Journalize entries for the disposal of plant assets 9-2 © 2018 Pearson Education, Inc. 1 2

Transcript of Chapter 9 Plant Assets, Natural Resources, and Intangibles

8/28/2019

1

Chapter 9Plant Assets,

Natural Resources, and

Intangibles

Chapter 9 Learning Objectives

1. Measure the cost of property, plant, and equipment

2. Account for depreciation using the straight-line, units-of-production, and double-declining-balance methods

3. Journalize entries for the disposal of plant assets

9-2© 2018 Pearson Education, Inc.

1

2

8/28/2019

2

Chapter 9 Learning Objectives

4. Account for natural resources

5. Account for intangible assets

6. Use the asset turnover ratio to evaluate business performance

7. Journalize entries for the exchange of plant assets (Appendix 9A)

9-3© 2018 Pearson Education, Inc.

Learning Objective 1

Measure the cost of property, plant, and equipment

9-4© 2018 Pearson Education, Inc.

3

4

8/28/2019

3

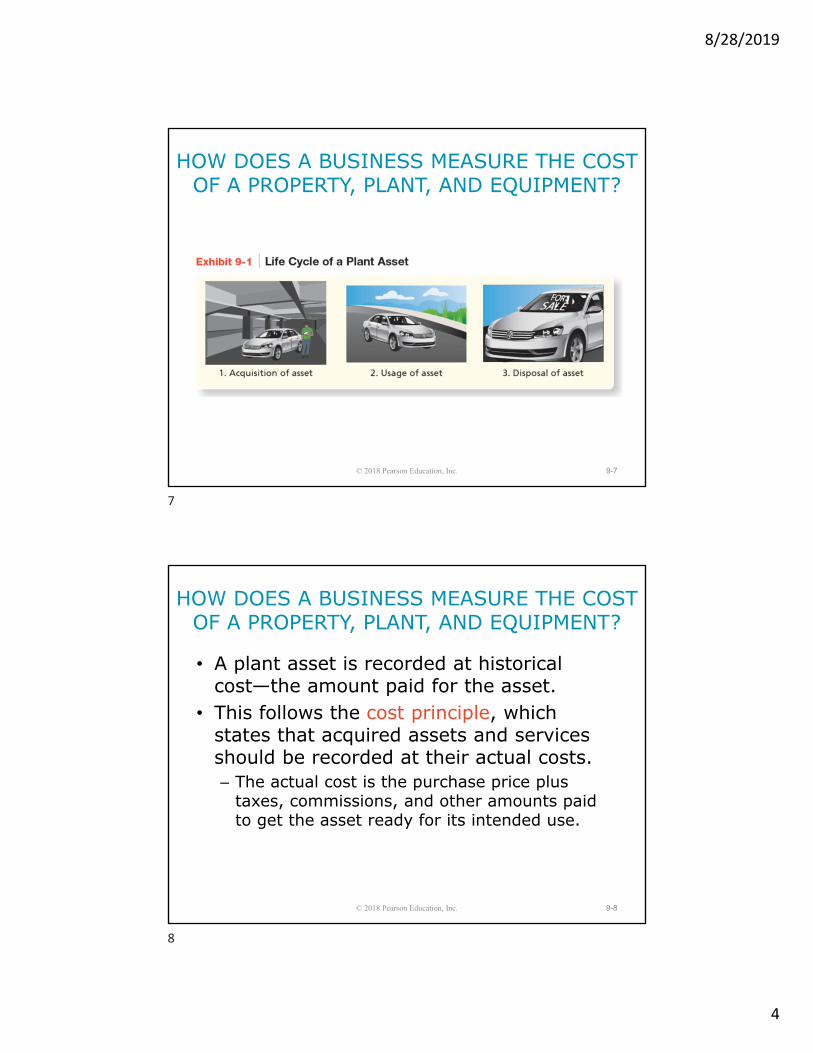

HOW DOES A BUSINESS MEASURE THE COST OF A PROPERTY, PLANT, AND EQUIPMENT?

9-5

• Property, plant, and equipment (PP&E) are long-lived, tangible assets used in the operations of a business.

• Examples:– Land– Buildings– Equipment– Furniture– Fixtures– Automobiles

© 2018 Pearson Education, Inc.

9-6

• Plant assets are different from other assets because plant assets are long-term (lasting several years).

• The cost of a plant asset is allocated to an expense over the years that the asset is expected to be used.

• The allocation of a plant asset’s cost over its useful life is called depreciation and follows the matching principle.

© 2018 Pearson Education, Inc.

HOW DOES A BUSINESS MEASURE THE COST OF A PROPERTY, PLANT, AND EQUIPMENT?

5

6

8/28/2019

4

9-7© 2018 Pearson Education, Inc.

HOW DOES A BUSINESS MEASURE THE COST OF A PROPERTY, PLANT, AND EQUIPMENT?

9-8

• A plant asset is recorded at historical cost—the amount paid for the asset.

• This follows the cost principle, which states that acquired assets and services should be recorded at their actual costs.– The actual cost is the purchase price plus

taxes, commissions, and other amounts paid to get the asset ready for its intended use.

© 2018 Pearson Education, Inc.

HOW DOES A BUSINESS MEASURE THE COST OF A PROPERTY, PLANT, AND EQUIPMENT?

7

8

8/28/2019

5

Land and Land Improvements

• The cost of land includes the following amounts paid by the purchaser:

9-9

Purchase price

Brokerage commission

Survey and legal fees

Delinquent property taxes

Title transfer fees

Cost of clearing the

land

© 2018 Pearson Education, Inc.

Land and Land Improvements

9-10

• The cost of land does not include:

• These separate plant assets are called land improvements and, unlike land, are subject to depreciation.

Fencing PavingSprinkler systems

Lighting Signs

© 2018 Pearson Education, Inc.

9

10

8/28/2019

6

Land and Land Improvements

Smart Touch Learning purchases land on August 1, 2019, for $50,000 with a note payable. Other costs include $4,000 in delinquent property taxes, $2,000 in transfer taxes, $5,000 to remove an old building, and a $1,000 survey fee.

9-11© 2018 Pearson Education, Inc.

Land and Land Improvements

The entry to record the purchase of the land on August 1, 2019:

Smart Touch Learning capitalizes the cost of the land at $62,000. • Capitalized means that an asset account was debited

(increased) because the company acquired an asset.

9-12© 2018 Pearson Education, Inc.

11

12

8/28/2019

7

Land and Land Improvements

Smart Touch Learning then pays $20,000 for fences, paving, lighting, and signs on August 15, 2019:

Land and land improvements are two entirely separate assets.• Land improvements are depreciated.

9-13© 2018 Pearson Education, Inc.

Buildings

Constructing a Building• Architectural fees• Building permits• Contractor charges• Payments for materials,

labor, and miscellaneous costs

Purchasing an Existing Building• Purchase price• Costs to renovate the

building to ready the building for use, which may include any of the charges listed under the “Constructing a Building” column

9-14© 2018 Pearson Education, Inc.

The costs of a building include:

13

14

8/28/2019

8

Machinery and Equipment

• The cost of machinery and equipment includes:– Purchase price (less any discounts)– Transportation charges– Insurance while in transit– Sales tax and other taxes– Purchase commission– Installation costs– Testing costs (prior to use of the asset)

9-15© 2018 Pearson Education, Inc.

Furniture and Fixtures

• Examples of furniture and fixtures include:– Desks– Chairs– File cabinets

• The costs of furniture and fixtures include:– Purchase price (less any discounts)– All other costs to ready the asset for its

intended use

9-16© 2018 Pearson Education, Inc.

15

16

8/28/2019

9

Lump-Sum Purchase

9-17

• A company may pay a single price for several assets as a group; this is called a lump-sum purchase.– Also called a basket purchase

• The company must identify the cost of each asset purchased.

• The total cost paid is divided among the assets according to their relative fair market values. This is called the relative-market-value method.

© 2018 Pearson Education, Inc.

Lump-Sum PurchaseSuppose Smart Touch Learning paid $100,000 on August 1, 2019, for the land and building. An appraisal indicates the land’s market value is $30,000, and the building’s market value is $90,000.

9-18© 2018 Pearson Education, Inc.

17

18

8/28/2019

10

Lump-Sum Purchase

For Smart Touch Learning, the land is assigned a cost of $25,000, and the building is assigned a cost of $75,000, calculated as follows:

9-19© 2018 Pearson Education, Inc.

Lump-Sum Purchase

Assume Smart Touch Learning purchased the assets by signing a note payable. The entry to record the purchase of the land and building is:

9-20© 2018 Pearson Education, Inc.

19

20

8/28/2019

11

Capital and Revenue Expenditures

• Accountants divide spending on plant assets after the acquisition into two categories:– Capital expenditures increase the asset’s

capacity or efficiency or extends the asset’s useful life.• Includes extraordinary repairs, which are

repairs that extend the asset’s useful life– Revenue expenditures are expenses incurred

to maintain the asset in working order.

9-21© 2018 Pearson Education, Inc.

Capital and Revenue Expenditures

Spending $3,000 to rebuild the engine on a five-year-old truck is an extraordinary repair because it extends the asset’s life past the normal expected life.

9-22© 2018 Pearson Education, Inc.

21

22

8/28/2019

12

Capital and Revenue Expenditures

Smart Touch Learning paid $500 cash to replace tires on the truck. This expenditure does not extend the useful life of the truck or increase its efficiency.

9-23© 2018 Pearson Education, Inc.

Capital and Revenue Expenditures

9-24© 2018 Pearson Education, Inc.

23

24

8/28/2019

13

Learning Objective 2

Account for depreciation using the straight-line, units-of-production, and double-declining-balance methods

9-25© 2018 Pearson Education, Inc.

WHAT IS DEPRECIATION, AND HOW IS IT COMPUTED?

• Depreciation matches the expense against the revenue generated from using an asset.

• All assets, except land, wear out as they are used.

• Some assets may become obsolete before they wear out. An asset is obsolete when a newer asset can perform the job more efficiently.

9-26© 2018 Pearson Education, Inc.

25

26

8/28/2019

14

Factors in Computing Depreciation

Depreciation of a plant asset is based on three main factors:1. Capitalized cost2. Estimated useful life, which is how long the

company expects it will use the asset.3. Estimated residual value, which is the expected

value of a depreciable asset at the end of its useful life.– Cost minus estimated residual value is called

depreciable cost.

9-27© 2018 Pearson Education, Inc.

Depreciation Methods

Three most commonly used depreciation methods:1. Straight-line method2. Units-of-production method3. Double-declining-balance method

9-28© 2018 Pearson Education, Inc.

27

28

8/28/2019

15

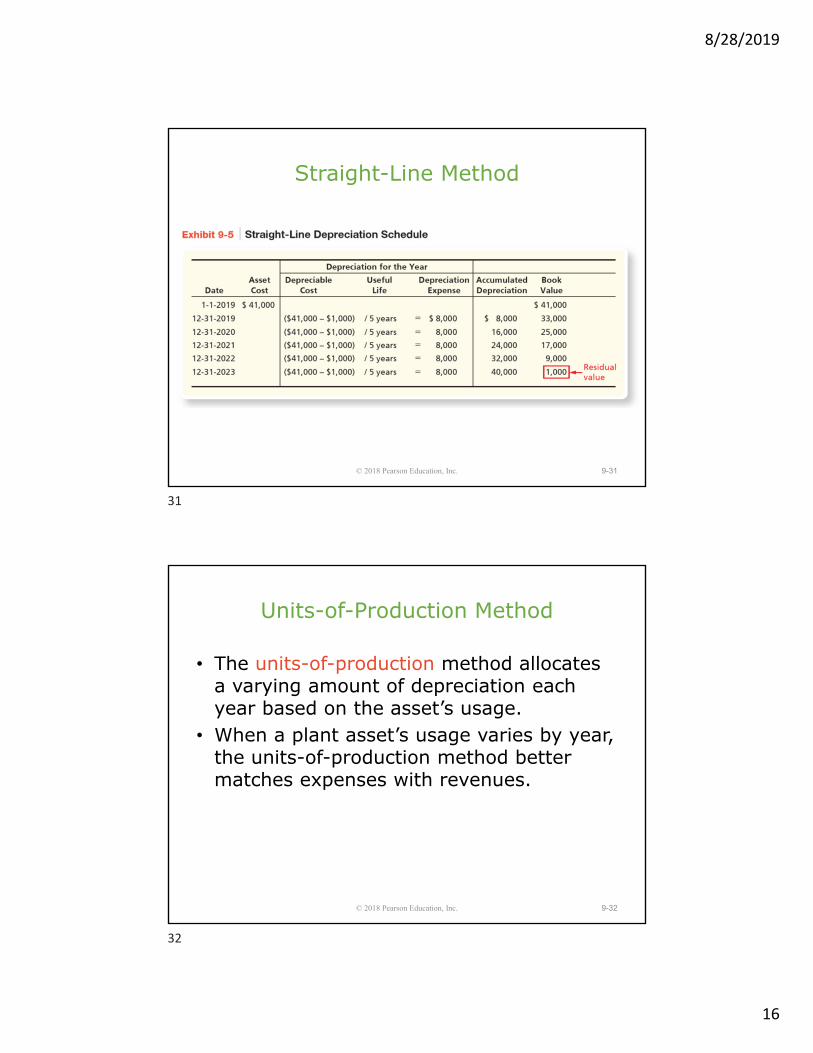

Straight-Line Method

The straight-line method allocates an equal amount of depreciation to each year and is computed as follows:

The entry to record the year’s depreciation expense:

9-29© 2018 Pearson Education, Inc.

Straight-Line Method

• Depreciation expense is reported on the income statement.

• The book value of the asset, cost minus accumulated depreciation, is reflected on the balance sheet.

9-30© 2018 Pearson Education, Inc.

29

30

8/28/2019

16

Straight-Line Method

9-31© 2018 Pearson Education, Inc.

Units-of-Production Method

9-32

• The units-of-production method allocates a varying amount of depreciation each year based on the asset’s usage.

• When a plant asset’s usage varies by year, the units-of-production method better matches expenses with revenues.

© 2018 Pearson Education, Inc.

31

32

8/28/2019

17

Units-of-Production Method

Smart Touch Learning expects to drive the truck 20,000 miles the first year, 30,000 miles the second, 25,000 the third, 15,000 the fourth, and 10,000 the fifth—for a total of 100,000 miles.

9-33© 2018 Pearson Education, Inc.

Units-of-Production Method

9-34© 2018 Pearson Education, Inc.

33

34

8/28/2019

18

Double-Declining Balance Method

9-35

• An accelerated depreciation method expenses more of the asset’s cost near the start of an asset’s life and less at the end of its useful life.– The main accelerated method of depreciation is

the double-declining-balance method.– The double-declining-balance method

multiplies an asset’s decreasing book value by a constant percentage that is twice the straight-line depreciation rate.

© 2018 Pearson Education, Inc.

Double-Declining Balance Method

9-36

• Double-declining-balance amounts can be computed using the following formula:

• For the first year of the truck:

• In year 2:

© 2018 Pearson Education, Inc.

35

36

8/28/2019

19

Double-Declining Balance Method

9-37© 2018 Pearson Education, Inc.

Comparing Depreciation Methods

9-38© 2018 Pearson Education, Inc.

37

38

8/28/2019

20

Comparing Depreciation Methods

9-39© 2018 Pearson Education, Inc.

Depreciation for Tax Purposes

9-40

• The Internal Revenue Service (IRS) requires that companies use the Modified Accelerated Cost Recovery System (MACRS) for tax purposes.– Under MACRS, assets are divided into specific

classes such as 3-year, 5-year, 7-year, and 39-year property.

– The IRS specifies the life of the asset.– Residual value ignored– MACRS is not acceptable for GAAP

© 2018 Pearson Education, Inc.

39

40

8/28/2019

21

Partial-Year Depreciation

• When a business purchases an asset during the year (other than January 1), it should record depreciation for only the portion of the year that the asset was used in the operations of the business.

• The modified half-month convention is used for assets purchased during the month– Record depreciation for the entire month if the

asset was purchased on or before the 15th.– Do not record depreciation in the purchase

month if the asset was purchased after the 15th.

9-41© 2018 Pearson Education, Inc.

Partial-Year Depreciation

Assume a truck costing $41,000 was placed into service on July 1, 2019. It has a $1,000 residual value and a 5 year life.

9-42© 2018 Pearson Education, Inc.

41

42

8/28/2019

22

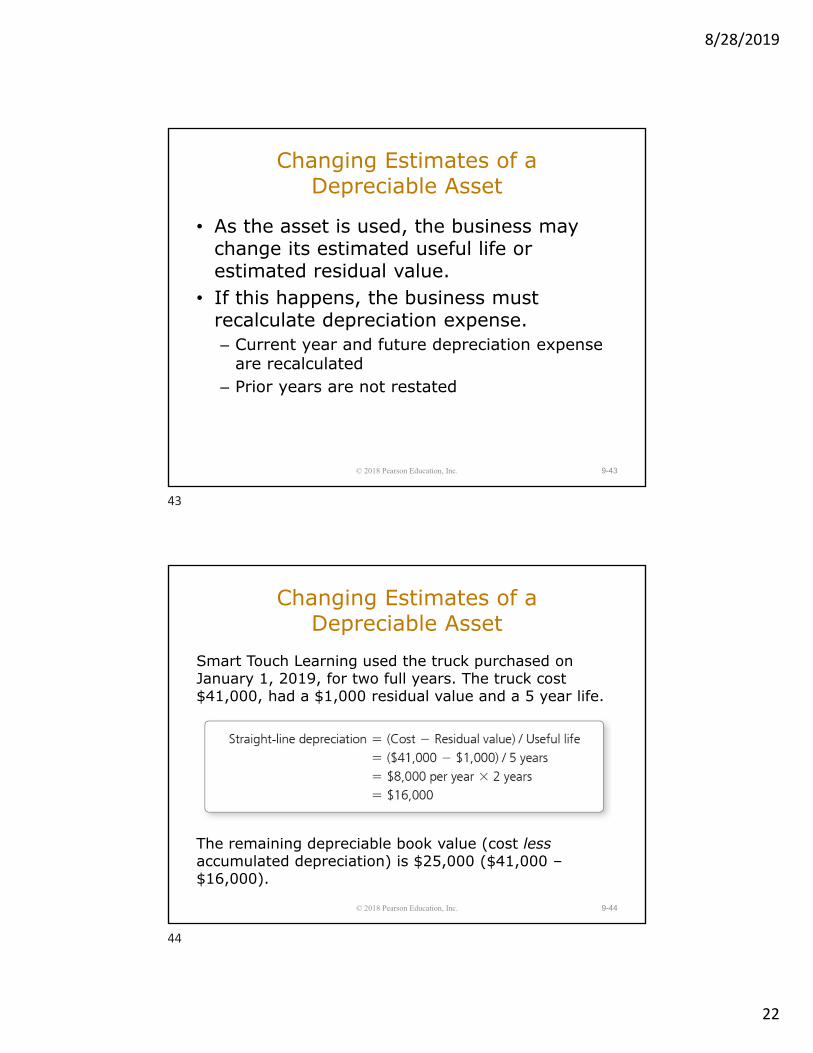

Changing Estimates of a Depreciable Asset

• As the asset is used, the business may change its estimated useful life or estimated residual value.

• If this happens, the business must recalculate depreciation expense.– Current year and future depreciation expense

are recalculated– Prior years are not restated

9-43© 2018 Pearson Education, Inc.

Changing Estimates of a Depreciable Asset

Smart Touch Learning used the truck purchased on January 1, 2019, for two full years. The truck cost $41,000, had a $1,000 residual value and a 5 year life.

The remaining depreciable book value (cost less accumulated depreciation) is $25,000 ($41,000 –$16,000).

9-44© 2018 Pearson Education, Inc.

43

44

8/28/2019

23

Changing Estimates of a Depreciable Asset

Smart Touch Learning believes the truck will remain useful for six more years (for a total of eight years). Residual value is unchanged. At the start of 2021, the company would recompute depreciation as follows:

9-45© 2018 Pearson Education, Inc.

Changing Estimates of a Depreciable Asset

In years 2021 to 2026, the yearly depreciation entry based on the new useful life would be as follows:

9-46© 2018 Pearson Education, Inc.

45

46

8/28/2019

24

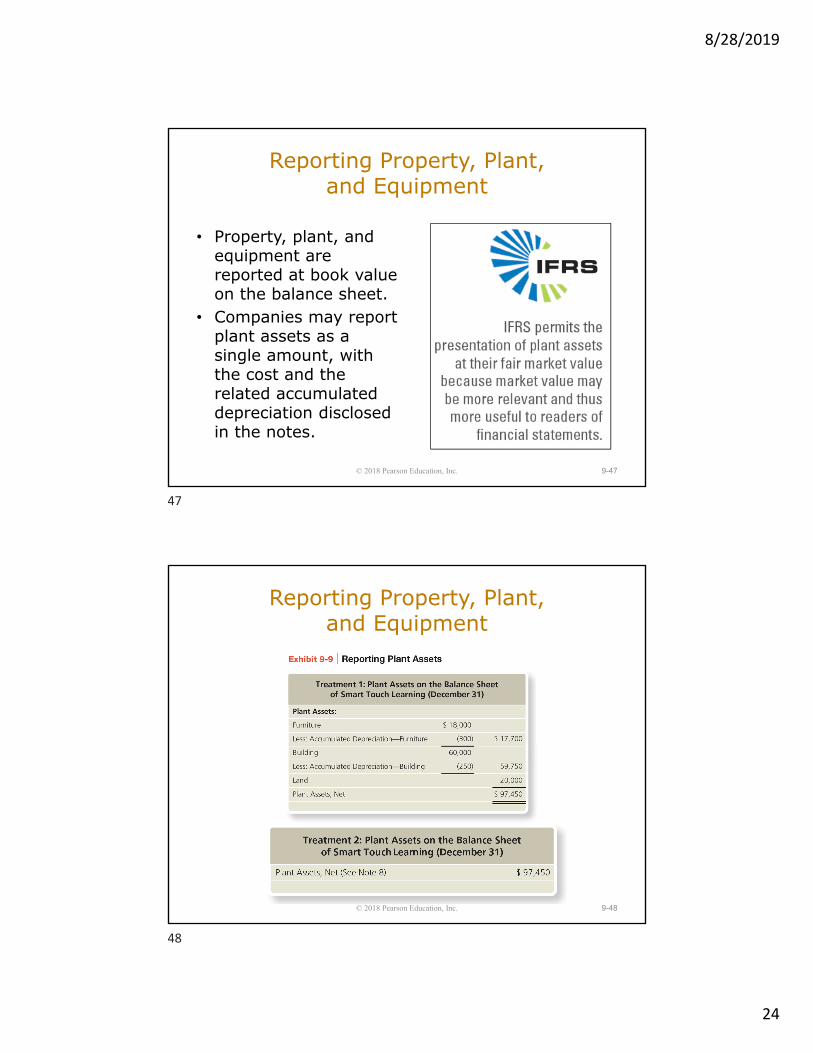

Reporting Property, Plant, and Equipment

• Property, plant, and equipment are reported at book value on the balance sheet.

• Companies may report plant assets as a single amount, with the cost and the related accumulated depreciation disclosed in the notes.

9-47© 2018 Pearson Education, Inc.

Reporting Property, Plant, and Equipment

9-48© 2018 Pearson Education, Inc.

47

48

8/28/2019

25

Learning Objective 3

Journalize entries for the disposal of plant assets

9-49© 2018 Pearson Education, Inc.

HOW ARE DISPOSALS OF PLANT ASSETS RECORDED?

9-50

• Eventually, an asset wears out or becomes obsolete. The business then has several options:– Discard the plant asset.– Sell the plant asset.– Exchange the plant asset for another asset.

© 2018 Pearson Education, Inc.

49

50

8/28/2019

26

HOW ARE DISPOSALS OF PLANT ASSETS RECORDED?

• Regardless of the type of disposal, there are four steps:1. Bring the depreciation up to date.2. Remove the old, disposed-of asset and

associated accumulated depreciation from the books.

3. Record the value of any cash received (or paid).

4. Determine the amount of any gain or loss.

9-51© 2018 Pearson Education, Inc.

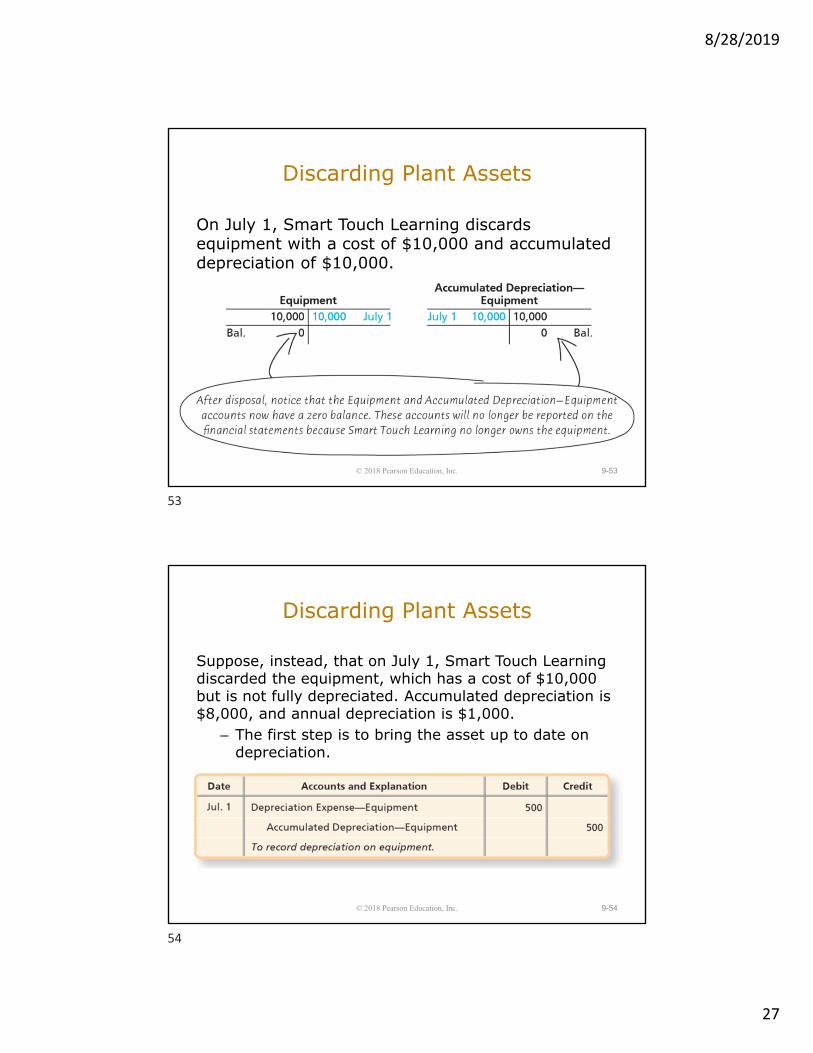

Discarding Plant Assets

9-52

On July 1, Smart Touch Learning discards equipment with a cost of $10,000 and accumulated depreciation of $10,000.

© 2018 Pearson Education, Inc.

51

52

8/28/2019

27

Discarding Plant Assets

On July 1, Smart Touch Learning discards equipment with a cost of $10,000 and accumulated depreciation of $10,000.

9-53© 2018 Pearson Education, Inc.

Discarding Plant Assets

9-54

Suppose, instead, that on July 1, Smart Touch Learning discarded the equipment, which has a cost of $10,000 but is not fully depreciated. Accumulated depreciation is $8,000, and annual depreciation is $1,000.

– The first step is to bring the asset up to date on depreciation.

© 2018 Pearson Education, Inc.

53

54

8/28/2019

28

Discarding Plant Assets

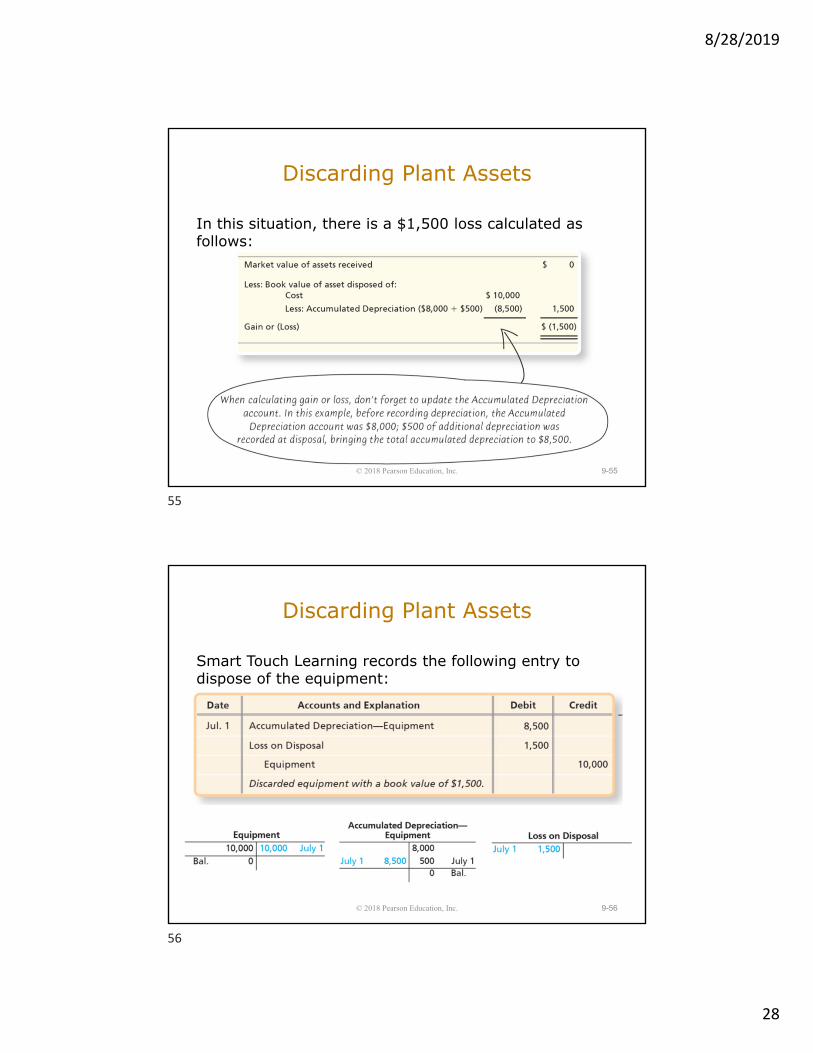

9-55

In this situation, there is a $1,500 loss calculated as follows:

© 2018 Pearson Education, Inc.

Discarding Plant Assets

9-56

Smart Touch Learning records the following entry to dispose of the equipment:

© 2018 Pearson Education, Inc.

55

56

8/28/2019

29

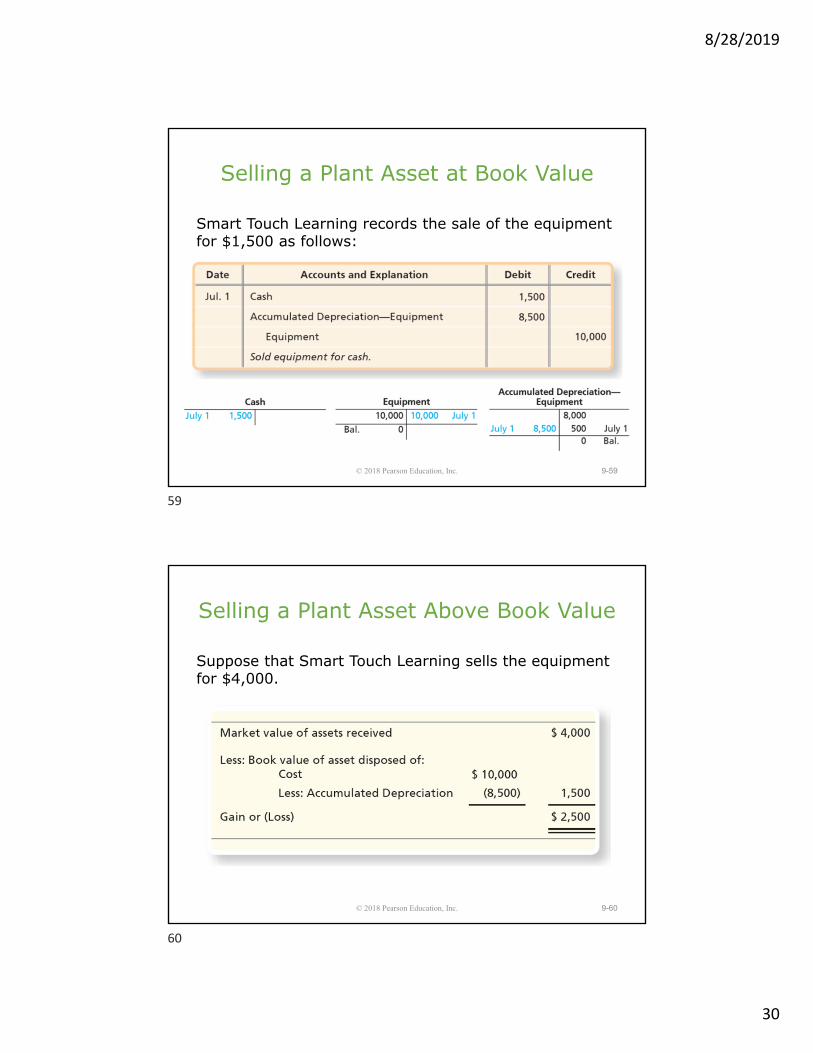

Selling Plant Assets

On July 1, the company sells equipment with a historical cost of $10,000 and accumulated depreciation, as of December 31 of the previous year, of $8,000. Annual depreciation is $1,000. The first step is to bring the depreciation up to date:

9-57© 2018 Pearson Education, Inc.

Selling a Plant Asset at Book Value

Suppose that Smart Touch Learning sells the equipment for $1,500.

9-58© 2018 Pearson Education, Inc.

57

58

8/28/2019

30

Selling a Plant Asset at Book Value

Smart Touch Learning records the sale of the equipment for $1,500 as follows:

9-59© 2018 Pearson Education, Inc.

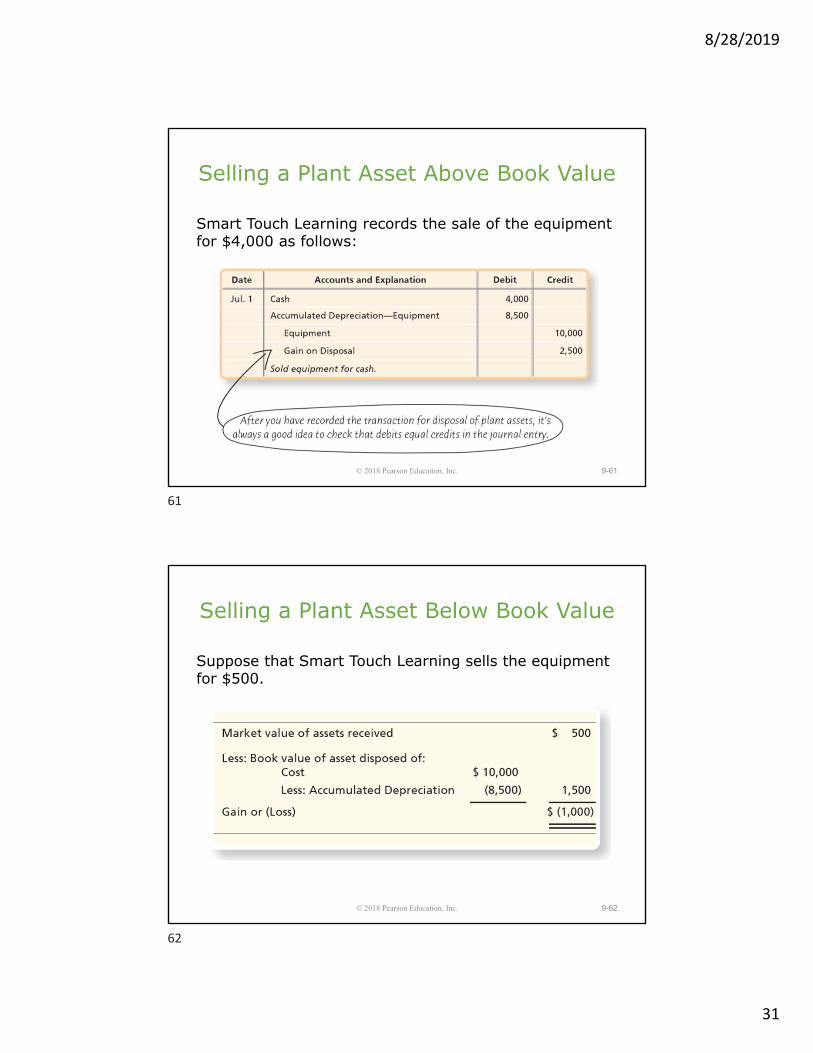

Selling a Plant Asset Above Book Value

Suppose that Smart Touch Learning sells the equipment for $4,000.

9-60© 2018 Pearson Education, Inc.

59

60

8/28/2019

31

Selling a Plant Asset Above Book Value

Smart Touch Learning records the sale of the equipment for $4,000 as follows:

9-61© 2018 Pearson Education, Inc.

Selling a Plant Asset Below Book Value

Suppose that Smart Touch Learning sells the equipment for $500.

9-62© 2018 Pearson Education, Inc.

61

62

8/28/2019

32

Selling a Plant Asset Below Book Value

Smart Touch Learning records the sale of the equipment for $500 as follows:

9-63© 2018 Pearson Education, Inc.

Summary

9-64© 2018 Pearson Education, Inc.

63

64

8/28/2019

33

Exhibit 9-10 summarizes the journal entries for

discarding and selling of plant assets.

9-65© 2018 Pearson Education, Inc.

Summary

RS1

Learning Objective 4

Account for natural resources

9-66© 2018 Pearson Education, Inc.

65

66

Slide 65

RS1 Replace art with jpg provided.Roberta Sherman, 4/17/2017

8/28/2019

34

HOW ARE NATURAL RESOURCES ACCOUNTED FOR?

• Natural resources are assets that come from the earth that are consumed.

• Depletion is the process by which businesses spread the allocation of a natural resource’s cost to expense over its usage.

• Depletion is computed by the units-of-production method.

9-67© 2018 Pearson Education, Inc.

HOW ARE NATURAL RESOURCES ACCOUNTED FOR?

Assume an oil well cost $700,000 and is estimated to hold 70,000 barrels of oil. There is no residual value. 3,000 barrels are extracted during the year.

9-68© 2018 Pearson Education, Inc.

67

68

8/28/2019

35

HOW ARE NATURAL RESOURCES ACCOUNTED FOR?

The depletion entry for the year is as follows:

9-69© 2018 Pearson Education, Inc.

HOW ARE NATURAL RESOURCES ACCOUNTED FOR?

Accumulated Depletion is a contra asset account similar to Accumulated Depreciation.• Natural resources can be reported on the balance

sheet as:

9-70© 2018 Pearson Education, Inc.

69

70

8/28/2019

36

Learning Objective 5

Account for intangible assets

9-71© 2018 Pearson Education, Inc.

HOW ARE INTANGIBLE ASSETS ACCOUNTED FOR?

• Intangible assets are assets that have no physical form.

• Examples of intangible assets include: – Patents– Copyrights– Trademarks– Other creative works

9-72© 2018 Pearson Education, Inc.

71

72

8/28/2019

37

Accounting for Intangibles

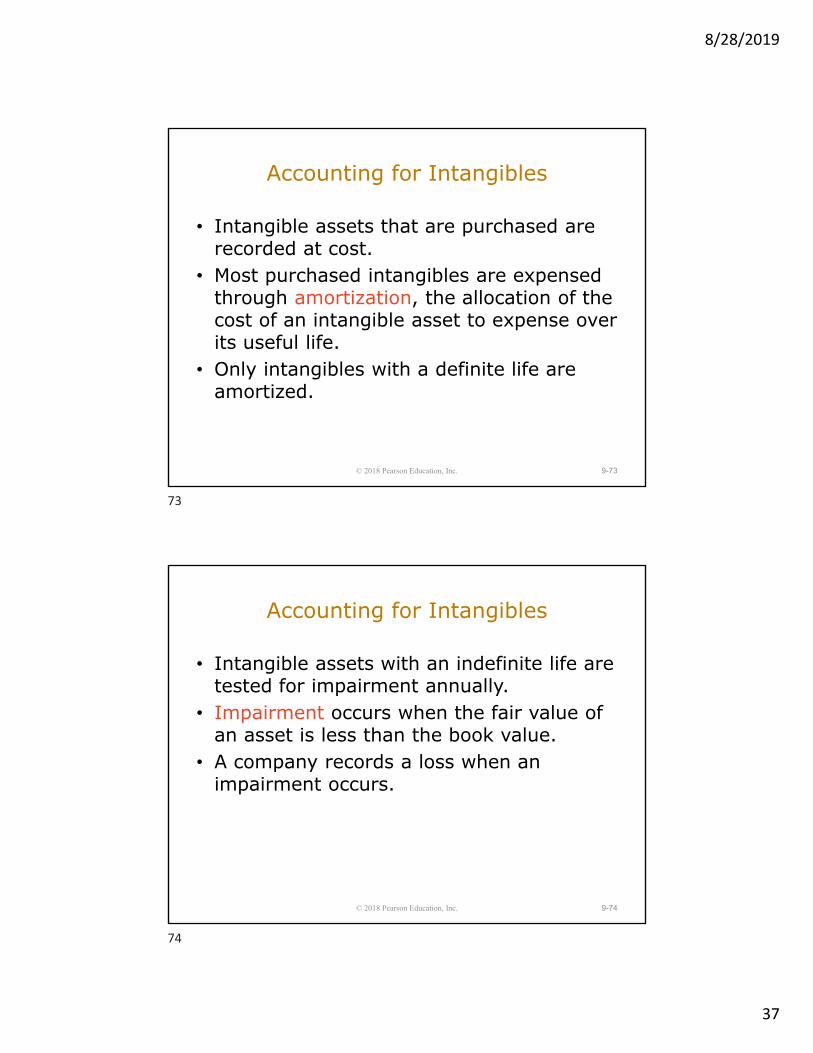

• Intangible assets that are purchased are recorded at cost.

• Most purchased intangibles are expensed through amortization, the allocation of the cost of an intangible asset to expense over its useful life.

• Only intangibles with a definite life are amortized.

9-73© 2018 Pearson Education, Inc.

Accounting for Intangibles

• Intangible assets with an indefinite life are tested for impairment annually.

• Impairment occurs when the fair value of an asset is less than the book value.

• A company records a loss when an impairment occurs.

9-74© 2018 Pearson Education, Inc.

73

74

8/28/2019

38

Patents

• A patent is an intangible asset that is a federal grant conveying an exclusive 20-year right to produce and sell an invention.

• The invention may be a process, product, or formula.

• The acquisition cost of a patent is debited to the Patent account.

9-75© 2018 Pearson Education, Inc.

Patents

Assume Smart Touch Learning pays $200,000 to acquire a patent on January 1. Acquisition entry:

9-76© 2018 Pearson Education, Inc.

75

76

8/28/2019

39

Patents

Assume Smart Touch Learning pays $200,000 to acquire a patent on January 1. The useful life of the patent is determined to be five years.

9-77© 2018 Pearson Education, Inc.

Patents

Adjusting entry to record amortization:

• A company may credit an intangible asset directly when recording amortization expense, or it may use Accumulated Amortization.

9-78© 2018 Pearson Education, Inc.

77

78

8/28/2019

40

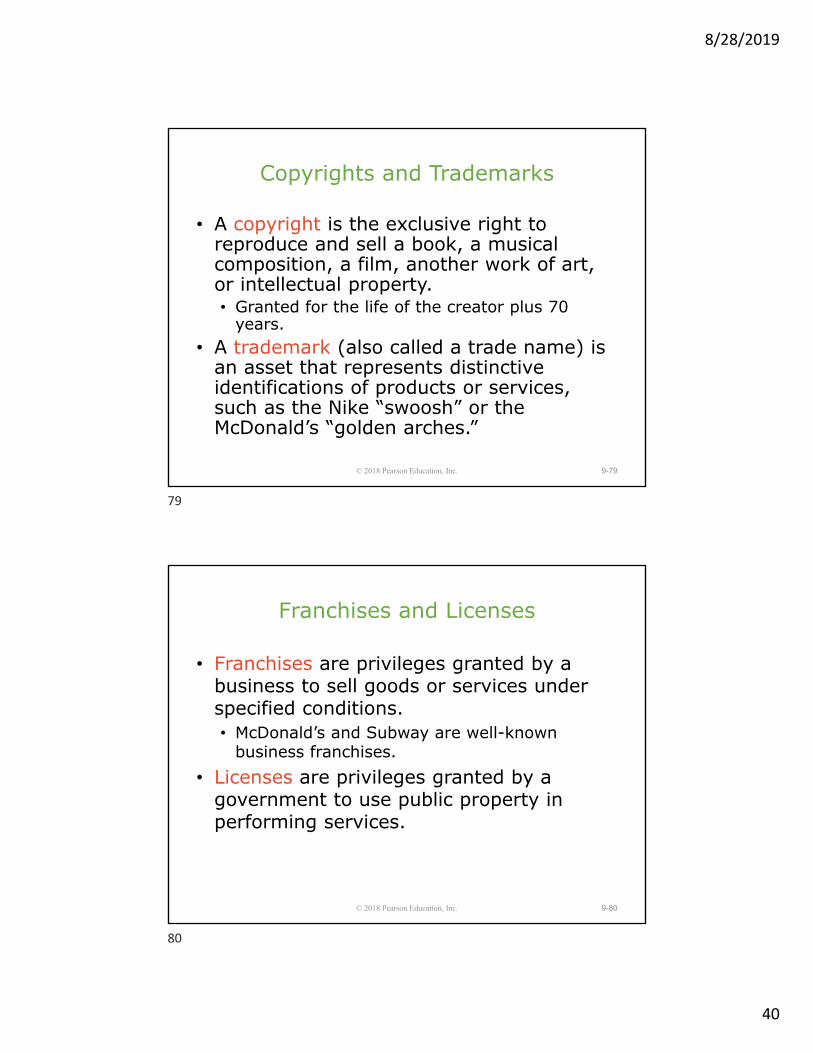

Copyrights and Trademarks

• A copyright is the exclusive right to reproduce and sell a book, a musical composition, a film, another work of art, or intellectual property.• Granted for the life of the creator plus 70

years.• A trademark (also called a trade name) is

an asset that represents distinctive identifications of products or services, such as the Nike “swoosh” or the McDonald’s “golden arches.”

9-79© 2018 Pearson Education, Inc.

Franchises and Licenses

• Franchises are privileges granted by a business to sell goods or services under specified conditions.• McDonald’s and Subway are well-known

business franchises.• Licenses are privileges granted by a

government to use public property in performing services.

9-80© 2018 Pearson Education, Inc.

79

80

8/28/2019

41

Goodwill

• Goodwill is the value paid above the net worth of a company’s assets and liabilities.

• Special features of goodwill:• It is recorded by an acquiring company when it

purchases another company for more than the market value of the net assets acquired.

• Goodwill is not amortized.

9-81© 2018 Pearson Education, Inc.

Goodwill

White Corporation acquired Mocha, Inc. on January 1, 2018. The sum of the market values of Mocha’s assets was $9 million and its liabilities totaled $1 million, so Mocha’s net assets totaled $8 million. Suppose White paid $10 million to purchase Mocha.

9-82© 2018 Pearson Education, Inc.

81

82

8/28/2019

42

Goodwill

White’s entry to record the purchase of Mocha:

9-83© 2018 Pearson Education, Inc.

Reporting of Intangible Assets

9-84© 2018 Pearson Education, Inc.

83

84

8/28/2019

43

Learning Objective 6

Use the asset turnover ratio to evaluate business performance

9-85© 2018 Pearson Education, Inc.

HOW DO WE USE THE ASSET TURNOVER RATIO TO EVALUATE BUSINESS

PERFORMANCE?

• The asset turnover ratio measures the amount of net sales generated for each average dollar of total assets invested.

• To compute this ratio, we divide net sales by average total assets.

• A high asset turnover ratio is desirable.

9-86© 2018 Pearson Education, Inc.

85

86

8/28/2019

44

HOW DO WE USE THE ASSET TURNOVER RATIO TO EVALUATE BUSINESS

PERFORMANCE?Asset turnover ratio based on Kohl’s 2015 Annual Report:

9-87© 2018 Pearson Education, Inc.

Learning Objective 7

Journalize entries for the exchange of plant assets (Appendix 9A)

9-88© 2018 Pearson Education, Inc.

87

88

8/28/2019

45

HOW ARE EXCHANGES OF PLANT ASSETS ACCOUNTED FOR?

• A business may exchange a plant asset for another plant asset.

• An exchange has commercial substance if the future cash flows change as a result of the transaction.

• Exchanges that have commercial substance require any gain or loss on the transaction to be recognized.

9-89© 2018 Pearson Education, Inc.

Exchange of Plant Assets—Gain Situation

9-90

On December 31, Smart Touch Learning exchanges $2,000 cash plus used equipment with a historical cost of $10,000 and accumulated depreciation of $9,000 for new equipment. The new equipment has a market value of $8,000. The exchange has commercial substance.

© 2018 Pearson Education, Inc.

89

90

8/28/2019

46

Exchange of Plant Assets—Gain Situation

9-91

Journal entry to record the exchange:

© 2018 Pearson Education, Inc.

Exchange of Plant Assets—Loss Situation

9-92

On December 31, Smart Touch Learning exchanges $2,500 cash plus used equipment with a historical cost of $10,000 and accumulated depreciation of $9,000 for new equipment. The new equipment has a market value of $3,000. The exchange has commercial substance.

© 2018 Pearson Education, Inc.

91

92

8/28/2019

47

Exchange of Plant Assets—Loss Situation

9-93

Journal entry to record the exchange:

© 2018 Pearson Education, Inc.

9-94© 2018 Pearson Education, Inc.

93

94