CHAPTER 8icm.clsbe.lisboa.ucp.pt/docentes/url/rireis/fall05/sm_ch08.pdf · 8-1 Tangible assets are...

69

Chapter 8 Long-Lived Assets and Depreciation 371 CHAPTER 8 8-1 Tangible assets are those that can be seen and touched. Intangible assets are those rights or economic benefits that are not physical in nature. 8-2 All three terms refer to an allocation of costs over time. Reduction of intangible assets is generally called amortization. Depreciation is a reduction in buildings and equipment and other tangible assets. Depletion is a reduction in natural resources. 8-3 Cash discounts are reductions in original cost, not income. 8-4 When an expenditure is capitalized, it is not credited to stockholders' equity. Rather, it becomes an asset with a useful life in excess of one year. An asset is debited and generally either cash or a liability is credited. 8-5 Accumulated depreciation is not cash; if specific cash is being accumulated for the replacement of assets, such cash will be an asset specifically labeled as a "cash fund for replacement and expansion" or a "fund of marketable securities for replacement and expansion." Accumulated depreciation is the cumulative amount of an asset’s depreciable value that has been expensed. 8-6 Valuation implies some measure of present market value. In contrast, depreciation is the systematic allocation of the original cost of the asset as an expense on the income statement over the useful life of the asset. 8-7 Depreciation is a method of cost allocation , not valuation. It simply allocates the cost of an asset to the periods that benefit from its use.

Transcript of CHAPTER 8icm.clsbe.lisboa.ucp.pt/docentes/url/rireis/fall05/sm_ch08.pdf · 8-1 Tangible assets are...

Chapter 8 Long-Lived Assets and Depreciation 371

CHAPTER 8 8-1 Tangible assets are those that can be seen and touched.

Intangible assets are those rights or economic benefits that are not physical in nature.

8-2 All three terms refer to an allocation of costs over time.

Reduction of intangible assets is generally called amortization. Depreciation is a reduction in buildings and equipment and other tangible assets. Depletion is a reduction in natural resources.

8-3 Cash discounts are reductions in original cost, not income. 8-4 When an expenditure is capitalized, it is not credited to

stockholders' equity. Rather, it becomes an asset with a useful life in excess of one year. An asset is debited and generally either cash or a liability is credited.

8-5 Accumulated depreciation is not cash; if specific cash is being

accumulated for the replacement of assets, such cash will be an asset specifically labeled as a "cash fund for replacement and expansion" or a "fund of marketable securities for replacement and expansion." Accumulated depreciation is the cumulative amount of an asset’s depreciable value that has been expensed.

8-6 Valuation implies some measure of present market value. In

contrast, depreciation is the systematic allocation of the original cost of the asset as an expense on the income statement over the useful life of the asset.

8-7 Depreciation is a method of cost allocation, not valuation. It

simply allocates the cost of an asset to the periods that benefit from its use.

372

8-8 No. Keeping two sets of books is necessary if two separate purposes are being legally fulfilled. In many cases two sets of books are required, sometimes more than two. Requirements include external financial reporting, internal managerial needs and tax reporting.

8-9 Both choices are between initially greater current income and

asset values (straight-line and FIFO) versus initially smaller current income and asset values (accelerated and LIFO). This statement assumes rising price levels for inventory items. The choices differ because the FIFO-LIFO choice affects cash flows via its tax consequences. Why? Because the IRS requires all firms using LIFO for tax purposes to use it for financial reporting purposes as well. On the other hand the accelerated versus straight-line choice does not affect cash flow because a firm does not have to change its depreciation method used for tax reporting because of this choice for financial reporting.

8-10 No. Depreciation, by itself, generates no cash. 8-11 Accelerated depreciation used for tax purposes usually leads

to higher depreciation expense early in an asset’s life and hence lower pretax income. Because pretax income is lower, taxes are lower. Depreciation does not affect cash, but taxes do. Lower taxes mean more cash. Remember, however, that many firms use accelerated MACRS depreciation for tax purposes and straight-line for financial reporting to the public.

8-12 The costs of repairs and maintenance are expenses of the

current period. They maintain a fixed asset in operating condition. In contrast, capital improvements or betterments are capitalized and then depreciated because they add to the future benefits of an existing asset, often by either extending its life or decreasing its operating costs.

Chapter 8 Long-Lived Assets and Depreciation 373

8-13 The division's expenditures, including cash outlays to acquire new assets, are likely to fall, but expenses (which include depreciation on the new capital facilities) will probably not fall.

8-14 Gain on sale of equipment is a net result: revenue (that is,

proceeds) minus expense (that is, book value) equals gain. Complete reporting would show the proceeds, the book value, and the gain.

8-15 Patents grant the inventor exclusive rights to the invention for

a specified period of time. Copyrights give similar rights to printed or artistic items. Trademarks are distinctive identifications of a product or service. Franchises are privileges granted to sell a specific product or service under defined conditions. Goodwill is the excess of the cost of an acquired company over the net market value of the identifiable individual assets and liabilities acquired.

8-16 Internally acquired patents are essentially research costs,

which must be written off to expense as they are incurred. Externally acquired patents are assets that are subject to amortization and/or impairment review.

8-17 The preoccupation with physical evidence often results in the

expensing of outlays that many think should be treated as assets. Thus, expenditures for research, advertising, employee training, and the like are usually expensed, although it seems clear that, in an economic sense, such expenditures represent expected future benefits.

8-18 No. Improvements to leased property are capitalized just like

capital improvements or betterments except that they are amortized over the remaining life of the lease if it is shorter than the useful life of the improvements or betterments.

374

8-19 The $5,000 gain is double-counted. The increase in cash was $20,000, not $25,000. The $20,000 proceeds includes the $5,000 gain. Under the indirect method of the statement of cash flows, the gain must be subtracted from net income in the operating section of the statement of cash flows. Under the direct method it does not appear in the statement at all.

8-20 The asset was sold for $5,000 + $4,000 = $9,000. The entire

$9,000 should be reported as a cash inflow from investing activities. In an indirect method statement of cash flows, the $4,000 gain must be deducted from net income in computing net cash provided by operating activities.

8-21 No. In a basket purchase, different assets are often depreciated

over different time periods. For example, basket purchases sometimes include land and a building. The building is depreciated while the land remains on the books at original cost.

8-22 No. The recoverability test determines whether or not there is

evidence of impairment. The impairment loss is the amount by which the book value of the asset exceeds its fair value.

8-23 The manager has a point. However, under cost-based

accounting the historical cost of long-lived assets is allocated to the periods during which the assets will be used. We do not recognize income from the appreciation of long-lived assets. The complaint that the depreciation is large is worth considering. Normally we depreciate the asset over its useful life down to its residual value. Thus, it may be that the company has underestimated both the residual values and the lives of these assets.

Chapter 8 Long-Lived Assets and Depreciation 375

8-24 Treating research and development costs as assets is generally more consistent with the corporate perspective of the value inherent in R&D. Companies undertake R&D in hopes of creating future benefits, as asset accounting would suggest.

8-25 The statement of cash flows has a section that reports on the

financing actions the company has taken during the accounting period. Both borrowing and issuing of common stock would appear there. Of course, some capital is also generated by operations and some could be generated by the sale of assets. These sources of capital are revealed in the operating and investing segments of the statement of cash flows.

8-26 Due to continual changes in the purchasing power of the dollar,

we normally observe an increase in the value of land over time. Over 90 years have passed since the land was acquired, so the value today is likely to have little relationship to the value when it was purchased. In contrast, the equipment is recently acquired and is being depreciated over its useful life. Its book value is likely to be closer to its market value.

8-27 (10-15 min.)

Land: Cash, $600,000 + $150,000 demolition $ 750,000 Note 3,000,000 Total cost $ 3,750,000 Building: Cash $ 3,000,000 Mortgage 7,000,000 Total cost $10,000,000

The important point here is to see that the $150,000 demolition cost is a cost of land because the outlay is necessary to get the land ready for its intended use.

376

8-27 (continued)

Land 3,600,000 Cash 600,000 Note payable 3,000,000 Land 150,000 Cash 150,000 This could also be accomplished by the following compound entry:

Land 3,750,000 Cash 750,000 Note payable 3,000,000

The second entry is:

Building 10,000,000 Cash 3,000,000 Mortgage note payable 7,000,000

The payment terms of the note and the mortgage are irrelevant until financial statements must be prepared or payments must be made. Some students may prepare entries for the first year. Assuming end of year payment, these would be:

Note payable 300,000 Interest expense 300,000 Cash 600,000

Mortgage note payable 250,000 Interest expense 700,000 Cash 950,000

Chapter 8 Long-Lived Assets and Depreciation 377

8-28 (5-10 min.) The sales commission, the purchasing manager's salary, and the cost of repairs after the equipment is placed in use are irrelevant. The pertinent costs are:

Invoice price, gross $400,000 Deduct: 2% cash discount 8,000 Invoice price, net $392,000 Freight-in 4,400 Installation costs 8,000 Repair costs prior to use 9,000 Total acquisition cost $413,400

8-29 (5-10 min.) In the absence if more reliable data, the assessed values for property taxes are frequently used as a guide to allocating the costs of a basket purchase.

(1) (2) (3) (2) x (3)

Assessed Total Cost Allocated Value Weighting to Allocate Costs Land $200,000 20/60 $720,000 $240,000 Building 400,000 40/60 720,000 480,000 Total $600,000 $720,000

378

8-30 (10 min.) Player contracts may be amortized for tax purposes, but the sports franchise itself may not. Allen would want to allocate $299,999,999 to the contracts. In this way, he could get tax deductions. No part of the amount allocated to the franchise is deductible as amortization. Note: Through the years, the Internal Revenue Service has developed a rule for these transactions. The amount the buyer allocates to player contracts may not exceed what the seller allocates. This is limited to no more than 50 percent, unless the taxpayer can prove a greater allocation is proper.

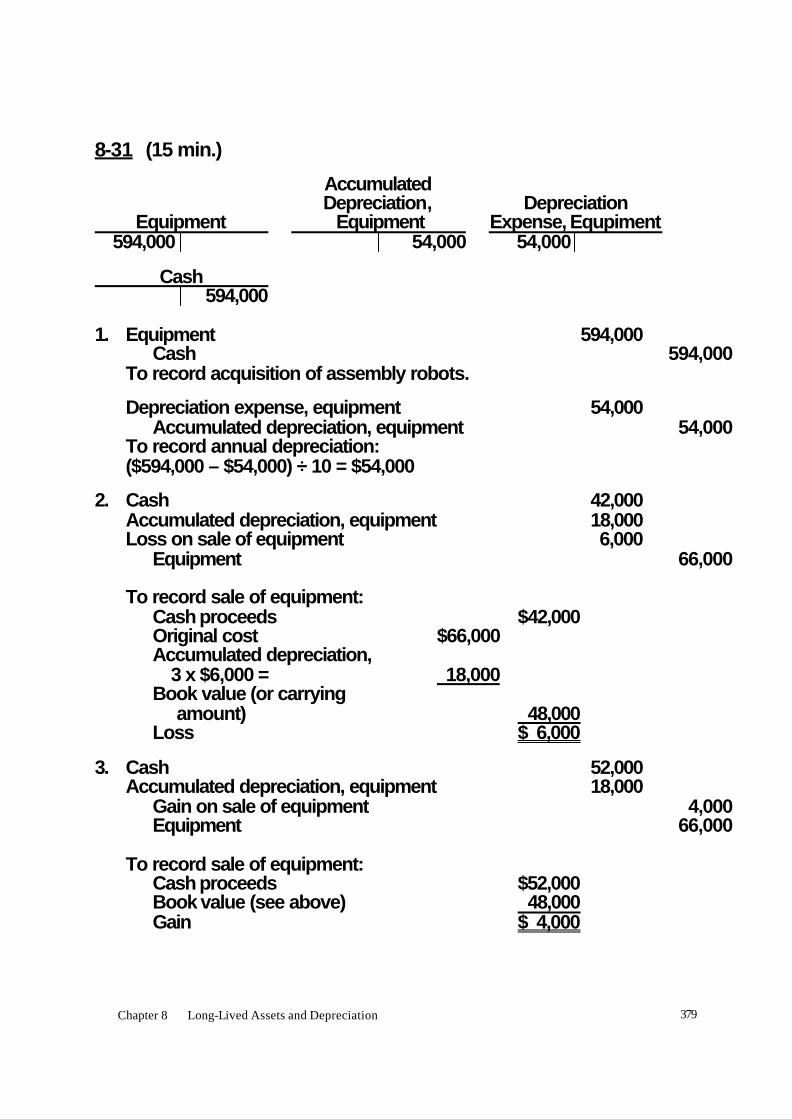

Chapter 8 Long-Lived Assets and Depreciation 379

8-31 (15 min.)

Accumulated Depreciation, Depreciation Equipment Equipment Expense, Equpiment 594,000 54,000 54,000

Cash 594,000 1. Equipment 594,000 Cash 594,000 To record acquisition of assembly robots.

Depreciation expense, equipment 54,000 Accumulated depreciation, equipment 54,000 To record annual depreciation: ($594,000 – $54,000) ÷ 10 = $54,000

2. Cash 42,000 Accumulated depreciation, equipment 18,000 Loss on sale of equipment 6,000 Equipment 66,000 To record sale of equipment: Cash proceeds $42,000 Original cost $66,000 Accumulated depreciation, 3 x $6,000 = 18,000 Book value (or carrying amount) 48,000 Loss $ 6,000

3. Cash 52,000 Accumulated depreciation, equipment 18,000 Gain on sale of equipment 4,000 Equipment 66,000 To record sale of equipment: Cash proceeds $52,000 Book value (see above) 48,000 Gain $ 4,000

380

8-32 (10-15 min.) You may want to use T-accounts too. 1. Depreciation expense, equipment 160,000 Accumulated depreciation, equipment 160,000 To record annual depreciation: ($880,000-$80,000) ÷ 5 = $160,000 2. Cash 160,000 Accumulated depreciation, equipment 80,000 Equipment 220,000 Gain on sale of equipment 20,000 To record sale of equipment: Cash proceeds $160,000 Original cost $220,000 Accumulated depreciation, 2 x $40,000 = 80,000 Book value (or carrying amount) 140,000 Gain on sale $ 20,000 3. Cash 110,000 Accumulated depreciation, equipment 80,000 Loss on sale of equipment 30,000 Equipment 220,000 To record sale of equipment: Cash proceeds $110,000 Book value (see above) 140,000 Loss on sale $ 30,000

Chapter 8 Long-Lived Assets and Depreciation 381

8-33 (10-15 min.) You may want to use T-accounts too. 1. Depreciation expense, equipment 300,000 Allowance for depreciation, equipment 300,000 To record annual depreciation: ($1,800,000 – $300,000) ÷ 5 = $300,000 2. Cash 32,000 Allowance for depreciation, equipment 22,000 Loss on sale of equipment 6,000 Equipment 60,000 To record sale of equipment: Cash proceeds $32,000 Original cost $60,000 Allowance for depre- ciation, 2 x $11,000 22,000 Book value (or carrying amount) 38,000 Loss $ 6,000 3. Cash 40,000 Allowance for depreciation, equipment 22,000 Equipment 60,000 Gain on sale of equipment 2,000

To record sale of equipment: Cash proceeds $40,000 Book value (see above) 38,000 Gain $ 2,000

382

8-34 (10-15 min.)

Year Conveyor* Truck** 1 $6,600 2/3 x $18,000 = $12,000 2 $6,600 2/3 x $ 6,000 = $ 4,000 3 $6,600 $500***

* Each year is 1/5 x ($38,000 – $5,000) = $6,600. ** DDB rate is 2 x (1/3) = 2/3. *** $500 of depreciation reduces the book value to the $1,500 residual

value. If the DDB schedule had continued, the depreciation of 2/3 x $2,000 = $1,333 would have reduced the book value below the residual value.

8-35 (10 min.)

1. (250,000)

$5,000)($80,000n

RCD

−=

−= = $.30 per mile

Depreciation expense: Year 1: $.30 x 60,000 = $18,000 Year 2: $.30 x 90,000 = $27,000 2. Net book value when sold: $80,000 – $18,000 – $27,000 =

$35,000. Gain on sale: $40,000 – $35,000 = $5,000.

Chapter 8 Long-Lived Assets and Depreciation 383

8-36 (15-25 min.) Numbers are in thousands.

Declining Balance at Twice the Straight Straight-Line* Line Rate (DDB)** Annual Book Annual Book Depreciation Value Depreciation Value At acquisition $1,200 $1,200 Year 1 $250 950 $600 600 2 250 700 300 300 3 250 450 100 200 4 250 200 0 200 Total $1,000 $1,000

* Depreciation is the same each year, 25% of ($1,200,000 – $200,000). ** Straight-line rate is 100% ÷ 4 = 25%. The DDB rate is 50%.

Depreciation in the first year is 50% of $1,200,000; in the second year it is 50% of ($1,200,000 – $600,000); in the third year depreciation is 50% of [$1,200,000 – ($600,000 + $300,000)] etc. This continues until the residual value is reached. Therefore, using DDB in this instance, depreciation for the third year would be 50% of $300,000, or $150,000; however, only $100,000 is shown because the residual value of $200,000 is thereby reached. Although not requested in this problem, another alternative is to use Modified DDB.

8-37 (10-15 min.)

Unit Year Depreciation Straight-Line* DDB** 1 (60 ÷ 150) x $400,000 = $160,000 $133,333 $293,333 2 (45 ÷ 150) x $400,000 = 120,000 133,333 97,778 3 (45 ÷ 150) x $400,000 = 120,000 133,333 8,889*** Total depreciation $400,000 $400,000 $400,000 * (1/3) x $400,000 = $133,333 each year ** 2 x (1/3) x $440,000 = $293,333; 2 x (1/3) x ($440,000 – $293,333) =

$97,778

384

*** Application of DDB would result in depreciation of 2 x 1/3 x ($440,000 - $293,333 - $97,778) = $32,593. However, this would depreciation the asset below its residual value of $40,000. Therefore, depreciation is only $8,889.

Chapter 8 Long-Lived Assets and Depreciation 385

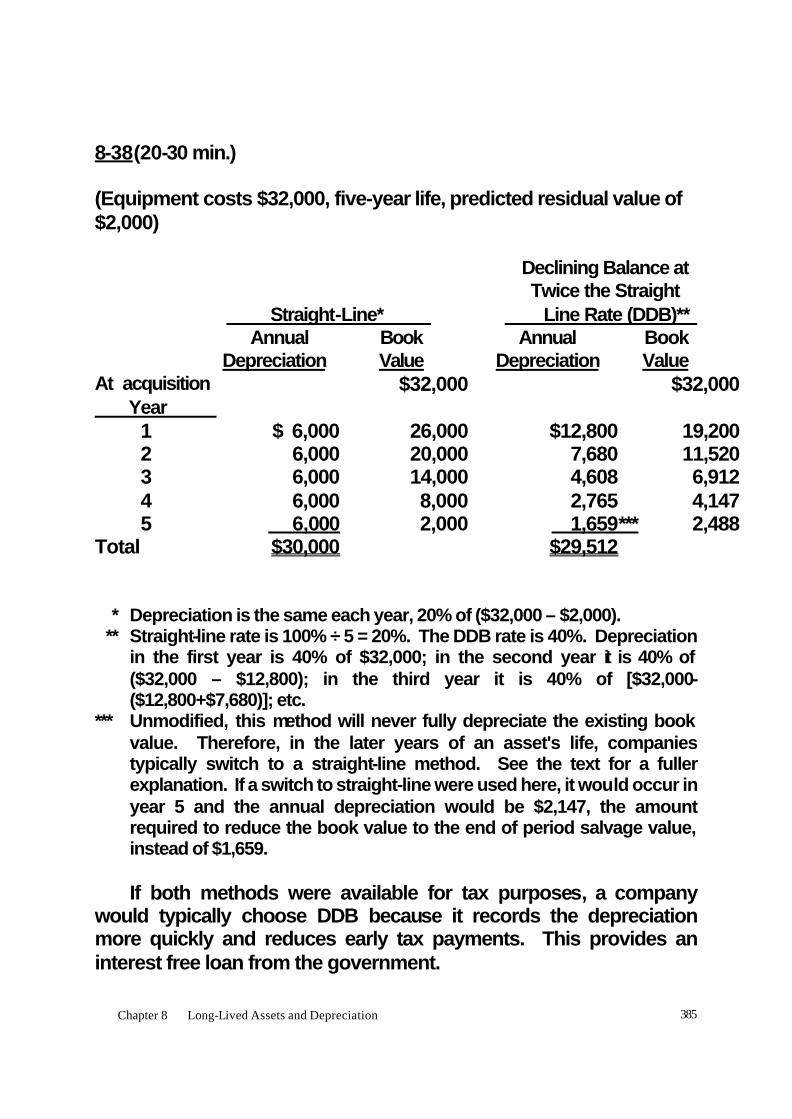

8-38 (20-30 min.) (Equipment costs $32,000, five-year life, predicted residual value of $2,000) Declining Balance at Twice the Straight Straight-Line* Line Rate (DDB)** Annual Book Annual Book Depreciation Value Depreciation Value At acquisition $32,000 $32,000 Year 1 $ 6,000 26,000 $12,800 19,200 2 6,000 20,000 7,680 11,520 3 6,000 14,000 4,608 6,912 4 6,000 8,000 2,765 4,147 5 6,000 2,000 1,659*** 2,488 Total $30,000 $29,512 * Depreciation is the same each year, 20% of ($32,000 – $2,000). ** Straight-line rate is 100% ÷ 5 = 20%. The DDB rate is 40%. Depreciation

in the first year is 40% of $32,000; in the second year it is 40% of ($32,000 – $12,800); in the third year it is 40% of [$32,000-($12,800+$7,680)]; etc.

*** Unmodified, this method will never fully depreciate the existing book value. Therefore, in the later years of an asset's life, companies typically switch to a straight-line method. See the text for a fuller explanation. If a switch to straight-line were used here, it would occur in year 5 and the annual depreciation would be $2,147, the amount required to reduce the book value to the end of period salvage value, instead of $1,659.

If both methods were available for tax purposes, a company

would typically choose DDB because it records the depreciation more quickly and reduces early tax payments. This provides an interest free loan from the government.

386

8-39 (20-30 min.) Amounts are in thousands of dollars. Accelerated Depreciation Declining Balance at Twice the Straight Straight-Line* Line Rate (DDB)** Annual Book Annual Book Depreciation Value Depreciation Value At acquisition 280 280 Year 1 32.5 247.5 70.0 210.0 2 32.5 215.0 52.5 157.5 3 32.5 182.5 39.4 118.1 * Depreciation is the same each year, 1/8 x [($280,000 – $20,000)] =

32,500. ** Straight-line rate is 100% ÷ 8 = 12.5%. The DDB rate is 25%.

Depreciation in the first year is 25% of $280; in the second year it is 25% of ($280 – $70.0); in the third year it is 25% of ($280 – $70.0 – $52.5); etc. Unmodified, this method will never fully depreciate the existing book value. In the later years of an asset's life, companies typically switch to a straight-line method. The asset is never depreciated below its estimated residual value, even though the latter is ignored when applying the depreciation rate.

Chapter 8 Long-Lived Assets and Depreciation 387

8-40 (10 min.)

BOEING COMPANY Property, Plant, and Equipment

December 31, 2003 (In Millions)

Land $ 457 Buildings 9,171 Machines and equipment 10,824 Construction in progress 943 Less: Accumulated depreciation (12,963)* Net property, plant, and equipment $ 8,432

*$457 + $9,171 + $10,824 + $943 − $8,432 = $12,963 8-41 (10 - 15 min.) Amounts are in thousands.

1. Historical cost = $477,581 + $440,607 = $918,188

2. Most of Oregon Steel’s assets are slightly less than 9 years old. We know this because the accumulated depreciation is less than half of the original cost of the property, plant, and equipment:

$440,607 ÷ $918,888 = .48, which is slightly less than .5.

or: 18 x .48 = 8.64 years average age

388

8-42 (15 min.) Amounts are in the thousands of dollars. Original Revised Straight-line* Straight-line** Annual Book Annual Book Depreciation Value Depreciation Value At acquisition year 75 75 2004 7 68 7 68 2005 7 61 7 61 2006 7 54 7 54 2007 7 47 7 47 2008 7 40 15.33 31.67 2009 7 33 15.33 16.34 2010 7 26 15.34 1 2011 7 19 2012 7 12 2013 7 5 Total $70 $73 *Depreciation is the same each year, 1/10 x (75,000- 5,000) = $7,000. ** Depreciation is the same for the first four years (2004 though 2007). In 2008, Nowling must recompute depreciation for the years 2008, 2009 and 2010 based on revised estimates: 1/3 x (47,000 – 1,000) ] = $15,333. 8-43 (30-45 min.)

1. See Exhibit 8-43 on the following page.

390

EXHIBIT 8-43 1. FLECK COMPANY

Income Statement For the Year Ended December 31, 20X2

(In Thousands of Dollars) Before Taxes After Taxes Straight–line DDB Straight–line DDB Depreciation Depreciation Depreciation Depreciation Income Statement

Cash sales $180 $180 $180.0 $180 Operating expenses 100 100 100.0 100 Depreciation expense* 9 20 9.0 20 Pretax income 71 60 71.0 60 Income taxes – – 28.4 24 Net income $ 71 $ 60 $ 42.6 $ 36

Statement of Cash Flows Cash $180 $180 $180.0 $180 Cash operating expenses 100 100 100 100 Cash tax payments – – 28.4 24 Net cash provided by operations $ 80 $ 80 $ 51.6 $ 56 * SL = 1/5 ($50,000 − $5,000) = $9,000; DDB = 2 x (1/5) x $50,000 = $20,000

Chapter 8 Long-Lived Assets and Depreciation 391

8-43 (continued) 2. By itself, depreciation expense does not provide cash. This

point is illustrated by the part of requirement 1 that compares the amounts shown before taxes. Note that the cash provided by operations is exactly the same under straight-line and DDB depreciation methods. No matter what depreciation expense is allocated to the year (whether $9,000, $20,000, $45,000, or zero), the $80,000 cash provided by operations will be unaffected.

Examine the part of requirement 1 that compares amounts

after taxes. Again, by itself, depreciation does not affect the cash inflow provided by operations. Only sales to customers can provide more cash receipts from operations. However, depreciation does affect the cash outflow for income taxes. The use of accelerated depreciation, such as DDB, results in a strange combination of showing less net income but conserving more cash. The DDB method shows net income of $36,000 (compared with $42,600 using straight-line), but DDB shows an increase in net cash provided by operations (less income taxes) of $56,000 (compared with $51,600 using straight-line). Accordingly, the final cash balance is $4,400 higher for DDB than for straight-line.

392

8-43 (continued) 3. The doubling of depreciation would cause net income to

decrease but would have no effect on the $80,000 of cash provided by operations (shown on the third line of the following table):

Straight-line DDB Depreciation Depreciation Before Doubled Before Doubled Sales $180 $180 $180 $180 Cash operating expenses 100 100 100 100 Cash provided by operations $ 80 $ 80 $ 80 $ 80 Depreciation expense 9 18 20 40 Income before income taxes $ 71 $ 62 $ 60 $ 40 Income tax expense – – – – Net income $ 71 $ 62 $ 60 $ 40 8-44 (5-10 min.) 1. Acceleration of depreciation for tax purposes is caused by a 3-

year instead of a 5-year depreciation schedule and the use of the DDB method instead of the straight-line method. DDB charges twice the straight-line rate in the first year.

2. Shareholder reporting: $1.8 million ÷ 5 = $360,000 Tax purposes: 2 x (1/3) x $1.8 million = $1,200,0000

Chapter 8 Long-Lived Assets and Depreciation 393

8-45 (5 min.) Leasehold Improvements would be increased, and Cash would be decreased by $120,000. The annual amortization would be based on the remaining life of the lease: $120,000 ÷ 4 years = $30,000 per year. Note that amortization is over the remaining lease term, not the physical life of the improvements. 8-46 (10 min.) 1. and 2. Neither expenses "charged to the P & L" nor "depreciation and amortization" generate cash. Only revenue generates cash. However, although Riccardo's statements are misleading, they have a certain logic. If operating income is zero, revenue is equal to cash expenses plus noncash expenses (primarily depreciation and amortization). Therefore, revenue generates enough cash to cover cash expenses (including the $3.75 billion charged to the P & L) and have an amount equal to depreciation and amortization left over (60% x $3.75 billion = $2.25 billion in this case). Positive operating income (less taxes on that income) will contribute to covering the remaining $1.5 billion that is needed. The key to interpreting Riccardo's statement is that he presumes that revenues are high enough to cover all expenses; these presumed revenues generate the cash to which he refers.

394

8-47 (10 min.) 1. a, c 2. b, d, g, h, i, j. The key questions to ask are whether the expenditure should be capitalized as an asset (a, c) or written off immediately as an expense (b, d, g, h, i, and j). The other outlays (e,f) are neither capitalized nor expensed. 8-48 (10 min.) a. E e. C b. C f. C c. E g. E d. E

Chapter 8 Long-Lived Assets and Depreciation 395

8-49 (10-15 min.)

The first two items would reduce cash and increase Repairs and Maintenance Expense by $200 and $450, respectively.

The third item would reduce cash and increase Equipment by $21,000. However, the increase in the residual value from $10,000 to $11,000, results in an increase in the new depreciable amount of only $20,000. Subsequent depreciation would be revised so that the new unexpired cost is spread over the remaining three years as follows:

Original Revised Depreciation Depreciation Schedule Schedule Year Amount Year Amount 1 $16,000 1 $ 16,000 2 16,000 2 16,000 3 16,000 3 16,000 4 16,000 4 16,000a 5 16,000 5 12,000 6 12,000 7 12,000 Accumulated depreciation $80,000b $100,000b

a New depreciable amount is ($90,000 – $64,000 + $21,000) – $11,000 residual value = $36,000.

New depreciation expense is $36,000 divided by remaining useful life of 3 years, or $12,000 per year.

b Recapitulation: Net Book Value Original Revised Original outlay $90,000 $ 90,000 Major overhaul – 21,000 Total $90,000 $111,000 Accumulated depreciation 80,000 100,000

396

Residual value $10,000 $ 11,000

Chapter 8 Long-Lived Assets and Depreciation 397

8-50 (10-15 min.) 1. Proceeds $12,000 Net book value of equipment sold is $29,000 − (4 x $5,000)

a 9,000

Gain on sale of equipment $ 3,000 A = L + SE Accumulated Depreciation, Retained Cash + Equipment + Equipment Earnings +12,000 -29,000 +20,000 = +3,000* *Gain on sale of equipment. a Annual depreciation is 1/5 x [$29,000 – $4,000] = $5,000. Accumulated

depreciation for four years is 4 x $5,000 = $20,000. The effect on assets of removing the net book value is a decrease of $9,000, consisting of a decrease in Equipment of $29,000 and a decrease in Accumulated Depreciation of $20,000. Note that the effect of a decrease in Accumulated Depreciation (by itself) is an increase in assets. This $9,000 decrease in assets is offset by the $12,000 in cash received, resulting in a net $3,000 increase in assets.

b The $3,000 is usually carried separately in the general ledger until

the end of the year as Gain on Sale of Equipment, or Gain on Disposal of Equipment.

Income statement effects: Gain on Sale of Equipment may be shown as a separate item on an income statement as a part of "other income" or some similar category.

398

8-50 (continued) In single-step income statements the gain is shown at the top along with other revenue items, for example: Revenue: Sales of products $XXX Interest income X Other income: gain on sale of equipment X Total sales and other income $XXX In multiple-step income statements, the gain is often shown after the operating income generated by the sales of major products. 2. a. Cash 12,000 Accumulated depreciation 20,000 Equipment 29,000 Gain on sale of equipment 3,000 b. Cash 7,000 Accumulated depreciation 20,000 Loss on sale of equipment 2,000 Equipment 29,000

Chapter 8 Long-Lived Assets and Depreciation 399

8-51 (10 min.) 1. Cash received $25,000 Book value, $45,000 – (3 x $8,000) 21,000 Gain on sale of fixed assets $ 4,000 Cash 25,000 Accumulated depreciation 24,000 Equipment (van) 45,000 Gain on sale of fixed assets 4,000 2. Cash received $17,000 Book value (see above) 21,000 Loss on sale of fixed assets $ 4,000 Cash 17,000 Accumulated depreciation 24,000 Loss on sale of fixed assets 4,000 Equipment (van) 45,000

400

8-52 (10 min.) 1. The only effect would be a $30,000 cash inflow listed with the investing activities: Proceeds from the sale of equipment $30,000

2. The proceeds should be listed as an investing activity: Proceeds from the sale of equipment $40,000 In addition, a $10,000 gain appeared on Icarus’s income

statement, calculated as: proceeds of $40,000 less book value of $30,000 ($120,000 cost less $90,000 of accumulated depreciation). In the statement reconciling net income and net cash provided by operating activities, the gain must be removed from net income by deducting the $10,000 from net income in the reconciliation of net income to net cash provided by operating activities:

Net income $XXXXXX Deduct: gain on sale of equipment 10,000

3. The proceeds should be listed as an investing activity: Proceeds from the sale of equipment $20,000 In addition, a $10,000 loss appeared in Icarus’s income

statement (proceeds of $20,000 less book value of $30,000). The loss must be added back to net income in the reconciliation of net income to net cash provided by operating activities:

Net income $XXXXXX Add: loss on sale of equipment 10,000

Chapter 8 Long-Lived Assets and Depreciation 401

8-53 (10-20 min.)

1. $3,000,000 ÷ 2 = $1,500,000 2. Company C must record the $6 million as an expense of 20X1,

whereas Company D must show the $6 million as an asset—Patents -- on its balance sheet of December 31, 20X1. Company D must then amortize the $6 million on a straight-line basis over the useful life of the patents. The useful life of an intangible asset is the shorter of its economic life and lit legal life, if any.

3. $420,000 ÷ 4 = $105,000 4. a) Goodwill 4,000,000 Assets 22,000,000 Liabilities 16,000,000 Cash 10,000,000 b) Yes. The journal entry is: Impairment loss 1,000,000 Goodwill 1,000,000 8-54 (10-15 min.)

1. $800,000 ÷ 5 = $160,000 2. Income statement: a) Total amount charged as an expense. b) Nothing charged as an expense. This assumes that the

purchase was late enough in December that no amortization is charged in 2002.

Balance sheet: a) Nothing recorded. b) $1,000 million recorded as an asset, to be amortized over

the useful life of patents.

402

8-54 (continued) 3. The key is that in a stable process, year-to-year expense

recognition would not change but the amount shown on the balance sheet would be larger. Assume all projects are finished at year end and appear in the balance sheet at full cost and then are amortized over the next three years. At any year-end the asset account would reflect that year’s spending, plus 2/3 of the prior year, plus 1/3 of the second year prior for a total of 1 + 2/3 + 1/3 = 2 times spending. The expense each year would be 3 x (1/3) = 1 times spending. If the amortization period changes to four years, the balance sheet asset account would rise to 1 + 3/4 + 2/4 + 1/4 = 2.5 times spending. The annual amortization in year five and subsequent years would be the same as the annual amount spent as long as annual spending was constant. The expense would be 4 x (1/4) = 1 times spending.

8-55 (10 min.)

Step 1: Recoverability test. The net book value of $11 million exceeds the undiscounted expected future cash flows of $9 million, so there is evidence of impairment. Step 2: The net book value of $11 million exceeds the fair value of $7.5 million so Vincent must record an impairment loss of $11 million - $7.5 million = $3.5 million.

Chapter 8 Long-Lived Assets and Depreciation 403

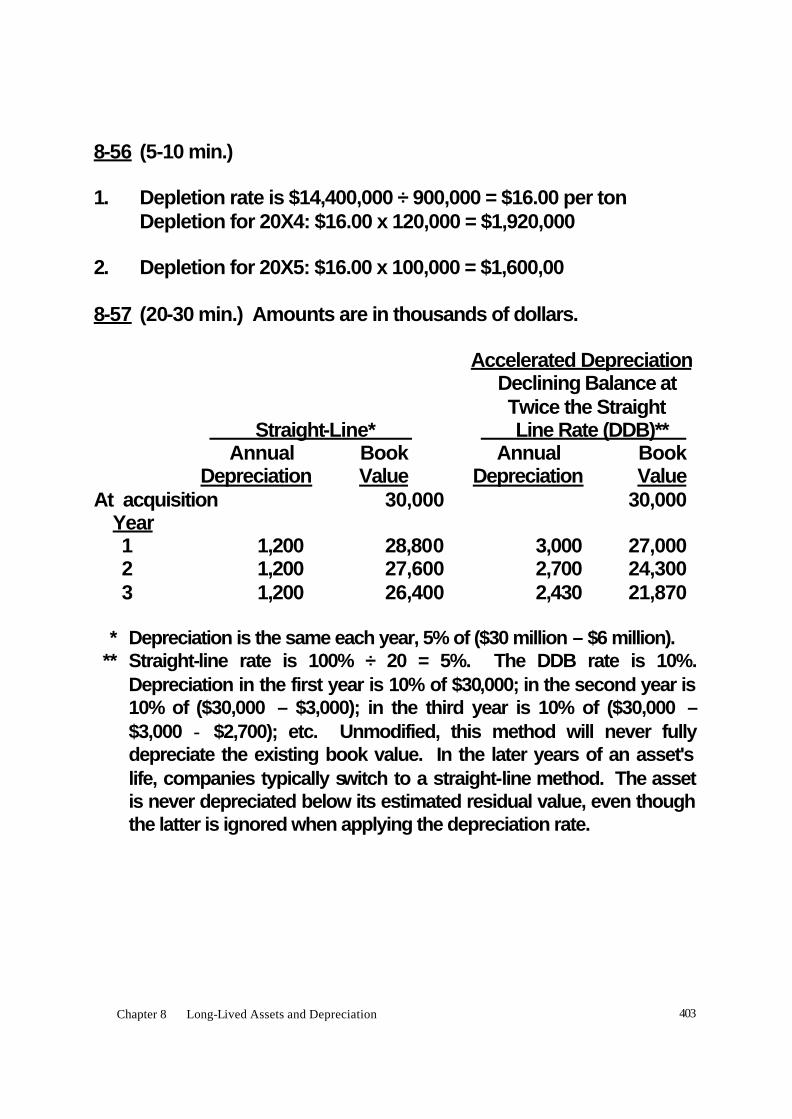

8-56 (5-10 min.)

1. Depletion rate is $14,400,000 ÷ 900,000 = $16.00 per ton Depletion for 20X4: $16.00 x 120,000 = $1,920,000

2. Depletion for 20X5: $16.00 x 100,000 = $1,600,00 8-57 (20-30 min.) Amounts are in thousands of dollars. Accelerated Depreciation Declining Balance at Twice the Straight Straight-Line* Line Rate (DDB)** Annual Book Annual Book Depreciation Value Depreciation Value At acquisition 30,000 30,000 Year 1 1,200 28,800 3,000 27,000 2 1,200 27,600 2,700 24,300 3 1,200 26,400 2,430 21,870 * Depreciation is the same each year, 5% of ($30 million – $6 million). ** Straight-line rate is 100% ÷ 20 = 5%. The DDB rate is 10%.

Depreciation in the first year is 10% of $30,000; in the second year is 10% of ($30,000 – $3,000); in the third year is 10% of ($30,000 – $3,000 − $2,700); etc. Unmodified, this method will never fully depreciate the existing book value. In the later years of an asset's life, companies typically switch to a straight-line method. The asset is never depreciated below its estimated residual value, even though the latter is ignored when applying the depreciation rate.

404

8-58 (10-15 min.) Amounts are in millions of dollars. 1. Let X = amount written off. Land, Buildings, and Equipment Balance 4,618 Write-offs X Additions 711 Balance 4,929 4,618 + 711 – X = 4,929 X = 400 2. Let Y = accumulated depreciation written off Accumulated Depreciation Write-offs Y Balance 1,854 Depreciation 365 Balance 1,949

1,854 + 365 – Y = 1,949 Y = 270 3. Book value of assets written off = $400 – 270 = $130. The

amounts in requirements 1 and 2 can be checked using the information that there was no gain or loss on disposal of assets:

Gain or loss = cash received – book value 0 = 130 – 130

Chapter 8 Long-Lived Assets and Depreciation 405

8-59 (15 min.) Amounts are in millions. 1. Buildings ¥158,424 + ¥216,865 = ¥375,289 Machinery and equipment ¥156,156 + ¥875,757 = ¥1,031,913 Land ¥63,150 Construction in progress ¥22,089 Other ¥15,374 + ¥86,795 = ¥102,169 2. Land is not depreciated, and depreciation has not started yet

on the construction in progress. 3. If Asahi had used straight-line depreciation, the net values of

the assets would be larger and the accumulated depreciation would be less. It is more difficult to determine the average age of a company’s assets if a company uses declining-balance depreciation rather than straight-line depreciation. For example, almost 85% (¥875,757 ÷ ¥1,031,913) of Asahi’s cost of machinery and equipment has been depreciated. If straight-line depreciation had been used, it would be clear that these assets had passed the midpoint of their economic life. But with declining-balance depreciation, it is possible that the assets are still in the first half of their economic life because more than half of the depreciation is taken before the midpoint of an asset’s life.

406

8-60 (30-40 min.) Gradually, students should become familiar with the effects of typical transactions. All numbers are in millions of dollars. Here are the T-accounts: Land, Plant, and Equipment Balance 52,981 Disposals at Acquisitions, original cost Z at cost ZZ Balance 60,113 Accumulated Depreciation Accum. depreciation Balance 26,568 on disposals YY Depreciation for current year Y Balance 30,112 Special Tools, net Balance 9,939 Amortization for Acquisitions 3,000 current year X Disposals, book value 0 Balance 11,992 1. Let X = special tool amortization 9,939 + 3,000 – X = 11,992 X = 947 2. The cost of new acquisitions was $8,113. Using the T-

accounts, this can be computed using the following three steps:

a. If depreciation plus amortization = $5,472, depreciation

was $5,472 − $947 = $4,525 = Y

Chapter 8 Long-Lived Assets and Depreciation 407

8-60 (continued)

b. There is now one unknown in the Accumulated Depreciation T-account, so:

Let YY = Accumulated depreciation of items disposed 26,568 + 4,525 – YY = 30,112 YY = 981

c. For fully depreciated assets accumulated depreciation is the same as total historical cost so Z = $981

Use the T account. Let ZZ = current acquisitions at cost 52,981 + ZZ – 981 = 60,113 ZZ = 8,113

408

8-61 (15-25 min.) This problem is not difficult, but it may appear so because the topic was not discussed in the text. It forces students to think about the meaning of accumulated depreciation and net book value. Amounts are in millions. 1. Total depreciable value ÷ average useful life = average annual

depreciation.

131,755 ÷ X = 8,500 X = 131,755 ÷ 8,500 = 15.5 years 2. Accumulated depreciation ÷ average age of assets = average

annual depreciation.

83,265 ÷ X = 8,500 X = 83,265 ÷ 8,500 = 9.8 years. or Average age of assets = (Accumulated depreciation ÷ total

depreciable value) x average useful life

= ($83,265 ÷ $131,755) x 15.5 = 9.8 years

Chapter 8 Long-Lived Assets and Depreciation 409

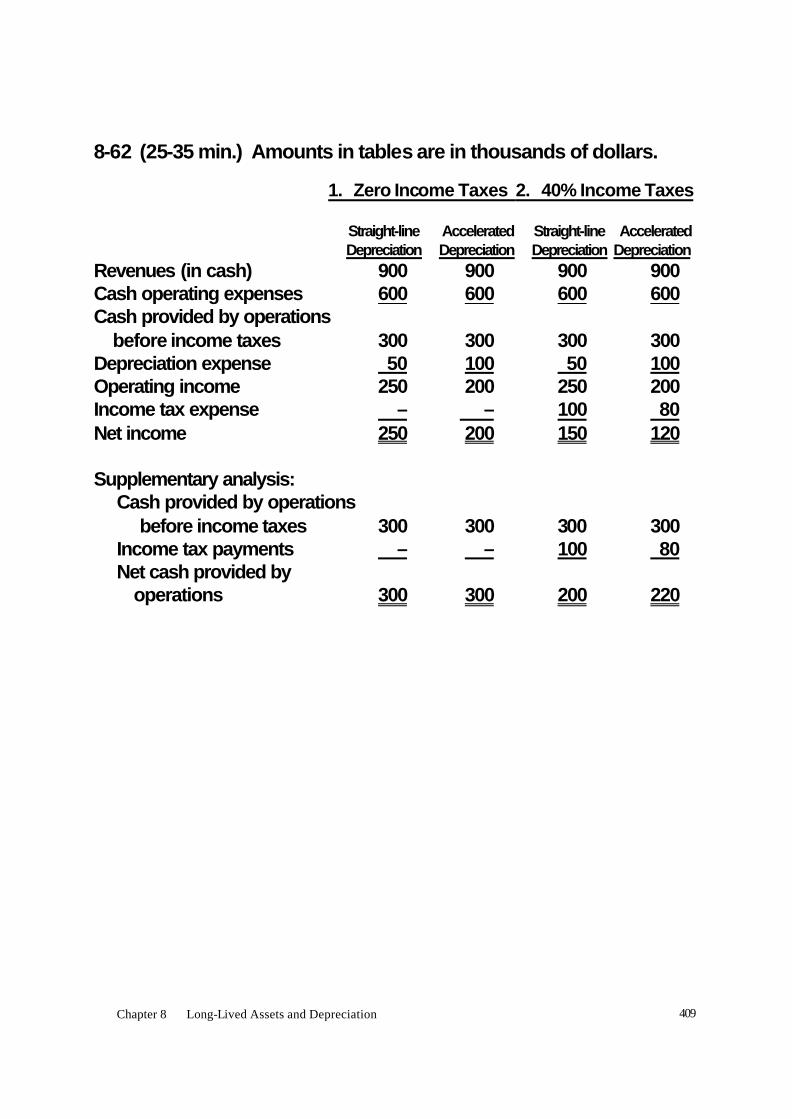

8-62 (25-35 min.) Amounts in tables are in thousands of dollars. 1. Zero Income Taxes 2. 40% Income Taxes Straight-line Accelerated Straight-line Accelerated Depreciation Depreciation Depreciation Depreciation Revenues (in cash) 900 900 900 900 Cash operating expenses 600 600 600 600 Cash provided by operations before income taxes 300 300 300 300 Depreciation expense 50 100 50 100 Operating income 250 200 250 200 Income tax expense – – 100 80 Net income 250 200 150 120 Supplementary analysis: Cash provided by operations before income taxes 300 300 300 300 Income tax payments – – 100 80 Net cash provided by operations 300 300 200 220

410

8-62 (continued) 3. By itself, depreciation expense does not provide cash. This

point is illustrated by part 1 that compares the amounts shown before taxes. Note that the cash provided by operations (and the ending cash balances) are exactly the same. No matter what depreciation expense is allocated to the year (whether $50,000, $100,000, or zero), the $300,000 cash provided by operations and the ending cash will be unaffected.

Examine part 2, that compares amounts after taxes. Again, by

itself, depreciation does not affect the cash inflow provided by operations. However, depreciation does affect the cash outflow for income taxes. The use of accelerated depreciation results in a strange combination of showing less net income but conserving more cash. The accelerated method shows net income of $120,000 (compared with $150,000 using straight-line), but accelerated shows a net increase in cash provided by operations (less income taxes) of $220,000 (compared with $200,000 using straight-line). Accordingly, the final cash balance is $20,000 higher for accelerated than for straight-line.

4. Journal entries (not required) may clarify the effects: Depreciation expense 50,000 more Accumulated depreciation 50,000 more Income tax expense 20,000 less Cash 20,000 less

Note: A smaller credit to cash increases the balance in cash.

Chapter 8 Long-Lived Assets and Depreciation 411

8-62 (continued) The reduction of retained earnings would be $50,000 – $20,000. That is, net income (and hence retained earnings) would be $30,000 lower. In summary:

Cash, increase by tax savings, .40 x $50,000 = $20,000 Accumulated depreciation, increase by $50,000 Operating income, decrease by $50,000 Income tax expense, decrease by $20,000 Retained earnings, decrease by $30,000 5. The doubling of depreciation would cause net income to

decrease but in the absence of tax effects would have no effect on cash provided by operations:

Straight-line Accelerated Depreciation Depreciation Before Doubled Before Doubled Revenues (all cash) 900 900 900 900 Cash operating expenses 600 600 600 600 Cash provided by operations 300 300 300 300 Depreciation expense 50 100 100 200 Income before income taxes 250 200 200 100 Income tax expense − − − − Net income 250 200 200 100

412

8-63 (25-35 min.) Amounts are in millions of dollars. 1. Zero Income Taxes 2. 40% Income Taxes Straight-line Accelerated Straight-line Accelerated Depreciation Depreciation Depreciation Depreciation Revenues $246,525 $246,525 $246,525$246,525 Cash operating expenses 229,449 229,449 229,449 229,449 Cash provided by operations before income taxes 17,076 17,076 17,076 17,076 Depreciation expense 3,432 5,432 3,432 5,432 Operating income 13,644 11,644 13,644 11,644 Income tax expense − − 5,458 4,658 Net income $ 13,644 $ 11,644 $ 8,186 $ 6,986 Supplementary analysis: Cash provided by operations before income taxes $17,076 $17,076 $17,076 $17,076 Income tax expense − − 5,458 4,658 Net cash provided by operations $17,076 $17,076 $11,618 $12,418 3. By itself, depreciation expense does not provide cash. This

point is illustrated by part 1, which compares the amounts shown with zero income taxes. Note that the cash provided by operations (and the ending cash balances) are exactly the same. No matter what depreciation expense is allocated to the year (whether $3,432 million, $5,432 million, or zero), the $17,076 million cash provided by operations and the ending cash will be unaffected.

Chapter 8 Long-Lived Assets and Depreciation 413

8-63 (continued)

Examine part 2, that compares amounts after taxes. Again, by itself, depreciation does not affect the cash inflow provided by operations. Only sales to customers can provide more cash receipts from operations. However, depreciation does affect the cash outflow for income taxes. The use of accelerated depreciation results in a strange combination of showing less net income but conserving more cash. The accelerated method shows net income of $6,986 million (compared with $8,186 million using straight-line), but accelerated shows a net increase in cash provided by operations after considering income taxes of $12,418 million (compared with $11,618 million using straight-line). Accordingly, the final cash balance would be $800 million higher for accelerated than for straight-line.

4. Cash, increase by tax savings, .40 x $2,000 million = $800 million

Accumulated depreciation, increase by $2,000 million Operating income, decrease by $2,000 million Income tax expense, decrease by $800 million Retained earnings, decrease by $1,200 million New balances: cash, $2,758 million + $800 million = $3,558

million Accumulated depreciation, $15,147 million + $2,000 million =

$17,147 million

Journal entries (not required) may clarify the effects (in millions):

Depreciation expense 2,000 more Accumulated depreciation 2,000 more Income tax expense 800 less Cash 800 less Note: A smaller credit to cash increases the balance in cash.

414

The effect on retained earnings would be $2,000 million – $800 million = $1,200 million. That is, net income (and hence retained earnings) would be $1,200 million lower.

Chapter 8 Long-Lived Assets and Depreciation 415

8-63 (continued) 5. The $2,500 million increase of depreciation would cause net

income to decrease but would have no effect on cash provided by operations.

Straight-line Accelerated Depreciation Depreciation Before After Before After Sales $246,525 $246,525 $246,525$246,525 Cash operating expenses 229,449 229,449 229,449 229,449 Cash provided by operations 17,076 17,076 17,076 17,076 Depreciation expense 3,432 5,932 5,432 7,932 Income before income taxes 13,644 11,144 11,644 9,144 Income tax expense − − − − Net income 13,644 11,144 11,644 9,144

416

8-64 (25-35 min.) Amounts in table and narrative are in millions of Euros.

1. Zero Income Taxes 2. 60% Income Taxes Straight-line Accelerated Straight-line Accelerated Depreciation Depreciation Depreciation Depreciation Revenues (all cash) 50,288 50,288 50,28850,288 Cash operating expenses (47,884 – 1,974) 45,910 45,910 45,91045,910 Cash provided by operations before income taxes 4,378 4,378 4,378 4,378 Depreciation expense 1,974 2,474 1,974 2,474 Operating income 2,404 1,904 2,404 1,904 Income tax expense − − 1,442 1,142 Net income 2,404 1,904 962 762 Supplementary analysis: Cash provided by operations before income taxes 4,378 4,378 4,378 4,378 Income tax expense − − 1,442 1,142 Net cash provided by operations 4,378 4,378 2,936 3,236 3. By itself, depreciation expense does not provide cash. This

point is illustrated by part 1, which compares the amounts shown before taxes. Note that the cash provided by operations and the ending cash balances are exactly the same. No matter what depreciation expense is allocated to the year (whether €1,974, €2,474, or zero), the €4,378 cash provided by operations and the ending cash will be unaffected.

Chapter 8 Long-Lived Assets and Depreciation 417

8-64 (continued) Examine part 2, which compares amounts after taxes. Again,

by itself, depreciation does not affect the cash inflow provided by operations. Only sales to customers can provide more cash receipts from operations. However, depreciation does affect the cash outflow for income taxes. The use of accelerated depreciation results in a strange combination of showing less net income but conserving more cash. The accelerated method shows net income of €762 (compared with €962 using straight-line), but accelerated depreciation shows a net increase in cash provided by operations (less income taxes) of €3,236 (compared with €2,936 using straight-line). Accordingly, the final cash balance is €300 higher for accelerated than for straight-line depreciation.

4. Journal entries (not required) may clarify the effects: Depreciation expense 500 more Accumulated depreciation 500 more Income tax expense 300 less Cash 300 less

Note: A smaller credit to cash increases the balance in cash.

The effects on retained earnings would be €500 – €300. That is, net income (and hence retained earnings) would be €200 lower. In summary:

418

8-64 (continued) Cash, increase by reduction in taxes, .60 x €500 = €300 Accumulated depreciation, increase by €500 Operating income, decrease by €500 Income tax expense, decrease by €300 Retained earnings, decrease by €200 New balances: Cash, €7,666 + €300 = €7,966 Accumulated Depreciation €17,230 + €500 = €17,730 5. The doubling of depreciation would cause net income to

decrease but would have no effect on cash provided by operations:

Straight-line Accelerated Depreciation Depreciation Before Doubled Before Doubled Sales 50,288 50,288 50,288 50,288 Cash operating expenses 45,910 45,910 45,910 45,910 Cash provided by operations 4,378 4,378 4,378 4,378 Depreciation expense 1,974 3,948 2,474 4,948 Income before income taxes 2,404 430 1,904 (570) Income tax expense − − − − Net income (loss) 2,404 430 1,904 (570)

Chapter 8 Long-Lived Assets and Depreciation 419

8-65 (30 min.) All amounts are stated in thousands of Deutchmarks. 1. and 2. Part (1) Part (2) 20X8 Change 20X9 20X8 Change 20X9 Revenue DM2,100 DM1,000 DM3,100 DM2,100 DM1,000 DM3,100 Operating expense other than depreciation 1,700 800 2,500 1,700 800 2,500 Cash (C) provided by operations DM 400 DM 200 DM 600 DM 400 DM 200 DM 600 Depreciation 200 100 300 200 50 250 Income before income taxes DM 200 DM 100 DM 300 DM 200 DM 150 DM 350 3. Part (3a) Part (3b) 20X8 Change 20X9 20X8 Change 20X9 Income before income taxes DM 200 DM 100 DM 300 DM 200 DM 150 DM 350 Income taxes at 30% 60 30 90 60 45 105 Net income after income taxes DM 140 DM 70 DM 210 DM 140 DM 105 DM 245 Cash provided by operations after income taxes [(C) above minus income taxes] DM 340 DM 170 DM 510 DM 340 DM 155 DM 495 4. By itself, depreciation does not provide "cash inflow" (cash

provided by operations). Note in parts (1) and (2) that the cash provided by operations went up from DM400 to DM600, a DM200 increase, because revenues (the basic source of cash) increased by DM1,000 and operating expenses increased by DM800. Whether depreciation is DM50, DM100, DM1,000, or zero will not affect cash provided by operations (if income taxes are ignored).

420

8-65 (continued) Depreciation does affect the amount of income tax cash

outflow. If only DM50 rather than DM100 is deducted as depreciation, the income tax bill will be DM15 higher, 30% of (DM100 - DM50). That is why cash provided by operations is less by DM15 in part (3b). The important point is that income tax cash outflows are affected by depreciation. Otherwise, depreciation has no direct effect on cash inflows or outflows.

8-66 (15-25 min.) This problem is more challenging than most because it raises conceptual issues regarding how to account for depreciation. Dollar amounts are in millions. 1. Depreciation expense 4.5 Accumulated depreciation 4.5 To record 3 months of depreciation: Acquisition cost $70.0 Predicted residual value 52.0 Depreciable amount $18.0 Amount per month, $18 ÷ 12 $ 1.5 For 3 months: $1.5 per month x 3 months $ 4.5 2. Depreciation expense 13.5 Accumulated depreciation 13.5 To record 9 months of depreciation (9 months x $1.5 per month)

Chapter 8 Long-Lived Assets and Depreciation 421

8-66 (continued)

3. Cash 58 Accumulated depreciation 18 Revenue-earning equipment 70 Depreciation expense 6 To record the sale of equipment

Note the entry to depreciation expense instead of gain on sale of automobiles. This method recognizes that, if the autos were sold for $58, the residual value was underestimated, and therefore too much depreciation was charged. The entry adjusts the depreciation expense for this estimation error.

4. This part illustrates how the predictions of useful lives and residual values can affect depreciation expenses. It also underscores the general "prospective" approach to depreciation expense. That is, 2003 depreciation charges would not be "corrected" retroactively. However, up-to-date knowledge can affect depreciation being taken currently (2004).

2003 2004 As Perfect As Perfect Reported Prediction Reported Prediction Depreciation in millions 4.5 3 7.5* 9

*$13.5 – $6 Depreciation expense for the 12 months of ownership spread over the two calendar years is $12. Under the same circumstances, some companies would show depreciation expense of 9 x $1.5 = $13.5 for 2004 for a total of $18 and show a $6 gain on sale of equipment. This underscores the fact that the final gains or losses on sales of fixed assets are affected by the depreciation policies followed while the assets are in service.

422

8-67 (10-15 min.) Conceptually, a strong case can be made for deferring the $2 million and amortizing it over the useful life of the product or process developed. However, the FASB requires that research and development costs be written off to expense as they are incurred. The history of accounting for research and development may be of interest as an illustration of a long debate about the meaning and measurement of an asset. Until the FASB requirement for expensing this cost as incurred became effective in 1975, many companies deferred research costs and amortized them. There was no uniformity, to say the least. For example, in 1973, the American Institute of CPAs issued an audit guide that pertained to companies "in the development stage." The accounting for the Mori Pharmaceuticals Company would have been covered by this audit guide, which required the capitalization of these costs as "investments for the future" unless such costs were clearly unrecoverable. In a sense, then, one set of principles was applicable to companies in the development stage that may not have been equally applicable to mature companies having similar outlays. Incidentally, the audit guide took the following position regarding established companies:

"The guide does not apply to established companies developing new products, services, or markets, or to the development activities of their subsidiaries, even though the subsidiaries are in the development stage, when included in consolidated financial statements. It does, however, apply to separate financial statements of a subsidiary in the development stage and is applicable to consolidated financial information when the group as a whole is considered to be in the development stage."

Chapter 8 Long-Lived Assets and Depreciation 423

8-68 (15-20 min.) The purpose of this problem is to stress the limitations of the use of historical costs, particularly where there are significant amounts of property, plant, and equipment.

The balance sheet values do not come close to the current market value of the land and building, $1,800,000 ÷ .60, or $3,000,000. Consequently, in terms of current values before expansion and modernization, stockholders' equity is understated (in thousands):

Market value of land and building $3,000 Net book value: Land $500 Building 200 700 Excess of market value over net book value $2,300 As conventionally prepared after the expansion and modernization, the balance sheet would be (in thousands): Cash $ 300 Liabilities: Land 500 Mortgage Building at cost $2,600 payable $1,800 Accumulated Stockholders' depreciation 600 equity 1,000 Net book value 2,000 Total liabilities and Total assets $2,800 stockholders’ equity $2,800

The balance sheet would be unusually deceiving. The mortgage would appear to be exceedingly high in relation to the book value of the assets. The historical costs and resulting stockholders' equity have lost all meaning.

Note that, on a market value basis, the land and building are worth $3,000,000 before the borrowing and the renovation and therefore worth $4,800,000 after. This is $2,300,000 above the book

424

value of the land and building of $2,500,000. Measured at market values, the stockholders' equity would be $3,300,000.

Chapter 8 Long-Lived Assets and Depreciation 425

8-69 (10-15 min.) The answers are drawn from The Accountant's Weekly Report, published by Prentice Hall, Inc. Sometimes drawing a line is difficult. Legal fees paid in connection with a taxpayer's business are deductible as business expenses. But no current deduction is allowed for capital expenditures, and such expenses as the cost of defending or perfecting title to business property are considered capital expenditures. 1. (a) Yes, it’s deductible. Here the litigation was to allow Rock to

continue in business. Since the claim arose out of his profit-seeking activities, the legal expense is deductible.

2. (b) They’re capital expenditures. Here the suit originated in

Rock's wish to expand the business by adding to the property. Since the crusher was a permanent improvement, all the expenses of acquiring it, including legal fees, must be capitalized -- and recovered through depreciation.

426

8-70 (20-30 min.) This problem illustrates how some companies follow "more conservative" accounting policies than others -- even though the equipment is identical and the industry is the same. 1. The change may not be judged as material in relation to the

total depreciation expense. However, in relation to net income, it is material. Additional depreciation of $9,000,000 would have decreased net income by .54 x $9,000,000 = $4,860,000. This is 11.5 percent of reported net income.

2. All other things being equal, depreciation would be halved: .5 x

$220,979,000 = $110,489,500. Accordingly, net income would be higher by .54 x $110,489,500 = $59,664,330. The latter is 40.7 percent of reported net income.

3. Useful Lives in Years 10 20 Depreciation

† 72,000,000 36,000,000

Net income 22,793,000* 42,233,000 † ($800 million – residual value of $80 million) ÷ useful life * $42,233,000 – [.54 x ($72,000,000 – $36,000,000)] or $42,233,000 –

$19,440,000

Chapter 8 Long-Lived Assets and Depreciation 427

8-71 (15-20 min.) Data are in millions. 1. Proceeds $22 Net book value of equipment sold is $26 − (6 x $1) 20 Gain on sale of equipment $ 2 A = L + SE Accumulated Depreciation, Retained Cash + Equipment + Equipment Earnings +22,000 -26,000 +6,000a =

+2,000b

a Accumulated depreciation for six years is 6 x $1 = $6. The effect of removing the net book value is $20, consisting of a decrease in Equipment of $26 and a decrease in Accumulated Depreciation of $6. Thus, $22 – $20 = $2. Note that the effect of a decrease in Accumulated Depreciation (by itself) is an increase in assets.

b The $2 is usually carried separately until the end of the year as Gain on Sale of Equipment, or Gain on Disposal of Equipment.

Income statement effects:

Alaska would include the Gain on Sale of Equipment as a part of "other income (expense)."

2. a. Cash 22 Accumulated depreciation 6 Equipment 26 Gain on sale of equipment 2 b. Cash 19 Accumulated depreciation 6 Loss on sale of equipment 1

428

Equipment 26

Chapter 8 Long-Lived Assets and Depreciation 429

8-72 (15-20 min.) Amounts are in millions of dollars. 1. Proceeds $ 4.0 Net book value of equipment sold $4 − ($8.5) = 12.5 Loss on sale of equipment (given) $ 8.5 Book value = Original cost – Accumulated depreciation $12.5 = $65 – Accumulated depreciation Accumulated depreciation = $65 – $12.5 = $52.5 A = L + SE

−=++

Equip

men

t

of Sale

on

Loss

Decr

ease

b

8.5

onDepr

eciat

i

dAccu

mula

teDe

crea

se

a

52.5

Equip

men

tDe

crea

se

65-

Cash

Incr

ease

4

a Accumulated depreciation is $52.5. The effect on assets of

removing the net book value is a decrease of $12.5, consisting of a decrease in Equipment of $65 and a decrease in Accumulated Depreciation of $52.5. Note that the net effect of a decrease in Accumulated Depreciation (by itself) is an increase in assets.

b The $8.5 is usually carried separately until the end of the year as Loss on Sale of Equipment, or Loss on Disposal of Equipment.

Income statement effects:

Loss on Sale of Equipment may be shown as a separate item on an income statement as a part of "other expense" or some similar category. In single-step income statements the loss is shown along with other expense items, for example:

430

8-72 (continued)

Revenue: Sales of products $XXX Interest income X Total sales and other income $XXX Cost of goods sold X Selling, general and administrative expense X Other expense: loss on sale of equipment X Income before taxes $XXX

In multiple-step income statements, the loss is often shown after the operating income generated by the sales of major products.

2. a. Loss on sale of equipment 8.5 Cash 4.0 Accumulated depreciation 52.5 Equipment 65 Cash Equipment 4 65

Accumulated Depreciation, Equip. Loss on Sale of Equipment 52.5 8.5

b. Assume that the equipment and accumulated depreciations amounts from part a do not change:

Cash 14.0 Accumulated depreciation 52.5 Equipment 65.0 Gain on sale of equipment 1.5

Cash Equipment 14 65

Accumulated Depreciation, Equip. Gain on Sale of Equipment

Chapter 8 Long-Lived Assets and Depreciation 431

52.5 1.5

432

8-73 (10-20 min.) A lively discussion usually ensues. This problem could also be assigned near the end of the course as an example of the strengths and weaknesses of accounting theory. 1. There would be a "gain from insurance on crashed airplane"

recognized on the income statement: Insurance payment received $6,500,000 Book value of airplane 962,000 Gain from insurance on crashed airplane $5,538,000 Total assets would increase by $5,538,000, the amount of the

gain. The fleet of airplanes would be the same as before the crash, but a 727 with a book value of $6.5 million has replaced a similar 727 with a book value of only $962,000.

2. Accounting for casualties is very controversial. It gets to the

heart of the question of what is income and what is capital. Does the $6.5 million insurance payment represent a return of capital or a payment of both capital and income?

The historical-cost model (using nominal dollars) ignores

changes in general purchasing power and intervening changes in specific prices while an asset is held. When an asset is disposed of, the gain or loss is measured in nominal dollars (almost always without regard to the intended use of the proceeds).

Chapter 8 Long-Lived Assets and Depreciation 433

8-73 (continued) Many theorists and practitioners define the income of a going

concern to be a function of whether the proceeds will be reinvested in the same types of assets. These individuals maintain that no gain is realized on the airplane crash, because the $6.5 million is really a return of capital (where capital is thought of in physical terms as airplanes, inventories, etc.). Thus, the "gain" would not be shown in the income statement. Instead, it would appear as a special balance sheet item called Revaluation Equity, or a similar title.

8-74 (10-15 min.) Amounts are in millions. This case highlights how current values of equipment may have little relation to book values. 1. Sales price, 7 x $25 $175 Book value: Acquisition cost, 7 x $25 = 175 Accumulated depreciation:

7 x 8 yrs. x 10yrs.

$2.5$25 − = 126 49

Gain on sale $126 2. Cash (or Receivables) 175 Accumulated depreciation 126 Aircraft 175 Gain on sale of aircraft 126

434

8-75 (15 min.) 1. 20X1: Research and development expense 800,000 Cash 800,000 20X2: Research and development expense 400,000 Cash 400,000 Capitalized software development costs 1,000,000 Cash 1,000,000 2. The capitalized software development costs must be amortized .

Note: The amortization of capitalized software costs was not

discussed in the text. However, the instructor may be interested in discussing the amortization process. If total estimated sales are $4,000,000 and 20X3 actual sales revenue is $800,000, amortization would be computed as follows.

20X3 Revenue ÷ Total Revenue = $800,000 ÷ $4,000,000 = .20 20X3 Amortization = .20 x $1,000,000 = $200,000 Amortization of capitalized software development costs 200,000 Capitalized software development costs 200,000

Chapter 8 Long-Lived Assets and Depreciation 435

8-76 (10-15 min.)

This problem illustrates how choices among accounting alternatives can be important to both managers and accountants. Note that the covenant will be amortized over three years.

1. The tangible assets are deductible over a period of ten years

compared to a three-year amortization of the covenant, so the buyer should favor Allocation One. In this way, the buyer will get larger deductions during the first three years, [($72,000 ÷ 3) + ($28,000 ÷ 10) = $26,800 per year, instead of ($48,000 ÷3) + $52,000 ÷10) = $21,200], but smaller deductions in the next seven years ($2,800 per year instead of $5,200).

2. Managers and accountants differ as to proper reporting to

shareholders. Because the tangible assets are depreciated over ten years and the covenant is amortized over three years for shareholder reporting, many would favor Allocation Two because reported income before taxes would be $5,600 higher during each of the first three years (in dollars).

Each of Next First three Seven Years Years Allocation ONE TWO ONE TWO Amortization expense: Covenant 24,000 16,000 -- -- Tangible assets 2,800 5,200 2,800 5,200 Total 26,800 21,200 2,8005,200 Effects on reported income of Allocation Two 5,600 higher 2,400 lower

436

8-77 (10 min.)

Choosing a lengthy economic life for depreciation purposes is not inherently unethical, provided it is within the guidelines of generally accepted accounting principles (GAAP). However, GAAP allows great flexibility in its depreciation rules, and when a company uses methods that do not fairly reflect the underlying economics of a situation, a possible ethical violation occurs.

Some accountants would maintain that any financial reporting policies that are consistent with GAAP are ethical. These same persons might maintain that any business practices that do not violate the law are ethical. The authors do not advocate such a position. Ethical standards go beyond the law. Therefore, even reporting policies that meet GAAP are unethical if they deliberately try to mislead users of the financial statements.

GAAP is intentionally flexible so that different economic situations can be reflected differently. For example, one theater may legitimately plan to remodel its theaters every five years while another plans remodeling only every ten years. The economic life of the seats, carpets, etc. should reflect this management philosophy. Nevertheless, there are some economic assumptions that are so far from reality as to be absurd. Often these can be identified when one company's policies are far from the norm of the industry. Both Cineplex Odeon and Blockbuster may fit this category.

Another sign that depreciable lives are chosen to manipulate income rather than to reflect economic reality is when changes to longer lives are made just when additional income is needed. It is unethical to manipulate income by changing accounting policies when the new policies are clearly in conflict with the economics of the situation.

In summary, using different accounting policies than other similar companies is not unethical if the underlying economics support the differences. However, when differences are intended to mislead users of the financial statements, there is a clear ethical violation.

Chapter 8 Long-Lived Assets and Depreciation 437

8-78 (60 min. or more) The purpose of this exercise is to help students see what can be learned from the fixed asset section of a company’s balance sheet. They can estimate the average age of the company’s assets, and they can see how this is affected by the depreciation method used. Comparisons are especially insightful if some companies use accelerated depreciation; students can see how difficult it is to compare the fixed assets of a straight-line company to those of an accelerated-depreciation company. The ranking of companies by the ratio of their accumulated depreciation to the original cost of assets can lead to insights into how the average age of assets can depend on the industry, the growth rate of the company, management strategies, and other factors. 8-79 (30-60 min.) Each solution will be unique and will change each year. The purpose of this problem is to examine how using different depreciation methods affects the financial statements.

438

8-80 (20-30 min.) (Amounts in millions of dollars) 1. Note 1 reveals that equipment is depreciated over two to seven

years; buildings over 30 to 40 years; and leasehold improvements over the shorter of their estimated useful lives or the related lease life, generally 10 years.

2. If lives are increased by 50%, depreciation is reduced by one

third. For example a $400 asset amortized over 4 years is $400÷4 =$100 per year, over 6 years it is $400 ÷6 = $66.67. If depreciation and amortization were reduced by one third, it would have been $158,538, $79,269 less than the reported $237,807. But this would increase pretax earnings and taxes. The apparent tax rate is $167,989/$436,335 = 38.5%. Thus net earnings would go up by $79,269 (1-.385) = $48,750, rising from $268,346 to $317,096, an increase of 18.2%

8-81 (30-60 min.)

NOTE TO INSTRUCTOR. This solution is based on the web site as it was in late 2004. Be sure to examine the current web site before assigning this problem, as the information there may have changed.

1. Gap is a global specialty retailer of casual apparel, accessories and personal care products for men, women and children. They sell their products under several brand names including Gap, Banana Republic and Old Navy. Gap sells their products through both traditional retail stores and online stores. You would expect Gap to have buildings, furniture, display equipment and leasehold improvements.

Chapter 8 Long-Lived Assets and Depreciation 439

2. Information on the method of depreciation and amortization used is found in Note A to the financial statements: Summary of Significant Accounting Policies. The company uses straight-line depreciation and amortization. Other information available in this note are: 1) estimated useful lives of property and equipment, 2) interest capitalized on property and equipment under construction, 3) the fact that property and equipment are stated at cost, and 4) items listed under property and equipment.

3. Technically leasehold improvements are intangible assets, but they are listed in Note A as property and equipment. Leasehold improvements are amortized over the life of the lease, not to exceed 12 years. Gap also has lease rights estimated at $170 million as of January 31, 2004. These rights represent costs to acquire the lease of specific commercial property. They are amortized over the estimated useful lives of the leases, not to exceed 20 years. These rights are probably included in “other assets” on the balance sheet. At January 31, 2004, the balance sheet lists other assets of $286 million, so Gap may have other intangible assets.

4. The amount listed on the balance sheet for property and equipment represents cost. If Gap purchases no additional property and equipment, the net book value will decrease over time.

5. Depreciation and amortization expense for the year ended January 31, 2004 was $664 million. This number is found on the statement of cash flows where it is added back to net income in order to arrive at net cash provided by operating activities. Depreciation and amortization expense is not obvious from looking at the income statement because it is combined with other costs. It likely appears in the line items called Cost of Goods Sold and Occupancy Expenses and/or Operating Expenses.

![Bio 111 Final Exam Fall05[1]](https://static.fdocuments.in/doc/165x107/54f641d04a79596c4a8b4dcd/bio-111-final-exam-fall051.jpg)