Chapter 8: Completing the Accounting Cycle · PDF fileChapter 8: Completing the Accounting...

29

1 Chapter 8: Completing the Accounting Cycle 8.1 The Adjustment Process Pages 268 278 Extremely important for financial statements to be accurate, current, and consistent from year to year. Therefore, accountants must ensure the following: • accounts are brought up to date • late transactions are taken into account • calculations have been made correctly • accounting principles and standards have been followed (IFRS emphasize the importance of financial statements that are current and based on solid evidence so that readers can make meaningful comparisons)

Transcript of Chapter 8: Completing the Accounting Cycle · PDF fileChapter 8: Completing the Accounting...

1

Chapter 8: Completing the Accounting

Cycle

8.1 The Adjustment Process Pages 268 278

Extremely important for financial statements to be accurate, current, and consistent from year to year.

Therefore, accountants must ensure the following:• accounts are brought up to date• late transactions are taken into account• calculations have been made correctly• accounting principles and standards have been followed (IFRS emphasize the importance of financial statements that are current and based on solid evidence so that readers can make meaningful comparisons)

2

Accrual accounting recording revenues and expenses when they happen.

Revenues and expenses can occur without the clerk's knowledge. For example, earning interest on a bank account or office supplies being used.

At the end of the fiscal period, all of this must be taken into consideration so that financial statements can be prepared accurately (time period concept).

If the time period concept has been followed, statements from year to year can be compared.

adjusting entry a journal entry that assigned an amount of revenue or expense to the appropriate accounting period.

3

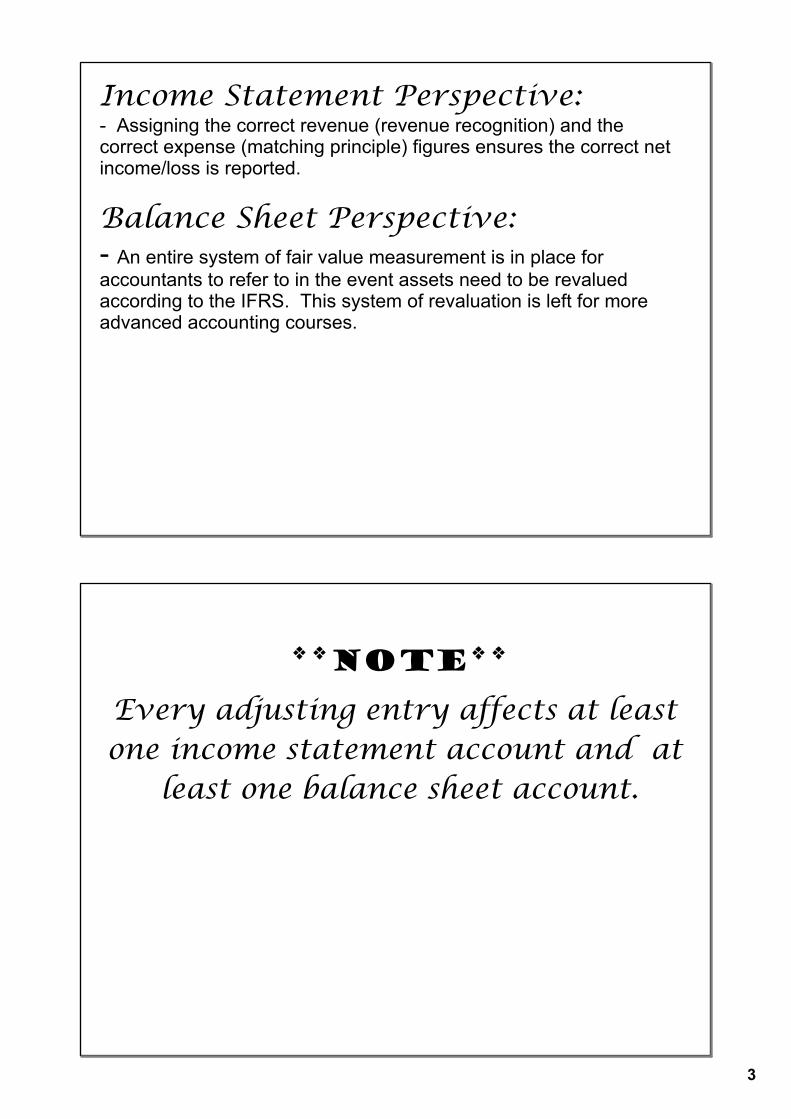

Income Statement Perspective: Assigning the correct revenue (revenue recognition) and the correct expense (matching principle) figures ensures the correct net income/loss is reported.

Balance Sheet Perspective: An entire system of fair value measurement is in place for accountants to refer to in the event assets need to be revalued according to the IFRS. This system of revaluation is left for more advanced accounting courses.

**NOTE**

Every adjusting entry affects at least one income statement account and at

least one balance sheet account.

4

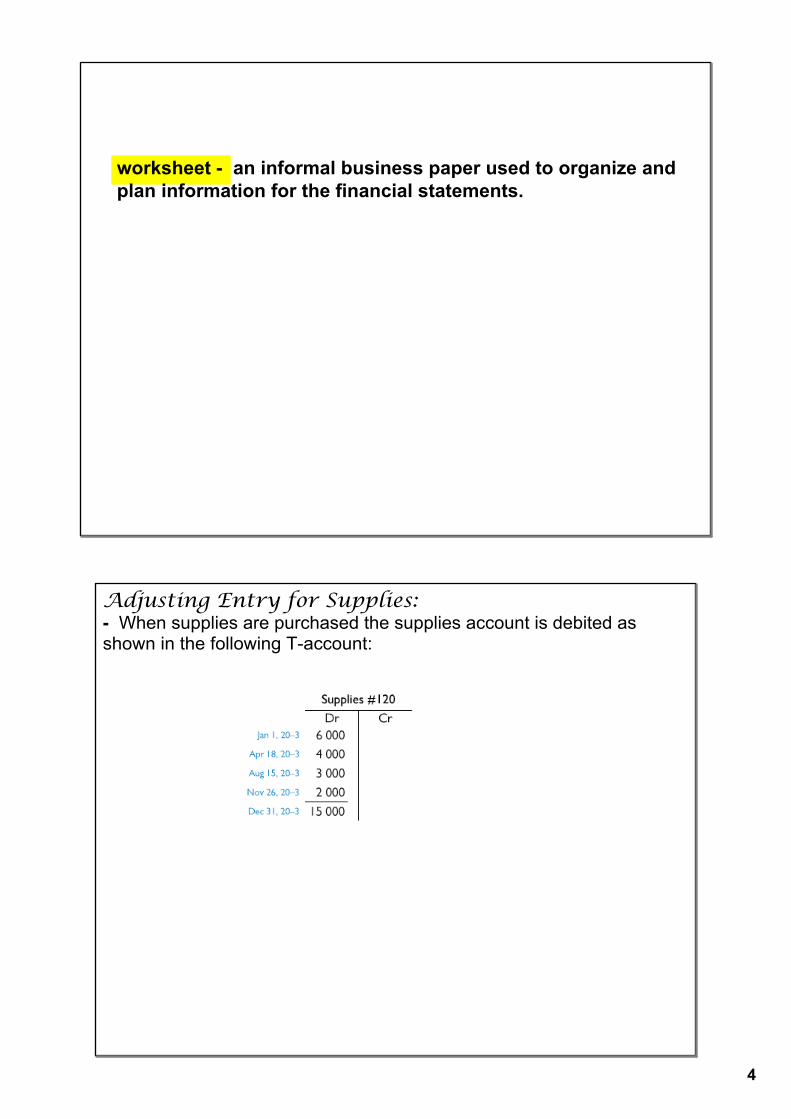

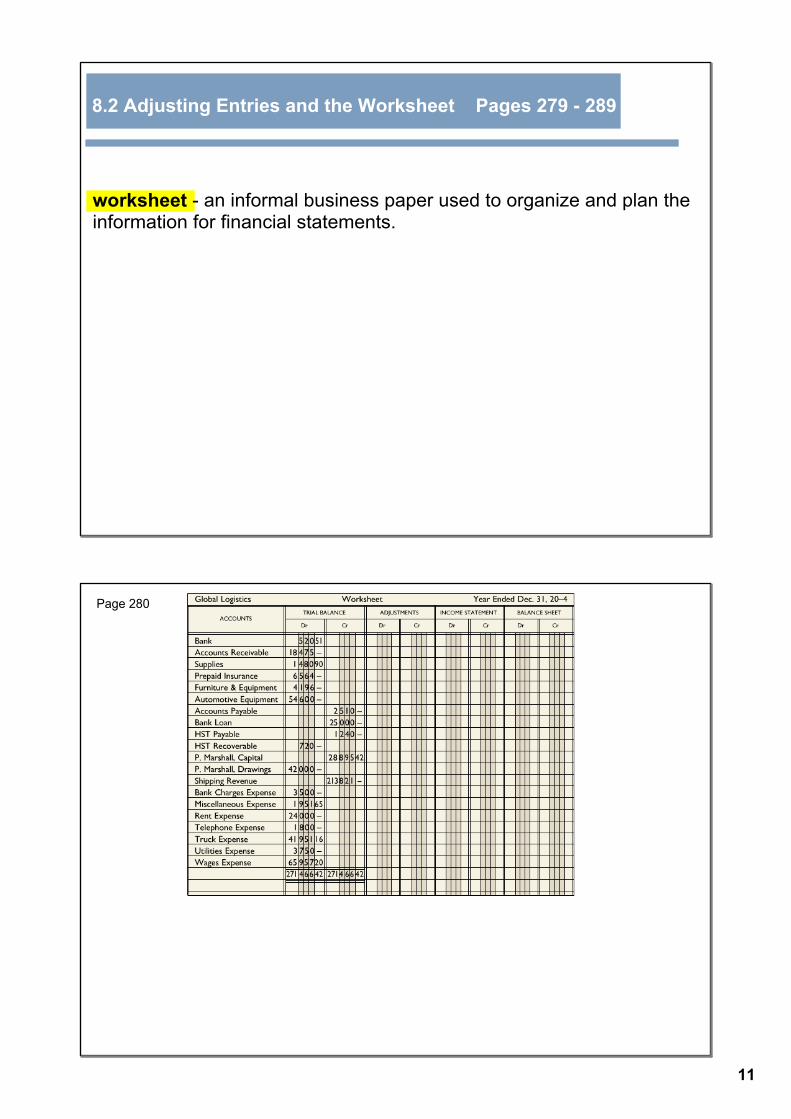

worksheet an informal business paper used to organize and plan information for the financial statements.

Adjusting Entry for Supplies: When supplies are purchased the supplies account is debited as shown in the following Taccount:

5

Throughout the year, supplies were used daily, but corresponding accounting entries were not made. This would be impractical and inefficient. As a result, the balance of the supplies account is inaccurate.

The supplies used helped to generate revenue. As a result, an expense account needs to be considered. If the expense is not accounted for, reported net income would be higher, resulting in higher income tax remittance and a very unimpressed boss.

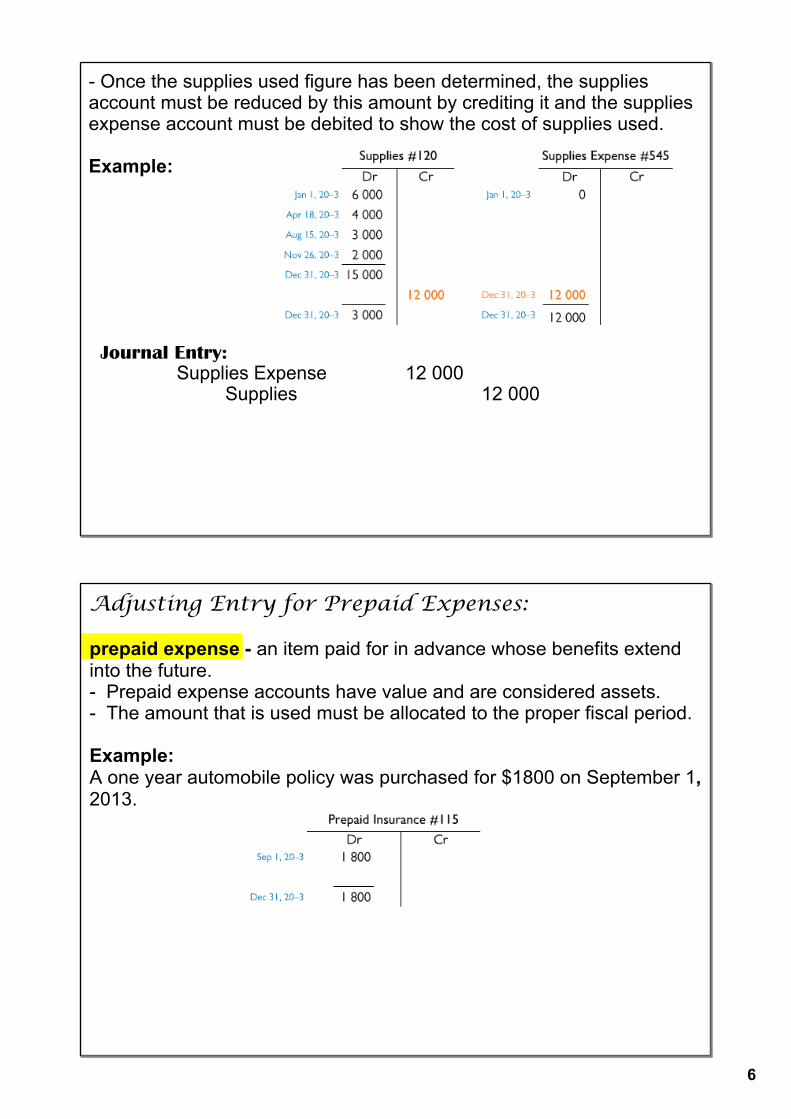

To bring the supplies account up to date and to record the appropriate expense, an inventory of supplies must be completed. Once inventory is completed, it is subtracted from the balance in the supplies account to determine the amount of supplies used.

Example:Ending inventory of supplies was determined to be $3000.

Supplied used = Balance inventorySupplies used = $15 000 3 000Supplies Used = $12 000

6

Once the supplies used figure has been determined, the supplies account must be reduced by this amount by crediting it and the supplies expense account must be debited to show the cost of supplies used.

Example:

Journal Entry:Supplies Expense 12 000

Supplies 12 000

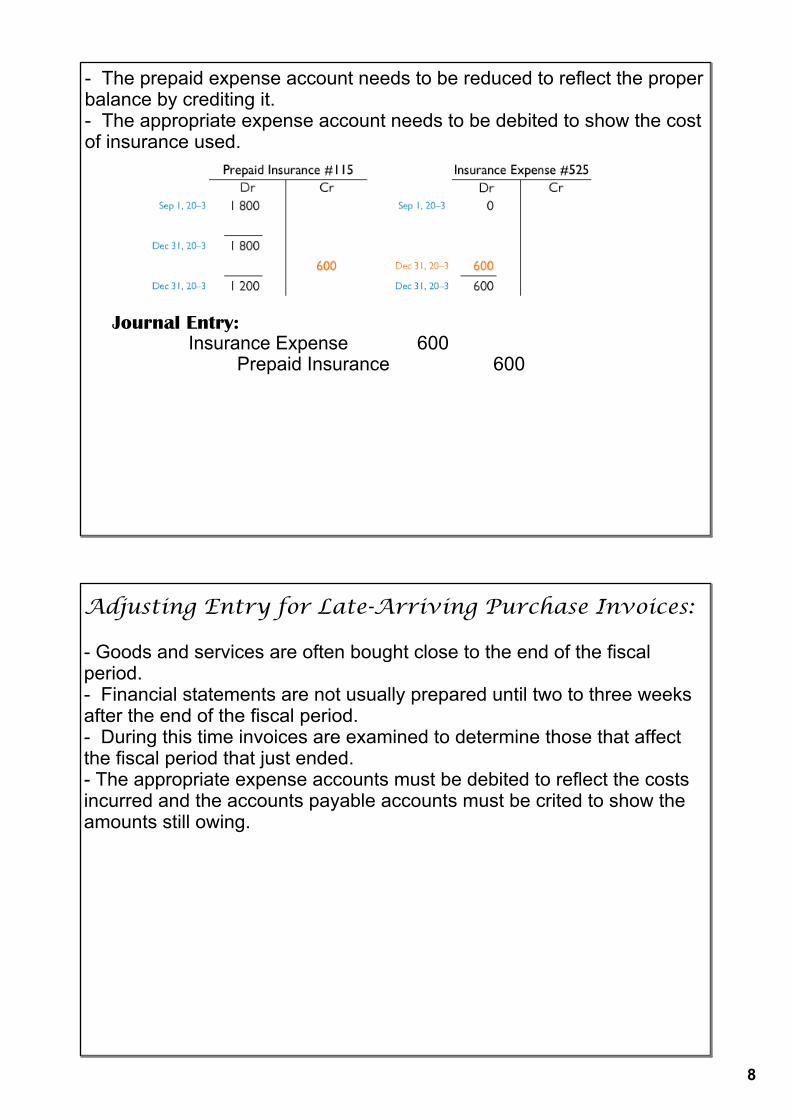

Adjusting Entry for Prepaid Expenses:

prepaid expense an item paid for in advance whose benefits extend into the future. Prepaid expense accounts have value and are considered assets. The amount that is used must be allocated to the proper fiscal period.

Example:A one year automobile policy was purchased for $1800 on September 1, 2013.

7

The adjustment for a prepaid expense is the same as the one for supplies. The unused amount has to be determined using a simple calculation:

Value of policy x number of months remaining = Value remaining number of months on the policy

Example:A 12 months insurance policy purchased for $1800 on September 1, 2013. Determined the value remaining on December 31, 2013.

The prepaid expense account needs to be brought up to date to reflect the proper balance:

8

The prepaid expense account needs to be reduced to reflect the proper balance by crediting it. The appropriate expense account needs to be debited to show the cost of insurance used.

Journal Entry:Insurance Expense 600

Prepaid Insurance 600

Adjusting Entry for Late-Arriving Purchase Invoices:

Goods and services are often bought close to the end of the fiscal period. Financial statements are not usually prepared until two to three weeks after the end of the fiscal period. During this time invoices are examined to determine those that affect the fiscal period that just ended. The appropriate expense accounts must be debited to reflect the costs incurred and the accounts payable accounts must be crited to show the amounts still owing.

9

Example: Financial statements were being prepared on January 15, 2014. The following invoices were determined to be latearriving and should be accounted for in the previous fiscal period: telephone $212 and utilities $315.

Journal Entry:Telephone Expense 212Utilities Expense 315

Accounts Payable 527

Adjusting Entry for Unearned Revenue:

This adjustment is necessary when payment for services is in advance. If recorded before the revenue is actually earned, the revenue recognition principle is violated. Amount needs to be removed from the revenue account in order to have an accurate income statement. The revenue account needs to be debited and the Unearned revenue account (a liability) needs to be credited.

10

Example:At the end of the fiscal period, it is discovered that the business was paid $5000 for a service yet to be performed.

Adjusting Entries in the Journal:Page 275

11

worksheet an informal business paper used to organize and plan the information for financial statements.

8.2 Adjusting Entries and the Worksheet Pages 279 289

Page 280

12

Steps in Preparing a Worksheet:1. Write the heading.

2. Enter all the accounts and their balances in the first two columns and total them. DO NOT proceed unless the trial balance balances.

3. Enter the adjustments and total the two columns. DO NOT proceed unless the adjustments columns balance.

4. Extend the balance sheet accounts (A, L, C, D) to the balance sheet columns and the income statement accounts (R, E) to the income statement columns. Add or subtract depending upon what is in the adjustments columns.

5. Balance the worksheet by:a) Total the income statement (IS) and balance sheet (BS) columns.b) Calculate the difference between the IS columns and the BS columns. If they are equal, complete the balance sheet. If not, a mistake has occurred which must be found.

c) Place the difference found in b) under the smaller figure in both the IS columns and the BS columns.

Net Income: Extreme columnsNet Loss: Middle columns.

d) Total the IS columns, which should balance, and the BS columns, which should also balance.

e) Write in Net Income/Loss in the Accounts Column

13

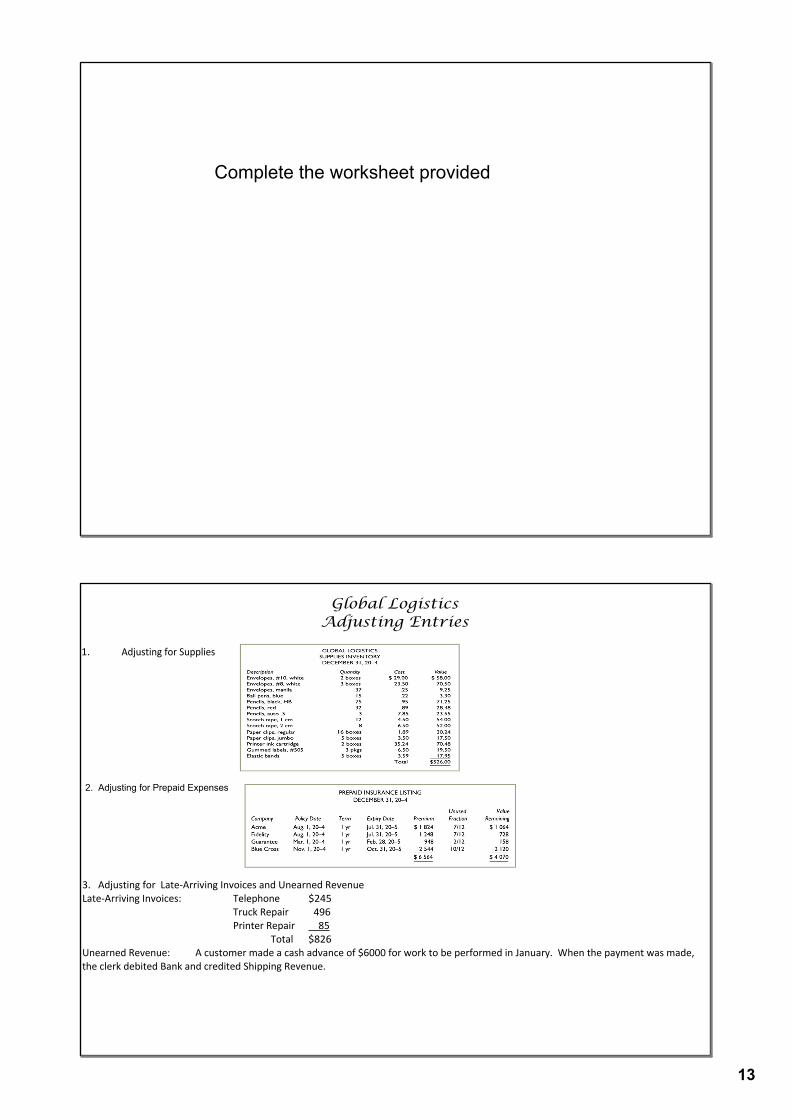

Complete the worksheet provided

Global LogisticsAdjusting Entries

1. Adjusting for Supplies

2. Adjusting for Prepaid Expenses

3. Adjusting for Late‐Arriving Invoices and Unearned RevenueLate‐Arriving Invoices: Telephone $245

Truck Repair 496Printer Repair 85

Total $826Unearned Revenue: A customer made a cash advance of $6000 for work to be performed in January. When the payment was made,the clerk debited Bank and credited Shipping Revenue.

14

Preparing the Financial Statements: All information needed is provided on the worksheet.

15

16

Journalizing and Posting the Adjusting Entries: Adjusting entries need to be recorded in the journal and then posted to the appropriate accounts.

17

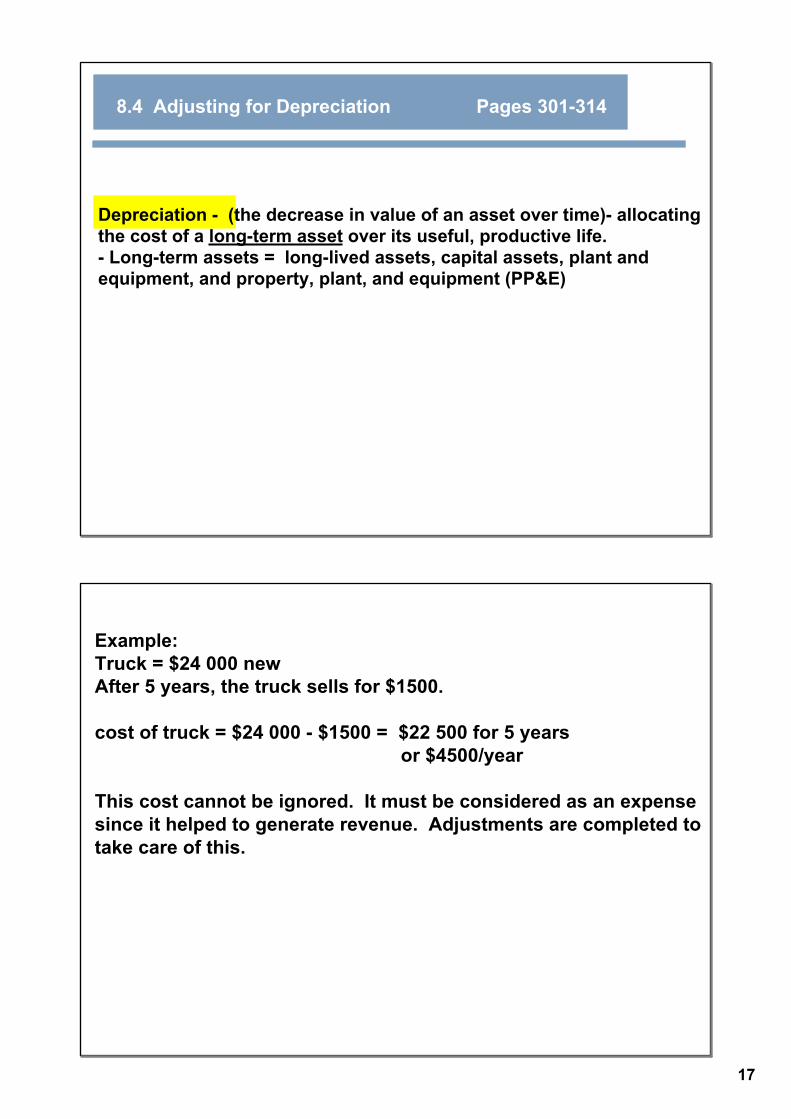

8.4 Adjusting for Depreciation Pages 301314

Depreciation (the decrease in value of an asset over time) allocating the cost of a longterm asset over its useful, productive life. Longterm assets = longlived assets, capital assets, plant and equipment, and property, plant, and equipment (PP&E)

Example:Truck = $24 000 newAfter 5 years, the truck sells for $1500.

cost of truck = $24 000 $1500 = $22 500 for 5 years or $4500/year

This cost cannot be ignored. It must be considered as an expense since it helped to generate revenue. Adjustments are completed to take care of this.

18

Impossible to determine the exact value of depreciation until the end of the asset's useful life.

Depreciation, however, must be included in financial statements.

Depreciation, therefore, must be estimated while the asset is still in use.

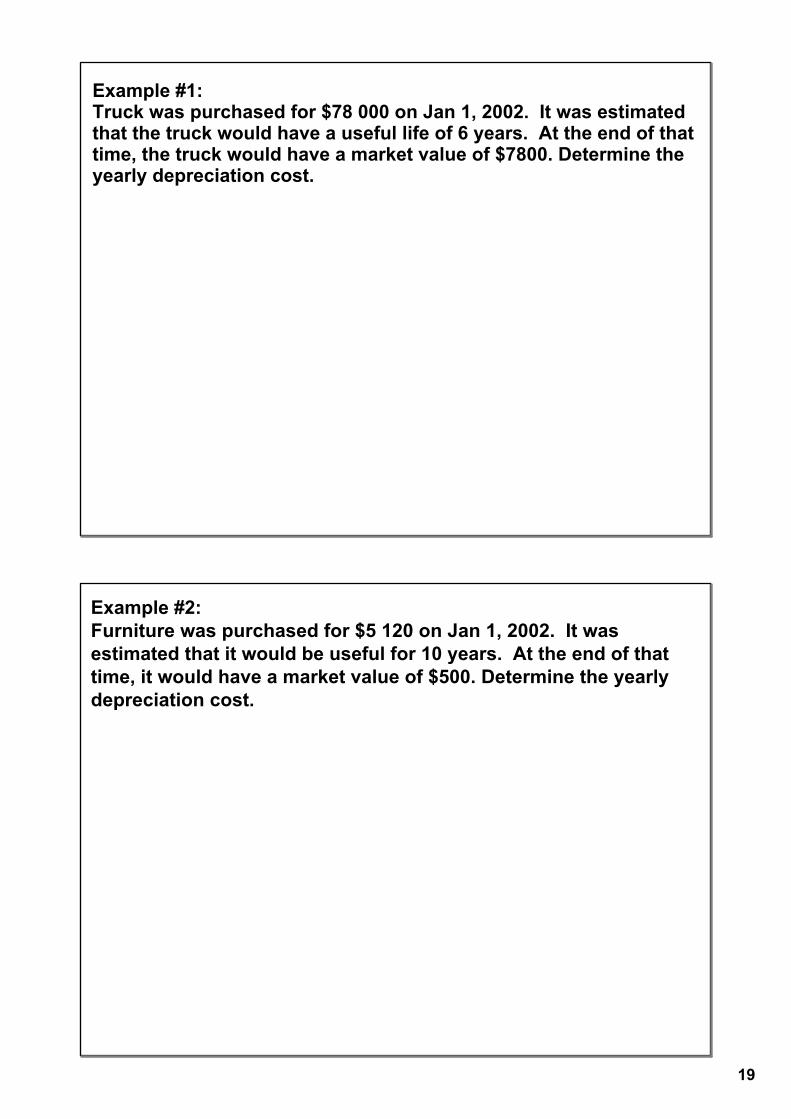

Two Methods of Calculating Depreciation:1. Straight Line Method divides the net cost of an asset equally over the years of the asset's life.Formula:

SLM = original cost of asset estimated salvage value Estimated number of periods in the life of the asset

19

Example #1: Truck was purchased for $78 000 on Jan 1, 2002. It was estimated that the truck would have a useful life of 6 years. At the end of that time, the truck would have a market value of $7800. Determine the yearly depreciation cost.

Example #2: Furniture was purchased for $5 120 on Jan 1, 2002. It was estimated that it would be useful for 10 years. At the end of that time, it would have a market value of $500. Determine the yearly depreciation cost.

20

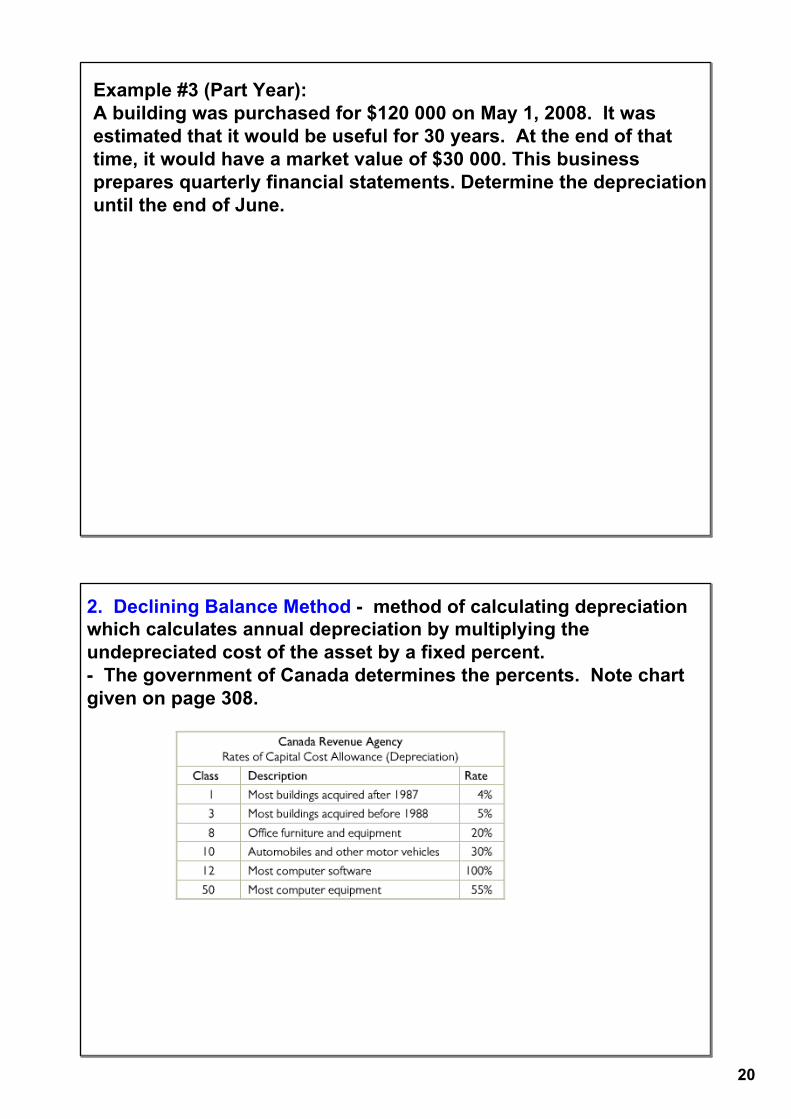

Example #3 (Part Year): A building was purchased for $120 000 on May 1, 2008. It was estimated that it would be useful for 30 years. At the end of that time, it would have a market value of $30 000. This business prepares quarterly financial statements. Determine the depreciation until the end of June.

2. Declining Balance Method method of calculating depreciation which calculates annual depreciation by multiplying the undepreciated cost of the asset by a fixed percent. The government of Canada determines the percents. Note chart given on page 308.

21

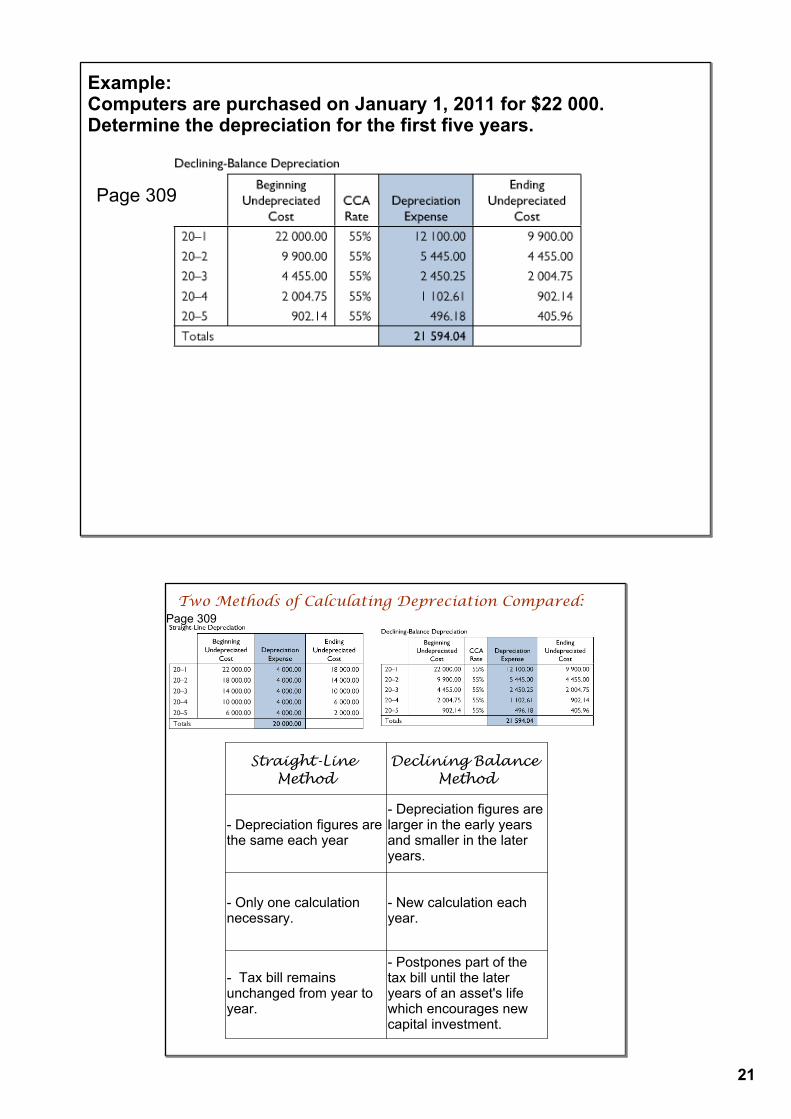

Example:Computers are purchased on January 1, 2011 for $22 000. Determine the depreciation for the first five years.

Page 309

Two Methods of Calculating Depreciation Compared:Page 309

Straight-Line Method

Declining Balance Method

Depreciation figures are the same each year

Depreciation figures are larger in the early years and smaller in the later years.

Only one calculation necessary.

New calculation each year.

Tax bill remains unchanged from year to year.

Postpones part of the tax bill until the later years of an asset's life which encourages new capital investment.

22

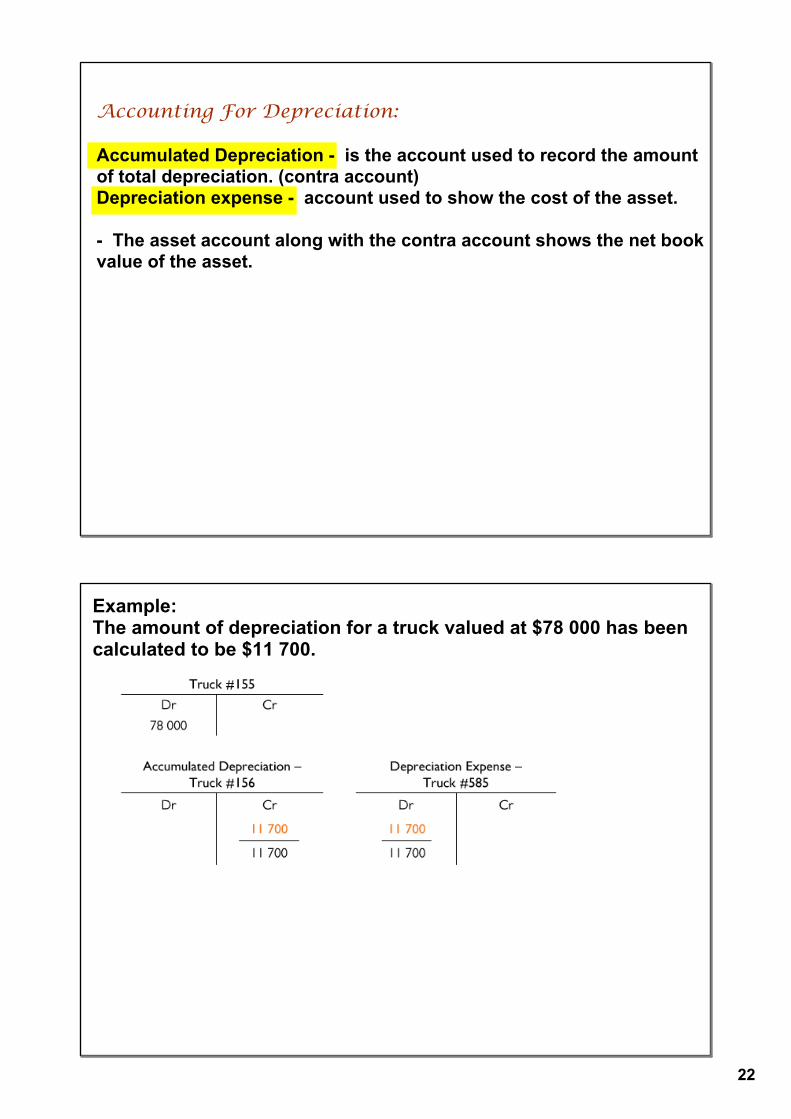

Accounting For Depreciation: Accumulated Depreciation is the account used to record the amount of total depreciation. (contra account) Depreciation expense account used to show the cost of the asset.

The asset account along with the contra account shows the net book value of the asset.

Example:The amount of depreciation for a truck valued at $78 000 has been calculated to be $11 700.

23

To Summarize:The adjusting entry for depreciation: Records the depreciation in a depreciation expense account.

Increases the specific accumulated depreciation account for the asset which reduces the net book value of the asset.

Page 306

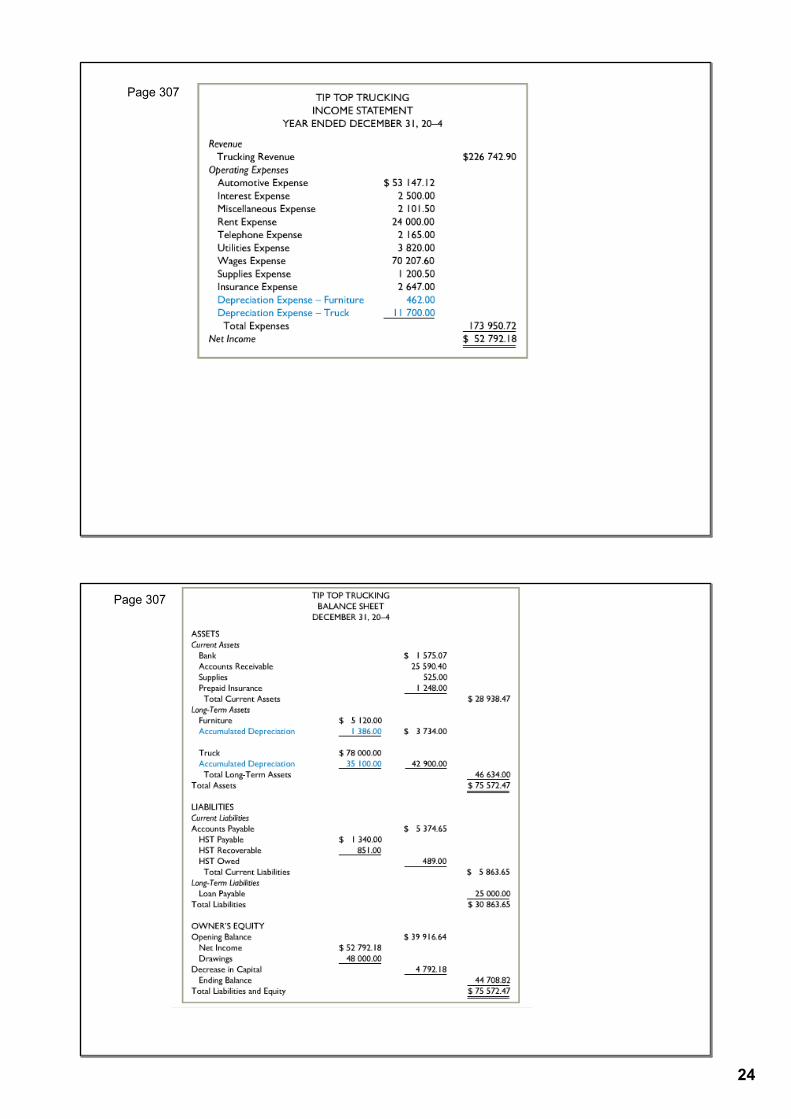

24

Page 307

Page 307

25

8.3 Preparing for New Fiscal Years Pages 289 301

Once financial statements have been prepared, many amounts in the ledger are no longer needed since they apply to the previous fiscal period.

To prepare for the next fiscal period, the balance in these accounts need to be reset or closed

Real (Permanent) accounts accounts whose balances will continue into the next fiscal period. These pertain to the balance sheet accounts. The only real account whose balance changes during the closing process is the capital account.

Nominal (temporary) accounts accounts whose balances will not continue into the next fiscal period. With the exception of the drawings account, these pertain to the income statement accounts.

26

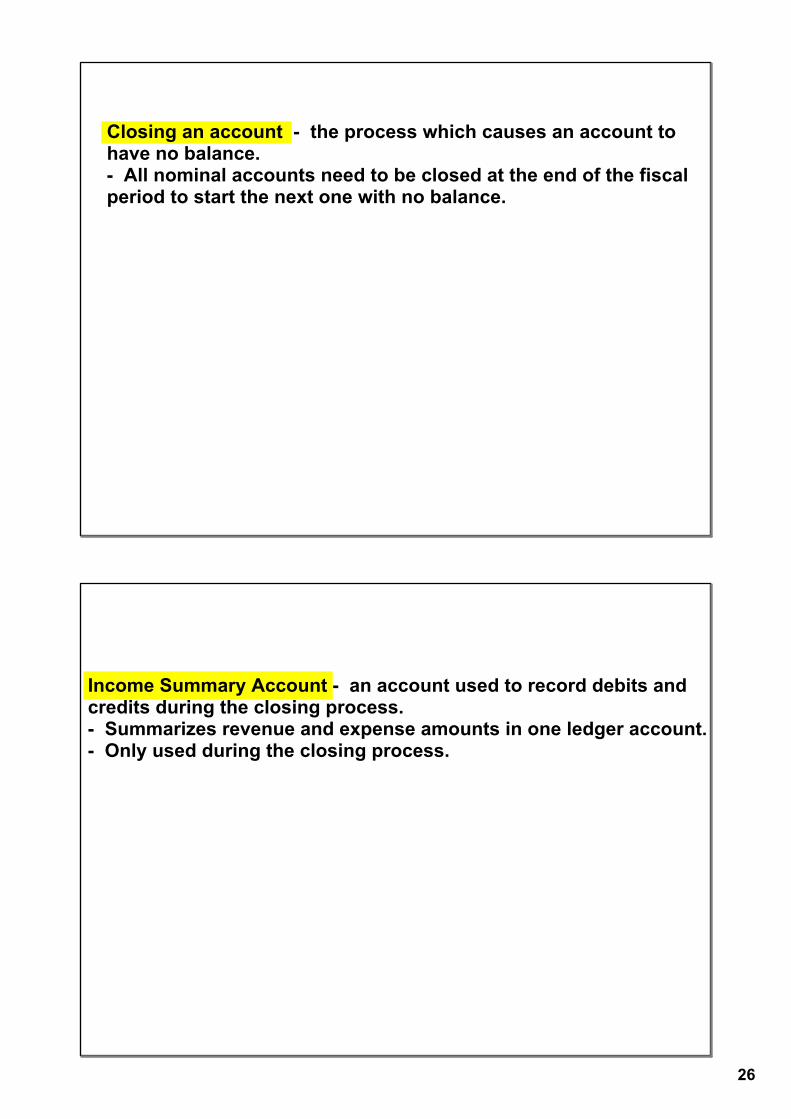

Closing an account the process which causes an account to have no balance. All nominal accounts need to be closed at the end of the fiscal period to start the next one with no balance.

Income Summary Account an account used to record debits and credits during the closing process. Summarizes revenue and expense amounts in one ledger account. Only used during the closing process.

27

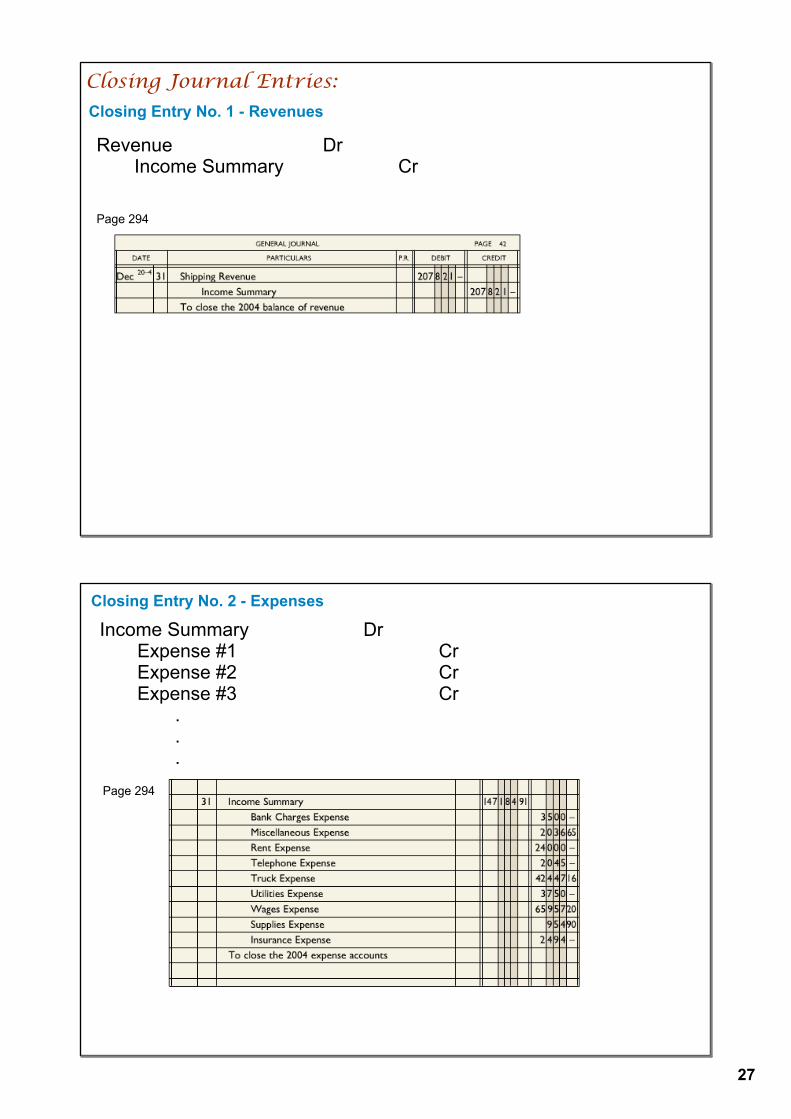

Closing Journal Entries:

Revenue DrIncome Summary Cr

Page 294

Closing Entry No. 1 Revenues

Income Summary DrExpense #1 CrExpense #2 CrExpense #3 Cr

.

.

.Page 294

Closing Entry No. 2 Expenses

28

Closing Entry No. 3 Income SummaryNet Income:Income Summary Dr

Capital Cr

Net Loss:Capital Dr

Income Summary Cr

Page 295

Closing Entry No. 4 Drawings

Capital DrDrawings Cr

Page 295

29

Closing Journal Entries Summarized:

Once all the closing entries have been completed the capital account has been brought up to date to reflect the equity section on the balance sheet.

Post Closing Trial Balance a trail balance prepared using the remaining real accounts to ensure the closing process was completed accurately.

Page 290