Chapter 7 Individual From AGI Deductions © 2014 by McGraw-Hill Education. This is proprietary...

13

Chapter 7 Individual From AGI Deductions © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

-

Upload

ruth-jefferson -

Category

Documents

-

view

219 -

download

2

Transcript of Chapter 7 Individual From AGI Deductions © 2014 by McGraw-Hill Education. This is proprietary...

Chapter 7

Individual From AGI Deductions

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

7-2

Learning objectives

1. Describe the different types of itemized deductions available to individuals and compute itemized deductions

2. Explain the operation of the standard deduction, determine the deduction for personal and dependency exemptions, and compute taxable income

7-3

Itemized Deductions

Medical Expenses Taxpayers may deduct medical expenses incurred to

treat themselves, their spouse, and their dependents Qualifying medical expenses include unreimbursed

payments for care, prevention, diagnosis or cure of injury, disease, or bodily function

Taxpayers using personal automobiles for medical transportation purposes may deduct a standard mileage allowance (24 cents per mile in 2013) in lieu of actual costs

7-4

Itemized Deductions

Hospitals and Long-term Care Facilities Taxpayers may deduct the costs of actual medical

care whether the care is provided at hospitals or other long-term care facilities

Medical Expenses Deduction Limitation It is limited to the amount of unreimbursed qualifying

medical expenses paid during the year which is reduced by 10% (7.5% for a taxpayer or spouse age 65 or older) of the taxpayer’s AGI

7-5

Taxes Individuals may deduct itemized deductions

payments for following taxes State, local, and foreign income taxes Real estate taxes on property held for personal or

investment purposes Personal property taxes that are assessed on the value

of the specific property

Sales Tax deduction State and local sales taxes can be deducted in lieu of

state and local income taxes

Itemized Deductions

7-6

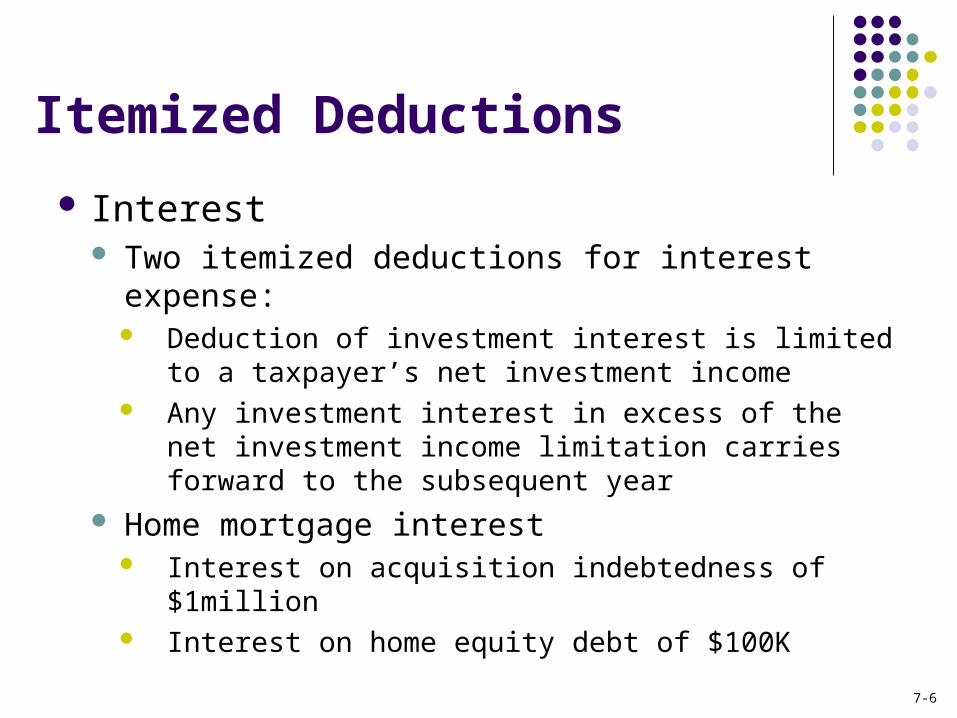

Itemized Deductions

Interest Two itemized deductions for interest expense:

Deduction of investment interest is limited to a taxpayer’s net investment income

Any investment interest in excess of the net investment income limitation carries forward to the subsequent year

Home mortgage interest Interest on acquisition indebtedness of $1million Interest on home equity debt of $100K

7-7

Charitable Contributions Contribution of money or property must be made

to a qualified charity

Special rules apply to charitable contributions of property depending on the type of property: Capital gain property Ordinary income property

Itemized Deductions

7-8

Itemized Deductions

Casualty and theft losses on personal-use assets

The amount of the tax loss from any specific casualty event (including theft) is the lesser of

decline in value of the property caused by the casualty or

taxpayer’s tax basis in the damaged or stolen asset

7-9

Itemized Deductions

Casualty Loss Deduction Floor Limitations It must exceed two separate floor limitations to

qualify as itemized deductions $100 for each casualty during the year 10 percent of AGI floor limit applied to the sum of

all casualty losses for the year (after applying the $100 floor)

In other words, the itemized deduction is the aggregate amount of casualty losses that exceeds 10 percent of AGI

7-10

Itemized Deductions

Miscellaneous Itemized Deductions Subject to AGI Floor Employee Business Expenses

Travel and transportation Employee expense reimbursements

Investment Expenses Tax Preparation Fees Hobby losses Total miscellaneous itemized deductions are

subject to a 2 percent of AGI floor limit

7-11

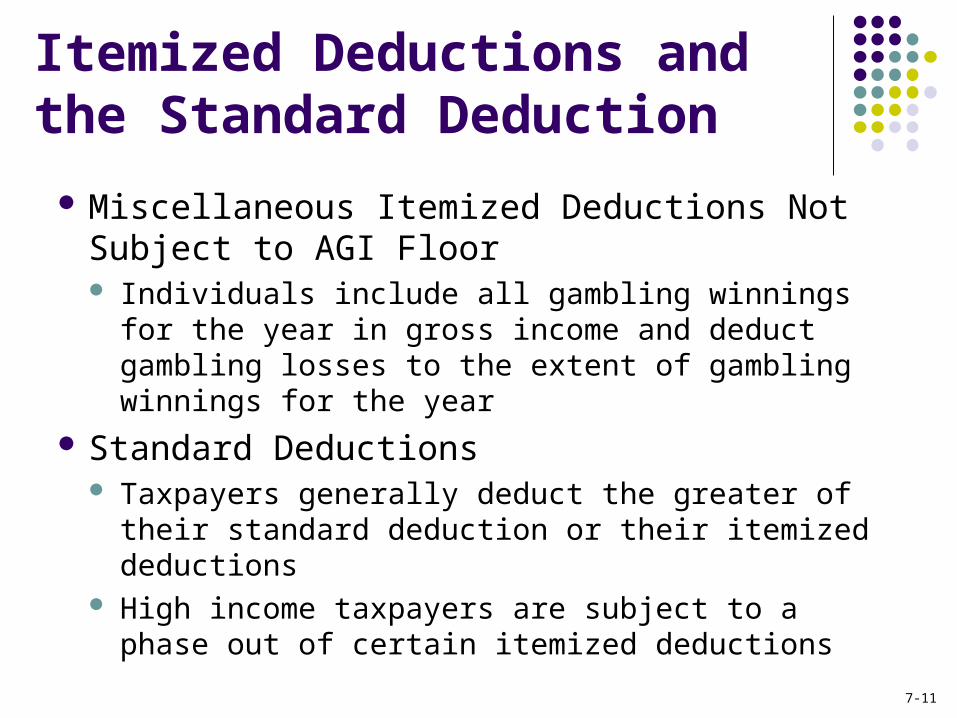

Itemized Deductions and the Standard Deduction

Miscellaneous Itemized Deductions Not Subject to AGI Floor Individuals include all gambling winnings for the

year in gross income and deduct gambling losses to the extent of gambling winnings for the year

Standard Deductions Taxpayers generally deduct the greater of their

standard deduction or their itemized deductions High income taxpayers are subject to a phase out

of certain itemized deductions

7-12

Standard Deductions & Exemptions

Bunching Itemized Deductions Tax benefit can be gained by implementing simple

timing tax-planning strategy Taxpayers with itemized deductions that fall just short

of the standard deduction amount These itemized deductions do not produce any tax

benefit Rather than deduct the standard deduction every

year time deductions (when possible) to bunch together in one year

7-13

Standard Deductions & Exemptions

Deduction for Personal and Dependency Exemptions $3,900 for the taxpayer $3,900 for the taxpayer’s spouse $3,900 for each dependent Subject to phase-out for high income taxpayers

![thetrove.is [multi]/6th Edition...RTG —5-(7)— Initiative Intentbns Movement perception Stealth RIG 5(6) .2 ATT Agi Agi Agi Agi Agi Cha Cha 10 12(13) 14(15) 12(13) 14(1S) 4 A A](https://static.fdocuments.in/doc/165x107/60bfa9da6453b801736552d8/multi6th-edition-rtg-a5-7a-initiative-intentbns-movement-perception.jpg)