Chapter 7. Deductions FROM AGI Howard Godfrey, Ph.D., CPA Professor of Accounting ©Howard...

91

Chapter 7. Deductions FROM AGI Howard Godfrey, Ph.D., CPA Professor of Accounting ©Howard Godfrey-2015

-

Upload

barry-campbell -

Category

Documents

-

view

256 -

download

1

Transcript of Chapter 7. Deductions FROM AGI Howard Godfrey, Ph.D., CPA Professor of Accounting ©Howard...

Chapter 7.Deductions FROM AGI

Howard Godfrey, Ph.D., CPAProfessor of Accounting ©Howard Godfrey-2015

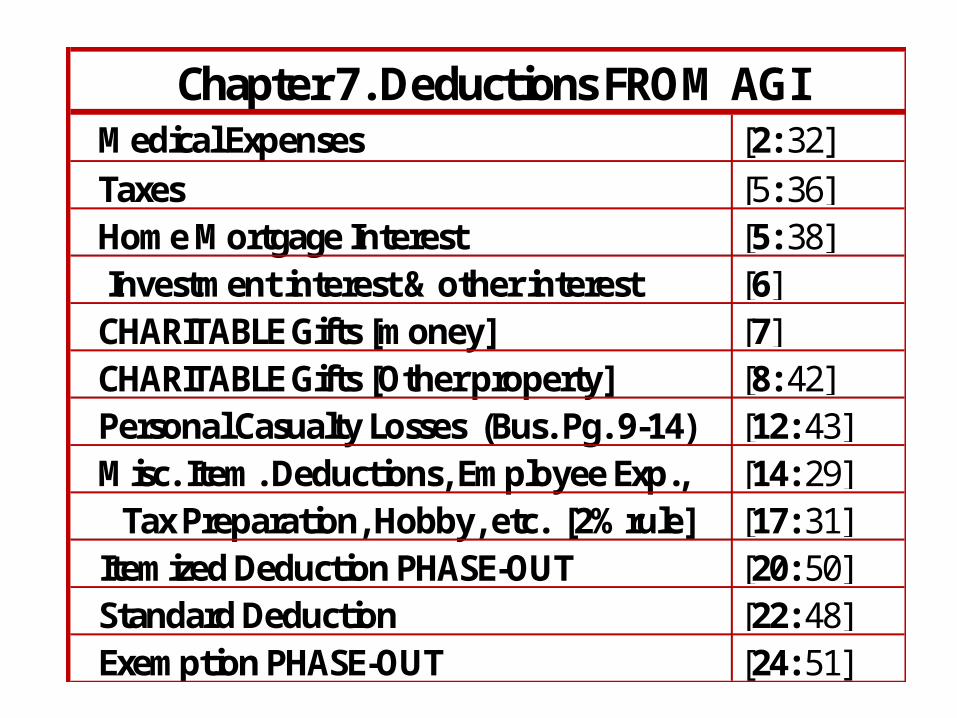

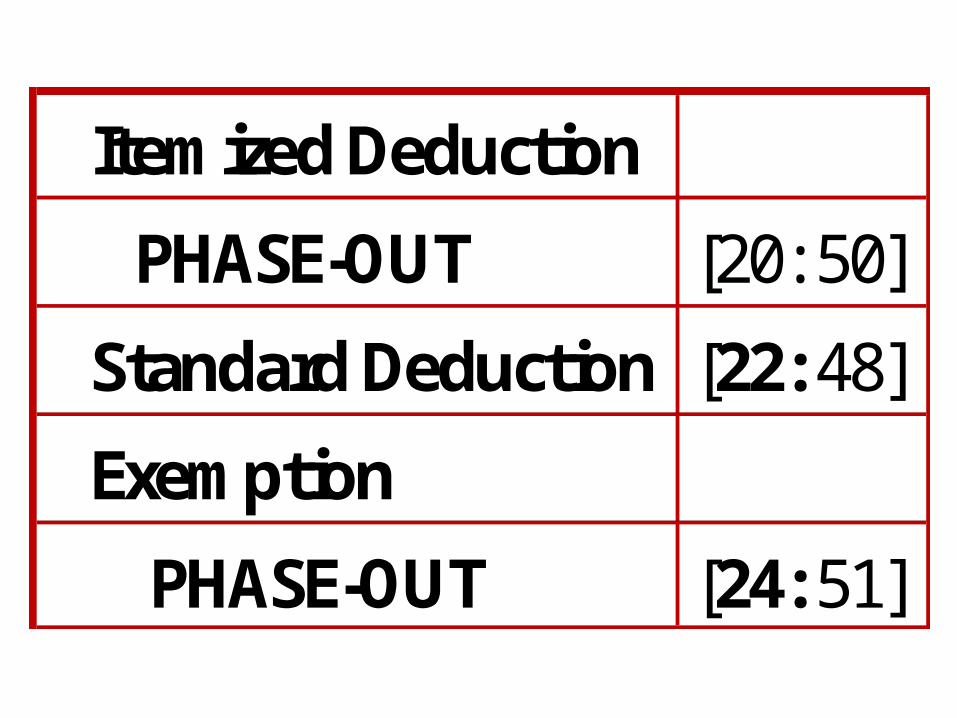

Medical Expenses [2: 32]Taxes [5: 36]Home Mortgage Interest [5: 38] Investment interest & other interest [6]CHARITABLE Gifts [money] [7]CHARITABLE Gifts [Other property] [8: 42]Personal Casualty Losses (Bus. Pg. 9-14) [12: 43]Misc. Item. Deductions, Employee Exp., [14: 29] Tax Preparation, Hobby, etc. [2% rule] [17: 31]Itemized Deduction PHASE-OUT [20: 50]Standard Deduction [22: 48]Exemption PHASE-OUT [24: 51]

Chapter 7. Deductions FROM AGI

Medical [2: 32]Taxes [5: 36]

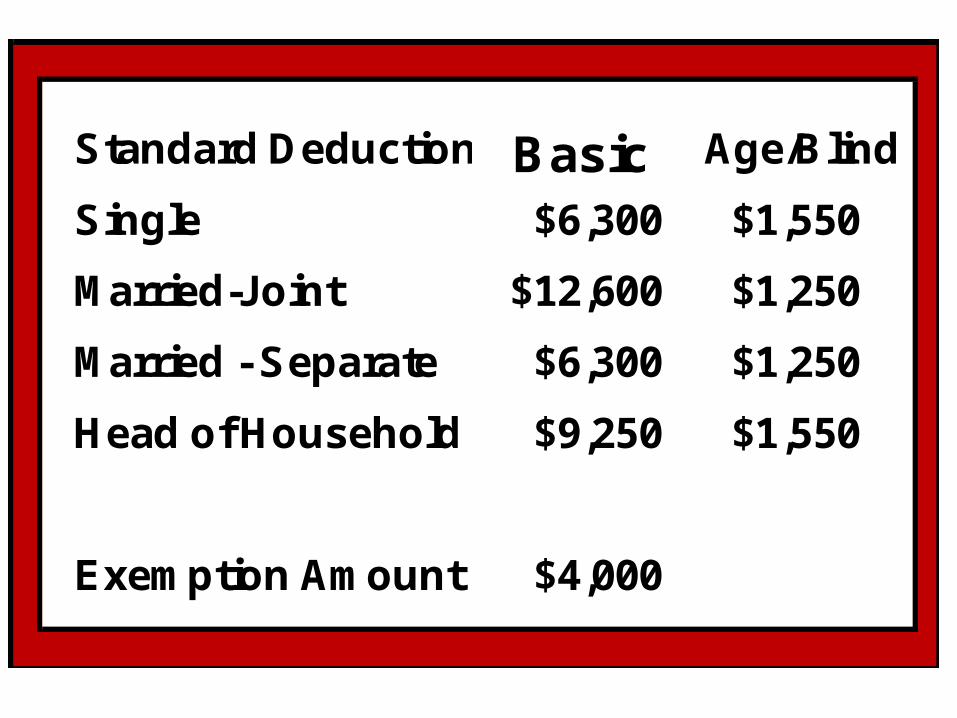

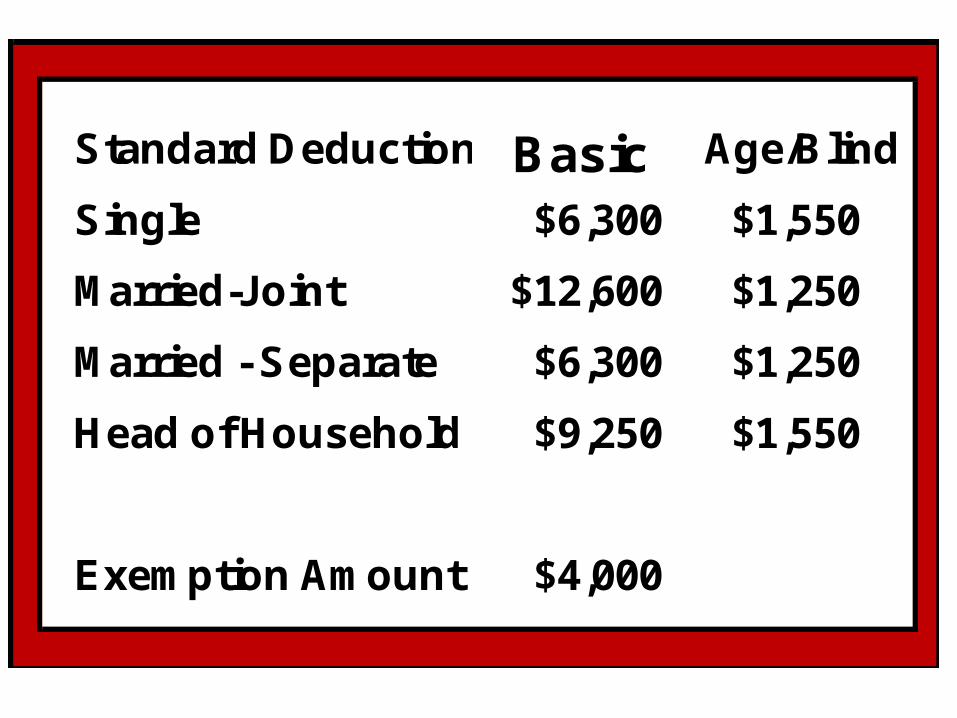

Standard Deduction Basic Age/Blind

Single $6,300 $1,550

Married-Joint $12,600 $1,250

Married - Separate $6,300 $1,250

Head of Household $9,250 $1,550

Exemption Amount $4,000

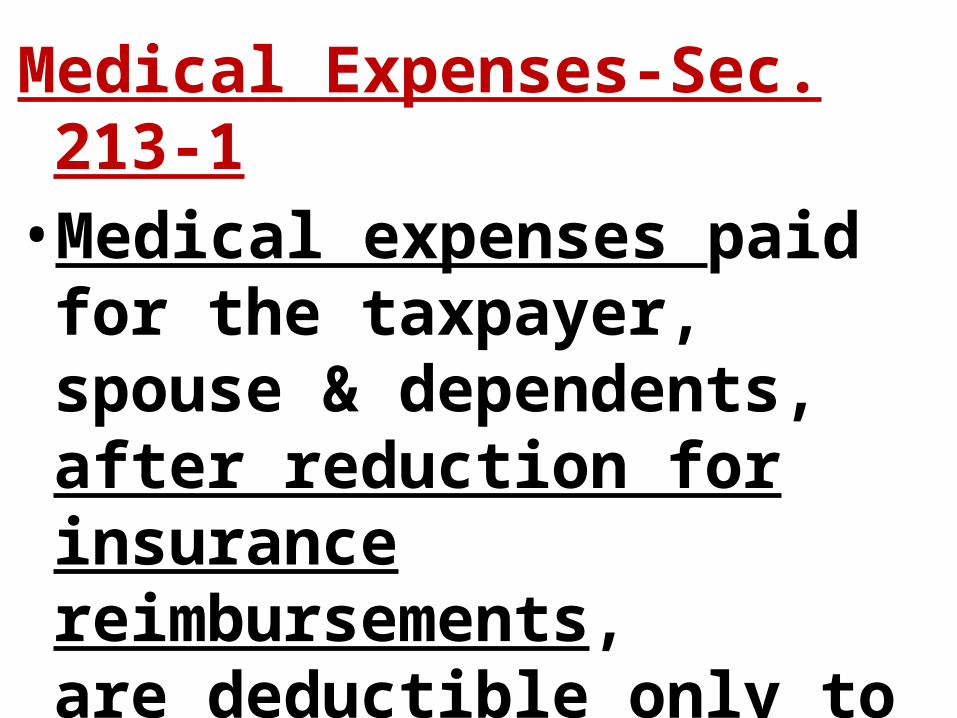

Medical Expenses-Sec. 213-1• Medical expenses paid for the

taxpayer, spouse & dependents, after reduction for insurance reimbursements, are deductible only to the extent they exceed 10% of AGI for the year.

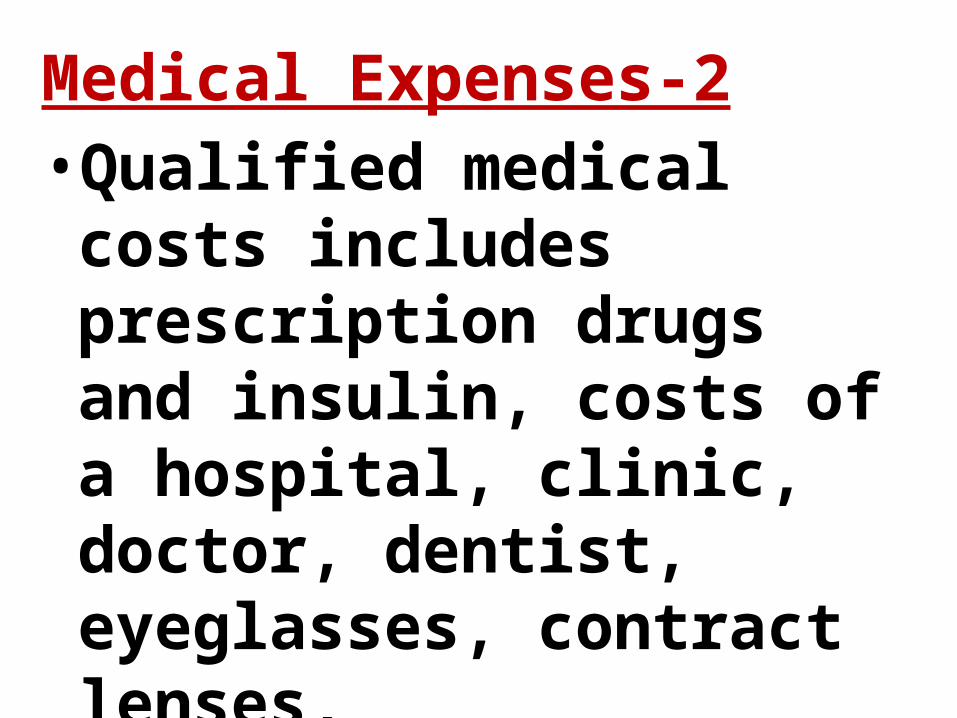

Medical Expenses-2• Qualified medical costs

includes prescription drugs and insulin, costs of a hospital, clinic, doctor, dentist, eyeglasses, contract lenses, transportation for medical care and health insurance costs.

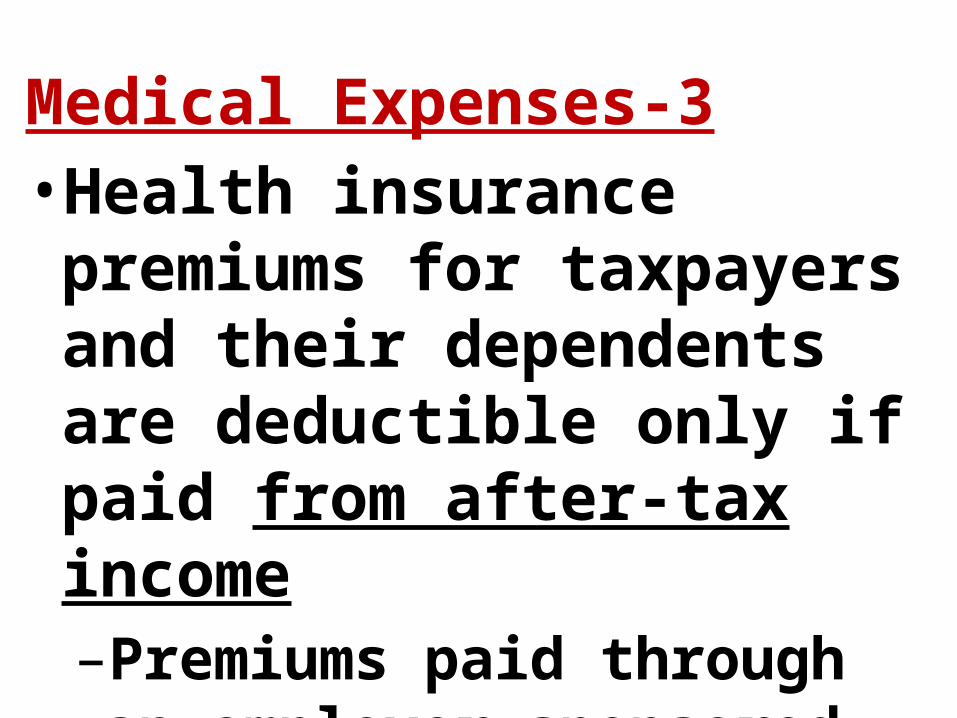

Medical Expenses-3• Health insurance premiums for

taxpayers and their dependents are deductible only if paid from after-tax income–Premiums paid through an

employer-sponsored cafeteria plan are not deductible

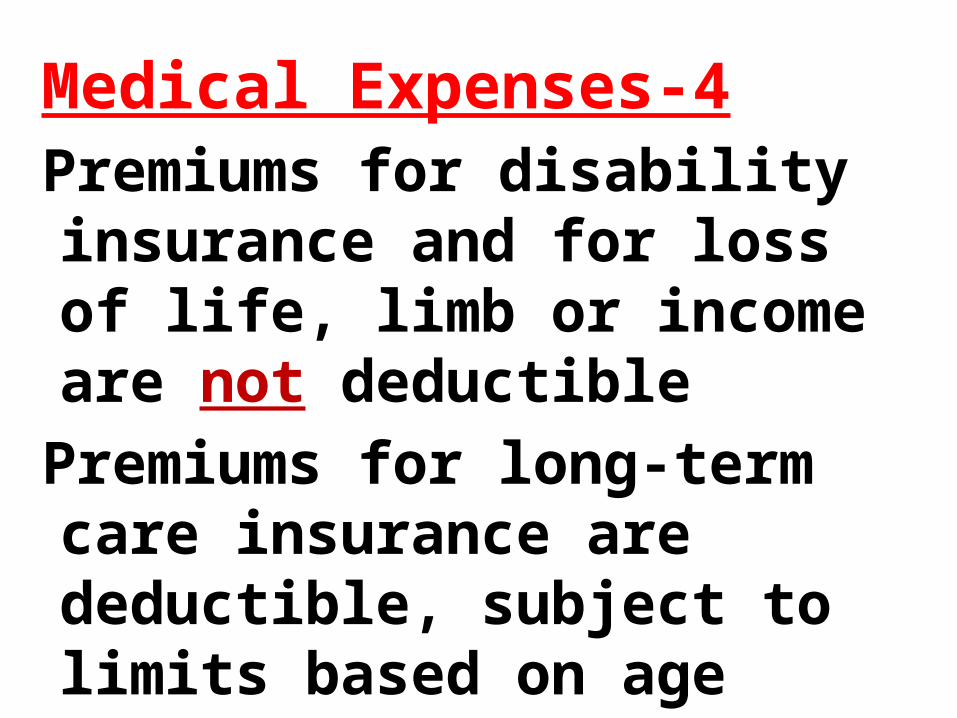

Medical Expenses-4Premiums for disability insurance and for loss of life, limb or income are not deductible

Premiums for long-term care insurance are deductible, subject to limits based on age

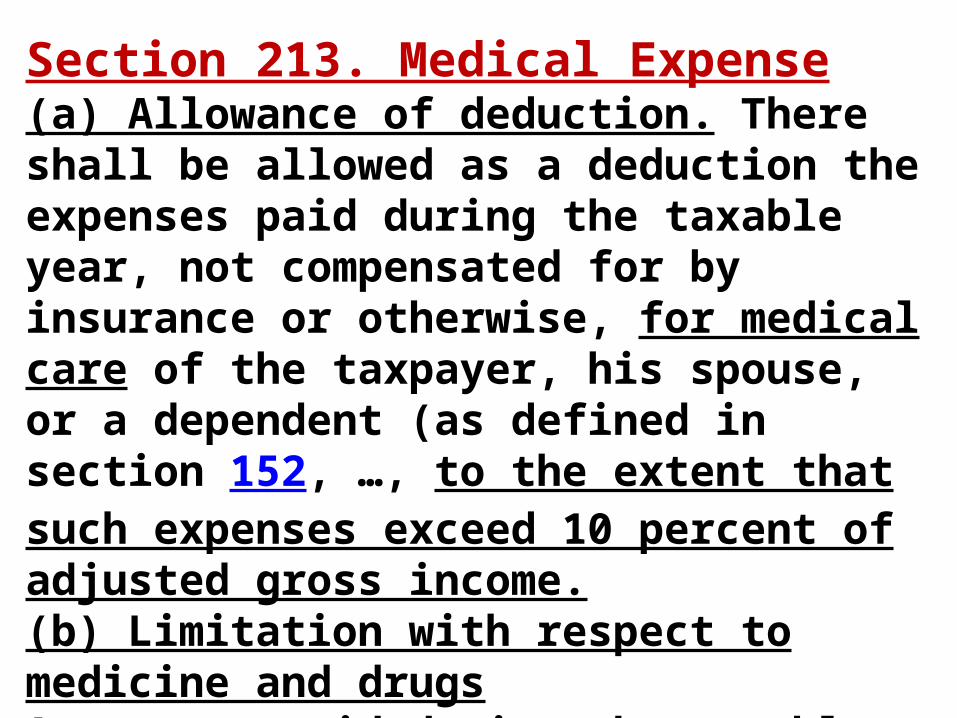

Section 213. Medical Expense(a) Allowance of deduction. There shall be allowed as a deduction the expenses paid during the taxable year, not compensated for by insurance or otherwise, for medical care of the taxpayer, his spouse, or a dependent (as defined in section 152, …, to the extent that such expenses exceed 10 percent of adjusted gross income.(b) Limitation with respect to medicine and drugsAn amount paid during the taxable year for medicine or a drug shall be taken into account under subsection (a) only if such medicine or drug is a prescribed drug or is insulin.

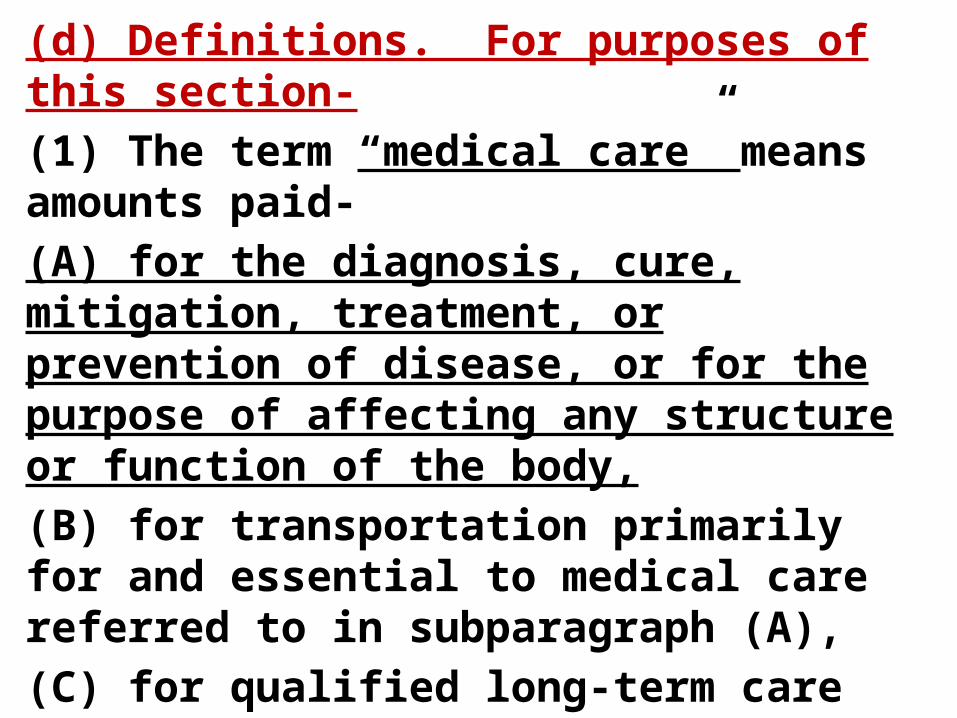

(d) Definitions. For purposes of this section-(1) The term “medical care” means amounts paid-(A) for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body,(B) for transportation primarily for and essential to medical care referred to in subparagraph (A),(C) for qualified long-term care services …, or(D) for insurance …covering medical care referred to in subparagraphs (A) and (B) or for any qualified long-term care insurance contract (as defined in section 7702B (b)).

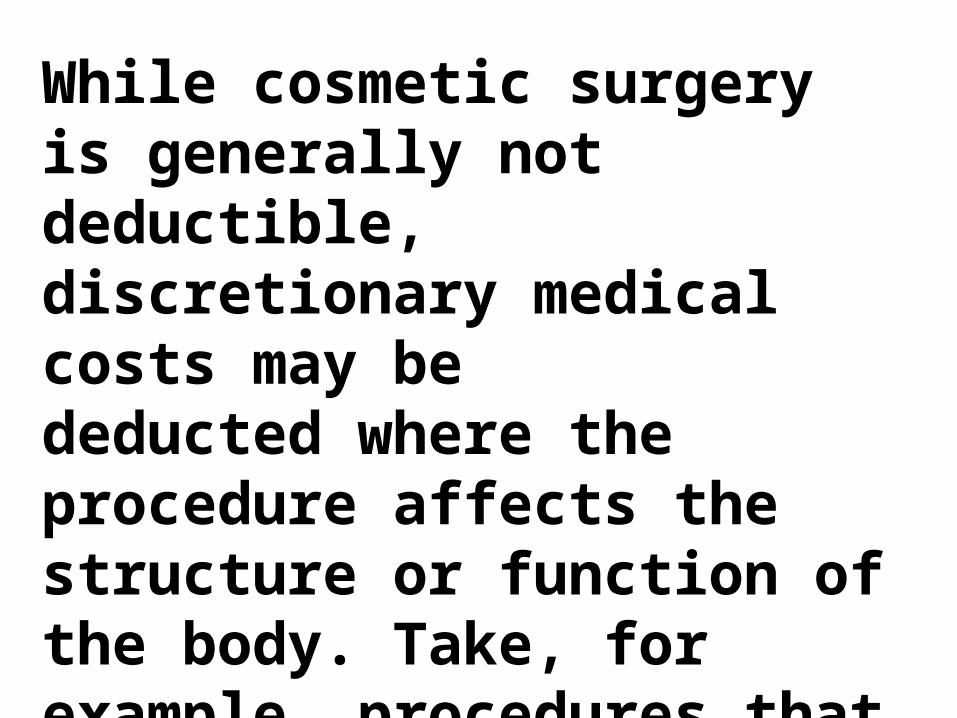

While cosmetic surgery is generally not deductible, discretionary medical costs may be deducted where the procedure affects the structure or function of the body. Take, for example, procedures that facilitate pregnancy by overcoming infertility.

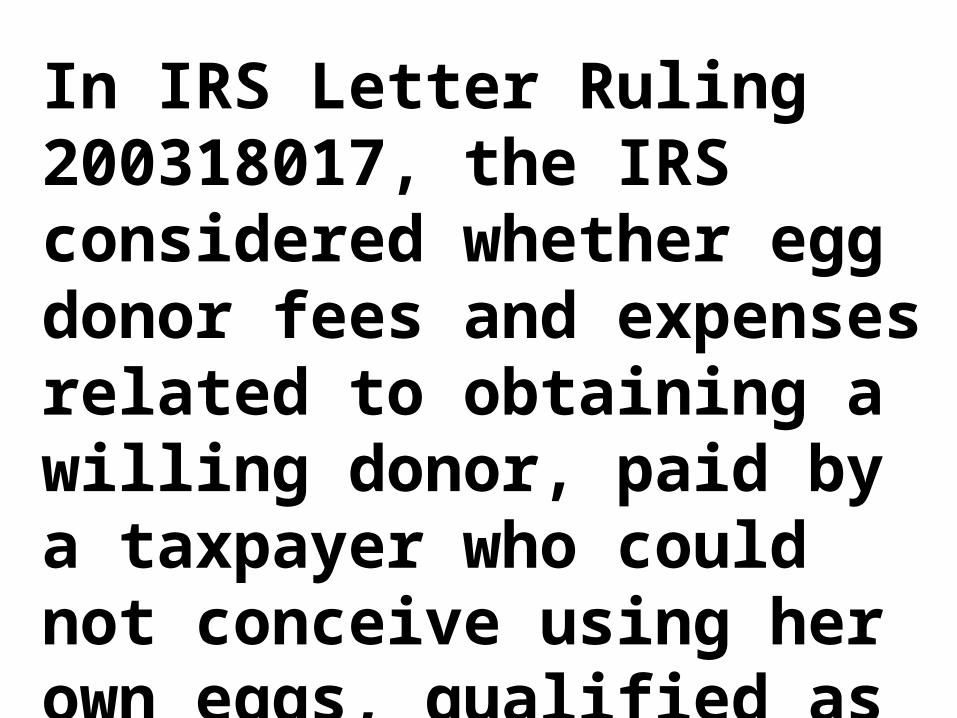

In IRS Letter Ruling 200318017, the IRS considered whether egg donor fees and expenses related to obtaining a willing donor, paid by a taxpayer who could not conceive using her own eggs, qualified as deductible medical expenses.

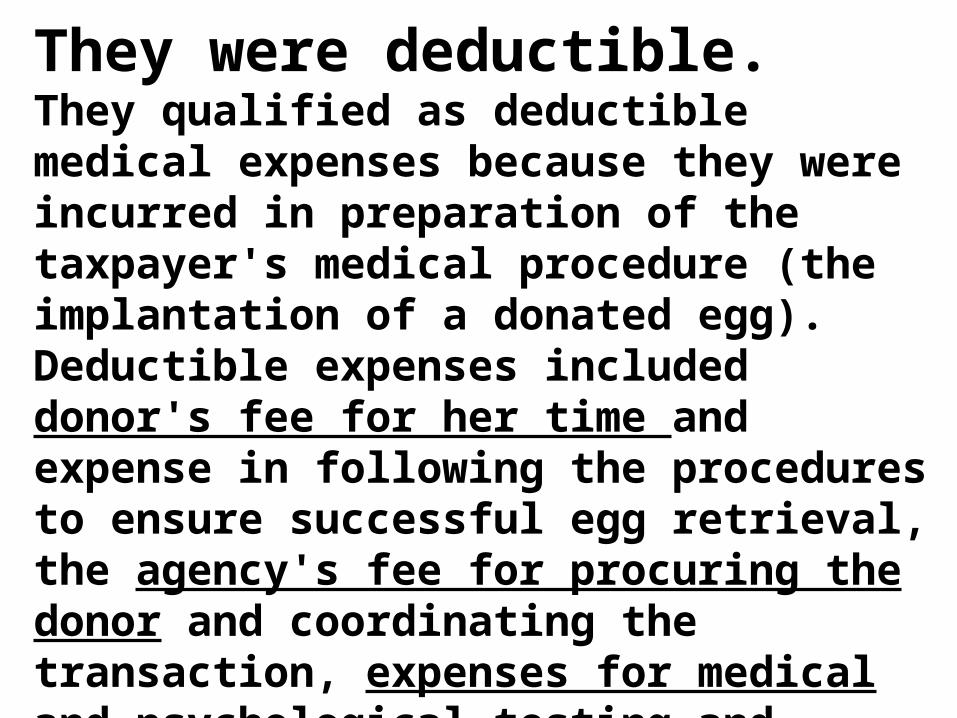

They were deductible.They qualified as deductible medical expenses because they were incurred in preparation of the taxpayer's medical procedure (the implantation of a donated egg). Deductible expenses included donor's fee for her time and expense in following the procedures to ensure successful egg retrieval, the agency's fee for procuring the donor and coordinating the transaction, expenses for medical and psychological testing and assistance of the donor before and after the procedure, and legal fees for preparing a contract between the taxpayer and the donor.

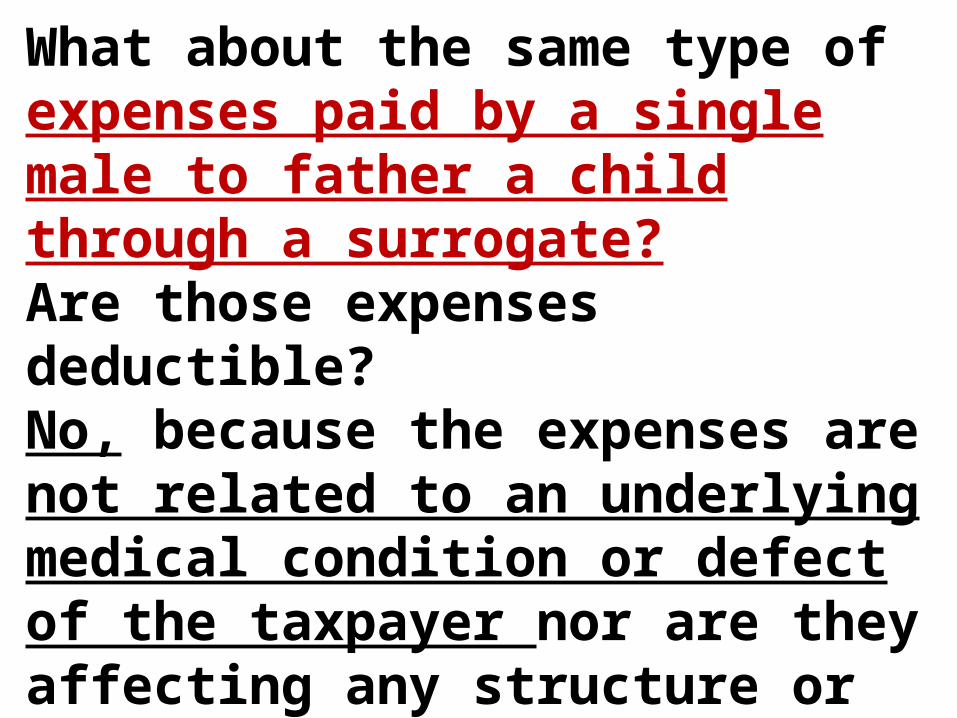

What about the same type of expenses paid by a single male to father a child through a surrogate?Are those expenses deductible? No, because the expenses are not related to an underlying medical condition or defect of the taxpayer nor are they affecting any structure or function of his body. See William Magdalin, TC Memo 2008-293.

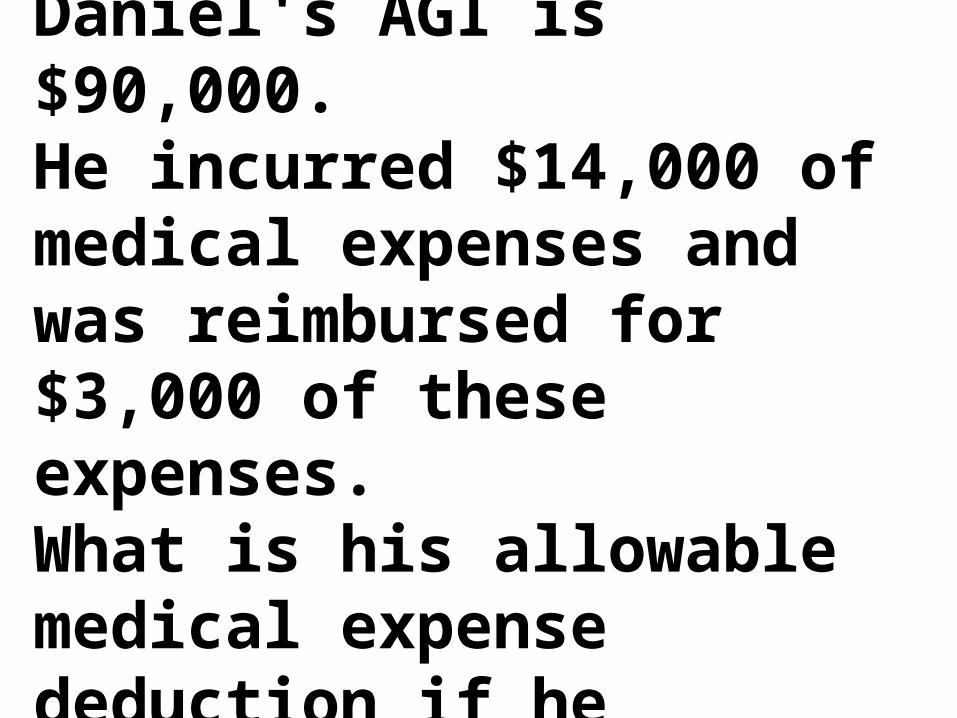

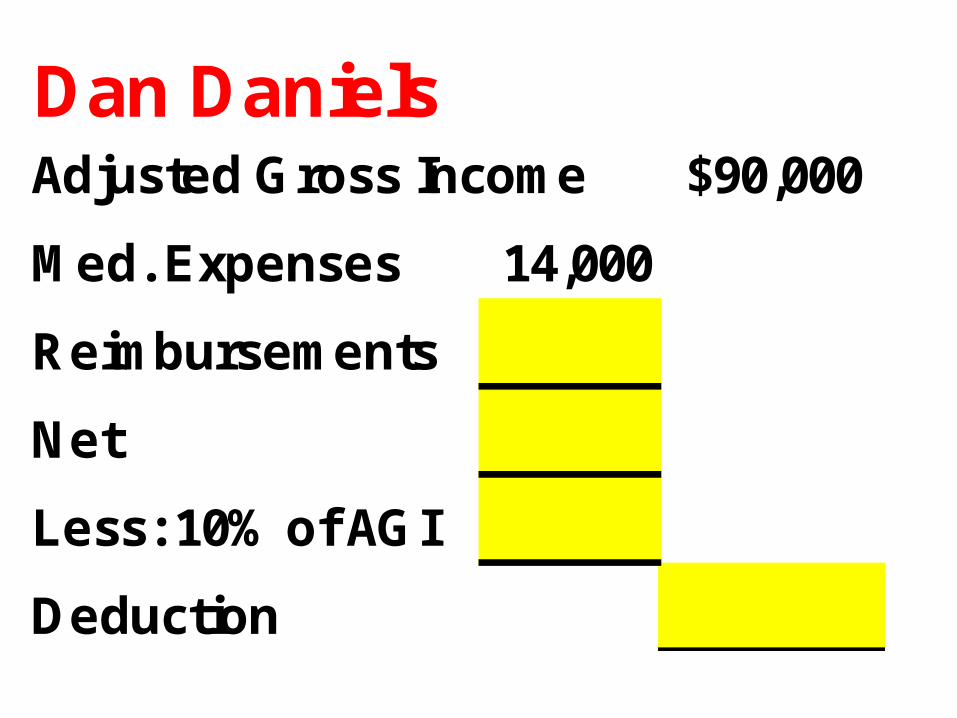

Medical Expense DeductionDaniel's AGI is $90,000. He incurred $14,000 of medical expenses and was reimbursed for $3,000 of these expenses. What is his allowable medical expense deduction if he itemizes?

Dan DanielsAdjusted Gross Income $90,000

Med. Expenses 14,000

Reimbursements

Net

Less: 10% of AGI

Deduction

Dan DanielsAdjusted Gross Income $90,000

Med. Expenses Paid 14,000

Reimbursements (3,000)

Net 11,000

Subtract 10% of AGI (9,000)

Deduction - Med. Expenses $2,000

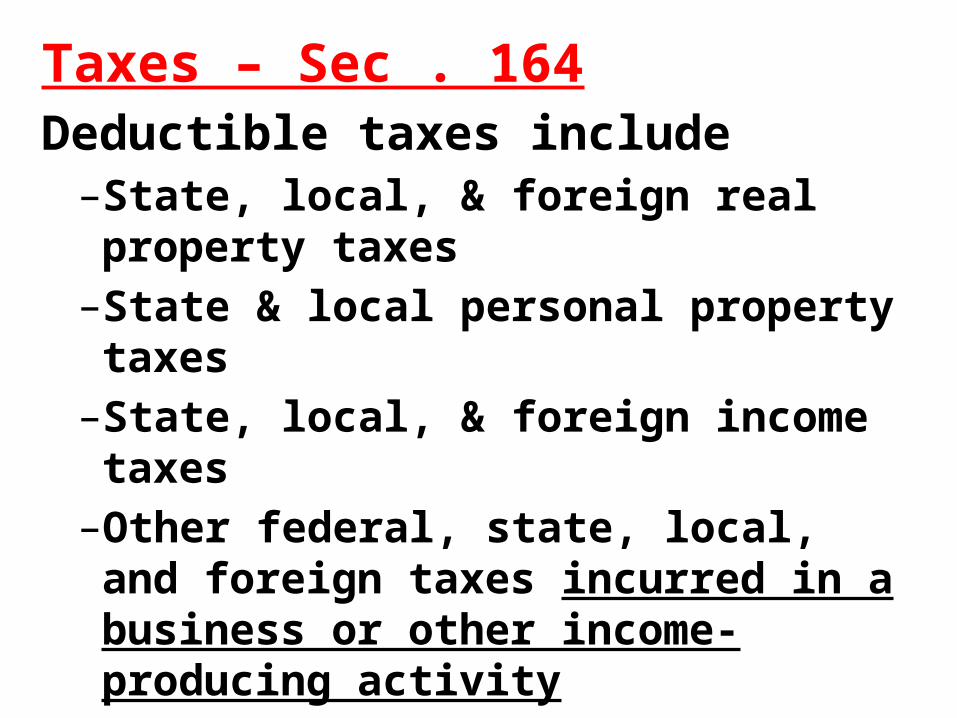

Taxes – Sec . 164Deductible taxes include

–State, local, & foreign real property taxes–State & local personal property taxes–State, local, & foreign income taxes–Other federal, state, local, and foreign taxes

incurred in a business or other income-producing activity

–Can elect to deduct state & local general sales taxes instead of state & local income taxes

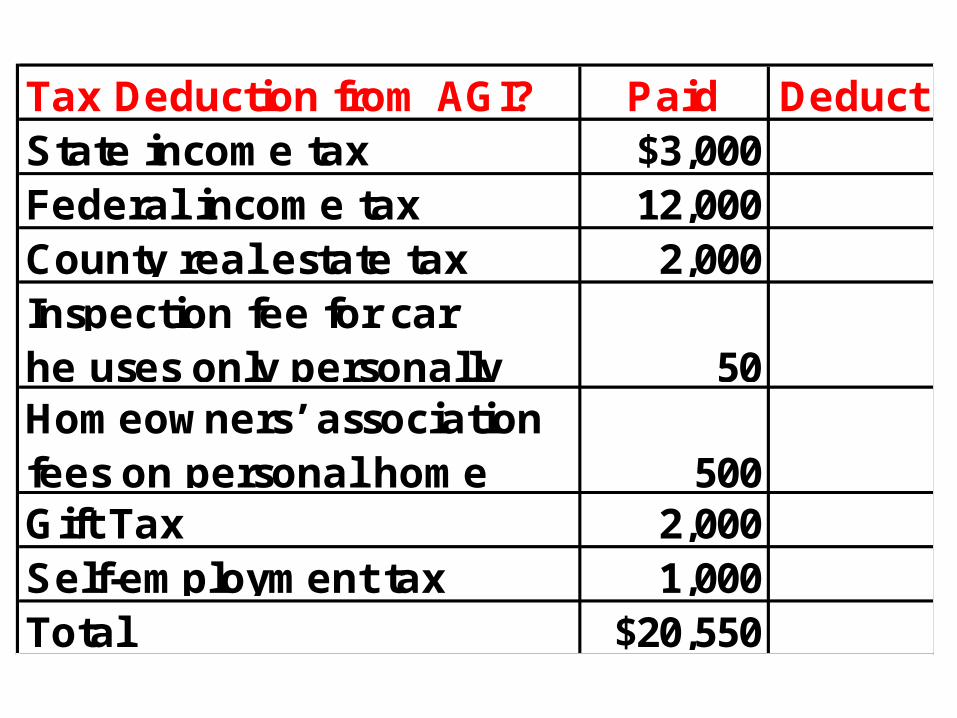

Tax Deduction from AGI? Paid DeductState income tax $3,000 Federal income tax 12,000County real estate tax 2,000Inspection fee for carhe uses only personally 50Homeowners’ association fees on personal home 500Gift Tax 2,000Self-employment tax 1,000Total $20,550

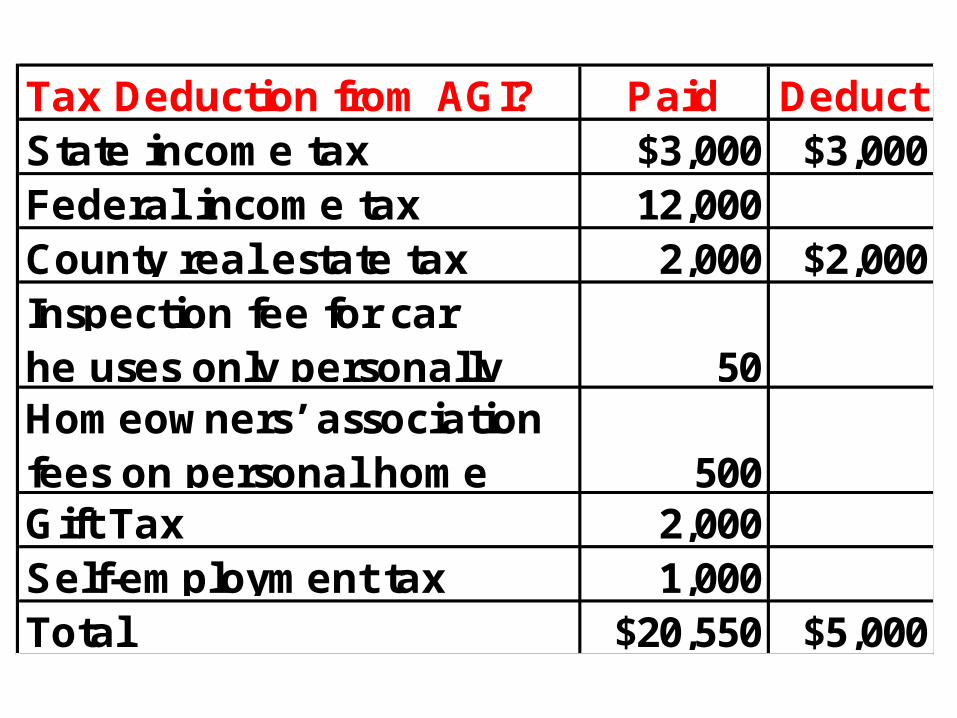

Tax Deduction from AGI? Paid DeductState income tax $3,000 $3,000 Federal income tax 12,000County real estate tax 2,000 $2,000 Inspection fee for carhe uses only personally 50Homeowners’ association fees on personal home 500Gift Tax 2,000Self-employment tax 1,000Total $20,550 $5,000

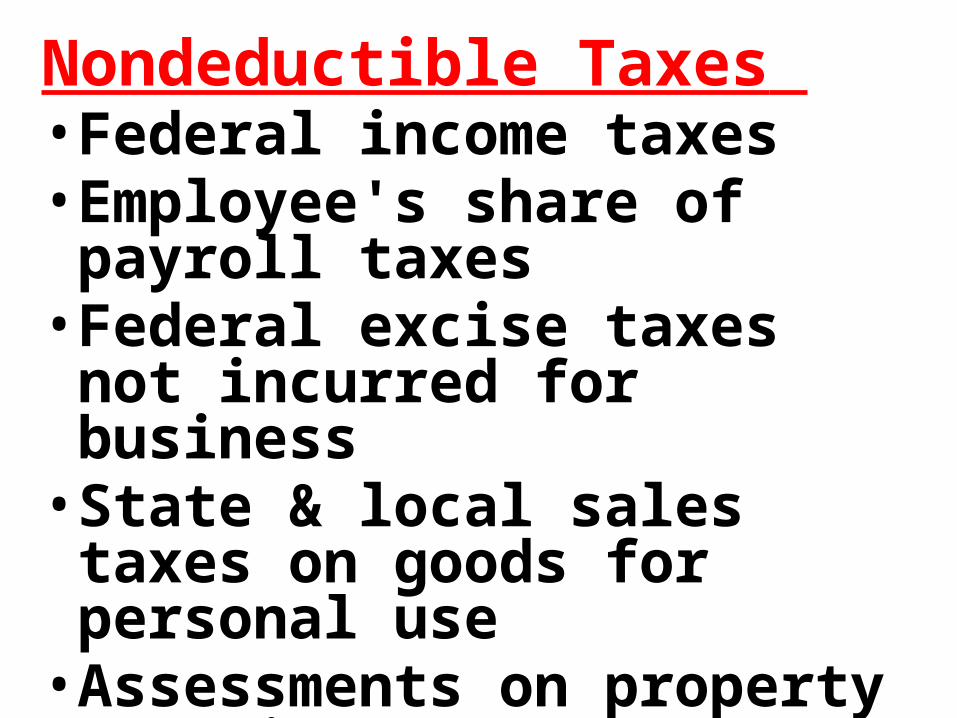

Nondeductible Taxes • Federal income taxes• Employee's share of payroll taxes • Federal excise taxes not incurred

for business• State & local sales taxes on goods

for personal use• Assessments on property that

increase property value

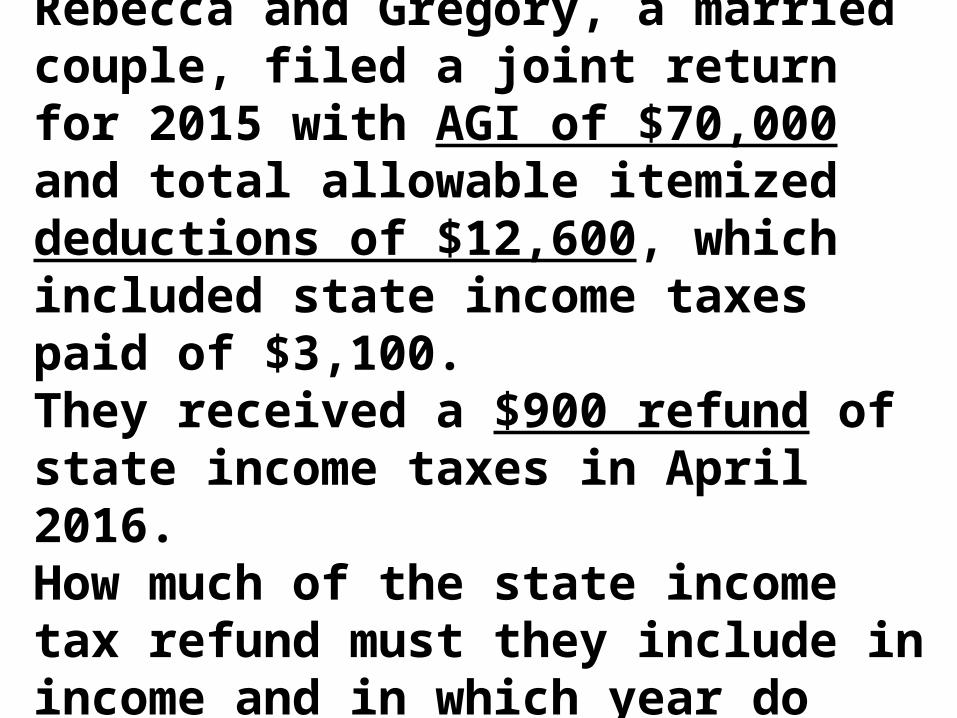

Tax Benefit Rule-1Rebecca and Gregory, a married couple, filed a joint return for 2015 with AGI of $70,000 and total allowable itemized deductions of $12,600, which included state income taxes paid of $3,100. They received a $900 refund of state income taxes in April 2016.How much of the state income tax refund must they include in income and in which year do they include it?

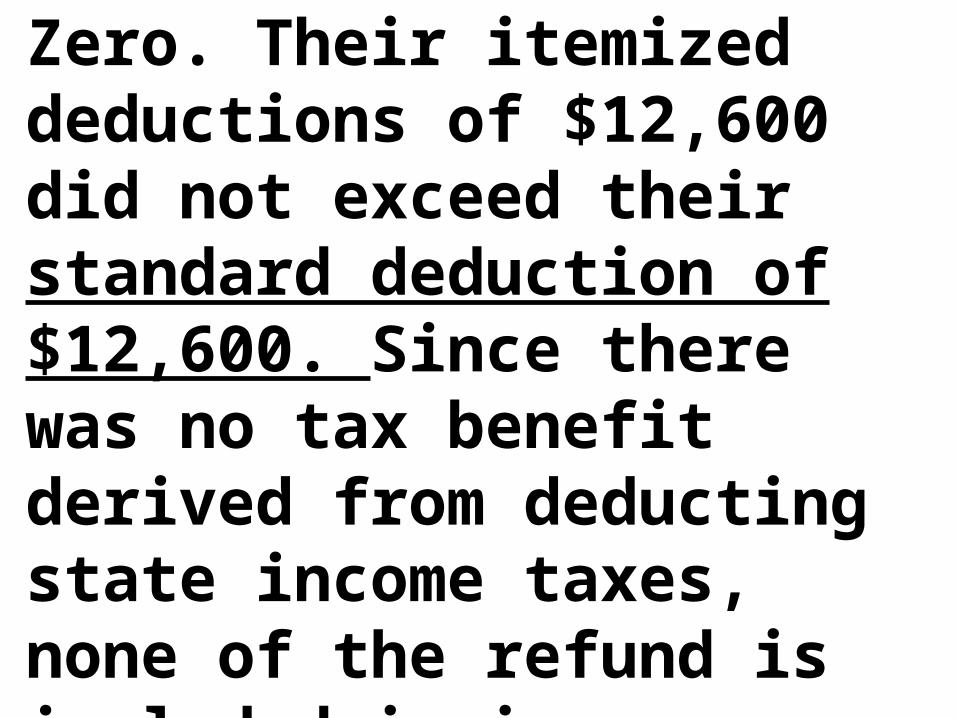

Tax Benefit Rule-2Zero. Their itemized deductions of $12,600 did not exceed their standard deduction of $12,600. Since there was no tax benefit derived from deducting state income taxes, none of the refund is included in income.

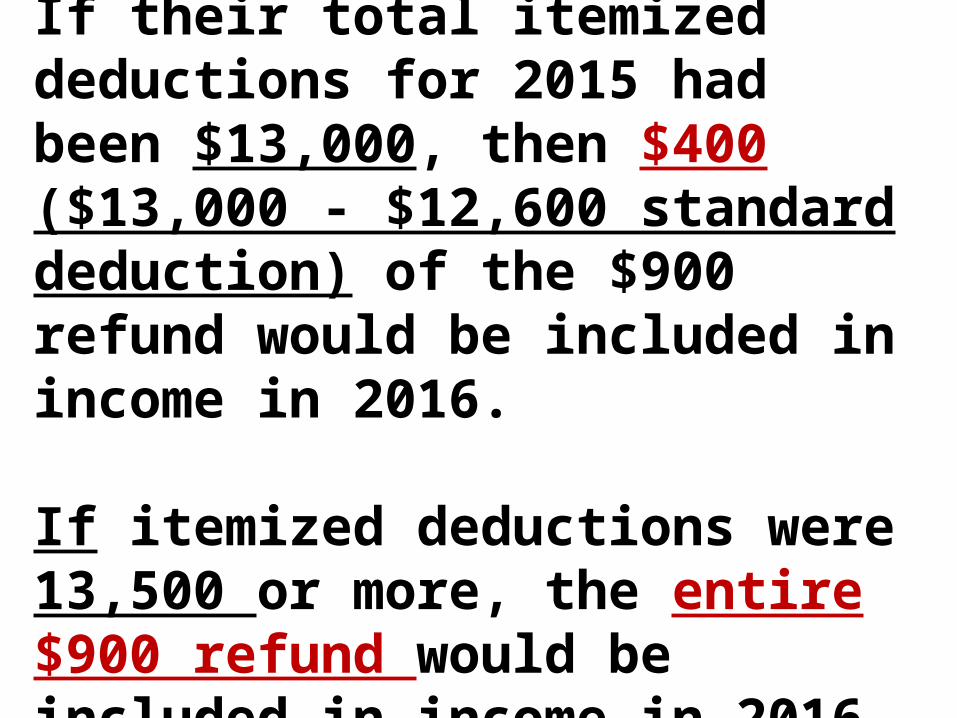

Tax Benefit Rule-3If their total itemized deductions for 2015 had been $13,000, then $400 ($13,000 - $12,600 standard deduction) of the $900 refund would be included in income in 2016.

If itemized deductions were 13,500 or more, the entire $900 refund would be included in income in 2016.

Standard Deduction Basic Age/Blind

Single $6,300 $1,550

Married-Joint $12,600 $1,250

Married - Separate $6,300 $1,250

Head of Household $9,250 $1,550

Exemption Amount $4,000

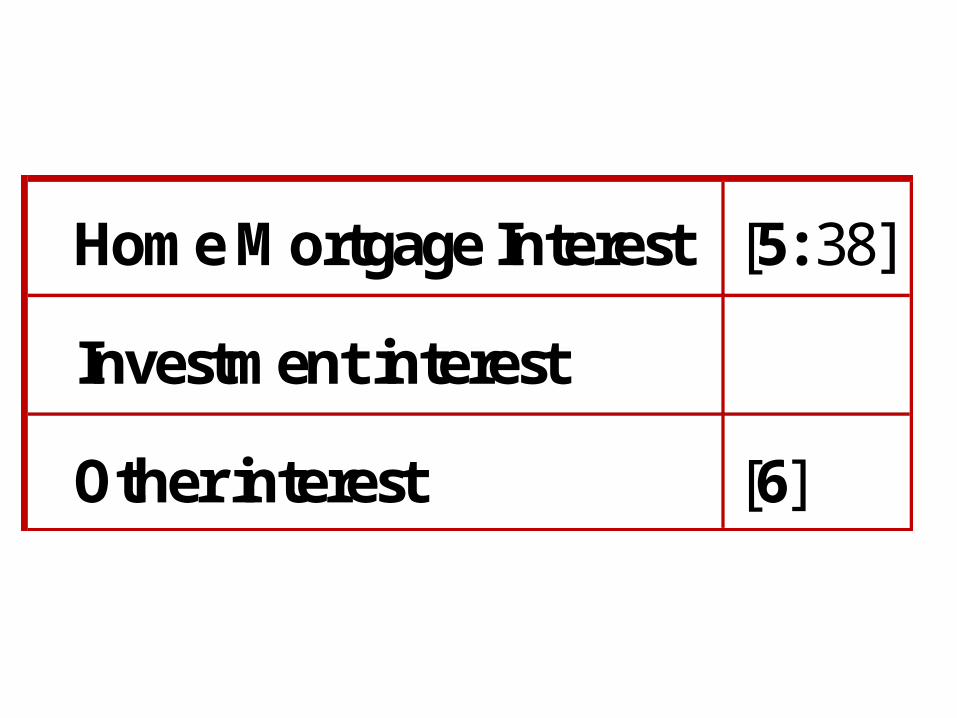

Home Mortgage Interest [5: 38]

Investment interest

Other interest [6]

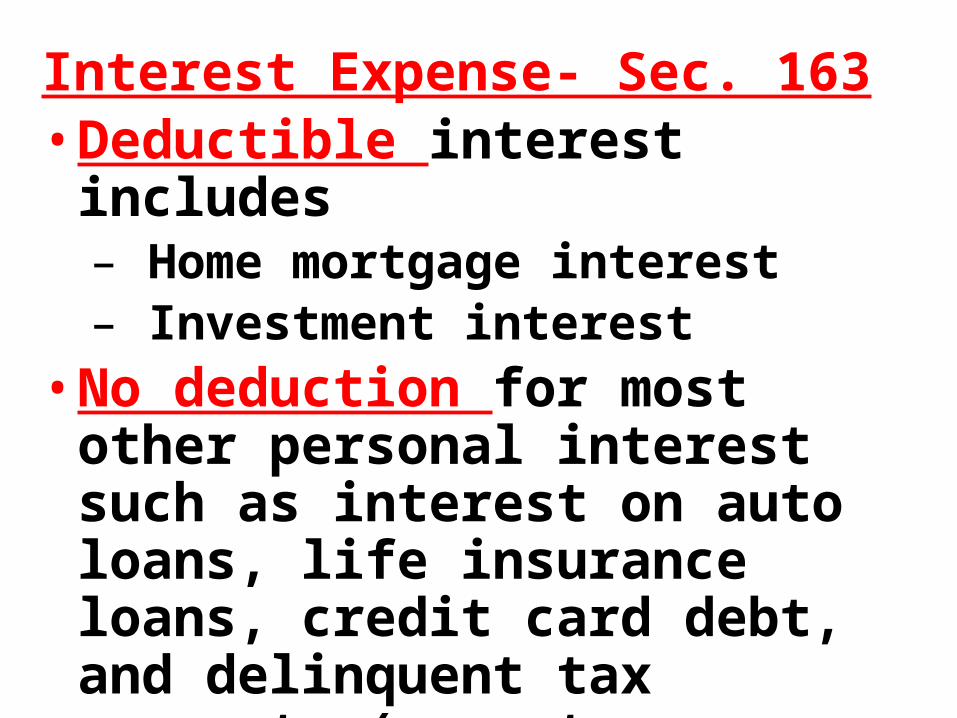

Interest Expense- Sec. 163• Deductible interest includes

– Home mortgage interest– Investment interest

• No deduction for most other personal interest such as interest on auto loans, life insurance loans, credit card debt, and delinquent tax payments (except previously mentioned student loan interest)

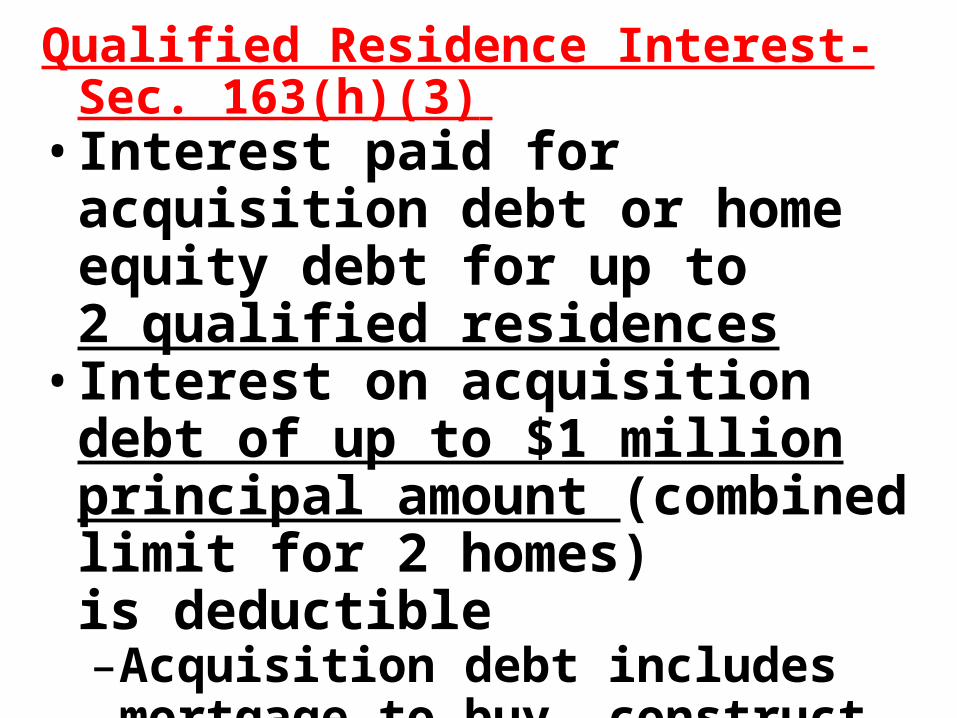

Qualified Residence Interest- Sec. 163(h)(3) • Interest paid for acquisition debt or

home equity debt for up to 2 qualified residences

• Interest on acquisition debt of up to $1 million principal amount (combined limit for 2 homes) is deductible–Acquisition debt includes mortgage to

buy, construct, or improve the residence.

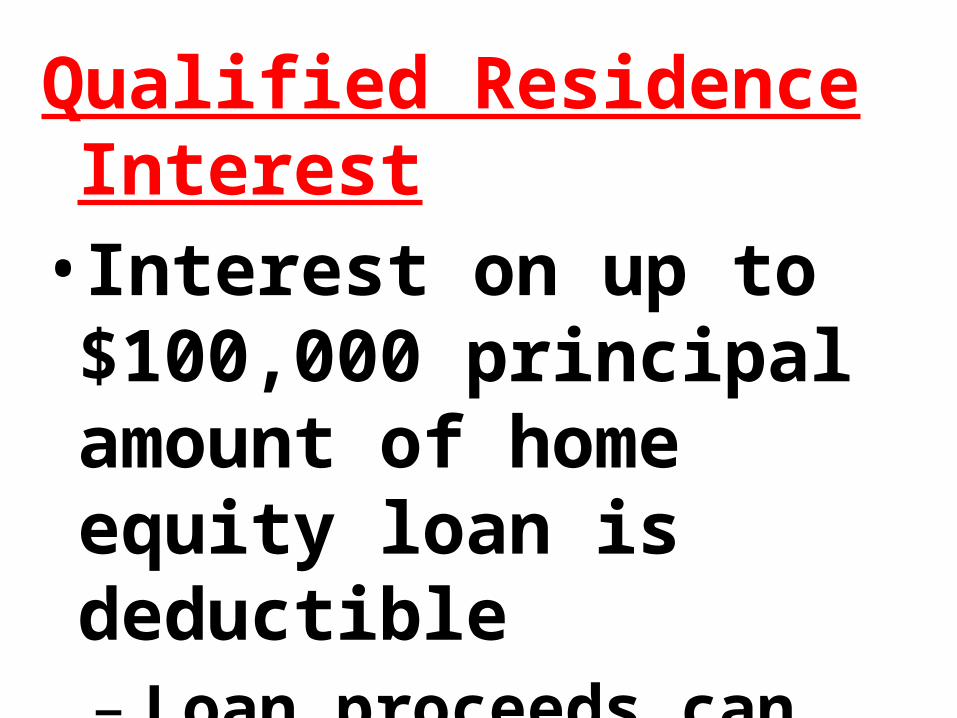

Qualified Residence Interest• Interest on up to $100,000

principal amount of home equity loan is deductible– Loan proceeds can be used

for any purpose

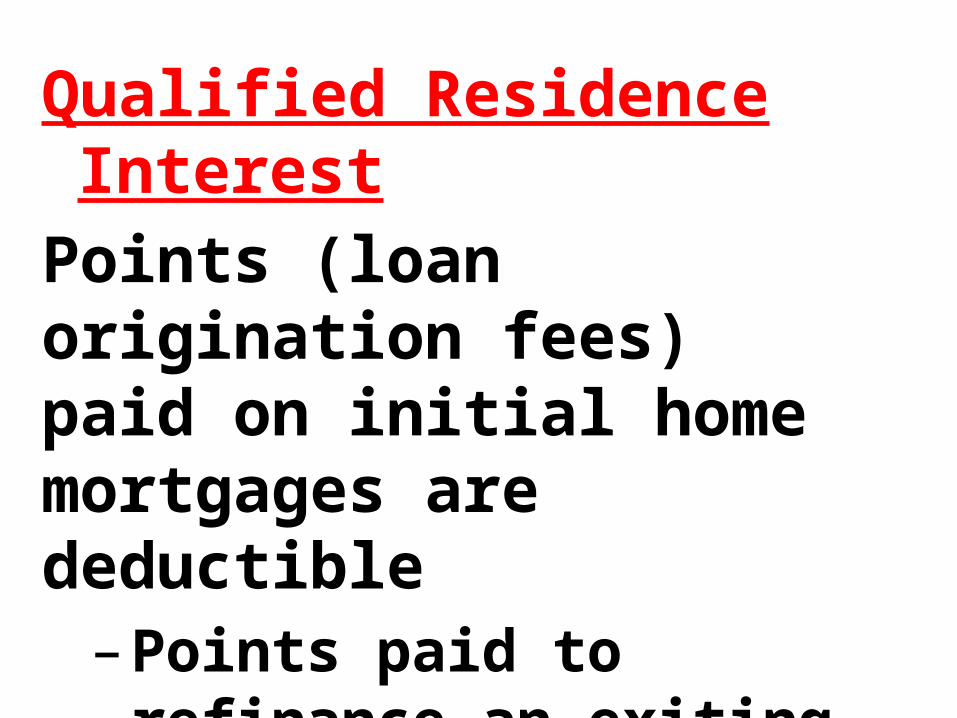

Qualified Residence InterestPoints (loan origination fees) paid on initial home mortgages are deductible

– Points paid to refinance an exiting loan must be amortized over life of loan.

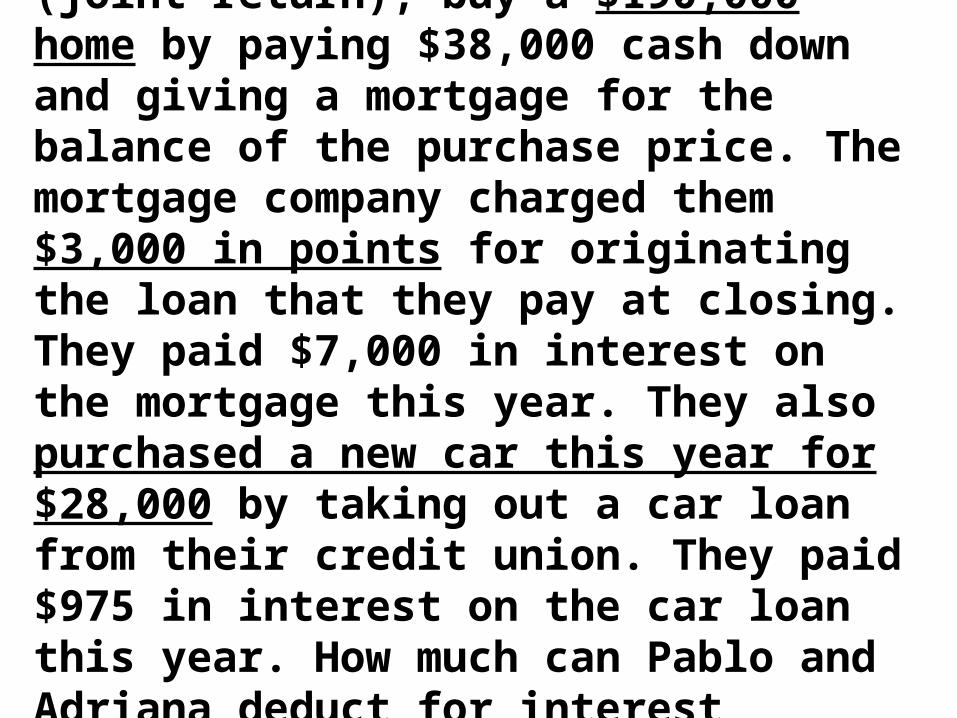

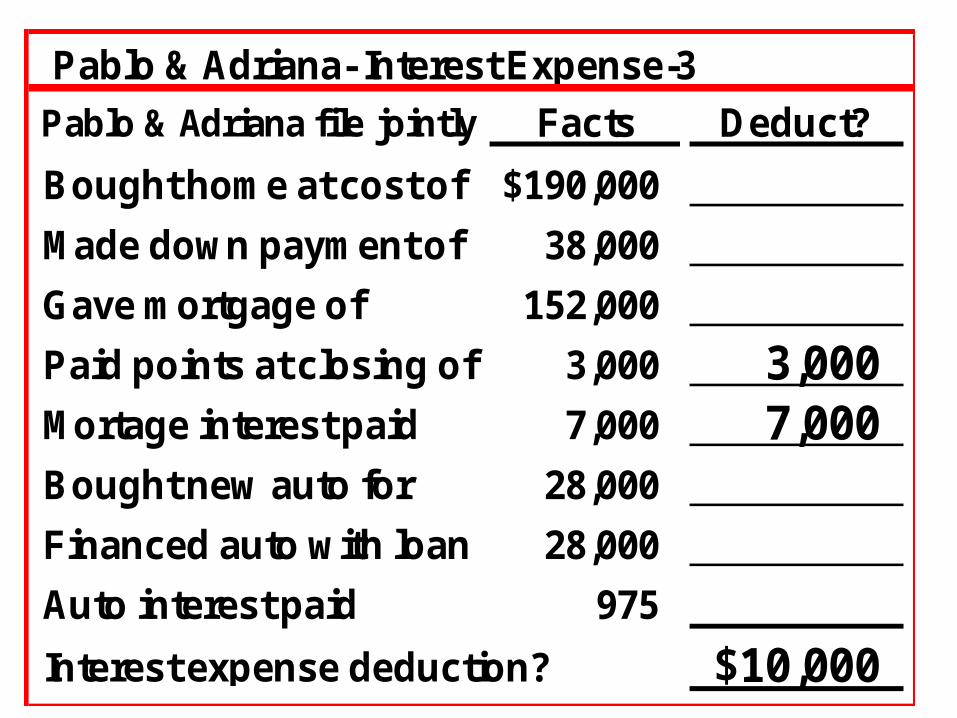

Pablo & Adriana, Interest Expense-1Pablo & Adriana, a married couple (joint return), buy a $190,000 home by paying $38,000 cash down and giving a mortgage for the balance of the purchase price. The mortgage company charged them $3,000 in points for originating the loan that they pay at closing. They paid $7,000 in interest on the mortgage this year. They also purchased a new car this year for $28,000 by taking out a car loan from their credit union. They paid $975 in interest on the car loan this year. How much can Pablo and Adriana deduct for interest expense this year if they itemize their deductions?

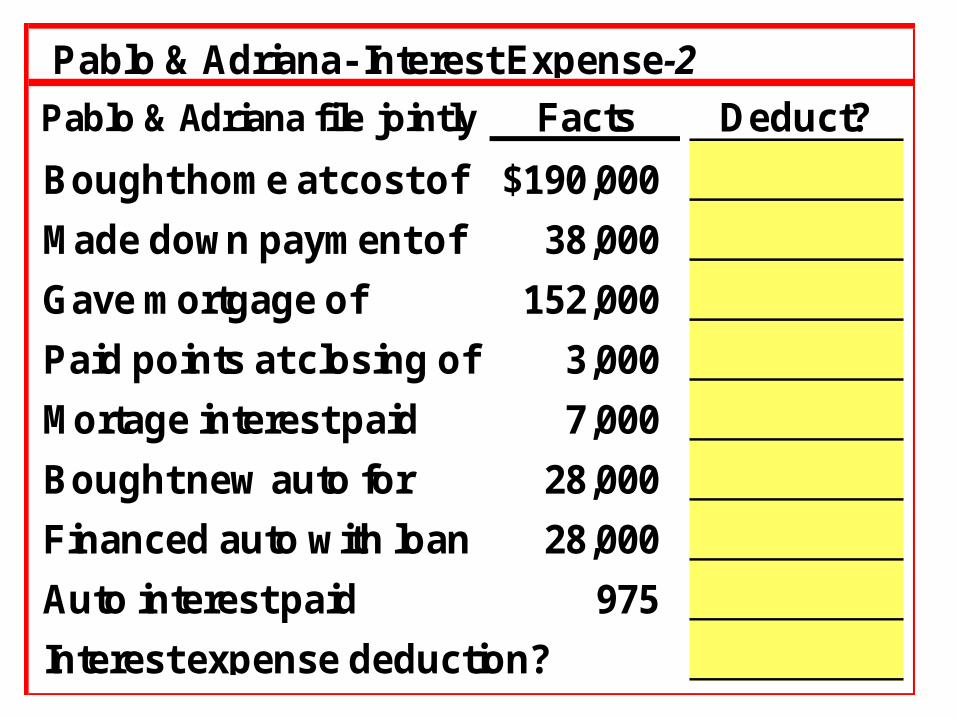

Pablo & Adriana- Interest Expense-2

Pablo & Adriana file jointly Facts Deduct?

Bought home at cost of $190,000

Made down payment of 38,000

Gave mortgage of 152,000

Paid points at closing of 3,000

Mortage interest paid 7,000

Bought new auto for 28,000

Financed auto with loan 28,000

Auto interest paid 975

Interest expense deduction?

Pablo & Adriana- Interest Expense-3

Pablo & Adriana file jointly Facts Deduct?

Bought home at cost of $190,000

Made down payment of 38,000

Gave mortgage of 152,000

Paid points at closing of 3,000 3,000 Mortage interest paid 7,000 7,000 Bought new auto for 28,000

Financed auto with loan 28,000

Auto interest paid 975

10,000$ Interest expense deduction?

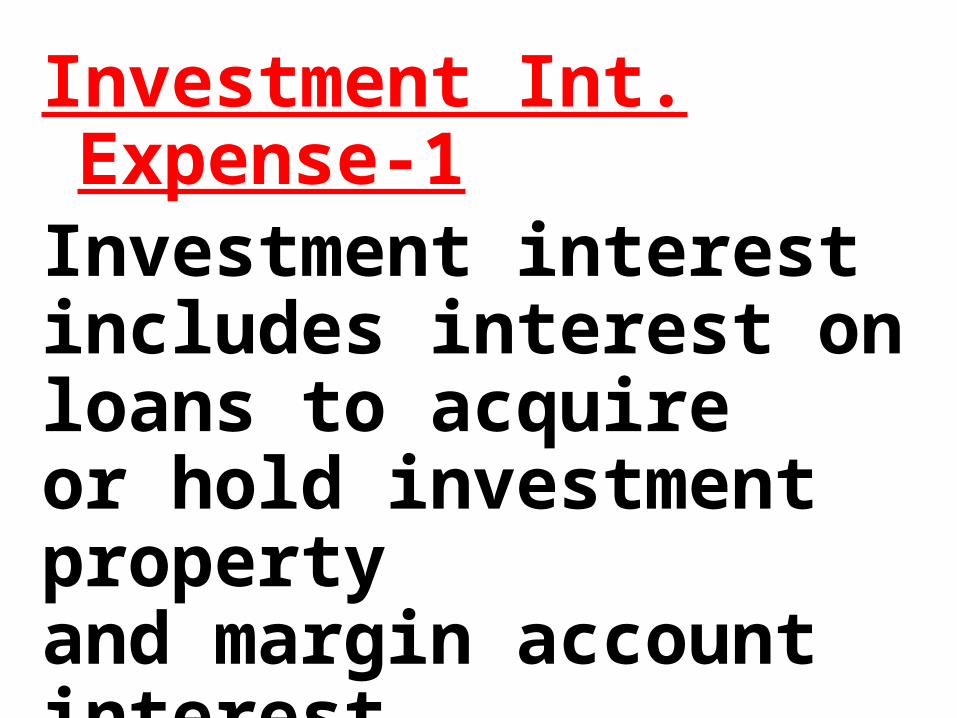

Investment Int. Expense-1Investment interest includes interest on loans to acquire or hold investment property and margin account interest paid to a broker.

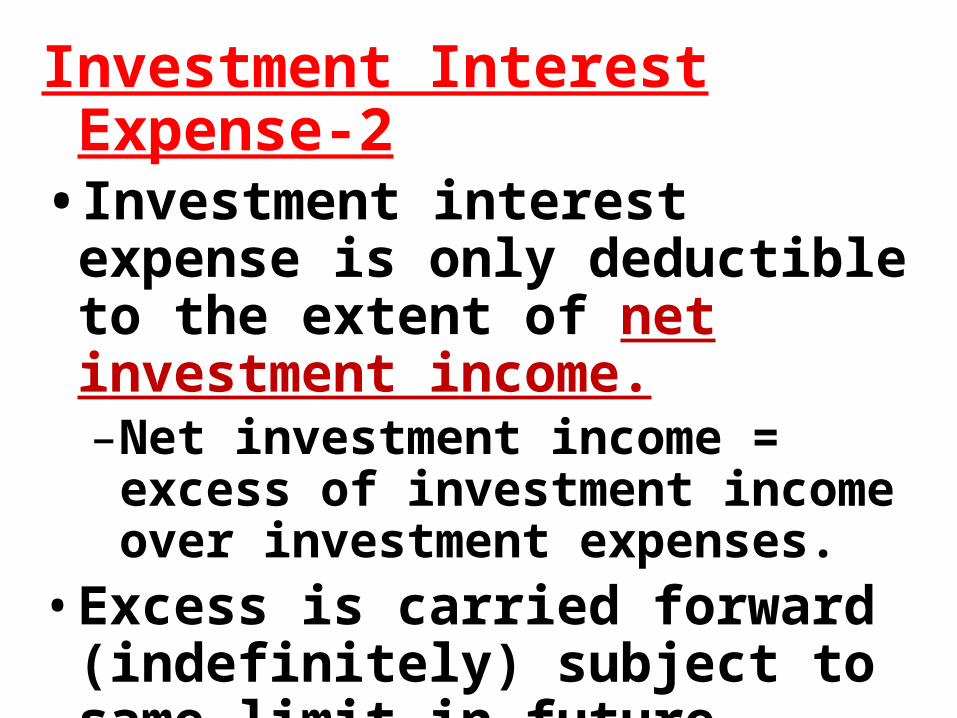

Investment Interest Expense-2• Investment interest expense is only

deductible to the extent of net investment income.–Net investment income = excess of

investment income over investment expenses.

• Excess is carried forward (indefinitely) subject to same limit in future years.

CHARITABLE

Gifts [money] [7]

CHARITABLE

Gifts [Other prop.] [8: 42]

Charitable Contributions – Sec. 170• Congress allows individuals,

corporations, estates and trusts to deduct contributions to certain qualified organizations.

• Partnerships & S corps pass the contributions through to partners and shareholders who then claim deductions on their own tax returns.

Charitable Contributions• Qualified charitable organizations

– Government units (federal, state and local government) and entities formed and operated exclusively for religious, charitable, scientific, literary or educational purposes, including churches, nonprofit hospitals, school and universities, libraries, and social service agencies

• Direct contributions to needy individuals are not deductible

Charitable Contributions•No deduction allowed to the extent that valuable goods or services are received in return for the contribution– Exception - contributors to universities

who receive preferred rights to purchase tickets for university athletic events may deduct 80% of the amount of their contribution.

This important rule is not in our text.

Charitable Contributions• Individuals can deduct up to 50% of AGI–Excess contributions may

be carried forward up to 5 years

Charitable Contributions• No deduction for contributions of the

taxpayer’s services and rent-free use of the taxpayer’s property–Out-of-pocket costs incurred for

volunteer work for a qualifying charity are deductible

• Property other than long-term capital gain property is valued at lesser of FMV or basis

Contributions of LTCG Property•LTCG property is valued at FMV (which is often greater than adjusted basis) – Tangible personalty given to a

charity which does not use the property in its tax-exempt activity is valued at the lower adjusted basis

Contributions of LTCG Property• Deduction for LTCG property valued

at FMV is limited to 30% of AGI– 30% limit can be avoided

(and 50% AGI limit applied) if taxpayer elects to use lower basis

– If made, election applies to all LTCG contributions that year

– Important rule, even though it is not in textbook. May be on the test.

Charitable Contributions• Stocks or other income producing

property that have declined in value should be sold, so that the loss can be claimed with the sale proceeds donated

• Fees incurred for appraisals of donated property may be deducted as a misc. itemized deductions

• Deduction for donated vehicles sold by charity limited to gross sales proceeds

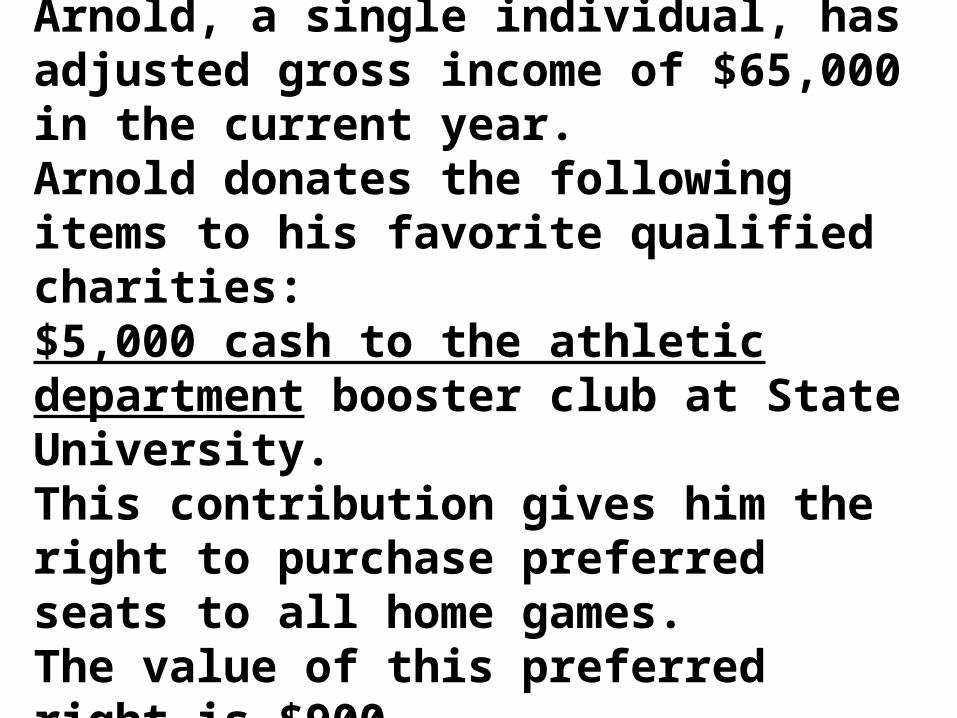

Arnold - Charitable Contributions-1Arnold, a single individual, has adjusted gross income of $65,000 in the current year. Arnold donates the following items to his favorite qualified charities:$5,000 cash to the athletic department booster club at State University. This contribution gives him the right to purchase preferred seats to all home games. The value of this preferred right is $900.Continued on next slide

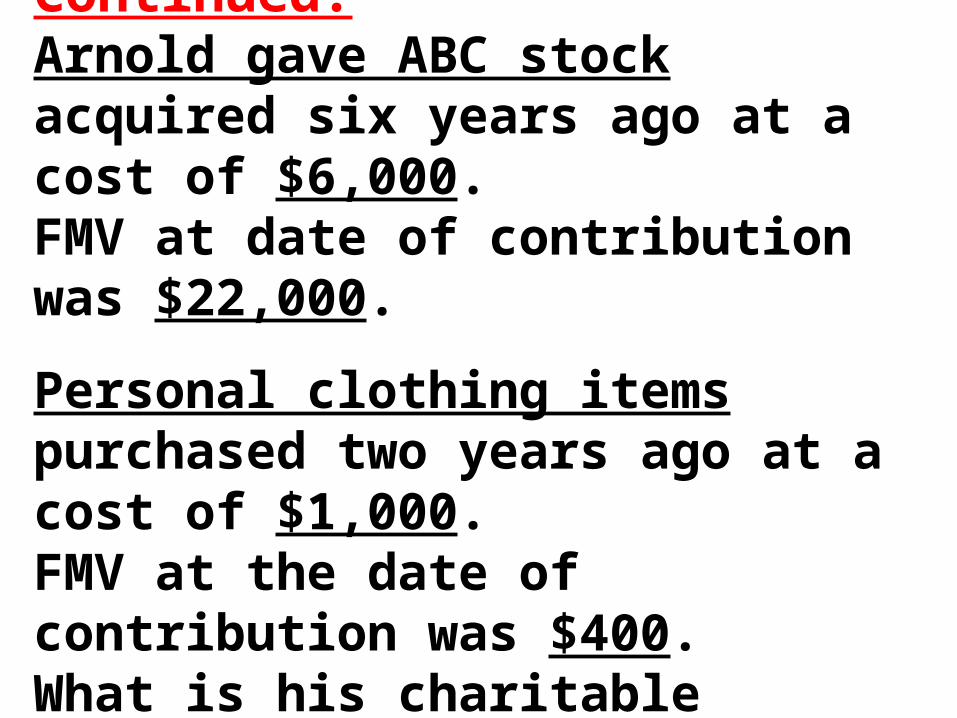

Arnold - Charitable Contributions-2Continued.Arnold gave ABC stock acquired six years ago at a cost of $6,000. FMV at date of contribution was $22,000.

Personal clothing items purchased two years ago at a cost of $1,000. FMV at the date of contribution was $400.What is his charitable contribution deduction for the current year?

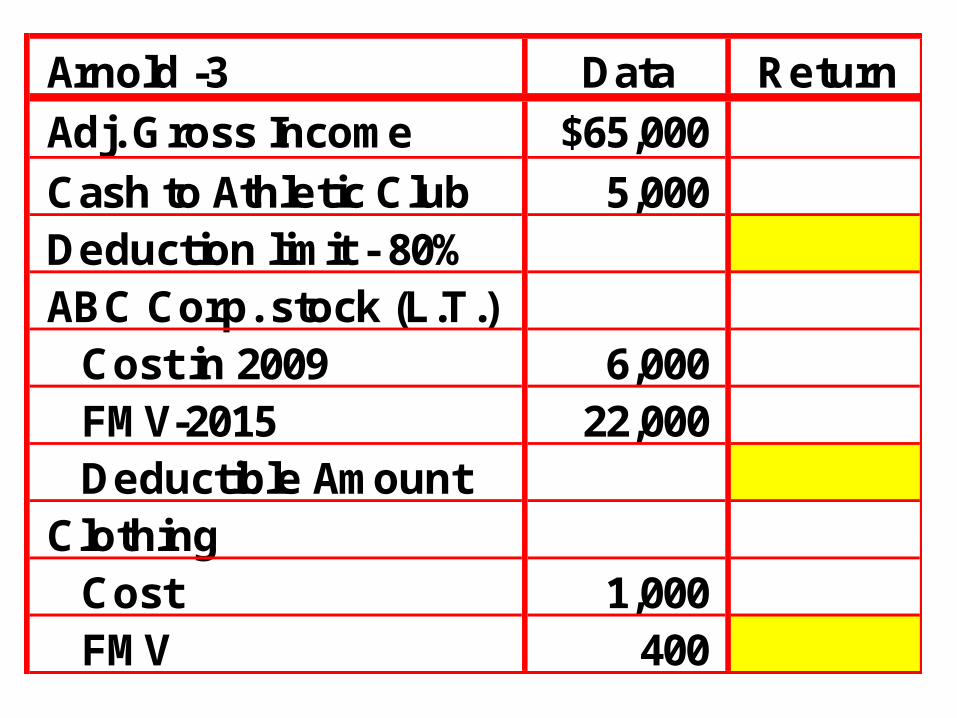

Arnold -3 Data Return

Adj. Gross Income $65,000

Cash to Athletic Club 5,000Deduction limit - 80%ABC Corp. stock (L.T.)

Cost in 2009 6,000FMV-2015 22,000Deductible Amount

ClothingCost 1,000FMV 400

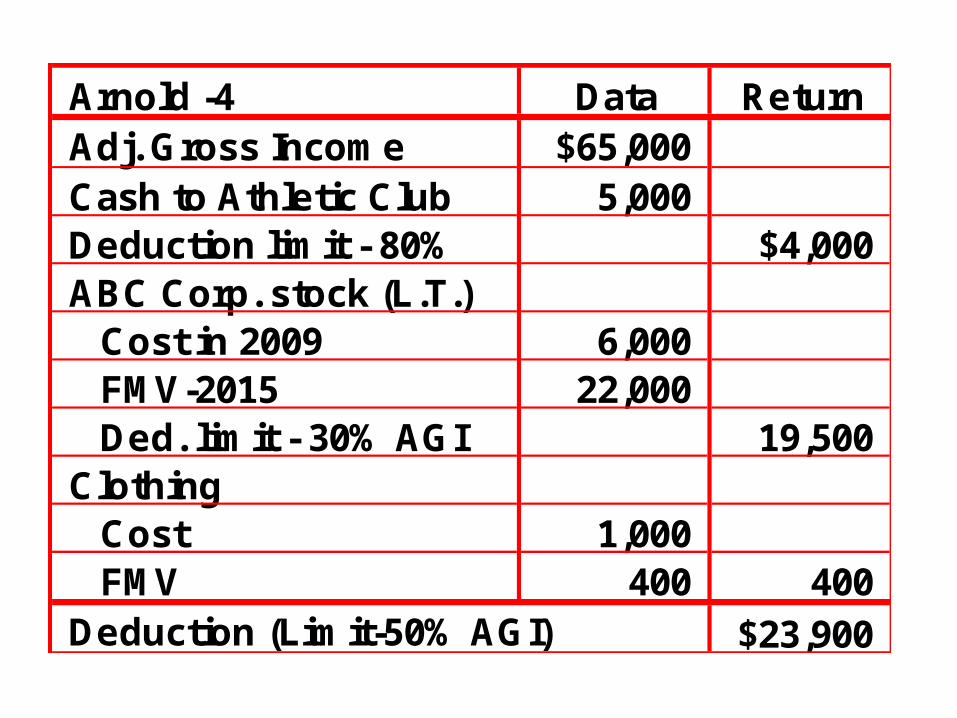

Arnold -4 Data ReturnAdj. Gross Income $65,000Cash to Athletic Club 5,000Deduction limit - 80% $4,000ABC Corp. stock (L.T.)

Cost in 2009 6,000FMV-2015 22,000Ded. limit - 30% AGI 19,500

ClothingCost 1,000FMV 400 400

$23,900Deduction (Limit-50% AGI)

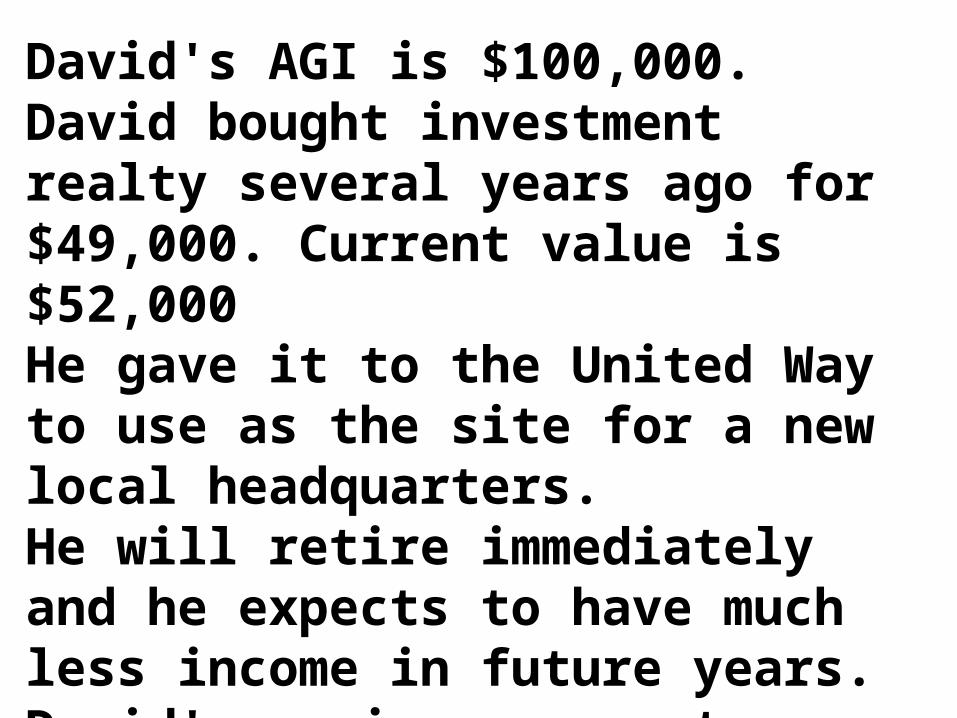

David's AGI is $100,000. David bought investment realty several years ago for $49,000. Current value is $52,000 He gave it to the United Way to use as the site for a new local headquarters. He will retire immediately and he expects to have much less income in future years.David's maximum current year contribution deduction is:a. $30,000 b. $49,000 c. $50,000 d. $52,000

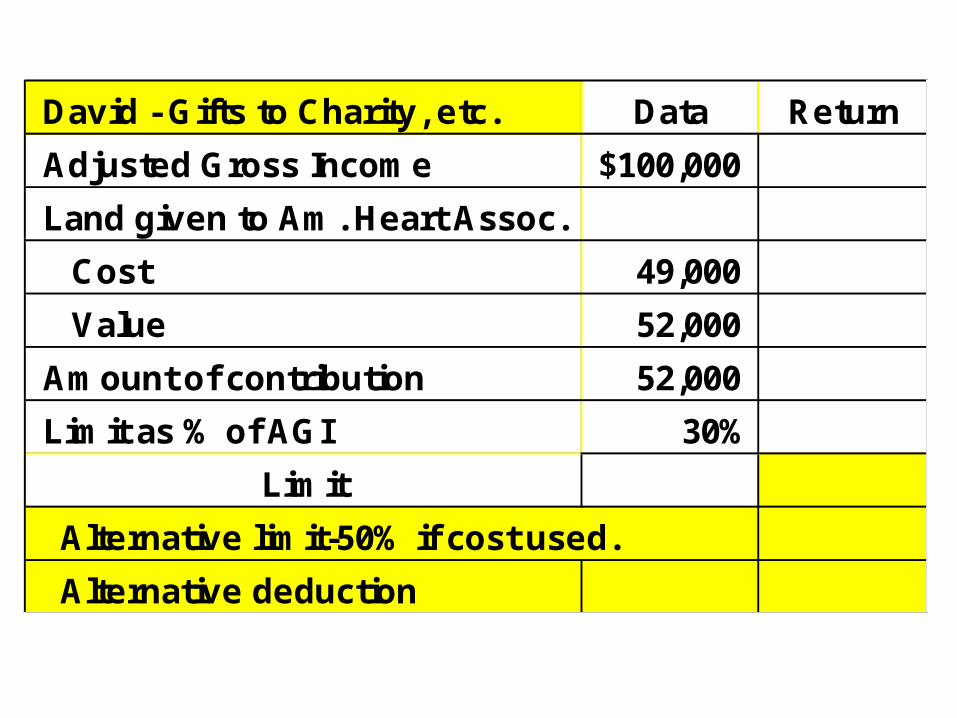

David - Gifts to Charity, etc. Data Return

Adjusted Gross Income $100,000

Land given to Am. Heart Assoc.

Cost 49,000

Value 52,000

Amount of contribution 52,000

Limit as % of AGI 30%

Limit

Alternative limit-50% if cost used.

Alternative deduction

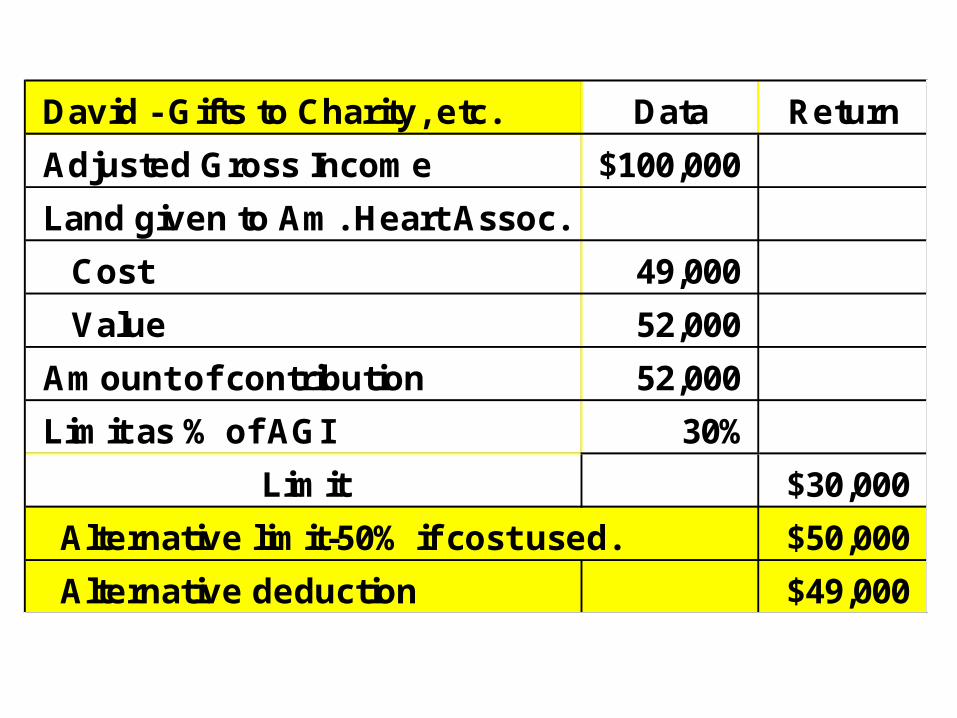

David - Gifts to Charity, etc. Data Return

Adjusted Gross Income $100,000

Land given to Am. Heart Assoc.

Cost 49,000

Value 52,000

Amount of contribution 52,000

Limit as % of AGI 30%

Limit $30,000

Alternative limit-50% if cost used. $50,000

Alternative deduction $49,000

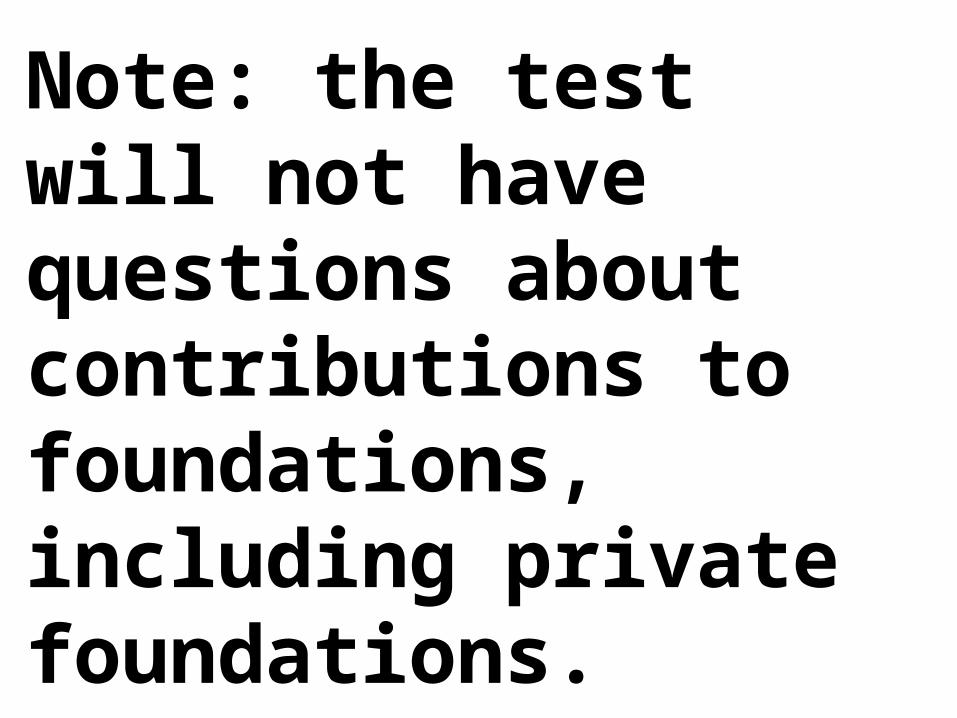

Note: the test will not have questions about contributions to foundations, including private foundations.

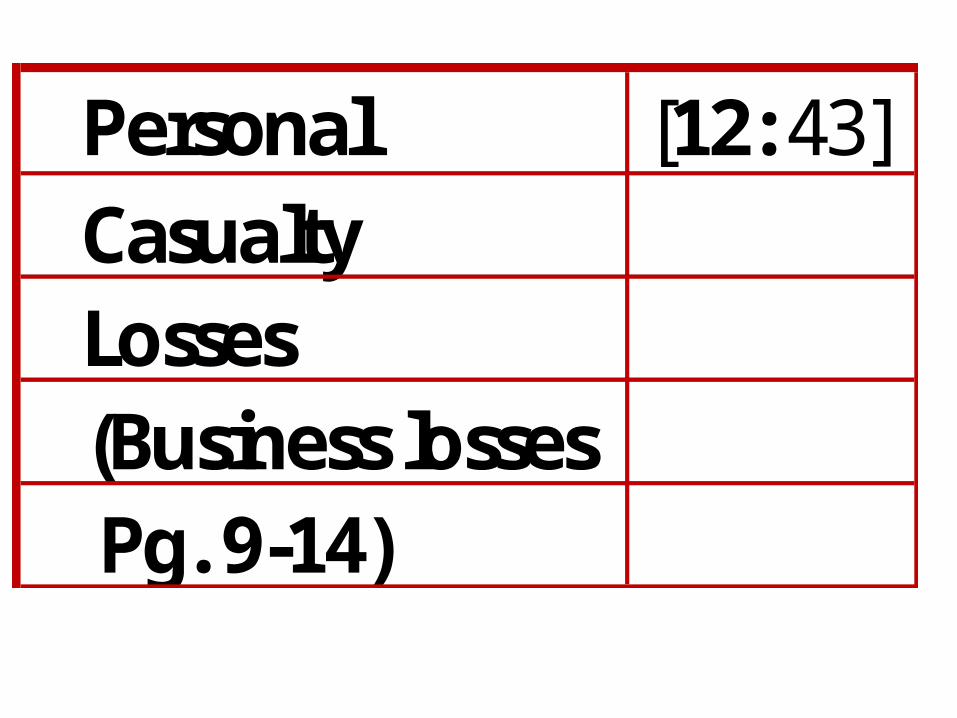

Personal [12: 43]Casualty Losses (Business losses Pg. 9-14)

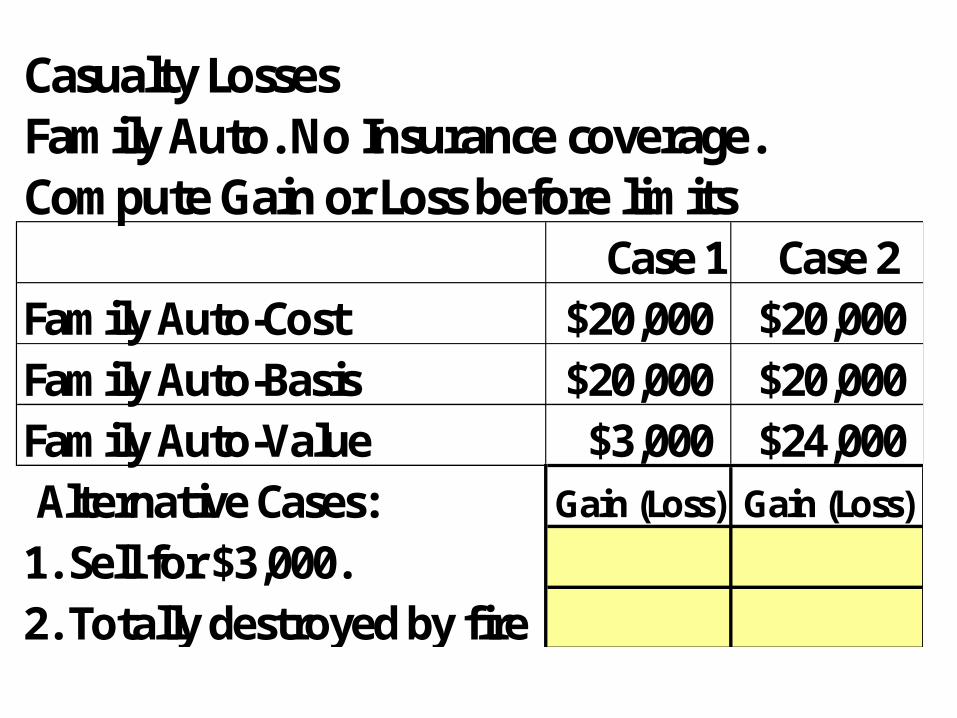

Casualty LossesFamily Auto. No Insurance coverage.Compute Gain or Loss before limits

Case 1 Case 2Family Auto-Cost $20,000 $20,000Family Auto-Basis $20,000 $20,000Family Auto-Value $3,000 $24,000Alternative Cases: Gain (Loss) Gain (Loss)

1. Sell for $3,000.2. Totally destroyed by fire

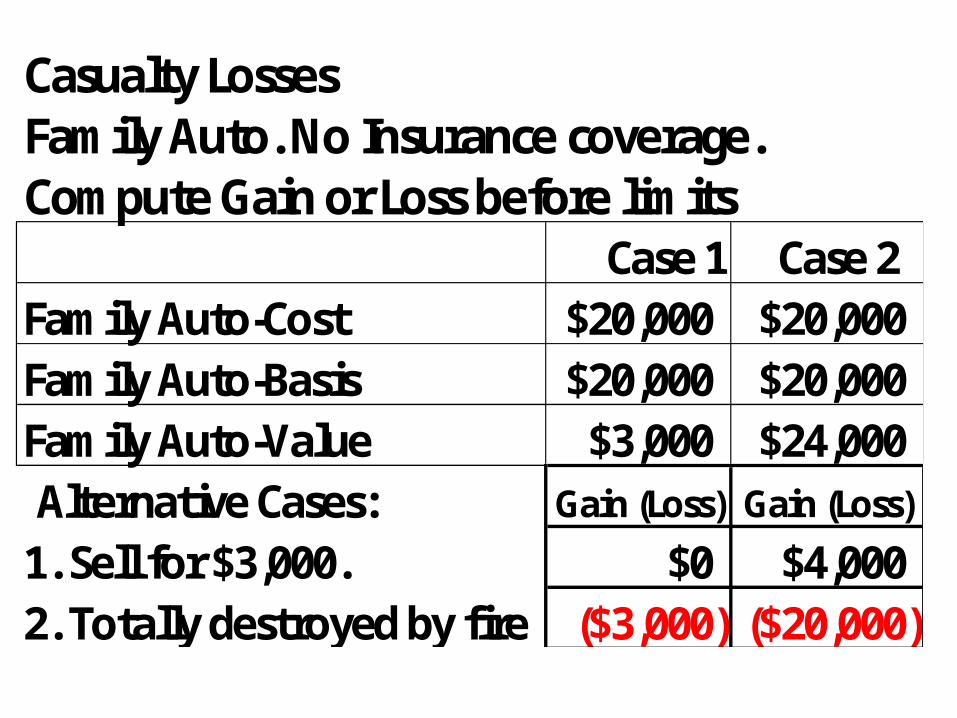

Casualty LossesFamily Auto. No Insurance coverage.Compute Gain or Loss before limits

Case 1 Case 2Family Auto-Cost $20,000 $20,000Family Auto-Basis $20,000 $20,000Family Auto-Value $3,000 $24,000Alternative Cases: Gain (Loss) Gain (Loss)

1. Sell for $3,000. $0 $4,0002. Totally destroyed by fire ($3,000) ($20,000)

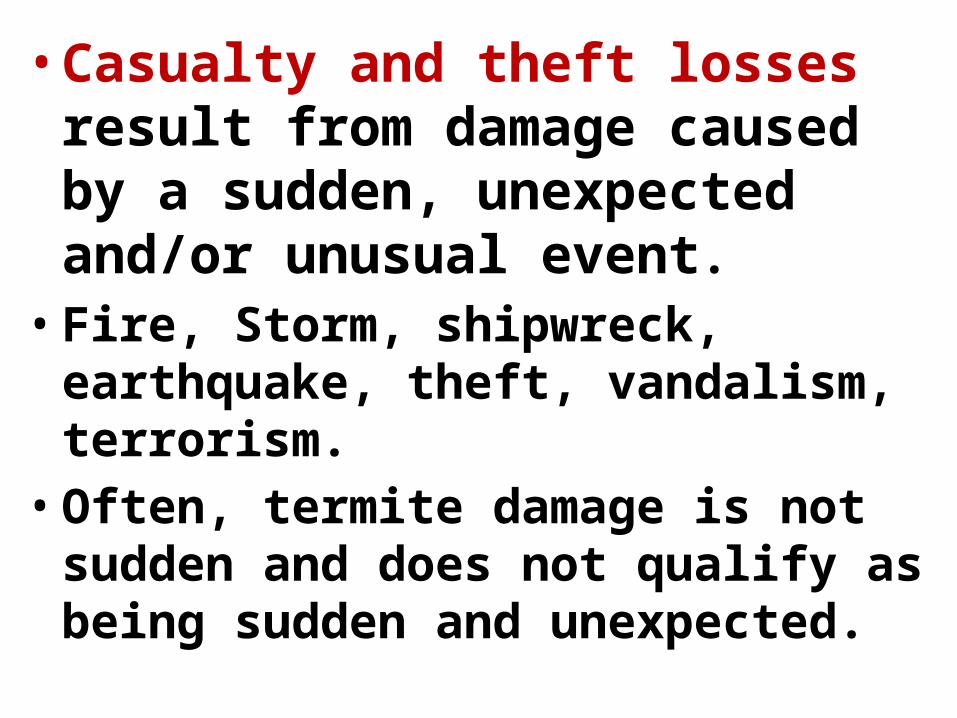

• Casualty and theft losses result from damage caused by a sudden, unexpected and/or unusual event.

• Fire, Storm, shipwreck, earthquake, theft, vandalism, terrorism.

• Often, termite damage is not sudden and does not qualify as being sudden and unexpected.

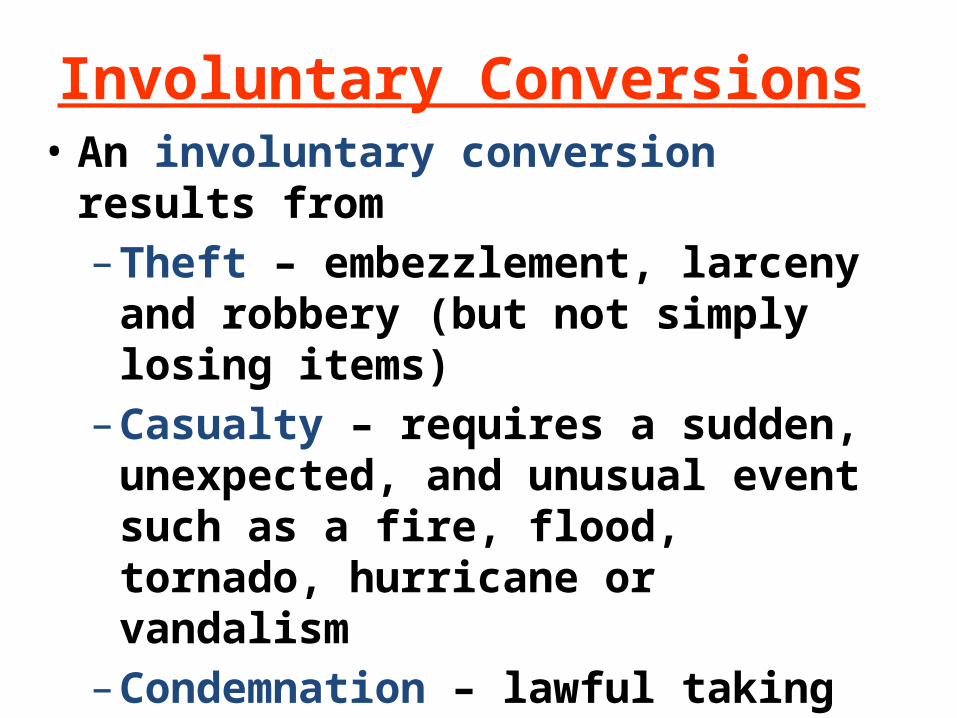

Involuntary Conversions • An involuntary conversion results from

– Theft – embezzlement, larceny and robbery (but not simply losing items)

– Casualty – requires a sudden, unexpected, and unusual event such as a fire, flood, tornado, hurricane or vandalism

– Condemnation – lawful taking of property for its fair market value by a government under the right of eminent domain

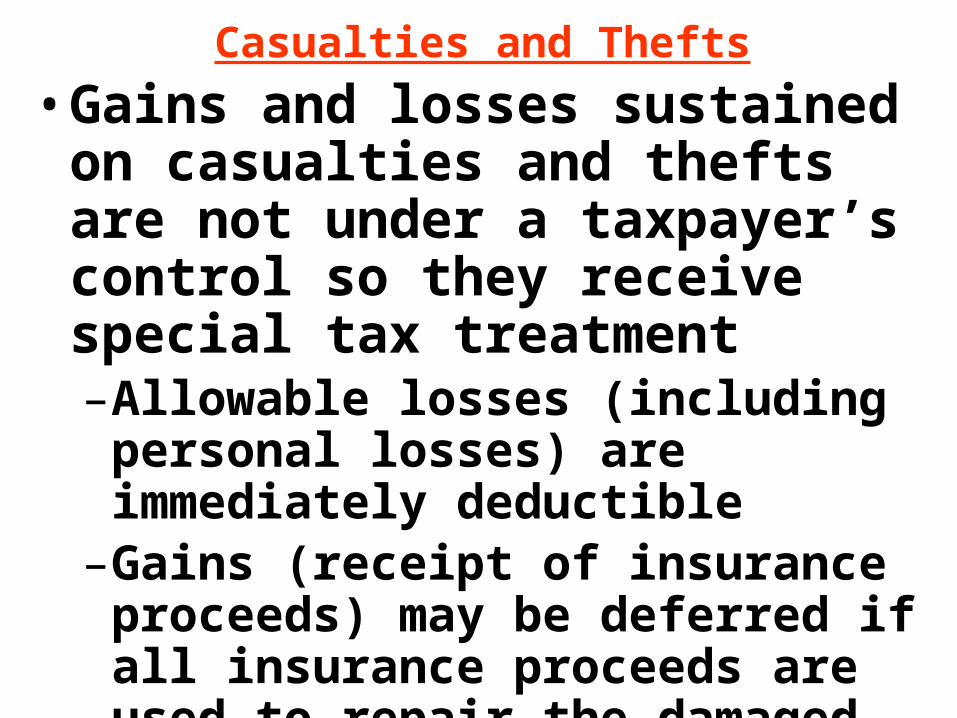

Casualties and Thefts• Gains and losses sustained on

casualties and thefts are not under a taxpayer’s control so they receive special tax treatment–Allowable losses (including personal

losses) are immediately deductible–Gains (receipt of insurance proceeds)

may be deferred if all insurance proceeds are used to repair the damaged property or to acquire qualifying replacement property (see later chapter)

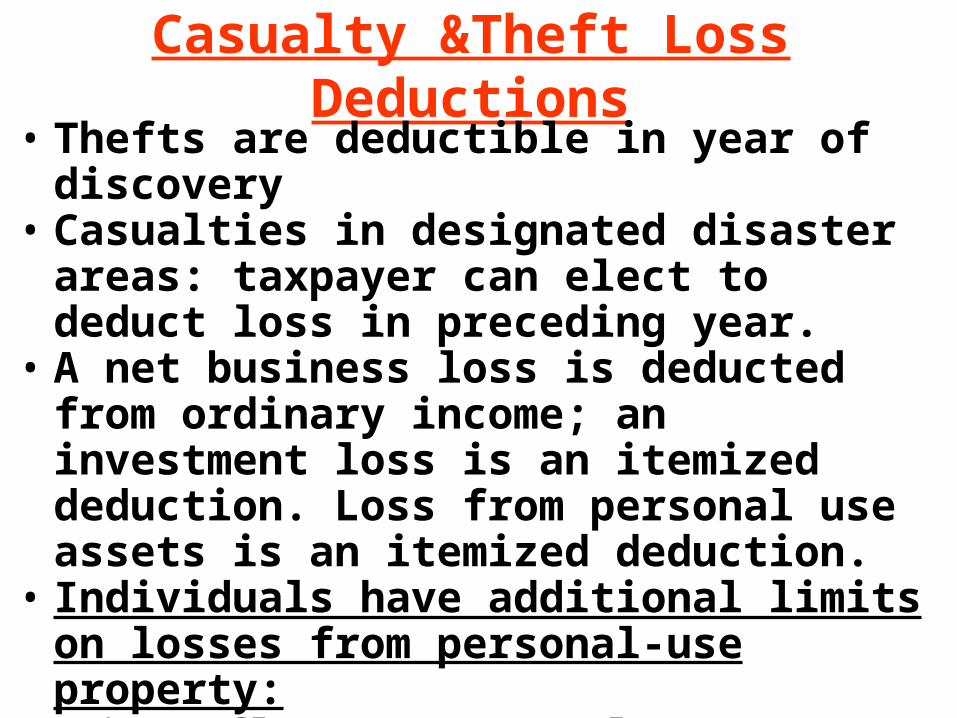

Casualty &Theft Loss Deductions• Thefts are deductible in year of discovery• Casualties in designated disaster areas: taxpayer

can elect to deduct loss in preceding year.• A net business loss is deducted from ordinary

income; an investment loss is an itemized deduction. Loss from personal use assets is an itemized deduction.

• Individuals have additional limits on losses from personal-use property:– $100 floor per casualty (per event) – 10% of AGI threshold– Must itemize to deduct the loss

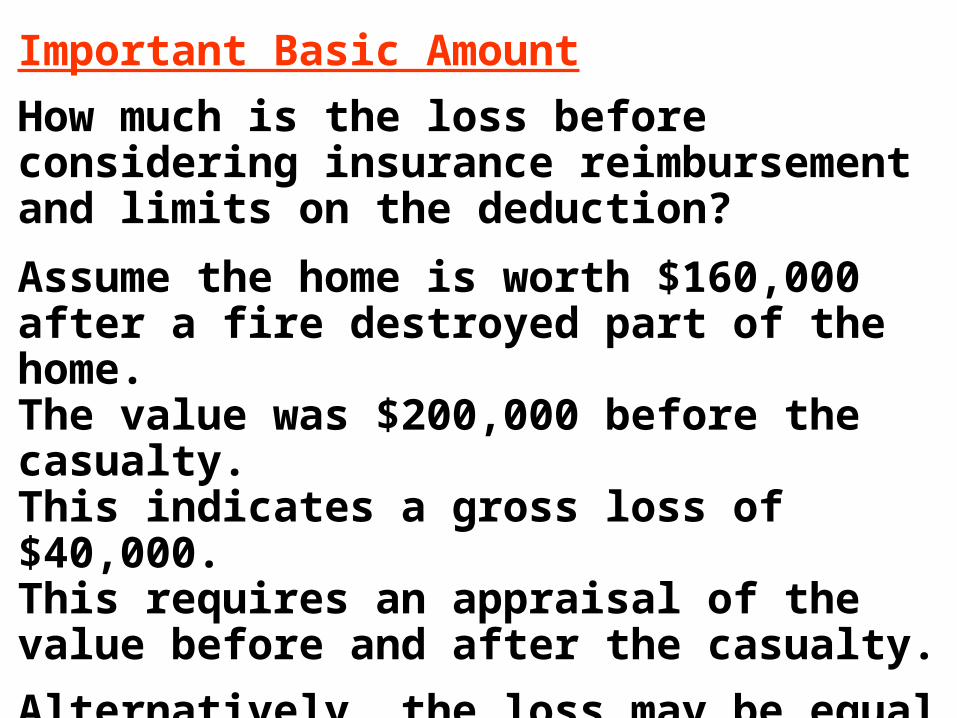

Important Basic Amount

How much is the loss before considering insurance reimbursement and limits on the deduction?

Assume the home is worth $160,000 after a fire destroyed part of the home.The value was $200,000 before the casualty.This indicates a gross loss of $40,000.This requires an appraisal of the value before and after the casualty.

Alternatively, the loss may be equal to the cost of repairs that return the property to its condition before the fire.

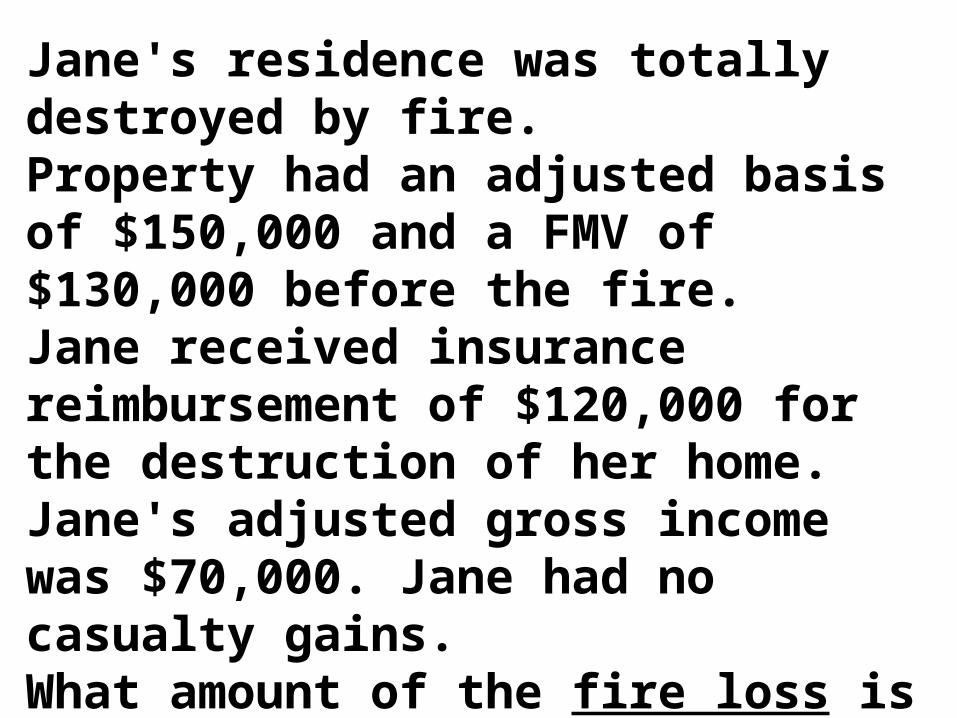

Jane's residence was totally destroyed by fire. Property had an adjusted basis of $150,000 and a FMV of $130,000 before the fire. Jane received insurance reimbursement of $120,000 for the destruction of her home. Jane's adjusted gross income was $70,000. Jane had no casualty gains. What amount of the fire loss is Jane entitled to claim as an itemized deduction on her tax return?

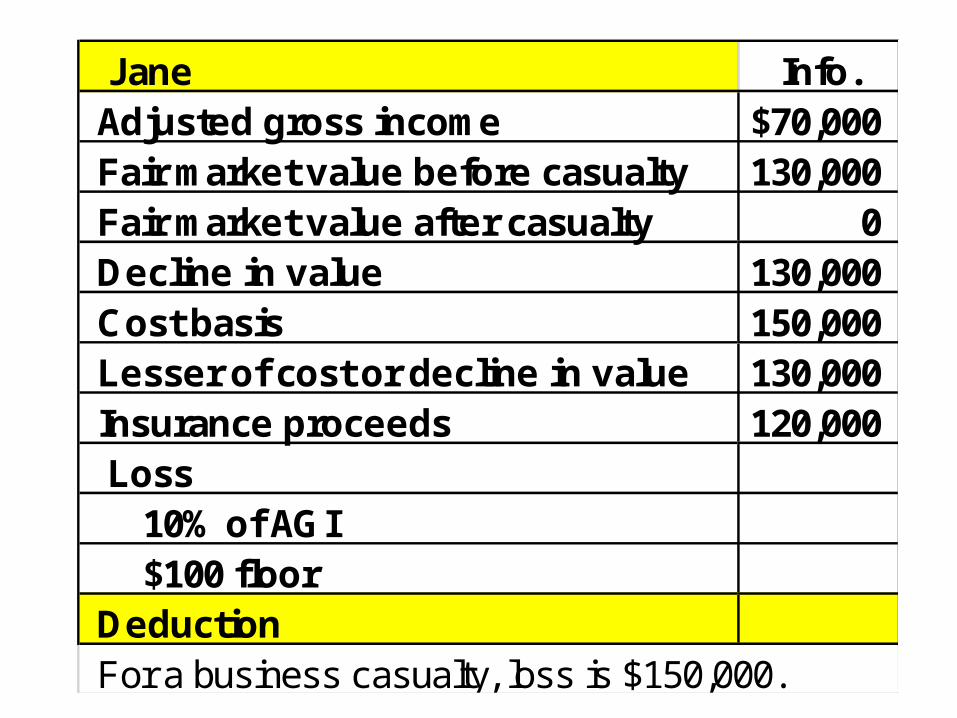

Jane Info.Adjusted gross income $70,000Fair market value before casualty 130,000Fair market value after casualty 0Decline in value 130,000Cost basis 150,000Lesser of cost or decline in value 130,000Insurance proceeds 120,000Loss

10% of AGI$100 floor

DeductionFor a business casualty, loss is $150,000.

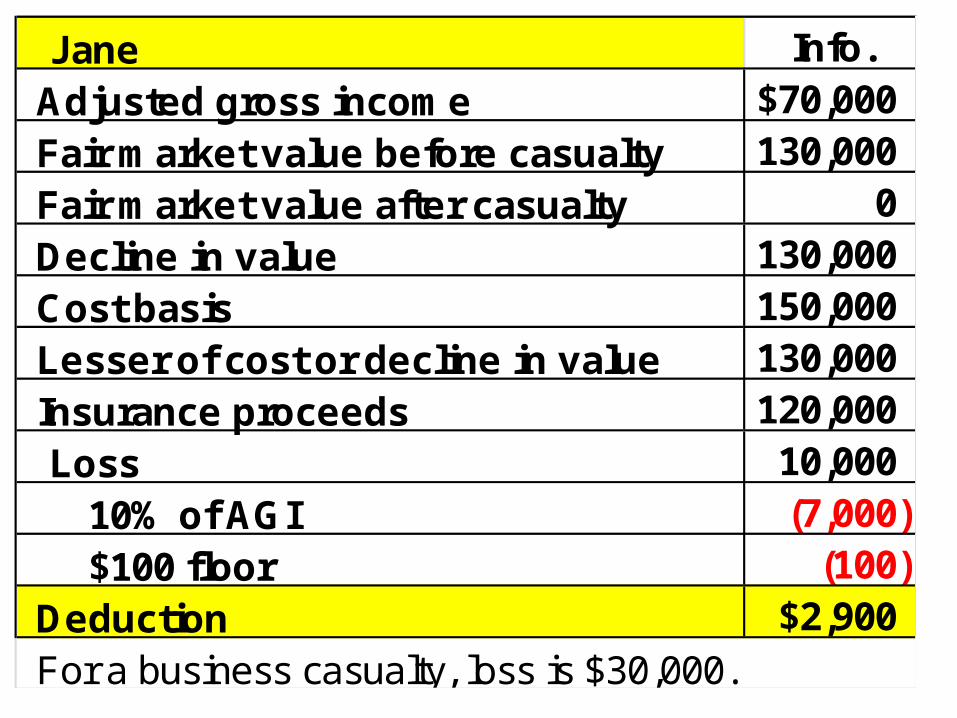

Jane Info.Adjusted gross income $70,000Fair market value before casualty 130,000Fair market value after casualty 0Decline in value 130,000Cost basis 150,000Lesser of cost or decline in value 130,000Insurance proceeds 120,000Loss 10,000

10% of AGI (7,000)$100 floor (100)

Deduction $2,900For a business casualty, loss is $30,000.

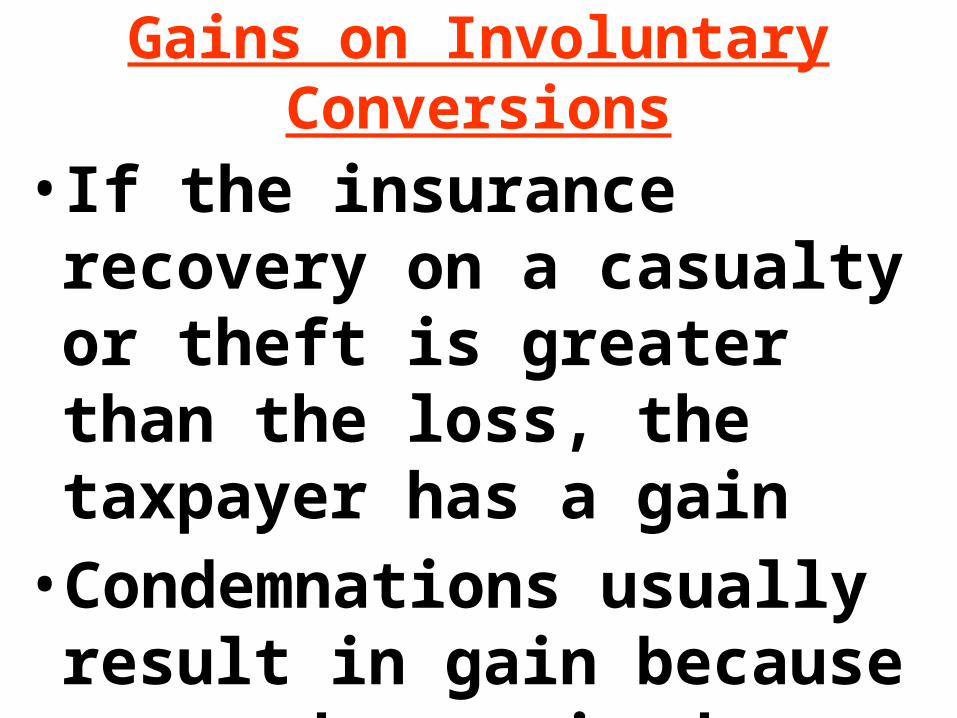

Gains on Involuntary Conversions

• If the insurance recovery on a casualty or theft is greater than the loss, the taxpayer has a gain

• Condemnations usually result in gain because proceeds received are usually fair market value

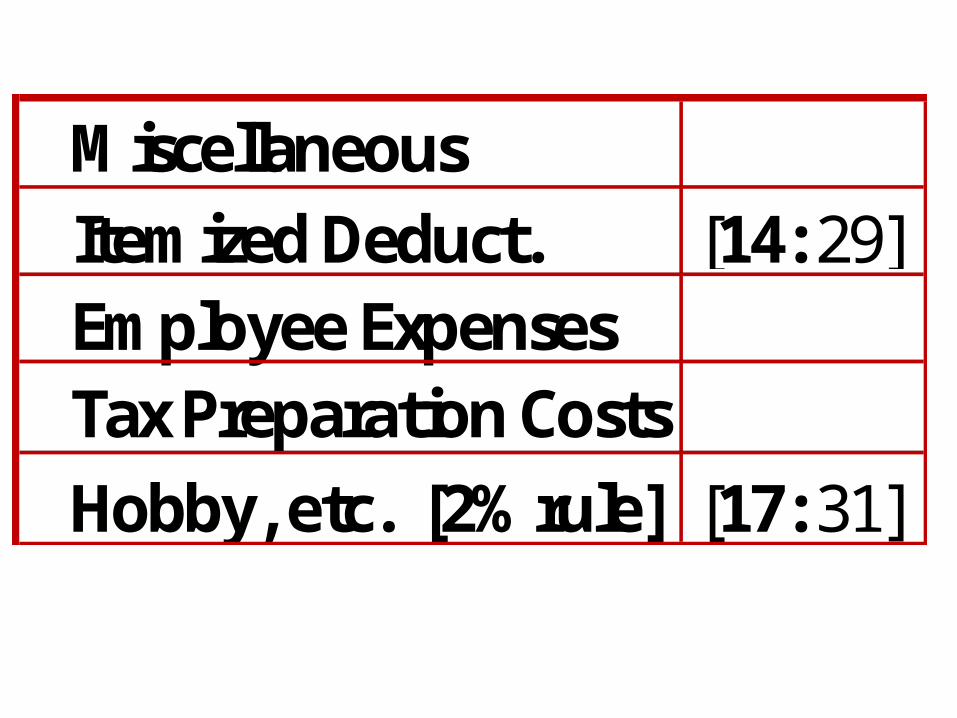

MiscellaneousItemized Deduct. [14: 29]Employee ExpensesTax Preparation Costs

Hobby, etc. [2% rule] [17: 31]

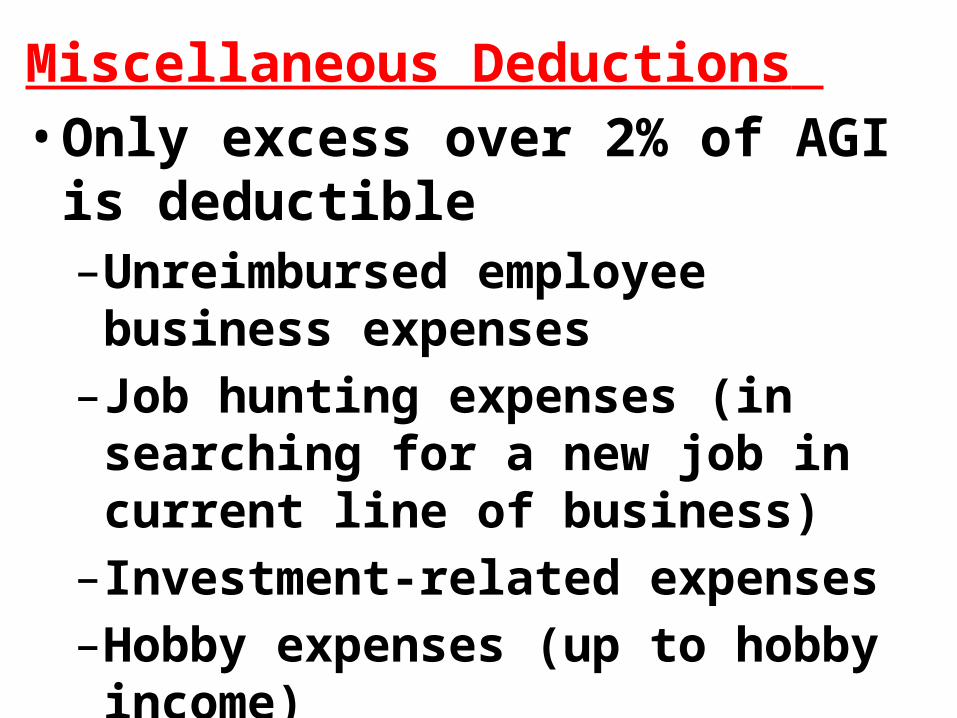

Miscellaneous Deductions • Only excess over 2% of AGI is

deductible–Unreimbursed employee business

expenses–Job hunting expenses (in searching for a

new job in current line of business)–Investment-related expenses–Hobby expenses (up to hobby income)–Tax preparation and planning advice

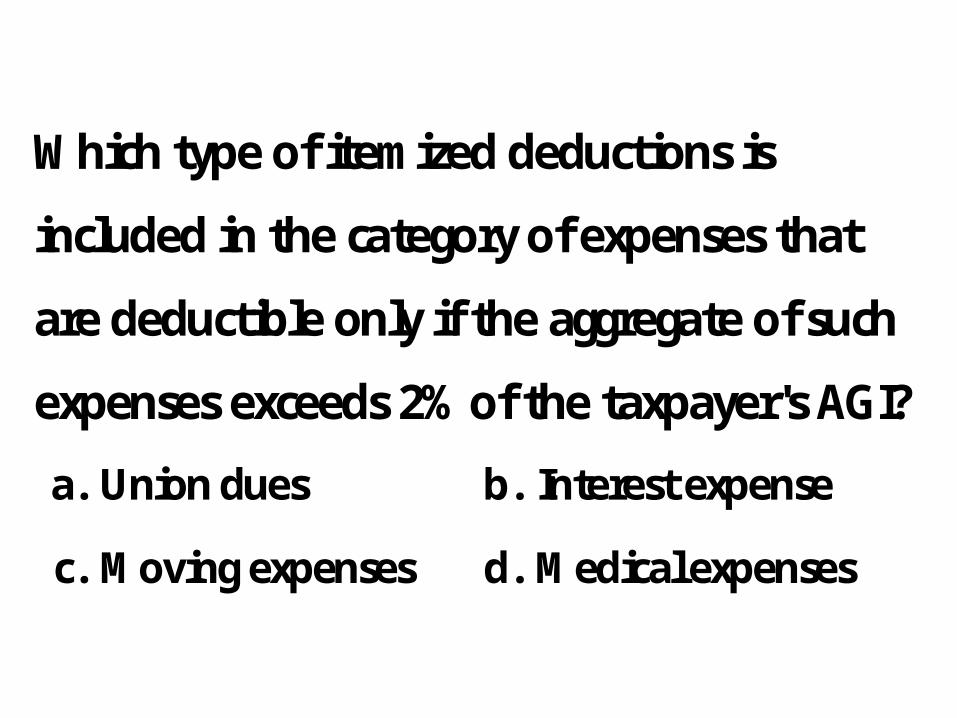

Which type of itemized deductions is

included in the category of expenses that

are deductible only if the aggregate of such

expenses exceeds 2% of the taxpayer's AGI?

a. Union dues b. Interest expense

c. Moving expenses d. Medical expenses

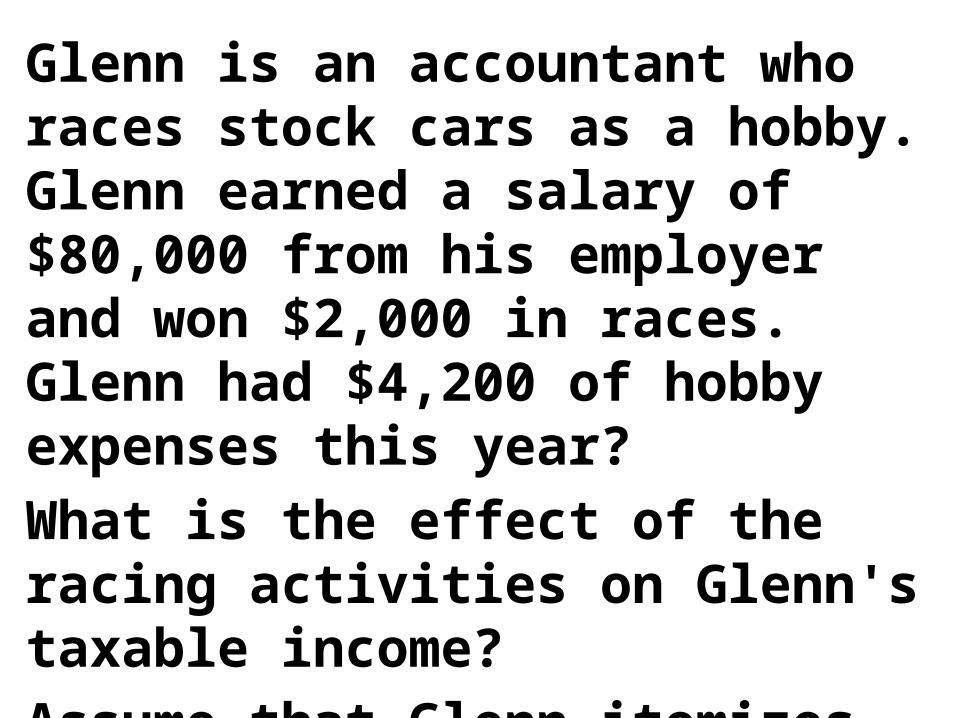

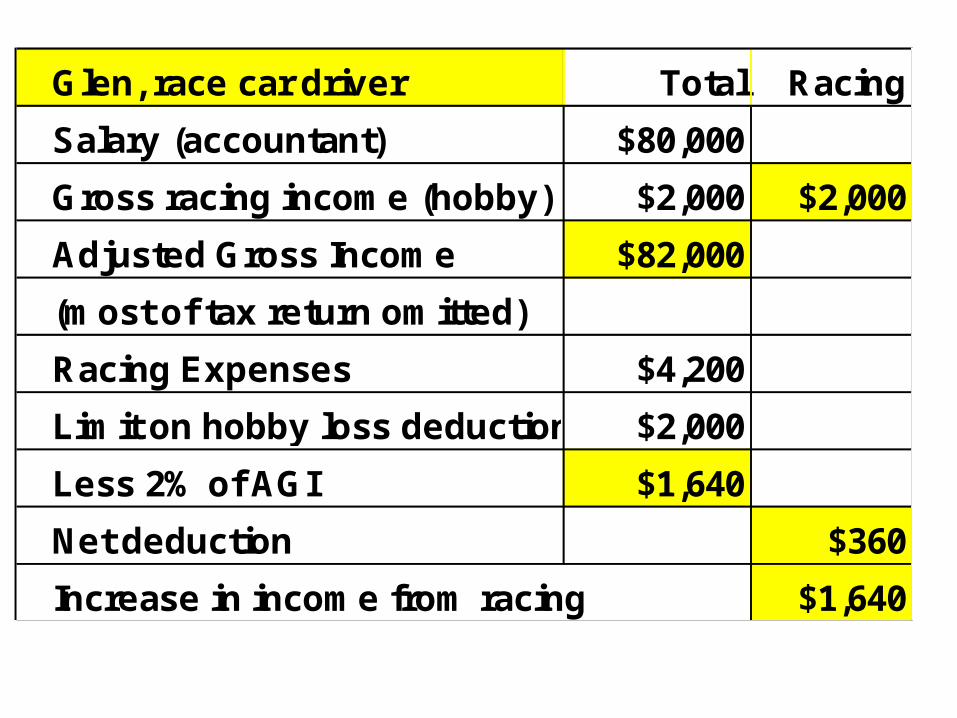

Glenn is an accountant who races stock cars as a hobby. Glenn earned a salary of $80,000 from his employer and won $2,000 in races. Glenn had $4,200 of hobby expenses this year? What is the effect of the racing activities on Glenn's taxable income?Assume that Glenn itemizes his deductions but has no other miscellaneous itemized deductions.

Glen, race car driver Total Racing

Salary (accountant) $80,000

Gross racing income (hobby) $2,000 $2,000

Adjusted Gross Income $82,000

(most of tax return omitted)

Racing Expenses $4,200

Limit on hobby loss deduction $2,000

Less 2% of AGI $1,640

Net deduction $360

Increase in income from racing $1,640

Itemized Deduction

PHASE-OUT [20: 50]

Standard Deduction [22: 48]

Exemption

PHASE-OUT [24: 51]

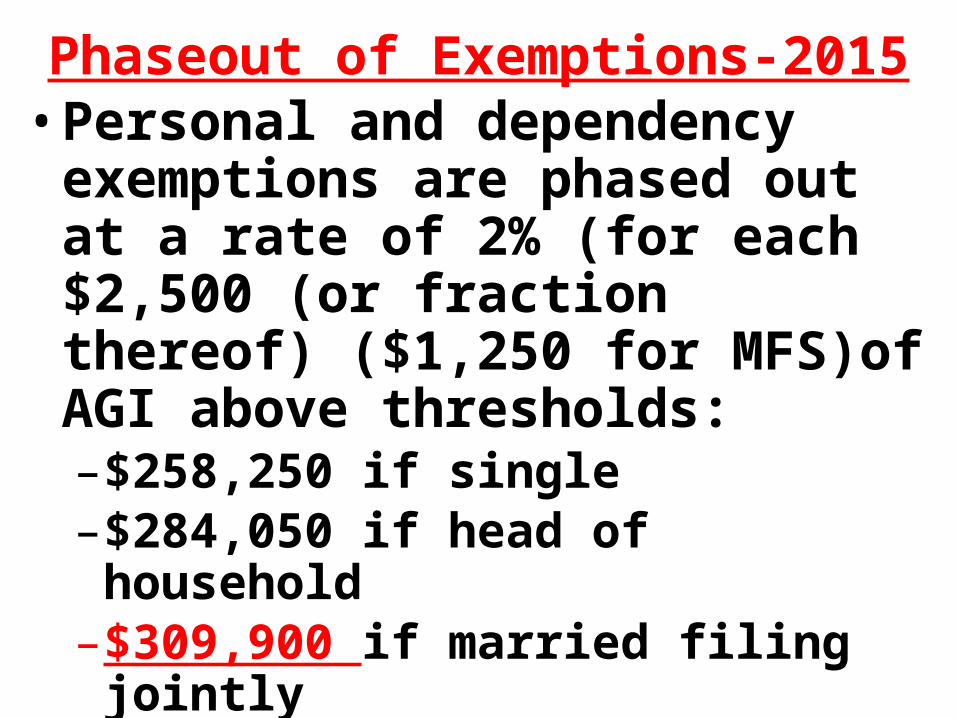

Phaseout of Exemptions-2015• Personal and dependency exemptions

are phased out at a rate of 2% (for each $2,500 (or fraction thereof) ($1,250 for MFS)of AGI above thresholds:–$258,250 if single–$284,050 if head of household–$309,900 if married filing jointly

or surviving spouse–$154,950 if married filing separately

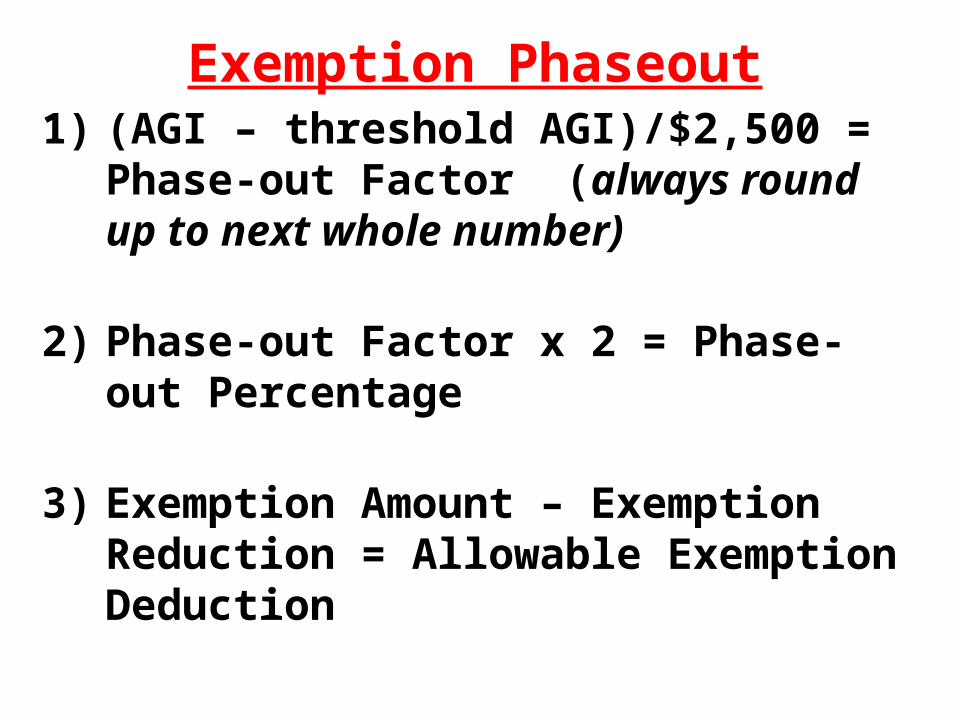

Exemption Phaseout1) (AGI – threshold AGI)/$2,500 = Phase-out

Factor (always round up to next whole number)

2) Phase-out Factor x 2 = Phase-out Percentage

3) Exemption Amount – Exemption Reduction = Allowable Exemption Deduction

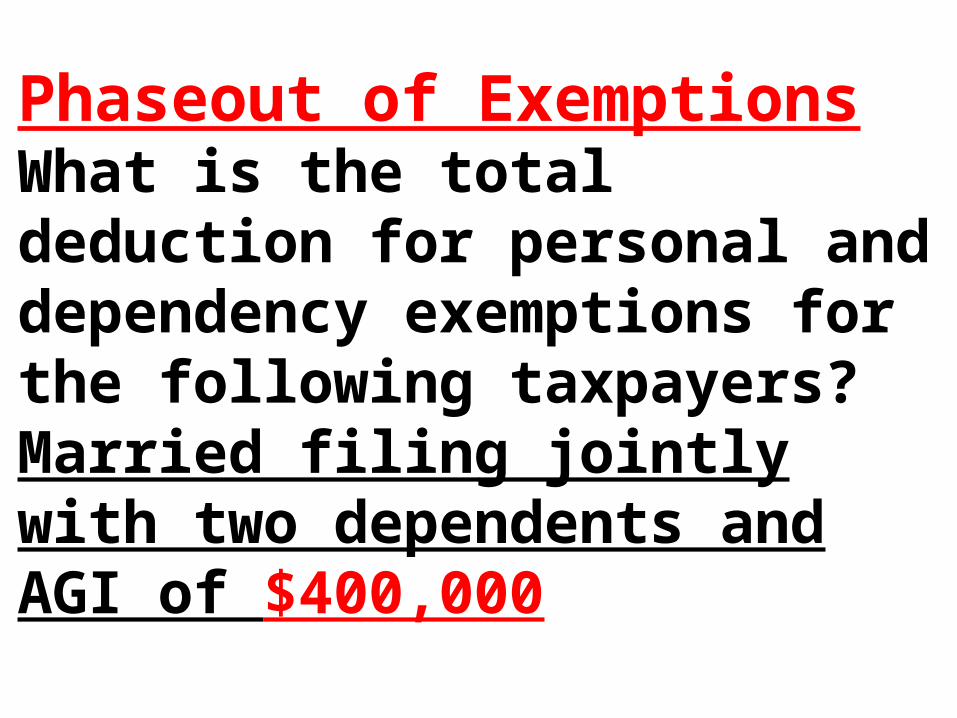

Phaseout of ExemptionsWhat is the total deduction for personal and dependency exemptions for the following taxpayers?Married filing jointly with two dependents and AGI of $400,000

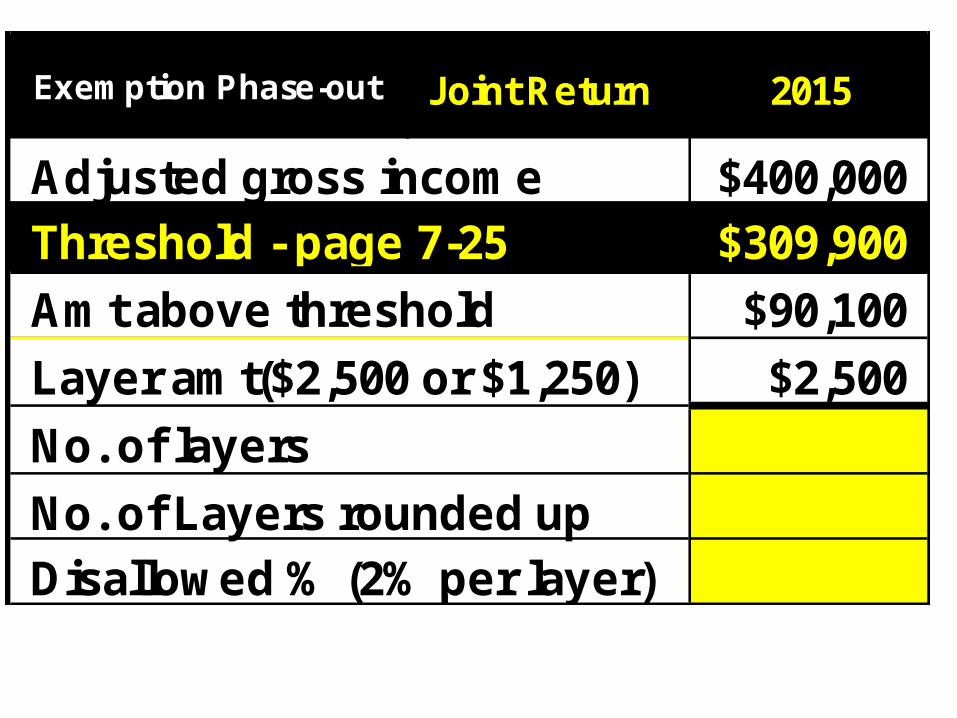

Exemption Phase-out Joint Return 2015

Adjusted gross income $400,000Threshold - page 7-25 $309,900

Amt above threshold $90,100

Layer amt($2,500 or $1,250) $2,500

No. of layers

No. of Layers rounded upDisallowed % (2% per layer)

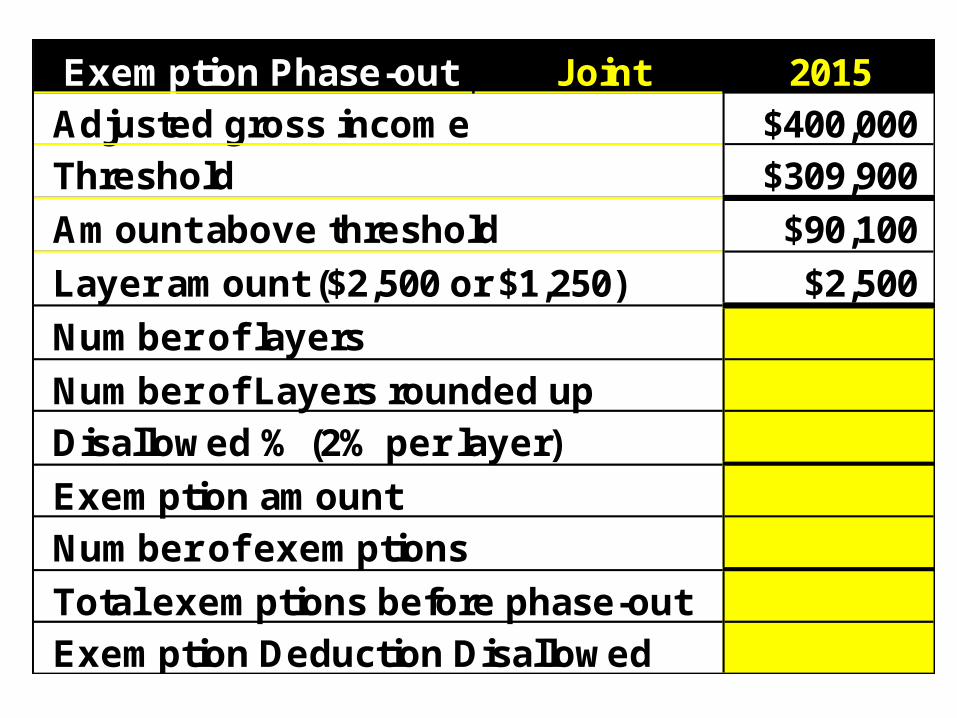

Exemption Phase-out Joint 2015Adjusted gross income $400,000Threshold $309,900

Amount above threshold $90,100

Layer amount ($2,500 or $1,250) $2,500

Number of layers

Number of Layers rounded upDisallowed % (2% per layer)

Exemption amount Number of exemptions

Total exemptions before phase-out Exemption Deduction Disallowed

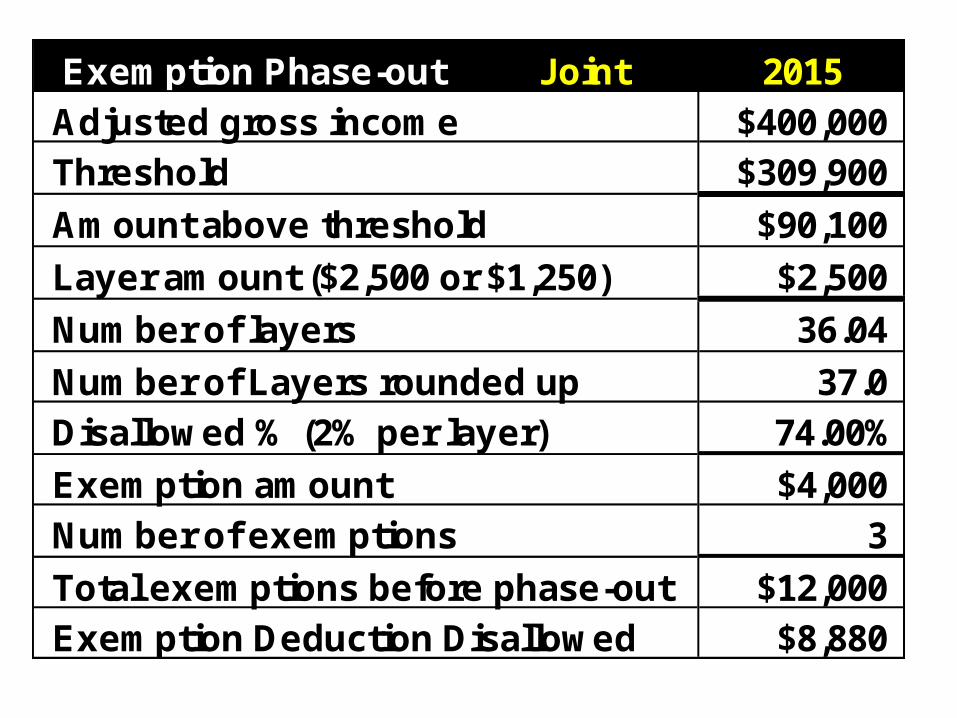

Exemption Phase-out Joint 2015Adjusted gross income $400,000Threshold $309,900

Amount above threshold $90,100

Layer amount ($2,500 or $1,250) $2,500

Number of layers 36.04

Number of Layers rounded up 37.0Disallowed % (2% per layer) 74.00%

Exemption amount $4,000Number of exemptions 3

Total exemptions before phase-out $12,000Exemption Deduction Disallowed $8,880

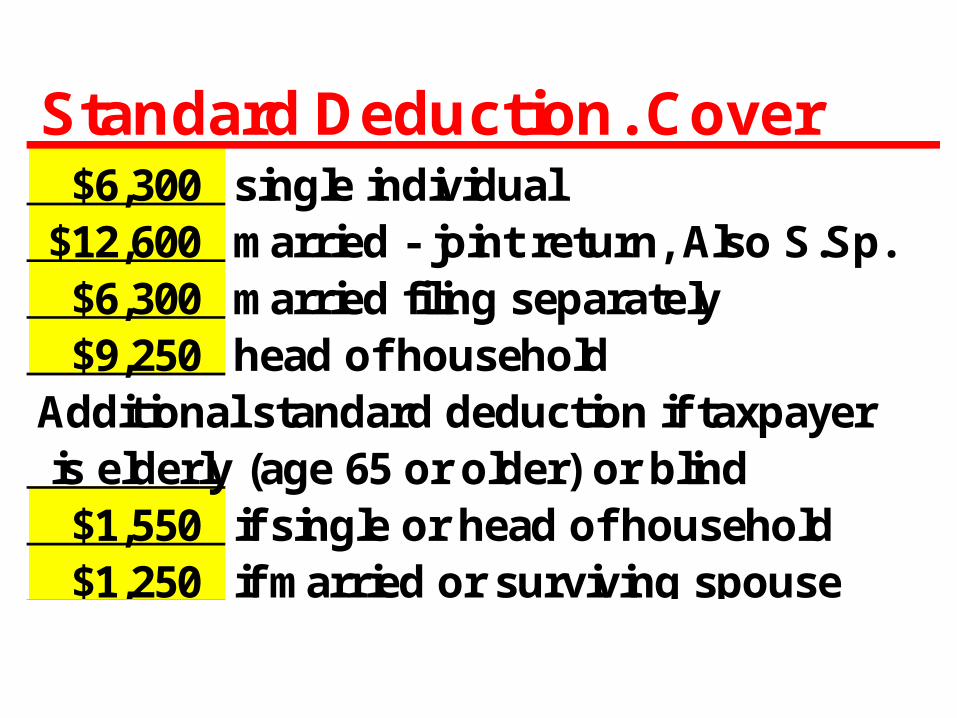

Standard Deduction. Cover$6,300 single individual

$12,600 married - joint return, Also S.Sp.$6,300 married filing separately $9,250 head of household

Additional standard deduction if taxpayer is elderly (age 65 or older) or blind

$1,550 if single or head of household $1,250 if married or surviving spouse

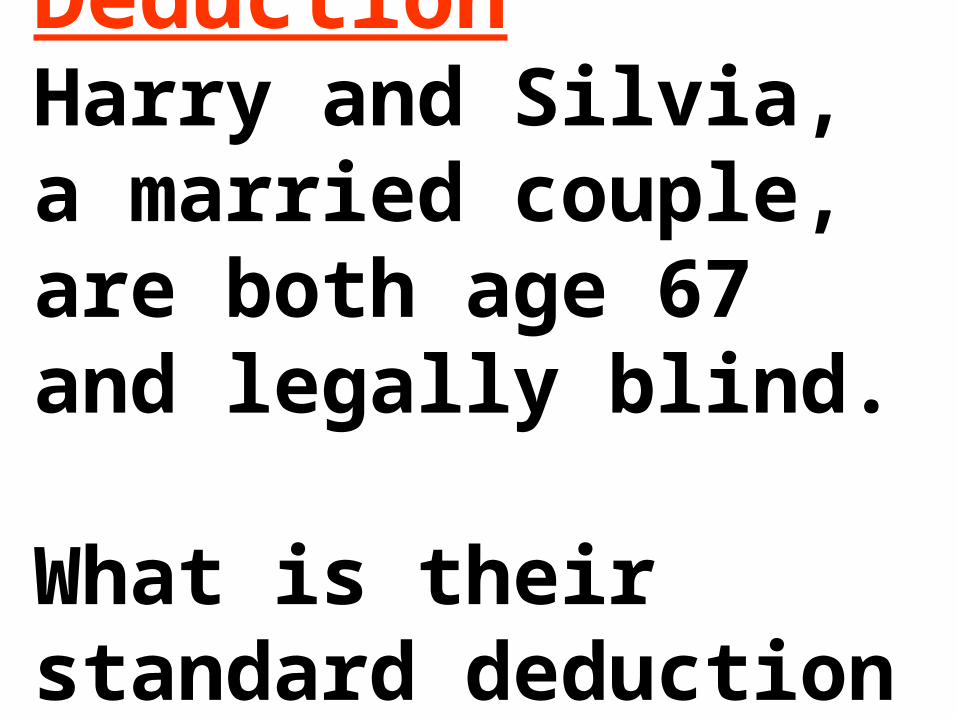

Standard DeductionHarry and Silvia, a married couple, are both age 67 and legally blind. What is their standard deduction for 2015?

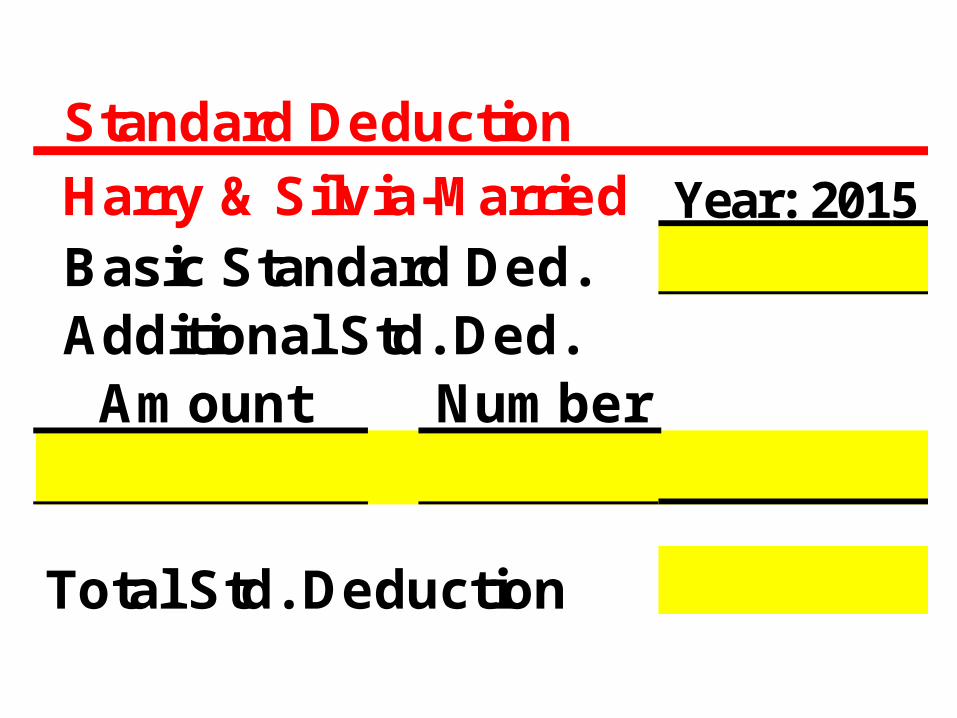

Standard DeductionHarry & Silvia-Married Year: 2015Basic Standard Ded.Additional Std. Ded.

Amount Number

Total Std. Deduction

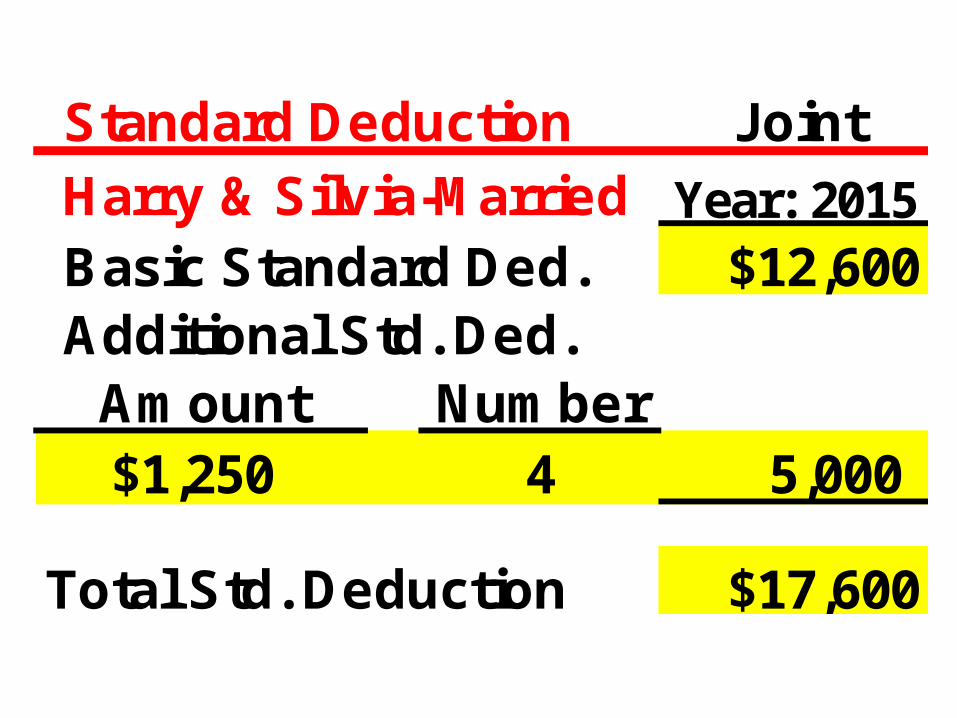

Standard Deduction JointHarry & Silvia-Married Year: 2015Basic Standard Ded. $12,600Additional Std. Ded.

Amount Number$1,250 4 5,000

Total Std. Deduction $17,600

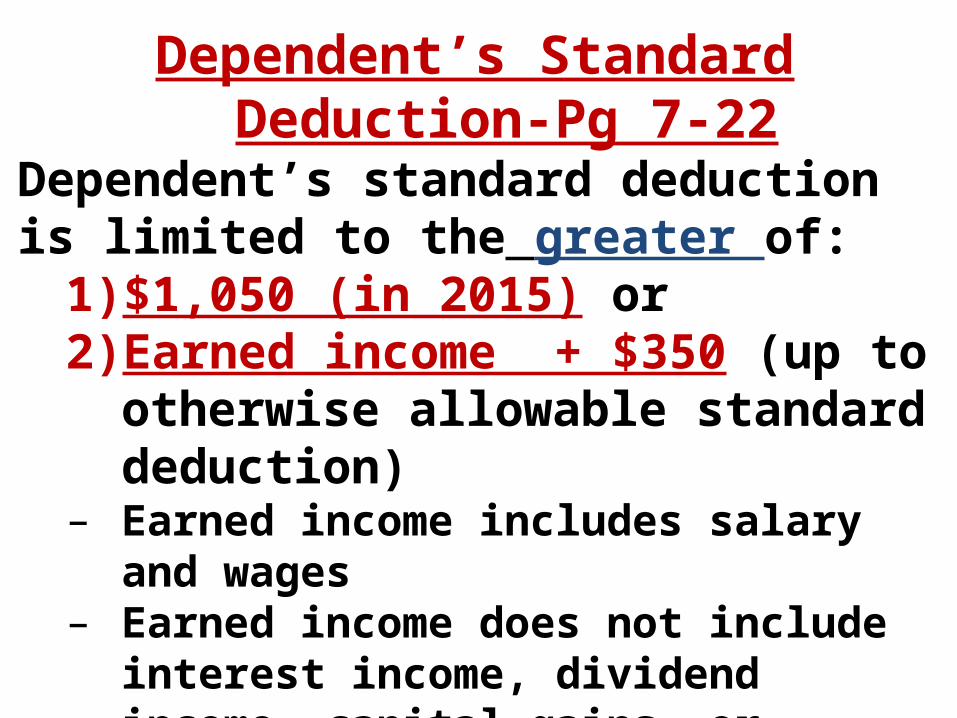

Dependent’s Standard Deduction-Pg 7-22Dependent’s standard deduction is limited to the greater of:

1) $1,050 (in 2015) or2) Earned income + $350 (up to otherwise

allowable standard deduction)– Earned income includes salary and wages– Earned income does not include interest

income, dividend income, capital gains, or income as beneficiary of a trust

Subject to regular limit of $6,300 (Single)

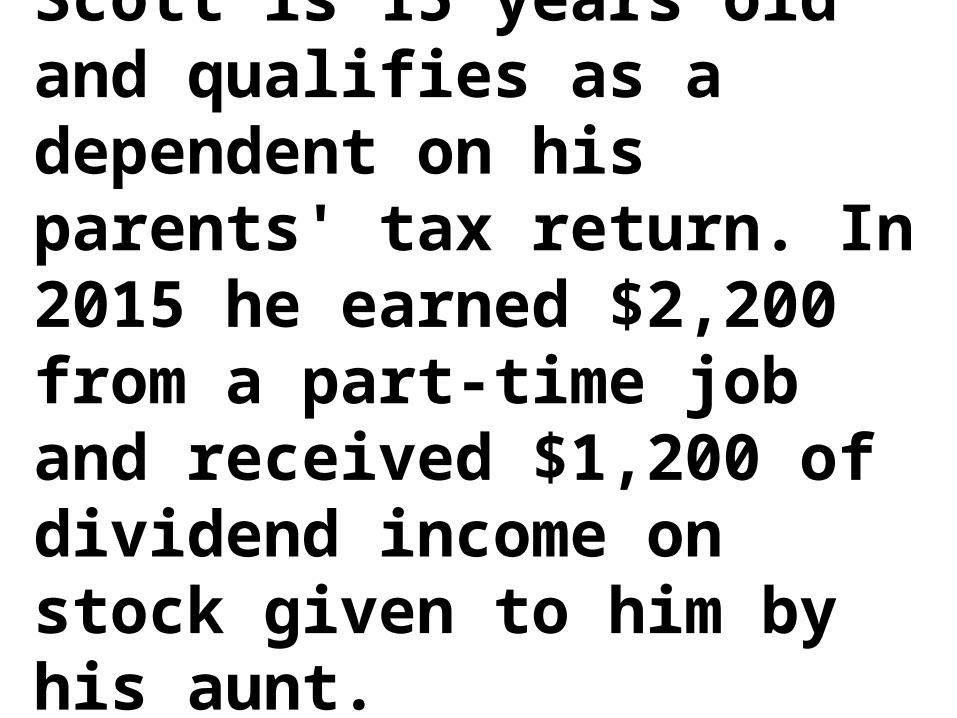

Dependent’s Taxable IncomeScott is 15 years old and qualifies as a dependent on his parents' tax return. In 2015 he earned $2,200 from a part-time job and received $1,200 of dividend income on stock given to him by his aunt. What is Scott’s taxable income?

Scott 2015Wages $2,200Dividend Income 1,200Adjusted Gross Income 3,400Standard Deduction:Greater of:1. Base deduction2. Earned income + $350Taxable Income

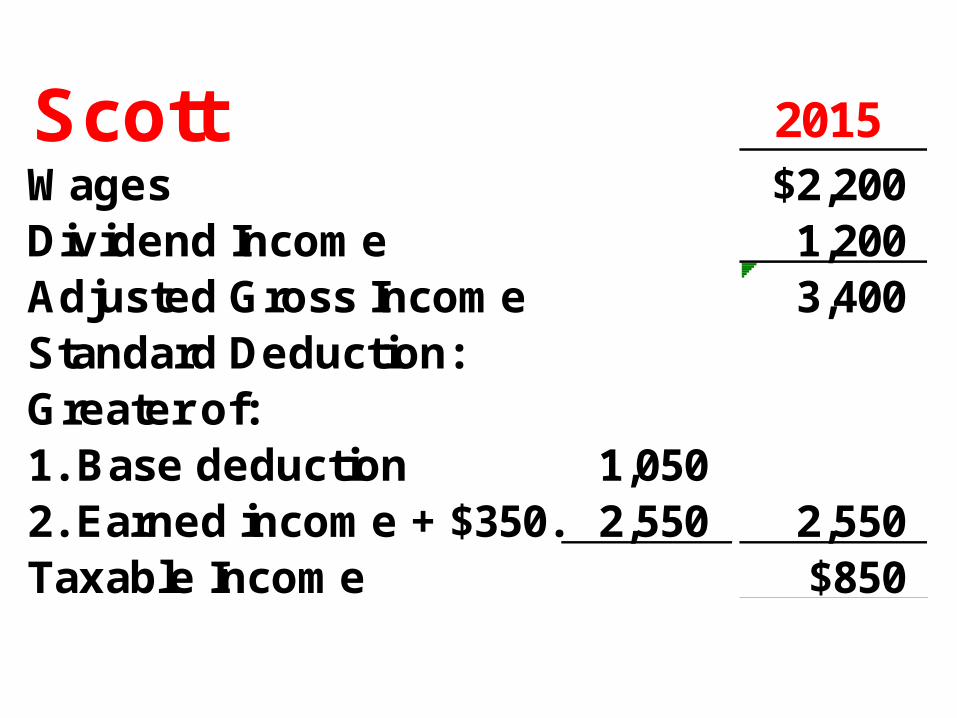

Scott 2015Wages $2,200Dividend Income 1,200Adjusted Gross Income 3,400Standard Deduction:Greater of:1. Base deduction 1,050 2. Earned income + $350. 2,550 2,550Taxable Income $850

Itemized Deductions• Itemized deductions provide tax

benefit only to the extent that, in total, they exceed the taxpayer’s standard deduction

• Taxpayers can maximize use of the standard deduction and itemized deductions by timing certain deductible payments

Deduction LimitsHigh income taxpayers’ deductionStandard deduction for dependent children

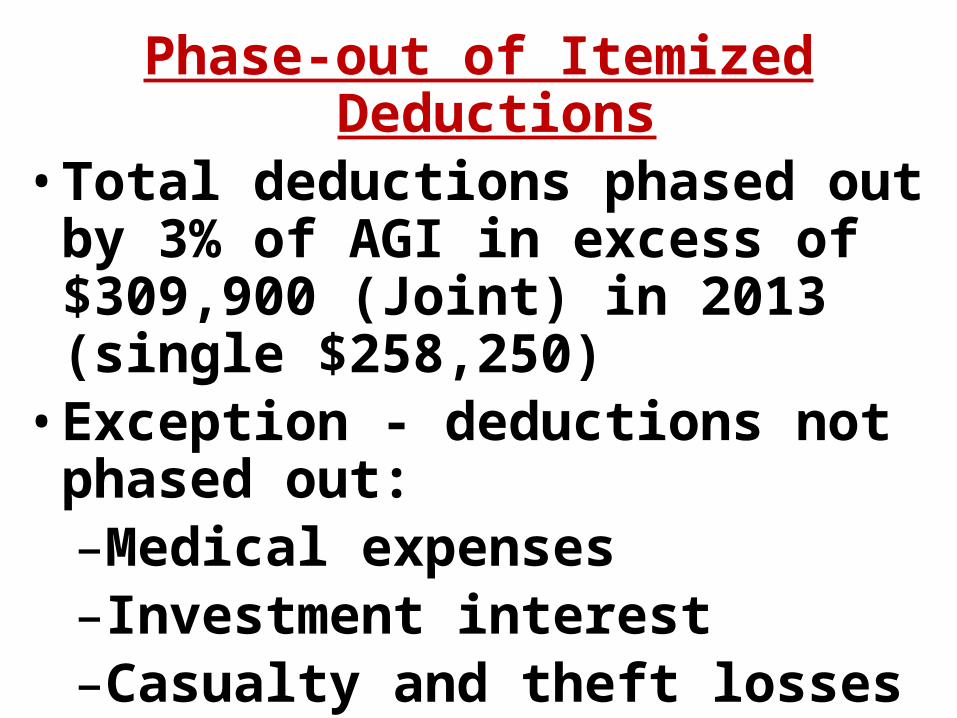

Phase-out of Itemized Deductions• Total deductions phased out by 3% of

AGI in excess of $309,900 (Joint) in 2013 (single $258,250)

• Exception - deductions not phased out:–Medical expenses–Investment interest–Casualty and theft losses

• Total deductions are not reduced by more than 80% regardless of type

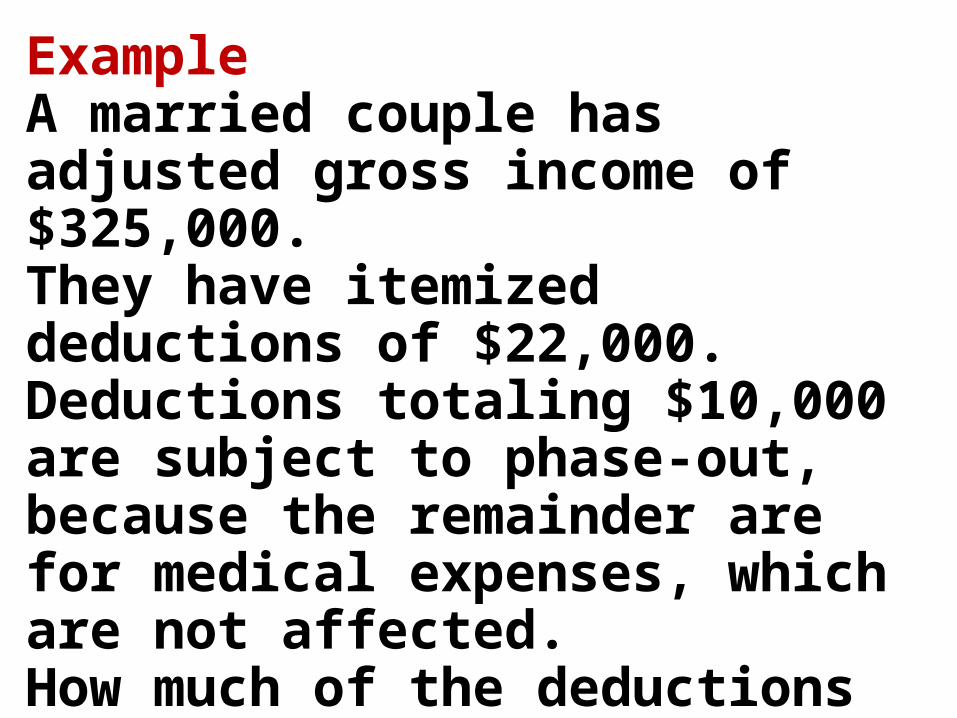

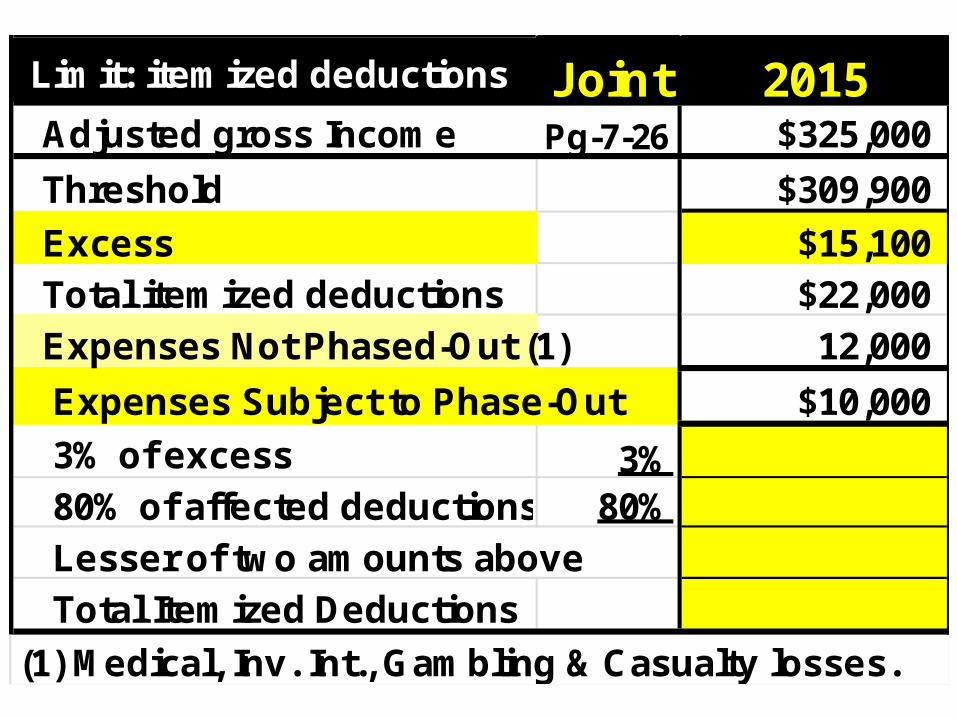

ExampleA married couple has adjusted gross income of $325,000.They have itemized deductions of $22,000.Deductions totaling $10,000 are subject to phase-out, because the remainder are for medical expenses, which are not affected.How much of the deductions are phased out for 2015? See slides that follow.

Limit: itemized deductions Joint 2015Adjusted gross Income Pg-7-26 $325,000

Threshold $309,900

Excess $15,100Total itemized deductions $22,000Expenses Not Phased-Out (1) 12,000

Expenses Subject to Phase-Out $10,000

3% of excess 3% 80% of affected deductions 80% Lesser of two amounts above Total Itemized Deductions

(1) Medical, Inv. Int., Gambling & Casualty losses.

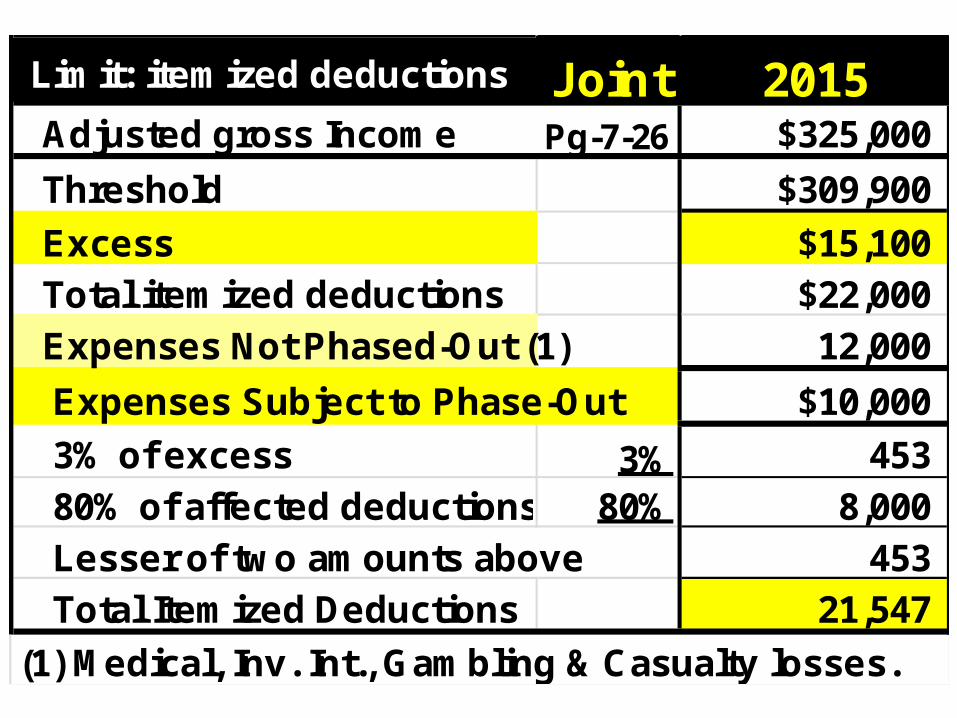

Limit: itemized deductions Joint 2015Adjusted gross Income Pg-7-26 $325,000

Threshold $309,900

Excess $15,100Total itemized deductions $22,000Expenses Not Phased-Out (1) 12,000

Expenses Subject to Phase-Out $10,000

3% of excess 3% 453 80% of affected deductions 80% 8,000 Lesser of two amounts above 453 Total Itemized Deductions 21,547

(1) Medical, Inv. Int., Gambling & Casualty losses.

End