CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

of 19

Transcript of CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

1/19

CHAPTER 4TIME VALUE OF MONEY

PART 1:

INTEREST & ECONOMICEQUIVALENCE

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

2/19

Interest Interest can be thought of as "rentof money".

Interest is a feepaid on borrowed assets.

It is the price paid for the use of borrowedmoney,[1]

Money earned by deposited funds

Interest is a rental amount charged by financialinstitutions for the use of money.

It is expressed on an annual basis.

For the lender, it consists, for convenience, of (1)risk of loss, (2) administrative expenses, and (3)profit or pure gain.

For the borrower, it is the cost of using a capitalfor immediately meeting his or her needs.

http://en.wikipedia.org/wiki/Renthttp://en.wikipedia.org/wiki/Feehttp://en.wikipedia.org/wiki/Feehttp://en.wikipedia.org/wiki/Rent -

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

3/19

Interest Rate The percentage of money being borrowed that

is paid to the lender on some time basis

Interest Rate is a measure of the interest for given

loan during the loan period and usually denotedby iand expressed in percentage (%)

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

4/19

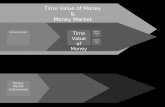

Time Value Of Money

The time-value of money is the relationship betweeninterest and time. i.e. Figure 1 : Time-Value of Money

Money has time-value because the purchasingpower of a ringgit changes with time.

0 1 2 3

years

nn-1

Now

RMRM+Interest

Figure 1

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

5/19

Power Of Money Earning Power Of Money The earning power of money represents funds borrowed

for the prospect of gain. Often these funds will be exchanges for goods, services,

or production tools, which in turn can be employed togenerate and economic gain.

Purchasing Power Of Money The prices of goods and services can go upward or

downward, and therefore, the purchasing power ofmoney can change with time.

Price Reductions : Caused by increases in productivityand availability of goods. Price Increases : Caused by government policies, price

support schemes, and deficit financing.

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

6/19

Cash Flow Diagrams

Cash flow diagrams are a means of visualizing(and simplifying) the flow of receipts anddisbursements

The diagram convention is as follows:

Horizontal Axis : The horizontal axis is marked off in equalincrements, one per period, up to the duration of theproject.

Revenues : Revenues (or receipts) are represented byupward pointing arrows.

Disbursements : Disbursements (or payments) arerepresented by downward pointing arrows.

Net Cash Flow : The arithmetic sum of receipts (+) and

disbursements (-) that occur at the same point in time.

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

7/19

Cash Flow DiagramsAll disbursements and receipts (i.e. cash flows) are

assumed to take place at the end of the year inwhich they occur. This is known as the "end-of-year"convention.

Arrow lengths are approximately proportional to themagnitude of the cash flow.

Expenses incurred before time = 0 are sunk costs,and are not relevant to the problem.

Since there are two parties to every transaction, it isimportant to not that cash flow directions in cashflow diagrams depend upon the point of viewtaken.

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

8/19

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

9/19

Cash Flow DiagramsRM 1000

RM 1000RM 1120

RM 1120

Borrower point of view Lender point of view

RM 120 RM 120 RM 120 RM 120

RM 120 RM 120 RM 120 RM 120

Example 1: Figure 2 shows cash flow diagrams for a transaction spanningfive years. The transaction begins with a RM1000.00 loan. For years two,three and four, the borrower pays the lender RM120.00 interest. At year five,

the borrower pays the lender $120.00 interest plus the RM1000.00 principal.

0 1 2 3 4 5

0 1 2 3 4 5

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

10/19

Methods of Calculating Interest Simple Interest : the practice of

charging an interest rate only toan initial sum (principal amount).

I = Pni.P = Principali = Interest rate

n = Number of years (or periods)I = Interest

Example 2 : Suppose that RM1000 is borrowed at a simpleinterest rate of 8% per annum.

Principle + Interest at end of Year 1 = 1000 * 0.08 * 1 = RM 80 Year 2 = 1000 * 0.08 * 2 = RM 160

Year

Amount atstart of

year (RM)

Interestat end of

year(RM)

Principle+

Interest

0 1,000 - -

1 - 80 1,080

2 - 80 1160

3 - 80 1240

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

11/19

Methods of Calculating Interest Compound Interest: the practice of charging an interest rate to an

initial sum and to any previously accumulated interest that has notbeen withdrawn

Example 3

Year Amount at start ofyear (RM)

Interest at endof year (RM)

EndingBalance

1 1,000 80 1,080

2 1,080 86.40 1,166.40

3 1,166.40 93.31 1,259.71

P= RM1,000 i = 8% n = 3years

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

12/19

Economic equivalence EE exists between cash flows that have the same economic

effect and could therefore be traded for one another.

EE refers to the fact that a cash flow-whether a singlepayment or a series of payments-can be converted to anequivalent cash flow at any point in time.

Even though the amounts and timing of the cash flows maydiffer, the appropriate interest rate makes them equal

RM 1,259.71RM1000

50

i = 8%

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

13/19

Economic equivalence Example 4: A loan of $1,000 is made at an interest of 12% for 5

years. The interest is due at the end of each year with the

principal is due at the end of the fifth year. The following table

shows the resulting payment schedule:

Year Amount at start ofyear

Interest at end ofyear

Owed amountat end of year

Payment

1 1000 120 1120 120

2 1000 120 1120 120

3 1000 120 1120 120

4 1000 120 1120 120

5 1000 120 1120 1120

Principal P = $1000.00 Interest Rate i = 0.12. Number of years (or periods) n = 5.

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

14/19

Economic equivalence Example 5: A loan of $1,000 is made at an interest of

12% for 5 years. The principal and interest are due atthe end of the fifth year. The following table shows theresulting payment schedule:

Year Amount at start ofyear

Interest at end ofyear

Owed amountat end of year

Payment

1 1000 120 1200 0

2 1000 134.40 1254.40 0

3 1000 150.53 1404.93 0

4 1000 168.59 1573.52 0

5 1000 188.82 1762.34 1762.34

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

15/19

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

16/19

Nominal And Effective Interest Rates

Nominal Interest Rate

Interest rate quoted based on an annual period

without adjustment for the full effect of compounding

Cannot be used for calculating the interest

An interest rate is called nominalif the frequency of compounding(e.g. a month) is not identical to the basic time unit(normally a year).

Example, :

12% per year compounded monthly

What It Really Means?

Interest rate per month (i) = 12%/12 = 1% (One percent per month)

Number of interest periods per year (N) = 12

In words, bank will charge 1% interest each month on your unpaidbalance, if you borrowed money.

You will earn 1% interest each month on your remaining balance, ifyou deposited mone

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

17/19

Nominal And Effective Interest Rates Effective interest rate, ie

Actual interest earned or paid in a year or some other time period with adjustment for the full effect of compounding Application: to compare the annual interest between loans with

different compounding terms Example : 12% per year compounded monthly

Effective interest rate per month = 1% Effective interest rate per year = ?????

The effective rate is calculated in the following wayie= ( 1 + r / M )

M1 ,Where

ie= Effective interest rate,r = Nominal interest rateM = number of compounding periods (eg.how many months)

For example, : 12% per year compounded monthly Effective interest rate per year = ieyear= ( 1 + r / M )

M1=

(1+[(12%/100)/12])12

-1 = 0.126%

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

18/19

For example, :

12% per year compounded monthly Effective interest rate per year = ieyear= ( 1 + r /

M )M1= (1+[(12%/100)/12])12 -1 = 0.126%

Another example (based on the above) :

Interest 1% per month, with the saving of 1k, so after1 year, you will get 1,130 in total.

** Original Saving + Interest = 1,000 + 13 % = 1,130

-

8/10/2019 CHAPTER 4 TIME VALUE OF MONEY Part 1 Interst and Equivalent.ppt

19/19

NOMINAL AND EFFECTIVE INTEREST RATES

Effective Annual Rate Based on Frequency of Compounding

Nominal

RateSemi-

AnnualQuarterly Monthly Daily Continuous

1% 1.00% 1.00% 1.01% 1.01% 1.01%

5% 5.06% 5.10% 5.12% 5.13% 5.13%

10% 10.25% 10.38% 10.47% 10.52% 10.52%

15% 15.56% 15.87% 16.08% 16.18% 16.18%

20% 21.00% 21.55% 21.94% 22.13% 22.14%

30% 32.25% 33.55% 34.49% 34.97% 34.99%

40% 44.00% 46.41% 48.21% 49.15% 49.18%

50% 56.25% 60.18% 63.21% 64.82% 64.87%