Chapter 3 3 The Corporate Income Tax. Filing Requirements and Computing the Tax.

23

Chapter 3 The Corporate Income Tax

-

Upload

astrid-yerton -

Category

Documents

-

view

222 -

download

4

Transcript of Chapter 3 3 The Corporate Income Tax. Filing Requirements and Computing the Tax.

ChapterChapter33

The Corporate Income TaxThe Corporate Income Tax

Filing Requirements and Computing the Tax

Filing Requirements and Computing the Tax

Slide C3-3

Filing RequirementsFiling Requirements

C corporations are separate tax-paying and tax-reporting entities from their owners

Annual tax returns requiredForm 1120 or Form 1120-A (corporations with gross

receipts, total income and total assets < $500,000)Original due date is the 15th day of the third month

following the fiscal year-end [IRC §6072(b)] Can obtain an automatic 6 month extension of time to

file using Form 7004 [IRC §6081] Extension of time to file the tax return does not extend

the time for paying the tax

Slide C3-4

The Corporate Tax FormulaThe Corporate Tax Formula

For C Corporations: Total Income- Allowable DeductionsTaxable Income before NOLs and Special Deductions- NOLs and Special Deductions=Taxable Income

Slide C3-5

Corporate Tax Rates [IRC §11(b)(1)]Corporate Tax Rates [IRC §11(b)(1)]

If TI is over But not over The tax is: Of TI less:

$0 50,000 15% $0

50,000 75,000 $7,500 + 25% 50,000

75,000 100,000 13,750 + 34% 75,000

100,000 335,000 22,250 + 39% 100,000

335,000 10,000,000 113,900 + 34% 335,000

10,000,000 15,000,000 3,400,000 + 35% 10,000,000

15,000,000 18,333,333 5,150,000 + 38% 15,000,000

18,333,333 --------------- 6,416,667 + 35% 18,333,333

Slide C3-6

Corporate Tax RatesCorporate Tax Rates

Exception: Personal Service CorporationsTaxed at a flat 35% [IRC §11(b)(2)]Definition [IRC §448(d)(2)]

Slide C3-7

Example 1a: Computing the TaxExample 1a: Computing the Tax

The Purple Corporation has taxable income of $125,000. What is the tax before credits if this corporation is not a personal service corporation?Answer:

22,250 + (125,000 – 100,000) x 39% = $32,000

Slide C3-8

Example 1b: Computing the TaxExample 1b: Computing the Tax

The Purple Corporation has taxable income of $125,000. What is the tax before credits if this corporation is a personal service corporation?Answer:

125,000 x 35% = $43,750

Slide C3-9

Example 2a: Computing the TaxExample 2a: Computing the Tax

The Green Corporation has taxable income of $425,000. What is the tax before credits if this corporation is not a personal service corporation?Answer:

113,900 + (425,000 – 335,000) x 34% = $144,500Alternatively: 425,000 x 34% = $144,500

Slide C3-10

Example 2b: Computing the TaxExample 2b: Computing the Tax

The Green Corporation has taxable income of $425,000. What is the tax before credits if this corporation is a personal service corporation?Answer: 425,000 x 35% = $148,750

Tax Accounting PeriodsTax Accounting Periods

Slide C3-12

Accounting PeriodsAccounting Periods

Generally, a corporation’s tax period is the same as its fiscal period for financial accounting purposes [IRC §441(b)(1) and (c)]Can be any 12 month period ending on the last day of

any month [IRC §441(d) and (e)]Can elect a 52/53 week around the end of any month

[IRC §441(f)]Short tax periods (less than 12 months) may occur in

a corporation’s first or last years of business, or in the year of a change in accounting period

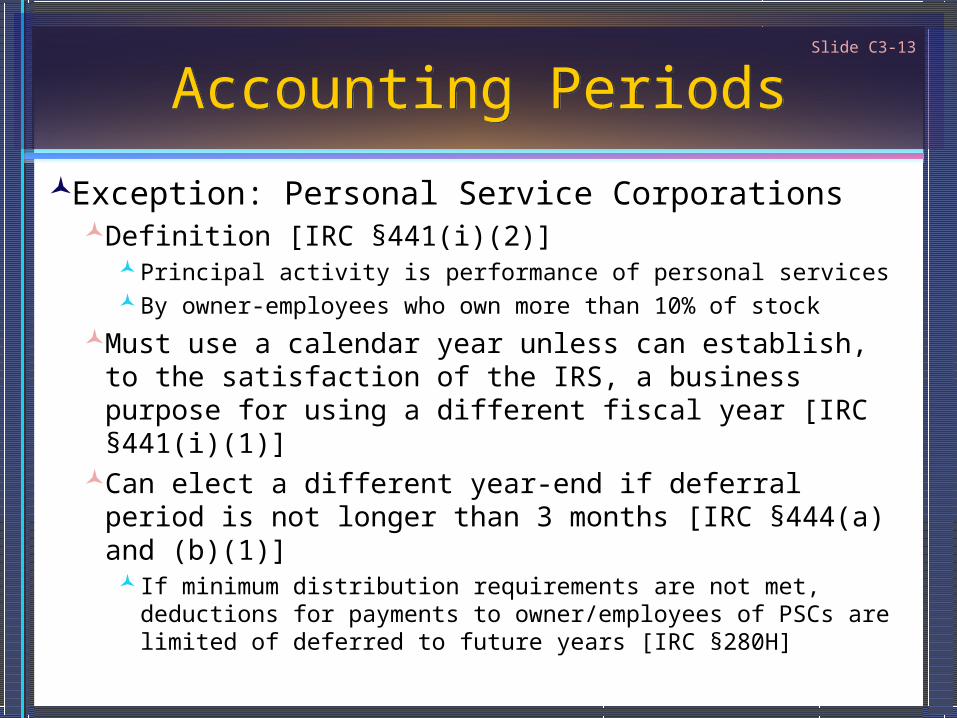

Slide C3-13

Accounting PeriodsAccounting Periods

Exception: Personal Service CorporationsDefinition [IRC §441(i)(2)]

Principal activity is performance of personal servicesBy owner-employees who own more than 10% of stock

Must use a calendar year unless can establish, to the satisfaction of the IRS, a business purpose for using a different fiscal year [IRC §441(i)(1)]

Can elect a different year-end if deferral period is not longer than 3 months [IRC §444(a) and (b)(1)] If minimum distribution requirements are not met, deductions

for payments to owner/employees of PSCs are limited of deferred to future years [IRC §280H]

Slide C3-14

Changing Accounting PeriodsChanging Accounting Periods

Corporation can just pick a year-end for its first tax return but after that, IRS approval is generally required to change tax years [IRC §442]Regulations and Rev. Proc 2002-37 allow an automatic

approval of a change in accounting period if certain conditions are strictly met [Reg. §1.442-1(c)]

Slide C3-15

Changing Accounting PeriodsChanging Accounting Periods

If a short period return results from a change in accounting period, the tax is calculated using the “annualized” taxable income method [IRC §443]

Slide C3-16

Example 3a: Short PeriodsExample 3a: Short Periods

The Blue Corporation (not a PSC) files a tax return for the short period September 1st to December 31st. Taxable income reported in the short period return is $82,000. What is the tax for the short-period if this is the corporation’s first year of business?Answer:

13,750 + (82,000 – 75,000) x 34% = $16,130

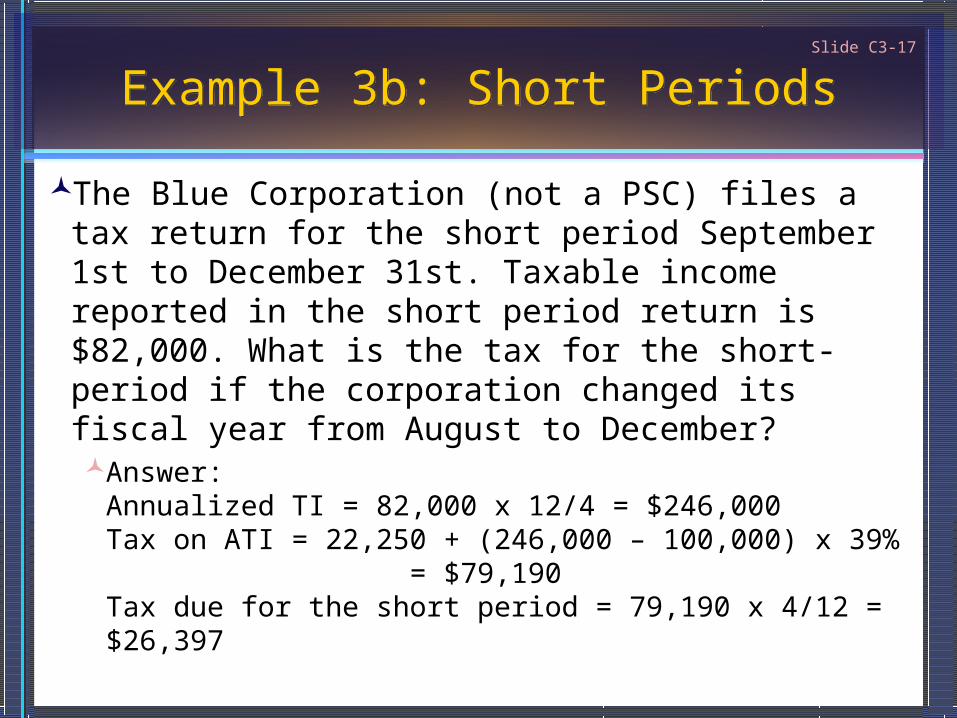

Slide C3-17

Example 3b: Short PeriodsExample 3b: Short Periods

The Blue Corporation (not a PSC) files a tax return for the short period September 1st to December 31st. Taxable income reported in the short period return is $82,000. What is the tax for the short-period if the corporation changed its fiscal year from August to December?Answer:

Annualized TI = 82,000 x 12/4 = $246,000 Tax on ATI = 22,250 + (246,000 – 100,000) x 39% = $79,190 Tax due for the short period = 79,190 x 4/12 = $26,397

Tax Accounting MethodsTax Accounting Methods

Slide C3-19

Accounting MethodsAccounting Methods

Accounting method determines when an item of income or expense is included in taxable incomeMethod is selected in the corporation’s first tax returnMust get IRS consent to change accounting methods

once established [IRC §446(e) and (f)]Method taxpayer regularly uses to compute income in

per books [IRC §446(a)]Method must “clearly reflect income” or IRS can impose

a different method [IRC §446(b)]

Slide C3-20

Accounting MethodsAccounting Methods

Overall accounting methods that are generally permissible include [IRC §446]: Cash methodAccrual methodHybrid method

Slide C3-21

Accounting MethodsAccounting Methods

Exception: C corporations generally cannot use the cash method [IRC §448(a)(1)] Exception 1: Qualified farming businesses may use

cash method [IRC §448(b)(1) and (d)(1)]Exception 2: Qualified personal service corporations

may use cash method [IRC §448(b)(2) and (d)(2)]Exception 3: Corporations with gross receipts of not

more than $5,000,000 may use cash method [IRC §448(b)(3)]

Slide C3-22

Cash MethodCash Method

Income is generally taxable when it is received or constructively received [Reg. §1.446-1(c)(1)(i)]Exception: Inventory sales must be accounted for using

the accrual method [Reg. §1.446-1(c)(2)(i)]

Slide C3-23

Cash MethodCash Method

Expenses are generally deductible when they are actually paid [Reg. §1.446-1(c)(1)(i)]Exception: Inventory purchases and cost of goods

sold must be accounted for using the accrual method [Reg. §1.446-1(c)(2)(i)]

Exception: Prepaid interest must be deducted when accrued rather than when paid [IRC §461(g)]

Exception: Payments creating assets with useful lives of more than one year must be capitalized [IRC §263]These may then be depreciated or amortized