Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions

date post

21-Dec-2015Category

view

221download

4

CHAPTER 12CHAPTER 12

Audit Strategy in Response to Audit Strategy in Response to Assessed RisksAssessed Risks

Fall 2007Fall 2007

CHAPTER 12CHAPTER 12

Audit Strategy in Response to Audit Strategy in Response to Assessed RisksAssessed Risks

Fall 2007Fall 2007

Designing Substantive Tests Special Consideration in

Designing Substantive Tests

Designing Substantive TestsDesigning Substantive Tests

In each audit, there are certain substantive procedures that must be performed:

1. Initial procedures2. Analytical procedures3. Tests of details of transactions4. Tests of balances including estimates5. Tests of disclosures

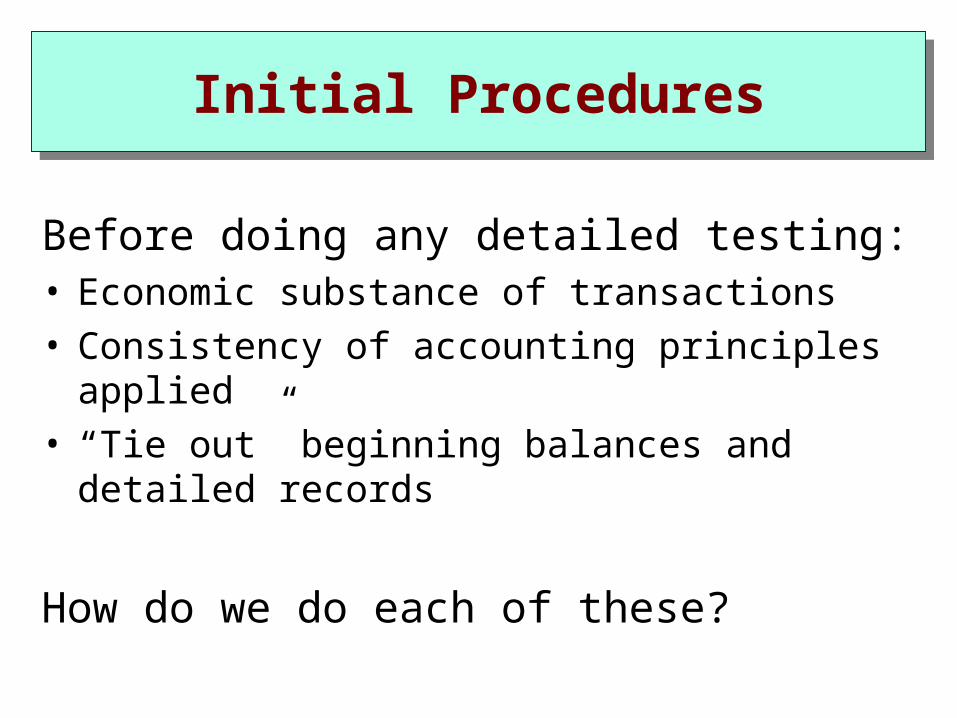

Initial ProceduresInitial Procedures

Before doing any detailed testing:• Economic substance of transactions• Consistency of accounting principles applied• “Tie out” beginning balances and detailed

records

How do we do each of these?

Recall the AR ModelRecall the AR Model

AR = IR x CR x AP x TD

When do we focus on each category of substantive tests?– Analytical procedures– Tests of transactions– Tests of balances

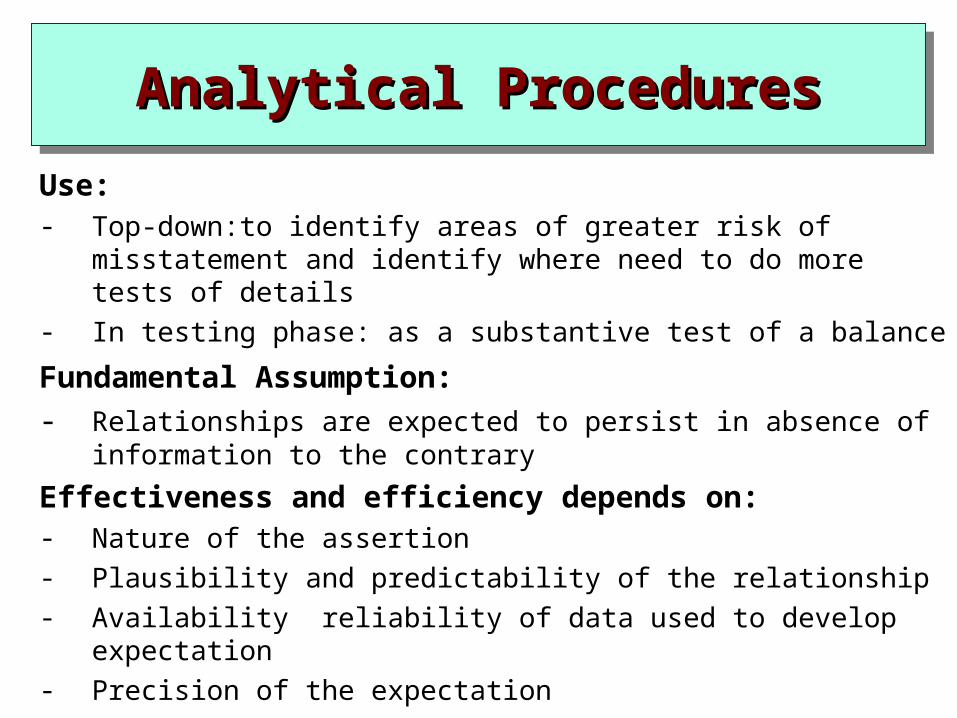

Use:- Top-down:to identify areas of greater risk of misstatement

and identify where need to do more tests of details - In testing phase: as a substantive test of a balance

Fundamental Assumption: - Relationships are expected to persist in absence of

information to the contrary

Effectiveness and efficiency depends on:- Nature of the assertion- Plausibility and predictability of the relationship- Availability reliability of data used to develop expectation- Precision of the expectation

Analytical ProceduresAnalytical ProceduresAnalytical ProceduresAnalytical Procedures

Analytical Procedures cont’dAnalytical Procedures cont’dAnalytical Procedures cont’dAnalytical Procedures cont’d

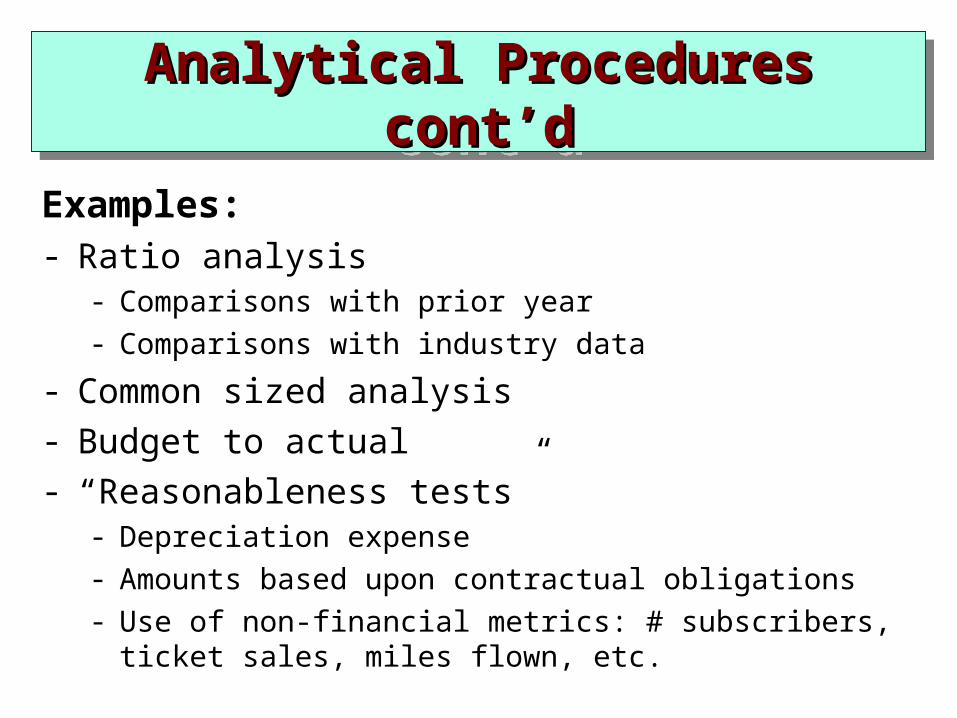

Examples:- Ratio analysis

- Comparisons with prior year- Comparisons with industry data

- Common sized analysis- Budget to actual- “Reasonableness tests”

- Depreciation expense- Amounts based upon contractual obligations- Use of non-financial metrics: # subscribers, ticket

sales, miles flown, etc.

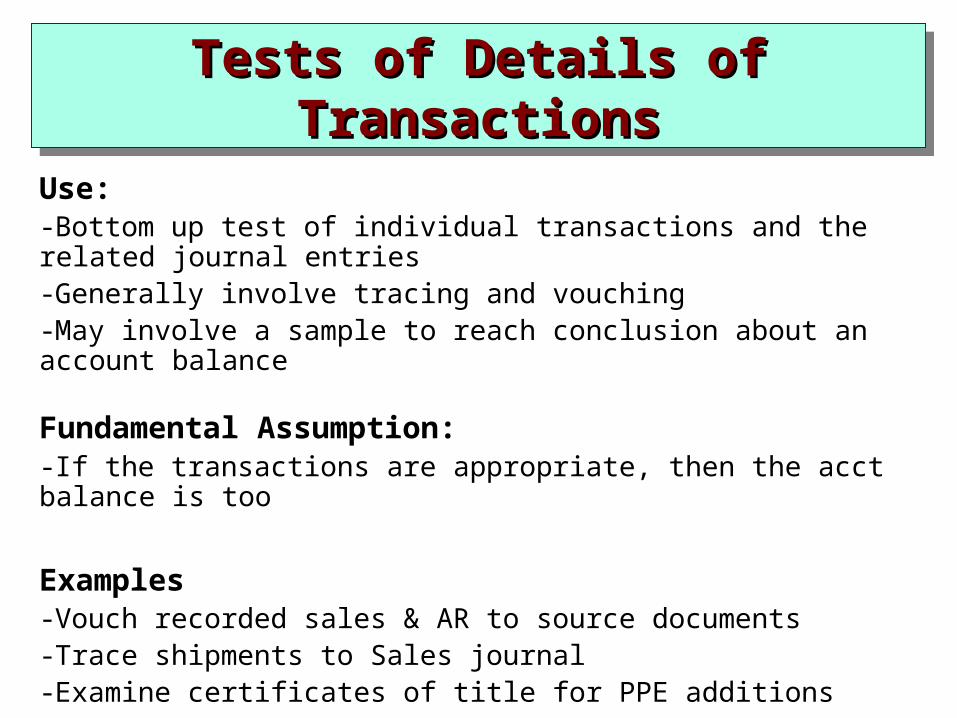

Use:-Bottom up test of individual transactions and the related journal entries-Generally involve tracing and vouching-May involve a sample to reach conclusion about an account balance

Fundamental Assumption: -If the transactions are appropriate, then the acct balance is too

Examples-Vouch recorded sales & AR to source documents-Trace shipments to Sales journal-Examine certificates of title for PPE additions

Tests of Details of Tests of Details of TransactionsTransactions

Tests of Details of Tests of Details of TransactionsTransactions

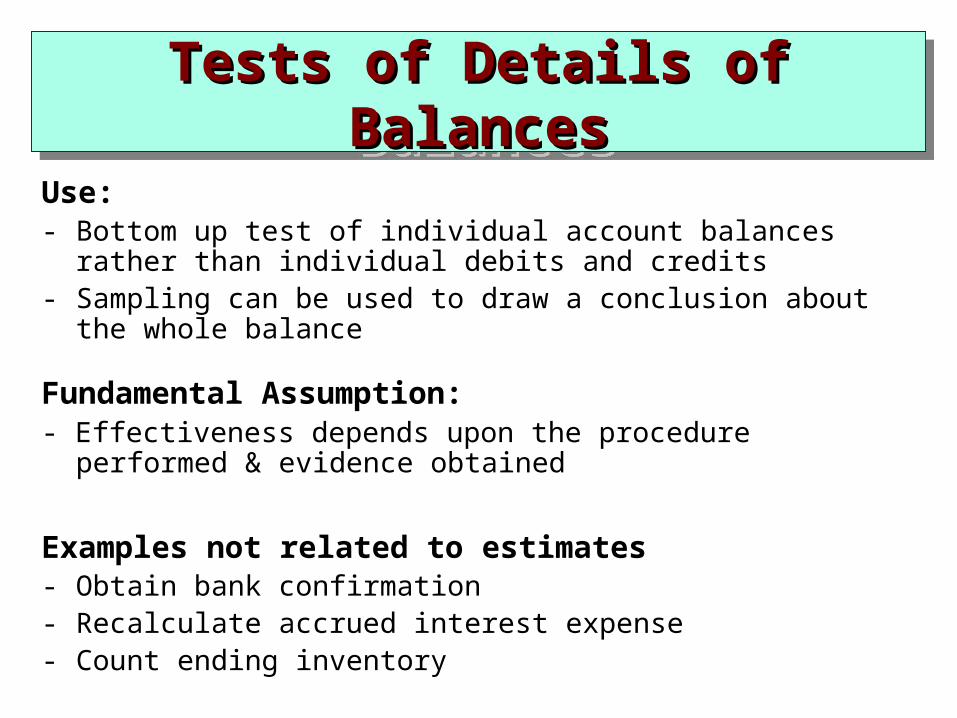

Tests of Details of BalancesTests of Details of BalancesTests of Details of BalancesTests of Details of Balances

Use:- Bottom up test of individual account balances rather

than individual debits and credits- Sampling can be used to draw a conclusion about the

whole balance

Fundamental Assumption: - Effectiveness depends upon the procedure performed &

evidence obtained

Examples not related to estimates- Obtain bank confirmation- Recalculate accrued interest expense- Count ending inventory

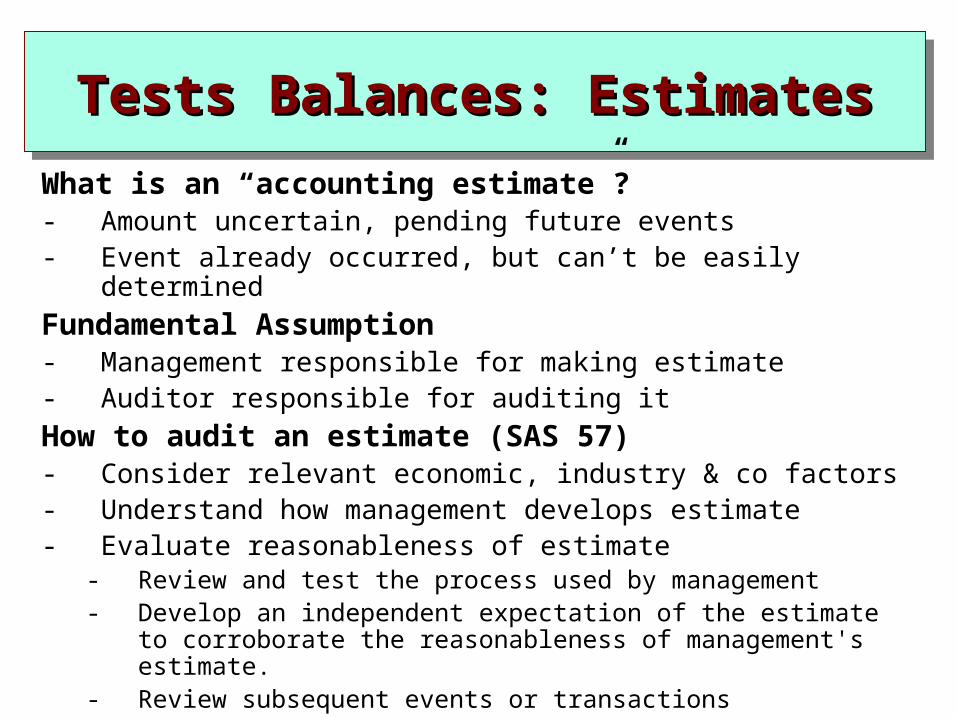

Tests Balances: EstimatesTests Balances: EstimatesTests Balances: EstimatesTests Balances: Estimates

What is an “accounting estimate”?- Amount uncertain, pending future events- Event already occurred, but can’t be easily determinedFundamental Assumption- Management responsible for making estimate- Auditor responsible for auditing itHow to audit an estimate (SAS 57)- Consider relevant economic, industry & co factors- Understand how management develops estimate- Evaluate reasonableness of estimate

- Review and test the process used by management - Develop an independent expectation of the estimate to

corroborate the reasonableness of management's estimate.

- Review subsequent events or transactions

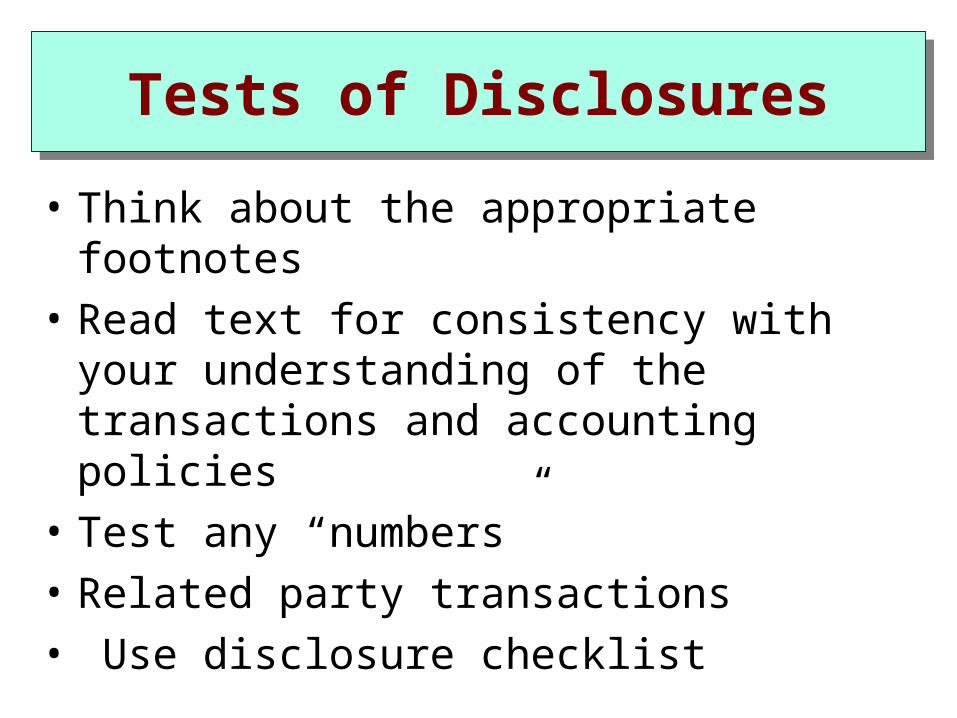

Tests of DisclosuresTests of Disclosures

• Think about the appropriate footnotes• Read text for consistency with your

understanding of the transactions and accounting policies

• Test any “numbers”• Related party transactions• Use disclosure checklist

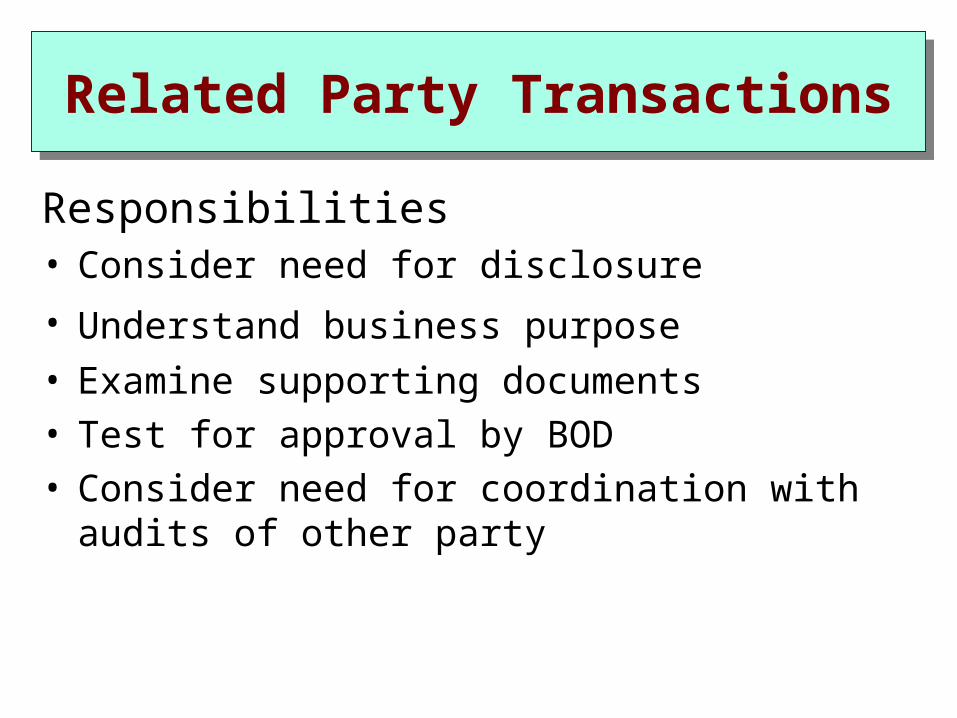

Related Party TransactionsRelated Party Transactions

Responsibilities• Consider need for disclosure

• Understand business purpose • Examine supporting documents• Test for approval by BOD• Consider need for coordination with audits

of other party

More evidence is needed to achieve a low acceptable level of detection risk than a high detection risk.

“Extent” is used in practice to mean the number of items or $ as a percentage of total to which a particular test or procedure is applied. This generally involves sampling.

Extent of Substantive TestsExtent of Substantive TestsExtent of Substantive TestsExtent of Substantive Tests