KANNUR BRANCH OF SIRC OF ICAI KANNUR 22.03.2014 By CA A Mony, B Com, FCA, DISA.

Upload

vuongnguyetCategory

view

216download

0

1

Dear Professional Colleagues,

At the outset I would like to express my

sincere thanks to all the members for having reposed

confidence on me as the founder Chairman of the

Branch. It is indeed very happy to note that , our long

cherished dream of having a branch status was thmaterialized on 6 February 2012. Yes, It was a

memorable day when the Kannur branch of SIRC of

ICAI was formally inaugurated by the then

honourable president of ICAI, CA G.Ramaswamy

FCA in the presence of CA Shanmugha Sundaram

(Former Chairman, SIRC), CA Babu Abrahm

Kallivayalil (Former chairman, SIRC), CA Jose.V.X

(Member, SIRC) and CA Shyju Sebastian (Chairman,

Calicut Branch). I would like to express my sincere

gratitude to all the stalwarts of the Institute

particularly the then president of ICAI G.

Ramaswamy FCA for their unstinting support and

guidance for the formation of the Kannur Branch of

SIRC of ICAI. On this occasion, I humbly salute all

the Past Presidents of Cannanore Chartered

Accountants Association for their remarkable role of

taking initiatives to provide quality programmes for

continuous professional education and learning for

members and students. A brief history of the

transformation of Cannannore CA Association to the

Kannur branch of ICAI is published elsewhere in this

news letter.

Since its inception, the Branch has been conducting

workshops and seminars on various topics of

professional interest for members and students. A few

of them I may cite:

1) Two days workshop on advanced Excel Software

for members;

2) Two days workshop on service tax for members;

3) One day Seminar on Revised Schedule VI for

members and students;

4) One day individual training programme for

students;

As you know the Indian economy faces

challenging times as growth has slowed down and

inflation has remained high. The eminent economists,

while evaluating the economic situation of our

country, estimate that the growth will come down to

5.3% of GDP against 7.6% targeted in the budget. The

fiscal and current account deficits are precariously

high. In order to tide over this challenging scenario,

the government may take certain positive steps such

as withdrawal of all forms of subsidies and put

restriction on unproductive expenditures. Besides,

We as the partners in nation building have to play a

pivotal role by providing fiscal prudence and

financial discipline in boosting the growth. We have

to uphold the fundamental principles of our

profession vis- a- vis the ethical rules and code of

conduct of ICAI.

I am very glad to inform that, the Kannur

Chairman Writes :

2

Branch of SICASA was inaugurated by Dr. Michael

Tharakan, the Vice-Chancellor of Kannur University,

on 03-07-2012. It is indeed very happy to note that,

Kannur branch of SICASA under the able leadership

of its Chairman CA Jayaprakash is doing well.

We are regularly conducting the orientation

programme and training on information technology

for students. Further we also plan to conduct coaching

classes, study circle / workshops / seminars for the

benefit of the students community. Besides, we take

keen interest for conducting cultural/ sports/ games

activities for students. I appeal to all students to make

use of various opportunities available at your door

steps.

“ I wish all a prosperous New Year "Yours in professional services

CA P D Emmanuval,Chairman, Kannur Branch of SIRC of ICAI.Email : [email protected]

Place : Kannur,

Date : 01/01/2013.

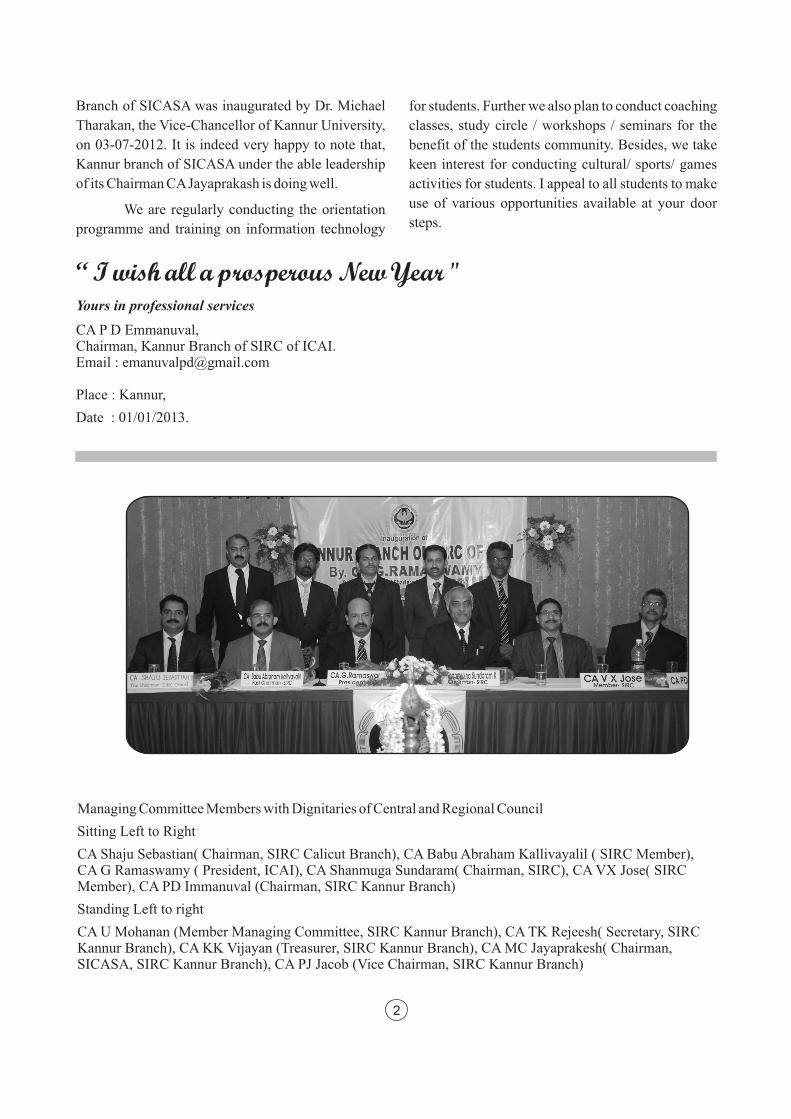

Managing Committee Members with Dignitaries of Central and Regional Council

Sitting Left to Right

CA Shaju Sebastian( Chairman, SIRC Calicut Branch), CA Babu Abraham Kallivayalil ( SIRC Member), CA G Ramaswamy ( President, ICAI), CA Shanmuga Sundaram( Chairman, SIRC), CA VX Jose( SIRC Member), CA PD Immanuval (Chairman, SIRC Kannur Branch)

Standing Left to right

CA U Mohanan (Member Managing Committee, SIRC Kannur Branch), CA TK Rejeesh( Secretary, SIRC Kannur Branch), CA KK Vijayan (Treasurer, SIRC Kannur Branch), CA MC Jayaprakesh( Chairman, SICASA, SIRC Kannur Branch), CA PJ Jacob (Vice Chairman, SIRC Kannur Branch)

3

Cannanore Chartered Accountants Association was formed by the members of the Kannur area 25 years ago as a registered society with Reg. No. 188/1987 on 10-06-87 and has been super active from its very inception till date. They used to organize regular executive committee meetings, general body meetings, annual general body meeting, CPE Seminars, Residential CPE Seminars etc. In view of their active status SIRC granted permission to start a CPE Chapter which was inaugurated on 03-02-2004. The orientation programme for students under the auspices of board of studies was organized by the Kannur CPE chapter in an excellent way. The Kannur CPE chapter was sanctioned to conduct the 100 hours Information Technology Training Centre to be supervised by them under Calicut branch of ICAI. This was inaugurated by the then SIRC Chairman CA Babu Abraham Kallivayalil on 19-08-2010 in the gracious presence of CA.V.X Jose, Member SIRC and CA. V.C James, Past Central Council Member.

On the happy occasion of upgrading as a branch, they miss three bright stars of the profession from Kannur who had to leave for their heavenly abode. Late CA Vijayan who initiated and started the Cannanore CA Association and was also the founder president, CA A I Thomas past president and the young CA K R Ganesh Kumar who was secretary of the association and deputy convenor of CPE chapter.

It is a great honour and privilege that CA Dr.O.K.Narayanan, Vice President of ITAT Mumbai Bench is one of the distinguished charter members of Cannanore Chartered Accountants Association. The following eminent members have visited Cannanore Chartered Accountants Association on various occasions as faculty, guests, or speakers, in the past.

CA G.Ramaswamy, Immediate Past President, ICAI

CA Madhukar Hiregange, Central Council Member

CA P.Rajendra Kumar, Central Council Member

CA V.C.James, Past Central Council Member

CA Jose Pottekaran, Past Central Council Member

CA Babu Abraham Kallivayalil, Past SIRC Chairman

CA V.X.Jose, SIRC Member

CA Gopalkrishna Raju, SIRC Member

CA Arjun Raj, Past SIRC Chairman

CA Venugopal C Govind

CA Shaju Sebastian, Chairman, Calicut Branch

CA A.Ramesh, Past Chairman, Calicut Branach

CA Vaman Kamath, Past Chairman, Mangalore branch

From July 2011onwards under the dynamic and vibrant leadership of CA P D Emmanuval, CA T K Rejeesh and CA K K Vijayan the Cannanore Chartered Accountants Association and Kannur CPE Chapter has been rollicking in their activities by organizing 8 CPE programmes, 4Batches of 100 Hours ITT Course, Individual Development Programme for Students on Effective Communication, Blood Donation Camp for Members, Family and Students in which 48 units of Blood donated to the District Head Quarters Hospital Blood Bank and

th st ndthe Residential CPE Seminar at Upavan Resorts, Lakkidi in Wyanad on 20 , 21 and 22 January 2012 was an ever memorable event for the 20 odd participants and their families.

The following are the CPE programmes conducted by the Kannur CPE Chapter in 2011-'12 under the new team:

06-08-2011 Tax Audit u/s. 44 AB of the IT Act CA C Suresh Kumar, FCA

History of Cannanore Chartered Accountants Association &

Kannur CPE Chapter which is upgraded as Kannur Branch of SIRC of ICAI

4

12-08-2011 Auditors' Report under Companies Act CA V Sathyanarayanan, FCA

12-08-2011 Accounting Standards - CA M C Jayaprakash, FCA A seasonal Refreshment

17-09-2011 VAT Audit CA P J Johney, FCA

22-10-2011 Intangible Assets & Its Valuation Prof Dr Pradeep Kumar Singh

19-11-2011 XBRL Financial Reporting CA Gopal Krishna Raju, FCA

21-12-2011 Taxation of Co-Operative Banks CA P J Jacob, FCA

20-01-2012 Residential CPE Seminar at Upavan Resorts, Prof Vargheese Vydyan

to Lakkidi, Wayanad CA P Mohan

22-01-2012 CA Jomon K George

CA T V Ranjith Kumar &

CA Saju Sreedhar

The detailed report of activities of the Cannanore Chartered Accountants Association in 2011-'12 is as given below:

04-07-2011 Annual General Body Meeting

04-07-2011 First Executive Committee Meetingth

16-07-2011 24 Anniversary Celebration at The Pearlview Regency, Thalassery

20-07-2011 Second Executive Committee Meeting

31-08-2011 First Batch of 100 Hrs ITT Training Centre inaugurated - 19 Students

05-09-2011 Third Executive Committee Meeting

06-10-2011 Second Batch of 100 Hrs ITT Training Centre started - 7 Students

16-11-2011 Fourth Executive Committee Meeting

26-11-2011 Individual Development Programme for Students on Communication Skills

17-12-2011 Mega Blood Donation Camp - 48 units of Blood donated

03-12-2011 Third Batch of 100 Hrs ITT Training Centre started - 17 Students

02-01-2012 Fifth Executive Committee Meeting

04-01-2012 Extra Ordinary General Body Meeting

09-01-2012 Fourth Batch of 100 Hrs ITT Training Centre started - 17 Students

11-01-2012 Kannur Branch Inauguration Organising Committee Meeting

17-01-2012 Extra Ordinary General Body Meeting

25-01-2012 Kannur Branch Inauguration Organising Committee Meeting

th The Association was upgraded as a Branch of the Institute of Chartered Accountants of India on 6 February

2012 by the Honorable President CA G Ramaswamy in a grand function held at Hotel Royal Omars, Thavakkara, Kannur. CA Shanmugasundaram, SIRC Chairman presided over the inaugural ceremony. CA Babu Abraham Kallivayalil, Immediate Past SIRC Chairman, CA V X Jose, SIRC Member and CA Shaju Sebastian, Vice Chairman, Calicut Branch of SIRC of ICAI felicitated on the occasion. 6 Students viz., Rasiga Raghupathy daughter of CA R Raghupathy, Krishna Mohan daughter of CA U Mohanan, Hareesh, Shijith, Shaleep and Hari who qualified in the final examination conducted in November 2011were honoured by the branch with President CA G Ramaswamy presenting mementoes to them. Chairman of the branch CA P D Emmanuval proposed vote of thanks. The managing committee includes CA P J Jacob - Vice Chairman, CA Rejeesh T K - Secretary, CA K K Vijayan - Treasurer, CA M C Jayaprakesh - SICASA Chairman and CA U Mohanan - Member. They are sure that with the blessings and guidance of leaders and the senior members of the profession they will be able to run the branch in a very smooth manner. The members and students of Kannur and adjoining areas will be hugely benefited by the branch.

5

Date Programme Chief Guest/ Faculty/Beneficiaries

_______________________________________________________________________________________

06-02-2012 Inauguration of the branch at Hotel Royal Omars CA G Ramaswamy, Coimbatore st

28-02-2012 1 Managing Committee Meeting

04-03-2012 CPE Seminar on Recent Amendments in Service Tax CA P Rajendrakumar, Chennai

nd15-03-2012 2 Managing Committee Meeting

20-03-2012 Discussion on Union Budget jointly with CA C Suresh Kumar, Kannur

Malabar Chamber of Commerce

24-03-2012 3 Hours CPE Seminar on Bank Audit CA A Mony, Calicut

Hotel Malabar Residency

29-03-2012 CPE Committee Meeting

21-04-2012 3 Hours CPE Seminar on Labour Laws Adv C B Mukundan, Thrissurrd21-04-2012 3 Managing Committee Meetingth09-05-2012 4 Managing Committee Meeting

19-05-2012

& 12 Hours CPE Workshop on Advanced EXCEL CA Gopalkrishna Raju, Chennai

20-05-2012 for 2 daysst07-06-2012 1 Batch of 100 Hours ITT Programme 19 Studentsth05-06-2012 5 Managing Committee Meeting

08-06-2012 6 Hours CPE Seminar on Taxation of Charitable CA Phalgunakumar, Thirupathi

Trusts & Real Estate Transactionsst

15-06-2012 1 Batch of 35 Hours Orientation Programme 47 Students nd

28-06-2012 2 Batch of 100 Hours ITT Programme 19 Students

01-07-2012 CA Day Celebration at Hotel Central Avenue Prof Richard Hay (Principal Rtd.)

Dept. of Collegiate Education

03-07-2012 Inauguration of Kannur Branch of SICASA Dr P K Michael Tharakan,

at Hotel Malabar Residency Vice Chancellor, Kannur University

03-07-2012 Full day Workshop on Revised Schedule VI CA Saravana Prasath, Chennai

for Students at Hotel Malabar Residency

14-07-2012 12 Hours CPE Workshop on Service Tax CA V Prasannakrishnan, Chennai

& for 2 days at Hotel Malabar Residency CA T R Rajeshkumar, Bangalore

15-07-2012 CA Ganesh Prabhu, Chennaird23-07-2012 3 Batch of 100 Hours ITT Programme 19 Students

27-07-2012 First Annual General Body Meeting

18-08-2012

Activities of Kannur Branch of SIRC of ICAI

6

& SIRC Conference at Bangalore 23 Members

19-08-2012th

23-08-2012 4 Batch of 100 Hours ITT Programme 14 Students

01-09-2012 Seminar on Stress Management Yogacharya Vijayaraghavan, Calicut

01-09-2012 Onam Celebration at Hotel Malabar Residency CA M P Parameswaran Namboodirith

08-09-2012 6 Managing Committee Meeting

22-09-2012 National Debate Contest

06-10-2012 3 Hours CPE Seminar on Issues in Central Excise CA V Prasannakrishnan, Chennai

19-10-2012 Library Committee Meetingth08-11-2012 7 Managing Committee Meeting

10-11-2012 3 Hours CPE Programme - Interaction with ROC Mr Joseph Jackson, ROCth 19-11-2012 5 Batch of 100 Hours ITT Programme (Morning) 19 Studentsth 19-11-2012 6 Batch of 100 Hours ITT Programme (Afternoon) 19 Studentsth

30-11-2012 8 Managing Committee Meetingnd

02-12-2012 2 Batch of 35 Hours Orientation Programme 50 Students rd09-12-2012 3 Batch of 35 Hours Orientation Programme 53 Studentsth 10-12-2012 7 Batch of 100 Hours ITT Programme (Morning) 19 Students th

10-12-2012 8 Batch of 100 Hours ITT Programme (Afternoon) 19 Students

14-12-2012 ID Course for Students - Expect the Unexpected JC Er K Pramod Kumar

JCI Corporate Trainer

22-12-2012 3 Hours CPE Workshop on Capacity Building Mr Kannan Nambi, Chennai

Measures through IT Tools Mr C P Nisar, Bangalore

th 26-12-2012 9 Batch of 100 Hours ITT Programme (Morning) 19 Studentsth

26-12-2012 10 Batch of 100 Hours ITT Programme (Afternoon) 19 Studentsth

01-01-2013 4 Batch of 35 Hours Orientation Programme 50 Students th03-01-2013 9 Managing Committee Meeting

11-01-2013 12 Hours Residential CPE Conference CA C Suresh Kumar,Kannur

to at Kadkani River Resort, Ammathi, CA T V Ranjith Kumar, Payyannur

13-01-2013 Madikkeri, Karnataka CA Prasanth D Pai, Kannur

JC Cherian Varghese, Kottayam

JCI Corporate Trainer th

14-01-2013 11 Batch of 100 Hours ITT Programme (Morning) 19 Studentsth 14-01-2013 12 Batch of 100 Hours ITT Programme (Afternoon) 19 Students

th 20-01-2013 5 Batch of 35 Hours Orientation Programme 40 Studentsth

24-01-2013 10 Managing Committee Meeting

7

The Finance Minister presented the Budget th

for the year 2012-13 on 16 March, 2012. The Finance Act, 2012, containing 119 sections relating to Direct Taxes was passed by both Houses of Parliament and received the assent of the President on 28.05.2012.

Relief in Income tax for Individuals, HUF,

AOP, BOI etc. Basic exemption limit enhanced from

Rs.1.8 lac to Rs.2 lac. Upto Rs.8 lakh income these

assesses will get a benefit of Rs.2,000/- If total

income exceeds Rs.10 lac benefit of Rs.22,000/-

For other assesses no change in rates of

taxes. MAT payable at 18.5% and Dividend

distribution tax @ 15% alongwith surcharge and

education cess.

Provisions of Alternate Minimum Tax

(AMT) @ 18.5% plus education cess payable by all

assesses other than a company from 13.14 A.Y.

Surcharge on Income Tax – No surcharge is

payable by non-corporate assesses. In the case of

company, surcharge is 5% on income tax, if income

exceeds Rs. 1 crore

No surcharge on TDS/TCS. Surcharge on

Dividend Distribution tax u/s.115O and 115R @ 5%

on tax of 15%. For foreign companies, the rate of

surcharge on income tax is 2% of tax, if taxable

income exceeds Rs. 1 crore.

Education cess: Existing rate of 3%

(including 1% higher education cess) retained. No

education cess is applicable on TDS or TCS from

payments to all residents (including Companies).

However, if tax is deducted from payments made to

(a) foreign companies (b) non-residents or (c) on

salary payments to residents or non-residents,

education cess of 3% of tax and surcharge is to be

deducted.

Amendments in Direct Tax provisions by the Finance Act, 2012

CA C Suresh KumarKannur

Tax Deductions and collection at source.

Sec.193 – Existing limit of Rs.2,500/- for non

deduction enhanced to Rs.5000/- w.e.f. 01.07.2012 on

interest payable to resident individual on debentures

issued by a limited company. This concession

extended to HUF as well and debentures issued by

unlisted public companies.

Sec.194 J – Company to deduct TDS from any

remuneration, fees or commission paid or payable to a

director, if no tax is deductible u/s.192 under the head

salary. Rate is 10% Basic limit of Rs.30,000

provided u/s.194J as regards professional fees,

technical service fees, royalty etc. not applicable.

Hence payment of fees to non executive directors and

independent directors tax at 10% to be deducted even

if less than Rs.30,000/-. To be effective from

01.07.2012.

Sec.194LA – Existing limit of Rs.1 lac is enhanced to

Rs. 2 lac w.e.f. 01.07.2012.

Sec.194LC: - New section introduced w.e.f.

01.07.2012. It provides for deduction of tax at the

concessional rate of 5% plus applicable surcharge and

education cess, in respect of interest paid to a non-

resident, other than a foreign company on certain

borrowings.

Sec.201:- The existing time limit of 4 years from the

end of the financial year in a case where no returns for

tax deducted at source have been filed available for

the Assessing Officer to pass order, enhanced to 6

years with retrospective effect from 01.04.2010.

Sec.206C – TCS provisions extended to sale of

minerals, being coal or lignite or iron ore @ 1% on

sale price. However, exempted if buyer of such goods

has given declaration in Form NO.37C

8

Seller of bullion or jewellery to collect 1% of

sale consideration as TCS Basic exemption limit Rs.2

lakhs for bullion and Rs. 5 lacs for jewellery. Bullion

does not include gold coins or any other article

weighing ten grams or less. So person buying for

personal use to lose as they cannot claim credit for TCS.

Sec.207 – A senior citizen who has no income from

business or profession need not pay any advance tax.

Exemptions and deductions:

Charitable Trust – New sub section (8) has been

inserted in Sec. 13 and a proviso added in

Sec.10(23C), with retrospective effect from A.Y.

2009-10, to provide that the trust or institution will

not be granted exemption only for the year in which

such receipts exceeds Rs.25 lakhs and such loss of

exemption in that year will not affect the registration

of the trust or institution u/s.12AA

Section 10(10D) – The existing limit for premium

payment of 20% of the actual capital sum assured for

claiming exemption is reduced to 10%. This is

applicable only for policies taken after 01.04.2012.

Similar amendment made u/s.80C as well. Actual

capital sum assured also defined to exclude bonus or

value of any premiums agreed to be returned.

A few amendments also made in Section 10(23FB) –

Venture capital company, Sec.10(23BBH) Prasar

Bharati, Sec. 10(48) income of foreign company

received in India, in Indian currency, on account of

sale of crude oil to any person in India.

Sec.80CCG – Resident individuals whose gross total

income for the relevant assessment year does not

exceed Rs.10 lakhs, will be allowed deduction of 50%

of the amount invested subject to a limit of deduction

of Rs.25,000/- in the computation of income for the

year of investment. The assessee should make the

above investment in retail category specified in the

scheme and the investment should be in listed equity

shares specified under the scheme with a minimum

lock in period of 3 years. If the assessee fails to

comply with any of the above conditions in any year,

the amount of deduction allowed in earlier years will

be taxable in that year.

Sec.80D – The benefit under this section extended to

payments upto Rs.5000 in a year for preventive health

check up. Deduction will be allowed within the

existing ceiling limit of Rs.15,000 normally and

Rs.20,000/- for senior citizens. Age limit for senior

citizens is reduced from 65 years to 60 years.

Sec. 80G and 80GGA – Deductions for donations of

Rs.10,000 or more will be allowed only if the same is

not paid in cash.

Sec.80 IA(4)(iv) – The existing time limit to begin its

activities on or before 31.03.2012 is extended to on

or before 31.03.2013.

Section 80TTA – In the case of an individual or HUF

interest from savings bank account with a bank, co-

operative bank or post office bank upto Rs.10,000

will not be taxable. This provision will not apply to

fixed deposit interest.

Section 115-O – By amendment of this section,

effective from 01.07.2012, the condition that “the

company is not a subsidiary of any other company”

in the existing section for claiming the deduction is

removed.

Income from business or profession:

Section 32(1)(iia): The benefit of additional

depreciation of 20% of the cost of new plant and

machinery in the year of acquisition is extended to an

assessee engaged in the business of generation or

generation and distribution of power as well.

Section 35(2AB) – The existing time limit of

31.03.2012 for this deduction of 200% of

expenditure on approved inhouse research and

development by a company engaged in the business

of biotechnology or in the manufacture of specified

articles is extended upto 31.03.2017.

Sec.35AD –

1. Investment linked deduction of 100% of capital

expenditure (excluding for land, good will or

financial instrument) allowed for existing 8 specified

businesses extended to 3 more businesses viz: setting

up and operating (1) inland container depot or

container freight station (2) warehousing facility for

storage of sugar and (3) beekeeping and production

of honey bee wax which commence operations on

or after 01.04.2012.

2. The above investment linked deduction enhanced

to 150% of the capital expenditure incurred on or

after 01.04.2012 in respect of certain specified

businesses which commence operations on or after

9

01.04.2012. These specified businesses are setting up

and operating (a) cold chain facility, (b) warehousing

facility for agricultural produce, (c) building and

operating a hospital with at least 100 beds (d)

developing and building affordable housing project

and (e) production of fertilizer in India.

3. Assessee who builds a hotel of two star or above

category as classified by the Central Government and

subsequently, while continuing to own the hotel,

transfers the operation thereof, shall be deemed to be

engaged in specified business and will be eligible to

claim benefit u/s.35AD. This amendment has been

made with effect from A.Y. 2011-12.

New sections 35CCC and 35CCD: When an assessee

incurs any capital or revenue expenditure for

agricultural extension project notified by the CBDT,

deduction of 150% of such expenditure will be

allowed under Sec. 35CCC.

Where a company incurs expenditure (other than

expenditure on any land or building) on any skill

development project notified by the CBDT, it will be

allowed deduction of 150% of such expenditure.

Sec.40(a)(ia) – By amendment of this section it is

provided that if the assessee establishes that the

resident payee (deductee) has paid tax on this income

before furnishing his return of income, the

expenditure shall not be disallowed under this section.

This amendment is made from A.Y. 2013-14.

Consequential amendments made in Sec.201 as well,

w.e.f. 01.07.2012. However, the payer will have to

pay interest from the due date till the date of filing of

the return by the payee. It may be possible to argue

that the above beneficial amendment will have

retrospective effect in view of the decision in CIT vs.

Virgin Creations of the Calcutta High Court.

Presumptive taxation:

It is now provided that this section will not apply to a

person having income from (i) a profession, (ii)

commission or brokerage or (iii) any agency business.

This amendment is made effective from A.Y. 2011-12.

Further, the limit of Rs.60 lac for total turnover is

increased to Rs.1 crore w.e.f. A.Y. 2013-14

(Accounting year 2012-13).

Section 44AB:- The limit of turnover/gross receipts

for tax audit u/s.44AB has also been increased for

business to Rs.1 cr. and for profession to Rs.25 lac

w.e.f. A.Y. 2013-14.

Capital Gains.

Section 47(vii)

It is now provided that when a subsidiary company

amalgamates with a holding company, the

requirement of the issue of shares of the amalgamated

company on amalgamation will not apply.

Section 49:

It is now provided, w.e.f. A.Y. 1999-2000, that the cost of

assets on conversion of a proprietary concern or a firm into a

company u/s.47 (xiii), or 47(xiv), in the hands of the

company shall be the same as in the hands of the converting

enterprise. Similarly, when an unlisted company is

converted into LLP u/s.47(xiiib), the cost of assets in the

case of the company shall be treated as cost in the case of the

LLP.

Section 50D:

It provides that where the consideration received or accrued

for transfer of a capital asset is not ascertainable or cannot

be determined, then the fair market value of the said asset

shall be deemed to be the full value of the consideration on

the date of transfer for computing the capital gain. This

situation may arise in a case where the capital asset is

transferred in exchange of another capital asset.

Section 54B

This provision is amended, w.e.f. A.Y. 2013-14, to provide

that even if such land was used by the HUF, in which the

assessee or his parent was a member, this exemption can be

claimed.

Section 54GB

This is a new section which is inserted w.e.f. AY. 2013-14 to

provide that if an individual or HUF makes capital gains on

sale of a residential house or plot, he can claim exemption

from capital gains tax if he invests the net consideration in

equity shares of a new SME company. Such SME company

is required to invest this amount in purchase of new plant

and machinery. This exemption can be claimed subject to

satisfying specified conditions.

Section 55A – Reference to Valuation Officer:

In some cases it is held that when the assessee exercises his

option to substitute fair market value of the capital asset as

on 01.04.1981, for the cost of the asset, and if the AO is of

the view that such market value as declared by the assessee

10

was more, he cannot make a reference to the Valuation

Officer. To overcome this position, this amendment

provides that w.e.f. 01.07.2012 the AO can make such

reference to the Valuation Officer. This amended provision

will apply w.e.f. 01.07.2012 but will have retrospective

effect, inasmuch as, the AO can make such a reference to

the Valuation Officer in respect of all pending assessment

of earlier years.

Securities Transaction Tax (STT)

Section 98 of the Finance (No.2) Act, 2004, providing for

rates of STT has been amended w.e.f. 01.07.2012. The

revised rate of STT in Cash Delivery Segment is reduced

from 0.125% to 0.1%.

Income from other Sources:

Section 56(2)(vii)

It is now provided, w.e.f. 01.10.2009, that gifts received by

HUF from its members will be exempt.

Section 56(2)(viib):

This is a new provision inserted from the A.Y.2013-14. It is

now provided that where a closely held company issues

shares to a resident, for amount received in excess of the

fair market value of the shares, it will be deemed to be the

income of the company under the head “income from other

Sources”.

This provision will not apply to amounts received by a

venture capital undertaking from a venture capital fund or a

venture capital company.

Section 68:

This section now provides that in the case of a closely held

company, if the amount credited in the name of a resident is

by way of share application money, share capital, share

premium or any such amount, by whatever name called,

and the explanation offered for the credit is not considered

to be satisfactory, such amount will be considered as

income of the company.

This provision does not apply to amount received from a

venture capital fund or a venture capital company. It will

also not apply to the amount received from a non-resident

or a foreign company.

Section 115BBE

This is a new section inserted from A.Y. 2013-14. The

section provides that unexplained amounts treated as

income (i) u/s.68 cash credits, (ii)u/s.69 unexplained

investment, (iii) u/s.69A unexplained money, bullion,

jewellery or other valuable articles, (iv) u/s.69B amount of

investments, expenditure on jewellery, bullion or other

valuable articles not fully disclosed in books, (v) u/s.69C –

Unexplained expenditure, and (vi) u/s.69D – Amount

borrowed or repaid on a Hundi in cash, will now be taxed at

a flat rate of 30% plus applicable surcharge and education

cess. No deduction for any expenditure or allowance will

be allowed against such income.

Minimum Alternate Tax (MAT)(sec 115JB)

(i) The section is amended w.e.f. A.Y. 2013-14 to provide

that in the case of a company, such as insurance, banking,

electricity company, etc., for which the form of Profit &

Loss A/c. and Balance Sheet is prescribed in the Act

governing such companies, the book profit shall be

determined on the basis of the Form of Profit & Loss A./c.

prescribed under that Act. Further, it is provided that in

respect of companies to which the Companies Act applies,

the book profit will be computed on the basis of the revised

format of Schedule VI.

(ii) By another amendment of this section effective from

A.Y. 2013-14, it is now provided that the book profit will

be increased by the amount standing to the credit of

revaluation reserve relating to revalued asset which has

been discarded or disposed of, if the same is not credited to

the Profit & Loss Account.

Alternate Minimum Tax (AMT)

Sections 115JC to 115JE for levy of AMT on adjusted total

income of LLP have now been extended to other non-

corporate assesses such as individual, HUF, AOP, BOI,

Firm, etc. w.e.f. A.Y.2013-14. New section 115JEE has

also been added from A.Y. 2013-14.

Specified domestic transactions:

Section 40A(2), Sections 10AA, 8oA, 8oIB, etc.

In all these sections, the concept of 'fair market value' has

not been specifically explained. Therefore, the Supreme

Court in the case of CIT v. Glaxo Smithkline Asia (P) Ltd.,

195 Taxman 35 (SC) observed that in order to reduce

litigation, sections 40A(2) and 8o1A(10) need to be

amended to empower the AO to make adjustments to the

income declared by the assessee, having regard to the

market value of the transactions between related parties,

by applying any of the generally accepted methods for

determination of Arm's Length Price(ALP), including

methods provided under Transfer Pricing Regulations. In

view of the above, amendments are made in sections

11

40A(2), 10AA, 8oA and 8o1A to provide that the 'Specified

domestic transactions' will now be subject to Transfer

Pricing Regulations contained in sections 92,93BA to 02F

– from A.Y. 2013-14 (Accounting Year 01.04.2012 to

31.03.2013)

It is also provided that the transfer pricing provisions will

not apply if the aggregate amount relating to the above

transactions entered into by the assessee, in relevant

accounting year, does not exceed 5 crores..

Taxation of non-residents:

Many sections dealing with taxation of non-residents have

been amended with retrospective effect. These

amendments will have far reaching effect. While

presenting the Budget the Finance Minister has not made

any mention about these far-reaching changes affecting

the non-residents in his Budget Speech. However, in the

Explanatory Memorandum attached to the Finance Bill,

2012, the reasons for these retrospective amendments have

been explained.

Amendments have been made by the Finance Act, 2012 in

the following Section viz:.

Section 2(14): Section 2(47),Section 9:Section 9(i)(vi) –

Royalty: Sections 90 and 90A: Section 195:Section 163

Section 119 of the Finance Act, 2012 Section 115A

Section 115BBA and Section 112.

The effect of these amendments with retrospective effect

will be that cases of many assesses may be reopened and

they may be required to pay tax, interest or penalty for last

16 years. It appears that these amendments provide for

taxing gain on sale of shares in foreign countries and

therefore, the time limit of 16 years for reopening the

assessments will apply to such transactions. It is,

therefore, necessary that a specific provision should have

been made so that no interest or penalty will be payable if

tax levied as a result this retrospective amendment is paid

by the assessee.

It is hoped that the CBDT issues Circular in respect of the

tax payable as a result of these retrospective amendments

made by the Finance Act, 2012.

Transfer pricing provisions in

Section 92B, Section 92C, Section 92CA Advance

Pricing Agreement amended

General Anti-Avoidance Rule (GAAR) In new Chapter

X-A, Sections 95 to 102 have been inserted originally,

made applicable from Assessment year 2014-15.

GAAR provisions Section 95, Impermissible

Avoidance Arrangement (section 96),Lack of

commercial substance (section 97), Consequence of

impermissible avoidance arrangement (section 98),

Section 99, Section 144BA etc. were introduced.

This is a new concept introduced in the Income Tax Act

by the Finance Act, 2012. Very wide powers are given

to the Tax Authorities by these provisions. However,

due to uproar from Industry and public an expert

Committee under the Chairmanship of Dr. Partha

Sarathy Shome was appointed later on. On the

r ecommenda t ion o f th i s Commi t t ee the

implementation of these provisions are deferred till

Asst. year 2017-18.

Assessment, reassessment and appeals:

Section 139 – Return of income:

(i) This section is amended from A.Y. 2012-13 (Accounting

year ending 31.03.2012). The amendment now requires

that a resident and ordinarily resident, who is otherwise not

required to furnish a return of income, will be required to

furnish his return of income before the due date for filing

the return in the following cases:

(a) If the person has any asset located outside India.

This will mean that if the person owns any immovable

property outside India, any shares in a foreign

company, any bank account or other assets outside

India, he will have to file return even if the total

income is below the taxable limit.

(b) If the person has any financial interest in any entity

in a foreign country. This will mean that if the person is

a beneficiary in any specific or any discretionary foreign

trust, he will have to file his return of income whether he

has received any benefit from the turst or not.

(c) If the person has signing authority in any account

located outside India.

It may be noted that in a case where the person

(whether resident or non-resident) has taxable income

in India, he will have to give information about the

above items in the form of return of income

prescribed for A.Y. 2012-13.It is now provided that th

the extended time limit up to 30 November will

apply to all assesses who are required to file Transfer

Pricing Report u/s.92E.

Section 143 – Procedure for assessment:

At present, the return is required to be processed

12

u/s.143(1) even if the case is selected for scrutiny. The

section is now amended, effective from 01.07.2012, to

provide that if the case is selected for scrutiny, the AO

is not required to process the return of income

u/s.143(1). This will mean that if the person has

claimed refund in the return of income and his case is

taken up for scrutiny, the refund if due, will be issued

only after completion of assessment u/s.143(3).

Section 144C – Reference to DRP

This section is now amended w.e.f. 01.10.2009 to

provide that the DRP can consider any other matter

relating to the draft assessment order while enhancing

the variation. It may be noted that this amendment

does not clarify whether the DRP can consider any

other matter brought to its notice by the assessee

which has the effect of reducing the income or

increasing the loss.

It may be noted that from A.Y. 2013-14, cases in which

specified domestic transactions are there will now be

referred to TPO. Therefore, the above procedure of

making draft order and reference to DRP will apply in

such cases also.

Sections 147 and 149 – Reassessment of income:

These two sections dealing with income-escaping

assessment and time limit for reopening assessment

have been amended w.e.f. 01.07.2012.

At present, the time limit for reopening assessment is 6

years. In a case where assessment is made u/s.143(3)

and the income-escaping assessment is not due to

failure of the asessee to disclose fully and truly all

material facts necessary for assessment for that year,

the time limit for reopening is 4 years. This time limit

is now enhanced in specified cases.

It is now provided that if the income in relation to any

asset (including financial interest in any entity)

located outside India, chargeable to tax, has escaped

assessment for any year, the time limit for reopening

the assessment shall be 16 years. For this purpose,

where a person is found to have any asset or any

financial interest in any entity located outside India,

shall be deemed to be a case where income chargeable

to tax has escaped assessment. This provision will

apply to a resident or a non-resident.

It is now provided that if a person has failed to furnish

the Transfer Pricing Report u/s.92E in respect of any

international transaction, income shall be deemed to

have escaped assessment.

Similar amendments are made in the Wealth Tax Act

also.

Sections 153 and 153B –Time limit for completion of

assessments:

These sections are amended w.e.f. 01.07.2012. At

present, the time limit for completion of assessment or

reassessment proceedings is 21 months. In a case

where reference is made to the Transfer Pricing

Officer, the time limit for completion of assessment is

33 months This time limit is extended 3 months.

Sections 153A and 153C – Assessment in case of

search or requisition:

It is now provided that the Central Government can

notify cases or class of cases where the Assessing

Officer shall not be required to issue notice for

initiation of assessment/ reassessment proceedings for

six preceding assessment years and proceedings may

only be taken up for the assessment year relevant to the

year of search or requisition.

Sections 154 and 156:

It is now provided that any mistake apparent from the

record in the intimation issued u/s.200A shall be

rectifiable u/s.154. It is also provided that the

intimation issued u/s.200A shall also be deemed to be

a notice of demand u/s.156 and an appeal can be filed

with the Commissioner of income tax (Appeals)

u/s.246A.

Section 245C – Settlement Commission:

At present an application can be filed before the

Settlement Commission u/s.245C by a related person

who has substantial interest of more than 20% of the

profits of the business at any time during the previous

year. Now, it is provided that the substantial interest

should exist on the date of search and not at any time

during the previous year.

Section 245N: Authority for Advance Ruling

(AAR)

By this amendment it is provided that an assessee can

approach the AAR for determination or decision

whether an arrangement which is proposed to be

undertaken by any person (resident or non-resident) is

an impermissible arrangement as provided in sections

95 to 102. This will enable the person entering into an

13

arrangement to get an Advance Ruling from AAR if he

apprehends that the AO may invoke GAAR

provisions during assessment proceedings.

Section 245Q – Fees for filing application for

Advance Ruling:

Fees for filing an application before the Authority for

Advance Ruling is increased from Rs.2,500 to

Rs.10000 w.e.f. 01.07.2012.

Section 246A – Appealable orders before CIT(A)

The list of orders against which appeals can be filed

before the CIT (A) has now been expanded.

i. The tax deductor can file appeal on after

01.07.2012 against the intimation issued

u/s.200A relating to short deduction of tax at

source.

ii. The assessee can file appeal against the order

passed by the AO u/s.153A in search cases if

such order is not passed in pursuance of the

directions of the DRP. This will be effective

from 01.10.2009.

iii. The assessee can file appeal against the order

of assessment or reassessment passed under

new section 92CD(2) after furnishing the

modified return based on the Advance Pricing

Agreement as provided in the new section

92CC.

iv. Penalty order passed under new section 271

AAB where search has been initiated. This is

effective from 01.07.2012.

Section 253 – Appeals before ITA Tribunal:

i. The following amendment is made w.e.f.

01.04.2013

Any order passed by the AO u/s.143(3), 147,

153A or 153C in pursuance of the order

passed by the CIT u/s.144BA(12) in

accordance with the directions by the

Approving Panel or the CIT, declaring any

arrangement as impermissible avoidance

arrangement, is appealable directly to the ITA

Tribunal.

ii. The following amendments are made with

reference to DRP cases:

a) The directions given by the DRP in the case of

a foreign company or any person in whose

case variation in the income arises due to

order of the Transfer Pricing Officer are

binding on the Assessing Officer. It is now

provided that the Assessing Officer can also

file an appeal before the ITA Tribunal against

an order passed in pursuance of directions of

the DRP in respect of objections filed on or st

after 1 July, 2012.

b) The Assessing Officer or the assessee is

entitled to file memorandum of cross

objections on receipt of notice that an appeal

has been filed by the other party.

c) Any order passed u/s.153A or 153C in

pursuance of directions of the DRP shall be

directly appealable to the ITA Tribunal w.e.f. st

1 October, 2009. Presently, such appeals are

being filed with the Commissioner

(Appeals).

Section 292CC

In the case of CIT v. Smt. Vandana Verma, 330 ITR

533 (All.) it was held that if search warrant is in the

name of more than one person, then assessment

cannot be made individually in the absence of any

search warrant in the individual name. To overcome

this judgment, it is now provided in this new section,

with retrospective effect from 01.04.1976, that where

a search warrant has been issued mentioning names of

more than one persons, the assessment/reassessment

can be made separately in the name of each of the

persons mentioned in such search warrant.

Penalties and prosecution:

Section 234E – Fees for delay in furnishing

TDS/TCS statement:

Newly inserted section 234E now provides for levy of

fees of Rs.200 for every day of the delay in furnishing

TDS/TCS statements. However the total fee shall not

be more than the amount of tax deductible/collectible

for the quarter for which the TDS/TCS statement is

delayed. The fee is to be paid before the delivery of

the TDS/TCS statements. Consequently levy of

penalty provided in section 272A(2)(k) is deleted. It

may be noted that no appeal against levy of fees

payable u/s.234E is provided in section 246A.

14

Section 271 – Penalty for concealment –

Amendment w.e.f. 01.04.2013

The transfer pricing regulations are extended to

specified domestic transactions entered into by

domestic related parties. If any amount is added or

disallowed, based on the arm's length price

determined by the Assessing Officer, it is now

provided that such addition/disallowance shall be

deemed to represent the income in respect of which

particulars have been concealed or inaccurate

particulars have been furnished as provided in

Explanation 7 to section 271(1) and it is liable to

penalty accordingly.

Section 271AA – Penalty for failure to report, etc.

of international and specified domestic

transactions:

A levy of penalty at the rate of 2% of the value of the

international transaction is provided, if the taxpayer.

a) fails to keep and maintain prescribed

information and documents u/s.92D(1) or (2)

b) fails to report any international transaction

u/s.92E, or

c) maintains or furnishes any incorrect

information or documents.

ii) Amendment w.e.f. 01.04.2013.

Section 271G – Penalty for failure to furnish

information or documents u/s.92D

At present section 271G provides for levy of penalty at

2% of the value of transaction for failure to furnish

information or documents u/s.92D which requires

maintenance of certain information and documents in the

prescribed proforma by the persons entering into an

international transaction. This penal provision will now

apply to persons entering into specified domestic

transactions for such failure effective from A.Y. 2013-14.

Section 271H Penalty for failure to furnish

TDS/TCS statements:

A penalty ranging from Rs.10,000 to Rs.1,00,000 is

leviable for these failures. No appeal against the levy

of this penalty is provided u/s.246A.

It is also provided that no such penalty will be levied if

the deductor delivers the statement within a year from

the due date and the person has paid the tax along with

fees and interest before delivering the statement.

Sections 271AAA and 271AAB – Penalty on

undisclosed income found in the course of search:

(i) At present, penalty in the case of search initiated on st

or after 1 June, 2007 is not leviable u/s.271AAA

subject to certain conditions, such as:

a) the assessee admits the undisclosed income in a

statement u/s.132(4) recorded during the search,

b) he specifies the manner in which such income has

been derived, and

c) he pays the tax together with interest, if any, in

respect of such income.

Now, section 271AAA will not apply to search stinitiated on or after 1 July, 2012.

(ii) Newly inserted section 271AAB now provides for

levy of penalty on undisclosed income of specified

previous years where search has been initiated on or st

after 1 July, 2012 as under:

a) If the assessee admits undisclosed income

during the course of search in a statement

u/s.132(4), specifies the manner in which

such income has been derived, pays the tax

with interest on such income and furnishes

return of income declaring such income,

penalty shall be 10% of undisclosed income.

b) If undisclosed income is not so admitted

during the course of search, but disclosed in the

return of income filed after the search and he pays

the tax with interest, penalty shall be 20% of

undisclosed income.

c) In other cases, the minimum penalty shall be

30% subject to maximum of 90% of the

undisclosed income.

Other amendments

Senior citizens:

In various section of the income tax Act the age limit

for senior citizens was fixed at 65 years. This has

now been reduced to 60 years w.e.f. A.Y. 2013-14

(Accounting year 2012-13)

Sec.44AB audit

The limit of turnover or gross receipts for this

purpose has now been increased to Rs.1 crore in the

case of business and Rs.25 lac in the case of

profession. Further, date for obtaining tax audit

15

threport which is 30 September has been changed to

the due date of filing return of income u/s.139(1) as

applicable to the assessee. The amendment

increasing the limit for turnover/gross receipts will

come into force from A.Y. 2013-14.

Section 115VG – Computation of daily tonnage

income for shipping companies.

By this amendment these rates are enhanced.

Section 209 – Advance tax calculation

At present, for the purpose of calculation of advance

tax liability, tax deductible or collectable at source

was required to be reduced even though the tax was

actually not deducted. Therefore, in such cases, there

was no interest liability. Now it is provided that

unless such tax is actually deducted, there will be

advance tax liability. This amendment is made w.e.f.

01.04.2012.

Section 234D – Interest on excess refund:

The Delhi High Court in DIT v. Jacobs Civil

Incorporated, (2011) 330 ITR 578 held that this

provision will apply from the A.Y. 2004-05 and no

interest is payable for the earlier assessment years. To

overcome this decision, it is now provided that

interest shall be payable u/s.234D on excess refund

for any earlier assessment years if the proceedings in

respect of such assessment are completed after

01.06.2003.

Wealth Tax Act, 1957.

Section 2 (ea) – Definition of 'Assets'

At present, any residential unit allotted to officers,

employees or whole-time directors is exempt from

wealth tax if the gross annual salary of such person is

less than Rs.5 lac. This limit of gross annual salary is

increased to Rs.10 lac. This amendment is effective

from A.Y. 2013-14.

Section 17 – Weath- escaping asssessment

This section is amended w.e.f. 01.07.2012 – It is now

provided in this section that if any person is found to

have any asset or financial interest in any entity

located outside India, it will be deemed to be a case

where net wealth chargeable to tax has escaped

assessment. In such cases the wealth tax assessment

can be reopened by the AO within 16 years.

The author is a fellow member of the Institute of Chartered Accountants of India, who can be reached at [email protected]

Section 17A – Time limit for completion of

assessment and reassessment

This section is amended w.e.f. 01.07.2012. This

amendment has the effect of increasing the time limit

by 3 months for completion of assessment/

reassessment proceedings.

Section 45

This section provides for exemption from wealth tax

to section 25 companies, co-operative societies,

social clubs, recognized political parties, mutual

funds, etc. This list is now expanded to provide that

the 'Reserve Bank of India' will not be liable to pay

wealth tax w.e.f. 01.04.1957.

Though the tax burden of individuals, HUF etc. have been reduced and some beneficial provisions have been introduced to remove practical difficulties, there are many areas in which the tax payers will have to face many practical difficulties.

News Letter Committee

1. CA Dinesh K Kumar

2. CA Gangadharan TO

3. CA Reji PJ

4. CA Jacob PJ

5. CA Prasanth D Pai

Cover Design and Layout

CA Sreejith T

16

1. (2012) Tax Corp(ST) 12001 (HC-AP) -

Back office services do not come under the ambit of 'information technology service' The High Court held that back office services like preparation of federal tax returns, co-sourcing services, analyzing client data and calculating estimates of tax amount do not come under the ambit of 'information technology service' even though said services are performed by using computer programmes. Further, the High Court also observed that if a decision of Tribunal is approved by the Supreme Court by a non-speaking order, it does not mean that the reasoning in the order of Tribunal is also approved by the Supreme Court. 2. (2012) Tax Corp (ST) 12003 (HC-DELHI) INTERCONTINENTAL CONSULTANTS AND TECHNORATS PVT. LTD vs UOI & Ars –

High Court struck down constitutional validity of Rule 5 of the Service Tax (Determination of Value) Rules, 2006 to the extent it includes reimbursement of expenses The High Court struck down constitutional validity of Rule 5 of the Service Tax (Determination of Value) Rules, 2006 to the extent it includes reimbursement of expenses in value of taxable services for the purpose of charging service tax on the ground that it ultra virus Section 66 and 67 of Chapter V of the Finance Act, 1994 (“the Finance Act”) because it goes beyond charging provisions. 3. (2012) TaxCorp(ST) 11395 (CESTAT-NEW DELHI) –

Supply of materials in course of Annual Maintenance

SERVICE TAX – Recent Amendments, Notifications under Negative List, and Case Laws

CA P J RejiKannur

Contracts (AMCs) amounts to 'sale' and is eligible for deduction in computing value of taxable serviceSupply of materials in course of Annual Maintenance Contracts (AMCs) amounts to 'sale' of such materials, and value of such sale is eligible for deduction in computing value of taxable service. The dispute involved is that the appellants were not paying service tax on the full value realised under the contracts but were deducting value of materials supplied under each of the contract and was paying service tax on the service component – Held ,The issue is no longer res integra that in a contract for providing service of the type involved in this case the service component and value of materials can be separated - Notification 12/2003-ST also recognised this principle. 4 . M A P R A N A M F I N A N C E A N D INVESTMENT COMPANY (P) LTD vs UOI and Others (High Court) –

Whether the activity of the Chitty establishments was constituting any 'cash management' to attract service tax. Held, yes Service Tax on Chitty business - Consequence of the amendment to Section 65 (12)(a)(v) of the Finance Act 1994 in the year 2007, deleting the words "but does not include cash management" and the effect of the subsequent Circular bearing No. 6/7/2007-ST dated 23/08/2007 issued by the CBEC of the Ministry of Finance, New Delhi. As a result of the said amendment, the petitioners, who are running chitty business in the State of Kerala, were sought to be brought within the purview of the Service Tax Net which is under challenge. In the light of the definition of the terms, 'Banking and Financial Institutions under Section 65(12)(a)(v), "Taxable Service" under 65(105)(ZM) and the reference made to Section 45-

17

1, of the RBI Act under Section 65 (45) of the Finance Act 1994, defining the term 'Financial Institution' as inclusive of 'Chitty business' as well, under sub Clause (c)(v).

5. M/s NAGRJUNA CONSTRUCTION CO. LTD vs GOI & ANR (Supreme Court) –

Works contract, where service tax had already been paid, no option to pay service tax under the Composition Scheme could be exercised. (Service Tax - Works Contracts (Composition Scheme for Payment of Service Tax) Rules, 2007) In respect of a works contract, where service tax had already been paid, no option to pay service tax under the Composition Scheme can be exercised. Assessee who wants to avail of the benefit under Rule 3 of the 2007 Rules must opt to pay service tax in respect of a works contract before payment of service tax in respect of the works contract and the option so exercised is to be applied to the entire works contract and the assessee is not permitted to change the option till the said works contract is completed.

6. Institution Of Valuers vs UOI - Service Tax on Valuers

Held, Don't levy service tax on valuers. Services rendered as valuers don't fall within the ambit of services rendered by a consulting engineer as defined under the Finance Act, 1994. The government cannot levy service tax on land valuers because they are not necessarily consulting engineers. The “Consulting Engineers” throughout India (where the Finance Act has applicability) are not liable to pay service tax for the services provided by them as Valuers.”

7. Bazpur Co-operative Sugar Factory Ltd. Vs Commissioner of Central Excise, Meerut-II –

Individual truck owners are not liable for service tax CESTAT, NEW DELHI BENCH

Assessee, a manufacturer of sugar, collected raw material viz. sugarcane from farmers at various collection centres. Assessee engaged individual farmers for transportation of sugarcane from collection centres to factory and paid transportation charges. Assessee didn't pay service tax on transportation charges as recipient of service.- Department contended that individual truck-owners were goods transport agency and services provided by them were liable to service tax. It was held that only

persons issuing consignment notes are covered within 'goods transport agency'. A person who doesn't issue consignment note cannot be regarded as 'goods transport agency' and cannot be asked to issue consignment note under Rule 4B Hence, prima facie, goods transport services by individual truck owners viz. farmers was not liable to service tax. 8. M/s AMRAPALI BARTER PVT LTD & M/s VIJAY LAXMI PROMOTERS PVT LTD vs COMMISSIONER OF SERVICE TAX – No late fee / penalty when Nil returns filed Assessee although registered with the department had not provided any service during the period April, 2005 to March, 2008 and had not filed any returns. Assessee filed six ST-3 returns together for the period on 18/11/2008. Penalty was imposed u/s 77, simultaneously CIT(A) dropped the penalty and upheld the order of AO for late fees u/r 7C of STR. CESTAT observed that as per Rule 7C of the Service Tax Rule, in the event 'nil' returns are filed, the assessing officer had the discretion to waive the late fees for filing the ST-3 Returns. The order of the Ld. Commissioner (Appeals) is set aside and the appeals filed by the Appellants are hereby allowed.

9. Life Care Medical Systems vs. Comm. of ST –

Service used, rendered & enjoyed in India – Taxable in India

The hon'ble apex court in the case of All India Federation of Tax Practitioners v. Union of India [2007] 10 STT 166 (SC) makes the economic concept of service tax abundantly clear that to make the service activity leviable to tax, the services should be rendered in India. In the instant case, the service rendered is promotion/marketing of the goods of the client in India by rendering various services such as demonstration, installation, after sales warranty and advertising services for which the appellant received a consideration. These activities are rendered in India and their effective use and enjoyment are in India and therefore, the benefit of the services rendered also accrue in India and hence leviable to service tax.

The author is a fellow member of the Institute

of Chartered Accountants of India, who can be

reached at [email protected]

18

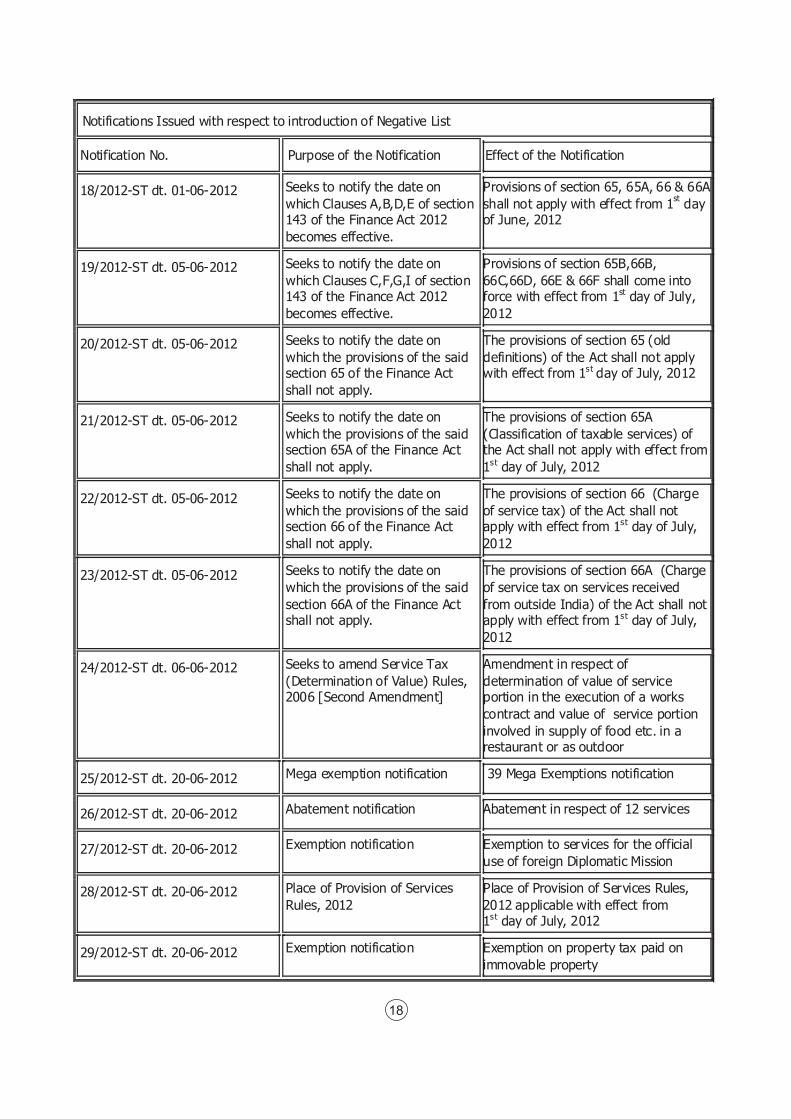

Notifications Issued with respect to introduction of Negative List

Notification No. Purpose of the Notification Effect of the Notification

18/2012-ST dt. 01-06-2012 Seeks to notify the date on

which Clauses A,B,D,E of section 143 of the Finance Act 2012

becomes effective.

Provisions of section 65, 65A, 66 & 66A

shall not apply with effect from 1st day

of June, 2012

19/2012-ST dt. 05-06-2012 Seeks to notify the date on

which Clauses C,F,G,I of section 143 of the Finance Act 2012

becomes effective.

Provisions of section 65B,66B,

66C,66D, 66E & 66F shall come into force with effect from 1st day of July,

2012

20/2012-ST dt. 05-06-2012 Seeks to notify the date on

which the provisions of the said section 65 of the Finance Act

shall not apply.

The provisions of section 65 (old

definitions) of the Act shall not apply with effect from 1st day of July, 2012

21/2012-ST dt. 05-06-2012 Seeks to notify the date on

which the provisions of the said section 65A of the Finance Act

shall not apply.

The provisions of section 65A

(Classification of taxable services) of the Act shall not apply with effect from

1st day of July, 2012

22/2012-ST dt. 05-06-2012 Seeks to notify the date on

which the provisions of the said section 66 of the Finance Act

shall not apply.

The provisions of section 66 (Charge

of service tax) of the Act shall not apply with effect from 1st day of July,

2012

23/2012-ST dt. 05-06-2012 Seeks to notify the date on

which the provisions of the said

section 66A of the Finance Act shall not apply.

The provisions of section 66A (Charge

of service tax on services received

from outside India) of the Act shall not apply with effect from 1st day of July,

2012

24/2012-ST dt. 06-06-2012 Seeks to amend Service Tax

(Determination of Value) Rules, 2006 [Second Amendment]

Amendment in respect of

determination of value of service portion in the execution of a works

contract and value of service portion

involved in supply of food etc. in a restaurant or as outdoor

25/2012-ST dt. 20-06-2012 Mega exemption notification 39 Mega Exemptions notification

26/2012-ST dt. 20-06-2012 Abatement notification Abatement in respect of 12 services

27/2012-ST dt. 20-06-2012 Exemption notification Exemption to services for the official

use of foreign Diplomatic Mission

28/2012-ST dt. 20-06-2012 Place of Provision of Services

Rules, 2012

Place of Provision of Services Rules,

2012 applicable with effect from 1st day of July, 2012

29/2012-ST dt. 20-06-2012 Exemption notification Exemption on property tax paid on

immovable property

19

30/2012-ST dt. 20-06-2012 Notification under sub-section

(2) of section 68

Applicability of reverse charge of service

tax on 10 items

31/2012-ST dt. 20-06-2012 Exemption notification Exemption to specified services received by exporter of goods

32/2012-ST dt. 20-06-2012 Exemption notification Exemption of services provided by

TBI/STEP

33/2012-ST dt. 20-06-2012 Exemption notification Exemption to small service providers of

taxable value not exceeding ten lakhs

34/2012-ST dt. 20-06-2012 Rescinding of certain

notifications

Rescinded 81 notification s issued from

30/06/1994 to 17/03/2012 w.e.f. 1st July, 2012

35/2012-ST dt. 20-06-2012 Rescinding of certain

notification

Rescinds the notification No. 32/ 2007 –

Service Tax, dated the 22nd May, 2007

36/2012-ST dt. 20-06-2012

Corrigendum dt. 02-07-2012

Seeks to amend Service Tax

Rules

Amendment in Service Tax Rules, 1994

and added RULE 6A - Export of services

37/2012-ST dt. 20-06-2012 Seeks to amend point of

Taxation Rules

Amendment in Point of Taxation Rules,

2011

38/2012-ST dt. 20-06-2012 Amendment Notification Amendment of Notification No. 28/2011-

ST

39/2012-ST dt. 20-06-2012 Notification under rule 6A of Service Tax Rules

Granting rebate of the whole of the duty paid on excisable inputs or the whole of

the service tax and cess paid on all input

services used in providing service exported

40/2012-ST dt. 20-06-2012 Exemption on services provided

to SEZ authorised operations

Exempts the services on which service tax

is

leviable received by a unit located in a Special Economic Zone or Developer of

SEZ

41/2012-ST dt. 29-06-2012 Seeks to provide refunds on

specified services to the exporter of goods

Grants rebate of service tax paid on the

taxable services which are received by an exporter of goods and used for export of

goods

42/2012-ST dt. 29-06-2012 Exemption Notification. Seeks to Exempt certain specified services

received by exporter of goods.

43/2012-ST dt. 02-07-2012 Exemption Notification. Seeks to Exempt certain specified services

provided by the Indian Railways upto and including the 30th day of

September, 2012.

20

MICRO FINANCE IN INDIA AND INCLUSIVE GROWTH CA Saju Sreedhar

Kannur

Microfinance is a vital and powerful tool in the financial sector for poverty alleviation. It is a financial innovation and a model designed for serving the poor by the Nobel Peace prize winner (2006) Prof. Mohd. Yunus. According to Gandhiji “India lives in its villages” and village economy is the backbone of Indian economy. For the development of India rural economy upliftment of rural poor is imperative. Though financial institutions were formed in India with this as one of their stated objectives, the failure of these financial institutions in meeting the credit needs of millions of rural as well as urban poor led to the emergence of Micro finance in India.

Microfinance is the provision of financial services such as loans, savings, insurance, and training to people living in poverty. It is one of the great success stories in the developing world and is widely recognized as a just and sustainable solution in alleviating global poverty. Ultimately, the goal of microfinance is to give low income people an opportunity to become self-sufficient by providing a means of saving money, borrowing money and insurance

IntroductionThe Concept Micro Finance was an innovation by the Nobel Prize winner Prof. Mohammed Yunus. The Nobel Prize committee put poverty as an international agenda because lasting peace cannot be achieved unless there are ways to break out poverty. Prof. Yunus have changed the lives of millions of poor people by proving that providing proper financial and guidance to the poorest of poor who are willing to work hard can create wonders in their lives and contribute to nation building. Emergence of micro finance in Bangladesh played a pivotal role in development in the country. In India the micro finance system based on self help groups evolved and progressed in the 1990's .The need for micro finance has arisen due to failure of financial institutions in meeting the credit needs of rural poor which the government has created as part of upliftment of rural poor. Today Micro finance is considered as a vital and

efficient tool and instrument specially designed for poverty alleviation and empowerment of weaker sections of the society.

What is Micro Finance?

Microfinance is the provision of financial services to low-income clients or solidarity lending groups including consumers and the self-employed, who traditionally lack access to banking and related services. Microfinance is not just about giving micro credit to the poor rather it is an economic development tool whose objective is to assist poor to work their way out of poverty. It covers a wide range of services like credit, savings, insurance, remittance and also non-financial services like training, counselling etc. The Reserve Bank of India has defined micro credit “as provision of thrift, credit and other financial services and products of very small amount to the poor in rural, semi urban areas for enabling them to raise their income levels and improve living standards.”

Scope of Micro Finance in IndiaIndian is a natural candidate for microfinance considering the fact that a quarter of our population live in poverty. India is regarded as the one of the fastest growing economies in the world clocking impressive growth rates in GDP year on year. However, the entire country is not participating in this growth, with the rich getting richer and the poor getting poorer. A major concern that needs to be addressed is how to obtain a balanced and inclusive growth to bridge the gap between the rich and poor. Banks and financial institutions in the country are beyond the reach of the poor in the country for meeting their credit requirement forcing the poor to rely on money lenders for their credit requirements at exorbitant interest rates. The efforts by RBI in this direction by establishing regional rural banks and co-operative banks did not meet with expected success either. In this scenario microfinance provides an effective instrument for meeting the credit requirement of the poor while keeping the cost of lending low. It is a means for lifting the poor above

21

the level of poverty by providing them self employment opportunities and making them credit worthyComponents of Micro FinanceMicro CreditMicro credit is the extension of loans of very small amounts to impoverished borrowers who lack collateral, steady employment and a verifiable credithistory. It is designed not only to support entrepreneurship and alleviate poverty, but also in many cases to empower women and uplift entire communities by extension. These individuals lack collateral, steady employment and a verifiable credit history and therefore cannot meet even the most minimal qualifications to gain access to traditional credit. Introduction of micro credit has been very successful in engaging people in self employment projects by allowing them to generate income and thereby reducing poverty.

Micro SavingsA branch of microfinance, consisting of a small deposit account offered to lower income families or individuals as an incentive to save funds for future use. This is a policy of financial inclusion which aims at making available a basic banking 'no frills' account either with nil or very minimum balances as well as charges that would make such accounts accessible to vast sections of the population. This is a means of promoting the habit of thrift among those below the poverty line. Promoting micro savings helps in shielding the poor people from the clutches of money lenders and encourages them to be save more for the future. Savings serve as a security against unpredictable risks.

Micro InsuranceMicro insurance is the protection of low-income people against specific perils in exchange for regular premium payment proportionate to the likelihood and cost of the risks involved. Micro insurance is a term increasingly used to refer to insurance characterized by low premium and low caps or low coverage limits, sold as part of typical risk-pooling and marketing arrangements, and designed to service low-income people and businesses not served by typical social or commercial insurance schemes. There are various products of micro insurance like crop insurance, health insurance, insurance for equipments, personal accident cover etc.

Green Micro Finance

Green microfinance is the latest development in the field of microfinance which seeks to integrate the principles of sustainable development all lending policies and programs on microfinance. It provides

the poor with microfinance and encourages them to use more sustainable environmental-friendly practice. It is a means of addressing climate change and ensuring environmental justice by providing education and sharing knowledge on microfinance and eco friendly practices. Non renewable sources of energy are expensive and in shortage and there is an obvious need for energy substitutes for the poor. Green micro finance tries to address this issue by providing sources for renewable energy to the poor and by creating awareness and need for adopting environmental-friendly practice. With the help of micro finance institutions poor people are able to develop natural disaster and manmade disaster management skills. Green micro finance can support both social and environmental goals by incorporating environmental education and by supporting ideas for green business. Green Microfinance seeks to lead the field of microfinance and has the potential to address pervasive poverty, financial exclusion and energy inequality.

Micro Finance and Inclusive Growth

For sustainable development of the country and for inclusive growth, financial inclusion is necessary. Inclusive growth focuses on economic growth and sustained growth by ensuring participation of all sections of the society especially those below the poverty line. The key components of the inclusive growth include poverty reduction by increase in investments in rural area, rural infrastructure and agriculture development, spurt in credit for farmers, increase in rural employment. Micro finance is a major tool for inclusive growth; it enhances options available to the poor by providing financial support, creating self employment opportunities, encouraging saving, developing and empowering women and to generate income by protecting the environment.

Conclusion

Micro finance is a powerful tool for poverty alleviation. It is a means of developing a financial system with a social objective and is designed to serve the poor. It is considered as a major tool for socio economic and rural transformation by increasing the standard of living of the poor. India has, over the years made steady progress in developing Microfinance in the country and has made appreciable progress in this direction. However there in no scope for complacency and a lot more in required to be achieved in this field so as to increase the reach of microcredit in the country and to cover the entire population living below the poverty line. Hence promotion and growth of microfinance sector for achieving an inclusive growth is the priority of the nation.

The author is a fellow member of the Institute of Chartered Accountants of India, who can be reached at [email protected]

22

Introduction:

The world is getting smaller and the distance between continents are reducing because of the rapid changes in technology. Products become obsolete within minutes of being launched. I phone 16GB became obsolete within minutes because I phone 32GB was launched. With such changes in technology and life style of the people, the style and method of doing business also has to become dynamic.

If we compare the business and industries in 1950's and 2012, we can see the developments in the business world. As the economy grows, the services sector shows a marked increase and hence the emphasis is more on service industries than on traditional industries and agriculture. Against this background it is interesting to note the emergence from trading and manufacturing industries to service, BPO, KPO and information technology industries.

These developments in the business and industries are demanding a different role for chartered accountants and this is the professional opportunities for CA's.

Role of CA's in the complex business worldToday's business is very complex because of involvement of technologies and legal & other compliances including data security issues. Development in the technologies has opened new method and ways of doing business.

The banking system of today is the typical example showing revolutionary change in the method of doing business. In 1970's and 80's the banking system was mainly (wholly) based on manual record keeping and reporting system. Today the banking system has moved from manual system to core banking system

Changing the Role of CA's in the Emerging World CA Sreejith K

Mahe

and it is working like as 'self service' mode. The customer can logon in to his bank account from home or office and they can do the transaction himself without any support from bank officials like transfer of fund, payment of tax etc.