Centro Healthcare Category

35

HEALTHCARE Category Overview April 2015

-

Upload

centro -

Category

Healthcare

-

view

288 -

download

0

Transcript of Centro Healthcare Category

HEALTHCARE Category Overview April 2015

A SHIFTING INDUSTRY

The U.S. healthcare industry is currently worth $2.8 trillion with consumer healthcare spending projected to increase 6.8% in 2015; the biggest increase since

the recession began in 2008.

With the Affordable Care Act, the number of insured Americans will drastically increase in the next 4 years, bringing millions of new consumers into

the healthcare marketplace.

Additionally, there is a major demographic shift happening in America. Baby Boomers are getting older, and soon 1 in 5 Americans will be a senior citizen. As these consumers age, they will have a

greater need for healthcare.

The U.S is also seeing an increase in many preventable diseases, such as diabetes, obesity, and

hypertension. Healthcare providers have an opportunity to educate consumers about

preventative care and create a sense of urgency to visit a medical provider on a regular basis.

INDUSTRY OPPORTUNITIES

THERE IS A GOLDEN OPPORTUNITY

IN FRONT OF US

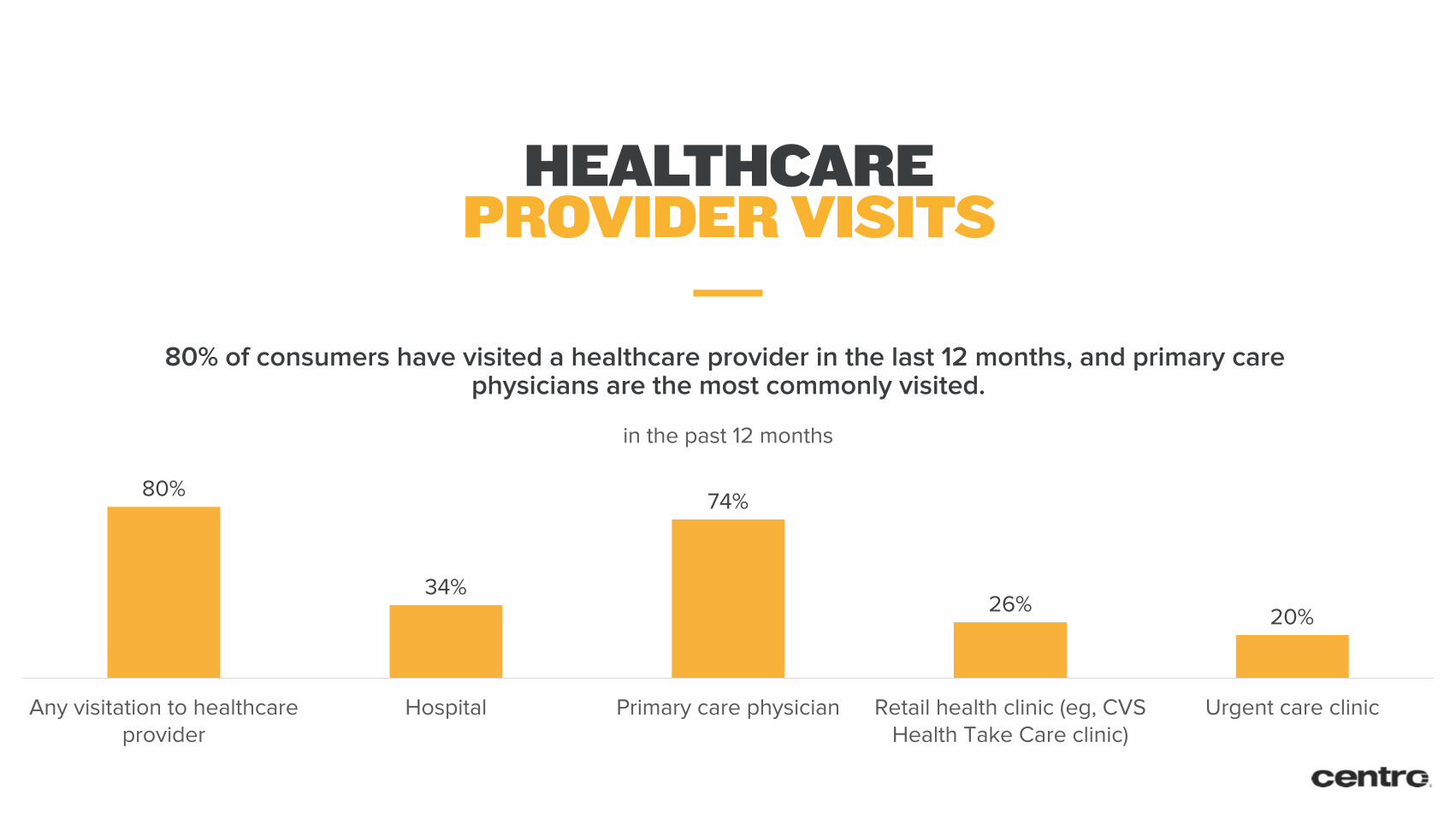

HEALTHCARE PROVIDER VISITS

80% of consumers have visited a healthcare provider in the last 12 months, and primary care physicians are the most commonly visited.

80%

34%

74%

26% 20%

Any visitation to healthcare provider

Hospital Primary care physician Retail health clinic (eg, CVS Health Take Care clinic)

Urgent care clinic

in the past 12 months

Projected health insurance enrollment over the next 4 years will bring millions of new consumers into the marketplace.

THE NEWLY INSURED

SELECTING A HEALTHCARE PROVIDER

Managing Your Health - US - January 2015 - Selecting a Healthcare Provider

Hospital Primary care

physician

Retail health clinic (eg, CVS Health Take Care clinic) Urgent care clinic

% % % % Best quality of care 19 59 4 5 Closest to my home/work 16 49 13 12 Most convenient hours 22 29 15 22 Accepts my insurance 18 62 5 6 In my network 12 67 4 3 Least expensive 5 40 22 9 Fastest treatment 10 36 16 25 Has the newest technology 51 25 4 5 Most approachable staff 12 61 9 6 Newest facility 33 28 8 13 Best reputation 28 48 4 4

The reasons consumers select a healthcare provider vary by the type of provider. Consumers visiting a primary care physician value the best quality of care, those visiting a hospital value the newest in technology, and those visiting a retail health clinic value the least expensive option.

BABY BOOMERS DOMINATE HEALTHCARE SPENDING

of All Prescription

Drug Use

of All Doctor Visits

of All Healthcare Spending

Citizens age 65+ spend an average of $4,769 out-of-pocket on health expenditures, while the total population spends an average of $3,313.

60% of adults 50-64 suffer from at least 1 chronic health condition.

40% 1/3 1/3

In 2014, 8 million Americans gained health insurance through the Affordable Care Act. This

increase is leading to longer wait times, less available physicians, and ultimately more visits to retail health clinics. Retail healthcare clinics are currently estimated to account for 10.8 million

visits per year.

Additionally, younger generations are relying less on traditional medical care. Millennials are even seeking options that could bypass a trip to the physical doctor’s office like health monitoring

apps/systems and virtual opportunities.

Finally, consumers are adopting more healthful habits like taking vitamins, watching their diet, and regularly exercising. This could impact the industry long-term if these reduce reliance on

medication and lead to a diminishing of avoidable ailments, both of which drive doctor visits.

INDUSTRY THREATS

FACING A BUMPY

ROAD AHEAD

IMPACT OF RETAIL HEALTHCARE CLINICS

of all consumers will have visited a retail healthcare clinic by 2015

The increase in the number of retail

healthcare clinics by 2015

of consumers are interested in a self-serve clinic

at retailers

Visits to retail healthcare clinics will save an estimated $800 million per year in overall healthcare expenditures.

Of all visits to retail healthcare clinics in 2014, 54% went for an immunization/shot, 31%

went for an ailment/injury, and 15% went for another reason.

25%-30% 26% 37%

In 2014, about half of Millennials visited a doctors office – compared to three-quarters

of non-Millennials.

71% of Millennials believe they’re already doing everything they can to maintain a

healthy lifestyle.

74% of Millennials prefer retail care clinics, and 25% prefer acute care clinics – double the number of baby boomers and seniors.

Millennials are more inclined than other

generations to request and receive estimates before undergoing treatment.

54% of Millennials have reported delaying or avoiding treatment due to costs, double that

of baby boomers and seniors.

MILLENNIALS & HEALTHCARE

HEALTH TECHNOLOGIES THAT U.S. MILLENNIAL PATIENTS ARE INTERESTED IN USING

73%

71%

63%

61%

60%

57%

Having their doctor use mobile devices during appointments to share info

Mobile apps to actively manage well-being for preventative care, review health records, schedule appointments

Proactively providing health data to doctor/provider via Wi-Fi/wearable devices so they can monitor their well-being

3-D printing for necessary health devices (prosthetics, hearing aids, etc.)

Using telehealth options (e.g., video chat with a doctor) so they don't have to come into the office for an appointment

Cutting-edge devices like pills that can monitor their internal vitals when swallowed

THE IMPACT OF TECHNOLOGY

As the healthcare industry is growing it is also evolving and taking a more digital approach.

This year, the U.S. Food and Drug

Administration is poised to review a record number of mobile health apps to respond to

the growing demand for mHealth.

According to a recent report by Mintel, 31% of consumers would use a mobile app to detect

or diagnose illness.

The number of electronic health records increased from 38% in 2008 to 78% in 2013.

Half of doctors believe that e-visits could replace more than 10% of in-office patient

appointments.

75% of doctors said they would prescribe an app to help patients manage chronic diseases,

such as diabetes.

TECHNOLOGY’S ROLE

HEALTHCARE IS BECOMING MORE

DIGITALLY-DRIVEN

TIME SPENT RESEARCHING HEALTH INFORMATION

Consumers are researching their health information online more frequently, with more than 60%

of consumers 45+ spending up to 5 hours per week researching.

Weekly Time Spent Researching Health Information* Among US Internet Users, by Age, Jan 2015 (% of respondents in each group)

18-34 35-44 45-65 66+ Total None 18% 16% 27% 35% 23%

<1 hour 34% 36% 40% 41% 37% 1-5 hours 35% 39% 31% 21% 32%

6-10 hours 7% 5% 2% 1% 4% 11-15 hours 3% 3% 1% 1% 2%

16-20 hours 1% 1% na 1% na 20+ hours 2% 1% 1% 1% 1%

METHODS FOR MANAGING HEALTH

Preferred Method for Managing Health According to US Internet Users, by Age, March 2014 (% of respondents in each group)

Digital channels Facility visits Phone/mail In-home/in person Other 18-24 40% 23% 18% 12% 6% 25-34 39% 27% 18% 10% 6% 35-44 36% 31% 20% 8% 6% 45-54 28% 38% 18% 11% 5% 55-64 22% 40% 19% 13% 5% 65+ 18% 43% 19% 15% 5%

Source: Strategy& (formerly Booz & Company), "The Birth of the Healthcare Consumer" in partnership with PricewaterhouseCoopers (PwC), Oct 14, 2014

Methodology: Data is from the October 2014 Strategy& (formerly Booz & Company) report titled "The Birth of the Healthcare Consumer" in partnership with PricewaterhouseCoopers (PwC). 2,339 US internet users ages 18+ were surveyed online during March 2014. The survey captured a representative sample of consumers across age, gender, health status (e.g., healthy, high risk/catastrophic, low risk/acute), income level and insurance type (e.g., employer outside exchange, Medicaid, Medicare, private exchange, public exchange and other).

Note: n=2,339; numbers may not add up to 100% due to rounding; read as 40% of respondents ages 18-24 prefer to manage their health via digital channels

Among younger generations, digital channels are becoming the preferred way to manage health.

HEALTH RELATED DIGITAL ACTIVITIES

Gen Y (21-33) Gen X (34-48) Baby boomers (49-67) Silent generation (68+) Total Find info about medical condition or drug 77% 79% 84% 78% 80% Find info about doctors 62% 51% 44% 34% 48% Visit a website to see personal health info 37% 30% 27% 22% 29% Find how much a medical procedure may cost 41% 22% 23% 13% 25% Visit a website to request a prescription refill 30% 23% 18% 16% 22%

Source: Catalyst Healthcare Research, "What's Reasonable?" May 13, 2014

Methodology: Data is from the May 2014 Catalyst Healthcare Research study titled "What's Reasonable?" 433 US internet users ages 21+ were surveyed online during December 20, 2013-February, 19, 2014. The margin of error is +/-4.7 percentage points at a 95% confidence level.

Note: n=433; in the past 2 years

Health-Related Digital Activities Conducted by US Internet Users, by Generation, Feb 2014 (% of respondents in each group)

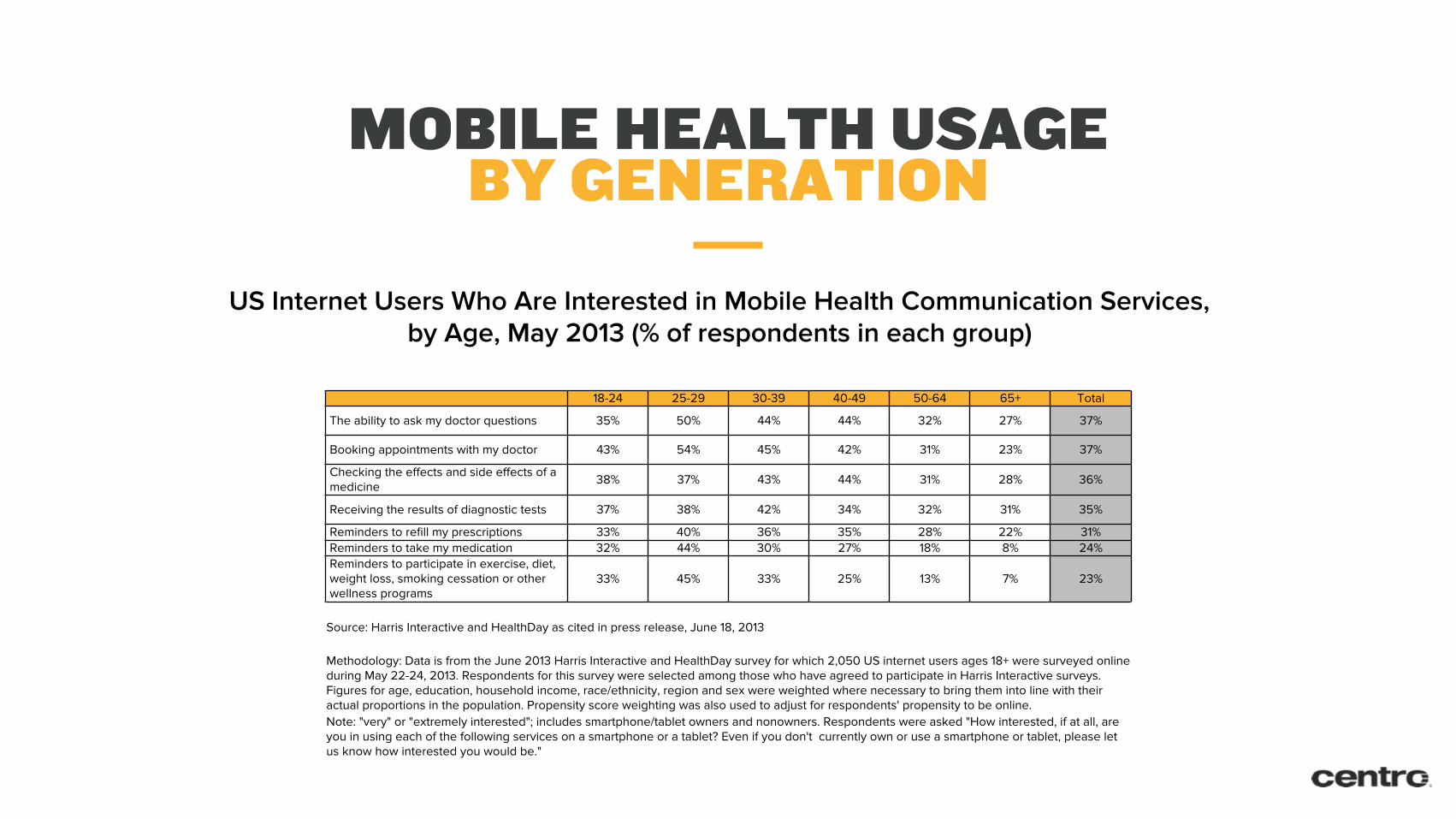

MOBILE HEALTH USAGE BY GENERATION

18-24 25-29 30-39 40-49 50-64 65+ Total

The ability to ask my doctor questions 35% 50% 44% 44% 32% 27% 37%

Booking appointments with my doctor 43% 54% 45% 42% 31% 23% 37%

Checking the effects and side effects of a medicine 38% 37% 43% 44% 31% 28% 36%

Receiving the results of diagnostic tests 37% 38% 42% 34% 32% 31% 35%

Reminders to refill my prescriptions 33% 40% 36% 35% 28% 22% 31% Reminders to take my medication 32% 44% 30% 27% 18% 8% 24% Reminders to participate in exercise, diet, weight loss, smoking cessation or other wellness programs

33% 45% 33% 25% 13% 7% 23%

Source: Harris Interactive and HealthDay as cited in press release, June 18, 2013

Methodology: Data is from the June 2013 Harris Interactive and HealthDay survey for which 2,050 US internet users ages 18+ were surveyed online during May 22-24, 2013. Respondents for this survey were selected among those who have agreed to participate in Harris Interactive surveys. Figures for age, education, household income, race/ethnicity, region and sex were weighted where necessary to bring them into line with their actual proportions in the population. Propensity score weighting was also used to adjust for respondents' propensity to be online. Note: "very" or "extremely interested"; includes smartphone/tablet owners and nonowners. Respondents were asked "How interested, if at all, are you in using each of the following services on a smartphone or a tablet? Even if you don't currently own or use a smartphone or tablet, please let us know how interested you would be."

US Internet Users Who Are Interested in Mobile Health Communication Services, by Age, May 2013 (% of respondents in each group)

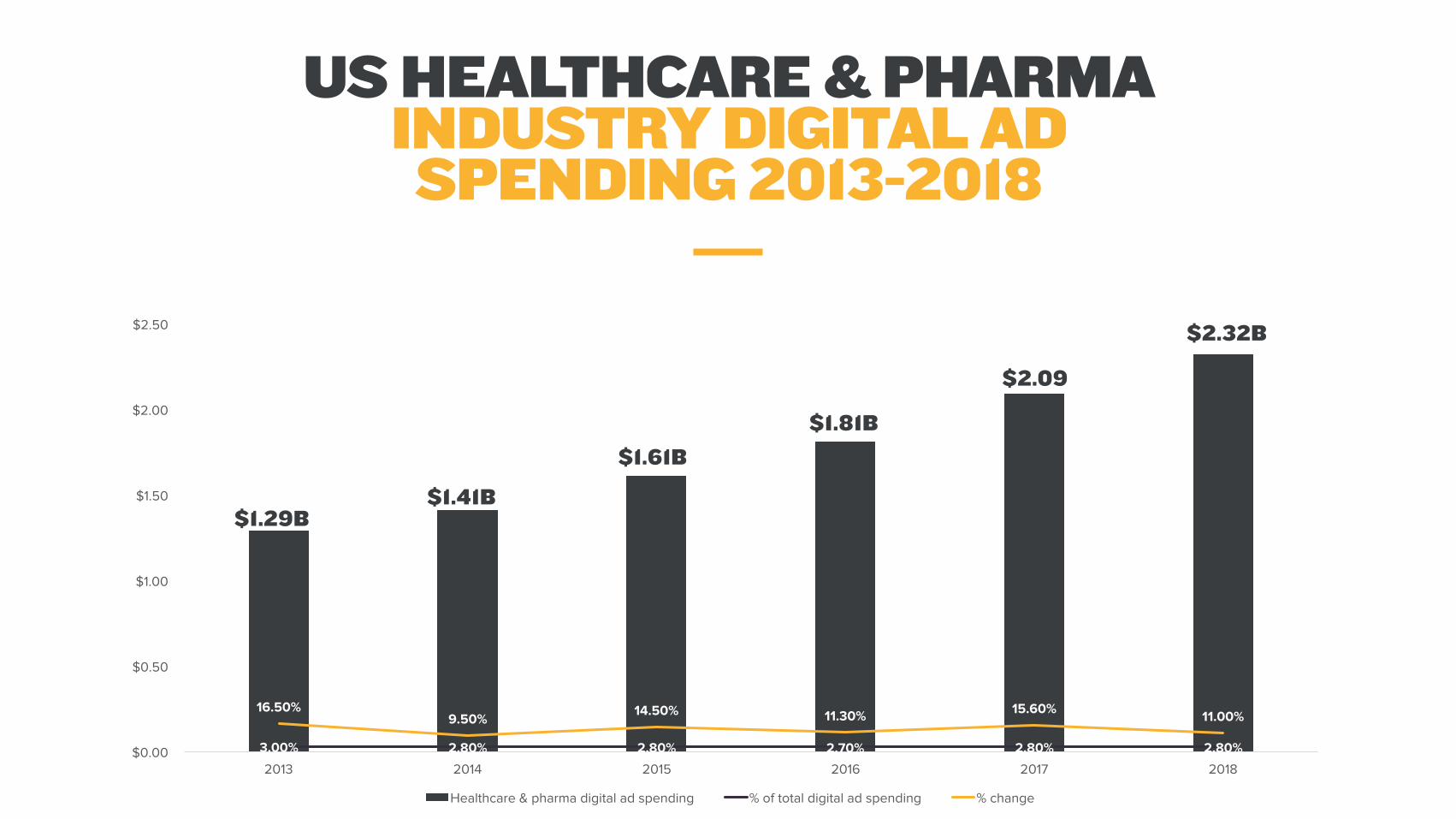

HEALTHCARE AD SPENDING TRENDS

DIGITAL AD SPENDING BY INDUSTRY

Healthcare & Pharma are expected to see 12.6% digital ad spend growth per year from 2014-2019, the 5th highest of all industries.

US Digital Ad Spending, by Industry, 2014-2019 (billions and CAGR)

2014 2015 2016 2017 2018 2019 CAGR (2014-2019)

Retail $11.19 $12.91 $14.71 $16.38 $18.17 $19.98 12.30% Automotive $6.23 $7.30 $8.49 $9.60 $10.82 $12.08 14.20% Financial services $6.28 $7.19 $8.16 $9.08 $9.99 $10.90 11.70% Telecom $5.67 $6.49 $7.36 $8.11 $8.92 $9.72 11.40% CPG & consumer products $4.25 $4.97 $5.82 $6.55 $7.35 $8.17 14.00% Travel $4.20 $4.85 $5.55 $6.10 $6.69 $7.27 11.60% Computing products & consumer electronics $3.85 $4.44 $5.08 $5.66 $6.28 $6.90 12.40% Media $2.83 $3.39 $3.95 $4.32 $4.79 $5.27 13.20% Entertainment $2.38 $2.80 $3.21 $3.65 $4.13 $4.63 14.30% Healthcare & pharma $1.41 $1.61 $1.81 $2.09 $2.32 $2.55 12.60% Other $2.43 $2.64 $2.95 $3.22 $3.48 $3.74 9.00% Total $50.73 $58.61 $67.09 $74.77 $82.95 $91.22 12.50%

US HEALTHCARE & PHARMA INDUSTRY DIGITAL AD SPENDING 2013-2018

3.00% 2.80% 2.80% 2.70% 2.80% 2.80%

16.50% 9.50% 14.50% 11.30% 15.60% 11.00%

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2013 2014 2015 2016 2017 2018

Healthcare & pharma digital ad spending % of total digital ad spending % change

$1.29B $1.41B

$1.61B $1.81B

$2.09B

$2.32B

$-

$500,000,000.00

$1,000,000,000.00

$1,500,000,000.00

$2,000,000,000.00

$2,500,000,000.00

YEAR 2010 YEAR 2011 YEAR 2012 YEAR 2013 YEAR 2014

Non-Digital Digital

TOTAL SPEND OF HOSPITALS, CLINICS & MEDICAL CENTERS

2010-2014

$1.2B

$1.6B $1.8B

$2.0B

$2.3B

From 2010-2014, non-digital media investments grew +76% but digital media investments grew +125%.

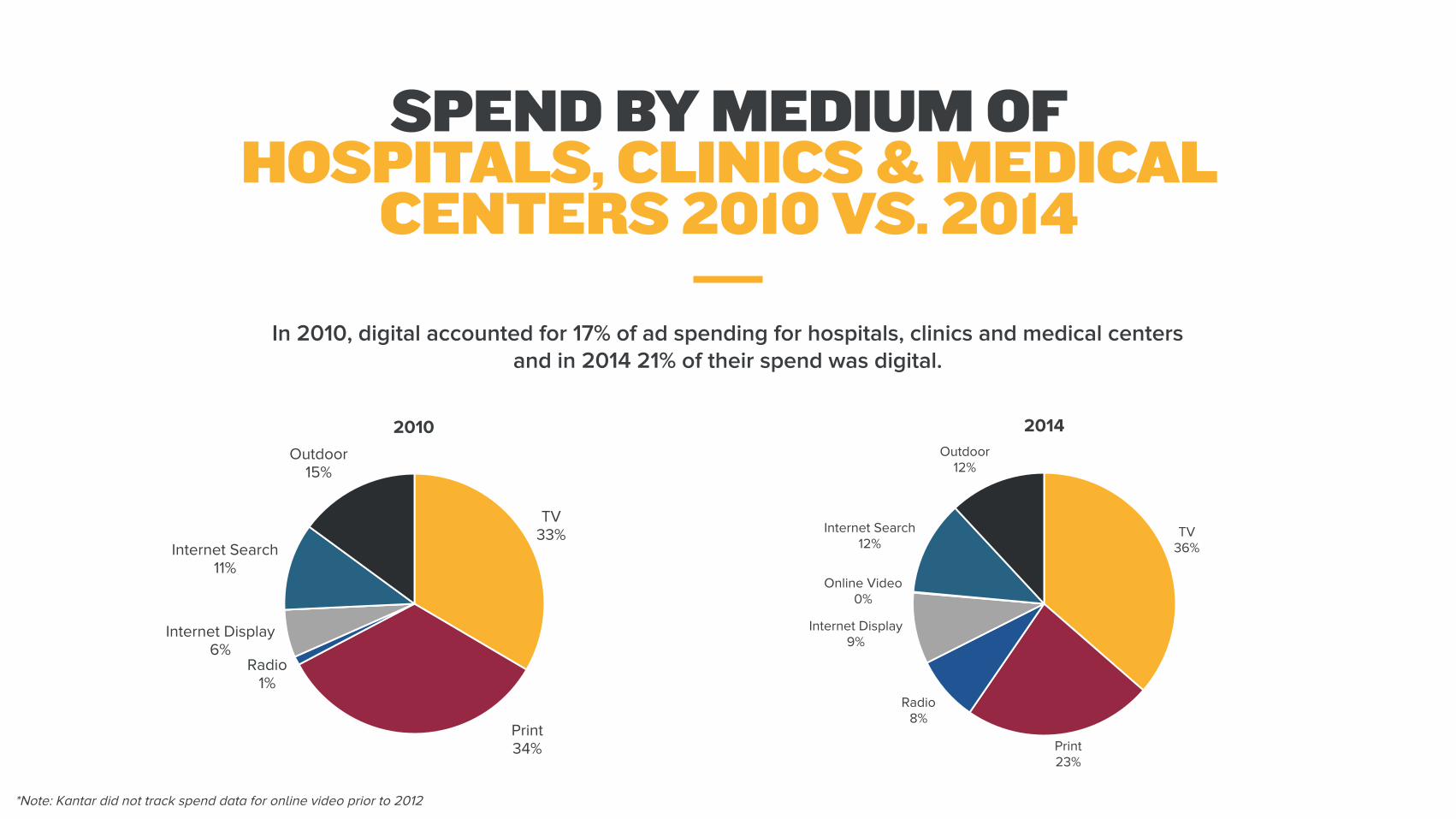

SPEND BY MEDIUM OF HOSPITALS, CLINICS & MEDICAL

CENTERS 2010 VS. 2014

TV 36%

Print 23%

Radio 8%

Internet Display 9%

Online Video 0%

Internet Search 12%

Outdoor 12%

2014

TV 33%

Print 34%

Radio 1%

Internet Display 6%

Internet Search 11%

Outdoor 15%

2010

*Note: Kantar did not track spend data for online video prior to 2012

In 2010, digital accounted for 17% of ad spending for hospitals, clinics and medical centers and in 2014 21% of their spend was digital.

CHANGE IN MARKETING SPEND BY INDUSTRY

Change in Marketing Spend According to US Marketers, by Industry, Feb 2015 (% change)

Healthcare/pharmaceutical

Digital marketing spending 19.20%

New product introductions 1.10%

Customer relationship management 4.00%

Brand building 9.40%

Traditional ad spending -0.20%

New service introductions 4.20%

Total marketing spending 10.70%

Of all marketing efforts, healthcare & pharma marketers reported the largest increase in

digital marketing spend at 19.2%. The second highest category was brand building at 9.4%

YOY SPEND OF TOP HOSPITAL GROUPS

2010 2011 2012 2013 2014 Adventist Health $ 526,787.00 $ 605,545.00 $ 637,771.00 $ 995,066.00 $ 738,410.00 Ascension Health $ 1,199,963.00 $ 1,420,780.00 $ 2,231,881.00 $ 3,236,077.00 $ 6,698,400.00 CHE Trinity Inc $ 2,664,480.00 $ 4,067,343.00 $ 10,170,997.00 $ 9,661,722.00 $ 2,845,069.00 Community Health Systems Inc $ 1,080,008.00 $ 1,296,389.00 $ 1,029,413.00 $ 1,048,420.00 $ 1,328,186.00 Dignity Health $ 1,188,884.00 $ 951,679.00 $ 3,151,357.00 $ 11,917,507.00 $ 11,328,573.00 Kaiser Permanente $ 4,750,141.00 $ 5,985,530.00 $ 7,238,948.00 $ 8,257,192.00 $ 10,844,577.00 Lifepoint Hospitals Inc $ 7,107.00 $ 46,599.00 $ 128,987.00 $ 247,735.00 $ 340,090.00 Mayo Clinic $ 1,741,699.00 $ 4,321,953.00 $ 3,488,622.00 $ 3,528,775.00 $ 9,916,411.00 Tenet Healthcare Corp $ 4,842,855.00 $ 6,166,062.00 $ 4,338,390.00 $ 4,744,689.00 $ 5,440,718.00 Universal Health Services Inc $ 1,938,224.00 $ 1,987,410.00 $ 2,050,203.00 $ 2,670,105.00 $ 2,550,529.00 TOTAL $ 19,940,148.00 $ 26,849,290.00 $ 34,466,569.00 $ 46,307,288.00 $ 52,030,963.00

SPEND BY MEDIUM OF TOP HOSPITAL GROUPS

2010 VS 2014

**Note: Kantar did not track spend data for online video prior to 2012

*Note: Data is representative of 10 hospital groups displayed in the previous slide

TV 31%

Print 28%

Radio 0%

Internet Display 6%

Internet Search 3%

Outdoor 32%

2010

TV 26%

Print 13%

Radio 15%

Internet Display 19%

Online Video 1%

Internet Search 6%

Outdoor 20%

2014

Leading hospital groups are adopting digital tactics at a quicker rate. In 2010 9% of their spend was digital and in 2014, 26% of their spend was digital.

MARKETING OPPORTUNITIES

2000+ AGENCIES

6,000+ BRANDS

50,000+ CAMPAIGNS

Centro has supported 500+ healthcare organizations in the past 2 years.

• Top trusted local news & broadcast sites

• Geo-targeted banner & mobile ads

• Homepage take-overs, display, video, mobile

LOCAL AND ENDEMIC

• Sight + sound across variety of screens: desktop, mobile, tablet, digital place based, connected TV

• TV retargeting based on demo, daypart, location, weather, device, carrier, and behavioral

VIDEO AND AUDIO

• Reach consumers on-the-go with mobile, during work/leisure time with tablet

• Use geo-fencing to pinpoint exact location of consumer and enable conquest strategies

MOBILE AND TABLET

• Target consumers currently in-market for a healthcare provider

• Target based on insurance coverage

• Use Nielsen and Neustar for more defined audience targeting

PROGRAMMATIC

DIGITAL OPPORTUNITIES

SAMPLE HEALTHCARE

CONSUMER PROFILE

“My family is the most important thing in my life and knowing that we are all healthy means a lot to me. The internet has made it easier than ever to be sure we’re

getting quality care. I use my mobile device to research hospitals and medical centers, and read their reviews at

home or on-the-go. I’ve also used social media to get the opinions on doctors and facilities of my friends and

relatives. When it comes to my family’s health I won’t trust just anyone.”

Adults 25-54

Female skew (index 105)

56% are parents (index 178)

50% have graduated college or higher (index 176)

HHI $50k+

Has visited any doctor in the last 12 months

Has medical insurance

83% are Caucasian (index 109)

11% are Hispanic

8% are African American

4% are Asian (index 131)

HEALTHCARE CONSUMER

WHAT MATTERS TO ME

“I value services that are quality and can fit into my lifestyle, especially with healthcare.”

If a product is made by a company I trust, I’ll buy it

even if it is more expensive. (index 102)

Spending time with my family is my top priority.

(index 113)

I often use the internet to obtain medical

information. (index 140)

Juggling work and family demands is very

stressful for me. (index 111)

I am so busy, I often can’t finish everything I

need to do in a day (index 121)

My children and spouse have a significant impact on the brands I choose.

(index 105)

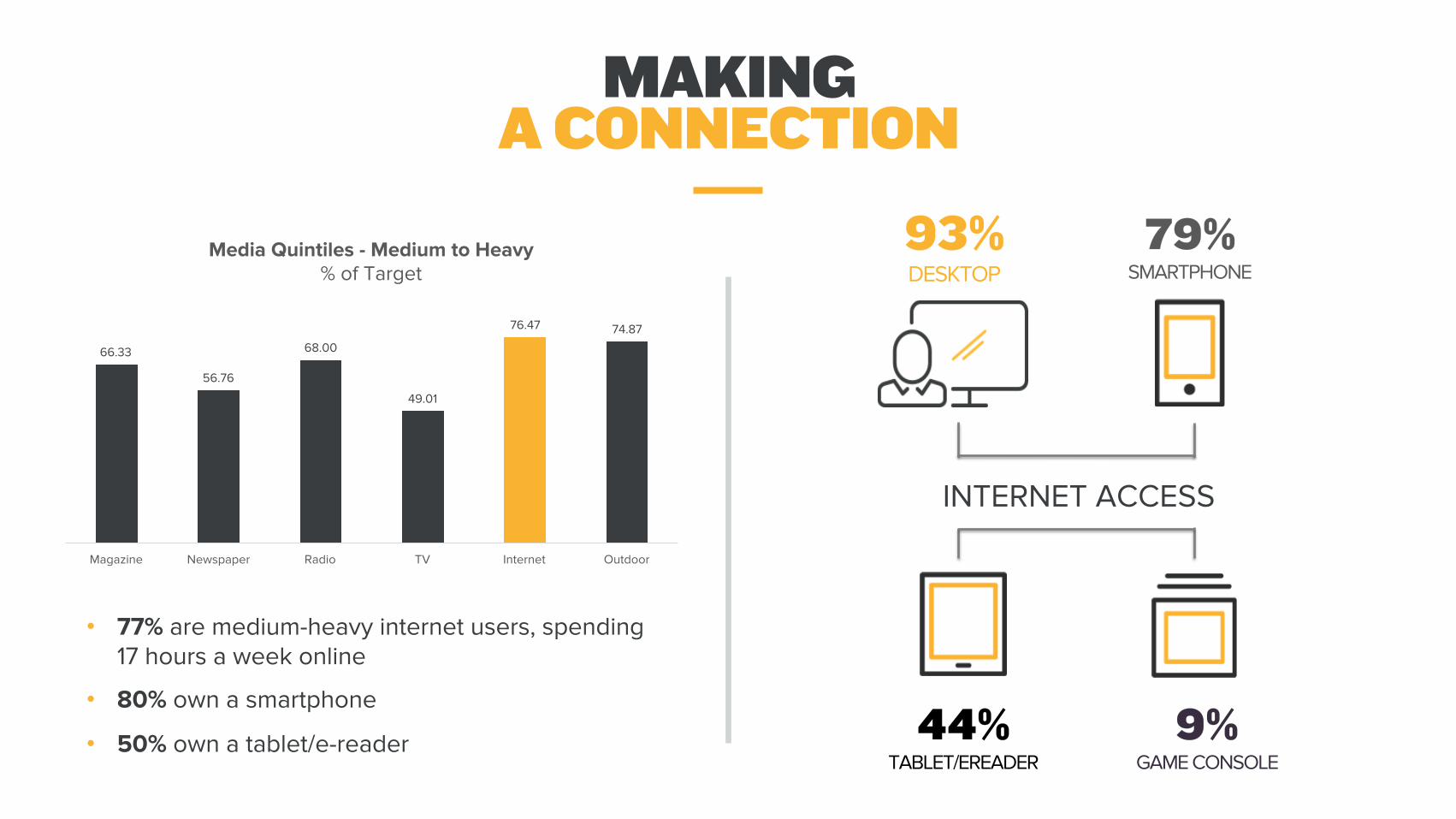

66.33

56.76

68.00

49.01

76.47 74.87

Magazine Newspaper Radio TV Internet Outdoor

Media Quintiles - Medium to Heavy % of Target

MAKING A CONNECTION

• 77% are medium-heavy internet users, spending 17 hours a week online

• 80% own a smartphone

• 50% own a tablet/e-reader

INTERNET ACCESS

44% TABLET/EREADER

9% GAME CONSOLE

93% DESKTOP

79% SMARTPHONE

92% used Google in the last 30 days

24% used Bing in the

last 30 days

64% used search engines on their mobile phone

41% used Yahoo! in the

last 30 days

SEARCH

20% are mobile ad and app happy

58% used apps

40% listen to music

53% visit a website for news

14% use health/fitness apps

MOBILE

44% watched a video on social media

20% watched a video on their

mobile phone

18% watched a movie online

11% uploaded video to social media

VIDEO

85% used a social network in the last 30 days

47% used social networks on

their mobile phone

42% posted that they like something

43% posted a picture

SOCIAL

DIGITAL MEDIA CONSUMPTION

48% go to the doctor regularly for checkups

29% are always looking for new ways to live a healthier life

23% say medication has improved their quality of life

66% agree that doctor knows best

After seeing a healthcare ad:

9% have made an appointment to see a doctor (index 127)

7% have visited a product or drug website (index 159)

4% discussed the ad with a friend or family member (index 127)

In the last 12 months:

55% have visited a general/family practitioner (index 133)

28% have visited an OBGYN (index 181)

15% have visited a pediatrician (index 227)

HEALTH ATTITUDES & BEHAVIORS

GET TO KNOW YOUR PATIENTS

THANK YOU.