CD Equisearch Pvt Ltd - Business Standardbsmedia.business-standard.com/_media/bs/data/... · CD...

16

CD Equisearch Pvt Ltd April 26, 2016 Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance Source: LICHFL LIC Housing Finance Ltd (LICHFL) No. of shares (m) 504.7 Mkt cap (Rs crs/$m) 23056/3457.4 Current price (Rs/$) 457/6.9 Price target (Rs/$) 578/8.7 52 W H/L (Rs.) 524/389 Book Value (Rs/$) 181/2.7 Beta 1.4 Daily volume (avg. monthly) 2504350 P/BV (FY17e/18e) 2.1/1.8 P/E (FY17e/18e) 11.7/9.9 Cost to Income (FY16/17e/18e) 14.7/15.0/15.3 EPS growth (FY16/17e/18e) 19.8/18.6/18.3 NIM (FY16/17e/18e) 2.6/2.6/2.7 ROE (FY16/17e/18e) 19.6/19.8/19.9 ROA(FY16/17e/18e) 14./1.4/1.5 D/E ratio (FY16/17e/18e) 12.1/11.8/11.3 BSE Code 500253 NSE Code LICHSGFIN Bloomberg LICHF IN Reuters LICH.BO Shareholding pattern % Promoters 40.3 MFs / Banks / FIs 15.7 Foreign 35.0 Govt. Holding 0.0 Total Public 9.0 Total 100.0 As on Mar 31, 2016 Recommendation BUY Phone: + 91 (33) 4488 0043 E- mail: [email protected] Figures (Rs crs) FY14 FY15 FY16 FY17e FY18e Net Interest Income 1915.90 2265.83 2984.64 3488.97 4128.77 Non Interest Income 244.39 225.58 194.06 242.03 281.17 Pre-Provision Profits 1847.03 2109.19 2710.02 3171.35 3735.22 Net profit 1317.19 1386.19 1660.79 1969.36 2329.40 EPS(Rs) 26.10 27.47 32.91 39.02 46.16 EPS growth (%) 28.7 5.2 19.8 18.6 18.3 Company Brief LIC Housing provides long term finance to individuals/businesses for purchase or construction of house or flat for residential purpose/repair or renovation of existing flat/houses. It also provides finance on existing property for business/personal needs and also gives loans to professionals. Highlights Government of India’s much talked up scheme like "Housing for All by 2022” would doubtlessly boost growth of housing finance industry. Backed by State subsidy, the government proposes to set up 110 million houses. The main focus will be on the slum redevelopment where land will be pooled and given to private real estate developers. With new initiatives like priority sector lending, target is to bring housing loans up to Rs 50 lakhs under affordable housing. To race ahead of the competition, LICHFL increased its focus on the high yield non-core portfolio. In FY16, the share of LAP (loan against property) portfolio increased to 8.8% from 6.4% in FY15. The smaller ticket size on the LAP portfolio keeps the yield to be around 200 bps higher than the home loans. It has also designed a new product called “hospital loans” which will yield around 12% (yield on home loans 10-11%). LICHFL’s healthy margin of 2.7% last quarter was the best the company has reported in the past 19 quarters and the improvement is mainly attributed to the change in product mix, low cost of funds and the conversion of floating rate loans to fixed rate loans. However, stiff competition in the market impacted the yields (10.9% in Q4FY16) as LICHFL had to keep the lending rate at lower levels. LICHFL also made movement towards market instruments improving its borrowing basket by reducing bank borrowings to 12.7% of the total mix (17.6% in FY15) and substituting it by cheaper NCDs, which constitutes 77.3% of the borrowings. This helped the company to keep the cost of funds low thereby supporting the expansion in margins. The stock currently trades at 2.1x FY17e BV (11.7x FY17e EPS) and 1.8x FY18e BV (9.9x FY18e EPS). LICHFL’s renewed focus on boosting the high margin yielding LAP portfolio would galvanize its order book over the next few years. Healthy growth in loan book supplemented by marginal rise in NIMs would culminate in over 18% growth (annual) in earnings over the next two years; needless to mention its industry beating return on equity. We therefore assign “buy” rating with a target of Rs 578 based on 2.3x FY18e BV (average of last three years), over a period of 6-9 months.

Transcript of CD Equisearch Pvt Ltd - Business Standardbsmedia.business-standard.com/_media/bs/data/... · CD...

CD Equisearch Pvt Ltd April 26, 2016

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Source: LICHFL

LIC Housing Finance Ltd (LICHFL)

No. of shares (m) 504.7

Mkt cap (Rs crs/$m) 23056/3457.4

Current price (Rs/$) 457/6.9

Price target (Rs/$) 578/8.7

52 W H/L (Rs.) 524/389

Book Value (Rs/$) 181/2.7

Beta 1.4

Daily volume (avg. monthly) 2504350

P/BV (FY17e/18e) 2.1/1.8

P/E (FY17e/18e) 11.7/9.9

Cost to Income (FY16/17e/18e) 14.7/15.0/15.3

EPS growth (FY16/17e/18e) 19.8/18.6/18.3

NIM (FY16/17e/18e) 2.6/2.6/2.7

ROE (FY16/17e/18e) 19.6/19.8/19.9

ROA(FY16/17e/18e) 14./1.4/1.5

D/E ratio (FY16/17e/18e) 12.1/11.8/11.3

BSE Code 500253

NSE Code LICHSGFIN

Bloomberg LICHF IN

Reuters LICH.BO

Shareholding pattern %

Promoters 40.3

MFs / Banks / FIs 15.7

Foreign 35.0

Govt. Holding 0.0

Total Public 9.0

Total 100.0

As on Mar 31, 2016

Recommendation

BUY

Phone: + 91 (33) 4488 0043

E- mail: [email protected]

Figures (Rs crs)

FY14 FY15

FY16

FY17e

FY18e

Net Interest Income 1915.90 2265.83 2984.64 3488.97 4128.77

Non Interest Income 244.39 225.58 194.06 242.03 281.17

Pre-Provision Profits 1847.03 2109.19 2710.02 3171.35 3735.22

Net profit 1317.19 1386.19 1660.79 1969.36 2329.40

EPS(Rs) 26.10 27.47 32.91 39.02 46.16

EPS growth (%) 28.7 5.2 19.8 18.6 18.3

Company Brief LIC Housing provides long term finance to individuals/businesses for purchase

or construction of house or flat for residential purpose/repair or renovation of

existing flat/houses. It also provides finance on existing property for

business/personal needs and also gives loans to professionals.

Highlights � Government of India’s much talked up scheme like "Housing for All by

2022” would doubtlessly boost growth of housing finance industry. Backed

by State subsidy, the government proposes to set up 110 million houses.

The main focus will be on the slum redevelopment where land will be

pooled and given to private real estate developers. With new initiatives like

priority sector lending, target is to bring housing loans up to Rs 50 lakhs

under affordable housing.

� To race ahead of the competition, LICHFL increased its focus on the high

yield non-core portfolio. In FY16, the share of LAP (loan against property)

portfolio increased to 8.8% from 6.4% in FY15. The smaller ticket size on

the LAP portfolio keeps the yield to be around 200 bps higher than the

home loans. It has also designed a new product called “hospital loans”

which will yield around 12% (yield on home loans 10-11%).

� LICHFL’s healthy margin of 2.7% last quarter was the best the company

has reported in the past 19 quarters and the improvement is mainly

attributed to the change in product mix, low cost of funds and the

conversion of floating rate loans to fixed rate loans. However, stiff

competition in the market impacted the yields (10.9% in Q4FY16) as

LICHFL had to keep the lending rate at lower levels.

� LICHFL also made movement towards market instruments improving its

borrowing basket by reducing bank borrowings to 12.7% of the total mix

(17.6% in FY15) and substituting it by cheaper NCDs, which constitutes

77.3% of the borrowings. This helped the company to keep the cost of

funds low thereby supporting the expansion in margins.

� The stock currently trades at 2.1x FY17e BV (11.7x FY17e EPS) and 1.8x

FY18e BV (9.9x FY18e EPS). LICHFL’s renewed focus on boosting the high

margin yielding LAP portfolio would galvanize its order book over the

next few years. Healthy growth in loan book supplemented by marginal

rise in NIMs would culminate in over 18% growth (annual) in earnings

over the next two years; needless to mention its industry beating return on

equity. We therefore assign “buy” rating with a target of Rs 578 based on

2.3x FY18e BV (average of last three years), over a period of 6-9 months.

2

2

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

[

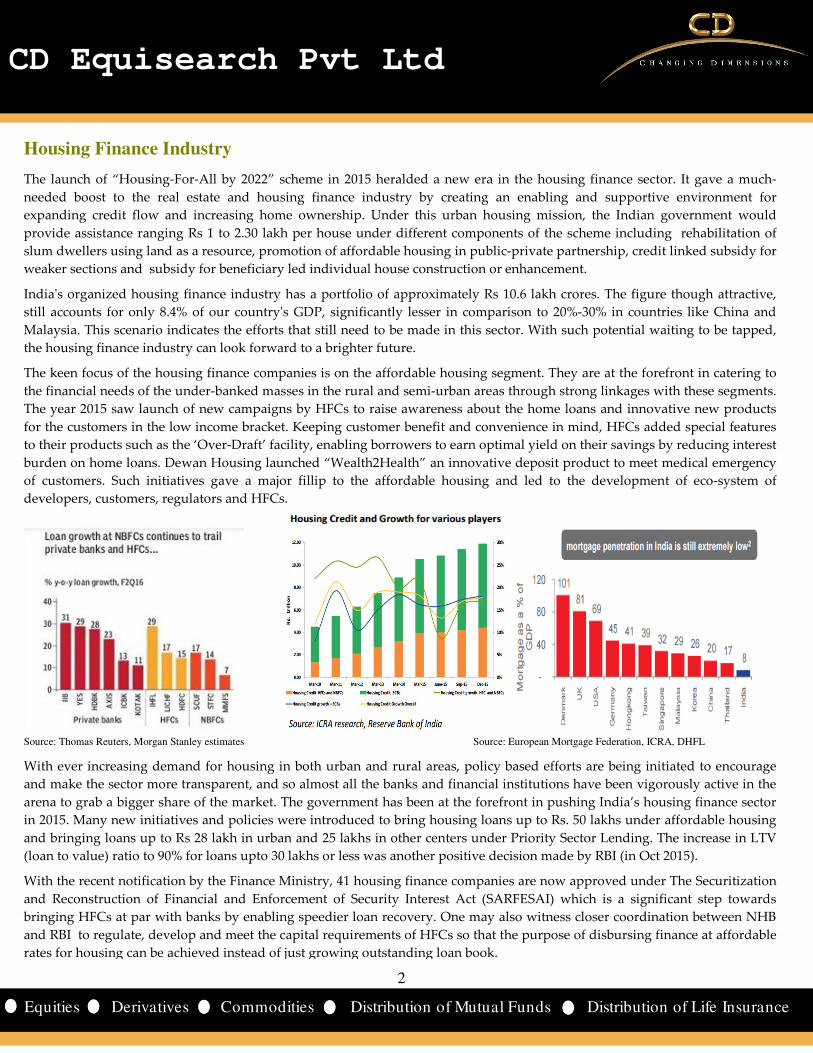

Housing Finance Industry

The launch of “Housing-For-All by 2022” scheme in 2015 heralded a new era in the housing finance sector. It gave a much-

needed boost to the real estate and housing finance industry by creating an enabling and supportive environment for

expanding credit flow and increasing home ownership. Under this urban housing mission, the Indian government would

provide assistance ranging Rs 1 to 2.30 lakh per house under different components of the scheme including rehabilitation of

slum dwellers using land as a resource, promotion of affordable housing in public-private partnership, credit linked subsidy for

weaker sections and subsidy for beneficiary led individual house construction or enhancement.

India's organized housing finance industry has a portfolio of approximately Rs 10.6 lakh crores. The figure though attractive,

still accounts for only 8.4% of our country's GDP, significantly lesser in comparison to 20%-30% in countries like China and

Malaysia. This scenario indicates the efforts that still need to be made in this sector. With such potential waiting to be tapped,

the housing finance industry can look forward to a brighter future.

The keen focus of the housing finance companies is on the affordable housing segment. They are at the forefront in catering to

the financial needs of the under-banked masses in the rural and semi-urban areas through strong linkages with these segments.

The year 2015 saw launch of new campaigns by HFCs to raise awareness about the home loans and innovative new products

for the customers in the low income bracket. Keeping customer benefit and convenience in mind, HFCs added special features

to their products such as the ‘Over-Draft’ facility, enabling borrowers to earn optimal yield on their savings by reducing interest

burden on home loans. Dewan Housing launched “Wealth2Health” an innovative deposit product to meet medical emergency

of customers. Such initiatives gave a major fillip to the affordable housing and led to the development of eco-system of

developers, customers, regulators and HFCs.

Source: Thomas Reuters, Morgan Stanley estimates Source: European Mortgage Federation, ICRA, DHFL

With ever increasing demand for housing in both urban and rural areas, policy based efforts are being initiated to encourage

and make the sector more transparent, and so almost all the banks and financial institutions have been vigorously active in the

arena to grab a bigger share of the market. The government has been at the forefront in pushing India’s housing finance sector

in 2015. Many new initiatives and policies were introduced to bring housing loans up to Rs. 50 lakhs under affordable housing

and bringing loans up to Rs 28 lakh in urban and 25 lakhs in other centers under Priority Sector Lending. The increase in LTV

(loan to value) ratio to 90% for loans upto 30 lakhs or less was another positive decision made by RBI (in Oct 2015).

With the recent notification by the Finance Ministry, 41 housing finance companies are now approved under The Securitization

and Reconstruction of Financial and Enforcement of Security Interest Act (SARFESAI) which is a significant step towards

bringing HFCs at par with banks by enabling speedier loan recovery. One may also witness closer coordination between NHB

and RBI to regulate, develop and meet the capital requirements of HFCs so that the purpose of disbursing finance at affordable

rates for housing can be achieved instead of just growing outstanding loan book.

3

3

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Source: LICHFL, CD Equisearch

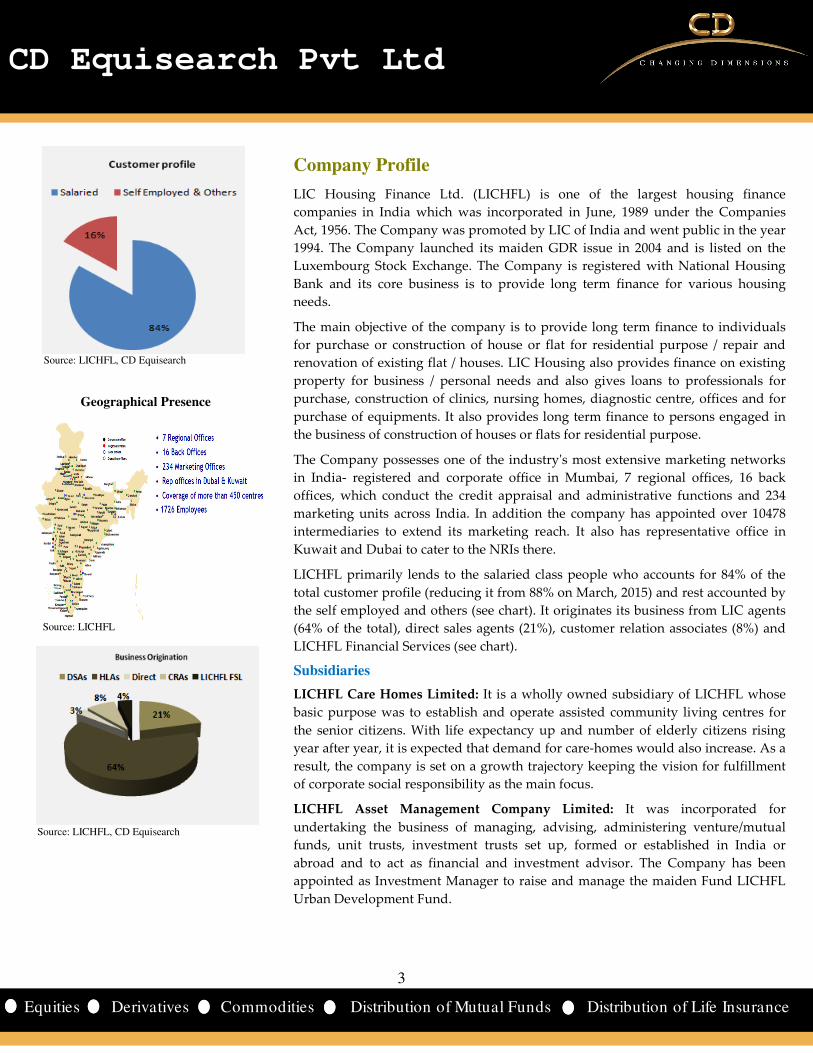

Geographical Presence

Source: LICHFL

Source: LICHFL, CD Equisearch

Company Profile

LIC Housing Finance Ltd. (LICHFL) is one of the largest housing finance

companies in India which was incorporated in June, 1989 under the Companies

Act, 1956. The Company was promoted by LIC of India and went public in the year

1994. The Company launched its maiden GDR issue in 2004 and is listed on the

Luxembourg Stock Exchange. The Company is registered with National Housing

Bank and its core business is to provide long term finance for various housing

needs.

The main objective of the company is to provide long term finance to individuals

for purchase or construction of house or flat for residential purpose / repair and

renovation of existing flat / houses. LIC Housing also provides finance on existing

property for business / personal needs and also gives loans to professionals for

purchase, construction of clinics, nursing homes, diagnostic centre, offices and for

purchase of equipments. It also provides long term finance to persons engaged in

the business of construction of houses or flats for residential purpose.

The Company possesses one of the industry's most extensive marketing networks

in India- registered and corporate office in Mumbai, 7 regional offices, 16 back

offices, which conduct the credit appraisal and administrative functions and 234

marketing units across India. In addition the company has appointed over 10478

intermediaries to extend its marketing reach. It also has representative office in

Kuwait and Dubai to cater to the NRIs there.

LICHFL primarily lends to the salaried class people who accounts for 84% of the

total customer profile (reducing it from 88% on March, 2015) and rest accounted by

the self employed and others (see chart). It originates its business from LIC agents

(64% of the total), direct sales agents (21%), customer relation associates (8%) and

LICHFL Financial Services (see chart).

Subsidiaries

LICHFL Care Homes Limited: It is a wholly owned subsidiary of LICHFL whose

basic purpose was to establish and operate assisted community living centres for

the senior citizens. With life expectancy up and number of elderly citizens rising

year after year, it is expected that demand for care-homes would also increase. As a

result, the company is set on a growth trajectory keeping the vision for fulfillment

of corporate social responsibility as the main focus.

LICHFL Asset Management Company Limited: It was incorporated for

undertaking the business of managing, advising, administering venture/mutual

funds, unit trusts, investment trusts set up, formed or established in India or

abroad and to act as financial and investment advisor. The Company has been

appointed as Investment Manager to raise and manage the maiden Fund LICHFL

Urban Development Fund.

4

4

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

LICHFL TRUSTEE Company Private Limited: It was incorporated to undertake the business of trusteeship. In the year 2010

the Company has registered LICHFL Urban Development Fund with SEBI as Venture Capital Fund (VCF) under the SEBI

(Venture Capital Funds) Regulations, 1996. The Fund launched its maiden Scheme LICHFL Urban Development Fund

(Fund) for which 30th March, 2013 was declared as Final Closure Date of the Fund after successfully garnering fund raising

of Rs 529.35 crore as against the target of Rs 500 crore.

LICHFL Financial Services Limited: LICHFL Financial Services Limited, a wholly owned subsidiary of LICHFL, was

incorporated for undertaking non fund based activities like marketing of housing loans, insurance products (life insurance

and general insurance), credit cards, mutual funds, fixed deposits etc. It has become operational in March 2009 and at present

has got 38 offices spread over 10 states.

Service Profile

Retail Home Loans

In the current scenario, both banks and HFCs have been thriving on retail lending. Retail lending of banks includes various

types of retail residential mortgages, consumer credit cards, automobile and personal loans, loans against securities, and

small business loans. However, home loans constitute the largest percentage of retail loans in India.

The home loan amount offered to the resident and non resident Indians by LICHFL is of a minimum of Rs 1 lakh. For the

resident Indians, the maximum loan term is 30 years for salaried professionals and 20 years for self employed and others. The

loan to property cost is 85% (including stamp duty & registration charges) for loan upto 20 lakhs, 80% of the total cost of the

property for loan between 20 lakhs-75 lakhs and 75% of the loan above 75 lakhs. In case of loan for purchase of residential

plot from statutory authority, the loan to property cost is 75% of the property value and the maximum loan term is 15 years.

For the non resident Indians, the loan term is 15 years for the people with professional qualification and 10 years for others.

For the pensioners, loans can be availed for purchase, construction, extension of house/flat. The pensioners (before

retirement) whose age is 50 or more and having a pension scheme after retirement can apply for the loan. The term of the

loan will be 15 years or 70 years of age whichever is earlier. For pensioners (after retirement) having a stable income

throughout their life from pension may apply for loans and the loan is to be repaid before the applicant attains the age of 70

years. LIC HOSUING FINANCE

Source: CD Equisearch Source: deal4loans.com

Developer Funding / Construction Finance / Project Finance

It is a unique offering under which funding is directly made to real estate developers for carrying out their projects. Few

banks have come up with innovative housing loan schemes in association with developers / builders. These schemes are

popularly known as the 80:20, 75:25 Schemes.

5

5

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

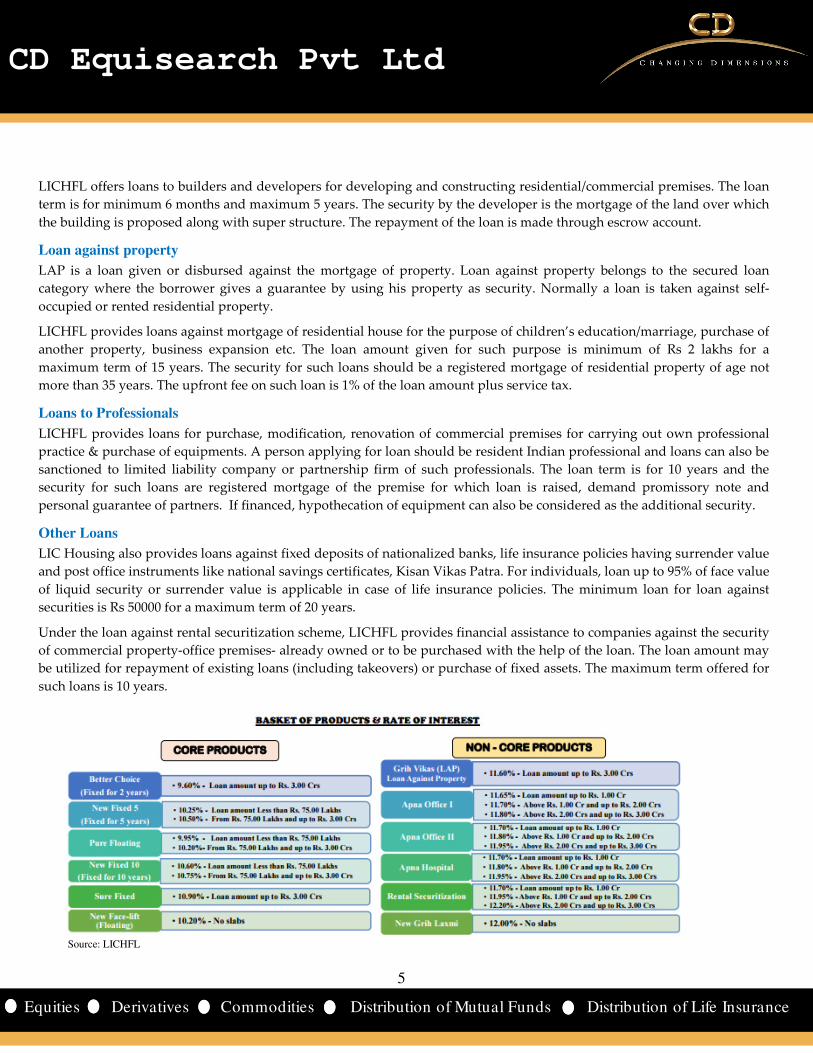

LICHFL offers loans to builders and developers for developing and constructing residential/commercial premises. The loan

term is for minimum 6 months and maximum 5 years. The security by the developer is the mortgage of the land over which

the building is proposed along with super structure. The repayment of the loan is made through escrow account.

Loan against property

LAP is a loan given or disbursed against the mortgage of property. Loan against property belongs to the secured loan

category where the borrower gives a guarantee by using his property as security. Normally a loan is taken against self-

occupied or rented residential property.

LICHFL provides loans against mortgage of residential house for the purpose of children’s education/marriage, purchase of

another property, business expansion etc. The loan amount given for such purpose is minimum of Rs 2 lakhs for a

maximum term of 15 years. The security for such loans should be a registered mortgage of residential property of age not

more than 35 years. The upfront fee on such loan is 1% of the loan amount plus service tax.

Loans to Professionals

LICHFL provides loans for purchase, modification, renovation of commercial premises for carrying out own professional

practice & purchase of equipments. A person applying for loan should be resident Indian professional and loans can also be

sanctioned to limited liability company or partnership firm of such professionals. The loan term is for 10 years and the

security for such loans are registered mortgage of the premise for which loan is raised, demand promissory note and

personal guarantee of partners. If financed, hypothecation of equipment can also be considered as the additional security.

Other Loans

LIC Housing also provides loans against fixed deposits of nationalized banks, life insurance policies having surrender value

and post office instruments like national savings certificates, Kisan Vikas Patra. For individuals, loan up to 95% of face value

of liquid security or surrender value is applicable in case of life insurance policies. The minimum loan for loan against

securities is Rs 50000 for a maximum term of 20 years.

Under the loan against rental securitization scheme, LICHFL provides financial assistance to companies against the security

of commercial property-office premises- already owned or to be purchased with the help of the loan. The loan amount may

be utilized for repayment of existing loans (including takeovers) or purchase of fixed assets. The maximum term offered for

such loans is 10 years.

Source: LICHFL

6

6

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Source: KPMG

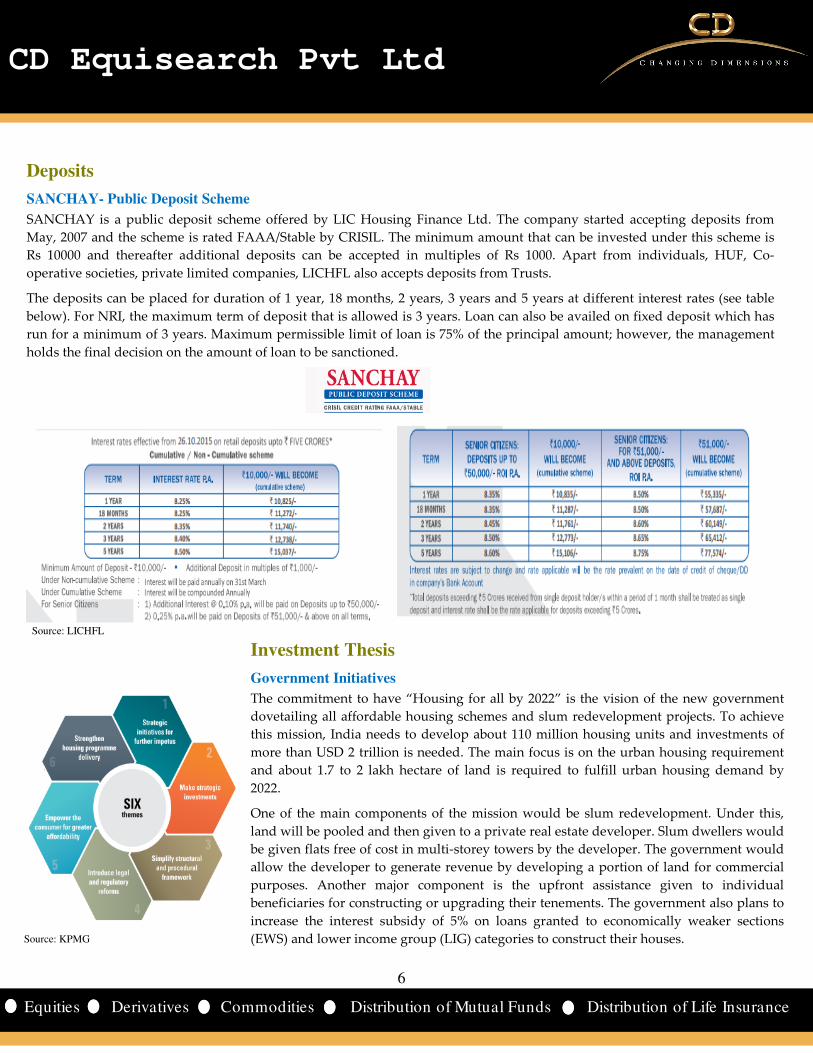

Deposits

SANCHAY- Public Deposit Scheme

SANCHAY is a public deposit scheme offered by LIC Housing Finance Ltd. The company started accepting deposits from

May, 2007 and the scheme is rated FAAA/Stable by CRISIL. The minimum amount that can be invested under this scheme is

Rs 10000 and thereafter additional deposits can be accepted in multiples of Rs 1000. Apart from individuals, HUF, Co-

operative societies, private limited companies, LICHFL also accepts deposits from Trusts.

The deposits can be placed for duration of 1 year, 18 months, 2 years, 3 years and 5 years at different interest rates (see table

below). For NRI, the maximum term of deposit that is allowed is 3 years. Loan can also be availed on fixed deposit which has

run for a minimum of 3 years. Maximum permissible limit of loan is 75% of the principal amount; however, the management

holds the final decision on the amount of loan to be sanctioned.

Source: LICHFL

Investment Thesis

Government Initiatives

The commitment to have “Housing for all by 2022” is the vision of the new government

dovetailing all affordable housing schemes and slum redevelopment projects. To achieve

this mission, India needs to develop about 110 million housing units and investments of

more than USD 2 trillion is needed. The main focus is on the urban housing requirement

and about 1.7 to 2 lakh hectare of land is required to fulfill urban housing demand by

2022.

One of the main components of the mission would be slum redevelopment. Under this,

land will be pooled and then given to a private real estate developer. Slum dwellers would

be given flats free of cost in multi-storey towers by the developer. The government would

allow the developer to generate revenue by developing a portion of land for commercial

purposes. Another major component is the upfront assistance given to individual

beneficiaries for constructing or upgrading their tenements. The government also plans to

increase the interest subsidy of 5% on loans granted to economically weaker sections

(EWS) and lower income group (LIG) categories to construct their houses.

7

7

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Stable Financials

Loan Portfolio

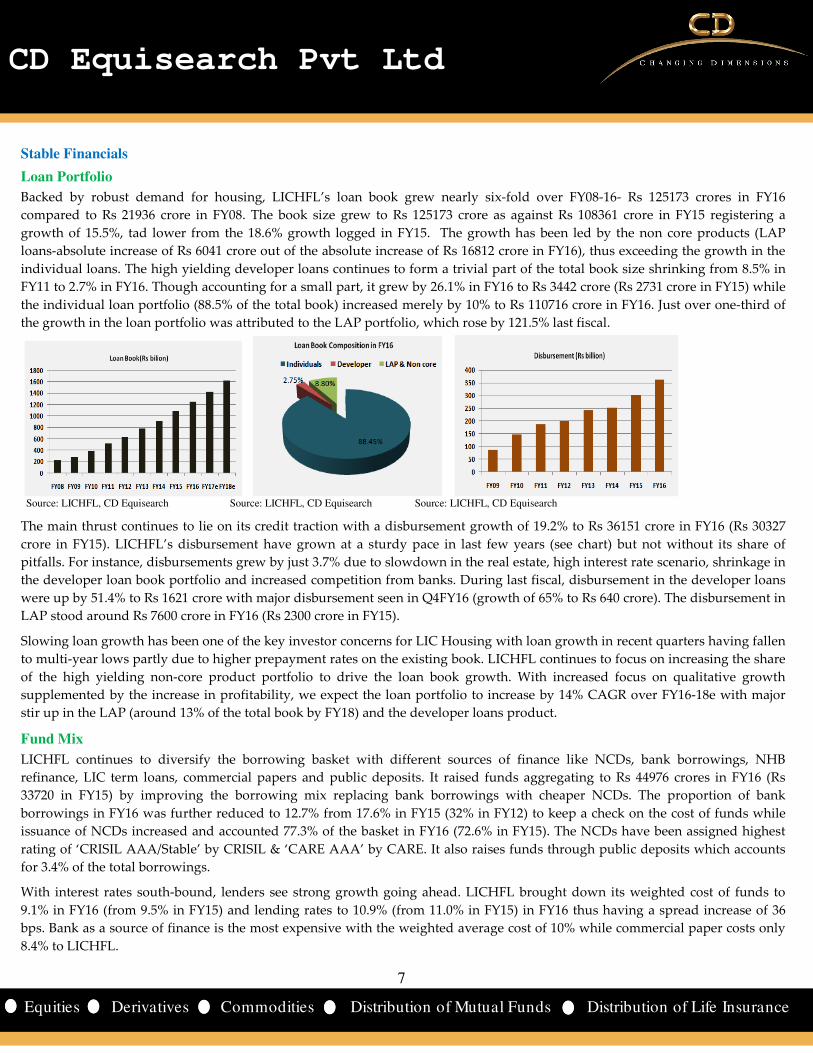

Backed by robust demand for housing, LICHFL’s loan book grew nearly six-fold over FY08-16- Rs 125173 crores in FY16

compared to Rs 21936 crore in FY08. The book size grew to Rs 125173 crore as against Rs 108361 crore in FY15 registering a

growth of 15.5%, tad lower from the 18.6% growth logged in FY15. The growth has been led by the non core products (LAP

loans-absolute increase of Rs 6041 crore out of the absolute increase of Rs 16812 crore in FY16), thus exceeding the growth in the

individual loans. The high yielding developer loans continues to form a trivial part of the total book size shrinking from 8.5% in

FY11 to 2.7% in FY16. Though accounting for a small part, it grew by 26.1% in FY16 to Rs 3442 crore (Rs 2731 crore in FY15) while

the individual loan portfolio (88.5% of the total book) increased merely by 10% to Rs 110716 crore in FY16. Just over one-third of

the growth in the loan portfolio was attributed to the LAP portfolio, which rose by 121.5% last fiscal.

Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch

The main thrust continues to lie on its credit traction with a disbursement growth of 19.2% to Rs 36151 crore in FY16 (Rs 30327

crore in FY15). LICHFL’s disbursement have grown at a sturdy pace in last few years (see chart) but not without its share of

pitfalls. For instance, disbursements grew by just 3.7% due to slowdown in the real estate, high interest rate scenario, shrinkage in

the developer loan book portfolio and increased competition from banks. During last fiscal, disbursement in the developer loans

were up by 51.4% to Rs 1621 crore with major disbursement seen in Q4FY16 (growth of 65% to Rs 640 crore). The disbursement in

LAP stood around Rs 7600 crore in FY16 (Rs 2300 crore in FY15).

Slowing loan growth has been one of the key investor concerns for LIC Housing with loan growth in recent quarters having fallen

to multi-year lows partly due to higher prepayment rates on the existing book. LICHFL continues to focus on increasing the share

of the high yielding non-core product portfolio to drive the loan book growth. With increased focus on qualitative growth

supplemented by the increase in profitability, we expect the loan portfolio to increase by 14% CAGR over FY16-18e with major

stir up in the LAP (around 13% of the total book by FY18) and the developer loans product.

Fund Mix

LICHFL continues to diversify the borrowing basket with different sources of finance like NCDs, bank borrowings, NHB

refinance, LIC term loans, commercial papers and public deposits. It raised funds aggregating to Rs 44976 crores in FY16 (Rs

33720 in FY15) by improving the borrowing mix replacing bank borrowings with cheaper NCDs. The proportion of bank

borrowings in FY16 was further reduced to 12.7% from 17.6% in FY15 (32% in FY12) to keep a check on the cost of funds while

issuance of NCDs increased and accounted 77.3% of the basket in FY16 (72.6% in FY15). The NCDs have been assigned highest

rating of ‘CRISIL AAA/Stable’ by CRISIL & ‘CARE AAA’ by CARE. It also raises funds through public deposits which accounts

for 3.4% of the total borrowings.

With interest rates south-bound, lenders see strong growth going ahead. LICHFL brought down its weighted cost of funds to

9.1% in FY16 (from 9.5% in FY15) and lending rates to 10.9% (from 11.0% in FY15) in FY16 thus having a spread increase of 36

bps. Bank as a source of finance is the most expensive with the weighted average cost of 10% while commercial paper costs only

8.4% to LICHFL.

8

8

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch

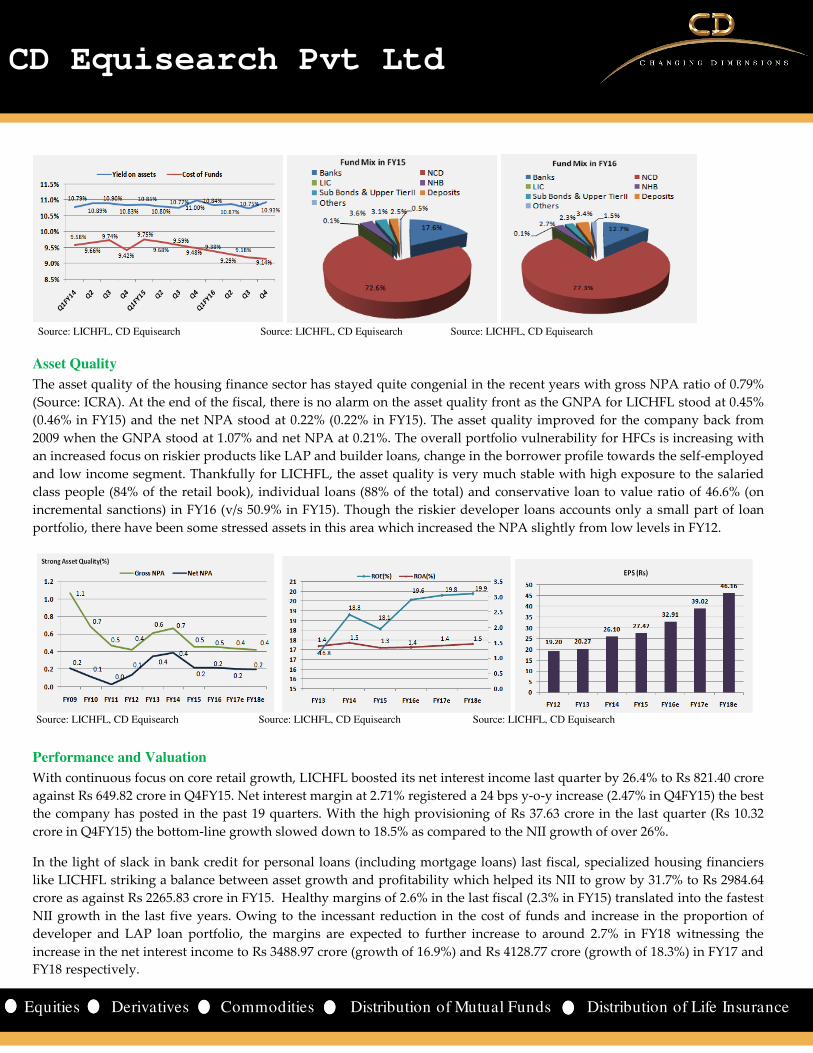

Asset Quality

The asset quality of the housing finance sector has stayed quite congenial in the recent years with gross NPA ratio of 0.79%

(Source: ICRA). At the end of the fiscal, there is no alarm on the asset quality front as the GNPA for LICHFL stood at 0.45%

(0.46% in FY15) and the net NPA stood at 0.22% (0.22% in FY15). The asset quality improved for the company back from

2009 when the GNPA stood at 1.07% and net NPA at 0.21%. The overall portfolio vulnerability for HFCs is increasing with

an increased focus on riskier products like LAP and builder loans, change in the borrower profile towards the self-employed

and low income segment. Thankfully for LICHFL, the asset quality is very much stable with high exposure to the salaried

class people (84% of the retail book), individual loans (88% of the total) and conservative loan to value ratio of 46.6% (on

incremental sanctions) in FY16 (v/s 50.9% in FY15). Though the riskier developer loans accounts only a small part of loan

portfolio, there have been some stressed assets in this area which increased the NPA slightly from low levels in FY12.

Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch

Performance and Valuation

With continuous focus on core retail growth, LICHFL boosted its net interest income last quarter by 26.4% to Rs 821.40 crore

against Rs 649.82 crore in Q4FY15. Net interest margin at 2.71% registered a 24 bps y-o-y increase (2.47% in Q4FY15) the best

the company has posted in the past 19 quarters. With the high provisioning of Rs 37.63 crore in the last quarter (Rs 10.32

crore in Q4FY15) the bottom-line growth slowed down to 18.5% as compared to the NII growth of over 26%.

In the light of slack in bank credit for personal loans (including mortgage loans) last fiscal, specialized housing financiers

like LICHFL striking a balance between asset growth and profitability which helped its NII to grow by 31.7% to Rs 2984.64

crore as against Rs 2265.83 crore in FY15. Healthy margins of 2.6% in the last fiscal (2.3% in FY15) translated into the fastest

NII growth in the last five years. Owing to the incessant reduction in the cost of funds and increase in the proportion of

developer and LAP loan portfolio, the margins are expected to further increase to around 2.7% in FY18 witnessing the

increase in the net interest income to Rs 3488.97 crore (growth of 16.9%) and Rs 4128.77 crore (growth of 18.3%) in FY17 and

FY18 respectively.

9

9

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch Source: LICHFL, CD Equisearch

The operating expense last fiscal was up by 23.6% to Rs 468.68 crore was mainly due to payments of commission (nearly

1%) on the non core business of the company. Also, due to the non core business, the provisions also increased in FY16 to

Rs 146.46 crore as the company maintains provisioning rate of 1% in the non core and 0.4% in the standard assets. This led

to just 19.8% increase in net profit (compared to the NII growth) to Rs 1660.79 crores (Rs 1386.19 crore in FY15). Going

ahead, we expect the profits to rise by 18.6% in FY17 to Rs 1969.36 crore and by 18.3% to Rs 2329.40 crore in FY18. The

return ratios like ROE (19.6% in FY16) and return on loan assets (1.4% in FY16) also improved owing to increase in the

profits. We expect ROE to further increase to around 19.8% current fiscal while return on loan assets to increase to 1.5% in

the next two years.

The stock currently trades at 2.1x FY17e BV (11.7x FY17e EPS) and 1.8x FY18e BV (9.9x FY18e EPS). LICHFL’s renewed

focus on boosting the high margin yielding LAP portfolio would galvanize its order book over the next few years. Healthy

growth in loan book supplemented by marginal rise in NIMs would culminate in over 18% growth (annual) in earnings

over the next two years; needless to mention its industry beating return on equity. We therefore assign “buy” rating with a

target of Rs 578 based on 2.3x FY18e BV (average of last three years), over a period of 6-9 months.

.

Risks and Concerns

Slowdown in Real Estate Sector

Adverse developments in the real estate sector causing delay and default in completion of projects may cause a setback to

disbursement of new loans. With pressure on both the demand and supply side, residential real estate has gone into a

vicious cycle of ever increasing cost, falling demand, liquidity crunch and, delay in approvals adding to the woes of the

developers.

Margins Pressure

Lending is the main activity of housing finance companies requiring maximum prudence on the part of lending financial

institutions. Inflationary trends, increased cost of borrowings, narrowing down of margins and intense competition pose

big challenge for sustaining profitability on a consistent basis. With interest rates declining and the home loan sector facing

declining asset quality, HFCs will face pressure on margins. The volatile macroeconomic environment, more precisely

fluctuations in interest rates, makes housing finance institutions more vulnerable to certain risks such as credit risk,

liquidity risk, and interest rate risk.

Stiff Competition

Spurt in competition, coupled with an intensive fight for market share between HFCs and Commercial Banks within the

same space can heighten the risk profile with aggressive underwriting standards. Over reliance on aggressively disbursing

loans as an easier option to build size and price war, and squeezing margins to undesirable levels are other areas of possible

threats.

10

10

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

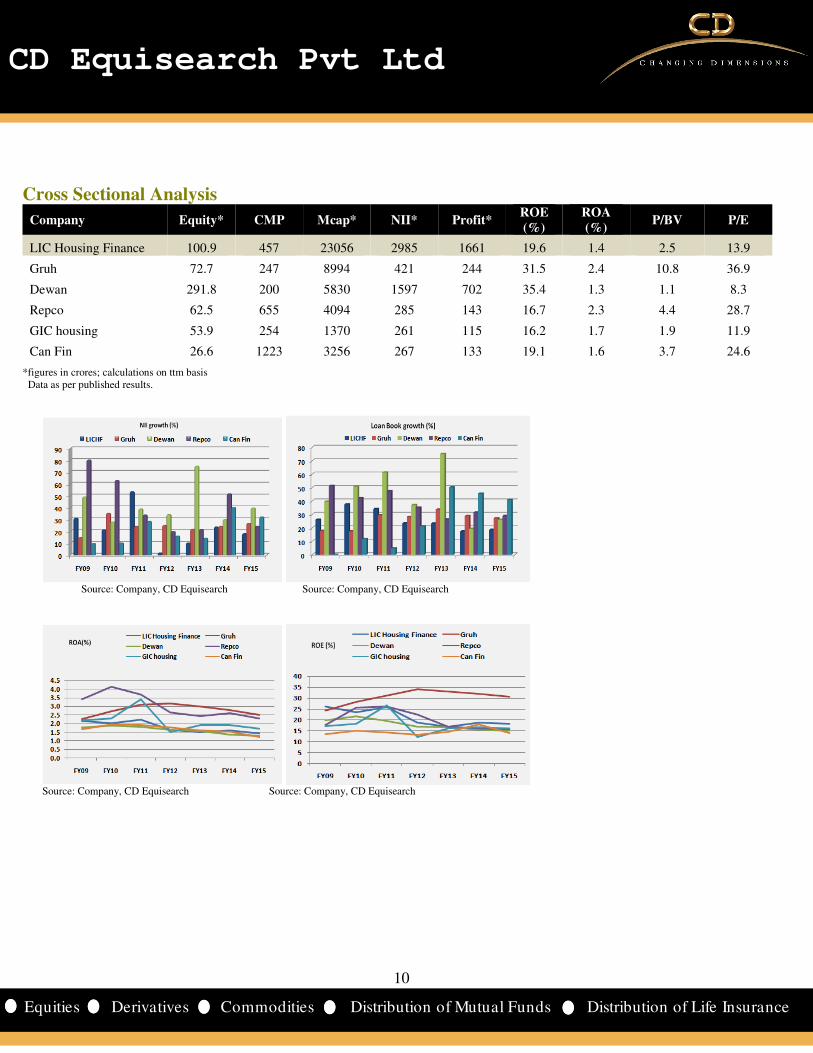

Cross Sectional Analysis

Company Equity* CMP Mcap* NII* Profit* ROE

(%)

ROA

(%) P/BV P/E

LIC Housing Finance 100.9 457 23056 2985 1661 19.6 1.4 2.5 13.9

Gruh 72.7 247 8994 421 244 31.5 2.4 10.8 36.9

Dewan 291.8 200 5830 1597 702 35.4 1.3 1.1 8.3

Repco 62.5 655 4094 285 143 16.7 2.3 4.4 28.7

GIC housing 53.9 254 1370 261 115 16.2 1.7 1.9 11.9

Can Fin 26.6 1223 3256 267 133 19.1 1.6 3.7 24.6

*figures in crores; calculations on ttm basis Data as per published results.

Source: Company, CD Equisearch Source: Company, CD Equisearch

Source: Company, CD Equisearch Source: Company, CD Equisearch

11

11

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financials

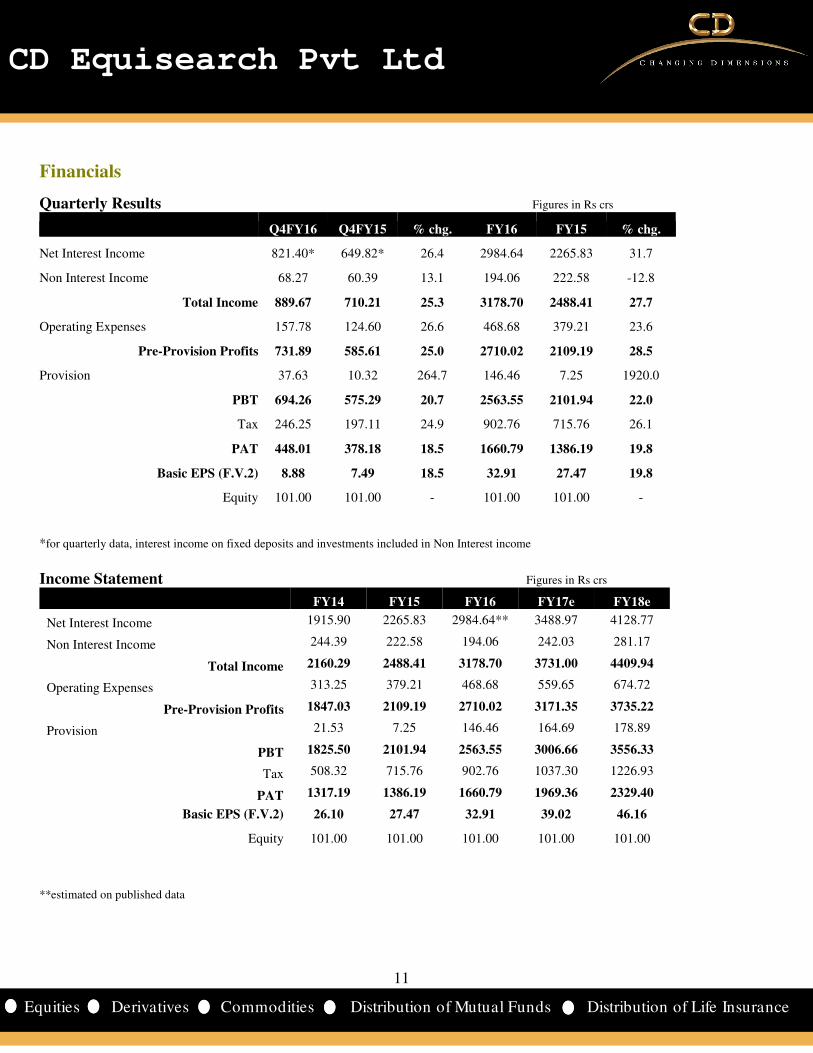

Quarterly Results Figures in Rs crs

Q4FY16 Q4FY15 % chg. FY16 FY15 % chg.

Net Interest Income 821.40* 649.82* 26.4 2984.64 2265.83 31.7

Non Interest Income 68.27 60.39 13.1 194.06 222.58 -12.8

Total Income 889.67 710.21 25.3 3178.70 2488.41 27.7

Operating Expenses 157.78 124.60 26.6 468.68 379.21 23.6

Pre-Provision Profits 731.89 585.61 25.0 2710.02 2109.19 28.5

Provision 37.63 10.32 264.7 146.46 7.25 1920.0

PBT 694.26 575.29 20.7 2563.55 2101.94 22.0

Tax 246.25 197.11 24.9 902.76 715.76 26.1

PAT 448.01 378.18 18.5 1660.79 1386.19 19.8

Basic EPS (F.V.2) 8.88 7.49 18.5 32.91 27.47 19.8

Equity 101.00 101.00 - 101.00 101.00 - *for quarterly data, interest income on fixed deposits and investments included in Non Interest income

Income Statement Figures in Rs crs

FY14 FY15 FY16 FY17e FY18e

Net Interest Income 1915.90 2265.83 2984.64** 3488.97 4128.77

Non Interest Income 244.39 222.58 194.06 242.03 281.17

Total Income 2160.29 2488.41 3178.70 3731.00 4409.94

Operating Expenses 313.25 379.21 468.68 559.65 674.72

Pre-Provision Profits 1847.03 2109.19 2710.02 3171.35 3735.22

Provision 21.53 7.25 146.46 164.69 178.89

PBT 1825.50 2101.94 2563.55 3006.66 3556.33

Tax 508.32 715.76 902.76 1037.30 1226.93

PAT 1317.19 1386.19 1660.79 1969.36 2329.40

Basic EPS (F.V.2) 26.10 27.47 32.91 39.02 46.16

Equity 101.00 101.00 101.00 101.00 101.00 **estimated on published data

12

12

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

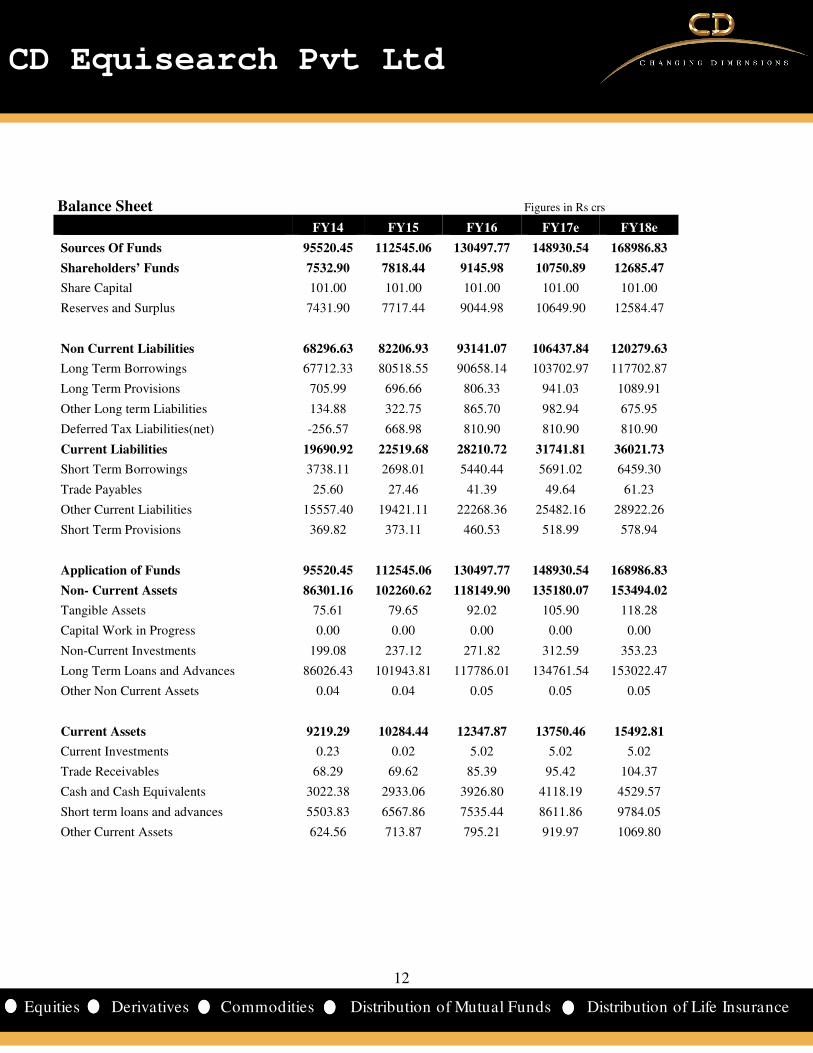

Balance Sheet Figures in Rs crs

FY14 FY15 FY16 FY17e FY18e

Sources Of Funds 95520.45 112545.06 130497.77 148930.54 168986.83

Shareholders’ Funds 7532.90 7818.44 9145.98 10750.89 12685.47

Share Capital 101.00 101.00 101.00 101.00 101.00

Reserves and Surplus 7431.90 7717.44 9044.98 10649.90 12584.47

Non Current Liabilities 68296.63 82206.93 93141.07 106437.84 120279.63

Long Term Borrowings 67712.33 80518.55 90658.14 103702.97 117702.87

Long Term Provisions 705.99 696.66 806.33 941.03 1089.91

Other Long term Liabilities 134.88 322.75 865.70 982.94 675.95

Deferred Tax Liabilities(net) -256.57 668.98 810.90 810.90 810.90

Current Liabilities 19690.92 22519.68 28210.72 31741.81 36021.73

Short Term Borrowings 3738.11 2698.01 5440.44 5691.02 6459.30

Trade Payables 25.60 27.46 41.39 49.64 61.23

Other Current Liabilities 15557.40 19421.11 22268.36 25482.16 28922.26

Short Term Provisions 369.82 373.11 460.53 518.99 578.94

Application of Funds 95520.45 112545.06 130497.77 148930.54 168986.83

Non- Current Assets 86301.16 102260.62 118149.90 135180.07 153494.02

Tangible Assets 75.61 79.65 92.02 105.90 118.28

Capital Work in Progress 0.00 0.00 0.00 0.00 0.00

Non-Current Investments 199.08 237.12 271.82 312.59 353.23

Long Term Loans and Advances 86026.43 101943.81 117786.01 134761.54 153022.47

Other Non Current Assets 0.04 0.04 0.05 0.05 0.05

Current Assets 9219.29 10284.44 12347.87 13750.46 15492.81

Current Investments 0.23 0.02 5.02 5.02 5.02

Trade Receivables 68.29 69.62 85.39 95.42 104.37

Cash and Cash Equivalents 3022.38 2933.06 3926.80 4118.19 4529.57

Short term loans and advances 5503.83 6567.86 7535.44 8611.86 9784.05

Other Current Assets 624.56 713.87 795.21 919.97 1069.80

13

13

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

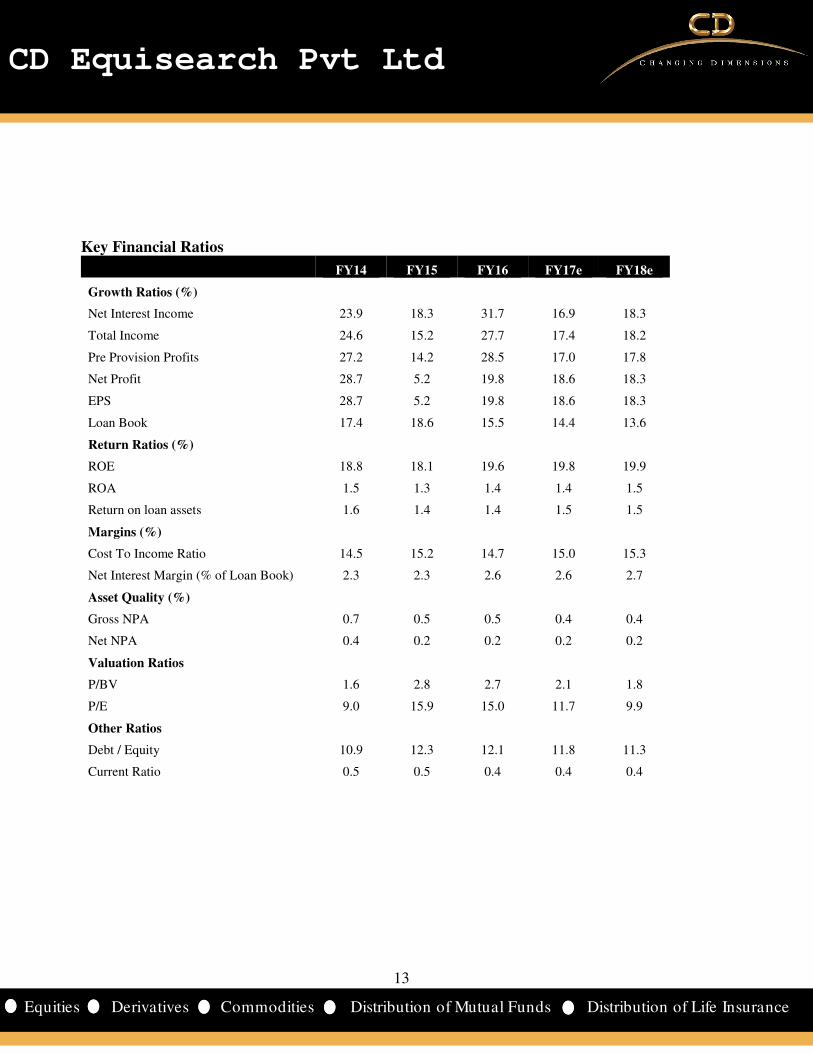

Key Financial Ratios

FY14 FY15 FY16 FY17e FY18e

Growth Ratios (%)

Net Interest Income 23.9 18.3 31.7 16.9 18.3

Total Income 24.6 15.2 27.7 17.4 18.2

Pre Provision Profits 27.2 14.2 28.5 17.0 17.8

Net Profit 28.7 5.2 19.8 18.6 18.3

EPS 28.7 5.2 19.8 18.6 18.3

Loan Book 17.4 18.6 15.5 14.4 13.6

Return Ratios (%)

ROE 18.8 18.1 19.6 19.8 19.9

ROA 1.5 1.3 1.4 1.4 1.5

Return on loan assets 1.6 1.4 1.4 1.5 1.5

Margins (%)

Cost To Income Ratio 14.5 15.2 14.7 15.0 15.3

Net Interest Margin (% of Loan Book) 2.3 2.3 2.6 2.6 2.7

Asset Quality (%)

Gross NPA 0.7 0.5 0.5 0.4 0.4

Net NPA 0.4 0.2 0.2 0.2 0.2

Valuation Ratios

P/BV 1.6 2.8 2.7 2.1 1.8

P/E 9.0 15.9 15.0 11.7 9.9

Other Ratios

Debt / Equity 10.9 12.3 12.1 11.8 11.3

Current Ratio 0.5 0.5 0.4 0.4 0.4

14

14

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

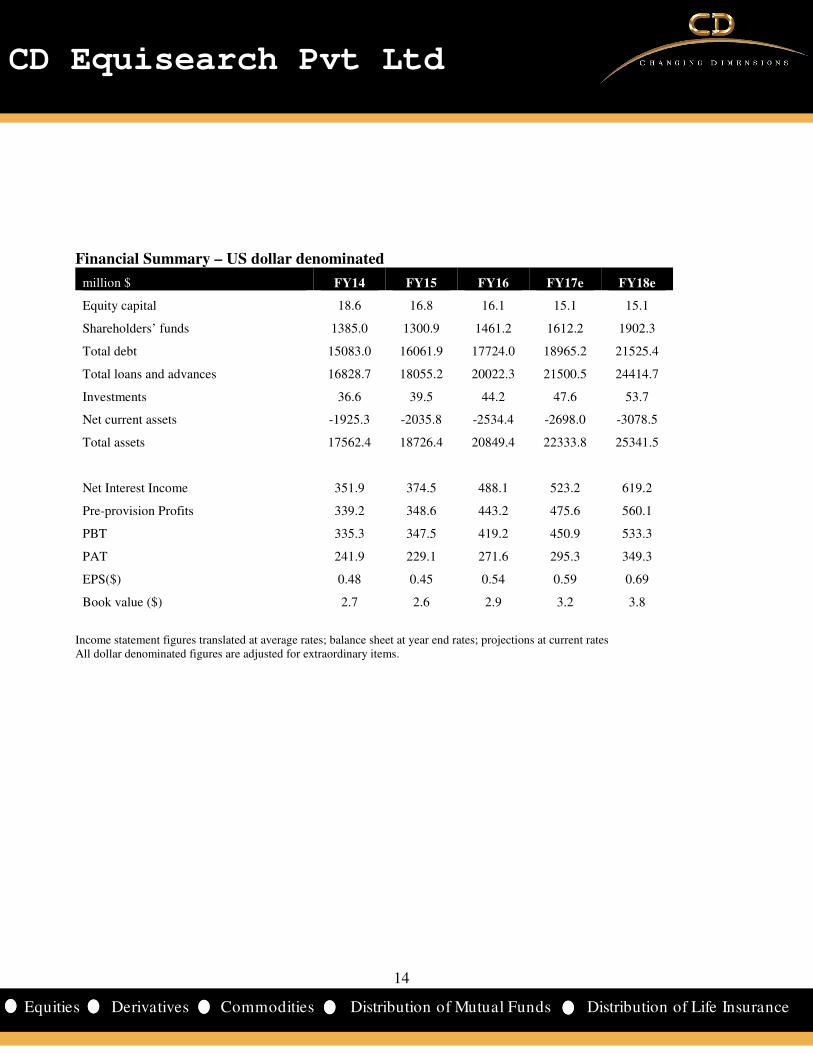

Financial Summary – US dollar denominated

million $ FY14 FY15 FY16 FY17e FY18e

Equity capital 18.6 16.8 16.1 15.1 15.1

Shareholders’ funds 1385.0 1300.9 1461.2 1612.2 1902.3

Total debt 15083.0 16061.9 17724.0 18965.2 21525.4

Total loans and advances 16828.7 18055.2 20022.3 21500.5 24414.7

Investments 36.6 39.5 44.2 47.6 53.7

Net current assets -1925.3 -2035.8 -2534.4 -2698.0 -3078.5

Total assets 17562.4 18726.4 20849.4 22333.8 25341.5

Net Interest Income 351.9 374.5 488.1 523.2 619.2

Pre-provision Profits 339.2 348.6 443.2 475.6 560.1

PBT 335.3 347.5 419.2 450.9 533.3

PAT 241.9 229.1 271.6 295.3 349.3

EPS($) 0.48 0.45 0.54 0.59 0.69

Book value ($) 2.7 2.6 2.9 3.2 3.8

Income statement figures translated at average rates; balance sheet at year end rates; projections at current rates All dollar denominated figures are adjusted for extraordinary items.

15

15

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Recommendation

The Housing Finance Sector in India can be classified as one of the sunshine sectors as it rides on a host of structural

factors that are expected to continue fuelling growth in years to come. The housing finance has managed to grow at an

annual rate of 18% during FY11 to FY16, much higher than overall bank credit growth rate. HFCs which initially lost a

significant market share to banks, have managed to regain some of their lost ground with a combined market share of

37 per cent in FY16 (Source: ICRA). Housing credit growth picked up from Q2FY16 onwards, supported by

disbursements against construction linked loans, growth in small ticket affordable housing segment and renewed

demand from Tier II and III cities.

To achieve the “Housing for all by 2022” mission, India needs to develop about 110 million housing units and

investments of more than USD 2 trillion is needed. The main focus is on the urban housing requirement and about 1.7

to 2 lakh hectare of land is required to fulfill urban housing demand by 2022. Under the slum redevelopment, land will

be pooled and then given to a private real estate developer. Slum dwellers would be given flats free of cost in multi-

storey towers by the developer. The government also plans to increase the interest subsidy of 5% on loans granted to

economically weaker sections (EWS) and lower income group (LIG) categories to construct their houses. The higher

cap on lending spread set by NHB, RHF and the UHF from 2% earlier to 3.5% has proved positive for the sector,

especially HFCs operating in small ticket housing loans segment.

Investor sentiment for the housing sector has been good so far as reflected by the capital infusion of around Rs 45

billion in FY16. In ICRA’s estimate, HFCs will require external capital of Rs 185-280 billion for the mortgage

penetration to improve further and achieve an annual growth of 20-22% over the next five years.

One of the biggest challenges facing the housing finance industry is the lack of formal credit flow to the lower income

segments for their housing needs. This has resulted in a huge shortage of housing for these segments and a multi

prolonged effort is required to address the problem in all its dimensions. This broadening gap between the demand

and supply of affordable housing units and lack of adequate/appropriate financial solutions needs a prolonged effort.

LICHFL, in the past few years, has not only managed to post robust earnings growth but also broadened its product

portfolio. With the growth in the individual retail loans, it has also kept the pace of the developer loans and is focusing

more on the LAP product in years to come. The loan portfolio is expected to clock Rs 143209 crores in FY17 which is a

growth of 14.4% and to Rs 162625 crores in FY18 with LAP constituting 13% of the total portfolio.

The steady improvement in the margins has also translated in robust NII growth in the recent years and is expected to

further grow at a CAGR of 17.6% over the next two years. The company expects builder’s interest in the affordable

housing to gather pace and it would like to cater to this segment. The loan portfolio of LICHFL is expected to grow at a

CAGR of 14% for the next two years with stable asset quality. The cost of funds is expected to further come down

benefitting the net interest margins for the company.

The stock currently trades at 2.1x FY17e BV (11.7x FY17e EPS) and 1.8x FY18e BV (9.9x FY18e EPS). LICHFL’s renewed

focus on boosting the high margin yielding LAP portfolio would galvanize its order book over the next few years.

Healthy growth in loan book supplemented by marginal rise in NIMs would culminate in over 18% growth (annual)

in earnings over the next two years; needless to mention its industry beating return on equity. We therefore assign

“buy” rating with a target of Rs 578 based on 2.3x FY18e BV (average of last three years), over a period of 6-9 months.

16

16

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Disclosure& Disclaimer CD Equisearch Private Limited (hereinafter referred to as ‘CD Equi’) is a Member registered with National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX Stock Exchange Limited). CD

Equi is also registered as Depository Participant with CDSL and AMFI registered Mutual Fund Advisor. The associates of CD Equi are

engaged in activities relating to NBFC-ND - Financing and Investment, Commodity Broking, Real Estate, etc.

CD Equi is registered under SEBI (Research Analysts) Regulations, 2014. Further, CD Equi hereby declares that –

• No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

• CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more than one percent/material

conflict of interest in the subject company(s).

• CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve

months.

• CD Equi/its research analysts has not served as an officer, director or employee of company covered by analysts and has not been

engaged in market making activity of the company covered by analysts.

This document is solely for the personal information of the recipient and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such

investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in

this document (including the merits and risks involved) and should consult their own advisors to determine the merits and risks of such an

investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading

volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general

guidance only. CD Equi or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to

any person from any inadvertent error in the information contained in this report. CD Equi has not independently verified all the information

contained within this document. Accordingly, we cannot testify nor make any representation or warranty, express or implied, to the accuracy,

contents or data contained within this document.

While, CD Equi endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or

other reasons that prevent us from doing so.

This document is being supplied to you solely for your information and its contents, information or data may not be reproduced, redistributed

or passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liable for any loss or damage that may

arise from or in connection with the use of this information.

CD Equisearch Private Limited (CIN: U67120WB1995PTC071521)

Registered Office: 37, Shakespeare Sarani, 1st Floor, Kolkata – 700 017; Phone: +91(33) 4488 0000; Fax: +91(33) 2289 2557; Corporate Office: 10,

Vasawani Mansion, 2nd Floor, Dinshaw Wachha Road, Churchgate, Mumbai – 400 020; Phone: +91(22) 2283 0652/0653; Fax: +91(22) 2283, 2276

Website: www.cdequi.com; Email: [email protected]

buy: >20% accumulate: >10% to ≤20% hold: ≥-10% to ≤10% reduce: ≥-20% to <-10% sell: <-20%