Capital Budegeting Finall

47

Capital Budgeting T echniques

-

Upload

nitesh-singh -

Category

Documents

-

view

224 -

download

0

Transcript of Capital Budegeting Finall

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 1/47

Capital Budgeting Techniques

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 2/47

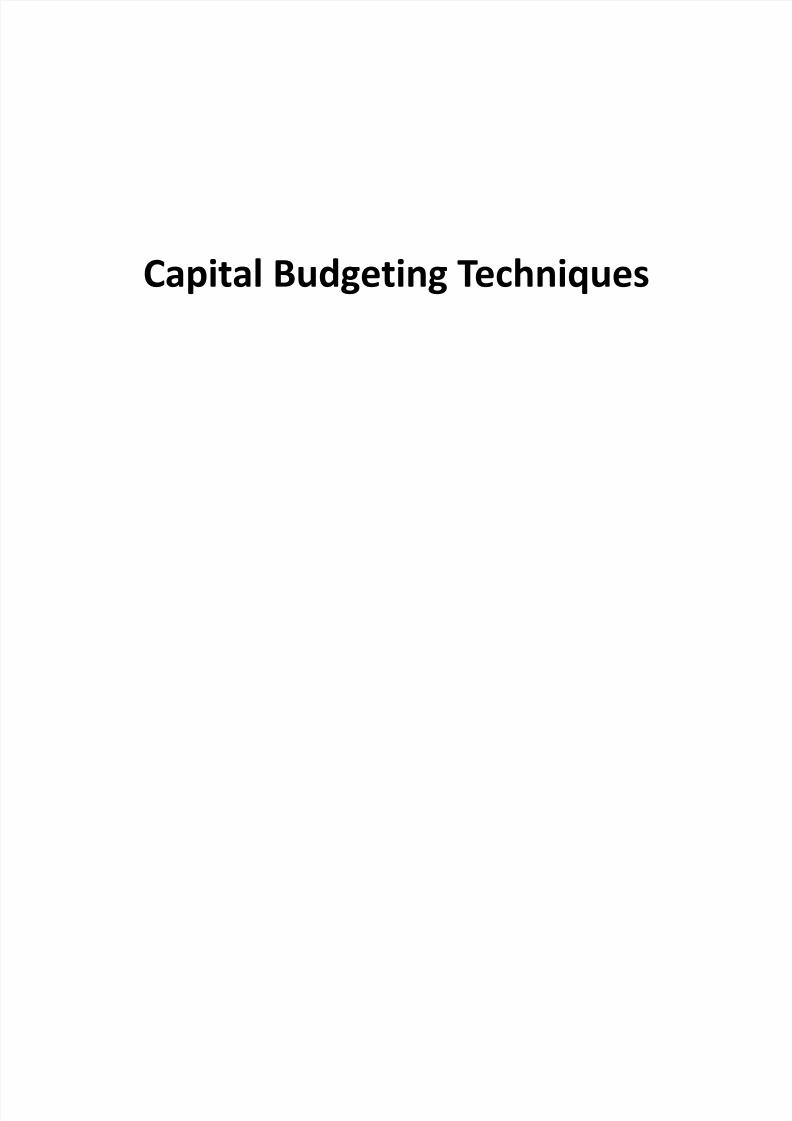

` The investment decisions of a firm are generally knownas the capital budgeting, or capital expendituredecisions.

` The firm¶s investment decisions would generally include

expansion, acquisition, modernization and replacementof the long-term assets. Sale of a division or business(divestment) is also as an investment decision.

` Decisions like the change in the methods of sales

distribution, or an advertisement campaign or aresearch and development programme have long-termimplications for the firm¶s expenditures and benefits, andtherefore, they should also be evaluated as investmentdecisions.

Nature of Investment Decisions

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 3/47

� The exchange of current funds for future

benefits.

� The funds are invested in long-term assets.� The future benefits will occur to the firm over

a series of years.

Features of Investment Decisions

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 4/47

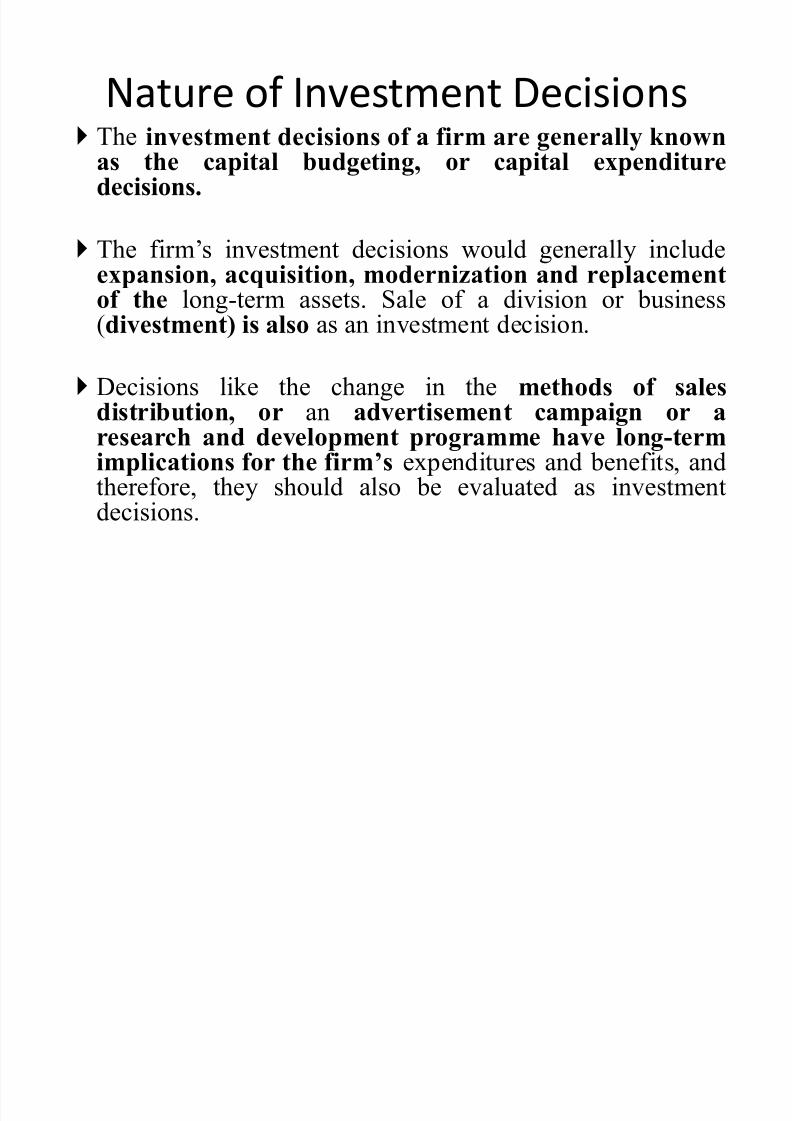

� Three steps are involved in the evaluation of

an investment:

1. Estimation of cash flows2. Estimation of the required rate of return (the

opportunity cost of capital)

3. Application of a decision rule for making th

echoice

Investment Evaluation Criteria

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 5/47

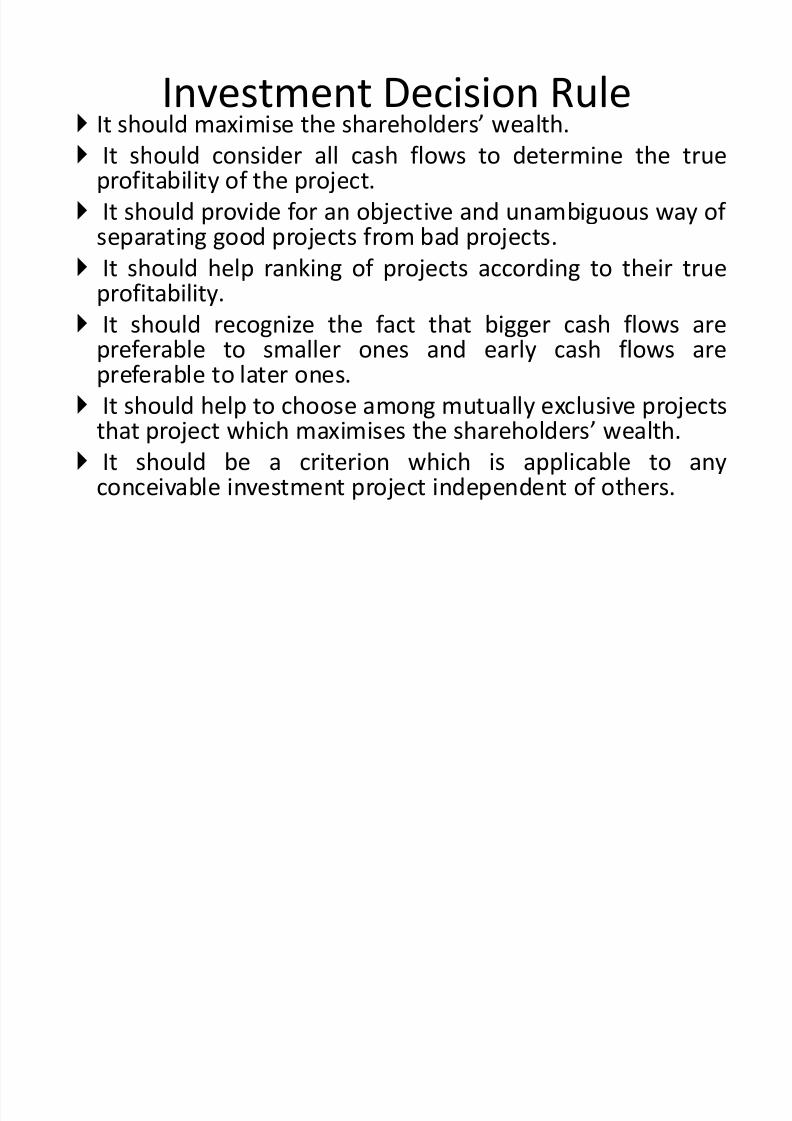

` It should maximise the shareholders wealth.

` It should consider all cash flows to determine the trueprofitability of the project.

` It should provide for an objective and unambiguous way of separating good projects from bad projects.

`It s

hould

help ranking of projects according to t

heir trueprofitability.

` It should recognize the fact that bigger cash flows arepreferable to smaller ones and early cash flows arepreferable to later ones.

`It s

hould

help to c

hoose among mutually exclusive projectsthat project which maximises the shareholders wealth.

` It should be a criterion which is applicable to anyconceivable investment project independent of others.

Investment Decision Rule

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 6/47

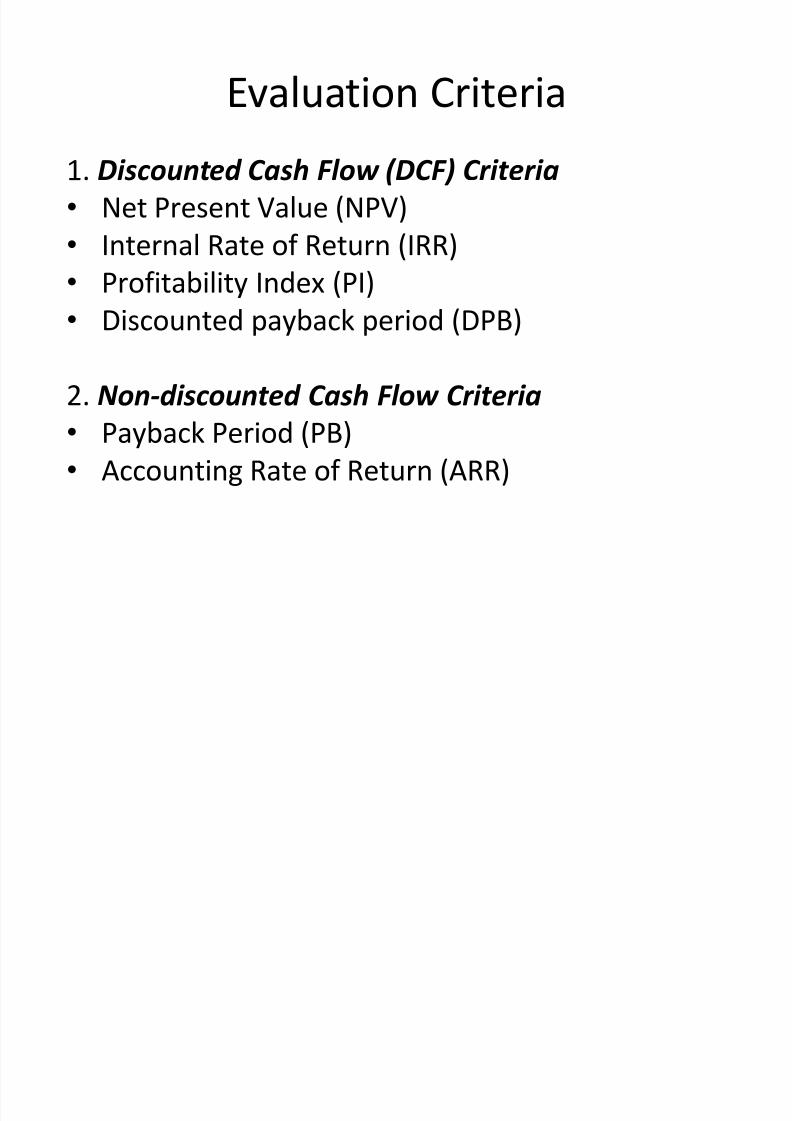

1. Discounted Cash Flow (DCF) Criteria

� Net Present Value (NPV)

� Internal Rate of Return (IRR)

� Profitability Index (PI)� Discounted payback period (DPB)

2. N on-discounted Cash Flow Criteria

� Payback Period (PB)

� Accounting Rate of Return (ARR)

Evaluation Criteria

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 7/47

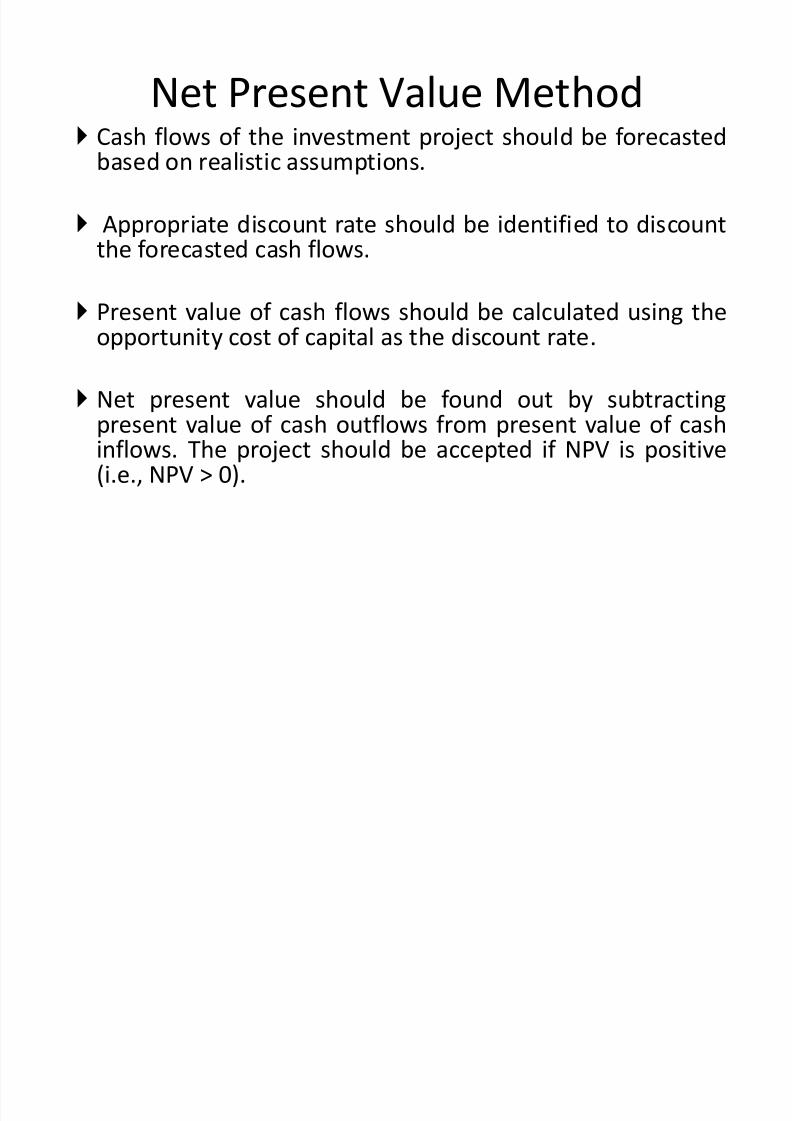

` Cash flows of the investment project should be forecastedbased on realistic assumptions.

` Appropriate discount rate should be identified to discountthe forecasted cash flows.

` Present value of cash flows should be calculated using theopportunity cost of capital as the discount rate.

` Net present value should be found out by subtractingpresent value of cash outflows from present value of cash

inflows. The project should be accepted if NPV is positive(i.e., NPV > 0).

Net Present Value Method

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 8/47

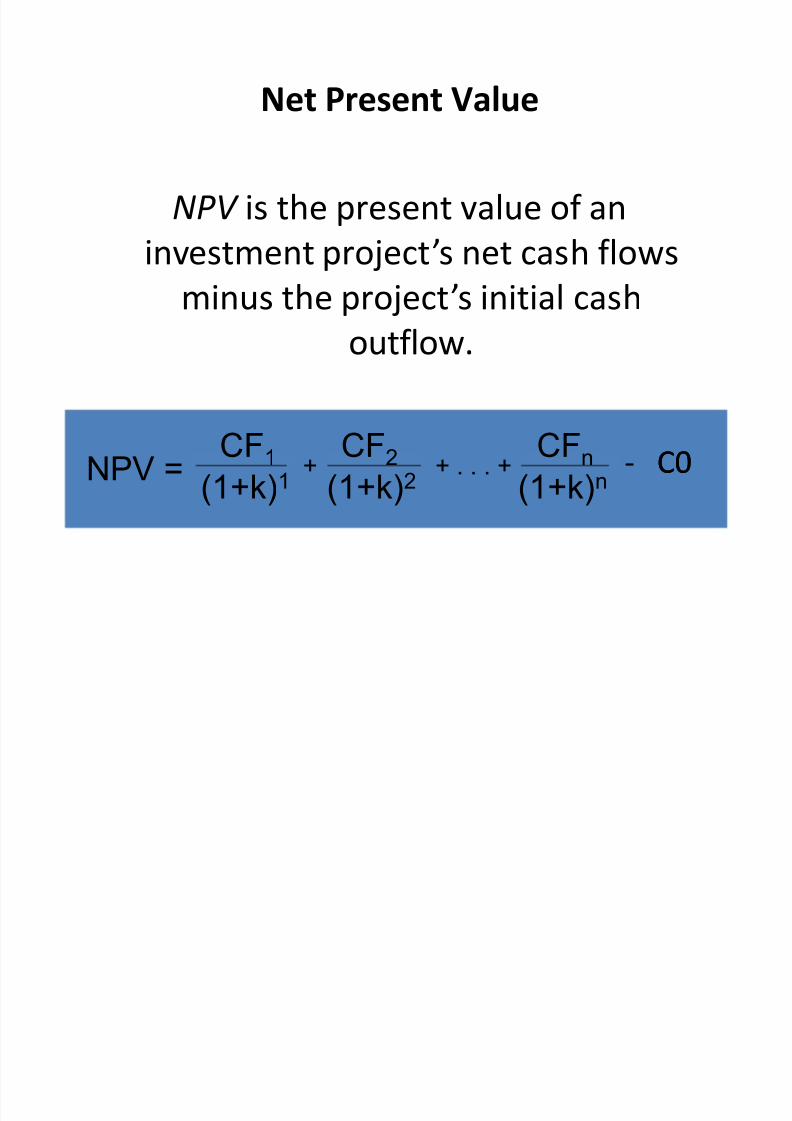

Net Present Value

NPV is the present value of an

investment projects net cash flows

minus the projects initial cash

outflow.

CF1 CF2 CFn

(1+k)1 (1+k)2 (1+k)n+ . . . ++ - C0C0NPV =

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 9/47

� Accept the project when NPV is positive NPV > 0

� Reject the project when NPV is negative NPV < 0

� May accept the project when NPV is zero NPV = 0

� The NPV method can be used to select between mut ually

ex cl usiv e pr oject s; the one w i th the higher NPV should be selected.

Acceptance Rule

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 10/47

NPV is most acceptable investment rule for the

following reasons:

` Time value

` Measure of true profitability

` Value-additivity` Shareholder value

Limitations:

` Involved cash flow estimation

` Discount rate difficult to determine

` Mutually exclusive projects

` Ranking of projects

Evaluation of the NPV Method

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 11/47

Julie Miller is evaluating a new project for her

firm, Bask et Wonders ( BW). She has

determined that the after-tax cash flows for the

project will be $10,000; $12,000; $15,000;$10,000; and $7,000, respectively, for each of

the Years 1 through 5. The initial cash outlay

will be $40,000. The discount rate (k) for thisproject is 13%. Should this project be

accepted?

Julie Miller is evaluating a new project for her

firm, Bask et Wonders ( BW). She has

determined that the after-tax cash flows for the

project will be $10,000; $12,000; $15,000;$10,000; and $7,000, respectively, for each of

the Years 1 through 5. The initial cash outlay

will be $40,000. The discount rate (k) for thisproject is 13%. Should this project be

accepted?

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 12/47

` Assume that the cost of capital is 6% for a project involvinga lumpsum cash outflow of Rs.8,200 and cash inflow of Rs.2,000 per annum for 5 years. What will be the NetPresent Value ?

` Suppose we are asked to decide whether or not a newconsumer product should be launched. Based on projectedsales and costs, we expect that the cash flows over the five-year life of the project will be Rs.2,000 in the first two

years, Rs.4,000 in th

e next two, and Rs.5,000 in th

e lastyear. It will cost about Rs.10,000 to begin production. Weuse a 10 % discount rate to evaluate new products. Whatshould we do here?

Questions

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 13/47

` Suppose the cash revenues from a fertilizerbusiness will be Rs.20,000 per year, assumingeverything goes as expected. Cash costs(including taxes) will be Rs.14,000 per year. Thebusiness will wind down in eight years. The plant,property, and equipment will be worth Rs.2,000as salvage at that time. The project costsRs.30,000 to launch. We use a 15 percent

discount rate on new projects such as this one. Isthis a good investment? If there are 1,000 sharesof stock outstanding, what will be the effect onthe price per share of taking this investment?

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 14/47

`̀ PBPPBP is the period of time required for the cumulative expected cash

flows from an investment project to equal the initial cash outflow.

` Loosely, the payback is the length of time it takes to recover ourinitial investment

` Business enterprises following payback period use "stipulatedpayback period", which acts as a standard for screening the project.

� This method is very flawed, primarily because it ignores later year

cash flows and the present value of future cash flows.

Payback Period

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 15/47

� If the project generates constant annual cash

inflows, th

e payback period can be computed bydividing cash outlay by the annual cash inflow.That is:

� Payback = Initial Investment = Co

Annual Cash Inflow C

� Unequal cash flows In case of unequal cash

inflows, th

e payback period can be found out byadding up the cash inflows until the total is equalto the initial cash outlay.

Payback Period

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 16/47

� The project would be accepted if its payback

period is less than the maximum or standard

payback period set by management.

� As a ranking method, it gives highest ranking

to the project, which has the shortest payback

period and lowest ranking to the project with

highest payback period.

Acceptance Rule

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 17/47

� Assume that a project requires an outlay of

Rs.50,000 and yields annual cash inflow of

Rs12,500 for 7 years. The payback period for the

project will be.

� Suppose that a project requires a cash outlay of

Rs 20,000, and generates cash inflows of Rs8,000; Rs 7,000; Rs 4,000; and Rs 3,000 during

the next 4 years. What is the projects payback?

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 18/47

Julie Miller is evaluating a new project for her

firm, Bask et Wonders ( BW). She has

determined that the after-tax cash flows for the

project will be $10,000; $12,000; $15,000;

$10,000; and $7,000, respectively, for each of

the Years 1 through 5. The initial cash outlay

will be $40,000.

Julie Miller is evaluating a new project for her

firm, Bask et Wonders ( BW). She has

determined that the after-tax cash flows for the

project will be $10,000; $12,000; $15,000;

$10,000; and $7,000, respectively, for each of

the Years 1 through 5. The initial cash outlay

will be $40,000.

Proposed Project Data

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 19/47

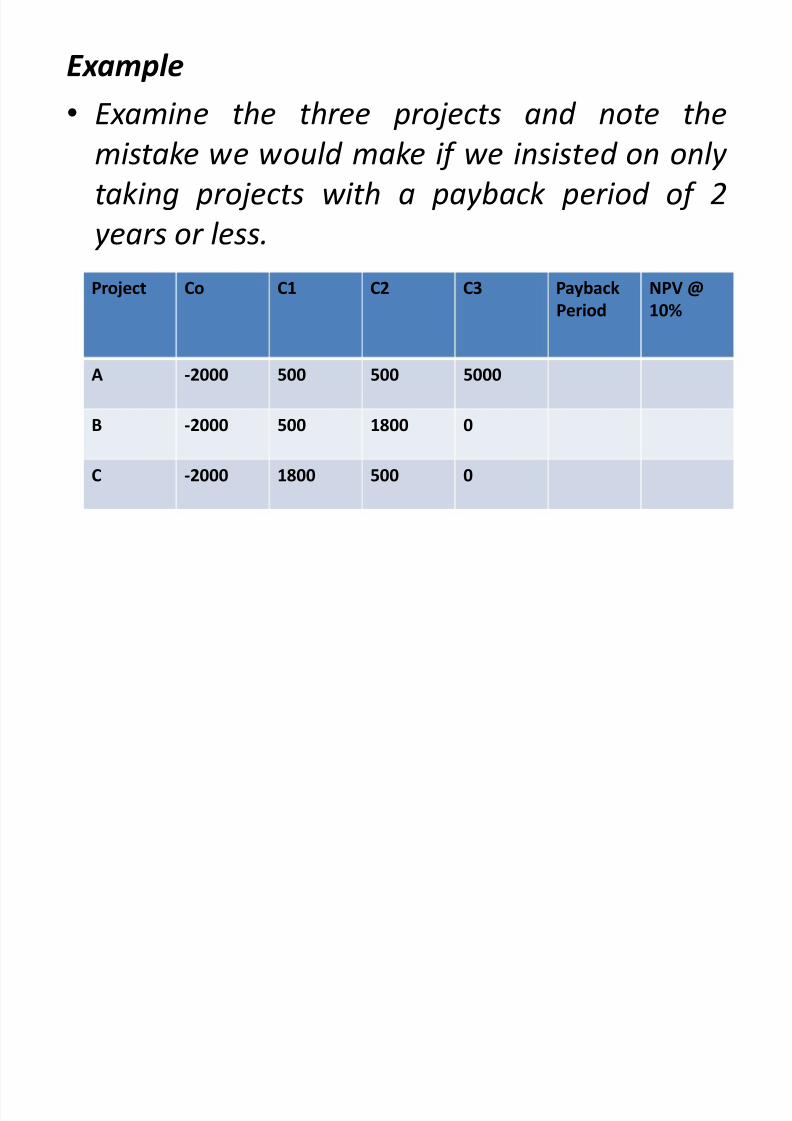

Ex ample

� E x amine the thr ee pr oject s and note the

mist ak e we would mak e if we insisted on only

t aking pr oject s w i th a pay back peri od o f 2

years or less.

Project Co C1 C2 C3 Payback

Period

NPV @

10%

A -2000 500 500 5000

B -2000 500 1800 0

C -2000 1800 500 0

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 20/47

� The discounted payback period is the length of time until the sum of the discounted cash flows is

equal to the initial investment.

� Loosely speaking, Using Discounted PBP, we getour money back, along with the interest we could

have earned elsewhere, in four years.

� If a project ever pays back on a discounted basis,

then it must have a positive NPV

� The cutoff still has to be arbitrarily set and cash

flows beyond that point are ignored.

Discounted Payback

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 21/47

� PI is the ratio of the present value of cash inflows to the present value of cash outflows.The present values of cash flows are obtained

at a discount rate equivalent to cost of capital� Select all projects whose profitability index is

greater than 1

� Wh

en th

ere are mutually exclusive projects,select the project with highest PI

Profitability Index/ BCR

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 22/47

� Assume that the cost of capital is 6% for a project involving a

lumpsum cash outflow of Rs.8,200 and cash inflow of Rs.2,000per annum for 5 years. What will be the P I ?

� Suppose we are asked to decide whether or not a newconsumer product should be launched. Based on projected

sales and costs, we expect that the cash flows over the five-year life of the project will be Rs.2,000 in the first two years,Rs.4,000 in the next two, and Rs.5,000 in the last year. It willcost about Rs.10,000 to begin production. We use a 10 %discount rate to evaluate new products. What should we do

here?

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 23/47

� The accounting rate of return is the ratio of the average after tax profit divided by theaverage investment. The average investment

would be equal to half of the originalinvestment if it were depreciated constantly.

� A variation of th

e ARR meth

od is to divideaverage earnings after taxes by the originalcost of the project instead of the average cost.

Accounting Rate of Return method

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 24/47

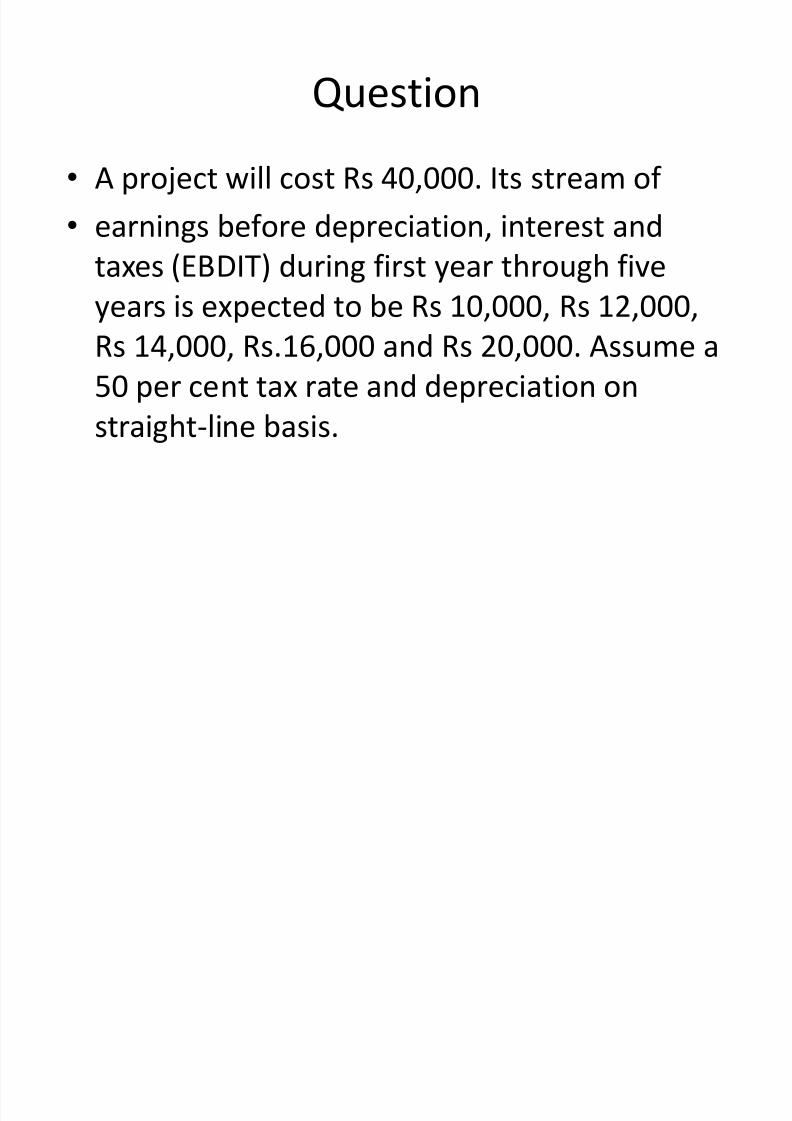

� A project will cost Rs 40,000. Its stream of

� earnings before depreciation, interest and

taxes (EBDIT

) during first year th

rough

fiveyears is expected to be Rs 10,000, Rs 12,000,

Rs 14,000, Rs.16,000 and Rs 20,000. Assume a

50 per cent tax rate and depreciation on

straight-line basis.

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 25/47

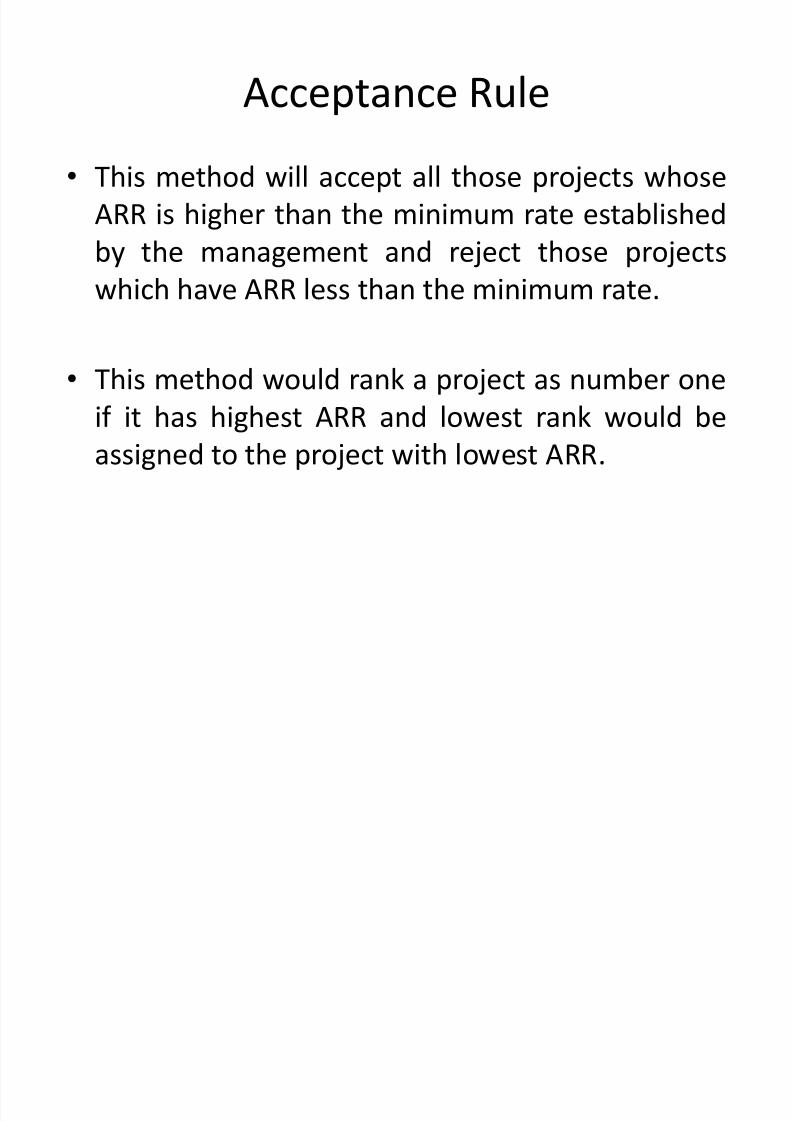

� This method will accept all those projects whose

ARR is higher than the minimum rate established

by the management and reject those projects

which have ARR less than the minimum rate.

� This method would rank a project as number one

if it has highest ARR and lowest rank would beassigned to the project with lowest ARR.

Acceptance Rule

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 26/47

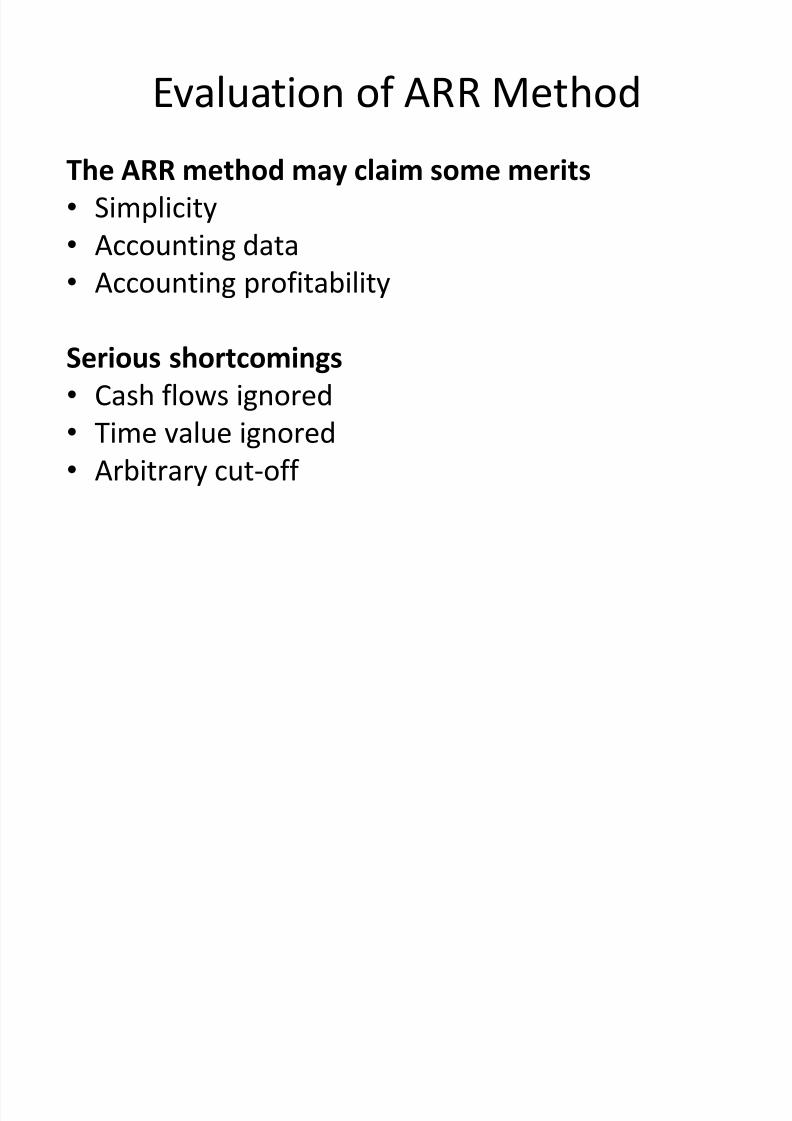

The ARR method may claim some merits

� Simplicity

� Accounting data

� Accounting profitability

Serious shortcomings

� Cash flows ignored

� Time value ignored

� Arbitrary cut-off

Evaluation of ARR Method

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 27/47

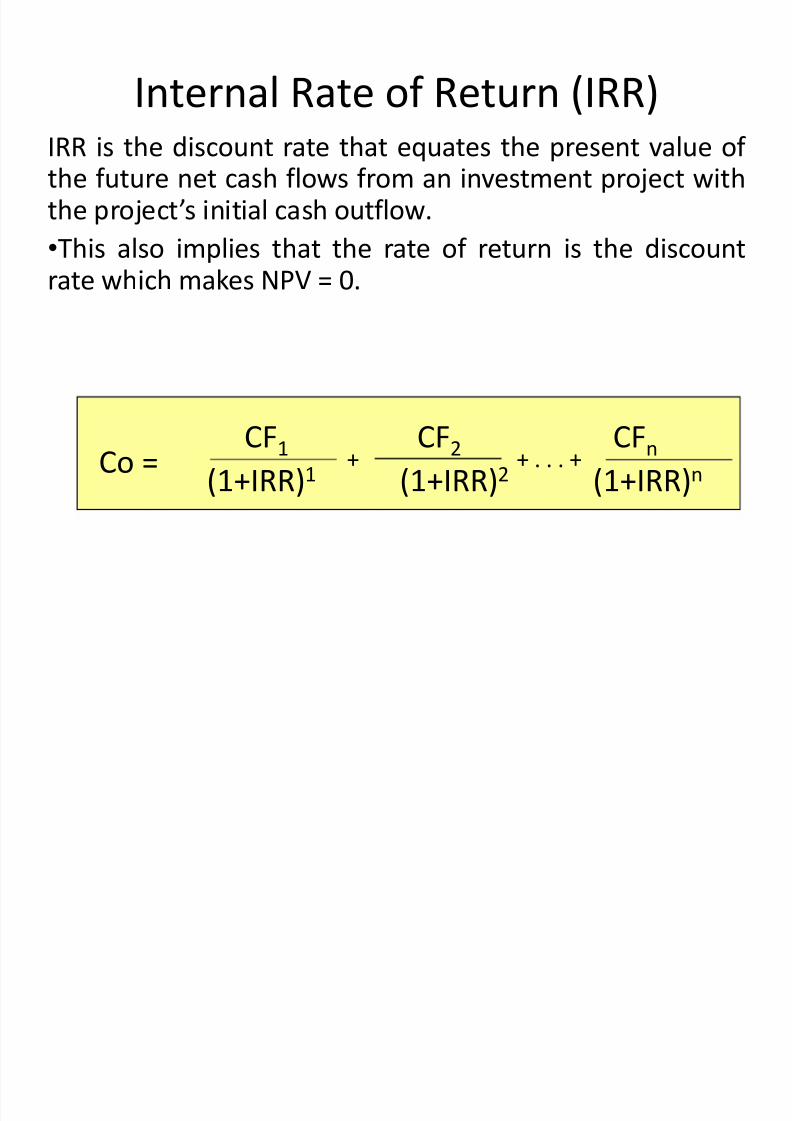

IRR is the discount rate that equates the present value of the future net cash flows from an investment project with

the projects initial cash outflow.

�This also implies that the rate of return is the discount

rate which makes NPV = 0.

Internal Rate of Return (IRR)

CF1 CF2 CFn

(1+IRR)1 (1+IRR)2 (1+IRR)n+ . . . ++Co =

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 28/47

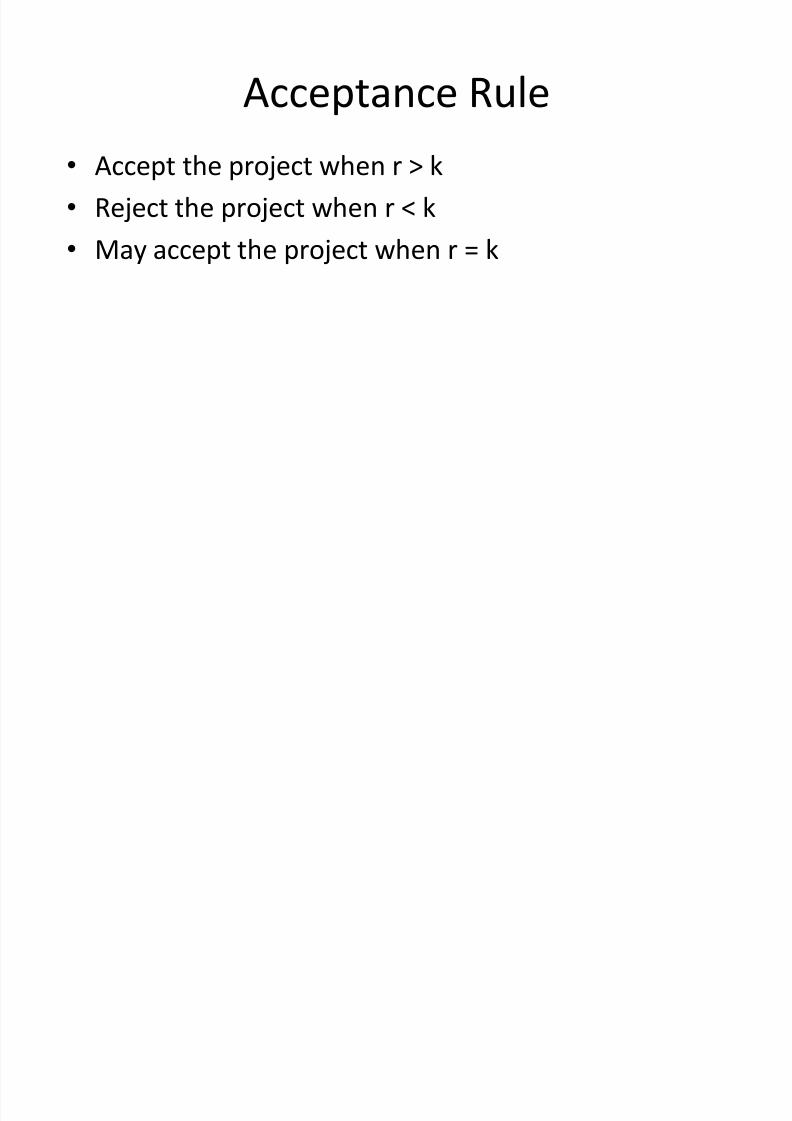

� Accept the project when r > k

� Reject the project when r < k

� May accept the project when r = k

Acceptance Rule

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 29/47

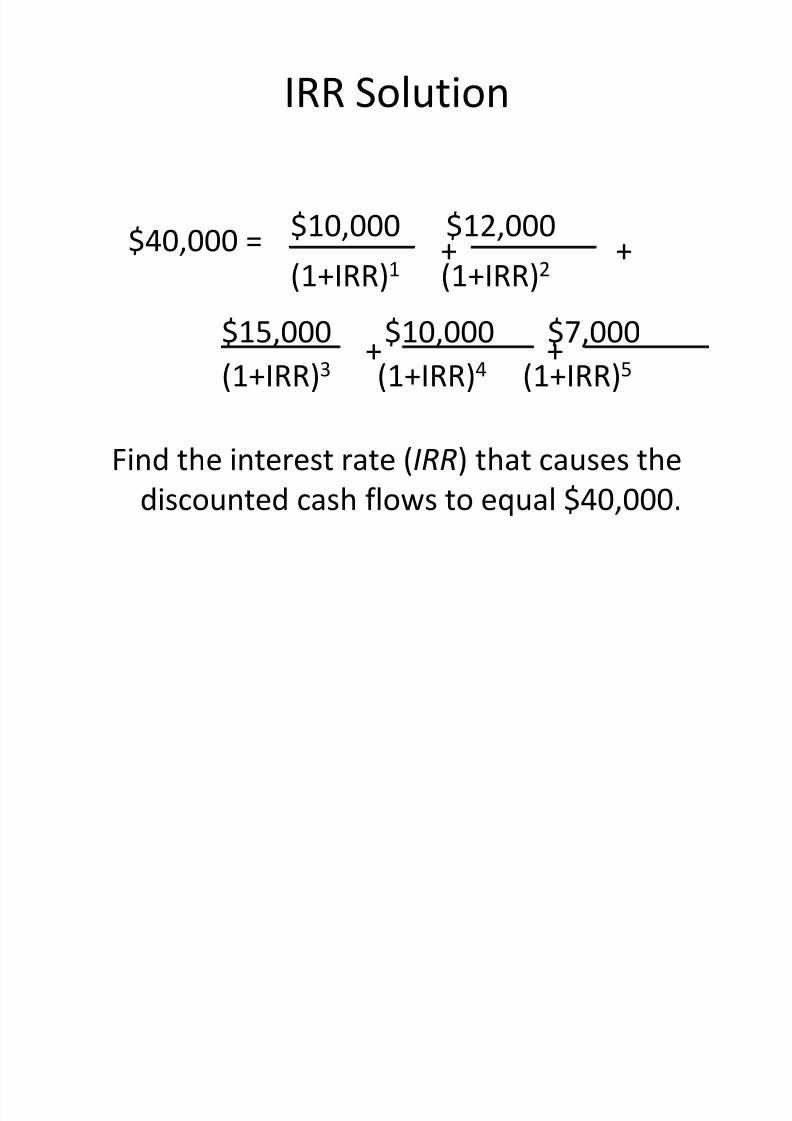

$15,000 $10,000 $7,000

$10,000 $12,000

(1+IRR)1

(1+IRR)2

Find the interest rate (IRR) that causes the

discounted cash flows to equal $40,000.

IRR Solution

+ +

++$40,000 =

(1+IRR)3 (1+IRR)4 (1+IRR)5

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 30/47

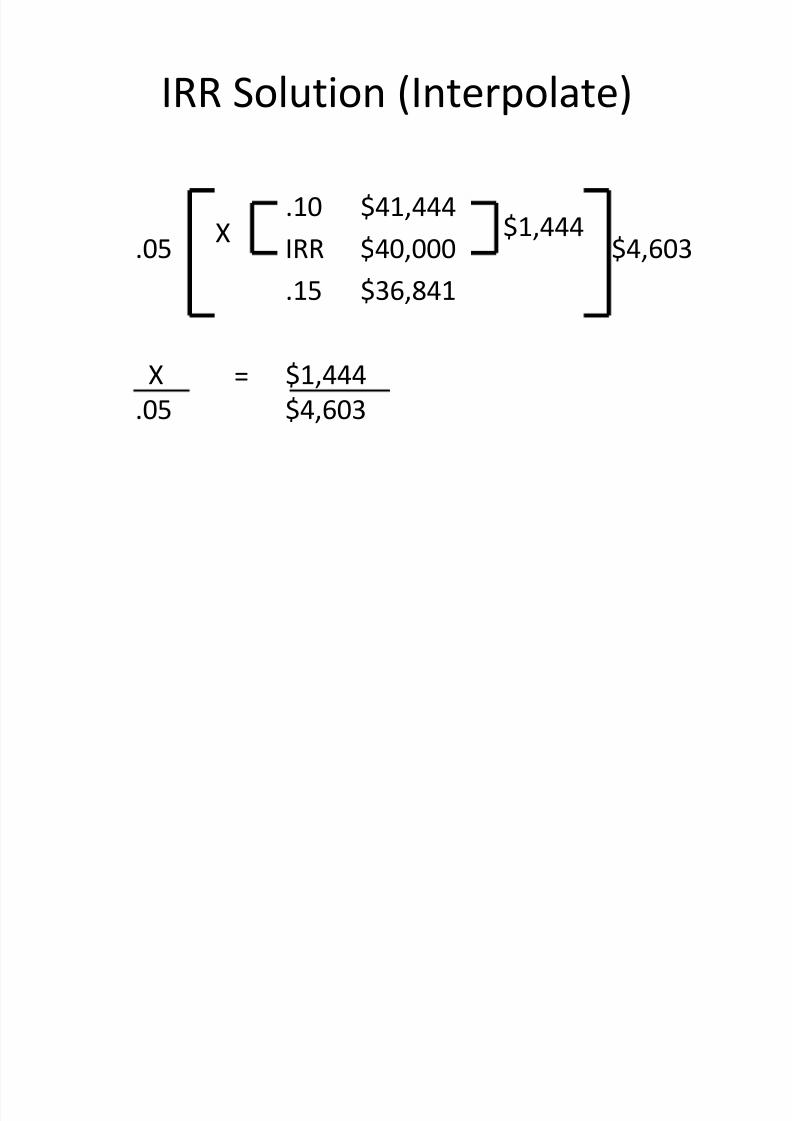

.10 $41,444

.05 IRR $40,000 $4,603

.15 $36,841

X $1,444

.05 $4,603

IRR Solution (Interpolate)

$1,444X

=

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 31/47

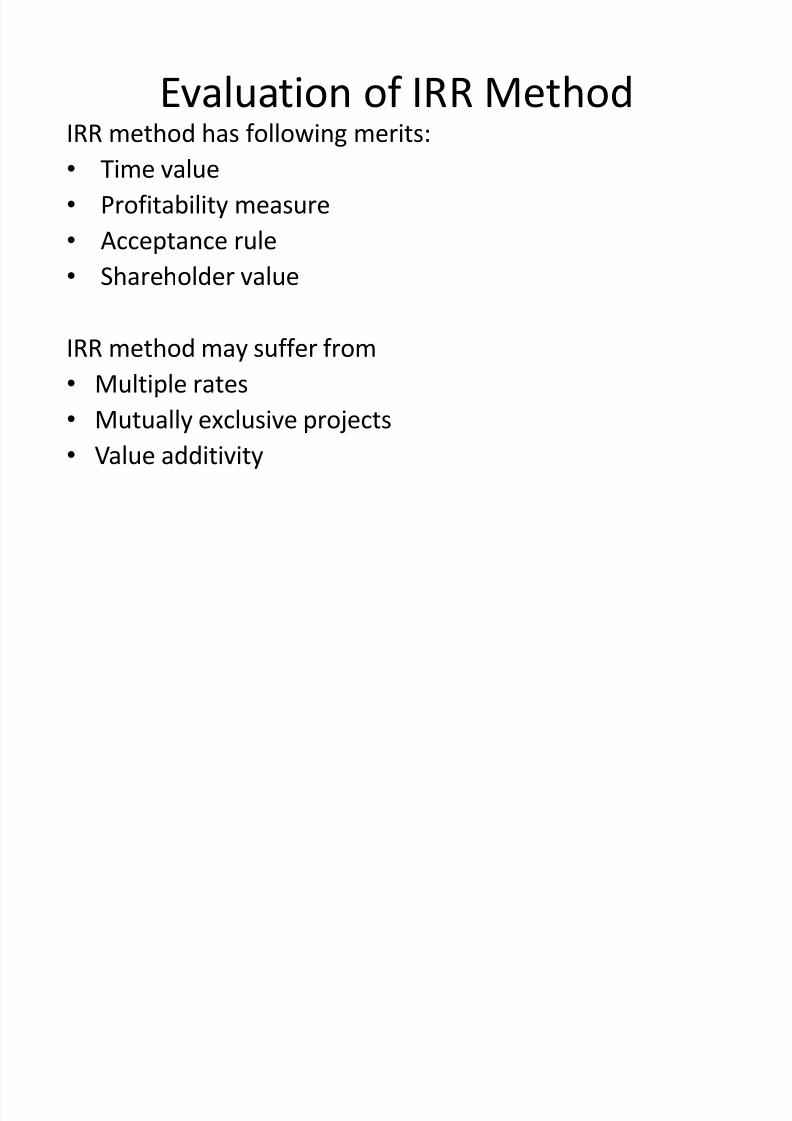

IRR meth

odh

as following merits:� Time value

� Profitability measure

� Acceptance rule

� Shareholder value

IRR method may suffer from

� Multiple rates

� Mutually exclusive projects� Value additivity

Evaluation of IRR Method

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 32/47

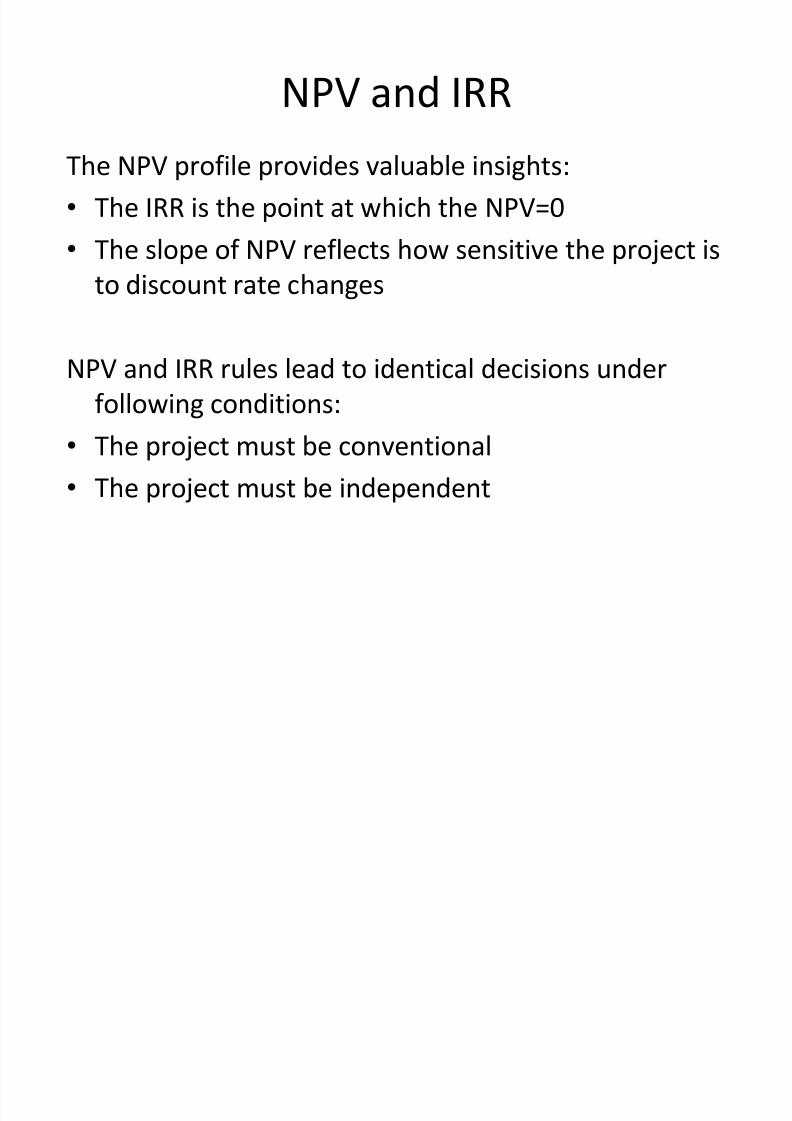

The NPV profile provides valuable insights:

� The IRR is the point at which the NPV=0

� The slope of NPV reflects how sensitive the project is

to discount rate changes

NPV and IRR rules lead to identical decisions under

following conditions:

� The project must be conventional

� The project must be independent

NPV and IRR

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 33/47

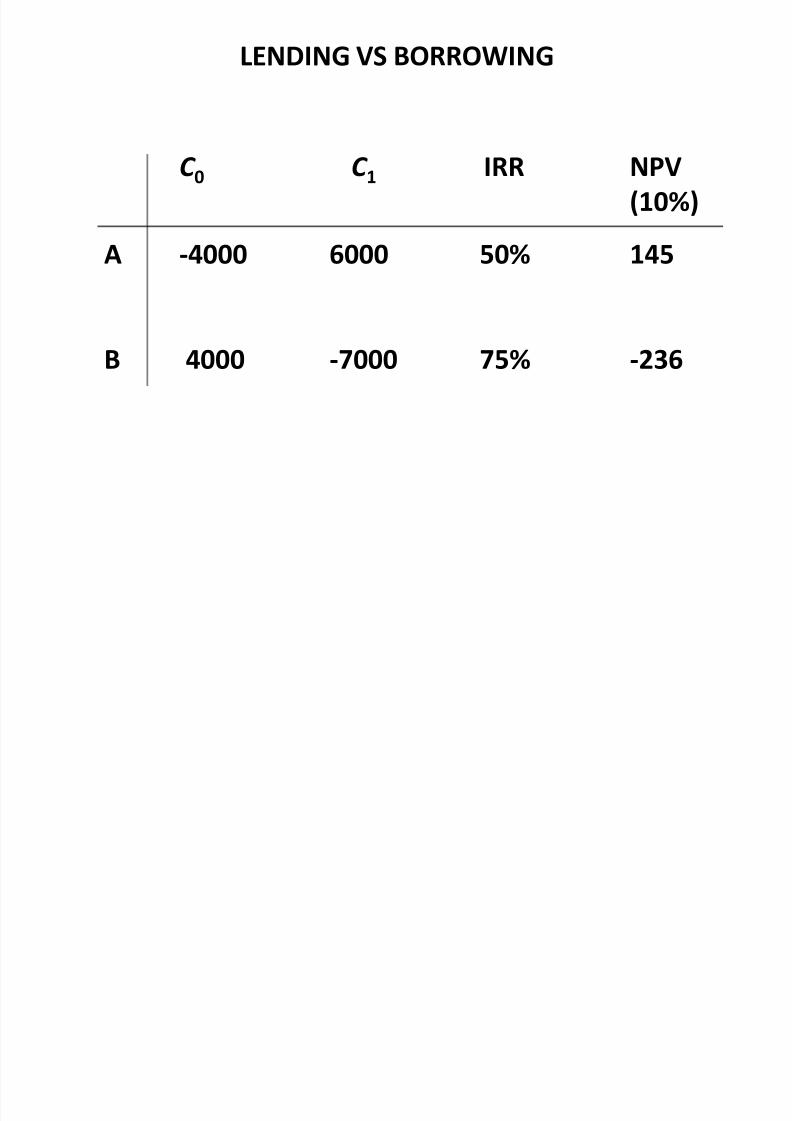

� Pitfall 1 - Lending or Borrowing?

IRR cannot distinguish between lending and borrowing

so a high IRR is not always desirable

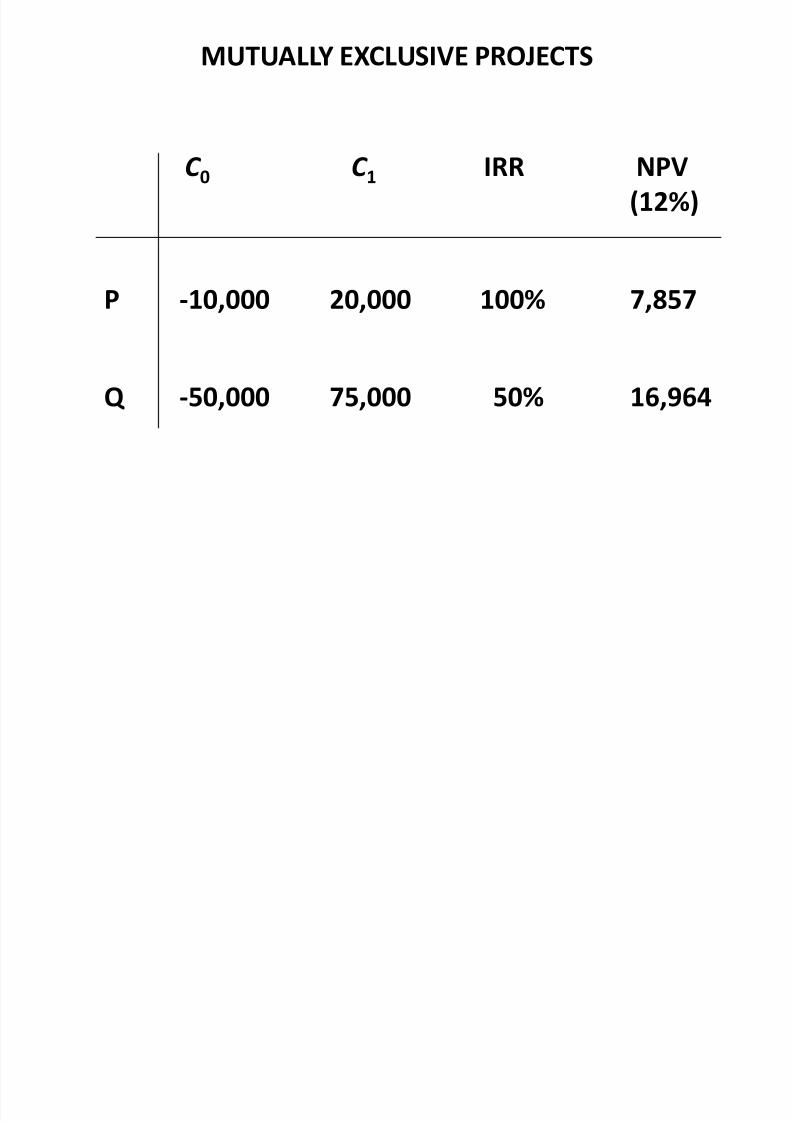

� Pitfall 2 - Mutually Exclusive Projects

IRR sometimes ignores the magnitude of the project.

IRR - Pitfalls

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 34/47

LENDING VS BORROWING

C 0 C 1 IRR NPV

(10%)

A -4000 6000 50% 145

B 4000 -7000 75% -236

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 35/47

MUTUALLY EXCLUSIVE PROJECTS

C 0 C 1 IRR NPV

(12%)

P -10,000 20,000 100% 7,857

Q -50,000 75,000 50% 16,964

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 36/47

� Pitfall 3 - Multiple Rates of Return

Simple solution is to use NPV to make decision

� Pitfall 4 Differences between the short term and

long term interest rates

IRR

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 37/47

MIRR overcomes the shortcoming of regular IRR

The procedure for calculating MIRR is as follows:

� Calculate the PVC associated with the project, using the cost of

capital as the discount rate

� Calculate the terminal value of the cash inflows expected formthe project

� Obtain MIRR by solving the following equation

PVC = TV

(1+MIRR)^n

Modified IRR

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 38/47

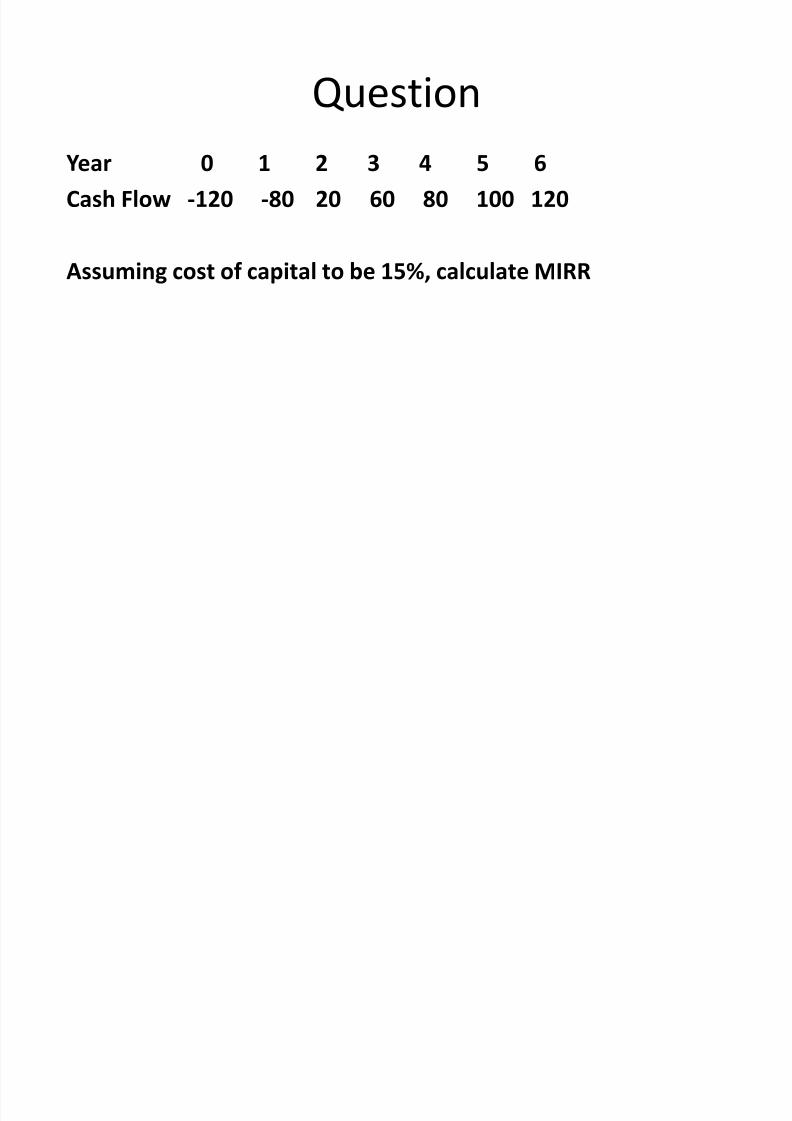

Year 0 1 2 3 4 5 6

Cash Flow -120 -80 20 60 80 100 120

Assuming cost of capital to be 15%, calculateM

IRR

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 39/47

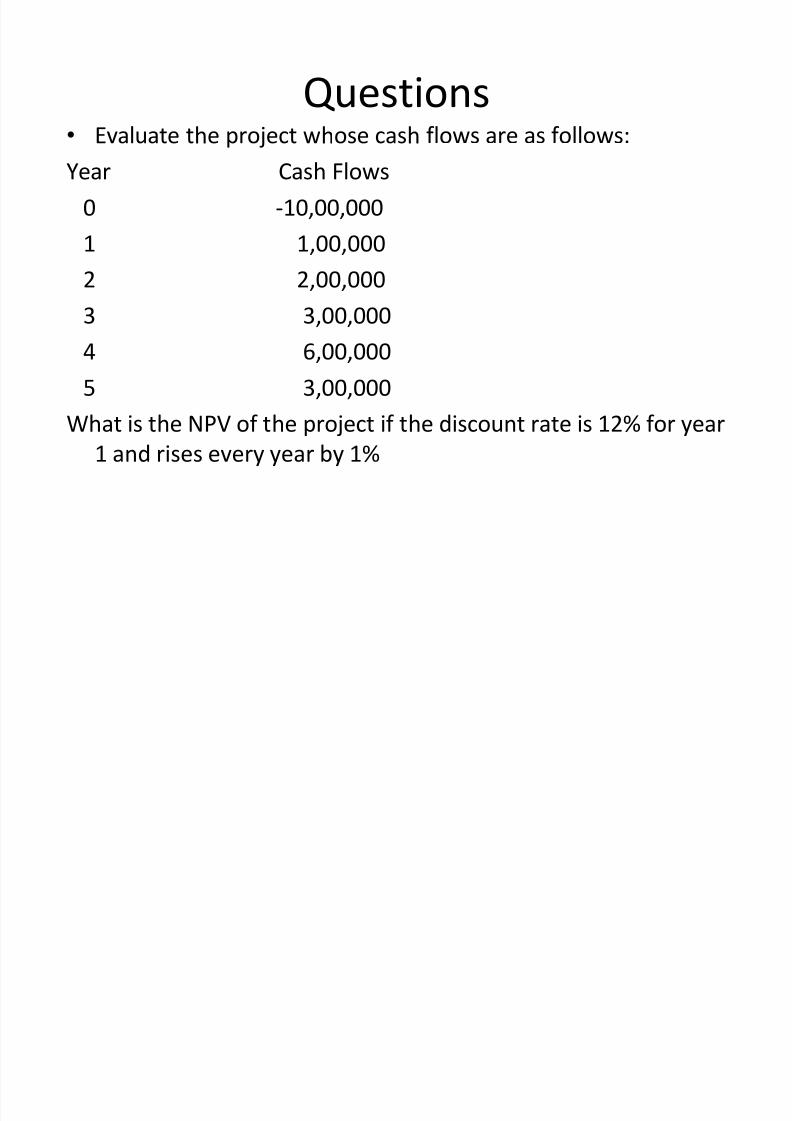

� Evaluate th

e project wh

ose cash

flows are as follows:Year Cash Flows

0 -10,00,000

1 1,00,000

2 2,00,0003 3,00,000

4 6,00,000

5 3,00,000

What is the NPV of the project if the discount rate is 12% for year1 and rises every year by 1%

Questions

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 40/47

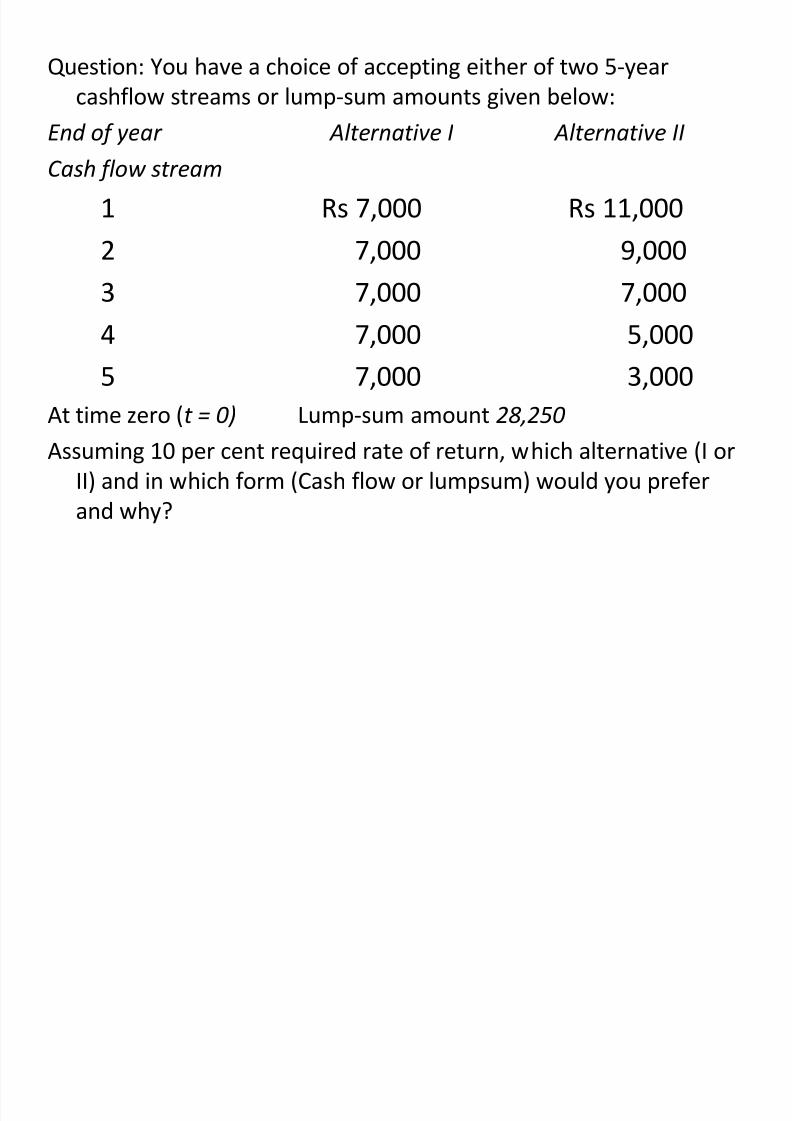

Question: You have a choice of accepting either of two 5-year

cashflow streams or lump-sum amounts given below:

E

nd o f year Alternat iv e I

Alternat iv e II

C ash f low st r eam

1 Rs 7,000 Rs 11,000

2 7,000 9,000

3 7,000 7,000

4 7,000 5,000

5 7,000 3,000

At time zero (t = 0 ) Lump-sum amount 28,250Assuming 10 per cent required rate of return, which alternative (I or

II) and in which form (Cash flow or lumpsum) would you prefer

and why?

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 41/47

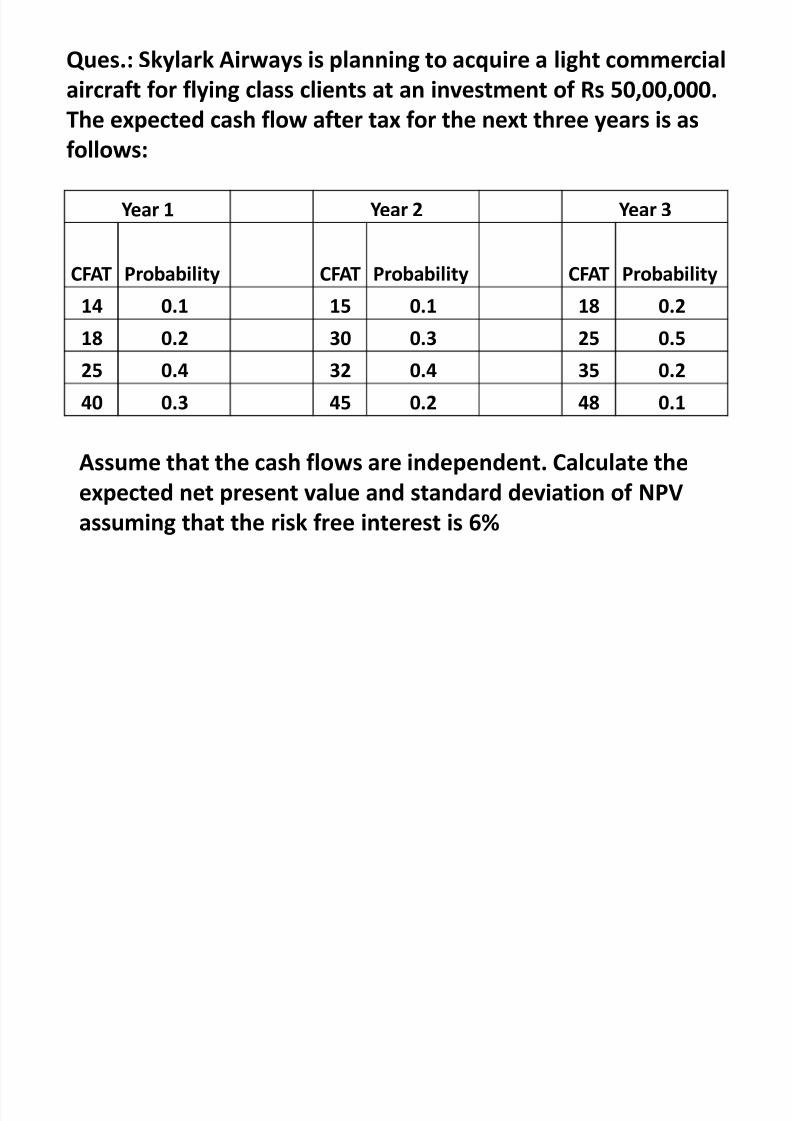

Ques.: Skylark Airways is planning to acquire a light commercial

aircraft for flying class clients at an investment of Rs 50,00,000.

The expected cash flow after tax for the next three years is as

follows:

Year 1 Year 2 Year 3

CFAT Probability CFAT Probability CFAT Probability14 0.1 15 0.1 18 0.2

18 0.2 30 0.3 25 0.5

25 0.4 32 0.4 35 0.2

40 0.3 45 0.2 48 0.1

Assume that the cash flows are independent. Calculate the

expected net present value and standard deviation of NPV

assuming that the risk free interest is 6%

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 42/47

� If an equipment costs Rs. 5,00,000 and lasts 8 years,what should be the minimum annual cash inflow

before it is worthwhile to purchase the equipment?

Assume that the cost of capital is 10%.

� X has taken a 20-month car loan of Rs 6,00,000. The

rate of interest is 12 per cent per annum. What will be

the amount of monthly loan amortization?

Question

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 43/47

� A conventional investment has cash flows the pattern of an

initial cash outlay followed by cash inflows. Conventional

projects have only one change in the sign of cash flows; for

example, the initial outflow followed by inflows, i.e., + + +.

� A non-conventional investment, on the other hand, has cash

outflows mingled with cash inflows throughout the life of the

project. Non-conventional investments have more than one

change in the signs of cash flows; for example, + + + ++ +.

Conventional & Non-Conventional

Cash Flows

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 44/47

� inflation is the increase in the general level of prices for all

goods and services in an economy

� nominal values are the actual amount of money making up

cash flows

� real values reflect the purchasing power of the cash flows

� real values are found by adjusting the nominal values for the

rate of inflation

� (1 + Nominal Rate) = (1 + Real Rate) * (1 + Inflation Rate)

Inflation and Capital Budgeting

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 45/47

± PROJECTED CASH FLOWS

± DISCOUNT RATE

� if projected cash flows are in real terms, thediscount rate used should be a real rate.

� if projected cash flows are in nominal terms,the discount rate used should be a nominalrate.

INFLATION EFFECTS TWO ASPECTS OF CAPITAL

BUDGETING

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 46/47

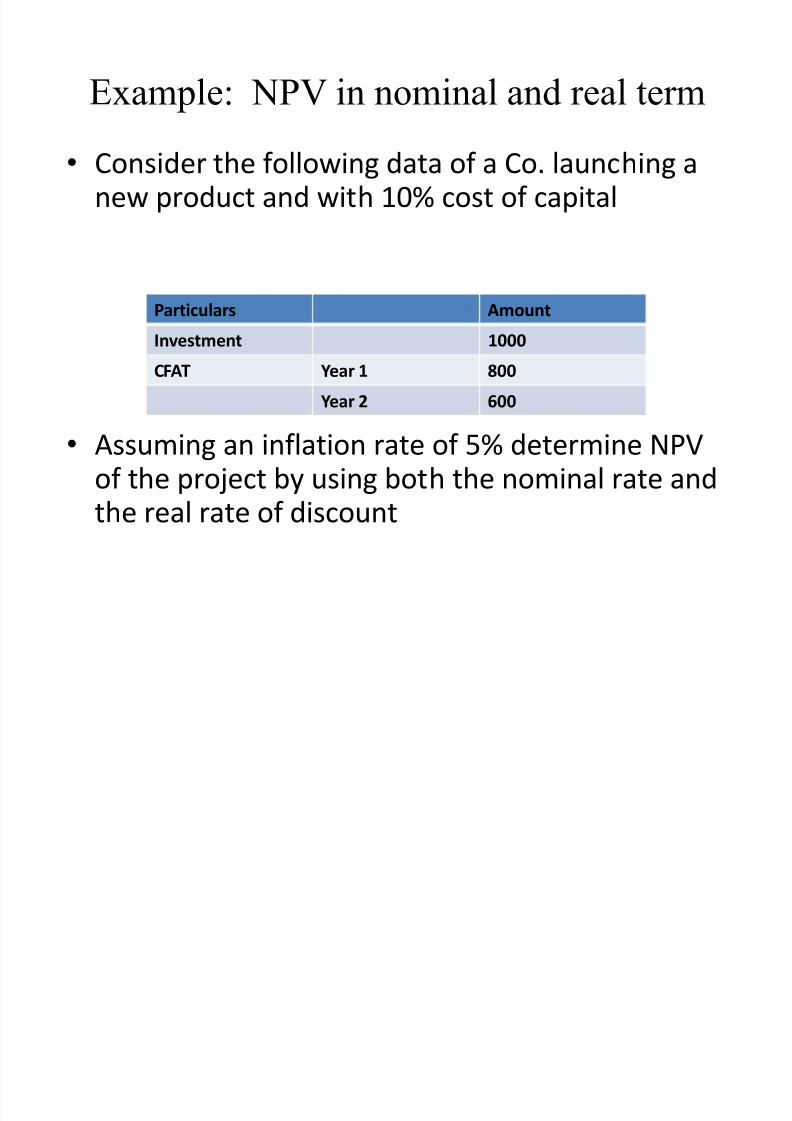

� Consider the following data of a Co. launching anew product and with 10% cost of capital

� Assuming an inflation rate of 5% determine NPVof the project by using both the nominal rate andthe real rate of discount

Example: NPV in nominal and real term

Particulars Amount

Investment 1000

CFAT Year 1 800

Year 2 600

8/7/2019 Capital Budegeting Finall

http://slidepdf.com/reader/full/capital-budegeting-finall 47/47

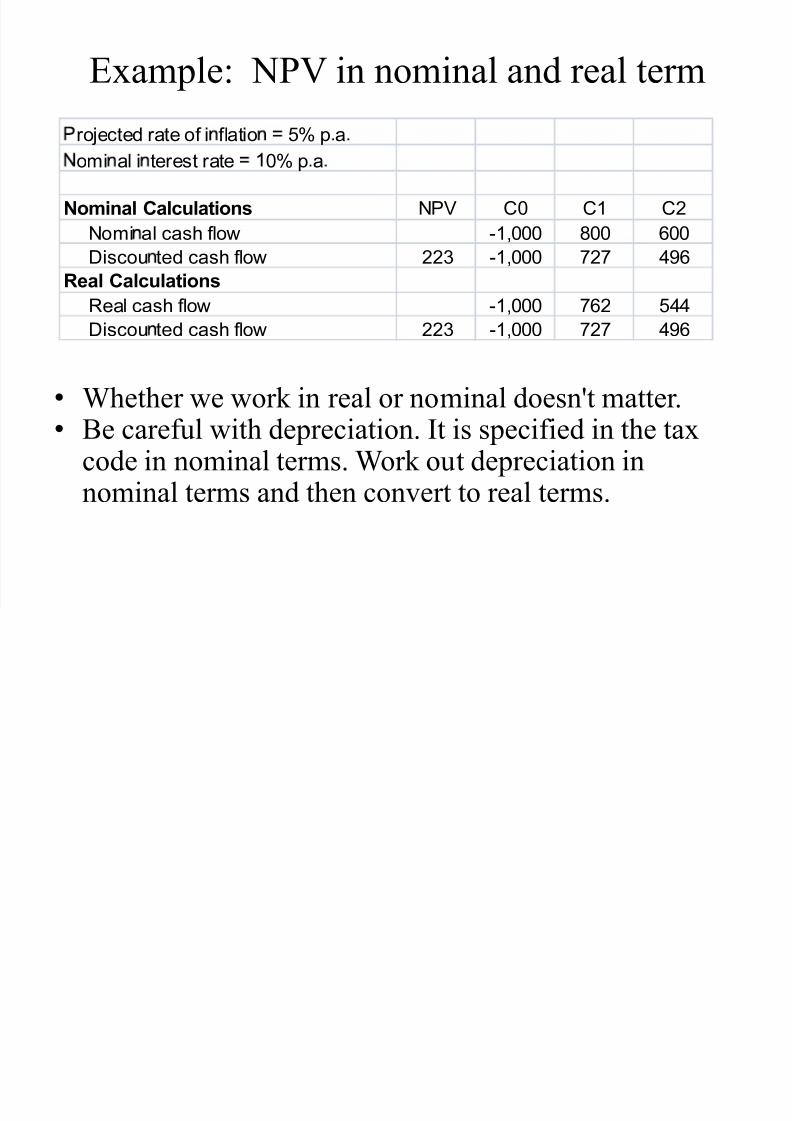

Example: NPV in nominal and real term

� Whether we work in real or nominal doesn't matter.

� Be careful with depreciation. It is specified in the taxcode in nominal terms. Work out depreciation innominal terms and then convert to real terms.

rojected rate of i flatio 5% p a

omi al i terest rate 0% p a

Nominal Calculations NPV C0 C1 C2

Nomi al cash flow -1,000 800 600

Discou ted cash flow 223 -1,000 727 496

Real CalculationsReal cash flow -1,000 762 544

Discou ted cash flow 223 -1,000 727 496