Caldwell Parish School Board - LLA Default Homepage

52

RECEIVED EG'S! ATivf AUDITOR 06 JAN-3 AM 10:56 CALDWELL PARISH SCHOOL BOARD Columbia, Louisiana SCHOOL ACTIVITY FUND AGREED-UPON PROCEDURE REPORT FOR THE YEAR ENDED JUNE 30,2005 Under provisions of state law, this report is i public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court. Release Date 2 - ( ' 2<=> &£>

Transcript of Caldwell Parish School Board - LLA Default Homepage

RECEIVEDEG'S! ATivf AUDITOR

06 JAN-3 AM 10:56

CALDWELL PARISH SCHOOL BOARDColumbia, Louisiana

SCHOOL ACTIVITY FUNDAGREED-UPON PROCEDURE REPORTFOR THE YEAR ENDED JUNE 30,2005

Under provisions of state law, this report is i publicdocument. Acopy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date 2 - ( ' 2<=> &£>

CALDWELL PARISH SCHOOL BOARD

Columbia, Louisiana

SCHOOL ACTIVITY FUND

AGREED-UPON PROCEDURE REPORT

FOR THE YEAR ENDED JUNE 30,2005

TABLE OF CONTENTS

SCHEDULE PAGE

INDEPENDENT ACCOUNTANTS' REPORT 1

CALDWELL HIGH SCHOOL 2

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS 1 3-5

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS 2 6-8

CALDWELL JUNIOR HIGH SCHOOL 9

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS 3 10-12

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS 4 13-15

CALDWELL PRE-SCHOOL 16

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS 5 17-19

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS 6 20-21

COLUMBIA ELEMENTARY 22

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS 7 23-25

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS 8 26-28

GRAYSON ELEMENTARY 29

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS 9 30-32

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS 10 33-35

CALDWELL PARISH SCHOOL BOARDColumbia, Louisiana

SCHOOL ACTIVITY FUNDAGREED-UPON PROCEDURE REPORTFOR THE YEAR ENDED JUNE 30, 2005

TABLE OF CONTENTS (Continued)

SCHEDULE PAGE

KELLY ELEMENTARY

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS

UNION CENTRAL ELEMENTARY

DESCRIPTION OF PROCEDURES FOR SELECTED RECORDS ANDTRANSACTIONS

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONS

36

11

12

13

14

37-39

40-42

43

44-46

47-49

BONNIE T. ROBINETTE, CPA99A Lakeshore Drive

Monroe, LA 71203(318)342-8000

Fax:(318)342-8001

INDEPENDENT ACCOUNTANTS' REPORT

TO THE BOARD OF DIRECTORSCALDWELL PARISH SCHOOL BOARDColumbia, Louisiana

I have performed the procedures enumerated below, which were agreed to by the Caldwell Parish School Board and theLegislative Auditor of the State of Louisiana solely to assist you in evaluating the accounting records of the School Activity Fundof Caldwell Parish School as of and for the year ended June 30,2005. This engagement to apply agreed-upon procedures wasperformed in accordance with standards established by the American Institute of Certified Public Accountants. The sufficiencyof the procedures is solely the responsibility of the specified users of this report. Consequently, I make no representationregarding the sufficiency of the procedures described below either for the purpose for which this report has been requested orfor any other purpose.

The procedures I performed and the accounts to which they pertained are set forth in the accompanying Description ofProcedures for Selected Records and Transactions, and my findings relative thereto are set forth in the related accompanyingSummary of Findings, Observations and Recommendations, both of which are an integral part of this report.

I was not engaged to, and did not, perform an audit, the objective of which would be the expression of an opinion onthe School Activity Fund. Accordingly, I do not express such an opinion. Had I performed additional procedures, other mattersmight have come to my attention that would have been reported to you.

This report is intended solely for the use of the specified users listed above and should not be used by those who havenot agreed to the procedures and taken responsibility for the sufficiency of the procedures for their purposes.

Monroe, LouisianaOctober 10,2005

CALDWELL HIGH SCHOOL

CALDWELL PARISH SCHOOL BOARD SCHEDULE 1Columbia, Louisiana

CALDWELL HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30,2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for (he one bank account.

Caldwell Bank & Trust $51,418.09

d. I determined the propriety of deposits in transit, if any.

There were no deposits in transit.

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. I supported the outstanding checks by comparing to the checks clearing in subsequent month bank statement.

2. I obtained a list of certificates of deposit for the year and:

a. There were no certificates of deposit at June 30, 2005.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955, 39:327.

One bank account was in existence at June 30, a public NOW account at Caldwell Bank & Trust.

4. There were no outstanding checks over 90 days old.

CALDWELL PARISH SCHOOL BOARD SCHEDULE 1Columbia, Louisiana

CALDWELL HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that the receiptsbatch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacher log/receipt,concessions inventory or admission ticket reconciliation, etc.

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was tested forthese attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable.

CALDWELL PARISH SCHOOL BOARD SCHEDULE 1Columbia, Louisiana

CALDWELL HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

C. EXPENDITURES (Continued)

9. Bids obtained if applicable.

10. Expenditure is allowable under allocable laws.

The results of those tests are discussed in the accompanying Summary of Findings, Observations and Recommendations.

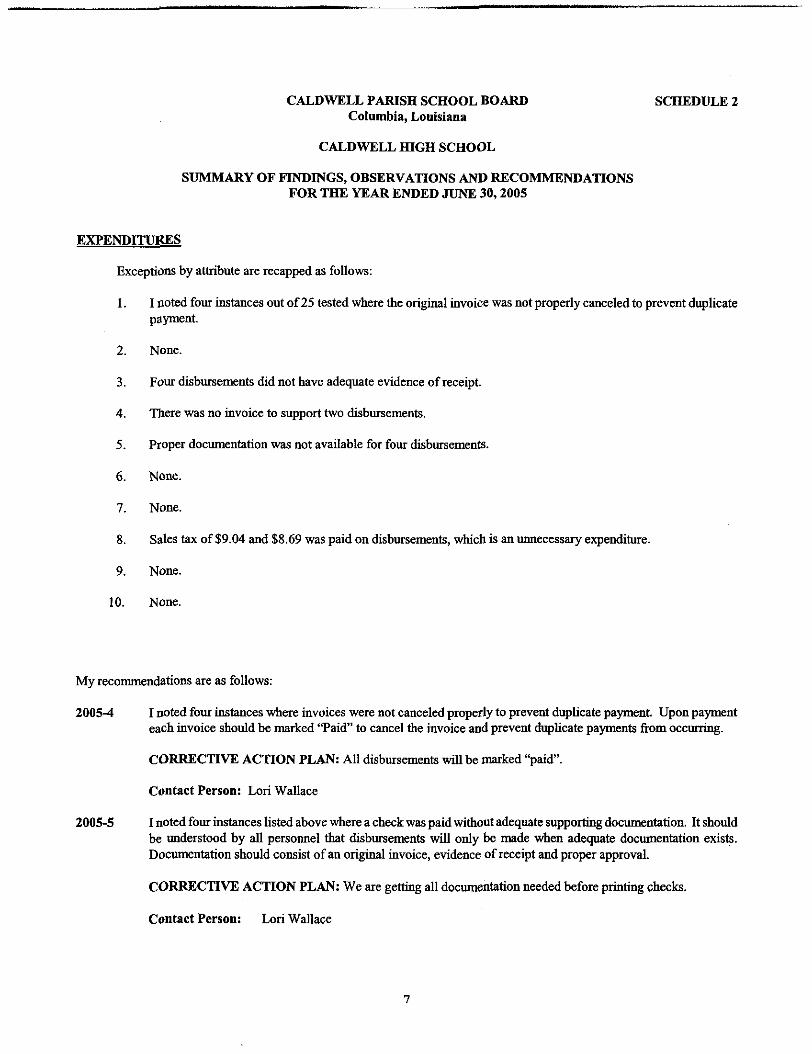

CALDWELL PARISH SCHOOL BOARD SCHEDULE 2Columbia, Louisiana

CALDWELL HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, Description of Procedures for Selected Records and Transactions of CALDWELLHigh School.

CASH

2005-1 There was a difference of $59 between the bank reconciliation and the general ledger. School personnel shoulddetermine the cause of the difference and make the proper adjustment to correct the accounting records.

CORRECTIVE ACTION PLAN: We will make the proper adjustment to the account and correct the accountingrecords.

Contact Person: Lori Wallace

REVENUES

A. None.

B. I noted 6 of the 15 receipts were not deposited in a timely manner with time lags of 6 days to 53 days aftercollection.

C. None.

D. None.

I recommend the school implement controls over receipts as follows:

2005-2 All deposits should be made on a timely basis. Teachers should be instructed to turn all money in to the officedaily. All money should be deposited by the office daily.

CORRECTIVE ACTION PLAN: We will make sure deposits are done daily.

Contact Person: Lori Wallace

2005-3 Pre-numbeied tickets should be used for all significant admission events such as football games. A reconciliationshould be made of tickets issued, sold and the proceeds collected. Games with small attendance, such as baseball,should have dual control over receipts, as two persons should sign off on the gate receipts.

CORRECTIVE ACTION PLAN: We are currently following this procedure.

Contact Person: Lori Wallace

CALDWELL PARISH SCHOOL BOARD SCHEDULE 2Columbia, Louisiana

CALDWELL HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS ANP RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. I noted four instances out of 25 tested where the original invoice was not properly canceled to prevent duplicatepayment.

2. None.

3. Four disbursements did not have adequate evidence of receipt.

4. There was no invoice to support two disbursements.

5. Proper documentation was not available for four disbursements.

6. None.

7. None.

8. Sales tax of $9.04 and $8.69 was paid on disbursements, which is an unnecessary expenditure.

9. None.

10. None.

My recommendations are as follows:

2005-4 I noted four instances where invoices were not canceled properly to prevent duplicate payment. Upon paymenteach invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: All disbursements will be marked "paid".

Contact Person: Lori Wallace

2005-5 I noted four instances listed above where a check was paid without adequate supporting documentation. It shouldbe understood by all personnel that disbursements will only be made when adequate documentation exists.Documentation should consist of an original invoice, evidence of receipt and proper approval.

CORRECTIVE ACTION PLAN: We are getting all documentation needed before printing checks.

Contact Person: Lori Wallace

CALDWELL PARISH SCHOOL BOARD SCHEDULE 2Columbia, Louisiana

CALDWELL HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES - continued

2005-6 Two checks were noted which included payment of sales tax. Since the school is tax exempt, this results in anunnecessary expenditure. Steps should be taken to avoid paying sales tax.

CORRECTIVE ACTION PLAN: Invoices will be checked for sales tax before paying.

Contact Person: Lori Wallace

CALDWELL JUNIOR HIGH SCHOOL

CALDWELL PARISH SCHOOL BOARD SCHEDULE 3Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30, 2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Citizen's Progressive Bank $53,766.17

d. I determined the propriety of deposits in transit, if any.

There was a deposit from October 13, 2004 that had not cleared the bank..

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. I supported the outstanding checks by comparing to the checks clearing in the subsequent month bankstatement.

2. There were no certificates of deposit at June 30,2005.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955, 39:327

4. The following outstanding checks were over 90 days old at year-end:

6221 Tioga High School 50.00 March 4,2004

10

CALDWELL PARISH SCHOOL BOARD SCHEDULE 3Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that the receiptsbatch total matched the deposit total.

d. I traced me individual receipts within the deposit to their related account ledger card, teacher log/receipt,concessions inventory or admission ticket reconciliation, etc.

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was tested forthese attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.i

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

11

CALDWELL PARISH SCHOOL BOARD SCHEDULE 3Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

C. EXPENDITURES (Continued)

8. Charge appears to be necessary and reasonable.

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in the accompanying Summary of Findings, Observations and Recommendations.

12

CALDWELL PARISH SCHOOL BOARD SCHEDULE 4Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of CALDWELL JUNIORHIGH SCHOOL.

CASH AND CASH EQUIVALENTS

2005-1 There was one outstanding checks over one year old. This check should be investigated. If the check was lostor incorrectly issued, it should be voided. Unclaimed checks should be remitted to the state.

CORRECTIVE ACTION PLAN: The check was determined to be lost, so it has now been voided to correctthe accounting records.

Contact Person: Dianne Childress, Elaine Dauzat

2005-2 The bank reconciliation included a deposit listed as in transit since October 13, 2004. This deposit should beinvestigated to determine why the bank did not give credit or if the deposit was actually made. This deposit shouldhave been resolved in the prior year. Timely resolution of reconciling items is essential in preventing losses tothe school.

CORRECTIVE ACTION PLAN: The deposit was made on October 14,2004. An adjustment was made inthe reconciliation. '

Contact Person: Dianne Childress, Elaine Dauzat

2005-3 During my tests I noted the bank reconciliation did not agree with the ledger records by $38.00. This differenceshould be resolved and an adjustment made to correct the accounting records.

CORRECTIVE ACTION PLAN: The $38.00 was voided and an adjustment was made to the record.

Contact Person: Dianne Childress, Elaine Dauzat

REVENUES

I noted the following exceptions in my tests of 15 receipts selected at random:

A. None

B. None. ;

C. None.

D. There was no evidence to indicate accounting control over 7 of the 15 receipts tested.

13

CALDWELL PARISH SCHOOL BOARD SCHEDULE 4Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

REVENUES. Continued

I recommend the school implement controls over receipts as follows:

2005-4 As of the date of my test procedures, there was no documentation to indicate dual control over concessions. Irecommend the school implement a policy where two individuals count the money and sign to indicate the amountof money collected.

CORRECTIVE ACTION PLAN: Vending machines have been installed for the 2005-06 school year.

Contact Person: Dianne Childress, Elaine Dauzat

2005-5 All teachers or club sponsors who handle money should maintain a log to record all collections of monies fromstudents. The amounts collected should be recorded on the log and given to the principal or secretary for receiptwhen the money is turned in. The teacher's log book should be turned in to the school office at year-end toprovide an audit trail of the receipts.

CORRECTIVE ACTION PLAN: The office will keep a bound receipt book with a copy of the teacher's log.The receipt number will be on the log.

Contact Person: Dianne Childress, Elaine Dauzat

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Seven of the 25 disbursements tested were not properly canceled to prevent duplicate payment.

2. None.

3. Four disbursements did not have adequate evidence of receipt.

4. None.

5. Proper documentation was not available for four of the disbursements tested.

6. Two of the disbursements selected for testing involved the payment of past-due invoices.

7. None.

8. Two invoices included late charges, which is an unnecessary expense.

9. None.

10. None.

14

CALDWELL PARISH SCHOOL BOARD SCHEDULE 4Columbia, Louisiana

CALDWELL JUNIOR HIGH SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES. Continued

I recommend the following changes:

2005-6 I noted two invoices which were paid late. Care should be taken to pay invoices on a timely basis so thatunnecessary late charges are not incurred.

CORRECTIVE ACTION PLAN: Invoices will be paid on time.

Contact Person: Dianne Childress, Elaine Dauzat

2005-7 I noted four instances listed above where a check was paid without adequate supporting documentation. It shouldbe understood by all personnel that disbursements will only be made when adequate documentation exists.Documentation should consist of an original invoice, evidence of receipt and proper approval.

CORRECTIVE ACTION PLAN: Invoice and receipt will be attached to the check to receive approval.

Contact Person: Dianne Childress, Elaine Dauzat

2005-8 I noted several instances where invoices were not canceled properly to prevent duplicate payment. Upon paymenteach invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: CPJH has now purchased a "paid"stamp with the date on it.

Contact Person: Dianne Childress, Elaine Dauzat

15

CALDWELL PRE-SCHOOL

16

CALDWEIX PARISH SCHOOL BOARD SCHEDULE 5Columbia, Louisiana

CALDWELL PRE-SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30, 2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Homeland Federal Savings Bank $6,913.50

d. I determined the propriety of deposits in transit, if any.

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. I supported the outstanding checks by comparing to the checks clearing in subsequent month bank statement.

2. I obtained a list of certificates of deposit as of June 30, 2005:

a. There were no certificates of deposit at June 30,2005.

b. I tested the reasonableness of interest income.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955, 39:327.

17

CALDWELL PARISH SCHOOL BOARD SCHEDULE 5Columbia, Louisiana

CALDWELL PRESCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS (Continued)

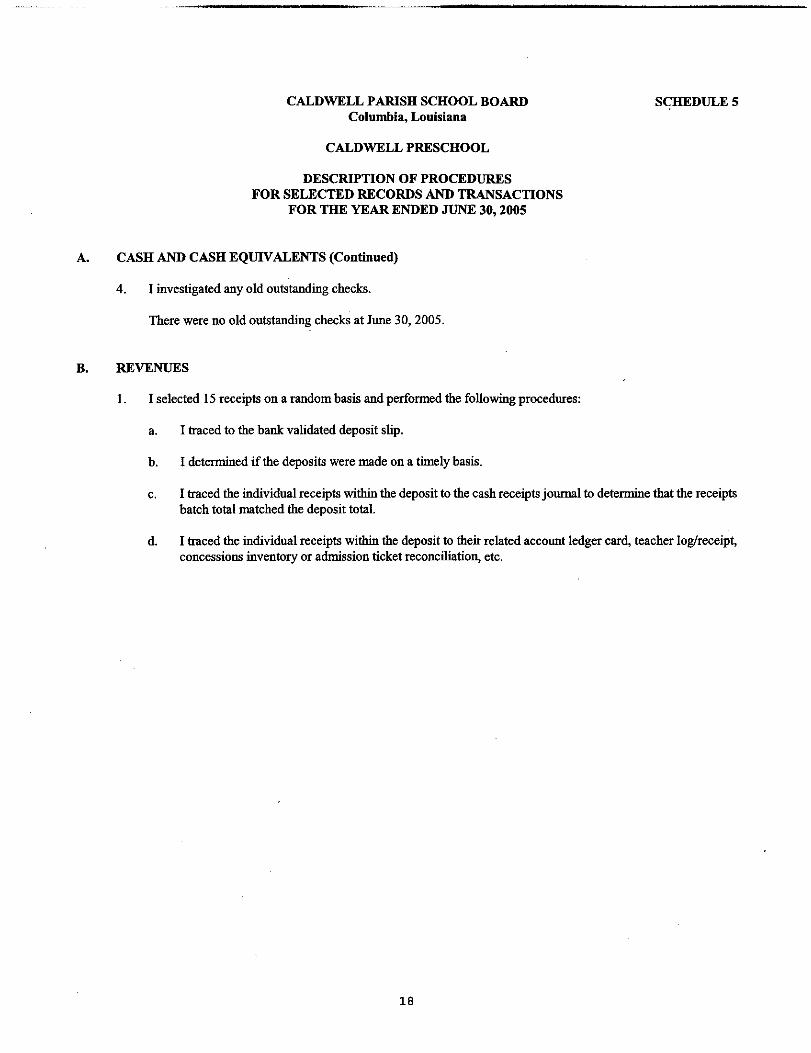

4. I investigated any old outstanding checks.

There were no old outstanding checks at June 30, 2005.

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that the receiptsbatch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacher log/receipt,concessions inventory or admission ticket reconciliation, etc.

18

CALDWELL PARISH SCHOOL BOARD SCHEDULE 5Columbia, Louisiana

CALDWELL PRESCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30, 2005

3. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was tested forthese attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable.

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in Schedule 6, Summary of Findings, Observations and Recommendations.

19

CALDWELL PARISH SCHOOL BOARD SCHEDULE 6Columbia, Louisiana

CALDWELL PRESCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of CALDWELLPRESCHOOL.

REVENUES

I noted the following exceptions in my test of 15 receipts selected at random.

A. None.

B. None.

C. None.

D. None.

20

CALDWELL PARISH SCHOOL BOARD SCHEDULE 6Columbia, Louisiana

CALDWELL PRESCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Eight of the 25 disbursements tested were not properly canceled to prevent duplicate payment.

2. None.

3. Three disbursements did not have adequate evidence of receipt.

4. Two invoices did not match the amount of the payment.

5. Proper documentation was not available for four disbursements.

6. One disbursement was made for a past-due invoice.

7. None.

8. None.

9. None.

10. None.

My recommendations are as follows:

2005-1 I noted four instances listed above where a check was paid without adequate supporting documentation. It shouldbe understood by all personnel that disbursements will only be made when adequate documentation exists.Documentation should consist of an original invoice, evidence of receipt and proper approval.

CORRECTIVE ACTION PLAN: All disbursements will be more carefully made and paid from originalinvoices. All persons involved in ordering/purchasing supplies have been made aware of these procedures.

Contact Person: Monica Coates

2005-2 I noted eight instances where invoices were not canceled properly to prevent duplicate payment. Upon paymenteach invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: In the future all invoices will be marked paid to prevent duplicate payment.

Contact Person: Monica Coates

2005-3 I noted one invoice which was paid late. Care should be taken to pay invoices on a timely basis so thatunnecessary late charges are not incurred.

CORRECTIVE ACTION PLAN: All invoices will be paid in a timely manner so that unnecessary late chargesdo not occur.Contact Person: Monica Coates

21

COLUMBIA ELEMENTARY SCHOOL

22

CALDWELL PARISH SCHOOL BOARD SCHEDULE 7Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30, 2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Citizen's Progressive Bank $22,920.75

d. I determined the propriety of deposits in transit, if any.

There were no deposits in transit.

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. I traced outstanding checks to the checks clearing in the subsequent month bank statement

2. I obtained a list of certificates of deposit for the year and:

a. There were no certificates of deposit at June 30,2005.

b. I tested the reasonableness of interest income.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955,39:327.

4. There were no old outstanding checks on the bank reconciliation.

23

CALDWELL PARISH SCHOOL BOARD SCHEDULE 7Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that the receiptsbatch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacher log/receipt,concessions inventory or admission ticket reconciliation, etc.

24

CALDWELL PARISH SCHOOL BOARD SCHEDULE 7Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

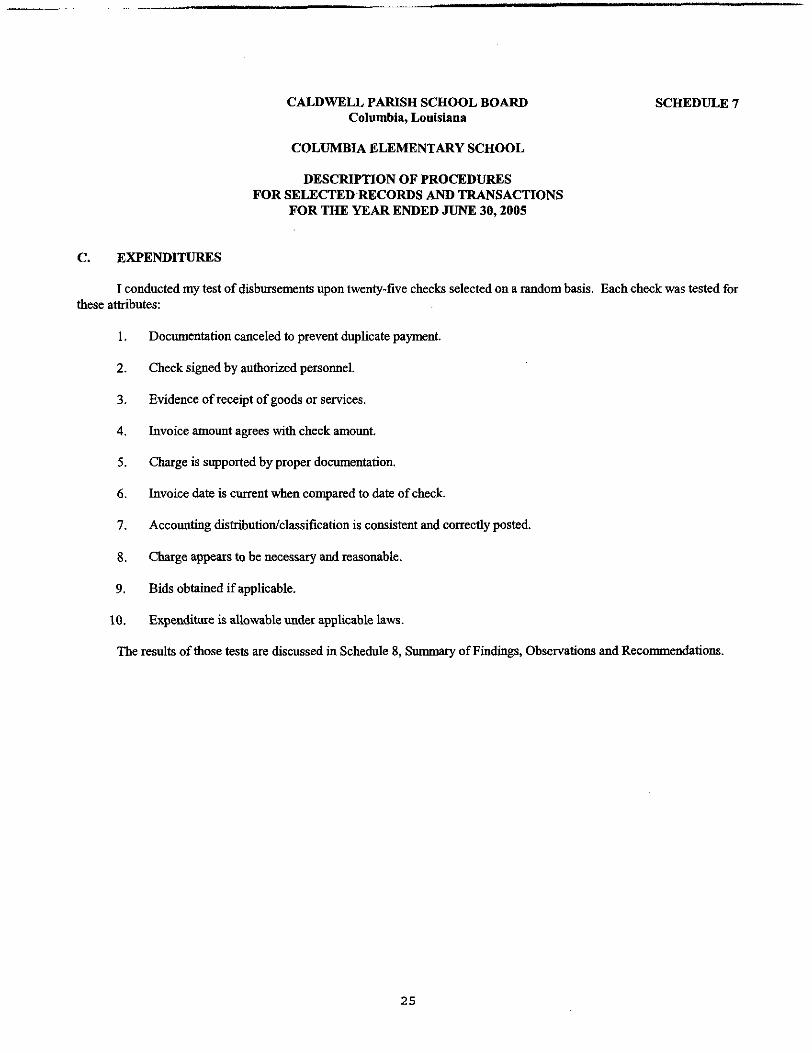

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was tested forthese attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services,

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable,

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in Schedule 8, Summary of Findings, Observations and Recommendations.

25

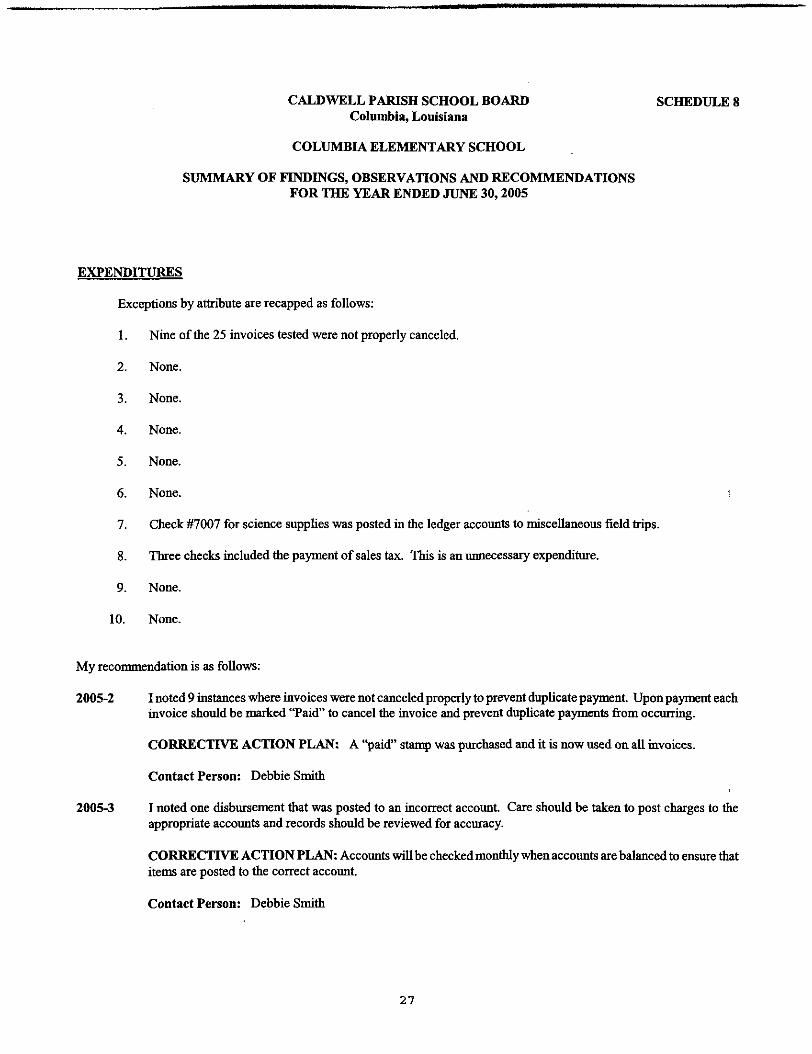

CALDWELL PARISH SCHOOL BOARD SCHEDULE 8Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30, 2005

This section of die report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of COLUMBIAELEMENTARY SCHOOL.

REVENUES

I noted the following exceptions in my test of 15 receipts selected at random.

A. None.

B. None.

C. None.

D. There was no evidence to indicate control over receipts for two of the 15 receipts tested.

I recommend the following: ,

2005-1 All teachers or club sponsors who handle money should maintain a log to record all collections of monies fromstudents. The amounts collected should be recorded on the log and given to the principal or secretary for receiptwhen the money is turned in. The teacher's log book should be turned in to the school office at year-end toprovide an audit trail of the receipts.

CORRECTIVE ACTION PLAN: Procedures for maintaining money log records and receipts are reviewed withteachers and club sponsors. The secretary keeps a copy of money logs and issues receipts.

Contact Person: Debbie Smith

26

CALDWELL PARISH SCHOOL BOARD SCHEDULE 8Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Nine of the 25 invoices tested were not properly canceled.

2. None.

3. None.

4. None.

5. None.

6. None. \

1, Check #7007 for science supplies was posted in the ledger accounts to miscellaneous field trips.

8. Three checks included the payment of sales tax. This is an unnecessary expenditure.

9. None.

10. None.

My recommendation is as follows:

2005-2 I noted 9 instances where invoices were not canceled properly to prevent duplicate payment. Upon payment eachinvoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: A "paid" stamp was purchased and it is now used on all invoices.

Contact Person: Debbie Smith

2005-3 I noted one disbursement that was posted to an incorrect account. Care should be taken to post charges to theappropriate accounts and records should be reviewed for accuracy.

CORRECTIVE ACTION PLAN: Accounts will be checked monthly when accounts are balanced to ensure thatitems are posted to the correct account.

Contact Person: Debbie Smith

27

CALDWELL PARISH SCHOOL BOARD SCHEDULE 8Columbia, Louisiana

COLUMBIA ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES. CONTINUED

2005-4 Three checks were noted which included the payment of sales tax. Since the school is tax-exempt, this resultsin an unnecessary expenditure. Steps should be taken to avoid paying sales tax.

CORRECTIVE ACTION PLAN: Item amounts will be checked twice to ensure that sales tax is not paid.

Contact Person: Debbie Smith

28

GRAYSON ELEMENTARY SCHOOL

29

CALDWELL PARISH SCHOOL BOARD SCHEDULE 9Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30,2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Homeland Federal Savings Bank $20,509.88

N d. I determined the propriety of deposits in transit, if any.

There were no deposits in transit.

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. I supported the outstanding checks by comparing to the checks clearing in the subsequent month bankstatement.

2. I obtained a list of certificates of deposit for the year:

a. There were no certificates of deposit at June 30,2005.

b. I tested the reasonableness of interest income.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955, 39:327.

4. There were no outstanding checks over 90 days old.

30

CALDWELL PARISH SCHOOL BOARD SCHEDULE 9Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that thereceipts batch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacherlog/receipt, concessions inventory or admission ticket reconciliation, etc.

31

CALDWELL PARISH SCHOOL BOARD SCHEDULE 9Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30, 2005

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each, check was testedfor these attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable.

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in Schedule 10, Summary of Findings, Observations and Recommendations.

32

CALDWELL PARISH SCHOOL BOARD SCHEDULE 10Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of GRAYSONELEMENTARY SCHOOL.

REVENUES

I noted the following exceptions in my test of 15 receipts selected at random.

A. None.

B. None.

C. None.

D. There was no evidence to support control over receipts for 4 of the 15 receipts tested.

My recommendations are as follows:

2005-1 At the time of our test procedures, there is no documentation to indicate control over concession receipts. Irecommend the school implement a policy where two individuals count the concession money and sign toindicate the amount of money collected.

CORRECTIVE ACTION PLAN: New procedures implemented this school year require two concessionworkers to count concession receipts and sign a form mat lists the amount of money collected and the numberof items sold.

Contact Person: Cheryl Mullican

33

CALDWELL PARISH SCHOOL BOARD SCHEDULE 10Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30, 2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Ten of the 25 invoices tested were not properly canceled.

2. None.

3. None.

4. Check #1733 included a duplicate payment to Coca-Cola in the amount of $42.48.

5. Documentation was not adequate for the check discussed in item 4 above.

6. None.

7. Check #1817 for $88.00 was incorrectly posted to school maintenance. The charge was for helium to fillballoons.

8. One invoice included the payment of sales tax.

9. None.

10. None.

I recommend the following:

2005-2 I noted 10 instances where invoices were not canceled properly to prevent duplicate payment. Upon paymenteach invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: All invoices will be marked "paid" to cancel the invoice.

Contact Person: Cheryl Mullican

2005-3 I noted one disbursement that was posted to an incorrect account. Care should be taken to post charges to theappropriate accounts and records should be reviewed for accuracy.

CORRECTIVE ACTION PLAN: Care will be taken to post disbursements for the correct amount. Carewill be taken to post charges to the appropriate accounts. Records will be reviewed for accuracy.

Contact Person: Cheryl Mullican

34

CALDWELL PARISH SCHOOL BOARD SCHEDULE 10Columbia, Louisiana

GRAYSON ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES, continued

2005-4 I noted one instance listed above where a check was paid without adequate supporting documentation. Itshould be understood by all personnel that disbursements will only be made when adequate documentationexists. Documentation should consist of an original invoice, evidence of receipt and proper approval.

CORRECTIVE ACTION PLAN: Payment will only be made with proper documentation which shallinclude: original invoice, evidence of receipt and prior approval.

Contact Person: Cheryl Mullican

2005-5 One check was noted which included payment of sales tax. Since the school is tax exempt, mis results in anunnecessary expenditure. Steps should be taken to avoid paying sales tax.

CORRECTIVE ACTION PLAN: Sales tax will not be paid. Care will be taken to provide tax-exemptinformation at every available opportunity.

Contact Person; Cheryl Mullican

35

KELLY ELEMENTARY SCHOOL

36

CALDWELL PARISH SCHOOL BOARD SCHEDULE 11Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30, 2005

CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30,2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Citizen's Progressive Bank $10,387.47

d. I determined the propriety of deposits in transit, if any.

There were no deposits in transit at June 30, 2005.

e. I examined all interfimd transfers, if any.

There were no interfund transfers. •

f. There were no outstanding checks at June 30, 2005.

2. I obtained a list of certificates of deposit for the year and:

a. There were no certificates of deposit at June 30, 2005.

b. I tested the reasonableness of interest income.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955,39:327.

4. There were no old, outstanding checks at June 30,2005.

37

CALDWELL PARISH SCHOOL BOARD SCHEDULE 11Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30, 2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that thereceipts batch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacherlog/receipt, concessions inventory or admission ticket reconciliation, etc.

38

CALDWELL PARISH SCHOOL BOARD SCHEDULE 11Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was testedfor these attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable.

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in Schedule 12, Summary of Findings, Observations and Recommendations.

39

CALDWELL PARISH SCHOOL BOARD SCHEDULE 12Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of KELLYELEMENTARY SCHOOL.

REVENUES

I noted the following exceptions in my test of 15 receipts selected at random.

A. None.

B. None.

C. None.

D. There was no evidence to support control over receipts for 8 of the 15 receipts tested.

I recommend the school implement the following recommendations :

2005-1 At the time of our test procedures, there is no documentation to indicate control over concession receipts. Irecommend the school implement a policy where two individuals count the concession money and sign toindicate the amount of money collected.

CORRECTIVE ACTION PLAN: We are now using a daily canteen log sheet. The persons who collectand turn in the money sign the log sheet and the secretary signs upon receipt.

Contact Person: Melanie White

2005-2 All teachers or club sponsors who handle money should maintain a log to record all collections of moniesfrom students. The amounts collected should be recorded on the log and given to the principal or secretary forreceipt when the money is turned in. The teacher's log book should be turned in to the school office at year-end to provide an audit trail of the receipts.

CORRECTIVE ACTION PLAN: Any money collected by teachers is recorded on a log sheet which is thenturned in to the office and a receipt is given.

Contact Person: Melanie White

2005-3 The school is currently posting all concession activity to general accounts. A separate concession accountshould be set up in order to evaluate the profit or loss generated and to provide accountability.

CORRECTIVE ACTION PLAN: The concession account is now maintained on Quickbooks. We have a"canteen revenue" account and a separate "canteen expense" account.

Contact Person: Kristy Dauzat

40

CALDWELL PARISH SCHOOL BOARD SCHEDULE 12Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Eleven of the 25 invoices selected for testing were not properly canceled.

2. None.

3. None.• *

4. None.

5. Proper documentation was not available for three disbursements.

6. None.

7. None.

8. Check #1759 to Sam's Club included items which did not indicate a school purpose.

9. None.

10. None.

My recommendations are as follows:

2005-4 I noted three instances listed above where a check was paid without adequate supporting documentation. Itshould be understood by all personnel that disbursements will only be made when adequate documentationexists. Documentation should consist of an original invoice, evidence of receipt and proper approval. ;

CORRECTIVE ACTION PLAN: All checks written will be supported with a bill/receipt/invoice/packingslip/purchase order. Canceled checks will be attached to the proper documentation.

Contact Person: Kristy Dauzat

2005-5 I noted 11 instances where invoices were not canceled properly to prevent duplicate payment. Upon paymenteach invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments from occurring.

CORRECTIVE ACTION PLAN: All invoices will be marked "paid" with the date the payment was made.

Contact Person: Kristy Dauzat

41

CALDWELL PARISH SCHOOL BOARD SCHEDULE 12Columbia, Louisiana

KELLY ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES, continued

2005-06 State law dictates how public funds can be spent. School officials should familiarize themselves with theserestrictions in order to keep from violating these statutes.

CORRECTIVE ACTION PLAN: I have read the School Activity Fund Manual in order to be aware of howpublic funds can be spent. I also know to ask if I am ever in doubt.

Contact Person: Kristy Dauzat i

42

UNION CENTRAL ELEMENTARY SCHOOL

43

CALDWELL PARISH SCHOOL BOARD SCHEDULE 13Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

A. CASH AND CASH EQUIVALENTS

1. I obtained bank reconciliations for all bank accounts as of June 30,2005 and performed the following:

a. I verified the mathematical accuracy of the reconciliation.

b. I agreed the balance per the bank statement to the amount shown on bank reconciliation.

c. I compared the reconciled book balance to the general ledger for one bank account.

Caldwell Bank & Trust $26,652.41

d. I determined the propriety of deposits in transit, if any.

e. I examined all interfund transfers, if any.

There were no interfund transfers.

f. There were no outstanding checks at June 30,2005.

2. I obtained a list of certificates of deposit for the year and:

a. There were no certificates of deposit at June 30, 2005.

b. I tested the reasonableness of interest income.

3. I determined that cash has been sufficiently invested as required by LSA R.S. 39:2955,39:327, cash wasinvested in a public NOW account and a money market account.

4. There were no outstanding checks at June 30,2005 over 90 days old.

44

CALDWELL PARISH SCHOOL BOARD SCHEDULE 13Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

B. REVENUES

1. I selected 15 receipts on a random basis and performed the following procedures:

a. I traced to the bank validated deposit slip.

b. I determined if the deposits were made on a timely basis.

c. I traced the individual receipts within the deposit to the cash receipts journal to determine that thereceipts batch total matched the deposit total.

d. I traced the individual receipts within the deposit to their related account ledger card, teacherlog/receipt, concessions inventory or admission ticket reconciliation, etc.

45

CALDWELL PARISH SCHOOL BOARD SCHEDULE 13Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

DESCRIPTION OF PROCEDURESFOR SELECTED RECORDS AND TRANSACTIONS

FOR THE YEAR ENDED JUNE 30,2005

C. EXPENDITURES

I conducted my test of disbursements upon twenty-five checks selected on a random basis. Each check was testedfor these attributes:

1. Documentation canceled to prevent duplicate payment.

2. Check signed by authorized personnel.

3. Evidence of receipt of goods or services.

4. Invoice amount agrees with check amount.

5. Charge is supported by proper documentation.

6. Invoice date is current when compared to date of check.

7. Accounting distribution/classification is consistent and correctly posted.

8. Charge appears to be necessary and reasonable.

9. Bids obtained if applicable.

10. Expenditure is allowable under applicable laws.

The results of those tests are discussed in Schedule 14, Summary of Findings, Observations and Recommendations.

46

CALDWELL PARISH SCHOOL BOARD SCHEDULE 14Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

This section of the report summarizes my findings, observations and recommendations as a result of performing theprocedures described in the preceding section, description of procedures for records and transactions of UNIONCENTRAL ELEMENTARY SCHOOL.

REVENUES

I noted the following exceptions in my test of 15 receipts selected at random.

A. Receipt #437654 was not deposited in the bank.

B. One of the 15 receipts tested were deposited late.

C. None.

D. One of the 15 receipts tested lacked supporting documents or evidence of control over the receipts.

I recommend the following:

2005-1 One of the 15 deposits selected for testing were deposited late. Teachers should be instructed to turn allmoney in to the office promptly. Bank deposits should be made by the office on a daily basis.

CORRECTIVE ACTION PLAN: Teachers are now instructed to turn in money with log daily. Deposits aremade every day by 4:15pm.

Contact Person: Nicki McCann, Amber Dannehl

2005-2 All teachers or club sponsors who handle money should maintain a log to record all collections of moniesfrom students. The amounts collected should be recorded on the log and given to the principal or secretary forreceipt when the money is turned in. The teacher's log book should be turned in to the school office at year-end to provide an audit trail of the receipts.

CORRECTIVE ACTION PLAN: Copies of teacher logs and issued receipts will be kept in monthly foldersand filed with yearly financial records.

Contact Person: Nicki McCann, Amber Dannehl

47

CALDWELL PARISH SCHOOL BOARD SCHEDULE 14Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30, 2005

EXPENDITURES

Exceptions by attribute are recapped as follows:

1. Seven invoices out of 25 selected for testing were not canceled to prevent duplicate payment.

2. None.

3. Evidence of receipt was lacking on one of the disbursements tested, check #6824 to McDonald's.

4. There was no invoice that agreed to the payment for check #6824 listed above.

5. Proper documentation was not available for the check listed in item 3 above.

6. None.

7. Check # 6756 was issued for $126.59; it was posted to the general ledger for $126.50.

8. None.

9. None.

10. None.

My recommendations are as follows:

2005-3 I noted seven instances where invoices were not canceled properly to prevent duplicate payment. Uponpayment each invoice should be marked "Paid" to cancel the invoice and prevent duplicate payments fromoccurring.

CORRECTIVE ACTION PLAN: The principal will stamp each invoice with date paid and check number.

Contact Person: Nicki McCann

48

CALDWELL PARISH SCHOOL BOARD SCHEDULE 14Columbia, Louisiana

UNION CENTRAL ELEMENTARY SCHOOL

SUMMARY OF FINDINGS, OBSERVATIONS AND RECOMMENDATIONSFOR THE YEAR ENDED JUNE 30,2005

EXPENDITURES, continued

2005-4 I noted one instance listed above where a check was paid without adequate supporting documentation. Itshould be understood by all personnel that disbursements will only be made when adequate documentationexists. Documentation should consist of an original invoice, evidence of receipt and proper approval.

CORRECTIVE ACTION PLAN: Careful attention is given to be sure that each check has adequatedocumentation and is filed in check number order to ensure all checks are accounted for.

Contact Person: Nicki McCann

2005-5 I noted one disbursement that was posted incorrectly. Care should be taken to post charges to the appropriateaccounts and records should be reviewed for accuracy.

CORRECTIVE ACTION PLAN: By using QuickBooks to reconcile bank statements and manageaccounts, records are monitored more accurately,

Contact Person: Nicki McCann

49