Cagny 2009 v10print - IIS Windows...

25

1 2009 CAGNY February 19, 2009 Jon Moeller Chief Financial Officer Growth thru Recessions Sales 9 24 39 84 0 10 20 30 40 50 60 70 80 90 1979 1990 2001 2008 Sales, $Billions

Transcript of Cagny 2009 v10print - IIS Windows...

1

2009 CAGNYFebruary 19, 2009

Jon Moeller

Chief Financial Officer

Growth thru Recessions Sales

9

24

39

84

0102030405060708090

1979 1990 2001 2008

Sal

es, $

Bill

ion

s

2

Sales Growth

9x CAGR 8%

ProfitGrowth

Productivity

21xCAGR 11%

+350%

Growth thru 3 Recessions 1979 - Today

P&G Share Price Since 1979

$0

$10

$20

$30

$40

$50

$60

$70

$80

1979

1981

1982

1984

1986

1988

1989

1991

1993

1995

1996

1998

2000

2002

2003

2005

2007

P&

G S

hare

Pri

ce

Increasing Dividends

Dividends per Share$1.55

1956 1969 1982 1995 2008

3

Base Tide Liquid Laundry Retail Pricing

$0.18

$0.19

$0.20

$0.21

$0.22

FY 00/01 FY01/02 FY 02/03 FY 03/04 FY 04/05 FY 05/06 FY 06/07 FY 07/08 OND '08

Ret

ail P

rice

/use

5 Year Corporate Credit SpreadsVS U.S. Treasuries

0

50

100

150

200

250

300

350

400

JFM'07 AMJ'07 JAS'07 OND'07 JFM'08 AMJ'08 JAS'08 OND'08

Spr

ead

(bps

)

GDP Growth Slowing Worldwide

2008 Q4 GDP Growth

US -3.8

UK -1.8

China 6.8

Japan -3.3

Source: Global Insight & Government statistics

Note - US figures are annualized

Germany -1.7

4

U.S. Dollar vs G-7 Currency Basket(CAD-GBP-EUR Equal Weighting)

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

JFM'07 AMJ'07 JAS'07 OND'07 JFM'08 AMJ'08 JAS'08 OND'08

Pri

ce (U

.S. D

olla

rs /

Fore

ign

Cur

renc

y)

22% Depreciation

The Magnitude of FX Moves in OND’08(10/1/08 to 12/31/08)

30.30.3%CNY20.1-0.3%EUR

201.6-4.6%INR1602.5-13.7%CAD1602.5-18.8%BRL

17 thousand3.9-20.2%PLN350 thousand4.5-19.3%GBP

20 million5.3-13.3%RUB> 1 trillion7.6-22.3%MXN

Likelihood (1 in x)

Number of Std Deviations% MoveCCY

Foreign Exchange12

• Transaction

• Balance Sheet Revaluation

• Translation

5

FY ’09 Q2 Results

EPS

Global Value Share

All Six Business Segments Flat or Up^

+2%Organic Sales

�

�

�

(^) – Refers to Organic Sales.

Looking Forward

Inventory Impacts

Commodities

Pricing

Cost Savings, Productivity

& Simplification

Market Growth

Foreign Exchange

Key Materials Price EvolutionSpot Price VS Year Ago

Index

0 50 100 150 200 250

Material 1Material 2Material 3Material 4Material 5Material 6Material 7Material 8Material 9Material 10Material 11Material 12Material 13Material 14Material 15Material 16Material 17Material 18Material 19Total Total

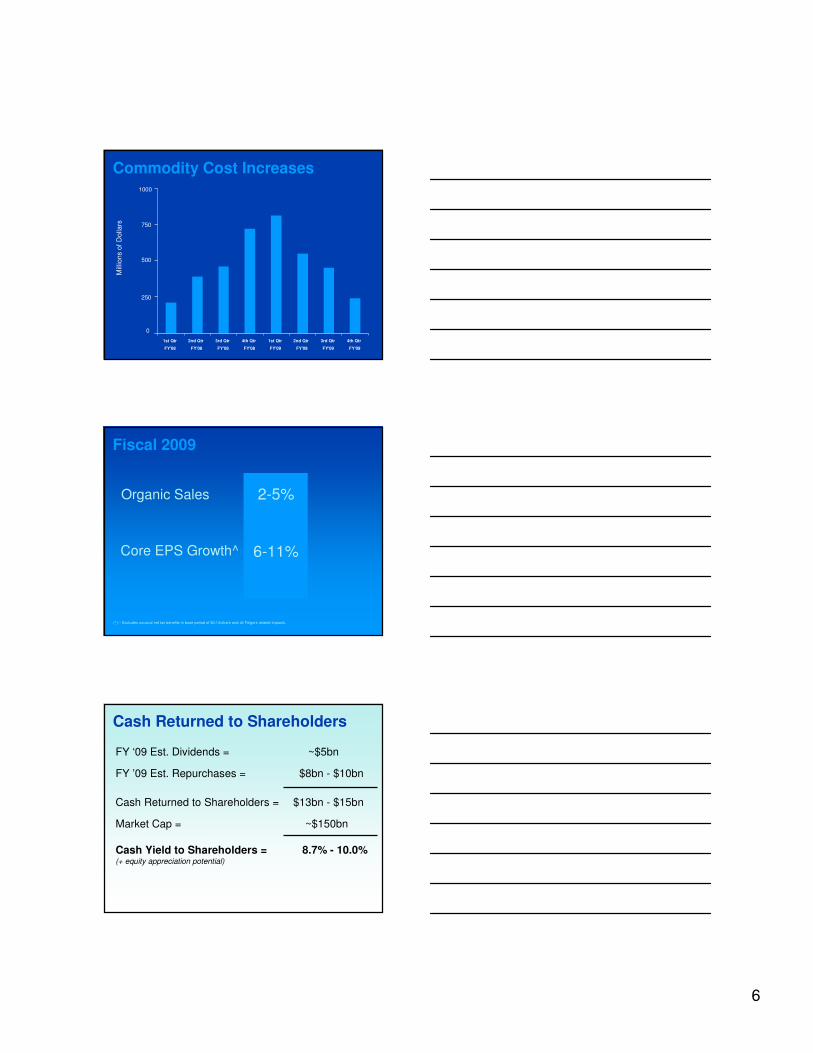

6

Mill

ions

of D

olla

rs

0

250

500

750

1000

1st Qtr

FY'08

2nd Qtr

FY'08

3rd Qtr

FY'08

4th Qtr

FY'08

1st Qtr

FY'09

2nd Qtr

FY'09

3rd Qtr

FY'09

4th Qtr

FY'09

Commodity Cost Increases

Fiscal 2009

(^) – Excludes unusual net tax benefits in base period of $0.14/share and all Folgers related impacts.

2-5%Organic Sales

Core EPS Growth^ 6-11%

FY ‘09 Est. Dividends = ~$5bn

FY ’09 Est. Repurchases = $8bn - $10bn

Cash Returned to Shareholders = $13bn - $15bn

Market Cap = ~$150bn

Cash Yield to Shareholders = 8.7% - 10.0%(+ equity appreciation potential)

Cash Returned to Shareholders

7

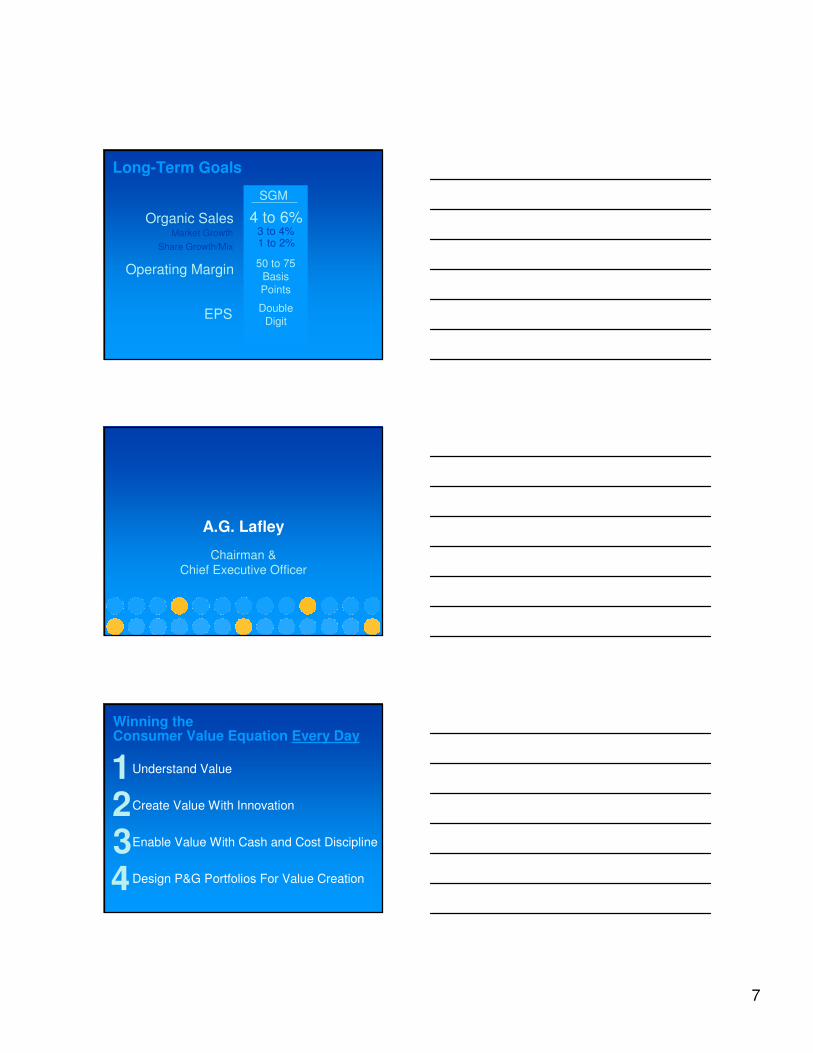

Long-Term Goals

4 to 6%Organic Sales

EPS DoubleDigit

Market GrowthShare Growth/Mix

3 to 4%1 to 2%

SGM

Operating Margin 50 to 75BasisPoints

A.G. Lafley

Chairman &Chief Executive Officer

Winning the Consumer Value Equation Every Day

Understand Value

Create Value With Innovation

Enable Value With Cash and Cost Discipline

Design P&G Portfolios For Value Creation

1234

8

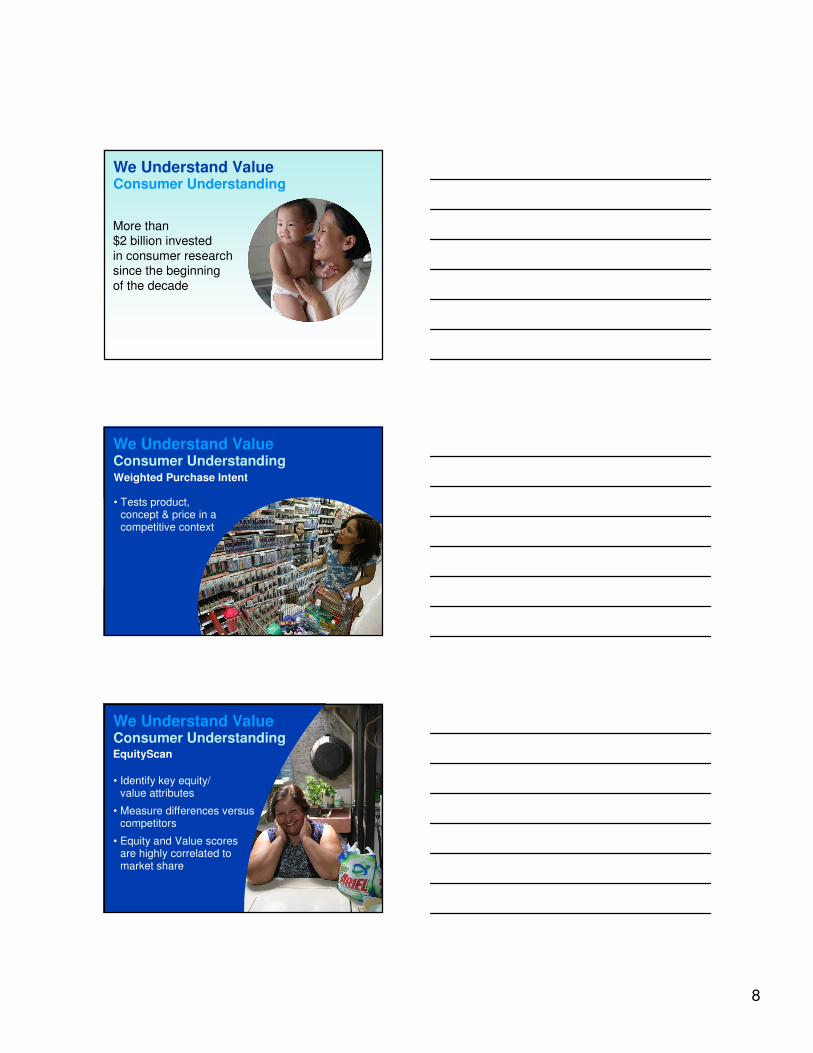

We Understand ValueConsumer Understanding

More than $2 billion invested in consumer research since the beginning of the decade

Weighted Purchase Intent

• Tests product,concept & price in acompetitive context

We Understand ValueConsumer Understanding

EquityScan

• Identify key equity/value attributes

• Measure differences versus competitors

• Equity and Value scoresare highly correlated tomarket share

We Understand ValueConsumer Understanding

9

Consumer Behavior

•Shopping less often

•Reducing home inventories

•Shopping discount stores

•Promotional buying

•Avoiding temptations

•Planning trips

New Coping Strategies% U.S. Consumers Saying They Will “Reduce Spending”

13

20

26

27

39

44

50

57

0 10 20 30 40 50 60

Food staples

House Cleaning And Paper Products

Health And Beauty Care

beverages

deli

clothing

housewares and linens

electronics and small appliances

Olay Skin Care Boutiques

~$40~$12 ~$20 ~$30~$7

We Understand ValueValue Reframing

10

• Stimulates growth and prevents commoditization

• Reduces costs, increases productivity and enables sharp pricing

• Differentiates our brands

We Create Value With Innovation

We Create Value With InnovationInnovation Investment

0

500

1000

1500

2000

2500 Spending versus competition

P&G Unilever L'Oreal Henkel KC CP RB Clorox Avon Energizer

Mill

ions

11

Median Scores for Consumer Products in the US from 1980 - 2008

1980-1

1982-3

1984-5

1986-7

1988-9

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Purchase Intent

Value Perceptions

Med

ian

Val

ue���������������� �������������������

We Create Value With InnovationPurchase Interest and Value Perceptions of Innovations

We Create Value With Innovation New Products Success Rate

�

�

�

�

�

��

��

��

��

���� ���� ���� ���� ���� ���� ���� ���� ���� ���� ���� ���� ���� ����

���

�

!��"���#������ ����$%����

BASES Success RateMisery Index the sum of the inflation rate and unemployment rate

Denotes Period of Recession in the U.S.

•••••••

• • • • • • •

• • • • • • •• • • • • • •

•••••••

••••••• •••

••••

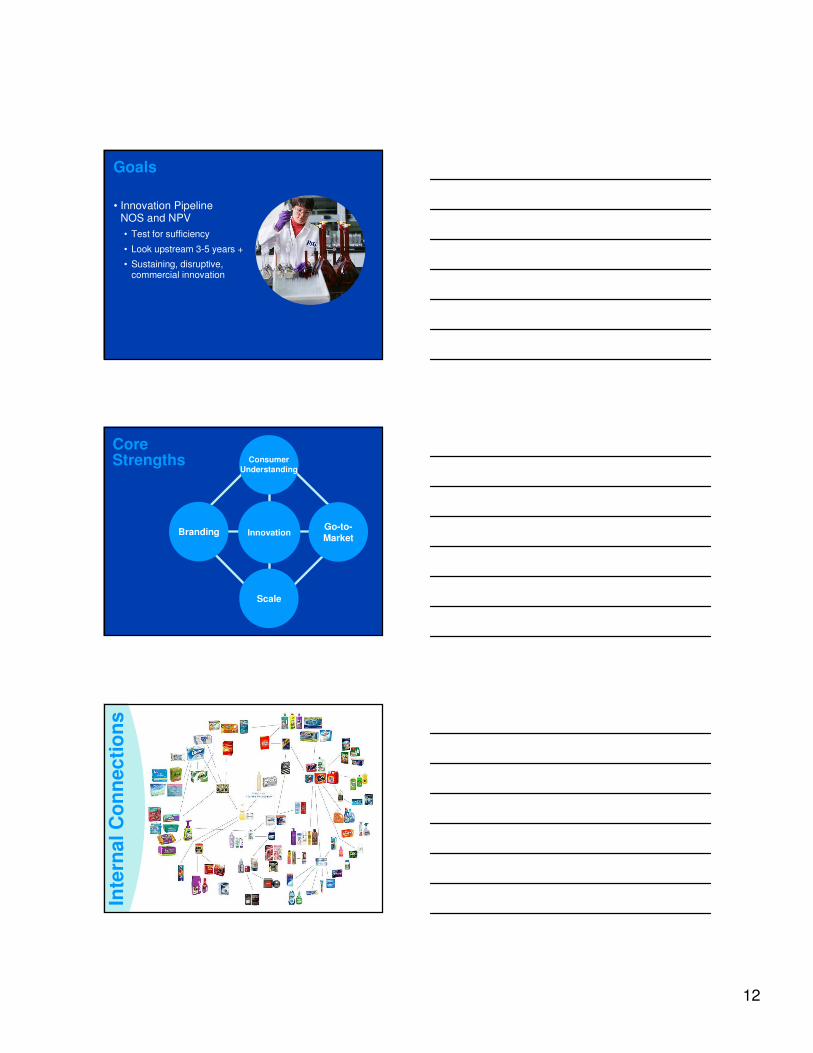

Goals

Strategies

Structure/Systems

Purpose

Strengths

Culture

Leadership

P&

G In

nova

tion

Mod

el

12

Goals

• Innovation Pipeline NOS and NPV• Test for sufficiency

• Look upstream 3-5 years +

• Sustaining, disruptive, commercial innovation

Branding Go-to-Market

ConsumerUnderstanding

Innovation

Scale

Core Strengths

Inte

rnal

Con

nect

ions

13

We Create Value With InnovationTide Total Care

• 60% price premium

• $150MM year 1 sales

• Good Housekeeping Very Innovative Product (VIP) award

• 30% price premium

• 3+% value share• 50% bigger than Green Works

• 33% incremental

We Create Value With Innovation Dawn Hand Renewal

We Create Value With Innovation Always Infinity

• 60% price premium

• 6% value share

• Absorbs 10x its weight

14

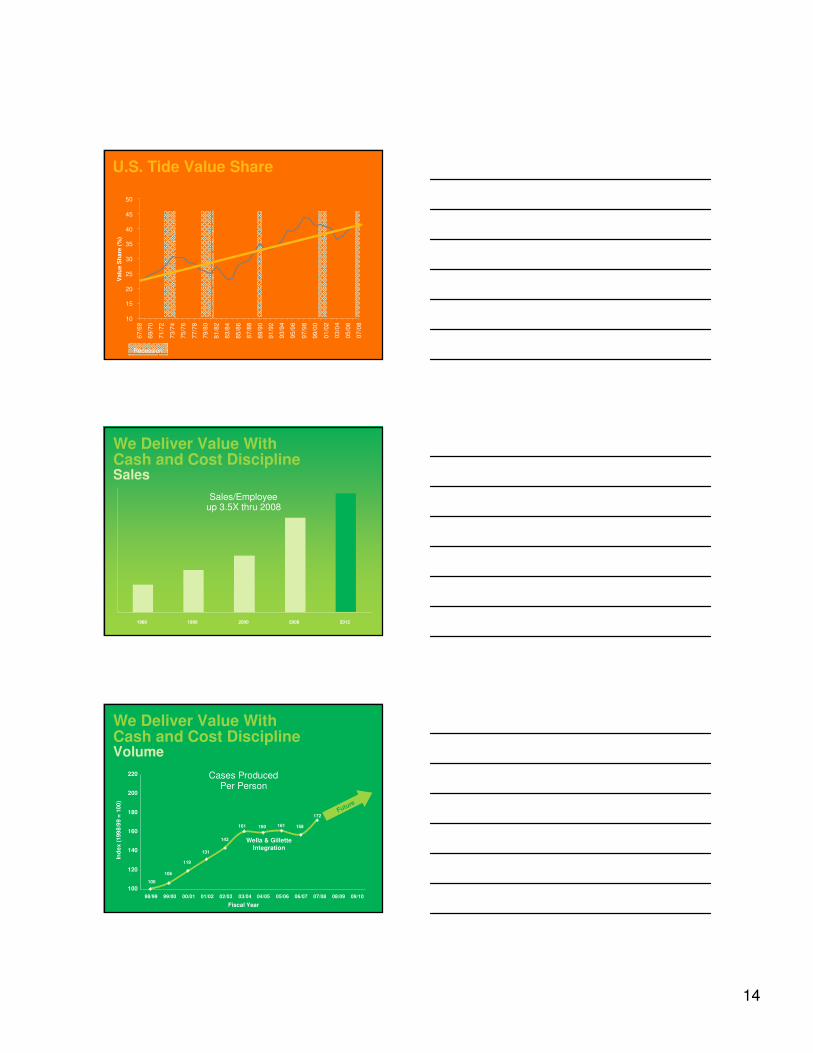

U.S. Tide Value Share

Recession

10

15

20

25

30

35

40

45

50

67/6

8

69/7

0

71/7

2

73/7

4

75/7

6

77/7

8

79/8

0

81/8

2

83/8

4

85/8

6

87/8

8

89/9

0

91/9

2

93/9

4

95/9

6

97/9

8

99/0

0

01/0

2

03/0

4

05/0

6

07/0

8

Val

ue S

hare

(%)

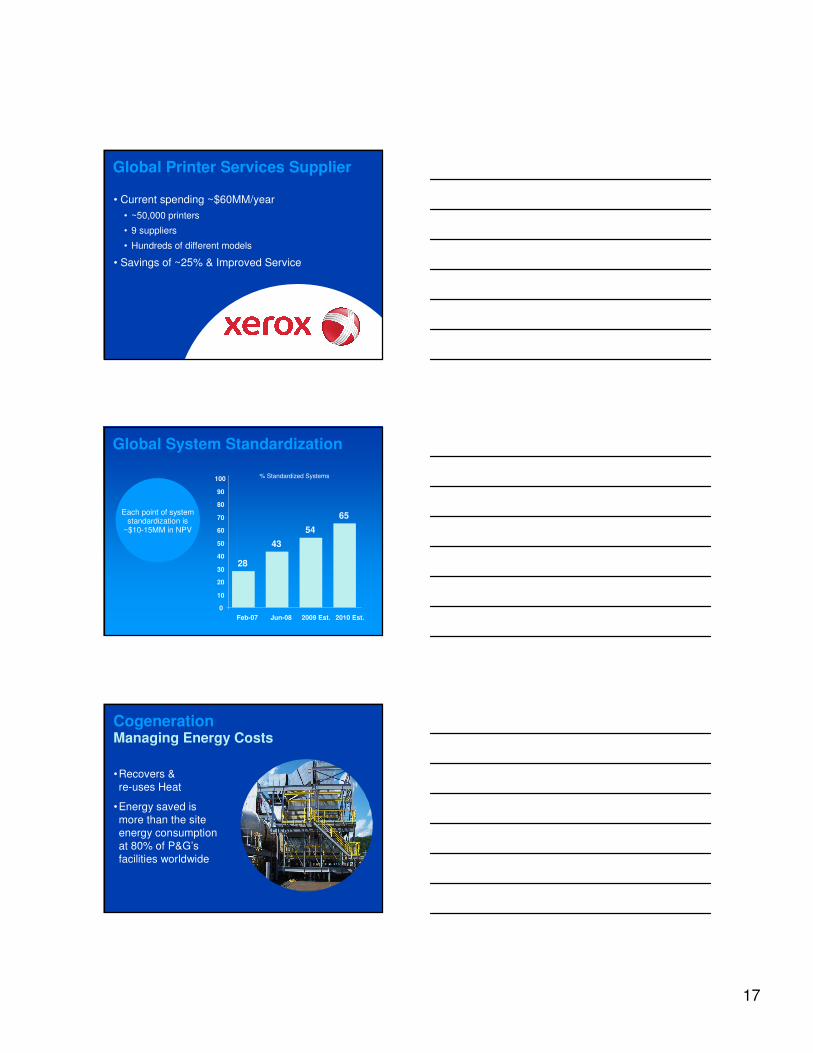

Sales/Employee up 3.5X thru 2008

1980 1990 2000 2008 2012

We Deliver Value With Cash and Cost DisciplineSales

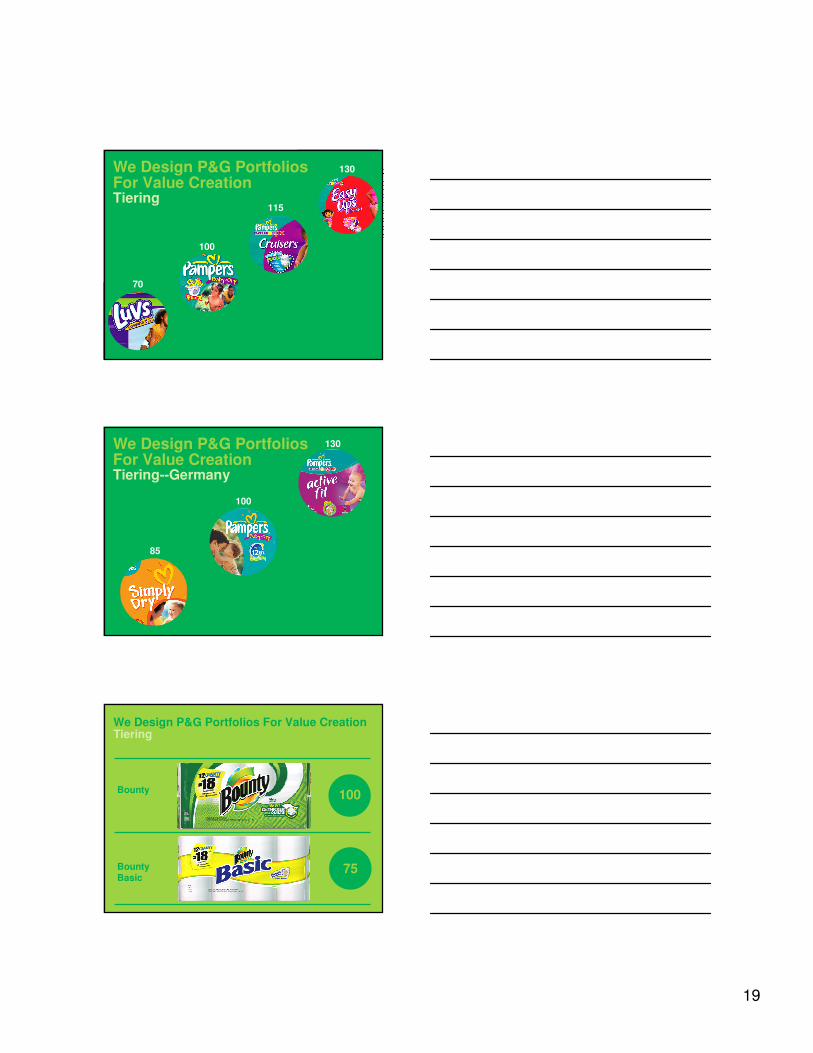

Wella & Gillette Integration

Future

119

160 161 158

100

131

161

172

106

143

100

120

140

160

180

200

220

98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10

Fiscal Year

Inde

x (1

998/

99 =

100

)

Cases Produced Per Person

We Deliver Value With Cash and Cost DisciplineVolume

15

Net Earnings/Employee up 8X thru 2008

1980 1990 2000 2008 2012

We Deliver Value With Cash and Cost DisciplineProfit

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

FY '02 FY '03 FY '04 FY '05 FY '06 FY '07 FY '08

We Deliver Value With Cash and Cost DisciplineOperating Margin Trends

Free

Cas

h Fl

ow, $

Bn

$0

$2

$4

$6

$8

$10

$12

$14

FY '03 FY '04 FY '05 FY '06 FY '07 FY '08 FY '09E

We Deliver Value With Cash and Cost DisciplineFree Cash Flow

16

Ongoing Productivity

Simplifying our work, decision-

making and structure

Frees up investment for growth

Frees up capacity for innovation

Connect& Develop

HOG

TravelReduction

Small BrandPortfolio

ExpatReduction

NOG

ReducedHierarchy

Productivity& Cost

Discipline

Modeling &Simulation

AcquisitionSynergies

Multi-CategoryPlants

DistributionCenter

Redesign

Low CostCapital

Locations

ZOG

ModularDesign

End to End Network Planning

Shop in Shop

Plant FacilitySite Services

TransportationTransformation

Partnerships

Productivity Improvement& Cost Discipline

Global Business ServicesCost Savings

•Reduced costs as a % of sales by 1/3rd since 2003•Additional 1/3rd in the next 5 years

$600 Million in Savings

$1 Billion in Savings

17

Global Printer Services Supplier

• Current spending ~$60MM/year• ~50,000 printers

• 9 suppliers

• Hundreds of different models

• Savings of ~25% & Improved Service

Each point of systemstandardization is

~$10-15MM in NPV

Global System Standardization

28

43

54

65

0

10

20

30

40

50

60

70

80

90

100

Feb-07 Jun-08 2009 Est. 2010 Est.

% Standardized Systems

•Recovers & re-uses Heat

•Energy saved is more than the site energy consumption at 80% of P&G’s facilities worldwide

CogenerationManaging Energy Costs

18

•Reduce the number of color options by up to 50%

•Potential to save as much as $50MM/year

Color Cost Reduction

Outsourcing• Outsourced talent & music negotiations

• Leverages talent & music across medias

• Direct access to industry experts

• $20MM / year savings

• Broad re-application

Purchasing

Base Tide

We Design P&G Portfolios For Value CreationTiering

65

Tide Total Care

Tide Value Adds

Gain

Cheer

Era

80

90

100

120

160

Pric

e In

dex

19

100

70

115

130We Design P&G Portfolios For Value CreationTiering

100

85

130We Design P&G Portfolios For Value CreationTiering--Germany

Bounty Basic

Bounty

75

100

We Design P&G Portfolios For Value CreationTiering

20

CharminBasic

CharminUltra

75

100

We Design P&G Portfolios For Value CreationTiering

JFM '05 AMJ '05 JAS '05 OND '05 JFM '06AMJ '06JAS '06 OND '06JFM '07AMJ '07JAS '07 OND '07JFM '08AMJ '08JAS '08 OND '080

50

100

150

200

250

300

350

400

450

Crest Pro-Health Rinse

JFM ‘05

Crest Pro-Health

ToothpasteJAS ‘06

OralB Pulsar Pro-Health

JFM ’07

Crest Pro-HealthWhiteningJAS ‘08

*Source: P&G Internal All Outlet Data

Annualized Q

uarterly Sales ($ M

illion)

OralB Cross Action Pro-Health

JFM ‘08Colgate TotalLaunched 1997

Crest Pro-Health NightToothpaste & Rinse

JAS ‘07

Pro-HealthRinse

Pro-Health Toothpaste

Pro-Health Toothbrush

We Design P&G Portfolios For Value CreationTiering

US Recessions in Past 100 years• Nearly 97 Quarters of official “contraction” over the past 400 quarters• 24% of the time in a various degrees of contraction

US Business Cycles - Past 100 yrs

1907

1911

1915

1919

1923

1927

1931

1935

1939

1943

1947

1951

1955

1959

1963

1967

1971

1975

1979

1983

1987

1991

1995

1999

2003

2007

Recession

21

P&G Total Shareholder Return: Since Periods Of Contraction

P&G CAGR10.6%

Pre-Depression to today1929 => 2009

P&GCAGR14.4%

P&GCAGR6.8%

Early 80’s Contraction to todayJan 1980 => 2009Vs. S&P 500 return of +7%

Technology Bubble to todayJan 2001 => 2009Vs. S&P 500 decline of -6%

Includes Share appreciation and Dividends thru Feb 13, 2009

P&G Strategies

Growing From The Core: Big Categories, Big Brands, Big Countries

Accelerating Growth in Faster-Growing, Higher Margin Businesses: Beauty, Health and Personal Care

Winning With Low Income Consumers/Winning In Emerging Markets

123

Sales Growth Profit Growth

Largest 6 core P&G Categories: Baby Care, Fabric Care, Family Care, Fem Care, Hair Care, and Home Care

6 Largest businesses delivered ~50% of Sales and Profit Growth

Gillette29%

Other22%

49%

Gillette27%

Other24%

49%

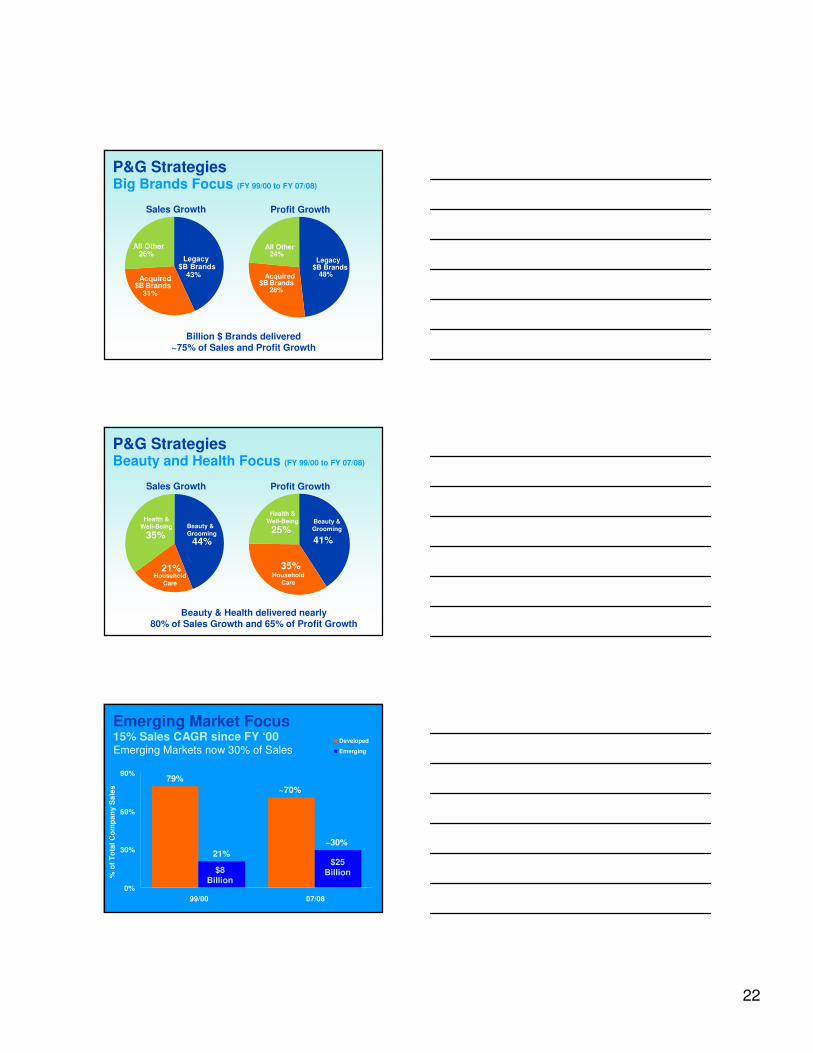

P&G Strategies Core Category Focus (FY 99/00 to FY 07/08)

22

Legacy $B Brands

48%Acquired $B Brands

28%

All Other24%

Billion $ Brands delivered ~75% of Sales and Profit Growth

Acquired Billion $ Brands: Gillette, Mach 3, Fusion , Oral B, Wella, Duracell, and Braun

Legacy $B Brands

43%Acquired $B Brands

31%

All Other26%

P&G Strategies Big Brands Focus (FY 99/00 to FY 07/08)

Sales Growth Profit Growth

Health &Well-Being

HouseholdCare

Beauty & Grooming

Health &Well-Being

HouseholdCare

Beauty & Grooming

41%

35%

25%44%

21%

35%

Beauty & Health delivered nearly 80% of Sales Growth and 65% of Profit Growth

P&G Strategies Beauty and Health Focus (FY 99/00 to FY 07/08)

Sales Growth Profit Growth

Emerging Markets now 30% of Sales

79%~70%

21%~30%

0%

30%

60%

90%

99/00 07/08

% o

f Tot

al C

om

pan

y S

ales

Developed

Emerging

$25Billion$8

Billion

Emerging Markets now 30% of Sales

Emerging Market Focus15% Sales CAGR since FY ‘00

23

Household Care Market Attractiveness• $200 billion global market

• P&G’s global share is 19%• 29% in the countries where we compete

• Huge opportunities for growth

Beauty & GroomingMarket Attractiveness• $250 billion global market

• Highly fragmented market• P&G leading with approximately 12%• L’Oreal just below 12%

• $240 billion global market • Growing 5% to 6% annually• Healthy margin structure• Highly fragmented market

Consumer Health CareMarket Attractiveness

24

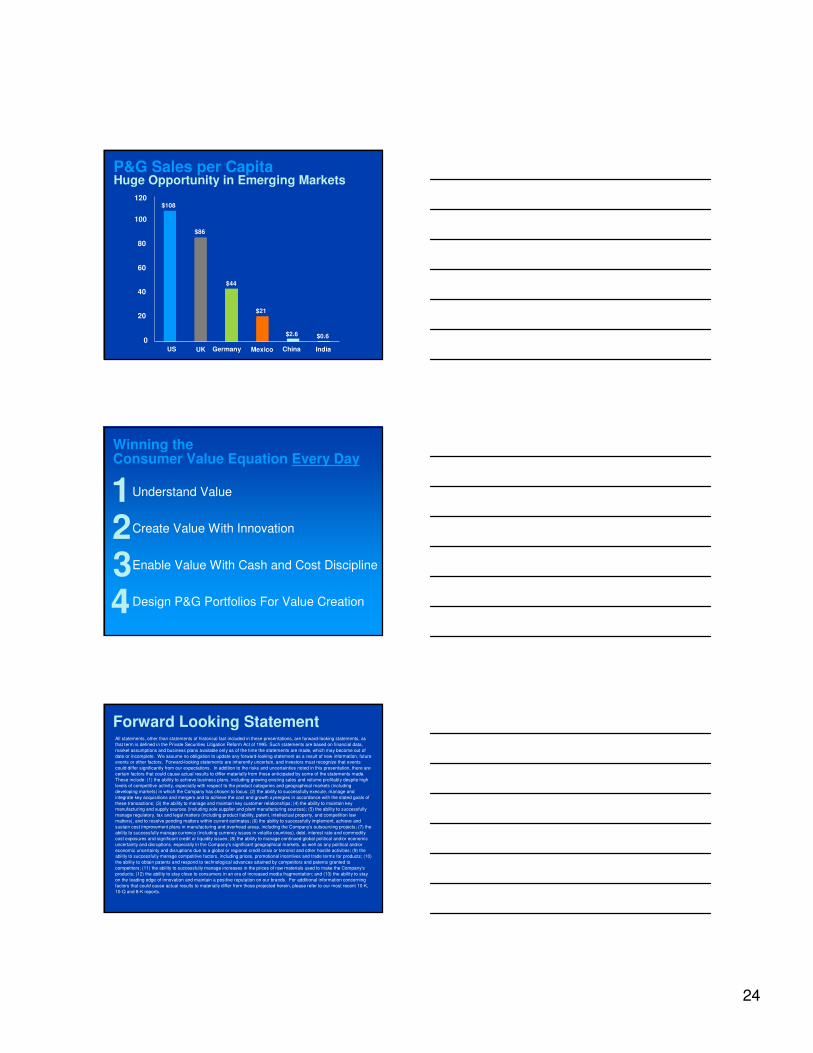

P&G Sales per Capita

0

20

40

60

80

100

120

US Germany ChinaUK IndiaMexico

$108

$86

$44

$21

$2.6 $0.6

Huge Opportunity in Emerging Markets

Winning the Consumer Value Equation Every Day

Understand Value

Create Value With Innovation

Enable Value With Cash and Cost Discipline

Design P&G Portfolios For Value Creation

1234

Forward Looking StatementAll statements, other than statements of historical fact included in these presentations, are forward-looking statements, as that term is defined in the Private Securities Litigation Reform Act of 1995. Such statements are based on financial data, market assumptions and business plans available only as of the time the statements are made, which may become out of date or incomplete. We assume no obligation to update any forward-looking statement as a result of new information, future events or other factors. Forward-looking statements are inherently uncertain, and investors must recognize that events could differ significantly from our expectations. In addition to the risks and uncertainties noted in this presentation, there are certain factors that could cause actual results to differ materially from those anticipated by some of the statements made. These include: (1) the ability to achieve business plans, including growing existing sales and volume profitably despite high levels of competitive activity, especially with respect to the product categories and geographical markets (including developing markets) in which the Company has chosen to focus; (2) the ability to successfully execute, manage and integrate key acquisitions and mergers and to achieve the cost and growth synergies in accordance with the stated goals of these transactions; (3) the ability to manage and maintain key customer relationships; (4) the ability to maintain key manufacturing and supply sources (including sole supplier and plant manufacturing sources); (5) the ability to successfully manage regulatory, tax and legal matters (including product liability, patent, intellectual property, and competition law matters), and to resolve pending matters within current estimates; (6) the ability to successfully implement, achieve and sustain cost improvement plans in manufacturing and overhead areas, including the Company's outsourcing projects; (7) the ability to successfully manage currency (including currency issues in volatile countries), debt, interest rate and commodity cost exposures and significant credit or liquidity issues; (8) the ability to manage continued global political and/or economic uncertainty and disruptions, especially in the Company's significant geographical markets, as well as any political and/or economic uncertainty and disruptions due to a global or regional credit crisis or terrorist and other hostile activities; (9) the ability to successfully manage competitive factors, including prices, promotional incentives and trade terms for products; (10) the ability to obtain patents and respond to technological advances attained by competitors and patents granted to competitors; (11) the ability to successfully manage increases in the prices of raw materials used to make the Company's products; (12) the ability to stay close to consumers in an era of increased media fragmentation; and (13) the ability to stay on the leading edge of innovation and maintain a positive reputation on our brands. For additional information concerning factors that could cause actual results to materially differ from those projected herein, please refer to our most recent 10-K, 10-Q and 8-K reports.

25

Regulation G Disclosure

For full reconciliation, visit:www.pg.com/investors