Cadillac Tax for Employers 101 - How to Avoid Penalties?

33

-

Upload

benefitexpress -

Category

Recruiting & HR

-

view

649 -

download

0

Transcript of Cadillac Tax for Employers 101 - How to Avoid Penalties?

Law of Unintended Consequences

Revenue

• As one of the Affordable Care Act’s principal “pay-fors,” the Cadillac tax was initially expected to raise $137 Billion in the first 10 years.

• After examining recent cost trends in employer-sponsored health benefits, that estimate was revised, and now CBO expects the Cadillac tax will generate about $80 billion over the next 10 years

• True cost next will reveal itself in the next 20 years

Medicare Secondary Payer Rules

Purpose / Debate

• Health economists for some time have argued that rich benefit structures create price insensitivity in consumers who demand more and more expensive services

• Consumers, plans, and providers need “skin” in the game for reform to work. Does the Cadillac tax achieve this?

Opposition arguments: public exchange time bomb, employer ante at health reform table.

The Reality

• The Cadillac tax will affect fairly modest plans

• Depending upon source roughly half of employers will hit thresholds in 2018.

Much higher numbers in the next 10 years

State governments, unions, employers all subject to tax

• Takeaway: Plans can only reduce richness to a point. – Long term avoidance requires more than benefit buy downs.

• Takeaway: Because much of the Cadillac tax is statutory, legislation is likely needed to fix big ticket items.

Recent subregulatory guidance will allow employer feedback before regulations are issued similar to mandate

• Beyond statute interpretation unlikely given recent case.

The Basics

Beginning in 2018, employer-sponsored plans will be subject to a 40 percent non-deductible excise tax on the dollar amount of coverage that exceeds certain specified thresholds.

• Was originally slated to take effect in 2013 and original thresholds just indexed to 2018 dollars.

• Why 2018…

2018 threshold for individual coverage is $10,200 and the threshold for family coverage is $27,500.

• Adjusted by “health cost adjustment percentage”

• Adjusted upwards for early retirees and individuals in high-risk professions

• Indexed for inflation

How does it work?

The Cadillac tax applies to the dollar amount that exceeds the specified threshold using the following formula:

• “The aggregate cost of the applicable employer sponsored coverage of the employee for the month, over

• An amount equal to 1/12 of the annual limitation for the calendar year in which the month occurs.”

Example: If an employer offered individual coverage that cost $12,000 per employee, the excess amount for a month would be calculated by ($12,000 / 12 months) − ($10,200 / 12) = $150. Therefore, the employer would be taxed 40 percent of $150, or $60 per employee per month. Over a year, the Cadillac tax liability per employee would be $720.

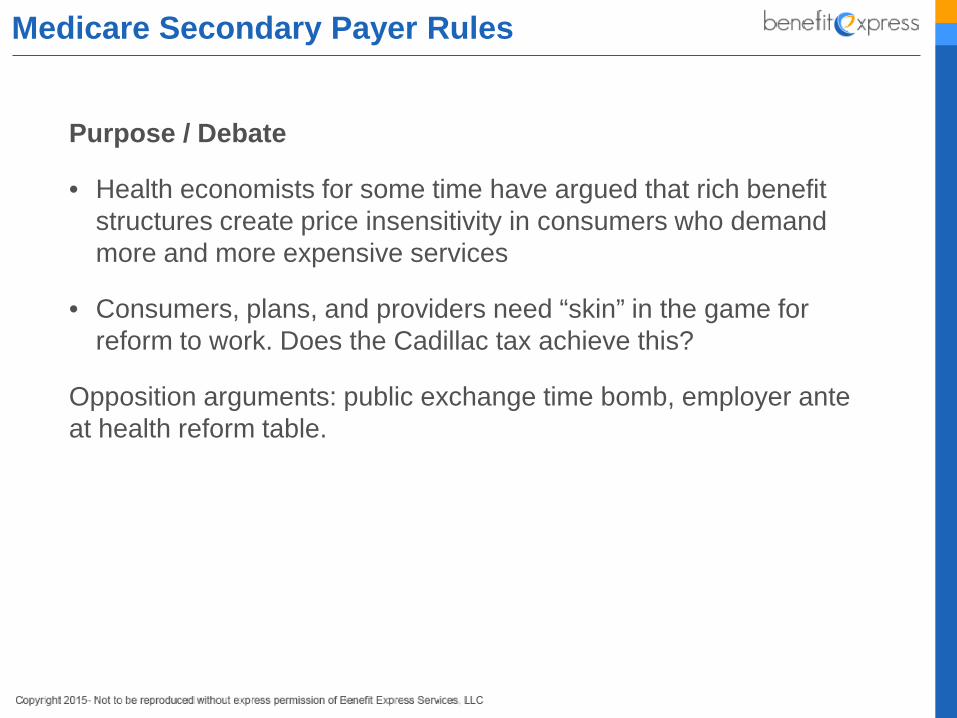

Thresholds

• The $10,200 / $27,200 thresholds amounts Increased in 2018 for Health Cost Adjustment Percentage

• The health cost adjustment percentage is designed to increase the thresholds in the event that the actual growth in the cost of U.S. health care between 2010 and 2018 exceeds the projected growth for that period.

The health cost adjustment percentage is equal to 100 percent plus the excess (if any) of:

• the percentage by which the per employee cost for providing coverage under the Blue Cross/Blue Shield standard benefit option under FEHBP for plan year 2018 (determined by using the benefit package for such coverage in 2010) exceeds such cost for plan year 2010;

• over 55 percent.

• Example: If the cost of standard FEHBP coverage increases by 60 percent from 2010 to 2018, then the health cost adjustment percentage would be (60 percent − 55 percent) + 100 percent = 105 percent.

Health Cost Adjustment

Thresholds

In 2019, the threshold amounts, after application of the health cost adjustment percentage in 2018, if any, are indexed to the CPI-U, as determined by the Department of Labor, plus one percentage point, rounded to the nearest $50.

In 2020 and thereafter, the threshold amounts are indexed to the CPI-U as determined by the Department of Labor, rounded to the nearest $50.

Health Cost Adjustment

Thresholds Age and Gender Adjustment

• The $10,200 / $27500 threshold amounts are increased for any taxable period by the Age and Gender Adjustment

• Is an amount equal to the excess (if any) of—

the premium cost of the Blue Cross/Blue Shield standard benefit option under the FEHBP Plan for the type of coverage provided such individual in such taxable period if priced for the age and gender characteristics of all employees of the individual’s employer, over

the premium cost for the provision of such coverage under such option in such taxable period if priced for the age and gender characteristics of the national workforce.

• Example: If the cost of standard FEHBP coverage for the age and gender characteristics of the employer’s workforce is $11,500 and the cost of standard FEHBP coverage for the age and gender characteristics of the national workforce is $10,500, then the age and gender adjustment would be $11,500 − $10,500 = $1,000.

Thresholds Age and Gender Adjustment

• The IRS is considering whether to use a snapshot approach for the determination of the age and gender characteristics of a particular employer's population.

• Employers generally would be required to determine age and gender as of the first day of the plan year.

• All adjustments and calculations would be determined separately for self-only coverage and for other than self-only coverage.

• The IRS anticipates developing age and gender adjustment tables for use in making the calculation.

Thresholds Retirees and High Risk Professions

• The $10,200 / $27,500 threshold amounts are increased for individual qualified retirees or those who participate in a plan sponsored by an employer the majority of whose employees covered by the plan are engaged in a high-risk profession.

• Qualified Retirees: individuals over 55 who are not Medicare eligible and receiving employer- sponsored retiree health coverage.

• High Risk Professions: Line workers; Law enforcement officers ; Fire protection personnel; Individuals who provide out-of-hospital emergency medical care (including EMTs, paramedics, and first-responders) ;Longshoremen; Construction, mining, agriculture (not including food processing), forestry, and fishing personnel; retirees with 20 years in these industries.

• In 2018 thresholds for Individual Coverage increased $1,650 or for Family Coverage increased $3,450.

Thresholds Retirees and High Risk Professions

In 2019, the additional $1,650 and $3,450 amounts are indexed to the CPI-U, plus one percentage point, rounded to the nearest $50; and

In 2020 and later years, the additional threshold amounts are indexed to the CPI-U, rounded to the nearest $50.

Thresholds Retirees and High Risk Professions

Future guidance might explain:

How an employer determines that an employee is not eligible for enrollment under the Medicare program; and

How an employer determines whether the majority of employees covered by a plan are engaged in a high-risk profession, what the term “plan” means in that context, and how an employer determines that an employee was engaged in a high-risk profession for at least 20 years

Thresholds Indexing

Medical inflation has historically risen faster than CPI-U

Holding everything constant plans will come closer to threshold by virtue of indexing.

Holding everything constant if subject to the tax the amount will grow each year.

To whom does the Cadillac Tax apply?

• The ACA states that each “coverage provider” is responsible for payment of the tax.

• In the context of insured group health plans, the coverage provider is the health insurance company.

For self-insured plans, the entity that administers the plan is the covered provider responsible for payment of the tax.

• Regulations identify the plan sponsor

HSA contributions the coverage provider is the employer

Other coverage, the administrator

• While the penalties may technically apply to the health insurance company, the cost of the penalties will be passed down to the employer.

To whom does the Cadillac Tax apply?

The IRS is considering a proposal that would identify the entity that administers the plan benefits either using:

• the person responsible for performing the day-to-day functions that constitute the administration of plan benefits; or

• the person that has the ultimate authority or responsibility under the plan or arrangement regarding the administration of the plan benefits, even if the person does not routinely exercise that authority or responsibility.

What benefits are included?

• The Cadillac Tax applies to “applicable employer-sponsored coverage.”

• Applicable employer-sponsored coverage includes coverage under any group health plan made available to the employee by an employer which is excludable from the employee’s gross income or would be excludable if it were employer-provided coverage.

Major medical coverage and coverage provided under account-based plans (e.g., FSAs and HSAs) are likely includable in the calculations.

Wellness likely includable if not excepted benefits

• Coverage treated as applicable employer- sponsored coverage without regard to whether the employer or employee pays for the coverage.

What benefits are included?

Account Based Plans:

• FSAs: Includes the employee’s salary reduction and any employer contribution

• HSAs: Includes the employer contribution

Proposal to include employee pretax contributions as well

• HRA: Includes full amount of coverage purchased through an HRA

What benefits are included?

• Governmental plans—coverage for civilian employees is included but military coverage is not included;

• On-site medical clinic coverage; but proposed regulations might exclude on-site medical clinics that offer only de minimis medical care to employees;

• Multiemployer plan (as defined in §414(f)) coverage;

• Retiree coverage;

• Coverage described in §9832(c)(3) (which includes coverage only for a specified disease or illness and hospital indemnity or other fixed indemnity insurance), if the payment for the coverage or insurance is excluded from gross income or a deduction under §162(l) is allowed for it; 34 and

• Executive physical programs—proposed regulations might designate these programs, although not listed in the statute, as applicable coverage based on the general definition.

What benefits are excluded?

Not taken into account in determining the value of employer-sponsored coverage for purposes of the excise tax are the following

• Long-term care insurance;

• Coverage only for accident or disability income insurance, or a combination;

• Coverage issued as a supplement to liability insurance;

• Liability insurance, including general liability insurance and automobile liability insurance;

• Workers' compensation or similar insurance;

• Automobile medical payment insurance;

• Credit-only insurance;

• Other similar insurance coverage, specified in regulations, under which benefits for medical care are secondary or incidental to other insurance benefits;

• Separately-covered benefits for the treatment of the mouth or the eye; proposed regulations might indicate that self-insured limited scope dental and vision coverage that qualifies as an excepted benefit under Treasury regulations would be excluded from applicable coverage, as whether coverage is insured or self-insured generally is not relevant for purposes of the excise tax;

• Coverage only for a specified disease or illness or for hospital indemnity or other fixed indemnity insurance, if the payment for the coverage or insurance is not excluded from gross income or a deduction under §162(l) is not allowed for it; 40 and

• Governmental plan coverage for members of the military

How cost is calculated

The ACA says that the cost of coverage will be determined under rules similar to the rules used for calculating cost of coverage under COBRA.

The subregulatory guidance provides detailed methodologies for determining cost using COBRA rules

Proposal to allow for geographic differences

How cost is calculated

The amount subject to the excise tax is the sum of the aggregate premiums for health insurance coverage, the amount of any salary reduction contributions to a medical FSA for the taxable year, and the dollar amount of employer contributions to an HSA or an Archer MSA, minus the dollar amount of the threshold.

The IRS is considering an approach under which contributions to account-based plans would be allocated on a previous pro-rata basis over the period to which the contribution relates, regardless of the timing of the contributions during the period.

How cost is calculated

• The coverage amount that is compared to the dollar limit is based on the applicable coverage in which the employee is enrolled, not on the coverage offered to the employee (which might be the same).

• The aggregate premiums for health insurance coverage include all employer-sponsored health insurance coverage including coverage for any supplementary health insurance coverage.

• The applicable premium for health coverage provided through an HRA is also included in this aggregate amount.

Taxable and Determination Period

• Under the statute, the tax is assessed on a calendar-year basis.

• The IRS anticipates that the taxable period will be the calendar year for all taxpayers.

• The IRS anticipates that employers will be required to determine the cost of applicable coverage sufficiently soon after the end of the year to allow coverage providers to timely pay any tax due.

Penalty for Failure to Report Correct Amounts

The employer or plan sponsor is subject to penalties for failure to properly calculate the amount of excess benefit during any period.

The employer or plan sponsor must pay an amount equal to the additional excise tax due, plus interest at the underpayment rate for the period.

Penalty for Failure to Report Correct Amounts

No penalty applies if:

• the employer or plan sponsor neither knew nor, exercising reasonable diligence, would have known of the failure; or

• the failure was due to reasonable cause and not to willful neglect and is corrected during the 30-day period beginning on the first date on which the employer knew, or exercising reasonable diligence would have known, of the failure. 68

If a failure to report the correct amount is due to reasonable cause, the Treasury Secretary may waive this penalty to the extent that its payment is excessive or otherwise inequitable relative to the failure involved.

Employer Response

• A fight for our life:

Given the indexing issue if thresholds are hit it is unlikely that the most plans will continue to offer coverage.

• Hard to justify increasing non-deductible business expenses that do not provide additional benefit to employees.

• At this point mostly compliance focused. Evaluation of plans starting.

• Reducing benefit richness

State benefit mandates

Recruitment and retention issues

Cadillac tax avoiding plans

• More migration to HDHPs

• Likely that only one benefit option will be offered

• Lowest common denominator with stand-alone add o

Employer Response

Value Based Purchasing/ Population Health Management

• In its infancy for employers.

Most programs only include provider incentives

• Takes time to bend the cost curve

• Need market share to negotiate

Provider Innovation

• Looking to telehealth, and other non-traditional settings.

Congress to the Rescue???

The Middle Class Health Benefits Tax Repeal Act

• Would repeal the Cadillac Tax

• Introduced by Joe Courtney (108 Co-Sponsors (mostly D’s))

The Patient Choice, Affordability, Responsibility, and Empowerment Act

• Introduced by Burr, Hatch and Upton

• Repeals Cadillac Tax and caps employee exclusion for employer provided health care at $12,000; $30,000 for family

• Indexed at CPI + 1

Congress to the Rescue???

Legislative solution

• Must maintain system transformative qualities

• Must account for regulatory, geographic, and demographic characteristics of plans

• Must be fiscally responsible

Questions?