Business Report 201730 Regional Engagement 31 Enabling Services 32 TECHNOLOGY AND OPERATIONS...

59

Business Report 2017

Transcript of Business Report 201730 Regional Engagement 31 Enabling Services 32 TECHNOLOGY AND OPERATIONS...

Business Report 2017

WE BUILD MUTUAL DIGITAL INFRASTRUCTURE THAT CONNECTS ECONOMIES

1 About this report

2 Snapshot of BankservAfrica

5 INDUSTRY OVERVIEW

6 Snapshot of the payments industry

12 Payments evolution through collaboration

15 WHO WE ARE AND WHAT WE DO

16 Joint leadership review: Chairman and Chief Executive Officer

20 Our leadership

22 Our structure

24 STRATEGIC PORTFOLIO OVERVIEW

25 Overview from Martin Grunewald: Acting Chief Payments Officer

27 Digital Infrastructure

28 Retail Payments

29 Information Services

30 Regional Engagement

31 Enabling Services

32 TECHNOLOGY AND OPERATIONS OVERVIEW

33 Overview from Emile Burger: Chief Operating Officer

36 SUPPORT SERVICES OVERVIEW

37 Overview from Parusha Gajathar: Chief Financial Officer

38 Corporate Integrity

43 Internal Audit

44 Legal Services

45 Human Capital

48 SUMMARISED ANNUAL FINANCIAL STATEMENTS

56 GLOSSARY

56 CONTACT DETAILS

Table of contents

Business Report 2017

1

About this report

SCOPE AND BOUNDARYWe are pleased to present our business report for the financial year 1 July 2016 to 30 June 2017. This business report (hereinafter referred to as “the report”) is designed to provide stakeholders with a summary of what was achieved in the financial year and an overview of our positioning and plans for the future.

Since our last report, every aspect of group activity has been reviewed and realigned around a revised corporate strategy. This represents a rediscovery of the original purpose of the organisation – to serve our members and their mutual communities. Our purpose has been updated to reflect and contend with a rapidly evolving social, economic and technological environment. In line with our core purpose, we have restructured our operations and sold off non-core business units (see page 37). This report outlines the changes we have made, and our plans for the future.

References to ‘BankservAfrica,’ ‘the company,’ ‘the group,’ ‘we,’ ‘us’ and ‘our’ refer to BankservAfrica and its consolidated subsidiaries, unless otherwise stated.

References to our shareholders, owners and members refer to BankservAfrica’s mutual ownership by the banking community (page 3). References to customers and stakeholders refer to those we serve either directly or indirectly. Our owners are also our customers.

Our annual financial statements (included in a separate publication) and our summarised annual financial statements (included in this report) cover all operations consolidated in terms of International Financial Reporting Standards.

More information about the company and our operations is available at www.bankservafrica.com.

ASSURANCEWe use a combined assurance model, matching key risks that affect the group with assurance obtained from management and other internal and external assurance providers. Management provides the board with assurance that it has implemented and monitored the group’s risk management plan, and that it is integrated into the daily activities of the organisation. These internal controls are the first line of defence, and include a dedicated internal audit team and programme to monitor control effectiveness.

Deloitte & Touche are our external auditors and provide external assurance on the group’s annual financial statements and an opinion on fair presentation. Their scope does not include any non-financial or operating indicators contained in this report.

STAKEHOLDER FEEDBACKWe welcome feedback on our report. Please direct any questions or comments and requests for copies to Wendy du Preez at [email protected].

AFRICA’S LARGEST PAYMENTSCLEARING HOUSE

2

Snapshot of BankservAfrica

We work with government, regulators, shareholders and other stakeholders to move the payments industry forward.BankservAfrica is the largest automated clearing house in Africa. We are authorised as a payments system operator by the Payments Association of South Africa (PASA) under the National Payment System Act. We build and operate South Africa’s core payments infrastructure.

BankservAfrica also defines, builds and operates other digital infrastructure to support African communities and economies.

We build mutual digital infrastructure that connects economies

OUR CORE PURPOSE

What this means

Mutual We collaborate within communities of members and users to create shared platforms that benefit everyone, building on multi-lateral relationships of trust.

InfrastructureWe focus on the networks of relationships and processes that support economic activity. These include business, legal and governance relationships, as well as technological networks and systems.

Connects economies Our mutual infrastructure supports competitive provision of financial services by our customers, and in doing so supports market economies, national economies and regional economies.

OUR TWO-YEAR STRATEGIC HORIZON FOCUSES ON DELIVERING EXCELLENCE IN THE

NATIONAL PAYMENTS INFRASTRUCTURE.

Business Report 2017

3

WHAT WE DO – OUR ROLE IN THE NATIONAL PAYMENTS SYSTEMThe group is a trusted partner to the South African financial services industry and is an integral part of the country’s National Payments System (NPS).We facilitate quality transactions in a regulated financial system that is compliant with international banking best practice and standards, while reducing risk and complexity in the industry.

Leading systems, infrastructure, tools and expertise have ensured that BankservAfrica remains the industry leader in electronic payment and information switching services.

The group’s operational abilities include:

» multiple electronic delivery capabilities;

» facilitation of connectivity;

» message management; and

» billing and compiling management information.Privacy, safety and security of transmitted and stored data is critical to all of these operational abilities and is managed and governed as a priority.

CERTIFICATIONS AND AFFILIATIONS » We are a level 2 certified broad-based black economic

empowerment (BBBEE) company.

» We successfully completed an assessment by Trustwave against the Payment Card Industry Data Security Standard V3.1 (PCI DSS V3.1).

» We are affiliated to the International Payments Framework Association.

All certificates and affiliations are available for viewing at www.bankservafrica.com

OUR OWNERSHIP STRUCTURE We are owned by the banking community and our mutual ownership supports our core purpose. We are not a profit-maximising company. We seek to create opportunities for profit for our mutual shareholders through cost-effective service provision.

Dandyshelf 3 (Pty) Ltd (Bidvest Ltd, Capitec Bank Ltd, Citibank NA South African, Investec Bank Ltd, Mercantile Bank Ltd, South African Bank of Athens, Sasfin Ltd and uBank Ltd)

FirstRand Investment Holdings (Pty) Ltd

The Standard Bank of South Africa Ltd

Nedbank Ltd

Absa Bank Ltd

23.125% 23.125% 23.125% 23.125% 7.5%

OUR FIVE-YEAR HORIZON GOAL EXPANDS THIS FOCUS TO DELIVERING EXCELLENCE IN REGIONAL

DIGITAL FINANCIAL INFRASTRUCTURE.

4

Business Report 2017

5

INDUSTRY OVERVIEW

Business Report 2017

76

Snapshot of the payments industry

The world is changing and so are payments systems. New user demands, new technology, competition, and regulation are all evolving. These drivers are bringing about more convenient, secure and faster ways of paying.A brief history of the payments system in South Africa1

1 Reference: Research performed by Leo Lipis Advisors, jointly commissioned by BankservAfrica and PASA.

1992 1

985 1

981

1

977

1

972

1

968

1

967

1

966 1793 1993 1995 1996 1998

200

0 20

03 2006 2010 2013

1793: The first bank in South Africa, Lombard Bank, is established in Cape Town 1993: Bankserv is founded in December to provide interoperability between participating banks

1966: Standard Bank obtains the franchise rights to Diners Club cards 1995: PASA is established in September

1967: Nedbank issues the first American Express gold card

1996: Internet banking services offering basic payment capability and statement enquiries is launched

1968: Barclays Bank Dominion, Colonial and Overseas (DCO) issues the first Visa branded Barclays card

1998: • Absa launches first franchised ATMs

• South African Multiple Option Settlement (SAMOS) goes live

• The NPS Act is promulgated

1972: The Automated Clearing Bureau (ACB) is established by the banks

2000: • Absa is the first bank to offer SMS mobile banking service with MTN

• Absa and FNB enables the purchase of MTN pre-paid top-up vouchers

1977: United Building Society (now Absa) launches the first ATM

2003: Europay, Mastercard and Visa (EMV) compliant POS terminals go live with Absa

1981: The first debit orders are cleared through the ACB2006: Banks implement prioritised collections or early debit order (EDO) payments

1985: The Saswitch system goes live 2010: South African Post Office/Postbank is the first non-bank to be designated

1992: The first electronic point of sale (POS) services are deployed 2013: All ATMs and POS terminals become EMV compliant

8

Snapshot of the payments industry (continued)

The existing South African payments system

South Africans primarily use four payment streams for low-value payments: cash, electronic funds transfer (EFT), card and cheques.

All the information shown above is a part of the research performed by Leo Lipis Advisors, jointly commissioned by BankservAfrica and PASA.

CASH

EFT

Cash currently dominates the payments culture in South Africa.

EFT remains a popular payment method.

The notes and coins in circulation in 2016 were on average R2 520 per person and almost R3 900 per working age population.

Notes and coins in circulation have increased in nominal terms in line with the gross domestic product (GDP) and amounted to R140.8 billion during the fourth quarter of 2016.

EFT credit payments made up 79% of the value of retail payments in 2016. This is a 70% increase from 2010.

The EFT payment system works well; however, little change has taken place over the past 25 to 30 years.

A need for reinvention of this payment method is evident. 22% of South Africans made purchases using EFT credit as their preference, while uptake of real-time clearing (RTC) payments remained poor.

The total value of EFTs processed increased from around R22 billion per quarter in 1989 to more than R2.4 trillion per quarter in 2016. This equates to an average value of more than R8 600 per 150 transactions in 2016.

More than 50% of the value of consumer transactions are completed with notes and coins, according to a recent Mastercard/Genesys study.

RR

The number of EFTs processed has

increased from under 20 million transactions per quarter in 1998 to over 280 million transactions per quarter in 2016.

INC

REASED

Business Report 2017

9

CARD Card payments are primarily used for frequent, small value purchases.

Card payments make up more than half of transaction volumes but only 7% of retail volumes in 2016. Card usage has increased from 45% to 56% of retail volumes since 2010.

Transaction costs remain a concern due to affordability for certain segments. In rural areas the lack of infrastructure, such as ATMs, means cards are not used for withdrawals. Despite the South African Social Security Agency (SASSA) introducing cards to increase financial inclusion, many South Africans still only use these cards for withdrawal of their full grant amount, and not for retail purchases.

The total value of credit card purchases has increased from around R1.3 billion per quarter in the late 1980s to an average of R80 billion per quarter in 2016. This equates to an average value of more than R570 per transaction in 2016.

Quarter four in 2016 saw the highest number of transactions at 147.8 million and largest total value of R85.9 million. This implies 2.6 transactions per capita during the quarter or 4.1 transactions per working age population.

The number of credit card purchases has

increased from around 20 million per quarter in the late 1980s to close to 140 million transactions per quarter in 2016.

CHEQUES Cheques are the least popular payment method in South Africa.

The use of cheques has reduced over the past 10 years, with most merchants not accepting this form of payment. Cheques make up 1% of the value of retail payments and 0.2% of the volumes. The South African Reserve Bank (SARB) has begun the process of eliminating cheques as a means of payment.

The value of cheques has decreased from a nominal peak of approximately R1.4 trillion per quarter in 1994, to just above R30 billion per quarter during 2016.

The value and number of cheques processed quarterly by Automated Clearing Bureau has

decreased from over 80 million per quarter in the 1990s to less than two million per quarter during 2016.

INC

REASED

DEC

REASED

10

1 https://www.statista.com/statistics/226530/mobile-payment-transaction-volume-forecast/, accessed 26 October 20172 http://fletcher.tufts.edu/CostofCash/~/media/Fletcher/Microsites/Cost%20of%20Cash/CostofCashStudyFinal.pdf, accessed 26 October 20173 https://blockchain.info/charts, accessed 26 October 2017

INTERNATIONAL PAYMENTS LANDSCAPEIn the developed world, existing payments models are seeing large-scale industry overhauls. At the same time, developing economies are building a new payments infrastructure as a platform to fast-track economic development. New payment solutions and unregulated environments require us to rethink the future and explore new risks and new opportunities for the economies we serve and for our current systems.

Payment evolution trends

Mobile payments: more consumers are using mobile phones as a means of payment. Worldwide mobile payment revenue is expected to surpass U$1 trillion in 20191.

Blockchain and Bitcoin: these cryptocurrencies have been unregulated until recently. Bitcoin faces an uncertain future as countries decide how to manage it, while blockchain is being explored for business uses.

The aggregate number of confirmed Bitcoin transactions was over 300 000 per day3 in 2017.

Biometrics: biometric authentication is being developed to identify the user and authorise the deduction of funds from a bank account.

Digital: payments made through digital modes are increasing, offering an instant and convenient way to make payments. Paper payment methods are in decline.

A 2013 study by Tufts University concluded that the cost of using cash amounts to around U$200 billion per year – about U$637 per person2.

Contactless payment systems: credit cards and debit cards, key fobs, smart cards, or other devices, including smartphones that use radio-frequency identification or near field communication to make payments, are being incorporated into the payment landscape.

Real-time payments: all over the world, developed economies are replacing daily batch payment systems with real-time systems that execute payments in seconds, carry richer data and are architected for flexibility to meet the needs of the future digital economy.

Snapshot of the payments industry (continued)

Business Report 2017

11

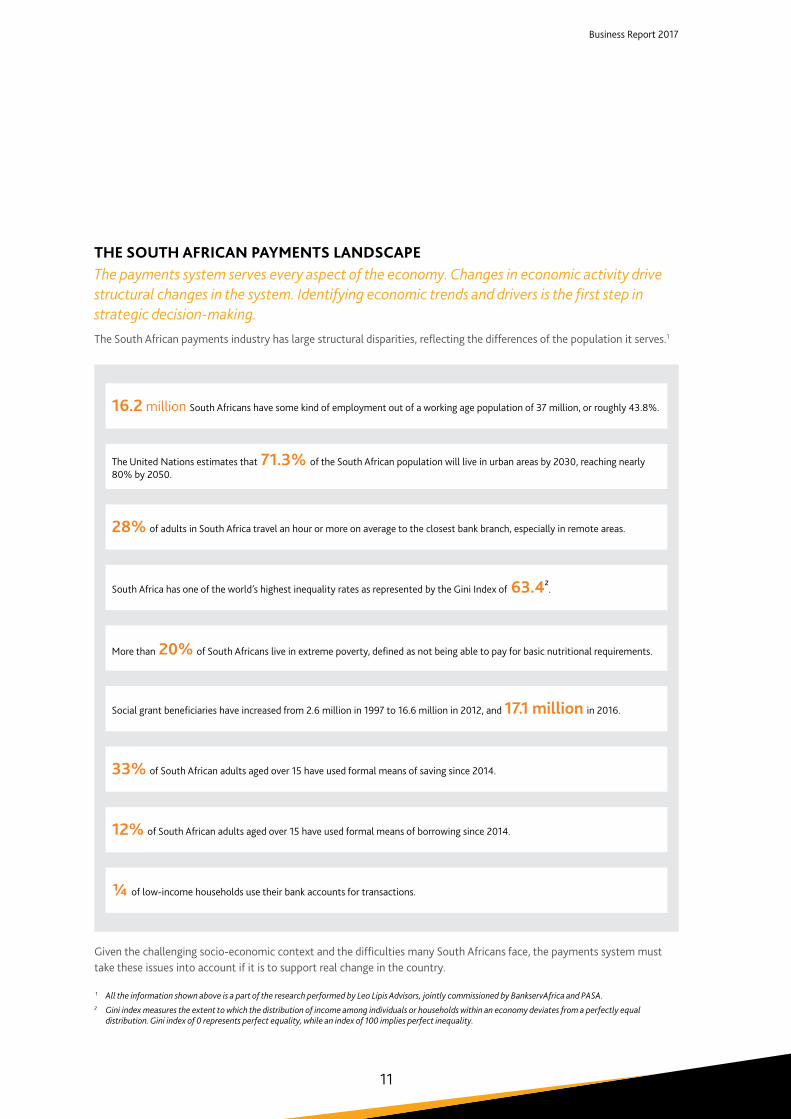

THE SOUTH AFRICAN PAYMENTS LANDSCAPEThe payments system serves every aspect of the economy. Changes in economic activity drive structural changes in the system. Identifying economic trends and drivers is the first step in strategic decision-making.The South African payments industry has large structural disparities, reflecting the differences of the population it serves.1

Given the challenging socio-economic context and the difficulties many South Africans face, the payments system must take these issues into account if it is to support real change in the country.

1 All the information shown above is a part of the research performed by Leo Lipis Advisors, jointly commissioned by BankservAfrica and PASA.2 Gini index measures the extent to which the distribution of income among individuals or households within an economy deviates from a perfectly equal

distribution. Gini index of 0 represents perfect equality, while an index of 100 implies perfect inequality.

16.2 million South Africans have some kind of employment out of a working age population of 37 million, or roughly 43.8%.

¼ of low-income households use their bank accounts for transactions.

The United Nations estimates that 71.3% of the South African population will live in urban areas by 2030, reaching nearly 80% by 2050.

28% of adults in South Africa travel an hour or more on average to the closest bank branch, especially in remote areas.

South Africa has one of the world’s highest inequality rates as represented by the Gini Index of 63.4².

More than 20% of South Africans live in extreme poverty, defined as not being able to pay for basic nutritional requirements.

Social grant beneficiaries have increased from 2.6 million in 1997 to 16.6 million in 2012, and 17.1 million in 2016.

33% of South African adults aged over 15 have used formal means of saving since 2014.

12% of South African adults aged over 15 have used formal means of borrowing since 2014.

12

In this rapidly changing environment, industry collaboration is pivotal to ensuring the evolution of a secure and convenient payments system.

The payments system of a country, and its payments clearing-house, are critical infrastructures for economic activity, and can be catalysts and enablers to economic growth. An efficient and appropriate NPS increases the ease of doing business and is indispensable to the functioning of the interbank, money, and capital markets.

Conversely, a weak payments system acts as a brake on the stability and developmental capacity of a national economy.

A RAPIDLY EVOLVING CONTEXTThe world is changing around us, driven by mass social change and new technology with unknown potential. The digital economy of the 21st century will change the way payments happen.

A national clearing-house is shaped by social, economic, regulatory and technological trends. Some of the trends that are likely to impact the economies in which we operate over the next few years include:

» Globalisation: As the world becomes increasingly interconnected cross-border linkages in Africa are likely to increase.

» Inequality and inclusion: Rising income and wealth disparity is the social issue of our era. Economic networks will be put under increasing stress as they struggle to meet all needs.

» Digital interconnectedness: Symmetrical growth in connected entities means an explosion in digital activity, including payments.

» Digital capital: Data will be the strategic asset of the next era.

» Cybersecurity: Cybercrime is on the rise as economies are digitised.

» Digital identity: The digital world requires new ways of establishing an entity’s identity online.

» Renewal of infrastructure: Digital infrastructure must be modernised to unlock value.

Industry volatility, social and public-sector needs, the emergence of new financial participants and the already saturated technology environment all make it likely that the payments industry will need to look at how to modernise the payments system to respond effectively to future needs and demands. While these issues present significant risks, the process of modernising the payments system presents many opportunities.

FINDING THE RIGHT SOLUTION FOR SOUTH AFRICADesigning a robust payments system to serve the current and future South African economy.Payments systems between and within countries are complex and serve different agendas and business needs.

Automated payments infrastructure for cards and EFT was architected in the 80s and has retained its basic shape ever since. New networks and technologies have been added over the years to improve service, manage increased volume and add new value. These systems are plumbed into banks, service providers, merchants and other enterprises of all sizes throughout the South African economy. Given this complexity, infrastructure redesign is costly, complicated and contentious. As a result, restructuring only takes place every 20 to 30 years.

The time for a new South African design is now. Many countries are on this path, and there is much to learn from overseas examples. Without structural change South Africa risks falling behind. Therefore, we need to holistically consider technological, social and political factors to provide a robust payments system that will serve the current and future South African economy.

The payments community will debate the objectives and design of a new national payments infrastructure in the coming year. Some key issues have emerged from research thus far, including the need for financial inclusion, digital enablement and regional extensibility.

Payments evolution through collaboration

Business Report 2017

13

It seems clear that the new payments system will need to serve the economically disadvantaged. This should encourage formal economic participation of under-represented and excluded citizens while also meeting the needs of wealthier, established segments. This is one way to address the social challenges the country faces.

There is also a need to future-proof our payments infrastructure by providing the flexibility to meet future needs as technology evolves - including needs we cannot yet see.

Finally, the prosperity of South Africa is tied to the prosperity of our region and our continent. Anything we design now must allow for cross-border use and the free flow of digital commerce to uplift our own and surrounding economies.

Well-designed payments systems have the potential to reduce friction in commercial and consumer payments, indirectly supporting economic development and financial inclusion.For the digital economy of the future, we need to start thinking creatively, applying an approach that is rigorous and inclusive for all.

WHERE WE ARE GOINGResearch and collaboration to streamline the payments industry.To address the changing payments landscape, PASA and BankservAfrica jointly commissioned a research programme aimed at reviewing international modernisation efforts and identifying practices and techniques that were successful or have failed. The goal is to apply these learnings to the South African payments industry.

We see this research as the basis of an extensive industry conversation about the payments landscape and the opportunity for payments modernisation in support of broader South African economic goals. We aim to leverage this research to create a collaborative environment for the public and private sectors to find common ground and agree on common goals.

We look forward to working with the South African Reserve Bank, PASA, our mutual owners and other stakeholders on developing a shared consensus for action on a new payments infrastructure.

At BankservAfrica, we believe there’s no substitute for industry players doing it themselves together. Co-created networks are always better than government-built networks or compliance-driven outcomes.

Streamlining the payments industry through a business-led process can be powerful and galvanising. It can radically reduce the cost base, while revolutionising the industry.

Business Report 2017

15

WHO WE ARE AND WHAT WE DO

16

Joint leadership review: Chairman and Chief Executive Officer

BankservAfrica processes close to three billion low-value interbank payment transactions each year with a value of approximately R8 trillion.

In South Africa, we have a 45-year history that includes several world firsts. These include Saswitch, same-day cheque clearing, real-time clearing (RTC), early debit order (EDO), electronic funds transfer (EFT), and the integrated cash management system (ICMS).

Using this core purpose to guide us, we have developed a strategy that will help us better serve our payments community. The thread running through this strategic blueprint is our emphasis on ‘mutuality’: stakeholder collaboration to develop infrastructure that supports our community and the economies we all serve. This is the bedrock on which we are building a world-class payments infrastructure.

For a strategy to be effective it must be lived in the organisation. We have spent a large amount of time as a team understanding the intricacies involved in achieving our strategic aims, unpacking BankservAfrica’s priorities, and planning how to operationalise these principles as part of our everyday work. Through this, we have created a roadmap that embodies and guides our direction, structure, and priorities and gives shape to the organisational restructure we underwent during 2016.

Our two-year goal focuses on achieving excellence in South African payments; our more ambitious five-year goal is focused on excellence in regional digital infrastructure. We understand that we need to enhance the trust and confidence of customers to achieve this, while developing a reputation for delivery. This is the commitment we make to our owners.

THE SOUTH AFRICAN PAYMENTS EVOLUTIONOur priority is on the projects addressing the challenge of payments modernisation. We consider this a ‘stay in business’ priority for BankservAfrica. It also has long-term implications for South Africa’s economy. We need to succeed in this process to avoid falling behind the world’s leading digital economies. Successful payments modernisation will provide the support South Africa needs for growth. A project of this size and impact requires world-class, large, industry-wide project management.

To keep up with the demands of business and consumers and the future payment needs of our economy, we must approach payments system modernisation scientifically, inclusively, holistically, and collaboratively.

The design process is critical and, as an industry, we need to find a way to navigate this fundamental change and do so systematically. System design doesn’t happen by itself, it needs intense collaboration.

We are proud of these achievements and excited about the path we are on – one that captures the technological innovation of the emerging digital economy and brings us full circle back to our original purpose: to build mutual digital infrastructure that connects economies.

Business Report 2017

CHRIS HAMILTONChief Executive Officer

MANNE DIPICOChairperson

CHRIS HAMILTONChief Executive Officer

MANNE DIPICOChairperson

17

18

We believe that co-created networks are more likely to succeed than government-built networks or compliance-driven outcomes. The base of good payments systems is empirical research that is inquisitive, inclusive, intentional, and gets business to lead.

DEVELOPING A SOLUTION FOR AFRICA BY AFRICAPayments infrastructure is the plumbing of every national economy, which makes it so important for regulators and financial institutions to get it right. It is critical that those involved understand the implications for success and failure in this arena – a well-designed payments infrastructure can fast-track economic development and financial inclusion on the continent, while unstable plumbing will hamper growth.

Africa is facing a ‘leap-frog’ moment. As economies develop, we have the opportunity to roll out modern systems that combine all of the best practices from global leaders without the legacy issues. We are aware that the challenges in Africa are vast and unique and that a one-size-fits-all approach does not work for payments systems.

We look forward to engaging with our African peers as we work towards forging a shared vision to develop African economies through a regional payments system that harvests Africa’s potential.

CONCLUSIONBankservAfrica is midway through a shift from commercialisation and diversification to mutuality and infrastructure. A change of this size impacts all aspects of the business. Alignment and coordination are critical. We need to successfully negotiate that shift and establish the trust of stakeholders and their belief in our ability to deliver change, then the objectives we have set for ourselves become achievable.

We extend thanks and gratitude to our board for their contribution, guidance and support as we have realigned BankservAfrica to its core purpose.

On behalf of our leadership team, we also thank our BankservAfrica team. The last 18 months have seen a significant amount of change within our business as we found our way back to our core purpose and then worked together to understand how best to structure ourselves to meet our goals in terms of our purpose. We have been asking ourselves difficult questions and making big changes in the business, all to better serve our stakeholders. The level of engagement and commitment from the BankservAfrica team has been inspiring. Thank you for your dedication and passion in moving us forward.

To our payments community members, we are excited about the year ahead and look forward to working with you to move South Africa and the African continent forward.

Manne Dipico Chairperson

After nine years of service as Chairman of the board, Manne Dipico has decided to retire in 2017. The Board thanks Manne for his leadership and commitment to BankservAfrica and the communities we serve. We wish Manne well for the future.

Chris Hamilton Chief Executive Officer

Joint leadership review: Chairman and Chief Executive Officer (continued)

Business Report 2017

19

LEADING: BankservAfrica is the industry leader in building digital payment infrastructure solutions that connects economies through electronic payment and information switching services.

20

Our leadership

1.

2.

3.

4.

5.

6.

7.

8.

9. 10.

11.

12.

Inde

pend

ent n

on-executive directors Non-executive directors

Executive directors

Board

Business Report 2017

21

INDEPENDENT NON-EXECUTIVE DIRECTORS 1. Dr Manne Dipico (58), ChairpersonKey skills

Leadership and decision-making Communication

Negotiation Analytical

Creative thinking Conflict resolution

Appointed to the board in November 2008. Became chairperson of the board in September 2010.

2. Henri Slabbert (61), Chairperson of the technology board subcommittee and member of the audit board subcommitteeKey skills

Audit IT

eCommerce Payments

Strategy Research

Appointed to the board in November 2007.

3. Dr Yvonne Muthien (60), Chairperson of the human resources and social and ethics board subcommitteesKey skills

Ethics GovernanceStrategy ResearchProblem solving Results orientation

Appointed to the board in June 2014.

NON-EXECUTIVE DIRECTORS4. Francis Brand (54)Key skills

Finance Governance

Human resources Legal

Risk management Change management

Appointed to the board in June 2014.

5. Matthew Coaker (54)Key skills

Regulation Problem solving

Analytics Banking (ATM, batch, EDO, AC)

Payments Strategy

Appointed to the board in June 2009.

6. Larry Mccarthy (46)Key skills

Finance Governance

Negotiation Payments

Strategy Private equity and investment banking

Appointed to the board in November 2015.

7. Vusi Ndwandwe (36)Key skills

Finance Governance

Analytics Economics

Payments Operations and planning

Appointed to the board in October 2016.

8. Ravi Shunmugam (44)Key skills

Risk management Problem solving

eCommerce Payments

Operations and planning Strategy

Appointed to the board in June 2016.

EXECUTIVE DIRECTORS9. Peter Scaife (69), Deputy chairperson, chairperson of the audit board subcommittee and member of the social and ethics and human resources and technical board subcommitteesKey skills

Retail and corporate banking International finance

Foreign exchange and Merchant banking andtrade finance offshore trusts

Audit, risk and compliance Cash, Cheque, Card and Electronic Payments

Appointed to the board in 1999. Reappointed in March 2008.

10. Chris Hamilton (53), Chief executive officer of BankservAfricaKey skills

Business strategy Leadership

Decision-making Payments

Banking Risk management

Appointed to the board in June 2016.

11. Parusha Gajathar (38), Chief financial officer of BankservAfricaKey skills

Financial management Governance

Ethics Risk management

People management Operations management

Appointed to the board in March 2016.

12. Emile Burger (44), Chief operations officer of BankservAfricaKey skills

Payments Technology

Banking Operations and planning

Organisational efficiency People management

Appointed to the board in March 2016.

22

Our structure

To better serve our clients and the economies we operate within, we have restructured our business this year. Our new company structure is a matrix, with the reporting relationships set up as a grid rather than in the traditional hierarchical sense. We believe this allows us to address customers’ needs now and into the future, while ensuring we leverage capabilities to drive efficiencies and innovation.

Control Support Deliver Define Present

Support Services

Page 36

Ensures that the delivery of products and services to customers is executed in a governed and compliant manner

» Corporate Integrity

» Internal Audit

» Legal Services

» Human Capital

» Finance

» Procurement

Supports the strategic portfolios to deliver what is required by the customer and the BankservAfrica product teams

» Operations

» Network

» Platform

» Applications

» Security

Technology and

Operations

Page 32

Delivers against our core purpose. We have realigned our business around five strategic portfolios, namely:

» Digital Infrastructure

» Retail Payments

» Information Services

» Regional Engagement

» Enabling Services

Strategic Portfolios

Page 24

Stakeholder communities served by

Business Report 2017

23

SPECIALIST: BankservAfrica provides interbank switching, clearing and settlement services to the banking sector through five strategic business portfolios.

We have realigned our business around five strategic portfolios, namely:

1. Digital Infrastructure The traditional core of our business, taking care of our payments services including EFT, RTC and EDO.

2. Retail Payments Covers card services, including 3D Secure. This area will consider how card services should strategically evolve to best serve

our market.

3. Information Services A business unit provides value-adding information rich services using core infrastructure. Information Services

includes transactional fraud mitigation (TFM), MIS Cognition and RiskNet Card Fraud Services.

4. Regional Engagement Considers opportunities to offer services to new communities of customers on the African continent

with a focus on the SADC region.

5. Enabling Services Offers customers a range of products and services that provide end-to-end solutions in the field of data

digitisation and data management.

Strategic portfolio overview

24

Business Report 2017

25

The business looked inwards and aligned our operations to our core purpose.It is my pleasure to present our first strategic portfolio review. Our newly formed strategic portfolios represent the customer-facing part of our business. It is an amalgamation of our previous products and services, aligned and adjusted to support our future ambitions. Each of these businesses offer value to our communities by creating an internal focus to deliver on our core purpose. However, they face strategic challenges in the future as the payments landscape continues to evolve.

Our Digital Infrastructure portfolio is the traditional core of the current business, taking care of many of our payments services. This business will face a challenging period and will need to work with other industry participants to understand how to deliver the next generation of South African payments infrastructure.

Our Retail Payments portfolio covers card services, including 3D Secure. We are focused on engaging with our members to agree on a way forward for South Africa taking into account the global changes underway in card services.

Our Information Services portfolio provides value-adding offerings using our core infrastructure. An example is the current launch of the first-of-its kind TFM service. We see potential for more offerings in the future.

The Regional Engagement portfolio is focused on serving customers and economies on the African continent. This will help to strengthen leadership, collaboration and capacity. We have a vision of supporting the payments infrastructure across the SADC region in support of the SARB and our stakeholders.

Lastly, Enabling Services offers our customers a range of products and services that provide end-to-end solutions in the field of data digitisation and data management.

Our portfolios are supported by sound delivery platforms – Operations, Network, Platform, Applications and Security – that give ‘legs’ to the market-facing functions.

South Africa is regarded as an innovation hub. Our banking infrastructure is sound, efficient and sophisticated. We have led the way in Africa in payments infrastructure, data provision and analytics. The digital landscape is evolving at unprecedented speed, offering risk and reward opportunities. Our stakeholders’ expectations are high and they expect reliability, balanced with future adaptability and integrity.

We believe our new purpose and structure will enable us to deliver a sound customer and stakeholder value proposition for Africa keeping this challenging context in mind.

Overview from Martin Grunewald: Acting Chief Payments Officer

26

ATM

Debit card (POS)

Credit card authorisations (POS)

Credit card clearing and settlement (POS)

EFT credit

EFT debit

AEDO

RTC

NAEDO

Zaps

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

12 000 000

2016 –2017

2015 –2016

2014 –2015

2013 –2014

2012 –2013

2011 –2012

2010 –2011

2009 –2010

2008 –2009

2007 –2008

2006 –2007

2005 –2006

2004 –2005

2003 –2004

2002 –2003

CLC

Transaction values (million)

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2016 –2017

2015 –2016

2014 –2015

2013 –2014

2012 –2013

2011 –2012

2010 –2011

2009 –2010

2008 –2009

2007 –2008

2006 –2007

2005 –2006

2004 –2005

2003 –2004

2002 –2003

Transaction volumes (million)

ATM

Debit card (POS)

Credit card authorisations (POS)

Credit card clearing and settlement (POS)

EFT credit

EFT debit

AEDO

RTC

NAEDO

ZapsCode line clearing (CLC)

Overview from Martin Grunewald: Acting Chief Payments Officer (continued)

Business Report 2017

27

Digital Infrastructure

WHAT WE OFFERKey products and services Description

Electronic funds transfers (EFTs)

Offers bank account to bank account credit transfer clearing management, and same day transfer request or pre-dated transfer warehousing. The service also calculates bank-to-bank settlement and reconciliation.

Code-line clearing (CLC)

An electronic cheque clearing facility that receives and validates cheque code line data from acquiring (collecting) banks and forwards settlement information to the treasury departments of the issuing (homing/paying) banks to the SARB.

Physical cheques are matched overnight with electronic data overnight and dispatched to the respective issuing banks early the following day, while an image repository facilitates quick query resolution.

Early debit order (EDO)

A bulk collections processing service, with the major benefit being to improve payment ratios. The system caters for debit order requests and facilitates randomised EDO collections within the banking systems. The service is known as ‘early’ as it processes these collections immediately after salary credits, thereby allowing for a better chance of payment fulfilment.

Real-time clearing (RTC)

Allows customers to move single credit payments in real-time to beneficiaries 24 hours a day, seven days a week, and 365 days a year.

This real-time clearing system is integrated with the central bank settlement service which supports multiple settlement windows and includes the ability to force settlement when a participating bank’s daily exposure limit is reached.

Account verification service (AVS)

The account verification batch service is utilised to achieve greater levels of efficiency and as an additional fraud prevention measure by ensuring that bank account details match recipient identity details. Customers are able to verify account information using the account verification service batch service, allowing end users to avoid unnecessary charges for attempting to process payments to non-existent accounts.

Integrated cash management (ICMS)

Automates the supply chain of wholesale physical cash at a national level. This improves the control of cash in circulation by banks and central banks and removes duplicated functions while adding efficiency to the remaining functions.

Highlights

» All service level agreements (SLAs) were met and delivered.

» We launched a modernisation research programme with PASA.

» Our authenticated collections solution was developed and progressed into pilot stage as scheduled.

» The structural consolidation of payments and collections services were implemented.

» The integration of the managed network services portfolio was integrated into the Digital Infrastructure business.

» We consolidated our payments and collections services into discrete portfolios, while the managed network services portfolio was absorbed into the Digital Infrastructure portfolio.

Challenges

» Managing the operational risk posed by the modernisation project to our IT architecture methodology.

» Ensuring all businesses are aligned and that there is clarity on joint and separate responsibilities following the restructure.

Looking forwardWe will review and rationalise current portfolios and associated resource structures, ensuring we have the right capabilities. We intend to introduce a research team to support and formalise our thought leadership goals.

We will continue to standardise services and improve perceived value to critical stakeholders. We will do this through better business intelligence and non-contradictory account management, and through appropriate pricing of services.

We are committed to participating in industry-focused discussions on the future of the payments landscape – a priority for the business.

28

Retail Payments

WHAT WE OFFERKey products and services Description

ATM switching and settlement

Enables clients of any participating bank to draw money from ATMs belonging to any other participating bank, for credit and debit cardholders.

In-country card payments switching service

Allows a country to host its own card payments infrastructure to switch, clear and settle card payments on point-of-sale (POS) and cash withdrawals from ATMs belonging to banks other than the cardholder’s bank. This enables interoperability between banks.

Card not presentAllows for secure internet shopping for buyers (cardholders) and sellers (retailers). This is done by enabling card issuers to verify a cardholder’s registered PIN online and provides results to the merchant/retailer in real-time during the checkout process.

Debit card

SMS service facilitates interbank debit card transactions at POS and includes the provision of automated billing, management information and access to a reliable processing infrastructure. Our system is key in transmitting the transaction to the merchant’s bank, which passes the transaction to BankservAfrica to route it to the issuing (customer’s) bank for authorisation.

Credit card clearing and settlement

Credit and debit card services and facilitated interbank clearing and settlement of card transactions processed at POS for all types of credit and debit cards. This includes automated billing, management information and statistical data reporting and access to a reliable card processing infrastructure.

BIC ISO translation Translates real-time messages from international card schemes format to BIC ISO format and back.

International scheme routing Routes messages to and from UnionPay International, VISA and MasterCard to local banks.

Credit card authorisationProvides credit and debit card authorisation services and facilitates interbank authorisations of card transactions processed at POS.

Highlights

» We recorded fewer system disruptions and high levels of system availability.

» Pleasing progress has been made on the card payment tokenisation project, with approval granted to run a proof of concept with one or more participants.

» The business exceeded revenue targets and volume growth thanks to the enhancement of its product portfolio and investment in technology infrastructure, which included an IT hardware overhaul (see page 34 for more information).

» We completed the migration to a 3D Secure environment, resulting in lower client costs, improved reliability and risk-based levels of authentication.

» To achieve our goal of SLA 100, a managed network service continues to be rolled out to our South African network users.

Challenges

» A deteriorating economic landscape poses a challenge to customers.

» The increased competition and a need to reduce costs of services while expanding service offering and improving efficiencies remain difficult.

Looking forwardAs the digital economy advances at speed, the Retail Payments portfolio looks to the future, in which real-time retail payments, within a secure environment and decreasing fraud, is emboldened through a blueprint. We continually evaluate our core and value-added services to enhance customer experience and accommodate regulatory requirements.

BankservAfrica is building infrastructure to support service providers who wish to use tokenisation to further secure card numbers on mobile devices and merchant databases.

The portfolio seeks to ensure universal access to the retail payments infrastructure to promote reliability, security, competition and innovation in South African retail payments.

Business Report 2017

29

WHAT WE OFFERKey products and services Description

MIS CognitionCognition is an internal and external data analytics service that provides insights, statistics and trends through online application services.

Transactional fraud mitigation (TFM) services

TFM is a newly designed and launched near real-time transactional fraud monitoring service. It profiles and alerts interbank transactions on EFT, RTC and early debit order/non-authenticated early debit order data streams.

RiskNet card fraud services RiskNet is a hosted card fraud solution.

Information Services is a data-driven business focused on the provision of value-added services derived from the NPS. It enables business, regulators and the banking community to make informed decisions across multiple verticals, channels and platforms. The portfolio is focused on data-driven analytical services split across business analytics and fraud detection services. The team publishes economic trend indicators for the industry, including:

» the BankservAfrica Economic Transactions Index (BETI), which is the broadest and earliest business cycle indicator on the economic calendar and gives the fastest overview of South African growth trends;

» the BankservAfrica Disposable Salary Index (BDSI), which monitors how much cash salaried consumers have at their disposal and is released quarterly; and

» the BankservAfrica Private Pensions Index (BPPI) which provides an income gauge of monthly private pension payments paid into bank accounts of those 60 years of age and over.

For more information on these economic trend indicators, please see www.bankservafrica.com

Highlights

» We launched the TFM service, a global-first strategic project with over 100 million transactions processed, that alerts fraudulent transactions.

» Our ATM project is in pilot phase to enhance data integrity, POS online and settlement procedures in the pipeline.

» Significant advancement towards the launch of a global-first national profiling and alerting service was made.

» Upgrades to increase analytical capabilities and introduce data modelling and design were completed.

Challenges

» Attracting and retaining the necessary skills remain challenging, with large-scale projects requiring additional technical skills and capacity.

Looking forwardInformation Services will focus on building on the successes of 2017 to establish the business as the provider of data-driven analytical services. Analytics-as-a-service and TFM across channels and platforms are new opportunities. These will be explored as digital disruption speeds up discussions around data-sharing capabilities and the modernisation of payments. Real-time digital identity and fraud profiling and alerting will become paramount to protect banks and consumers.

Information Services

30

WHAT WE OFFERKey products and services Description

Regional clearing house (RCH)

Provides efficient processing of high-volume day-to- day, low-value payments. Providing oversight and interoperability, the cost-effective and reliable service ensures the secure movement of money across borders.

Democratic Republic of Congo (DRC) card switch

The card switch in the DRC offers interoperability at ATMs and POS terminals. The project supports ATM and debit card transactions.

The Regional Engagement business is focused on efforts to strengthen leadership, collaboration and capacity within the African geographic footprint. Regulatory compliance and a zero-tolerance commitment to ethics underscore the activities within the SADC.

On a practical level, the Regional Engagement business acts as a regional clearing-house that ensures the efficient processing of high-volume, day-to- day, low-value payments. The business provides oversight and interoperability for secure, time-sensitive, cross-border transactions.

Critical to the success of this business is a transparent engagement with officials at the helm of central banks, in-country banks, banking associations and industry associations.

Highlights

» We implemented a unified Africa strategy, aligned to the group’s core purpose, moving from sales to supporting countries and economies.

» We advanced our approach to modernise African payments infrastructure, thereby making a grassroots contribution to the economic growth of fast-growing regional markets.

» The card switch in the DRC recorded a steady monthly volume increase, reflecting market acceptance of ATM interoperability and POS terminals.

Challenges

» Regulatory bottlenecks in unstable economic and politically volatile markets continued to hamper growth.

» Attracting and retaining critical skills and competencies remain challenging.

Looking forwardThe Regional Engagement business will continue to work with its partners and members to design and adopt a sustainable payments infrastructure across the region that supports all payment types.

Proof of concept and compliance for this cross-border initiative is a priority during the 2018 financial year.

Regional Engagement

Business Report 2017

31

WHAT WE OFFERKey products and services Description

Electronic bill payment and presentment (EBPP) solution

Allows banks’ merchants to present bills and banks’ customers to pay them on the internet. This is done via a pre-formatted system that does reconciliations and invoicing.

Society for Worldwide Interbank Financial Telecom-munication (SWIFT) services

Offers the global financial community a highly secure and reliable network to exchange electronic financial messages. BankservAfrica operates a SWIFT bureau for customers across Africa, reducing their infrastructure and support costs while providing certainty of processing and required levels of security.

Back office outsourcing Offers reduced costs for cheque processing through innovation and economies of scale.

Business process automation

Offers a comprehensive document imaging and management services that automate client business processes digitally. In lowering costs and optimising the security, storage, access and management of your information, our solutions enable compliance with the evolving legislation governing this key business function.

The Enabling Services strategic portfolio offers customers a range of products and services that provide end-to-end solutions in the field of data digitisation and data management. Repositioned and streamlined, this division recognises digital data as a key strategic asset for customers, helping them to protect and grow their market share and competitive advantage.

We seek to add value to payments instructions by providing solutions to customers which incorporate reliable, digital platforms and applications operating on common infrastructure.

Our goal is to create operational effectiveness and efficiencies through digitisation, common infrastructure and process improvements.

Highlights » The business gained traction in the provision of technical support via work flow improvement and process improvement advice to an

increasingly discerning, cost-sensitive and security-conscious client base.

» We successfully concluded the disposal of our contact centre services.

Challenges » Ensuring the business unit remains profitable post-restructuring is a priority.

» Obtaining consensus support for our Financial Intelligence Centre Act (FICA) solution is ongoing.

Looking forwardWe will ensure that we promote the role of the newly formed Enabling Services division and reconcile direct sales targets with our core purpose and mutuality.

We are working on a FICA solution that offers client screening and validation for accountable institutions. This will include proof of the client’s existence and an audit trail of verifications performed by accountable institutions. There is a request for proposals underway and once finalised, the solution will be built, incorporating best-of-breed commercial features.

We will drive strategic projects, such as the FICA solution and EBPP forward, while seeking operational efficiencies wherever possible.

Enabling Services

The Technology and Operations division supports the strategic portfolios to deliver what is asked for by customers and the BankservAfrica product teams.

1. Operations Day-to-day customer support, helpdesk and support services to orchestrate the flow of transactions.

2. Networks Networks facilitate and enable seamless inter-site routing through overlay transport virtualisation.

3. Platform Our physical and virtual computing infrastructure hosting the associated operating system

and management tools.

4. Applications Creation of the most optimal, supportable environment with the lowest risk exposure.

5. Security Monitoring and managing risks in our day-to-day business.

Technology and Operations overview

32

Business Report 2017

33

Overview from Emile Burger: Chief Operating Officer

To us, mutuality does not just mean connecting technology; mutuality is about creating the ecosystem that serves our stakeholders.

BUILDbuild new

FIXrebuild trust

In 2017, we focused on building the following services:

» Authenticated collections

» TFM

FOCUS ON THE 3 RsIn 2017, we focused on building:

» Resilience

» Responsiveness

» Reliability

FOCUS ON THE 3 Es Post-2017, we will focus on:

» Excellence

» Execution

» Enablement

Post-2017, we will focus on:

» Capacity management

» Continuous improvement

Shift of effort and focus over time

Underpinned by governance and security

2017

Post

-201

7

BIMODAL APPROACH

34

applications, databases, network and the way that it all interacts with each other. This was done without having any down time.

Data is our currency. Therefore, protecting the integrity of data is our priority. We have created multiple failure points, introducing a level of redundancy within our systems. This has resulted in improved network speeds and connectivity between our two sites. Furthermore, we have enhanced the resilience and reliability of the system due to these changes – reducing recovery time from four hours on average to a few seconds.

I believe we now have best of breed across all possible elements of our system – a world-class platform.

We have started to move away from monitoring whether a system is available, to whether a service is available. Having a system available means that the application is working, but it does not mean that a customer can transact. To address this, we are focusing on providing an end-to-end monitoring and managing service, not application availability. We have started the journey and made good inroads, but I believe we have some ways to go to entrench this mutuality mindset.

We are striving to foster mutuality throughout our business, from the services we provide to the way we resolve problems. We are committed to ongoing and proactive engagement between ourselves and customers, and between industry participants focused on sharing best practices.

Looking forward, our focus will change from the three Rs to the three Es – excellence, execution and enablement. We will still address capacity management and continuous improvement through our three Rs. However, we now have a platform that can support bolder long-term ambitions.

For the year that lies ahead, under the three Es, our focus will be on building a bigger portfolio of capabilities to support our strategic portfolios. The payments modernisation programme, tokenisation, card not present enhanced capability, and fraud mitigation are some of the projects we are looking at as we transition from legacy issues to future proofing our business.

Overview from Emile Burger: Chief Operating Officer (continued)

Our Technology and Operations business unit is a key component in how we meet our stakeholder mandates. The division looks after the interconnected areas of Operations, Networks, Platforms, Applications and Security. These carry sensitive payment information, and in future will carry other forms of complex information.

As an integral part of the payments system, one of the challenges we face is how do we plan and coordinate the process to address the existing issues in a system, while at the same time building for future requirements – without disrupting the services offered to customers.

To address this, we adopted a bimodal approach to our infrastructure projects. This has allowed us to manage two approaches: one focused on fixing current and legacy issues in our architecture, and the other focused on building our offerings and future proofing the business so that we can support customers going forward. We believe that in time, the balance of effort will move away from fixing towards building.

One of our strategic priorities is to enhance trust with our stakeholders. For us, trust means that our stakeholders have a belief in the reliability and availability of our systems to help them deliver to their clients. To do this they need to rely on us as an integral part of their businesses. Our primary focus is on fixing our existing system to rebuild this trust while we continue to build new offerings.

Our efforts are to address legacy issues centred around a programme we called ‘the three Rs’, namely building resilience, responsiveness and reliability into our operations. This embodies the qualities we believe must be entrenched in our operating environment. To create an environment that embodies these qualities, I need to borrow a metaphor from Chris, our CEO: “if we at BankservAfrica are the plumbing of the economy, we had to reinforce the plumbing”.

The purpose of the three Rs programme was to strengthen Operations, Networks, Platforms, Applications and Security. This had to be done while taking into account the changing payments and the competitive and economic landscape of South Africa. This enormous undertaking was conducted in stages to minimise disruption. Ultimately, we refreshed our entire ecosystem, including infrastructure,

Business Report 2017

35

MODERN: BankservAfrica is focused on modernising transactional payment digital infrastructure networks, improving service levels, investing in strategic industry projects and expansions into Africa.

Ensuring the delivery of products and services to customers is executed in a well governed, compliant manner.

1. Corporate Integrity Responsible for overseeing risk, compliance, BBBEE, occupational health and safety (OHS) and ethics, and providing an integrated view on risk.

2. Internal Audit Provides an independent and objective assessment of the governance, risk management and control processes within BankservAfrica.

3. Legal Services A cross-cutting enabler that ensures that day-to-day operations are appropriately supported while offering thought leadership on

current and impending legislation.

4. Human Capital An enablement function, helping the business reach its strategic goals by attracting and retaining

specialist skills.

Support Services overview

36

Business Report 2017

37

We believe our reorganised Support Services team will bolster BankservAfrica by offering leaner and more specialised support functions to enable the group to achieve its ambition of being a leader in payments and transactions.2017 marks my first financial year with BankservAfrica as Chief Financial Officer. This year was characterised by a substantial amount of internal change as we aligned the business with its five-year strategy.

From a Support Services perspective, we have restructured several of our operations and added new functions, such as our Legal Services team, to ensure that we have the capabilities that meet our ambitions.

Restructuring can be challenging; however, it presents us with an opportunity to reflect on better ways to work. In the past, we had multiple groups responsible for governance, risk and compliance functions. Many of these teams worked in isolation, struggled to share information and had multiple frameworks and systems. This resulted in inefficiencies and hampered our ability to get a clear view of risk.

To address this, the Corporate Integrity function was created, responsible for overseeing risk, compliance, BBBEE, OHS and ethics. By integrating functions, we enhanced our ability to understand risk and thus grow and protect value.

We continued to streamline our balance sheet and rationalise business activities that did not support the new strategy. To that end and subsequent to year end, we disposed of our call centre, and the non-call centre business units part of BSVA Integrated Services (Pty) Ltd were transferred into South Africa Bankers. This was effective as of 30 June 2017. We have found reporting to be quicker and easier with the balance sheet simplified. This has allowed us to access information faster.

To address risks arising from increasing volumes and ageing legacy systems, we refreshed our core infrastructure to ensure reliable service delivery and to improve our resilience in supporting the South African economy.

Overview from Parusha Gajathar: Chief Financial Officer

We have since integrated these functions to enable BankservAfrica to define its principles and goals, determine how it will address risks and uncertainties, and grow and protect value.

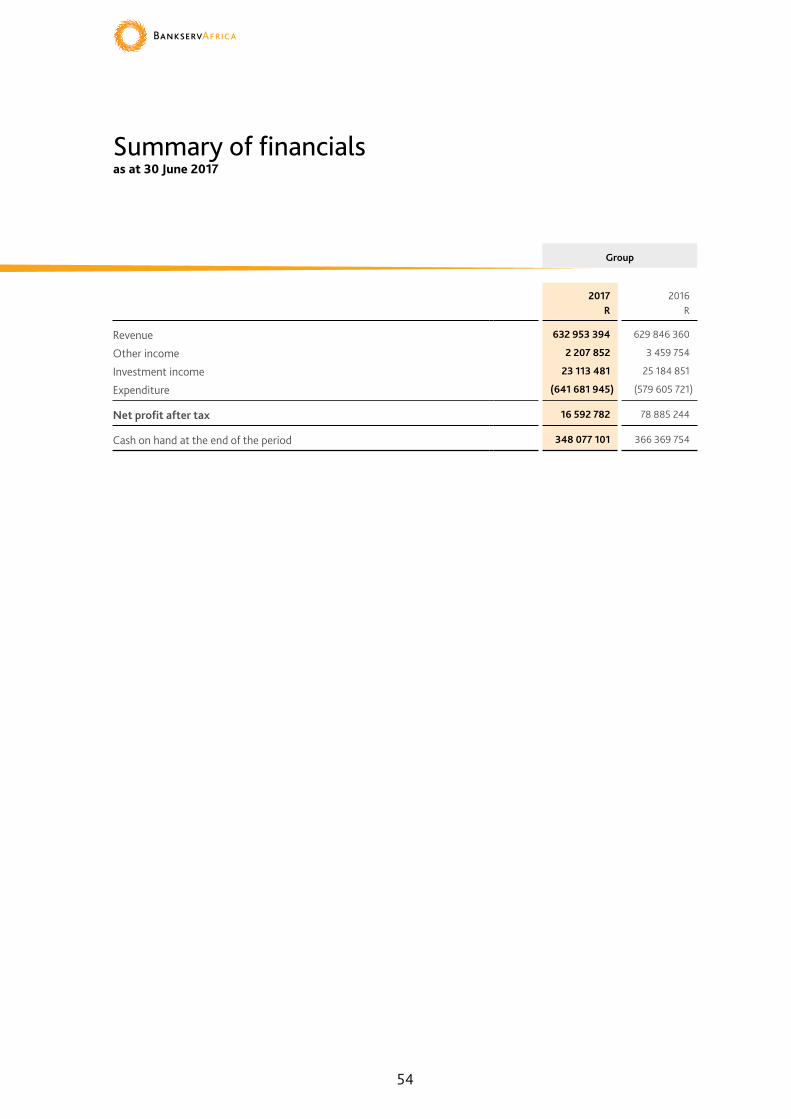

In line with our mutual approach, we did not pass on any significant price increases to our clients. In fact, most increases were inflationary and in certain cases, like 3D Secure, we were able to pass on savings to our customers. Total revenue for the year was in line with the comparative period; the significant growth in volumes from our EFT and card services was off-set by lower than expected new business growth in Enabling Services. Digital Infrastructure and Retail Payments were our strongest revenue earners, contributing 47.9% and 34.4% respectively.

While our revenue remained in line with 2016, our costs increased significantly, resulting in decreased profitability. Total expenses (including operating expenses and impairments) increased by R111 million (22%). Our investment in our IT refresh has not only significantly changed our balance sheet over the last 18 months, but also negatively impacted our income statement. This is due to the effects of depreciation (44% up on the prior year) and computer-related charges (up 27% on the prior year) which hampered profitability. Staff costs increased by 14% to R38 million. Above normal salary increases reflect our investment in the skills base we need to operationalise key projects and priorities.

As a result of this, BankservAfrica produced a net profit before tax of R34 million. This is a decrease of 73% from 2016. While this is a large decrease, it’s in line with the business’s intention not to focus on profit maximisation.

We believe we add value by enabling our members’ businesses. This means that we are interested in financial sustainability over the long term, not profit maximisation. We would rather see benefits to our stakeholders multiply as the network expands and adds more value for users. Looking forward, we will continue to drive efficiencies, sustainability and reliability to better serve our customer base.

We encourage our readers to refer to our summarised annual financial statements on page 49 for more information.

38

Corporate Integrity

GOVERNANCEBankservAfrica is committed to the standards of good corporate governance and mindful compliance, as is envisaged by the King IV Report on Corporate Governance for South Africa, 2016 (King IV). The board applies the sentiment that the King Code recommends to achieve the four cornerstones of good governance: fairness, transparency, responsibility and accountability.

The board has an overarching corporate approval framework to provide certainty and any limitations on the authority and powers within the BankservAfrica Group. This includes a summary of the powers and authorities of the shareholders, the board, the delegation of authorities and the authorities of its committees and the executive.

We believe that good governance adds value to the business by enhancing transparency and accountability, ensuring effective leadership and decision-making.

Governance is also concerned with sustainable development. We actively promote and support corporate social investment initiatives to ensure we remain a responsible corporate citizen.

Highlights

» Our new company strategy was approved, with a two-year horizon focused on delivering excellence in the national payments infrastructure. Our five-year horizon goal expands this focus to deliver excellence in the regional digital financial infrastructure.

» The board appointed new independent auditors, Deloitte & Touche.

Challenges

» Ensuring a greater focus on alignment to industry standards is ongoing.

Looking forward

The governance support service will be aiming for 100% policy alignment and compliance.

We will roll out our board evaluation programme and will use the feedback to improve governance practices and processes. We will also continue to create more awareness of the importance of good governance in the organisation.

Business Report 2017

39

RISKWe recognise that sound risk management increases our customers’ confidence in us as a trusted partner. As such we are committed to managing risks through the continual improvement and implementation of best-practice risk management policies and frameworks relating to enterprise risk management and business continuity management.

The board and its subcommittees oversee the implementation of risk management and monitor its performance. The committees review development and maintenance of the external and internal controls that are in place to ensure that identified risks are effectively managed. Our enterprise risk management and business continuity management frameworks deal with risk philosophy, methodology, strategies and processes. These frameworks are reviewed annually by these committees. The committees satisfy themselves that the nature, intent and effectiveness of the risk control infrastructure within BankservAfrica are adequate and effective.

Highlights

» We streamlined policies, processes and structure to focus on our core businesses and reassess risk for non-core operations.

» The implementation of the business continuity work plan progressed with facilitated training and simulated emergency scenarios conducted.

» Risk reporting was streamlined across all operations with the development of key risk indicators, increasing the understanding of the risks the business faces.

Challenges

» Enhancing the understanding of risk and embedding a risk culture ethos across the group.

» A shortage of appropriate talent and skills exacerbates human capital mapping.

Looking forward

In collaboration with the Corporate Integrity function, the risk committee will take on a more proactive role in risk management. We will continue to address the risks that are outside of the BankservAfrica risk tolerance level as a matter of priority. We will also attempt to reduce risk within the tolerance level or appetite. We will align business continuity management and disaster recovery practices following IT refresh.

40

COMPLIANCEOur compliance function ensures that the organisation implements an effective compliance and robust policy framework. BankservAfrica complies with applicable laws and binding regulations. We comply with South African company law and with those laws and regulations laid out specifically by PASA and the SARB. The compliance function considers adherence to:

» non-binding rules;

» standards and codes according to the shareholder mandate;

» constraints set out in the memorandum of incorporation (MOI); and

» together with its obligation to all stakeholders as set out in the prevailing regulatory, legislative and King IV requirements.

Highlights

» We once again attained authorisation as a payment clearing-house system operator.

» The annual reviews on the company’s MOI were completed.

» We submitted our annual employment equity report to the Department of Labour.

Challenges

» Moving towards an integrated and collaborative approach between teams while ensuring a compliance culture is instilled and ongoing.

» Data centralisation remains a challenge.

» Increased awareness is needed around our compliance methodology to ensure the purpose and approach is understood and not viewed as inflexible.

Looking forward

We are implementing a roadmap to apply the King IV compliance framework. Compliance continues to ensure that products, services and new business ventures are aligned to relevant legislation and regulations from the development stage onwards.

We will ensure that BankservAfrica leads an effective programme that strives to embed compliance within the company’s DNA to create value for the business.

Corporate Integrity (continued)

Business Report 2017

41

BROAD-BASED BLACK ECONOMIC EMPOWERMENT (BBBEE)We support the objectives of BBBEE to stimulate the participation of previously disadvantaged groups in the economy to increased economic growth. Executives and their respective line managers are responsible for implementing transformation imperatives with measurable scorecards within each business unit.

Highlights

» We implemented our strategic black economic empowerment roadmap.

» We obtained a level 2 BBBEE score.

Challenges

» Transformation is a long-term business imperative, but targets are often short term, which can be challenging.

Looking forward

We have set group-wide BBBEE targets, and frameworks and policies were aligned to these targets. We follow the Financial Sector Charter targets, which are not formally approved yet. We also follow the recent Department of Trade and Industry changes to the generic codes, with targets set for each element.

Broad-based black economic empowerment scorecard

2016/2017 2015/2016 2014/2015

Ownership 14.56 14.7 14.9

Management control 7.83 7.5 5.4

Employment equity 10.88 9.06 7.1

Skills development 7.73 5.65 3.9

Preferential procurement 12.9 14.32 12.0

Enterprise development 15 15 15

Socio-economic development 3 3 3

BBBEE LEVEL Level 2 Level 2 Level 3

As South Africa continues on its journey to inclusivity and diversity in the workplace, BankservAfrica is committed to driving change in the payments infrastructure industry.

42

ETHICSWe are committed to being a trusted partner in the National Payments System. This requires that we have an ethical foundation to all dealings with stakeholders. Our formalised ethics management programme and our code of ethics are in line with the requirements of King IV and offer the business a clear framework under which to operate.

Our ethics officer reports to and works with our CEO, the ethics steering committee and the social and ethics board sub-committee to ensure the business operates according to the highest ethical standards, protecting our reputation as a trusted partner.

OCCUPATIONAL HEALTH AND SAFETY (OHS)The OHS function is concerned with raising awareness to reduce potential workplace injuries. We have an OHS policy in place and conduct awareness and training to protect our employees.

Highlights

» We launched the ethics steering committee, which assists in ensuring that the company conducts its business within the ethical standards for acceptable behaviour.

Challenges

» A lack of confidence from employees in the ethics hotline

Looking forward

We are committed to embedding an ethical culture throughout the organisation. Our new values will be rolled out in the 2018 financial year and to enhance the effectiveness of our ethics hotlines, training will be conducted in 2018. We will also continue to work with industry bodies, such as the Ethics Institute, to ensure we remain abreast of industry best practices.

Highlights

» Two planned evacuations and the first shelter-in-place drill was conducted.

» Our annual baseline risk assessment was completed.

Challenges

» Our challenge is to communicate the value that OHS delivers to combat compliance-based perceptions.

Looking forward

During the year, 12 incidents occurred, resulting in 19 working days lost.

We are working on minimising hazards and OHS risks within the workplace, crafting an effective ergonomics plan, and improving OHS practices.

Corporate Integrity (continued)

Business Report 2017

43

Internal Audit

The Internal Audit support function enables the delivery of BankservAfrica’s strategy by providing an independent and objective assessment of the organisation’s governance, risk management and control processes.

The support function oversees the implementation of the internal audit plan and provides quarterly reports on progress against it; provides quality assurance on business controls; performs application control reviews; and engages and liaises with external auditors, risk management and compliance as part of the combined assurance approach.

Highlights

» We implemented a combined assurance model, enabling an effective control environment.

» We increased our employee complement and now have three full-time internal auditors. We also have additional budget for specialist skills when necessary.

» We have commenced automation of the audit process by procuring and implementing an audit tool so that audit files are no longer manual/paper based and the audit process is more efficient.

Challenges

» Addressing the negative perception of auditing in the organisation and of the audit profession as a whole in the country.

» Inadequate technical capability within Internal Audit to perform value-adding assurance activities in a modernisation era.

» The ever-increasing regulatory requirements in the payments industry remains a challenge to the business, and thus Internal Audit.

Looking forward

Our goal is to be an assurance provider and a ‘trusted advisor’ within BankservAfrica. Internal Audit is responsible for giving independent objective assurance that the organisation is operating as intended to achieve its objectives, and provides insight for improving controls and reducing risk.

44

Legal Services

Legal Services is an enabling and cross-cutting function that impacts the delivery of our core purpose and all its strategic projects.