Business Plan 2010-2011

25

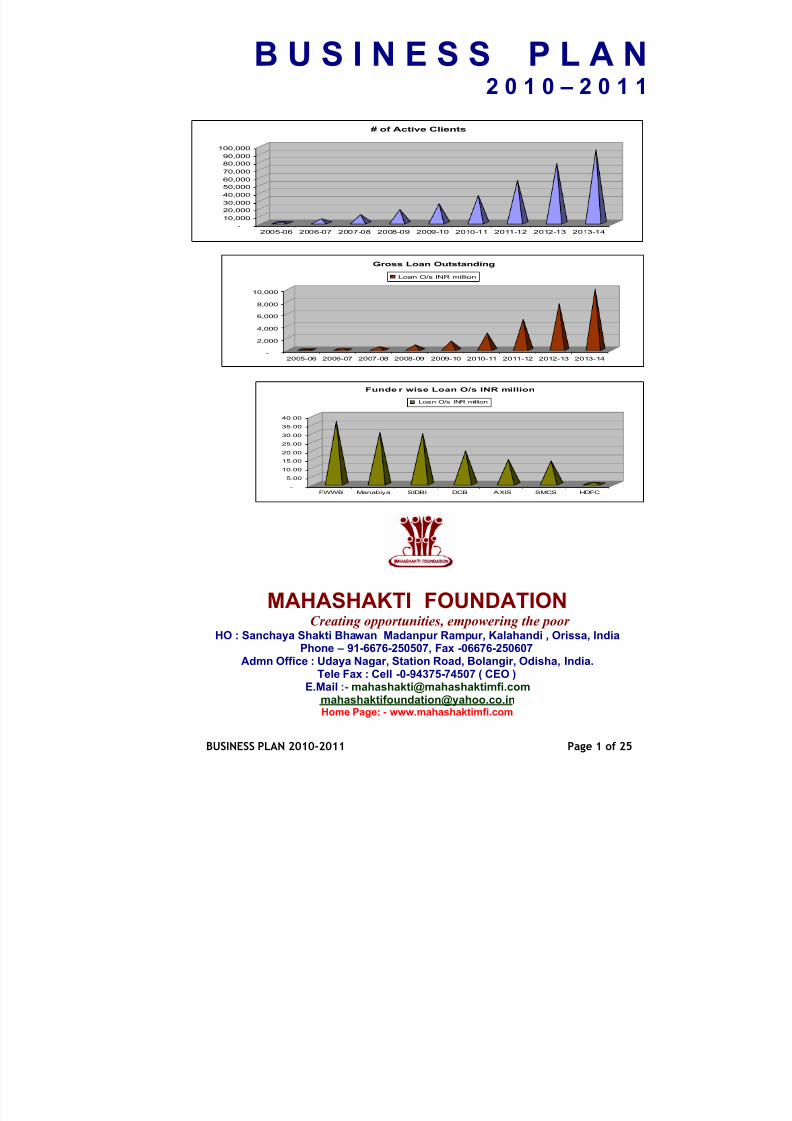

BUSINESS PLAN 2010-2011 Page 1 of 25 B U S I N E S S P L A N 2 0 1 0 – 2 0 1 1 - 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000 2005- 06 2006- 07 2007- 08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 # of Active Clients - 2,000 4,000 6,000 8,000 10,000 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 Gross Loan Outstanding Loan O/s INR million - 5.00 10.00 15.00 20.00 25.00 30.00 35.00 40.00 FWWB Manabiya SI DBI DCB AXI S SMCS HDFC Funde r wise Loan O/s INR million Loan O/s INR million MAHASHAKTI FOUNDATION Creating opportunities, empowering the poor HO : Sanchaya Shakti Bha wan Madanpur Rampur, Kalahandi , Orissa, India Phone – 91-6676-250507, Fax -06676-250607 Admn Office : Udaya Nagar, Station Road, Bolangir, Odisha, India. Tele Fax : Cell -0-94375- 74507 ( CEO ) E.Mail :- [email protected] [email protected] Home Page: - www.mahashaktimfi.com

-

Upload

anithaasrii -

Category

Documents

-

view

222 -

download

0

Transcript of Business Plan 2010-2011

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 1/25

BUSINESS PLAN 2010-2011 Page 1 of 25

B U S I N E S S P L A N 2 0 1 0 – 2 0 1 1

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

# of Active Clients

-

2,000

4,000

6,000

8,000

10,000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Gross Loan Outstanding

Loan O/s INR million

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

FWWB Manabiya SIDBI DCB AXIS SMCS HDFC

Funde r wise Loan O/s INR million

Loan O/s INR million

MAHASHAKTI FOUNDATIONCreating opportunities, empowering the poor HO : Sanchaya Shakti Bhawan Madanpur Rampur, Kalahandi , Orissa, India

Phone – 91-6676-250507, Fax -06676-250607Admn Office : Udaya Nagar, Station Road, Bolangir, Odisha, India.

Tele Fax : Cell -0-94375-74507 ( CEO ) E.Mail :- [email protected]

[email protected] Home Page: - www.mahashaktimfi.com

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 2/25

BUSINESS PLAN 2010-2011 Page 2 of 25

Table of Contents

Organization Profile

Background

Vision & Mission

Core Activities

SWOT Analysis

Methodology Adopted & HR

Products and Services

Social Impact, Market Potential

Organ gram

Governing Board

Management

Leverage Status as on March 2010

Future Plans and Projections

Income Statement

Balance Sheet

Ratios

Cash flow Statement

Esteemed Partners and Collaborators

Other activities and Transformation Process

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 3/25

BUSINESS PLAN 2010-2011 Page 3 of 25

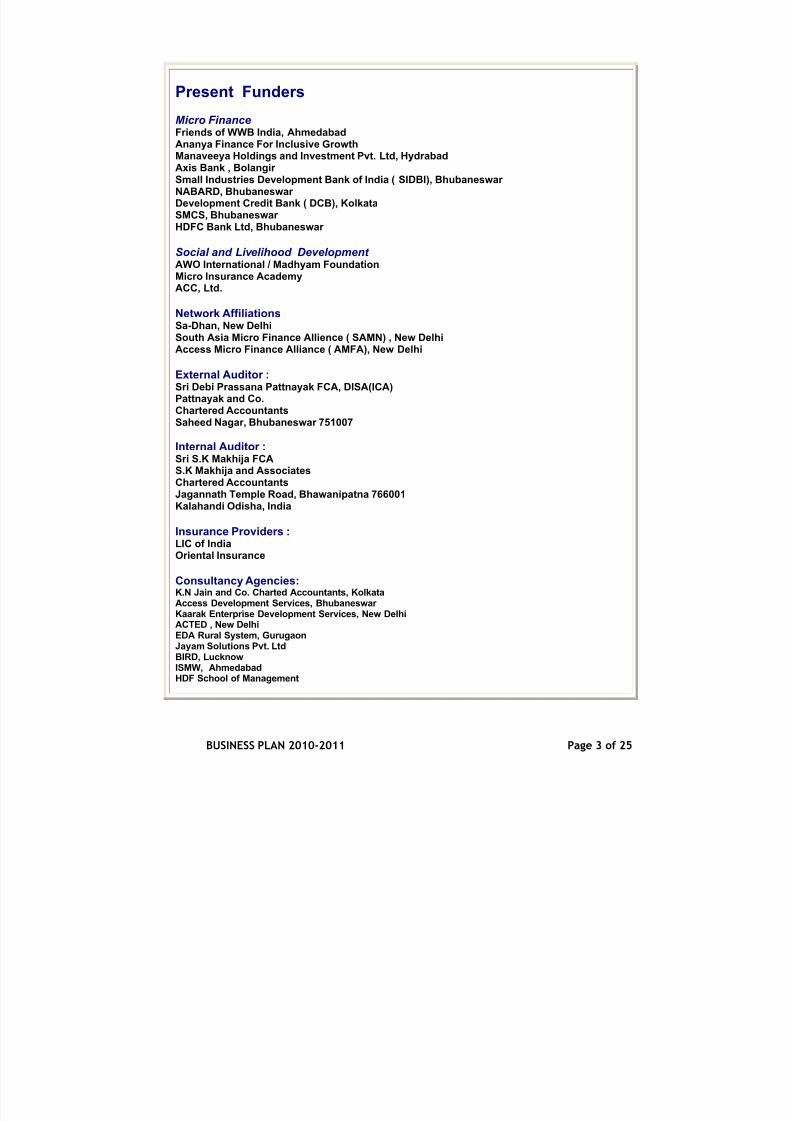

Present Funders

Micro FinanceFriends of WWB India, AhmedabadAnanya Finance For Inclusive GrowthManaveeya Holdings and Investment Pvt. Ltd, HydrabadAxis Bank , Bolangir Small Industries Development Bank of India ( SIDBI), Bhubaneswar NABARD, Bhubaneswar Development Credit Bank ( DCB), KolkataSMCS, Bhubaneswar HDFC Bank Ltd, Bhubaneswar

Social and Livelihood Development AWO International / Madhyam FoundationMicro Insurance AcademyACC, Ltd.

Network AffiliationsSa-Dhan, New DelhiSouth Asia Micro Finance Allience ( SAMN) , New DelhiAccess Micro Finance Alliance ( AMFA), New Delhi

External Auditor :Sri Debi Prassana Pattnayak FCA, DISA(ICA)Pattnayak and Co.Chartered AccountantsSaheed Nagar, Bhubaneswar 751007

Internal Auditor :Sri S.K Makhija FCAS.K Makhija and AssociatesChartered AccountantsJagannath Temple Road, Bhawanipatna 766001Kalahandi Odisha, India

Insurance Providers :LIC of IndiaOriental Insurance

Consultancy Agencies:K.N Jain and Co. Charted Accountants, Kolkata

Access Development Services, Bhubaneswar Kaarak Enterprise Development Services, New DelhiACTED , New DelhiEDA Rural System, GurugaonJayam Solutions Pvt. LtdBIRD, LucknowISMW, AhmedabadHDF School of Management

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 4/25

BUSINESS PLAN 2010-2011 Page 4 of 25

MAHASHAKTI FOUNDATION – B R I E F I N G

MAHASHAKTI FOUNDATION IS REGISTERED AS A TRUST

WE ARE IN THE PROCESS OF TRANSFORMATION INTO AN NBFC AND WE HOPE TOACCOMPLISH THE TRANSFER BY AUGUST 2010

OUR MIS IS AUTOMATED BY FIMO SOFTWARE ( BEING PROVIDED JAYAM SOLUTIONS)AND ALL OF OUR BRANCHES ARE COMPUTERISED WITH HO COMPLIENCE SYSTEM.

WE ARE PRESENTLY SUPPORTED BY SIDBI, FWWB, ANANYA AXIS BANK, DEVELOPMENTCREDIT BANK , HDFC, CARE, SMCS, ACCESS DEVELOPMENT SERVICES , OIKO CREDIT,NABARD, AWO INTERNATIONAL, RABO BANK FOUNDATION FOR LOAN FUND,LIVELIHOOD DEVELOPMENT, CAPACITY BUILDING AND TECHINICAL ASSISTANCESUPPORT AND WE PLAN TO PARTNER A FEW MORE PUBLIC AND PRIVATE INSTITUTIONSIN THE CURRENT FISCAL YEAR…

WE HAVE INCORPORATED SPM AS AN OPERATIONAL AND EVALUATORY TOOL FOR OUR OPERATIONS AND WE ARE IN THE PROCESS OF DEVELOPING MODELS TO IMPLEMENTTHE SAME AT ALL OUR OPERATIONAL LEVELS

WE MAINTAIN THE BEST PORTFOLIO QUALITY WITH OUR RECOVERYRATE AT 99 % AND PAR (> 30 DAYS) EQUATING TO 0.52 % (MARCH 2010)

Investors Highlights

⌦ Mahashakti Foundation is presently working with 27,000Customers in 5 of the most backward districts of Odisha.

⌦ We hope to reach 40,000 client outreach by the end of 2010-2011and more than one lakh clients by 2014

⌦ Having client satisfied MF products with a competitive rate.

⌦ Already reached 100% OSS.

⌦ Rated by CRISIL as mFR 4. (August’09)

⌦ Debt required : Rs. 25.00 Crores ( 2010 - 2011 )

⌦ Equity support : Rs. 03.00 Crores ( 2010 - 2011 )

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 5/25

BUSINESS PLAN 2010-2011 Page 5 of 25

OPERATIONAL HIGHLIGHTS AS ON MARCH 2010

SL Components Details

01 Total Groups 4602

02 Total Members 2682403 Total Active members 24835

04 Total Branches 10

05 Total Loan Outstanding 14.31 Crores

06 Cumulative Disbursement 34.51 Crores

07 Total Leverage from DifferentAgencies

29 Crores

08 Borrowers per loan officer 460

09 Avg. Loan Outstanding per loan

officer

26.50 Lakhs

10 Borrowing Outstanding with Funders 14.41 Crores

11 No of Loans with Over dues 160

12 Amount of Overdue 2,25,625

13 Recovery Rate 99 %14 PAR > 30 Days 0.52%

15 Average loan O/s Size per Client 5761

16 EXISTING FUNDERS NABARDSIDBI

AXIS BANKHDFC BANKDCBFWWBANANYA FINANCEMANABIYAHOLDINGSSMCS

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 6/25

BUSINESS PLAN 2010-2011 Page 6 of 25

BRIEF ORGANISATION PROFILE

Sl.# Particulars Components

01 Name of the Institution Mahashakti Foundation

02 Date of Incorporation 19.10.2004

03 Registered Office Sanchaya Shakti Bhawan , Madanpur Rampur

Kalahandi Odisha –766102 , Phone-06676-250507 Fax06676-250607, Cell :-94375-74507E.Mail :- [email protected] [email protected] Website :- www.mahashaktimfi.com

Administrative Office Smruti Nilaya, Udaya Nagar, Station Road Balangir,Odisha, IndiaTele Fax : 06652 231290

04 Constitution and Regd No. Indian Trust Act 1882Regd No – 584 / IV -3 of 19th / 10/ 2004

05 PAN No AABTM8206H

06 Name of the CEO Jugal Kishore Pattnayak

Managing Director Cell - 0-94375-74507, 0-80182-27507

07 Operational Area 5 Districts of Odisha ( India )Rayagada , Kalahandi , Balangir, Nuapada andSubarnapur

08 Total # of Branches (10) M.Rampur , Madanpur, Kesinga, Bhawanipatna,Rayagada, Muniguda ,Gunpur,Bolangir, Tusura, Khariar.

09 Total Staff Members 104Full Time – All, Top Management Team : - 13Managerial :- 31 , Field Level :-54 , Supporting staff :-

06

10 IT Support Provider Jayam Solutions Pvt. Ltd. Hyderabad

11 Technical SupportProvider

Access Development Services, FWWB , SIDBI, EDARural Systems,BIRD

12 RLF Support Provider NABARD, SIDBI, FWWB, AXIS BANK, DCB, HDFC,CARE, MANABIYA HOLDINGS, ANANYA FINANCE

13 Insurance Partners LIC of India ( Janashree Bima Yojana )

14 Micro Finance Model JLG , Grameen

15 Cumulative Disbursement

till Date

34.51 Crores ( During 2009-10- 16.08 Crores )

16 Loan Outstanding( Mar - 2010 )

14.31 Crores

17 Ratings Rated by ACCESS- Grade A (March 10’) Rated by CRISIL – mFR 4 ( August 09’ )

18 Network Affiliations Sa-Dhan, Access Micro Finance Alliance, (AMFA)South Asia Micro Finance Network ( SAMN)

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 7/25

BUSINESS PLAN 2010-2011 Page 7 of 25

1. Background

Mahashakti Foundation is a Micro Finance Institution founded in the year 2004. It ispromoted by one of the leading NGOs of Odisha FARR¹. FARR started its Microfinance programme from the year 1995 with the RLF and technical support of State

Bank of India, KAGB, NABARD, CARE –CASHE² project, Planet Finance and FWWBIndia. As per the mandate of CARE-CASHE Project, FARR planned to promote aseparate MFI to handle the micro finance programme independently in the year 2004.In the process of building community micro finance institutions FARR gave more focuson establishing professionally managed sustainable micro finance institution.Mahashakti Foundation was founded in the year 2004 and is registered under IndianTrust Act-1882.

“Micro Finance” refers to small savings, credit and insurance services extended tosocially and economically disadvantaged segments of the society. In Indian contextterms like small and marginal farmers, rural artisans and economically weaker sections have been used to broadly define micro finance customers. The recent task

force¹ on micro finance has defined it as provision of thrift, credit and other financialservices and products of very small amounts to the poor in rural ,urban and semiurban areas for enabling them to raise their economic levels and improve livingstandards”. At present a large part of micro finance activity is confined to credit only.“Women constitute a vast majority of users of micro credit and savings services”².

2. “Micro Finance” - We believe in …

• Life time Process

• Needs Professional Approach

• Must be System Driven

•

Needs Automation of MIS• Needs Specialization

• Needs Appropriate Legal Entity

• Needs Strong Monitoring and Internal Control System

• Needs Good Governance and dynamic leaderships

• Needs remuneration based on performance

• It must include SPM as a tool to provide for Impact and Change

_____________________________________________________________ ¹ FARR – Friends Association for Rural Reconstruction is a NGO working for thesustainable development of Orissa from 1983 ( www.farrorissa.org.)² CARE-CASHE – Credit and savings for household enterprise is a micro finance

program implemented in 5 states of India by CARE –India from the yr. 2000 to 2007 toincrease the income level of low income households supported by DFID-UK . ( www.careindia.org.)

¹Task force on micro finance NABARD -1991²Taken from the publication “Micro in India” available at publication section of www.basix.com.

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 8/25

BUSINESS PLAN 2010-2011 Page 8 of 25

3. Operational Philosophy

1. Business principles based on justice, mercy and humility.2. Good governance which is every stake holder’s expectation.3. Operational excellence through transparency in systems and processes.

4. Compassion for poor and respect for individuals.5. Human approach to business-focused on relationship building rather than

short term gains.

4. Vision

“To be a sustainable and established MFI by enabling the poor to change their quality of lives for a better and secured tomorrow”.

5. Mission

“Organize the poor, build up their capacities and access to them relevant

micro finance and livelihood services with transparency and in a dignified way”

6. Goal

“Promote one lakh micro entrepreneurs by 2014”.

7. Our Core Values

In order to achieve its mission and objectives the organization will strive towork with the following values.

1. Honesty - in all transactions with all the stakeholders of our organisation.2. Transparency - by inculcating high degree of commitment through reporting

exactly on what is and what is not expected of us.3. Empathy - in understanding the concerns and ideas of people all around

whether within or external to the organisation and be cordial to them at alltimes.

4. Courage -in finding the right solutions and outcomes for issues, problemswithout compromising on any of the values in the face of adversity.

5. Teamwork - as a means to success in achieving the set mission andobjectives by respecting each other.

6. Punctuality - respecting and honouring organisational commitments within

the scheduled time frame.7. Excellence - in each and every sphere of organisational activity and achievingresults that is better than those already achieved.

8. Communication and candour - encourage and practice continuous andeffective communication by expressing opinions freely and frankly withoutinhibitions.

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 9/25

BUSINESS PLAN 2010-2011 Page 9 of 25

8. Our Core Activities

⌦ Micro Finance⌦ Micro Insurance⌦ Micro Enterprise

⌦ Livelihood Development⌦ Women’s Empowerment⌦ Training and Exposure on Micro Finance

9. Lending Processes We Adopt

We follow the JLG Model in our lending system. The major steps of the said model are asfollows:

Loan Application: -Mahashakti adopts the JLG Model in its operation. It needs to serve a large number of rural customers in an economic way with lower transaction cost and lower lending risk. All

SHG members and 90% of JLG members are women. Members are provided 3 daysCOMPULSORY GROUP TRAINIG (CGT) by Credit Officers (CO) and examined byManager by a GROUP RECOGNITION TEST (GRT) method. Then the loan application isprocessed. Loan application contains the borrower name, proposed purpose of loan,required amount, group name etc. We also maintain the compulsory KYC norms i.e. IDand residence proof. Credit Officer prepares it at the group meeting only after grouprecognition test. Selection of the project or occupation is purely member’s choice. For security of the loan all other members of the group signed on the loan application bypromising and providing collateral security on behalf of the group. It means that they areresponsible to repay the due amounts of the applicant (if any). As the application isprepared with the consent of all the members of the group “Peer Pressure” on membersin case the members became defaulter (if any). Preparation of loan application by CO ismust for sanctioning a loan to the members.

Loan Appraisal: -Appraisal by branch manager is a must after the loan application submitted by CO. At thistime the Manager also take the counterpart sign of 2 members of the same village other than the members of the group for testing the honesty and business viability of theclients. Mahashakti provides the loans to the existing entrepreneurs only.

Loan committee meeting: -The loan Committee meeting held at regional level with at least 3 BM and presided byRegional Manager or Manager Operation where managers of different branches present

their application and get it passed through Loan committee.

HR: - Capacity Building of Staff :Mahashakti Foundation believes that its employees are its most valuable assets and realresource, hence is committed to developing their potential, confidence, knowledge andskill base through various internal as well as external training programmes. Mahashaktimakes a plan in a systematic manner for CB for each staff based on their annualperformance assessment.

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 10/25

BUSINESS PLAN 2010-2011 Page 10 of 25

10. Products and Services

The products and services of Mahashakti Foundation are very simple andcustomized as per the need of customers and limitation of concern funders. The

products are designed differently for both rural and semi urban areas. Themaximum term of the loan is 24 months and maximum loan amount is Rs 40,000/-per member. The products and services are also evaluated in every year andrevised as per the need of the clients and market.

Type of Product

Rate of Interest

Other Charges

LoanSize per client

LoanTerm

Repayment Mode

Gender %Portfolio

MicroEnterpriseLoan

12.50 %Flat

Rs.200/- 4,000to30,000

45weeks

Weekly Female 39 %

SmallBusinessLoan

24.00 %Declining

Rs.200/- 4,000to20,000

25By-weeks

By-weekly Female 21 %

SeasonalBusinessLoan

14.00 %Flat

Rs.200/- 4,000to10,000

12months

Monthly Female 39%

RuralSanitationLoan

18%

Declining

Rs.200/- 10,000to20,000

24 to36months

Monthly Female 1%

11. Insurance Products :

Sl Components Features

01 Name of the Insurance Product Janashree Bima Yojana02 Name of Insurance Company and

Sponsor Life Insurance Company Ltd(LIC ) and Govt of India

03 Type of Product Group Insurance04 Premium Amount INR 200/- Per Year 05 Subsidized by Govt INR 100/- Per person.06 Premium amount for members INR 100/- Per person06 Eligibility Criteria for membership Member of a Group

Age Limit from 18 to 59Benefits07 Natural Death INR 30,000 to the nominee08 Accidental Death INR 75,000 to the nominee09 Permanent Total Disability INR 75,000 to the Member

10 Permanent Partial Disability INR 37,500 to the Member

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 11/25

BUSINESS PLAN 2010-2011 Page 11 of 25

12. Social Impact: -

Mahashakti Foundation is established to give women the opportunity to raise their livelihood in a dignified way. The only other option available for women to start their

own business is to pay extortionate rates of interests to moneylenders.Moneylenders in Odisha charge up to 120% where as Mahashakti asks for just 24%(Declining) and with doorstep services.

Unlike the majority of MFIs in India, Mahashakti only provides loans for incomegenerating activities. Income generating loans often lack the much needed structureto help build feasible enterprises most notably in regard to upsetting the supply anddemand balance. Mahashakti is able to overcome this problem using its LivelihoodDevelopment Services (with loan support). This ensures the loan create maximumimpact on the women’s level of income.

Clients are also asked to talk about the affect of services provided and to suggest

additional useful services to Mahashakti Foundation could provide as per the needof clients from time to time.

We focus exclusively on the poor especially below the poverty line women. Of thewomen we have serviced since inception, 5 % have been lifted above the povertyline as assessed by “SAMPAARK” a Bangalore based Impact Assessment team.

13. Market Potential: -

The Market demand is very high in the operational areas of Mahashakti FoundationMarket Size: - most of the micro finance customers used to believe and afford our products and services due to simplification and need based. As we are in same

operational area for last 10 years (Previously –Mahashakti’s promoting institution-FARR) people have more believe and trust on our products and services.

Market Demand: -The potential number of borrowers in the operational area of Mahashakti is above 3, 00,000

Market Supply: ¹ - As of December 2009, the micro finance institutions includingFFIs and RRBs has only served to 777,000 borrowers in the said operational area.( low income client )

The biggest strength of Mahashakti is for its’ client focused outlook. Mahashaktiresearches client behavior and preferences to respond directly to client needs.

The Livelihood Development Services is a result of this research. We are also triedour level best to satisfy our clients need by diversifying our loan products from timeto time. We are also concentrating in a particular underdeveloped area by providingrepeated loan support to the underdevelopment community for more impact andsustainable development.

¹Based on our internal study by our research and development dept…

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 12/25

BUSINESS PLAN 2010-2011 Page 12 of 25

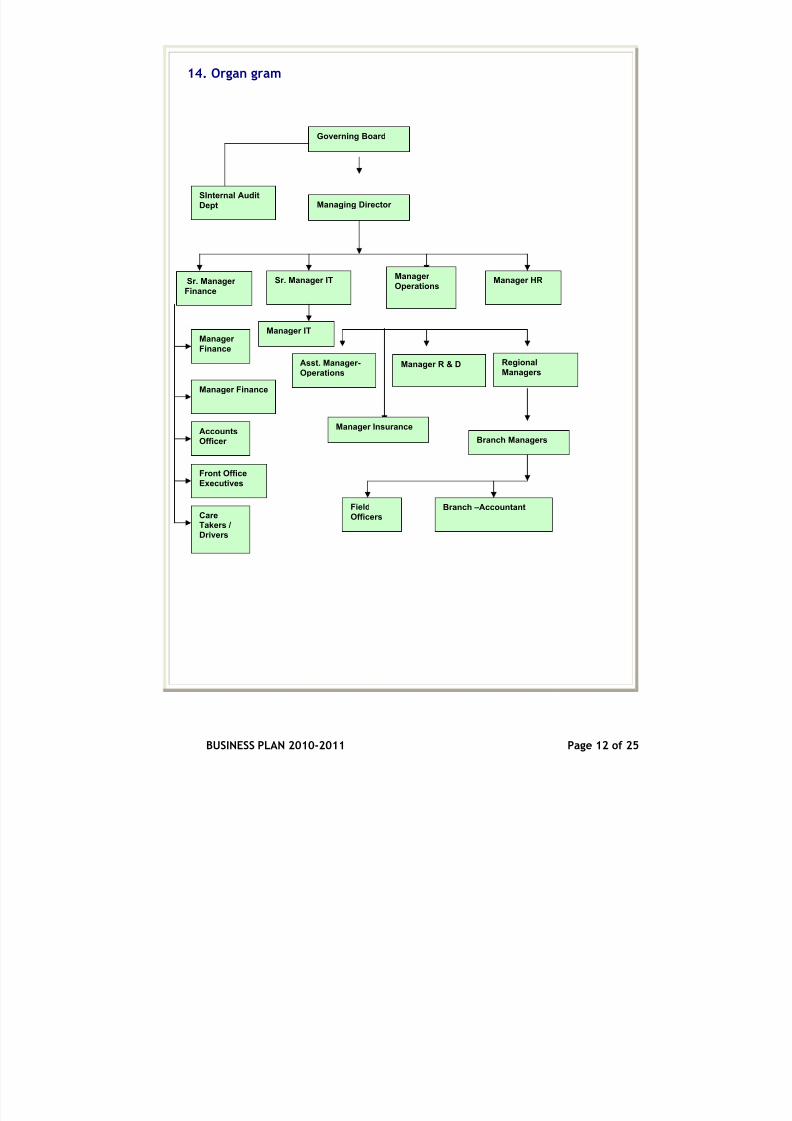

14. Organ gram

Governing Board

Managing Director

Manager HRManager

OperationsSr. Manager ITSr. Manager

Finance

Manager

Finance

AccountsOfficer

Manager Finance

Manager IT

Asst. Manager-

OperationsManager R & D Regional

Managers

Branch Managers

Branch –Accountant

SInternal Audit

Dept

Field

Officers

Front Office

Executives

CareTakers /Drivers

Manager Insurance

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 13/25

BUSINESS PLAN 2010-2011 Page 13 of 25

15. The Governing Board

Mahashakti is governed by 7-members board consisting of experts in the field of Micro finance,Banking, Rural Development, Women Empowerment, law, as well as highly experiencedmanagement team.

Name QualificationExperience

Designation

Smt.AradhanaNanda

MA inEconomics fromUtkal University

25 years experience in the field of MF &Social Development. Served in differentNGOs since 1978 with the responsibilityof planning and coordination of entireprogram, staff assessment, monitoring &supervision of women , child development, training &development, HIV/AIDS counseling, gender training,capacity building, livelihood developmentand Micro Finance operations.

President

Sri SanjeebNayak

B.A ( Hons )LLB from

Sambalpur University

Involved in different social development forums since10 years and former employee Of State Bank of India

with 28 years of experience in formal banking sector and He is also a Certified insurance Advisor by IRDA.

VicePresident

Ms. RojaleenBhuyan

MSW , MA inPol. Sc

B.ED from UtkalUniversity

Development Practitioner for the last 10 years and has5 years of experience in the field of programmeoperations in MF & development

Secretary

Sri JoganandaBehera

MBA inPersonalManagementfrom Berhampur

University

Development Practitioner since last 10 years and 5years of experience in the field of programmeoperation in MF & development Presently He is theTraining Coordinator of Cluster Livelihood Resource

Centre , Kalahandi , supported by DFID

AsstSecretary

Smt.KalendriBhoi

10TH

Development Practitioner , Having 10 years experiencein community mobilization, Group strengthening, She isthe clients representative in the Governing Board

Treasurer

Sri Karna Bag B.Com fromSambalpur University

Former Bank employee of Bhawanipatna CentralCooperative Bank and later on promoted as Auditor tothe Cooperative Department –Govt. of Orissa .Having25 years experience I the formal financial institutionsand cooperative sector.

Member

Sri Jugal

KishorePattnayak

MA, (Pol.Sc.)

LLB,PGDHRDfrom Berhampur University.Diploma inMicro Financefrom IndianInstitute for Banking andFinance,Mumbai

20 years experience in the field of MF & Development.

Served in a state level NGO since 1991 with theresponsibility of planning and coordination of entireprogram, staff assessment, monitoring & supervision of credit operation . Worked as the CEO of CASHE( Credit and Savings for House hold Enterprise ) of CARE ( DFID Supported ) for 6 years. (2000-2006 )

Member

CumManagingDirector

( CEO )

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 14/25

BUSINESS PLAN 2010-2011 Page 14 of 25

16. Senior Management

Mahashakti has hired experienced and professional human resource in the senior management. Most of the staff members are working with Mahashakti sinceinception.

Name and Designation Qualification Previous ExperienceSri . Jugal KishorePattnayakManaging Director ( CEO )

M.A., LLB, PGDiploma in HRManagement andMicro Finance fromIIBF-Mumbai

5 years Experience in RuralDevelopment.15 Years Experience with MFIManagement. Former CEO of FARR -CARE CASHE Program – 2000- 06.

Sri . Jyotiranjan MohapatraManager – Operations

M.Com. ICWAI 12 years Experience on FinancialManagement ,Handling Operationswith MFIs.

Sri . RamaballabhPattnayakSenior Manager-IT

M.Com HWA 7 years Experience in Managing MISand MIS software’s of MFIs.

Sri .Bikram Kesari PatraSenior Manager-Finance

M.Com , 12 years Experience in FinancialManagement and Internal & ExternalAudit

Sri. Vidya Sagar MundManager –Research andDevelopment

M.A. (EnglishLiterature), MBA(HR, Strategy &Planning, Banking),DISM (APTECH),AMFI & IRDAcertified, continuingLLB and M.A. inSociology

2 years of experience in formal banking,wealth management and HR. 6 monthsof experience in Print Media, four months in Strategy & PlanningManagement, 3 years in Socialdevelopment and microfinance

Sri Arun Kumar PattnayakSenior Manager-InternalAudit

M.ComMBA- Finance

2 years Experience in Micro Financesector.

Miss Mita Rani BalManager –HR

BA ( Eco.) MBA (Agri-Business )

1 year Experience in NHBC

Mr. Rajib Lochan BeheraAsst. Manager-Operations

B.Com MBA( Agri-Business)

1 Year Exp in Handling Operations of MFIs

Sri Gobardhan DashManager –Finance

M.Com 8 years Experience in a reputedchartered Firm

Sri Prakash Ch. SahuRegional Manager

B.A.,PGDCA 20 years experience in RuralDevelopment and 10 years experiencein MFI.

Sri Simanchal Pattanayak

Regional Manager

B.A , PGDCA 18 years experience in Rural

Development and 10 years experiencein MFI.

Sri Bimal Kanta PandaRegional Manager

BA, PGDCA 20 years experience in RuralDevelopment and 10 years experiencein MFI

Ramesh Chandra PradhanRegional Accountant

MBA in HRManagement andFin. ManagementIIET Hydrabad

4 years Experience in MFIManagement

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 15/25

BUSINESS PLAN 2010-2011 Page 15 of 25

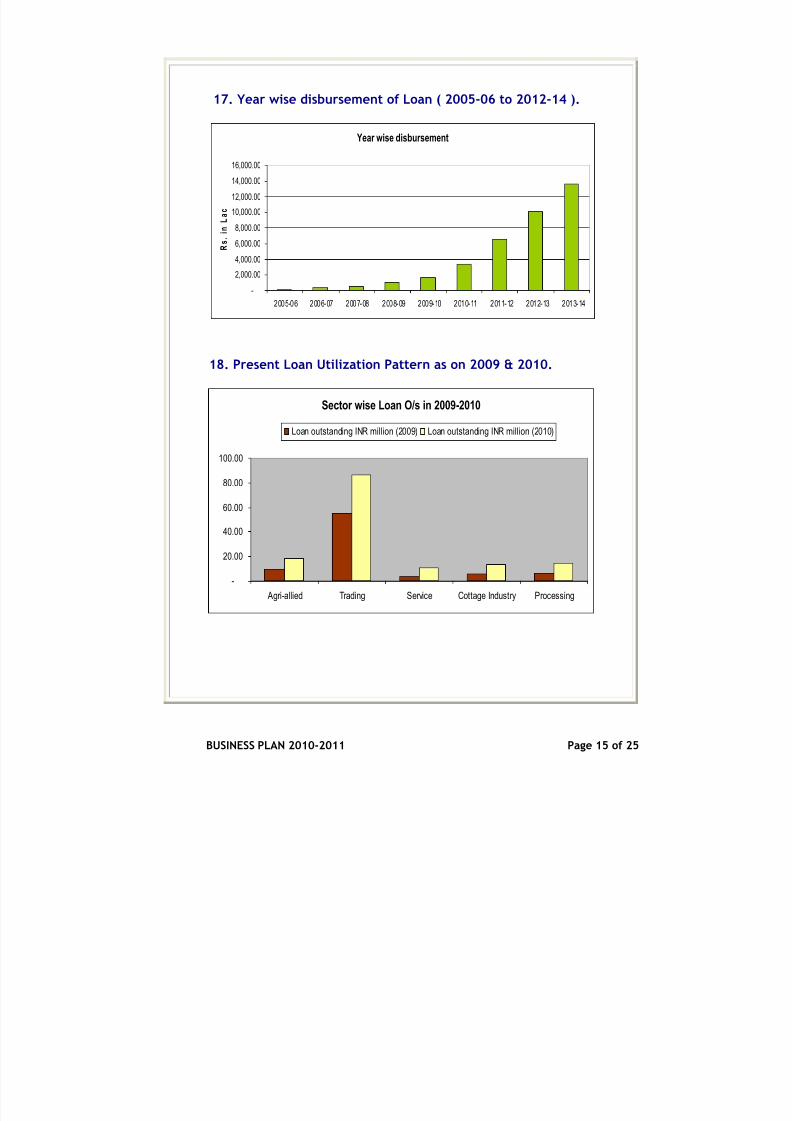

17. Year wise disbursement of Loan ( 2005-06 to 2012-14 ).

Year wise disbursement

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

R

s .

i n

L a c

18. Present Loan Utilization Pattern as on 2009 & 2010.

Sector wise Loan O/s in 2009-2010

-

20.00

40.00

60.00

80.00

100.00

Agri-allied Trading Service Cottage Industry Processing

Loan outstanding INR million (2009) Loan outstanding INR million (2010)

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 16/25

BUSINESS PLAN 2010-2011 Page 16 of 25

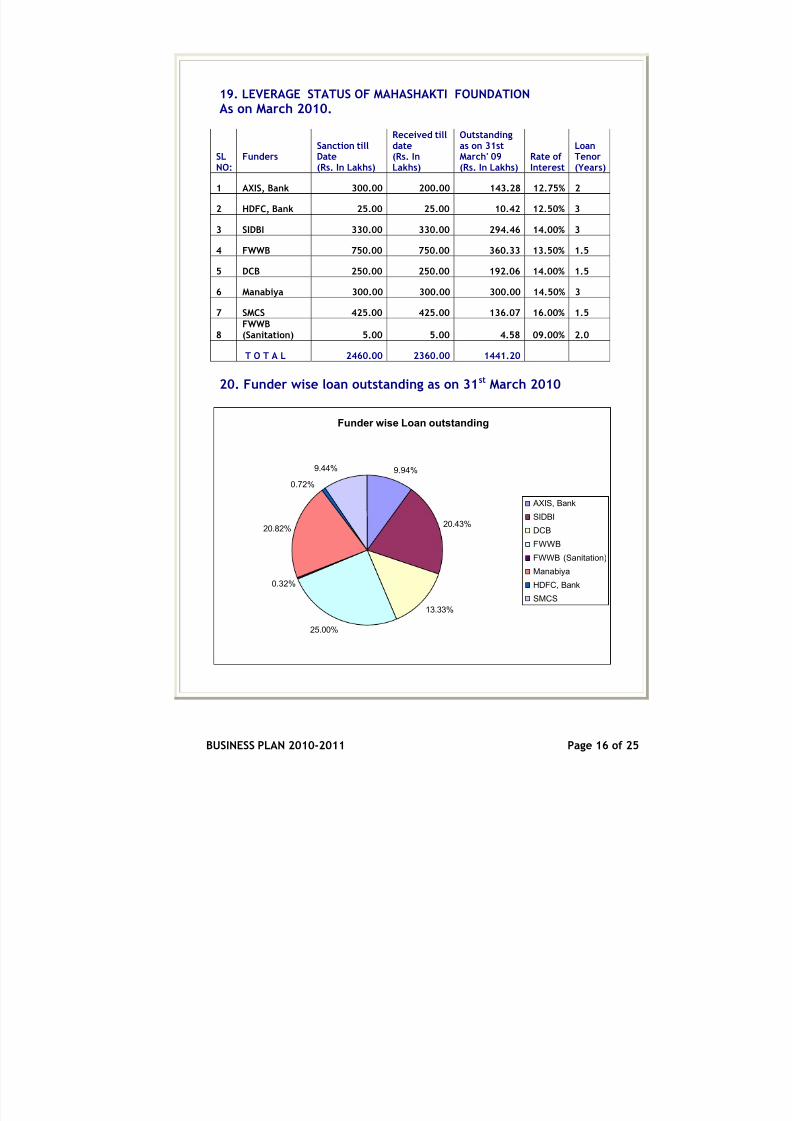

19. LEVERAGE STATUS OF MAHASHAKTI FOUNDATION

As on March 2010.

SLNO:

FundersSanction tillDate(Rs. In Lakhs)

Received tilldate(Rs. InLakhs)

Outstandingas on 31stMarch' 09(Rs. In Lakhs)

Rate of Interest

LoanTenor(Years)

1 AXIS, Bank 300.00 200.00 143.28 12.75% 2

2 HDFC, Bank 25.00 25.00 10.42 12.50% 3

3 SIDBI 330.00 330.00 294.46 14.00% 3

4 FWWB 750.00 750.00 360.33 13.50% 1.5

5 DCB 250.00 250.00 192.06 14.00% 1.5

6 Manabiya 300.00 300.00 300.00 14.50% 3

7 SMCS 425.00 425.00 136.07 16.00% 1.5

8FWWB(Sanitation) 5.00 5.00 4.58 09.00% 2.0

T O T A L 2460.00 2360.00 1441.20

20. Funder wise loan outstanding as on 31st March 2010

Funder wise Loan outstanding

9.94%

20.43%

13.33%

25.00%

0.32%

20.82%

0.72%

9.44%

AXIS, Bank

SIDBI

DCB

FWWB

FWWB (Sanitation)

Manabiya

HDFC, Bank

SMCS

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 17/25

BUSINESS PLAN 2010-2011 Page 17 of 25

21. Year wise Active Clients ( 2005-06 to 2013-14)

Year wise active clients

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 22. Year wise Gross Loan Outstanding : ( 2005-06 to 2013-14)

Year wise Gross Loan O/s

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 18/25

BUSINESS PLAN 2010-2011 Page 18 of 25

23. SWOT Analysis

Strengths –

Professional, experienced, motivated and dedicated staff System process in line with organizational ethics and core values All manuals, notices and circulars in place Dedicated core teams for individual purposes High valued quality output Adherence to time, sincerity and quality in all operations Well equipped infrastructure Good will among stakeholders and clients Strong network in the industry Proven track record of operational effectiveness & efficiency Strong and modern Training and development modules

Weaknesses-

Lack of proper leverage Lack of proper equity funding Geographical disadvantage owing to operations linked with the rural poor

Opportunities –

Huge Market demand Operational area having immense potential Large scope for livelihood intervention Large scope for financial intervention

Trust worthy people in the operational area Huge potential in the micro-savings and the micro-insurance area Huge potential in the micro-housing and sanitation area

Threats –

Natural calamity Political Interference Unnecessary regulations

24-28 Projections

We have analyzed the Past financial data for last five years and based on that theProjections of Mahashakti foundation are made for next four years (up to 2014) inSl. # 24 to 28.

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 19/25

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 20/25

8/3/2019 Business Plan 2010-2011

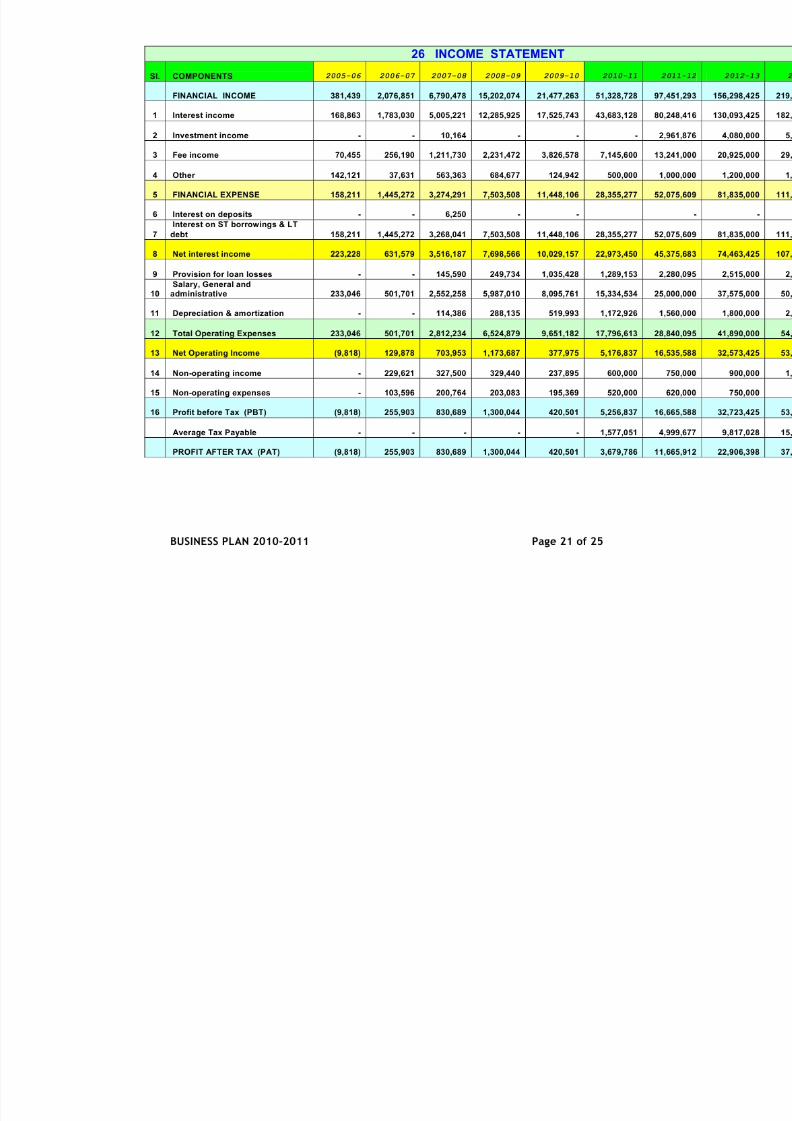

http://slidepdf.com/reader/full/business-plan-2010-2011 21/25

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 22/25

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 23/25

BUSINESS PLAN 2010-2011 Page 23 of 25

28 . DIRECT STATEMENT OF CASH FLOWS

Sl. COMPONENTS QUARTERLY CASH FLOW STATEMENT 20

A SOURCES OF CASH Q1 APR-JUN Q2 JUL-SEP Q3 OCT-DEC Q4 JAN-MAR T

1 Opening Balance 585,755 462,361 482,361 607,771

2

Loan from FinancialInstitutions 56,834,792 58,939,856 65,113,903 71,775,988 252

3 Capital / Equity - - 2,000,000 3,000,000 5

4 Loan repaid by Clients 38,435,874 46,730,805 54,479,307 62,590,716 202

5 Interest & Fees Incomes 9,891,749 12,309,854 13,687,530 15,439,595 51

6 Non Operational Receipts 150,000 150,000 150,000 150,000

T O T A L 105,898,170 118,592,876 135,913,101 153,564,069 512

B UTILISATION OF CASH

1 Loan disbursed to Clients 71,532,000 77,220,000 86,400,000 96,000,000 331

2

Loan repaid to FinancialInstitutions 19,516,387 24,207,383 28,626,732 33,271,200 105

3 Interest Paid 5,464,588 6,611,593 7,628,584 8,650,512 28

4

AdministrativePayments 2,965,960 3,547,553 4,114,034 4,706,987 15

5 Non Operational Payments 130,000 130,000 130,000 130,000

6 Investment 5,683,479 5,893,986 6,511,390 7,177,599 25

7 Purchased of Fixed Assets - 350,000 544,590 1,040,780 1

8 Refund of securities 143,394 150,000 1,350,000 1,300,000 2

9

Refund of AccountsPayable - - - 595,249

T O T A L 105,435,809 118,110,515 135,305,330 152,872,327 511

Closing Balance 462,361 482,361 607,771 691,742

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 24/25

BUSINESS PLAN 2010-2011 Page 24 of 25

29. Our Esteemed Partners and Collaborators

Sl Name of the agency Purpose

O1 SMALL INDUSTRIES DEVELOPMENT BANK OF INDIAGrant and Loan Fund support from Bhubaneswar Branch

02 AXIS BANK , BOLANGIRLoan Fund Support from Bolangir Branch

03 HDFC BANK , BHUBANESWARLoan Fund support from Bhubaneswar Branch

04 FRIENDS OF WORLD WOMEN BANKINGLoan fund for Housing , Sanitation and Capacity buildingsupport from the central office Ahmedabad.

05 Loan Fund support from the HO New Delhi.

06 DEVELOPMENT CREDIT BANKLoan Fund support from Kolkata Branch .

07 LIFE INSURANCE CORPORATION OF INDIAProviding Group life Insurance for the Clients of Mahashakti

Foundation08 ORIENTAL INSURANCE COMPANY

Providing general insurance for the clients and the institution.

09 ACCESS DEVELOPMENT SERVICES, BHUBANESWARTechnical Assistance for the development of micro financeprogram from the state office BBSR.

10 ACTEDTechnical Assistance for the Transformation Process andInternational Exposure.

11 \ SADHAN

Network support for capacity building and mutual learning,Dissemination of MFI data at national and internationalforums.

12 ACCESS MICRO FINANCE ALLIANCENetwork support for capacity building, Fund leverage, mutuallearning etc..

13 Micro Insurance Academy for promoting community basedhealth Insurance in rural areas for better health services.

14 ANANYA FINANCE ANANYA FINANCE FOR INCLUSIVE GRPWTH , AHMEDABADLoan Fund Support .

15 JAYAM SOLUTIONS JAYAM SOLUTIONS PVT. LTD.

IT Support provider for MIS

16 MANAVEEYA HOLDINGS( Oiko Credit)

Manaveeya Holdings and Investment Pvt Ltd, Hydrabad, Loanfund Support.

17

NABARD

NABARD – Capital Equity Support

a c c e s s m i c r o f i n a n c e

A L L I A N C Ea c c e s s m i c r o f i n a n c e

A L L I A N C E

8/3/2019 Business Plan 2010-2011

http://slidepdf.com/reader/full/business-plan-2010-2011 25/25

30. Vertical Growth Strategy :

Mahashakti Foundation believes in following the Vertical Strategy to achieveconsistent growth. We are of the thought that, we should focus in expanding our operational growth by focusing on our bunch of clients who have been with us in our journey. Necessarily because we have a dream of creating an impact by creating a

visible shift in the way the people live their lifestyles. We follow this strategy becausewe wish to provide quality products and services to our clients who in turn wouldmake us sustainable. Also such a strategy helps us in being focused towards thesocial goals and objectives that we have, here in we can also resort to better methods of Client Satisfaction and a method of developing trust and mutualcooperation that calls for growth oriented, inclusive growth.

31 Partnering with Access, FWWB, ISMW, BIRD,EDA , ACTED and SIDBI :

Mahashakti is partnering with above institutions for the capacity building of staff members in a periodic basis. Institutions like SIDBI, FWWB, ACTED are also

providing financial support for organizing the training for staff and clients.Consultants of Access Development Services providing training to the field levelstaff members regularly.

32 International Exposures:

Mr. Jugal Kishore Pattnayak CEO of Mahashakti Foundation visited to the MFIs of Bangladesh and Sri Lanka with the support of SIDBI and ACTED in last financialyear. Mr. Jyoti Ranjan Mohapatra, Head –Operations visited PARIS( FRANCE) toattend in the international investment fair organized by ACTED and South AsiaMicro Finance Network ( SAMN ) during April 2009.

33. Transformation of Micro Finance Operation to NBFC :

Mahashakti is partnering with ACTED –New Delhi and taking the consultancysupported by ACTED to transform itself to a for profit company during this financialyear. The process has already started. The name of the NBFC is Hans PropertiesPrivate Limited and the authorized capital for the said house is Rs.30 lakhs.Mahashakti Foundation has developed a dedicated team for the management of theNBFC developed here on. There have been three top level meetings regarding theNBFC formation and all the decisions taken thereof have been positive towards thespeeding up of the process of getting converted into an NBFC. The transformationprocess is taken care of by Ms/ K.N.Jain and associates Kolkata.

For More information please visit our home page : www.mahashaktimfi.com Please mail us : [email protected], [email protected]

Call us : 0-94375 74507 / 0-80182 27507 : Jugal Kishore Pattnayak –CEOCall Us 0-94373 94507 / 96688 44493 : Mr J.R Mohapatra, Head –Operations

![Business Plan 2010[1]](https://static.fdocuments.in/doc/165x107/577d36ab1a28ab3a6b93b052/business-plan-20101.jpg)

![2010-2015 Business Plan Milan.ppt [modalità compatibilità] · 2016-06-16 · 2010 - 2015 Business Plan Presentation2015 Business Plan Presentation September 23, 2010. Mr. Paolo](https://static.fdocuments.in/doc/165x107/5f10a44a7e708231d44a1b9c/2010-2015-business-plan-milanppt-modalit-compatibilit-2016-06-16-2010-.jpg)