Business Owners Program Oregon - Stillwater …...©2016 STILLWATER INSURANCE GROUP Business Owners...

51

Business Owners Program Oregon ©2016 STILLWATER INSURANCE GROUP

Transcript of Business Owners Program Oregon - Stillwater …...©2016 STILLWATER INSURANCE GROUP Business Owners...

Business Owners Program

Oregon

©2016 STILLWATER INSURANCE GROUP

©2016 STILLWATER INSURANCE GROUP

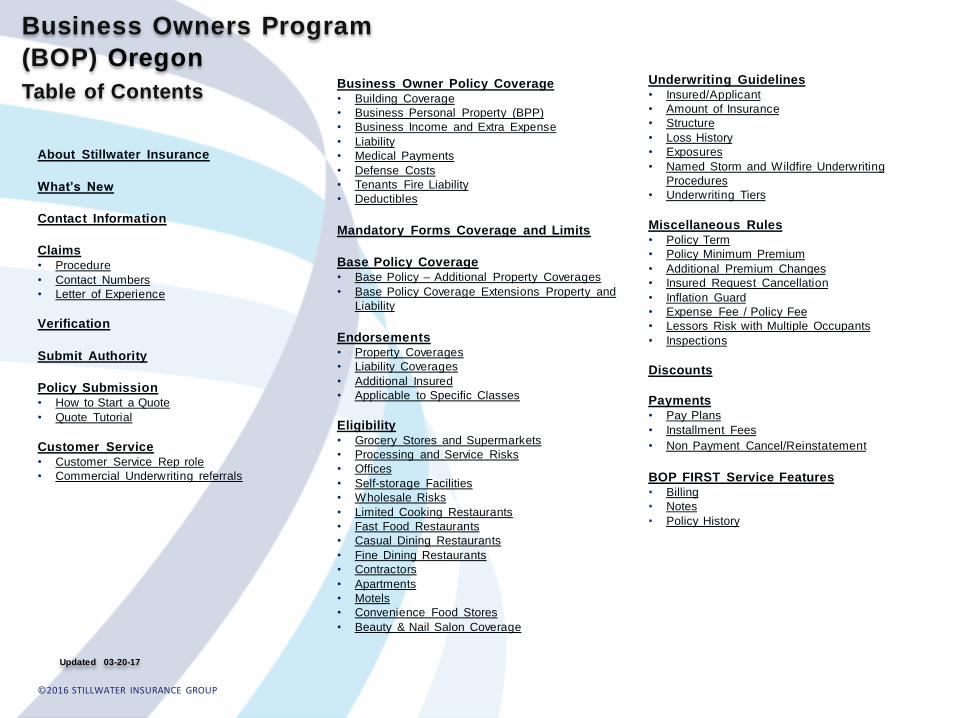

Business Owners Program

(BOP) Oregon

Table of Contents

Updated 03-20-17

About Stillwater Insurance

What’s New

Contact Information

Claims • Procedure

• Contact Numbers

• Letter of Experience

Verification

Submit Authority

Policy Submission • How to Start a Quote

• Quote Tutorial

Customer Service • Customer Service Rep role

• Commercial Underwriting referrals

Business Owner Policy Coverage • Building Coverage

• Business Personal Property (BPP)

• Business Income and Extra Expense

• Liability

• Medical Payments

• Defense Costs

• Tenants Fire Liability

• Deductibles

Mandatory Forms Coverage and Limits

Base Policy Coverage • Base Policy – Additional Property Coverages

• Base Policy Coverage Extensions Property and

Liability

Endorsements • Property Coverages

• Liability Coverages

• Additional Insured

• Applicable to Specific Classes

Eligibility • Grocery Stores and Supermarkets

• Processing and Service Risks

• Offices

• Self-storage Facilities

• Wholesale Risks

• Limited Cooking Restaurants

• Fast Food Restaurants

• Casual Dining Restaurants

• Fine Dining Restaurants

• Contractors

• Apartments

• Motels

• Convenience Food Stores

• Beauty & Nail Salon Coverage

Underwriting Guidelines • Insured/Applicant

• Amount of Insurance

• Structure

• Loss History

• Exposures

• Named Storm and Wildfire Underwriting

Procedures

• Underwriting Tiers

Miscellaneous Rules • Policy Term

• Policy Minimum Premium

• Additional Premium Changes

• Insured Request Cancellation

• Inflation Guard

• Expense Fee / Policy Fee

• Lessors Risk with Multiple Occupants

• Inspections

Discounts

Payments • Pay Plans

• Installment Fees

• Non Payment Cancel/Reinstatement

BOP FIRST Service Features • Billing

• Notes

• Policy History

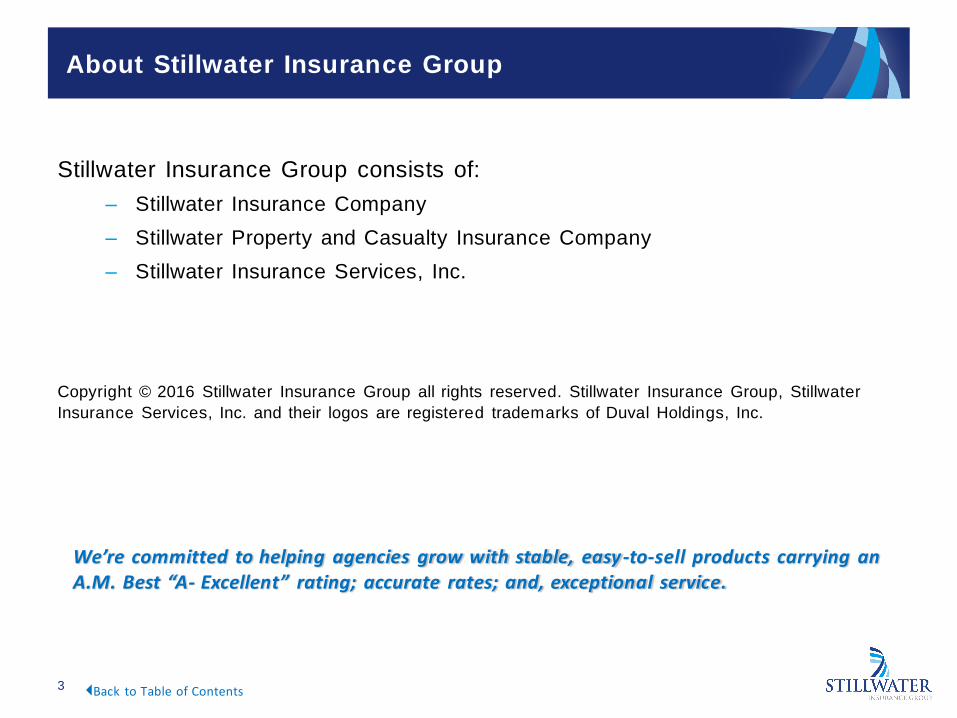

About Stillwater Insurance Group

1

1

3

5

Stillwater Insurance Group consists of:

– Stillwater Insurance Company

– Stillwater Property and Casualty Insurance Company

– Stillwater Insurance Services, Inc.

Copyright © 2016 Stillwater Insurance Group all rights reserved. Stillwater Insurance Group, Stillwater

Insurance Services, Inc. and their logos are registered trademarks of Duval Holdings, Inc.

3

We’re committed to helping agencies grow with stable, easy -to-sell products carrying an A.M. Best “A- Excellent” rating; accurate rates; and, exceptional service.

Back to Table of Contents

Commercial BOP What’s New?

What’s New?

Important Updates are archived on FIRST and provide information on system changes to FIRST.

Click here to view the Important Updates – Archive.

4 Updated 03-20-17 Back to Table of Contents

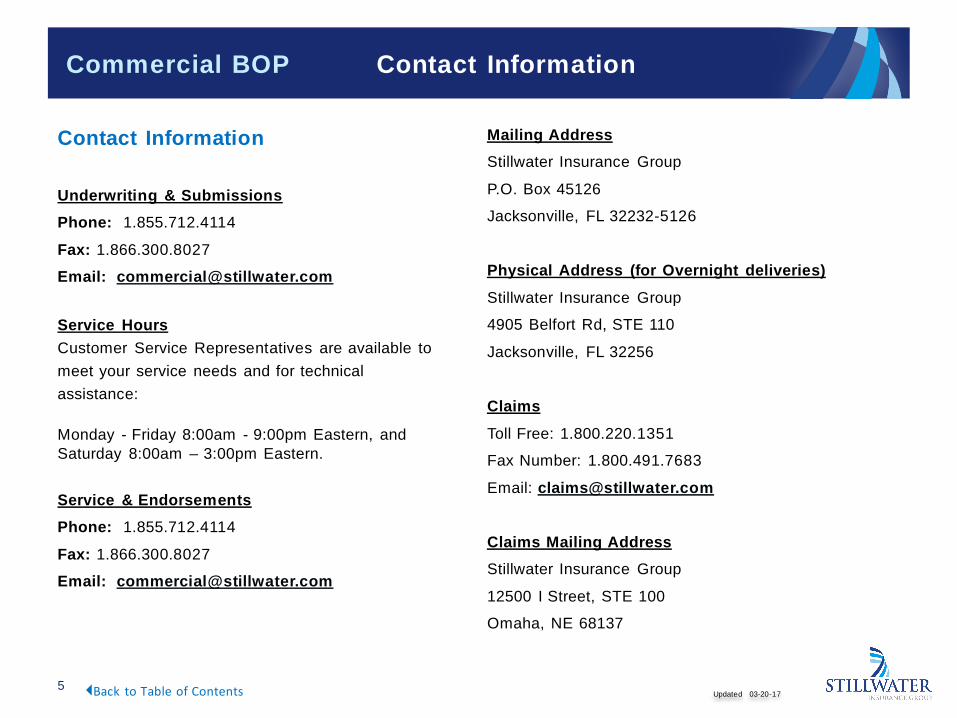

Commercial BOP Contact Information

Contact Information

Underwriting & Submissions

Phone: 1.855.712.4114

Fax: 1.866.300.8027

Email: [email protected]

Service Hours

Customer Service Representatives are available to

meet your service needs and for technical

assistance:

Monday - Friday 8:00am - 9:00pm Eastern, and

Saturday 8:00am – 3:00pm Eastern.

Service & Endorsements

Phone: 1.855.712.4114

Fax: 1.866.300.8027

Email: [email protected]

Mailing Address

Stillwater Insurance Group

P.O. Box 45126

Jacksonville, FL 32232-5126

Physical Address (for Overnight deliveries)

Stillwater Insurance Group

4905 Belfort Rd, STE 110

Jacksonville, FL 32256

Claims

Toll Free: 1.800.220.1351

Fax Number: 1.800.491.7683

Email: [email protected]

Claims Mailing Address

Stillwater Insurance Group

12500 I Street, STE 100

Omaha, NE 68137

5 Updated 03-20-17 Back to Table of Contents

Commercial BOP Claim Procedures

Claims Procedure

All claims should be immediately reported to Stillwater Claims

Service.

For fast claims service, and to completely eliminate your time

involved in processing claims forms, please instruct your

insureds and claimants to call our claims department directly.

Remember, you have no claims settlement authority.

General Information:

• Toll-free Claims: 1.800.220.1351.

• Stillwater Staffed::

– Monday - Friday 8:00am - 8:00pm ET

– Saturday 9:00am - 6:00pm ET

– After hours, Lynx Services LLC answers the line taking

first notice of losses and providing limited remediation

guidance (in the event of water damage, etc.). Note,

they cannot verify coverage. Lynx Services LLC is

available 24/7.

• If there is a severe emergency or loss, Lynx Services can put

a Stillwater adjuster in touch with your client.

• We offer a translation service – including dozens of languages

such as Hmong, Farsi, Punjabi, Mandarin, Cantonese and

Vietnamese.

Claims Contact Numbers:

• Phone 1.800.220.1351

• Fax 1.800.491.7683

• Email: [email protected]

Letter of Experience(LOE)

Stillwater Insurance is able to provide a letter that shows

the insured’s Loss History while insured with Stillwater

Insurance Group.

Send requests to: [email protected]

or via fax: 1.800.491.7683

• Please include policy numbers.

• Allow 24 - 48 hours to process.

• Letters of Experience will be emailed.

• Include other party contact information, if an LOE

needs to be sent to others.

6 Updated 03-20-17 Back to Table of Contents

Commercial BOP Verification

7

File Maintenance and Audit Requirements

Producers are required to maintain relevant

documentation for a period of seven years after policy

expiration. Agents should expect occasional file audits to

confirm required signatures and agency file

documentation. Namely, these documents are required

to be maintained in agency records:

• Signed applications

• Signed EFT Authorization when this pay plan is used

• Letters of Experience related to claims.

• Copy of support documents for discounts

Verification

As a part of new business process we may utilize third-party

data sources to provide or verify information, including:

• Public Records Data

• NCF – National Credit File. This helps determine

Insurance Bureau Score(IBS).

Our quote process recognizes underwriting issues – in turn it

may create an underwriting referral or may result in certain

risks being declined based upon eligibility or acceptability

rules.

Contact customer service at 1.855.712.4114 if you have

questions with respect to report information.

Updated 03-20-17 Back to Table of Contents

Commercial BOP Submit Authority/Policy Submission

Submit Authority

• Submit authority (or binding authority) may be

suspended for new business submissions or

requests for increased coverage endorsements

during periods of imminent danger from natural

disasters, or when the National Weather Service

has issued a severe weather warning.

• Types of natural disasters include, but are not

limited to, Earthquake, Earth movement (landslide,

mudslide, sinkhole, etc.), Wild Fire, Hurricane,

Tropical Storm, Tornado, and Flood.

• We reserve the right to suspend submission

authority as we deem fit, and as allowed by state

regulations and emergency orders.

• In the event of such suspension, we will issue a

moratorium on FIRST. During moratoriums no

new business or increased coverage

endorsements may be submitted.

Application Submission

FIRST is a real-time Quoting and Underwriting system

designed to assist our Producers in quoting and issuing

insurance policies. This system provides an easy way of doing

business by indicating whether risks are eligible and allows

producers to instantly issue policies.

Risk Acceptability

Responses to questions during quoting will determine if there

are underwriting eligibility conflicts. Producers do not have

authority to submit coverage for any property exhibiting a

conflict with underwriting rules.

We may be contacted for prior approval regarding acceptability

in gray areas. Policy submission is subject to acceptance of

the risk based on our product design and regulatory filings.

Requests or questions should be emailed to

Submitting

Policies are only valid when they are issued on FIRST with a

policy number.

Click below for information on starting a Quote on FIRST:

How to Start a BOP Quote

8 Updated 03-20-17 Back to Table of Contents

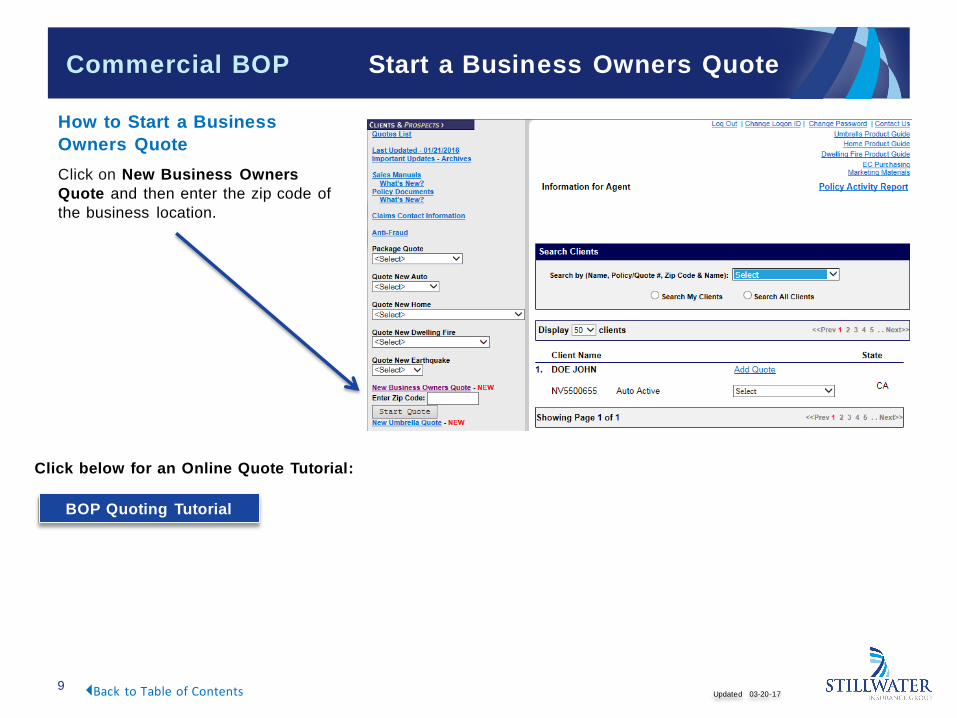

Commercial BOP Start a Business Owners Quote

9

How to Start a Business

Owners Quote

Click on New Business Owners

Quote and then enter the zip code of

the business location.

BOP Quoting Tutorial

Click below for an Online Quote Tutorial:

Updated 03-20-17 Back to Table of Contents

Commercial BOP Customer Service Role

10 Updated 03-20-17 Back to Table of Contents

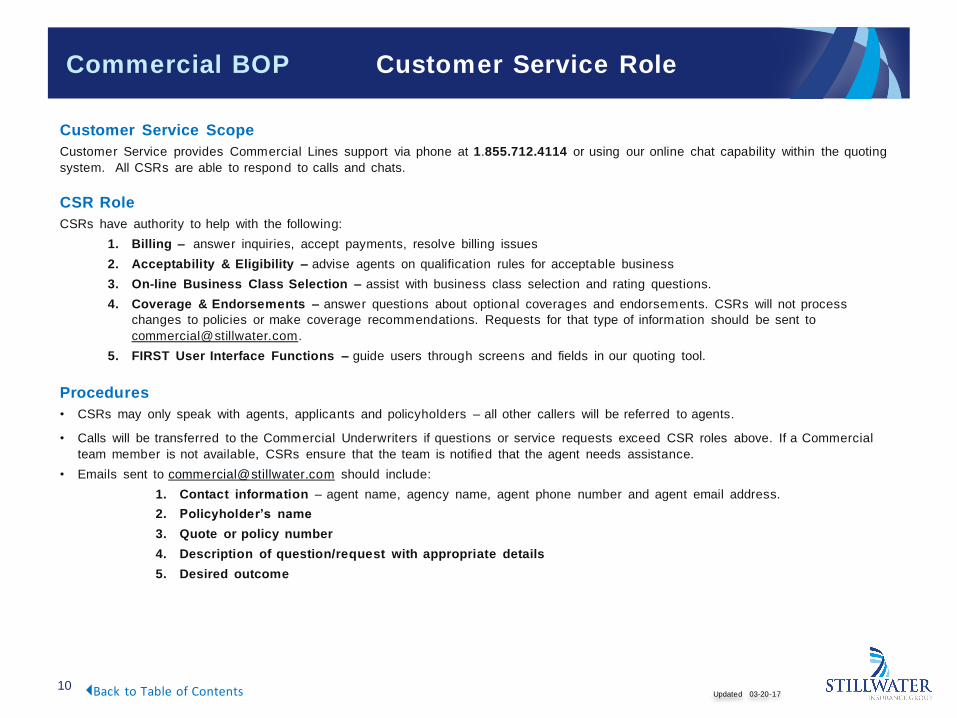

Customer Service Scope

Customer Service provides Commercial Lines support via phone at 1.855.712.4114 or using our online chat capability within the quoting

system. All CSRs are able to respond to calls and chats.

CSR Role

CSRs have authority to help with the following:

1. Billing – answer inquiries, accept payments, resolve billing issues

2. Acceptability & Eligibility – advise agents on qualification rules for acceptable business

3. On-line Business Class Selection – assist with business class selection and rating questions.

4. Coverage & Endorsements – answer questions about optional coverages and endorsements. CSRs will not process

changes to policies or make coverage recommendations. Requests for that type of information should be sent to

5. FIRST User Interface Functions – guide users through screens and fields in our quoting tool.

Procedures

• CSRs may only speak with agents, applicants and policyholders – all other callers will be referred to agents.

• Calls will be transferred to the Commercial Underwriters if questions or service requests exceed CSR roles above. If a Commercial

team member is not available, CSRs ensure that the team is notified that the agent needs assistance.

• Emails sent to [email protected] should include:

1. Contact information – agent name, agency name, agent phone number and agent email address.

2. Policyholder’s name

3. Quote or policy number

4. Description of question/request with appropriate details

5. Desired outcome

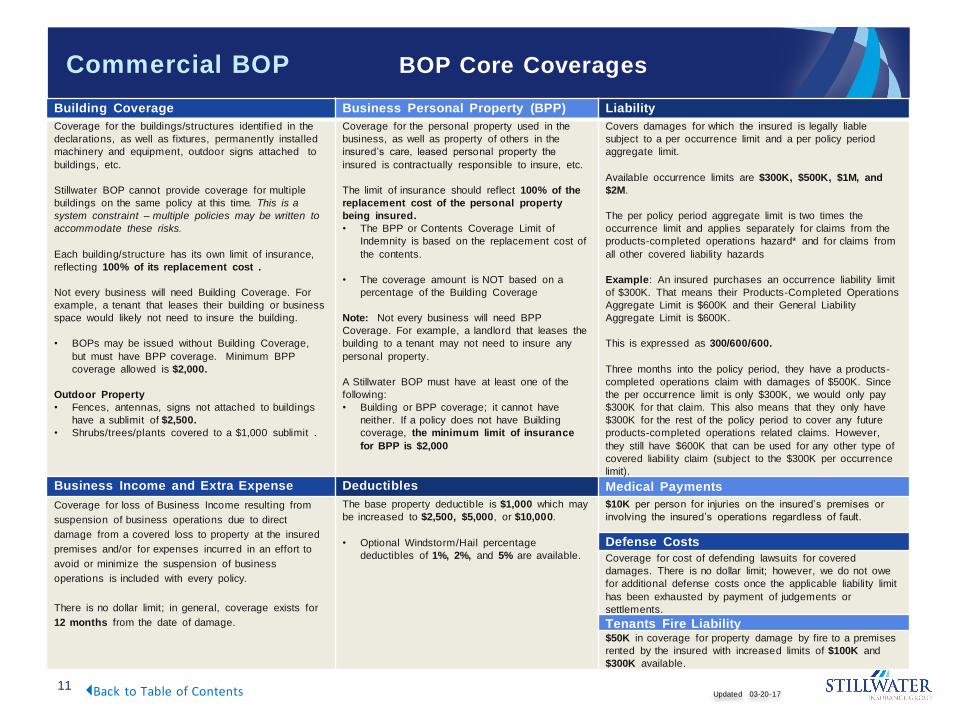

Commercial BOP BOP Core Coverages

11

Building Coverage Business Personal Property (BPP) Liability

Coverage for the buildings/structures identified in the

declarations, as well as fixtures, permanently installed

machinery and equipment, outdoor signs attached to

buildings, etc.

Stillwater BOP cannot provide coverage for multiple

buildings on the same policy at this time. This is a

system constraint – multiple policies may be written to

accommodate these risks.

Each building/structure has its own limit of insurance,

reflecting 100% of its replacement cost .

Not every business will need Building Coverage. For

example, a tenant that leases their building or business

space would likely not need to insure the building.

• BOPs may be issued without Building Coverage,

but must have BPP coverage. Minimum BPP

coverage allowed is $2,000.

Outdoor Property

• Fences, antennas, signs not attached to buildings

have a sublimit of $2,500.

• Shrubs/trees/plants covered to a $1,000 sublimit .

Coverage for the personal property used in the

business, as well as property of others in the

insured’s care, leased personal property the

insured is contractually responsible to insure, etc.

The limit of insurance should reflect 100% of the

replacement cost of the personal property

being insured.

• The BPP or Contents Coverage Limit of

Indemnity is based on the replacement cost of

the contents.

• The coverage amount is NOT based on a

percentage of the Building Coverage

Note: Not every business will need BPP

Coverage. For example, a landlord that leases the

building to a tenant may not need to insure any

personal property.

A Stillwater BOP must have at least one of the

following:

• Building or BPP coverage; it cannot have

neither. If a policy does not have Building

coverage, the minimum limit of insurance

for BPP is $2,000

Covers damages for which the insured is legally liable

subject to a per occurrence limit and a per policy period

aggregate limit.

Available occurrence limits are $300K, $500K, $1M, and

$2M.

The per policy period aggregate limit is two times the

occurrence limit and applies separately for claims from the

products-completed operations hazard* and for claims from

all other covered liability hazards

Example: An insured purchases an occurrence liability limit

of $300K. That means their Products-Completed Operations

Aggregate Limit is $600K and their General Liability

Aggregate Limit is $600K.

This is expressed as 300/600/600.

Three months into the policy period, they have a products-

completed operations claim with damages of $500K. Since

the per occurrence limit is only $300K, we would only pay

$300K for that claim. This also means that they only have

$300K for the rest of the policy period to cover any future

products-completed operations related claims. However,

they still have $600K that can be used for any other type of

covered liability claim (subject to the $300K per occurrence

limit).

Business Income and Extra Expense Deductibles Medical Payments

Coverage for loss of Business Income resulting from

suspension of business operations due to direct

damage from a covered loss to property at the insured

premises and/or for expenses incurred in an effort to

avoid or minimize the suspension of business

operations is included with every policy.

There is no dollar limit; in general, coverage exists for

12 months from the date of damage.

The base property deductible is $1,000 which may

be increased to $2,500, $5,000, or $10,000.

• Optional Windstorm/Hail percentage

deductibles of 1%, 2%, and 5% are available.

$10K per person for injuries on the insured’s premises or

involving the insured’s operations regardless of fault.

Defense Costs

Coverage for cost of defending lawsuits for covered

damages. There is no dollar limit; however, we do not owe

for additional defense costs once the applicable liability limit

has been exhausted by payment of judgements or

settlements.

Tenants Fire Liability $50K in coverage for property damage by fire to a premises

rented by the insured with increased limits of $100K and

$300K available.

Back to Table of Contents Updated 03-20-17

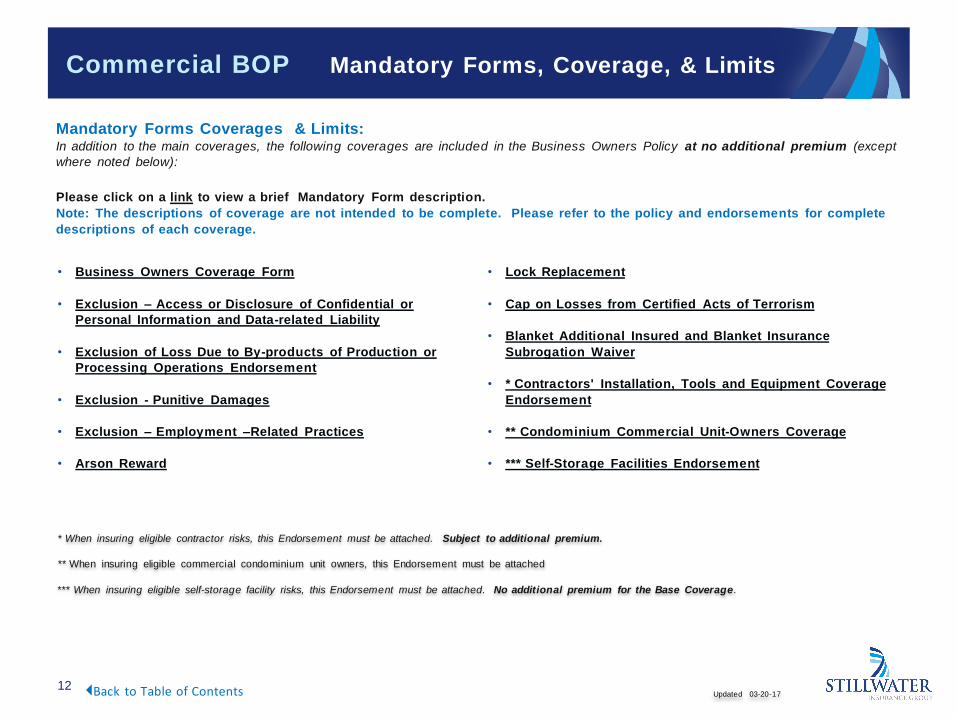

Commercial BOP Mandatory Forms, Coverage, & Limits

12 Updated 03-20-17

• Business Owners Coverage Form

• Exclusion – Access or Disclosure of Confidential or

Personal Information and Data-related Liability

• Exclusion of Loss Due to By-products of Production or

Processing Operations Endorsement

• Exclusion - Punitive Damages

• Exclusion – Employment –Related Practices

• Arson Reward

• Lock Replacement

• Cap on Losses from Certified Acts of Terrorism

• Blanket Additional Insured and Blanket Insurance

Subrogation Waiver

• * Contractors' Installation, Tools and Equipment Coverage

Endorsement

• ** Condominium Commercial Unit-Owners Coverage

• *** Self-Storage Facilities Endorsement

Back to Table of Contents

Mandatory Forms Coverages & Limits: In addition to the main coverages, the following coverages are included in the Business Owners Policy at no additional premium (except

where noted below):

Please click on a link to view a brief Mandatory Form description.

Note: The descriptions of coverage are not intended to be complete. Please refer to the policy and endorsements for complete

descriptions of each coverage.

* When insuring eligible contractor risks, this Endorsement must be attached. Subject to additional premium.

** When insuring eligible commercial condominium unit owners, this Endorsement must be attached

*** When insuring eligible self-storage facility risks, this Endorsement must be attached. No additional premium for the Base Coverage.

Commercial BOP Mandatory Forms, Coverage, & Limits

13

Updated 03-20-17

Business Owners Coverage Form: (BP 00 03)

Property Coverage

• Coverage is provided for direct physical loss or damage to Building and/or

Business Personal Property, as well as for Business Income and Extra

Expense.

Liability and Medical Expenses Coverage

• Liability and Medical Expenses Coverage is provided on a comprehensive

occurrence basis for all operations and premises owned, operated or leased

by the insured. Coverage includes Bodily Injury, Property Damage, Medical

Expenses (subject to an additional "per person" limit), Personal and

Advertising Injury and Tenant's Fire Liability Coverage (subject to a separate

limit).

Limits of Insurance

• Liability and Medical Expenses Coverage is provided at a basic limit of

insurance of $300,000 per occurrence which may be increased to either

$500,000, $1,000,000, or $2,000,000.

• An aggregate limit of twice the per occurrence limit applies for all hazards

other than Products-Completed Operations.

• An aggregate limit of twice the per occurrence limit applies separately for

Products-Completed Operations hazard.

• Tenant's Fire Liability Coverage is provided at a basic limit of $50,000, with

increased limits of $100,000 and $300,000 available, and is a separate limit.

• A "per person" Medical Expenses limit of $10,000 applies which may be

decreased to $5,000.

Deductibles

• The base property deductible is $1,000 which may be increased to $2,500,

$5,000, or $10,000.

• The policy’s property deductible is applicable to all property coverages

unless otherwise noted in the description for a specific coverage.

• There is no deductible for liability coverages unless otherwise noted in the

description for a specific coverage.

• Optional Windstorm/Hail percentage deductibles of 1%, 2%, and 5% are

available. (Use SB 03 01 for Wind/Hail deductibles)

Back to Mandatory Form Menu

Exclusion – Access or Disclosure of Confidential or

Personal Information and Data-related Liability (BP 15 05

or BP 15 06)

Description of Coverages

• Exclusion – Access or Disclosure of Confidential or Personal

Information and Data-related Liability – Limited Bodily Injury

Exception Not Included Endorsement: (BP 15 05) - This endorsement

excludes liability arising out of any access to or disclosure of any person's

or organization's confidential or personal information.

• Exclusion – Access or Disclosure of Confidential or Personal

Information (Personal and Advertising Injury Only) Endorsement: (BP

15 06) - This endorsement excludes liability arising out of any access to or

disclosure of any person's or organization's confidential or personal

information only with respect to personal and advertising injury.

Note/Rule

• BP 15 05 should be attached to all policies unless Electronic Data Liability

– Broad Coverage BP 05 96 is attached to the policy; in which case BP 15

06 should be attached in lieu of BP 15 05.

Premium Modification

• There is no premium impact associated with either of these.

Exclusion of Loss Due to By-products of Production or

Processing Operations Endorsement: (SB 04 17)

Description of Coverage

• This endorsement explicitly excludes coverage for Property Damage or

Business Interruption resulting from any substance released in the course

of production or processing operations. SB 04 17 must be attached to all

policies.

Premium Modification

• There is no premium impact associated with this endorsement.

Back to Table of Contents

Commercial BOP Mandatory Forms, Coverage, & Limits

14

Updated 03-20-17

Exclusion - Punitive Damages: (SB 04 03)

Description of Coverage

• This endorsement explicitly excludes coverage for punitive or exemplary

damages imposed on any insured. SB 04 03 must be attached to all

policies.

Premium Modification

• There is no premium impact associated with this endorsement.

Exclusion – Employment – Related Practices: (BP 04 17)

Description of Coverage

• This endorsement explicitly excludes coverage bodily injury and personal

injury arising out of employment-related practices. BP 04 17 must be

attached to all policies.

Premium Modification

• There is no premium impact associated with this endorsement.

Arson Reward: (SB 04 02)

Description of Coverage

• Coverage is provided for the payment of a reward on the named insureds

behalf for information leading to an arson conviction in connection with a fire

at a covered property, subject to a limit of 10% of the amount paid for the

direct physical loss, or damage to, the covered property up to a maximum of

$10,000. SB 04 02 must be attached to all policies.

Premium Modification

• There is no premium impact associated with this endorsement.

Note:

• Do not attach SB 04 02 if BP 07 78 (Restaurants) is attached.

Lock Replacement: (SB 04 06)

Description of Coverage

• $1,000 of coverage is provided for the cost of replacing locks on an insured

premises made necessary by a lost or stolen key. SB 04 06 must be

attached to all policies.

Premium Modification

• There is no premium impact associated with this endorsement.

Note:

• Do not attach SB 04 06 if BP 07 78 (Restaurants) is attached.

Cap on Losses from Certified Acts of Terrorism: (BP 05 23

and BP 05 15)

Description of Coverage

• BP 05 23 specifies that covered losses resulting from certified acts of

terrorism are subject to the statutory cap on liability for losses as established

by the Terrorism Risk Insurance Act (TRIA). BP 05 15 discloses information

related to the Terrorism Risk Insurance Act. BP 05 23 and BP 05 15 must be

attached to all policies.

Premium Modification

• There is no premium impact associated with these endorsements.

Blanket Additional Insured and Blanket Insurance

Subrogation Waiver: (SB 04 36)

Description of Coverage

• Blanket Additional Insured - SB 04 36 automatically provides coverage for

any entity having a written agreement to be listed as an Additional Insured.

• Insurance Subrogation Waiver - declares that when there is an Additional

Insured, our policy is primary , and we will not seek contribution from that

Additional Insured’s carrier.

Premium Modification

• There is no premium impact associated with this endorsement.

Note

• See Miscellaneous Rules page for more details.

Back to Table of Contents

Back to Mandatory Form Menu

Commercial BOP Mandatory Forms, Coverage, & Limits

15

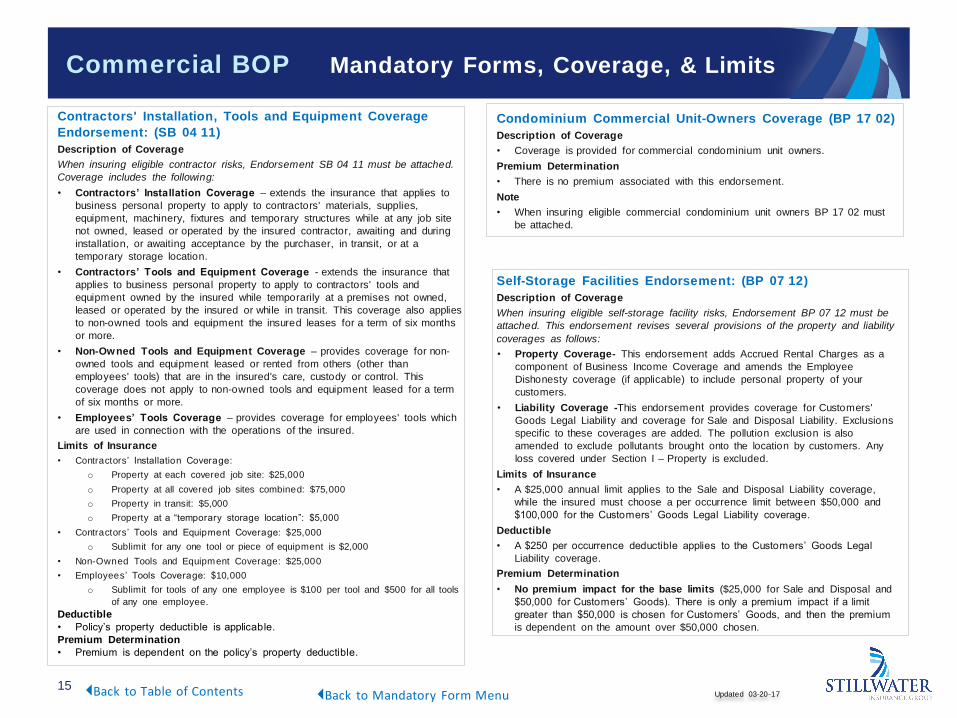

Contractors' Installation, Tools and Equipment Coverage

Endorsement: (SB 04 11)

Description of Coverage

When insuring eligible contractor risks, Endorsement SB 04 11 must be attached.

Coverage includes the following:

• Contractors’ Installation Coverage – extends the insurance that applies to

business personal property to apply to contractors' materials, supplies,

equipment, machinery, fixtures and temporary structures while at any job site

not owned, leased or operated by the insured contractor, awaiting and during

installation, or awaiting acceptance by the purchaser, in transit, or at a

temporary storage location.

• Contractors’ Tools and Equipment Coverage - extends the insurance that

applies to business personal property to apply to contractors' tools and

equipment owned by the insured while temporarily at a premises not owned,

leased or operated by the insured or while in transit. This coverage also applies

to non-owned tools and equipment the insured leases for a term of six months

or more.

• Non-Owned Tools and Equipment Coverage – provides coverage for non-

owned tools and equipment leased or rented from others (other than

employees' tools) that are in the insured's care, custody or control. This

coverage does not apply to non-owned tools and equipment leased for a term

of six months or more.

• Employees’ Tools Coverage – provides coverage for employees' tools which

are used in connection with the operations of the insured.

Limits of Insurance

• Contractors’ Installation Coverage:

o Property at each covered job site: $25,000

o Property at all covered job sites combined: $75,000

o Property in transit: $5,000

o Property at a “temporary storage location”: $5,000

• Contractors’ Tools and Equipment Coverage: $25,000

o Sublimit for any one tool or piece of equipment is $2,000

• Non-Owned Tools and Equipment Coverage: $25,000

• Employees’ Tools Coverage: $10,000

o Sublimit for tools of any one employee is $100 per tool and $500 for all tools

of any one employee.

Deductible

• Policy’s property deductible is applicable.

Premium Determination

• Premium is dependent on the policy’s property deductible.

Updated 03-20-17

Condominium Commercial Unit-Owners Coverage (BP 17 02)

Description of Coverage

• Coverage is provided for commercial condominium unit owners.

Premium Determination

• There is no premium associated with this endorsement.

Note

• When insuring eligible commercial condominium unit owners BP 17 02 must

be attached.

Self-Storage Facilities Endorsement: (BP 07 12)

Description of Coverage

When insuring eligible self-storage facility risks, Endorsement BP 07 12 must be

attached. This endorsement revises several provisions of the property and liability

coverages as follows:

• Property Coverage- This endorsement adds Accrued Rental Charges as a

component of Business Income Coverage and amends the Employee

Dishonesty coverage (if applicable) to include personal property of your

customers.

• Liability Coverage -This endorsement provides coverage for Customers'

Goods Legal Liability and coverage for Sale and Disposal Liability. Exclusions

specific to these coverages are added. The pollution exclusion is also

amended to exclude pollutants brought onto the location by customers. Any

loss covered under Section I – Property is excluded.

Limits of Insurance

• A $25,000 annual limit applies to the Sale and Disposal Liability coverage,

while the insured must choose a per occurrence limit between $50,000 and

$100,000 for the Customers’ Goods Legal Liability coverage.

Deductible

• A $250 per occurrence deductible applies to the Customers’ Goods Legal

Liability coverage.

Premium Determination

• No premium impact for the base limits ($25,000 for Sale and Disposal and

$50,000 for Customers’ Goods). There is only a premium impact if a limit

greater than $50,000 is chosen for Customers’ Goods, and then the premium

is dependent on the amount over $50,000 chosen.

Back to Table of Contents Back to Mandatory Form Menu

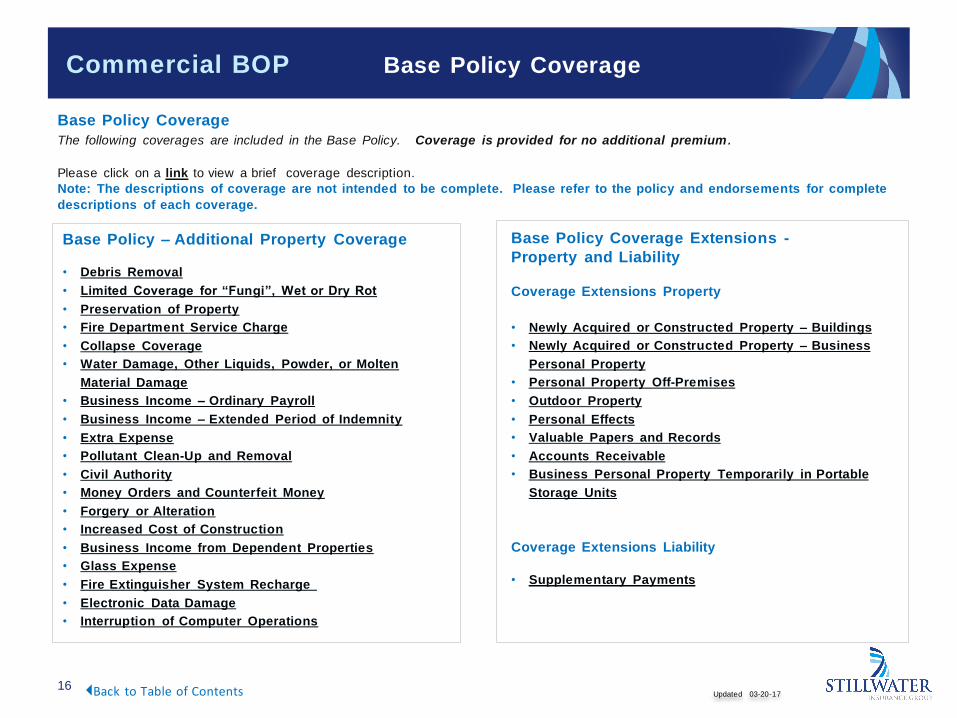

Commercial BOP Base Policy Coverage

16 Updated 03-20-17 Back to Table of Contents

Base Policy – Additional Property Coverage

• Debris Removal

• Limited Coverage for “Fungi”, Wet or Dry Rot

• Preservation of Property

• Fire Department Service Charge

• Collapse Coverage

• Water Damage, Other Liquids, Powder, or Molten

Material Damage

• Business Income – Ordinary Payroll

• Business Income – Extended Period of Indemnity

• Extra Expense

• Pollutant Clean-Up and Removal

• Civil Authority

• Money Orders and Counterfeit Money

• Forgery or Alteration

• Increased Cost of Construction

• Business Income from Dependent Properties

• Glass Expense

• Fire Extinguisher System Recharge

• Electronic Data Damage

• Interruption of Computer Operations

Base Policy Coverage Extensions -

Property and Liability

Coverage Extensions Property

• Newly Acquired or Constructed Property – Buildings

• Newly Acquired or Constructed Property – Business

Personal Property

• Personal Property Off-Premises

• Outdoor Property

• Personal Effects

• Valuable Papers and Records

• Accounts Receivable

• Business Personal Property Temporarily in Portable

Storage Units

Coverage Extensions Liability

• Supplementary Payments

Base Policy Coverage

The following coverages are included in the Base Policy. Coverage is provided for no additional premium.

Please click on a link to view a brief coverage description.

Note: The descriptions of coverage are not intended to be complete. Please refer to the policy and endorsements for complete

descriptions of each coverage.

Commercial BOP Base Policy – Additional Property Coverage

17

Debris Removal: Description of Coverage

• Coverage is provided for removal of debris that is caused by or results from a

covered cause of loss at a limit of 25% of the sum of the deductible plus the

amount paid for the direct physical loss or damage to the covered property.

However, if the combined amounts of the direct physical loss or damage and

the debris removal exceed the limit of insurance, an additional amount of up

to $25,000 for Debris Removal is available.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Limited Coverage for “Fungi”, Wet or Dry Rot: Description of Coverage

• $15,000 (per year aggregate) of coverage for loss or damage from fungi, wet

rot, or dry rot when the loss or damage is the result of a “specified cause of

loss” other than fire or lightning that occurs during the policy period.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Preservation of Property: Description of Coverage

• Coverage is provided to covered property that suffers direct physical loss or

damage while it is being moved or while temporarily stored at another

location, when it was necessary to move that property to preserve it form

loss or damage by a covered cause of loss. Loss or damage must occur

within 30 days after the property is first moved.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Fire Department Service Charge:

Description of Coverage

• $2,500 (at each premises) of coverage for fire department service charges is

provided in the base Business Owners coverage form. Increased limits are

not offered.

Deductible

• No deductible applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Collapse Coverage:

Description of Coverage

• Coverage is provided for direct physical loss or damage to covered property

(building and/or personal property) from the collapse of a building or a part of

a building

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Water Damage, Other Liquids, Powder, or Molten Material

Damage: Description of Coverage

• Coverage is provided for the cost to tear out and replace any part of the

building or structure in order to repair damage to a system from which water

or other substance escaped, when there is a covered loss caused by such

substance.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Base Policy – Additional Property Coverage

18

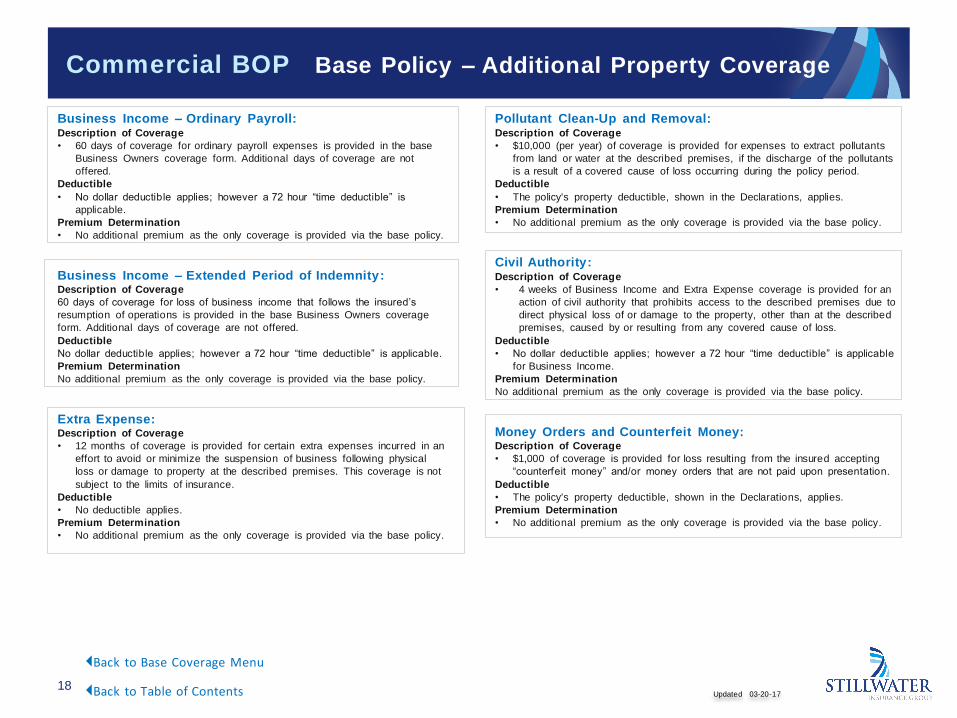

Business Income – Ordinary Payroll: Description of Coverage

• 60 days of coverage for ordinary payroll expenses is provided in the base

Business Owners coverage form. Additional days of coverage are not

offered.

Deductible

• No dollar deductible applies; however a 72 hour “time deductible” is

applicable.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Business Income – Extended Period of Indemnity: Description of Coverage

60 days of coverage for loss of business income that follows the insured’s

resumption of operations is provided in the base Business Owners coverage

form. Additional days of coverage are not offered.

Deductible

No dollar deductible applies; however a 72 hour “time deductible” is applicable.

Premium Determination

No additional premium as the only coverage is provided via the base policy.

Extra Expense: Description of Coverage

• 12 months of coverage is provided for certain extra expenses incurred in an

effort to avoid or minimize the suspension of business following physical

loss or damage to property at the described premises. This coverage is not

subject to the limits of insurance.

Deductible

• No deductible applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Pollutant Clean-Up and Removal: Description of Coverage

• $10,000 (per year) of coverage is provided for expenses to extract pollutants

from land or water at the described premises, if the discharge of the pollutants

is a result of a covered cause of loss occurring during the policy period.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Civil Authority: Description of Coverage

• 4 weeks of Business Income and Extra Expense coverage is provided for an

action of civil authority that prohibits access to the described premises due to

direct physical loss of or damage to the property, other than at the described

premises, caused by or resulting from any covered cause of loss.

Deductible

• No dollar deductible applies; however a 72 hour “time deductible” is applicable

for Business Income.

Premium Determination

No additional premium as the only coverage is provided via the base policy.

Money Orders and Counterfeit Money: Description of Coverage

• $1,000 of coverage is provided for loss resulting from the insured accepting

“counterfeit money” and/or money orders that are not paid upon presentation.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Base Policy – Additional Property Coverage

19

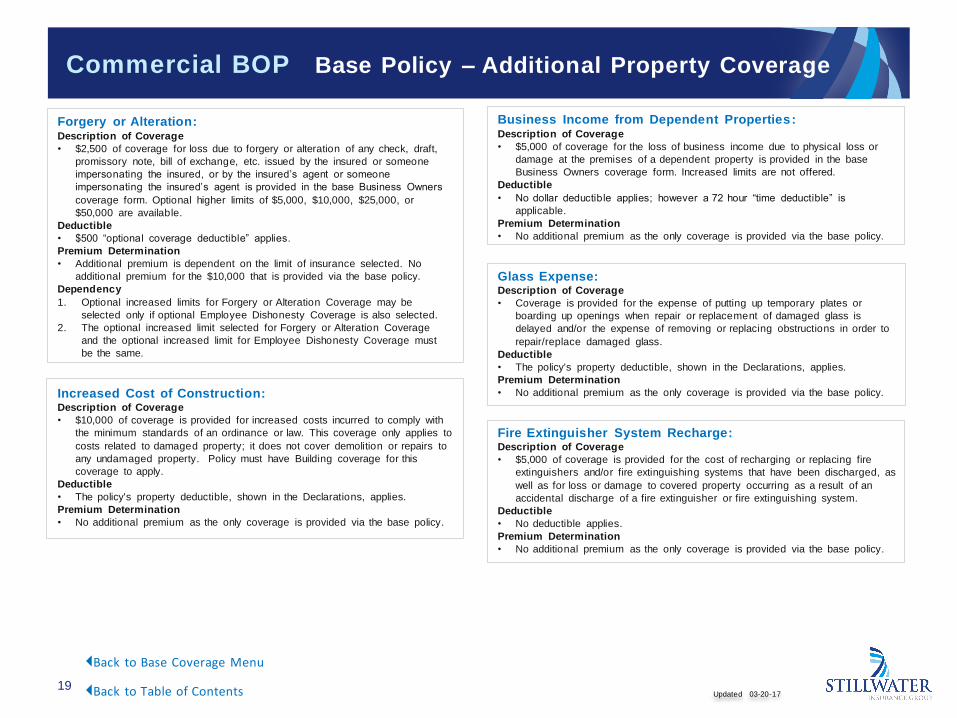

Forgery or Alteration: Description of Coverage

• $2,500 of coverage for loss due to forgery or alteration of any check, draft,

promissory note, bill of exchange, etc. issued by the insured or someone

impersonating the insured, or by the insured’s agent or someone

impersonating the insured’s agent is provided in the base Business Owners

coverage form. Optional higher limits of $5,000, $10,000, $25,000, or

$50,000 are available.

Deductible

• $500 “optional coverage deductible” applies.

Premium Determination

• Additional premium is dependent on the limit of insurance selected. No

additional premium for the $10,000 that is provided via the base policy.

Dependency

1. Optional increased limits for Forgery or Alteration Coverage may be

selected only if optional Employee Dishonesty Coverage is also selected.

2. The optional increased limit selected for Forgery or Alteration Coverage

and the optional increased limit for Employee Dishonesty Coverage must

be the same.

Increased Cost of Construction: Description of Coverage

• $10,000 of coverage is provided for increased costs incurred to comply with

the minimum standards of an ordinance or law. This coverage only applies to

costs related to damaged property; it does not cover demolition or repairs to

any undamaged property. Policy must have Building coverage for this

coverage to apply.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Business Income from Dependent Properties: Description of Coverage

• $5,000 of coverage for the loss of business income due to physical loss or

damage at the premises of a dependent property is provided in the base

Business Owners coverage form. Increased limits are not offered.

Deductible

• No dollar deductible applies; however a 72 hour “time deductible” is

applicable.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Glass Expense: Description of Coverage

• Coverage is provided for the expense of putting up temporary plates or

boarding up openings when repair or replacement of damaged glass is

delayed and/or the expense of removing or replacing obstructions in order to

repair/replace damaged glass.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Fire Extinguisher System Recharge: Description of Coverage

• $5,000 of coverage is provided for the cost of recharging or replacing fire

extinguishers and/or fire extinguishing systems that have been discharged, as

well as for loss or damage to covered property occurring as a result of an

accidental discharge of a fire extinguisher or fire extinguishing system.

Deductible

• No deductible applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Base Policy – Additional Property Coverage

20

Electronic Data Damage: Description of Coverage

• Electronic data (other than electronic data which is integrated in and

operates or controls the building's elevator, lighting, heating, ventilation, air

conditioning or security system) is Property Not Covered, except as

provided under this Additional Coverage, which provides coverage for the

cost to replace or restore electronic data that has been destroyed or

corrupted by a Covered Cause Of Loss. Coverage is subject to an annual

aggregate limit of $10,000. The aggregate limit is the maximum payable in

any one policy year, regardless of the number of occurrences of loss or

damage or the number of premises, locations or computer systems

involved. The Additional Coverage – Electronic Data does not apply to

electronic data which is integrated in and operates or controls a building's

elevator, lighting, heating, ventilation, air conditioning or security system,

because such electronic data is Covered Property as part of coverage on

the building. Increased limits are not offered. Policy must have BPP

coverage for this coverage to apply.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base

policy.

Interruption of Computer Operations: Description of Coverage

• $10,000 of coverage for Business Income and Extra Expenses applicable to

loss sustained in a suspension of operations due to destruction or corruption

of electronic data by a Covered Cause of Loss is provided in the base

Business Owners coverage form. The aggregate limit is the maximum

payable in any one policy year, regardless of the number of interruptions or

the number of premises, locations or computer systems involved. This

coverage does not apply when loss or damage to electronic data involves

only electronic data which is integrated in and operates or controls a

building's elevator, lighting, heating, ventilation, air conditioning or security

system, because such electronic data is Covered Property as part of

coverage on the building. Increased limits are not offered. Policy must have

BPP coverage for this coverage to apply.

Deductible

• No dollar deductible applies; however a 72 hour “time deductible” is

applicable for Business Income (not Extra Expense).

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Base Policy Coverage Extensions –Property

21

Newly Acquired or Constructed Property - Buildings: Description of Coverage

• $250,000 of temporary property coverage for new buildings while being built

on the described premises and/or buildings acquired at a premises other

than one that is described on the declarations; as long as the acquired

building is intended for a similar use as that of the building described in the

declarations or is intended for use as a warehouse. This temporary

coverage expires 30 days after the acquisition of the property or 30 days

after the beginning of construction.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Newly Acquired or Constructed Property – Business

Personal Property: Description of Coverage

• $100,000 of temporary property coverage for Business Personal Property at

newly acquired premises and/or at newly constructed or acquired buildings

at a premises described in the declarations. This temporary coverage

expires 30 days after the acquisition of the property or 30 days after the

beginning of construction.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Personal Property Off-Premises: Description of Coverage

• $10,000 of property coverage for covered property (other than money,

securities, valuable papers and records, or accounts receivable) while it is in

the course of transit or at a premises that the insured does not own, lease,

or operate.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Outdoor Property: Description of Coverage

• $2,500 of coverage for outdoor property is provided under the Coverage

Extensions Section of the Business Owners Coverage Form. Increased limits

are not offered.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Personal Effects: Description of Coverage

• $2,500 of property coverage for personal effects owned by the insured

and/or an officer, partner, employee, etc. of the insured. Tools or equipment

used in the insured’s business and/or loss or damage by theft is not covered.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Valuable Papers and Records: Description of Coverage

• $10,000 of on-premises coverage and $5,000 of off-premises coverage is

provided for valuable papers and records owned by the insured or in the

insured’s care, custody, or control.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Base Policy Coverage Extensions

Property / Liability

22

Coverage Extensions Property (cont.):

Accounts Receivable: Description of Coverage

• $10,000 of on-premises and $5,000 of off-premises coverage is provided for

loss or damage to the insured’s records of accounts receivable. Increased

limits (on-premises only) of $25,000, $50,000, and $100,000 are available

for additional premium. Policy must have BPP coverage for this coverage to

apply.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• Additional premium is dependent on the limit of insurance selected. No

additional premium for the $10,000 that is provided via the base policy.

Business Personal Property Temporarily in Portable

Storage Units: Description of Coverage

• $10,000 of coverage is provided for Business Personal Property temporarily

stored in a portable storage unit located within 100 feet of the described

premises. This coverage is only valid for the first 90 days that the storage

unit is in place. Increased limits are not offered.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Coverage Extension Liability:

Supplementary Payments: Description of Coverage

The following liability costs and/or expenses are in addition to the limit of

insurance.

• All expenses that we (the insurer) incur in defending a claim or suit against

the insured.

• Up to $250 for cost of bail bonds required because of accidents or traffic

violations arising out of the use of vehicles to which BI Liability coverage

applies.

• The cost of bonds to release attachments.

• Reasonable expenses the insured incurs at our (the insurer) request to assist

in the investigation of defense of a claim or suit. This includes up to $250/day

for time off from work.

• All court costs taxed against the insured in a suit, not including attorneys’

fees or attorneys’ expenses taxed against the insured.

• Prejudgment interest awarded against the insured. However, when an offer is

made to pay the Limit of Insurance, prejudgment interest will not be paid for

the period after that offer.

• Interest that accrues between the time a judgment is entered and

subsequently paid.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• No additional premium as the only coverage is provided via the base policy.

Back to Table of Contents

Back to Base Coverage Menu

Updated 03-20-17

Commercial BOP Endorsements

23 Updated 03-20-17 Back to Table of Contents

Property Coverages

• Outdoor Signs

• Money and Securities

• Employee Dishonesty

• Equipment Breakdown

• Computer Fraud and

Funds Transfer Fraud

Coverage

• Loss Payable Clauses

• Ordinance or Law

• Spoilage Coverage

• Utility Services Coverage

• Vacancy Permit Coverage

• Identity Fraud Expense

Coverage

• Fine Arts Coverage

• Water Back-up and Sump

Overflow

• Increased Cost of Loss and

Related Expenses for

Green Upgrades

• Wind/Hail Exclusion

• Condo Commercial Unit-

owners Optional

Coverages

Additional Insured

• Blanket Additional Insured

and Blanket Insurance

Subrogation Waiver

Liability Coverages

• Abuse or Molestation

Exclusion

• Electronic Data Liability –

Broad Coverage

• Employee Benefits Liability

• Exclusion-Personal and

Advertising Injury

• Hired Auto and Non-owned

Auto Liability

• Employment-related

Practices Liability

• Limitation of Coverage to

Designated Premises or

Project

• Exclusion – Products

Completed Operations

• Exclusion – Personal and

Advertising Injury –

Lawyers

• Liquor Liability

Specific Classes

• Barber Shops and Hair

Salons Professional

Liability

• Beauty Salons

Professional Liability

• Funeral Directors

Professional Liability

• Optical and Hearing Aid

Establishments

Professional Liability

• Printer’s Errors and

Omissions Liability

• Veterinarians Professional

Liability

• Pastoral Counseling

Professional Liability

• Extended Medical

Payments Churches

• Residential Cleaning

Services

• Photography Endorsement • Restaurants Endorsement

Endorsements • All Endorsements to existing policies must be requested via fax or email:

• The following Endorsements are available depending on the class of Business.

Coverage can be purchased for additional premium.

Please click on a link to view a brief coverage description.

Note: The descriptions of coverage are not intended to be complete. Please refer to the policy and endorsements for complete

descriptions of each coverage.

Fax: 1.866.300.8027

Email: [email protected]

Commercial BOP Endorsements – Property Coverage

24

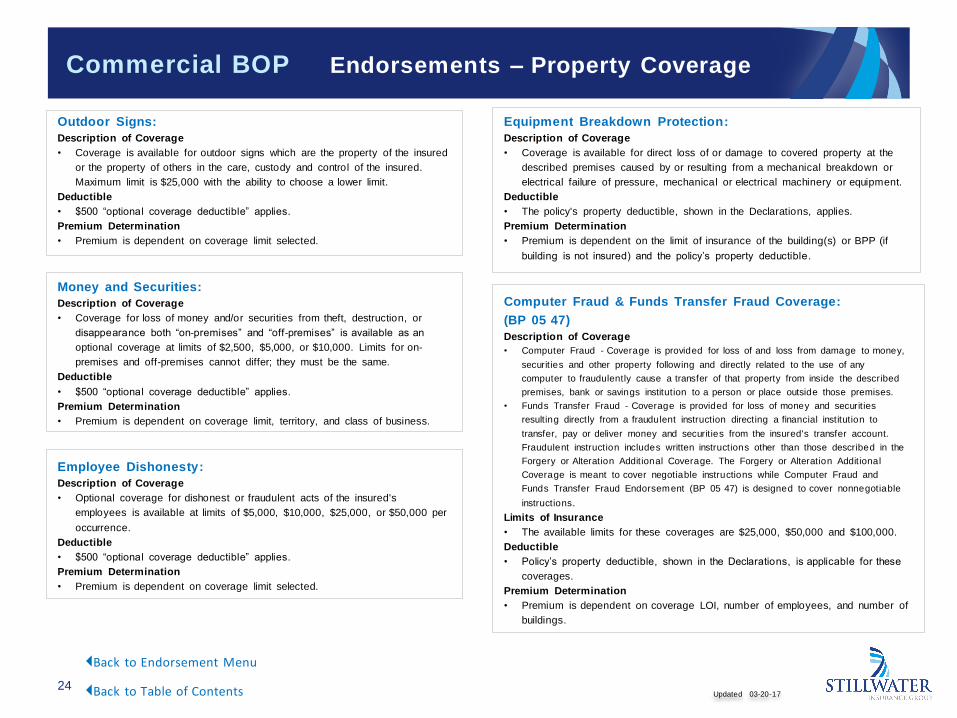

Outdoor Signs: Description of Coverage

• Coverage is available for outdoor signs which are the property of the insured

or the property of others in the care, custody and control of the insured.

Maximum limit is $25,000 with the ability to choose a lower limit.

Deductible

• $500 “optional coverage deductible” applies.

Premium Determination

• Premium is dependent on coverage limit selected.

Money and Securities: Description of Coverage

• Coverage for loss of money and/or securities from theft, destruction, or

disappearance both “on-premises” and “off-premises” is available as an

optional coverage at limits of $2,500, $5,000, or $10,000. Limits for on-

premises and off-premises cannot differ; they must be the same.

Deductible

• $500 “optional coverage deductible” applies.

Premium Determination

• Premium is dependent on coverage limit, territory, and class of business.

Employee Dishonesty:

Description of Coverage

• Optional coverage for dishonest or fraudulent acts of the insured's

employees is available at limits of $5,000, $10,000, $25,000, or $50,000 per

occurrence.

Deductible

• $500 “optional coverage deductible” applies.

Premium Determination

• Premium is dependent on coverage limit selected.

Equipment Breakdown Protection:

Description of Coverage

• Coverage is available for direct loss of or damage to covered property at the

described premises caused by or resulting from a mechanical breakdown or

electrical failure of pressure, mechanical or electrical machinery or equipment.

Deductible

• The policy's property deductible, shown in the Declarations, applies.

Premium Determination

• Premium is dependent on the limit of insurance of the building(s) or BPP (if

building is not insured) and the policy’s property deductible.

Computer Fraud & Funds Transfer Fraud Coverage:

(BP 05 47)

Description of Coverage

• Computer Fraud - Coverage is provided for loss of and loss from damage to money,

securities and other property following and directly related to the use of any

computer to fraudulently cause a transfer of that property from inside the described

premises, bank or savings institution to a person or place outside those premises.

• Funds Transfer Fraud - Coverage is provided for loss of money and securities

resulting directly from a fraudulent instruction directing a financial institution to

transfer, pay or deliver money and securities from the insured's transfer account.

Fraudulent instruction includes written instructions other than those described in the

Forgery or Alteration Additional Coverage. The Forgery or Alteration Additional

Coverage is meant to cover negotiable instructions while Computer Fraud and

Funds Transfer Fraud Endorsement (BP 05 47) is designed to cover nonnegotiable

instructions.

Limits of Insurance

• The available limits for these coverages are $25,000, $50,000 and $100,000.

Deductible

• Policy’s property deductible, shown in the Declarations, is applicable for these

coverages.

Premium Determination

• Premium is dependent on coverage LOI, number of employees, and number of

buildings.

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Property Coverage

25

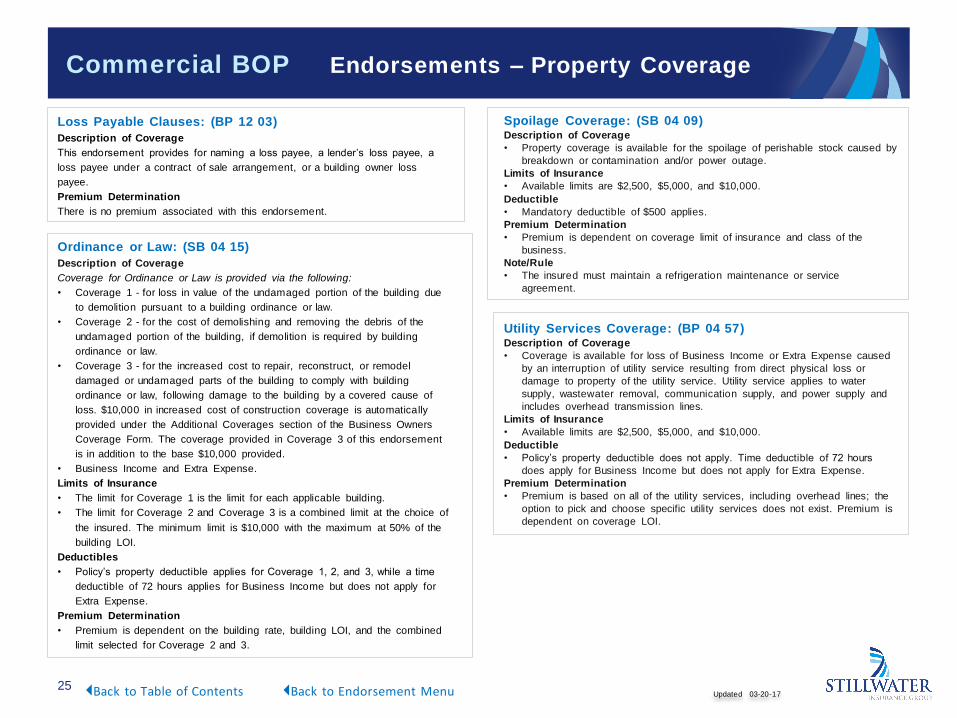

Loss Payable Clauses: (BP 12 03) Description of Coverage

This endorsement provides for naming a loss payee, a lender’s loss payee, a

loss payee under a contract of sale arrangement, or a building owner loss

payee.

Premium Determination

There is no premium associated with this endorsement.

Ordinance or Law: (SB 04 15) Description of Coverage

Coverage for Ordinance or Law is provided via the following:

• Coverage 1 - for loss in value of the undamaged portion of the building due

to demolition pursuant to a building ordinance or law.

• Coverage 2 - for the cost of demolishing and removing the debris of the

undamaged portion of the building, if demolition is required by building

ordinance or law.

• Coverage 3 - for the increased cost to repair, reconstruct, or remodel

damaged or undamaged parts of the building to comply with building

ordinance or law, following damage to the building by a covered cause of

loss. $10,000 in increased cost of construction coverage is automatically

provided under the Additional Coverages section of the Business Owners

Coverage Form. The coverage provided in Coverage 3 of this endorsement

is in addition to the base $10,000 provided.

• Business Income and Extra Expense.

Limits of Insurance

• The limit for Coverage 1 is the limit for each applicable building.

• The limit for Coverage 2 and Coverage 3 is a combined limit at the choice of

the insured. The minimum limit is $10,000 with the maximum at 50% of the

building LOI.

Deductibles

• Policy’s property deductible applies for Coverage 1, 2, and 3, while a time

deductible of 72 hours applies for Business Income but does not apply for

Extra Expense.

Premium Determination

• Premium is dependent on the building rate, building LOI, and the combined

limit selected for Coverage 2 and 3.

Spoilage Coverage: (SB 04 09) Description of Coverage

• Property coverage is available for the spoilage of perishable stock caused by

breakdown or contamination and/or power outage.

Limits of Insurance

• Available limits are $2,500, $5,000, and $10,000.

Deductible

• Mandatory deductible of $500 applies.

Premium Determination

• Premium is dependent on coverage limit of insurance and class of the

business.

Note/Rule

• The insured must maintain a refrigeration maintenance or service

agreement.

Utility Services Coverage: (BP 04 57) Description of Coverage

• Coverage is available for loss of Business Income or Extra Expense caused

by an interruption of utility service resulting from direct physical loss or

damage to property of the utility service. Utility service applies to water

supply, wastewater removal, communication supply, and power supply and

includes overhead transmission lines.

Limits of Insurance

• Available limits are $2,500, $5,000, and $10,000.

Deductible

• Policy’s property deductible does not apply. Time deductible of 72 hours

does apply for Business Income but does not apply for Extra Expense.

Premium Determination

• Premium is based on all of the utility services, including overhead lines; the

option to pick and choose specific utility services does not exist. Premium is

dependent on coverage LOI.

Back to Table of Contents Back to Endorsement Menu Updated 03-20-17

Commercial BOP Endorsements – Property Coverage

26

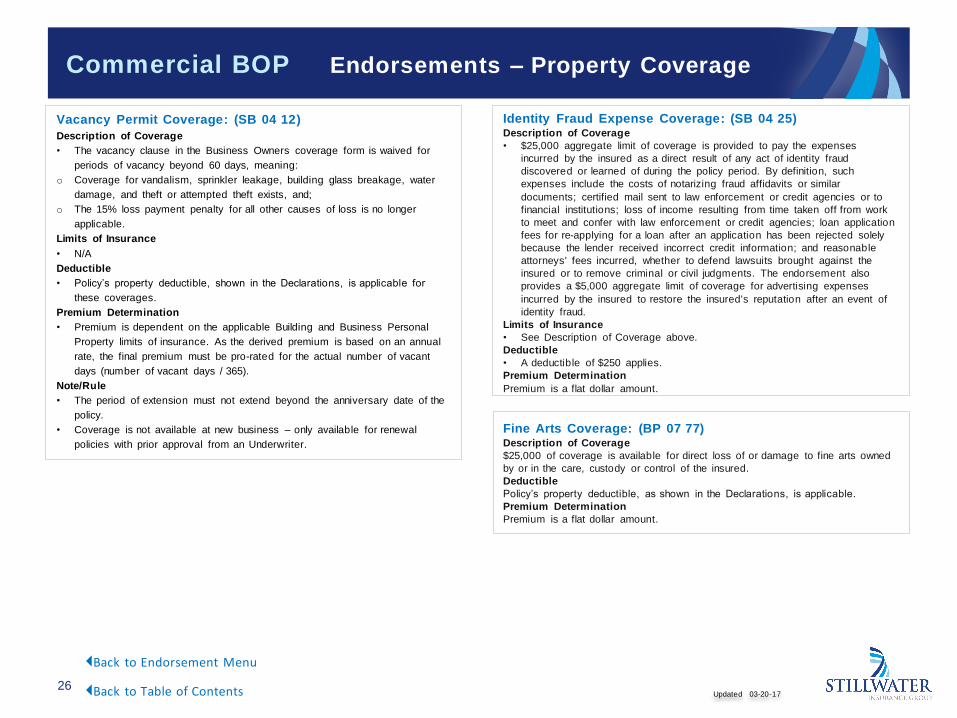

Vacancy Permit Coverage: (SB 04 12) Description of Coverage

• The vacancy clause in the Business Owners coverage form is waived for

periods of vacancy beyond 60 days, meaning:

o Coverage for vandalism, sprinkler leakage, building glass breakage, water

damage, and theft or attempted theft exists, and;

o The 15% loss payment penalty for all other causes of loss is no longer

applicable.

Limits of Insurance

• N/A

Deductible

• Policy’s property deductible, shown in the Declarations, is applicable for

these coverages.

Premium Determination

• Premium is dependent on the applicable Building and Business Personal

Property limits of insurance. As the derived premium is based on an annual

rate, the final premium must be pro-rated for the actual number of vacant

days (number of vacant days / 365).

Note/Rule

• The period of extension must not extend beyond the anniversary date of the

policy.

• Coverage is not available at new business – only available for renewal

policies with prior approval from an Underwriter.

Identity Fraud Expense Coverage: (SB 04 25) Description of Coverage

• $25,000 aggregate limit of coverage is provided to pay the expenses

incurred by the insured as a direct result of any act of identity fraud

discovered or learned of during the policy period. By definition, such

expenses include the costs of notarizing fraud affidavits or similar

documents; certified mail sent to law enforcement or credit agencies or to

financial institutions; loss of income resulting from time taken off from work

to meet and confer with law enforcement or credit agencies; loan application

fees for re-applying for a loan after an application has been rejected solely

because the lender received incorrect credit information; and reasonable

attorneys' fees incurred, whether to defend lawsuits brought against the

insured or to remove criminal or civil judgments. The endorsement also

provides a $5,000 aggregate limit of coverage for advertising expenses

incurred by the insured to restore the insured's reputation after an event of

identity fraud.

Limits of Insurance

• See Description of Coverage above.

Deductible

• A deductible of $250 applies.

Premium Determination

Premium is a flat dollar amount.

Fine Arts Coverage: (BP 07 77) Description of Coverage

$25,000 of coverage is available for direct loss of or damage to fine arts owned

by or in the care, custody or control of the insured.

Deductible

Policy’s property deductible, as shown in the Declarations, is applicable.

Premium Determination

Premium is a flat dollar amount.

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Property Coverage

27

Water Back-up and Sump Overflow: (SB 04 21) Description of Coverage

$5,000 of coverage is provided for loss or damage to Covered Property caused

by:

• Water which backs up through sewers or drains; or

• Water which overflows from a sump even if such overflow results from the

mechanical breakdown of the sump pump. This coverage does not apply to

direct physical loss of the sump pump, or related equipment, which is caused

by mechanical breakdown; and

• Business Income and Extra Expense losses sustained as a result of loss or

damage to Covered Property.

Limits of Insurance

• The limit is an annual aggregate limit and is per location. Increased limits of

$7,500, $10,000, and $25,000 are available for additional premium

Deductible

• The policy's property deductible, shown in the Declarations, applies to this

endorsement.

Premium Determination

• Premium is dependent on the coverage limit of insurance.

Increased Cost of Loss and Related Expenses for Green

Upgrades (SB 04 16) Description of Coverage

This endorsement amends various Section I – Property coverage provisions to

address green upgrades to real and personal property, and related expenses via

the following:

• Green Upgrade Coverage – modifies Replacement Cost Coverage to

address loss settlement of damaged property using more energy-efficient,

environmentally-preferable materials, products or methods in design,

construction, manufacture or operation as recognized by a Green standards-

setter.

• Business Interruption – the period of restoration is extended for up to 30

days to recognize the increased period of time attributable to green

upgrades and related expenses.

• Related Expenses – optional coverage is available for the following related

expenses with respect to property to which Green Upgrade Coverage

applies:

a. Waste reduction and recycling

b. Design and engineering professional fees

c. Certification fees and related equipment testing

d. Building air-out and related testing

Limits of Insurance

• The limit for Green Upgrade Coverage is 20% of the applicable Building

and/or BPP limit of insurance. No other limit is available.

• The limit for the optional Related Expenses coverage is $10,000. No other

limit is available.

Deductibles

• Policy’s property deductible applies.

Premium Determination

• Green Upgrade Coverage – premium is dependent on the Building and/or

BPP rate and Building and/or BPP LOI.

• Business Interruption – no additional premium (outside of that for Green

Upgrade Coverage).

• Related Expenses - premium is dependent on the Building and/or BPP rate.

Note

• Green Upgrade Coverage does not include Ordinance or Law coverage, and

therefore will not pay any additional cost above the cost of Green Upgrades,

solely for the purpose of satisfying an ordnance or law. Ordinance or Law

coverage is addressed in a separate endorsement (see rule 3 above).

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Property Coverage

28

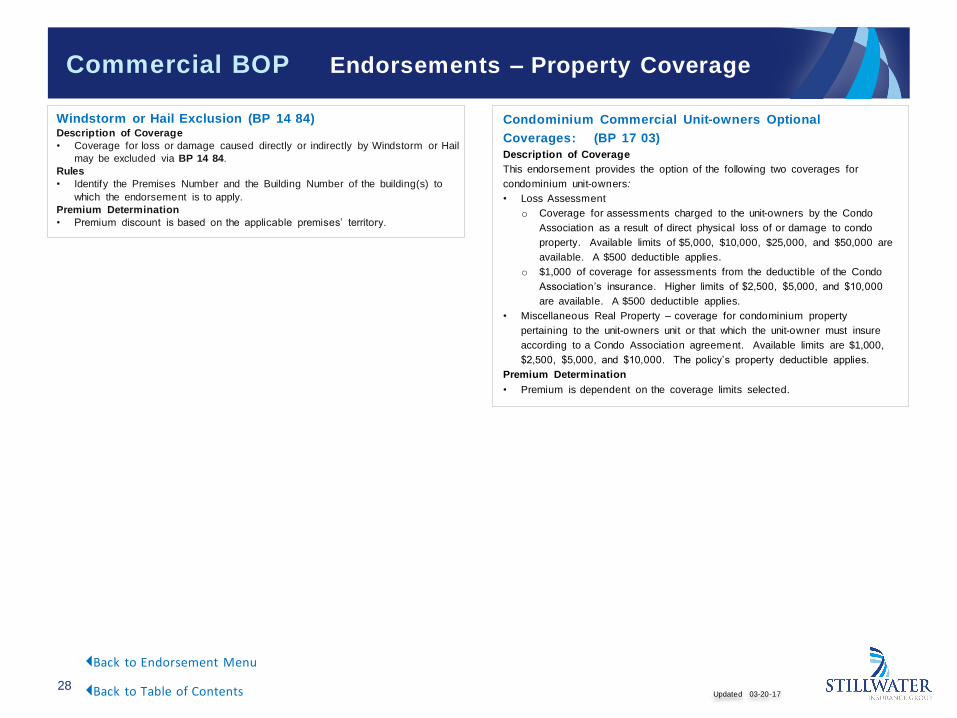

Windstorm or Hail Exclusion (BP 14 84) Description of Coverage

• Coverage for loss or damage caused directly or indirectly by Windstorm or Hail

may be excluded via BP 14 84.

Rules

• Identify the Premises Number and the Building Number of the building(s) to

which the endorsement is to apply.

Premium Determination

• Premium discount is based on the applicable premises’ territory.

Condominium Commercial Unit-owners Optional

Coverages: (BP 17 03) Description of Coverage

This endorsement provides the option of the following two coverages for

condominium unit-owners:

• Loss Assessment

o Coverage for assessments charged to the unit-owners by the Condo

Association as a result of direct physical loss of or damage to condo

property. Available limits of $5,000, $10,000, $25,000, and $50,000 are

available. A $500 deductible applies.

o $1,000 of coverage for assessments from the deductible of the Condo

Association’s insurance. Higher limits of $2,500, $5,000, and $10,000

are available. A $500 deductible applies.

• Miscellaneous Real Property – coverage for condominium property

pertaining to the unit-owners unit or that which the unit-owner must insure

according to a Condo Association agreement. Available limits are $1,000,

$2,500, $5,000, and $10,000. The policy’s property deductible applies.

Premium Determination

• Premium is dependent on the coverage limits selected.

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Liability Coverage

29

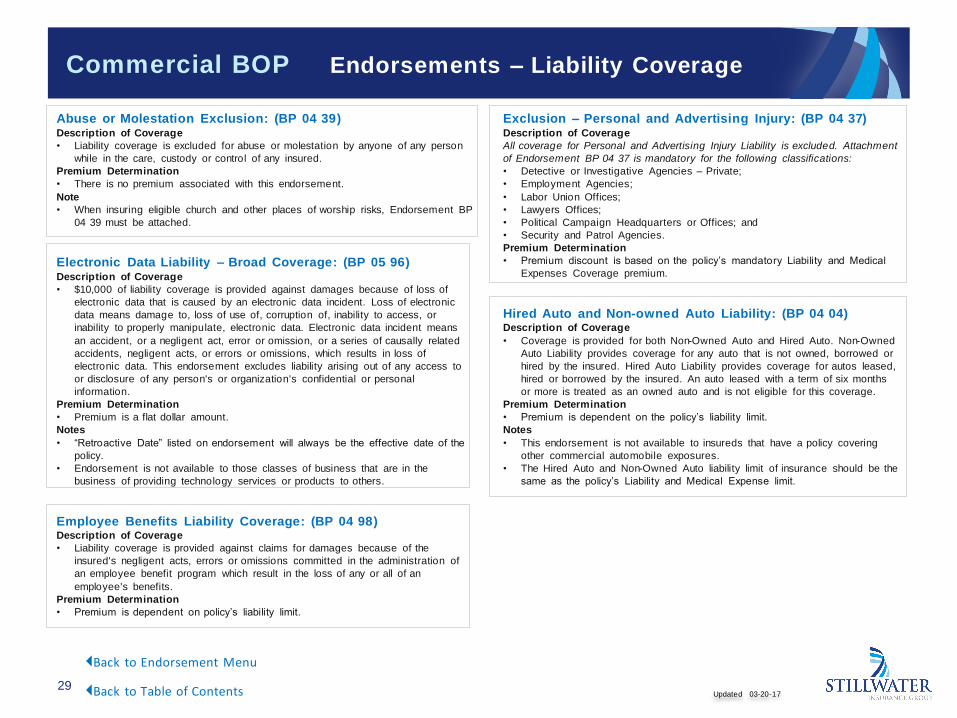

Abuse or Molestation Exclusion: (BP 04 39) Description of Coverage

• Liability coverage is excluded for abuse or molestation by anyone of any person

while in the care, custody or control of any insured.

Premium Determination

• There is no premium associated with this endorsement.

Note

• When insuring eligible church and other places of worship risks, Endorsement BP

04 39 must be attached.

Electronic Data Liability – Broad Coverage: (BP 05 96) Description of Coverage

• $10,000 of liability coverage is provided against damages because of loss of

electronic data that is caused by an electronic data incident. Loss of electronic

data means damage to, loss of use of, corruption of, inability to access, or

inability to properly manipulate, electronic data. Electronic data incident means

an accident, or a negligent act, error or omission, or a series of causally related

accidents, negligent acts, or errors or omissions, which results in loss of

electronic data. This endorsement excludes liability arising out of any access to

or disclosure of any person's or organization's confidential or personal

information.

Premium Determination

• Premium is a flat dollar amount.

Notes

• “Retroactive Date” listed on endorsement will always be the effective date of the

policy.

• Endorsement is not available to those classes of business that are in the

business of providing technology services or products to others.

Employee Benefits Liability Coverage: (BP 04 98) Description of Coverage

• Liability coverage is provided against claims for damages because of the

insured's negligent acts, errors or omissions committed in the administration of

an employee benefit program which result in the loss of any or all of an

employee's benefits.

Premium Determination

• Premium is dependent on policy’s liability limit.

Exclusion – Personal and Advertising Injury: (BP 04 37) Description of Coverage

All coverage for Personal and Advertising Injury Liability is excluded. Attachment

of Endorsement BP 04 37 is mandatory for the following classifications:

• Detective or Investigative Agencies – Private;

• Employment Agencies;

• Labor Union Offices;

• Lawyers Offices;

• Political Campaign Headquarters or Offices; and

• Security and Patrol Agencies.

Premium Determination

• Premium discount is based on the policy’s mandatory Liability and Medical

Expenses Coverage premium.

Hired Auto and Non-owned Auto Liability: (BP 04 04) Description of Coverage

• Coverage is provided for both Non-Owned Auto and Hired Auto. Non-Owned

Auto Liability provides coverage for any auto that is not owned, borrowed or

hired by the insured. Hired Auto Liability provides coverage for autos leased,

hired or borrowed by the insured. An auto leased with a term of six months

or more is treated as an owned auto and is not eligible for this coverage.

Premium Determination

• Premium is dependent on the policy’s liability limit.

Notes

• This endorsement is not available to insureds that have a policy covering

other commercial automobile exposures.

• The Hired Auto and Non-Owned Auto liability limit of insurance should be the

same as the policy’s Liability and Medical Expense limit.

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Liability Coverage

30

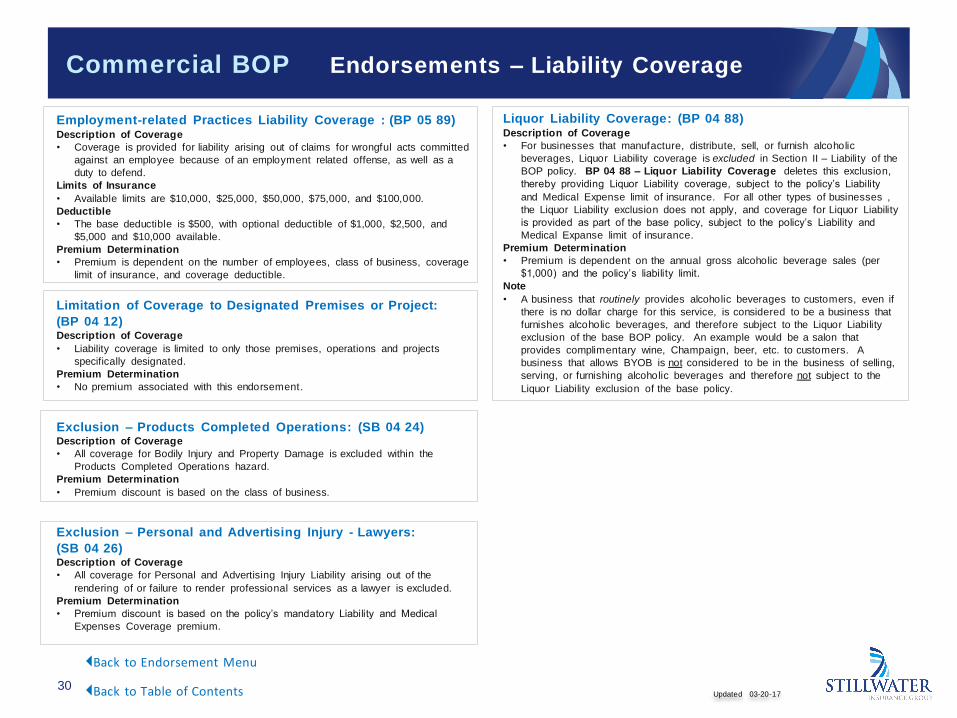

Employment-related Practices Liability Coverage : (BP 05 89) Description of Coverage

• Coverage is provided for liability arising out of claims for wrongful acts committed

against an employee because of an employment related offense, as well as a

duty to defend.

Limits of Insurance

• Available limits are $10,000, $25,000, $50,000, $75,000, and $100,000.

Deductible

• The base deductible is $500, with optional deductible of $1,000, $2,500, and

$5,000 and $10,000 available.

Premium Determination

• Premium is dependent on the number of employees, class of business, coverage

limit of insurance, and coverage deductible.

Limitation of Coverage to Designated Premises or Project:

(BP 04 12) Description of Coverage

• Liability coverage is limited to only those premises, operations and projects

specifically designated.

Premium Determination

• No premium associated with this endorsement.

Exclusion – Products Completed Operations: (SB 04 24) Description of Coverage

• All coverage for Bodily Injury and Property Damage is excluded within the

Products Completed Operations hazard.

Premium Determination

• Premium discount is based on the class of business.

Exclusion – Personal and Advertising Injury - Lawyers:

(SB 04 26) Description of Coverage

• All coverage for Personal and Advertising Injury Liability arising out of the

rendering of or failure to render professional services as a lawyer is excluded.

Premium Determination

• Premium discount is based on the policy’s mandatory Liability and Medical

Expenses Coverage premium.

Liquor Liability Coverage: (BP 04 88) Description of Coverage

• For businesses that manufacture, distribute, sell, or furnish alcoholic

beverages, Liquor Liability coverage is excluded in Section II – Liability of the

BOP policy. BP 04 88 – Liquor Liability Coverage deletes this exclusion,

thereby providing Liquor Liability coverage, subject to the policy’s Liability

and Medical Expense limit of insurance. For all other types of businesses ,

the Liquor Liability exclusion does not apply, and coverage for Liquor Liability

is provided as part of the base policy, subject to the policy’s Liability and

Medical Expanse limit of insurance.

Premium Determination

• Premium is dependent on the annual gross alcoholic beverage sales (per

$1,000) and the policy’s liability limit.

Note

• A business that routinely provides alcoholic beverages to customers, even if

there is no dollar charge for this service, is considered to be a business that

furnishes alcoholic beverages, and therefore subject to the Liquor Liability

exclusion of the base BOP policy. An example would be a salon that

provides complimentary wine, Champaign, beer, etc. to customers. A

business that allows BYOB is not considered to be in the business of selling,

serving, or furnishing alcoholic beverages and therefore not subject to the

Liquor Liability exclusion of the base policy.

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Specific Classes

31

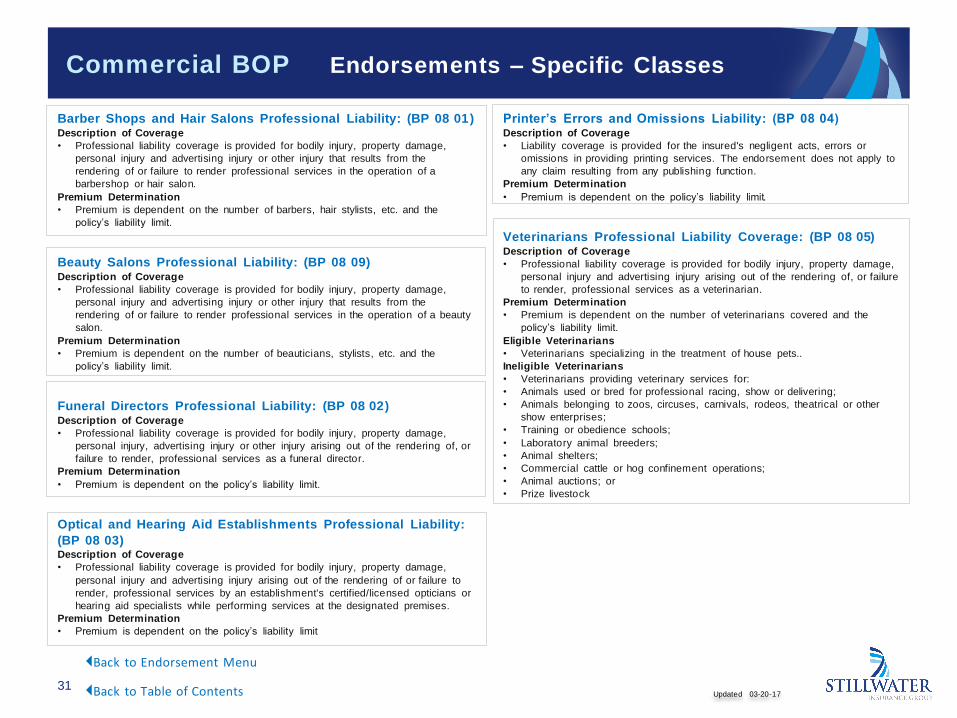

Barber Shops and Hair Salons Professional Liability: (BP 08 01) Description of Coverage

• Professional liability coverage is provided for bodily injury, property damage,

personal injury and advertising injury or other injury that results from the

rendering of or failure to render professional services in the operation of a

barbershop or hair salon.

Premium Determination

• Premium is dependent on the number of barbers, hair stylists, etc. and the

policy’s liability limit.

Beauty Salons Professional Liability: (BP 08 09) Description of Coverage

• Professional liability coverage is provided for bodily injury, property damage,

personal injury and advertising injury or other injury that results from the

rendering of or failure to render professional services in the operation of a beauty

salon.

Premium Determination

• Premium is dependent on the number of beauticians, stylists, etc. and the

policy’s liability limit.

Funeral Directors Professional Liability: (BP 08 02) Description of Coverage

• Professional liability coverage is provided for bodily injury, property damage,

personal injury, advertising injury or other injury arising out of the rendering of, or

failure to render, professional services as a funeral director.

Premium Determination

• Premium is dependent on the policy’s liability limit.

Optical and Hearing Aid Establishments Professional Liability:

(BP 08 03) Description of Coverage

• Professional liability coverage is provided for bodily injury, property damage,

personal injury and advertising injury arising out of the rendering of or failure to

render, professional services by an establishment's certified/licensed opticians or

hearing aid specialists while performing services at the designated premises.

Premium Determination

• Premium is dependent on the policy’s liability limit

Printer’s Errors and Omissions Liability: (BP 08 04) Description of Coverage

• Liability coverage is provided for the insured's negligent acts, errors or

omissions in providing printing services. The endorsement does not apply to

any claim resulting from any publishing function.

Premium Determination

• Premium is dependent on the policy’s liability limit.

Veterinarians Professional Liability Coverage: (BP 08 05) Description of Coverage

• Professional liability coverage is provided for bodily injury, property damage,

personal injury and advertising injury arising out of the rendering of, or failure

to render, professional services as a veterinarian.

Premium Determination

• Premium is dependent on the number of veterinarians covered and the

policy’s liability limit.

Eligible Veterinarians

• Veterinarians specializing in the treatment of house pets..

Ineligible Veterinarians

• Veterinarians providing veterinary services for:

• Animals used or bred for professional racing, show or delivering;

• Animals belonging to zoos, circuses, carnivals, rodeos, theatrical or other

show enterprises;

• Training or obedience schools;

• Laboratory animal breeders;

• Animal shelters;

• Commercial cattle or hog confinement operations;

• Animal auctions; or

• Prize livestock

Back to Table of Contents

Back to Endorsement Menu

Updated 03-20-17

Commercial BOP Endorsements – Specific Classes

32

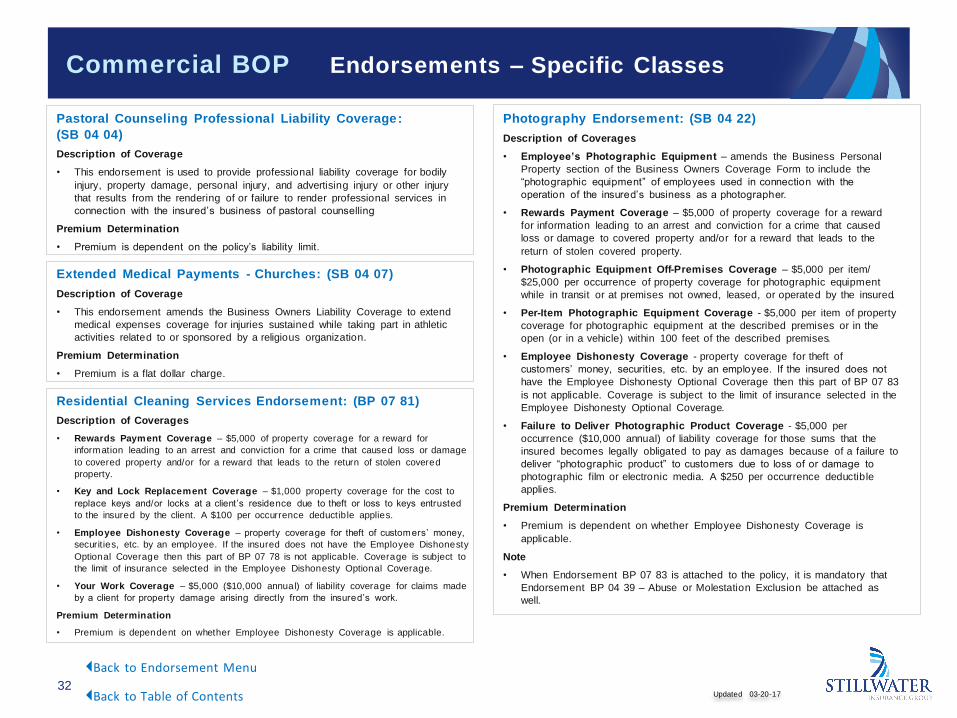

Pastoral Counseling Professional Liability Coverage:

(SB 04 04)

Description of Coverage

• This endorsement is used to provide professional liability coverage for bodily

injury, property damage, personal injury, and advertising injury or other injury

that results from the rendering of or failure to render professional services in

connection with the insured’s business of pastoral counselling

Premium Determination

• Premium is dependent on the policy’s liability limit.