Building the balance - EY · implement a new system without fixing the issues with the old. •...

16

Building the balance: Cooperative compliance in practice

Transcript of Building the balance - EY · implement a new system without fixing the issues with the old. •...

Building the balance:Cooperative compliance in practice

In this report

1Executive summary

2Introduction

3From an ‘enhanced relationship’ to ‘cooperative compliance’

5Understanding the issues

8Meeting the challenge

10What could a Service Level Agreement look like?

12A roadmap to success

Building the balance:Cooperative compliance in practice

The administration of our tax regime is a key factor in the attractiveness of the UK as a place to live and do business. At the most fundamental level, the tax system needs to be robust and if the administration of it does not work effectively, there is a risk to both HMRC and UK businesses. As well as money and resource, that risk includes more intangible issues such as delays in commercial decision-making and the impact on long-term planning.

Executive summary

At a time when the relationship between HMRC and large business is under discussion, we believe it is crucial that any changes are properly debated. Building on discussions from our 2015 Tax Director Workshop programme, we worked with a Panel of FTSE100 Tax Directors to understand their experiences. That discussion focused on proposals from HMRC around cooperative compliance which asks business for earlier and greater disclosure than required by statute. Our Panel considered what it should be able to expect in return. We also surveyed the wider Tax Director population to test their conclusions. The key points arising from that process include:

• Our Panel highly values the Customer Relationship Manager (CRM) relationship.

• Similarly, almost 60% of respondents to our 2016 Tax Director survey rate maintaining their existing constructive relationship with the CRM as the first, second or third most important factor in the Cooperative Compliance Framework.

• The pace of market change, the evolving tax environment and greater public scrutiny of tax paid by large businesses means a shift of approach is to be expected.

• The way that large businesses and HMRC interact plays a significant part in the attractiveness of the UK as a place to do business. Getting it wrong could, therefore, harm the UK economy.

• Our Panel highlighted the impact that existing issues are having on business and the ability to respond to commercial decisions quickly.

• ►For our Panel it would be wrong to implement a new system without fixing the issues with the old.

• While often intangible, the issues are significant and our Panel expressed concern that if the system does not deliver its objectives, HMRC will revert to previously unworkable approaches.

With all of this in mind, we believe that a positive step in the relationship between HMRC and large businesses would be to introduce parameters

along the lines of a Service Level Agreement (SLA). Alongside measurable key performance indicators, such an Agreement should accommodate the intangible factors that have such a key impact on the ability of UK businesses to operate competitively in the global marketplace.

If both parties sign up to the SLA, we believe it would demonstrate the Government’s commitment to a constructive taxpayer/tax authority relationship and could help the UK to stand out as a place to do business. We expect HMRC’s proposals around a Framework for Cooperative Compliance will be included in a Business Tax Roadmap to be announced as part of, or very soon after, this year’s Budget.

Before that process is finalised, the steps to the SLA need to be properly debated and agreed. Our Panel has shown a willingness to engage in that debate. It’s time for HMRC to do the same.

Tim Steel

UK&I Tax Markets Leader 020 7951 1149 [email protected]

Chris Sanger

UK&I Head of Tax Policy 020 7951 0150 [email protected]

1

IntroductionKeeping the UK ‘open for business’ is a term often used by the Government – and by HMRC in particular – to represent the need to attract and retain investment that generates growth, creates jobs and makes a significant contribution to the public finances. While often positioned as part of the Corporate Tax Roadmap, facilitating this ongoing investment rests not just on the attractiveness of the tax system but also on the certainty, stability and predictability of its administration. In short, the relationship between large businesses and HMRC is fundamental to the appeal of the UK as a place to do business.

In the almost ten years since the Large Business Service was created and the role of Customer Relationship Manager (CRM) was introduced, the business world and ways of doing business have evolved significantly. It should come as no surprise then that HMRC has been working to develop a new framework for working with large businesses. However, we believe that there is a very real risk that significant problems will be

carried forward from the old to the new framework unless steps are taken to address them in the interim.

With a strong relationship between large businesses and HMRC playing such a key part in the ‘open for business’ message, it is crucial that the starting point is not only to get the framework right but also to ensure that the practical application works for both parties. With this in

mind, we asked a panel of FTSE100 Tax Directors to help us identify a set of parameters (like a Service Level Agreement) for the ongoing relationship between large businesses and HMRC. This report outlines the proposed Agreement and offers a view on the most effective way to take it forward. We believe that such an Agreement would differentiate the UK taxpayer/tax authority relationship in the global market.

2

From an ‘enhanced relationship’ to ‘cooperative compliance’

Delivery of Sir David Varney’s 2006 ‘Review of Links with Large Business’ focused on three key outcomes:

• An increased percentage of the right tax paid at the right time

• A professional and trusted service

• Increased attractiveness of the UK as a place to do business.

HMRC’s Large Business Service created

2005 2006 2007 2009 2015 2016

Review of links with Large Business published

Risk framework introduced

HMRC’s Large Business strategy adopted

Consultation on Large Business Tax Compliance

Cooperative Compliance Framework expected to apply from [April] 2016

This was formalised through the CRM whose primary role was to manage what was termed the ‘enhanced relationship’ between the business and HMRC across all taxes and duties.

Since then, HMRC adopted three new strategic objectives for the Department and these are referred

to in HMRC’s recent consultation on Large Business Tax Compliance:

• Maximising revenues

• Making sustainable cost savings

• Improving the customer experience.

3Building the balance: Cooperative compliance in practice

Developments in the interim – including the G20/OECD’s Action Plan on Base Erosion and Profit Shifting (BEPS) – have shown that, while the original thinking around the need for a cooperative approach to compliance is still valid, the focus on compliance per se is now seen as pivotal. However, our question is around the interpretation of the term ‘cooperative’ and what that means in practice.

HMRC’s 2015 consultation on Improving Large Business Tax Compliance included a Code of Practice on Taxation for Large Businesses to which HMRC proposed that relevant businesses would become signatories. However, in its summary of responses published in December 2015, HMRC conceded that ‘the overwhelming theme of responses was that the Code was missing an element of mutuality, that is, it did not outline what large businesses could expect of HMRC’. As a result, a draft ‘Framework for Cooperative Compliance’ was published and this is expected to be implemented by April 2016.

Both our Tax Director Panel and the 165 respondents to our subsequent 2016 Tax Director Survey strongly endorse the CRM model. Indeed when asked what factors they would most like to see in the Cooperative Compliance Framework, over a third of our survey respondents ranked a continuation of their existing constructive relationship with their CRM as the most important factor. In fact, over half ranked that as the first, second or third most important factor.

However, despite being such strong advocates for the CRM model, the issue of mutuality was a theme that ran through our Tax Director discussions. While there was a strong sense that the prospect of a Framework for Cooperative Compliance represents a significant opportunity for the UK to distinguish itself for the effectiveness of its tax administration, there clearly remained a desire to ensure that the large business tax administration process lives up to its potential. With this in mind, there was a tangible concern amongst our Panel that if the system failed to meet the objectives set, HMRC could decide to move away from cooperation altogether. It is, therefore, crucial that the process works for both sides from the outset.

• Preparing an integrated risk assessment for the business and then sharing the HMRC view of risk with the business, both to identify and resolve any differences of view and to involve the business in planning future interventions at the business.

• Ensuring that interventions, e.g., system audits and enquiries, fully reflect the risks at the business and are carried out effectively, making appropriate use of the range of specialist resource available within HMRC and ensuring that issues are resolved in line with the HMRC approach to settlement and litigation.

• Responding to queries and requests for clearance from the customer in a timely fashion and ensuring that HMRC meets agreed deadlines.

• Keeping the business informed about how their issues are progressing and when they can expect a response to a request and why, exceptionally, some issues might take longer because of their inherent complexity or difficulty.

58%ranked ‘continuing their existing constructive relationship with the CRM’ as the first, second or third most important factor in the cooperative compliance framework

The distinction between the two approaches may be subtle but it reflects a shift in emphasis that has evolved over the past decade, particularly in the area of ‘maximising tax revenues’. Our concern, as highlighted in our recent report ‘Striking a balance’, is that the shift from what was seen as an ‘enhanced relationship’ in 2005 to what is, today, described as ‘cooperative compliance’ has been accompanied by a move away from cooperation and towards coercion.

HMRC 2006: Role of the CRM

4

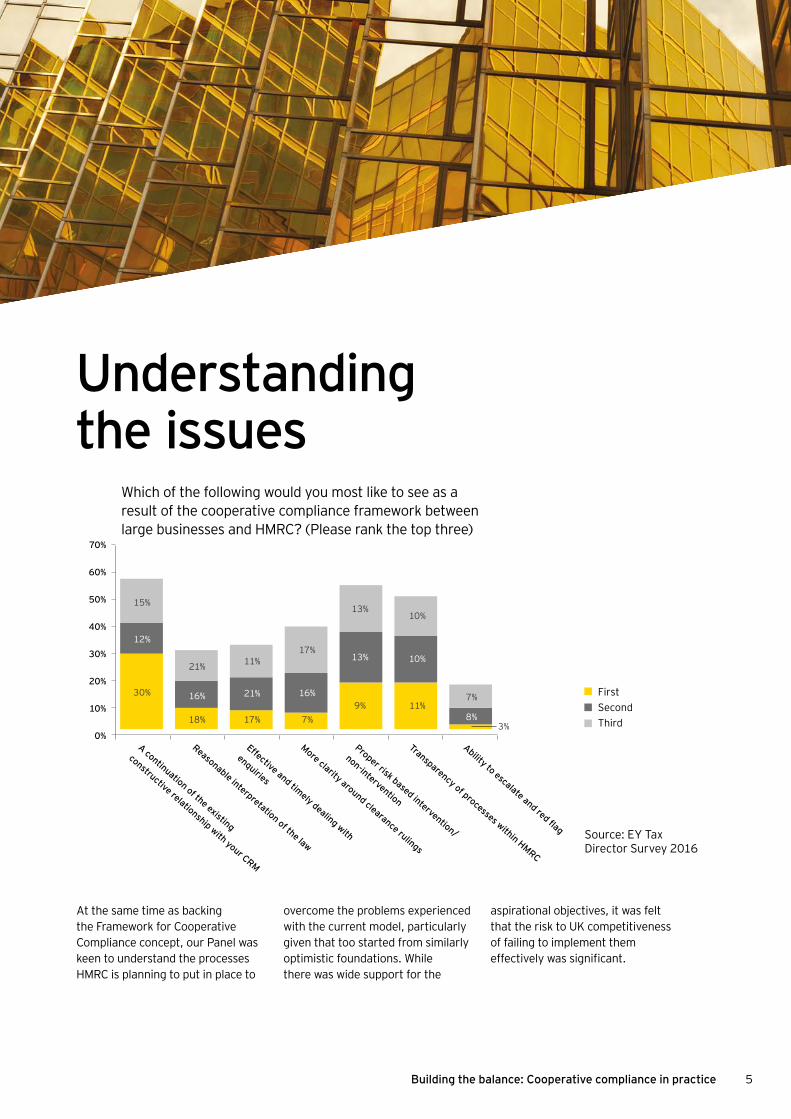

Which of the following would you most like to see as a result of the cooperative compliance framework between large businesses and HMRC? (Please rank the top three)

Source: EY Tax Director Survey 2016

70%

60%

50%

40%

30%

20%

10%

0%A continuation of the existing

constructive relationship with your CRM

Reasonable interpretation of the law

Effective and timely dealing with

enquiries

More clarity around clearance rulings

Proper risk based intervention/

non-intervention

Transparency of processes within HMRC

Ability to escalate and red flag

FirstSecondThird

At the same time as backing the Framework for Cooperative Compliance concept, our Panel was keen to understand the processes HMRC is planning to put in place to

overcome the problems experienced with the current model, particularly given that too started from similarly optimistic foundations. While there was wide support for the

aspirational objectives, it was felt that the risk to UK competitiveness of failing to implement them effectively was significant.

Understanding the issues

15%

12%

30%

21%

16%

18%

11%

21%

17%

17%

16%

7%

13%

13%

9%

10%

10%

11%7%

8%3%

5Building the balance: Cooperative compliance in practice

Although they also expressed clear support for the CRM model, our Tax Director Survey respondents highlighted a number of practical factors they would like to see as part of the Framework. Principal amongst these was effective and timely dealing with enquiries, reasonable interpretation of the law and transparency of processes within HMRC.

Large businesses are different

While our Panel supported the equitable application of the tax regime to all taxpayers, it was felt that the complexities associated with applying that regime to a large business should be acknowledged. Rather than apologising for treating large businesses differently, HMRC should be able to justify the need for an alternative approach. In reality, that approach means that large businesses are likely to come under far more scrutiny which naturally sets them apart from smaller businesses.

Focus and transparency of processOur Panel recognises that enquiries are inevitable from time to time given the scale of their operations. However, concern was expressed around the lack of transparency with respect to the process and its progress. It was felt that disclosures are often taken as an invitation for a ‘fishing expedition’ and that once other HMRC stakeholders are involved, they may seek to expand the scope of an enquiry In addition, there are arguably too many instances where matters are left open-ended, with enquiries not being closed within an acceptable period of time.

The decision-making powers and responsibilities of CRMs are not always clear and it is not always possible to understand the reasons why specific issues or enquiries are escalated or passed to specialists.

A point of escalation

The variable experience of interactions with CRMs also suggests a need to create greater clarity about HMRC processes and the possible routes for escalation when problems are encountered. Some of our Panel expressed concerns about their ability to raise issues or red flags without prejudice to their future engagement as well as uncertainty about the channels for doing so.

Our Tax Director Panel discussed these and other issues in more detail:

6

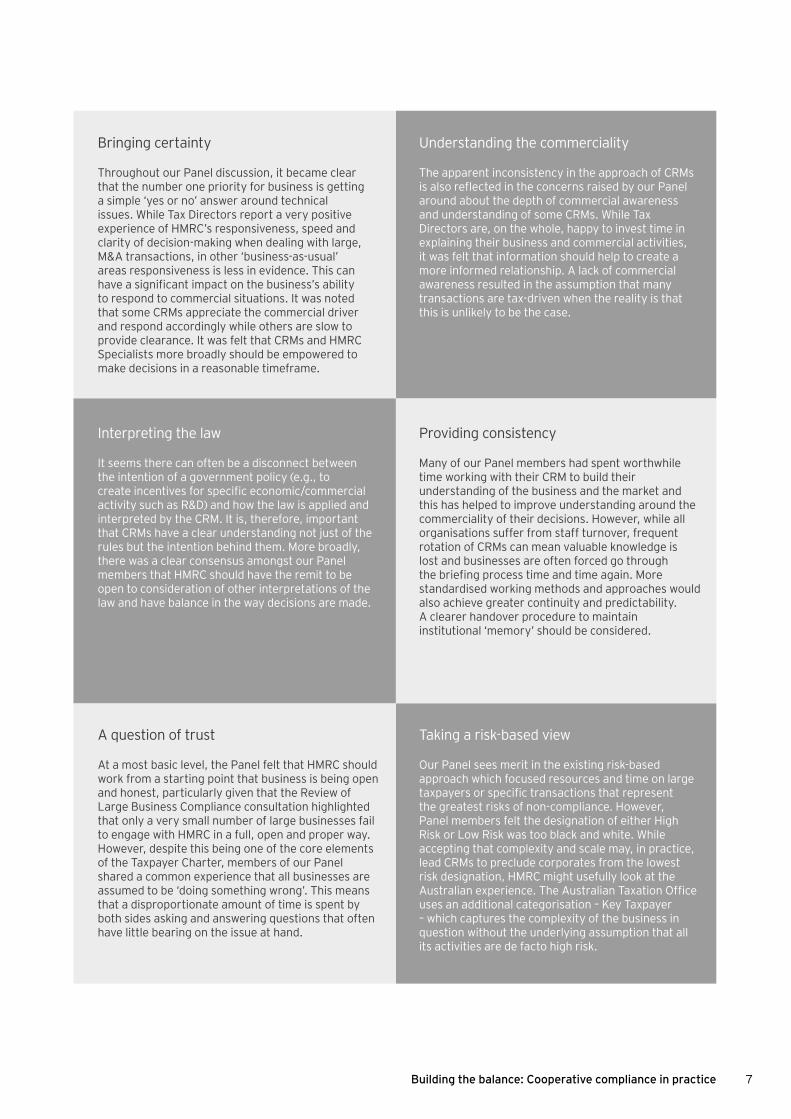

Bringing certainty

Throughout our Panel discussion, it became clear that the number one priority for business is getting a simple ‘yes or no’ answer around technical issues. While Tax Directors report a very positive experience of HMRC’s responsiveness, speed and clarity of decision-making when dealing with large, M&A transactions, in other ‘business-as-usual’ areas responsiveness is less in evidence. This can have a significant impact on the business’s ability to respond to commercial situations. It was noted that some CRMs appreciate the commercial driver and respond accordingly while others are slow to provide clearance. It was felt that CRMs and HMRC Specialists more broadly should be empowered to make decisions in a reasonable timeframe.

Interpreting the law

It seems there can often be a disconnect between the intention of a government policy (e.g., to create incentives for specific economic/commercial activity such as R&D) and how the law is applied and interpreted by the CRM. It is, therefore, important that CRMs have a clear understanding not just of the rules but the intention behind them. More broadly, there was a clear consensus amongst our Panel members that HMRC should have the remit to be open to consideration of other interpretations of the law and have balance in the way decisions are made.

A question of trust

At a most basic level, the Panel felt that HMRC should work from a starting point that business is being open and honest, particularly given that the Review of Large Business Compliance consultation highlighted that only a very small number of large businesses fail to engage with HMRC in a full, open and proper way. However, despite this being one of the core elements of the Taxpayer Charter, members of our Panel shared a common experience that all businesses are assumed to be ‘doing something wrong’. This means that a disproportionate amount of time is spent by both sides asking and answering questions that often have little bearing on the issue at hand.

Understanding the commerciality

The apparent inconsistency in the approach of CRMs is also reflected in the concerns raised by our Panel around about the depth of commercial awareness and understanding of some CRMs. While Tax Directors are, on the whole, happy to invest time in explaining their business and commercial activities, it was felt that information should help to create a more informed relationship. A lack of commercial awareness resulted in the assumption that many transactions are tax-driven when the reality is that this is unlikely to be the case.

Providing consistency

Many of our Panel members had spent worthwhile time working with their CRM to build their understanding of the business and the market and this has helped to improve understanding around the commerciality of their decisions. However, while all organisations suffer from staff turnover, frequent rotation of CRMs can mean valuable knowledge is lost and businesses are often forced go through the briefing process time and time again. More standardised working methods and approaches would also achieve greater continuity and predictability. A clearer handover procedure to maintain institutional ‘memory’ should be considered.

Taking a risk-based view

Our Panel sees merit in the existing risk-based approach which focused resources and time on large taxpayers or specific transactions that represent the greatest risks of non-compliance. However, Panel members felt the designation of either High Risk or Low Risk was too black and white. While accepting that complexity and scale may, in practice, lead CRMs to preclude corporates from the lowest risk designation, HMRC might usefully look at the Australian experience. The Australian Taxation Office uses an additional categorisation – Key Taxpayer – which captures the complexity of the business in question without the underlying assumption that all its activities are de facto high risk.

7Building the balance: Cooperative compliance in practice

Meeting the challenge

8

Running through the issues raised by our Panel are a set of behaviours that are fundamental to the effectiveness of the CRM model. If these remain under the new system, they may impact the following:

• The ability of HMRC to meet its objectives

• The extent to which UK businesses have certainty and predictability that allows them to compete in the global marketplace, and

• Maintaining the UK’s position as an attractive place to do business.

So how can we move from a shared commitment to an effective system?

We believe that more specific commitments are needed from both HMRC and the businesses they work with. By setting out the detailed parameters (such as in a Service Level Agreement (SLA)), both parties would have clarity around both what

is expected of them and what they can expect in return. Key to that SLA would be:

• Agreement from both parties around the ultimate goal – payment of the right tax at the right time

• Moving beyond rhetoric to real actions on both sides

• A recognition that it is not about a special set of rules but the application of those rules to complex circumstances

• Understanding that those complex circumstances mean that businesses need to be increasingly transparent and, in return, need consistency and clarity from HMRC

• Demonstrating the formality of the relationship between HMRC and large business – addressing the misperception of cosiness that has featured in the press.

A clear message from our Tax Director Panel is that business is just as concerned as HMRC to make the Framework for Cooperative Compliance work. However, the same thing was true ten years ago with the publication of the original Review of Links with Large Business.

9Building the balance: Cooperative compliance in practice

With their own issues in mind and a clear picture of HMRC objectives, our Tax Director Panel discussed what a Service Level Agreement might look like.

An effective SLA requires both parties to fully commit to their side of the agreement on a reciprocal basis. Key to this process will, therefore, be ensuring that there is a clear escalation process for failure to deliver the SLA commitments on either side.

On the business side, the potential penalties are already clear and will become even more stringent

What could a Service Level Agreement look like?

in the highest risk cases with the introduction of the ‘special measures’ in the Framework for Cooperative Compliance. The corresponding consequences for HMRC are more intangible. Quantifiable measures like revenue raised, response times and continuity of staff will not give the entire picture. A clear and constructive route of escalation

around the other factors will be just as important and it may be that this is a role for the Tax Assurance Commissioner or Tax Ombudsman. However, it is crucial that businesses are not forced to devote time and resource escalating issues so the ‘tone from the top’ within HMRC must be sufficiently supportive as to engage its people around the SLA.

10

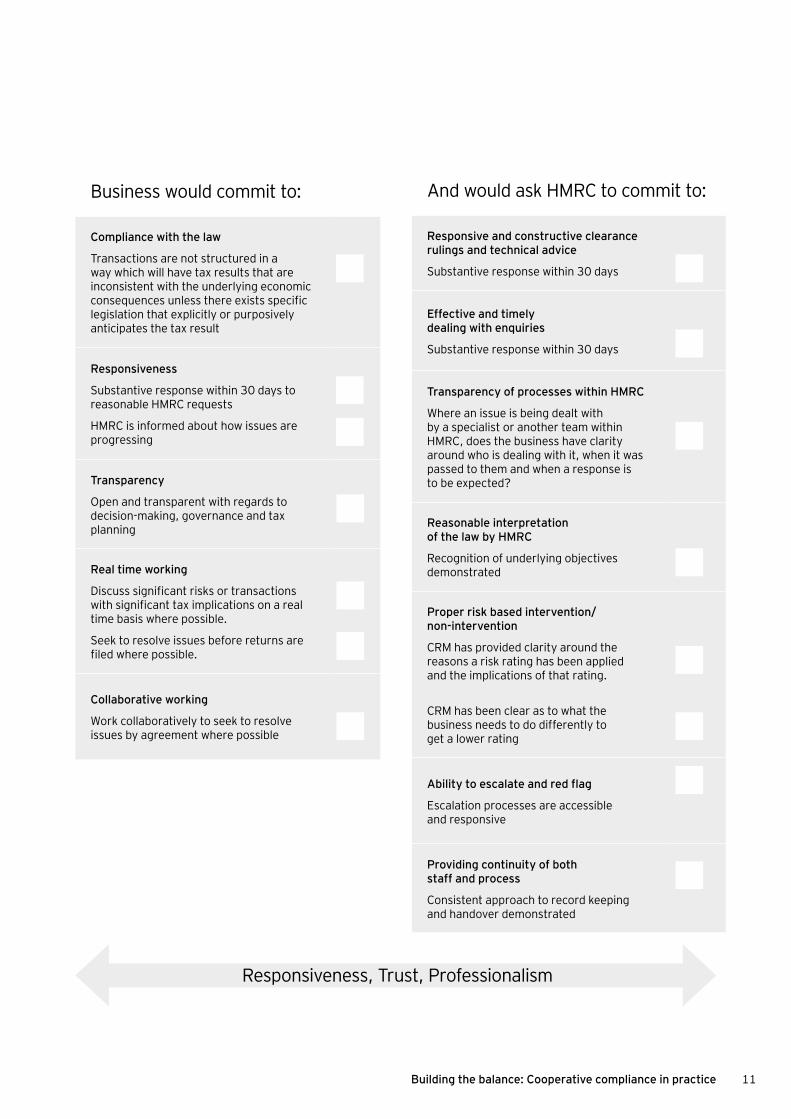

Business would commit to:

Compliance with the law

Transactions are not structured in a way which will have tax results that are inconsistent with the underlying economic consequences unless there exists specific legislation that explicitly or purposively anticipates the tax result

Responsiveness

Substantive response within 30 days to reasonable HMRC requests

HMRC is informed about how issues are progressing

Transparency

Open and transparent with regards to decision-making, governance and tax planning

Real time working

Discuss significant risks or transactions with significant tax implications on a real time basis where possible.

Seek to resolve issues before returns are filed where possible.

Collaborative working

Work collaboratively to seek to resolve issues by agreement where possible

And would ask HMRC to commit to:

Responsive and constructive clearance rulings and technical advice

Substantive response within 30 days

Effective and timely dealing with enquiries

Substantive response within 30 days

Transparency of processes within HMRC

Where an issue is being dealt with by a specialist or another team within HMRC, does the business have clarity around who is dealing with it, when it was passed to them and when a response is to be expected?

Reasonable interpretation of the law by HMRC

Recognition of underlying objectives demonstrated

Proper risk based intervention/ non-intervention

CRM has provided clarity around the reasons a risk rating has been applied and the implications of that rating.

CRM has been clear as to what the business needs to do differently to get a lower rating

Ability to escalate and red flag

Escalation processes are accessible and responsive

Providing continuity of both staff and process

Consistent approach to record keeping and handover demonstrated

Responsiveness, Trust, Professionalism

11Building the balance: Cooperative compliance in practice

A roadmap to success

12

As well as setting the agenda for taxation of businesses in the UK, this is expected to replace the existing Corporate Tax Roadmap as the statement of intent around UK competitiveness. This represents a real opportunity to differentiate the UK on the global stage.

Constructive debate around the structure of any form of SLA would not only raise the profile for the commitment on both sides (and provide a great advertisement for

the UK), it would also ensure that the road ahead leads to an effective and efficient system that works for all. Demonstrating the UK’s commitment to a constructive taxpayer/tax authority relationship in this way could truly differentiate the UK as a great place to do business.

Our Tax Director Panel has shown that business is willing to engage in a debate around making this work. We believe it is time for HMRC to do the same.

The Framework for Cooperative Compliance is expected to form a key part of the new Business Tax Roadmap.

13Building the balance: Cooperative compliance in practice

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

© 2016 Ernst & Young LLP. Published in the UK. All Rights Reserved.

EYG No: DF0237 ED None

In line with Ernst & Young’s commitment to minimise its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice

ey.com/UK/

EY | Assurance | Tax | Transactions | Advisory