Broadcast telecom CONVERGENCE ….The Journey Begins !!! BES Expo and Conference’ 2007; 1 st to 3...

31

broadca st teleco m CONVERGENCE ….The Journey Begins !!! S Expo and Conference’ 2007; 1 st to 3 rd Feb’20 ================================================================

-

Upload

carli-loveland -

Category

Documents

-

view

215 -

download

1

Transcript of Broadcast telecom CONVERGENCE ….The Journey Begins !!! BES Expo and Conference’ 2007; 1 st to 3...

broadcast

telecom CONVERGENCE

….The Journey Begins !!!

BES Expo and Conference’ 2007; 1st to 3rd Feb’2007================================================================

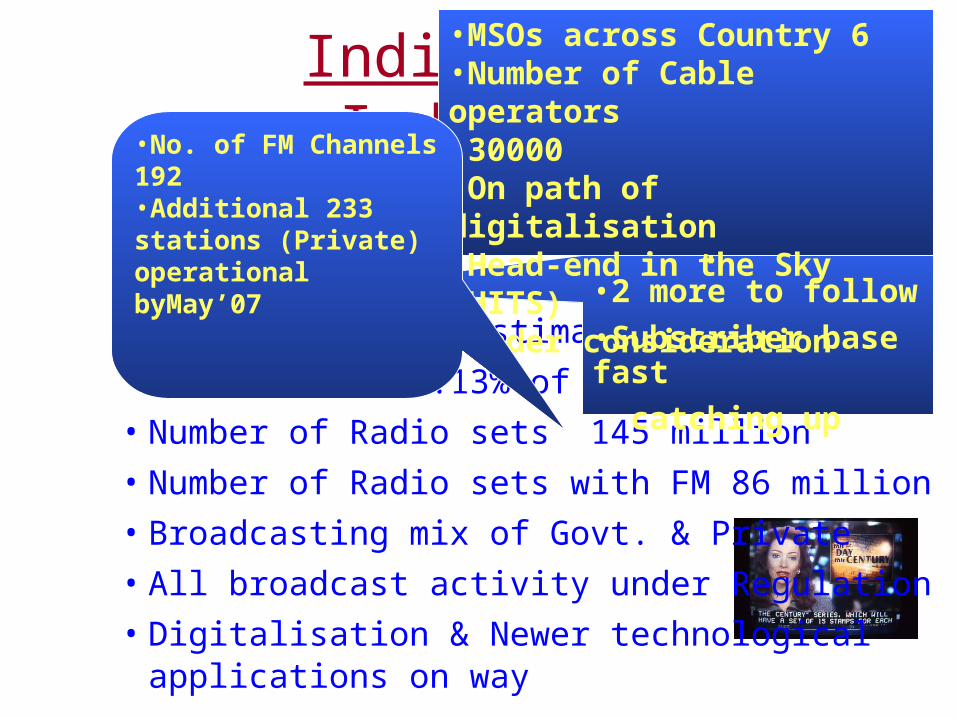

Indian Broadcast Industry

• Television Reach 112 million homes

• Cable & Satellite Homes 68 million homes

• DTH Subscribers estimated at 5 million

• Radio reach 99.13% of population

• Number of Radio sets 145 million

• Number of Radio sets with FM 86 million

• Broadcasting mix of Govt. & Private

• All broadcast activity under Regulation

• Digitalisation & Newer technological applications on way

•DTH Operators 03

•2 more to follow

•Subscriber base fast

catching up

•MSOs across Country 6•Number of Cable operators 30000•On path of digitalisation•Head-end in the Sky (HITS) under consideration

•No. of FM Channels 192•Additional 233 stations (Private) operational byMay’07

Indian Telecom Boom

• Tele-density over 15% rising from 2% in 2000• Mobile telephony opened in 1995; subscriber

base 130 million..rising @ 6mn per month• Land (Wired) phones 40 million• Fastest growing market in Asia• Both CDMA and GSM technologies in practice• Overall revenue rise to Rs. 86,720 Cr• Three Telecom companies estimated in first 10

biggest companies

In year 2000, this figure was just 2%

Internet Scene• Internet penetration is alarmingly low …does not find

relevance with the global scenario as well as the national economy.

• Countries like Macau, Poland, Iceland and Israel are far ahead than India

• India’s broadband penetration is below 3% in urban sector; whole India penetration is less than 0.5%.

• Estimated 60% of internet users depend on more than 10,000 cyber-café

• ISP –389; Internet subscriber less than 8mn

• Revenue in 2005-06 is Rs 492 cr

• Internet subscribers is projected to touch 18million figure by the end of 2007

Indian Market Scenario• Indian Media industry growing at 15%; faster

than National Economy in last few years• Trend continues --Business Optimism Index for

first half of this year is higher by 14% than last year

• Media expenditure increases across– Radio 24%, Internet 35% and Television 19% in the year ending 2005.

• E-Sales/Commerce activities on rise – increase by over 95% in last one year

• Telecom revenue rising by around 21%

Global figures much higher…. Europe during similar times showed 230% rise

INDIAN MEDIA CONSUMER CHARACTER

• Late Starters• Varied Tastes• Conservative in approach• Cautious Regulatory Eye• Non-Tech Savvy Viewers• Discouraging personal economy

Result: Delayed Technological applications & acceptance !!

INDUSTRY

EVOLUTION

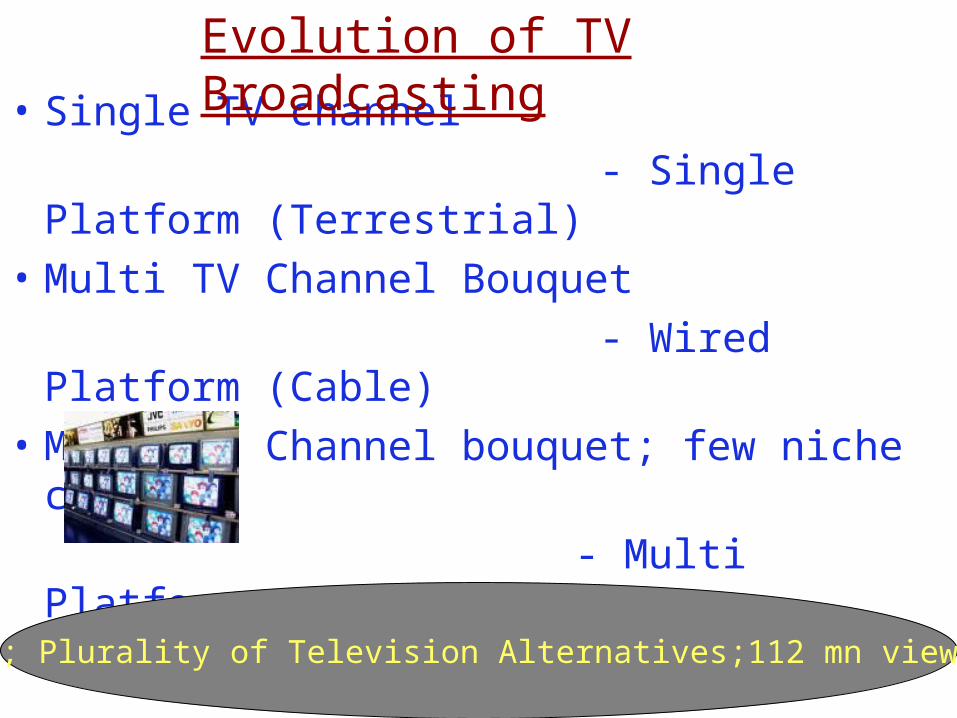

• Single TV channel

- Single Platform (Terrestrial)

• Multi TV Channel Bouquet

- Wired Platform (Cable)

• Multi TV Channel bouquet; few niche channels

- Multi Platforms options

( both wired & Unwired)

Evolution of TV Broadcasting

25 years; Plurality of Television Alternatives;112 mn viewer homes

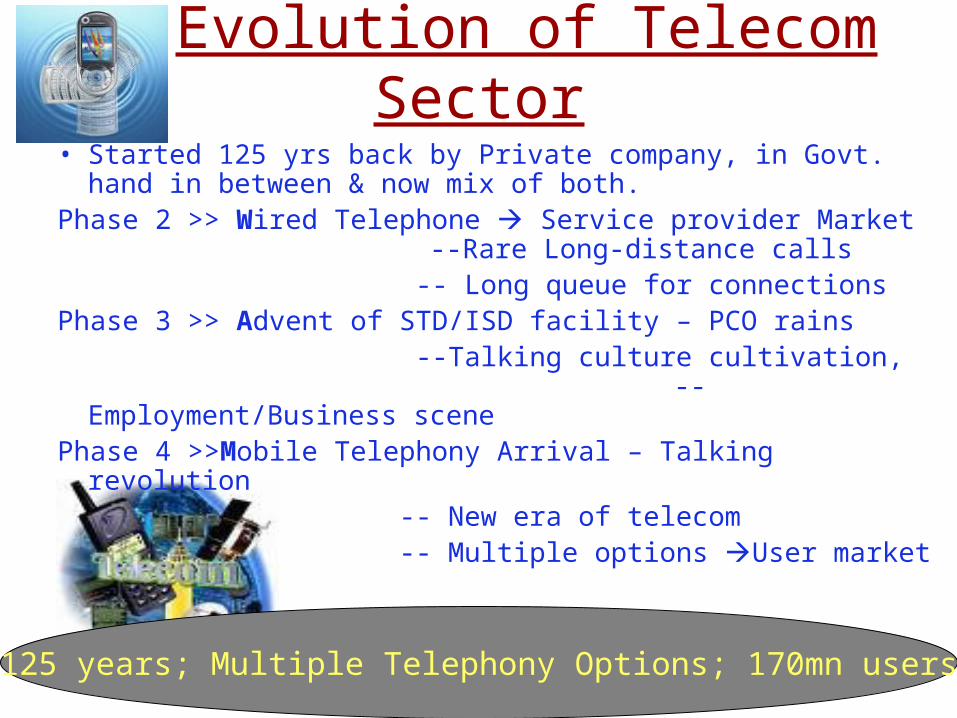

Evolution of Telecom Sector

• Started 125 yrs back by Private company, in Govt. hand in between & now mix of both.

Phase 2 >> Wired Telephone Service provider Market --Rare Long-distance calls

-- Long queue for connectionsPhase 3 >> Advent of STD/ISD facility – PCO rains --Talking culture cultivation,

-- Employment/Business scenePhase 4 >>Mobile Telephony Arrival – Talking revolution -- New era of telecom -- Multiple options User market

125 years; Multiple Telephony Options; 170mn users

Evolution Of Data Service• Internet an imaginary concept a decade ago• Development of infrastructure –670,000Km of

fibre laid

-Enhancement of Connectivity

- Lowering of cost• Huge dependence on networked Information

(Education to Business to Entertainment)• Internet/Broadband penetration still quite low

10 years; Life’s essentiality;

Over 7mn Internet users; 389 ISPs; More than 10,000Cyber cafe

The Consumer Behavior Evolution

•Trend towards Mecasting/Egocasting

•Zero Tolerant

•Looks for alternative solutions

•Wants more value of money

•King of the aspects

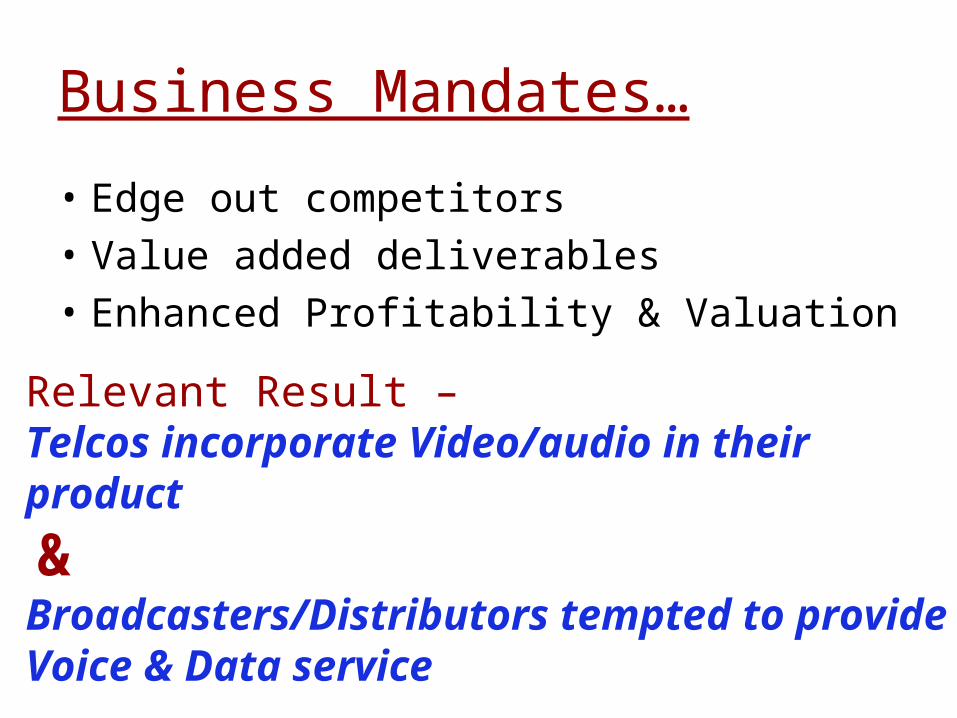

Business Mandates…

• Edge out competitors

• Value added deliverables

• Enhanced Profitability & Valuation

Relevant Result – Telcos incorporate Video/audio in their product

&Broadcasters/Distributors tempted to provide Voice & Data service

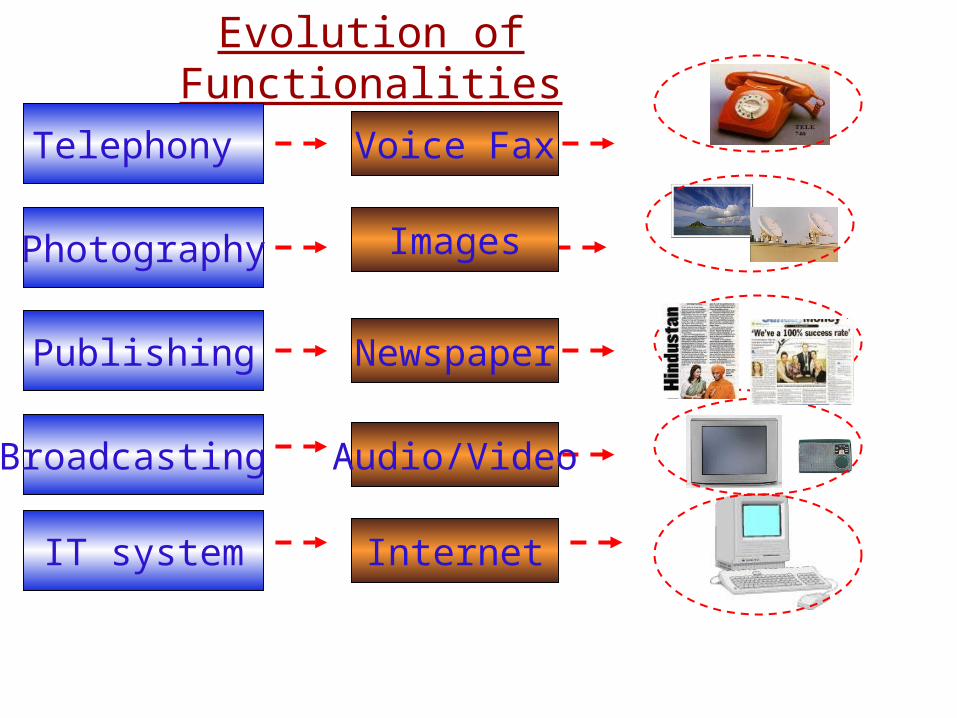

Evolution of Functionalities

Telephony

Photography

Publishing

Broadcasting

IT system

Images

Voice Fax

Newspaper

Audio/Video

Internet

Images

Voice

Text Information

Broadcasting

IT system

Distribution

Platform /

Application

SERVER

WITH

STORAGE

Evolution of Functionalities

Thus..Arrives Convergence !!!

…with Spirit of Intercativity.

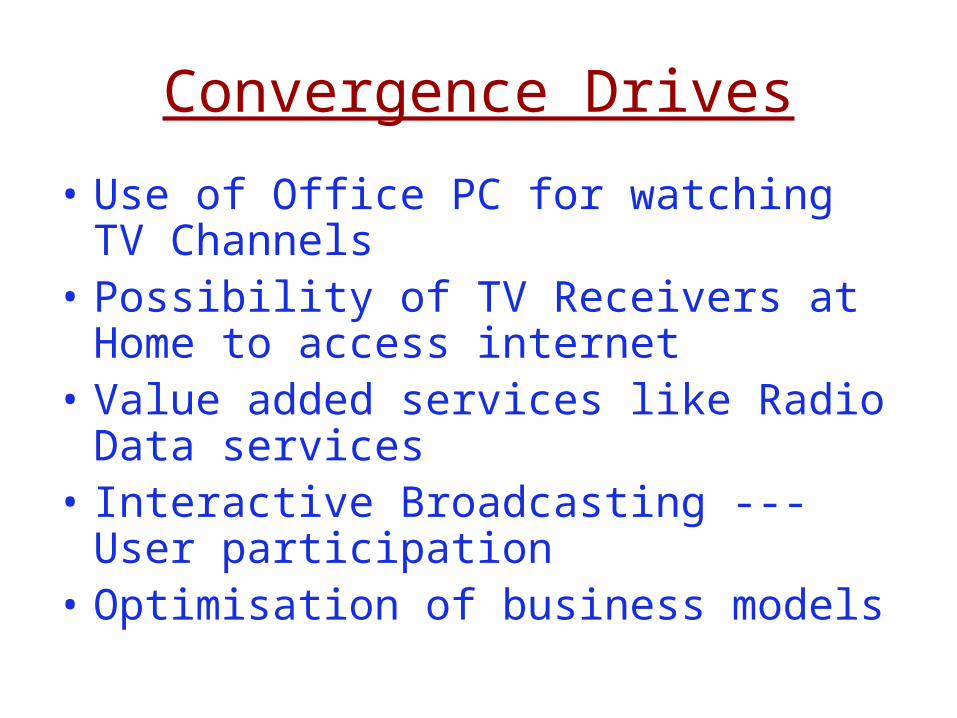

Convergence Drives

• Use of Office PC for watching TV Channels

• Possibility of TV Receivers at Home to access internet

• Value added services like Radio Data services

• Interactive Broadcasting --- User participation

• Optimisation of business models

Factors Driving Evolution

• Enhancing Economy … increased spending power

• Market competitiveness calling for value-add on by the service providers

• Technological advancements… creating enhanced solutions & applications

• Consumer behavior…more demanding • Social Values -- changing life-style owing to

reducing average age & increasing literacy levels

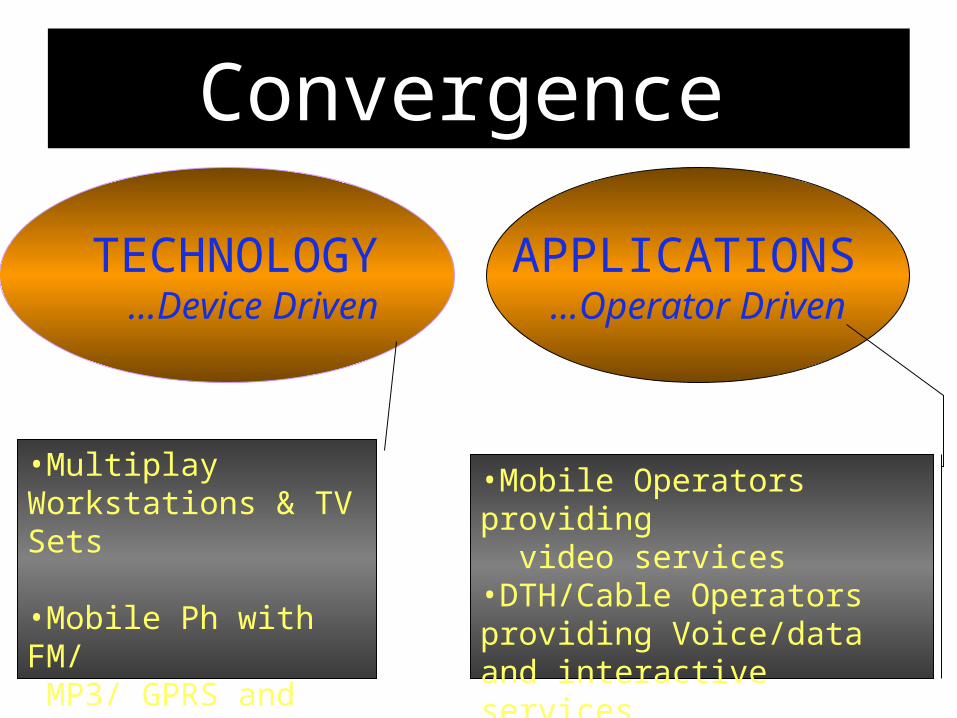

Convergence

TECHNOLOGY…Device Driven

APPLICATIONS …Operator Driven

•Multiplay Workstations & TV Sets

•Mobile Ph with FM/ MP3/ GPRS and now TV

•Mobile Operators providing video services•DTH/Cable Operators providing Voice/data and interactive services

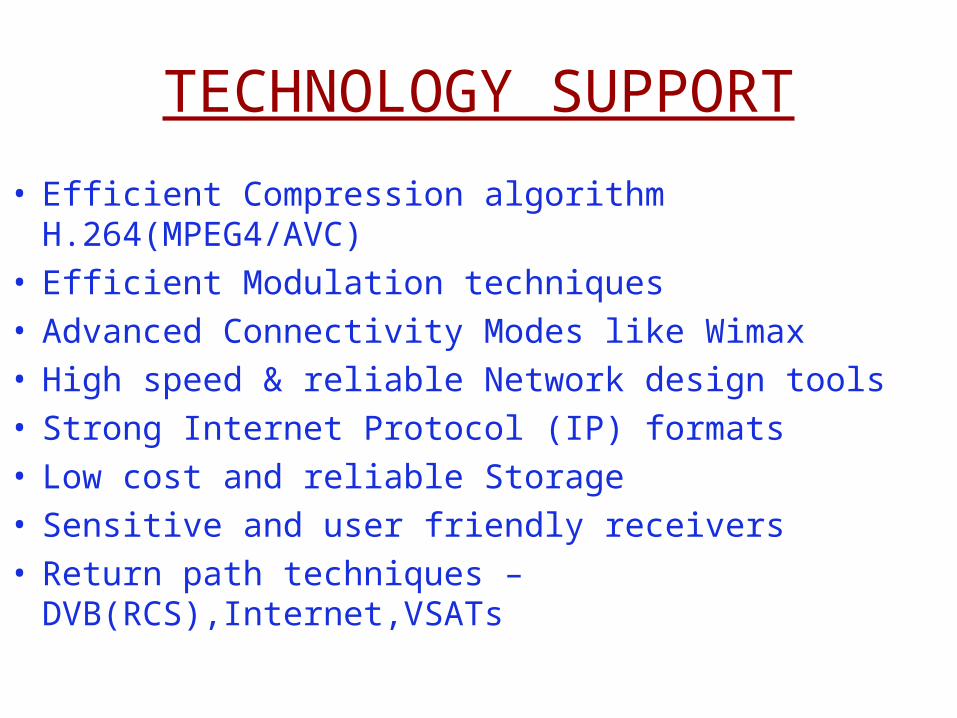

TECHNOLOGY SUPPORT

• Efficient Compression algorithm H.264(MPEG4/AVC)• Efficient Modulation techniques• Advanced Connectivity Modes like Wimax• High speed & reliable Network design tools• Strong Internet Protocol (IP) formats• Low cost and reliable Storage • Sensitive and user friendly receivers• Return path techniques –DVB(RCS),Internet,VSATs

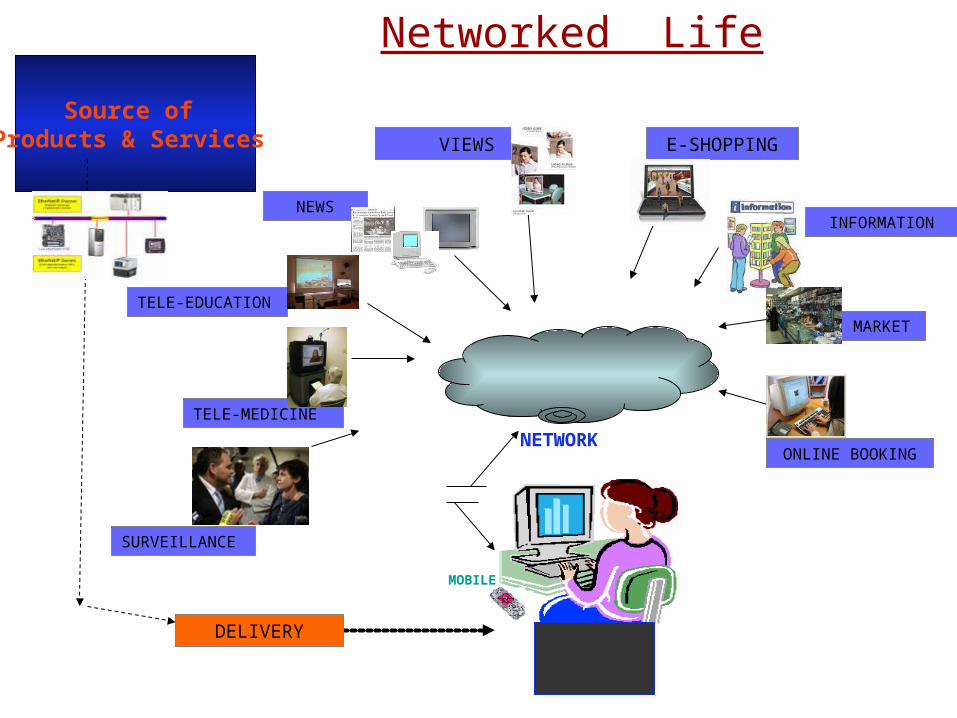

MOBILE

NEWS

VIEWS E-SHOPPING

INFORMATION

MARKET

ONLINE BOOKING

DELIVERY

NETWORK

TELE-EDUCATION

TELE-MEDICINE

SURVEILLANCE

Source of Products & Services

Networked Life

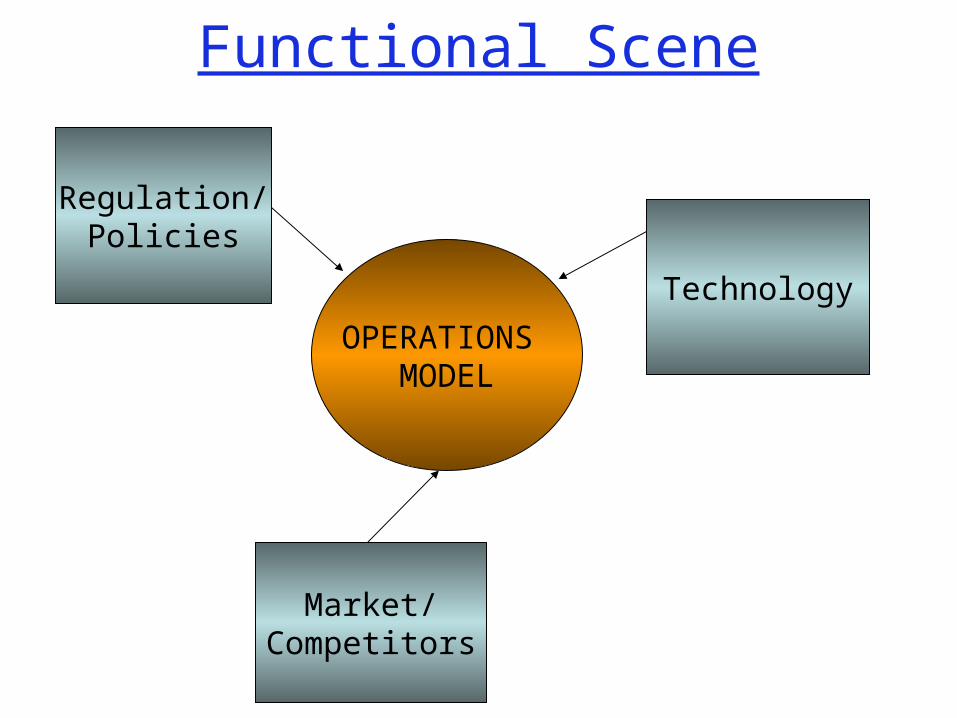

Functional Scene

OPERATIONS MODEL

Regulation/Policies

Market/Competitors

Technology

Content

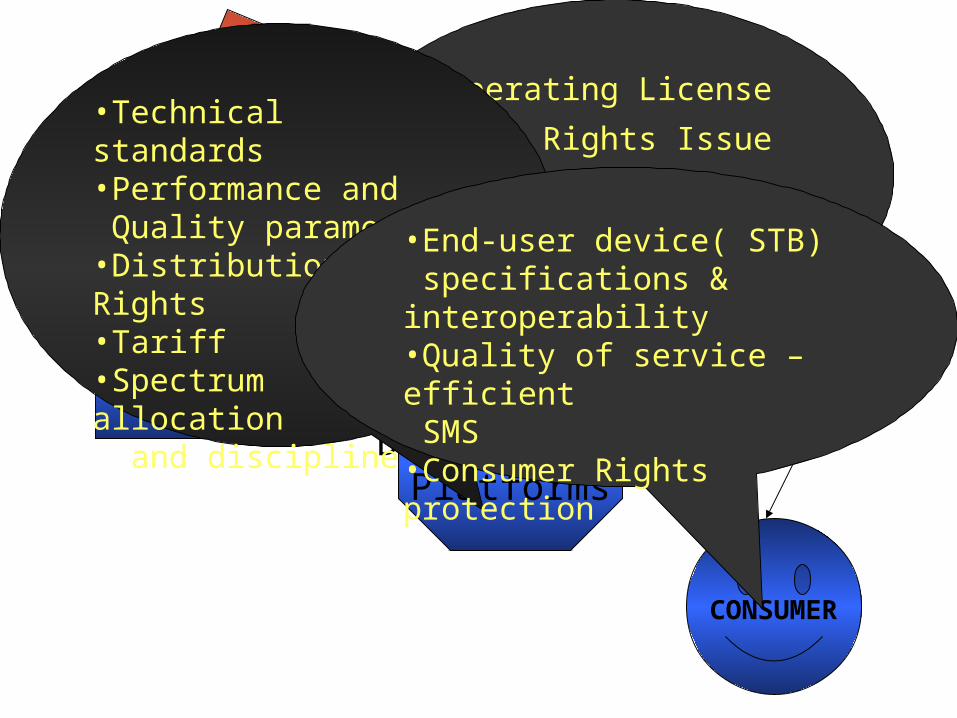

REGULATORY

CONSUMER

DistributionPlatforms

•Operating License

•Copy Rights Issue

•View Tariff

•Format standardisation

•Content Code adherence

•Technical standards•Performance and Quality parameters•Distribution Rights•Tariff •Spectrum allocation and discipline

•End-user device( STB) specifications & interoperability•Quality of service – efficient SMS•Consumer Rights protection

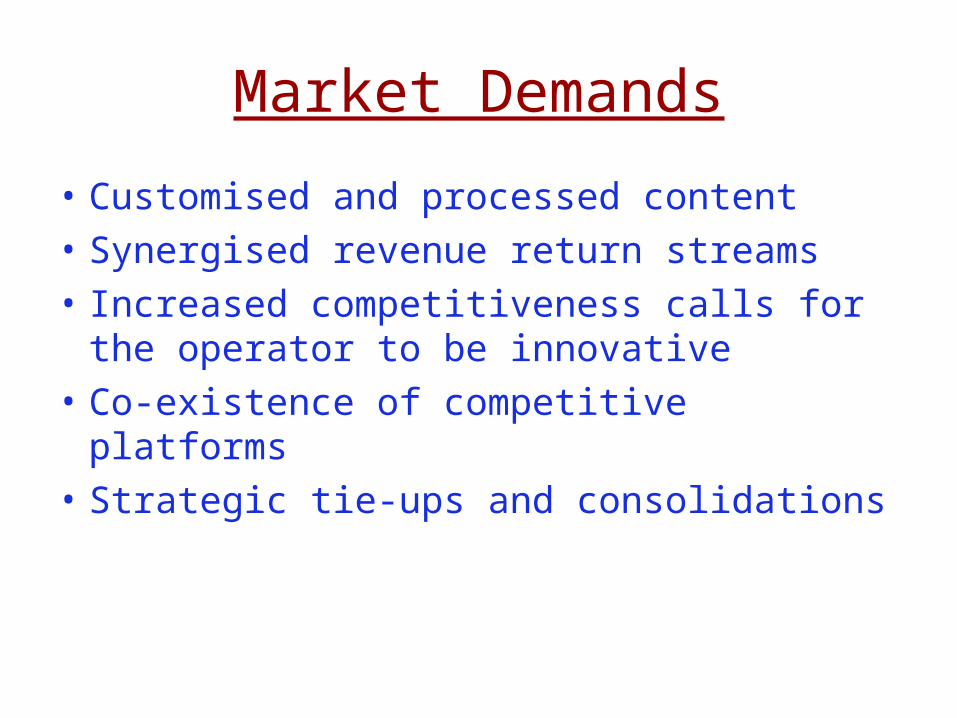

Market Demands

• Customised and processed content

• Synergised revenue return streams

• Increased competitiveness calls for the operator to be innovative

• Co-existence of competitive platforms

• Strategic tie-ups and consolidations

Technology Aspects

• Technology identification and standardisation

• Integration with the existing services

• Cost of the hardware and software applications

• Coping with the technology dynamics scene

• Return Path techniques

• Maximising product values

Challenges

Regulatory guidelinesContent protection and customisationCommercial practices and innovations

Technology would make the Convergence scenario possible and inescapable ….. But challenges stand on the face !!

Regulatory Issues

• Need for an Umbrella Regulator

• Cross-Media ownership

• Licensing process..both forward and return path

• Content Monitoring

• Spectrum planning

• Level Playing Fields – Telecom Service Providers & Broadcast Operators

•Customs Duities parity between IT & Broadcast sectors•Service tax anamoly on subscription for cable/DTH and Telecom service•FDI limit is different for IT/Telecom and Broadcast sector

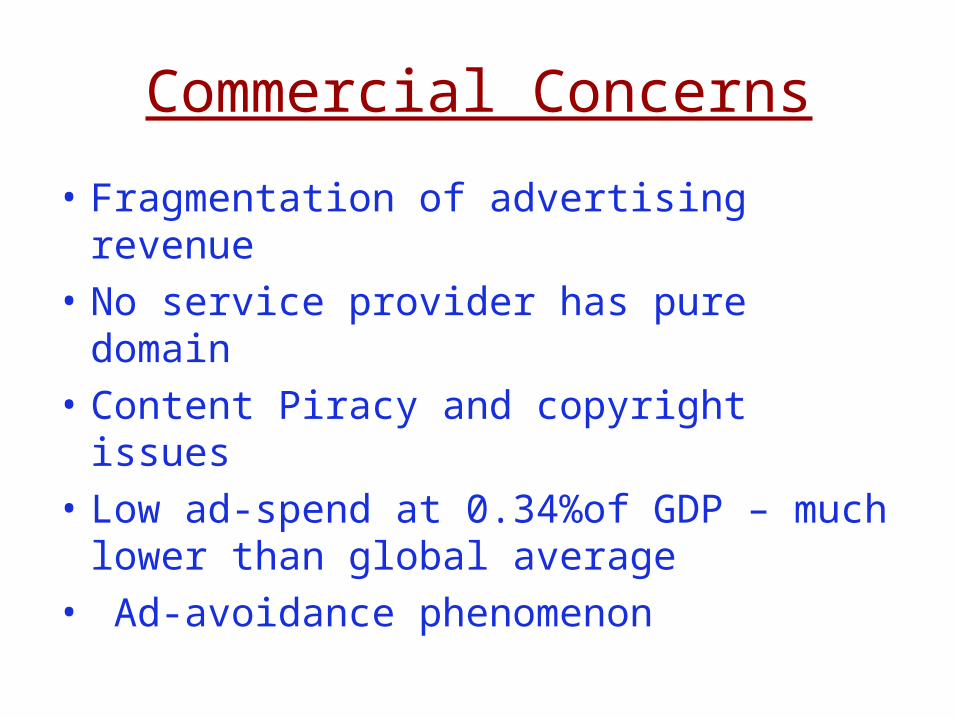

Commercial Concerns

• Fragmentation of advertising revenue

• No service provider has pure domain

• Content Piracy and copyright issues

• Low ad-spend at 0.34%of GDP – much lower than global average

• Ad-avoidance phenomenon

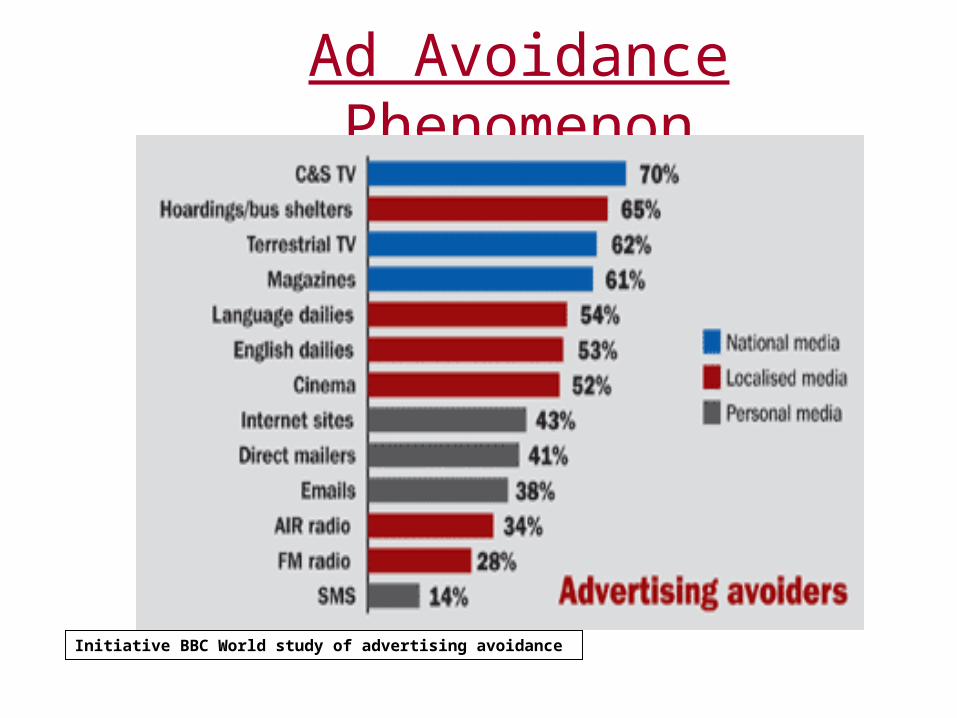

Ad Avoidance Phenomenon

Initiative BBC World study of advertising avoidance

Broadcasting

Mul

tiple

opt

ions

,In

tens

e C

ompe

titio

n

Telecom

Internet/Data

Consumer is King

The User Perspective --

Consumer Centric Business

…Immediate Implication

Consumer controlled content --- Interactive BroadcastingContent– Anywhere, AnytimeEnd product is Value RichBetter service at lower costExpansion of Market size

CONVERGENCE

A WIN-WIN SITUATION FOR ALL OF US

This is just the Beginning…!!

THANK YOU ALL