Pictures from Platts Global Energy Outlook Forum - Dec 12, 2013

Upload

apex-brasil-agencia-brasileira-de-promocao-de-exportacoes-e-investimentosCategory

view

881download

4description

17 Edition | December | 2012th

Brazilian Economic

OUTLOOK Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Ministry of Finance

December Edition | Year 2012

3

Foreword

Economic Activity

Employment and Income

Inflation

Interest Rates and Credit

Fiscal Policy

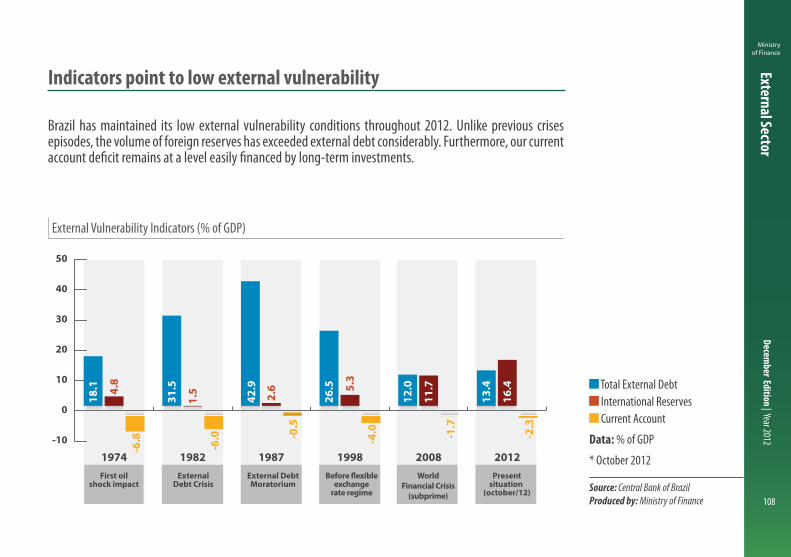

External Sector

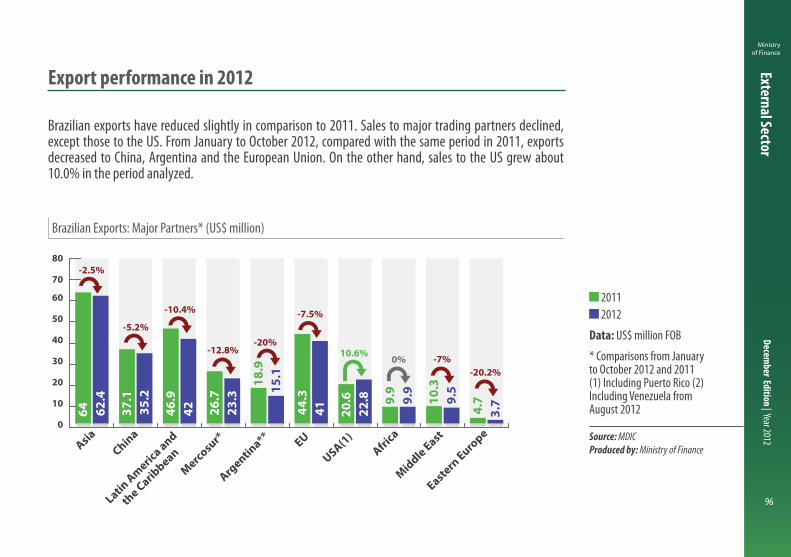

International Overview

Glossary

Summary

7

9

35

53

61

81

93

111

135

NOTE

The “Brazilian Economic Outlook” Report is published by the Ministry of Finance. It consolidates and updates the main macroeconomic variables related to the Brazilian economy. The report is coordinated by the Economic Policy Secretariat (SPE) with the contribution of the following Ministry of Finance´s bureaus: National Treasury Secretariat (STN), International Affairs Secretariat (SAIN), Secretariat for Economic Monitoring (SEAE) and Federal Revenue Secretariat (RFB). Data used in the report were updated until December 6th, 2012.

Ministry of Finance

December Edition | Year 2012

7

Ministry of Finance

Foreword

7

Brazilian economy prepared for a sustained economic growth

The Brazilian economy has shown strength in 2012, even with advanced economies remaining sluggish and world trade stagnated. Growth accelerated in the third quarter, and the economic outlook for 2013 is strong.

In order to boost the country’s productive capacity even further, this Administration has given incentives for investment and production, which have been showing consistent results. Not only do public sector investments play an important role, with emphasis on the Growth Acceleration Program (PAC 2), but also private investments are key to economic growth.

Public-private partnerships to fund relevant infrastructure projects are being stimulated, and incentives for the development of a long-term private credit market in Brazil are being implemented. As for production, payroll tax exemptions measures as well as energy cost actions have been taken, with benefits for several economic sectors.

Brazil is experiencing a very promising new macroeconomic balance with low interest rates and reduced financial costs of investment, a more competitive exchange rate, and sound fiscal results. The outcome of these measures has started to take effect, but a large part of their effects is still in the pipeline.

Brazilian Economy

OUTLOOK

Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Economic Activity

Ministry of Finance

December Edition | Year 2012

10

Economic Activity

10

Under the world economic slowdown, the Brazilian economy grew 2.4% in annual terms during the third quarter of 2012, showing that the country´s economic activity is resilient. In addition to that, data already released show positive results for fourth quarter. The economic outlook for 2013 is promising.

This Administration has taken a series of measures to increase the country´s competitiveness, encouraging investment and production. For instance, infrastructure investments, through the PAC 2 and concession programs, are already in place. Moreover, the payroll tax relief for 40 sectors, the program for reducing energy costs, and the new automotive regime for 2013-2017 are other measures which ensures growing productive capacity.

Recovery in economic activity

Ministry of Finance

December Edition | Year 2012

Economic Activity

11

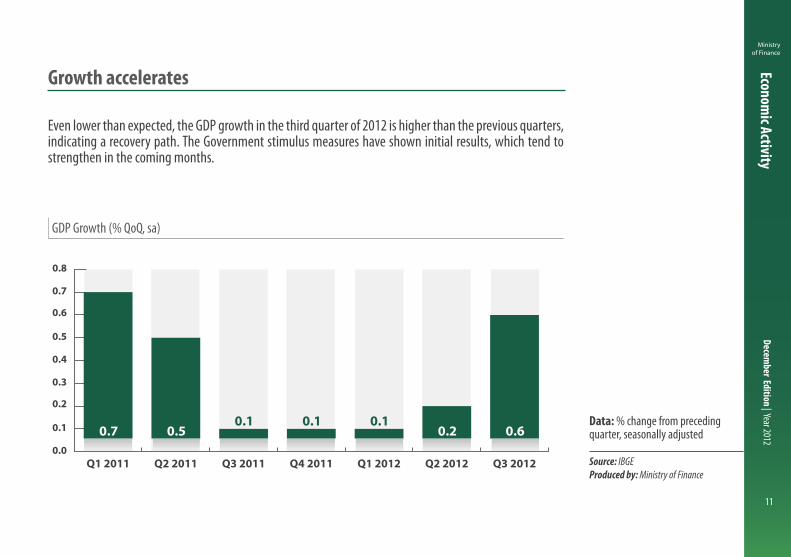

GDP Growth (% QoQ, sa)

Data: % change from preceding quarter, seasonally adjusted

Source: IBGEProduced by: Ministry of Finance

Growth accelerates

Even lower than expected, the GDP growth in the third quarter of 2012 is higher than the previous quarters, indicating a recovery path. The Government stimulus measures have shown initial results, which tend to strengthen in the coming months.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Q3 2012Q2 2012Q1 2012Q4 2011Q3 2011Q2 2011Q1 2011

0.7 0.50.1 0.1 0.1

0.2 0.6

Ministry of Finance

December Edition | Year 2012

Economic Activity

12

GDP Growth Rate: Demand and Supply (% QoQ, sa)

Q2 2012 Q3 2012

Data: % change from preceding quarter, seasonally adjusted

Source: IBGEProduced by: Ministry of Finance

Economic growth: supply and demand

From a supply-side perspective, the 3rd-quarter output was driven by the performances of the agricultural (2.5%) and industrial sectors (1.1%), highlighted by manufacturing and civil construction industries. From a demand-side perspective, household consumption supported GDP growth (0.9%).

-2

-1

0

1

2

3

4

5

6

7

8

Gross Fixed Capital

Formation

GovernmentConsumption

HouseholdConsumption

GDPServicesIndustryAgricultural

Supply Demand

2012Q3 2012Q2

2.5 1.

1

0.0 0.6 0.

9

0.1

6.8

0.5

0.2 0.7 1.0

-2.0

-1.8

-1.6

Ministry of Finance

December Edition | Year 2012

Economic Activity

13

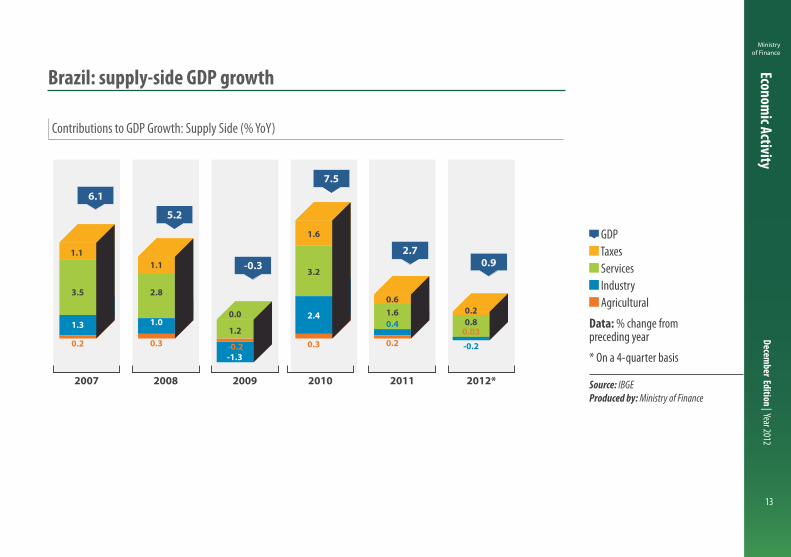

Contributions to GDP Growth: Supply Side (% YoY)

GDP Taxes Services Industry Agricultural

Data: % change from preceding year

* On a 4-quarter basis

Source: IBGEProduced by: Ministry of Finance

Brazil: supply-side GDP growth

2007 2008 2009 2010 2011 2012*

GDP

Services

Industry

Agriculture

Taxes

6.1

5.2

7.5

-0.32.7

0.91.1

3.5

1.3

0.2

1.1

2.8

1.0

0.3-1.3-0.2

0.0

1.2

1.6

3.2

2.4

0.3

0.61.60.4

0.2

0.20.8

0.03

-0.2

Ministry of Finance

December Edition | Year 2012

Economic Activity

14

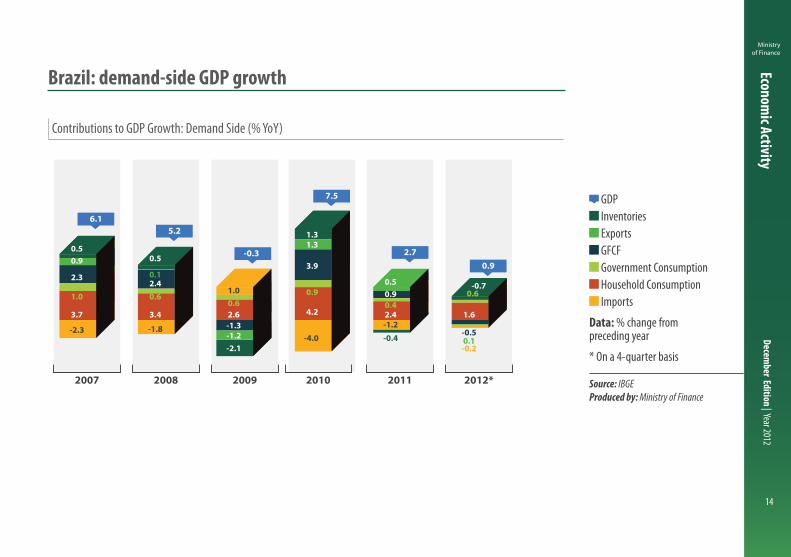

Contributions to GDP Growth: Demand Side (% YoY)

GDP Inventories Exports GFCF Government Consumption Household Consumption Imports

Data: % change from preceding year

* On a 4-quarter basis

Source: IBGEProduced by: Ministry of Finance

Brazil: demand-side GDP growth

2007 2008 2009 2010 2011 2012*

6.15.2

-0.3

7.5

2.70.9

GDP

Inventories

GFCF

Government consumption

Household consumption

Imports

Exports

0.9

2.3

3.7

1.0

0.5

-2.3

0.5

2.4

3.4

0.1

0.6

-1.8

1.00.62.6

-2.1-1.2-1.3

3.9

0.9

4.2

-4.0

1.31.3

0.50.90.42.4

-0.4

-1.2

0.6

1.6

0.1

-0.7

-0.5

-0.2

Ministry of Finance

December Edition | Year 2012

Economic Activity

15

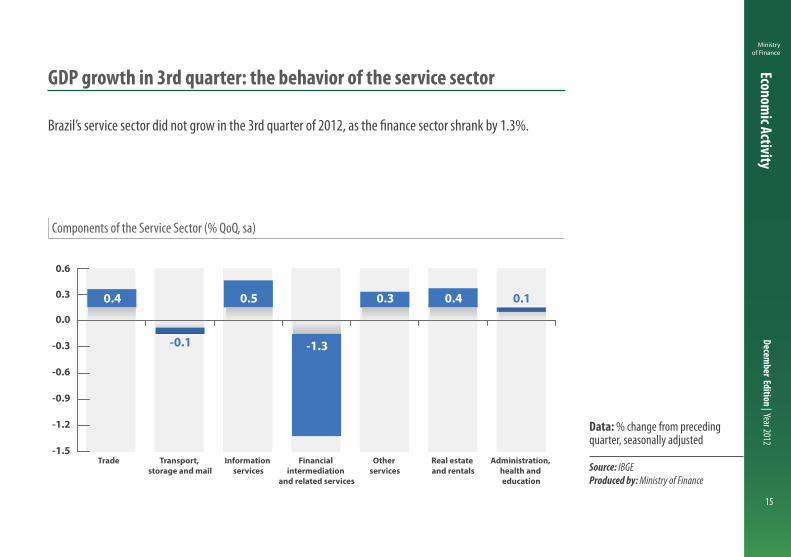

Components of the Service Sector (% QoQ, sa)

Data: % change from preceding quarter, seasonally adjusted

Source: IBGEProduced by: Ministry of Finance

GDP growth in 3rd quarter: the behavior of the service sector

Brazil’s service sector did not grow in the 3rd quarter of 2012, as the finance sector shrank by 1.3%.

-1.5

-1.2

-0.9

-0.6

-0.3

0.0

0.3

Administration, health and education

Real estate and rentals

Other services

Financial intermediation

and related services

Information services

Transport, storage and mail

Trade

0.6

0.4

-0.1

0.5

-1.3

0.3 0.4 0.1

Ministry of Finance

December Edition | Year 2012

Economic Activity

16

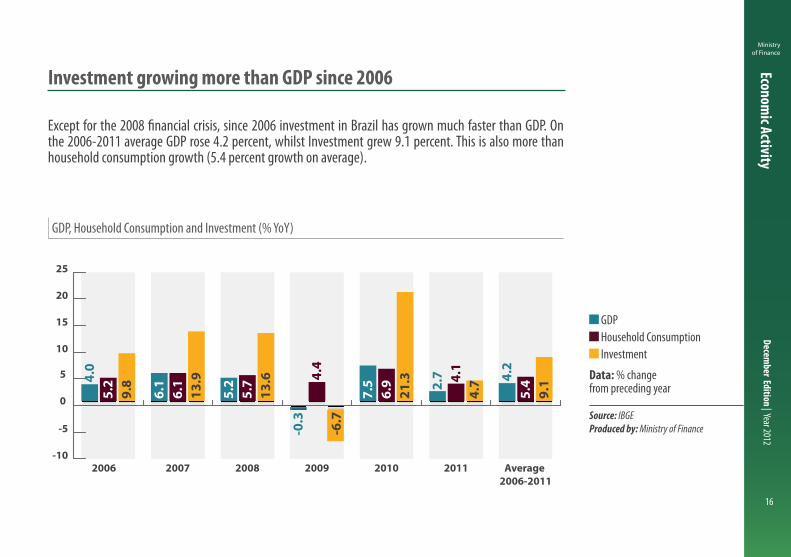

GDP, Household Consumption and Investment (% YoY)

GDP Household Consumption Investment

Data: % change from preceding year

Source: IBGEProduced by: Ministry of Finance

Investment growing more than GDP since 2006

Except for the 2008 financial crisis, since 2006 investment in Brazil has grown much faster than GDP. On the 2006-2011 average GDP rose 4.2 percent, whilst Investment grew 9.1 percent. This is also more than household consumption growth (5.4 percent growth on average).

-10

-5

0

5

10

15

20

25

-0.3

9.8

13.9

13.6

-6.7

21.3

4.7

9.1

5.2

6.1

5.7 4.

4

6.9 4.

1

5.44.

0

6.1

5.2

7.5 2.

7 4.2

Average 2006-2011

201120102009200820072006

GDPGFCF Household Consumption

Ministry of Finance

December Edition | Year 2012

Economic Activity

17

Industrial Production Index (index number, sa)

Data: index number, seasonally adjusted (average 2002 = 100)

Source: IBGEProduced by: Ministry of Finance

Industrial production points to growth recovery

Industrial production increased by 0.9% in October 2012 against September, sustained mainly by the manufacturing of intermediate goods (0.6%). The third quarter of 2012 had already recorded an 1.1% expansion. The result strengthens the optimism in relation to the activity recovery for the industrial sector.

90

95

100

105

110

115

120

125

130

135

Oct 2012

Sep 2012

Jun 2012

Mar 2012

Dec 2011

Sep 2011

Jun 2011

Mar 2011

Dec 2010

Sep 2010

Jun 2010

Mar 2010

Dec 2009

Sep 2009

Jun 2009

Mar 2009

Dec 2008

Sep 2008

Jun 2008

Mar 2008

Dec 2007

Sep 2007

127.0

Index-number (average 2002=100)

Ministry of Finance

December Edition | Year 2012

Economic Activity

18

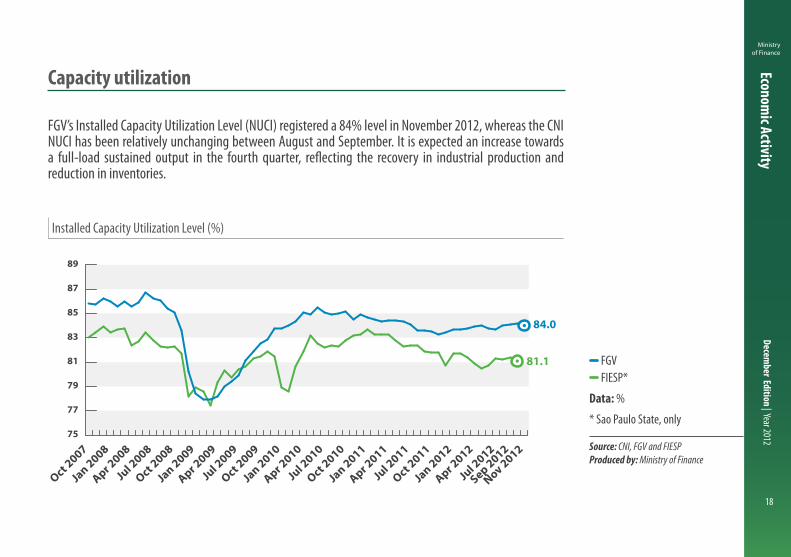

Installed Capacity Utilization Level (%)

FGV FIESP*

Data: %

* Sao Paulo State, only

Source: CNI, FGV and FIESPProduced by: Ministry of Finance

Capacity utilization

FGV’s Installed Capacity Utilization Level (NUCI) registered a 84% level in November 2012, whereas the CNI NUCI has been relatively unchanging between August and September. It is expected an increase towards a full-load sustained output in the fourth quarter, reflecting the recovery in industrial production and reduction in inventories.

75

77

79

81

83

85

87

89

84.0

81.1

NUCI - FIESP** NUCI - FGV

Nov 2012

Sep 2012

Jul 2

012

Apr 2012

Jan 2012

Oct 2011

Jul 2

011

Apr 2011

Jan 2011

Oct 2010

Jul 2

010

Apr 2010

Jan 2010

Oct 2009

Jul 2

009

Apr 2009

Jan 2009

Oct 2008

Jul 2

008

Apr 2008

Jan 2008

Oct 2007

Ministry of Finance

December Edition | Year 2012

Economic Activity

19

Retail Trade Survey (% YoY)

PMC Broad PMC*

Data: % change from preceding year

* Including vehicles, motorcycles, parts and pieces, and building materials

Source: IBGEProduced by: Ministry of Finance

Robust retail sales

Both retail sales indicators follow an acceleration trend, registering 8.1% and 6.6% on a 12-month basis, respectively.

8.1

6.6

0

2

4

6

8

10

12

14

Sep 2012

Jul 2

012

May 2012

Mar 2012

Jan 2012

Nov 2011

Sep 2011

Jul 2

011

May 2011

Mar 2011

Jan 2011

Nov 2010

Sep 2010

Jul 2

010

May 2010

Mar 2010

Jan 2010

Nov 2009

Sep 2009

Broad PMC Restricted PMC

Ministry of Finance

December Edition | Year 2012

Economic Activity

20

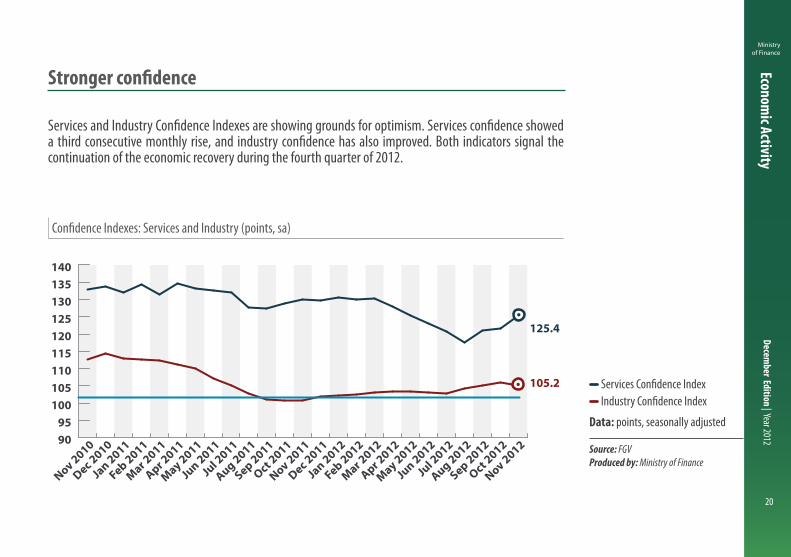

Confidence Indexes: Services and Industry (points, sa)

Services Confidence Index Industry Confidence Index

Data: points, seasonally adjusted

Source: FGVProduced by: Ministry of Finance

Stronger confidence

Services and Industry Confidence Indexes are showing grounds for optimism. Services confidence showed a third consecutive monthly rise, and industry confidence has also improved. Both indicators signal the continuation of the economic recovery during the fourth quarter of 2012.

9095

100105110115120125130135140

125.4

105.2

Industry Con�dence IndexServices Con�dence Index

Nov 2012

Oct 2012

Sep 2012

Aug 2012

Jul 2

012

Jun 2012

May 2012

Apr 2012

Mar 2012

Feb 2012

Jan 2012

Dec 2011

Nov 2011

Oct 2011

Sep 2011

Aug 2011

Jul 2

011

Jun 2011

May 2011

Apr 2011

Mar 2011

Feb 2011

Jan 2011

Dec 2010

Nov 2010

Ministry of Finance

December Edition | Year 2012

Economic Activity

21

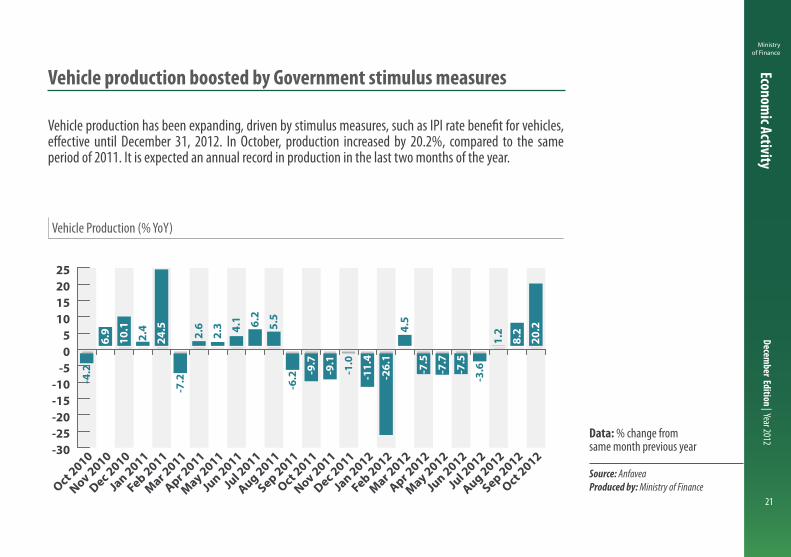

Vehicle Production (% YoY)

Data: % change from same month previous year

Source: AnfaveaProduced by: Ministry of Finance

Vehicle production boosted by Government stimulus measures

Vehicle production has been expanding, driven by stimulus measures, such as IPI rate benefit for vehicles, effective until December 31, 2012. In October, production increased by 20.2%, compared to the same period of 2011. It is expected an annual record in production in the last two months of the year.

-30-25-20-15-10

-505

10152025

Oct 2012

Sep 2012

Aug 2012

Jul 2

012

Jun 2012

May 2012

Apr 2012

Mar 2012

Feb 2012

Jan 2012

Dec 2011

Nov 2011

Oct 2011

Sep 2011

Aug 2011

Jul 2

011

Jun 2011

May 2011

Apr 2011

Mar 2011

Feb 2011

Jan 2011

Dec 2010

Nov 2010

Oct 2010

10.1

2.4

24.5

2.6

2.3 4.

1 6.2

4.5

1.2

20.2

-4.2

-7.2 -6.2 -2

6.1

-3.6

-11.

4

-7.5

-7.7

-7.5

-9.7

-9.1

-1.0

5.5

6.9

8.2

Ministry of Finance

December Edition | Year 2012

Economic Activity

22

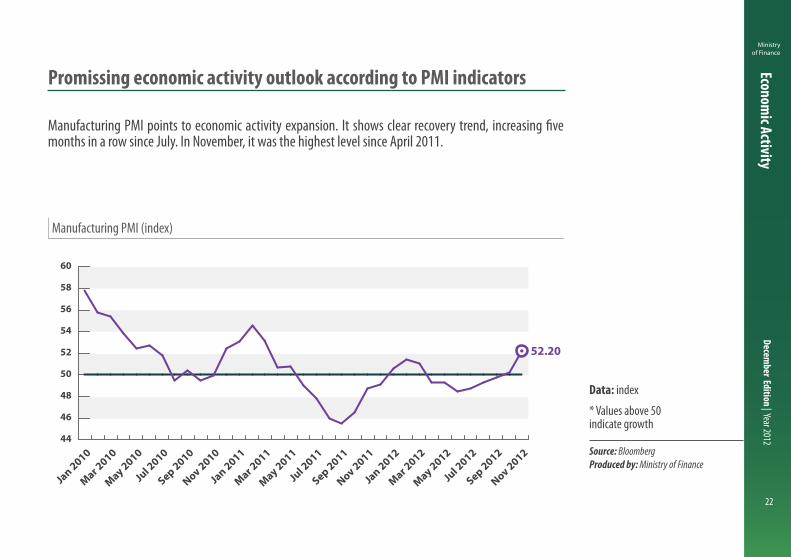

Manufacturing PMI (index)

Data: index

* Values above 50 indicate growth

Source: BloombergProduced by: Ministry of Finance

Promissing economic activity outlook according to PMI indicators

Manufacturing PMI points to economic activity expansion. It shows clear recovery trend, increasing five months in a row since July. In November, it was the highest level since April 2011.

44

46

48

50

52

54

56

58

60

PMI Brazil Manufacture

52.20

Nov 2012

Sep 2012

Jul 2

012

May 2012

Mar 2012

Jan 2012

Nov 2011

Sep 2011

Jul 2

011

May 2011

Mar 2011

Jan 2011

Nov 2010

Sep 2010

Jul 2

010

May 2010

Mar 2010

Jan 2010

Ministry of Finance

December Edition | Year 2012

Economic Activity

23

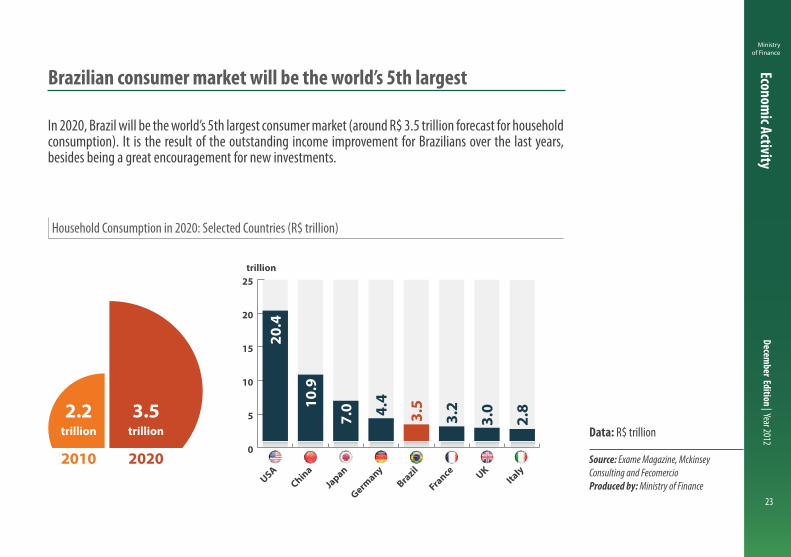

Household Consumption in 2020: Selected Countries (R$ trillion)

Data: R$ trillion

Source: Exame Magazine, Mckinsey Consulting and FecomercioProduced by: Ministry of Finance

Brazilian consumer market will be the world’s 5th largest

In 2020, Brazil will be the world’s 5th largest consumer market (around R$ 3.5 trillion forecast for household consumption). It is the result of the outstanding income improvement for Brazilians over the last years, besides being a great encouragement for new investments.

0

5

10

15

20

25

ItalyUK

France

Brazil

Germany

Japan

ChinaUSA

20.4

10.9

7.0 4.

4

3.5

3.2

3.0

2.8

2010 2020

2.2 3.5trillion

trillion

trillion

Ministry of Finance

December Edition | Year 2012

Economic Activity

24

Consumer Market (position)

Data: position

Source: Exame Magazine, Mckinsey Consulting, Escopo, Euromonitor, Anfavea and AbracicloProduced by: Ministry of Finance

Brazilian consumer market will attract more and more investments

Investors recognize the growing trend of the Brazilian consumer market and, despite the international crisis, Brazil continues as one of the leading investment destinations.

Brazilian ConsumptionSector 2012 2020

Perfumery Articles 1st 1st

Automobiles 4th 3rd

Food and beverages 4th 3rd

Clothing 5th 3rd

Domestic Aviation 4th -

Motorcycles 4th 3rd

Computers 3rd -

Refrigerators 3rd -

Products for Pet Animals 3rd 2nd

Ministry of Finance

December Edition | Year 2012

Economic Activity

25

Brazilian Grain Harvest (millions of tons)

Data: millions of tons

* Conab forecasts

Source: Conab/MAPAProduced by: Ministry of Finance

Record for the Brazilian harvest

The Brazilian grain harvest in 2011/2012 states a new record-breaking achievement, equal to 166.2 million of tons, despite the lower increase in the planted area. The growing trend of agricultural production is a result of increasing investment in the sector, and an even better result is expected for 2012/2013.

70

80

90

100

110

120

130

140

150

160

170

180

2012/2013*

2011/2012

2010/2011

2009/2010

2008/2009

2007/2008

2006/2007

2005/2006

2004/2005

2003/2004

2002/2003

2001/2002

2000/2001

1999/2000

83.0

100.3 96.8

123.2 119.1114.7

122.5

131.8

144.1135.1

149.3

162.8 166.2

180.2

Ministry of Finance

December Edition | Year 2012

Economic Activity

26

Agricultural Production in Selected Countries (index number)

Brazil Russia India China USA Canada European Union

Data: index number (average 2005 = 100)

Source: FAOProduced by: Ministry of Finance

Brazilian agriculture pushed to the forefront

Brazil is one of the world’s largest producer of agricultural goods and its production will grow even further in the coming years. Due to outstanding agricultural production, the country has already established itself as one of the main exporters of primary goods.

40

60

80

100

120

140

160

180

20192016

20132010

20072004

20011998

19951992

Brazil

Russia

China

CanadaEU*

United States

India

Estimates

2014

Ministry of Finance

December Edition | Year 2012

Economic Activity

27

Federal Government Investment (R$ billion and %)

2011 2012

Data: R$ billion and % change in the period

* YTD: year-to-date

Source: STN/Ministry of FinanceProduced by: Ministry of Finance

Federal investment has increased

Federal Government investment pace has increased in the last 12 months. Until October 2012, investments are 22.9% above the same period last year.

0

10

20

30

40

50

60

OctSepAugJulJunMayAprMarFeb Jan

27.9% 23.3%22.9%

-1.0%3.3%

23.5%28.9%

30.2%

29.4%

30.7%

7.7

9.6

15.7

21.1

26.2

32.8

38.8

42.5

45.2

50.9

7.8

9.3

12.7

16.4

20.2

25.1

30.0

33.2

36.7

41.4

Ministry of Finance

December Edition | Year 2012

Economic Activity

28

Public Sector Investment* (% of GDP)

State-owned companies States and Municipalities Government

Data: % of GDP

* Only investments carried out directly by the National Government (not including transfers to States and Municipalities, to private institutions or MCMV, which are accounted by the IBGE as GFCF);

** Ministry of Finance forecast

Source: STN/Ministry of FinanceProduced by: Ministry of Finance

Public investment is also increasing fast

The consolidated public investment is on an expansion track in 2012, contributing to better long-term economic prospects.

0

1

2

3

4

5

1.6 1.51.5

1.3

0.80.8

0.9

1.1

1.1 1.0 1.0

1.0 1.1

1.4

1.8

1.9

1.7

1.9

1.7 1.81.5

2.0

1.31.5 1.5

1.8

1.3 1.4 1.3

1.61.4

1.8 1.7

2.0

1.71.8

2012**2011

20102009

20082007

20062005

20042003

20022001

20001999

19981997

19961995

0.5 0.4 0.4 0.5 0.3 0.3 0.4 0.5 0.2 0.2 0.3 0.4 0.4 0.5 0.6 0.8 0.6 0.7

1.7 1.81.5

2.0

1.31.5 1.5

1.8

1.3 1.4 1.31.6

1.4

1.8 1.7

2.0

1.71.8

1.6 1.51.5

1.3

0.80.8

0.9

1.1

1.1 1.0 1.01.0 1.1

1.41.8

1.9

1.71.9

State-owned Companies States and Municipalities Federal Government

Ministry of Finance

December Edition | Year 2012

Economic Activity

29

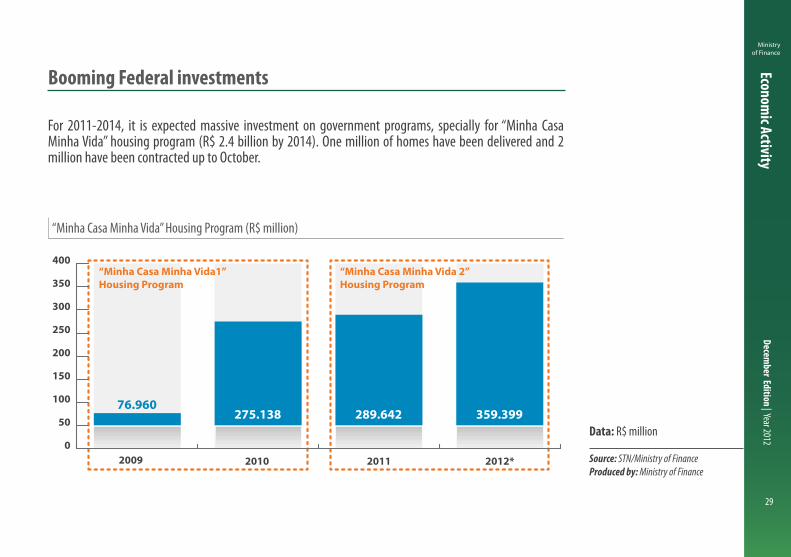

“Minha Casa Minha Vida” Housing Program (R$ million)

Data: R$ million

Source: STN/Ministry of FinanceProduced by: Ministry of Finance

Booming Federal investments

For 2011-2014, it is expected massive investment on government programs, specially for “Minha Casa Minha Vida” housing program (R$ 2.4 billion by 2014). One million of homes have been delivered and 2 million have been contracted up to October.

0

50

100

150

200

250

300

350

400

2012*201120102009

76.960 275.138 289.642 359.399

“Minha Casa Minha Vida1”Housing Program

“Minha Casa Minha Vida 2” Housing Program

Ministry of Finance

December Edition | Year 2012

Economic Activity

30

PAC Spending: 2011-2012 (R$ billion)

2011 2012

Data: R$ billion

* YTD: year-to-date

Source: STN/Ministry of FinanceProduced by: Ministry of Finance

PAC speeds up investments

PAC 2 investments have moved consistently upwards in 2012 compared to last year. For example, amounts paid up to October 2012 (R$ 26.6 billion) are larger 27.7% than in 2011 (R$ 20.8 billion). As a result, there will be increasing economic activity and higher country’s productive capacity.

0

5

10

15

20

25

30

5.6% 19.1%

46.9%50.0%

44.8%

52.6%36.3%

33.5%35.1%

27.7%

3.1

4.1

8.0

11.3

14.2

18.6

20.3

22.3

24.3

26.6

2.9

3.5

5.5

7.6

9.8

12.2

14.9

16.7

18.0

20.8

2012 2011

OctSepAugJulJunMayAprMarFebJan

Ministry of Finance

December Edition | Year 2012

Economic Activity

31

Petrobras Business Plan (US$ billion)

Data: US$ billion

* Released on June 14, 2012

Source: PetrobrasProduced by: Ministry of Finance

Petrobras: top 2 global energy investor

According to the International Energy Agency (IEA), Petrobras will invest US$ 47.3 billion in new projects in 2012, just below Petrochina (US$ 48 billion). Also, Petrobras will remain as a major worldwide investor over the next four years, based on the company’s business plan, which states a US$ 236.5 billion investment for 2012-2016.

Business Plan - Petrobras*, 2012 to 2016 (US$ billion)

Exploration and Production 141.865.5

Gas and Energy 13.8Petrochemical 5.0Distribution 3.6Biofuel 3.8Corporate 3.0Total 236.5

Re�ning, Transportation and trading

Ministry of Finance

December Edition | Year 2012

Economic Activity

32

Public Service Concession

Source: Secretariat of Civil AviationProduced by: Ministry of Finance

Concession Program will leverage investments in infrastructure

Infrastructure investments in Brazil will count on the private sector’s active involvement. The airport sector total investment will be approximately R$ 16 billion in the coming years, considering only airport concessions in Brasilia, Guarulhos and Viracopos. Also, the Logistics Investment Program considers R$ 133 billion for renovation and construction of federal highways and railways. Around 60% (R$ 79.5 billion) will be invested within 5 years.

Total Investment: R$ 133 billion (R$ 79.5 billionin 5 years and R$ 53.5 billion from 20 to 25 years

Airport Concession: Planned Investment R$ 16.2 billion

Investment on Highways R$ 42 billion

(7.500 km)(R$ 23.5 bi in 5 years and R$ 18.5 bi in 20 years)

Investment in Railways R$ 91 billion (10,000 km)

(R$ 56 bi in 5 years and R$ 35 bi in 25 years)

Guarulhos

Total in 25 years

R$ 2.85 bi

Total in 30 years

R$ 8.70 bi

ViracoposBrasília

Total in 20 years

R$ 4.70 bi

Planned Investment = 16.2 bi

Ministry of Finance

December Edition | Year 2012

Economic Activity

33

Energy Cost Reduction

* From January 2013

Source: Ministry of Mining and EnergyProduced by: Ministry of Finance

Government has adopted incentives to improve competitiveness

Among the measures aimed at increasing domestic firms’ competitiveness, the 20.2% average reduction in energy prices is directed to the industrial sector. The measure will also benefit consumers, reducing their energy bill.

Average reduction in eletricity prices*

Group Tari� Voltage level Deduction (%)

High Voltage A

A1 230 kV or more 28.0A2 88 to 138 kV 24.7A3 69 kV 21.5

A3a 30 to 44 kV 20.0A4 2,3 to 25 kV 19.4AS Underground 19.7

Low Voltage B B lower than 2,3 kV 16.2

Average 20.2

Ministry of Finance

December Edition | Year 2012

Economic Activity

34

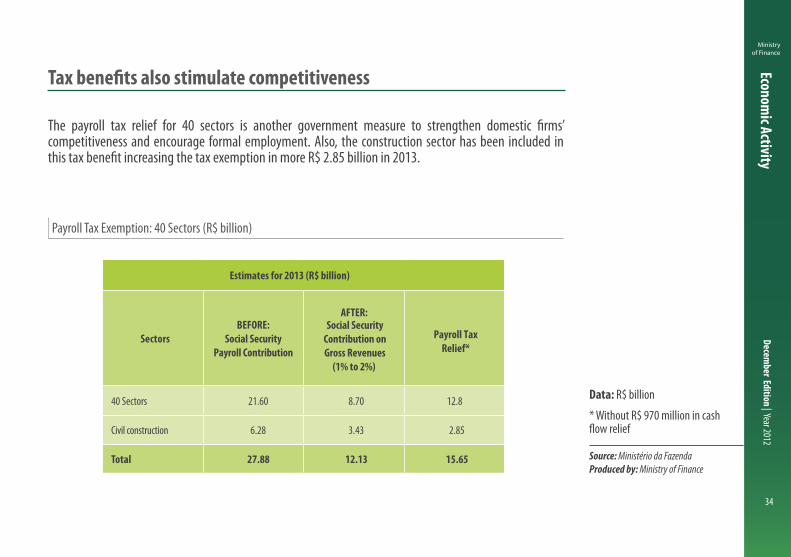

Payroll Tax Exemption: 40 Sectors (R$ billion)

Data: R$ billion

* Without R$ 970 million in cash flow relief

Source: Ministério da FazendaProduced by: Ministry of Finance

Tax benefits also stimulate competitiveness

The payroll tax relief for 40 sectors is another government measure to strengthen domestic firms’ competitiveness and encourage formal employment. Also, the construction sector has been included in this tax benefit increasing the tax exemption in more R$ 2.85 billion in 2013.

Estimates for 2013 (R$ billion)

Sectors

AFTER:

Payroll TaxRelief*

40 Sectors 21.60 8.70 12.8

Civil construction 6.28 3.43 2.85

Total 27.88 12.13 15.65

BEFORE:Social Security

Payroll Contribution

Social SecurityContribution onGross Revenues

(1% to 2%)

Brazilian Economy

OUTLOOK

Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Employment and Income

Ministry of Finance

December Edition | Year 2012

36

Employm

ent and Income

The labor market remains a key element in the process of upward social mobility. In this context, the unemployment rate reached 5.3% in October 2012 and approximately 1.7 million formal jobs were created in the year. Thus, it is expected that the increasing formalization and the expansion of policies related to guarantee of basic income, access to public services and productive inclusion continue driving the socioeconomic inclusion of the poorest.

The prospect is that the Brazilian economy will be even stronger with the increase of the middle class, or “C” class. According to the IPEA, the “C” class will incorporate 15 million people by 2014, reaching 59% of the population. This means an enormous consumption potential, which is fundamental to stimulate an increase in the productive capacity in Brazil.

It is also important to emphasize that the strengthening of the social safety net increases not only household consumption, but also the quality of the workforce that enters the labor market. The pro-equity social policies have contributed substantially towards the rise in labor productivity. In this sense, the share of the employed population with 11 years or more of schooling has increased from 33.6% to 46.3% between 2004 and 2011. This is another stimulus towards new investment.

Inclusive growth driven by increased schooling

Ministry of Finance

December Edition | Year 2012

37

Employm

ent and Income

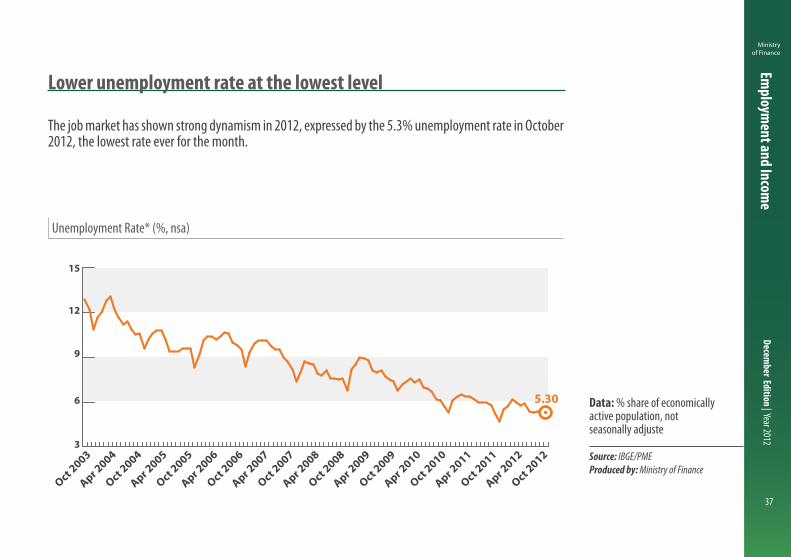

Unemployment Rate* (%, nsa)

Data: % share of economically active population, not seasonally adjuste

Source: IBGE/PMEProduced by: Ministry of Finance

Lower unemployment rate at the lowest level

The job market has shown strong dynamism in 2012, expressed by the 5.3% unemployment rate in October 2012, the lowest rate ever for the month.

3

6

9

12

15

5.30

Oct 2012

Apr 2012

Oct 2011

Apr 2011

Oct 2010

Apr 2010

Oct 2009

Apr 2009

Oct 2008

Apr 2008

Oct 2007

Apr 2007

Oct 2006

Apr 2006

Oct 2005

Apr 2005

Oct 2004

Apr 2004

Oct 2003

Ministry of Finance

December Edition | Year 2012

38

Employm

ent and Income

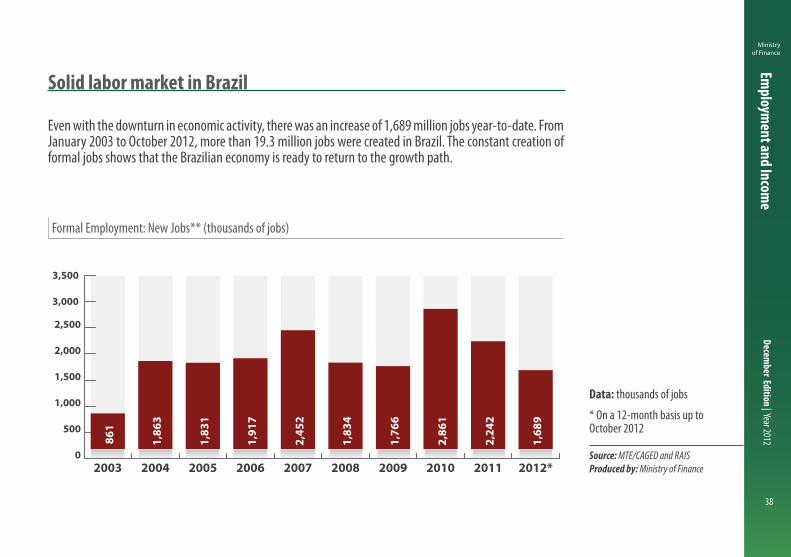

Formal Employment: New Jobs** (thousands of jobs)

Data: thousands of jobs

* On a 12-month basis up to October 2012

Source: MTE/CAGED and RAISProduced by: Ministry of Finance

Solid labor market in Brazil

Even with the downturn in economic activity, there was an increase of 1,689 million jobs year-to-date. From January 2003 to October 2012, more than 19.3 million jobs were created in Brazil. The constant creation of formal jobs shows that the Brazilian economy is ready to return to the growth path.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2012*201120102009200820072006200520042003

Formal employment (thousands)**

861

1,86

3

1,83

1

1,91

7

2,45

2

1,83

4

1,76

6

2,86

1

2,24

2

1,68

9

Ministry of Finance

December Edition | Year 2012

39

Employm

ent and Income

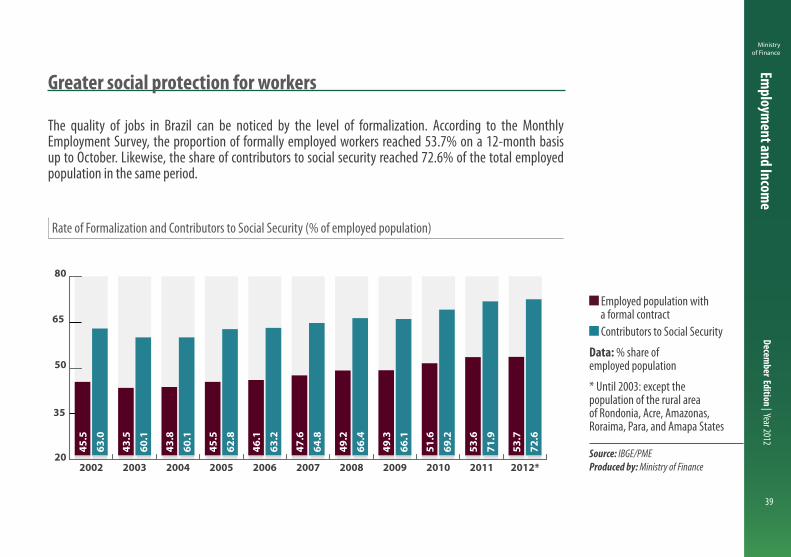

Rate of Formalization and Contributors to Social Security (% of employed population)

Employed population with a formal contract Contributors to Social Security

Data: % share of employed population

* Until 2003: except the population of the rural area of Rondonia, Acre, Amazonas, Roraima, Para, and Amapa States

Source: IBGE/PMEProduced by: Ministry of Finance

Greater social protection for workers

The quality of jobs in Brazil can be noticed by the level of formalization. According to the Monthly Employment Survey, the proportion of formally employed workers reached 53.7% on a 12-month basis up to October. Likewise, the share of contributors to social security reached 72.6% of the total employed population in the same period.

20

35

50

65

80

2012*2011201020092008200720062005200420032002

Contributors to Social Security

Employed population with a formal contract

63.0

60.1

60.1

62.8

63.2

64.8

66.4

66.1

69.2

71.9

72.6

45.5

43.5

43.8

45.5

46.1

47.6

49.2

49.3

51.6

53.6

53.7

Ministry of Finance

December Edition | Year 2012

40

Employm

ent and Income

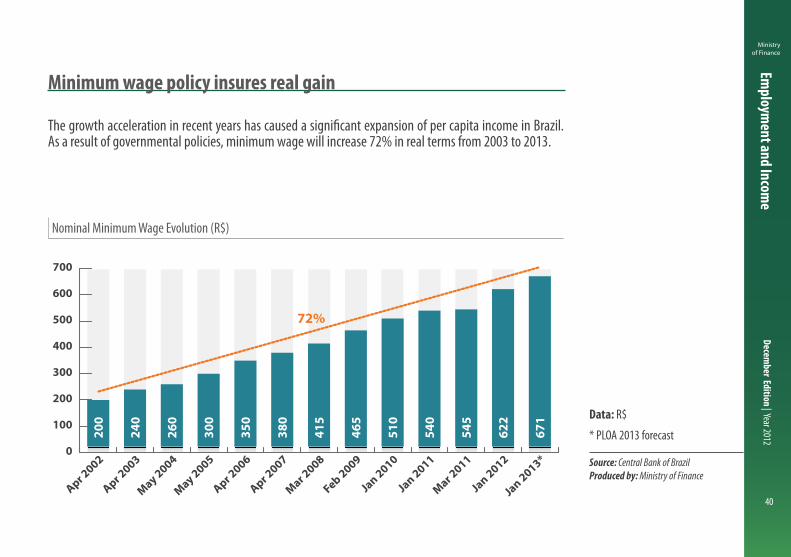

Nominal Minimum Wage Evolution (R$)

Data: R$

* PLOA 2013 forecast

Source: Central Bank of BrazilProduced by: Ministry of Finance

Minimum wage policy insures real gain

The growth acceleration in recent years has caused a significant expansion of per capita income in Brazil. As a result of governmental policies, minimum wage will increase 72% in real terms from 2003 to 2013.

0

100

200

300

400

500

600

700

Jan 2013*

Jan 2012

Mar 2011

Jan 2011

Jan 2010

Feb 2009

Mar 2008

Apr 2007

Apr 2006

May 2005

May 2004

Apr 2003

Apr 2002

72%

200

240

260

300

350

380

415

465

510

540

545

622

671

Ministry of Finance

December Edition | Year 2012

41

Employm

ent and Income

Minimum wage purchasing power for Washing Machine: 1994-2012 (R$)

Minimum Wage (R$) Nominal Price of Washing Machine (R$) Washing Machine/Minimum Wage Ratio

Data: R$

Source: IBGE, GfK and LCAProduced by: Ministry of Finance

Restoring the purchasing power of the minimum wage

0

200

400

600

800

1,000

1,200

20122011

20102009

20082007

20062005

20042003

20022001

20001999

19981997

19961995

19940

1

2

3

4

5

6

7

8

9

1.5

622

930

Minimum Wage (R$) Nominal Price of Washing Machine (R$) Washing Machine/Minimum Wage Ratio

(R$)

• 1994: a worker would spend 8 months’ worth of minimum wage to be able to afford a Washing Machine.

• 2012: he/she would spend only 1.5 month’s worth of minimum wage.

Ministry of Finance

December Edition | Year 2012

42

Employm

ent and Income

Minimum wage purchasing power for stoves: 1994-2012 (R$)

Minimum Wage (R$) Nominal Price of Stove (R$) Stove/Minimum Wage Ratio

Data: R$

Source: IBGE, GfK and LCAProduced by: Ministry of Finance

Restoring the purchasing power of the minimum wage

0

100

200

300

400

500

600

700

20122011

20102009

20082007

20062005

20042003

20022001

20001999

19981997

19961995

1994

0.00.2

0.4

0.6

0.8

1.01.2

1.4

1.6

1.8

2.0

0.5

622

330

Minimum Wage (R$) Nominal Price of Stove (R$) Stove/Minimum Wage Ratio

(R$)

• 1994: a worker would spend 1.9 months’ worth of minimum wage to be able to afford a stove.

• 2012: he/she would spend only 0.5 month’s worth of minimum wage.

Ministry of Finance

December Edition | Year 2012

43

Employm

ent and Income

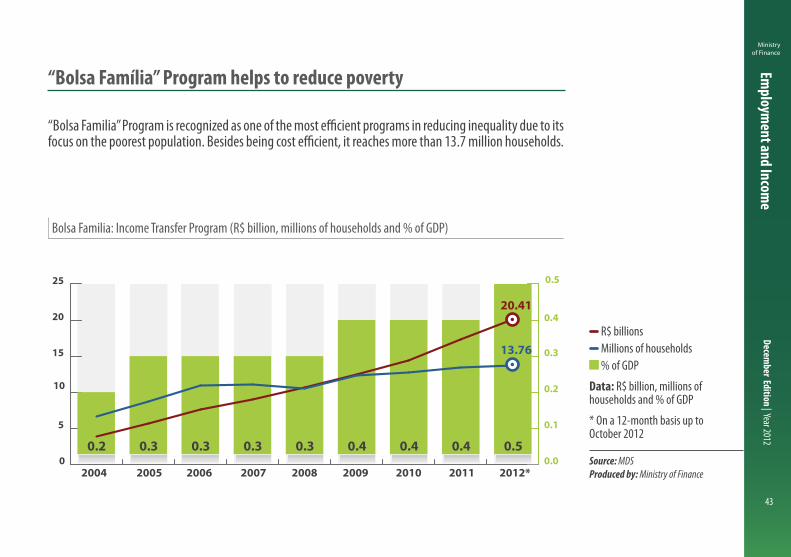

Bolsa Familia: Income Transfer Program (R$ billion, millions of households and % of GDP)

R$ billions Millions of households % of GDP

Data: R$ billion, millions of households and % of GDP

* On a 12-month basis up to October 2012

Source: MDSProduced by: Ministry of Finance

“Bolsa Família” Program helps to reduce poverty

“Bolsa Familia” Program is recognized as one of the most efficient programs in reducing inequality due to its focus on the poorest population. Besides being cost efficient, it reaches more than 13.7 million households.

0

5

10

15

20

25

0.0

0.1

0.2

0.3

0.4

0.5

2012*20112010200920082007200620052004

(% of GDP) R$ billion Number of households (million)

20.41

13.76

0.2 0.3 0.3 0.3 0.3 0.4 0.4 0.4 0.5

Ministry of Finance

December Edition | Year 2012

44

Employm

ent and Income

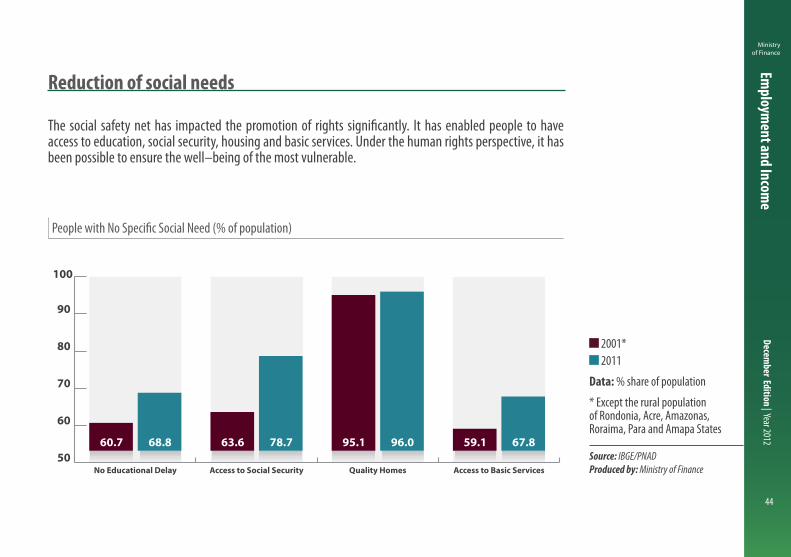

People with No Specific Social Need (% of population)

2001* 2011

Data: % share of population

* Except the rural population of Rondonia, Acre, Amazonas, Roraima, Para and Amapa States

Source: IBGE/PNADProduced by: Ministry of Finance

Reduction of social needs

The social safety net has impacted the promotion of rights significantly. It has enabled people to have access to education, social security, housing and basic services. Under the human rights perspective, it has been possible to ensure the well–being of the most vulnerable.

50

60

70

80

90

100

Access to Basic ServicesQuality HomesAccess to Social SecurityNo Educational Delay

68.8 78.7 96.0 67.860.7 63.6 95.1 59.1

2001*2011

Ministry of Finance

December Edition | Year 2012

45

Employm

ent and Income

Real Income Growth in Income Groups: 2004-2011* (%)

Data: % of simple classes, average monthly income from all jobs

* Except information from people with no declaration of income from all jobs. Deflated by INPC index.

Source: IBGE/PNADProduced by: Ministry of Finance

Income growth especially for the poorest

The real income growth was significant for the period from 2004 to 2011. Even more relevant than the 29.8% total expansion was the income growth for the 20% poorest of the population, which amounted to around 75%.

0

10

20

30

40

50

60

70

80

More th

an

90 to 100

More th

an

80 to 90

More th

an

70 to 80

More th

an

60 to 70

More th

an

50 to 60

More th

an

40 to 50

More th

an

30 to 40

More th

an

20 to 30

More th

an

10 to 20

Up to 10

Tota

l

29.8 73.8 75.3 48.5 49.9 43.8 38.4 36.5 30.3 24.8 20.8

2004-2011 Change

20%poorest

20%richest

Income deciles

Ministry of Finance

December Edition | Year 2012

46

Employm

ent and Income

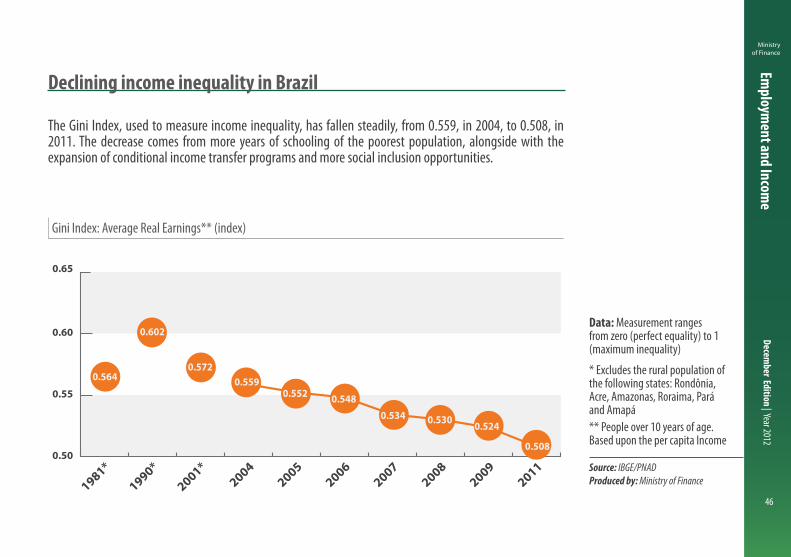

Gini Index: Average Real Earnings** (index)

Data: Measurement ranges from zero (perfect equality) to 1 (maximum inequality)

* Excludes the rural population of the following states: Rondônia, Acre, Amazonas, Roraima, Pará and Amapá** People over 10 years of age. Based upon the per capita Income

Source: IBGE/PNADProduced by: Ministry of Finance

Declining income inequality in Brazil

The Gini Index, used to measure income inequality, has fallen steadily, from 0.559, in 2004, to 0.508, in 2011. The decrease comes from more years of schooling of the poorest population, alongside with the expansion of conditional income transfer programs and more social inclusion opportunities.

0.50

0.55

0.60

0.6

0.6

0.6

0.6

0.6

0.5

20112009

20082007

20062005

20042001*

1990*

1981*

0.564

0.602

0.552 0.5480.534 0.530 0.524

0.508

0.5720.559

0.65

Ministry of Finance

December Edition | Year 2012

47

Employm

ent and Income

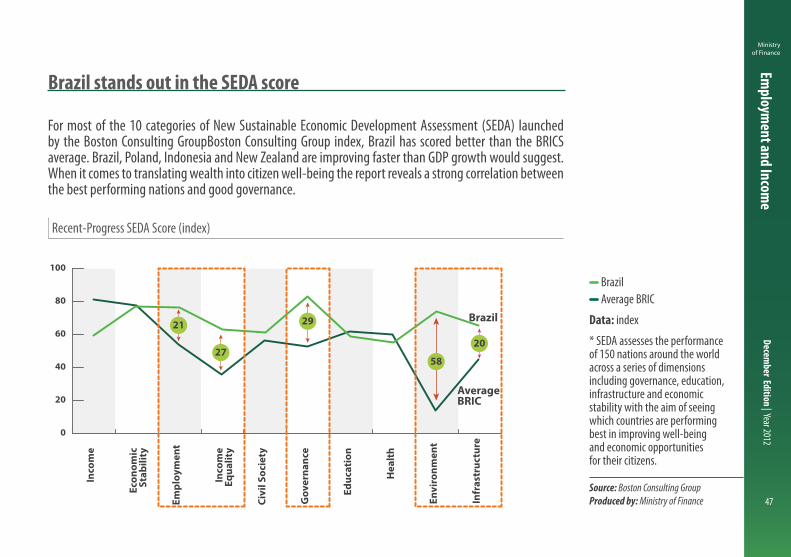

Recent-Progress SEDA Score (index)

Brazil Average BRIC

Data: index

* SEDA assesses the performance of 150 nations around the world across a series of dimensions including governance, education, infrastructure and economic stability with the aim of seeing which countries are performing best in improving well-being and economic opportunities for their citizens.

Source: Boston Consulting GroupProduced by: Ministry of Finance

Brazil stands out in the SEDA score

For most of the 10 categories of New Sustainable Economic Development Assessment (SEDA) launched by the Boston Consulting GroupBoston Consulting Group index, Brazil has scored better than the BRICS average. Brazil, Poland, Indonesia and New Zealand are improving faster than GDP growth would suggest. When it comes to translating wealth into citizen well-being the report reveals a strong correlation between the best performing nations and good governance.

0

20

40

60

80

100

Infr

astr

uctu

re

Envi

ronm

ent

Hea

lth

Educ

atio

n

Gov

erna

nce

Civi

l Soc

iety

Inco

me

Equa

lity

Empl

oym

ent

Econ

omic

Stab

ility

Inco

me

29

2027

21

58

Brazil

AverageBRIC

Ministry of Finance

December Edition | Year 2012

48

Employm

ent and Income

Social Classes (million of people)

Data: million of people

* Forecasts. Baseline: 6,5% YoY income growth rate

Source: IBGE and IPEAProduced by: Ministry of Finance

15 million additional Brazilian people can be included in the new middle class

The growth of ABC classes and consequent reduction of DE classes have been translated into poverty reduction and better income distribution, both playing a key role to the expansion of the domestic market. According to IPEA forecasts, C class should correspond to 59% of population by 2014.

A Class

B Class

C ClassD and EClasses

Total: 175 million Total: 188 million Total: 192 million Total: 196 million

2003 2009 2011 2014*

6.3

7.0

65.9

96.2

9.6

10.4

73.3

94.9

12.6

14.5

115.2

53.8

10.5

11.2

100.3

69.6

Ministry of Finance

December Edition | Year 2012

49

Employm

ent and Income

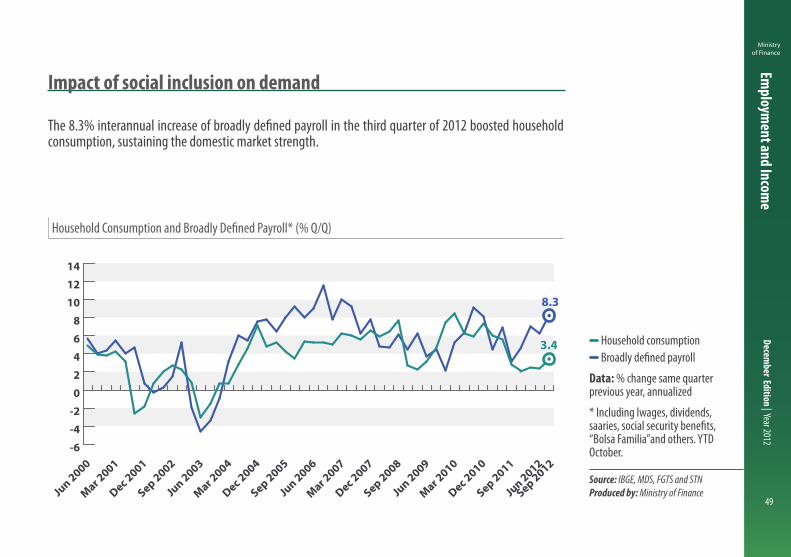

Household Consumption and Broadly Defined Payroll* (% Q/Q)

Household consumption Broadly defined payroll

Data: % change same quarter previous year, annualized

* Including lwages, dividends, saaries, social security benefits, “Bolsa Familia”and others. YTD October.

Source: IBGE, MDS, FGTS and STNProduced by: Ministry of Finance

Impact of social inclusion on demand

The 8.3% interannual increase of broadly defined payroll in the third quarter of 2012 boosted household consumption, sustaining the domestic market strength.

-6

-4

-2

0

2

4

6

8

10

12

14

Sep 2012

Jun 2012

Sep 2011

Dec 2010

Mar 2010

Jun 2009

Sep 2008

Dec 2007

Mar 2007

Jun 2006

Sep 2005

Dec 2004

Mar 2004

Jun 2003

Sep 2002

Dec 2001

Mar 2001

Jun 2000

8.3

3.4

Expanded Wage MassHousehold Consumption

Ministry of Finance

December Edition | Year 2012

50

Employm

ent and Income

People Employed with more than 11 Years of Schooling (% of total)

Data: % of total

Source: IBGE/PNADProduced by: Ministry of Finance

More qualified workers

One of the main elements for reducing income inequality and improving productivity is the educational level. Between 2004 and 2011, occupied population with more than 11 years of schooling went from 33.6% to 46.4%, respectively.

20

26

32

38

44

50

2011200920082007200620052004200320022001

28.8 30.7 32.5 33.6 35.2 37.4 39.0 41.2 43.2 46.4

Ministry of Finance

December Edition | Year 2012

51

Employm

ent and Income

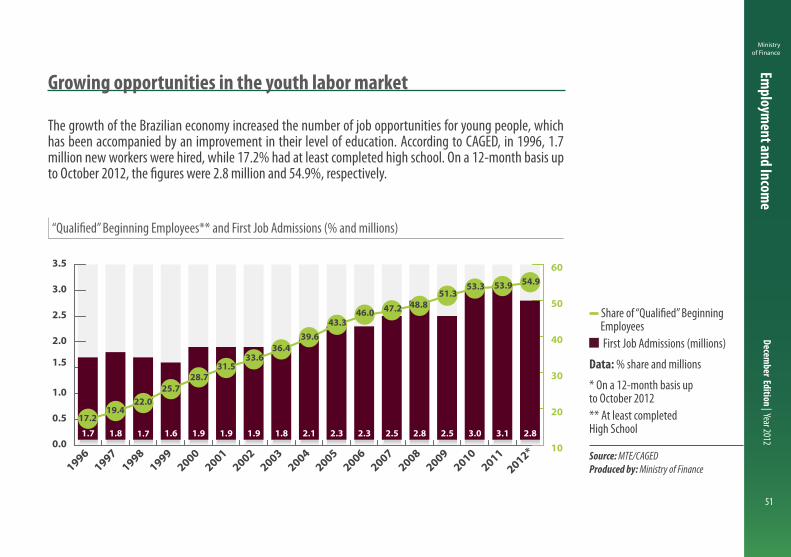

“Qualified” Beginning Employees** and First Job Admissions (% and millions)

Share of “Qualified” Beginning Employees First Job Admissions (millions)

Data: % share and millions

* On a 12-month basis up to October 2012 ** At least completed High School

Source: MTE/CAGEDProduced by: Ministry of Finance

Growing opportunities in the youth labor market

The growth of the Brazilian economy increased the number of job opportunities for young people, which has been accompanied by an improvement in their level of education. According to CAGED, in 1996, 1.7 million new workers were hired, while 17.2% had at least completed high school. On a 12-month basis up to October 2012, the figures were 2.8 million and 54.9%, respectively.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

10

20

30

40

50

60

2012*2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

First Job Admissions Share of "Quali�ed" Beginning Employees*

2.83.13.02.52.82.52.32.32.11.81.91.91.91.61.81.7 1.7

54.953.953.351.3

48.847.246.043.3

39.636.4

33.631.5

28.725.7

22.019.4

17.2

Brazilian Economy

OUTLOOK

Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Inflation

Ministry of Finance

December Edition | Year 2012

54

Inflation

Consumer price inflation rates increased in the third quarter of 2012, driven mainly by the impact of extreme weather conditions on agricultural production. The combination of higher than usual pressures in some fresh food prices in the Brazilian domestic market, and in important agricultural commodities in the international market, due to the drought in the US, caused an acceleration of inflation in mid-2012, which peaked in October.

Since then, inflation pressures have begun to ease, as producer prices related to important items such as soybeans, corn and wheat are clearly pointing to a retreat to lower levels. As well as that, several fresh food items are showing monthly deflation rates. This scenario shows that more relief should arrive in coming months, helping bring down consumer price inflation and also helping to drive the yearly IPCA to the center of the target set by the National Monetary Council.

Inflation rate under control

Ministry of Finance

December Edition | Year 2012

55

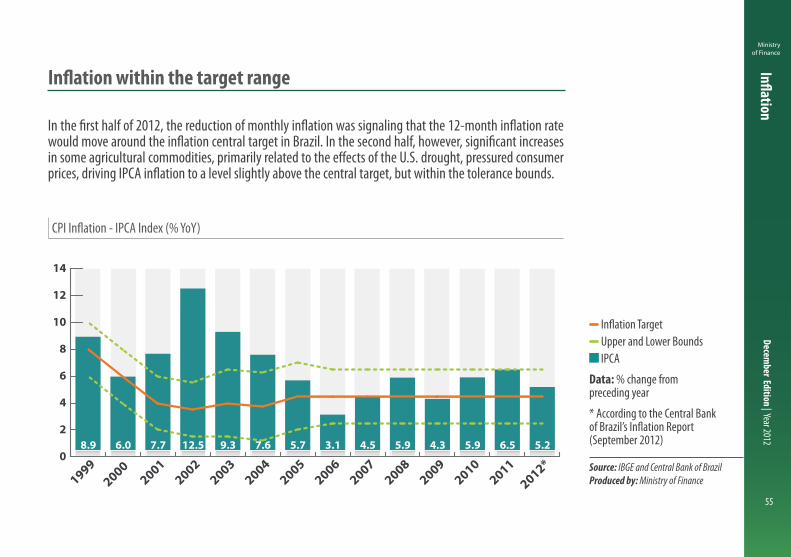

Inflation

CPI Inflation - IPCA Index (% YoY)

Inflation Target Upper and Lower Bounds IPCA

Data: % change from preceding year

* According to the Central Bank of Brazil’s Inflation Report (September 2012)

Source: IBGE and Central Bank of BrazilProduced by: Ministry of Finance

Inflation within the target range

In the first half of 2012, the reduction of monthly inflation was signaling that the 12-month inflation rate would move around the inflation central target in Brazil. In the second half, however, significant increases in some agricultural commodities, primarily related to the effects of the U.S. drought, pressured consumer prices, driving IPCA inflation to a level slightly above the central target, but within the tolerance bounds.

0

2

4

6

8

10

12

14

2012*2011

20102009

20082007

20062005

20042003

20022001

2000 1999

8.9 6.0 7.7 12.5 9.3 7.6 5.7 3.1 4.5 5.9 4.3 5.9 6.5 5.2

IPCA Target Center Upper and Lower Bounds

, ,

Ministry of Finance

December Edition | Year 2012

56

Inflation

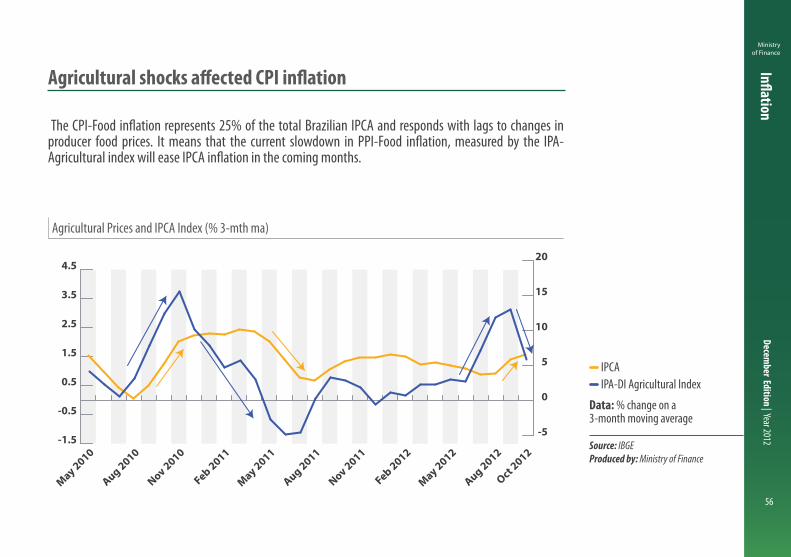

Agricultural Prices and IPCA Index (% 3-mth ma)

IPCA IPA-DI Agricultural Index

Data: % change on a 3-month moving average

Source: IBGEProduced by: Ministry of Finance

Agricultural shocks affected CPI inflation

The CPI-Food inflation represents 25% of the total Brazilian IPCA and responds with lags to changes in producer food prices. It means that the current slowdown in PPI-Food inflation, measured by the IPA-Agricultural index will ease IPCA inflation in the coming months.

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

Oct 2012

Aug 2012

May 2012

Feb 2012

Nov 2011

Aug 2011

May 2011

Feb 2011

Nov 2010

Aug 2010

May 2010

-5

0

5

10

15

20

IPCAIPA-DI Agricultural

IPCA, IPA-DI Agricultural

Ministry of Finance

December Edition | Year 2012

57

Inflation

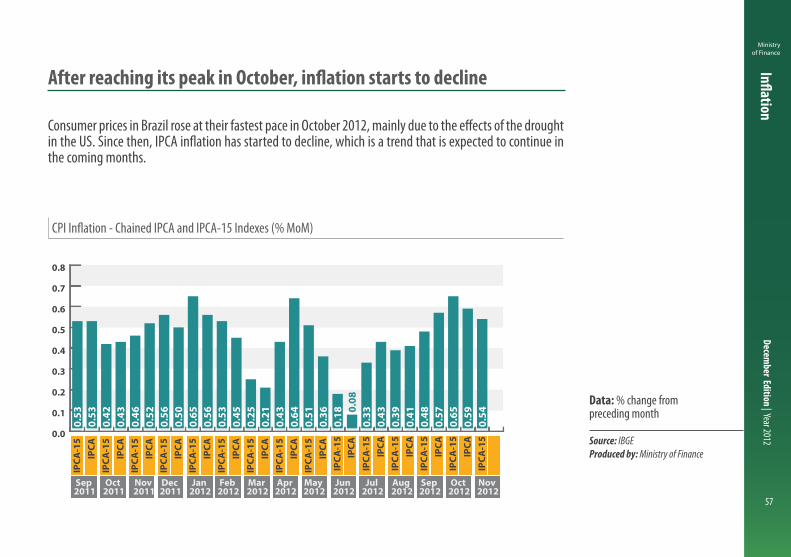

CPI Inflation - Chained IPCA and IPCA-15 Indexes (% MoM)

Data: % change from preceding month

Source: IBGEProduced by: Ministry of Finance

After reaching its peak in October, inflation starts to decline

Consumer prices in Brazil rose at their fastest pace in October 2012, mainly due to the effects of the drought in the US. Since then, IPCA inflation has started to decline, which is a trend that is expected to continue in the coming months.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

IPCA

-15

IPCA

IPCA

-15

IPCA

IPCA

-15

IPCA

IPCA

-15

IPCA

IPCA

-15

IPCA

IPCA

-15

IPCA

IP

CA-1

5 IP

CA

IPCA

-15

IPCA

IP

CA-1

5 IP

CA

IPCA

-15

IPCA

IP

CA-1

5 IP

CA

IPCA

-15

IPCA

IP

CA-1

5 IP

CA

IPCA

-15

IPCA

IP

CA-1

5

Nov 2012

Oct 2012

Sep 2012

Aug 2012

Jul 2012

Jun 2012

May 2012

Apr 2012

Mar 2012

Feb 2012

Jan 2012

Dec 2011

Nov 2011

Oct 2011

Sep 2011

0.53

0.53

0.42

0.43

0.46

0.52

0.56

0.50

0.65

0.56

0.53

0.45

0.25

0.21

0.43

0.64

0.51

0.36

0.18 0.

080.

330.

430.

390.

410.

480.

570.

650.

590.

54

Ministry of Finance

December Edition | Year 2012

58

Inflation

Inflation: IGP-M and Main Components (% YoY)

IGP-M IPA-M INCC-M IPC-M

Data: % change from preceding year on a 12-month basis

Source: FGVProduced by: Ministry of Finance

General Price Index already decelerating

After two consecutive quarters of acceleration, the 12-month General Price Index (IGP-M) inflation started a decreasing trend, reaching a percentage below 7.0% in November 2012. Lower producer prices (measured by the IPA index) in the past two months have played an important role in easing the pressure on the Brazilian IGP inflation.

-6

-3

0

3

6

9

12

15

Nov 2012

Sep 2012

Jul 2

012

May 2012

Mar 2012

Jan 2012

Nov 2011

Sep 2011

Jul 2

011

May 2011

Mar 2011

Jan 2011

Nov 2010

Sep 2010

Jul 2

010

May 2010

Mar 2010

Jan 2010

Nov 2009

7.33

6.967.30

5.77

INCC-MIPC-MIPA-MIGP-M

Ministry of Finance

December Edition | Year 2012

59

Inflation

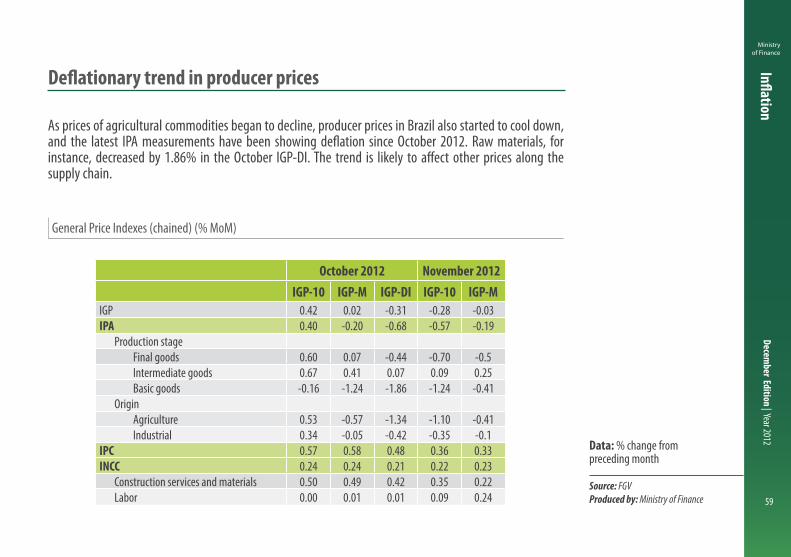

General Price Indexes (chained) (% MoM)

Data: % change from preceding month

Source: FGVProduced by: Ministry of Finance

Deflationary trend in producer prices

As prices of agricultural commodities began to decline, producer prices in Brazil also started to cool down, and the latest IPA measurements have been showing deflation since October 2012. Raw materials, for instance, decreased by 1.86% in the October IGP-DI. The trend is likely to affect other prices along the supply chain.

October 2012 November 2012IGP-10 IGP-M IGP-DI IGP-10 IGP-M

IGP 0.42 0.02 -0.31 -0.28 -0.03IPA 0.40 -0.20 -0.68 -0.57 -0.19

Production stageFinal goods 0.60 0.07 -0.44 -0.70 -0.5Intermediate goods 0.67 0.41 0.07 0.09 0.25Basic goods -0.16 -1.24 -1.86 -1.24 -0.41

OriginAgriculture 0.53 -0.57 -1.34 -1.10 -0.41Industrial 0.34 -0.05 -0.42 -0.35 -0.1

IPC 0.57 0.58 0.48 0.36 0.33INCC 0.24 0.24 0.21 0.22 0.23

Construction services and materials 0.50 0.49 0.42 0.35 0.22Labor 0.00 0.01 0.01 0.09 0.24

Brazilian Economy

OUTLOOK

Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Interest Rates and Credit

Ministry of Finance

December Edition | Year 2012

62

Interest Rates and Credit

From August 2011 up to October 2012, the Central Bank of Brazil lowered the policy rate by 525 basis-points, bringing both nominal and real rates to their lowest levels in the recent Brazilian monetary history. In fact, spreads and lending rates in the financial system have also fallen to record lows, although still at high levels.

Brazil is now even more focused on encouraging the development of the capital and long-term private credit markets. The country’s financial system is sound, operating in accordance with Basel principles, and it is actively participating in the development of important financial instruments, such as financial bills, FDICs, debentures, and other long-term corporate bonds.

As a matter of fact, this new environment of lower interest rates and investment opportunities has already begun to influence the decision-making process of economic agents. It will positively impact investment and production even further, as investors leave behind the time when the Brazilian economy was used to high short-term interest rate.

Interest rate at its lowest level ever

Ministry of Finance

December Edition | Year 2012

63

Interest Rates and Credit

Brazil: Real Ex-Ante Interest Rates* (% pa)

Data: % per annum

* 360-day swap deflated by inflation expectations for the 12 months ahead; 2012: November 30; 2001-2011: December 31

Source: Central Bank of BrazilProduced by: Ministry of Finance

Real interest rate at its lowest level due to sound macroeconomic fundamentals

Short-term real interest rates in Brazil have been showing a significant decrease for the past ten years, from 14.0% in December 2002 to 1.8% in November 2012. For the last 10 years, it has been a result of credible and sound monetary and fiscal policy coordination.

0

4

8

12

16

2012**2011201020092008200720062005200420032002

Average2002-2005 = 11.5

Average2006-2010 = 6.9

Average2011-2012 = 3.2

14.0 9.4 11.2 11.4 7.9 7.7 6.9 5.8 6.2 4.5 1.8

Ministry of Finance

December Edition | Year 2012

64

Interest Rates and Credit

Real and Nominal Interest Rates* (% pa)

SELIC interest rate target Real ex-ante interest rate*

Data: % per annum

* 360-day swap deflated by inflation expectations for the 12 months ahead

Source: Central Bank of BrazilProduced by: Ministry of Finance

Selic benchmark interest rate at its lowest level ever

Central Bank of Brazil has reduced its benchmark interest rate (Selic) since August 2011. The latest reduction in October 2012, from 7.50% to 7.25%, implied the lowest rate ever. The real interest rate reached 1.80% on November 30, 2012.

1.80

7.25

0

5

10

15

20

25

30

Real Ex-Ante Interest Rates Selic benchmark

Nov 2012

Oct 2012

Apr 2012

Oct 2011

Apr 2011

Oct 2010

Apr 2010

Oct 2009

Apr 2009

Oct 2008

Apr 2008

Oct 2007

Apr 2007

Oct 2006

Apr 2006

Oct 2005

Apr 2005

Oct 2004

Apr 2004

Nov 2003

Ministry of Finance

December Edition | Year 2012

65

Interest Rates and Credit

Interest Rates: DI Contracts* (% pa)

Jan 2013 Jan 2014 Jan 2015

Data: % per annum

* DI: one-day interbank deposits

Source: Central Bank of BrazilProduced by: Ministry of Finance

Long-term interest rates declining in Brazil

After a widespread decline throughout the last 12 months, the long-term rates traded in the futures DI stabilized at a level close to the current Selic rate. The difference between the curves expresses the risk associated with the exposure duration.

7.2 7.8

7.1 7

8

9

10

11

12

13

Nov 2012

Oct 2012

Jul 2

012

Apr 2012

Jan 2012

Oct 2011

Jul 2

011

Apr 2011

Jan 2011

Oct 2010

Jul 2

010

Apr 2010

Jan 2010

Jan 2015Jan 2013 Jan 2014

Ministry of Finance

December Edition | Year 2012

66

Interest Rates and Credit

Interest Rates and Average Maturity (% pa and days)

Average maturity (days) Interest rates (% YoY)

Data: % per annum and number of days

Source: Central Bank of BrazilProduced by: Ministry of Finance

Lower Selic rate and banking spreads benefit borrowers

Lower interest rates and banking spreads have been benefitting final borrowers. Interest rates on loans to individuals reached 35.4 percent, whereas rates on loans to corporations reached 22.1 percent. These percentages are well below the 2011 average and show sharp decline throughout 2012, with reductions of 9.7 p.p. and 6.6 p.p. for individuals and corporations, respectively. In the opposite direction, average maturity signaled slight increase in the period.

300

350

400

450

500

550

600

650

40

45

50

55

60

Oct 2012

Jun 2012

Dec 2011

Jun 2011

Dec 2010

Jun 2010

Dec 2009

Jun 2009

Dec 2008

May 2008200

250

300

350

400

450

Average Maturity

20

24

26

28

30

32

34

Interest Rates

Oct 2012

Jun 2012

Dec 2011

Jun 2011

Dec 2010

Jun 2010

Dec 2009

Jun 2009

Dec 2008

May 2008

Individuals Corporations

620.5

35.4

431.8

22.1

Average MaturityInterest Rates

Ministry of Finance

December Edition | Year 2012

67

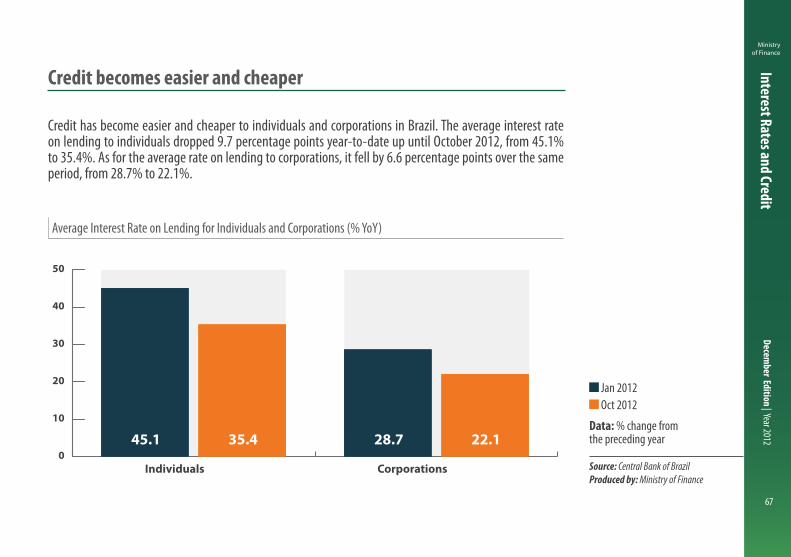

Interest Rates and Credit

Average Interest Rate on Lending for Individuals and Corporations (% YoY)

Jan 2012 Oct 2012

Data: % change from the preceding year

Source: Central Bank of BrazilProduced by: Ministry of Finance

Credit becomes easier and cheaper

Credit has become easier and cheaper to individuals and corporations in Brazil. The average interest rate on lending to individuals dropped 9.7 percentage points year-to-date up until October 2012, from 45.1% to 35.4%. As for the average rate on lending to corporations, it fell by 6.6 percentage points over the same period, from 28.7% to 22.1%.

0

10

20

30

40

50

CorporationsIndividualsOct 2012 Jan 2012

35.4 22.145.1 28.7

Ministry of Finance

December Edition | Year 2012

68

Interest Rates and Credit

Banking Spread to Individuals and Corporations (pp)

Jan 2012 Oct 2012

Data: percentage point

* Spread = Lending Rate - Funding Rate

Source: Central Bank of BrazilProduced by: Ministry of Finance

Lower banking spread to individuals and corporations

Although still high in comparison with other economies, spreads on loans to individuals and corporations have been declining in Brazil lately. The former went from 34.9 p.p. in January 2012 to 27.8 p.p. in October 2012, while the latter went from 18.5 p.p. to 15.0 p.p. in the same period.

0

5

10

15

20

25

30

35

40

45

50

CorporationsIndividualsOct 2012 Jan 2012

27.8 15.034.9 18.5

Ministry of Finance

December Edition | Year 2012

69

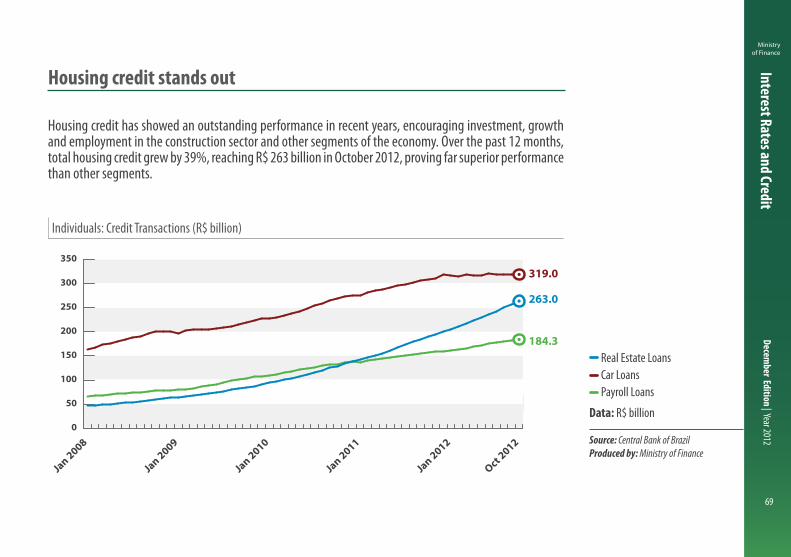

Interest Rates and Credit

Individuals: Credit Transactions (R$ billion)

Real Estate Loans Car Loans Payroll Loans

Data: R$ billion

Source: Central Bank of BrazilProduced by: Ministry of Finance

Housing credit stands out

Housing credit has showed an outstanding performance in recent years, encouraging investment, growth and employment in the construction sector and other segments of the economy. Over the past 12 months, total housing credit grew by 39%, reaching R$ 263 billion in October 2012, proving far superior performance than other segments.

0

50

100

150

200

250

300

350

Payroll Loans Car LoansReal Estate Loans

Oct 2012

Jan 2012

Jan 2011

Jan 2010

Jan 2009

Jan 2008

263.0

319.0

184.3

Ministry of Finance

December Edition | Year 2012

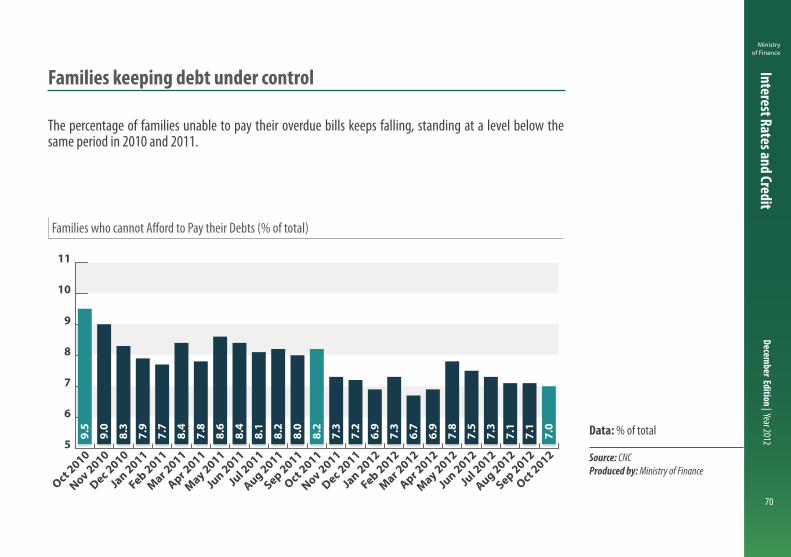

70

Interest Rates and Credit

Families who cannot Afford to Pay their Debts (% of total)

Data: % of total

Source: CNCProduced by: Ministry of Finance

Families keeping debt under control

The percentage of families unable to pay their overdue bills keeps falling, standing at a level below the same period in 2010 and 2011.

5

6

7

8

9

10

11

Oct 2012

Sep 2012

Aug 2012

Jul 2

012

Jun 2012

May 2012

Apr 2012

Mar 2012

Feb 2012

Jan 2012

Dec 2011

Nov 2011

Oct 2011

Sep 2011

Aug 2011

Jul 2

011

Jun 2011

May 2011

Apr 2011

Mar 2011

Feb 2011

Jan 2011

Dec 2010

Nov 2010

Oct 2010

9.5

9.0

8.3

7.9

7.7

8.4

7.8

8.6

8.4

8.1

8.2

8.0

8.2

7.3

7.2

6.9

7.3

6.7

6.9

7.8

7.5

7.3

7.1

7.1

7.0

Ministry of Finance

December Edition | Year 2012

71

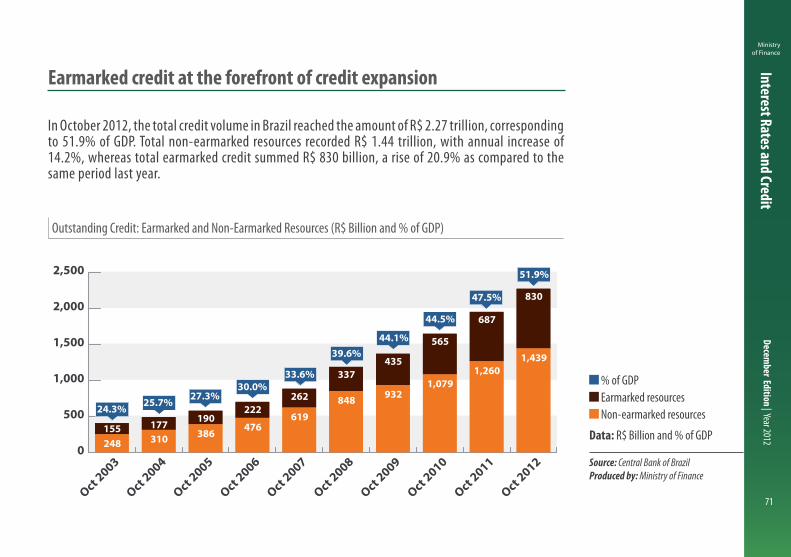

Interest Rates and Credit

Outstanding Credit: Earmarked and Non-Earmarked Resources (R$ Billion and % of GDP)

% of GDP Earmarked resources Non-earmarked resources

Data: R$ Billion and % of GDP

Source: Central Bank of BrazilProduced by: Ministry of Finance

Earmarked credit at the forefront of credit expansion

In October 2012, the total credit volume in Brazil reached the amount of R$ 2.27 trillion, corresponding to 51.9% of GDP. Total non-earmarked resources recorded R$ 1.44 trillion, with annual increase of 14.2%, whereas total earmarked credit summed R$ 830 billion, a rise of 20.9% as compared to the same period last year.

0

500

1,000

1,500

2,000

2,500

Oct 2012

Oct 2011

Oct 2010

Oct 2009

Oct 2008

Oct 2007

Oct 2006

Oct 2005

Oct 2004

Oct 2003

44.1%

44.5%

47.5%

51.9%

39.6%

33.6%30.0%

27.3%25.7%24.3%

155 177 190222

262

337435

565

687

830

248 310 386 476619

848 9321,079

1,2601,439

Earmarked Non-Earmarked % of GDP

Ministry of Finance

December Edition | Year 2012

72

Interest Rates and Credit

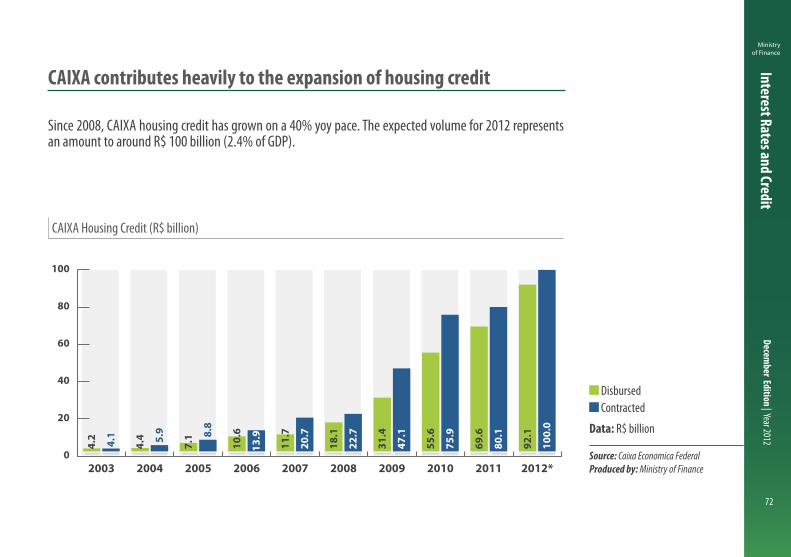

CAIXA Housing Credit (R$ billion)

Disbursed Contracted

Data: R$ billion

Source: Caixa Economica FederalProduced by: Ministry of Finance

CAIXA contributes heavily to the expansion of housing credit

Since 2008, CAIXA housing credit has grown on a 40% yoy pace. The expected volume for 2012 represents an amount to around R$ 100 billion (2.4% of GDP).

0

20

40

60

80

100

2012*201120102009200820072006200520042003

Contracted Disbursed

4.1 5.9 8.

8

13.9

20.7

22.7

47.1

75.9

80.1

100.

0

4.2

4.4

7.1

10.6

11.7

18.1

31.4

55.6

69.6

92.1

Ministry of Finance

December Edition | Year 2012

73

Interest Rates and Credit

Credit Operations in Brazil (% of GDP)

Earmarked resources* Non-Earmarked Resources

Data: % of GDP

* YTD October 2012

Source: Central Bank of BrazilProduced by: Ministry of Finance

Sustained rates of credit growth in Brazil

Credit operations as a share of GDP have been growing in a sustained pace in Brazil. In October 2012, lending with non-earmarked funds represented 32.9% of GDP, while earmarked credit stood at 19.0% of GDP. Mortgage has expanded at a rate of approximately 40% per annum, and now represents 6.0% of GDP.

0

10

20

30

40

50

60

Non-Earmarked Resource/GDP

2012*2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001 19.013.012.211.59.88.78.48.28.08.28.27.2

32.9

31.529.629.528.724.821.018.816.415.016.317.0

Earmarked Resource/GDP

Ministry of Finance

December Edition | Year 2012

74

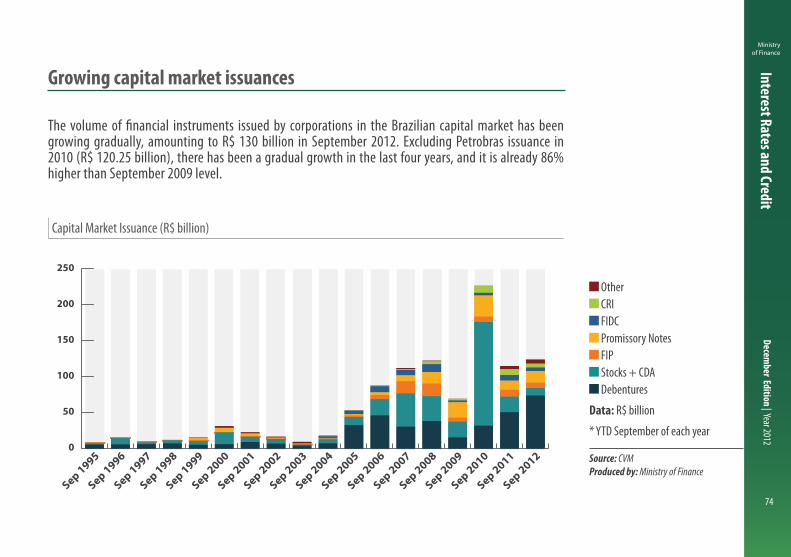

Interest Rates and Credit

Capital Market Issuance (R$ billion)

Other CRI FIDC Promissory Notes FIP Stocks + CDA Debentures

Data: R$ billion

* YTD September of each year

Source: CVMProduced by: Ministry of Finance

Growing capital market issuances

The volume of financial instruments issued by corporations in the Brazilian capital market has been growing gradually, amounting to R$ 130 billion in September 2012. Excluding Petrobras issuance in 2010 (R$ 120.25 billion), there has been a gradual growth in the last four years, and it is already 86% higher than September 2009 level.

0

50

100

150

200

250

0.4

1.91.1

0.2

0.5

4.85.7

0.8

0.93.7

2.5

9.2

7.95.4

8.6

7.511.1

2.3

3.8

7.84.7

3.7

8.2 16.0

21.6

29.4

12.716.3

5.7

16.8 17.6

7.3

9.67.6

22.746.4 34.4 21.6

10.4

FIDCOthersCerti�cate of Real Estate Receivables Promissory Notes FIP Common Stock Debentures

Sep 2012

Sep 2011

Sep 2010

Sep 2009

Sep 2008

Sep 2007

Sep 2006

Sep 2005

Sep 2004

Sep 2003

Sep 2002

Sep 2001

Sep 2000

Sep 1999

Sep 1998

Sep 1997

Sep 1996

Sep 1995

Ministry of Finance

December Edition | Year 2012

75

Interest Rates and Credit

Real Estate Investment - Public Offers - FIDC, CRI and FII (R$ billion*)

FIDC CRI FII

Data: R$ billion

* Current values

Source: CVMProduced by: Ministry of Finance

Significant increase in Real Estate Credit

0

5

10

15

20

25

30

3.8

7.8

4.7

4.1

13.1

7.1

FIDC

0.2 0.2 0.2 0.2 0.6 0.8 0.9 3.7 2.5 5.47.99.20.1 0.3

0.70.2

0.40.6 1.0

4.1 13.17.1

Sep 2012

Sep 2011

Sep 2010

Sep 2009

Sep 2008

Sep 2007

Sep 2006

Sep 2005

Sep 2004

Sep 2003

Sep 2002

Sep 2001

Sep 2000

FII CRI

0.3 0.31.0

2.65.0

8.67.5

11.1

2.3

3.8

7.8

4.7

Ministry of Finance

December Edition | Year 2012

76

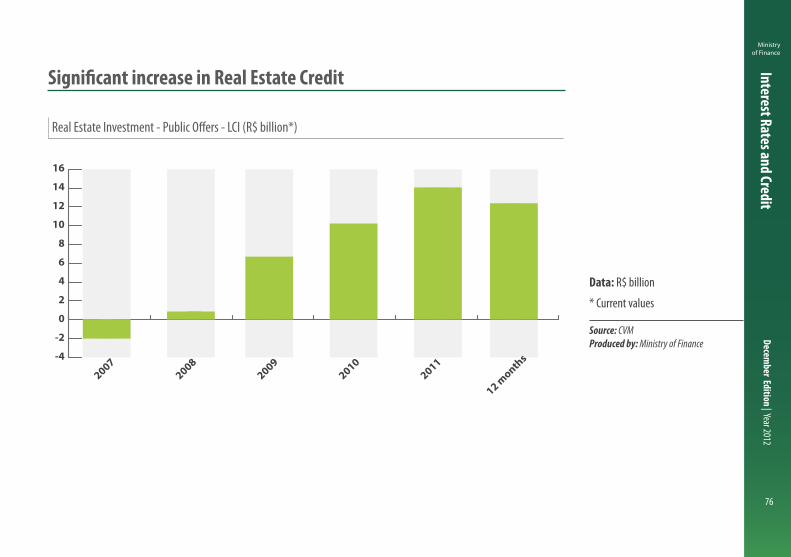

Interest Rates and Credit

Real Estate Investment - Public Offers - LCI (R$ billion*)

Data: R$ billion

* Current values

Source: CVMProduced by: Ministry of Finance

Significant increase in Real Estate Credit

-4

-2

0

2

4

6

8

10

12

14

16

12 month

s

20112010

20092008

2007

Ministry of Finance

December Edition | Year 2012

77

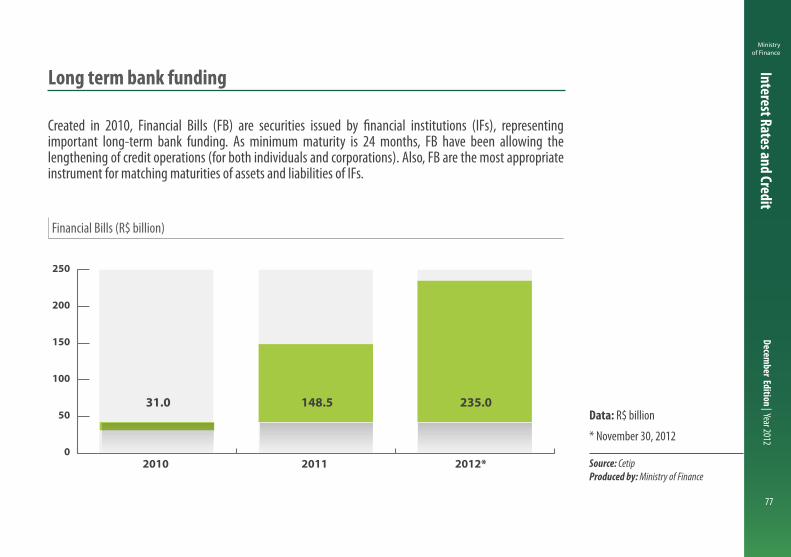

Interest Rates and Credit

Financial Bills (R$ billion)

Data: R$ billion

* November 30, 2012

Source: CetipProduced by: Ministry of Finance

Long term bank funding

Created in 2010, Financial Bills (FB) are securities issued by financial institutions (IFs), representing important long-term bank funding. As minimum maturity is 24 months, FB have been allowing the lengthening of credit operations (for both individuals and corporations). Also, FB are the most appropriate instrument for matching maturities of assets and liabilities of IFs.

0

50

100

150

200

250

2012*20112010

31.0 148.5 235.0

Ministry of Finance

December Edition | Year 2012

78

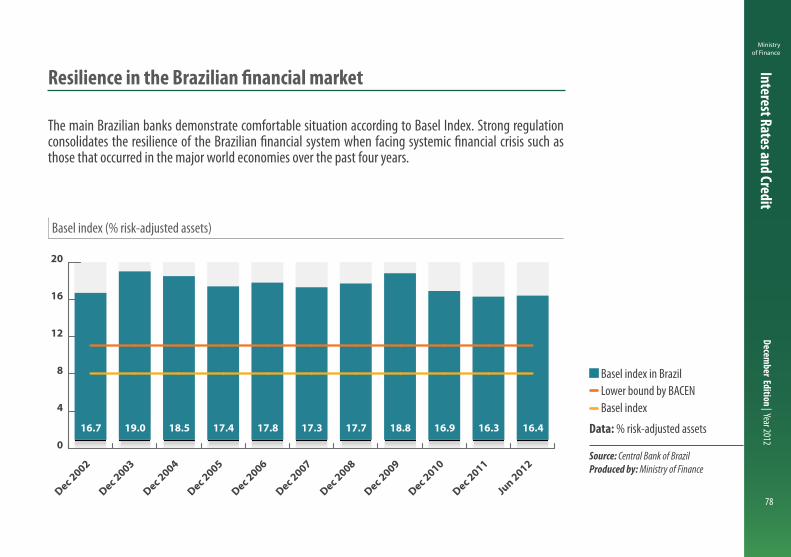

Interest Rates and Credit

Basel index (% risk-adjusted assets)

Basel index in Brazil Lower bound by BACEN Basel index

Data: % risk-adjusted assets

Source: Central Bank of BrazilProduced by: Ministry of Finance

Resilience in the Brazilian financial market

The main Brazilian banks demonstrate comfortable situation according to Basel Index. Strong regulation consolidates the resilience of the Brazilian financial system when facing systemic financial crisis such as those that occurred in the major world economies over the past four years.

0

4

8

12

16

20

Jun 2012

Dec 2011

Dec 2010

Dec 2009

Dec 2008

Dec 2007

Dec 2006

Dec 2005

Dec 2004

Dec 2003

Dec 2002

16.7 19.0 18.5 17.4 17.8 17.3 17.7 18.8 16.9 16.3 16.4

Basel index in Brazil Lower bound by BACEN Basel Index

Ministry of Finance

December Edition | Year 2012

79

Interest Rates and Credit

Produced by: Ministry of Finance

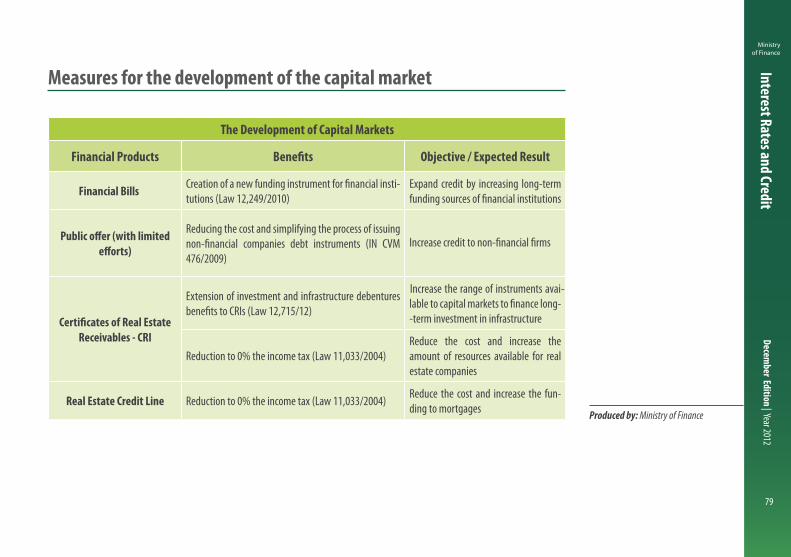

Measures for the development of the capital market

The Development of Capital Markets

Financial Products Objective / Expected Result

Financial Bills -tutions (Law 12,249/2010)

Expand credit by increasing long-term

Reducing the cost and simplifying the process of issuing

476/2009)Increase credit to non-�nancial �rms

Receivables - CRI

Extension of investment and infrastructure debentures Increase the range of instruments avai--

-term investment in infrastructure

Reduction to 0% the income tax (Law 11,033/2004)Reduce the cost and increase the amount of resources available for real estate companies

Real Estate Credit Line Reduction to 0% the income tax (Law 11,033/2004) Reduce the cost and increase the fun-ding to mortgages

Ministry of Finance

December Edition | Year 2012

80

Interest Rates and Credit

Produced by: Ministry of Finance

Measures for the development of the capital market

The Development of Capital Markets

Financial Products Objective / Expected Result

Investment DebenturesDecrease to 0 percent the rates of Financial Transaction Tax and Income Tax to foreign in-vestors (Law 12.431/11)

Encourage long-term Capital Markets as a way to broadenthe sources of funding for investments

Infrastructure Debentures

Decrease to 0 percent the rates of Financial Transaction Tax and Income Tax to foreign in-vestors, to 0 percent of income tax to individual domestic investors and decrease of 10 p.p. of

-panies (Law 12.431/11)

Develop long-term Capital Markets as a way to broaden the sources of funding for investments

Brazilian Economy

OUTLOOK

Ministry ofFinance

B R A Z I L I A N G O V E R N M E N T

Fiscal Policy

Ministry of Finance

December Edition | Year 2012

82

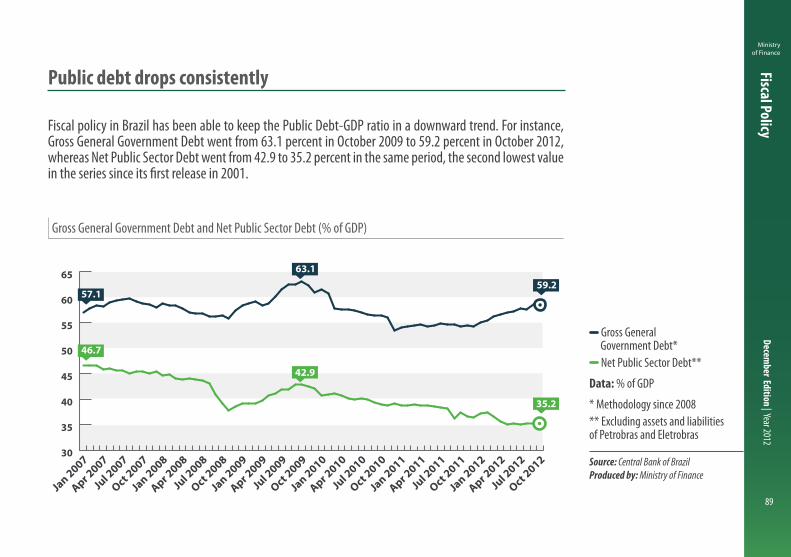

Fiscal PolicyIn 2012 Federal Government used fiscal policy instruments in order to avoid downturns on domestic economy due to the international crisis. The strategy also means to maintain fiscal fundamentals in a sound situation.

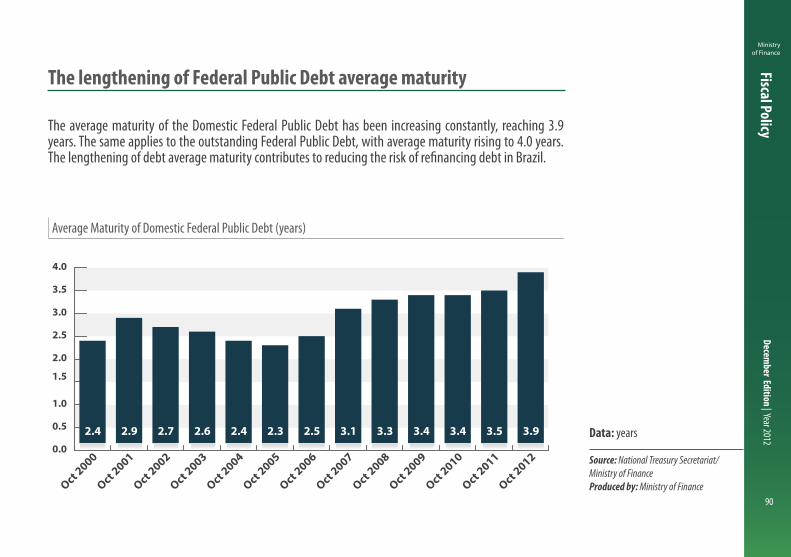

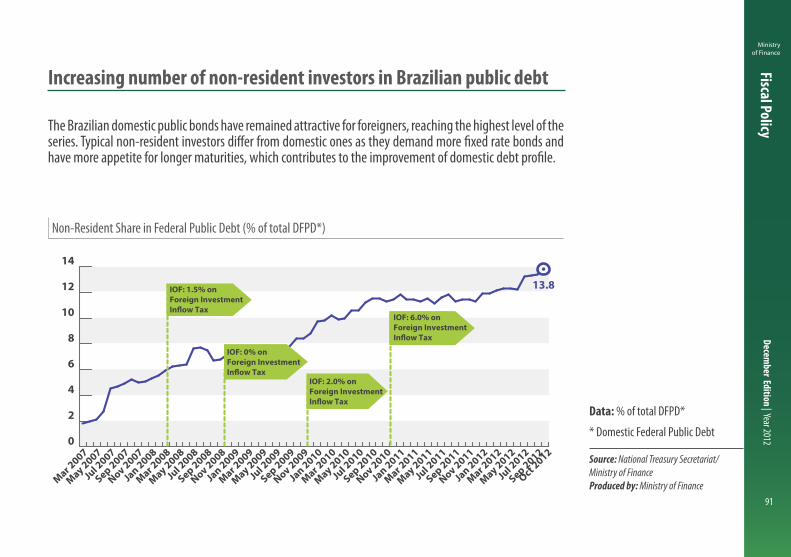

The strong fiscal results allows the Public Sector Net Debt at 35.2 percent of GDP close to the lowest series values. Also, the continuous improvement in Federal Public Debt profile, both in terms of composition and maturity, has been reflected on the declining rates of external issuances. The issuance of Global 2023 bond, in September, resulted on the lowest rate of all times for a Brazilian external public debt bond.

Moreover, consistent fiscal situation has still placed Brazil in a privileged position when compared to other G20 countries. It is expected the country should perform one of the greatest primary surpluses in the group, and one of the lowest nominal deficits.

Fiscal consolidation favors investment

Ministry of Finance

December Edition | Year 2012

83

Fiscal Policy

Public Sector Fiscal Result (% of GDP)

Public Sector Primary Result Central Government Primary Result Subnational Entities Primary Result (States and Municipalities) State-owned Companies Primary Result Public Sector Nominal Result

Data: % of GDP

* On a 12-month basis up to October 2012

Source: Central Bank of BrazilProduced by: Ministry of Finance

Economic growth with fiscal consolidation

The public sector continues to pursue the fiscal target in line with fiscal responsibility principles, one of the pillars of Brazilian economic policy. In fact, the fiscal and monetary policy coordination has sought to mitigate the effects of international crisis on domestic activity. Also, the projected targets will reduce even more both nominal deficit and public debt.

-6

-5

-4

-3

-2

-1

0

1

2

3

4

0.0

2.6

2.2

2012*2011201020092008200720062005200420032002

3.2 3.3

3.7 3.8

3.2 3.3 3.4

2.0

2.7

3.1

2.2

-4.4

-5.2

-2.9

-3.6 -3.6

-2.8

-2.0

-3.3

-2.5 -2.6 -2.7

3.2 3.33.7 3.8

3.2 3.3 3.4

2.02.7

3.1

2.2

-4.4-5.2

-2.9-3.6 -3.6

-2.8-2.0

-3.3-2.5 -2.6 -2.7

Nominal Result Primary Result State-owned Companies

State and Municipalities Central Government

0.1

0.00.

8

0.6

0.0

0.10.

6

0.5

1.3

2.1

2.20.1

0.2

-0.0

0.1

0.9

1.0

0.8

1.1

1.00.3

0.20.

7 0.8

2.2

2.3

2.7

2.6

2.2

2.2

2.40.2

1.6

Ministry of Finance

December Edition | Year 2012

84

Fiscal Policy

Primary and Nominal Results (% of GDP)

Primary Result Nominal Result

Data: % of GDP

* IMF forecasts - Fiscal Monitor October 2012. For Brazil, Focus Market Report - Central Bank of Brazil (November 30, 2012)

Source: Central Bank of Brazil and IMFProduced by: Ministry of Finance

Brazil stands out in the international fiscal scenario

Brazilian sound fiscal results stand out in comparison advanced and other emerging countries. For 2012, Brazil has one of the strongest levels of nominal and primary results, both as a share of GDP.

-10 -8 -6 -4 -2 0 2Japan

India

USA

UK

France

Canada

Italy

Mexico

Brazil

China

Germany

Russia

-10 -8 -6 -4 -2 0 2 4Japan

USA

UK

India

Canada

France

China

Mexico

Russia

Germany

BrazilItaly

Primary Fiscal Result (% of GDP) - 2012 Nominal Result (% of GDP) - 2012

-0.6

-2.2

-3.2

-5.2

-5.6

-6.5

-9.0

2.6

2.6

1.4

1.1

0.2

0.5

-0.4

-1.3

-2.3

-2.4

-2.7

-3.8

-4.7

-8.2

-8.7

-9.5

-10.0

Ministry of Finance

December Edition | Year 2012

85

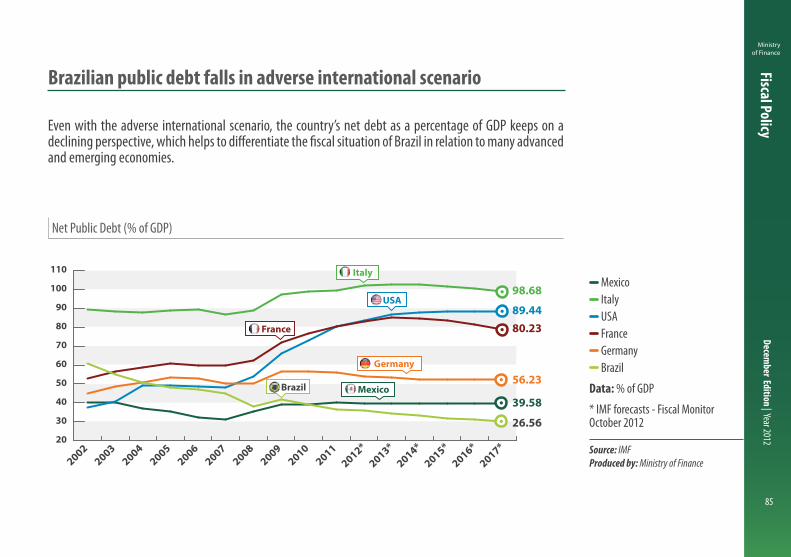

Fiscal Policy

Net Public Debt (% of GDP)

Mexico Italy USA France Germany Brazil

Data: % of GDP

* IMF forecasts - Fiscal Monitor October 2012

Source: IMFProduced by: Ministry of Finance

Brazilian public debt falls in adverse international scenario

Even with the adverse international scenario, the country’s net debt as a percentage of GDP keeps on a declining perspective, which helps to differentiate the fiscal situation of Brazil in relation to many advanced and emerging economies.

20

30

40

50

60

70

80

90

100

110

2017*

2016*

2015*

2014*

2013*

2012*2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

56.23

39.58

26.56

80.2389.44

98.68

Italy

France

Germany

MexicoBrazil

USA

Ministry of Finance

December Edition | Year 2012

86

Fiscal Policy

Central Government Primary Fiscal Result - Above the Line (% of GDP)Data: % of GDP

* On a 12-month basis up to October 2012 ** Including social security benefits, allowance and unemployment insurance, assistential benefits (LOAS and RMV) and “Bolsa Família” Program *** Including only investments classified as GND 4 **** Including the Sovereign Wealth Fund constitution (2008) and the capitalization operation of Petrobras (2010)

Source: National Treasury Secretariat/Ministry of Finance/SenateProduced by: Ministry of Finance

Brazil is improving its public expenditure profile

The Central Government fiscal results have gone through significant changes since 2002, due to the positive impact of job formalization on the economy, as well as the focus on reducing inequalities. The growth in net revenues has been directed to income transfers to households and to public investments.

% GDP 2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

*

Gross revenue 21.7 21.0 21.6 22.7 22.9 23.3 23.6 22.8 22.4 23.9 23.9Transfers to states and municipalities 3.8 3.5 3.5 3.9 3.9 4.0 4.4 3.9 3.7 4.2 4.1Net revenue 17.9 17.4 18.1 18.8 19.0 19.3 19.2 18.9 18.7 19.7 19.8Primary expenditure 15.7 15.1 15.6 16.4 17.0 17.1 16.4 17.7 17.4 17.5 18.2

- Payroll 4.8 4.5 4.3 4.3 4.5 4.4 4.3 4.7 4.4 4.3 4.2 - Income transfers to households** 6.8 7.2 7.6 8.1 8.4 8.5 8.1 8.7 8.5 8.6 9.1 - Investments*** 0.8 0.3 0.5 0.5 0.6 0.7 0.9 1.0 1.2 1.0 1.1

1.7 1.6 1.7 1.8 1.7 1.8 1.7 1.9 2.0 2.0 2.11.6 1.6 1.5 1.8 1.8 1.8 1.4 1.4 1.4 1.5 1.7

2.1 2.3 2.5 2.5 2.1 2.2 2.8 1.2 1.2 2.3 1.6

0.0 0.0 0.0 0.0 0.0 0.0 -0.5 0.0 0.8 0.0 0.0