Botswana Lesotho - iuj.ac.jp · COUNTRY REPORT Botswana Lesotho January 2001 The Economist...

40

COUNTRY REPORT Botswana Lesotho January 2001 The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom At a glance: 2001-02 OVERVIEW Opposition to the ruling Botswana Democratic Party (BDP) may strengthen in 2001 as the government enters its mid-term. Nonetheless, the domestic political scene will remain relatively stable over the forecast period. Regional instability will continue to cause concern. Prudent economic policies aimed at attracting foreign investment will remain to the fore. Limited mining growth will restrict real GDP, and poor performance in manufacturing and agriculture is expected to reduce overall growth from 6% in 2000/01 to 4.8% in 2001/02 and 5% in 2002/03. Average annual inflation will ease to 6.6% in 2001 and 5.2% in 2002. Higher non-mineral exports and a reduction in the import bill will increase the current-account surplus to US$225m (3.6% of GDP) in 2001 and US$308m (4.6% of GDP) in 2002. Key changes from last month Political outlook • The opposition Botswana National Front (BNF) has picked up defectors from other opposition parties. There may be a further slight improvement in the party’s position as the government comes under increasing criticism. However, the BNF will not pose a significant challenge to the BDP over the forecast period. Economic policy outlook • The public furore over Botswana’s generous foreign investment incentives may encourage the government to target more resources towards indigenous investors, although the foreign investment incentives are unlikely to be affected. Economic forecast • The risk of a sharp economic slowdown in the US has increased. This would hit demand for diamonds and might cause the EIU to downgrade its forecasts significantly.

Transcript of Botswana Lesotho - iuj.ac.jp · COUNTRY REPORT Botswana Lesotho January 2001 The Economist...

COUNTRY REPORT

Botswana

Lesotho

January 2001

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

At a glance: 2001-02OVERVIEWOpposition to the ruling Botswana Democratic Party (BDP) may strengthenin 2001 as the government enters its mid-term. Nonetheless, the domesticpolitical scene will remain relatively stable over the forecast period. Regionalinstability will continue to cause concern. Prudent economic policies aimedat attracting foreign investment will remain to the fore. Limited mininggrowth will restrict real GDP, and poor performance in manufacturing andagriculture is expected to reduce overall growth from 6% in 2000/01 to 4.8%in 2001/02 and 5% in 2002/03. Average annual inflation will ease to 6.6% in2001 and 5.2% in 2002. Higher non-mineral exports and a reduction in theimport bill will increase the current-account surplus to US$225m (3.6% ofGDP) in 2001 and US$308m (4.6% of GDP) in 2002.

Key changes from last monthPolitical outlook• The opposition Botswana National Front (BNF) has picked up defectors

from other opposition parties. There may be a further slight improvementin the party’s position as the government comes under increasingcriticism. However, the BNF will not pose a significant challenge to theBDP over the forecast period.

Economic policy outlook• The public furore over Botswana’s generous foreign investment incentives

may encourage the government to target more resources towardsindigenous investors, although the foreign investment incentives areunlikely to be affected.

Economic forecast• The risk of a sharp economic slowdown in the US has increased. This

would hit demand for diamonds and might cause the EIU to downgradeits forecasts significantly.

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising conferences and roundtables. The firm is a memberof The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at http://store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, onlinedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023New York: Dante Cantu Tel: (1.212) 554 0643 Fax: (1.212) 586 1181Hong Kong: Amy Ha Tel: (852) 2802 7288/2585 3888 Fax: (852) 2802 7720/7638

Copyright© 2001 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 1356-4021

Symbols in tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

1

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

Contents

3 Summary

Botswana

5 Political structure6 Economic structure6 Annual indicators7 Quarterly indicators8 Outlook for 2001-028 Political outlook9 Economic policy outlook

10 Economic forecast13 The political scene15 Economic policy17 The domestic economy18 Mining19 Agriculture19 Financial services21 Infrastructure22 Foreign trade and payments

Lesotho

24 Political structure25 Economic structure25 Annual indicators26 Quarterly indicators27 Outlook for 2001-0227 Political outlook28 Economic policy outlook28 Economic forecast30 The political scene34 Economic policy and the economy

List of tables

10 Botswana: international assumptions summary11 Botswana: forecast summary29 Lesotho: forecast summary34 Lesotho: progress in meeting targets of the IMF programme

2

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

List of figures

7 Botswana: foreign trade7 Botswana: foreign reserves

13 Botswana: gross domestic product13 Botswana: regional real exchange rates36 Lesotho: manufacturing output37 Lesotho: inflation

3

© The Economist Intelligence Unit Limited 2001 `EIU Country Report January 2001

Summary

January 2001

Botswana

Opposition to the ruling Botswana Democratic Party (BDP) may strengthenthrough 2001 owing to various sources of mid-term discontent, including apossible factional struggle within the party hierarchy. Nonetheless, thegovernment will not face a serious internal threat and the domestic politicalscene will remain relatively stable over the forecast period. Regional instabilitywill continue to cause concern. Prudent economic policies aimed at attractingforeign investment will remain to the fore. The government is unlikely tosucceed in controlling state expenditure. Limited mining growth will restrictreal GDP growth, and poor performance in manufacturing and agriculture isexpected to reduce it to 6% in 2000/01 and 4.8% in 2001/02. A pick-up inmanufacturing and services will lift real GDP growth to 5% in 2002/03.Average annual inflation will ease to 6.6% in 2001 and 5.2% in 2002, as theeffects of higher fuel prices and the fall in the pula against the US dollar in2000 drop out of the annual comparisons. Rising non-mineral exports and areduction in the import bill will increase the current-account surplus toUS$225m (3.6% of GDP) in 2001 and US$308m (4.6% of GDP) in 2002.

The government has faced domestic criticism over its handling of squatterevictions and student allowances. The Botswana National Front has beenpicking up support from other opposition parties. However, there has beenmore confusion over the future of the party’s leader. Botswana has joined acommittee to negotiate the use of the resources of the Orange River.

The VAT bill has had its second reading. Incentives for foreign investors havebeen placed under scrutiny after the assets of the Hyundai vehicle assemblyplant were sold and moved to South Africa. Plans have been announced for anew scheme to help small businesses.

Several manufacturers have left Botswana, although Waverley Blankets hasannounced that it plans to shift its operations to the country. Funding hasbeen approved for the development of a new diamond mine. Botswana hasbeen assured that the measures taken against conflict diamonds will not harmthe legal trade. A contract has been awarded to implement a national livestockidentification system. Four international banks have applied for licences tooperate in Botswana’s international financial services centre. New competitionhas been introduced into the banking sector.

The renegotiation of the SACU agreement has nearly been completed. The EUis likely to give aid to help offset any decline in customs revenues due to theEU-South Africa free-trade agreement.

Outlook for 2001-02

The political scene

Economic policy

The domestic economy

Foreign trade and payments

4

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Lesotho

Disagreement over voter registration technology and the electoral model maydelay the legislative election until after the deadline of May 26th 2001. Theruling Lesotho Congress for Democracy (LCD) remains likely to win theelection, whenever it is held, because of deep divisions within the oppositionparties. As long as the political situation does not degenerate into violence,foreign interest in Lesotho will be limited. The IMF is expected to allow thegovernment to access financial resources under the poverty reduction andgrowth facility (PRGF). Reducing the fiscal deficit will be a key policy objective.Privatisation is expected to continue. Until the election is out of the waybusiness confidence will be subdued, and real GDP growth of only 2% in 2001and 2.5% in 2002 is expected. Inflation will rise slightly in 2001, beforeslowing in 2002 as inflation in South Africa falls. The maloti will remainpegged to the South African rand at par. The deficit on the current account willremain over 20% of GDP during the forecast period.

The government and the Independent Political Authority (IPA) continue todisagree over the amount of seats that can be elected by proportionalrepresentation at the next election. Government objections to voteridentification technology prevented the voter registration process frombeginning in December. There have been bitter exchanges between thegovernment and the IPA. The Southern African Development Community hasdistanced itself from the stalled electoral process. All the main political partieshave been beset by factional infighting. The Lesotho Clothing and AlliedWorkers Union has announced that it plans to form a political party.

The government has satisfactorily completed a nine-month staff-monitoredIMF programme, however certain targets were missed over the course of theprogramme. A jump in textile production helped manufacturing productiongrow by over 19% year on year in the first half of 2000. A Taiwanese textilemanufacturer has announced a planned investment of over US$100m. Higherfuel prices pushed up annual inflation in October to 6.5%. A consortium haspurchased 70% of Lesotho Telecom from the government. Consultants havebeen appointed to establish the Lesotho Unit Trust.

Editors: Paul Gamble (editor); Pratibha Thaker (consulting editor)Editorial closing date: January 9th 2001

All queries: Tel: (44.20) 7830 1007 E-mail: [email protected] report: Full schedule on www.eiu.com/schedule

Outlook for 2001-02

The political scene

Economic policy and theeconomy

Botswana 5

© The Economist Intelligence Unit Limited 2001 `EIU Country Report January 2001

Botswana

Political structure

Republic of Botswana

Unitary republic

Roman-Dutch law; cases in rural areas are heard by customary courts

National Assembly consisting of 40 members elected by universal suffrage, the president,the attorney-general and four members appointed by the president. A 15-member Houseof Chiefs advises on tribal matters

October 1999 (legislative); next election due by October 2004 (legislative)

President, chosen by the National Assembly

The president, his appointed vice-president and cabinet

Botswana Democratic Party (BDP), the ruling party; Botswana Congress Party (BCP);Botswana National Front (BNF); Botswana Workers Front (BWF); Botswana People’s Party(BPP); United Action Party (UAP)

President Festus MogaeVice-president Ian Khama

Agriculture Johnnie SwartzCommerce & industry Tabeleo SeretseEducation George KgorobaFinance & development planning Baledzi GaolatheForeign affairs Mompati MerafheHealth Joy PhumaphiLabour & home affairs Thebe MoganiLocal government Margaret NashaLands & housing Jacob NkatePresidential affairs & public administration Thebe MoganiMineral resources, energy & water affairs Boometswe MokgothuWorks, transport & communications David Magang

Linah Mohohlo

Official name

Form of state

Legal system

National legislature

National elections

Head of state

National government

Main political parties

The government

Key ministers

Central bank governor

6 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

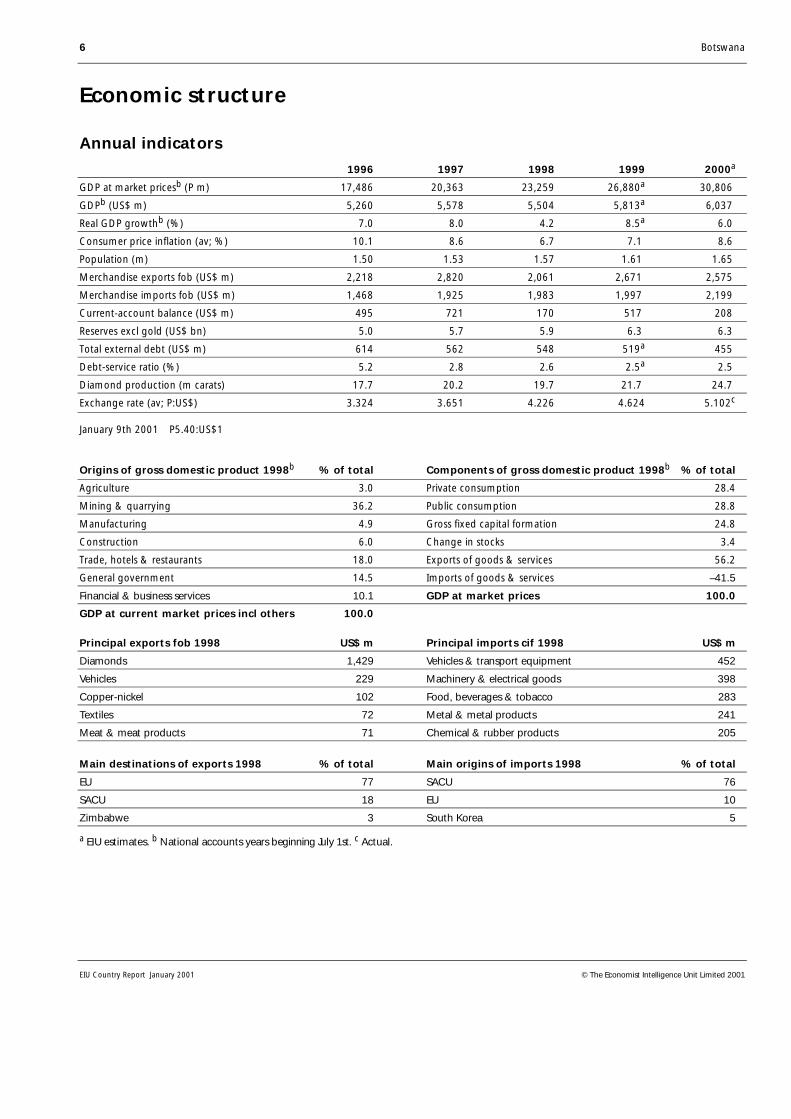

Economic structure

Annual indicators

1996 1997 1998 1999 2000a

GDP at market pricesb (P m) 17,486 20,363 23,259 26,880a 30,806

GDPb (US$ m) 5,260 5,578 5,504 5,813a 6,037

Real GDP growthb (%) 7.0 8.0 4.2 8.5a 6.0

Consumer price inflation (av; %) 10.1 8.6 6.7 7.1 8.6

Population (m) 1.50 1.53 1.57 1.61 1.65

Merchandise exports fob (US$ m) 2,218 2,820 2,061 2,671 2,575

Merchandise imports fob (US$ m) 1,468 1,925 1,983 1,997 2,199

Current-account balance (US$ m) 495 721 170 517 208

Reserves excl gold (US$ bn) 5.0 5.7 5.9 6.3 6.3

Total external debt (US$ m) 614 562 548 519a 455

Debt-service ratio (%) 5.2 2.8 2.6 2.5a 2.5

Diamond production (m carats) 17.7 20.2 19.7 21.7 24.7

Exchange rate (av; P:US$) 3.324 3.651 4.226 4.624 5.102c

January 9th 2001 P5.40:US$1

Origins of gross domestic product 1998b % of total Components of gross domestic product 1998b % of total

Agriculture 3.0 Private consumption 28.4

Mining & quarrying 36.2 Public consumption 28.8

Manufacturing 4.9 Gross fixed capital formation 24.8

Construction 6.0 Change in stocks 3.4

Trade, hotels & restaurants 18.0 Exports of goods & services 56.2

General government 14.5 Imports of goods & services –41.5

Financial & business services 10.1 GDP at market prices 100.0

GDP at current market prices incl others 100.0

Principal exports fob 1998 US$ m Principal imports cif 1998 US$ m

Diamonds 1,429 Vehicles & transport equipment 452

Vehicles 229 Machinery & electrical goods 398

Copper-nickel 102 Food, beverages & tobacco 283

Textiles 72 Metal & metal products 241

Meat & meat products 71 Chemical & rubber products 205

Main destinations of exports 1998 % of total Main origins of imports 1998 % of total

EU 77 SACU 76

SACU 18 EU 10

Zimbabwe 3 South Korea 5

a EIU estimates. b National accounts years beginning July 1st. c Actual.

Botswana 7

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

Quarterly indicators

1998 1999 20004 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr

Central government finance (P m)Revenue & grants 1,540.8 1,909.4 1,627.0 3,776.9 3,705.3 2,858.6 n/a n/aExpenditure & net lending 2,364.2 2,408.7 2,645.5 2,637.2 2,557.9 2,515.8 n/a n/aBalance –823.4 –499.3 –1,018.5 1,139.7 1,147.4 342.8 n/a n/a

PricesConsumer prices (1995=100) 130.2 133.0 136.2 137.8 139.6 142.5 146.1 151.8 % change, year on year 6.2 7.0 7.1 7.1 7.2 7.1 7.3 10.2

Financial indicatorsExchange rate P:US$ (av) 4.42 4.61 4.65 4.62 4.61 4.72 5.10 5.19 P:US$ (end-period) 4.46 4.67 4.63 4.53 4.63 4.85 5.12 5.27Interest rates (%) Bank (end-period) 12.50 132.5 13.25 13.25 13.25 13.75 13.75 13.75 Lending (av) 14.00 14.17 14.75 14.81 14.81 15.06 15.25 15.25M1 (end-period; P m) 1,513 1,646 1,783 1,842 1,775 1,680 1,784 1,838 % change, year on year 5.8 28.3 26.0 19.1 17.3 2.1 0.1 –0.2M2 (end-period; P m) 5,722 5,886 6,328 6,818 7,229 6,557 7,268 7,587 % change, year on year 39.4 30.6 24.4 20.1 26.3 11.4 14.9 11.3Stockmarket index (end-period; 1989=100) DCI 946.7 990.3 1035.5 1,417.1 1,399.3 1,470.8 1,434.7 1,475.1

Foreign trade and reservesExports fob (P m) 1,269 1,799 2,707 2,737 4,984 2,340 n/a n/a Diamonds (P m) 689 1,243 2,239 2,005 4,326 1,842 2,952 n/aImports cif (P m) –3,013 –2,541 –2,375 –2,574 –2,674 –2,636 n/a n/aTrade balance –1,744 –742 332 163 2,310 –296 n/a n/aReserves excl gold (end-period; US$ m) 6,025 5,742 5,802 5,769 6,299 6,177 6,175 6,133

Sources: IMF, International Financial Statistics; Bank of Botswana, Botswana Financial Statistics.

8 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Outlook for 2001-02

Political outlook

Opposition to the ruling Botswana Democratic Party (BDP) will probablystrengthen in 2001 as domestic discontent leads to a groundswell of supportfor the main opposition party, the Botswana National Front (BNF). Continuedhigh unemployment and a perception that foreign investors are taking jobsaway from locals are just some of the causes around which people will unite.The BDP’s situation will not be helped by the likelihood of continued internaldisunity. The party’s old guard, spearheaded by the former minister and partychairman, Pontashego Kedikilwe, will keep a check on the party’s leaders,especially the young vice-president, Ian Khama, who continues to display signsof political naivety. Although the BNF will try to make political capital out ofthe BDP’s weakness, its own leadership struggle will come to the fore in 2001.Kenneth Koma is expected to step down as leader of the party, and it seemsunlikely that the BNF will maintain its current political momentum into 2002,let alone until the next election in 2004.

The president, Festus Mogae, who remains on course for another term in office,is still trying to establish control over his party. A major difficulty will bepleasing the BDP’s old guard, while keeping Mr Khama in the fold. Mr Khama,a tribal chief and the eldest son of the country’s first president, Seretse Khama,commands a traditional following in the central region, which is seen as theheart of the BDP’s support base, and Mr Mogae would be unwilling to alienatethis core of support. Mr Khama will campaign against the complacency andlethargy which characterise the civil service, putting him at odds with many inthe cabinet. If he does not quickly achieve the results, and power, that hewants, he may yet quit formal politics. For the time being, however,Mr Mogae’s attempts to calm factional politics within his party may be working,especially as the party has been jerked from complacency by an unexpectedstrengthening of the BNF. This has taken the form of a local council by-electionvictory and defections from other opposition parties. It is unlikely to go muchfurther than this. The other small opposition parties will spend their timedebating internal matters and plotting against one another. Recent statementssuggest that opposition unity remains as elusive as ever.

Botswana’s main international concern will be regional instability. The mostserious threats are posed by the uncertain situation in Zimbabwe and thepossibility of destabilisation, mainly by the influx of refugees, by the Angolancivil war, which is increasingly spilling over into neighbouring Namibia.

Although the government remains wary of a diplomatic incident with theincreasingly erratic Zimbabwean leadership, it has admitted openly that it isconcerned about the situation there. While the direct economic impact of acollapse in Zimbabwe would be limited, tourism would suffer further and aninflux of refugees is possible. The impact on Botswana’s reputation is moresignificant, with negative implications for foreign investment and the pula.Botswana’s relations with Namibia remain calm, although tensions concerning

Domestic politicsDomestic politics

International relations

Botswana 9

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

their joint border may yet resurface. The issue of the extradition of Caprivisecessionists may cause some embarrassment, but so far Botswana has beenrelatively sympathetic to its neighbour’s needs. Botswana will continue topursue a higher profile internationally, not only through its mediation inregional conflicts, but also through the Southern African DevelopmentCommunity (SADC), which has its headquarters in Gaborone. One source ofdisharmony that may arise in this forum over the forecast period is thequestion of tax competition between countries.

Economic policy outlook

Prudent economic policies will characterise the forecast period, and the twinaims of economic diversification and balanced budgets will remain intact. Thelacklustre privatisation programme is set to move ahead, although someresistance can be expected, and the government will continue its investor-friendly policies. Attempts to combat the high unemployment rate and theimpact of AIDS will also be high on the policy agenda. Fiscal policy will remainfocused on improving expenditure control and increasing receipts, although itis likely to have only limited success. Monetary policy will remain tight inorder to control inflation.

The recent public furore over unscrupulous foreign investors who have takenadvantage of Botswana’s investment incentives may have an impact on thegovernment’s policies towards foreign investment. However, this will bemainly superficial in order to satisfy the domestic constituency, who wantmore help directed towards indigenous investors. No substantial change fromcurrent policies is expected. President Mogae has made it clear that foreigninvestment is both necessary and welcome. Furthermore, those at the top areonly too aware that the majority of fraud in the government assistanceschemes has in fact been carried out by locals (despite the high-profile case ofZimbabwe’s Billy Rautenbach and the Motor Company of Botswana).

There will be some slippage from the targets laid out in the budget for fiscalyear 2000/01 (April-March). Diamond earnings should achieve their target andthe hoped-for increase in customs union revenue is likely to be achieved, asthis comes from the largely predetermined Southern African Customs Union(SACU) pool. However, overspending on the Eighth National DevelopmentPlan will push up total spending significantly, as will the reconstruction workafter the floods in early 2000. It will, in any case, be very difficult for thegovernment to hit its target of 3% expenditure growth, after several years inwhich expenditure has risen by over 20% year on year. Nonetheless, someprogress is being made: preliminary data for the first quarter of 2000/01 showthat spending growth slowed to just under 15%.

Despite promises of revenue offsets to counter the overspending, there is littleprospect that the increase in charges for health and education that arecurrently being mooted will be implemented. The introduction of value-addedtax (VAT) to replace sales tax in 2001 is expected to have only a limited impacton revenue in the short term. Some pressure on the fiscal surplus is, therefore,

Fiscal policy

Policy trends

10 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

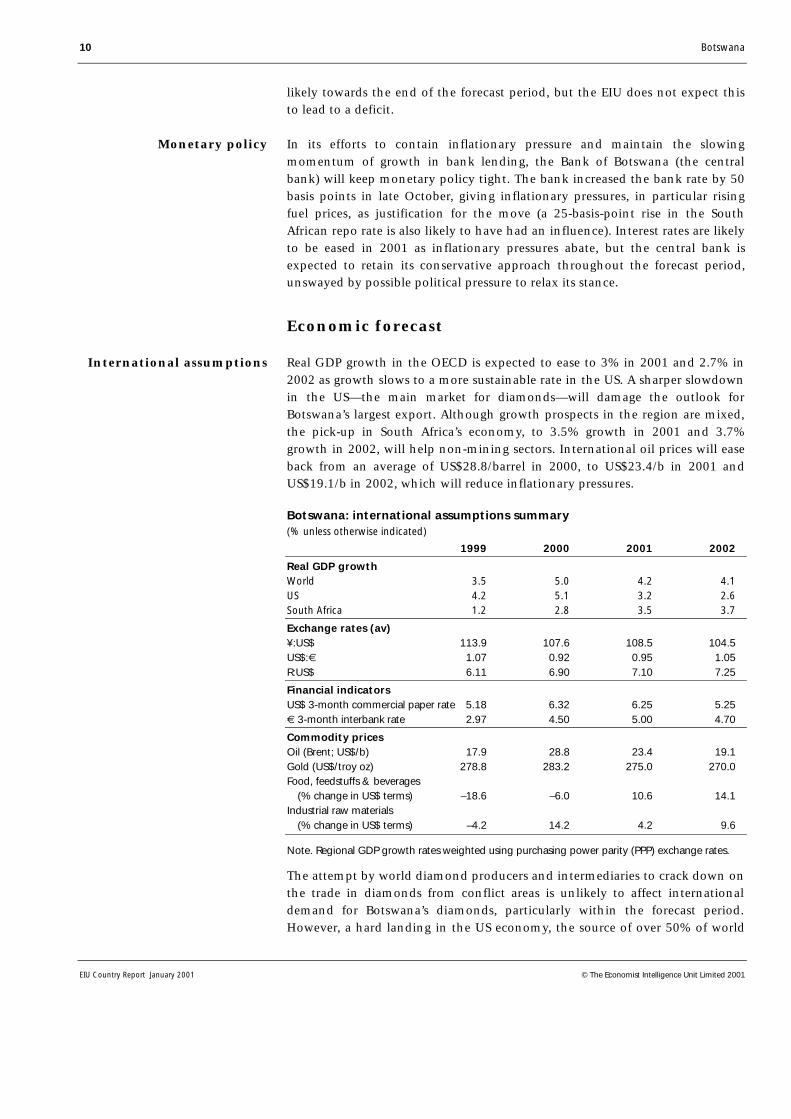

likely towards the end of the forecast period, but the EIU does not expect thisto lead to a deficit.

In its efforts to contain inflationary pressure and maintain the slowingmomentum of growth in bank lending, the Bank of Botswana (the centralbank) will keep monetary policy tight. The bank increased the bank rate by 50basis points in late October, giving inflationary pressures, in particular risingfuel prices, as justification for the move (a 25-basis-point rise in the SouthAfrican repo rate is also likely to have had an influence). Interest rates are likelyto be eased in 2001 as inflationary pressures abate, but the central bank isexpected to retain its conservative approach throughout the forecast period,unswayed by possible political pressure to relax its stance.

Economic forecast

Real GDP growth in the OECD is expected to ease to 3% in 2001 and 2.7% in2002 as growth slows to a more sustainable rate in the US. A sharper slowdownin the US—the main market for diamonds—will damage the outlook forBotswana’s largest export. Although growth prospects in the region are mixed,the pick-up in South Africa’s economy, to 3.5% growth in 2001 and 3.7%growth in 2002, will help non-mining sectors. International oil prices will easeback from an average of US$28.8/barrel in 2000, to US$23.4/b in 2001 andUS$19.1/b in 2002, which will reduce inflationary pressures.

Botswana: international assumptions summary(% unless otherwise indicated)

1999 2000 2001 2002

Real GDP growthWorld 3.5 5.0 4.2 4.1US 4.2 5.1 3.2 2.6South Africa 1.2 2.8 3.5 3.7

Exchange rates (av)¥:US$ 113.9 107.6 108.5 104.5US$:€ 1.07 0.92 0.95 1.05R:US$ 6.11 6.90 7.10 7.25

Financial indicatorsUS$ 3-month commercial paper rate 5.18 6.32 6.25 5.25€ 3-month interbank rate 2.97 4.50 5.00 4.70

Commodity pricesOil (Brent; US$/b) 17.9 28.8 23.4 19.1Gold (US$/troy oz) 278.8 283.2 275.0 270.0Food, feedstuffs & beverages

(% change in US$ terms) –18.6 –6.0 10.6 14.1

Industrial raw materials (% change in US$ terms) –4.2 14.2 4.2 9.6

Note. Regional GDP growth rates weighted using purchasing power parity (PPP) exchange rates.

The attempt by world diamond producers and intermediaries to crack down onthe trade in diamonds from conflict areas is unlikely to affect internationaldemand for Botswana’s diamonds, particularly within the forecast period.However, a hard landing in the US economy, the source of over 50% of world

Monetary policy

International assumptions

Botswana 11

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

diamond sales, is likely to hit Botswana’s diamond exports, although, in theabsence of a serious recession, Botswana’s current projections for annualdiamond sales remain broadly realistic. De Beers’s decision to introduce a moretransparent market for diamonds may, in the longer term, lead to more volatileprices and hence more volatile export and government revenue flows.

Botswana: forecast summary(% unless otherwise indicated)

1999a 2000b 2001c 2002c

Real GDP growth 8.5b 6.0 4.8 5.0

Industrial production growth 18.5b 6.2 3.4 3.7

Gross agricultural growth –1.0b –0.5 0.5 2.0

Consumer price inflation Average 7.1 8.6 6.6 5.2 Year-end 8.4 8.2 5.8 5.1

Short-term interbank rate 14.6 15.8 14.5 15.0

Government balance (% of GDP) 1.9b 1.1 1.5 1.1

Exports of goods fob (US$ bn) 2.7 2.6 2.5 2.5

Imports of goods fob (US$ bn) 2.0 2.2 2.1 2.1

Current-account balance (US$ m) 517 208 225 308 % of GDP 8.9 3.5 3.6 4.6

External debt (year-end; US$ m) 519b 455 438 817

Exchange rates P:US$ (av) 4.62 5.10 5.52 5.67 P:¥100 (av) 4.06 4.75 5.09 5.42 P:€ (year-end) 4.65 4.74 5.64 6.24 P:R (year-end) 0.75 0.77 0.78 0.76

a Actual. b EIU estimates. c EIU forecasts.

Limited mining growth and a dip in manufacturing will characterise theforecast period. Government expenditure will provide some impetus foreconomic expansion, even though spending increases are slowing.Construction activity seems set to plateau, although it may be stimulated if aplanned complex for financial services firms gets the go-ahead. Thegovernment’s continuing efforts to develop an international financial servicescentre (IFSC) should allow a modest growth in services. We expect overall realGDP growth to ease from 6% in 2000/01 (July-June) to 4.8% in 2001/02, beforeit picks up to 5% in 2002/03.

Real GDP growth will slow from the 8.5% estimated for 1999/2000 as theexpansion in diamond output nears it peak. The agricultural sector willcontract because of the continuing impact of the floods in February 2000.Manufacturing will also contract, owing to the closure of the Hyundai vehicleassembly plant. The effect of regional troubles on tourism will cause aslowdown in growth in the services sector. Mining will remain stable in2001/02, and agriculture should improve slightly, if only because of the lowbase this year. This also applies to manufacturing, especially if recentinvestments, such as the arrival of Waverley Blankets, South Africa’s largestblanket manufacturer, are followed through. The growth of governmentspending on construction projects will slow further, however. Further advances

Economic growth

12 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

in manufacturing are expected in 2002/03. At the same time constructionactivity associated with the IFSC should continue. Some recovery in tourismreceipts is likely in 2002/03, assuming that the regional political situation doesnot deteriorate further.

Inflationary pressures were raised in 2000 by higher international oil prices, aweakening of the pula against the US dollar and sharp increases in publichousing rents. However, these pressures should abate in 2001 as oil prices falland the US dollar slides. Botswana’s inflation will continue to be influenced bySouth Africa’s inflation (particularly the CPIX index, which strips out interestrate movements) because of its heavy dependence on imports from SouthAfrica. We expect annual average inflation to fall from 8.6% in 2000 to 6.6% in2001 and 5.2% in 2002 as South African inflation eases further.

Botswana’s exchange rate has been managed to follow the depreciation of theSouth African rand against the US dollar—maintaining the competitiveness ofnon-mining products in the region remains a priority for the authorities. Therand will continue to dominate the basket of currencies the authorities attemptto shadow. We expect an annual average exchange rate of P5.10:US$1 in 2000,falling to P5.52:US$1 in 2001 and P5.67:US$1 in 2002. Further bouts ofvolatility in the rand may rekindle debate within Botswana about the wisdomof the current exchange-rate policy, but nothing is expected to come of this.

Falling fuel prices and an increase in non-mineral exports will increase thetrade balance over the forecast period. The structural deficit on the servicesaccount will keep the balance of trade in invisibles in deficit. Overall, weexpect a current-account surplus of US$225m (3.6% of GDP) in 2001 andUS$308m (4.6% of GDP) in 2002.

A fall in fuel prices in 2001 will reduce the import bill, however this should beoffset by a reduction in diamond exports. The main risk to our forecast in 2001is that there may be a major contraction in US demand for diamonds—likely tobe caused by a sharp slowdown in the economy rather than the campaignagainst illegal diamonds. Following the relocation of the assets of theHyundai plant to South Africa, vehicle exports will be negligible, althoughthis will remove the need for the import of foreign auto components.Recent foreign investments will lead to an increase in exports from thetextiles sector. Non-mining exports will continue to grow in 2002, when afurther fall in fuel prices and a reduction in government spending willallow the trade balance to expand further.

The deficit on the invisibles account will improve slightly over the forecastperiod. This is despite a steady fall in receipts of current transfers, asexpatriate remittances fall because of the reduction in employment inSouth African mines. Lower fuel prices should allow transport costs to falland, with activity in the IFSC picking up in 2002, the deficit on the servicesaccount, although still large, will narrow. The reduction in diamondexports will cause a slight reduction in income debits (around 75% ofwhich are accounted for by Debswana transfers) and healthy returns on the

Inflation

Exchange ratesExchange rates

External sector

Botswana 13

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

stock of foreign-exchange reserves will result in a narrowing of the deficiton the income account.

The political scene

The ruling Botswana Democratic Party (BDP) is having a difficult time on thedomestic political scene, although it is of little consequence at this early stagein the electoral cycle (the next general election is not due for nearly four years)and there is no suggestion of looming political instability. Two incidentsillustrate the BDP’s recent troubles. First, the widespread criticism of thepresident, Festus Mogae, and the minister for lands, Jacob Nkate, over theremoval of squatters from land in Mgoditshane. The squatters were forciblyevicted, but complain that they have rights to the land, based largely on thefact that polling stations were erected for them during the 1999 generalelection. The president has found himself harangued in constituency meetingsand the BDP lost a council by-election in October to the opposition BotswanaNational Front (BNF) in Mgoditshane. The BDP has also been criticised bystudents, who protested against the low level of their living allowances (as wellas objecting to President Mogae’s suggestions that at least 300 of them wereHIV-positive, even though, based on national statistics, this is probably true).During the protest, the police, who denied being heavy handed, dispersed theunarmed students using tear gas and rubber bullets.

In addition to the squatter issue, Mr Nkate, has faced fresh corruptionallegations over the allocation of land to a friend, Eddie Norman, who is tryingto develop a shopping complex. Meanwhile, the vice-president, Ian Khama,continues to receive attention in the press for his political blunders. The latestincident concerns a promise reportedly made by the vice-president to hisparliamentary constituents (of whom he is also the traditional chief) that hewould find them jobs in Gaborone. Not only is he obviously unable to keepthis promise, but any such promise brings with it the whiff of corruption andnepotism as well as being contrary to the government’s attempts to stop rural-urban migration. As has been the case in the past, the media has not suggested

Criticism of the BDPincreases

14 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

that Mr Khama was planning to corruptly procure jobs for his constituents.Rather, the focus is on Mr Khama’s political ineptitude amidst ongoing concernthat he is not up to the job of vice-president.

Despite the setbacks to the BDP, most of Botswana’s opposition parties havecontinued their usual infighting. However, the position of the main oppositionparty, the BNF, has strengthened. The BDP’s troubles allowed the BNF an easyvictory in a local council by-election in Gabane North and the party has hadthe confidence to challenge some of the BDP’s general election victories incourt, claiming that there had been electoral irregularities. The BDP and theIndependent Electoral Commission tried to stifle the BNF’s challenge by raisingpreliminary objections in the High Court, but these were overruled in late2000, allowing the BNF’s case to proceed. It is unlikely that the BNF will be ableto back its claims with hard evidence and overturn any of the general electionresults. But while the challenge continues it will put pressure on the BDP.

As its position strengthens, the BNF has gained at the expense of otheropposition parties—notably the Botswana Congress Party (BCP), which brokeaway from the BNF in 1998 (4th quarter 1998, page 11). Several hundredordinary BCP members are reported to have defected and some high-levelfigures have also moved, including former parliamentary candidates andvarious publicity hungry politicians, notably the ex-MP for Gaborone West,Paul Rantao. These reduce the chance of reconciliation between the BNF andthe BCP. Nonetheless, the future of the BNF remains uncertain, as its leader,Kenneth Koma, is supposed to stand down in 2001. The veteran politician haslong promised to retire, but has not yet managed to. This time he insists hewill not contest the party leadership. However, he has already changed hismind with regard to ending his involvement with the party, and has suggestedthat he will remain a strong influence even if he hands over the leadership.The most likely outcome will be party infighting throughout 2001, whichcould shift the balance of power in opposition politics and ensure that the BDPfaces no serious threat to its dominant position.

Further chances of opposition unity were dispelled in November when theBotswana People’s Party, a marginal party, expelled 10 members of its executivecouncil for failing to abide by a resolution ordering a breaking of links with theopposition unity movement, the Botswana Alliance Movement (BAM). TheBAM is now establishing itself as a separate political party, having failed tounite the plethora of opposition parties.

The government has again been criticised abroad for its treatment of theindigenous Basarwa people. The Basarwa, often known as bushmen, have foryears been fighting the government’s decision to remove them from theirancestral lands in the Central Kalahari game reserve. They claim that they arebeing moved to make way for tourism and mining, but the government says itjust wants to provide proper housing, health and education. A conference ofindigenous peoples in South Africa has found the Botswanan governmentguilty of human rights abuses against the Basarwa, and a book, Once We WereHunters, has backed up these claims. The Basarwa are a small group and suchcriticism will have no impact on domestic policies, nor could the government’s

BNF successes are likely tobe temporary

Botswana is criticised overhuman rights

Botswana 15

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

actions be described as harsh enough to warrant international action. It couldhowever affect tourism, particularly Botswana’s high-spend low-volume eco-tourism, if foreign tourists have the impression that they are contributing tothe Basarwa’s plight.

In November Botswana joined Lesotho, Namibia and South Africa in acommission to negotiate the use of the resources of the Orange River, whichhas tributaries in all four countries. Water rights are a contentious issue in theregion, as evidenced by South Africa’s large expenditure on dams in Lesothoand Swaziland, and water access was probably one of the more subtle issuesbehind the dispute between Botswana and Namibia over the Sedudu islands(1st quarter 2000, page 14). Any forums of this kind to head off potentialproblems enhance regional stability. In the same vein Botswana has signedsecurity pacts with South Africa and Zimbabwe.

Economic policy

The government’s twin objectives of fiscal restraint and economicdiversification remain the cornerstone of economic policy, and both came tothe fore during the last quarter. With the first, the government has made someprogress in cutting civil service expenditure. The performance managementsystem that the government is introducing to the civil service, at a cost ofP26m (US$4.7m), has been vigorously defended in the press in response tocriticism that it is based on private-sector initiatives that are not suitable forcivil servants. Further evidence of the government’s resolve to reform the civilservice was the announcement by the minister of presidential affairs andpublic administration, Thebe Mogami, that contrary to expectations, and thefinding of the 1998 salaries commission, civil servants will not get a housingallowance equal to 15% of their pay. As yet there has been no reaction fromthe public-sector unions.

On the revenue side, progress has been made towards replacing Botswana’ssales tax with a value-added tax (VAT), which should improve revenuecollection in the long run. The VAT bill was presented to parliament for asecond reading in December and passed, although some reported commentssuggested that most parliamentarians did not fully understand what was beingpresented. The rationale for the introduction of VAT is:

• to broaden the tax base; at present the yield from consumer spending isextremely low: sales tax accounts for only 4% of government revenue and1.8% of GDP;

• to remove the cascading effect of sales tax as producers are allowed todeduct VAT paid on inputs at every stage of the production process; under salestax this did not happen;

• to ensure that investment goods and exports are zero-rated, so removingdistortions that the government feels are apparent under the sales tax regime.

Regional co-operation onwater increases

Civil service reform

The VAT bill is passed

16 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

It is unclear at what level the tax will be set, but the Ministry of Finance hasbeen at pains to assure consumers that there should be little or no change inthe prices paid in shops. All businesses with a turnover of over P250,000(US$45,000) will have to register, while smaller business will be able to registervoluntarily if they want to claim tax deductions on their inputs. Exemptionsfrom VAT will include sorghum, millet and maize for human consumption (thestaple diet in Botswana), financial services, some prescription drugs (forexample for HIV/AIDS), rentals for residential property and education. Mostgovernment services are not exempt from VAT, and central and localgovernment will lose their exemption from paying VAT on goods and services.Implementation of the tax is expected to take 18 months to ensure a well-publicised and smooth introduction. The government is likely to be aware ofthe problems suffered elsewhere by the introduction of VAT, wheremisunderstanding led to the belief that this was a completely new tax.However, since South Africa introduced VAT ten years ago many are familiarwith the concept, reducing the risk of any serious public misunderstanding.Other measures to restructure the tax system are also under way, in particular anew tax identification numbering system.

As regards economic diversification, the closure of the Hyundai plant ownedby the Motor Company of Botswana (MCB) and the shift of car production toSouth Africa (see The domestic economy) has understandably caused concernabout government incentives for foreign investors, and has led to increasedsuspicion of all foreign investment. However, this is unlikely to last, and thepresident has made it clear that foreign investment is still welcome. Moreimportantly, Botswana has recently had some good news about foreigninvestment. The announcement that Waverley Blankets, South Africa’s largestblanket manufacturer, is moving to Botswana and creating hundreds of newjobs should ease public feeling. Nonetheless, the MCB furore has forced thegovernment to look closely at its incentive schemes. In his state of the nationaddress in November, the president, Festus Mogae, referred to the closure ofMCB and Haltek and said that investment would be more closely scrutinised.He insisted, however, that Botswana continues to need foreign investment andwould not change its policy on trying to attract it. The Botswana DevelopmentCorporation (BDC) had exposures of P100m to Haltek and more than that toBDC; the government had forgone millions of pula in tax exemptions for theHyundai plant; and Haltek had benefited from a P51m government grant.

The wave of problems with foreign investors has prompted the government torefocus on assistance for indigenous companies. However, the assistant financeminister, Boyce Sebetela, has announced in parliament that the country’smicro-credit scheme, started in June 1999, had exhausted its P150m (US$27m)funds (supposed to last until mid 2002), because of an extremely poorrepayment rate. The result has been to devise a number of new approaches tothe small business sector. The Ministry of Commerce and Industry has passedlegislation to the attorney-general for presentation to parliament to establishan independent small business council to advise the government on policy tohelp small, micro and medium-sized enterprises (SMMEs). The ministry, inassociation with business groups, has also launched a small business database

Incentives for foreigninvestors under scrutiny

Small business schemes alsoneed overhauling

Botswana 17

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

to link large buyers and small producers, while the Botswana Institute ofAccountants has pledged that some 200 accountants will provide four hours oftheir time per month to help small business using the SMME credit scheme(July 2000, page 19). If implemented properly these measures may have somesuccess. The reason mooted by the press for the failure of the previous schemeswas the government’s rush to get the money out before the 1999 generalelection.

The domestic economy

Botswana’s dreams of economic diversification were dealt a number of blows inthe final quarter of 2000. Most high-profile was the sale of the equipment usedto make the cars at the former Hyundai plant in Gaborone. Despite thegovernment’s hopes of reviving Botswana’s role as a regional vehiclemanufacturer, the equipment was sold for P38m (US$7m) to a South Africanconsortium of companies, backed by the Kimberley municipality, for use in thetown of Kimberley. Madeliro, a wholly owned subsidiary of the BotswanaDevelopment Corporation (BDC) bought the land and buildings, for P29m,although they had an estimated open-market value of P195m. This means thatall the assets of the Motor Company of Botswana (MCB) raised only P70m atauction despite costing P300m. While MCB still had an outstanding BDC loanof P121m, BDC obviously benefited from the sale of the plant at below-marketprices.

A number of textile manufacturers have also gone to the wall, at least two ofwhich—Tex in Selbi Phikwe and Haltek in Gaborone—had benefited fromgovernment assistance. Zheng Ming, a knitwear manufacturer, also closeddown, and its owners fled the country owing the government P1.2bn(US$218m) and unpaid staff wages of P720,000. Finally, in November TAHoldings, a Zimbabwean venture, announced its decision to withdraw fromCresta Marakanelo Hotels because of declining earnings there. TA held 40% ofCresta, while BDC holds the remaining 60%. This has led to a public outcryover the use of the government’s financial assistance policy.

South Africa’s largest blanket manufacturer, Waverley Blankets, has announcedthat it will switch its operations from South Africa to Botswana. The companywill invest around P100m (US$18m) and create 860 jobs in the first half of2001. Waverley blamed high South African wages and stringent labourlegislation, as well as dumping in the South African market (although they willpresumably still face this problem, as most exports will go to South Africa).However, it is more likely that the company is taking advantage of Botswana’sgenerous incentives, which include a special 15% tax rate. Tax competitionbetween countries was discussed at a recent Southern African DevelopmentCommunity forum, and this issue may gain prominence in the future.

Not all troubled firms in Botswana have closed. Botswana’s ailing millingcompany, Bolux, which has been struggling against cheap South Africanimports, was taken over by Namib Mills of Namibia towards the end of 2000.

Several manufacturersleave Botswana

Waverly Blankets movesfrom South Africa

Foreigners step in to Bolux

18 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Namib Mills’ main strategy seems to be focused on trying to protect the localmarket from “unfair” South African competition, although there is also talkof regional expansion from Botswana. Bolux, which comprises South African,Zimbabwean and Australian investors, was forced to accept Namib Mills’P30m (US$5.5m) offer as the overdrafts on which it had been relying werenot being renewed.

Mining

Debswana has raised the possibility that it will open a new diamond mine,20 km east of Orapa. This comes after the discovery of four kimberlite pipesthat it is estimated will yield around 100,000 carats, 80% of which will beindustrial quality, the rest gem quality. Work on the new mine should beginnext year and commissioning is expected in 2002. The Debswana board hasapproved the expenditure of P225m (US$41m) on developing the open-castmine, which will employ around 180 people when fully operational and have alife span of 32 years. The development of the new mine comes as the Ministryof Mineral Resources, Energy and Water Affairs is waiting for the results of astudy to determine whether it is feasible to keep the Tswapong diamond mineopen; there is a strong possibility that the mine may close, leading to the lossof hundreds of jobs.

The strength of the relationship between Botswana’s diamond industry and theglobal diamond trader De Beers was emphasised in November when De Beersand the government of Botswana signed another five-year agreement. Theagreement obliges the bilateral joint venture, Debswana, to sell all its diamondsto De Beers, who guarantees to buy all of Debswana’s production, for the nextfive years. Details of pricing formulas and to what extent stockpiling can beused in the event of a global downturn have not been released. Debswanaexpects to produce in excess of US$2bn of diamonds each year.

The effect of the campaign led by the environmental and human rightspressure group, Global Witness against conflict diamonds (those sold to fundarmed groups engaged in civil conflict) on legitimate diamond sales remains anarea of concern for Botswana (July 2000, page 22). Botswana has won thesupport of the British foreign office minister, Peter Hain, and the US secretaryof state, Madeline Albright, both of whom visited the country in late 2000, toensure that action taken over conflict diamonds, distinguishes between illegaland legitimate sources of diamonds. Botswana has also hired an internationalconsultancy to ensure that the diamond-buying public can differentiatebetween the sources of diamonds. Balise Bonyongo, the plant manager ofAquarium, Botswana’s new hands-free treatment centre for diamonds at theJwaneng mine, has confirmed that the P360m (US$65m) plant will providehistorical evidence of production from open shaft pit up to the valuationpoint, thereby proving stones are not conflict diamonds.

New agreement signed withDe Beers

Steps to avoid fallout fromthe conflict diamonds issue

A fourth diamond mine isin the offing

Botswana 19

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

Agriculture

While Botswana’s mineral economy goes from strength to strength, theagricultural economy continues to flounder. The floods in early 2000 continueto take their toll and the Ministry of Agriculture has estimated that the countryfaces a grain deficit of 207,278 tonnes—the shortfall is to be made up byimports. Botswana also experienced a milk shortage in December because of atemporary ban on meat and dairy products from South Africa as a result of anoutbreak of foot and mouth disease there. The shortage and the ban weretemporary and were being resolved slowly in early 2001.

Although Botswana’s beef industry is still underperforming, the situation isimproving and the authorities are trying hard to ensure its future. One majorstep is recent progress in meeting EU guidelines on tracking the life history ofcattle. The government has awarded a contract for the design andimplementation of a National Livestock Identification and Trace Back systemto AST Botswana, which will involve implanting computerised identificationdevices in Botswana’s 2m cattle. The programme will cost P63m (US$11.5m)and the first phase, the development of a central database and identification ofcattle in pilot districts, is expected to be complete by May 2001; the system isexpected to be implemented countrywide by mid-2003.

The government’s plans to spray chemicals in the Okavango delta area toeradicate the tsetse fly are under attack from environmental groups. Thegovernment says it will go ahead with a three-stage plan to eradicate the fly,the first phase of which will be aerial spraying of a controversial chemical,endsulfan. The environmental groups claim the chemical will affect fish andbird life and in large doses can be fatal to humans. The government maintainsthat the chemical has been used for 20 years in Botswana and will beminimally used as the spraying will be followed by the release of sterile maleflies to mate with females who do not breed while the fertile males die out. Theissue has attracted widespread interest, as it is claimed that the cattle that grazein the Okavango belong only to a handful of cattle barons and that suchdrastic steps are being taken to protect the incomes of a small elite.

Financial services

Botswana continues to work towards establishing an International FinancialServices Centre (IFSC) but it is facing obstacles on the way. The latest potentialsetback was a statement by the South African minister of finance, TrevorManuel, that Botswana’s neighbour would itself establish an IFSC to act as aconduit for funds into other African countries. However, despite initial fearsthat this would upstage Botswana’s plans, it is not likely to be a major issue.Botswana’s IFSC will start with relatively modest proposals such as crossborderleasing and call centres, which it is hoped will create new jobs. If the SouthAfrican IFSC goes ahead, which is not a certainty, it is likely to target a moresophisticated market. In other respects too it is unlikely that South Africa posesan immediate threat to Botswana’s IFSC plans. Mr Manuel made the remarks at

A tsetse eradication schemeis attacked

Obstacles to the IFSC arebeing overcome

The beef industry movestowards EU standards

20 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

the opening of a new stock exchange building and the prospect of a low taxenvironment was most likely aimed to appease the domestic financialcommunity, who are concerned about the introduction of capital gains tax in2001. Additionally, South Africa is unlikely to risk the disapproval of OECDcountries, who may be more concerned about tax breaks in a large country likeSouth Africa than in a small country like Botswana.

A more serious issue for Botswana is South Africa’s plan to shift from source-based to residence-based taxation in 2001. This would be a blow for Botswanaas South African companies at present can establish a subsidiary to operate inlow tax environments, such as Botswana, and benefit from the tax breaks.Under the initial plans for a residence-based system, any company that isresident in South Africa would be liable to South African tax wherever thelocation of its operations, so that the South African Revenue Service wouldclaw back any tax saving made in a foreign country. This caused a furore inSouth Africa and after a series of negotiations Mr Manuel agreed someconcessions. The main concession appears to be that although the residence-based system will still be introduced, companies based in South Africa andoperating in Botswana will probably only have to pay the difference betweenthe tax rates when they remit profits or dividends. This is a good result forBotswana, nonetheless it does emphasis the fragility of plans for economicdiversification based on low taxes.

A boost to the IFSC plans came in October 2000 when it emerged that fourinternational banks have applied for operating licences from both South Africaand the UK—full details have yet to be made public. The EIU expects that thebanks will start off by opening small offices to explore the opportunities.

Botswana’s domestic financial scene appears to be going from strength tostrength. On the banking side two significant developments occurred in thelast quarter of 2000 which bode well for domestic consumers. India’s Bank ofBaroda has applied for and been granted an operating licence. Bank of Baroda(Botswana) will open in February, bringing the number of commercial banks inthe country to five. The bank claims it will target the local market, particularlytextiles, pharmaceuticals, electronics and small business loans.

Although not necessarily related to the new competition, more good news forconsumers in Botswana was an announcement by First National Bank (FNB)that it is shifting into the small personal loan market. FNB has established acompany, First Lending, with two local firms, Easy and Aelima BatswanaProperty, to target those in employment who do not have access to bank loans.FNB has provided the capital. Clients will contact First Lending via brokers andrepayment will be deducted from salaries. First Lending claims it will avoid theproblem, acute in South Africa, of whole salaries being wiped out, by ensuringthat a minimum salary is left over after loan repayments are deducted. Theloans will vary between P1,000 and P15,000. Interest rates will be linked to theprime rate and will be at present around 28%, this is high in real terms butlower, claims FNB, than most informal micro-lenders.

Botswana’s insurance industry also appears to be doing well. BotswanaInsurance Holdings reported that premium income in the first six months of

New ventures and goodresults in financial sector

Botswana 21

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

2000 was P138.6m, 50% up on the same period in 1999. Net recurringpremium income was up by 29%. On the back of this success BotswanaInsurance Fund Managers had a prosperous year and is expanding regionally. Ithas started with a Zambia office and hopes to broaden out in 2001. Much ofthe success of the insurance industry can be credited to improved marketingand the growing sophistication of both products and clients. More worrying isthe impact of rising AIDS deaths. Although life assurance is not available forHIV-positive people, a number of other insurance policies are, in particular topay funeral expenses.

Only 54% of the bonds issued by the Botswana Building Society on November30th (with a coupon of 14.25%) were taken up, and the sale raised P27minstead of the expected P50m. Much of this was due to general nervousnessthroughout global financial markets towards the end of 2000; had the issuebeen launched at another time it might have been more successful. On thepositive side the bond provides another addition to the fledgling bond marketas well as demonstrating again the government’s commitment to weaningparastatals off central government funding and onto private finance ahead ofprivatisation. However, it should sound a warning bell for the government thatprivate-sector finance is not automatically available for all public-sectorventures.

Botswana has continued to receive positive international press coverage in theform of investment surveys. An annual survey of country risk in emergingmarkets by Nord-Sud Export for the OECD categorised Botswana as “very smallrisk” for exporters and “small risk” for investors, the only African country toobtain such a high ranking. This comes after similarly glowing reports fromother NGOs such as Transparency International. This will please Botswana’sgovernment, which is trying to secure a credit rating this year to pave the wayfor official and private borrowing on the international capital markets. In thisregard the authorities will have watched with interest the rating given byStandard & Poor’s to Senegal, the first Sub-Saharan country outside SouthAfrica it has rated. Senegal was awarded a B+, which puts it on a par with Braziland Turkey. Although Senegal benefits from enforced monetary disciplinethrough the CFA franc, Botswana’s financing position is much stronger thanSenegal’s in terms of debt ratios, government finances, expected current-account balances and international assets. This may encourage the localauthorities to believe that they are entitled to a much higher rating, however;we expect Botswana to be awarded a rating just into investment grade status(which starts at BBB-).

Infrastructure

Botswana’s bid to become an international financial services centre (IFSC) restsnot only on the incentives it can offer, but also on being able to provide thephysical infrastructure necessary to support such services. Botswana is wellpositioned as it can make use of much of South Africa’s infrastructure.However, Botswana, like many countries in the region, continues to struggle to

Building society bond isundersubscribed

Botswana shines ininvestment surveys

Telecommunications mustbe improved

22 Botswana

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

keep up with telecommunications developments, especially at the parastatallevel, which is at least part of the reason for the success of private cell phonecompanies. Although the arrival of cell phones has helped to ease voice trafficproblems, landlines for Internet use remain expensive and difficult to obtain.Landlines are the sole preserve of the parastatal, Botswana TelecommunicationsCorporation (BTC). Costs are higher than in South Africa, and some firms haveclaimed that BTC has been giving unfair preference to its own Internet serviceprovider, Botsnet. Failure to improve the telecoms infrastructure could spoilBotswana’s chances of attracting significant international interest in the IFSC;much rests on whether the government decides to privatise BTC, or end itsmonopoly, rather than allowing the current service to continue.

Foreign trade and payments

Although originally scheduled to take only three months, six years later, anddespite several apparently inviolable deadlines, it now looks as if therenegotiation of the Southern African Customs Union (SACU) agreement isabout to reach a conclusion. The basic problem with the existing revenue-sharing formula was that it included a compensation element. This wassupposed to offset the fact that under South Africa’s old trade regime, exportsfrom South Africa to the BLNS states (Botswana, Lesotho, Namibia andSwaziland) were more expensive than on the world market. It was also meantto compensate for the concentration of industry within South Africa and theloss of policy discretion. However, with the end of apartheid and with SouthAfrica joining the WTO, the BLNS states continue to benefit from thestabilisation and compensation elements even though external trade barriersare now being lifted. The compensation element is also magnified, as importsinto the BLNS countries have grown more quickly than those into South Africaat a time when South Africa is in great need to increase fiscal revenue.

SACU’s new revenue-sharing deal

• Each country will receive a share of the common customs revenue poolbased on its imports from SACU as a proportion of total intra-SACUimports. Since the BLNS countries import much more from South Africathan it does from them, the formula is biased in their favour and implicitlytakes account of price-raising effects and other distortions which will inany case decline as tariffs are lowered under WTO obligations.

• 15% of total excise duties will be allocated to development, and will beshared on the basis of an inverse ratio of income per head to the SACUmean, reduced by a factor of 10 to smooth out distortions. Each membercountry will thus receive between 18% and 22% of the developmentallocation. Since excise duties are levied mainly on South Africanproduction, this is a way of redistributing to the BLNS countries.

• 85% of total excise duties will be allocated on the basis of GDP, whichimplicitly favours the poorer countries—Lesotho, and to a lesser extent,Swaziland—over the richer countries such as Botswana.

A new SACU agreement isimminent

Botswana 23

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

• It has been proposed that an independent SACU secretariat should beestablished to administer the new agreement. Previously, the agreementwas administered by the South African government, which was a source ofcontention. The new secretariat should also allow further reforms to beadopted more quickly.

It is likely that the new agreement will be implemented in stages: it is intendedto introduce the revised revenue-sharing arrangements on April 1st 2001, but itwill not be possible to redraft the entire agreement for ratification until theinstitutional structure has been finalised and other aspects relating to commonfarm and industrial policies have been agreed. It is also probable that the EUwill increase aid to the BLNS countries to offset any long-term decline inrevenue under either the revision of the SACU agreement or as a result of theEU-South Africa free-trade agreement, which will reduce the total customsrevenue accruing to the BLNS countries.

24 Lesotho

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Lesotho

Political structure

Kingdom of Lesotho

Monarchy

Based on Roman-Dutch law

Bicameral National Assembly elected according to the terms of the 1993 constitution;80 elected members in the lower house; 33 non-elected members in the upper house(Senate), 11 of whom are nominated by the king on the advice of the prime minister,plus the 22 principal chiefs of Lesotho. The Interim Political Authority (IPA), establishedin November 1998 to oversee preparations for the next election, consists of 24 members,representing 12 political parties. The IPA put forward a system whereby 80 members willbe elected on a first-past-the-post basis, and 50 members elected by proportionalrepresentation; the government wants only 40 members to be elected by PR. Subsequentelections are proposed to have a 50:50 split between members elected on the basis offirst-past-the-post and proportional representation; however, following delays in theholding of the election, the status of this agreement has become unclear

May 1998 (legislative); in May 2000 the government announced that the next electionwould be held between March and May 2001

Monarch; the succession is governed by custom; King Letsie III was sworn in onFebruary 7th 1996 and crowned on October 31st 1997

Prime minister and a 16-member cabinet, last reshuffled in August 1999

Party political organisation was legalised in May 1991. The main parties include:Lesotho Congress for Democracy (LCD, the ruling party); Basotho Congress Party (BCP);Basotho National Party (BNP); Marematlou Freedom Party (MFP); Kopanang BasothoParty (KBP); Popular Front for Democracy (PFD); Progressive National Party (PNP);Lesotho Labour Party (LLP); Communist Party of Lesotho (CPL)

Prime minister, defence & public services Pakalitha MosisiliDeputy prime minister, minister of finance & development planning Kelebone Maope

Agriculture, co-operatives & land reclamation Vova BulaneCommunications Nyane MphafiEducation Lesao LehohlaEmployment & labour Notsi MolopoEnvironment, gender & youth Mathabiso LeponoForeign affairs Tom ThabaneHealth & social welfare Tefo MaboteIndustry, trade & marketing Mpho MalieJustice, human rights, law, constitutional affairs & rehabilitation Shakhane MokhehleLocal government & home affairs Mopshatla MabitleNatural resources Monyane MolelekiPrime minister’s office Sephiri MotanyaneWorks & transport Mofelehetsi Moerane

Stephen Swaray

Official name

Form of state

Legal system

National legislature

National elections

Head of state

National government

Main political parties

The government

Key ministers

Central Bank governor

Lesotho 25

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

Economic structure

Annual indicators

1996 1997 1998 1999 2000a

GDP at market pricesb (M m) 4,053 4,720 4,921 5,636 6,098

Real GDP growthb (%) 9.7 4.1 –4.6 2.0c 1.2

Consumer price inflation (av; %) 9.3 8.5 7.8 8.7 6.1d

Population (m; mid-year) 1.97 2.02 2.06 2.11 2.16

Exports fob (US$ m) 187 196 193 172 201

Imports fob (US$ m) 999 1,024 866 780 700

Current-account balance (US$ m) –303 –269 –280 –230 –154

Reserves excl gold (year-end; US$ m) 461 572 575 500 430

Total external debt (US$ m) 670 660 692 705a 720

External debt-service ratio, paid (%) 6.4 6.2 8.4 7.5a 7.5

Migrant miners (year-end; ‘000) 101.7 95.9 80.4 68.8 60.0

Exchange rate (av; M:US$) 4.30 4.61 5.53 6.11 6.94d

January 9th 2001 M7.73:US$1

Origins of gross domestic product 1998b % of total Components of gross domestic product 1998b % of total

Agriculture 16.6 Private consumption 111.9

Industry 37.3 Public consumption 19.4

Manufacturing 16.5 Gross domestic investment 47.9

Construction 19.1 Exports of goods & services 26.4

Services 46.1 Imports of goods & services –105.6

GDP at factor cost 100.0 GDP at market prices 100.0

Principal exports fob 1998 US$ m Principal imports cif 1995c US$ m

Manufactures 144 Capital goods 368

Food & live animals 8 Food 328

Wool & mohair 4 Fuel & energy 216

Total incl others 193 Total incl others 1,168

Main destinations of exports 1998c % of total Main origins of imports 1998c % of total

Southern African Customs Union 65.1 Southern African Customs Union 89.6

North America 33.8 Asia 6.3

EU 0.7 North America 1.7

a EIU estimates b Fiscal years beginning April 1st. c Official estimates. d Actual.

26 Lesotho

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Quarterly indicators

1998 1999 20004 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr

Government finance (M m)Revenue & grants 549.7 611.0 521.4 593.3 570.3 658.7 n/a n/aExpenditure & net lending 586.9 725.9 574.2 613.2 875.4 641.5 n/a n/aBalance –37.2 –114.9 –52.8 –19.9 –305.1 17.2 n/a n/a

Employment, wages & pricesBasotho miners in South Africa Employed (av) 72,950 69,456 68,736 68,981 67,242 65,727 64,659 n/a Remittances (M ’000) 21,775 26,151 18,163 21,275 26,394 15,505 30,710 n/aConsumer prices (1995=100) 129.1 132.1 134.1 136.8 137.8 140.3 142.6 144.3 % change, year on year 4.65 7.33 8.95 9.26 6.76 6.2 6.3 5.5

Financial indicatorsExchange rate M:US$ (av) 5.78 6.09 6.13 6.10 6.13 6.30 6.86 7.00 M:US$ (end-period) 5.86 6.19 6.04 6.01 6.15 6.56 6.77 7.26 Nominal effective (1995=100) 67.9 65.5 66.3 66.9 66.7 65.9 61.8 61.4 Real effective (1995=100) 82.8 81.3 83.0 84.7 84.2 82.6 77.9 77.7Interest rates (%; av) Treasury bill 17.43 15.39 12.70 11.55 10.18 9.14 8.86 9.09 Lending 22.25 21.00 19.25 18.33 17.67 17.00 17.00 17.45M1 (end-period; M m) 971.4 973.5 980.8 908.0 943.9 982.6 940.1 938.4 % change, year on year 27.4 20.3 19.3 7.6 –2.8 0.9 –4.2 3.4M2 (end-period; M m) 1,746.7 1,730.8 1,694.7 1,625.1 1,658.0 1,701.4 1,666.7 1,635.7 % change, year on year 20.5 11.8 8.2 10.7 –5.1 –1.7 –1.6 0.7

Foreign trade and reservesExports fob (M m) 314.67 205.29 231.02 304.63 313.15 312.26 n/a n/aImports fob (M m) –1,141.58 –992.66 –1,329.51 –1,244.28 –1,194.99 –1,139.98 n/a n/aTrade balance (M m) –826.91 –787.37 –1,098.49 –939.65 –881.84 –827.72 n/a n/aServices balance (M m) –18.60 –14.19 –8.79 –8.66 –7.37 13.84 n/a n/aIncome balance (M m) 342.79 378.92 335.89 364.88 413.74 414.78 n/a n/aCurrent transfers (M m) 175.60 239.58 219.34 226.45 217.66 297.61 n/a n/a SACU non-duty receipts (M m) 159.82 168.85 208.05 212.31 203.55 212.63 n/a n/aCurrent-account balance (M m) –327.12 –183.06 –552.02 –356.98 –257.81 –101.49 n/a n/aReserves excl gold (end-period; US$ m) 575.1 410.1 520.0 535.4 499.6 469.2 425.5 447.9

Sources: IMF, International Financial Statistics; Central Bank of Lesotho, Quarterly Review.

Lesotho 27

© The Economist Intelligence Unit Limited 2001 EIU Country Report January 2001

Outlook for 2001-02

Political outlook

Progress towards holding the legislative election has ground to a halt and, inthe absence of a breakthrough, it looks increasingly likely that the May 26thdeadline set by the Independent Electoral Commission (IEC) will be missed.The electoral model has still to be finalised, with the dispute centring on thenumber of members of parliament to be elected by proportionalrepresentation. But agreement on this could be reached quite late withoutendangering the election. The major practical problem with keeping to theelection timetable is that voter registration did not begin as scheduled inDecember 2000. The government raised last-minute objections to the use ofthe proposed fingerprint technology, arguing that it was technically unsoundand too expensive.

These objections were not very convincing, but as a spoiling tactic theyproved quite effective, and the government may be having some success inwinning the propaganda war with the Independent Political Authority (IPA).This would particularly be the case if the government could convince thepopulation that the IPA is being deliberately intransigent. The governmentappears increasingly willing to sacrifice the electoral timetable yet again ratherthan be seen to be holding the elections under the directions of the Authority.In taking this line it may be encouraged that the Southern AfricanDevelopment Community (SADC) guarantors of the process have not made astand in favour of either side. This has been much to the frustration of theIPA, which has accused SADC of abandoning Lesotho.

Although it is responsible for delaying the election, the ruling LesothoCongress for Democracy (LCD) has the best chance of winning, despiteinternal disputes within the party. This is because the LCD has traditionallyhad the discipline to contain its problems (barring the odd lapse), whereasthose of the opposition parties are becoming far more open, as factions andcandidates jockey for position in anticipation of the election. The LeonCommission, which is investigating the causes of the unrest in 1998, willresume its work in January (after being adjourned in September 2000).Damaging accusations were aired at earlier hearings and, with those accusednow having to defend themselves, further acrimony is likely.

With the election process in deadlock Lesotho’s external relations seem tohave cooled. SADC appears to be distancing itself from the process, whilethere have been reports that European donors are reluctant to provide funds.At the same time, however, there are moves to strengthen the bilateralrelationship between Lesotho and South Africa. This is a reflection of thereality that South Africa cannot simply disengage itself from the affairs of itsfractious neighbour. As long as the present political situation does notdegenerate into violence, foreign governments do not have a strong interestin forcing the government to hold the election.

Domestic politics

International relations

28 Lesotho

EIU Country Report January 2001 © The Economist Intelligence Unit Limited 2001

Economic policy outlook

A nine-month IMF staff-monitored programme was successfully concluded inSeptember 2000. This is expected to lead to the agreement of a formalmedium-term programme with the Fund under its poverty reduction andgrowth facility (PRGF), which will serve to boost confidence in the economy.While policies outlined in the PRGF will aim to promote economic growth,the emphasis for both fiscal and monetary policy will be on prudence. Inparticular, fiscal policy will concentrate on reducing further the size of thebudget deficit relative to GDP. With the passage of the new Central Bank andFinancial Institutions Acts, the Central Bank of Lesotho will take on a moreprominent role regulating the financial sector and may be given greaterfreedom to act in monetary policy.

Several problems were encountered during the nine-month programme, andthese reflect areas that policy will need to address over the forecast period. Theestablishment of an implementation unit to oversee the introduction ofVAT—scheduled for April 2002—was only achieved very late, reinforcingconcerns about the administration’s capacity to manage the processeffectively. Some of the financial targets were missed during part of theprogramme period, highlighting problems with expenditure control,especially since revenue was more buoyant than forecast. Although thegovernment took remedial measures to cut back on expenditure and meet allfinancial targets by the end of the programme, it is clear that effectivebudgeting of recurrent expenditure remains a serious weakness.

After a successful year in 2000, when 70% of Lesotho Telecom and thegovernment’s remaining holding in Vodacom Lesotho were successfully sold,the momentum of the privatisation process is likely to be maintained over theoutlook period. The electricity corporation and water authority are now beingprepared for privatisation, while progress has been made in the troublesomearea of agricultural parastatals.

Economic forecast