Bond Valuation

47

9-1 Copyright © 2011 Pearson Prentice Hall. All rights reserved. Debt Valuation and Interest Rates Chapter 9

description

bv

Transcript of Bond Valuation

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 1/47

9-1Copyright © 2011 Pearson Prentice Hall. All rights reserved.

Debt Valuation

and InterestRates

Chapter 9

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 2/47

9-2Copyright © 2011 Pearson Prentice Hall. All rights reserved.

Overview of

Corporate Debt

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 3/47

9-3

Corporate Borrowings

• There are two main sources of borrowingfor a corporation:

1. Loan from a financial institution (known asprivate debt)

2. onds (known as public debt since the! can

be traded in public financial markets)

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 4/47

9-

Corporate Borrowings

• "maller firms choose to raise mone! frombanks in the form of loans because of thehigh costs associated with issuing bonds.

• Larger firms generall! raise mone! frombanks for short#term needs and depend on

the bond market for long#term financingneeds.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 5/47

9-!

Borrowing "one# in the $rivate%inan&ial "ar'et

• %inan&ial Institutions are an importantsource of capital for corporations. The loanmight be used to finance firm$s da!#to#da!

operations or it might be used for thepurchase of e%uipment or propert!.

• "uch loans are considered private (ar'ettransa&tions since it onl! involves the two

parties to the loan.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 6/47

9-)

Borrowing "one# in the $rivate%inan&ial "ar'et

• &n the private financial market' loans aret!picall! floating rate loans i.e. theinterest rate is periodicall! adusted based

on a specific benchmark rate.

• The most popular benchmark rate is the

*ondon Interban' Offered Rate+*IBOR,

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 7/47

9-

Borrowing "one# in the $rivate%inan&ial "ar'et

• *IBOR is the dail! interest rate that isbased on the interest rates at which banksoffer to lend in the London wholesale or

interbank market.

&nterbank market is the market where banksloan each other mone!.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 8/47

9-.

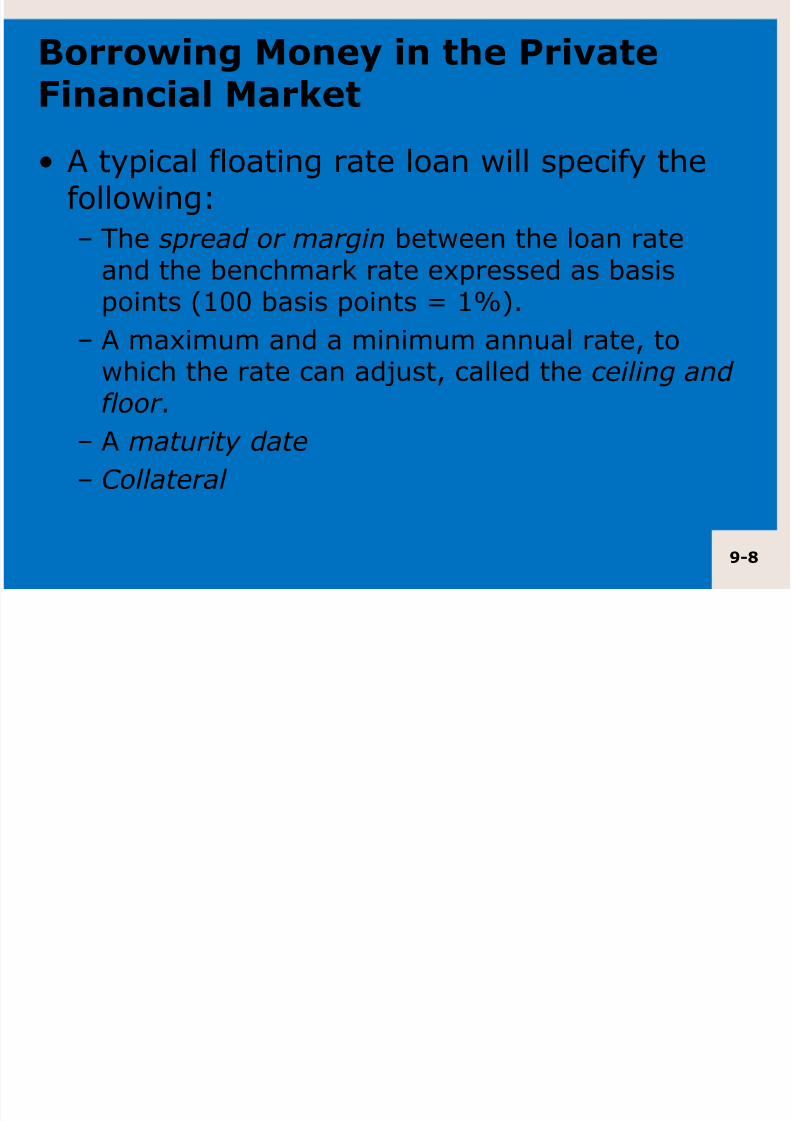

Borrowing "one# in the $rivate%inan&ial "ar'et

• * t!pical floating rate loan will specif! thefollowing:

The spread or margin between the loan rate

and the benchmark rate e+pressed as basispoints (1,, basis points - 1).

* ma+imum and a minimum annual rate' towhich the rate can adust' called the ceiling and

floor . * maturity date

Collateral

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 9/47

9-9

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 10/47

9-1/

Borrowing "one# in the $ubli&%inan&ial "ar'et

• /irms also raise mone! b! selling debtsecurities to individual investors andfinancial institutions.

• &n order to sell debt securities to thepublic' the issuing firm must meet thelegal re%uirements as specified b! thesecurities laws.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 11/47

9-11

Borrowing "one# in the $ubli&%inan&ial "ar'et

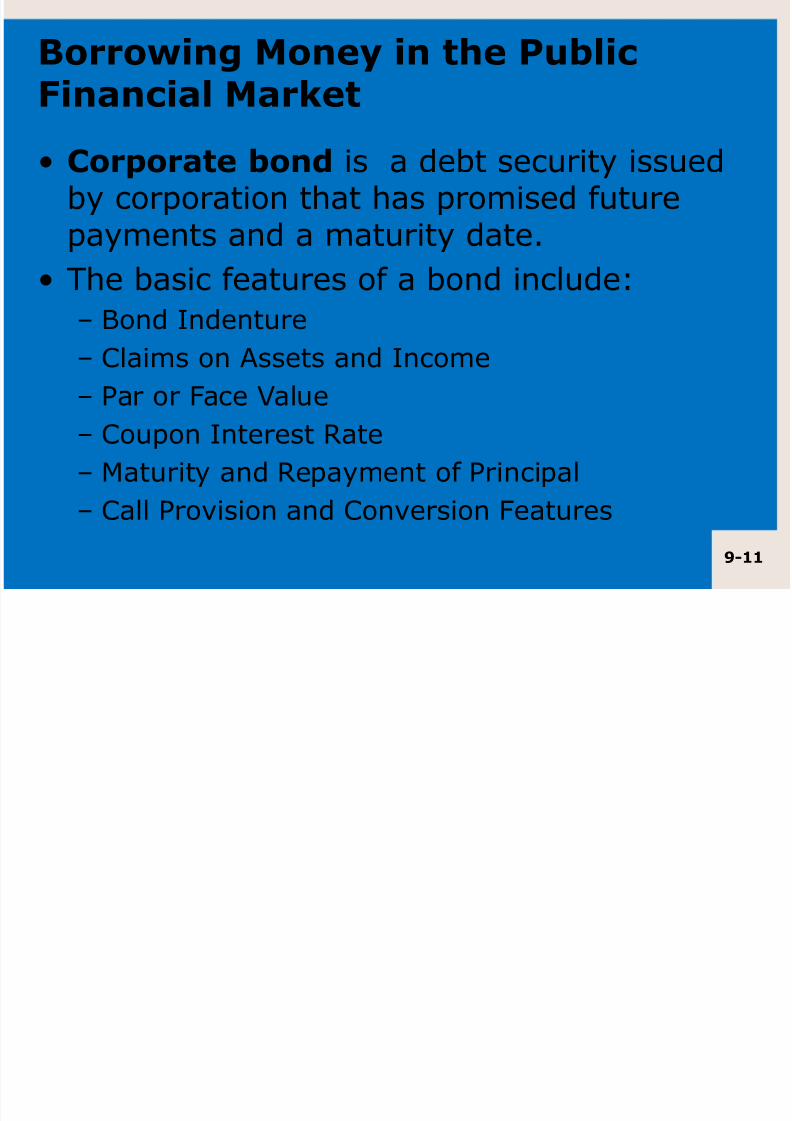

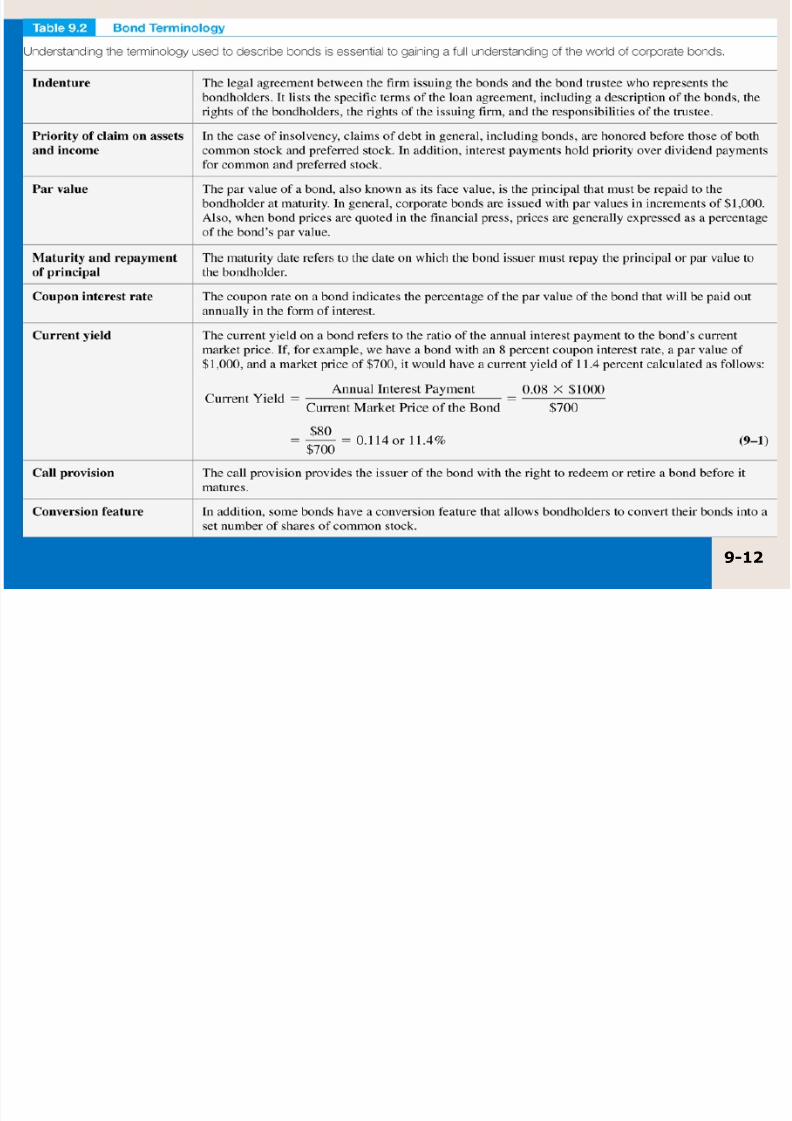

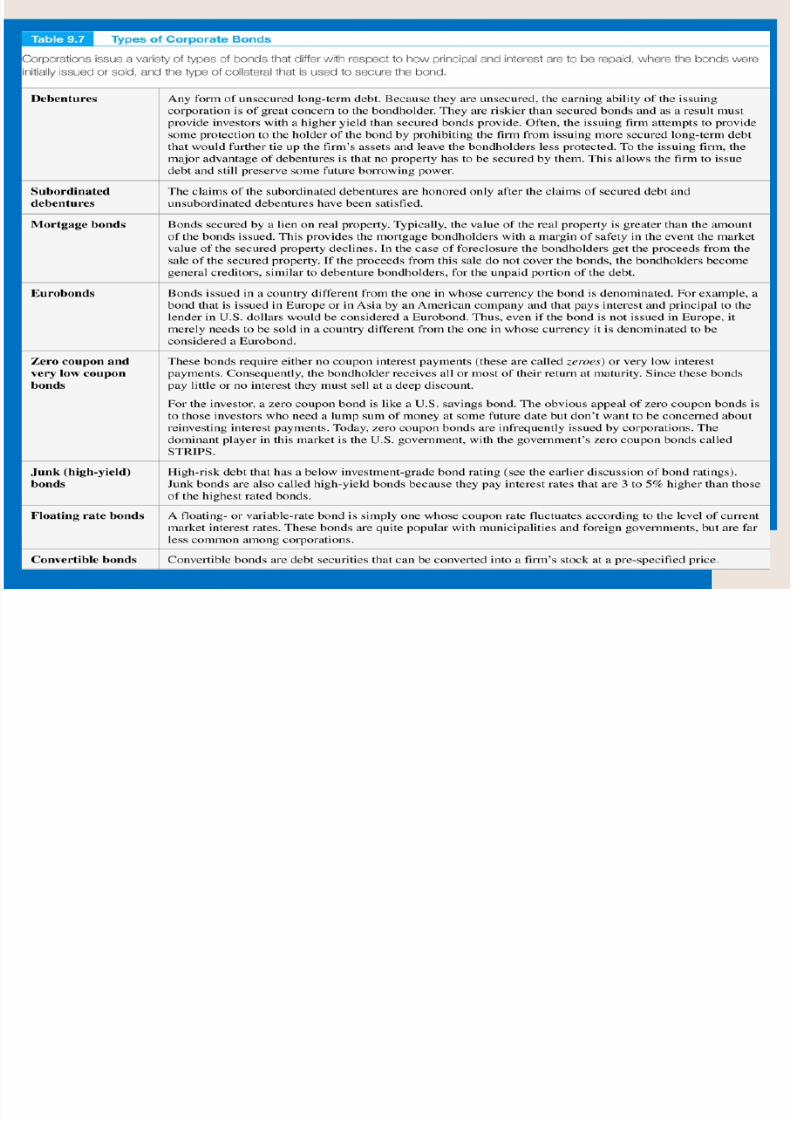

• Corporate bond is a debt securit! issuedb! corporation that has promised futurepa!ments and a maturit! date.

• The basic features of a bond include: ond &ndenture

0laims on *ssets and &ncome

ar or /ace alue

0oupon &nterest 3ate

4aturit! and 3epa!ment of rincipal

0all rovision and 0onversion /eatures

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 12/47

9-12

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 13/47

9-13

Bond %eatures

• * &all feature' which is included in mostcorporate issues' gives the issuer the opportunit!to repurchase the bond prior to maturit! at the callprice.

• &ssuers will e0er&ise the call feature when interestrates fall and the issuer can reissue at a lowercost.

• &ssuers t!picall! must pa! a higher rate to

investors for the call feature compared to issueswithout the feature.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 14/47

9-1

Bond %eatures

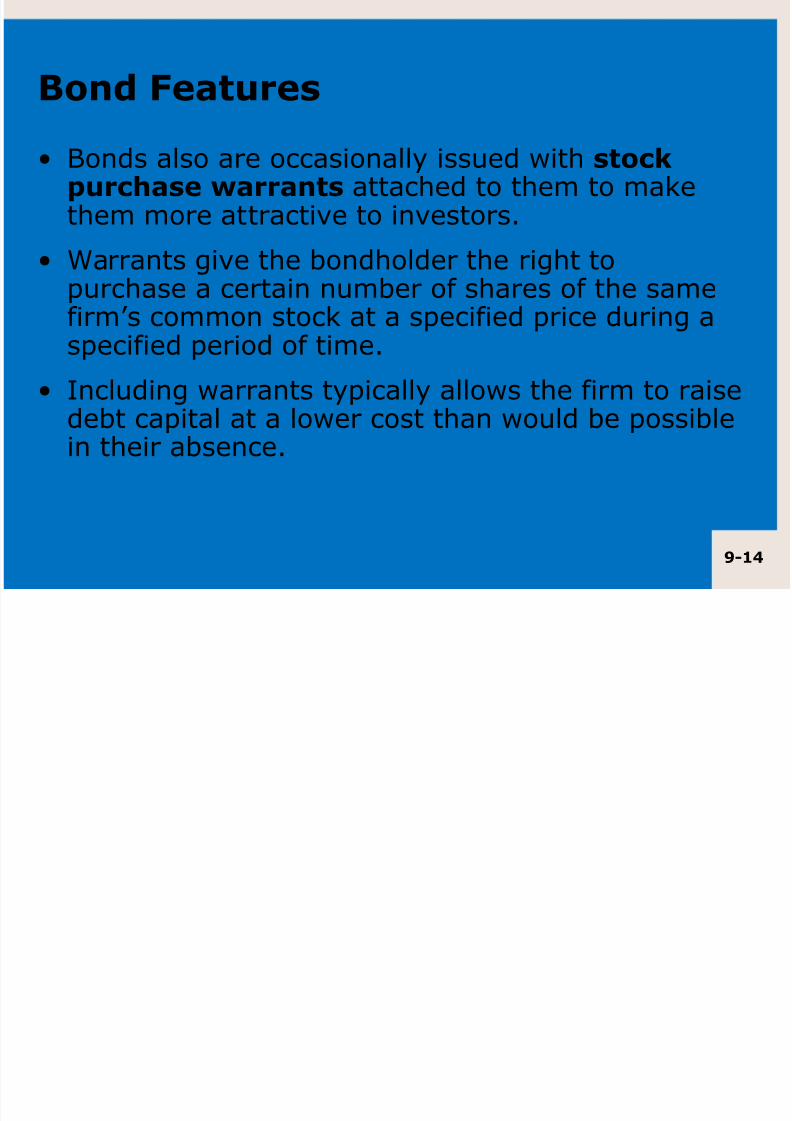

• onds also are occasionall! issued with sto&'pur&hase warrants attached to them to makethem more attractive to investors.

• 5arrants give the bondholder the right topurchase a certain number of shares of the samefirm$s common stock at a specified price during aspecified period of time.

• &ncluding warrants t!picall! allows the firm to raise

debt capital at a lower cost than would be possiblein their absence.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 15/47

9-1!

Bond %eatures

• The bond$s #ield-to-(aturit# is the !ield(e+pressed as a compound rate of return)earned on a bond from the time it is

ac%uired until the maturit! date of thebond.

• * #ield &urve graphicall! shows therelationship between the time to maturit!

and !ields for debt in a given risk class.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 16/47

9-1)

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 17/47

9-1

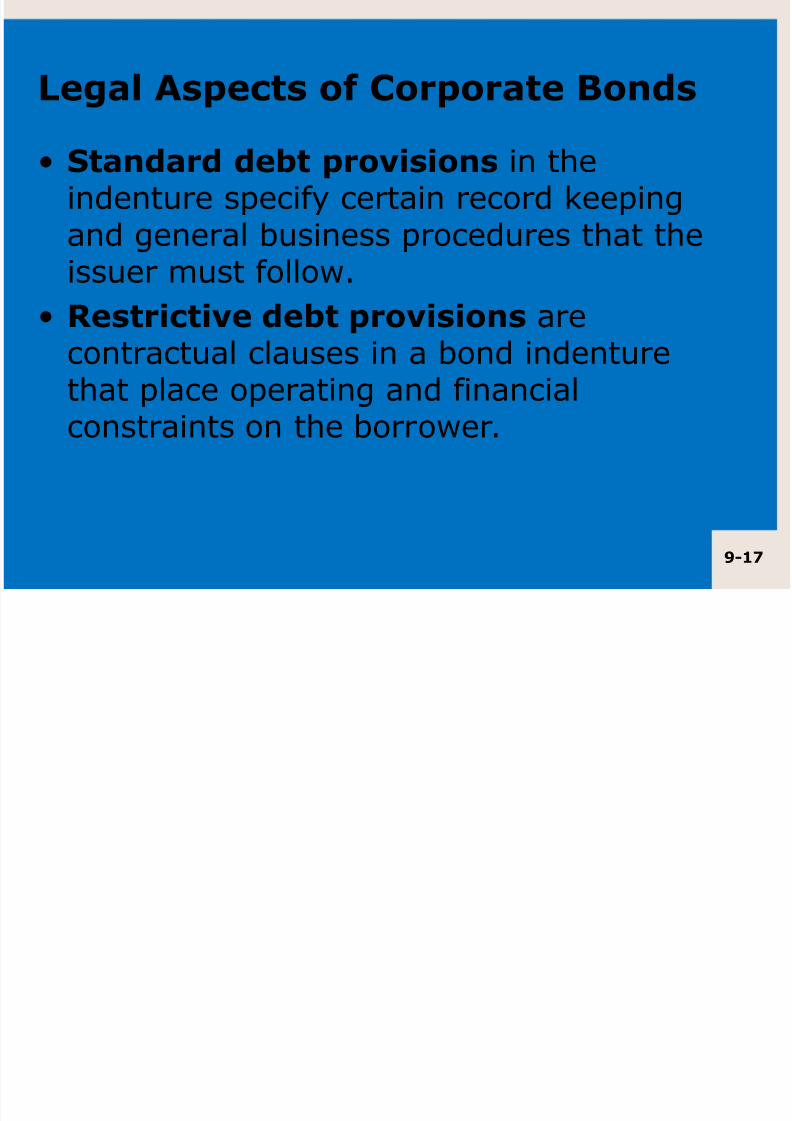

*egal spe&ts of Corporate Bonds

• tandard debt provisions in theindenture specif! certain record keepingand general business procedures that the

issuer must follow.• Restri&tive debt provisions are

contractual clauses in a bond indenturethat place operating and financial

constraints on the borrower.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 18/47

9-1.

*egal spe&ts of Corporate Bonds

• 0ommon restrictive covenants include provisionsthat specif!: 4inimum e%uit! levels

rohibition against factoring receivables

/i+ed asset restrictions 0onstraints on subse%uent borrowing

Limitations on cash dividends.

• &n general' violations of restrictive covenants give

bondholders the right to demand immediaterepa!ment.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 19/47

9-19

*egal spe&ts of Corporate Bonds

• in'ing fund reuire(ents are restrictiveprovisions often included in bond indentures thatprovide for the s!stematic retirement of bondsprior to their maturit!.

• The bond indenture identifies an! collateral(securit!) pledged against the bond and specifieshow it is to be maintained.

• * trustee is a paid individual' corporation' or

commercial bank trust department that acts as thethird part! to a bond indenture.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 20/47

9-2/

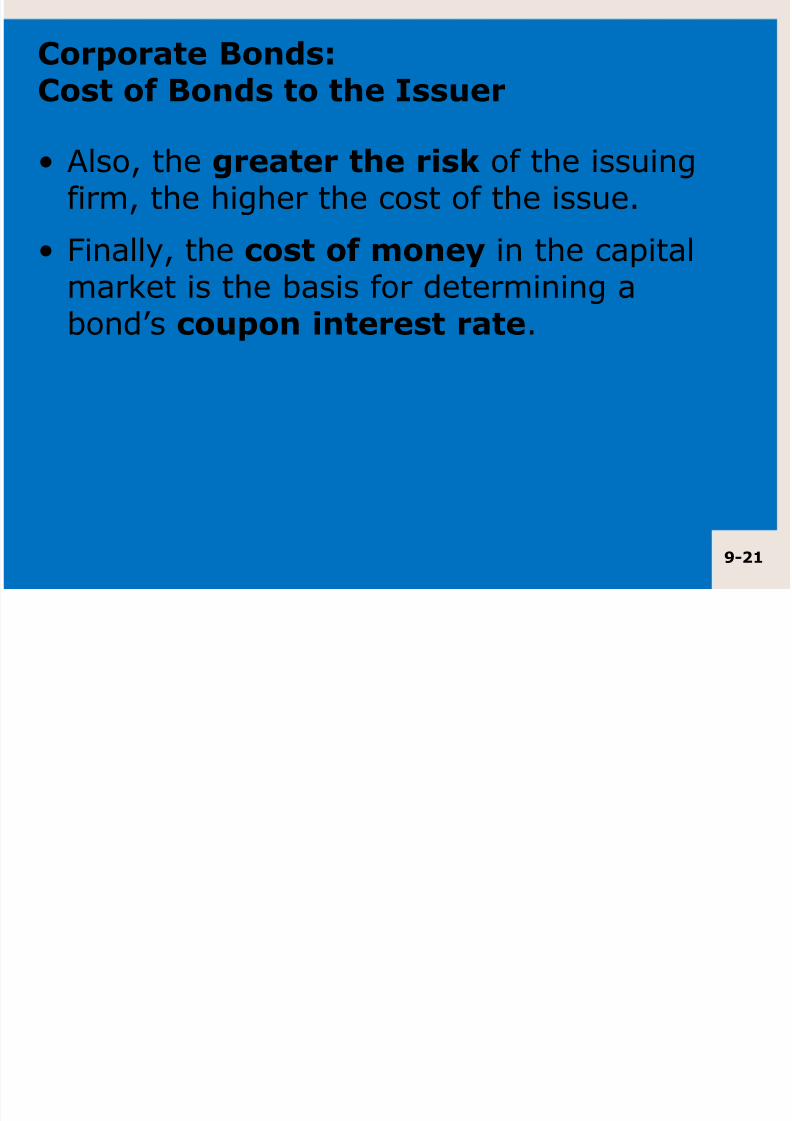

Corporate Bonds4Cost of Bonds to the Issuer

• &n general' the longer the bond5s (aturit#' thehigher the interest rate (or cost) to the firm.

• &n addition' the larger the si6e of the offering'the lower will be the cost (in terms) of the bond

since the flotation and administrative costs perpeso borrowed are likel! to decrease withincreasing offering si6e (although larger offeringsresult in greater risk of default).

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 21/47

9-21

Corporate Bonds4Cost of Bonds to the Issuer

• *lso' the greater the ris' of the issuingfirm' the higher the cost of the issue.

• /inall!' the &ost of (one# in the capital

market is the basis for determining abond$s &oupon interest rate.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 22/47

9-22

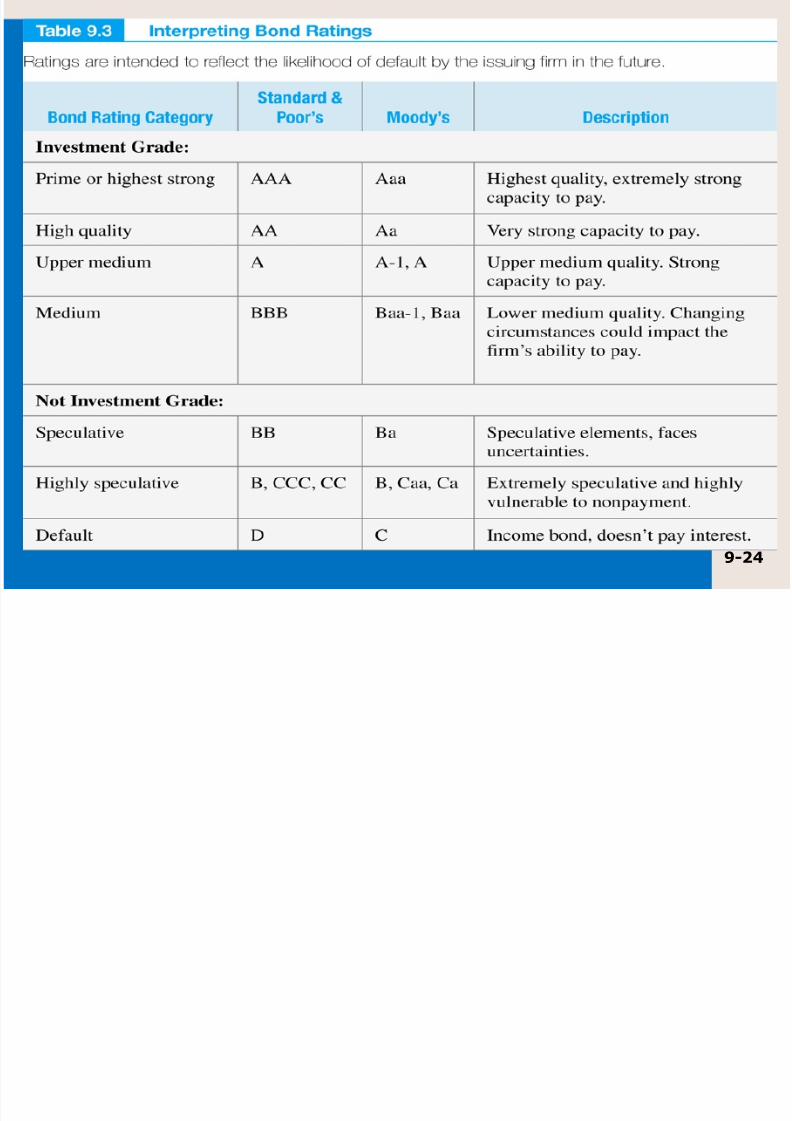

Bond Ratings and Default Ris'

• * &redit rating serves as an unbiased'independent evaluation of the creditworthiness ofa borrower.

• &t is a grading s!stem which provides an obectivemeasure of credit %ualit!' particularl! the abilit! topa! the financial obligations upon maturit!.

• * credit rating considers both the business andthe financial risks.

• 0redit ratings affect the rate of return that lendersre%uire of the firm and the firm$s cost ofborrowing.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 23/47

9-23

Bond Ratings and Default Ris'

• 0onsistent with rinciple 2 (There is a 3isk#3eturn Tradeoff)' the lower the bond rating'the higher the risk of default and higher therate of return demanded in the capital market.

• ond ratings are provided b! rating agencieslike "ood#5s7 tandard 8 $oor5s7 and %it&hInvestor ervi&es

• &n the hilippines' we have the $hilippineRating ervi&es Corporation+$hilRatings,

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 24/47

9-2

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 25/47

9-2!

$hilippine Ratings ervi&es +$hilRatings,#(bols

• The highest ratings assigned b! hil3atingsfor short#term and long#term issues are3" 1 and 3" *aa' respectivel!' while the

lowest are 3" 7 and 3" 0.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 26/47

9-2)Copyright © 2011 Pearson Prentice Hall. All rights reserved.

Valuing

Corporate Debt

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 27/47

9-2

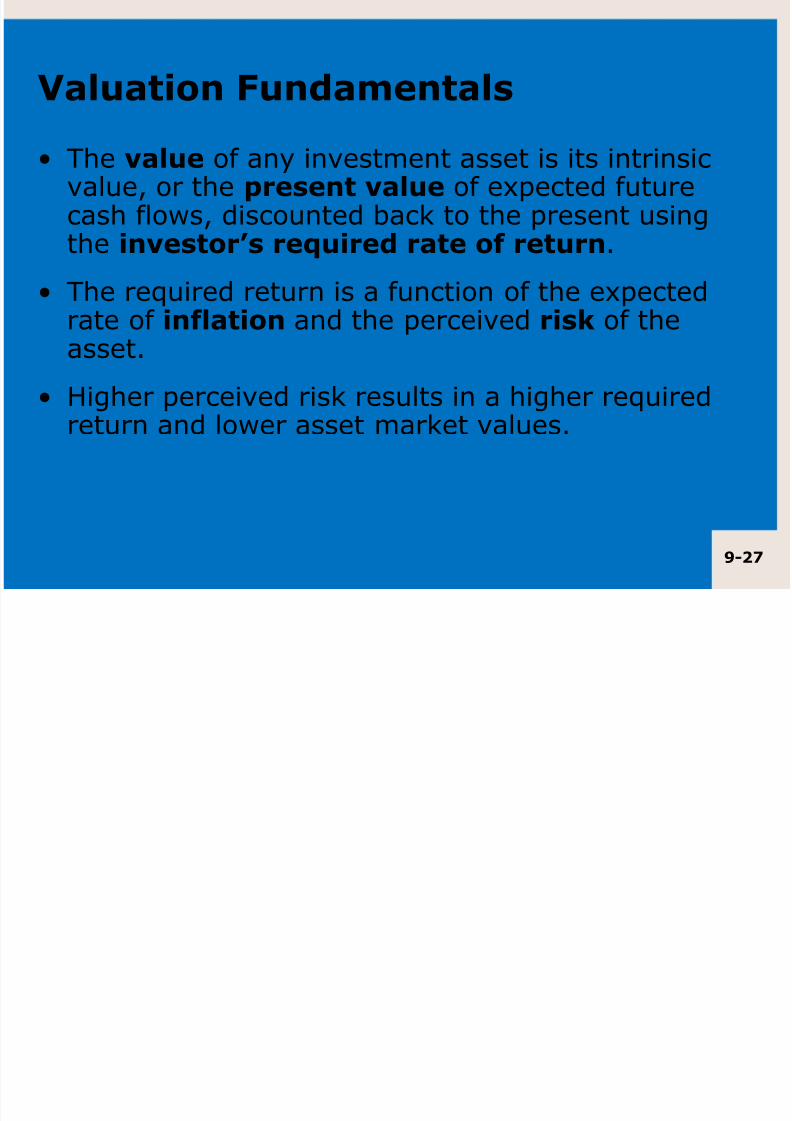

Valuation %unda(entals

• The value of an! investment asset is its intrinsicvalue' or the present value of e+pected futurecash flows' discounted back to the present usingthe investor5s reuired rate of return.

• The re%uired return is a function of the e+pectedrate of inflation and the perceived ris' of theasset.

• 8igher perceived risk results in a higher re%uired

return and lower asset market values.

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 28/47

9-2.

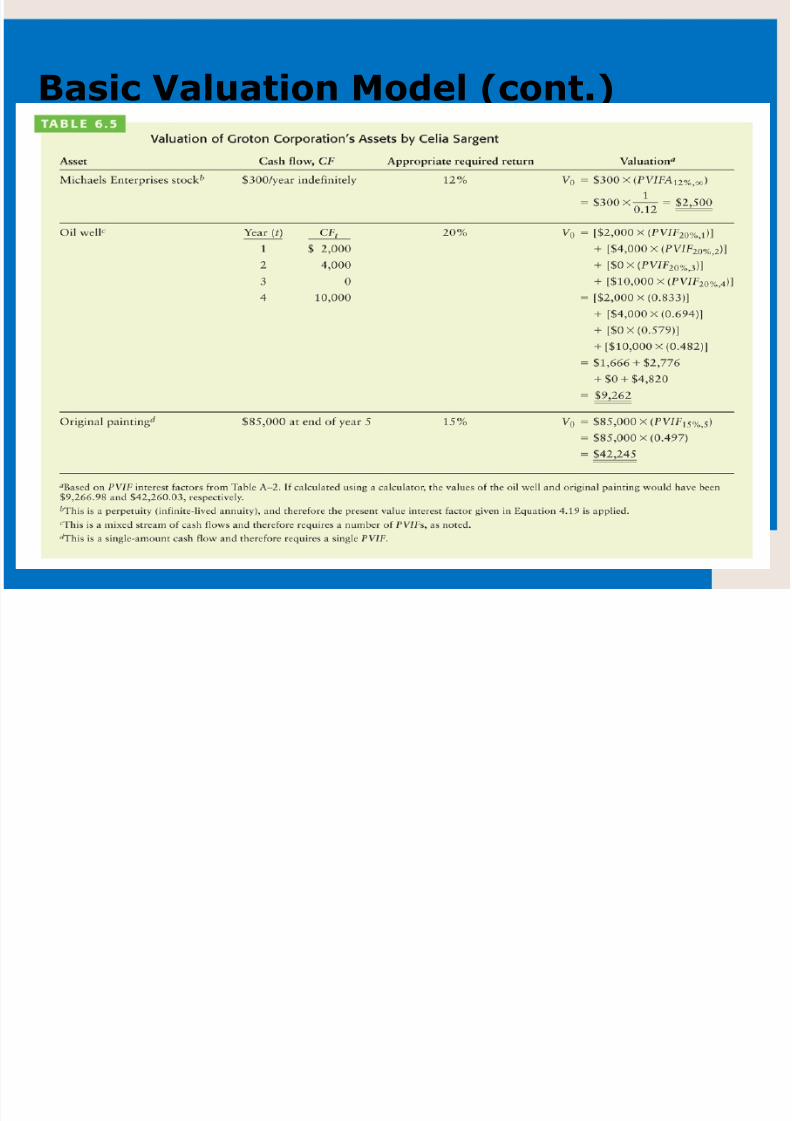

Basi& Valuation "odel

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 29/47

9-29

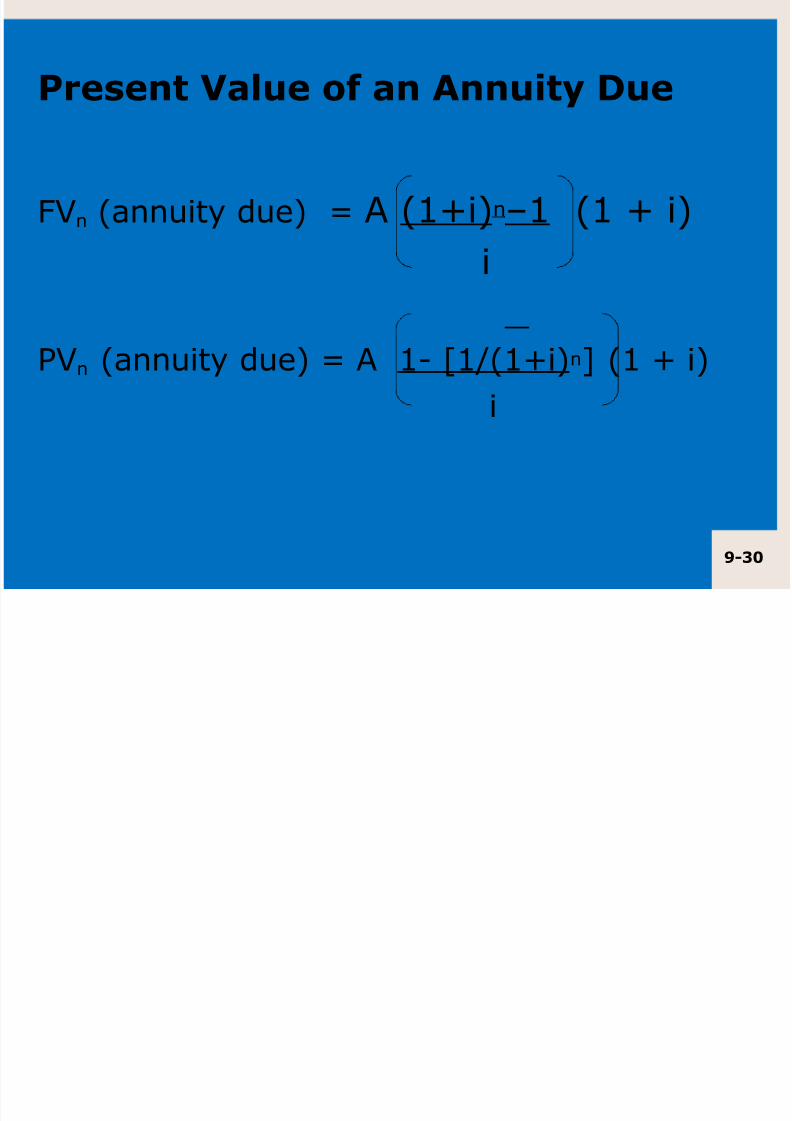

%our Basi& %or(ulas4 %uture Value and$resent Value

• FVn = PV0(1+in = PV ! (FV"Fi#n

• PV0 = FVn[1/(1+i)n] = FV x (PVIFi,n)

• FVAn = A (1+in $ 1 = A ! (FV"FAi#n

i

• PVA0 = A 1 - [1/(1+i)n] = A x (PVIFAi,n)

i

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 30/47

9-3/

$resent Value of an nnuit# Due

/n (annuit! due) - * (19i)n1 (1 9 i)

i

n (annuit! due) - * 1# 1;(19i)n< (1 9 i)

i

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 31/47

9-31

$resent Value of a $erpetuit#

of erpetuit! - * i

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 32/47

9-32

Basi& Valuation "odel +&ont,

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 33/47

9-33

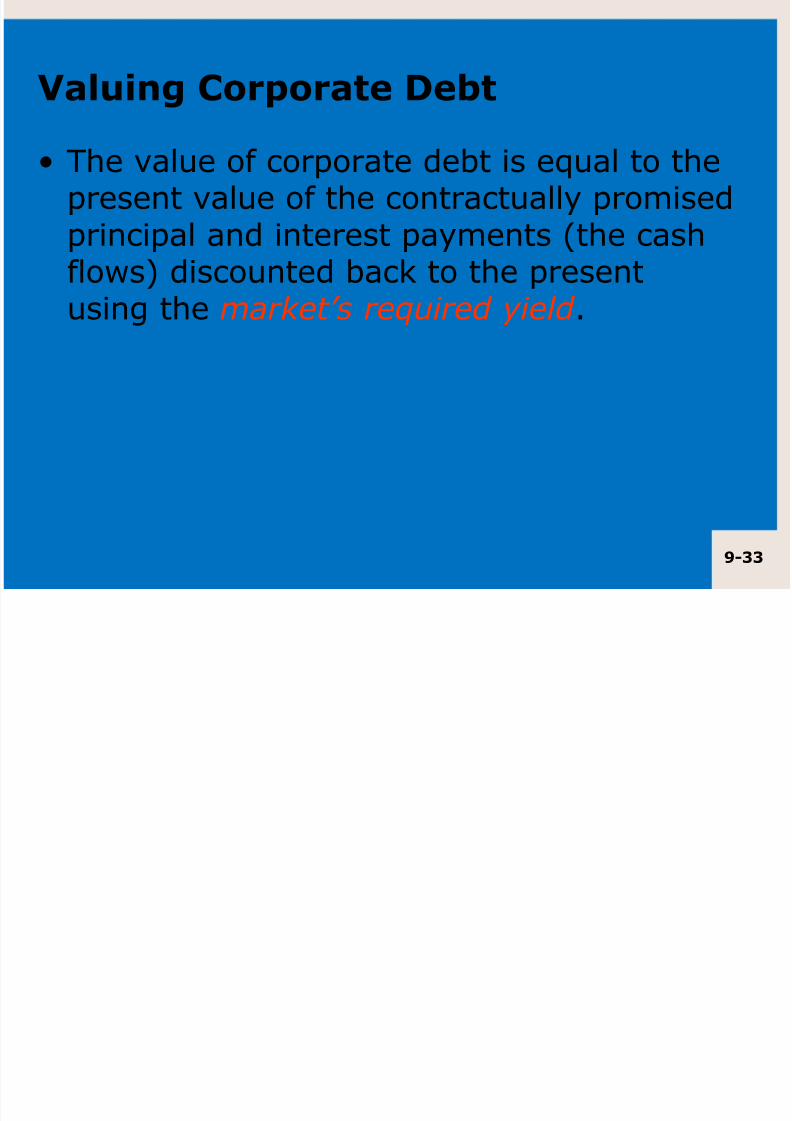

Valuing Corporate Debt

• The value of corporate debt is e%ual to thepresent value of the contractuall! promisedprincipal and interest pa!ments (the cash

flows) discounted back to the presentusing the market’s required yield .

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 34/47

9-3

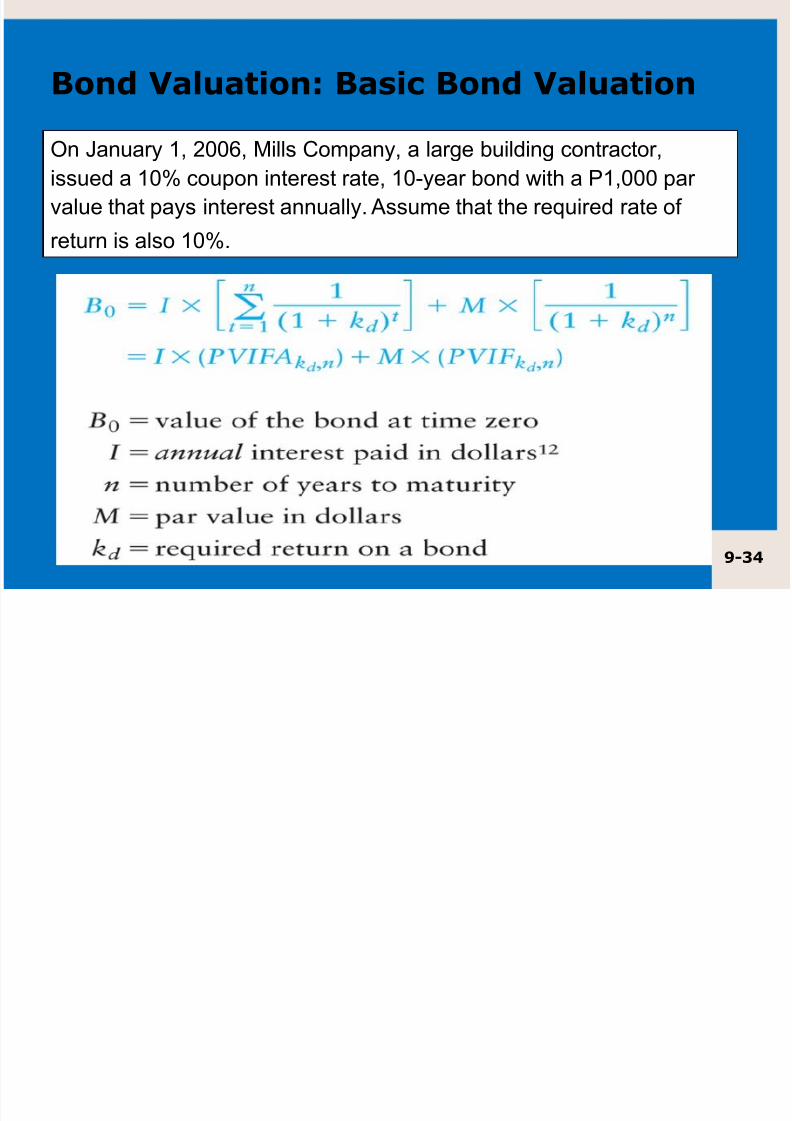

%n &an'ary 1# 200# )ills Co*pany# a large 'ilding contractor#

iss'ed a 10, co'pon interest rate# 10$year ond -ith a P1#000 par

val'e that pays interest ann'ally. Ass'*e that the re'ired rate o/

ret'rn is also 10,.

Bond Valuation4 Basi& Bond Valuation

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 35/47

9-3!

Bond Valuation4 Basi& Bond Valuation

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 36/47

9-3)

Bond Valuation4 Bond %unda(entals

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 37/47

9-3

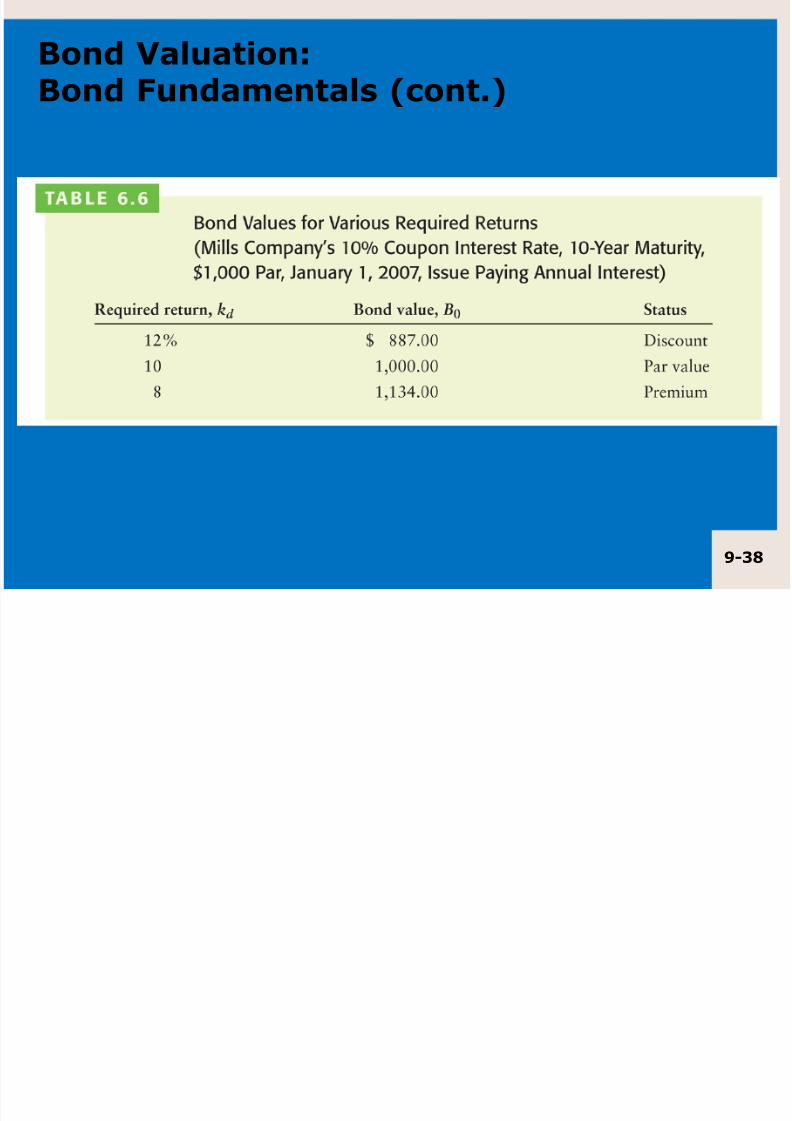

Bond Valuation4 Bond %unda(entals

Calculate the value of the bond if the required rateof return is:

• 12%

• 8%

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 38/47

9-3.

Bond Valuation4Bond %unda(entals +&ont,

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 39/47

9-39

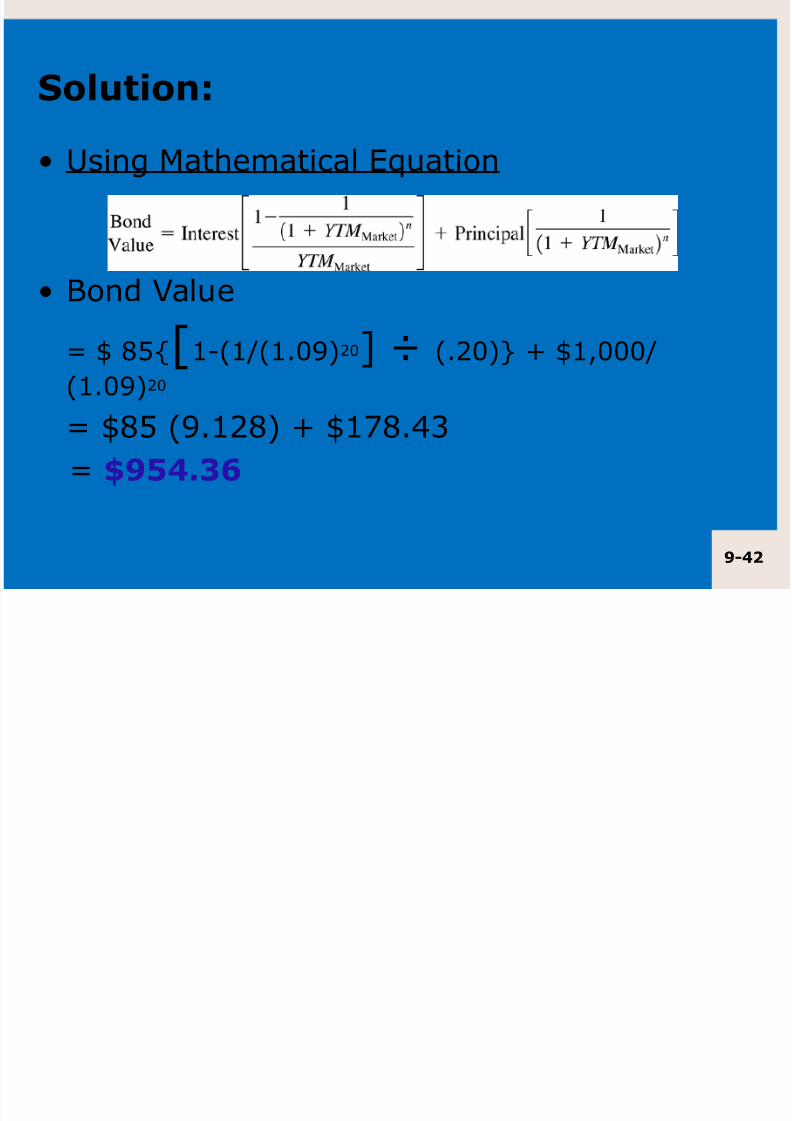

Che&'point 93 +:e0tboo' e0a(ple,

Valuing a Bond Issue

Consider a $1,000 par value bond issued by AT&T with a maturity dateof 2026 and a stated coupon rate of 8.5%. On January 1, 2007, the bondhad 20 years left to maturity, and the market$ s required yield to maturity

for similar rated debt was 7.5%. If the market$ s required yield to maturityon a comparable risk bond is 7.5%, what is the value of the bond?

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 40/47

9-/

Che&'point 93

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 41/47

9-1

Che&'point 93

0alculate the present value of the *T=Tbond should the !ield to maturit! forcomparable risk bonds rise to > (holding

all other things e%ual).

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 42/47

9-2

olution4

• ?sing 4athematical @%uation

• ond alue

- A BCD1#(1;(1.,>)2,< E (.2,)F 9 A1',,,;

(1.,>)2,

- ABC (>.12B) 9 A1GB.HI

- ;9!3)

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 43/47

9-3

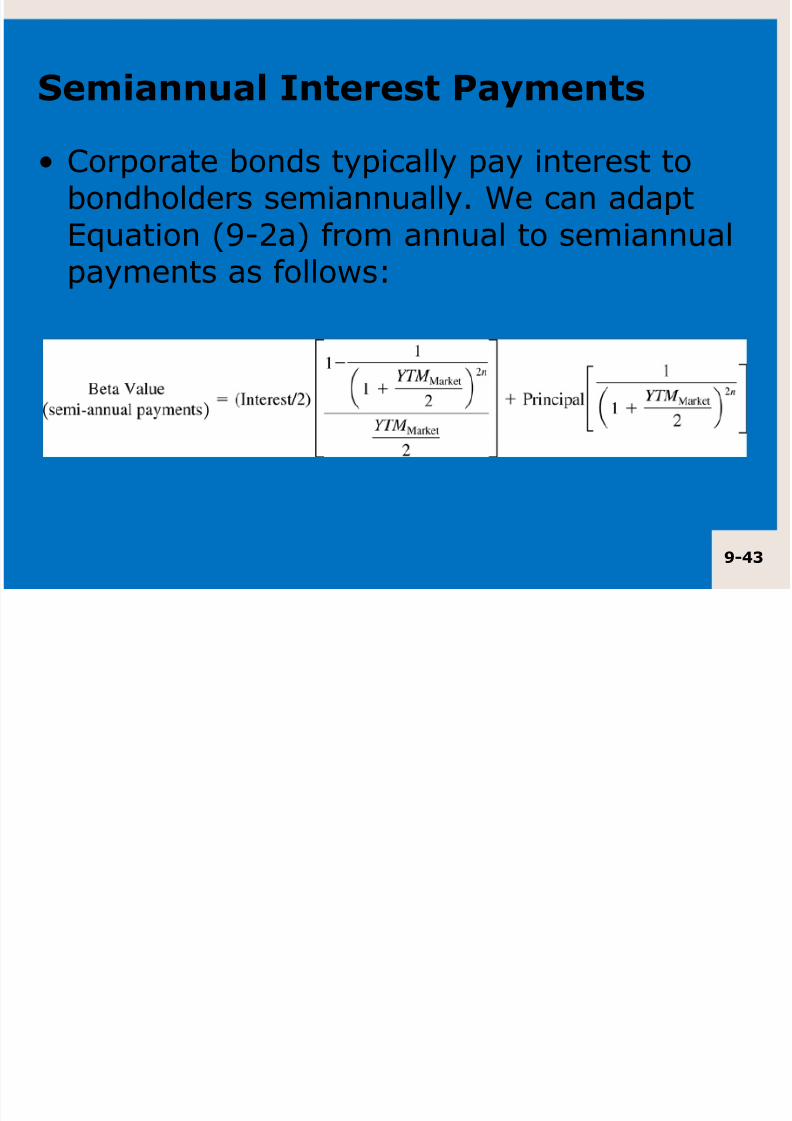

e(iannual Interest $a#(ents

• 0orporate bonds t!picall! pa! interest tobondholders semiannuall!. 5e can adapt@%uation (>#2a) from annual to semiannual

pa!ments as follows:

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 44/47

9-

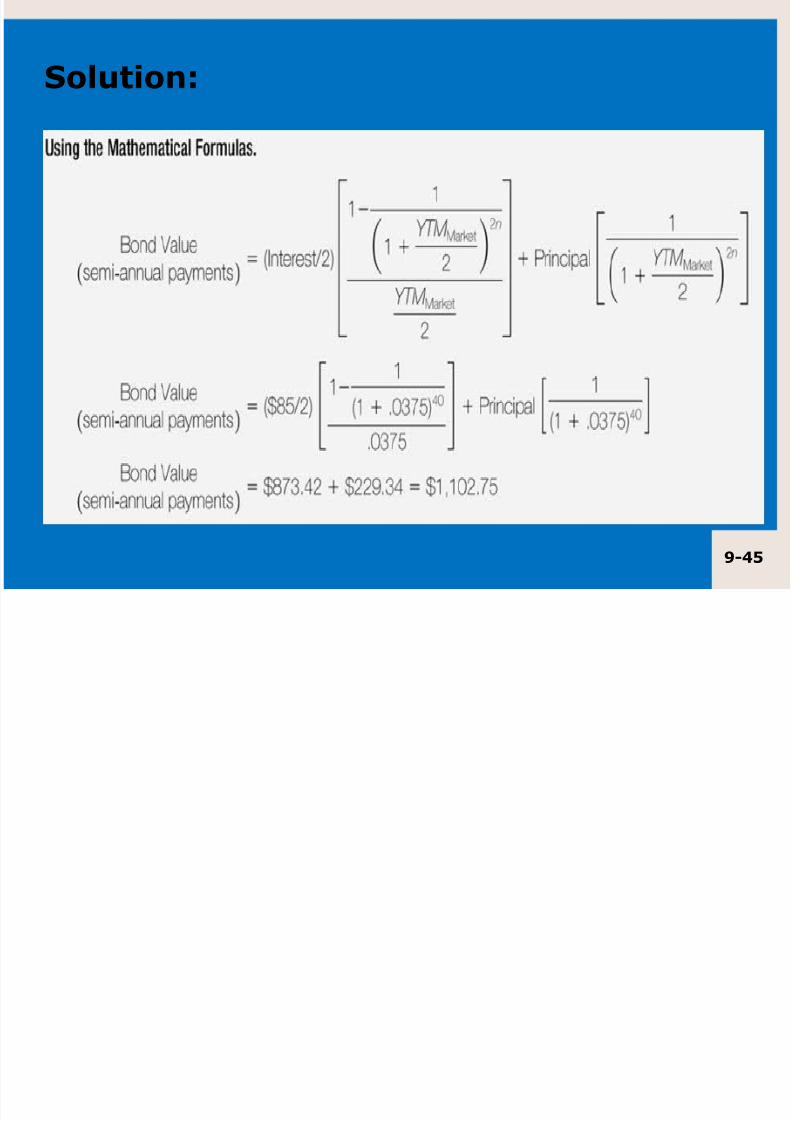

Che&'point 9 +:e0tboo' e0a(ple,

Valuing a Bond Issue :hat $a#se(iannual Interest3econsider the bond issued b! *T=T with a maturit! date of2,27 and a stated coupon rate of B.C. *T=T pa!s interest to

bondholders on a semiannual basis on Januar! 1C and Jul! 1C.Kn Januar! 1' 2,,G' the bond had 2, !ears left to maturit!. Themarket$s re%uired !ield to maturit! for a similarl! rated debtwas G.C per !ear or I.GC for si+ months. 5hat is the valueof the bond

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 45/47

9-!

olution4

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 46/47

9-)

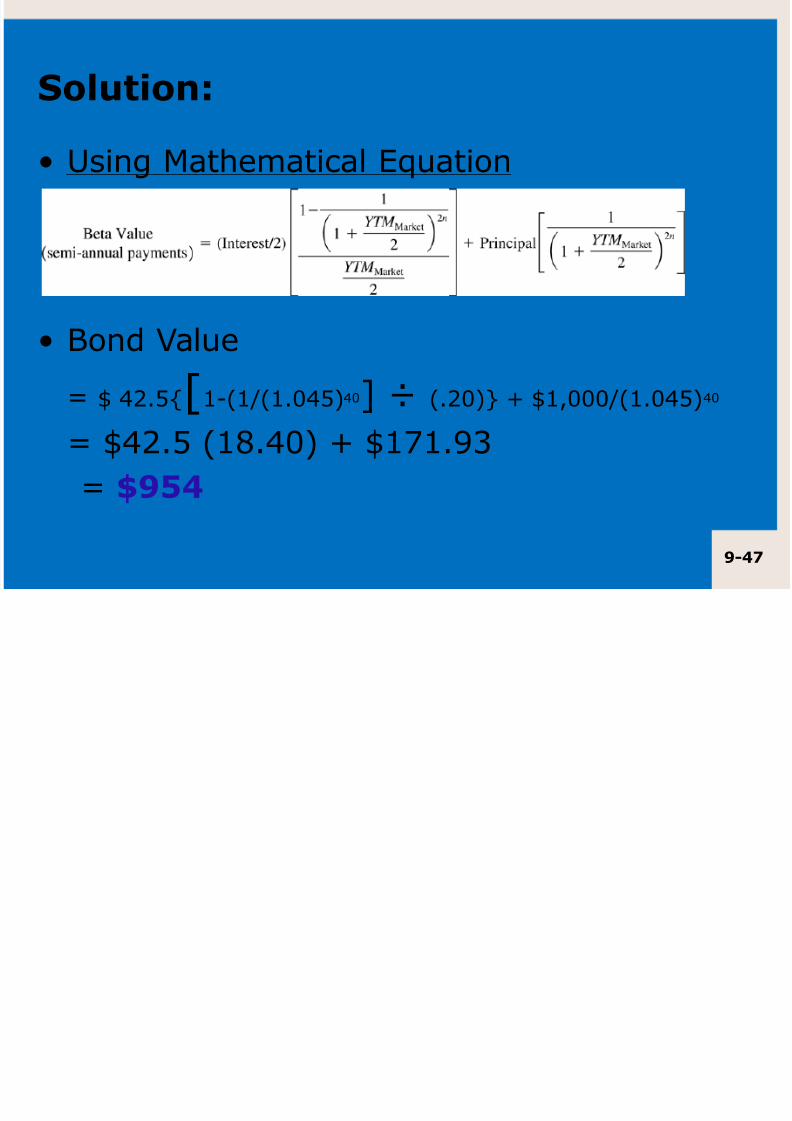

Che&'point 9

0alculate the present value of the *T=T bondshould the !ield to maturit! on comparable bondsrise to > (holding all other things e%ual).

7/18/2019 Bond Valuation

http://slidepdf.com/reader/full/bond-valuation-56970ad2f1dc1 47/47

olution4

• ?sing 4athematical @%uation

• ond alue

- A H2.CD1#(1;(1.,HC)H,< E (.2,)F 9 A1',,,;(1.,HC)H,

- AH2.C (1B.H,) 9 A1G1.>I

- ;9!