Bond Valuation

21

1 Bond Valuation Corporate Finance Dr. A. DeMaskey

-

Upload

remedios-dudley -

Category

Documents

-

view

24 -

download

0

description

Bond Valuation. Corporate Finance. Dr. A. DeMaskey. Learning Objectives. Questions to be answered: What is a bond? Who issues bonds? What are the key characteristics of bonds? How are bonds valued? What is the rate of return on a bond? What types of risk are bondholders exposed to?. - PowerPoint PPT Presentation

Transcript of Bond Valuation

1

Bond Valuation

Corporate Finance

Dr. A. DeMaskey

2

Learning Objectives

Questions to be answered: What is a bond? Who issues bonds? What are the key characteristics of bonds? How are bonds valued? What is the rate of return on a bond? What types of risk are bondholders exposed to?

3

Types of Bonds

Treasury Bonds

Corporate Bonds

Municipal Bonds

Foreign Bonds

4

Basic Terminology

Bond Par Value Coupon Interest Payment Coupon Interest Rate Maturity Date Bond’s Market Rate of Interest, kd

5

Financial Asset Valuation

PV =

CF

1+ k ... +

CF

1+k1 n

12

21

CF

kn .

0 1 2 nk

CF1 CFnCF2Value

...

+ ++

6

Required Rate of Return

The discount rate (ki) is the opportunity cost of capital, i.e., the rate that could be earned on alternative investments of equal risk.

ki = k* + IP + LP + MRP + DRP

7

Default Risk

Risk that issuer will not make interest or principal payments. Increases required rate of return Bond ratings provide one measure of

default risk Defaulting on bonds may result in

bankruptcy and/or reorganization

8

V

k kB

d d

$100 $1,

1

000

11 10 10 . . . +

$100

1+ kd

100 100

0 1 2 1010%

100 + 1,000V = ?

...

= $90.91 + . . . + $38.55 + $385.54= $1,000.

++++

Value of Bond

9

Annual Coupon Bonds

Nd

N

tt

d

B

k

M

k

INTV

111

10

Semiannual Coupon Bonds

Multiply years by 2 to get periods = 2n. Divide nominal rate by 2 to get periodic

rate = kd/2.

Divide annual INT by 2 to get PMT = INT/2.

Nd

N

tt

d

B

k

M

k

INTV 2

2

1 2/12/1

2/

11

General Observations About Bond Values

If coupon rate < kd, bond sells at a discount.

If coupon rate > kd, bond sells at a premium.

If coupon rate = kd, bond sells at its par value.

If kd rises, price falls; if kd falls, price rises.

At maturity, the value of a bond equals par.

12

Changes in Bond Values Over Time

At maturity, the value of any bond must equal its par value.

The value of a premium bond would decrease to $1,000.

The value of a discount bond would increase to $1,000.

A par bond stays at $1,000 if kd remains constant.

13

M

Bond Value ($)

Years remaining to Maturity

1,372

1,211

1,000

837

775

30 25 20 15 10 5 0

kd = 7%.

kd = 13%.

kd = 10%.

Time Path of Bond Value

14

Bond Yields

Yield-to-Maturity (YTM)

Effective Annual Return on Bond

Yield-to-Call

Current Yield

15

Yield-to-Maturity

YTM is the rate of return earned on a bond held to maturity, also called “promised yield.”

It is the discount rate that equates the present value of the interest and principal payments to the price of the bond. Annualized YTM = 2 x six-month yield Effective YTM = (1 + six-month yield)2 - 1

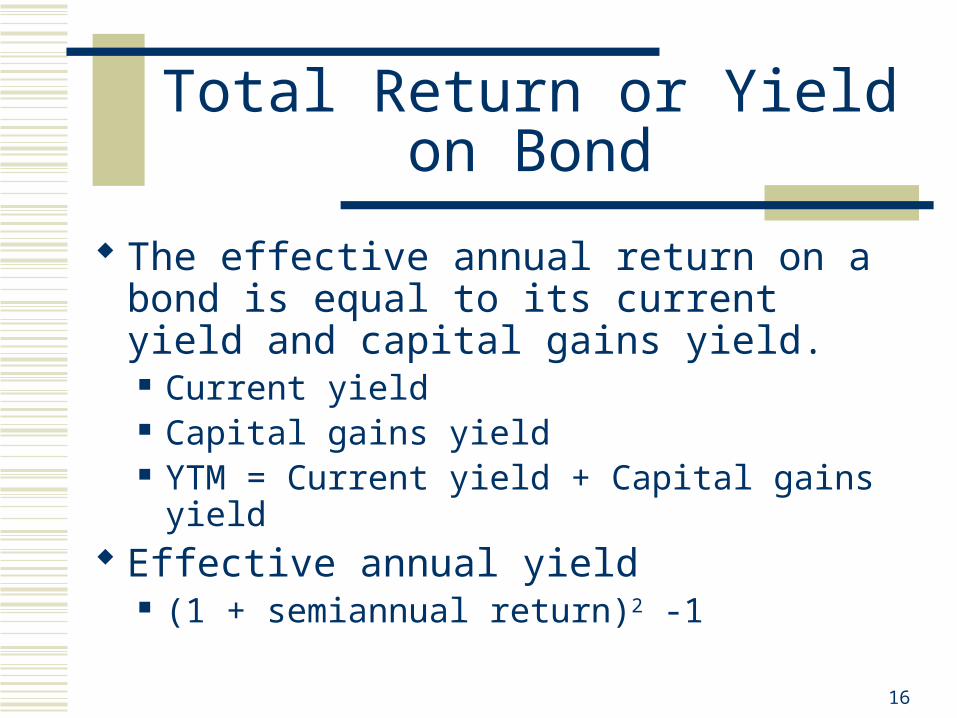

16

Total Return or Yield on Bond

The effective annual return on a bond is equal to its current yield and capital gains yield. Current yield Capital gains yield YTM = Current yield + Capital gains yield

Effective annual yield (1 + semiannual return)2 -1

17

Yield-to-Call

Call Provision Callable bonds Call premium Refunding operation

YTC is the average annual return an investor will receive if the bond is held until its expected call date.

18

Current Yield

Annual interest payment/Current value of bond

Provides information about cash income on bond.

Does not provide accurate measure of total expected return on bond.

19

kd 1-year Change 10-year Change

5% $1,048 $1,386

10% 1,000 4.8% 1,000 38.6%

15% 956 4.4% 749 25.1%

Interest Rate Risk

Rising interest rates have an adverse effect on bond values.

The longer the maturity of a bond, the greater the exposure to interest rate risk.

20

0

500

1,000

1,500

0% 5% 10% 15%

1-year

10-year

kd

Value

Interest Rate Risk

21

Reinvestment Rate Risk

The risk that CFs will have to be reinvested in the future at lower rates, reducing income.

The shorter the maturity of the bond, the greater the risk of a decrease in interest rates.