Big G - Brandeis University

112

Big G * Lydia Cox † , Gernot J. M¨ uller ‡ , Ernesto Pasten § , Raphael Schoenle ¶ , and Michael Weber June 14, 2021 Abstract “Big G” typically refers to aggregate government spending on a homogeneous good. In this paper, we open up this construct by analyzing the entire universe of procurement contracts of the U.S. federal government and establish five facts. First, government spending is granular; that is, it is concentrated in relatively few firms and sectors. Second, relative to private spending its composition is biased. Third, at the contract, firm and sectoral level moderate persistence characterizes spending. Fourth, idiosyncratic variation dominates fluctuations in spending. Last, government spending is concentrated in sectors with relatively sticky prices. Accounting for these facts within a stylized New Keynesian model offers new insights into the fiscal transmission mechanism and aligns the model predictions with the empirical evidence: Fiscal shocks hardly impact inflation, little crowding out of private expenditure occurs, markups can be either pro-cyclical or counter-cyclical, and the multiplier tends to be larger compared to a one-sector benchmark. Keywords: Government spending, federal procurement, granularity, sectoral heterogeneity, fiscal policy transmission, monetary policy JEL Classification: E62, E32 * We acknowledge outstanding research assistance by Jiacheng Feng. We thank Klaus Adam, Regis Barnichon, Christian Bayer, Benjamin Born, Gabriel Chodorow-Reich, Zeno Enders, Emmanuel Farhi, Xavier Gabaix, Yuriy Gorodnichenko, Edward Knotek, Valerie Ramey, Ludwig Straub and conference and seminar participants at the Banco Central de Chile Heterogeneity in Macroeconomics Conference, Federal Reserve Banks of Boston and Cleveland, the NBER Monetary Economics Meeting, PUC Santiago, the University of Tuebingen, and the VfS Monetary Meeting Frankfurt for valuable comments. Weber also thanks the Fama-Miller Center and the Fama Research Fund at the University of Chicago Booth School of Business for financial support. Schoenle and Weber also gratefully acknowledge support from the National Science Foundation under grant number 1756997. The views expressed herein are solely those of the authors and do not necessarily reflect the views of the Central Bank of Chile, the Federal Reserve Bank of Cleveland or the Federal Reserve System. † Harvard University. e-Mail: [email protected]. ‡ University of T¨ ubingen and CEPR. e-Mail: [email protected]. § Central Bank of Chile and Toulouse School of Economics. e-Mail: [email protected]. ¶ Brandeis University, Cleveland Fed, and CEPR. e-Mail: [email protected]. Booth School of Business, University of Chicago and NBER. e-Mail: [email protected].

Transcript of Big G - Brandeis University

Big G∗

Lydia Cox†, Gernot J. Muller‡, Ernesto Pasten§,Raphael Schoenle¶, and Michael Weber‖

June 14, 2021

Abstract

“Big G” typically refers to aggregate government spending on a homogeneous good. In thispaper, we open up this construct by analyzing the entire universe of procurement contracts ofthe U.S. federal government and establish five facts. First, government spending is granular;that is, it is concentrated in relatively few firms and sectors. Second, relative to privatespending its composition is biased. Third, at the contract, firm and sectoral level moderatepersistence characterizes spending. Fourth, idiosyncratic variation dominates fluctuationsin spending. Last, government spending is concentrated in sectors with relatively stickyprices. Accounting for these facts within a stylized New Keynesian model offers new insightsinto the fiscal transmission mechanism and aligns the model predictions with the empiricalevidence: Fiscal shocks hardly impact inflation, little crowding out of private expenditureoccurs, markups can be either pro-cyclical or counter-cyclical, and the multiplier tends to belarger compared to a one-sector benchmark.

Keywords: Government spending, federal procurement, granularity, sectoral heterogeneity,fiscal policy transmission, monetary policy

JEL Classification: E62, E32

∗We acknowledge outstanding research assistance by Jiacheng Feng. We thank Klaus Adam, Regis Barnichon,Christian Bayer, Benjamin Born, Gabriel Chodorow-Reich, Zeno Enders, Emmanuel Farhi, Xavier Gabaix, YuriyGorodnichenko, Edward Knotek, Valerie Ramey, Ludwig Straub and conference and seminar participants at theBanco Central de Chile Heterogeneity in Macroeconomics Conference, Federal Reserve Banks of Boston andCleveland, the NBER Monetary Economics Meeting, PUC Santiago, the University of Tuebingen, and the VfSMonetary Meeting Frankfurt for valuable comments. Weber also thanks the Fama-Miller Center and the FamaResearch Fund at the University of Chicago Booth School of Business for financial support. Schoenle and Weberalso gratefully acknowledge support from the National Science Foundation under grant number 1756997. Theviews expressed herein are solely those of the authors and do not necessarily reflect the views of the Central Bankof Chile, the Federal Reserve Bank of Cleveland or the Federal Reserve System.

†Harvard University. e-Mail: [email protected].‡University of Tubingen and CEPR. e-Mail: [email protected].§Central Bank of Chile and Toulouse School of Economics. e-Mail: [email protected].¶Brandeis University, Cleveland Fed, and CEPR. e-Mail: [email protected].‖Booth School of Business, University of Chicago and NBER. e-Mail: [email protected].

1 Introduction

What is “Big G”? In the national accounts, G represents government spending—the part of

GDP that comprises government consumption of goods and services plus investment.1 This

convention possibly helps explain why research on fiscal policy typically entertains a somewhat

crude notion of government spending as spending on a homogeneous good, isomorphic to GDP.

In empirical and theoretical work, we frequently refer to it as G, and the literature assumes

policymakers can freely adjust it over time. The recent “renaissance of fiscal research” surveyed

by Ramey (2019) has changed little in this regard. A number of recent papers have started

to study the role of heterogeneity for the fiscal transmission mechanism but focus exclusively

on heterogeneity on the household side (McKay and Reis, 2016; Auclert et al., 2018; Hagedorn

et al., 2019).

The starting point of our paper is the observation that government spending itself is

fundamentally heterogeneous. Government spending is not simply one large transaction. It

is composed of a large number of smaller transactions whose composition differs from the other

components of aggregate demand. We first establish five facts about government spending and

then reassess the fiscal transmission mechanism through the lens of a simple two-sector New

Keynesian model, which captures all five facts in a stylized way. Allowing for heterogeneity of

government spending has first-order effects on the transmission mechanism, aligning the model

prediction with the empirical evidence.

Our empirical anatomy of government spending relies on a database that has only recently

become accessible: USASpending.gov. The database provides detailed information on the entire

universe of procurement contracts by the federal government since 2001.2 For each year, the

database records several million government procurement transactions. While the database does

not cover all components of government spending, it is unique in detail and scope: it covers 40

percent of total federal spending, and 16 percent of general government spending. The facts

1Throughout, we refer to government spending even though our data does not cover government employment.Note that government spending does not include transfer payments. For details, see Figure 1.

2Data on government contracts go back further, see https://www.archives.gov/research/

electronic-records/reference-report/federal-contracts. The data, however, largely covers defensecontracts, and the data are not as comprehensive as USASpending.gov. Earlier work uses procurement data bythe Department of Defense to estimate fiscal multipliers or the effects of government spending shocks (Fisherand Peters, 2010; Nakamura and Steinsson, 2014; Dupor and Guerrero, 2017; Demyanyk et al., 2019; Auerbachet al., 2020). Hebous and Zimmermann (2021) use the data to study the effect of federal purchases on firminvestment. The data set has also been studied in other contexts: e.g. Decarolis et al. (2020) assess the impactof bureaucratic competence on procurement outcomes. Appendix A.2 provides additional details.

1

we document hold equally for procurement contracts of the Department of Defense (DOD) and

non-DOD procurement, the latter of which has not been studied in detail due to data limitations.

Our most important facts also extend to state and local spending, which account for another

21 percent of general government spending. In contrast to the existing literature, we focus on

heterogeneity, in particular on differences in government spending across contracts, firms and

sectors; differences relative to private spending; and differences in pricing frictions. Limited

availability of micro data precludes us from extending our analysis to government employment

and wages. The existing literature guides us in the choice of the dimension of heterogeneity we

study, such as the persistence of government spending or pricing frictions.

Our first fact is that government spending is granular in the sense of Gabaix (2011): it

is concentrated among few firms and sectors. For instance, the largest ten suppliers in terms

of average annual contract value receive over a third of government contract spending and

are concentrated in a few sectors. Firms in the largest three two-digit NAICS industries are

counter-party for more than 60 percent of all government contracts. Concentration in defense

and non-defense spending is similar, and it is equally pervasive at the state and local levels.

The second fact is a sectoral bias in government spending: the allocation of government

spending across sectors differs substantially from that of private spending. For instance, the

sector with the largest share in total government spending (manufacturing) receives 30 percent

of government spending, but accounts for only 13 percent of GDP. Conversely, the sector with

the largest share in GDP (health care and social assistance) accounts for 12 percent of GDP but

less than 2 percent of government contract spending. Again, this fact holds not only for federal

spending, but also for state and local government spending.3

Third, we study the persistence of government spending because of its key role for the

fiscal transmission mechanism (Baxter and King, 1993). We find only moderate persistence

of government spending at the contract, firm, and sectoral level. The median contract has a

duration of 31 days and 90 percent of contracts last less than one year. Moreover, the turnover

of firms which are counter-party to the government is large. The median firm is in the data

3In earlier work, Ramey and Shapiro (1998) stress the sectoral bias of military buildups—World War II,the Korean War, the Vietnam War, and the Carter-Reagan buildup—as well as the 1950s construction of theU.S. highway system and the rise of federal medical spending. They then explore its implication for the fiscaltransmission in a neoclassical two-sector model. We build on their work but use more disaggregated and recentdata, and we document the bias for the universe of spending. Most importantly, we focus on variation at thebusiness-cycle frequency rather than on long swings in spending mainly due to military spending. Also, in ourtheoretical analysis, we depart from their framework and show that sectoral bias interacts with price stickiness inways which fundamentally alter the fiscal transmission mechanism.

2

for less than two years, while the firm with the median value of average annual contracts is in

the data for less than one year. At the sectoral level, we fit AR(1) processes to the data to

measure persistence and to facilitate a mapping of our data into business cycle models. The

average monthly persistence parameter is 0.42. However, in line with the political economy

of government spending, government contracts tend to spike in September.4 If we filter out

such seasonality, persistence estimates can increase substantially, up to the level that implies a

half-life of government spending processes in line with those implied by estimated VAR models.

Fourth, at business cycle frequency, idiosyncratic variation of a few influential firms and

sectors accounts for the growth of aggregate government spending. To establish this fact, we

construct the granular residual of government spending following the approach of Gabaix (2011)

and find that it explains almost 40 percent of monthly variation in aggregate government

spending growth. An alternative approach based on a decomposition of spending growth

following Foerster et al. (2011) yields similar results. While our second fact shows high

concentration of government spending in the cross-section, this fourth fact shows concentration

over time in government spending growth.

Fifth, government spending tends to be concentrated in sectors with high degrees of price

stickiness—a key modeling feature for the fiscal transmission mechanism in the New Keynesian

literature. We find that the monthly frequency of price changes in the top three two-digit

NAICS sectors that supply goods to the government is 11 percent while it is 22 percent, on

average, for the remaining sectors. In contrast, the average frequency in the top three sectors

for private consumption is 17 percent. These frequencies are estimated on the basis of the micro

data underlying the producer price index (PPI) at the Bureau of Labor Statistics (BLS), but

we document the duration of contracts in the USASpending.gov data and their pricing nature

are consistent with these estimates.

In isolation and one-by-one, these facts may not appear surprising, but so far no systematic

documentation exists. We also show that accounting for heterogeneity of government spending

in terms of our five facts has first-order effects on the fiscal transmission mechanism. To do

so, we develop a two-sector New Keynesian model with government spending. The model is

deliberately stylized in order to account for the five facts in a transparent way while minimally

departing from the conventional one-sector model (e.g. Woodford, 2011). Importantly, rather

4This seasonality suggests part of government spending is predictable. We do not pursue further quantificationbut potential anticipation of fiscal shocks has been a major theme of the empirical literature on the fiscal multiplier(Ramey, 2011; Leeper et al., 2013).

3

than postulating a driving process for G, as is commonly done, we instead model government

spending at the sectoral level—in line with fact 4.5

In our analysis, we establish a number of results, both in closed form based on limiting

cases, and quantitatively based on model simulations. We show analytically that unlike in

a one-sector model, crowding out of private expenditure can be infinite and the government

spending multiplier negative if government spending increases in a sector in which prices are

fully flexible while prices are sticky in the other sector. However, a fiscal shock in the relatively

small and sticky-price sector, toward which government spending is biased in the data (facts 1,

2 and 5), induces a fiscal multiplier that is three to four times larger than what we observe for

the one-sector benchmark. Moreover, we find the multiplier is larger the more flexible prices are

in the sector in which private spending is concentrated. Hence, it is not the overall degree of

price stickiness in the economy that determines the size of the multiplier; instead the multiplier

increases in the relative stickiness in the sector in which government spending increases. This

result is in line with the finding that the relative extent of frictions is key for aggregate dynamics

in multi-sector economies (Barsky et al., 2007, 2016; Gilchrist et al., 2017).

The intuition for these findings follows from the interaction of our heterogeneous model

features and monetary policy, which is key for the fiscal transmission mechanism in the New

Keynesian model (Woodford, 2011; Christiano et al., 2011; Farhi and Werning, 2016). In this

model, because government spending is inflationary, it induces the central bank to raise interest

rates, and private spending is crowded out due to intertemporal substitution. A number of

recent contributions show that household heterogeneity and credit frictions limit intertemporal

substitution and instead make the model more “old Keynesian” (Galı et al., 2007; McKay

et al., 2016; Kaplan et al., 2018). Sectoral bias in government spending combined with sectoral

heterogeneity in pricing frictions has a similar effect. In a nutshell, if the government spends in

relatively sticky-price sectors compared to the private sector, monetary policy needs to respond

less (via higher interest rates) to a fiscal stimulus in order to keep inflation stable. Hence,

less crowding out occurs, rendering the multiplier larger. These effects become stronger, the

larger the sectoral bias, because in this case, more private spending is concentrated in the

relatively flexible-price sector. Following a given interest rate increase, private consumption

prices fall endogenously and strongly in this sector, stabilizing overall prices and requiring a

smaller contractionary interest rate increase.

5Our empirical analysis documents several facts in more detail than what we model. These additional detailsmay provide further guidance to modelers and policymakers.

4

Importantly, such a muted impact of fiscal shocks on inflation and interest rates is also

consistent with empirical observations from fiscal VARs (Mountford and Uhlig, 2009; Corsetti

et al., 2012; Ramey, 2016). Likewise, a muted response of inflation also means the fiscal multiplier

at the zero lower bound is not much larger compared to the baseline case due to a muted real rate

response, in line with recent evidence by Ramey and Zubairy (2018). Moreover, we show that

accounting for the heterogeneity of government spending across sectors goes some way towards

accounting for the response of markups to government spending shocks for which the one-sector

model delivers counterfactual predictions (Nekarda and Ramey, 2020). In sum, once we modify

the model to account for the heterogeneity that characterizes spending data at the micro level,

the model performance also improves at the macro level.

Our paper is also related to recent work on the effect of regional fiscal policies in monetary

unions (Galı and Monacelli, 2008; Acconcia et al., 2014; Nakamura and Steinsson, 2014;

Blanchard et al., 2017; Hettig and Muller, 2018).6 In this literature, government spending is

concentrated in some spatial partition of the economy, and its composition is biased relative to

the composition of private spending. In contrast to this earlier work, we model private spending

as being determined at the sectoral level rather than at the regional level.

We also share modeling features with a number of recent papers that account for

heterogeneity on the production side across sectors and firms, tracing out the implications for

business cycle fluctuations.7 Bouakez et al. (2020), in particular, study in contemporaneous

work the transmission of fiscal policy shocks in a two-sector network economy. Their analytical

work focuses on the role of networks in a real economy, whereas we emphasize the interaction of

monetary policy, sectoral bias and pricing frictions. Lastly, Woodford (2020) also investigates

sectoral fiscal policy, notably in the presence of demand failures, but his focus is on transfers

rather than on government spending.

2 Data

In the first part of this paper we present a detailed analysis of the USASpending.gov database.

We document the defining characteristics of government spending for macroeconomic modeling,

6Chodorow-Reich (2019) surveys recent empirical work on government spending multipliers based on cross-sectional data.

7Some recent contributions to this fast-growing literature include Acemoglu et al. (2012); Pasten et al.(2019a,b); Baqaee and Farhi (2020); La’O and Tahbaz-Salehi (2020); Bigio and La’o (2020); Ozdagli and Weber(2017); Rubbo (2020); Carvalho et al. (2021).

5

such as the size distribution of recipient firms and sectors and heterogeneity in price rigidity

across firms. We begin by describing how our data fit into the portion of GDP that comprises

the government sector overall, “Big G.” We then detail and define several fundamental concepts

before we analyze the data.

2.1 Background on USASpending

The database we use, USASpending.gov, was created in response to the Federal Funding

Accountability and Transparency Act (FFATA), which was signed into law on September 26,

2006. FFATA requires federal contract, grant, loan, and other financial assistance awards of

more than $25,000 to be publicly accessible on a searchable website, in an effort to provide

transparency to the American people on how the government spends their tax dollars. In

accordance with FFATA, federal agencies are required to collect and report data on federal

procurement. Agencies must report award data on a monthly basis through various government

systems such as the Federal Procurement Data System (FPDS-NG) for contract data and the

Data Act Broker for grant, loan, and other financial assistance data. The USASpending.gov

database, which the Treasury Department hosts, compiles the data from the various government

reporting systems. In addition to directly uploading the information that the federal agencies

report to systems like the FPDS-NG, the site also uses information collected from the recipients

of the awards themselves. Though FFATA was not signed into law until 2006, data are available

going back to 2001 through an external organization. Limited, less easily accessible contract

data are available even before 2001 through the National Archives,8 but are not comprehensive

enough for our purpose.

2.2 A Bird’s Eye View of the Data

We provide a schematic diagram of total government spending in Panel A. of Figure 1 to illustrate

which part of government spending our data cover. Total government spending consists of

government consumption expenditures (CE) and gross investment (GI). CE in turn consists of

spending by the government to produce and provide services to the public, such as national

defense and public school education. GI consists of spending by the government for fixed

assets that directly benefit the public, like highways, or that assist government agencies in

their production activities, such as purchases of military hardware. General government CE

8See https://www.archives.gov/research/electronic-records/reference-report/federal-contracts.

6

Figure 1: The Big Picture

A. Categories of G B. Contracts vs. National Accounts

100

200

300

400

500

600

Bill

ion

Dol

lars

2001 2003 2005 2007 2009 2011 2013 2015 2017

TotalDefenseNon−DefenseContractsNational Accounts

Notes: Contract data in USAspending.gov in Panel A. represent the categories “Purchases of intermediate goods andservices” as well as “Structures, equipment, and Software”. We use data from the BEA 2002 Make and Use Tables tocharacterize government spending at the state and local level (Facts 1 and 2). Panel B.: solid lines show actual contractspending from USASpending, dashed lines show the corresponding components of government spending in the nationalaccounts (federal purchases of intermediate goods and services and federal non-R&D investment), both in the full sample,as well as separately for defense and non-defense.

and GI include both federal spending (about 40 percent) and state and local spending (about

60 percent).

The figure further illustrates that government CE is equal to gross output of the government,

less own-account investment (which is included in gross government investment) and sales to

other sectors (recorded in the private sector). CE of the federal government is made up of two

components: value added (compensation of general government employees and consumption of

fixed capital) and government purchases of intermediate goods and services. GI is a measure of

the additions to, and replacements of the stock of government-owned fixed assets. It consists of

investment by both general government and government enterprises in structures (e.g., highways

and schools), equipment (e.g., military hardware), and intellectual property products (software

and R&D). It also includes own-account investment.

When we analyze government spending, our focus is on federal government procurement

contracts that include, at the federal level, both purchases of intermediate goods and services,

as well as investment in structures, equipment, and software. We highlight both components

in red in Panel A. of Figure 1. Our data do not include state or local government spending,

7

but using detailed BEA input-output tables for the year 2002 we verify that several of our key

facts characterize state and local data as well.9 Additionally, our contracts data do not include

compensation of government employees (note, they may include compensation for contractors)

or consumption of fixed capital. Also, most government investment in R&D comes through

grants, so it is also not included in the contracts data. Hence, our procurement contracts is

approximately equal to:

Contract Spending = CE + GI− (Value Added + R&D Investment)

= Intermediate Goods & Services Purchased + Non-R&D Investment

Panel B. of Figure 1 shows that contract spending closely aligns with the relevant portion

of government spending from the National Income and Product Accounts (NIPA). Solid lines in

the figure represent our data while dashed lines represent the relevant NIPA data. Moreover,

the match is equally good for both defense (medium-light blue lines) and non-defense (light

blue lines) spending. On average, our federal contracts data represent about 16 percent of total

government spending and 40 percent of total federal government spending. Including state and

local data, to the extent possible, increases the coverage to 37 percent of total government

spending.

2.3 Federal Government Contracts

Our data covers spending on goods and services via government contracts. The Federal

Acquisition Regulation (FAR) defines these “contract actions” as “any oral or written action

that results in the purchase, rent, or lease of supplies or equipment, services, or construction

using appropriated dollars over the micro-purchase threshold, or modifications to these actions

regardless of dollar value.” As the definition suggests, the goods and services that the government

consumes through contracts span a wide range, from janitorial services for federal buildings and

IT support services to airplanes and rockets. Contracts can be short term—e.g., a one-month

9“The Census Bureau’s Census of Governments is the primary source of data on the financial activities ofstate and local governments in the BEA input-output tables. This Census is conducted in the same years as theEconomic Census, but is a separate entity. The data collected represent direct summations of the individual unitscanvassed. In 1997, the sample included over 87,000 local government units. Additional data also come from theCensus Bureau’s Annual Survey of Government Finances, which covers all state governments and a sample of localgovernments. In 2000, the annual survey sample was drawn from the 1997 Census of Governments and includedall county governments with resident populations of 100,000 or more, all municipalities with populations of 75,000or more, all independent school districts with enrollments of 10,000 or more, and certain other governments thatmet specific criteria.” See https://www.bea.gov/sites/default/files/methodologies/IOmanual_092906.pdf.

8

contract awarded by the Department of Agriculture Rural Housing Service to Sikes Property

and Appraisal Service for single-family housing appraisals in September 2008—or longer-term

relationships—e.g., the 43-year and 10-month contract awarded by the Department of Energy

to Stanford University for the operation and management of the SLAC National Accelerator

Laboratory.

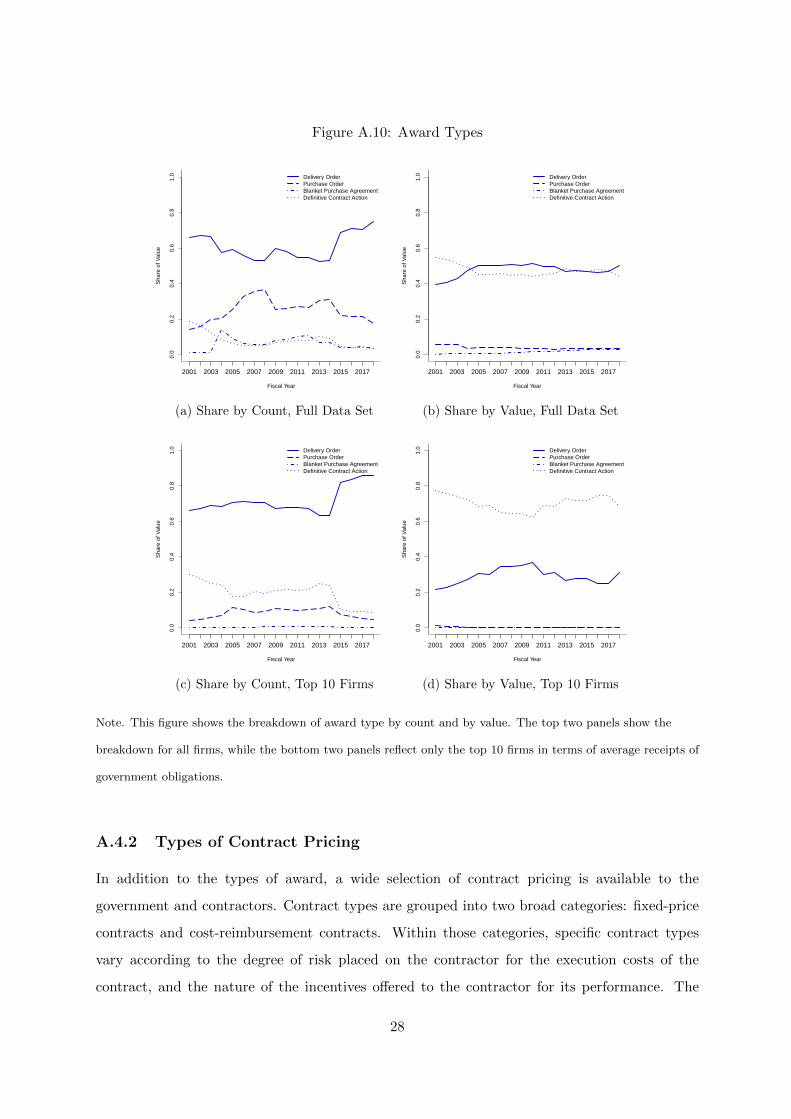

In awarding contracts, federal agencies must abide to the guiding principles set forth in

the FAR. The FAR includes directives on every aspect of contracting, from the structure and

pricing of contracts, to how they should promote competition and encourage small business

participation. The Supplemental Materials provide additional details on some of these aspects

such as the types of awarded contracts, the different pricing structures, and the extent of

competition.

2.4 Details and Scope of the Data Set

The data set includes the universe of federal government contracts from fiscal years 2001 through

2018. On average, 3.2 million individual contract records exist each year—with almost 5 million

annual contracts toward the end of the sample period. Recipients are over 160,000 parent

companies each year, spanning over 1,000 six-digit NAICS sectors. The median contract value

is $3,640, while the mean contract value is $206,023, suggesting the distribution is heavily

right skewed. The majority of contracts (82 percent) represent positive obligations from the

government to firms, but there are also de-obligations with a negative value, which occur when

a modification to an initial contract is performed (see Section 3.3 for details).

Each observation in the data traces a contract action from its origin (the parent agency)

to the recipient firm (which can be a subsidiary of a parent firm) and the sector and zip code

within which the award is executed (see Figure A.23 in Supplemental Materials Section A.6 for

a schematic representation of the data at the micro level).10

In the next section, we provide a number of facts at different levels of aggregation: individual

contracts; firm-level statistics, which aggregate contracts by the recipient parent firm; and sector-

level statistics, which aggregate contracts by NAICS sectors. Note that a contract can comprise

a number of transactions. Most (90 percent of all) contracts, however, are single-transaction

contracts. The value of each contract is given by the “federal action obligation,” the government’s

10Six variables uniquely identify each observation: (1) an award identification number, (2) a modificationnumber, (3) a transaction number, (4) a parent award identification number, (5) an awarding sub-agency code,and (6) a parent award modification number.

9

liability for a contract. Each contract is associated with a start date and an end date for the

period of performance, which we use to calculate the “duration” of the contract. Finally, a

contract will contain a “modification number” if it includes an action that makes a change to

an initial contract.

3 Facts on Government Spending

Government spending, “G”, is conventionally viewed as a homogeneous good, a relatively

constant fraction of GDP that is determined by an ethereal government entity. In this

section, we describe five facts about government spending that illustrate that “G” is in fact

quite heterogeneous, both in the cross-section and over time. In what follows we lay out the

heterogeneity in government spending in some detail in the context of five facts. The subsequent

model-based analysis accounts for all five facts in a stylized way and documents their relevance

for the fiscal transmission mechanism.

3.1 Granularity

This subsection presents our first fact: government spending is granular. We use different

methods to illustrate the granularity of government spending. A common definition of

granularity proposes that a few sectors or firms are disproportionately larger than others.

A stricter definition of granularity is in terms of fat tails (see, for example, Gabaix (2011)):

when the size distribution of firms or sectors exhibits fat tails, then some firms or sectors are

disproportionately large at any level of disaggregation.

Government spending is granular according to both definitions. First, it is concentrated

among a few firms and sectors. Second, a log-normal distribution approximates the government

spending distribution well at all levels of disaggregation.

Fact 1 Government spending is granular:

1. The top 1 percent of firms receive 80 percent of all contract obligations, the top 1 percent

of six-digit sectors receive 40 percent, and the top 3 two-digit sectors receive 70 percent

(where we define rank in terms of firm or sector sales).

2. Concentration in defense and non-defense is similar: the top 1 percent of firms capture

77 (71) percent of government contracts in defense (non-defense), the top 1 percent of

six-digit sectors 48 (49) percent in defense (non-defense) and the top 3 two-digit sectors

10

receive 73 (66) percent in defense (non-defense).

3. Granularity is similar at the state and local level: the top three six-digit sectors (top 1

percent) receive 20 percent of state and local government spending, the top 30 sectors (top

10 percent) 78 percent (compared to 30 and 82 percent for federal contracts).

4. Nearly 100 percent of the cross-sectional variation in contract spending is within firms

or sectors, rather than across, both in the full sample, in the defense sample, and in the

non-defense sample.

5. The size distribution of contracts at the transaction, firm, and sector levels has fat tails

and is approximately log-normal. This is true in the full sample, the defense sample, and

the non-defense sample.

3.1.1 Spending Is Concentrated Among a Few Firms and Sectors

The first sense in which government spending is granular is that it is highly concentrated among

a few firms and sectors. The ten largest suppliers of goods and services to the government (or

top 0.01 percent of recipient firms) account for about one-third of total government spending,

and the top 0.1 percent of firms account for just under one-half of total government spending.

Panel A. of Figure 2 illustrates this unequal distribution. To put these numbers into perspective,

on average some 160,000 firms exist in our sample each year.

Figure 2: Share of Obligations by Top Firms and Sectors

A. Firms B. NAICS 2 Sectors C. NAICS 6 Sectors

0.0

0.2

0.4

0.6

0.8

1.0

Sha

re o

f Tot

al C

ontr

act V

alue ●

●●●

●●●●●●●●

●●●●

●●●●●

●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●

●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●

●●●

2001 2003 2005 2007 2009 2011 2013 2015 2017

●

Top 10 FirmsTop 0.1 PercentTop 1 PercentTop 10 Percent 0.

00.

20.

40.

60.

81.

0

Sha

re o

f Tot

al C

ontr

act V

alue

●●●●●●

●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

2001 2003 2005 2007 2009 2011 2013 2015 2017

●

Top 1 SectorTop 2Top 5Top 10 0.

00.

20.

40.

60.

81.

0

Sha

re o

f Tot

al C

ontr

act V

alue

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●●

●●●●●●●

●●●●●●●●●●●

●

●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

2001 2003 2005 2007 2009 2011 2013 2015 2017

●

Top 5 SectorsTop 1 PercentTop 10 Percent

Notes: 12-month moving average of the monthly share of contract obligations awarded to the top firms (panelA.), six-digit NAICS sectors (panel B.), and two-digit NAICS sectors (panel C.).

A similar spending concentration exists among sectors. Panel B. of Figure 2 shows that

over 60 percent of contract obligations are directed toward the top three (out of 25) two-digit

11

Table 1: Summary Statistics: All Contracts, DOD and Non-DOD

All Defense Non-Defense

Contract Size (Mean) 193,454 242,286 134,462Contract Size (Median) 3,630 4,325 2,626Contract Size (Std Dev) 1,5622,793 1,8233,058 1,1717,756Duration (Mean) 127 117 139Duration (Median) 31 27 33Duration (Std Dev) 284 271 299Transactions per Contract (Mean) 1.34 1.34 1.34Transactions per Contract (Median) 1 1 1Transactions per Contract (Std Dev) 2.9 3.46 2.02Share Fixed Price Contracts 0.73 0.78 0.68Share Top 1 Pct of Firms 0.77 0.77 0.71Share Top 1 Pct NAICS 6 Sectors 0.47 0.49 0.48

Notes: Sample 2001-2018, pooled contract data. Duration measured in days.

NAICS sectors: 33—manufacturing; 54—professional, scientific, and technical services; and

56—administrative and waste management. Panel C. of Figure 2 shows similar patterns at

the more disaggregated sector level: the top 1 percent (of over 1000) six-digit NAICS sectors

account for about 40 percent of government spending, while the top 10 percent of six-digit sectors

account for over 80 percent of government spending. Figure 2 also shows that the concentration

of spending among firms and sectors has been fairly stable over time.

As a contribution to the empirical literature, which has focused on defense spending, our

federal contracts data allow us to show that non-defense spending does not markedly differ from

defense spending along multiple key dimensions, starting with the granularity of contracts. The

top 1 percent of firms capture 77 percent of the value of defense contracts and 71 percent of the

value of non-defense contracts, and roughly half of contract value is concentrated among the top

1 percent of six-digit sectors for both defense and non-defense. At the two-digit sector level, 73

(64) percent of defense (non-defense) contract value is concentrated among the top three sectors.

The top 2 sectors, 33—manufacturing, 54—professional, scientific, and technical services, are the

same for both defense and non-defense. For defense spending, the third most important sector

sector is sector 23—construction, and for non-defense spending, it is sector 56—administrative

and waste management. Table 1 presents these, and other, summary statistics.

While our primary focus is on federal contracts, the BEA input-output tables allow us to

show that state and local government spending is also granular at the sectoral level. According

to the BEA data, the top three of 341 six-digit sectors receive 20 percent of state and local

12

Figure 3: Fat Tails in the Contract Data

A. Transaction-Level B. Firm-Level C. Sector-Level

●

●

●●

●●

●●

●●

●●●●●●●●●●●●●●●●●●●

●●●●●●●

●●●●●●●

●●●●●●

●●●●●●

●●●●●●

●●●●●●

●●●●●

●●●●

●●●●

●●●●●●●

●●

●●

●●

●●

●

●

●

●

2 4 6 8 10 12 14

24

68

1012

14

Theoretical Quantiles

Act

ual Q

uant

iles

●

●

●

●●

●●●●●●●●●●●●●●●●

●●●●●

●●●●●

●●●●●●

●●●●●●

●●●●●●

●●●●●●

●●●●

●●●●

●●●●

●●●●

●●●●

●●●●

●●●●●●●●●

●●

●●

●●

●

●

●

●

●

6 8 10 12 14 16

68

1012

1416

18

Theoretical Quantiles

Act

ual Q

uant

iles

●

●

●●

●

●●

●●

●●

●●●

●●●●●●●

●●●●●

●●●●

●●●●●

●●●●

●●●●●

●●●●●

●●●●●

●●●●

●●●●

●●●●●

●●●●

●●●●●

●●●●

●●●●●●●●●●

●●

●●

●

●●

●

●

12 14 16 18 20 22 24 26

1214

1618

2022

2426

Theoretical Quantiles

Act

ual Q

uant

iles

Notes: The panels show quantile-quantile plots of the contract data, with actual quantiles of log transactions on the y-axisand theoretical quantiles from a log-normal distribution with the same mean and standard deviation plotted on the x-axis.Panel A. shows this relationship at the transaction level, Panel B. at the firm level, and Panel C. at the NAICS 6 sectorlevel. Data represent a single annual cross section from the year 2012, but the pattern is robust in any year in the sample.

government spending, compared to 30 percent for federal spending, and the top 30 of 341

sectors receive 78 percent of state and local government spending compared to 82 percent of

federal spending.

3.1.2 The Size Distribution of Contracts Has Fat Tails

Government spending is also granular in a statistical sense: the distribution of government

contracts is fat-tailed and is well-approximated by a log-normal distribution. A simple way to

illustrate this point is to look at a Q-Q (quantile-quantile) plot, in which we plot the actual

quantiles of the log values of individual contracts, of contracts aggregated up to the firm or to

the sector level against the quantiles from a simulated log-normal distribution with the same

mean and variance. If both sets of quantiles come from the same distribution, the plotted points

should line up along the 45-degree line.

Indeed, fat tails are present both in the full sample, in the defense sample, and in the

non-defense sample. Panel A. of Figure 3 shows the relationship for the sample of individual

contracts follows the 45-degree line across the entire distribution. Panels B. and C. show the

same scatter plots for firms and six-digit NAICS sectors, respectively.11 While a log-normal

distribution is the best fitting fat-tailed distribution for the full samples in all three panels, we

show in Supplemental Materials Section A.3.2 that a Pareto distribution, as in Gabaix (2011),

11Figure A.31 in the Supplemental Materials shows the equivalent plots for both defense and non-defensecontracts.

13

also provides a good fit to the right tail of the distribution.

3.2 Sectoral Bias

The second fact we present establishes that the government spending basket is special: the

composition of government spending across firms and sectors is distinct from the composition

of private spending across firms and sectors. Such differences exist for total federal government

spending as well as for state and local government spending, defense spending, and non-defense

spending. As a consequence of these composition biases, the identities of the most important

firms and sectors as suppliers to the government differ substantially from the identities of the

most important firms and sectors that supply to the rest of the economy.

Fact 2 Government spending is sectorally biased:

1. The sector with the largest share in total government spending (NAICS 33 — manufactur-

ing) receives 30 percent of government spending, but accounts for only 13 percent of GDP.

The sector with the largest share in GDP (NAICS 62—health care and social assistance)

accounts for 12 percent of GDP but less than 2 percent of government contract spending.

The top three two-digit sectors receive 70 percent of government spending, but account for

only 18 percent of GDP.

2. Spending in both defense and non-defense is similarly biased: the sector with the largest

share in federal defense spending (NAICS 33 — manufacturing) receives 40 percent of

government defense spending, but accounts for only 13 percent of GDP. The sector with

the largest share in federal non-defense spending (NAICS 54 — Professional, Scientific,

and Technical Services) accounts for 37 percent of government non-defense spending, but

only for 4 percent of GDP.

3. Spending at the state and local level is similarly biased: the sector with the largest share in

state and local government spending (NAICS 54 — Professional, Scientific, and Technical

Services) receives 15 percent of state and local government spending, but less than 5 percent

of GDP in the economy.

4. The top 0.01 percent of recipient firms (10 firms) of federal government spending account

for 17 percent of average annual government spending, but only 3 percent of average annual

sales.

We illustrate these facts graphically in Figure 4. The vertical axis in both panels measures

the share of a (six-digit) sector k in government spending, GkG . The horizontal axis measures

14

Figure 4: Sectoral Bias in Government Spending

−9 −8 −7 −6 −5 −4 −3 −2

−9

−8

−7

−6

−5

−4

−3

−2

GDP Shares (Logs)

Gov

ernm

ent S

pend

ing

Sha

res

(Log

s)

−9 −8 −7 −6 −5 −4 −3 −2

−9

−8

−7

−6

−5

−4

−3

−2 State and Local

Federal

−9 −8 −7 −6 −5 −4 −3 −2−

9−

8−

7−

6−

5−

4−

3−

2

GDP Shares (Logs)

Gov

ernm

ent S

pend

ing

Sha

res

(Log

s)

−9 −8 −7 −6 −5 −4 −3 −2−

9−

8−

7−

6−

5−

4−

3−

2 Federal DefenseFederal Non−Defense

Notes: Distribution of government spending across 350 sectors (measured along the y-axis) against the distribution ofsectoral GDP in the economy (x-axis), average values for 2001–2018. Sectoral GDP is calculated as total industry outputnet of output sold as intermediates to other sectors and net exports. The left panel distinguishes between federal governmentspending and state-level and local government spending, the right panel between spending by the department of defenseand federal non-defense spending. Data sources: BEA Input Output Accounts: Make Table and Use Table.

the share of the same sector in GDP, GDPkGDP . GDP is computed using the BEA “Make” and

“Use” tables as total industry output net of output sold as intermediates to other sectors and

net exports. The left panel focuses on federal (red dots) as well as state and local spending

shares (blue diamonds). The right panel focuses on the defense (blue star) and non-defense

(green triangle) subsets of federal spending. If government spending and private spending had

the same composition, then we would expect government spending shares and GDP shares to

align perfectly along a 45-degree line.

However, government and private spending shares differ substantially, that is, GkG 6=

GDPkGDP .

First, some sectors that are big suppliers to the federal government are almost negligible for

GDP. Sector 541300—Architectural, Engineering, and Related Services, for example, accounts

for 16 percent of total federal government spending but less than 1 percent of GDP. Second,

the same bias holds true for state and local spending: sector 517000—Telecommunications, for

example, accounts for over 6 percent of state and local government spending but less than 3

percent of GDP. Third, defense and non-defense spending exhibit a similar pattern: sectors

336411—Aircraft Manufacturing and 622000—Hospitals, for example, account for 8 and 11

percent of federal defense and non-defense spending, respectively, but less than 1 percent and 5

15

percent of GDP, respectively.

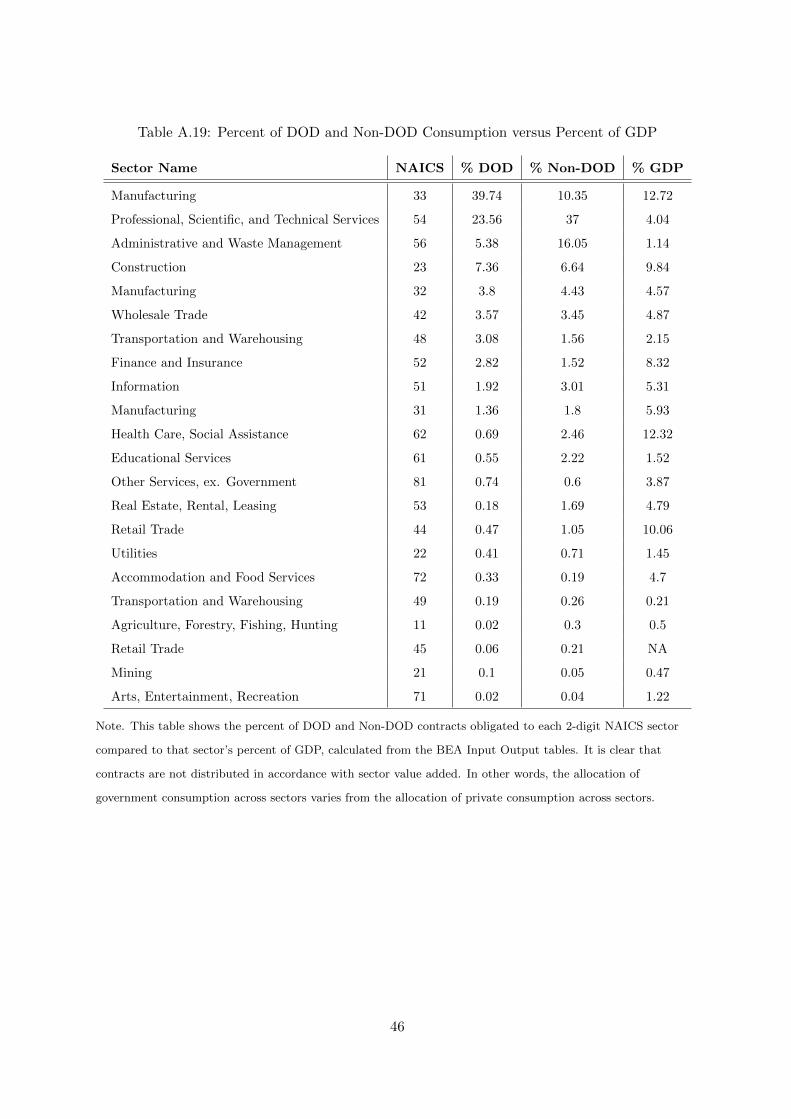

The converse also occurs, as we shown in Supplemental Materials Table A.4. Health care

and social assistance (NAICS 62) accounts for over 12 percent of GDP, but less than 2 percent

of government spending. Online Appendix Table A.4 and Suppemental Materials Table A.26

show similar patterns for state and local government, federal defense, and federal non-defense

spending. The Retail Trade Industry (NAICS 44), for example, accounts for 10 percent of GDP

but less than 1 percent of state and local government spending. The Finance and Insurance

Sector accounts for more than 8 percent of GDP but less than 3 percent of defense spending

and less than 2 percent of non-defense spending.

Finally, sectoral bias also occurs at the firm level—Table A.5 in the Online Appendix

compares the top 35 firms in terms of annual contract spending to the top 35 non-oil firms from

Orbis in terms of revenue in 2017. Little overlap exists in the firm lists, with only a few firms

like Boeing showing up in both the list of top government and top private sector suppliers, and

in very different orders. Taken together, our evidence indicates that government spending varies

across sectors and firms, and its composition does not mimic that of GDP.

3.3 Moderate Persistence

The dynamics of government spending are characterized by a moderate degree of persistence at

all levels of aggregation. At the contract level, the duration of contracts is short, while at the

firm level, turnover of firms which are counterparty to the government is large. At the sector

level, persistence is also moderate. Along all these dimensions no large differences exist between

defense and non-defense contracts.

Fact 3 Government spending is characterized by short contract durations:

1. The median contract has a duration of 31 days. Over 90 percent of contracts last less than

one year. Contracts are frequently modified: more than half of all contracts are subject to

some modification.

2. The firm with the median value of average annual obligations is in the data set for less

than one year.

3. The mean persistence of AR(1) processes at the two-digit sector level is 0.42. The average

persistence parameter in the top three two-digit sectors is 0.45—somewhat higher than

the average in the remaining sectors (0.37). Omitting the largest 1 percent of contracts

decreases persistence by 15 percent. Filtering seasonality from the data increases the

16

average persistence to 0.73.

4. The same findings hold for defense and non-defense spending: The median defense contract

lasts 27 days, the median non-defense contract 33 days. 90 percent of defense and non-

defense contracts last less than 1 year. The monthly, quarterly and annual persistence

estimates are 0.41, 0.50, and 0.76 for defense, and 0.41, 0.31 and 0.80 for non-defense.

We first measure persistence at the smallest unit of aggregation by using the duration of

contracts. Durations of contracts can range from 0 days—for example a one time-purchase

of a commercially manufactured good—to over a decade—a contract funding research and

development, for example. The length of the contracts depends entirely on the nature of the

relationship and the provided product or service. Overall, however, contracts tend to have short

life spans. Over the entire sample, the median contract has a duration of only 31 days.12 In

each year, about 90 percent of contracts have durations of less than one year.

Second, we also document moderate persistence at the firm level. Turnover of firms that

are counterparty to the government is large—in line with the short duration of contracts. For

the entire sample, most firms are in the data set for only short periods of time.13 In fact, the

median number of years a firm is in the data set is less than 2 years, and the firm with the

median value of average annual obligations is in the data set for less than 1 year. We illustrate

these results in Figure 5.

However, substantial heterogeneity in the persistence exists across the firm-size distribution:

the largest firms (the top 0.1 percent) are more likely to be in the data for longer periods.

The contracts with the longest durations are mostly related to the management of facilities and

investment around the government. They span sectors from information technology, professional,

scientific, and technical services; administrative and support and waste management and

remediation services; as well as manufacturing. Section A.6.5 in the Supplemental Materials

provides more detail on the identity of these firms and sectors.

Third, we characterize the persistence of government spending at the two-digit sector level

estimating AR(1) processes, which also serve to facilitate a mapping of our data into business

cycle models. We report results for monthly data in Table 2 (and for quarterly and annual

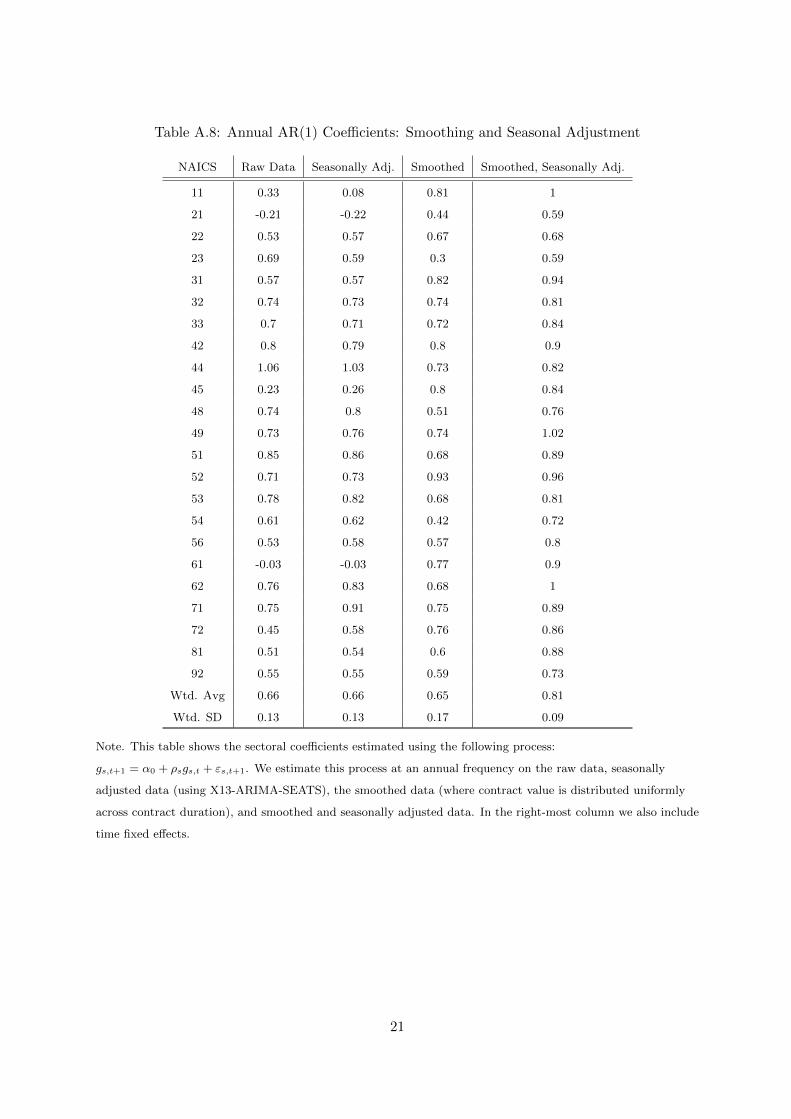

frequencies in Tables A.7 and A.8 in the Online Appendix). Considerable heterogeneity across

sectors exists in terms of estimated autocorrelation coefficients. In the raw data, the standard

12For this analysis we keep contracts with durations between 1 and 5500 days (15 years). These contractsrepresent more than 95 percent of the total value of obligations.

13To be “in the data” in a given year, a firm must receive a new contract in that year.

17

Figure 5: Distribution of Contract and Firm Duration

A. Contract Duration B. Firm Duration

0.0

0.2

0.4

0.6

0.8

1.0

Duration (Days)

Cum

ulat

ive

Sha

re

0 1000 2000 3000 4000 5000 6000

ContractsMulti−Transaction Contracts

0.0

0.1

0.2

0.3

0.4

●

●

●

●● ●

● ●● ● ●

●● ● ● ● ●

●

●

All FirmsTop 10 PercentTop 1 PercentTop 0.1 Percent

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Sha

re o

f Fir

ms

Number of Years in Dataset

Notes: Panel A. shows the empirical cumulative distribution function of the duration—the number of days between the startand end-date—of transactions and contracts. The dashed black line marks 365 days. Contracts with negative durations ordurations more than 5500 days (15 years) are excluded. Transactions represent the observation level of the data. Contractsare bundles of transactions that pertain to the same award. Multi-transaction Contracts are the subset of contracts thatare made up of more than one transaction. Panel B. shows the share of firms that show up in the data set (receive a newcontract) for 1,2,..., 18 years. The solid black line shows high turnover occurs among firms—most firms show up in the datain only 1 to 3 years. Conversely, relationships with the top 0.1 percent of suppliers to the government are more likely to belong-term in nature.

deviation across estimates is 0.12 and the average persistence parameter is 0.42, consistent with

the short duration of contracts. Persistence drops to 0.36 if we exclude the top 1 percent of

firms (see Online Appendix Table A.9), which is another illustration of granularity: a few large

firms are in the sample for a longer time.

However, persistence estimates can increase substantially depending on further data

treatments, up to the level which implies a half-life of the government spending process consistent

with the one implied by estimated VAR models. Galı et al. (2007), for instance, report values in

between 0.80 and 0.98. In line with the political economy of government spending, government

contracts tend to spike in September—the final month of the government fiscal year.14 Columns

2 to 4 in Table 2 report the estimated autocorrelation coefficients obtained from fitting AR(1)

processes to the seasonally-adjusted series, the smoothed series and series that are first smoothed

and then seasonally adjusted. We use the X-13 filter at the sector level to seasonally adjust, and

smooth the data by spreading spending uniformly over the contract duration as in Auerbach

14Figure A.8 in the Online Appendix illustrates this point by plotting the average total contract spending bymonth of year.

18

Table 2: Monthly AR(1) Coefficients: Smoothing and Seasonal Adjustment

Smoothed,NAICS Raw Data Seasonally Adj. Smoothed Seasonally Adj.

11 0.42 0.25 0.96 0.9421 0.20 0.09 0.47 0.5522 0.38 0.17 0.86 0.9623 0.23 0.69 0.48 0.9931 0.21 0.91 0.96 0.9632 0.25 0.33 0.96 0.9733 0.46 0.74 0.94 0.9542 0.66 0.75 0.97 0.9744 0.47 0.78 0.96 0.9645 0.58 0.53 0.97 0.9748 0.67 0.81 0.81 0.8749 0.51 0.65 0.56 0.5851 0.41 0.90 0.90 0.9352 0.31 0.70 0.99 0.9953 0.10 0.79 0.91 0.9354 0.45 0.87 0.76 0.8756 0.41 0.57 0.89 0.9261 0.27 0.08 0.92 0.9362 0.51 0.74 0.69 0.9271 0.32 0.39 0.89 0.9272 0.45 0.49 0.94 0.9481 0.33 0.46 0.70 0.9292 0.36 0.36 0.89 0.90

Weighted Avg 0.42 0.73 0.87 0.94Weighted SD 0.12 0.18 0.14 0.05

Notes. This table shows the sectoral coefficients estimated using the following process: gs,t+1 = α0 + ρsgs,t +

εs,t+1. We estimate this process at a monthly frequency on the raw data, seasonally adjusted data (using X13-

ARIMA-SEATS), the smoothed data (contract amount is distributed uniformly across the contract duration),

and smoothed and seasonally adjusted data.

et al. (2020). The average persistence parameters range between 0.74 and 0.94 across data

treatments.

Seasonality does not only matter because it directly affects AR(1) persistence estimates.

It also matters because it relates to the notion that government spending shocks are

unanticipated—a crucial assumption in much of the empirical work on the fiscal multiplier.

In line with earlier work, our analysis underscores the concern that at business-cycle frequency,

a strong anticipated component to government spending exists (Ramey, 2011; Leeper et al.,

2013).

Finally, if we consider defense and non-defense spending separately, we find similar evidence

19

of moderate persistence: the median defense contract lasts 27 days, and the median non-defense

contract 33 days. Moreover, 90 percent of both defense and non-defense contracts last less than

1 year. The persistence parameters at the monthly, quarterly and annual frequency are 0.41,

0.50 and 0.76 for defense, and 0.41, 0.31 and 0.80 for non-defense.

3.4 Idiosyncratic Shocks Drive Aggregate Variation At Business Cycle

Frequency

The fourth fact we establish is that at business cycle frequency, the growth of aggregate

government spending occurs via increases in government purchases for a small number of large

firms and sectors. In other words, shocks are idiosyncratic at the firm and sectoral levels rather

than aggregate. As we show below, the cross-sectional granularity of firms and sectors, our first

fact, is tightly linked to the variation over time.

Fact 4 Firm and sector shocks drive aggregate variation at business cycle frequency:

1. The granular residual explains 40 percent of aggregate government spending growth if

constructed at the firm level and 38 percent of aggregate government spending growth at

the six-digit NAICS sector level.

2. A similar result applies to defense and non-defense spending: The granular residual

explains 46 (38) percent of aggregate spending growth in defense, and 24 (34) percent

in non-defense spending if constructed at the firm level (six-digit NAICS sector level).

3.4.1 Granular Origin of Government Spending Fluctuations

We follow Gabaix (2011) and calculate the granular residual, Γt, to establish that idiosyncratic

variation of a few influential firms and sectors is crucial to account for the growth of aggregate

government spending.15 Let gi,t denote the total obligations to recipient firm or sector i in

month t. Then, the growth rate of government spending at the firm or sector level is given by

zi,t = ln(gi,t)− ln(gi,t−12), that is, the 12-month change in government contracts to firm or sector

15We list in Online Appendix Tables A.1-A.3 the largest five contracts in each of the three largest two-digitNAICS sectors in 2012. These contracts help illustrate some firm-specific and sector-specific drivers of variation.In Section A.3.4 of the Online Appendix we use the approach of Foerster et al. (2011) and obtain similar results.

20

i.16 The granular residual is then defined as:

Γt =K∑i=1

gi,t−12

Gt−12(zi,t − zt), (1)

where Gt is aggregate government spending in month t, and zt = Q−1∑Q

i=1 zi,t is the average

growth rate of spending over the top Q firms or sectors. In other words, the granular residual

is the weighted difference in growth rates for the top K firms or sectors relative to the average

growth rate for the top Q firms or sectors, where Q ≥ K. At the firm level, we calculate the

granular residual over the top K = 50 firms, and take averages over the top Q = 5000 firms. At

the sector level, we calculate the granular residual over the top K = 10 six-digit NAICS sectors,

and take averages over the top Q = 1000 sectors.

The granular residual provides a measure of the importance of idiosyncratic variation in

spending growth. To see this point, consider the case in which variation in government spending

is common to all firms or sectors. In this case, zit = zjt = zt and the granular residual would be

0. Instead, absent perfect correlation, some idiosyncratic deviations from the common increase

in government spending will matter—and the more so, the larger the firms or sectors that

experience them.

As in Gabaix (2011), we run a regression of aggregate growth, Zt = ln(Gt)− ln(Gt−12), on

the granular residual and its lags to study its quantitative importance. The granular hypothesis

suggests the granular residual accounts for a large part of the aggregate movement of government

spending. Specifically, we estimate:

Zt = β0 + β1Γt + β2Γt−1 + β3Γt−2.

Columns (1) and (2) of Table 3 shows the firm-level granular residual explains about 40

percent of the variation in aggregate government spending growth. Columns (3) and (4) show

that the sector-level granular residual explains 30 to 38 percent. When we consider only defense

(non-defense) data, we find the firm-level granular residual explains 46 (24) percent of aggregate

defense (non-defense) spending growth (see Supplemental Materials Tables A.22 and A.23) and

the sector-level granular residual explains 38 (34) percent of aggregate defense (non-defense)

spending growth (see Supplemental Materials Tables A.24 and A.25). Overall, these results are

16Note, we use the 12-month rather than 1-month changes due to the strong seasonal nature of governmentcontract spending.

21

in line with the estimates of Gabaix (2011) for the explanatory power of the granular residual

on GDP growth.

Table 3: Explanatory Power of the Granular Residual

(1) (2) (3) (4)∆G

(Firms)∆G

(Firms)∆G

(Sectors)∆G

(Sectors)

Γt 0.880∗∗∗ 0.849∗∗∗ 0.932∗∗∗ 1.012∗∗∗

(0.0805) (0.0793) (0.100) (0.0987)Γt−1 0.125 0.176

(0.0798) (0.100)Γt−2 -0.0940 -0.0882

(0.0786) (0.0939)Constant 0.228∗∗∗ 0.223∗∗∗ 0.121∗∗∗ 0.119∗∗∗

(0.0187) (0.0244) (0.0145) (0.0142)

Observations 201 199 201 199R2 0.375 0.395 0.303 0.377

Standard errors in parentheses∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

Note. We run a regression of the 12-month change in aggregate growth—Zt = ln(Gt) − ln(Gt−12)—on thegranular residual and its lags, where the granular residual is given by Γt =

∑Ki=1

gi,t−12

Gt−12(zi,t − zt). Gt is

aggregate government consumption in period t and zt is the average growth rate over the top Q sectors. For thefirm-level regressions in columns (1) and (2), we use Q = 5000, and for the sector-level regressions, we useQ = 1000.

3.5 Government Spending Is Concentrated in Sticky Sectors

The last fact is about government spending and pricing frictions: government spending tends

to be concentrated in sticky-price sectors—that is, sectors in which price changes are relatively

less frequent—while private spending is concentrated in more flexible-price sectors.

We document this fact in two complementary ways. First, we use micro data underlying

the PPI from the BLS to construct monthly frequencies of price adjustments for each sector in

the data. We then plot the frequencies against the size of the sectors from which the government

purchases and contrast it against the distribution of private sector purchases (to make explicit

the implication of biased government baskets, Fact 2, in this context).

One caveat of this analysis is that the frequency of price adjustment for private and

government consumption may not be identical. Therefore, we also study the price rigidity

of government contracts directly. Using inverse average contract durations from our data as

a measure of frequency of price changes, we find very similar frequencies of price changes

22

for government contracts as in the BLS data.17 Our main result holds for both defense and

non-defense spending.

Fact 5 Government spending is concentrated in sticky sectors:

1. The monthly frequency of price changes in the top three two-digit sectors supplying to the

government is 11 percent while it is 22 percent, on average, for the remaining sectors. The

frequency in the top three sectors for private consumption is 17 percent.

2. 80 percent of all contracts are fixed price in nature.

3. The monthly frequency of price changes in the top three two-digit sectors supplying to the

government is 13 percent for defense and 10 percent for non-defense spending, while it

is 20 percent and 21 percent, on average, for the non-top sectors. Overall, defense and

non-defense pricing frictions have very similar distributions.

Our main result is that government spending is concentrated in sticky-price sectors. Panel

A. of Figure 6 shows, in blue, the average annual share of government spending in each two-digit

sector (x-axis) plotted against the frequency of price changes in those sectors from the BLS. The

figure also plots in red the frequency and size of private sector consumption. The size of the circles

corresponds to the average sector share of annual aggregate spending—a larger circle means the

sector supplies a larger portion of government spending. The figure shows the government spends

the vast majority of dollars in sectors with low frequencies of price adjustment.

The frequency of price changes in the largest three sectors is 11 percent, while it is 22 percent

on average, for the remaining sectors. The same pattern hold for defenses and non-defense

contract spending. The frequency of price changes in the largest three defense (non-defense)

sectors is 13 (10) percent, while it is 20 (21) percent, on average, for the remaining sectors

(see Figure A.36 in the Supplemental Materials). At the same time, as the red dots illustrate,

private consumption is concentrated in more flexible-price sectors. This differential heterogeneity

relative to private consumption is a direct result of sectoral bias (Fact 2), but the bias itself does

not predict whether government or private consumption is characterized by stickier prices.

An important caveat is that the frequency of price adjustment from the BLS and the

frequency of price changes for only government spending might differ. We can make no definitive

statement about firms’ possible price discrimination across public and private buyers. We show,

however, a very similar picture for the frequency of price changes emerges based on a simple,

17As we discuss below, the majority of contracts has some form of fixed pricing suggesting the inverse contractduration is a good proxy for the frequency of price adjustment.

23

Figure 6: Frequency of Price Adjustment

A. BLS Frequency B. Inverse Duration

0.0 0.1 0.2 0.3 0.4

0.0

0.1

0.2

0.3

0.4

0.5

Share of Spending

Fre

quen

cy o

f Pric

e C

hang

es

●

●

●

●

●

●

●

●

●

●

●

●●

●

●

●●

●

●

●

●

●

●

●

●

●

●

●

●

●

●●

●

●

●

●

●

●

●

●

Government ContractsPrivate Spending

0.00 0.05 0.10 0.15 0.20 0.25 0.30

0.0

0.2

0.4

0.6

0.8

Share of Spending

Fre

quen

cy o

f Pric

e C

hang

es

●

●

●

●

● ●

●

●

●

●

●

●

●

●

●●

●

●

●

●

●

●

Notes. This figure shows the average annual share of government spending (in blue) and private consumption (in red) ineach two-digit sector (x-axis) plotted against the frequency of price changes in those sectors, based on BLS data in PanelA. and the frequency implied by contract durations, based on USAspending.gov data in Panel B. The size of the circlescorresponds to the average sectoral share of annual aggregate spending.

direct analysis of the contract data. To do so, we use inverse average durations from our data as a

measure of frequency of price changes. The intuition behind this approach is the following: Since

85% of all contracts include a fixed-price provision (see Table A.10 in the Online Appendix),

prices are usually sticky during the duration of a contract. Duration then provides a natural

lower bound on nominal price stickiness.18

We find very similar frequencies of price changes for government contracts as in the BLS

data. Moreover, the frequency of price changes implied by the average contract duration equals

21.5 percent, while the average frequency from the BLS equals 19.7 percent. Panel B. of Figure 6

18Of course, the analysis here is limited in that we do not have the data to study the allocative nature, thatis, whether a price remains fixed or adjusts little across contracts over time while quantities do adjust. However,allocativeness in the New Keynesian sense is likely a relevant feature of the data: More than half of the contractsin terms of value feature modification provisions, of which more than a third represent a “supplemental agreementfor work within scope” or “exercise an option.” In addition, a clause in the federal acquisition regulation suggestschanges to funding via modifications are supposed to be certified based on the initial negotiated price in that “(a)The contracting officer shall not execute a contract modification that causes or will cause an increase in fundswithout having first obtained a certification of fund availability [. . . ] (b) The certification required by paragraph(a) of this section shall be based on the negotiated price.”

24

illustrates this result closely resembling the picture for the BLS micro data.19

4 A New Keynesian Model with Sectoral Government Spending

We develop a two-sector New Keynesian model to assess the extent to which our novel results on

heterogeneity of government spending impacts the fiscal transmission mechanism. The model is

deliberately stylized, departing as little as possible from the one-sector model (e.g., Woodford,

2011). Sectors potentially differ along three dimensions: first, the shares of private and public

spending and hence, their size; second, the degree of price rigidity; third, the incidence of shocks.

Rather than postulating a process for “big G,” we model government spending in each sector as

distinct variable. In what follows, we outline the set-up in general terms and derive a number

of theoretical results. We then simulate the model to illustrate the quantitative relevance of the

five facts we document.

4.1 Set-up

We focus on the key equations of the model because it is a simple extension of the textbook

version of the New Keynesian model (Woodford, 2003; Galı, 2015). A representative household

chooses consumption and labor in order to solve an infinite horizon problem subject to a period

budget constraint:

max{C1t,C2t,L1t,L2t}∞t=0

E0

∞∑t=0

βt

(ln

(Cω1,tC

1−ω2,t

ωω(1− ω)1−ω

)− ξ1

L1+ϕ1t

1 + ϕ− ξ2

L1+ϕ2t

1 + ϕ+ f(G1t, G2t)

),

s.t. W1tL1t +W2tL2t + Πt + It−1Bt−1 = Bt + P1tC1t + P2tC2t + P1tG1t + P2tG2t.

Ckt and Gkt denote private and public consumption of sector-k goods, with k = {1, 2},

respectively. Gkt is determined exogenously and financed by lump-sum taxes for which we

substitute in the household budget constraint. Government spending provides utility according

to f(G1t, G2t), but independently of private consumption and leisure. Pkt is the price of sector-k

goods. Lkt and Wkt are labor employed and wages paid in sector k. Our specification assumes

sectoral segmentation of labor markets. Below, we set parameters ξk to ensure a symmetric

steady state across all firms. Households own firms and receive net income, Πt, as dividends.

19This finding also suggests the frequencies of price changes computed based on BLS data are not driven bythe fixed-price nature of procurement contracts. Procurement contracts represent only a fraction of total sectoractivity, so this finding suggests that frequencies of price changes are similar for transactions involving privatecounter-parties and the government.

25

Bonds, Bt−1, pay a nominal gross interest rate of It−1 and we rule out Ponzi schemes.

The optimal allocation of consumption expenditures across sectors requires:

C1t = ω

(P1t

PCt

)−1

Ct and C2t = (1− ω)

(P2t

PCt

)−1

Ct, (2)

where PCt = Pω1tP1−ω2t is the consumer price index. The consumption bundles in each sector, in

turn, are defined as a CES aggregate of differentiated goods indexed by j ∈ [0, n] in sector 1 and

j ∈ (n, 1] for sector 2:

C1t ≡[n−1/θ

∫ n

0C

1− 1θ

j1t dj

] θθ−1

, C2t ≡[(1− n)−1/θ

∫ 1

nC

1− 1θ

j2t dj

] θθ−1

, (3)

and analogously for government consumption G1t and G2t. Cost minimization implies the

demand for differentiated goods:

Cj1t =1

n

(Pj1tP1t

)−θC1t, Cj2t =

1

1− n

(Pj2tP2t

)−θC2t, (4)

and analogously for government consumption Gj1t and Gj2t. Lastly, the sectoral price indices

are given by:

P1t =

[1

n

∫ n

0P 1−θj1t dj

] 11−θ

, P2t =

[1

1− n

∫ 1

nP 1−θj1t dj

] 11−θ

. (5)

The household first-order conditions determine labor supply and define the Euler equation:

Wkt

PCt= ξkL

ϕktCt for k = {1, 2} , (6)

1 = Et

[β

(Ct+1

Ct

)−1

ItPCtPCt+1

]. (7)

Differentiated goods are produced according to: Yjkt = Ljkt. Firms are constrained in their

ability to set prices. With probability αk, which may differ across sectors, a firm may not adjust

its price in the next period. The pricing problem of firm j in sector k is:

maxPjkt

Et∞∑s=0

Qt,t+sαsk

[PjktYjkt+s − Ct+s(Yt+s|t)

], (8)

26

subject to the constraint that production adjusts to meet demand at posted prices:

Yjkt = Cjkt +Gjkt. (9)

Here, consumption demand for good j, Cjkt, depends on prices according to equation (4), and

equivalently for government spending.20 In expression (8), Qt,t+s is the stochastic discount

factor and Ct+k(·) are costs of production. The first-order condition is:

Et∞∑s=0

Qt,t+sαskYjkt+s [P ∗kt −MΨkt+s] = 0, (10)

where Yjkt+s is the total production of firm jk in period t + s, M ≡ θθ−1 denotes the desired

markup and Ψt+k = C′t+k(Yt+k) are marginal costs. The optimal price, P ∗kt, is the same for all

firms in a given sector. Thus, aggregating all prices within a sector yields:

Pkt =[(1− αk)P ∗1−θkt + αkP

1−θkt−1

] 11−θ

. (11)

We define sectoral output as follows:

Y1t ≡[n−1/θ

∫ n

0Y

1− 1θ

j1t dj

] θθ−1

, Y2t ≡[(1− n)−1/θ

∫ 1

nY

1− 1θ

j2t dj

] θθ−1

and write nominal GDP as:

PY tYt ≡ P1tY1t + P2tY2t. (12)

Here, PY t ≡ Pn1 P1−n2 is the GDP deflator. Analogously, we define aggregate government

spending (“Big G”) as:

PGtGt ≡ P1tG1t + P2tG2t. (13)