Economic indicators - Economic Monthly Overvies November 2012

Upload

seid-omerovicCategory

view

218download

0

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 1/12

Monthly Economic Report

Issue: No 1 December 2011

Bosnia & Herzegovina

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 2/12

2

Bosnia&Herzegovina Economic Report

HIGHLIGHTS ............................................................................................................ 3

POLITICS .................................................................................................................. 4

REAL ECONOMY ...................................................................................................... 5

Real economy in Bosnia and Herzegovina

INFLATION ............................................................................................................... 7

FISCAL POLICY ....................................................................................................... 8 BANKING SECTOR ................................................................................................... 9

EQUITY AND DEBT MARKET ................................................................................ 10

ECONOMIC OUTLOOK ........................................................................................... 11

IMPRESSUM .......................................................................................................... 12

Content

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 3/12

3

Source: Raiffeisen RESEARCH

Source: Agency for Statistics of B&H Raiffeisen RESEARCH

Analyst: Ivona Kristić, Srebrenko Fatušić

Tel.: +387 33 287 784e-mail:[email protected]@rbb-sarajevo.raiffeisen.at

Published by:

Raiffeisen BANK d.d. BiH

Investment BankingResearch & Analysis Department,

71 000 Sarajevo, Zmaja od Bosne bb

HighlightsNo end in sight to B&H longest institutional crisis in post-warperiod as country hits 15 month without formed State

Government. Due to political dead-lock, 2011 is already declared as year of stagnation regarding the EU membershiproad

Serious slowing down of positive momentum in Europeaneconomy seen in Q3 took its first impacts on BH economy.

As expected, firstly were hit exports and export-orientedindustrial production.

Real GDP growth of 1.9% yoy is expected in 2011 whichshould be accomplished due to strong rebound of export andindustrial output in first semester of 2011.

Inflation level eased to some extend in Oct.11 (+3.7% yoy)but still threatens to reaccelerate by the end of year. For2012, we expect overall inflation to ease down to feeble levelof 2.3% yoy mostly due to global economic slowdownFiscal deficits in FB&H and RS in Q3 2011 mostly in line withour expectations

B&H banking sector as of 30.09.2011 reported net profit of BAM 82.1 million. At the same time, credit and depositperformance continue to strengthen in Q3 2011, while firstsigns of slowing down in the credit performance we canexpect by the end of 2011

Total turnover on B&H markets fuelled by primary marketsdevelopments (public offering of bonds and T-bills)

Taking into account negative trends of main drivers of economic growth, B&H is facing stagnation in 2012 reflectedin forecasted 0% yoy real GDP growth

Source: Agency for Statistics of B&H, Central Bank of B&H, Raiffeisen RESEARCH

B&H Credit rating

Credit rating

Rating Outlook Rating Outlook

LT B Negative B2 NegativeDate

Activity

S&P Moody's

December-11 May-11

Declined Confirmed

Economic growth of B&H

Highlights

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 4/12

4

No end in sight to B&H longestInstitutional crisis in post-war period

Source: Raiffeisen RESEARCH

Source: Raiffeisen RESEARCH

Source: Raiffeisen RESEARCH

Bosnia and Herzegovina hits 15 month without completedprocess of the State Government forming (Council of

Ministers), as political leaders failed to reach an agreement oninaugurating of the State Council of Ministers. Therefore, afterBelgium appointed the new Government during last month,B&H left as the only one without the official government inEurope.

Despite numerous failed attempts to form a coalitiongovernment at the State level, B&H key political partiesremained on their firm standpoints, further deepening thepolitical crisis. The political leaders of 6 biggest parties (SDP,SDA, SNSD, SDS, HDZ, and HDZ 1990) without which thenew Government can’t be establish are still showing lack of will to achieve the compromise over the split of seats in the

new State Government. The last meeting of the key politicalfigures was held in Italian town of Cadenabbia on LakeComo, where the Konrad Adenauer Foundation organized atits political academy a seminar on the constitutional structureof Bosnia and Herzegovina. The meeting of the six politicalleaders was also expected to provide an opportunity for talkson the establishment of a new Central government. However,political leaders once again have not been able to agree. After the last afford to reach an agreement failed, B&Hpolitical analysis predicts two possible scenarios if the politicalstalemate continues. Theoretically, this situation may continueuntil the October of 2014, when B&H will hold the nextparliamentary elections. The State Constitution does notcontain any provisions as to how to get out of this crisis. By second scenario we can expect the extraordinary elections forthe State Parliament. All in all, both scenarios are still not ourbasic scenario, as we expect that political heads will finally find the “middle ground” under the pressure of theInternational Authorities.

Political stalemate, in which B&H plunged since the lastOctober’s general elections, worsened the EU perspective andplaced the country on margins of all EU and Internationalintegrations. This was officially confirmed by the latest AnnualEU Progress Report on B&H published by the European

Commission (EC). The EC report particularly underlined lackof common political vision related to EU progress. Accordingto the report, B&H also achieved just marginal result in areaof human rights, jurisdiction, press freedom, while progresstoward functional market economy is negligible and B&Hmust implement huge strategic reforms in order to becamecapable for responding the EU markets conditions. Hence,B&H still have to fulfill 3 conditions (Law on census, Law onState Help and Harmonization of the Constitute with theEuropean Convection on Human Rights) in order to acquiringthe EU Candidate Status over which the key political partiesare still deeply divided. Accordingly, 2011 is already declaredas year of stagnation regarding the EU membership road.

No progress towards EU membership

Key political persons in B&H

The High representative for B&H Valentin Incko

EU Special Representative in B&H Peter Sorensen

Three-member Presidency Ţeljko Komšić (chairman)

Nebojša RadmanovićBakir Izetbegović

State Prime Minister Nikola Špirić (Tehnical mandate)

Federation of B&H

President Ţivko Budimir (HSP)

First Vice-President Mirsad Kebo (SDA)

Second Vice-President Svetozar Pudarić (SDP)

Prime Minister Nermin Nikšić (SDP)

Republic of Srpska

President Milorad Dodik (SNSD)

First Vice-President Emil Vlajki (NDS)

Second Vice-President Enes Suljkanović (SDP)

Prime Minister Aleksandar Dţombić (SNSD)

Key political parties in B&H

Social Democratic Party (SDP) Left

Party of Independent Social

Democrats (SNSD)Left - Center

Party of Democratic Action (SDA) RightCroation Democratic Union (HDZ) Right

Serbian Democratic Party (SDS) Right

(HDZ 1990) Right

Croation Party of Rights (HSP) Right

Future (NSRZB) Left

Opposition Parties

Alliance for better future (SBB) Right - Center

Party of Democratic Progress (PDP) Center

(SBiH) Right

Democratic People's Party (DNZ) RightDemocratic People's Alliance (DNS) Center

Politics

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 5/12

5

Slowing down in European economiestook its first impact on B&H economy

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: State and Entity Agencies for Statistics, RaiffeisenRESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Industrial production and construction sector

After industrial production delivered first signs of slowing-down

in August 2011 (+4.5% yoy) and in September (+1.8% yoy),positive momentum almost diminish in October 2011 asindustry reported growth by mild 0.6% yoy, which representsthe lowest increase in 12 months. Fading base affect andworsening of the global economic momentum mutually contribute to lower industrial statistics while decreasing trendseems not to be temporary. Thus, in October 2011, “Miningand quarrying” and “Electricity gas and water supply”evidenced positive growth rate by +3.1% yoy and +4.1% yoy while at the same time “Manufacturing” evidenced negativesentiment declining by 0.9% yoy. The slump of “Manufacturing” was mostly affected by the gradual diminish

of the foreign demand for B&H industrial goods whichamplified the favorable industrial statistics in last 2 years. Accordingly, industrial output in overall terms continue to slideand stood at +6.1% yoy for period “Jan-Oct 2011” but with allthree sections in expansion: “Mining and quarrying” +18.5%yoy, “Manufacturing” +4.7 and “Electricity, gas and watersupply” +4.3% yoy. Nevertheless, by the end of 2011 weenvisage further slowdown of industrial output due to lackingof external demand which has paramount importance for theindustrial statistics. Although, the rejuvenate risk of the globalrecession could bring some volatile rates in Q4 2011, weremain positive on overall drift of industrial production (+6.5%yoy) solely owed to rapid performance in the first semester of 2011.

The construction sector which mostly suffered during the globalrecession, after two years of recession finally reported first signsof recovery in 2011. However, statistics on construction sectoris switching the opposite sides from month to month.Furthermore, after negative performance reported inSeptember 2011 in both, (FB&H and RS), value of performedconstruction works in October 2011 once again was greenish(+11.7% yoy in FB&H and 5.5% in RS). Hence, we do expectmild positive contribution of the construction sector to GDPgrowth in 2011 mostly due to low statistics base. However, therevival of the construction remains fairly pessimistic in year tocome, as political stalemate is repealing considerableinvestments in construction and delaying major publicinfrastructural projects (Corridor Vc, new hydro-plantsbuilding).

Foreign trade

The foreign trade of B&H which brightened the macroeconomicpicture of the country in recent period is still lively although theweaker foreign demand will definitely take its toll in month tocome. Analyzing the quarterly statistics on B&H export, thedownward trend was notable already in Q3 2011 whenexports grew by 13% yoy…

Labor market figures

Contruction sector vs industrail output

Industrial production (yoy)

Real Economy

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 6/12

6

Real GDP of 1.9% yoy is expected in 2011due to strong rebound in H1 of 2011

Source: Central Bank of B&H (CBBH), Raiffeisen RESEARCH

Source: Entity Agency ’s for Statistics, CBBH, RaiffeisenRESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

…. which is the lowest quarterly growth rate since the end of 2009. In October 2011, exports kept its rapid growth on yoy

level (+17% yoy) while at the same time reported monthly decline by 5% which represents the largest monthly fall in2011. Consequently, in 10 months of 2011 total realizedexports of goods amounted to BAM 6.8 billion (+17.4% yoy)benefiting by the strong figures in “Mineral products”, “Basemetals” “Machinery and mechanical appliances” whichaccounts to more than 50% of B&H export. The importsreported more or less the same dynamics, also showing firstsinges of calm-down in Q3 slipping to +10% yoy. In Oct-2011imports grew by 15% yoy and declined by 2.2% compared tomonth before. Accordingly, in period “Jan-Oct 2011” importsof goods reached value of BAM 12.8 bn (+15.2% yoy) with

“Mineral products”, Machinery” and “Prepared foodstuff” askey categories. Consequently, in 10 months of 2011, B&Htrade deficit totaled to BAM 5.9 bn with export/import ration of 53.5%. Hence, taking into account the gloomy perspective of the global economy coupled with the unfavorable foreign tradestructure of B&H (which depends on just few markets: Croatia,Germany, Italy and Serbia), it is evident that B&H will not beable to mitigate the slump of the foreign demand in period tocome, while only question remain how strong the impact of theglobal slow-down will be on B&H export performance.However, due to rebound in first semester of 2011 we do notquestioned the positive overall exports performance in 2011which will outpace the imports figures and remain the key driver of the positive economic performance in 2011.

Labor market and domestic consumption

Despite quite robust economic performance in H1 2011, B&Hdid not manage to report any significant progress related tothe labor market conditions as the major downside risk for theB&H economy. Furthermore, B&H has the highest officialunemployment rate (43.4%) in Europe with outlook on furtherrising. At the same time, average gross and net wagescontinue to growth with single-digit growth rates (yoy) whichare still bellow the inflation level. Average net wages in Sep2011 stood at BAM 813 (+1.8% yoy) while average gross

wages settled BAM 1,286 (+4.2% yoy). Therefore, revival of the domestic demand in 2011 will be limited to modestrecovery of domestic consumption which is the leadingcategory within the GDP. However, we reckon that domesticconsumption will finally contribute to GDP growth in 2011 aftertwo years of negative performance. Despite of the fragile labormarket figures, other indicators shows a moderate expansion(retail trade, Indirect Tax Authority, Retail loans andremittances). Taking into account all above-mentioned trendsof main drivers of private consumption, we expect to seepositive drift by 2.5% yoy respectively. Hence, we estimate realGDP growth of 1.9% yoy in 2011 which should be

accomplished due to strong rebound of exports and industrialproduction reported in first semester of 2011.

Key GDP categories (% yoy)

Retail trade and import figures (yoy)

B&H trade balance (yoy)

Real Economy

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 7/12

7

Inflation level eased to some extend in Oct.11But still threatens to reaccelerate by the end of year

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

After reaching its peak in May 2011 (+4.2% yoy) the inflationpressure eased to some extend during next few months but still

threatens to reaccelerate by the end of the year. Furthermore,the moderate improvement in the world markets whichcontributed to weakening of imported price pressure in Q2,was mostly compensated with hikes in gas (May) and electricity prices (July), keeping the inflation level on more or less thesame level. Hence, in September 2011 inflation level peakedto 4.0% yoy followed by slight cooling-down to 3.7% yoy inOctober 2011. The lower inflation level reported in October2011 is mostly result of the lower inflation pace in section“Housing, water, electricity, gas and other fuels” (+3.0% yoy)as result of the higher statistics base as in 2010 the electricity prices in October were calculated by higher (winter) tariffs.

Consequently, the consumer prices in period, January – October 2011 were higher by 3.7% yoy flavored by the hikes in“Alcohol and tobacco products” +8.1% yoy, “Transport“+7.5% yoy and “Food and non-alcoholic beverages” + 6.3%yoy. On the other hand, prices were lower in “Clothing andfootwear” by 7.5% yoy and “Health” by 2.1% yoy.

In months to come, due to new upward correction of naturalgas prices (second time in 2011) coupled with earlier hike inelectricity prices, we expect additional broad-base increase inall division within CPI structure by the principle of domino-effect. The increase of natural gas prices by 13.89% (from 01thNovember 2011) will directly influence the ““Housing, water,electricity, gas and other fuels” and “Food and non-alcoholicbeverages” divisions which accounts to 59.4% of CPI basket.This will additionally hamper the Purchasing power of the B&Hcitizens which is among the lowest in Europe (27% of the EUaverage GDP in PPPs). Consequently, the price pressurecoupled with the rising unemployment will mutually slow downthe more prominent revival of personal consumption which willmostly benefiting from the low statistic base affect in previousyears. Hence, we estimate that overall inflation pressure couldpeak to 4.0% yoy respectively, which is still moderate levelcompared to the estimated inflation levels from countries inregion (Serbia - 11.3% yoy, Romania – 5.9% yoy, Bulgaria –

4.3% yoy, Albania – 3.6% yoy Croatia – 2.3% yoy).

For 2012, we expect overall inflation to ease down to feeblelevel of 2.3% yoy due to global economic slowdown which willdeliver much lower imported prices, particularly prices relatedto oil and mineral products which were the main supply-sidefactors of CPI growth in 2011. The additional one-off hikes ondomestic supply side are not probable as well. Accordingly, thementioned factors will all lead to halved inflation level in 2012by 2.3% yoy respectively.

Inflation and real GDP growth

Consumer price index (yoy)

Structure of consumer price index (%)

Inflation

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 8/12

8

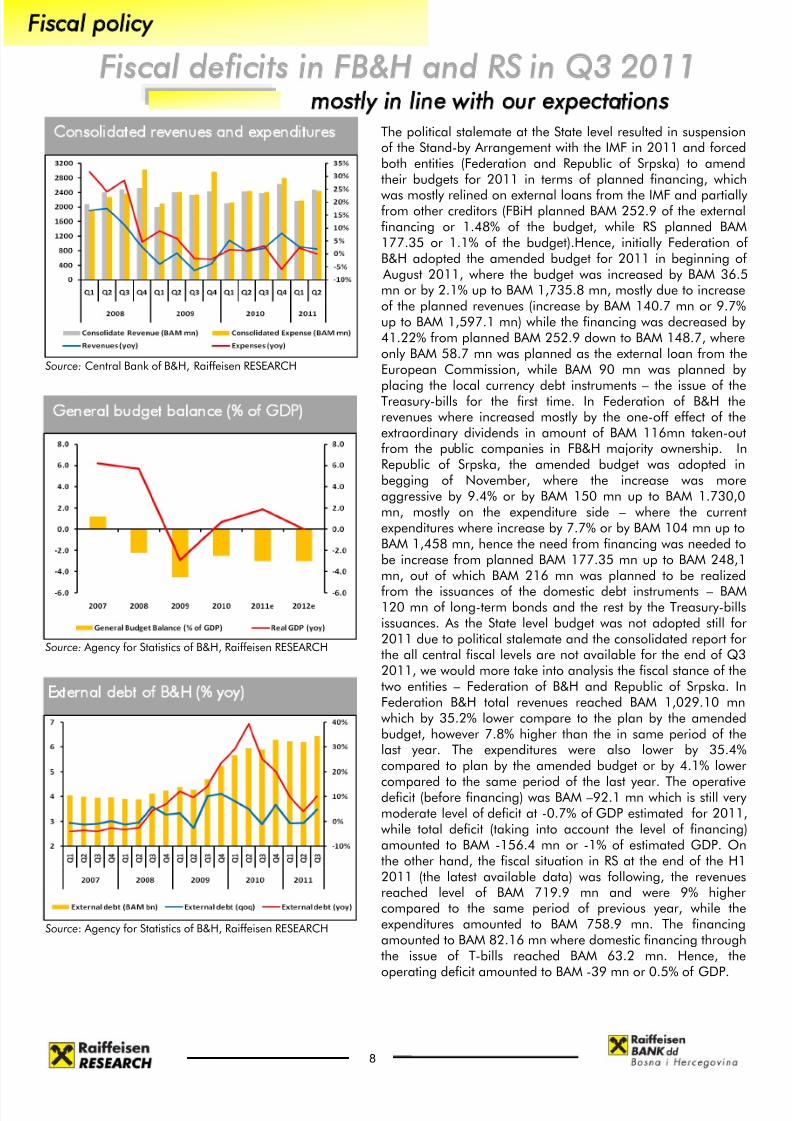

Fiscal deficits in FB&H and RS in Q3 2011mostly in line with our expectations

Source: Central Bank of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

The political stalemate at the State level resulted in suspensionof the Stand-by Arrangement with the IMF in 2011 and forcedboth entities (Federation and Republic of Srpska) to amendtheir budgets for 2011 in terms of planned financing, which

was mostly relined on external loans from the IMF and partially from other creditors (FBiH planned BAM 252.9 of the externalfinancing or 1.48% of the budget, while RS planned BAM177.35 or 1.1% of the budget).Hence, initially Federation of B&H adopted the amended budget for 2011 in beginning of August 2011, where the budget was increased by BAM 36.5mn or by 2.1% up to BAM 1,735.8 mn, mostly due to increaseof the planned revenues (increase by BAM 140.7 mn or 9.7%up to BAM 1,597.1 mn) while the financing was decreased by 41.22% from planned BAM 252.9 down to BAM 148.7, whereonly BAM 58.7 mn was planned as the external loan from theEuropean Commission, while BAM 90 mn was planned by placing the local currency debt instruments – the issue of theTreasury-bills for the first time. In Federation of B&H therevenues where increased mostly by the one-off effect of theextraordinary dividends in amount of BAM 116mn taken-outfrom the public companies in FB&H majority ownership. InRepublic of Srpska, the amended budget was adopted inbegging of November, where the increase was moreaggressive by 9.4% or by BAM 150 mn up to BAM 1.730,0mn, mostly on the expenditure side – where the currentexpenditures where increase by 7.7% or by BAM 104 mn up toBAM 1,458 mn, hence the need from financing was needed tobe increase from planned BAM 177.35 mn up to BAM 248,1mn, out of which BAM 216 mn was planned to be realized

from the issuances of the domestic debt instruments – BAM120 mn of long-term bonds and the rest by the Treasury-billsissuances. As the State level budget was not adopted still for2011 due to political stalemate and the consolidated report forthe all central fiscal levels are not available for the end of Q32011, we would more take into analysis the fiscal stance of thetwo entities – Federation of B&H and Republic of Srpska. InFederation B&H total revenues reached BAM 1,029.10 mnwhich by 35.2% lower compare to the plan by the amendedbudget, however 7.8% higher than the in same period of thelast year. The expenditures were also lower by 35.4%compared to plan by the amended budget or by 4.1% lower

compared to the same period of the last year. The operativedeficit (before financing) was BAM –92.1 mn which is still very moderate level of deficit at -0.7% of GDP estimated for 2011,while total deficit (taking into account the level of financing)amounted to BAM -156.4 mn or -1% of estimated GDP. Onthe other hand, the fiscal situation in RS at the end of the H12011 (the latest available data) was following, the revenuesreached level of BAM 719.9 mn and were 9% highercompared to the same period of previous year, while theexpenditures amounted to BAM 758.9 mn. The financingamounted to BAM 82.16 mn where domestic financing throughthe issue of T-bills reached BAM 63.2 mn. Hence, theoperating deficit amounted to BAM -39 mn or 0.5% of GDP.

External debt of B&H (% yoy)

General budget balance (% of GDP)

Consolidated revenues and expenditures

Fiscal policy

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 9/12

9

B&H banking sector as of 30.09.2011 reported net profit of BAM 82.1 million

Source: Central Bank of B&H, Raiffeisen RESEARCH

Source: Central Bank of B&H, Raiffeisen RESEARCH

Source: Central Bank of B&H, Raiffeisen RESEARCH

The financial soundness indicators in Q3 2011 mostly continued with downward trend. The Capital Adequacy (Netcapital to RWA) in Q3 2011 went down to 15.3% (from 15.5%in Q2) which represents the lowest value of the Capital Adequacy since Q2 2010. Furthermore, the NPAs to totalassets jumped from 8.6% in Q2 to 9.1% in Q3 2011 while atthe same time NPLs to total loans reached value of 12.6%from 11.8% in Q2 2011. On the other hand, the liquidity of the banking sector showed slight increase to 27.2%. Thebanking sector profitability remain stable with the profitability indicators of ROA = 0.4% and ROE = 3.5%. Furthermore,according to the Entity Banking Agencies data, bh. bankingsector as of 30.09.2011 reported positive financial results of BAM 82.1 million, comparing to the net loss of BAM 77.2reported in same period of 2010. The net profit was achievedby 22 banks (13 in FB&H and 1 in RS) in total amount of BAM

141.7 million while negative result was reported by 7 banks (6in FB&H and 1 in RS) in total amount of 59.6 million.

September 2011 delivered further strengthen of the B&Hbanking sector growth, as overall credit and depositperformance continued to report upward momentum.Furthermore, total loans of B&H banks grew by 7.3% yoy (representing the highest yoy growth rate reported since May 2009) up to BAM 15.29 bn. The credit performance is stillbenefiting from the upbeat in Corporate loans which also inSep-2011 reported the highest growth rate since May 2009,+8.6% yoy growing to BAM 8.1 bn. At the same time, thegrowth of the second largest loans category “Retail loans”

slowed down somewhat during Sep- 2011 increasing by 2.9%yoy up to BAM 6.46 billion. On the other side, value of totaldeposits by the end of Q3 2011 amounted to BAM 12.83billion (+4% yoy) The positive deposits performance is solely owed to unrelenting upturn in “Retail deposits” as the only deposit category which posted positive performance in 2011.Thus, the “Retail savings” as end of September totaled toBAM 6.88 billion increasing by 11.7%

Taking into account the latest negative developments on theworld financial markets, which will consequently lead toworsening of the domestic banks external financingpossibilities, we do expect slow-down in the credit

performance with annual average growth rate of about 5%yoy in Q4 2011. Furthermore, the rising risk aversion willnarrow the chance for further decline in active interest rateswhich will by the end of 2011 remain at the approximately same level as in Q3 2011. In 2012 we could expect morepronounced drying-up of the credit growth in B&H, as aindirect consequence of the European Banking Agency stipulation for achievement of 9% Tier 1 ration until June 30 th for all EU-zone banks. Hence, as the most of the EU ownedBH banks would need to achieve the level of risk weightedassets with purpose to support achievement of Tier 1adequacy ratio at the group level, this should consequently

lead to decline in overall credit growth rates in BH bankingsector.

Interest rates on loans with currency clause

Credit performance by categories (yoy)

Total loans and deposits (yoy)

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 10/12

10

Total turnover on B&H markets fuelled byprimary markets developments

Source: Sarajevo and Banja Luka Stock Exchange, RaiffeisenRESEARCH

Source: Sarajevo and Banja Luka Stock Exchange, RaiffeisenRESEARCH

Source: Sarajevo Stock Exchange, Raiffiesen RESEARCH

November’s trade on bh .markets hits record high valuethanks to primary market developments in particular public

offering of bonds and T-bills, while at the same time ordinary trade with shares and bonds remain extremely poor.Furthermore, first public offering of RS bonds which was heldon 15th and 16th November 2011 was 100% successful withBAM 108.56 million of sold bonds value. The last month waswealthy with the T-bills auctions as well. The third auction of RS T-bills was held on 29.11.2011 with 1570 T-billsauctioned, total value of BAM 15,283,950. The Auction wasclosed by a single equilibrium price of 97.35% with an interestrate of 4.0985%. Earlier on Sarajevo Stock Exchange (SASE)(November 08th) was held the second auction of 6M Treasury Bills of Federation B&H with 2500 auctioned T-bills, total valueof BAM 24,714,958.70. Auction was concluded with average

price of 98.863% or average interest rate of 2.31%. Hence,total value of bonds and T-bills public offerings amounted toBAM 148.6 million representing 90% of total turnover realizedin domestic markets in November 2011. As we expected, theprimary markets development are getting more intensive asthe entity Ministries of Finance are seeking the way to financethe budget deficit as they were left out of the planed tranchesfrom the IMF Stand–by Arrangement due to political stalemateon the State level. Therefore, in the forthcoming period we canexpect continuation of the primary markets issues of both,long-term and short-term debt instruments. Furthermore,according to the ambitious entity governments plans for the

new debt instruments issues in 2012, FB&H plans to issue BAM200 mn of T-bills with (3M – 6M maturity) while at the sametime RS plans auction of BAM 80 million of T-bills (6M – 9M).Furthermore, after first public offering of RS bonds, we couldexpect the same scenario in FB&H with the first 3Y bonds to beissued in amount of BAM 100 million according to thepreliminary plans of the Ministry of Finance of FB&H.

On the other side, equity markets continue to report decline intrading volumes. The financial crisis in euro-zone results inwithdraws the foreign investors while domestic investors arenot sufficient to support equity volumes traded. As a result, inNovember 2011 total turnover on both bh. markets amounted

to BAM 9.96 million or 6% of total turnover. The poor liquidity was followed by the major slump of the main blue-chipindexes. Furthermore, SASX-10 ended month at 785 pts andfurther sank to 760 pts by the middle of December 2011which is loss by 19.5% Ytd. At the same time, the BIRS as of end of November 2011 plunged to 892.5 index points andwent further into red to 835 by the middle of December 2011,reporting -12.6% Ytd. Hence, the B&H equity markets will notbe able to stay unaffected by the global economic turmoilwhich will we reflected in further deterioration of liquidity andindex values.

Most liquid FCS bonds - SASE (yield %)

Key indexes on SASE and BLSE

Ordinary trade with shares and bonds on SASEand BLSE

Equity and Debt Market

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 11/12

11

B&H is facing stagnation in 2012 reflected inforecasted 0% yoy real GDP growth

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

Source: Agency for Statistics of B&H, Raiffeisen RESEARCH

B&H in first semester of 2011 managed to report vigorousdynamics in industrial production and exports which were the

main GDP drivers (by production and expenditure sidemethodology) same as in year before. Hence the robustgrowth in the early months of the year was followed by amoderate slowing-down in economic momentum in Q3, asthe slump of economic fundamentals in euro-zone took its firstimpacts on BH economy. Accordingly the final quarter is nowlikely to see further deterioration in economic momentum.However, we estimate real GDP growth at 1.9% yoy in 2011which should be accomplished due to strong rebound of exports and industrial production reported in the first semesterof 2011 followed by slowing-down reported in the last twoquarters of 2011.

Furthermore, the recessionary trends in euro-zone should peakin H1 2012 and strongly take its toll on BH economy withsimilar economic scenario seen in “first wave of economiccrisis” back in 2008. Further worsening of external demandwill engulf the export and export-oriented industrial productionto low one-digit figures. The external demand from the euro-zone will fade away, in particular from Italy and Germany which were the main BH trade partners in euro-zone so far.Hence, the positive momentum in these two key economiccategories will be insufficient for overall positive growth as weexpect slump of domestic demand again down to recessionary levels. Moreover, cuts in risk weighted assets will lead todrying-up of credit flows from EU-owned BH banking sector,consequently leading to negative performance of credit-drivenprivate investments and consumption. Also the real cuts in netand gross wages along with limited rise in unemployment rateup to 43.4% will mutually hamper the domestic consumptionwhich should once again deliver mild negative momentum by 0.5 yoy in real terms. The political stalemate will mostprobably prolong further in H1 2012, which along witheconomic crisis will lead to further decline in FDIs inflows.Consequently, the gross fixed capital formation will also slumpby 5% yoy in 2012 after expected positive developments in2011 (estimate of real growth +6.0%).

Taking into account all above-mentioned trends of maindrivers of economic growth, we expect to see stagnation of BHeconomy in 2012 reflected through forecasted 0% yoy realGDP growth. Moreover, having in mind the gloomy EUperspective, BH economy could once again be stuck intorecession in 2012 even though it is still not our basic scenario.Hence, the final recovery can not be expected before 2013,although the growth rates will still be well below the pre-crisisperiod when average real GDP growth stood at respectablelevel of 5% yoy (2000-2008).

Real GDP of B&H vs real GDP of euro zone

Unemployment rate and real GDP

Industrial production and CPI (yoy)

8/3/2019 B&H Monthly Economic Report - December 2011

http://slidepdf.com/reader/full/bh-monthly-economic-report-december-2011 12/12

12

Raiffeisen Research

Raiffeisen BANK d.d. Bosna i HercegovinaInvestment Banking DivisionSanja Korene, Head of Investment Banking; Phone: + 387 33 28 71 22, e-mail: sanja.korene@rbb-

sarajevo.raiffeisen.atIvona Kristić, Head of Research; Phone: + 387 33 28 77 84, e-mail: [email protected] Grgić, Head of Capital Markets; Phone: + 387 33 28 71 26, e-mail:[email protected] Cenanović, Head of Brokerage Business and Investment Advisory; Phone: +387 33 28 7647, e-mail: [email protected]

Raiffeisen CAPITAL a.d. Banja LukaNataša Majstorović, Director; Phone: + 387 51 23 14 90, e-mail: natasa.majstorovic@rbb-

sarajevo.raiffeisen.at

PublisherRaiffeisen BANK d.d. Bosna i Hercegovina

Zmaja od Bosne bb, 71000 Sarajevowww.raiffeisenbank.baRaiffeisen direct info: +387 33 75 50 10 • Fax: +387 33 21 38 51

This publication was completed on December 26 th, 2011

Impressum

DisclaimerThis publication is prepared and published by Raiffeisen BANK d.d. Bosna i Hercegovina, Sarajevo(hereafter: Raiffeisen BANK). The publication is prepared only for information purposes and any of itsparts can not be defined as a proposal or invitation for purchase/sale of any assets, security or rightwhich is mentioned, and cannot be a substitute for an independent investment advice, and noobligation by its publishing is made for Raiffeisen BANK. The information, opinions, analyses,conclusions, prognoses and projections issued within the publication are based on publicly available

data, which Raiffeisen BANK rely on, but cannot guarantee for their accuracy.

All information, opinions, analyses, conclusions, prognoses and projections issued within thepublication are subjects to change which depends on change of source of information and changesoccurred in period between moment of creating and reading of the publication. No proposals orguaranties are stated or implied, and Raiffeisen BANK or its employees cannot take any responsibility/obligation for errors, omissions, misstatements, negligent or any direct or consequentialloss or damage suffered by any person as a result of relying on any part of the publication. Finaldecision for purchase/sale of any assets, securities or right is solely responsibility of the reader. Thedocument and its parts can not be copied or in any way reproduced without stating the informationsource.

![Monthly Economic Reviewbsl.gov.sl/MER October 2019- Finalised Version.pdf · Monthly Economic Review October 2019 Publisher: The Monthly Economic Review [MER] is published by the](https://static.fdocuments.in/doc/165x107/5eddde83ad6a402d66691757/monthly-economic-october-2019-finalised-versionpdf-monthly-economic-review-october.jpg)