BEYOND LENDING: MDB’S FINANCIAL ROLE AFTER THE CRISIS

15

BEYOND LENDING: MDB’S FINANCIAL ROLE AFTER THE CRISIS Guillermo Perry Center for Global Development Innovative Financial Solutions for Development AFD, WB and Gates Foundation Paris, March 4-5

-

Upload

elijah-logan -

Category

Documents

-

view

30 -

download

1

description

BEYOND LENDING: MDB’S FINANCIAL ROLE AFTER THE CRISIS. Guillermo Perry Center for Global Development Innovative Financial Solutions for Development AFD, WB and Gates Foundation Paris, March 4-5. THE FACTS: Growing access of emerging countries to private markets, but with high volatility. - PowerPoint PPT Presentation

Transcript of BEYOND LENDING: MDB’S FINANCIAL ROLE AFTER THE CRISIS

BEYOND LENDING:MDB’S FINANCIAL ROLE

AFTER THE CRISIS

Guillermo Perry

Center for Global Development

Innovative Financial Solutions for Development

AFD, WB and Gates Foundation

Paris, March 4-5

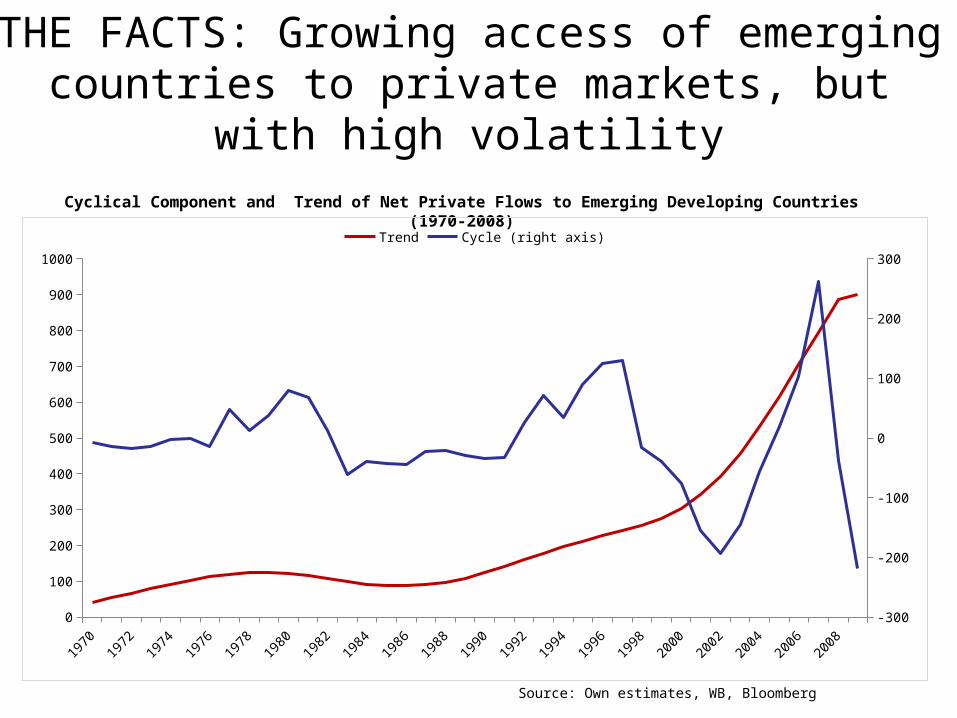

THE FACTS: Growing access of emerging countries to private markets, but with high volatility

Cyclical Component and Trend of Net Private Flows to Emerging Developing Countries (1970-2008)

Source: Own estimates, WB, Bloomberg

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

0

100

200

300

400

500

600

700

800

900

1000

-300

-200

-100

0

100

200

300

Trend Cycle (right axis)

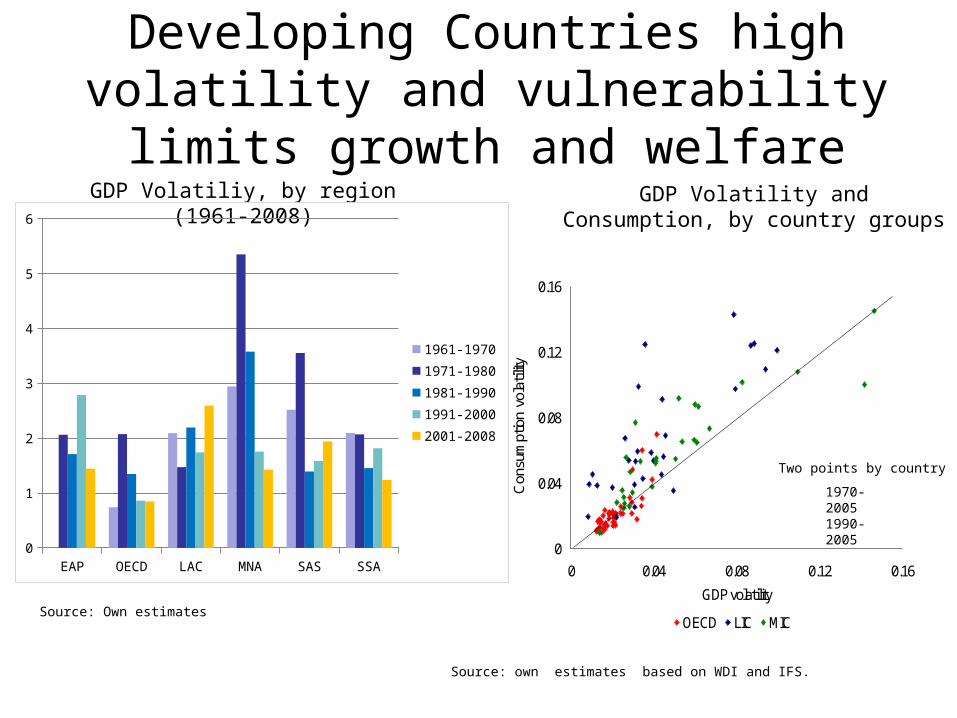

THE PROBLEM TO SOLVE: Developing Countries high volatility and vulnerability limits growth and welfare

Source: Own estimates

GDP Volatiliy, by region (1961-2008) GDP Volatility and Consumption, by country groups

Two points by country

1970-20051990-2005

0

0.04

0.08

0.12

0.16

0 0.04 0.08 0.12 0.16

Con

sum

ptio

n vo

latil

ity

GDP volatility

OECD LIC MIC

Source: own estimates based on WDI and IFS.

EAP OECD LAC MNA SAS SSA0

1

2

3

4

5

6

1961-1970

1971-1980

1981-1990

1991-2000

2001-2008

Developing Countries excess volatility is due to exogenous and endogenous causes

Source: Own calculations.

1975-2005 1990-2005

Oil; 1%Capital Flows Volatility; 9%

Financial Development; 51%

Terms of Trade Volatil-ity; 17%

Fiscal Volatility; 21%

Money Growth Volatility; -1%

Fiscal Volatility; 22%

Money Growth volatil-ity; 16%

Financial Development; 12%Capital Flows volatility; 8%

Terms of trade Volatility; 36%

Higher exposure to Exogenous Shocks

Volatility of Terms of Trade1975-2005

Frequency of natural disasters 1975-2005

Crisis Episodes

0

1

2

3

4

5

6

7

8

9

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

EM´s CrisisAsian Crisis

Crisis of the European Monetary System

LAC debt crsis

Source: Cavallo and Frankel (2006).

Source: Calderón, C, WB (2007)Source: Calderón, C, World Bank. (2007).

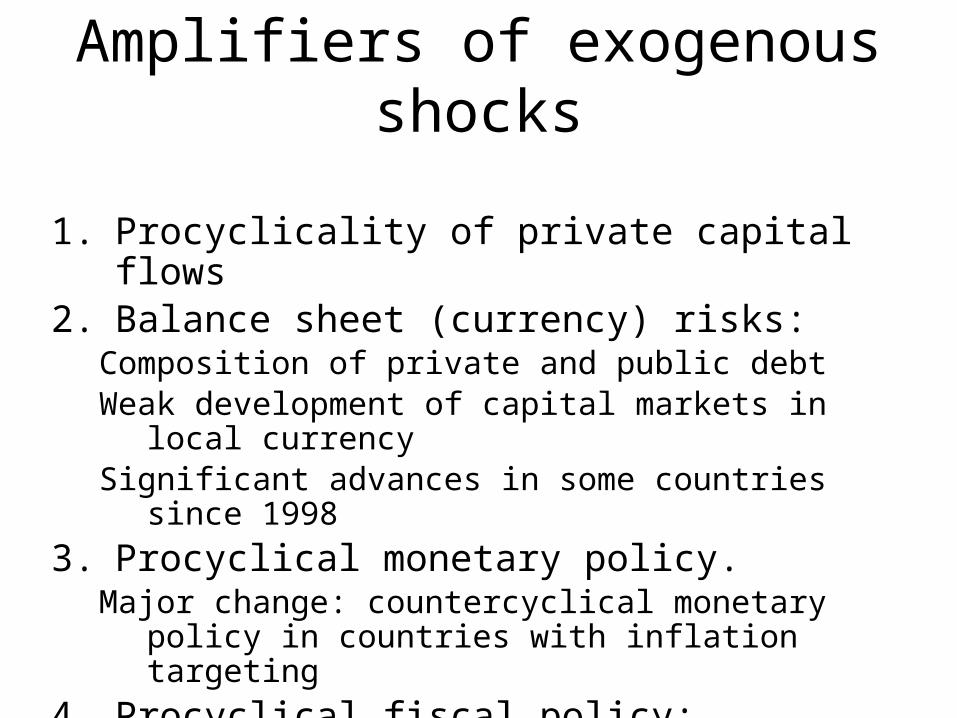

Amplifiers of exogenous shocks

1. Procyclicality of private capital flows2. Balance sheet (currency) risks:

Composition of private and public debtWeak development of capital markets in local currencySignificant advances in some countries since 1998

3. Procyclical monetary policy. Major change: countercyclical monetary policy in

countries with inflation targeting

4. Procyclical fiscal policy: With few exceptions (e.g. Chile)

Dealing with exogenous shocks:potential options

Source: Own elaboration

Action

Shock

Coping after the fact

Prevention: Risk Reduction

Self Insurance: Saving

Market Insurance/Hedging

Terms of Trade

Current Account and (pro cyclical) fiscal adjustment, Aid

DiversifyExports

Stabilization Funds Commodity Price Futures, Forwards and Options/Indexed Debt (TOT, CP)

Natural Disasters

Aid, Fiscal adjustment

ZoningBuilding codes

Emergency Funds Insurance & Reinsurance/CAT’s

Capital Flows Current Account and (pro cyclical) fiscal adjustment, Aid

Debt level & compositionCapital Market DevelopmentDe dollarization

International Reserves

Contingent Credit LinesCurrency and interest derivativesIndexed Debt (GDP)External debt in domestic currencies

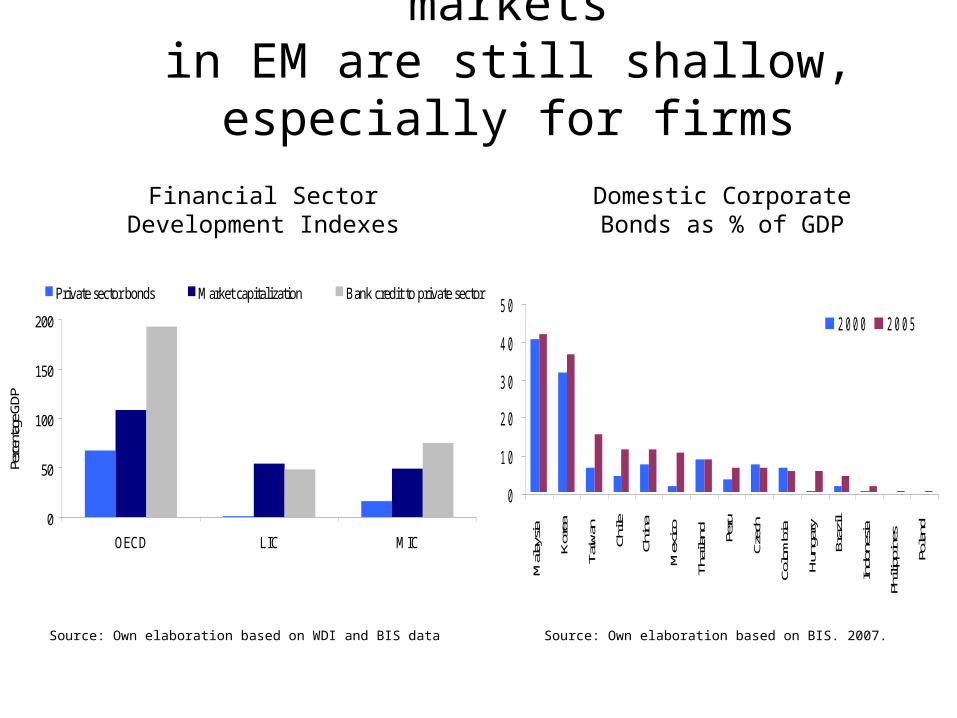

CHALLENGE: Domestic capital marketsin EM are still shallow, especially for firms

0

1 0

2 0

3 0

4 0

5 0

Mala

ysia

Kore

a

Taiw

an

Chile

Chin

a

Mex

ico

Thail

and

Peru

Czec

h

Colo

mbi

a

Hung

ary

Braz

il

Indo

nesia

Phili

ppin

es

Polan

d

2 0 0 0 2 0 0 5

Domestic Corporate Bonds as % of GDP

Source: Own elaboration based on BIS. 2007. Source: Own elaboration based on WDI and BIS data

Financial Sector Development Indexes

0

50

100

150

200

OECD LIC MIC

Perc

entag

e GDP

Private sector bonds Market capitalization Bank credit to private sector

CHALLENGE: Use of currency derivatives by EM’s still very low

0

0 . 3

0 . 6

0 . 9

1 . 2

L a t i n A m e r i c a A s i a C e n t r a l E u r o p e O E C D

1 9 9 8 2 0 0 1 2 0 0 4

0

1

2

3

4

5

L a t in A m e r ic a A s ia C e n t r a l E u r o p e O E C D

1 9 9 8 2 0 0 1 2 0 0 4

0

0 .2

0 .4

0 .6

L a t in A m e r ic a A s ia C e n t r a lE u r o p e

O E C D

1 9 9 8 2 0 0 1 2 0 0 4

FX Forwards as % GDP FX Swaps as % GDP

FX Options as % GDP

Source: Own elaboration based on BIS. 2007. “Financial stability and local currency bond markets”.

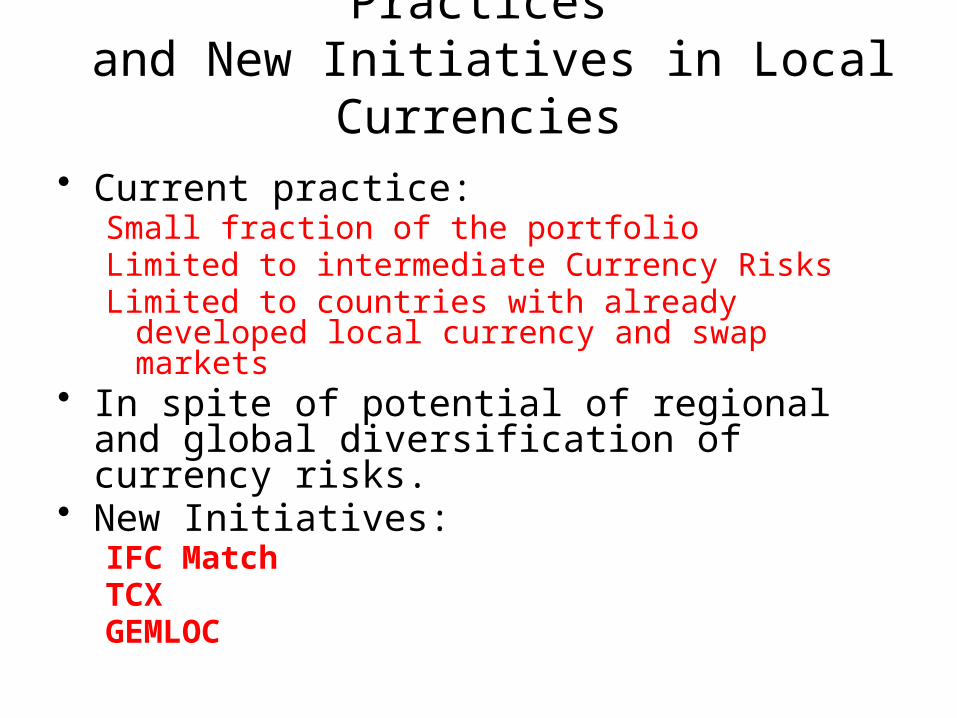

OPPORTUNITY: MDB’s Current Practices and New Initiatives in Local Currencies• Current practice:

Small fraction of the portfolioLimited to intermediate Currency RisksLimited to countries with already developed local

currency and swap markets• In spite of potential of regional and global

diversification of currency risks.• New Initiatives:

IFC MatchTCXGEMLOC

OPPORTUNITY: High Stabilizing Potential of GDP indexed bonds

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

-0.15

-0.1

-0.05

0

0.05

0.1

0.15 Am Am Est. Cycle

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

-0.1

-0.05

0

0.05

0.1

0.15

Amort AmortEst Cycle

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2AM AM Est Cycle

Argentina Mexico

Indonesia

Fuente: Cálculos propios, WDI, IMF.

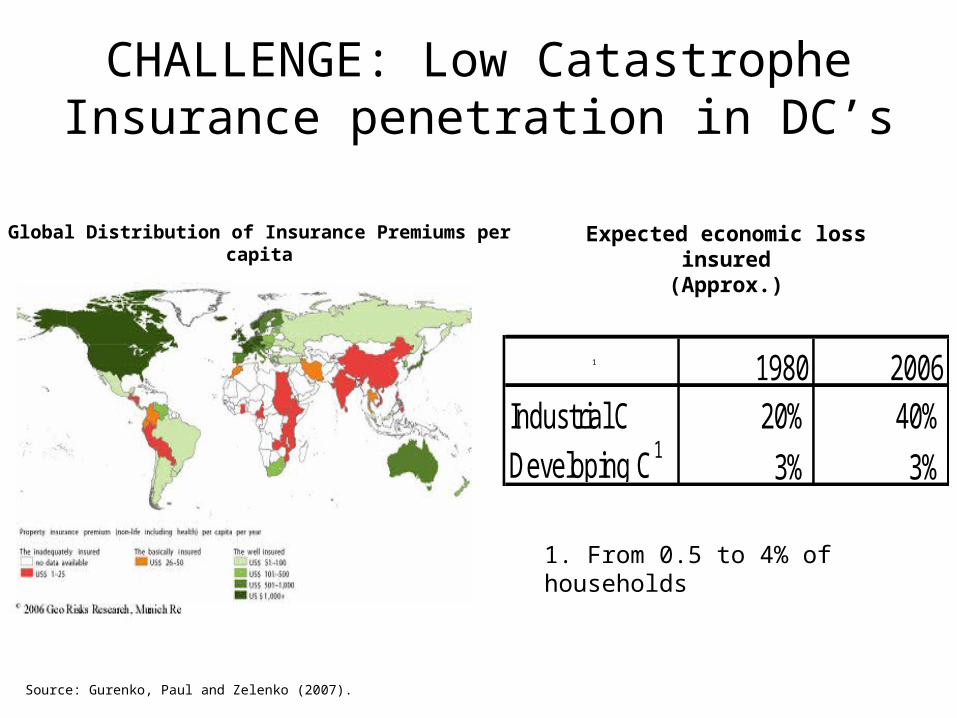

CHALLENGE: Low Catastrophe Insurance penetration in DC’s

Source: Gurenko, Paul and Zelenko (2007).

Global Distribution of Insurance Premiums per capita

Expected economic loss insured

(Approx.)

1 1980 2006Industrial C 20% 40%

Developing C13% 3%

1. From 0.5 to 4% of households

CHALLENGE: High and volatile fees of Catastrophe Reinsurance

Source: Lane Financial (2007) and Cordella and Levy yeyati, WB, (2007)

US catastrophe reinsurance price indices

Yucatán Peninsula South Pacific

Gulf of Mexico Interior

Homes 0.35% 0.12% 0.15% 0.08%

0.60% 0.30% 0.30% 0.08%

Buildings 0.35% 0.13% 0.15% 0.12%

1.40% 0.50% 0.50% 0.12%

Industrial Property 0.60% 0.25% 0.30% 0.14%

1.60% 0.80% 0.80% 0.14%

*/ -500 m from hide tide on the beach. Red numbers are values for 2004, black color for 2006

Zoning (Insured Property Location)

Zone Alfa 1

Mexico Insurance premia of hidrometeorological risk

As percentage of insured values

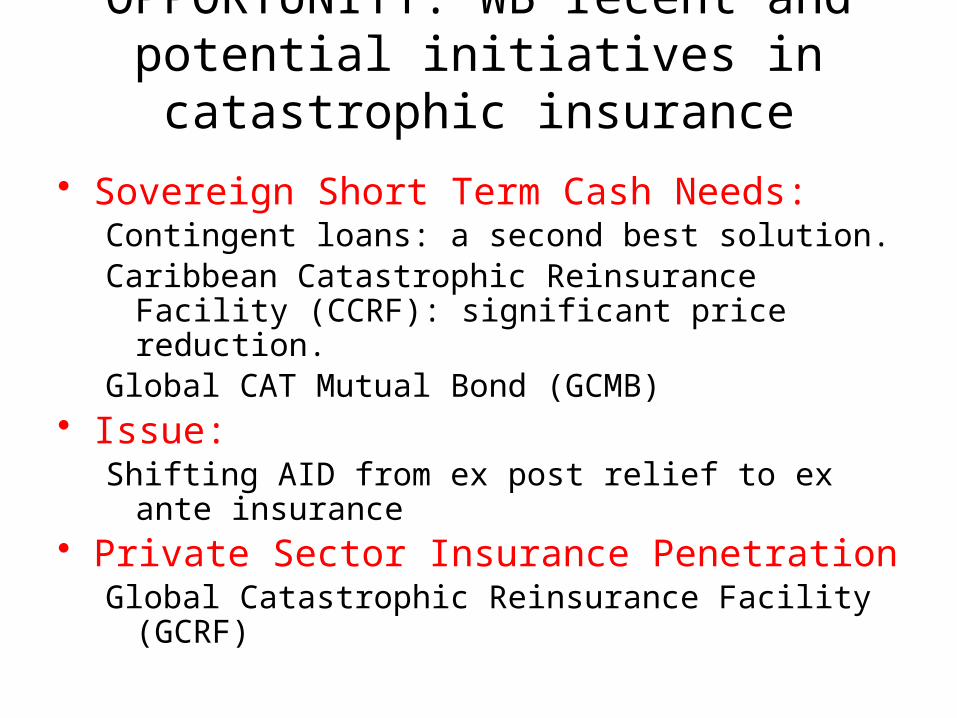

OPPORTUNITY: WB recent and potential initiatives in catastrophic insurance

• Sovereign Short Term Cash Needs:Contingent loans: a second best solution.Caribbean Catastrophic Reinsurance Facility (CCRF):

significant price reduction.Global CAT Mutual Bond (GCMB)

• Issue: Shifting AID from ex post relief to ex ante insurance

• Private Sector Insurance PenetrationGlobal Catastrophic Reinsurance Facility (GCRF)

CONCLUSIONS

• MDB´s have a key potential role in helping to develop insurance and hedging instruments and markets for developing countries.

• Thus helping them reduce vulnerabilities and macro volatility, that hinder long term growth, welfare and poverty reduction.

• The current urgent liquidity needs of EM’s should not lead MDB’s into complacency and set back efforts in financial innovation that were taking place before the crisis.