Beware of Low Frequency Data by Ernie Chan, Managing Member, QTS Capital Management, LLC.

22

Beware of Low Frequency Data Ernest Chan, Ph.D. QTS Capital Management, LLC.

-

Upload

quantopian -

Category

Economy & Finance

-

view

813 -

download

1

Transcript of Beware of Low Frequency Data by Ernie Chan, Managing Member, QTS Capital Management, LLC.

Beware of Low Frequency Data

Ernest Chan, Ph.D. QTS Capital Management, LLC.

• Previously, researcher at IBM T. J. Watson Lab in machine learning, researcher/trader for Morgan Stanley, Credit Suisse, and various hedge funds.

• Principal of QTS Capital Management, a commodity pool operator and trading advisor.

• Author: – Quan%ta%ve Trading: How to Build Your Own Algorithmic Trading Business (Wiley 2009).

– Algorithmic Trading: Winning Strategies and Their Ra%onale (Wiley 2013).

• Blogger: epchan.blogspot.com

About Me

2

GIGO

• Garbage in, garbage out is well-‐known to programmers.

• Data integrity is crucial to backtesVng trading strategies. – Common problem: Historical prices backtested weren’t the actual prices we could execute at.

– Typical outcome: backtest performance is greatly inflated compared to realisVc historical performance.

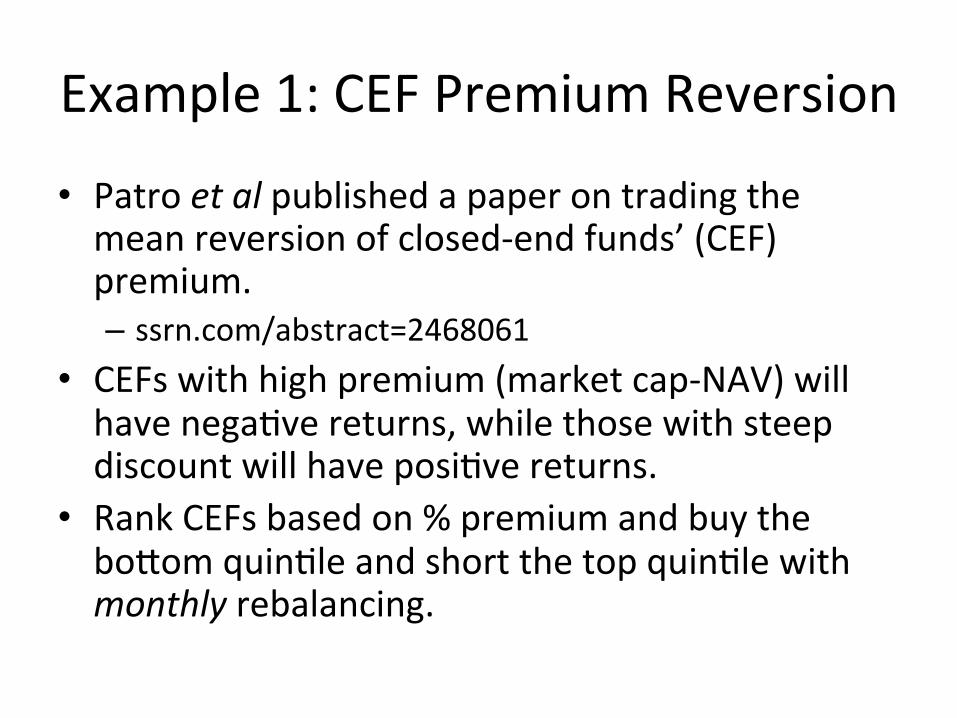

Example 1: CEF Premium Reversion

• Patro et al published a paper on trading the mean reversion of closed-‐end funds’ (CEF) premium. – ssrn.com/abstract=2468061

• CEFs with high premium (market cap-‐NAV) will have negaVve returns, while those with steep discount will have posiVve returns.

• Rank CEFs based on % premium and buy the bobom quinVle and short the top quinVle with monthly rebalancing.

Example 1: CEF Premium Reversion

• Authors obtained fund price and shares outstanding data from CRSP, and fund NAV data from Bloomberg.

• Sharpe raVo is 1.5 from 1998-‐2011. • I repeated their backtest also using CRSP prices, and fund NAV from Computstat from 2007-‐2014.

CEF Premium Reversion: closes

2008/01 2010/01 2012/01 2014/010

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Date

Cum

ulat

ive

Ret

urns

CEF Premium Reversion: midpoints

2008/01 2010/01 2012/01 2014/01-0.25

-0.2

-0.15

-0.1

-0.05

0

Date

Cum

ulat

ive

Ret

urns

Midpoints vs closes • The dramaVc differences in performance due to using closing prices vs midpoint between bid and ask prices at the close. – You wouldn’t think bid and ask prices maber for strategies that rebalance only monthly!

• Actual execuVons will use MOC (Market-‐on-‐close) or LOC (Limit-‐on-‐close) orders.

• Actual execuVon prices will be the close price (“closing cross”) at primary exchanges where aucVons take place, not consolidated closing prices which most backtests use. – Rf. Prof. Joel Hasbrouck “SecuriVes Trading” NYU Teaching Notes

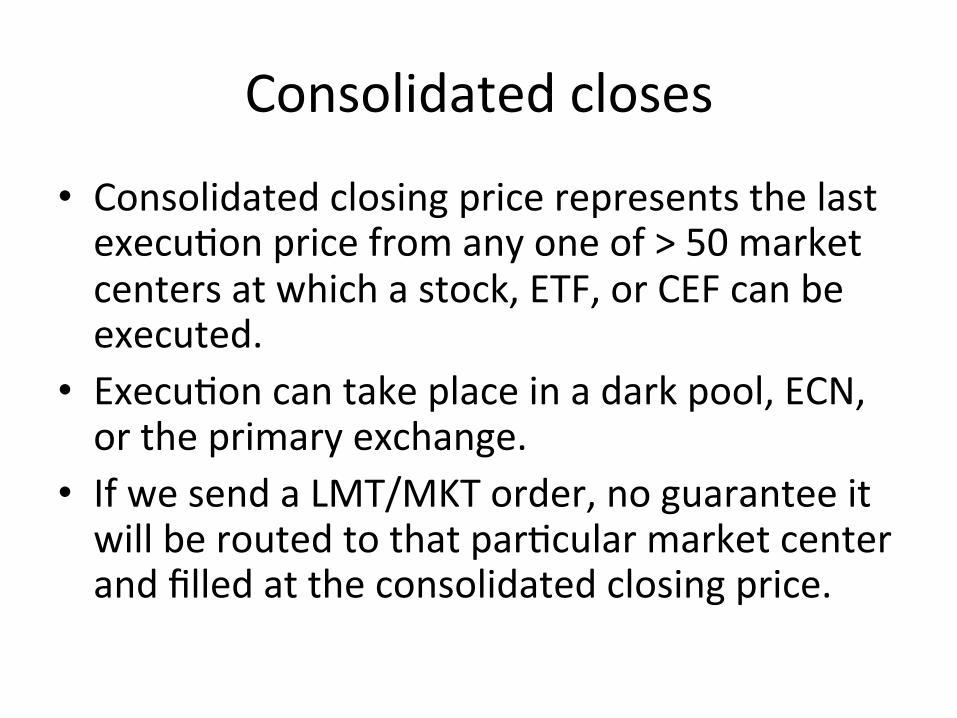

Consolidated closes

• Consolidated closing price represents the last execuVon price from any one of > 50 market centers at which a stock, ETF, or CEF can be executed.

• ExecuVon can take place in a dark pool, ECN, or the primary exchange.

• If we send a LMT/MKT order, no guarantee it will be routed to that parVcular market center and filled at the consolidated closing price.

Primary closes

• Where can we get historical primary exchange (“aucVon”, “official”, “crossing”) close prices? – Buy from the primary exchanges. – Subscribe to Bloomberg. – EsVmate using midpoints from CRSP.

• This is what I did. – Use Vck data and select the trades with the Cross flag*.

*Hat-‐Vp: Chris at QuantGo.com

Example 2: Opening gap

• Rank stocks based on their returns from previous close to today’s open: retGap.

• Apply fundamental and technical filters e.g. eliminaVng stocks which just had earnings announcements. – See my book “Algorithmic Trading”.

• Buy 10 stocks with the lowest retGap, and short 10 with the highest retGap at the open.

• Exit at the same day’s close. • Backtest from 2012-‐2014. • Live trading from mid 2013-‐2014.

Opening Gap: Backtest vs Live

2012/01 2013/01 2014/01-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Date

Cum

ulat

ive

Ret

urns

Backtest with 5 bps costLive

What happens at the open? • Backtest has already used midpoints at close: very near the closing crosses.

• Backtest also included 5 bps per trade transacVon cost.

• Live trading sVll underperformed backtest substanVally.

• Causes: – Open prices also need to use aucVon prices.

• Unfortunately CRSP does not provide bid/ask at open. – Need quotes at 9:28 (Nasdaq deadline for LOO/MOO orders) to generate trading signals.

Example 3: Futures momentum

• Intraday momentum strategy applied to various futures (E.g. RB or GC).

• Rank all trades (or quotes) in previous day’s trading session. – Long if last price above 95th percenVle.

• Exit long if last price below 60th percenVle. – Short if last price below 5th percenVle.

• Exit short if last price above 40th percenVle.

Futures momentum

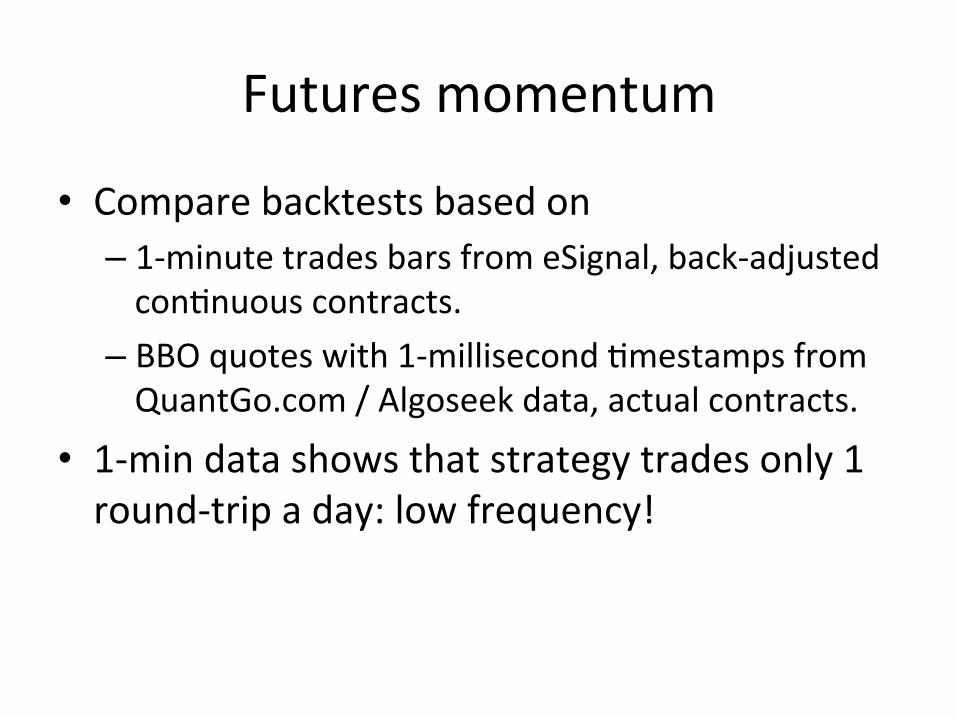

• Compare backtests based on – 1-‐minute trades bars from eSignal, back-‐adjusted conVnuous contracts.

– BBO quotes with 1-‐millisecond Vmestamps from QuantGo.com / Algoseek data, actual contracts.

• 1-‐min data shows that strategy trades only 1 round-‐trip a day: low frequency!

Futures momentum

• In all cases, 1-‐ms data produce much worse returns than 1-‐min data.

• 1-‐ms data shows that strategy someVmes flip-‐flops: rapid changes of last prices cause rapid succession of (losing) trades.

Example 4: Pair trading ETFs

• E.g. ETFs EWA (Australian stock index) and EWC (Canadian stock index) are good candidates for mean-‐reversion pair trading.

• Bollinger band strategy applied to spread. • Backtest on daily closes (aucVon or consolidated prices): good results.

• Why not live trade intraday, using Bollinger bands to set limit prices? – Expect more trading opportuniVes and more profits!

Pair trading ETFs

• Reality: Intraday live trading using InteracVve Brokers live Vck feed (250ms bars) osen suffers mysterious losses due to mysterious trades.

• Culprit: Flip-‐flopping due to order book “mini-‐flash crashes” – Small change in price on one leg leads to large % error in spread!

• These flip-‐flopping and losses disappear if we use Yahoo RealTime (1s bars).

Pair trading ETFs

• Moral of story: if you want to trade intraday, must use Vck data for backtest, even if holding period is long (e.g. hours).

• What if we restrict live data to 1-‐sec or longer bars? – This would be arVficial and nonsensical: why should we only trade at … 10:01, 10:02, 10:03, … instead of … 10:01:01, 10:01:02, 10:01:03, …?

LF backtest requires HF historical data

• CEF monthly rebalancing → need Vck data to find closing crosses (aucVon) prices (unless you have Bloomberg).

• Opening gap stocks strategy → need Vck data to find NBBO at 9:28 am and opening crosses.

• Intraday low-‐frequency futures momentum strategy → need Vck data to check for intra-‐1-‐min-‐bar flip-‐flopping/mini-‐flash crashes.

• Intraday low-‐frequency ETF mean reversion pair trading → need Vck data to check for intra-‐1-‐sec-‐bar flip-‐flopping/mini-‐flash crashes.

Conclusion

• Whether a trading strategy requires low or high frequency historical data depends not only on holding period, but also on: – How execuVon prices are determined. – How trading signals are triggered.

Thank you for your Vme!

www.epchan.com Twiber: @chanep

Blog: epchan.blogspot.com