Best Practices Made Easy - ALTA - American Land Title ...

67

Best Practices Made Easy! Presented By: Nicole Plath; CEO, Fortune Title Agency, Inc. Paula Zwiren, Esq.; President, Zwiren Title Agency, Inc. Jaime Johnson; Consultant, Minerva Title Advisors LLC Joseph A. Grabas CTP, NTP; CEO, Investors Title Agency, Inc.

Transcript of Best Practices Made Easy - ALTA - American Land Title ...

Best Practices Made Easy! Presented By: Nicole Plath; CEO, Fortune Title Agency, Inc. Paula Zwiren, Esq.; President, Zwiren Title Agency, Inc. Jaime Johnson; Consultant, Minerva Title Advisors LLC Joseph A. Grabas CTP, NTP; CEO, Investors Title Agency, Inc.

Our Resident Experts Kaitlin Kelly Fran Kelly Professional Liability LLC www.titleliability.com [email protected]

Jake Danielski Customers Bank www.customersbank.com [email protected]

Richard Schatzberg SWK Technologies, Inc. www.swktech.com [email protected]

Best Practices Made Easy

CHANGE When we least expect it, life sets us a challenge to test our courage and

willingness to change; at such a moment, there is no point in pretending that nothing has happened or in saying that we are not yet ready. The challenge will

not wait. Life does not look back. A week is more than enough time for us to decide whether or not to accept our destiny.”

Paulo Coelho

The Challenge WILL NOT Wait!

Dear Valued Partner, The Consumer Financial Protection Bureau (CFPB) Bulletin 2012-03 and the Office of the Comptroller of the Currency (OCC) Bulletin 2013-29 require financial institutions to oversee its service providers. To assist us in complying with the foregoing guidance please be aware that we are asking you, our title and settlement partners, to comply with the following requests and submission schedule. The American Land Title Association (ALTA) has published its “Title Insurance and Settlement Company Best Practices”; which should ideally already be in place for businesses providing title and closing services. XYZ Bank supports ALTA’s Best Practices and is requesting that a copy of your uncertified manual be provided as part of this examination. Your Best Practices manual should include policies and procedures for the following items: •Licensing, Escrow/Trust Accounting, Privacy and Information Security, Title and Settlement Pricing. Document Recordation, Title Policy Production/Premium Remittance, Professional Liability Insurance and Consumer Complaints.

In addition to your Best Practices manual we are requesting that you submit the following items for review as well:

•Training materials of your employees and agents that have consumer contact or compliance responsibilities. •Description of the process your organization conducts for the supervision of employees and agents that have consumer contact or compliance responsibilities. •Internal and External Audit Reports. •Litigation affecting the product or services your organization is or will be providing to XYZ. All of these items should be sent in their entirety 45 days from this notice to.

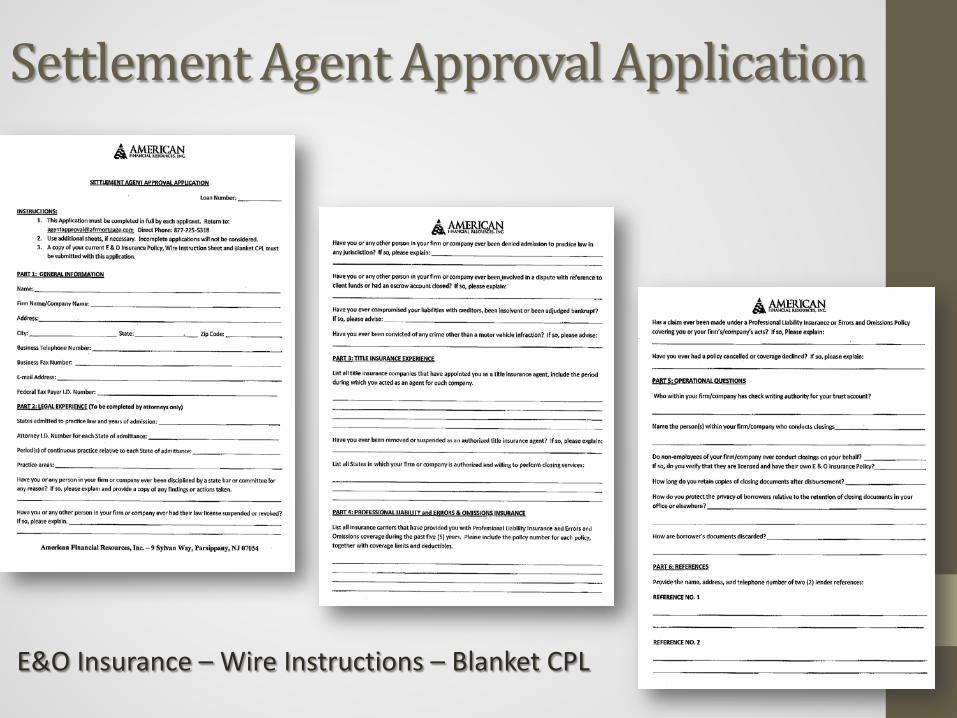

Settlement Agent Approval Application

E&O Insurance – Wire Instructions – Blanket CPL

STUFF THEY WANT TO KNOW Social Security Number

Years of Experience

Disciplinary Actions

Suspensions & Revocations

Client Fund Disputes

Escrow Accounts Closed

E&O Claims

Check Writing Authority

Closers

Document Retention

Privacy of NPI

Security

References

STUFF THEY WANT TO KNOW Type of Entity

Are You Licensed

Can you Act as Settlement Agent

Affiliated with mortgage lender

Other entities

Copy of License

E&O Insurance

Wiring Instructions

Acknowledgment Letter

Compliance Management Report • Benefits

• Demonstrates to lenders that you have implemented Best Practices

• Provides a self-assessment of Best Practices • Prepares you for a formal assessment • Identifies gaps within your company

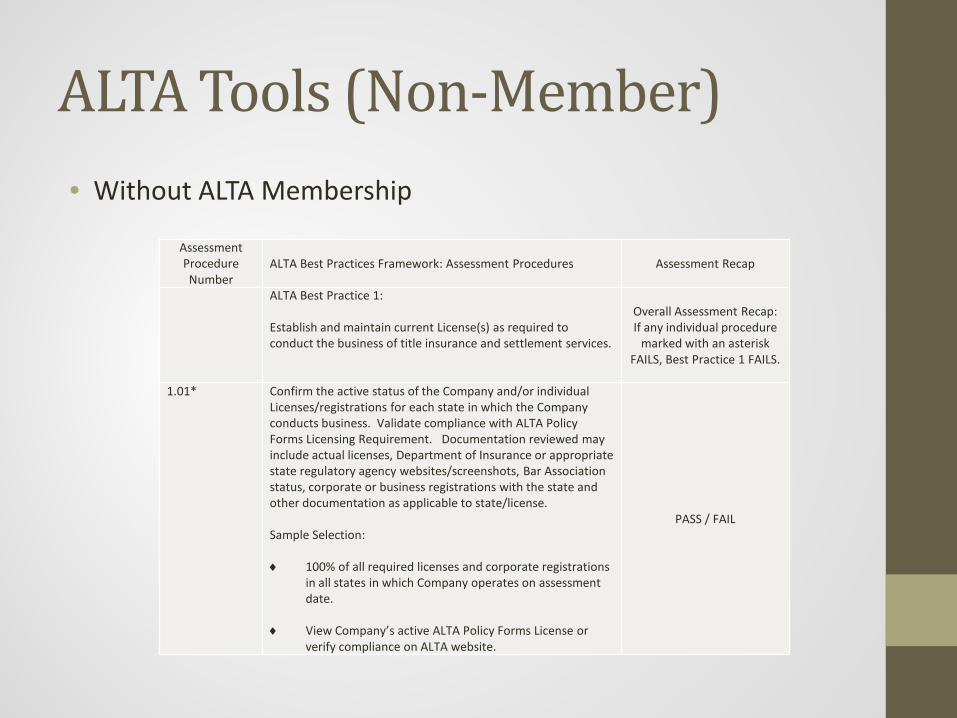

ALTA Tools (Non-Member) • Without ALTA Membership

ALTA Tools (Non-Member) • Without ALTA Membership

Assessment Procedure Number

ALTA Best Practices Framework: Assessment Procedures Assessment Recap

ALTA Best Practice 1:

Establish and maintain current License(s) as required to conduct the business of title insurance and settlement services.

Overall Assessment Recap: If any individual procedure

marked with an asterisk FAILS, Best Practice 1 FAILS.

1.01*

Confirm the active status of the Company and/or individual Licenses/registrations for each state in which the Company conducts business. Validate compliance with ALTA Policy Forms Licensing Requirement. Documentation reviewed may include actual licenses, Department of Insurance or appropriate state regulatory agency websites/screenshots, Bar Association status, corporate or business registrations with the state and other documentation as applicable to state/license.

Sample Selection:

♦ 100% of all required licenses and corporate registrations in all states in which Company operates on assessment date.

♦ View Company’s active ALTA Policy Forms License or verify compliance on ALTA website.

PASS / FAIL

ALTA Tools (Member) • With ALTA Membership

ALTA Tools (Member) • With ALTA Membership

Best Practice #1: Establish and maintain current license(s) as required to conduct the business of title insurance and settlement services.

10 Total Questions

Please review the Instructions prior to completing this Questionnaire. This chapter contains one questionnaire and one worksheet to complete. To prepare for an Assessment, a company should have these practices in place and included in a formal set of written procedures.

Corresponding Assessment Procedure

Question Response Control/Procedure

NOT Documented?

Control/Procedure Compliance NOT Documented? Questions YES NO Descriptions/Comments

1.01 1 In worksheet 1-A, list the states in which your company does business?

1.01 2 On an annual basis, does your Company have a procedure to review and determine your state licensing requirements? If yes, list the person(s) responsible for this procedure in the Descriptions/Comments Section.

1.01 3 Describe your Company's procedures to review and determine your state licensing requirements in the Descriptions/Comments Section.

1.01 4 List all of the Company's license and registration requirements on Worksheet 1-A.

1.01 5 List all of the licenses and registrations held by the Company and its employees and their expiration dates (or attach any existing document that includes such information) on Worksheet 1-A.

1.01 6

In the Descriptions/Comments Section list what resources your Company uses to determine the current licensing requirements for the states in which you do business? Examples include: state insurance department website or materials, state land title association materials, ALTA's Title Insurance Regulatory Survey.

1.01 7 Does your Company maintain current copies of state required licenses in a single location?

1.01 8 Is evidence retained that the Company and its employees comply with current licensing and registration requirements?

1.01 9

Does your Company possess an ALTA Policy Forms License? Your Company possesses an ALTA Policy Forms License if it is a member of ALTA, paid $195 for a Policy Forms License or obtained an Occassional Use Waiver because your Company conducts fewer than 50 transactions per year.

1.01 10 Are the Company and its employees compliant with the current licensing and registration requirements?

ALTA Tools (Member) • With ALTA Membership

WORKSHEET 1-A: Current Title Insurance & Settlement Services License Information

State Type of License Required Registration Requirements

State Licenses Number

Expiration Date

Employee Licenses Number (if applicable)

Expiration Date

New Jersey Corporate and Individual Agent/Producer 88007 5/31/2014

Pennsylvania Corporate or Agency Wide License Only

Example Compliance Management Report

Pillar 1 - Licensing

• Best Practice: Establish and maintain current license(s) as required to conduct the business of title insurance and settlement services.

• Purpose: Maintaining state-mandated insurance licenses and corporate registrations (as applicable) helps ensure the company remains in good standing with the state.

Source: American Land Title Association Title Insurance and Settlement Company Best Practices, Version 2.0, July 19, 2013

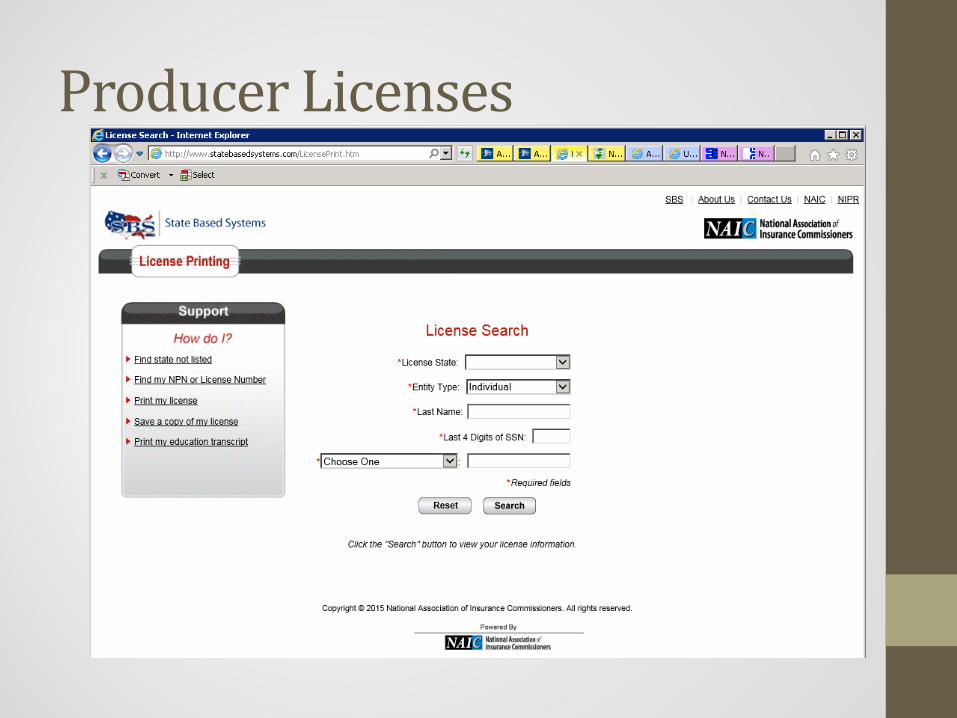

Pillar 1 – Licensing • State Licensing Requirements • Company and Individual Producer Licenses • ALTA Policy Forms Licenses • PROVE IT

State Licensing Requirements • http://www.naic.org/state_web_map.htm

State Licensing Requirements

Producer Licenses • http://www.nipr.com/producer_licensing_map.htm

Producer Licenses

ALTA Policy Forms License

PROVE IT!! Compliance Management Report

Pillar 2 – Escrow Trust Accounts

• Best Practice: Adopt and maintain appropriate written procedures and controls for escrow trust accounts allowing for electronic verification of reconciliation.

• Purpose: Appropriate and effective escrow controls and staff training help title and settlement companies meet client and legal requirements for the safeguarding of client funds. These procedures help ensure accuracy and minimize the exposure to loss of client funds. Settlement companies may engage outside contractors to conduct segregation of trust accounting duties.

Source: American Land Title Association Title Insurance and

Settlement Company Best Practices, Version 2.0, July 19, 2013

Pillar 2 – Escrow Trust Accounting • General Account Rules • Infrastructure/Organization of the Accounting • Reconciling/Balancing • Services a Bank can offer you to be Compliant

General Account Guidelines Relating to the Accounts • Name of the account • Dormant account

monitoring • Bank fees from

another account • Federally insured

accounts

Relating to the People • Employee credit

reports/background checks

• Removing inactive employees

• Routinely reviewing authorized signers

• Multiple signers • Training on company

policies

Infrastructure/Organization • Checks and deposit tickets should show name of the account

as trust/escrow • Checks and deposits should identify related file • Electronic security – user level • Physical security – locked/secured

Reconciling/Balancing • 3 way reconciliations • Individual file receipts and disbursements ledger • Trial balance, Deposits in transit, Outstanding

checks • Within 10 days of receiving the bank statement • Reconciliations available for underwriter review • Shortages • Policies on timeframes to address each type of

item showing • AUTOMATION: Rynoh, E-Reconcilliation

What You Need From Your Bank Feature or Service Benefit to You

Multi-Layer Authentication – (Hard Security Tokens, Call-Backs, Dual Control Approval)

Deters fraud - ensures additional security for client funds – especially when funds transfer is involved

Customizable Online Banking Allows for security restrictions at a user level, and segregation of account access, including dual approval requirements

Account Title Modifier or Escrow Product Designation

Ensures all escrow account statements show “Escrow” or “Trust”

FDIC Participation Ensures that the funds in your trust account are federally insured in the case of bank failure

Fee Analysis or Flat Fee Arrangement Ensures that any fees for your entire banking relationship to be deducted from a single account (not your escrow account)

International Wire Blocks Blocks or disallows any attempt to wire funds outside of the US where retrieval is unlikely

ACH Debit Blocking Blocks or disallows any attempt to debit your escrow account through the use of externally initiated Automatic Clearing Houses

Positive Pay (enhanced further with Payee Positive Pay)

Deters fraud – counterfeit checks or altered payee names will be brought to your attention to reject before they are paid.

Pillar 3 – Security of Nonpublic Personal Information • Best Practice: Adopt and maintain a written privacy and information

security program to protect nonpublic personal information as required by local, state and federal law.

• Purpose: Federal and state laws (including the Gramm-Leach-Bliley Act) require title companies to develop a written information security program that describes the procedures they employ to protect nonpublic personal information. The program must be appropriate to the company’s size and complexity, the nature and scope of the company’s activities, and the sensitivity of the customer information the company handles. A company evaluates and adjusts its program in light of relevant circumstances, including changes in the company’s business or operations, or the results of security testing and monitoring.

Source: American Land Title Association Title Insurance and Settlement Company Best Practices, Version 2.0, July 19, 2013

Pillar 3 • Physical & Network Security – Protect Money and Confidential

Information • Usually the most time consuming section • If you have not already started, do no wait any longer! • Adopt and maintain a WRITTEN privacy and information security

program to protect non-public personal information as required by local, state, and federal law

• This section includes both network and physical security • Written policies to consider:

• Privacy Policy • Disaster Recovery Policy • Clean Desk/Clear Screen Policy

Ways to Simplify Pillar 3 Compliance

• Use Resources provided by the ALTA

• Use Resources provided by the Underwriter

• This section is one where you may consider hiring outside,

third party providers for their expertise in: • Policies and Procedure Creation or Improvement • Information Technology and Security • Privacy and Protection of the consumer’s Personal, Private

Information • Training employees on Privacy and Security Issues

Ways to Simplify Pillar 3 – Don’t “reinvent the wheel”

Two major parts of Pillar 3: • Internal processes and practices – requires reviews and

checkpoints. The language and processes required of Pillar 3 will be (near) standard for most institutions. Work with partners and competitors alike to share common procedures and implement regularly scheduled reviews/self-audits. Incident tracking and reporting is critical. Human resource consultants and employment attorneys are strong resources to aid in this process.

• Network and Data Protection – Data/network protection and business continuity all play a critical role. For most title companies, this is the most challenging area. The technologies and methodologies at play are complicated and beyond the technical resources/skills found in most SMBs.

Suggestions for Meeting the Technical Requirements of Pillar 3

1. Start with a Network Assessment to understand the assets in your

network (servers, PCs, routers, etc.). A network services firm can perform this task for you often in half a day…and often for FREE. The network audit will identify the “low hanging fruit” for you.

2. Evaluate Managed Services and Business Continuity strategies from network service professionals, including email (Nuvotera, Spam Soap, etc.), web (OpenDNS, Websense, etc.), anti-virus and malware protection, as well as hosting options and Mobile Device Management (MDM). If performed correctly, managed services can provide complete traceability of systems access and transactions.

3. Perform regularly scheduled disaster recovery/business continuity tests and document the results and the corrective actions.

4. You may consider hiring an ethical hacker to break into your network and identify weaknesses/vulnerabilities and identify corrective actions.

5. PLEASE, PLEASE, PLEASE consider cyber liability insurance which can protect you from the penalties that will result from a breach.

Pillar 4 – Settlement Process • Best Practice: Adopt standard real estate settlement

procedures and policies that help ensure compliance with federal and state consumer financial laws as applicable to the settlement process.

• Purpose: Adopting appropriate policies and conducting ongoing employee training helps ensure the company can meet state, federal and contractual obligations governing the settlement.

Source: American Land Title Association Title Insurance and Settlement Company Best Practices, Version 2.0, July 19, 2013

Pillar 4 – Settlement Procedures and Policies

• Recording Procedures and Pricing Procedures • Incorporate Policies and Procedures into Manual and Training

• Department Specific • Position Specific

• Training – Written Policies and Documented Confirmation it was given and understood. • Signed Receipt of Training • Management Oversight – double check task items during quality

control

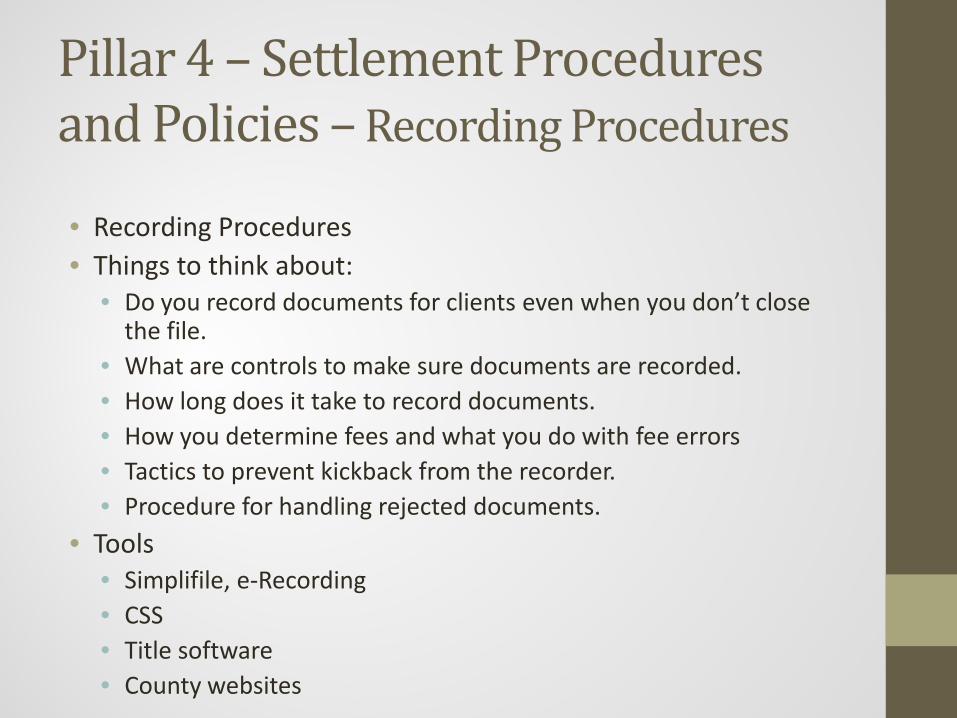

Pillar 4 – Settlement Procedures and Policies – Recording Procedures

• Recording Procedures • Things to think about:

• Do you record documents for clients even when you don’t close the file.

• What are controls to make sure documents are recorded. • How long does it take to record documents. • How you determine fees and what you do with fee errors • Tactics to prevent kickback from the recorder. • Procedure for handling rejected documents.

• Tools • Simplifile, e-Recording • CSS • Title software • County websites

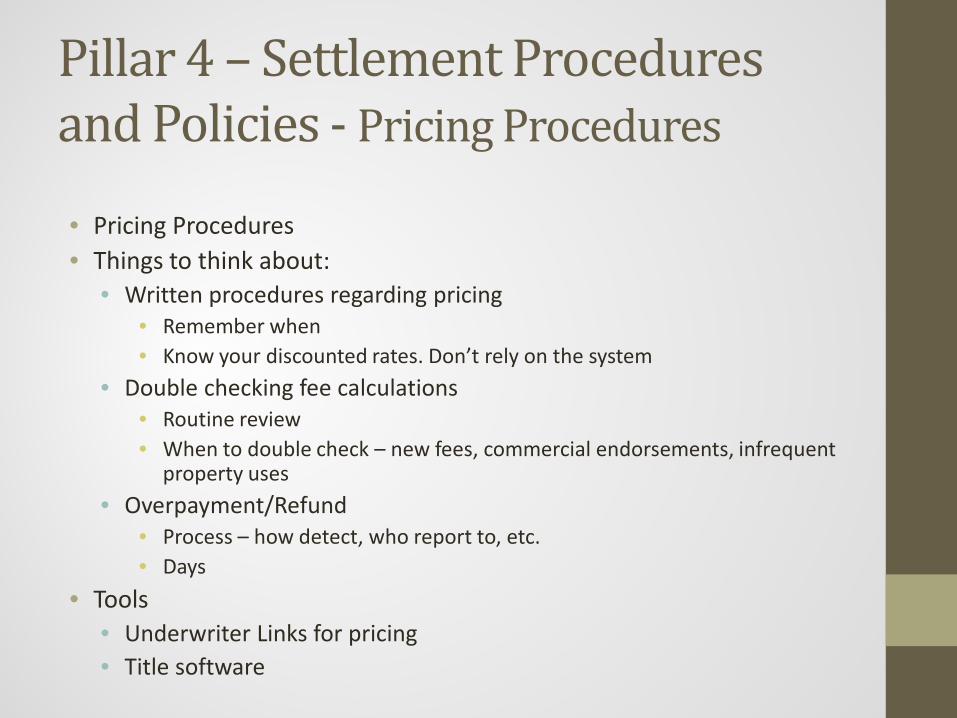

Pillar 4 – Settlement Procedures and Policies - Pricing Procedures

• Pricing Procedures • Things to think about:

• Written procedures regarding pricing • Remember when • Know your discounted rates. Don’t rely on the system

• Double checking fee calculations • Routine review • When to double check – new fees, commercial endorsements, infrequent

property uses • Overpayment/Refund

• Process – how detect, who report to, etc. • Days

• Tools • Underwriter Links for pricing • Title software

Pillar 5 – Policy Production and Remittance • Best Practice: Adopt and maintain written procedures related

to title policy production, delivery, reporting and premium remittance.

• Purpose: Adopting appropriate procedures for the production, delivery and remittance of title insurance policies helps ensure title companies can meet their legal and contractual obligations.

Source: American Land Title Association Title Insurance and Settlement Company Best Practices, Version 2.0, July 19, 2013

Pillar 5 – Title Policy Production

• Title Policy Production and Delivery • You are the expert, just document your process • Utilize software

• Tasks • Reporting

• Verify receipt of delivery • FedEx, UPS • Email read receipts

Pillar 5 - Title Policy Production • Policy Reporting

• You are the expert • Talk to your Underwriter

• Mail physical copy • Upload to a website

• Premium Remittance • You are the expert • Talk to your Underwriter

• Software or Underwriter generated reports • Check Lumping • Wire remittance upon closing

Pillar 6 – Insurance • Best Practice: Maintain appropriate professional liability

insurance and fidelity coverage.

• Purpose: Appropriate levels of professional liability insurance or errors and omissions insurance help ensure title agencies and settlement companies maintain the financial capacity to stand behind their professional services. In addition, state law and title insurance underwriting agreements may require a company to maintain professional liability insurance or errors and omissions insurance, fidelity coverage or surety bonds.

Source: American Land Title Association Title Insurance and

Settlement Company Best Practices, Version 2.0, July 19, 2013

Pillar 6 – Insurance Coverages • Document all coverages

• Compliance Management Report • Insurance Requirements

• State Banking & Insurance Website • Underwriter

• Evaluation of Policies • Pick the right broker

Update From The Expert • Check the definition of professional services

• In all inclusive states, make sure you have coverage for escrow, search/abstracting if you are doing these things.

• Not always necessarily included in the definition of professional services as a title agent.

• If a service is not included in the definition of professional services, make sure there are no exclusions pertaining to those services

• Watch out for exclusions pertaining to the handling and disbursement of funds.

• Evaluate your limits. Make sure they are comparable to the type of transactions you are doing • Residential vs. Commercial • Property values.

• State mandated deductibles.

Update From The Expert • Independent contractors

• How does your policy respond? • Are YOU covered for YOUR vicarious liability? • Does your policy require you to warrant their coverage? • Does it limit your coverage for your liability over the acts of

independent contractors? • Check the exclusions to make sure something you are doing is

not specifically excluded such as oil/gas/mineral/subsurface rights.

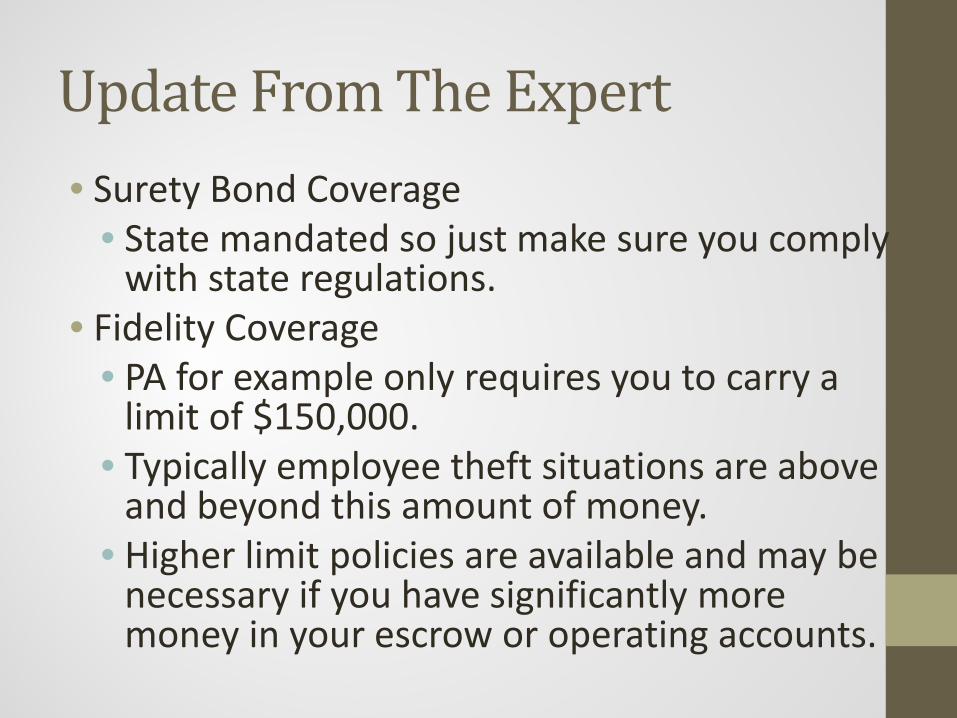

Update From The Expert • Surety Bond Coverage

• State mandated so just make sure you comply with state regulations.

• Fidelity Coverage • PA for example only requires you to carry a

limit of $150,000. • Typically employee theft situations are above

and beyond this amount of money. • Higher limit policies are available and may be

necessary if you have significantly more money in your escrow or operating accounts.

Update From The Expert • Unauthorized Transfer of Funds Coverage

• Great coverage to have as a title agent with all the money being wired in and out regularly.

• Included in most high limit fidelity polices • You can sometimes add it on to your

fidelity coverage or it is also offered in cyber liability policies.

• You want to have it somewhere!

Pillar 7 – Consumer Complaints • Best Practice: Adopt and maintain written procedures for

resolving consumer complaints

• Purpose: A process for receiving and addressing consumer complaints helps ensure reported instances of poor service or non-compliance do not go undiscovered

Source: American Land Title Association Title Insurance and Settlement Company Best Practices, Version 2.0, July 19, 2013

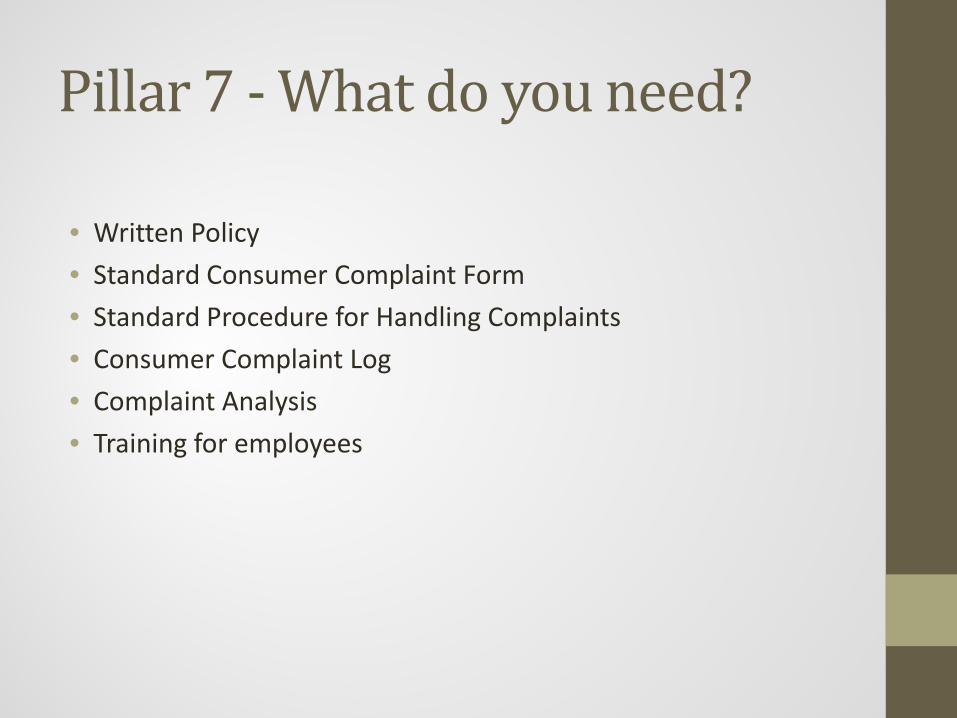

Pillar 7 - What do you need?

• Written Policy • Standard Consumer Complaint Form • Standard Procedure for Handling Complaints • Consumer Complaint Log • Complaint Analysis • Training for employees

Pillar 7 – Consumer Complaints • Standard Consumer Complaint Form

• Date of Complaint • Contact Information of person making complaint • File Number or Property Address • Description of Complaint • Description of Requested Resolution • Amount of Fees associated with transaction • Contact Information for person/department handling complaint • Actual Resolution of Complaint

• Word Document / Web Form / Spreadsheet • Outsource

Pillar 7 – Consumer Complaints • Consumer Complaint Log

• Date of Complaint • Contact Information of person making complaint • File Number or Property Address • Description of Complaint • Description of Requested Resolution • Amount of Fees associated with transaction • Contact Information for person/department handling complaint • Actual Resolution of Complaint • Date of resolution

• Word Document / Web Form / Spreadsheet • Outsource

What are Policies?

• The terms “policy” and “procedure” are often used interchangeably, but these two terms are different.

• A policy states the goals and objectives of the agency and describes what the agency wants to achieve with respect to a particular subject.

• Procedures set forth the specific steps that need to be taken to meet the title agency’s objectives.

Step 1: Determine the policies the agency needs. Policies should be created to cover every area of a title agency’s operations including:

• Human Resources: recruiting, hiring, termination, and training • Security: security awareness, privacy, and document retention and

destruction • Operations: Title examinations and review, accounting/escrow

accounts, real estate transaction processes

What are some of the Policies that should be part of your Best Practices?

• Disaster Recovery and Business Continuity Policy

• Privacy Policy

• Clear Desk and Clean Screen Policy

Disaster Recovery Policy

• Address the timely resumption from and prevention of

interruptions to business activities and processes caused by information-system failures

• Address protection and recovery of physical facilities and equipment from loss, damage, theft, or compromise

• Business continuity plans for all critical business processes

• Include detailed, up-to-date contact information for key individuals required for executing the plan

Privacy Policy

• Explain: • How your company collects information about the consumer • Where that information is shared • How that information is used • How that information is protected

• Identify the consumer’s right to opt out of the information being

shared with unaffiliated parties pursuant to the provisions of the Fair Credit Reporting Act.

• Consider Physical Security and Network Security of Personal, Private Information held by your company

• Train your employees on Privacy Matters

Clean Desk and Clear Screen Policy

• A written policy to ensure that files, documents and computer files

containing Personal, Private Information are stored in a secure manner

• Should address when an employee leaves their workstation for the day or an extended period of time

• Both paper and electronic files must be addressed

• Address procedures to insure all documents, files, portable devices and electronic media are secure

• Have a written policy in place and do periodic sweeps to ensure your staff is consistently following through with protecting any personal information they handle.

Other Policies You Should Have

• A written information security policy;

• An Acceptable Use of Information Technology policy. This policy lays

out the ways and circumstances under which employees may use Company owned technology (e.g., acceptable use of the Internet, email, and information resources).

• Policies and procedures that restrict access to Personal Information to authorized employees (this is called logical access restrictions). These restrictions can include password protection and should be applied to all systems including network, database, and individual application layers.

Additional Policies, Continued

• Policy and procedure restricting the use of removable media

(e.g., USB ports, CD/DVD writeable drives)

• Record Retention and Disposal policy. This policy should set out the minimum amount of time a file should be retained and require appropriate destruction of files.

• Finally, make sure your Company website includes a Privacy Statement.

Questions? Joseph A. Grabas, CTP, NTP Investor’s Title Agency http://www.njtitleweb.com/ [email protected]

Jaime Johnson Minerva Title Advisors www.minervatitleadvisors.com [email protected]

Paula Zwiren Zwiren Title Agency, Inc. http://www.zwirentitle.com/ [email protected]

Nicole Plath Fortune Title Agency, Inc. http://fortunetitle.net/ [email protected]

Alicia Kelly Fran Kelly Professional Liability LLC www.titleliability.com [email protected]

Jake Danielski Customers Bank www.customersbank.com [email protected]

Richard Schatzberg SWK Technologies, Inc. www.swktech.com [email protected]