Wabash Associates, LLC Wabash Associates, LLC Optimizing Talent.

TALENTWATCH® Bersin & Associates

First Quarter 2011

» Global Growth Creates

a New War for Talent

bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

i

The Bersin & Associates Membership ProgramThis document is part of the Bersin & Associates Research Library. Our research is provided exclusively to organizational members of the Bersin & Associates Research Program. Member organizations have access to the largest library of learning and talent management related research available. In addition, members also receive a variety of products and services to enable talent-related transformation within their organizations, including:

• Research – Access to an extensive selection of research reports, such as methodologies, process models and frameworks, and comprehensive industry studies and case studies;

• Benchmarking – These services cover a wide spectrum of HR and L&D metrics, customized by industry and company size;

• Tools – Comprehensive tools for HR and L&D professionals, including tools for benchmarking, vendor and system selection, program design, program implementation, change management and measurement;

• Analyst Support – Via telephone or email, our advisory services are supported by expert industry analysts who conduct our research;

• Strategic Advisory Services – Expert support for custom-tailored projects;

• Member Roundtables® – A place where you can connect with other peers and industry leaders to discuss and learn about the latest industry trends and best practices; and,

• IMPACT® Conference: The Business Of Talent – Attendance at special sessions of our annual, best-practices IMPACT® conference.

• Workshops – Bersin & Associates analysts and advisors conduct onsite workshops on a wide range of topics to educate, inform and inspire HR and L&D professionals and leaders.

For more information about our membership program, please visit us at www.bersin.com/membership.

3bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

TABLE OF CONTENTS

Talent Takeaway 4

Introduction 6

1. Current Business Outlook 8

2. Business Outlook Next Six Months 10

3. Key Business Challenges 12

4. Key Strategy And Organizational Changes 14

5. Key Talent Challenges 16

6. Talent Acquisition: Staffing Needs Today 18

7. Talent Acquisition: Staffing Needs Over The Next Six Months 20

8. Talent Shortages: Job Roles 22

9. Talent Shortages: Impact On Business 23

10. Geographic Talent Needs 24

11. Talent Readiness: By Job Role 25

12. Talent Readiness: Top Leadership 26

13. Talent Readiness: Overall Ability To Execute 28

14. Talent Investments: Change In HR Budgets 29

15. Talent Investments: Change In L&D Budgets 30

16. Talent Investments: Top Three Talent Priorities 32

17. Talent Investments: Top HR Priorities 34

Conclusions 36

Demographics Of The TalentWatch® Research 37

Numbers At-A-Glance 39

About Us 40

About This Research 40

About Bersin & Associates TalentWatch® 40

4bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

TALENT TAKEAWAY

4

» The 2008 and 2009 recession is over. Since our last report, more than 42 percent of all

organizations see business growth at or above plan, and 26 percent of respondents expect

their annual revenue growth to be greater than 10 percent. Globalization and expansion

into new markets are now top of mind among business leaders. Thirty-six percent of

respondents cite these as one of their top two priorities and 37 percent cited the “need to

accelerate innovation” as one of their top priorities for the year.

Coupled with this outlook, organizations have shifted their priorities toward new product

introductions, growth and acceleration in hiring. For the first time in almost three years,

talent shortages are cited as a significant factor in business results.

Addressing these challenges, HR organizations are now focused on programs to

encourage innovation, increase employee engagement and drive individual performance.

Skills gaps in supervisory-level and midlevel leadership are now becoming a major focus,

along with the need to identify and promote emerging talent.

We have entered what we call “the borderless workplace,” an environment in which age,

country, gender and organizational boundaries are going away. Thanks to websites like

Glassdoor.com, for example, a company’s internal employee satisfaction is now widely

available on the Internet. Companies must immediately address employee and customer

satisfaction issues, because they will appear on Twitter or Facebook quickly. This new

borderless environment means that high-impact HR, and learning and development (L&D)

practices must focus on empowerment, knowledge-sharing, the use of social networking

for recruiting and learning, and building collaborative leadership skills.

On a positive side, cuts in training and HR spending are over. This quarter, we see a

dramatic uptick in spending on HR programs, marking the first increase in more than two

years. This money and resources will be spent on a brand-new “war for talent,” one that

is different from what we have previously seen. Today’s high-performing companies must

focus on:

5bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

• Recruitingtechnicalandcustomerserviceprofessionalsinemergingeconomies,aswell

as in the U.S.;

• Buildingdeepskillsquicklyamongbothnewemployeesandseniorworkers;

• Activelyattractingemployeesthroughemploymentbrandingandsocialnetworking-

based marketing;

• Implementingintegratedtalentmanagementsoftwaretocreateinternalcareermobility

and succession plans; and,

• Creatingavibrant,highlyempoweredworkenvironmentthatdrivesperformance.

This new “war for talent” will once again differentiate high-performing companies.

Citibank, for example, is now reinvesting in its leadership development program because it

sees its business starting to grow again. Deloitte is actually building a corporate university,

meeting its need to stay ahead of its competitors in professional services and accounting.

Our recently published Talent Management Factbook®1 and Leadership Development

Factbook®2 reports show that executives and first-line leaders have suffered from a

lack of resources and funding over the last few years. Those days are now ending, as

organizations understand that leadership skills are critical to the new global,

slow-growing economy.

Today, the most common words we hear from HR executives are “HR transformation.”

We think corporate HR is going through a fundamental transition – to a new model that

we call, “business-linked HR.” We will be introducing that model later this year with the

launch of our High-Impact HR Organization®3 research. «

1 For more information, Talent Management Factbook 2010: Best Practices and Benchmarks in U.S. Talent Management, Bersin & Associates / Karen O’Leonard and Stacey Harris, September 2010. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/tmfactbook.

2 For more information, Leadership Development Factbook® 2009: Benchmarks and Analysis of Leadership Development Spending, Staffing and Programs, Bersin & Associates / Kim Lamoureux and Karen O’Leonard, October 2009. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/ldfactbook.

3 For more information, Talent Management Factbook 2010: Best Practices and Benchmarks in U.S. Talent Management, Bersin & Associates / Karen O’Leonard and Stacey Harris, September 2010. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/tmfactbook.

6bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

» Talent drives business. In a continuing effort to help business and HR leaders understand

how the global economy affects a company’s talent strategies, we have introduced the

Corporate TalentWatch®. This is a periodic research report designed to highlight global

trends in talent acquisition, talent readiness, leadership readiness, key talent strategies,

and talent and HR investments.

This research is designed to help business and HR leaders understand the changing

trends and benchmarks in talent acquisition, readiness and investment – with a focus on

providing industry-specific, actionable findings. This report should give you data

and insights that you can use in your own planning, benchmarking and strategy

review processes.

We title this issue, Global Growth Creates a New War for Talent – because it is clear that

business and HR leaders are now actively planning for growth. We believe that we are

reentering a marketplace in which talent is important. Instead of worrying about how to

rapidly restructure and lay off people, the next few quarters are going to shift attention

back toward skills development, globalization, innovation and rebuilding business growth.

All Bersin & Associates research4 discusses these trends in detail. TalentWatch® focuses on

the talent market as seen from the standpoint of a business leader – what are the real-

world changes taking place in the world of the business and HR executive.

We conduct this research by interviewing a set of senior business and human resource

leaders from among our global database of more than 450,000 business, HR and training

professionals. It is arranged in a set of eighteen (18) industry-oriented corporate talent

indices to help us track progress over time. For this issue, we selected 134 global

4 For more information on our research membership program, please visit www.bersin.com/membership.

INTRODUCTION

7bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

corporations to participate in this research, representing a wide range of industries (see

section, “Demographics of the TalentWatch Research”). In each issue, we update this

report to give you the “state of corporate talent” in each major industry.

We hope that this research helps you to understand key trends in your industry, and to

better plan and execute your organization’s talent strategies. «

8bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

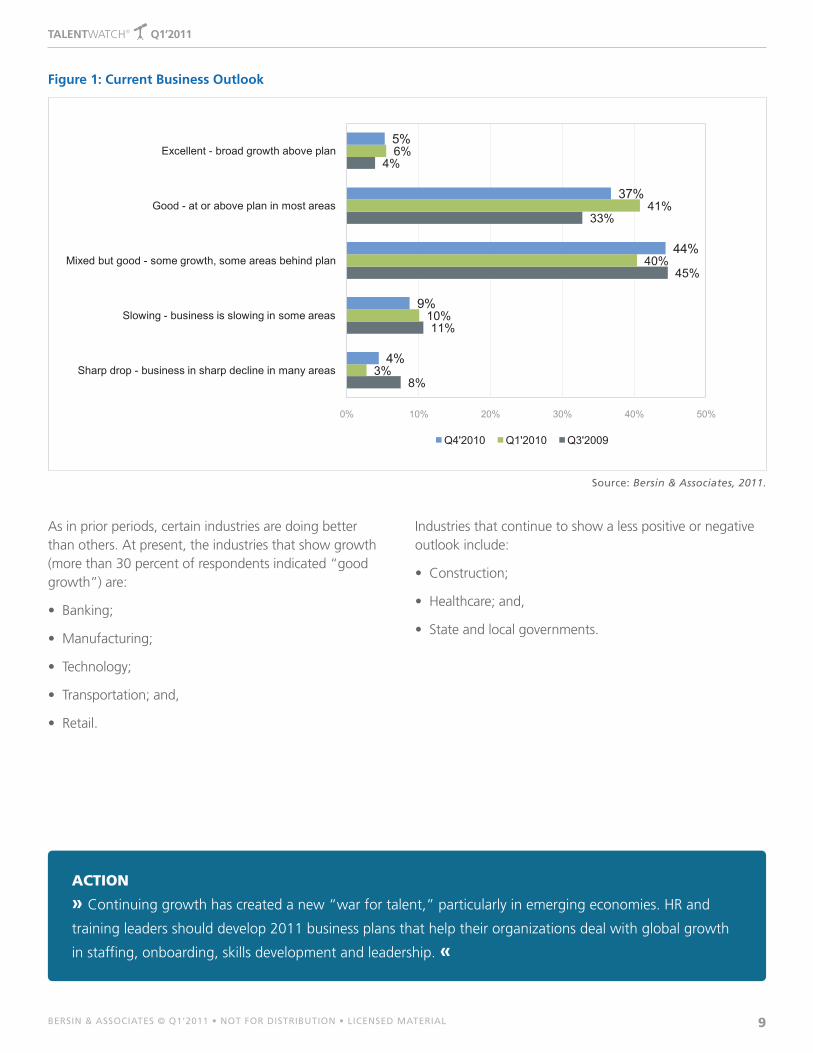

When asked how business looks against current business plans, companies are optimistic with 42 percent telling us that their outlooks are at or above their plans. Only 13 percent of respondents told us that they see their businesses slowing, which is identical to the findings from last summer and nearly a 50-percent drop from 29 percent in the spring of 2009.

The economic recovery, which was first felt by small organizations (companies with up to 5,000 employees) during the summer of 2010, has now spread to large global organizations. Today, the segment that forecasts the most optimistic growth is large organizations (those with 15,000-plus employees). These companies are nearly twice as optimistic as smaller organizations, with an aggregate growth index of more than 0.45 (versus the sample average of 0.3).

The industries showing the greatest growth for this period are:

• Financialservices;

• Manufacturing;

• Transportation;

• Foodservice;and,

• Technology.

These industries forecast growth that is 25 percent or more above the average. This is the second period which shows an increase in manufacturing growth and the first time that healthcare is not the fastest-growing segment in our sample.

Financial services and manufacturers are now benefitting from global demand. Our clients (including Bank of America, MetLife, Credit Suisse, Eaton, Danfoss, AP Moller and InBev) all tell us that they are seeing growth rates of 20 percent to 30 percent in their businesses in Eastern Europe, China, India and other emerging economies. While the U.S. and Western European markets are still recovering, these geographies are growing rapidly – forcing organizations to shift people resources and talent strategies into these economies.

Financial services companies have changed their perspectives. Citibank, one of the companies hardest hit by the global credit crisis, is now profitable again and is growing its leadership development strategy. This refocus on positive people strategies is a result of the turnaround in the banking sector.

This quarter, we saw a continued recovery in business outlook, with a slight slowdown from the summer of 2010, when this index was 0.37.

1. CURRENT BUSINESS OUTLOOK

+2 = Excellent Growth against Plan -2 = Sharp Drop versus Plan

RANGE

+.30ANALySIS:

Businesses forecast growth, large organizations accelerating

9bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

As in prior periods, certain industries are doing better than others. At present, the industries that show growth (more than 30 percent of respondents indicated “good growth”) are:

• Banking;

• Manufacturing;

• Technology;

• Transportation;and,

• Retail.

Industries that continue to show a less positive or negative outlook include:

• Construction;

• Healthcare;and,

• Stateandlocalgovernments.

ACTION

» Continuing growth has created a new “war for talent,” particularly in emerging economies. HR and

training leaders should develop 2011 business plans that help their organizations deal with global growth

in staffing, onboarding, skills development and leadership. «

Source: Bersin & Associates, 2011.

Figure 1: Current Business Outlook

8%

11%

45%

33%

4%

3%

10%

40%

41%

6%

4%

9%

44%

37%

5%

0% 10% 20% 30% 40% 50%

Sharp drop - business in sharp decline in many areas

Slowing - business is slowing in some areas

Mixed but good - some growth, some areas behind plan

Good - at or above plan in most areas

Excellent - broad growth above plan

Q4'2010 Q1'2010 Q3'2009

Jenny -- please do not include the bottom chart with all the data -- just the graphic itself in all of these ... thank

10bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

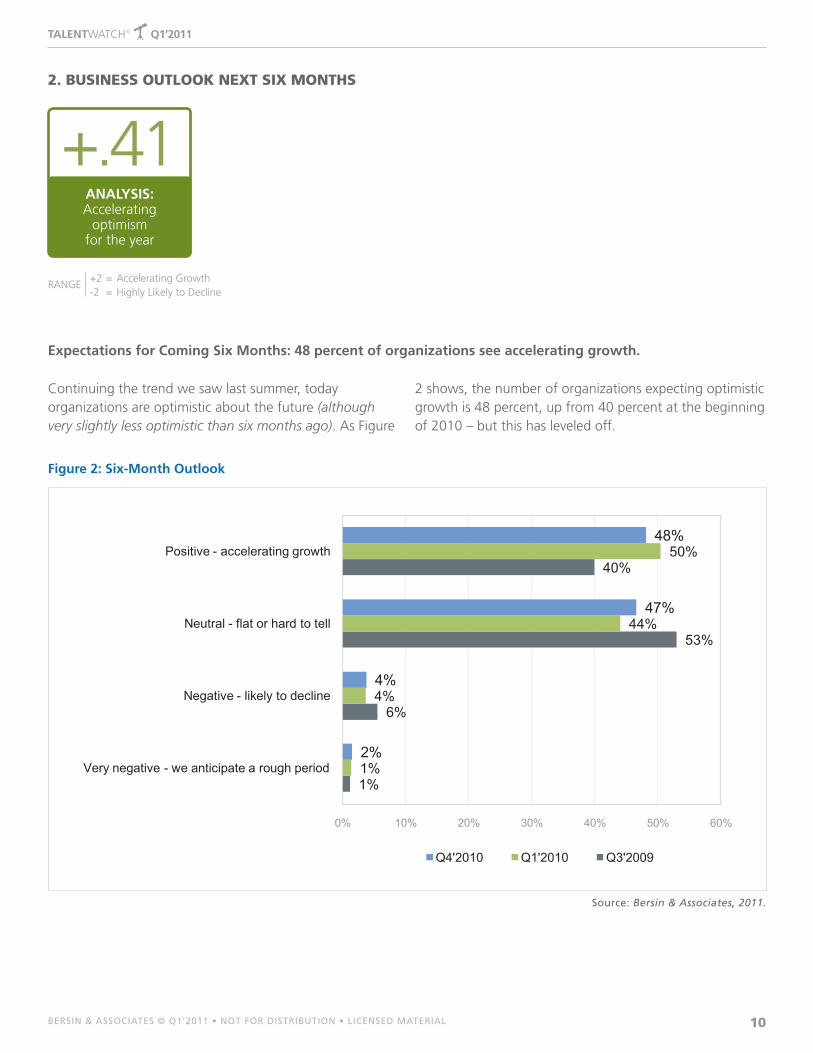

Continuing the trend we saw last summer, today organizations are optimistic about the future (although very slightly less optimistic than six months ago). As Figure

2 shows, the number of organizations expecting optimistic growth is 48 percent, up from 40 percent at the beginning of 2010 – but this has leveled off.

Expectations for Coming Six Months: 48 percent of organizations see accelerating growth.

2. BUSINESS OUTLOOK NEXT SIX MONTHS

+2 = Accelerating Growth -2 = Highly Likely to Decline

RANGE

+.41ANALySIS: Accelerating

optimism for the year

Source: Bersin & Associates, 2011.

Figure 2: Six-Month Outlook

1%

6%

53%

40%

1%

4%

44%

50%

2%

4%

47%

48%

0% 10% 20% 30% 40% 50% 60%

Very negative - we anticipate a rough period

Negative - likely to decline

Neutral - flat or hard to tell

Positive - accelerating growth

Q4'2010 Q1'2010 Q3'2009

11bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» Most companies have now seen several quarters of slowly growing revenues, so they are making

renewed investments in HR and L&D. The training industry, which shrunk by almost 22 percent over the

last three years, is now starting to come back.

Informal learning, skills development and talent mobility strategies are taking a high priority. Today, almost

70 percent of our research members tell us that they are actively involved in building new programs for

coaching, knowledge-sharing and other forms of informal learning. We also see a growing emphasis on

talent-retention programs and alumni programs to bring baby boomers back into the workforce. «

12bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

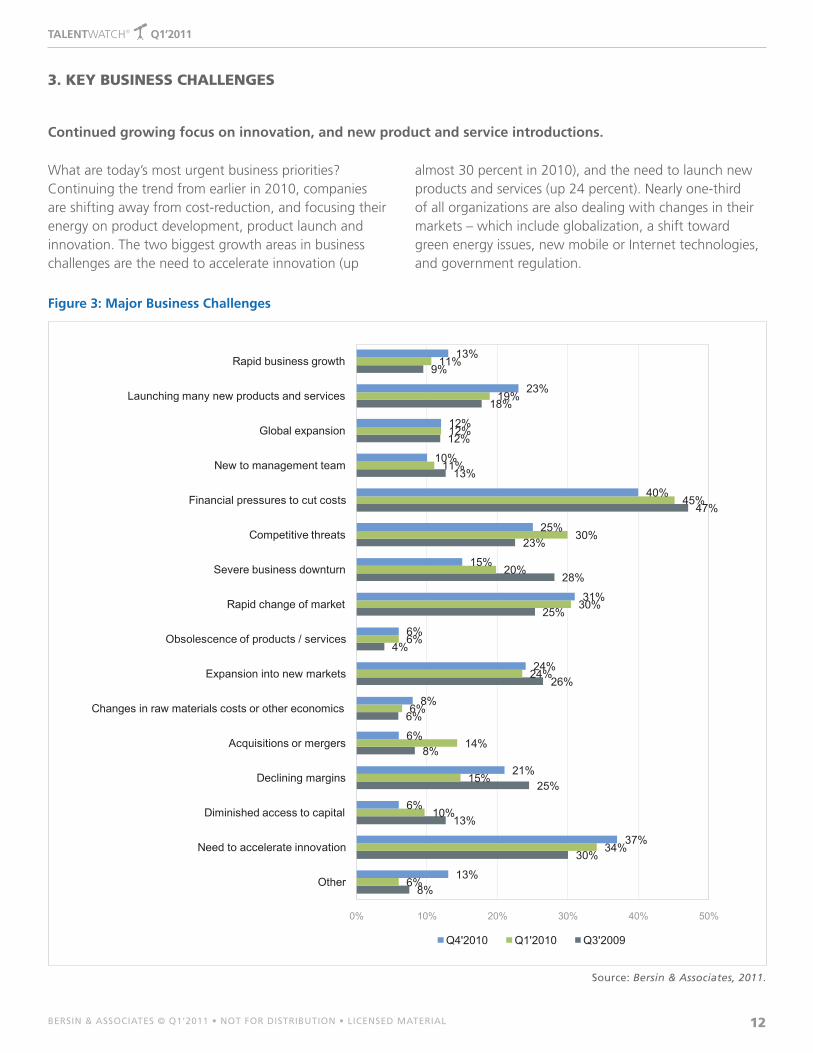

What are today’s most urgent business priorities? Continuing the trend from earlier in 2010, companies are shifting away from cost-reduction, and focusing their energy on product development, product launch and innovation. The two biggest growth areas in business challenges are the need to accelerate innovation (up

almost 30 percent in 2010), and the need to launch new products and services (up 24 percent). Nearly one-third of all organizations are also dealing with changes in their markets – which include globalization, a shift toward green energy issues, new mobile or Internet technologies, and government regulation.

Continued growing focus on innovation, and new product and service introductions.

3. KEY BUSINESS CHALLENGES

Source: Bersin & Associates, 2011.

Figure 3: Major Business Challenges

8%

30%

13%

25%

8%

6%

26%

4%

25%

28%

23%

47%

13%

12%

18%

9%

6%

34%

10%

15%

14%

6%

24%

6%

30%

20%

30%

45%

11%

12%

19%

11%

13%

37%

6%

21%

6%

8%

24%

6%

31%

15%

25%

40%

10%

12%

23%

13%

0% 10% 20% 30% 40% 50%

Other

Need to accelerate innovation

Diminished access to capital

Declining margins

Acquisitions or mergers

Changes in raw materials costs or other economics

Expansion into new markets

Obsolescence of products / services

Rapid change of market

Severe business downturn

Competitive threats

Financial pressures to cut costs

New to management team

Global expansion

Launching many new products and services

Rapid business growth

Q4'2010 Q1'2010 Q3'2009

13bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» Innovation and product introductions demand a new and different type of people strategy. If

your organization is now pushing for new products and services, you must refocus your energies on

empowerment, clarity of decision-making, internal skills development and expertise-sharing, and strong

rewards for performance. These talent programs drive new leadership strategies, and have recast a new

focus in HR and L&D. «

A perfect example of this is the dramatic turnaround taking place at Ford Motor Company, whose business is now growing. For instance, Ford’s engineering team is actively launching electric vehicles and new embedded communications technology. Another example is the company’s growing business in China and India. The

new Ford Figo, a car specifically designed for the Indian marketplace, was just rated the Indian “car of the year” for 2011. This is the type of global innovation that organizations in financial services, manufacturing, information services and technology are striving to execute in the coming few years.

14bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

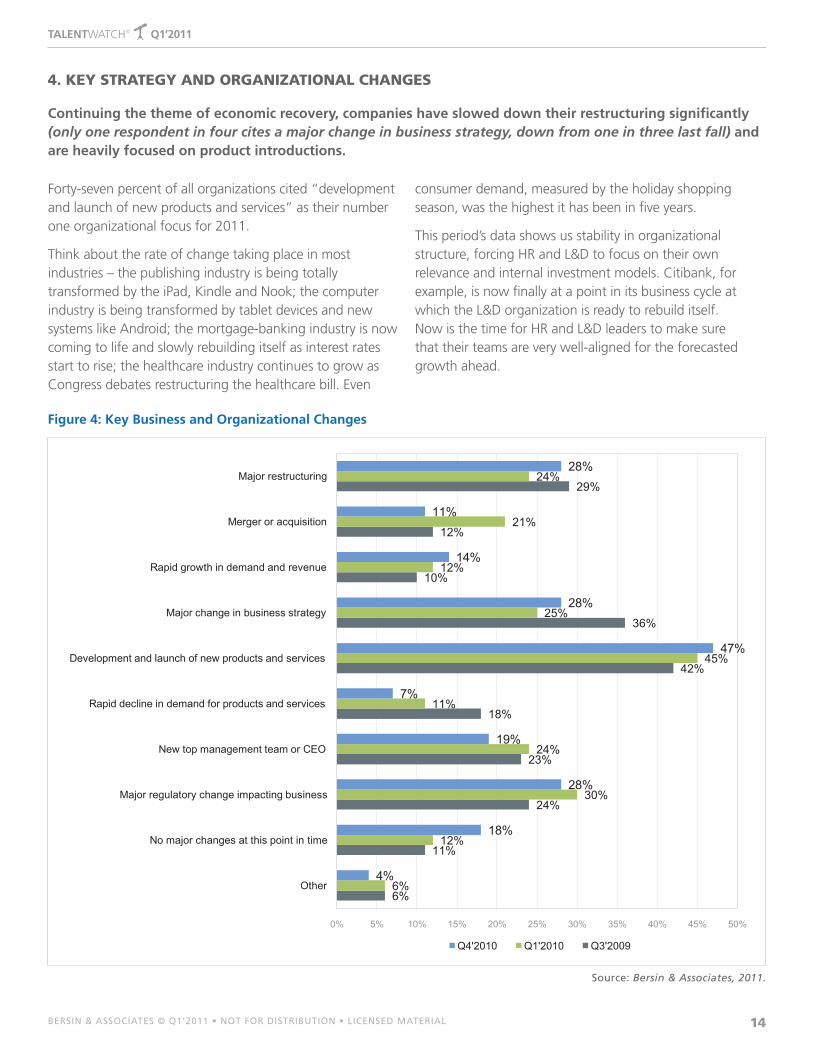

Forty-seven percent of all organizations cited “development and launch of new products and services” as their number one organizational focus for 2011.

Think about the rate of change taking place in most industries – the publishing industry is being totally transformed by the iPad, Kindle and Nook; the computer industry is being transformed by tablet devices and new systems like Android; the mortgage-banking industry is now coming to life and slowly rebuilding itself as interest rates start to rise; the healthcare industry continues to grow as Congress debates restructuring the healthcare bill. Even

consumer demand, measured by the holiday shopping season, was the highest it has been in five years.

This period’s data shows us stability in organizational structure, forcing HR and L&D to focus on their own relevance and internal investment models. Citibank, for example, is now finally at a point in its business cycle at which the L&D organization is ready to rebuild itself. Now is the time for HR and L&D leaders to make sure that their teams are very well-aligned for the forecasted growth ahead.

Continuing the theme of economic recovery, companies have slowed down their restructuring significantly (only one respondent in four cites a major change in business strategy, down from one in three last fall) and are heavily focused on product introductions.

4. KEY STRATEGY AND ORGANIZATIONAL CHANGES

Source: Bersin & Associates, 2011.

Figure 4: Key Business and Organizational Changes

6%

11%

24%

23%

18%

42%

36%

10%

12%

29%

6%

12%

30%

24%

11%

45%

25%

12%

21%

24%

4%

18%

28%

19%

7%

47%

28%

14%

11%

28%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Other

No major changes at this point in time

Major regulatory change impacting business

New top management team or CEO

Rapid decline in demand for products and services

Development and launch of new products and services

Major change in business strategy

Rapid growth in demand and revenue

Merger or acquisition

Major restructuring

Q4'2010 Q1'2010 Q3'2009

15bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» As organizations refocus on growth, stability in structure is resuming. This puts pressure on HR and

L&D to start reinvesting and restructuring to stay relevant, and to refocus energies on talent acquisition,

collaboration and leadership programs.«

16bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

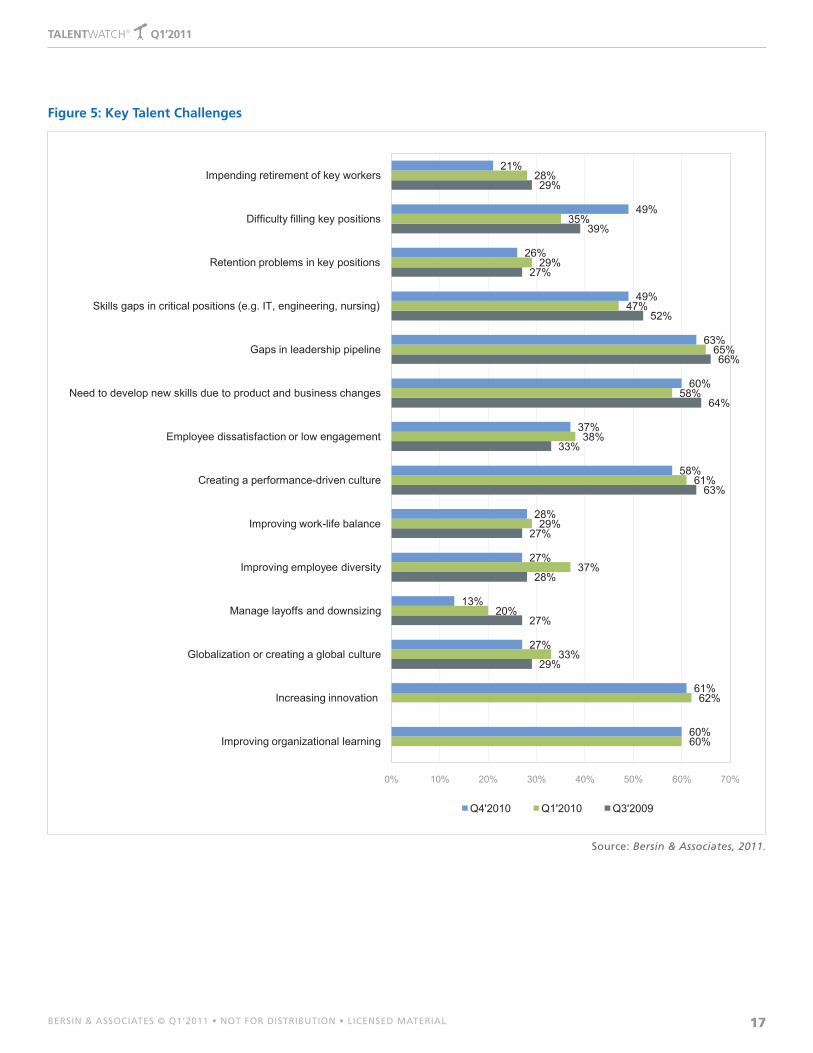

New focus on the need to fill key positions (49 percent cite “urgent” or “important” versus 35 percent from last period) and continued focus on building a culture of performance.

5. KEY TALENT CHALLENGES

5 For more information, The Corporate Learning Factbook® 2011: Benchmarks, Trends and Analysis of the U.S. Training Market, Bersin & Associates / Karen O’Leonard, January 2011. Available to research members at www.bersin.com or for purchase at www.bersin.com/factbook.

6 For more information, High-Impact Learning Culture: The 40 Best Practices for Creating an Empowered Enterprise, Bersin & Associates / David Mallon, June 2010. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/hilc.

7 For more information, High-Impact Learning Practices: The Guide to Modernizing Your Corporate Training Strategy through Social and Informal Learning, Bersin & Associates / David Mallon, July 2009. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/hilp.

When we ask organizations to cite their most urgent talent challenges to address these needs, we see a dramatic uptick in demand for talent acquisition. This period, nearly one-half of all organizations state that they are experiencing difficulty filling key positions (up from only 35 percent last period). The war for talent is back, particularly in technical positions and in emerging economies in which skills are scarce (e.g., India, China, the Middle East).

The baby-boomer retirement issue, which still looms large, has dropped in priority. Companies still understand this risk, but are now focused more heavily on hiring and skills transfer.

Fifty-eight percent of organizations still cite the need to drive a high-performance culture as a significant challenge – and this is now rated the number one cited “urgent” talent problem. In past business cycles, we saw this same effect – when a company sees its competitors growing, leadership focuses on making sure the entire team is functioning at top performance. So now, HR is being asked to rethink pay for performance, performance management and employee talent reviews again.

Earlier in 2010, we asked companies to evaluate their needs to drive innovation and organizational learning –

and again this period the problem looms large. But the second largest “critical” talent issue is the need to fill gaps in the leadership pipeline, which illustrates the problem that companies now have in finding emerging leaders and moving them into more senior positions. The top three “urgent” talent challenges are:

1. Creating a performance-driven culture;

2. Filling gaps in the leadership pipeline; and,

3. Developing new skills to address product and business changes.

Finally, the number three urgent challenge is now skills. As our new Corporate Learning Factbook®5 shows, companies are now finally reinvesting in employee development after two years of cutting costs.

We encourage you to read our highly acclaimed, new research reports, High-Impact Learning Culture®6, and High-Impact Learning Practices®7, which help organizations understand the new principles of L&D in today’s networked organization.

17bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

Source: Bersin & Associates, 2011.

Figure 5: Key Talent Challenges

29%

27%

28%

27%

63%

33%

64%

66%

52%

27%

39%

29%

60%

62%

33%

20%

37%

29%

61%

38%

58%

65%

47%

29%

35%

28%

60%

61%

27%

13%

27%

28%

58%

37%

60%

63%

49%

26%

49%

21%

0% 10% 20% 30% 40% 50% 60% 70%

Improving organizational learning

Increasing innovation

Globalization or creating a global culture

Manage layoffs and downsizing

Improving employee diversity

Improving work-life balance

Creating a performance-driven culture

Employee dissatisfaction or low engagement

Need to develop new skills due to product and business changes

Gaps in leadership pipeline

Skills gaps in critical positions (e.g. IT, engineering, nursing)

Retention problems in key positions

Difficulty filling key positions

Impending retirement of key workers

Q4'2010 Q1'2010 Q3'2009

18bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

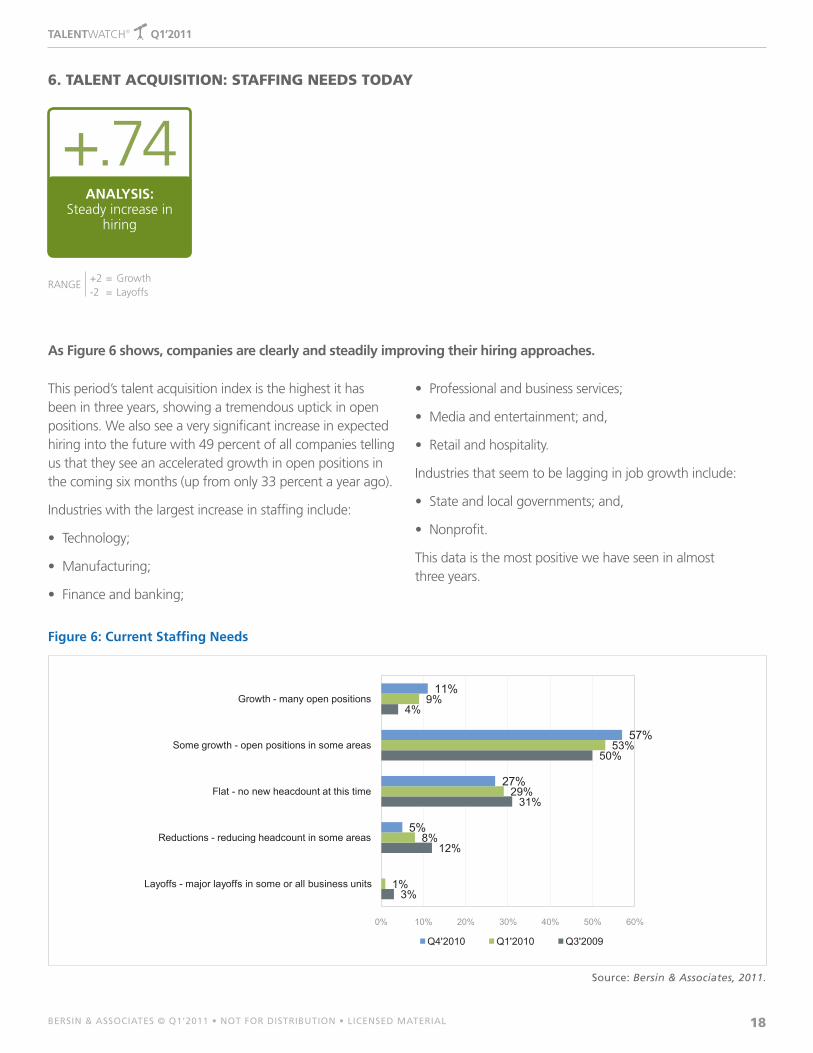

This period’s talent acquisition index is the highest it has been in three years, showing a tremendous uptick in open positions. We also see a very significant increase in expected hiring into the future with 49 percent of all companies telling us that they see an accelerated growth in open positions in the coming six months (up from only 33 percent a year ago).

Industries with the largest increase in staffing include:

• Technology;

• Manufacturing;

• Financeandbanking;

• Professionalandbusinessservices;

• Mediaandentertainment;and,

• Retailandhospitality.

Industries that seem to be lagging in job growth include:

• Stateandlocalgovernments;and,

• Nonprofit.

This data is the most positive we have seen in almost three years.

As Figure 6 shows, companies are clearly and steadily improving their hiring approaches.

6. TALENT ACQUISITION: STAFFING NEEDS TODAY

+2 = Growth -2 = Layoffs

RANGE

+.74ANALySIS:

Steady increase in hiring

Source: Bersin & Associates, 2011.

Figure 6: Current Staffing Needs

3%

12%

31%

50%

4%

1%

8%

29%

53%

9%

5%

27%

57%

11%

0% 10% 20% 30% 40% 50% 60%

Layoffs - major layoffs in some or all business units

Reductions - reducing headcount in some areas

Flat - no new heacdount at this time

Some growth - open positions in some areas

Growth - many open positions

Q4'2010 Q1'2010 Q3'2009

19bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» The talent acquisition marketplace has dramatically changed, driven by the rapid adoption of social

networking. Today’s recruiter must focus on employment branding, creating a pipeline of candidates over

time, and on using internal tools to create referrals and sourcing expertise. The power of job boards is

slowly waning, giving way to a whole new era of recruitment. Bersin & Associates introduced our new

Talent Acquisition research practice in 2010 – and we encourage you to join our membership program to

gain insights into modern best practices in this area. «

20bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

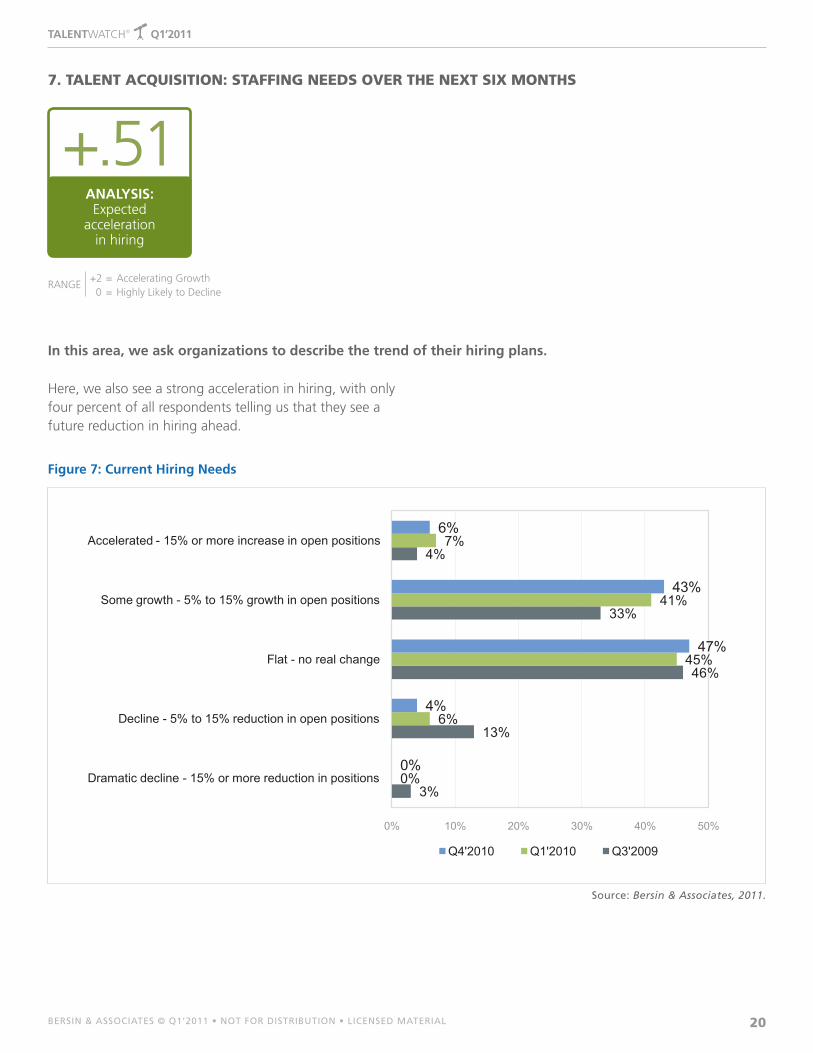

Here, we also see a strong acceleration in hiring, with only four percent of all respondents telling us that they see a future reduction in hiring ahead.

In this area, we ask organizations to describe the trend of their hiring plans.

7. TALENT ACQUISITION: STAFFING NEEDS OVER THE NEXT SIX MONTHS

Source: Bersin & Associates, 2011.

Figure 7: Current Hiring Needs

+.51ANALySIS: Expected

acceleration in hiring

3%

13%

46%

33%

4%

0%

6%

45%

41%

7%

0%

4%

47%

43%

6%

0% 10% 20% 30% 40% 50%

Dramatic decline - 15% or more reduction in positions

Decline - 5% to 15% reduction in open positions

Flat - no real change

Some growth - 5% to 15% growth in open positions

Accelerated - 15% or more increase in open positions

Q4'2010 Q1'2010 Q3'2009

+2 = Accelerating Growth 0 = Highly Likely to Decline

RANGE

21bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» Now that business news is positive, employers in some industries already realize that they have to

compete for candidates again. Even during the recession, organizations have continuously hired top people

for critical positions, but most have cut their external recruiting budgets to the bone. This period and

throughout this year, talent acquisition teams are growing – and are starting to actively use new tools and

systems for sourcing, recruiting, hiring and onboarding.

Many of the most powerful sourcing and recruiting strategies, which have developed in the last year, now

come from social networking and new Internet job sourcing systems. Our Talent Acquisition Systems 20118

research will help you to understand how talent acquisition software has evolved – and is now critical to

building an efficient process for recruiting in 2011. «

8 For more information, Talent Acquisition Systems 2011: Facts, Practical Analysis, Trends and Provider Profiles, Bersin & Associates / Madeline Laurano and Sarah White, March 2011. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/tas. (Buyers may purchase the Talent Acquisition Systems 2010 report today and receive the 2011 version, when available, at no extra charge.)

22bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

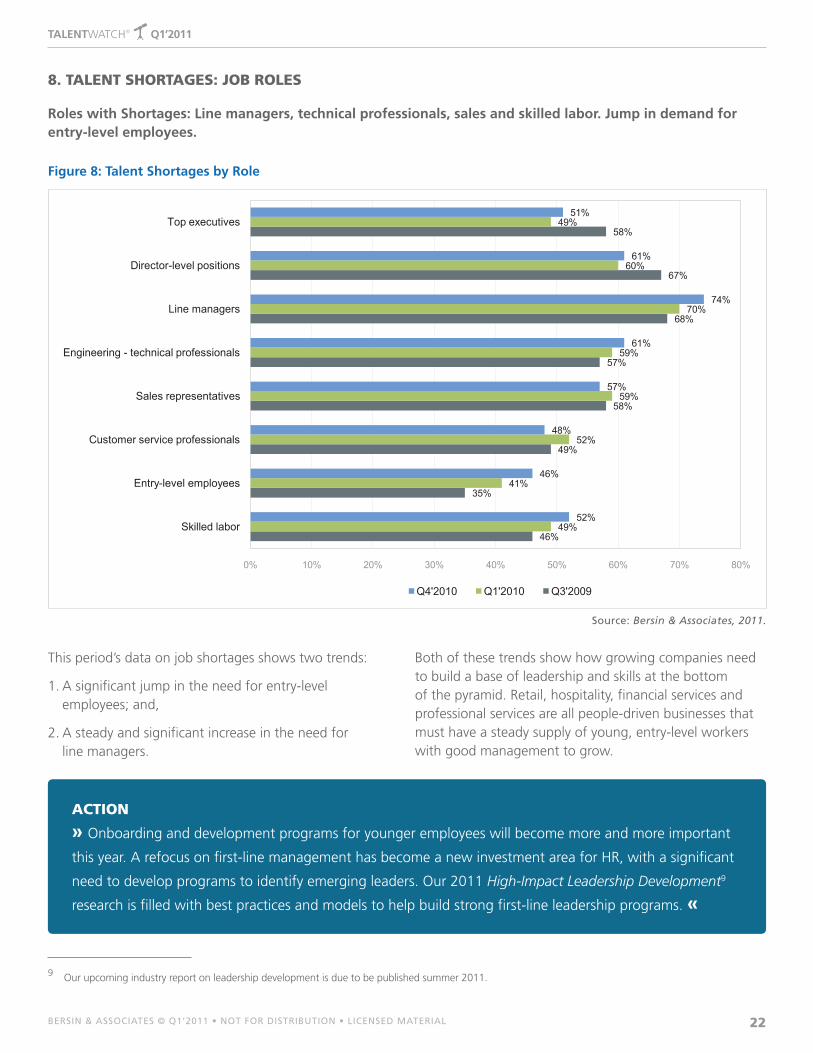

8. TALENT SHORTAGES: JOB ROLES

This period’s data on job shortages shows two trends:

1. A significant jump in the need for entry-level employees; and,

2. A steady and significant increase in the need for line managers.

Both of these trends show how growing companies need to build a base of leadership and skills at the bottom of the pyramid. Retail, hospitality, financial services and professional services are all people-driven businesses that must have a steady supply of young, entry-level workers with good management to grow.

Roles with Shortages: Line managers, technical professionals, sales and skilled labor. Jump in demand for entry-level employees.

Source: Bersin & Associates, 2011.

Figure 8: Talent Shortages by Role

46%

35%

49%

58%

57%

68%

67%

58%

49%

41%

52%

59%

59%

70%

60%

49%

52%

46%

48%

57%

61%

74%

61%

51%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Skilled labor

Entry-level employees

Customer service professionals

Sales representatives

Engineering - technical professionals

Line managers

Director-level positions

Top executives

Q4'2010 Q1'2010 Q3'2009

ACTION

» Onboarding and development programs for younger employees will become more and more important

this year. A refocus on first-line management has become a new investment area for HR, with a significant

need to develop programs to identify emerging leaders. Our 2011 High-Impact Leadership Development9

research is filled with best practices and models to help build strong first-line leadership programs. «

9 Our upcoming industry report on leadership development is due to be published summer 2011.

23bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

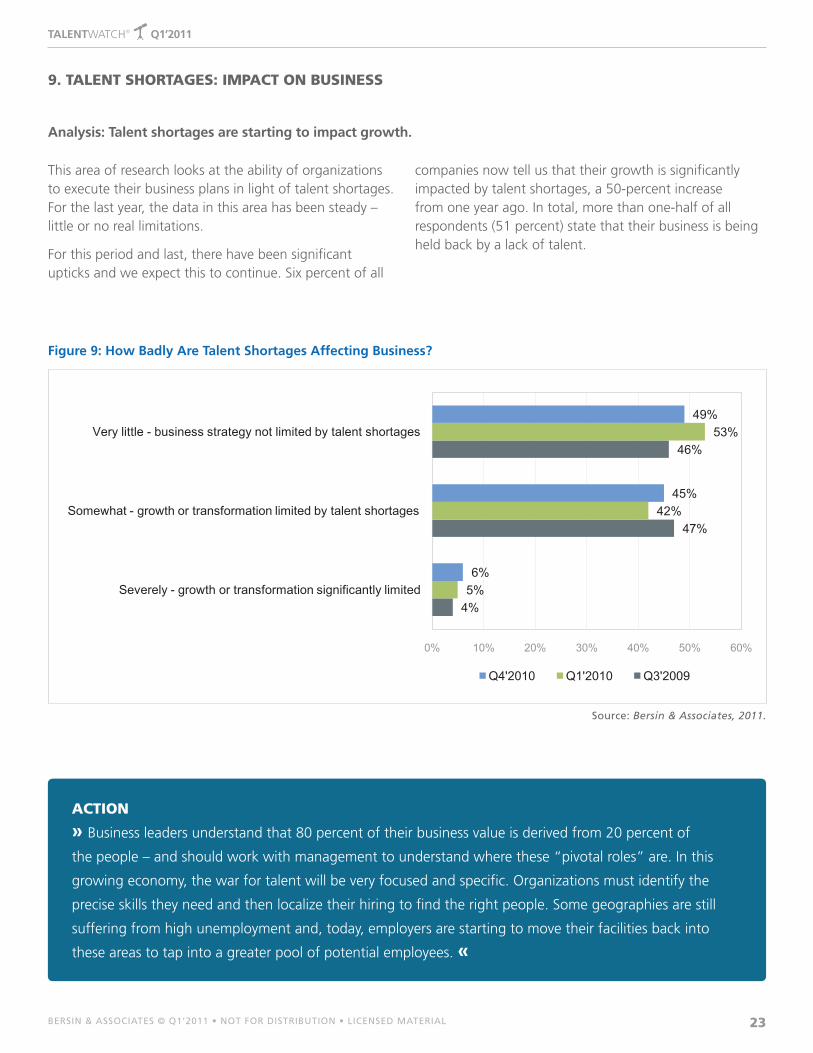

This area of research looks at the ability of organizations to execute their business plans in light of talent shortages. For the last year, the data in this area has been steady – little or no real limitations.

For this period and last, there have been significant upticks and we expect this to continue. Six percent of all

companies now tell us that their growth is significantly impacted by talent shortages, a 50-percent increase from one year ago. In total, more than one-half of all respondents (51 percent) state that their business is being held back by a lack of talent.

Analysis: Talent shortages are starting to impact growth.

9. TALENT SHORTAGES: IMPACT ON BUSINESS

Source: Bersin & Associates, 2011.

Figure 9: How Badly Are Talent Shortages Affecting Business?

ACTION

» Business leaders understand that 80 percent of their business value is derived from 20 percent of

the people – and should work with management to understand where these “pivotal roles” are. In this

growing economy, the war for talent will be very focused and specific. Organizations must identify the

precise skills they need and then localize their hiring to find the right people. Some geographies are still

suffering from high unemployment and, today, employers are starting to move their facilities back into

these areas to tap into a greater pool of potential employees. «

4%

47%

46%

5%

42%

53%

6%

45%

49%

0% 10% 20% 30% 40% 50% 60%

Severely - growth or transformation significantly limited

Somewhat - growth or transformation limited by talent shortages

Very little - business strategy not limited by talent shortages

Q4'2010 Q1'2010 Q3'2009

24bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

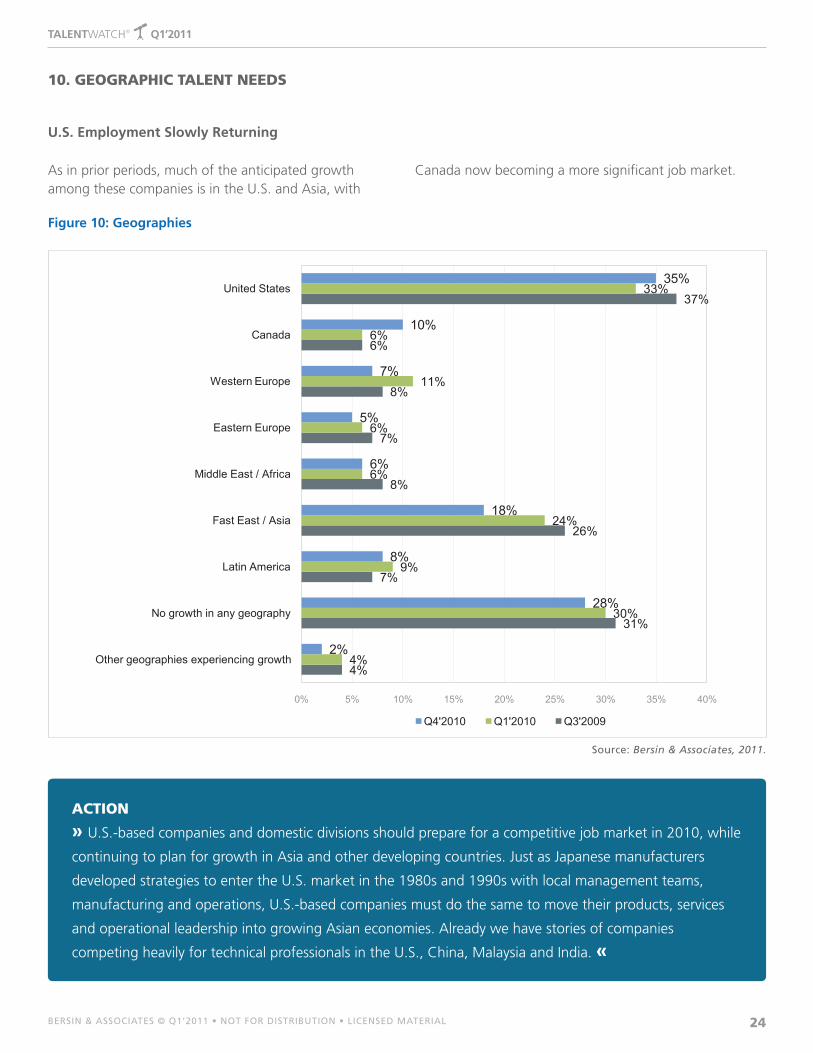

10. GEOGRAPHIC TALENT NEEDS

As in prior periods, much of the anticipated growth among these companies is in the U.S. and Asia, with

Canada now becoming a more significant job market.

U.S. Employment Slowly Returning

Source: Bersin & Associates, 2011.

Figure 10: Geographies

ACTION

» U.S.-based companies and domestic divisions should prepare for a competitive job market in 2010, while

continuing to plan for growth in Asia and other developing countries. Just as Japanese manufacturers

developed strategies to enter the U.S. market in the 1980s and 1990s with local management teams,

manufacturing and operations, U.S.-based companies must do the same to move their products, services

and operational leadership into growing Asian economies. Already we have stories of companies

competing heavily for technical professionals in the U.S., China, Malaysia and India. «

4%

31%

7%

26%

8%

7%

8%

6%

37%

4%

30%

9%

24%

6%

6%

11%

6%

33%

2%

28%

8%

18%

6%

5%

7%

10%

35%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Other geographies experiencing growth

No growth in any geography

Latin America

Fast East / Asia

Middle East / Africa

Eastern Europe

Western Europe

Canada

United States

Q4'2010 Q1'2010 Q3'2009

25bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

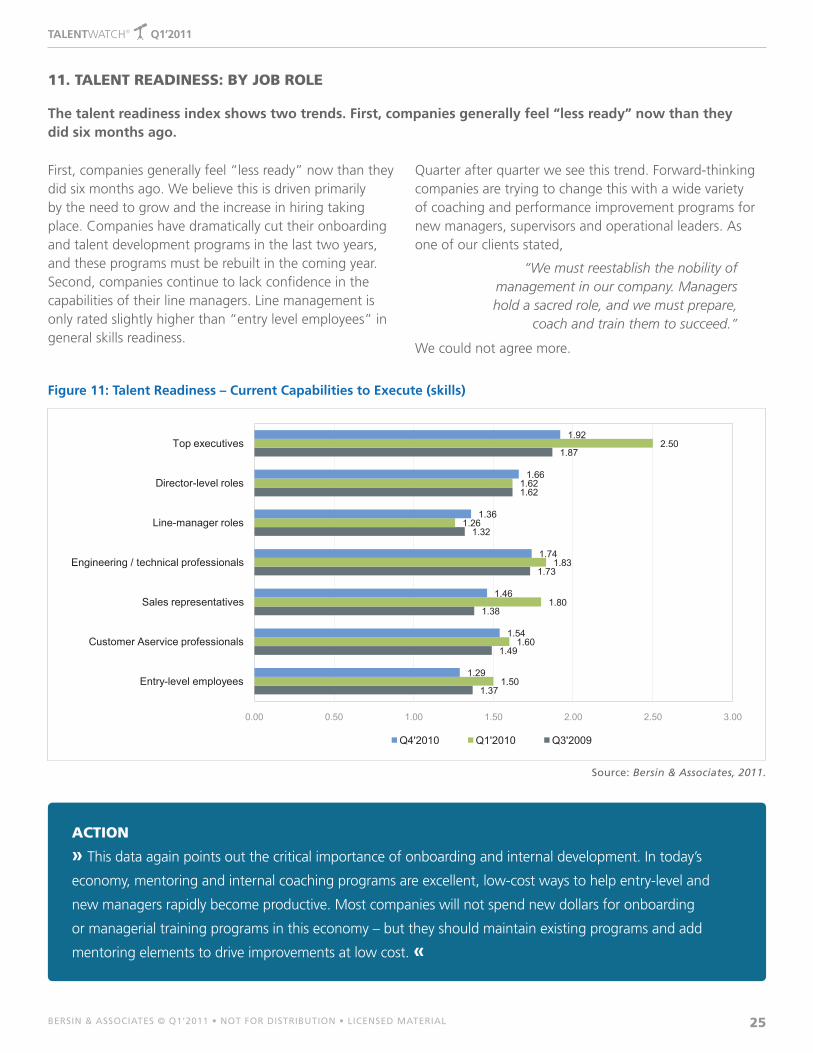

First, companies generally feel “less ready” now than they did six months ago. We believe this is driven primarily by the need to grow and the increase in hiring taking place. Companies have dramatically cut their onboarding and talent development programs in the last two years, and these programs must be rebuilt in the coming year. Second, companies continue to lack confidence in the capabilities of their line managers. Line management is only rated slightly higher than “entry level employees” in general skills readiness.

Quarter after quarter we see this trend. Forward-thinking companies are trying to change this with a wide variety of coaching and performance improvement programs for new managers, supervisors and operational leaders. As one of our clients stated,

“We must reestablish the nobility of management in our company. Managers hold a sacred role, and we must prepare,

coach and train them to succeed.”

We could not agree more.

The talent readiness index shows two trends. First, companies generally feel “less ready” now than they did six months ago.

11. TALENT READINESS: BY JOB ROLE

Source: Bersin & Associates, 2011.

Figure 11: Talent Readiness – Current Capabilities to Execute (skills)

ACTION

» This data again points out the critical importance of onboarding and internal development. In today’s

economy, mentoring and internal coaching programs are excellent, low-cost ways to help entry-level and

new managers rapidly become productive. Most companies will not spend new dollars for onboarding

or managerial training programs in this economy – but they should maintain existing programs and add

mentoring elements to drive improvements at low cost. «

1.37

1.49

1.38

1.73

1.32

1.62

1.87

1.50

1.60

1.80

1.83

1.26

1.62

2.50

1.29

1.54

1.46

1.74

1.36

1.66

1.92

0.00 0.50 1.00 1.50 2.00 2.50 3.00

Entry-level employees

Customer Aservice professionals

Sales representatives

Engineering / technical professionals

Line-manager roles

Director-level roles

Top executives

Q4'2010 Q1'2010 Q3'2009

26bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

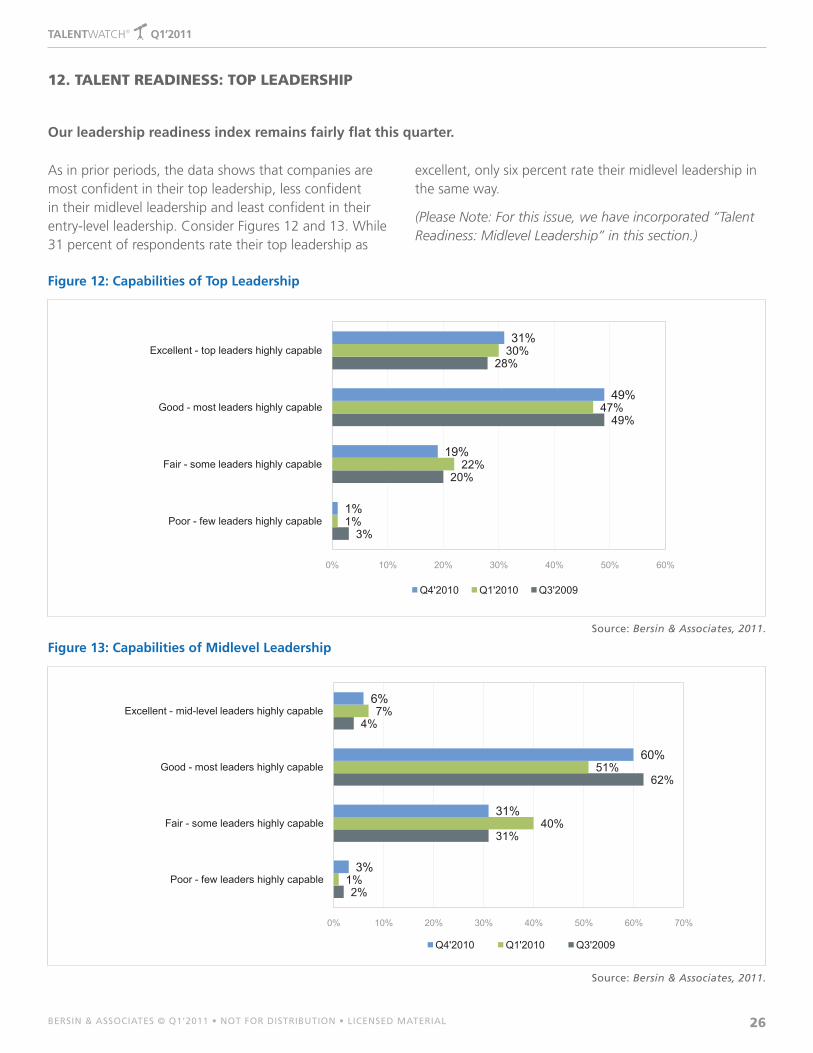

As in prior periods, the data shows that companies are most confident in their top leadership, less confident in their midlevel leadership and least confident in their entry-level leadership. Consider Figures 12 and 13. While 31 percent of respondents rate their top leadership as

excellent, only six percent rate their midlevel leadership in the same way.

(Please Note: For this issue, we have incorporated “Talent Readiness: Midlevel Leadership” in this section.)

Our leadership readiness index remains fairly flat this quarter.

12. TALENT READINESS: TOP LEADERSHIP

Source: Bersin & Associates, 2011.

Figure 12: Capabilities of Top Leadership

Source: Bersin & Associates, 2011.

Figure 13: Capabilities of Midlevel Leadership

3%

20%

49%

28%

1%

22%

47%

30%

1%

19%

49%

31%

0% 10% 20% 30% 40% 50% 60%

Poor - few leaders highly capable

Fair - some leaders highly capable

Good - most leaders highly capable

Excellent - top leaders highly capable

Q4'2010 Q1'2010 Q3'2009

2%

31%

62%

4%

1%

40%

51%

7%

3%

31%

60%

6%

0% 10% 20% 30% 40% 50% 60% 70%

Poor - few leaders highly capable

Fair - some leaders highly capable

Good - most leaders highly capable

Excellent - mid-level leaders highly capable

Q4'2010 Q1'2010 Q3'2009

27bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

This data reinforces our High-Impact Leadership Development10 research, which illustrates how complex it is to build leadership capabilities. Leaders are developed over many years, through a combination of formal

training, on-the-job experience, rotational assignments, coaching and other forms of development. Top leaders have 10 to 20 years’ more experience than young managers – and it shows.

ACTION

» Organizations should focus their leadership development dollars and energies at first-line and midlevel

leaders, building the leadership pipeline from the bottom up. Even in tough economic times, it is critical to

maintain investment in these programs, which can be enhanced through developmental assignments and

coaching when formal training dollars are thin.

Our Leadership Development Factbook®11 shows that organizations typically spend six times as much

money and time on top executive development than that which is spent on first-line managers. While

the biggest skills gaps exist at the bottom of the pyramid, organizations should segment their leadership

programs, so that top executives also get continuous development. Such executive programs (which often

include coaching, 360 assessments, executive education and rotational assignments) are critical to building

a continuous leadership pipeline and consistent culture of leadership within the organization. «

10 For more information, High-Impact Leadership Development 2009: Trends, Best Practices, Industry Solutions and Vendor Profiles, Bersin & Associates / Kim Lamoureux, November 2008. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/hild.

11 For more information, Leadership Development Factbook® 2009: Benchmarks and Analysis of Leadership Development Spending, Staffing and Programs, Bersin & Associates / Kim Lamoureux and Karen O’Leonard, October 2009.

28bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

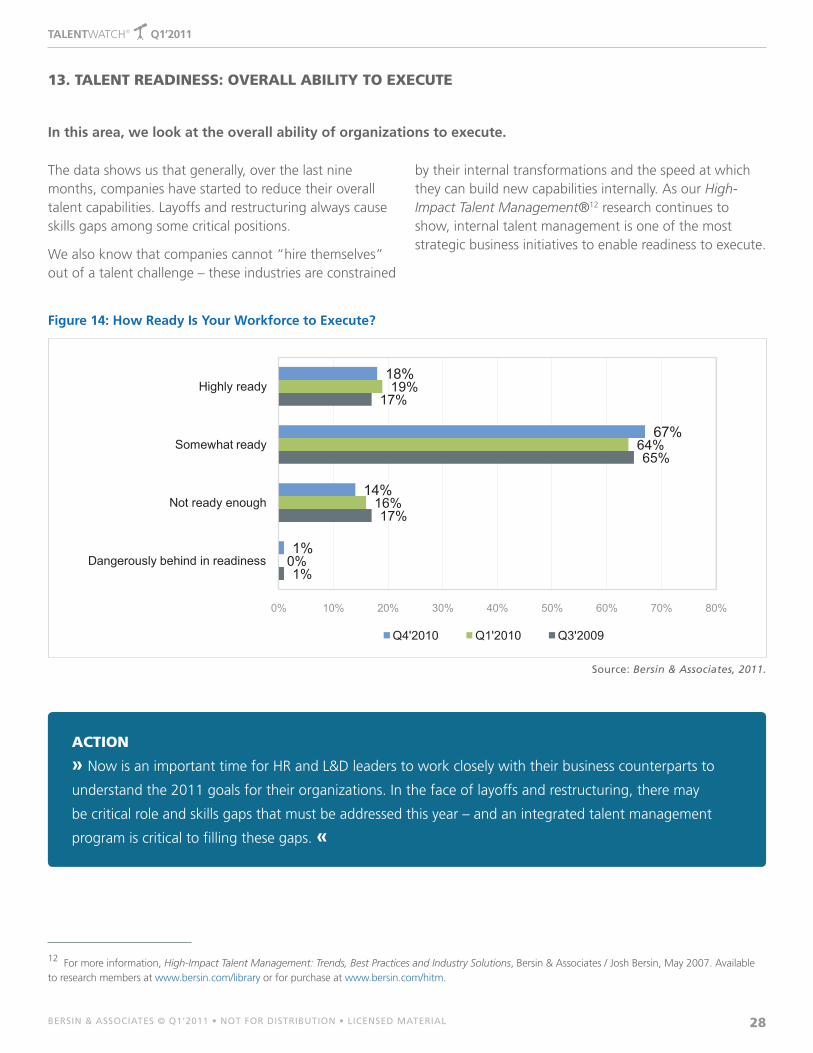

The data shows us that generally, over the last nine months, companies have started to reduce their overall talent capabilities. Layoffs and restructuring always cause skills gaps among some critical positions.

We also know that companies cannot “hire themselves” out of a talent challenge – these industries are constrained

by their internal transformations and the speed at which they can build new capabilities internally. As our High-Impact Talent Management®12 research continues to show, internal talent management is one of the most strategic business initiatives to enable readiness to execute.

In this area, we look at the overall ability of organizations to execute.

13. TALENT READINESS: OVERALL ABILITY TO EXECUTE

Source: Bersin & Associates, 2011.

Figure 14: How Ready Is your Workforce to Execute?

12 For more information, High-Impact Talent Management: Trends, Best Practices and Industry Solutions, Bersin & Associates / Josh Bersin, May 2007. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/hitm.

1%

17%

65%

17%

0%

16%

64%

19%

1%

14%

67%

18%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Dangerously behind in readiness

Not ready enough

Somewhat ready

Highly ready

Q4'2010 Q1'2010 Q3'2009

ACTION

» Now is an important time for HR and L&D leaders to work closely with their business counterparts to

understand the 2011 goals for their organizations. In the face of layoffs and restructuring, there may

be critical role and skills gaps that must be addressed this year – and an integrated talent management

program is critical to filling these gaps. «

29bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

After a strong reduction in HR spending per employee in 2009 and 2010, HR departments are seeing robust growth.

Fifteen percent of all respondents see a growth in HR spending of 10 percent or more – the highest level of increase in more than two years.

HR budgets are now increasing dramatically.

14. TALENT INVESTMENTS: CHANGE IN HR BUDGETS

13

13 For more information, The High-Impact HR Organization: Top 10 Best Practices on the Road to Excellence, Bersin & Associates / Stacey Harris, January 2011. Available to research members at www.bersin.com/library or for purchase at www.bersin.com/hihr.

Source: Bersin & Associates, 2011.

Figure 15: Growth in HR Budgets This Period over Prior Periods

ACTION

» Nearly every company we talk with is in the process of “transforming the HR function.” We believe

that there is actually a profound new model of HR being developed – one which redefines HR as not only

a “strategic partner,” but actually as a business delivery function like any other service organization. Our

just announced HR Research Practice and new research, The High-Impact HR Organization: Top 10 Best

Practices13, discuss these findings in detail. «

+7.0ANALySIS:

Nearly double the increase from six

months ago

Unweighted by Organization Size

9%

19%

63%

9%

0%

5%

14%

62%

14%

0%

1%

6%

70%

15%

0%

0% 20% 40% 60% 80%

Significant cut - 15% or more reduction over last year

Declining - 5% to 15% reduction over last year

Flat - even or within 5% of last year

Growing - 10% or more over last year

Significant - 15% or more over the last year

Q4'2010 Q1'2010 Q3'2009

30bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

14 For more information, The Corporate Learning Factbook® 2011: Benchmarks, Trends and Analysis of the U.S. Corporate Training Market, Bersin & Associates / Karen O’Leonard, January 2011

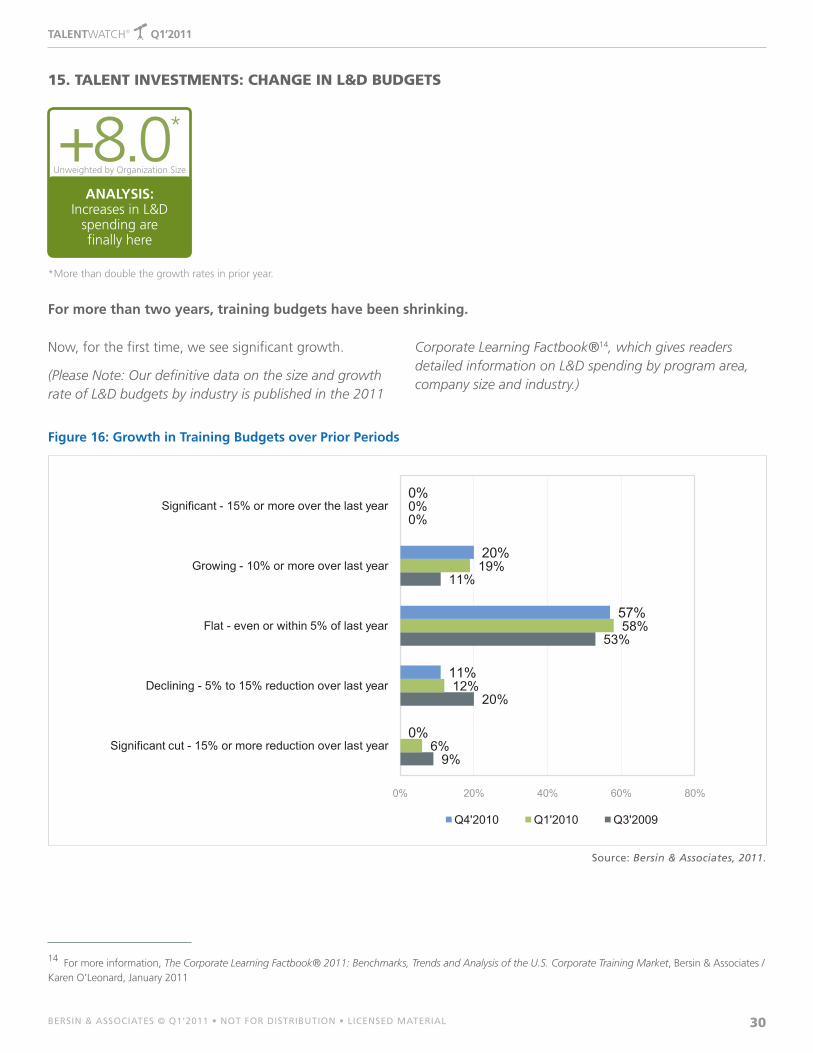

15. TALENT INVESTMENTS: CHANGE IN L&D BUDGETS

+8.0*

ANALySIS: Increases in L&D

spending are finally here

Unweighted by Organization Size

Now, for the first time, we see significant growth.

(Please Note: Our definitive data on the size and growth rate of L&D budgets by industry is published in the 2011

Corporate Learning Factbook®14, which gives readers detailed information on L&D spending by program area, company size and industry.)

For more than two years, training budgets have been shrinking.

Source: Bersin & Associates, 2011.

Figure 16: Growth in Training Budgets over Prior Periods

9%

20%

53%

11%

0%

6%

12%

58%

19%

0%

0%

11%

57%

20%

0%

0% 20% 40% 60% 80%

Significant cut - 15% or more reduction over last year

Declining - 5% to 15% reduction over last year

Flat - even or within 5% of last year

Growing - 10% or more over last year

Significant - 15% or more over the last year

Q4'2010 Q1'2010 Q3'2009

*More than double the growth rates in prior year.

31bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

ACTION

» Companies have finally realized that they must invest in L&D in order to meet the talent needs cited

earlier. During the recession, most companies shifted their resources toward informal learning, virtual

classroom technologies and self-study programs. Now organizations are reinvesting in formal training

and we expect the training industry to see a renaissance in 2011. For more information on the modern

practices for corporate training, please review our latest research, High-Impact Learning Practices®.15 «

15 For more information, High-Impact Learning Practices: The Guide to Modernizing Your Corporate Training Strategy through Social and Informal Learning, Bersin & Associates / David Mallon, July 2009.

32bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

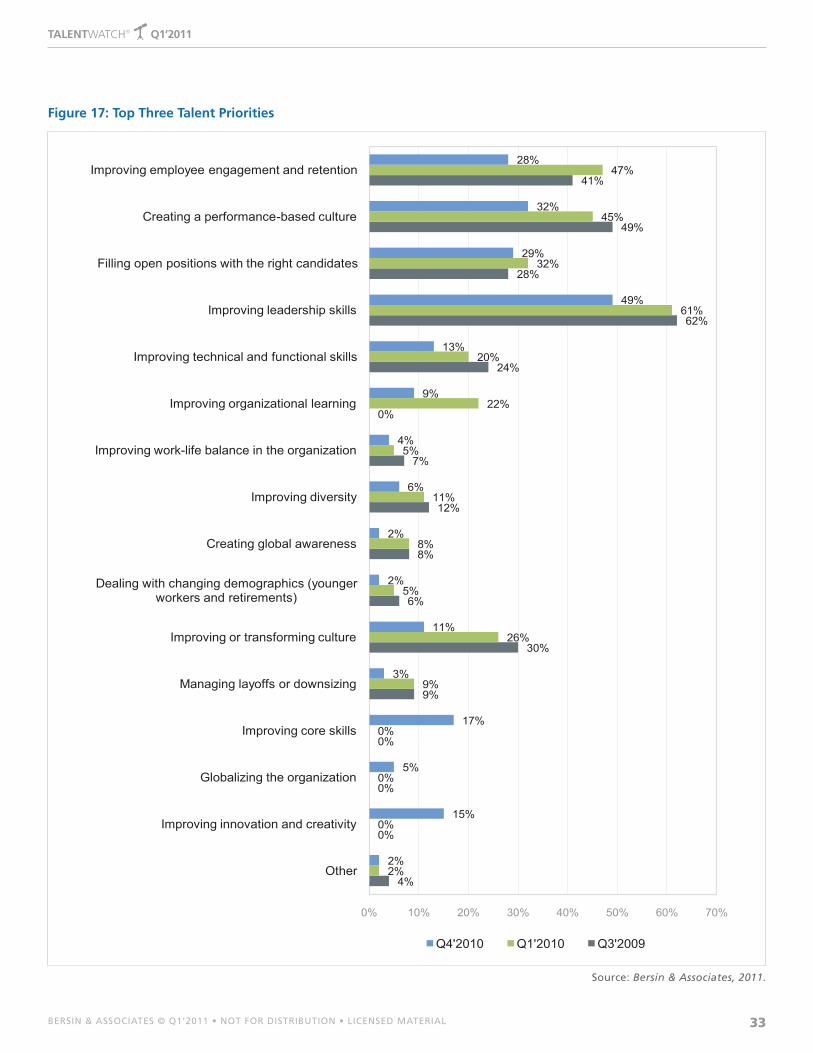

This quarter we expanded our categories of investment, so the data is not totally comparable with prior quarters. What it does clearly show, however, is that five key priorities are critical for the coming year:

1. Improving leadership skills;

2. Creating a performance-based culture;

3. Filling open positions with the right candidates;

4. Improving employee engagement and retention; and,

5. Improving innovation and creativity.

This information is consistent with all the other data in this report. Over the coming year, we see companies focusing heavily on the talent programs that drive growth and reengage employees in the company’s mission. Most

businesses had some type of layoff or restructuring over the last few years – engagement and retention are now becoming critical to success.

One of the other factors that now makes engagement a critical priority is the widespread use of social networking. Websites, like Glassdoor.com (which allows employees to publicly evaluate their workplace, job and CEO), Twitter and Facebook now make it very easy for employees to “rant” about their workplaces. Companies that have poor employment practices can no longer hide – so the impact of poor engagement has an immediate effect on hiring and recruiting. The next few years will be the years of “employee engagement focus” – driving management, leadership and wellness programs that make a difference in the lives of all employees.

Here, we asked organizations to rank their top talent priorities for the next six to 12 months.

16. TALENT INVESTMENTS: TOP THREE TALENT PRIORITIES

ACTION

» Take employee engagement seriously this year. Jobs will become more competitive to fill and your

employment brand will become well-known in the marketplace you serve. «

33bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

Source: Bersin & Associates, 2011.

Figure 17: Top Three Talent Priorities

4%

0%

0%

0%

9%

30%

6%

8%

12%

7%

0%

24%

62%

28%

49%

41%

2%

0%

0%

0%

9%

26%

5%

8%

11%

5%

22%

20%

61%

32%

45%

47%

2%

15%

5%

17%

3%

11%

2%

2%

6%

4%

9%

13%

49%

29%

32%

28%

0% 10% 20% 30% 40% 50% 60% 70%

Other

Improving innovation and creativity

Globalizing the organization

Improving core skills

Managing layoffs or downsizing

Improving or transforming culture

Dealing with changing demographics (younger workers and retirements)

Creating global awareness

Improving diversity

Improving work-life balance in the organization

Improving organizational learning

Improving technical and functional skills

Improving leadership skills

Filling open positions with the right candidates

Creating a performance-based culture

Improving employee engagement and retention

Q4'2010 Q1'2010 Q3'2009

34bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

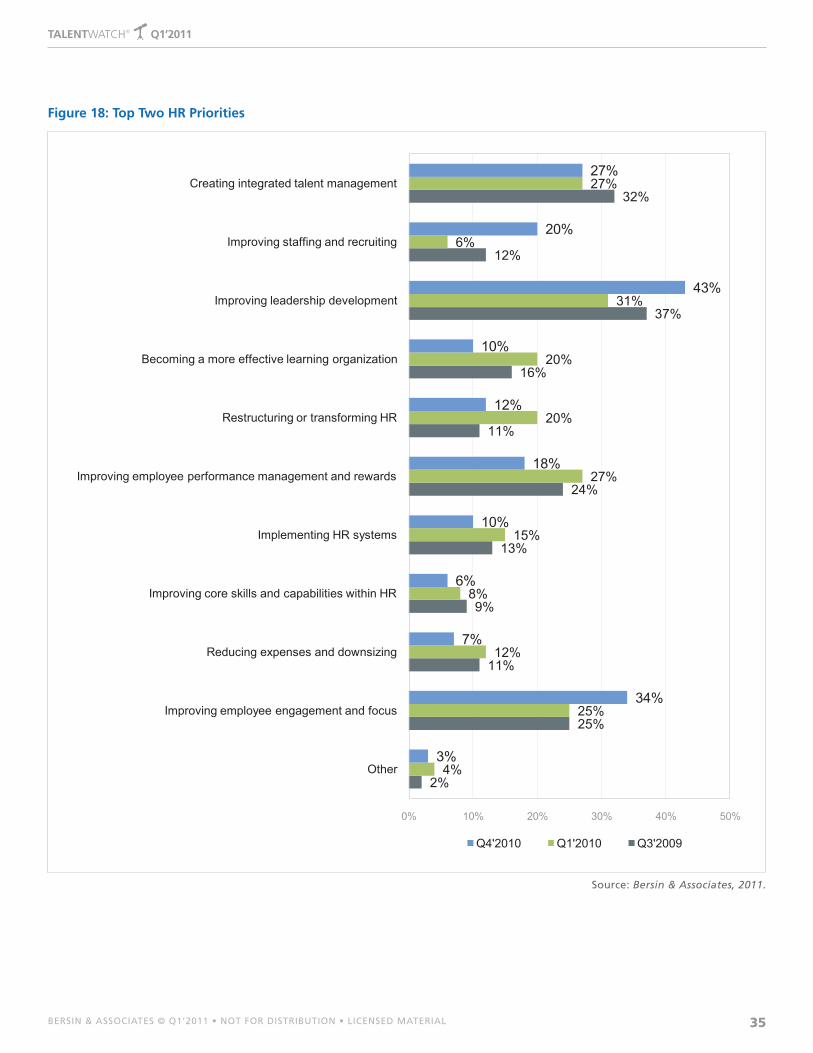

17. TALENT INVESTMENTS: TOP HR PRIORITIES

How can HR itself improve and refocus to address this period’s needs? As Figure 18 illustrates, we see HR and L&D teams focusing on several key areas.

• Afocusonemployeeengagementisasimportantasever. In 2011, HR organizations are becoming very focused on understanding the current state of employee engagement, as well as looking at their “Twitter brand” and “Facebook brand” to make sure that they do not appear on Glassdoor.com with heavily negative ratings. Our new HR Research Practice will give you great insights in this area.

• Integratedtalentmanagementcontinuestobeahighpriority, but it actually falls behind a focus on leadership, engagement and performance. The “hype” about integrated talent management is starting to wear off –

organizations are now realizing that talent management is not an end but, rather, a means to an end. Read our new Talent Management Maturity Model®16 to understand your evolution to talent management in more detail.

• Oneinfiverespondentstellsusthattheymustimprovestaffing and recruiting. During 2009 and 2010 most staffing teams were significantly downsized and many external recruiting contracts were cancelled. Now organizations must rebuild these teams and transform their skills to understand the power of social networking and employee branding in recruiting.

Finally, what are HR organizations doing to address all these issues?

ACTION

» HR priorities in a growing economy are quite different from those during a recession. For the next

few years, we believe high-impact HR organizations will focus heavily on employee engagement,

globalized and integrated recruiting, integrated talent management, and end-to-end leadership

development. Globalization and development of a strong learning culture continue to be huge areas for

competitive advantage. «

16 For more information, Talent Management Roadmap to Maturity, Bersin & Associates / Karen O’Leonard, November 4, 2010. Available to research members at www.bersin.com/library.

35bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

Source: Bersin & Associates, 2011.

Figure 18: Top Two HR Priorities

2%

25%

11%

9%

13%

24%

11%

16%

37%

12%

32%

4%

25%

12%

8%

15%

27%

20%

20%

31%

6%

27%

3%

34%

7%

6%

10%

18%

12%

10%

43%

20%

27%

0% 10% 20% 30% 40% 50%

Other

Improving employee engagement and focus

Reducing expenses and downsizing

Improving core skills and capabilities within HR

Implementing HR systems

Improving employee performance management and rewards

Restructuring or transforming HR

Becoming a more effective learning organization

Improving leadership development

Improving staffing and recruiting

Creating integrated talent management

Q4'2010 Q1'2010 Q3'2009

36bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

CONCLUSIONS

» As we enter 2011, it is clear that most organizations see global growth. While the U.S.

economy is still growing slowly, medium to large businesses are now investing in growth

opportunities in Asia, the Middle East, Eastern Europe and South America.

The most urgent talent problems ahead include building collaborative learning

environments, creating higher levels of employee engagement and developing new

leaders. Leadership continues to be the biggest gap that companies face – and they must

build leadership from the bottom up.

HR and L&D budgets are growing again, leading to new opportunities for HR and L&D

professionals.

Social networking and open web communications have transformed recruiting,

forcing companies to reinvest and rethink their talent acquisition strategies. In a global

“borderless” economy, it is critical for businesses to have an agile and consistent, yet

localized recruiting process. In the coming war for talent, these strategies will differentiate

winners from those who fall behind.

We hope that TalentWatch® gives you a good foundation for the business trends

occurring today. Only by staying vigilant in the alignment between people strategies,

business strategies, and the economic and workforce trends around us can we drive ever-

increasing levels of value to our organizations. «

37bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

DEMOGRAPHICS OF THE TalentWatch® RESEARCH

» Bersin & Associates captured the H2’2010 TalentWatch research during winter of 2010

from among 134 corporations in a wide variety of industries. The average organization

size of the sample is 21,500 employees, with 44 percent representing companies with less

than 5,000 employees. This is a global sample with:

• Seventy-sixpercentoforganizationsheadquarteredintheU.S.;

• EightpercentinWesternandEasternEurope;

• FivepercentinCanada;

• FourpercentinAsia-Pacific;and,

• SixpercentintheMiddleEastandothercountries.

As for the respondents to our survey, 32 percent are vice president-level, 32 percent are

director-level, 19 percent are CXO-level and 16 percent are manager-level.

Eighty percent of all respondents are corporations, 10 percent government, four percent

nonprofit and the remaining are educational institutions.

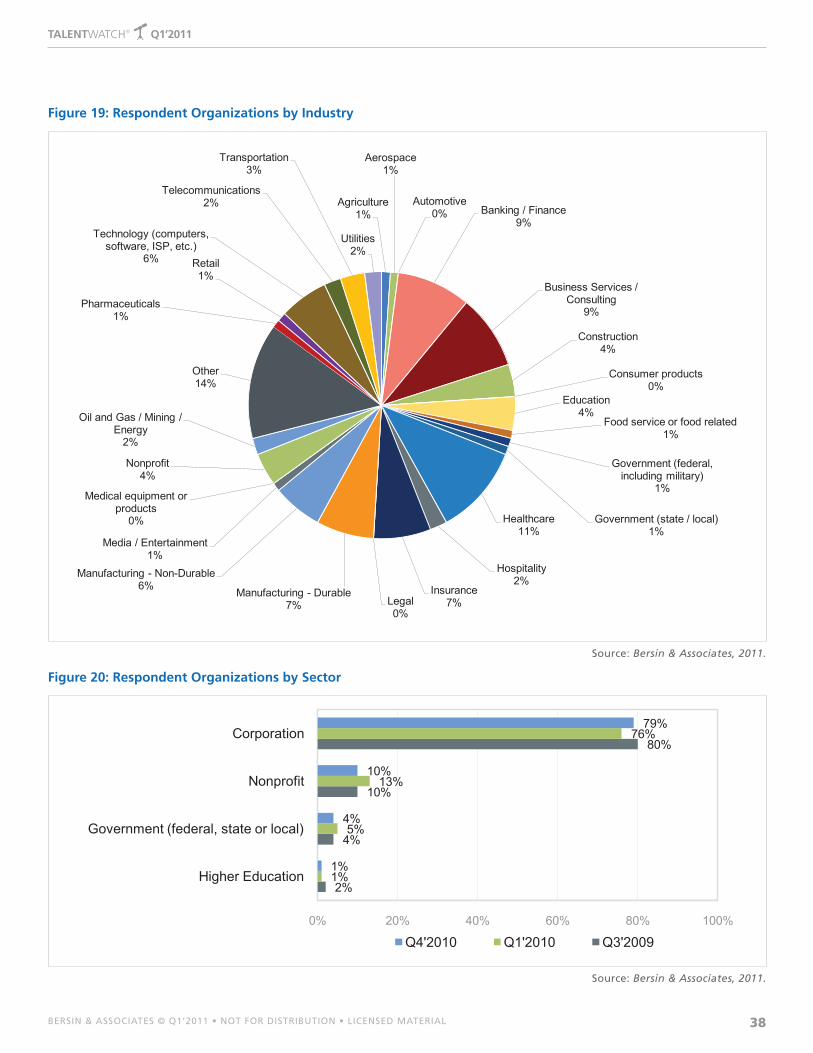

The industry breakdown is shown in Figure 19. «

38bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

Source: Bersin & Associates, 2011.

Figure 19: Respondent Organizations by Industry

Source: Bersin & Associates, 2011.

Figure 20: Respondent Organizations by Sector

Agriculture1%

Aerospace1%

Automotive0% Banking / Finance

9%

Business Services / Consulting

9%

Construction4%

Consumer products0%

Education4%

Food service or food related1%

Government (federal, including military)

1%

Government (state / local)1%

Healthcare11%

Hospitality2%

Insurance7%Legal

0%

Manufacturing - Durable7%

Manufacturing - Non-Durable6%

Media / Entertainment1%

Medical equipment or products

0%

Nonprofit4%

Oil and Gas / Mining / Energy

2%

Other14%

Pharmaceuticals1%

Retail1%

Technology (computers, software, ISP, etc.)

6%

Telecommunications2%

Transportation3%

Utilities2%

2%

4%

10%

80%

1%

5%

13%

76%

1%

4%

10%

79%

0% 20% 40% 60% 80% 100%

Higher Education

Government (federal, state or local)

Nonprofit

Corporation

Q4'2010 Q1'2010 Q3'2009

39bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

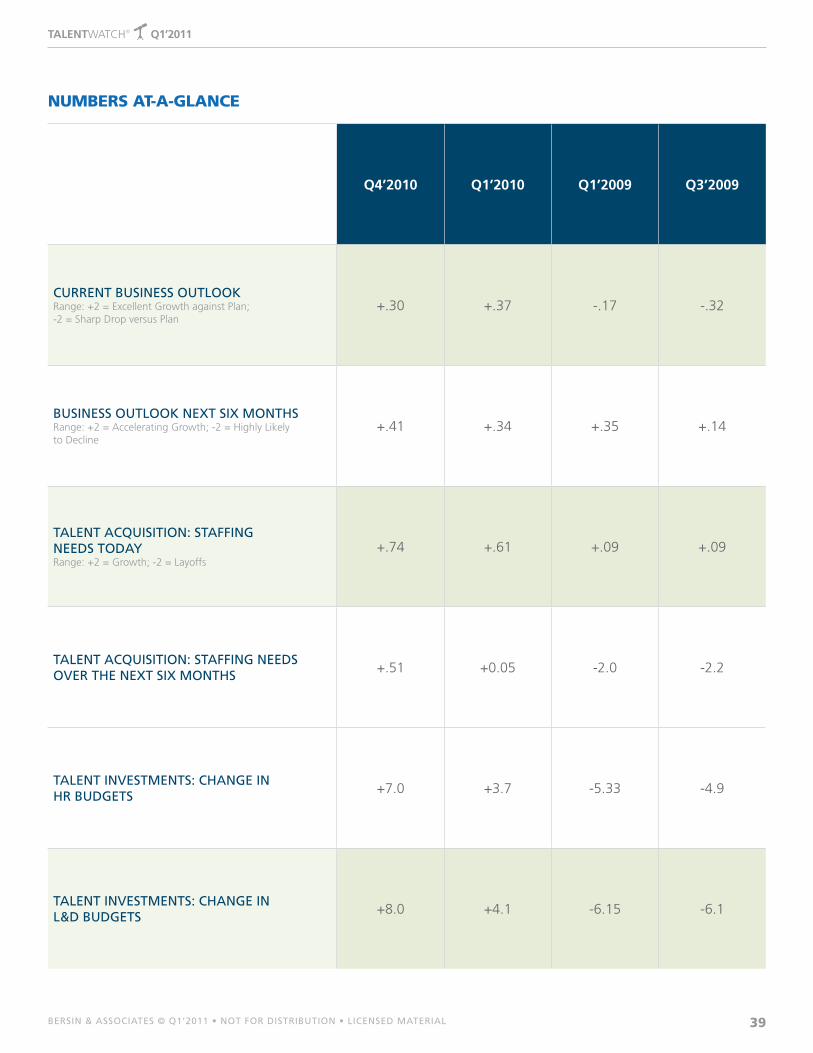

NUMBERS AT-A-GLANCE

Q4’2010 Q1’2010 Q1’2009 Q3’2009

current business outlookRange: +2 = Excellent Growth against Plan; -2 = Sharp Drop versus Plan

+.30 +.37 -.17 -.32

business outlook next six monthsRange: +2 = Accelerating Growth; -2 = Highly Likely to Decline

+.41 +.34 +.35 +.14

talent acQuisition: staffing needs todayRange: +2 = Growth; -2 = Layoffs

+.74 +.61 +.09 +.09

talent acQuisition: staffing needs over the next six months +.51 +0.05 -2.0 -2.2

talent investments: change in hr budgets +7.0 +3.7 -5.33 -4.9

talent investments: change in l&d budgets +8.0 +4.1 -6.15 -6.1

40bersin & associates © Q1’2011 • not for distribution • licensed material

TALENTWATCH® Q1’2011

Bersin & Associates, LLC180 Grand AvenueSuite 320Oakland, CA 94612(510) [email protected]

ABOUT USBersin & Associates is the only research and advisory consulting firm focused solely on WhatWorks® research in enterprise learning and talent management. With more than 25 years of experience in enterprise learning, technology and HR business processes, Bersin & Associates provides actionable, research-based services to help learning and HR managers and executives improve operational effectiveness and business impact.

Bersin & Associates research members gain access to a comprehensive library of best practices, case studies, benchmarks and in-depth market analyses designed to help executives and practitioners make fast, effective decisions. Member benefits include: in-depth advisory services, access to proprietary webcasts and industry user groups, strategic workshops, and strategic consulting to improve operational effectiveness and business alignment. More than 3,500 organizations in a wide range of industries (including more than 60 percent of the FORTUNE 100) benefit from Bersin & Associates research and services.

Bersin & Associates can be reached at www.bersin.com or at (510) 347-4300.

ABOUT THIS RESEARCHCopyright © 2011 Bersin & Associates. All rights reserved.

WhatWorks® and related names such as Rapid e-Learning:

WhatWorks® and The High-Impact Learning Organization®

are registered trademarks of Bersin & Associates. No materials

from this study can be duplicated, copied, republished,

or reused without written permission from Bersin &

Associates. The information and forecasts contained in

this report reflect the research and studied opinions of

Bersin & Associates analysts.

ABOUT BERSIN & ASSOCIATES TALENTWATCH®

TalentWatch® is Bersin & Associates semiannual business research on business trends in talent acquisition,

skills readiness, investments and leadership. Drawing upon our research database of more than 100,000

corporate, government and nonprofit organizations, this proprietary research analyzes a set of 18 indices

designed to give business, government and human resources leaders timely and actionable insights into

workforce trends and benchmarks. Available to Bersin & Associates corporate and enterprise research

members only, this unique report offers our perspectives and opinions on industry-specific talent trends

that affect business decision-making.