BEPS Webcast #7 - Update on project

70

LIVE WEBCAST UPDATE ON BEPS PROJECT 2015 DELIVERABLES AND BEYOND 8 June 2015 5:00pm – 6:00pm (CET)

-

Upload

oecdtax -

Category

Government & Nonprofit

-

view

11.629 -

download

0

Transcript of BEPS Webcast #7 - Update on project

LIVE WEBCAST UPDATE ON BEPS PROJECT 2015 DELIVERABLES AND BEYOND

8 June 2015 5:00pm – 6:00pm (CET)

INTRODUCTION

Pascal Saint-Amans Director, Centre for Tax Policy and Administration

Achim Pross Head, International Cooperation and Tax Administration

Marlies de Ruiter Head, Tax Treaty, Transfer Pricing and Financial Transactions

David Bradbury Head, Tax Policy and Statistics Andrew Hickman Head, Transfer Pricing Unit

Speakers

3

Ask questions and comment throughout the webcast

Join the discussion

Directly: Enter your question in the space provided Via email: [email protected] Via Twitter: Follow us on @OECDtax using #BEPS

4

STATE OF PLAY AND ROADMAP FOR

DELIVERY

• Work proceeding at BEPS Project pace • Since the last webcast: 7 discussion drafts

published and 6 public consultations held • Special meeting of the CFA in May to discuss

progress and approve CbC Implementation Package

6

State of play

• 27 May 2015 First procedural meeting of the ad hoc group • 5-6 November 2015 Inaugural meeting, Paris

• Members of the Group appointed the Chair (Mr. Mike Williams, UK) and three Vice-Chairs (Mr. Liao Tizhong, China; Mr. Mohammed Amine Baina, Morocco; and Mrs. Kim S. Jacinto-Henares, Philippines)

• International organisations have been invited as observers (UN, IMF, World Bank, CIAT, ATAF, CREDAF, IOTA, SGATAR, CARICOM and ATAIC)

• So far over 80 countries have joined the ad hoc group

Multilateral Instrument First procedural ad hoc meeting

7

• Meetings of CFA subsidiary bodies to finalise technical work on the action items

• Adoption at CFA meeting in September

• Delivery to OECD Council and to G20 Finance Ministers (October) and Leaders (November)

Next steps towards delivery

8

UPDATE ON THE BEPS WORK STREAMS

KEY ELEMENTS OF THE CBC IMPLEMENTATION PACKAGE

10

11

Key elements of the CbC implementation package

• Implementation package is third element of new transfer pricing reporting provisions that will encourage transparency and contribute to tackling BEPS.

• September 2014: report on transfer pricing documentation, requiring master file, local file, and country-by-country (CbC) report which sets out the MNE’s global allocation of income, taxes, and activity.

• February 2015: commitment to confidentiality, consistency, and appropriate use, and guidance on: when CbC reporting starts (FY 2016), which taxpayers have to file (750m euros turnover), and how (framework for implementation based on government-to-government exchange--now developed in the implementation package).

Two elements of the CbC Implementation Package

Model domestic legislation

Competent Authority Agreements - Based on the Multilateral Convention - Based on Double Tax Conventions - Based on TIEAs

12

Key elements of the CbC Implementation Package

13

Key elements of the CbC implementation package

• Key features of model domestic legislation • Filing obligation on resident ultimate parent company • Back-up local filing obligation on resident subsidiary, but only when:

– Ultimate parent company is not obliged to file in its jurisdiction, or – There is no competent authority agreement under existing exchange instrument with

that jurisdiction, or – There is a systemic failure to exchange after agreeing to do so.

• Where there are multiple subsidiaries in a jurisdiction, the MNE group can designate one to file on behalf of all

• MNE groups can elect a surrogate parent entity to file on behalf of ultimate parent (providing option to reduce scope of local filing)

14

Key elements of the CbC implementation package

Competent Authority Agreements

Multilateral Competent Authority Agreement, based on Article 6 of the Multilateral Convention

Model Competent Authority Agreement on the basis of Article 26 of a Double Tax Convention

Model Competent Authority Agreement on the basis of a TIEA

15

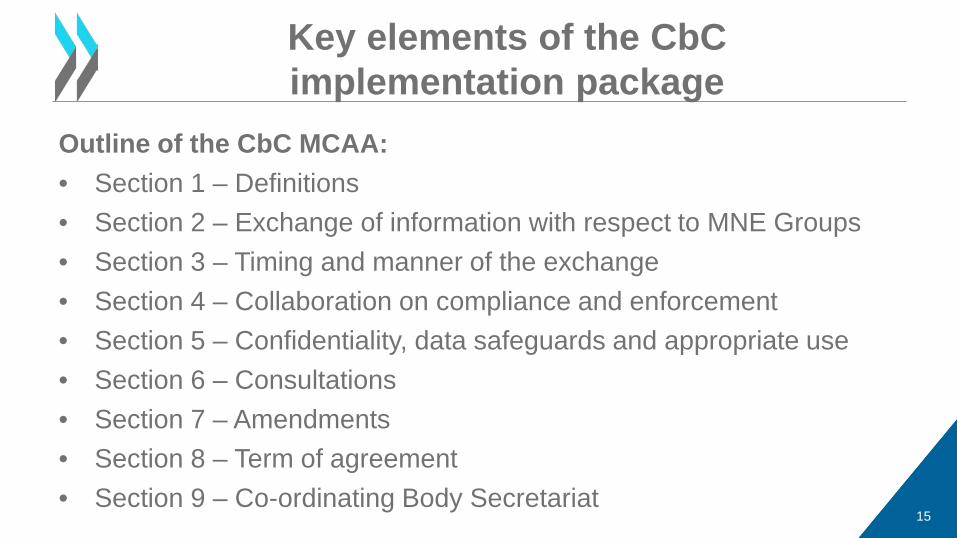

Key elements of the CbC implementation package

Outline of the CbC MCAA: • Section 1 – Definitions • Section 2 – Exchange of information with respect to MNE Groups • Section 3 – Timing and manner of the exchange • Section 4 – Collaboration on compliance and enforcement • Section 5 – Confidentiality, data safeguards and appropriate use • Section 6 – Consultations • Section 7 – Amendments • Section 8 – Term of agreement • Section 9 – Co-ordinating Body Secretariat

16

Key elements of the CbC implementation package

Example of the timing of the exchange (Section 3 CbC MCAA):

09/15 12/15 01/16 03/19

2015 2016 2017 2018 2019

06/18 12/17

Signing of MCAA

Activation under

Section 8

1st year to report

6 months for CA review

1st Filing deadline for MNEs

2nd Transmission of CbC Report

(for 2017)

1st Transmission of CbC Report

(for 2016)

12/18

2nd Filing deadline for MNEs

3 months for CA review

Key elements of the CbC implementation package

• Confidentiality and data safeguards rules correspond to those of the CRS MCAA

• The CbC MCAA contains specific rules on the appropriate use of CbC Reports (Section 5 (2))

17

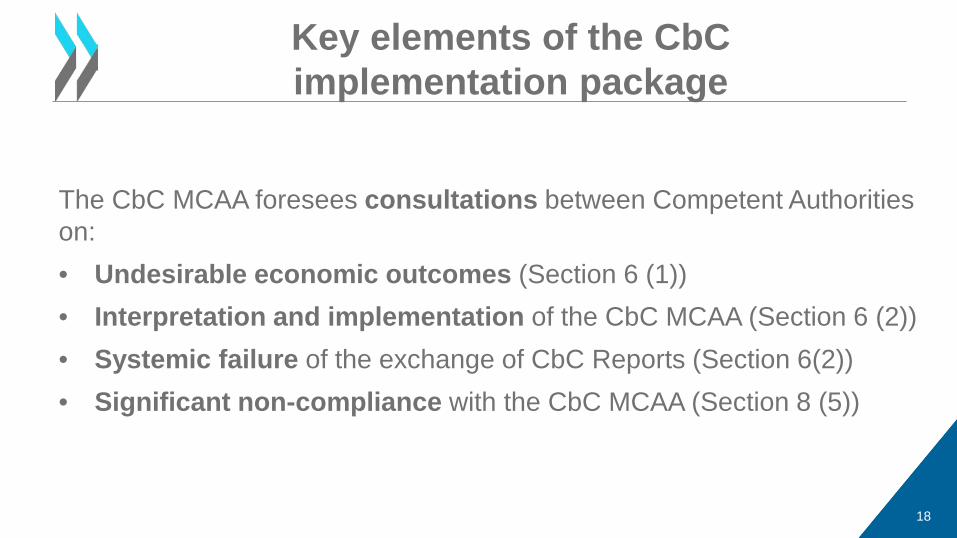

Key elements of the CbC implementation package

The CbC MCAA foresees consultations between Competent Authorities on: • Undesirable economic outcomes (Section 6 (1)) • Interpretation and implementation of the CbC MCAA (Section 6 (2)) • Systemic failure of the exchange of CbC Reports (Section 6(2)) • Significant non-compliance with the CbC MCAA (Section 8 (5))

18

ESTABLISHING

METHODOLOGIES TO COLLECT

AND ANALYSE DATA

19

20

Establishing methodologies to collect and analyse data

There are four elements to Action 11: • Identify and assess a range of existing data sources

• Recommend indicators of the scale and economic impact of BEPS

• Undertake an economic analysis of: – scale (fiscal effects) and economic impact of BEPS; and

– effectiveness of BEPS countermeasures

• Make recommendations regarding new data and tools to monitor and evaluate BEPS and countermeasures on an ongoing basis

21

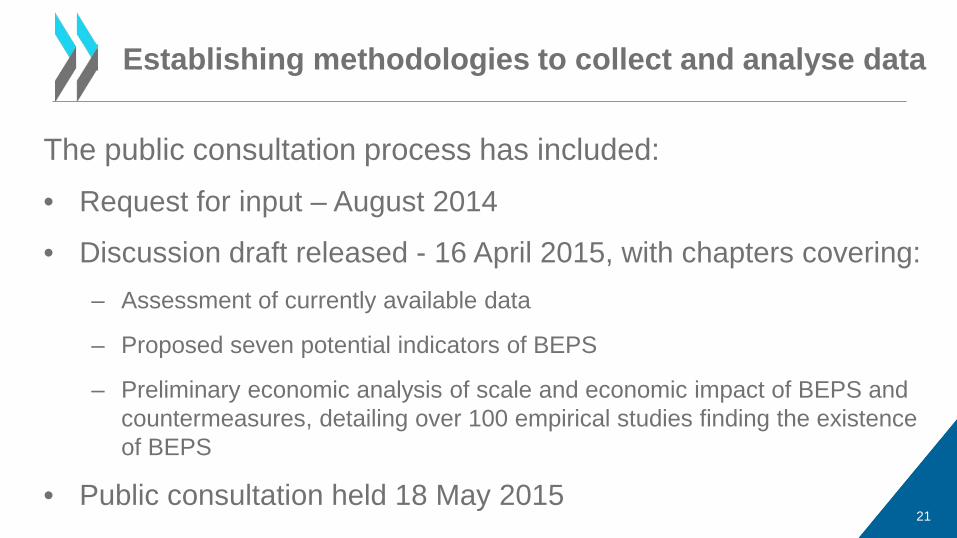

Establishing methodologies to collect and analyse data

The public consultation process has included:

• Request for input – August 2014

• Discussion draft released - 16 April 2015, with chapters covering: – Assessment of currently available data

– Proposed seven potential indicators of BEPS

– Preliminary economic analysis of scale and economic impact of BEPS and countermeasures, detailing over 100 empirical studies finding the existence of BEPS

• Public consultation held 18 May 2015

22

Establishing methodologies to collect and analyse data

Feedback received from the public consultations included: • Consensus regarding the conclusions that currently available data

sources are insufficient

• Concerns that indicators can be influenced by non-BEPS factors, but strong support for the qualifications and caveats in the paper

• Some support for the general approach presented for the economic analysis – i.e. multiple approaches to estimating the fiscal effects

• Many calls for new data to be made available, but concerns expressed about confidentiality and compliance costs

23

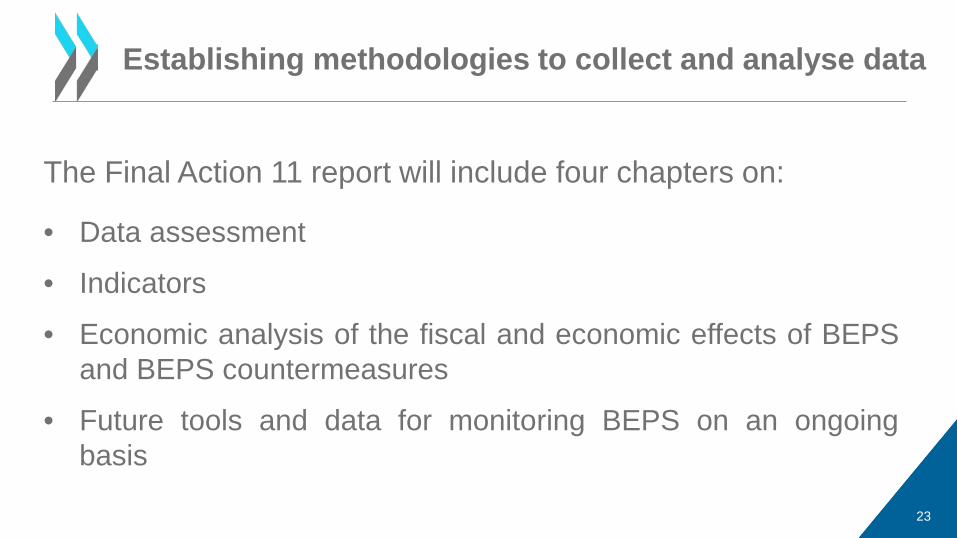

Establishing methodologies to collect and analyse data

The Final Action 11 report will include four chapters on:

• Data assessment

• Indicators

• Economic analysis of the fiscal and economic effects of BEPS and BEPS countermeasures

• Future tools and data for monitoring BEPS on an ongoing basis

UPDATE ON TRANSFER PRICING WORK STREAMS

24

• Discussion draft issued 4th June for comments by 18th June, and public consultation 6-7th July

• HTVI present some of the hardest transfer pricing challenges due to information asymmetry and therefore scope for mispricing

• Third parties use different pricing strategies to address uncertainties when setting prices, including pricing arrangements linked to the actual results

25

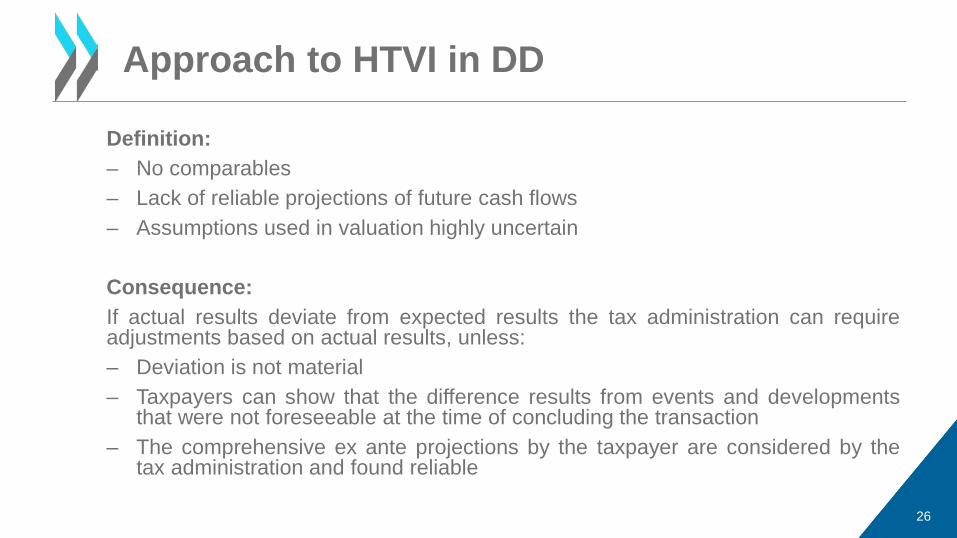

Hard to ValueIntangibles (HTVI)

Definition: – No comparables – Lack of reliable projections of future cash flows – Assumptions used in valuation highly uncertain

Consequence: If actual results deviate from expected results the tax administration can require adjustments based on actual results, unless: – Deviation is not material – Taxpayers can show that the difference results from events and developments

that were not foreseeable at the time of concluding the transaction – The comprehensive ex ante projections by the taxpayer are considered by the

tax administration and found reliable

26

Approach to HTVI in DD

• DD seeks comments in particular on additional exemptions and implementation guidance.

27

Discussion draft

• Comments (341 pages) on DD published 1st June. Public consultation 6-7th July.

• DD proposes more rigorous rules for CCAs, including requiring participants to have certain capability and for contributions to be measured at value.

• The proposals seek to align outcomes under CCAs with those under the revisions to Chapter VI on intangibles and Chapter I on risk, and to prevent the scope for CCAs to be used inappropriately to transfer intangibles at undervalue.

28

Cost Contribution Arrangements (“CCAs”)

• Commentators generally agree that pre-existing contributions to a CCA should be at value, but argue that current contributions (e.g. performance of R&D activities) should continue to be made at cost.

• Some commentators suggest that targeted rules could prevent the abuse of CCAs while preserving the commercial effectiveness of cost-based CCAs.

• Strong interest in grandfathering provisions if proposed changes are made, given the long-term nature of some CCAs.

29

Update on Transfer Pricing work streams

FORUM ON HARMFUL TAX PRACTICES

30

FHTP – status of discussion

31

• Substantial activity – Three open issues i) tracking and tracing ii) definition of IP assets iii) safeguards. – Very good progress on tracking and tracing with further guidance to be included

in the 2015 Report. Also progress on definition of income and safeguards. • Transparency

– General agreement that compulsory spontaneous exchange should include all rulings that could give rise to BEPS concerns in the absence of exchange.

– Limited to a number of defined categories and only exchanged with certain affected jurisdictions.

– Closely coordinated with work in EU – Differentiates between existing and future rulings – Exchanged via a standard template

DISPUTE RESOLUTION

32

• Minimum standard with respect to the resolution of treaty-related disputes so that:

– Treaty obligations related to MAP are fully implemented in good faith and cases are resolved in a timely manner

– Administrative processes for prevention and timely resolution of treaty-related disputes are implemented; and

– Ensure that taxpayers can access MAP when eligible.

• Arbitration for willing countries – Will be included in the multilateral instrument – See also G7 chair's summary: “…Establishing better and more effective dispute

resolution mechanisms between tax administrations to ensure that the risk of double taxation does not act as barrier to trade and investment, enhancing the collaboration of our tax administrations and conducting joint tax audits”. 33

Making Dispute Resolution Mechanisms Effective

CFC RULES

34

CFC rules

35

Action 3 CFCs

This work will be co-ordinated with other

work as necessary.

Develop recommendations

regarding the design of controlled foreign

company rules.

CFC rules: 2015 Report

36

• Definition of a CFC, including control • Low-tax exemption and threshold requirements • Definition of income • Rules for computing income • Rules for attributing income • Rules to prevent or eliminate double taxation

Building blocks for effective CFC rules

CFC rules: policy considerations

37

• CFC rules are part of a jurisdiction’s overall tax system, so the policy objectives of the tax system affect the policy objectives of CFC rules

• CFC rules that are part of worldwide systems may focus more on long-term deferral and foreign-to-foreign stripping

• CFC rules that are part of territorial systems may focus more on shifting out of the parent jurisdiction

General agreement that different CFC rules prioritise different policy objectives

CFC rules: indicia/factors

38

• Most jurisdictions have the same overall concern: income has been shifted into the CFC and separated from underlying value creation

• But different jurisdictions look at different indicia/factors:

legal classification, relatedness of parties, source of income, substance

• Recommendations must be flexible and not overly

prescriptive

Different CFC rules also look at different factors

CFC rules: definition of income

39

• Non-exhaustive list of approaches and combinations of approaches: • Categorical analyses – divide income based on legal

classification, relatedness of parties, and source of the income

• Substance analyses – look at various proxies, including people, premises, assets and risk

• Excess profits analysis – treats income above a normal return as CFC income

Discussion and public comments have focused on definition of income

INTEREST DEDUCTIBILITY

40

Interest deductibility The problem

“no or low taxation associated with practices that artificially

segregate taxable income from the activities that generate it”

BEPS Action Plan, chapter 3

location of third party interest in

high tax countries

quantity of related party interest, in

excess of group’s actual interest

cost

use of interest expense to fund

tax exempt income

41

Interest deductibility Action Item 4

42

Develop recommendations regarding best practices in the design of rules to prevent base erosion through the use of interest expense …

… to achieve excessive interest deductions or to finance the production of exempt or deferred income …

… for example, through the use of related party and third party debt …

… and other financial payments that are economically equivalent to interest.

42

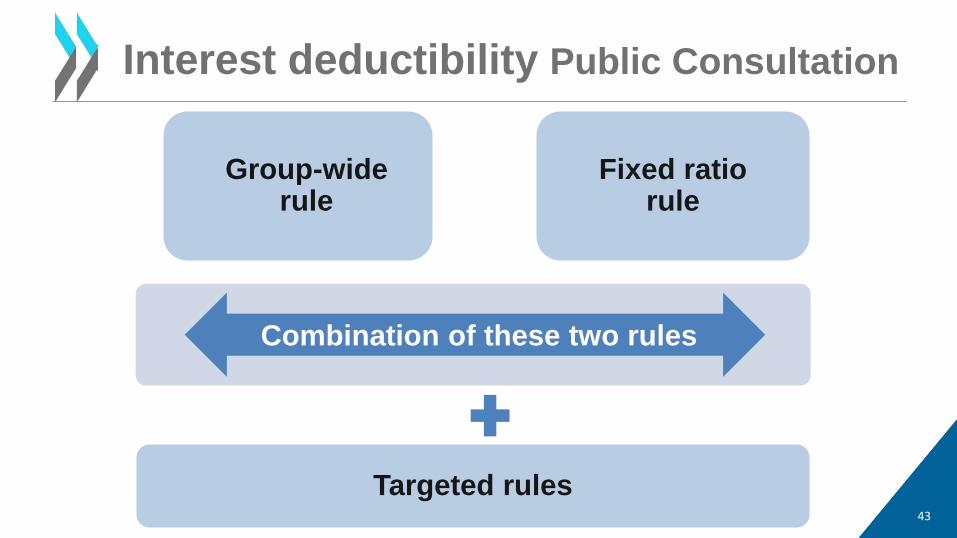

Interest deductibility Public Consultation

43

Targeted rules

Fixed ratio rule

Combination of these two rules

Group-wide rule

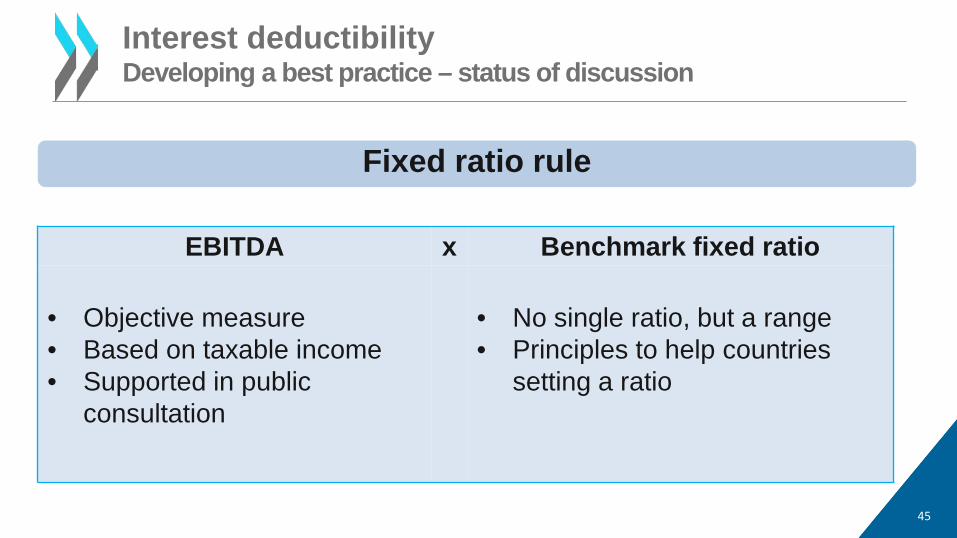

Interest deductibility Developing a best practice – status of discussion

44

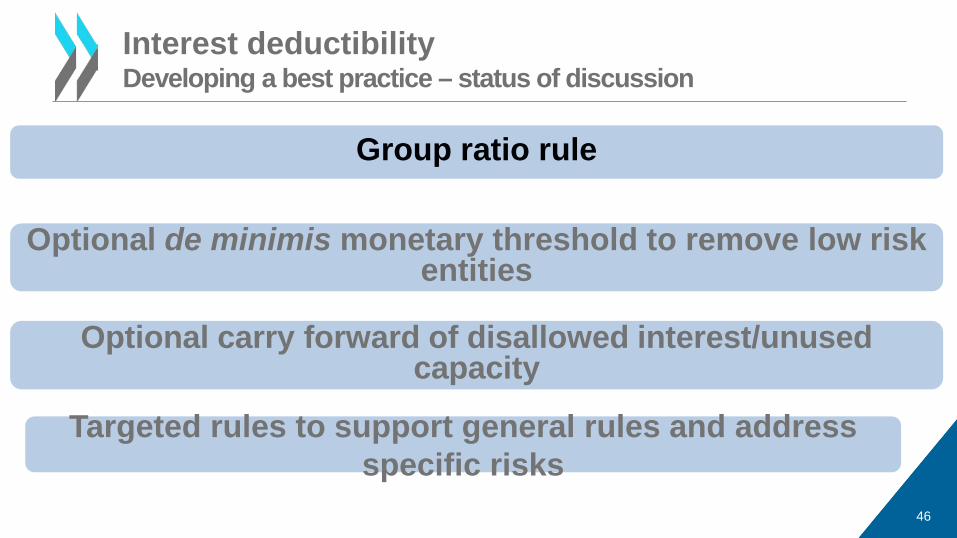

Group ratio rule

Optional carry forward of disallowed interest/unused capacity

Optional de minimis monetary threshold to remove low risk entities

Fixed ratio rule

Targeted rules to support general rules and address specific risks

Fixed ratio rule

EBITDA x Benchmark fixed ratio

• Objective measure • Based on taxable income • Supported in public

consultation

• No single ratio, but a range • Principles to help countries

setting a ratio

45

Interest deductibility Developing a best practice – status of discussion

46

Group ratio rule

Optional carry forward of disallowed interest/unused capacity

Optional de minimis monetary threshold to remove low risk entities

Targeted rules to support general rules and address specific risks

Interest deductibility Developing a best practice – status of discussion

47

Group ratio rule

Optional carry forward of disallowed interest/unused capacity

Optional de minimis monetary threshold to remove low risk entities

Targeted rules to support general rules and address specific risks

Interest deductibility Developing a best practice – status of discussion

48

Group ratio rule

Optional carry forward of disallowed interest/unused capacity

Optional de minimis monetary threshold to remove low risk entities

Targeted rules to support general rules and address specific risks

Interest deductibility Developing a best practice – status of discussion

49

Group ratio rule

Optional carry forward of disallowed interest/unused capacity

Optional de minimis monetary threshold to remove low risk entities

Targeted rules to support general rules and address specific risks

Interest deductibility Developing a best practice – status of discussion

TREATY ABUSE

50

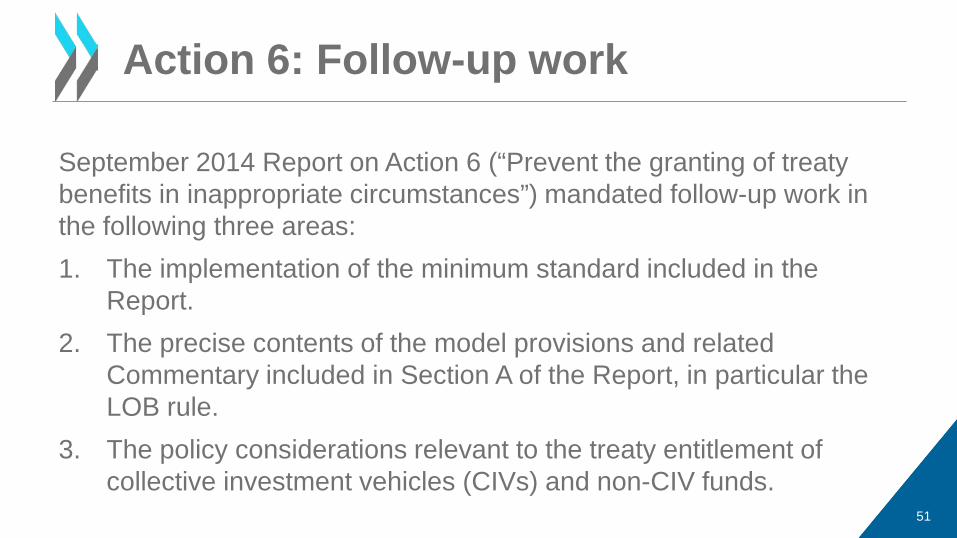

Action 6: Follow-up work

51

September 2014 Report on Action 6 (“Prevent the granting of treaty benefits in inappropriate circumstances”) mandated follow-up work in the following three areas: 1. The implementation of the minimum standard included in the

Report. 2. The precise contents of the model provisions and related

Commentary included in Section A of the Report, in particular the LOB rule.

3. The policy considerations relevant to the treaty entitlement of collective investment vehicles (CIVs) and non-CIV funds.

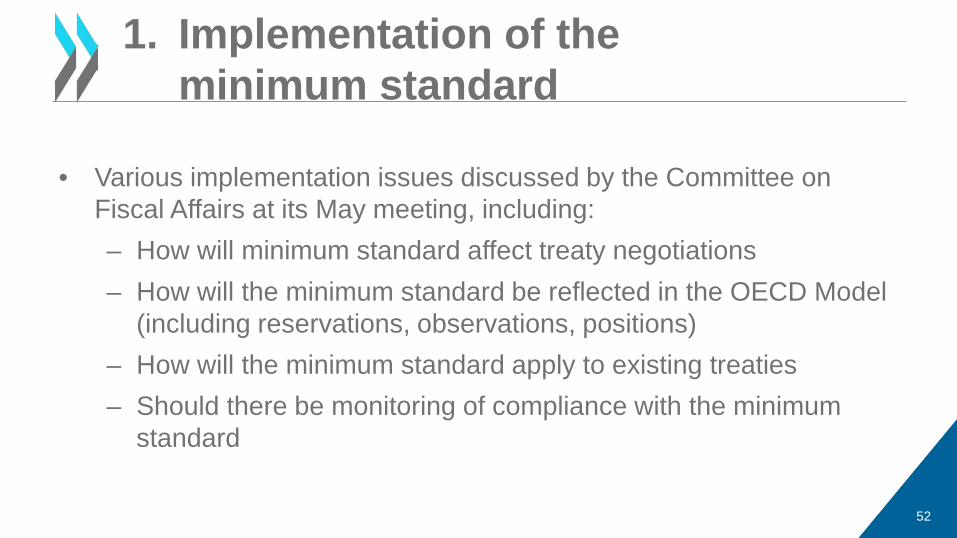

• Various implementation issues discussed by the Committee on Fiscal Affairs at its May meeting, including: – How will minimum standard affect treaty negotiations – How will the minimum standard be reflected in the OECD Model

(including reservations, observations, positions) – How will the minimum standard apply to existing treaties – Should there be monitoring of compliance with the minimum

standard

52

1. Implementation of the minimum standard

• Discussion draft released on 21 November 2014 invited comments on a number of technical issues related to the model provisions included in the Report on Action 6

• These issues were further discussed on the basis of the comments received and a revised discussion draft was released on 22 May

53

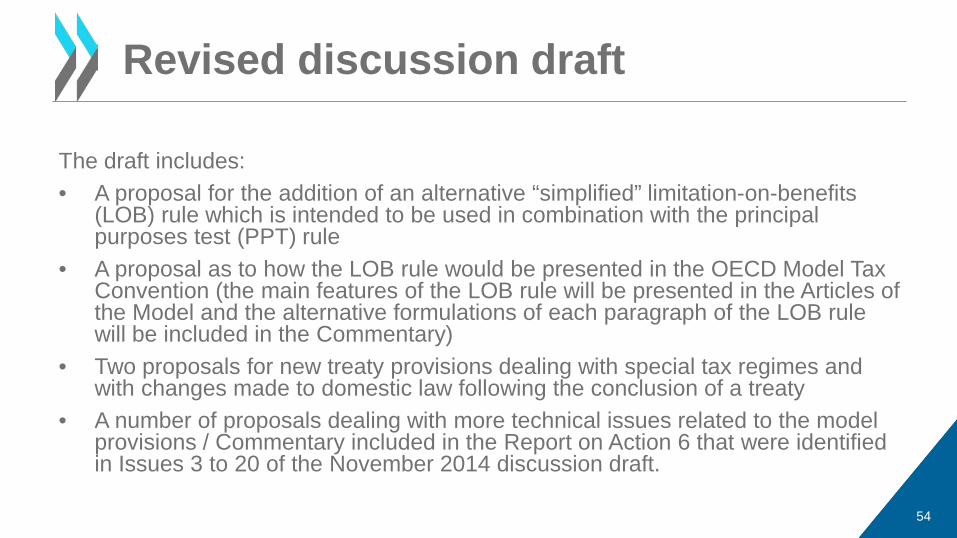

2. Model provisions included in the Report on Action 6

The draft includes: • A proposal for the addition of an alternative “simplified” limitation-on-benefits

(LOB) rule which is intended to be used in combination with the principal purposes test (PPT) rule

• A proposal as to how the LOB rule would be presented in the OECD Model Tax Convention (the main features of the LOB rule will be presented in the Articles of the Model and the alternative formulations of each paragraph of the LOB rule will be included in the Commentary)

• Two proposals for new treaty provisions dealing with special tax regimes and with changes made to domestic law following the conclusion of a treaty

• A number of proposals dealing with more technical issues related to the model provisions / Commentary included in the Report on Action 6 that were identified in Issues 3 to 20 of the November 2014 discussion draft.

54

Revised discussion draft

As indicated in the revised Discussion draft: • No need for additional changes to address issues related to CIVs

but the implementation of TRACE is important • The Report on Action 6 should recognise the conclusions of the

2008 REIT (Real Estate Investment Trusts) Report • WP1 will examine a proposal according to which a pension fund

would be considered to be a resident of the State in which it is constituted

• WP1 will continue to explore solutions to the broader question of the treaty entitlement of non-CIV funds. That work might continue after the September 2015 adoption of the final Report on Action 6 55

3. Treaty entitlement of CIV and non-CIV funds

ARTIFICIAL AVOIDANCE OF PE

56

• 14 options concerning commissionnaire arrangements and similar strategies, artificial avoidance of Art. 5(4) of the OECD Model, splitting-up of contracts for the purposes of benefiting from Art. 5(3), insurance companies that sell insurance in a local market without having a PE in that market

• 850 pages of comments; public consultation meeting on 21 January 2015

• The options were reviewed in the light of these comments and narrowed down to a few detailed proposals included in a new discussion draft released on 15 May

57

First discussion draft on Action 7 released on 31 October 2014

• Commissionnaire arrangements and similar strategies: Art. 5(5) and 5(6) of the OECD Model should be modified – to apply where a person “concludes contracts, or negotiates the

material elements of contracts”; – by referring to contracts in the name of the enterprise, for the transfer of

property of the enterprise or for the provision of services by the enterprise”; and

– by modifying the “independent agent” exception in Art. 5(6). • These changes to Art. 5(5) and 5(6) correspond to the option that a majority

of business commentators considered to be the least objectionable.

58

Second discussion draft of 15 May

• Art. 5(4) of the OECD Model should be modified so that each of the exceptions included in that paragraph would be restricted to activities that are otherwise of a “preparatory or auxiliary” character

• A new paragraph be added to the definition of PE in Article 5 of the OECD Model to prevent the application of Art. 5(4) where activities have been fragmented (by one enterprise or connected enterprises)

59

Art. 5(4) (specific activity exemptions)

• Splitting-up of contracts: Should be addressed through the Principal Purposes Test rule drafted as part of the work on Action 6 (Treaty Abuse): the Commentary on that rule should include an example of splitting-up of contracts. Commentary on Article 5 should also include an alternative provision to be used by States that wish to deal expressly with that issue and States that do not include the PPT in their treaties

• Insurance: No specific provision dealing with insurance activities should be included in Article 5 ; insurance should be subject to the general rules

• Profit attribution to PEs: Further work involving both WP1 and WP6 delegates should be carried on in this area.

60

Other proposals

• The second discussion draft includes detailed Commentary which clarifies various new concepts introduced by the proposed changes to Article 5 (e.g. meaning of “negotiates the material elements of contracts” and of “preparatory or auxiliary”).

61

Detailed Commentary

POST-BEPS AGENDA

Post-BEPS Agenda

63

Implementation and Monitoring: • Achieve the objectives of the work • Monitor implementation to level the playing field • Ensure principled implementation: focus on administerability

of the standards/limiting cost of compliance

Inclusiveness: • G20 countries on an equal footing • Extending the approach to developing countries • Global Forum type of approach

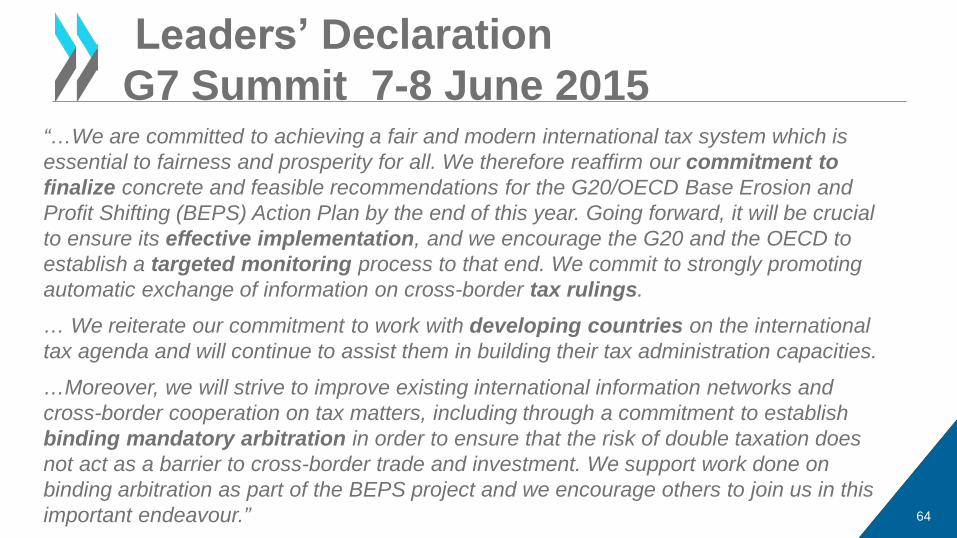

“…We are committed to achieving a fair and modern international tax system which is essential to fairness and prosperity for all. We therefore reaffirm our commitment to finalize concrete and feasible recommendations for the G20/OECD Base Erosion and Profit Shifting (BEPS) Action Plan by the end of this year. Going forward, it will be crucial to ensure its effective implementation, and we encourage the G20 and the OECD to establish a targeted monitoring process to that end. We commit to strongly promoting automatic exchange of information on cross-border tax rulings.

… We reiterate our commitment to work with developing countries on the international tax agenda and will continue to assist them in building their tax administration capacities.

…Moreover, we will strive to improve existing international information networks and cross-border cooperation on tax matters, including through a commitment to establish binding mandatory arbitration in order to ensure that the risk of double taxation does not act as a barrier to cross-border trade and investment. We support work done on binding arbitration as part of the BEPS project and we encourage others to join us in this important endeavour.” 64

Leadersʼ Declaration G7 Summit 7-8 June 2015

IMMEDIATE NEXT STEPS

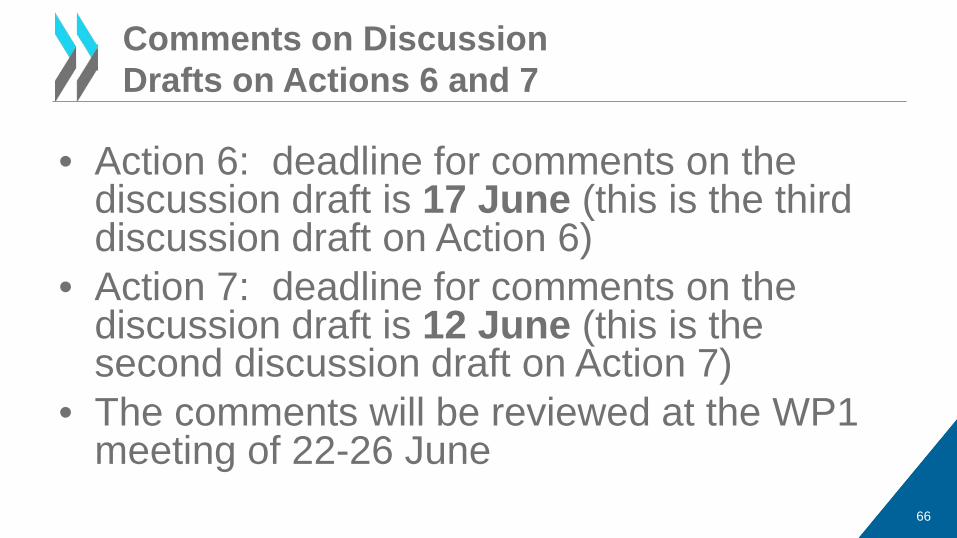

• Action 6: deadline for comments on the discussion draft is 17 June (this is the third discussion draft on Action 6)

• Action 7: deadline for comments on the discussion draft is 12 June (this is the second discussion draft on Action 7)

• The comments will be reviewed at the WP1 meeting of 22-26 June

Comments on Discussion Drafts on Actions 6 and 7

66

• Comments DD on CCAs published on June 1st. • Deadline for comments on DD on HTVI on June18th. • Chapter I on delineation of the actual transaction, risks and non-recognition:

presentation of the directions taken following the March 2015 Public Consultation at the next Public Consultation in July.

• Chapter VI: Changes to align with Chapter I are being made. No substantial changes to the approach. Presentation of relevant changes to the guidance at next Public Consultation in July.

• WP6 meetings from June 29th until July 10th. • Public Consultation on July 6th and 7th.

Comments and Public Consultation on Transfer Pricing issues

67

JOIN THE DISCUSSION

Ask questions and comment

Join the discussion

Directly: Enter your question in the space provided Via email: [email protected] Via Twitter: Follow us via @OECDtax using #BEPS

69

Keep in touch

Website: www.oecd.org/tax/beps.htm Contact: [email protected] Tax email alerts: www.oecd.org/ctp/tax-news.htm

Via Twitter: Follow us via @OECDtax