LIVE WEBCAST - The Transfer Pricing Hubtransferpricinghub.com/.../07/OECD-BEPS-webcast-6-.pdf ·...

50

LIVE WEBCAST UPDATE ON BEPS PROJECT 2015 DELIVERABLES AND BEYOND 12 February 2015 3:00pm – 4:00pm (CET)

Transcript of LIVE WEBCAST - The Transfer Pricing Hubtransferpricinghub.com/.../07/OECD-BEPS-webcast-6-.pdf ·...

LIVE WEBCAST UPDATE ON BEPS PROJECT 2015 DELIVERABLES AND BEYOND

12 February 2015 3:00pm – 4:00pm (CET)

INTRODUCTION

Pascal Saint-Amans Director, Centre for Tax Policy and Administration

Raffaele Russo Head, BEPS Project

Achim Pross Head, International Cooperation and Tax Administration

Marlies de Ruiter Head, Tax Treaty, Transfer Pricing and Financial Transactions

Piet Battiau Head, Consumption Taxes Unit

Speakers

3

Ask questions and comment throughout the webcast

Join the discussion

Directly: Enter your question in the space provided Via email: [email protected] Via Twitter: Follow us on @OECDlive using #BEPS

4

PROGRESS REPORTED TO THE G20 FINANCE MINISTERS 9-10 FEBRUARY 2015

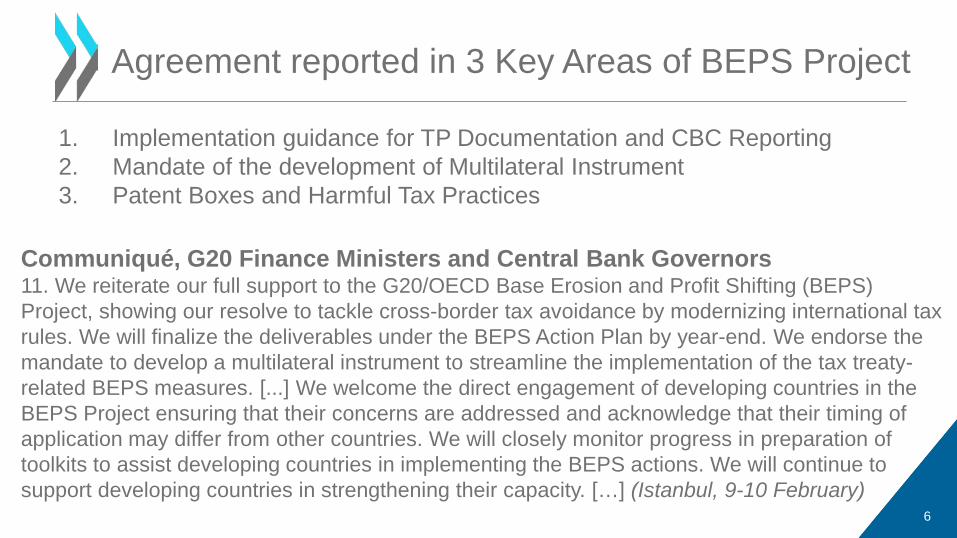

1. Implementation guidance for TP Documentation and CBC Reporting 2. Mandate of the development of Multilateral Instrument 3. Patent Boxes and Harmful Tax Practices

Agreement reported in 3 Key Areas of BEPS Project

Communiqué, G20 Finance Ministers and Central Bank Governors 11. We reiterate our full support to the G20/OECD Base Erosion and Profit Shifting (BEPS) Project, showing our resolve to tackle cross-border tax avoidance by modernizing international tax rules. We will finalize the deliverables under the BEPS Action Plan by year-end. We endorse the mandate to develop a multilateral instrument to streamline the implementation of the tax treaty-related BEPS measures. [...] We welcome the direct engagement of developing countries in the BEPS Project ensuring that their concerns are addressed and acknowledge that their timing of application may differ from other countries. We will closely monitor progress in preparation of toolkits to assist developing countries in implementing the BEPS actions. We will continue to support developing countries in strengthening their capacity. […] (Istanbul, 9-10 February)

6

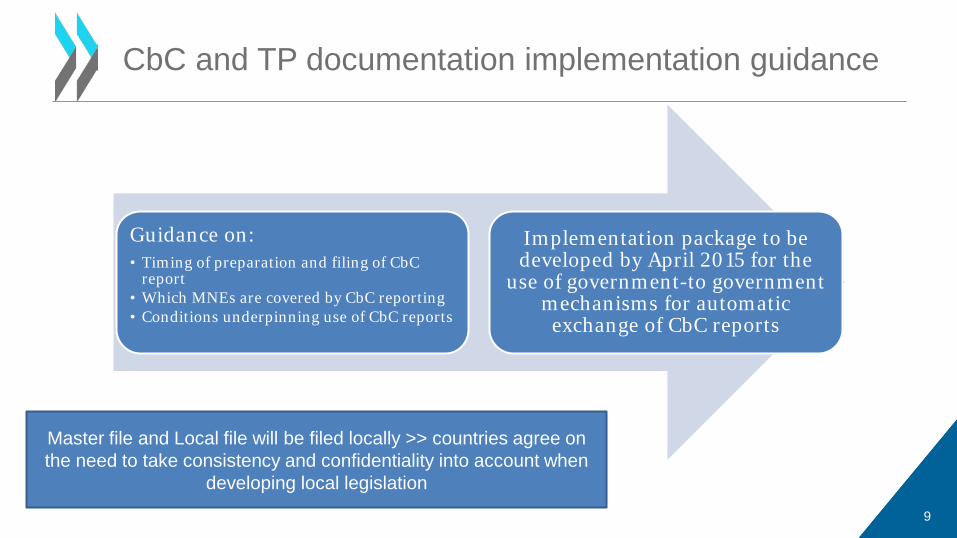

CBC AND TP DOCUMENTATION IMPLEMENTATION GUIDANCE

Background

New transfer pricing documentation guidance was published in September 2014 and presented to the G20 Finance Ministers at their September 2014 meeting and to G20 Leaders at their November 2014 meeting. Includes three types of documents:

Master file containing standardised background information regarding the MNE group.

Local file analysing specific transfer pricing compliance for material transactions of the local taxpayer.

Country-by-Country (CbC) report containing specific information relating to the global allocation of the MNE’s income, taxes paid and certain indicators of the geographic location of economic activity within the MNE group. 8

Guidance on: • Timing of preparation and filing of CbC

report • Which MNEs are covered by CbC reporting • Conditions underpinning use of CbC reports

Implementation package to be developed by April 2015 for the

use of government-to government mechanisms for automatic

exchange of CbC reports

CbC and TP documentation implementation guidance

Master file and Local file will be filed locally >> countries agree on the need to take consistency and confidentiality into account when

developing local legislation

9

Automatic exchange by the jurisdiction where the ultimate parent company is resident

Competent authority agreement(s)

Use of existing legal instruments for EoI as a basis of the Competent authority agreement(s)

Secondary mechanisms recognised as legitimate only in a few cases

Monitoring. Outcomes monitoring taken into account in review in 2020

GtG mechanism for exchange of the CbC report

10

HARMFUL TAX PRACTICES

Overview

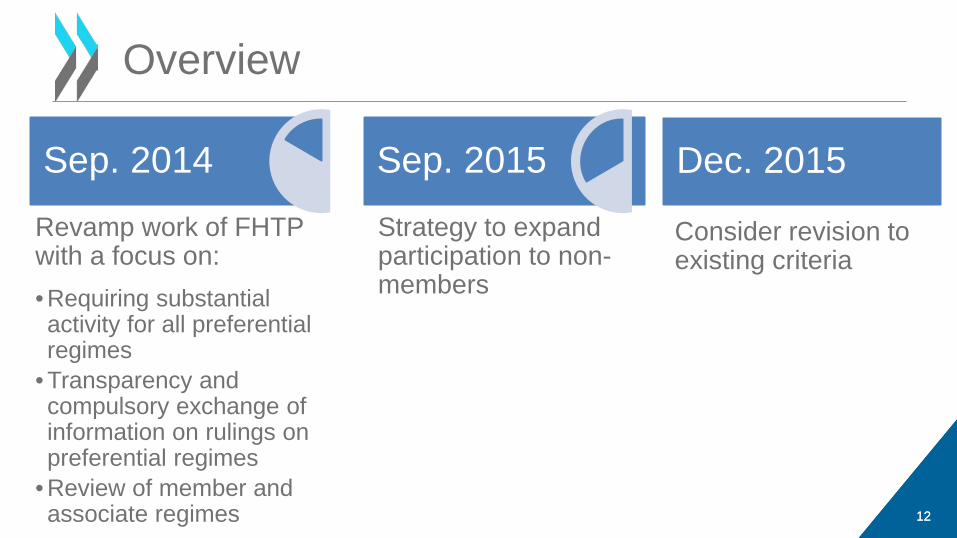

12

Sep. 2014 Sep. 2015 Dec. 2015

Revamp work of FHTP with a focus on:

• Requiring substantial activity for all preferential regimes

• Transparency and compulsory exchange of information on rulings on preferential regimes

• Review of member and associate regimes

Strategy to expand participation to non-members

Consider revision to existing criteria

12

Two main areas of focus: 1. Substantial activities 2. Transparency

Current work

13

HTP and patent boxes

• No consensus in the 2014 progress report but compromise proposal from Germany and the UK maintaining the principle of the nexus approach with some modifications

• Nexus approach now been agreed – agreement released on

6 February 2015

• Action 5 requires substantial activities in preferential regimes – initially focused on requiring substantial activities in IP regimes (patent boxes)

14

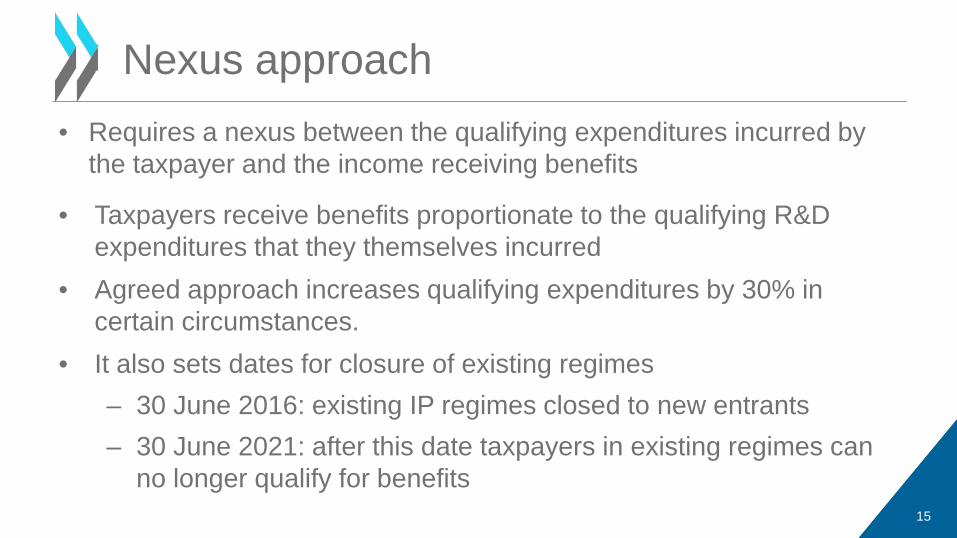

• Taxpayers receive benefits proportionate to the qualifying R&D expenditures that they themselves incurred

• Agreed approach increases qualifying expenditures by 30% in certain circumstances.

• It also sets dates for closure of existing regimes – 30 June 2016: existing IP regimes closed to new entrants – 30 June 2021: after this date taxpayers in existing regimes can

no longer qualify for benefits

Nexus approach • Requires a nexus between the qualifying expenditures incurred by

the taxpayer and the income receiving benefits

15

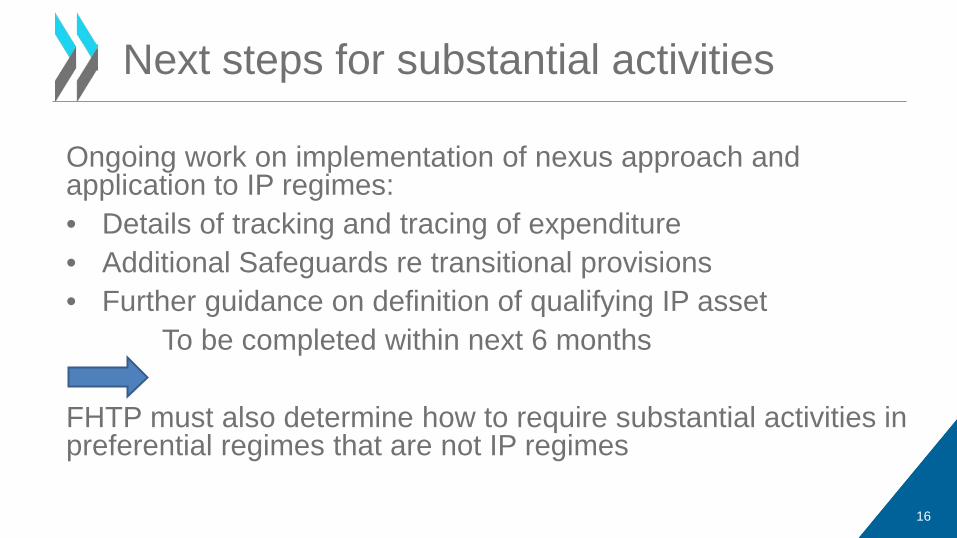

Next steps for substantial activities

Ongoing work on implementation of nexus approach and application to IP regimes: • Details of tracking and tracing of expenditure • Additional Safeguards re transitional provisions • Further guidance on definition of qualifying IP asset To be completed within next 6 months FHTP must also determine how to require substantial activities in preferential regimes that are not IP regimes

16

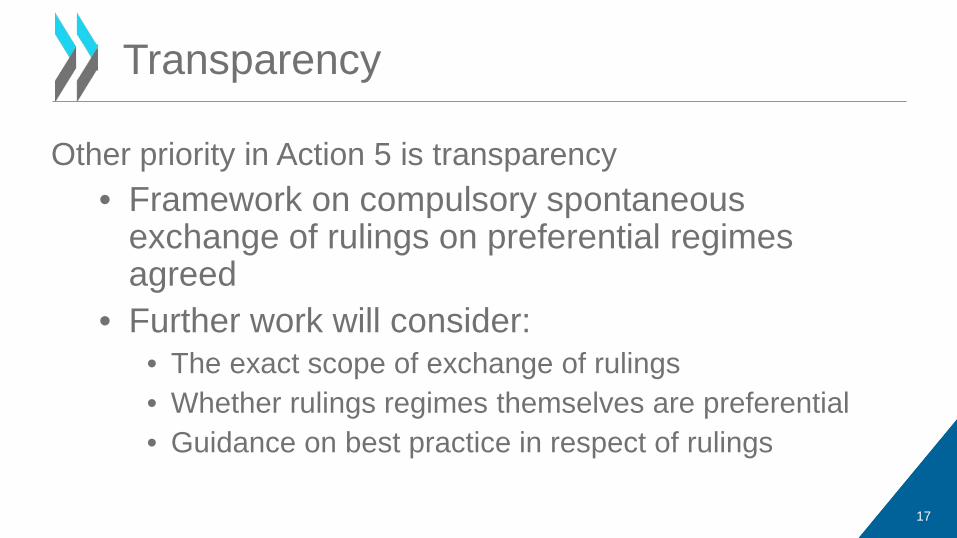

Transparency

Other priority in Action 5 is transparency • Framework on compulsory spontaneous

exchange of rulings on preferential regimes agreed

• Further work will consider: • The exact scope of exchange of rulings • Whether rulings regimes themselves are preferential • Guidance on best practice in respect of rulings

17

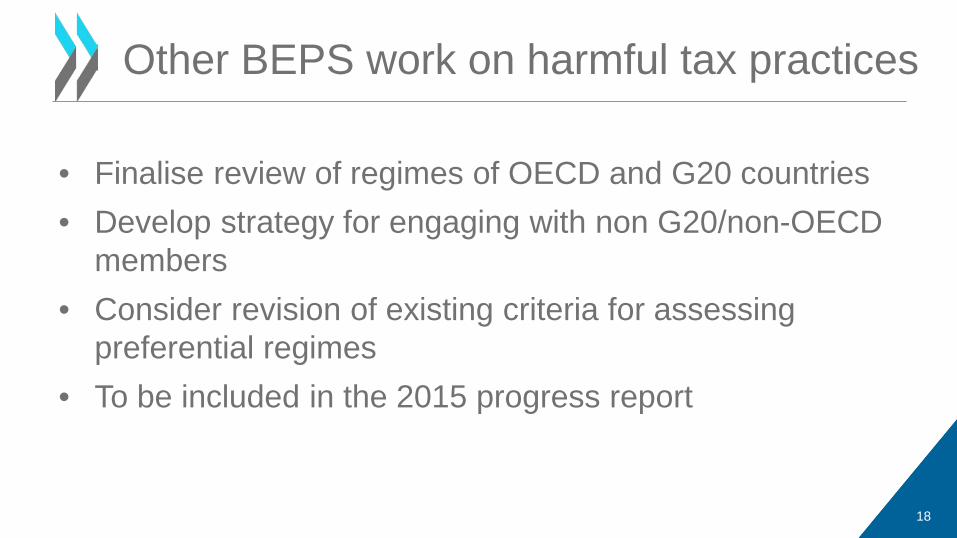

• Finalise review of regimes of OECD and G20 countries • Develop strategy for engaging with non G20/non-OECD

members • Consider revision of existing criteria for assessing

preferential regimes • To be included in the 2015 progress report

Other BEPS work on harmful tax practices

18

MANDATE FOR A MULTILATERAL INSTRUMENT

• September 2014: Report concluded that a multilateral instrument is feasible and desirable.

• January 2015: CFA approved a draft mandate for the negotiation of a multilateral instrument.

Mandate for a multilateral instrument

20

• Scope: Limited to modifying existing DTT to implement treaty-related measures developed. Candidates: – provisions on hybrid entities (Action 2) – Provisions on treaty abuse (Action 6) – Artificial avoidance of the PE (Action 7) – Dispute resolution (Action 14) – Other possible changes (Actions 8-10, etc.)

Mandate for a multilateral instrument: What

21

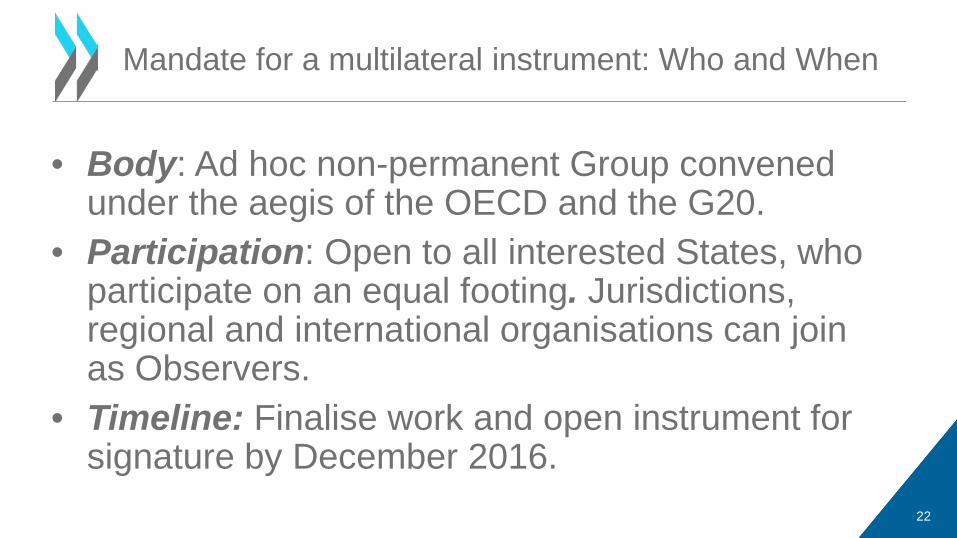

• Body: Ad hoc non-permanent Group convened under the aegis of the OECD and the G20.

• Participation: Open to all interested States, who participate on an equal footing. Jurisdictions, regional and international organisations can join as Observers.

• Timeline: Finalise work and open instrument for signature by December 2016.

Mandate for a multilateral instrument: Who and When

22

INVOLVEMENT OF DEVELOPING COUNTRIES

New structured dialogue process launched in November 2014

1. Direct participation in the Committee on Fiscal Affairs

and its subsidiary

bodies

2. Regional Networks of

tax policy and administration

officials

3. Capacity building support

24

Upcoming Regional Network meetings

– Asia and Pacific Region: Seoul, 12 – 13 February 2015 – Latin America and the Caribbean: Lima, 26-27 February 2015, in

partnership with CIAT – French-speaking countries: Gabon, 27 February 2015, in partnership

with CREDAF – Eurasia: Ankara, 4 - 5 March 2015, in partnership with Turkey – Africa: Pretoria, 20 – 21 April 2015, in partnership with ATAF (African

Tax Administration Forum)

Also open to business and civil society for input

25

RECENT DISCUSSION DRAFTS

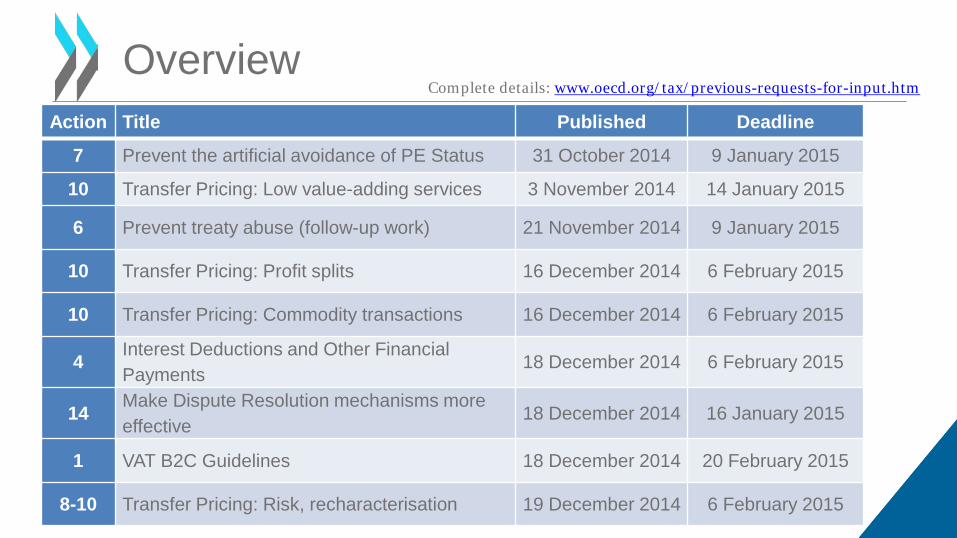

Overview Action Title Published Deadline

7 Prevent the artificial avoidance of PE Status 31 October 2014 9 January 2015

10 Transfer Pricing: Low value-adding services 3 November 2014 14 January 2015

6 Prevent treaty abuse (follow-up work) 21 November 2014 9 January 2015

10 Transfer Pricing: Profit splits 16 December 2014 6 February 2015

10 Transfer Pricing: Commodity transactions 16 December 2014 6 February 2015

4 Interest Deductions and Other Financial Payments

18 December 2014 6 February 2015

14 Make Dispute Resolution mechanisms more effective

18 December 2014 16 January 2015

1 VAT B2C Guidelines 18 December 2014 20 February 2015

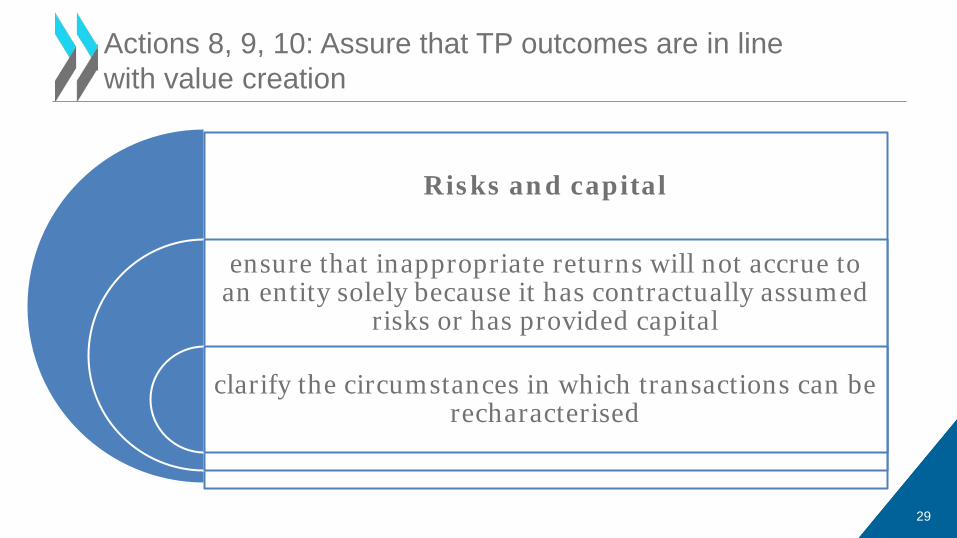

8-10 Transfer Pricing: Risk, recharacterisation 19 December 2014 6 February 2015

Complete details: www.oecd.org/tax/previous-requests-for-input.htm

DISCUSSION DRAFT ON REVISIONS TO CHAPTER 1 OF THE TRANSFER PRICING GUIDELINES (INCLUDING RISK, RECHARACTERISATION, AND SPECIAL MEASURES)

Risks and capital

ensure that inappropriate returns will not accrue to an entity solely because it has contractually assumed

risks or has provided capital

clarify the circumstances in which transactions can be recharacterised

Actions 8, 9, 10: Assure that TP outcomes are in line with value creation

29

Part I Proposed revision to Section D of Chapter

I, including new wording on functional analysis, risks and non-recognition (new

terminology for re-characterisation)

Part II Options for some draft special measures

Revisions to Chapter I of the TP guidelines

30

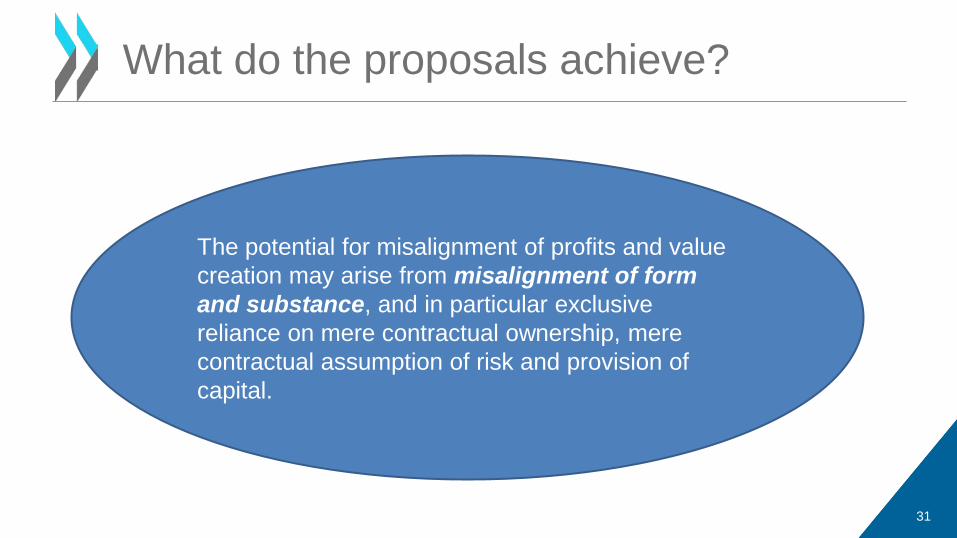

What do the proposals achieve?

The potential for misalignment of profits and value creation may arise from misalignment of form and substance, and in particular exclusive reliance on mere contractual ownership, mere contractual assumption of risk and provision of capital.

31

Revisions to Chapter I set out an analytical framework for:

Key first step of any TP analysis : accurately delineating the actual

transaction

Second step of the TP analysis: pricing the accurately delineated

actual transaction by finding comparables and choosing a TP

method

How to determine the ‘real deal’?

32

Looking at the written contracts

Carefully assess the conduct of the parties in the context of their commercial and financial relations

If the conduct of the parties contradicts or supplements the written contracts: the conduct of the parties is used to supplement or replace

the written contractual arrangements when delineating the actual transaction undertaken

How is the actual transaction delineated?

33

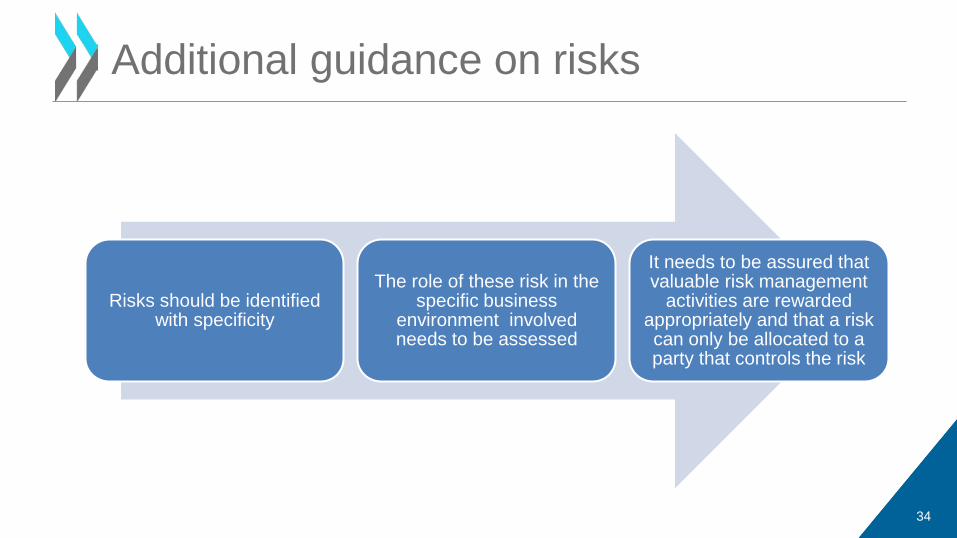

Risks should be identified with specificity

The role of these risk in the specific business

environment involved needs to be assessed

It needs to be assured that valuable risk management

activities are rewarded appropriately and that a risk can only be allocated to a party that controls the risk

Additional guidance on risks

34

Business reality is priced, not paper reality

Flexing the muscles of the arm’s length principle, making it work harder

Agreement on the directions taken, resulting in more

alignment in the approaches of countries

Illustrates that TP is not an exact science and is heavily reliant on facts. As a result

there is a high risk of unilateral adjustments

leading to double taxation. Effective dispute resolution

mechanisms are key.

35

What does the new guidance achieve?

Capability to make decisions to take on the risk and

Capability to make decisions on whether and how to manage the risk

including the actual performance of the decision-making functions and the functions related to assessing, monitoring and directing the outsourced measures

Where a decision is made to outsource risk mitigation, control of the risk would require capability to assess, monitor and direct the outsourced measures that affect risk outcomes

What is control over risk?

36

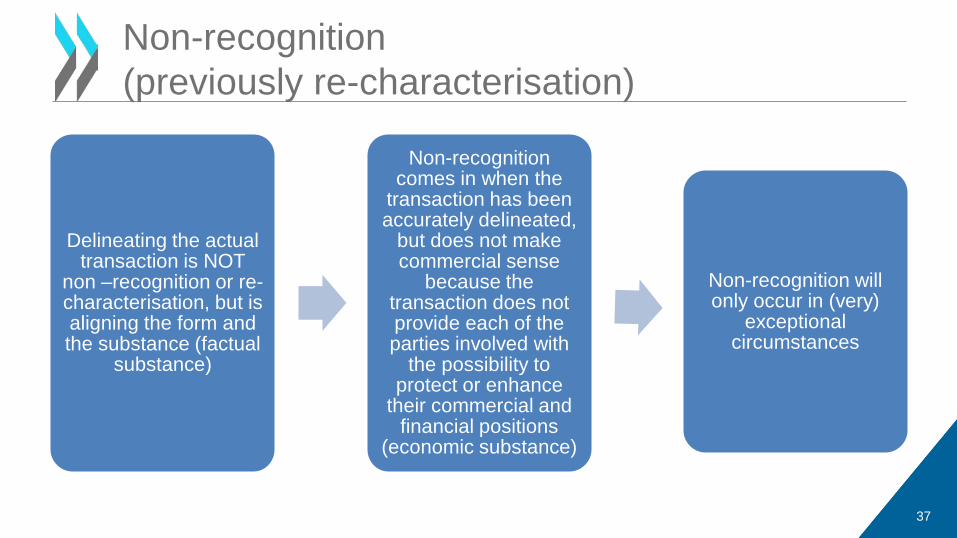

Delineating the actual transaction is NOT

non –recognition or re-characterisation, but is aligning the form and the substance (factual

substance)

Non-recognition comes in when the

transaction has been accurately delineated,

but does not make commercial sense

because the transaction does not provide each of the parties involved with

the possibility to protect or enhance

their commercial and financial positions

(economic substance)

Non-recognition will only occur in (very)

exceptional circumstances

Non-recognition (previously re-characterisation)

37

New guidance makes the arm’s length principle work harder, but may not prevent all BEPS risks.

Remaining risks mainly relate to information asymmetries and the allocation of capital to lowly-taxed minimal functional entities.

Part II of the DD outlines some potential special measures that could be considered as a basis to address these concerns.

Close interaction with other actions, including Action 3 on CFC rules and Action 4 on Interest deductibility.

Do BEPS risks remain?

38

Finalisation Actions 8/9/10 in September 2015 and Action 4 in December 2015

Public consultation meeting early July 2015

Discussion draft on CCA’s, intangibles, profit splits and financial transactions to be released between April-June

Public consultation meeting 19/20 March 2015

Deadline for comments was February 6th. 862 pages of comments received

Follow up steps

39

Late Oct 2014

Dec 2014

Mar 2015

Early Apr 2015

Early Jun 2015

Jul 2015

Sep 2015

Low value-adding services DD PC RD Finalisation: changes to TPG Ch VII

Risk, recharacterisation DD PC RD Finalisation: changes to Ch I, IX

Commodity transactions DD

PC RD Finalisation: changes to Ch II

Profit splits DD PC RD PC Finalisation: changes to Ch II

Cost contribution arrangements (CCAs)

DD PC Finalisation: changes to Ch VIII

Intangibles: RD 2014 report plus DD hard to value intangibles

RD DD PC Finalisation: changes to Ch VI

Financial transactions DD PC (Finalisation: December 2015)

Planned timetable on TP Actions

DD = discussion draft RD = revised drafts PC = public consultation 40

INTERNATIONAL VAT/GST GUIDELINES

GUIDELINES ON PLACE OF TAXATION FOR BUSINESS-TO-CONSUMER SUPPLIES OF SERVICES AND INTANGIBLES

International VAT/GST Guidelines B2C supplies of services and intangibles

Public consultation on 25 February 2015

• VAT payable in jurisdiction where customer has its usual residence

• Remote supplier to register and remit VAT in customer’s jurisdiction

• Simplified registration and compliance regime for remote suppliers – Obligations limited to what is required to collect/remit VAT

• International administrative cooperation in VAT to be strengthened, to support the effective collection of VAT from remote suppliers

Discussion draft released on 18 December 2014

42

MAKE DISPUTE RESOLUTION MECHANISMS MORE EFFECTIVE

Released on 18 December 2014

413 pages of public comments were received

Public consultation held on 23 January 2015

The discussion draft, comments received and webcast of the public consultation meeting are available on the OECD web site: ww.oecd.org/tax

Action 14 Discussion Draft

44

NEXT STEPS

• Action 11 (Late March 2015) • Action 12 (Late March 2015) • Action 3 (Early April 2015) • Actions 8-10 – Intangibles, Hard to Value

Intangibles, and Cost Contribution Arrangements (Early April 2015)

Upcoming Discussion Drafts

46

• Action 4 (17 February 2015) • VAT/GST Guidelines on B2C trade in services

and intangibles (25 February 2015) • Actions 8-10 (19-20 March 2015) • Action 11 (13 May 2015)

Upcoming Public Consultations

47

JOIN THE DISCUSSION

Ask questions and comment

Join the discussion

Directly: Enter your question in the space provided Via email: [email protected] Via Twitter: Follow us via @OECDlive using #BEPS

49

Further Information

Website: www.oecd.org/tax/beps.htm Contact: [email protected] Tax email alerts: www.oecd.org/oecddirect