Beggar-thy-Neighbor? The international effects of the ECB‘s ... · the ECB‘s unconventional...

32

Introduction Estimation Results Conclusion Beggar-thy-Neighbor? The international effects of the ECB‘s unconventional monetary policy measures Kristina Bluwstein 1 Fabio Canova 2 1 European University Institute 2 BI Norwegian Business School and CEPR ECB Workshop Non-standard monetary policy measures 19 April 2016 Bluwstein, Canova Beggar-thy-Neighbor? 1/32

Transcript of Beggar-thy-Neighbor? The international effects of the ECB‘s ... · the ECB‘s unconventional...

IntroductionEstimation

ResultsConclusion

Beggar-thy-Neighbor? The international effects ofthe ECB‘s unconventional monetary policy

measures

Kristina Bluwstein1 Fabio Canova2

1European University Institute

2BI Norwegian Business School and CEPR

ECB Workshop Non-standard monetary policy measures19 April 2016

Bluwstein, Canova Beggar-thy-Neighbor? 1/32

IntroductionEstimation

ResultsConclusion

"Quantitative easing policies (...) have triggered

(...) a monetary tsunami, have led to a currency

war and have introduced new and perverse forms of

protectionism in the world."

-Dilma Rousseff in 2012

I US tapering raised concern in Brazil, Turkey, India and SouthAfrica (Knyge, 2014)

I EA QE raises concern among non-Euro EU members due tostrong trade and financial ties

I Example: Switzerland abandoning cap in January 2015

Bluwstein, Canova Beggar-thy-Neighbor? 2/32

IntroductionEstimation

ResultsConclusion

Research Questions

I What are the effects of the ECB’s unconventional monetarypolicy (UMP) within the Euro Area?

I What are the spillover effects of the ECB’s unconventionalmonetary policy on other countries?

I Are they beggar-thy-neighbor policies?

I Are there differences among countries and if so, why?

Bluwstein, Canova Beggar-thy-Neighbor? 3/32

IntroductionEstimation

ResultsConclusion

Our Contribution

I Analyze the international transmission of the ECB’s UMP to 9European countries outside the Euro Area (EA)

I Use of Bayesian mixed-frequency SVAR to combine monthlymacro, daily financial and weekly policy data

I Evaluate trade and financial transmission channels of monetarypolicy

I Compare conventional and unconventional policy transmissionsince the onset of the financial crisis

Bluwstein, Canova Beggar-thy-Neighbor? 4/32

IntroductionEstimation

ResultsConclusion

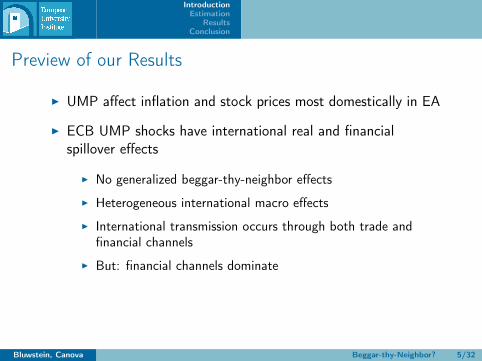

Preview of our Results

I UMP affect inflation and stock prices most domestically in EA

I ECB UMP shocks have international real and financialspillover effects

I No generalized beggar-thy-neighbor effects

I Heterogeneous international macro effects

I International transmission occurs through both trade andfinancial channels

I But: financial channels dominate

Bluwstein, Canova Beggar-thy-Neighbor? 5/32

IntroductionEstimation

ResultsConclusion

Countries in our Sample

Bluwstein, Canova Beggar-thy-Neighbor? 6/32

IntroductionEstimation

ResultsConclusion

Unconventional Policies in our SampleDate Tool in Bn of €

Dec. 2007-ongoing Reciprocal Currency Agreement 271.6

Mar. 2008-May 2010 6-month Long term refinancing operations 66

May–Dec. 2009 12-month Long term refinancing operations 614

Jun. 2009-Jun. 2010 Covered Bond Purchase Programme 45

May 2010-Aug. 2012 Securities Market Programme 195

Aug. 2011 12-month Long term refinancing operations 49.8

Oct. 2011 13-month Long term refinancing operations 57

Nov. 2011-Oct. 2012 Covered Bond Purchase Programme 2 15

Dec. 2011 36-month Long term refinancing operations 489

Feb. 2012 36-month Long term refinancing operations 530

Jul. 2012 Draghi‘s “Whatever it takes speech”

Aug. 2012-ongoing Outright Monetary Transaction

Jul. 2013 Forward GuidanceSource: ECB weekly Financial Statements; ECB Statistical Warehouse; Cecioni et al.

(2011).Bluwstein, Canova Beggar-thy-Neighbor? 7/32

IntroductionEstimation

ResultsConclusion

Transmission Channels in our SampleBa

lanc

e Sh

eet P

olic

y

Exchange Rate Channel

Credit Channel

Asset/Wealth Channel

Portfolio Rebalancing Channel

Liquidity

(Relative) Asset Prices

Risk

Out

put a

nd In

flatio

n

Trade & Import Prices

Investment & Consumption

Policy Transmission ChannelFinancial Spillovers

Macroeconomic Spillovers

Confidence Channel

Bluwstein, Canova Beggar-thy-Neighbor? 8/32

IntroductionEstimation

ResultsConclusion

Previous studies on domestic effects within the Euro Area

I Quarterly VARs with lending survey/ credit supplyI Output and inflation respond similar to conventional but

slower, less significant and stickier (Peersman, 2012)

I Positive output and inflation effects found by Darracq Parièsand De Santis (2013), Lenza et al. (2010) and Gambarcorta etal. (2012)

I (Quasi) Event studies/HF for financial variables andannouncement effects

I Reduction in market spreads after announcement (Angelini etal., 2011; Abbassi and Linzert, 2011; Beirne et al., 2011)

I Using intra-day data significant announcement effects on termpremia and government bonds (Ghysels et al. 2013 or Rogerset al., 2014)

Bluwstein, Canova Beggar-thy-Neighbor? 9/32

IntroductionEstimation

ResultsConclusion

Previous studies on international transmission of UMPT

I US QE: Dollar depreciation, rise in stock prices and decrease in CDSspreads (Neely, 2010; Chinn, 2013; Fratzscher et al., 2013 for QE2)

I Effect on emerging countries stronger (Chen et al., 2012)

I EA UMP: Decline in risk, positive equity spillovers, little effect onportfolio flows and yields, Euro depreciation (Fratzscher et al., 2014)

I Less output and bank lending effects in less capitalized countries(Boeckx et al., 2014)

I Problems:I High-frequency: macro - finance linkages not properly

accounted for because of time aggregation

I Low-frequency: policy endogeneity

Bluwstein, Canova Beggar-thy-Neighbor? 10/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

Our Model

Structural form of VARX:

A0yt = A(L)yt�1 + Bxt + ✏t , ✏t ⇠ N(0,⌃),

IThe endogenous variables are defined as yt = [zt , qt ]:

Izt are the variables with missing observation

Iqt are fully observed

IThe endogenous variables can be decomposed into yt = [yt,1, yt,2]:

IEA variables: y1t = [y⇤

t ,⇡⇤t ,UMPT

⇤t , sp

⇤t , l

⇤t , r

⇤t ]

0

IDomestic variables: y2t = [yt ,⇡t , et , spt , lt , r t ]0

IThe exogenous variables xt = [Newst , it , i

⇤t ,PCt ]

Bluwstein, Canova Beggar-thy-Neighbor? 11/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

The Estimation Approach

I Aggregate daily financial data, use weekly monetary policydata, and construct weekly macro data from monthlyobservations

I Bayesian Gibbs sampler approach: draw missing data frommultivariate normal distribution (Chiu et al., 2011, Qian,2013).

I Weekly frequency irregular

I Mid-point average data rather than end of the period sampling.Directly sample from constrained multivariate distributions

I Flat prior for all coefficientsBluwstein, Canova Beggar-thy-Neighbor? 12/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

Identification

I Block exogeneity of Euro area variables with respect to foreignvariables (see Cushman and Zha, 1997, Mackowiack, 2007)

I Baseline: Country blocks have recursive order

I Output and inflation predetermined within a week to UMPshocks

I Financial variables do not enter the UMP reaction function(more accurate for LTRO, less accurate for SMP)

I Ordering of financial variables arbitrary

I Perform robustness checks

I Contemporaneous restrictions very weak –> weekly

Bluwstein, Canova Beggar-thy-Neighbor? 13/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

The Data

I Sample: 18th December 2008-10th May 2014

I Avoid major structural breaks

I Avoid the high volatility period following the Lehman crisis

I Have a time period where UMP were frequently used

I Avoid negative interest rates (began June 2014)

I Countries:

I Mostly floating currency regimes

I 2 pegged (Denmark and Bulgaria)

I 1 hybrid (Switzerland, switched from floating to fixed regimein September 2011)

Bluwstein, Canova Beggar-thy-Neighbor? 14/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

I Variables:

I Monthly IP index and CPI index for output and inflation.

I Weekly UMP variable: sum of LTRO, SMP and Covered BondPurchase Programmes (CBP) (I and II).

I Daily financial variables: bilateral nominal exchange rate, theliquidity spread, stock market indices, and CDS spreads.

I Announcement dummy: sum of event dummies for LTROs,collateral changes, SMP, CBP I and II.

I PC indicator for global factors and US and UK monetarypolicy variables

Bluwstein, Canova Beggar-thy-Neighbor? 15/32

IntroductionEstimation

ResultsConclusion

Empirical ModelData

Research Questions

IWhat are the spillover effects of the ECB’s

unconventional monetary policy (UMP) within the Euro

Area?

I What are the spillover effects of the ECB’s unconventionalmonetary policy on other countries?

I Are they beggar-thy-neighbor policies?

I Are there differences among countries and if so, why?

Bluwstein, Canova Beggar-thy-Neighbor? 16/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Domestic Transmission of UMP shock

2 4 6 8 10 12 14 16

-0.2

0

0.2Unconventional Monetary Policy shock

Output

2 4 6 8 10 12 14 160

0.05

0.1

0.15

Inflation

2 4 6 8 10 12 14 160

5

10Monetary Policy

2 4 6 8 10 12 14 16

-0.5

0

0.5

Stock Prices

2 4 6 8 10 12 14 16

-0.01

0

0.01Liquidity

2 4 6 8 10 12 14 16-2-101

Risk (CDS)

2 4 6 8 10 12 14 16

0

0.1

0.2Conventional Monetary Policy shock

2 4 6 8 10 12 14 16-0.08

-0.04

0

0.04

2 4 6 8 10 12 14 16

-0.05

0

2 4 6 8 10 12 14 160

0.5

1

2 4 6 8 10 12 14 16

×10-3

-10

-5

0

5

2 4 6 8 10 12 14 16

-3-2-10

2 4 6 8 10 12 14 16

-2024

Announcement shock

2 4 6 8 10 12 14 16

-0.50

0.51

1.5

2 4 6 8 10 12 14 160

0.5

1

2 4 6 8 10 12 14 16

-0.50

0.51

2 4 6 8 10 12 14 16-0.02

0

0.02

0.04

2 4 6 8 10 12 14 16

-4

0

Bluwstein, Canova Beggar-thy-Neighbor? 17/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Summary of Results for Domestic Shock

I With unconventional monetary policy output responsesinsignificant

I Different to US and UK which had asset purchase programmesrather than interbank liquidity intervention

I For stronger output effects need bank lending channel to work(little evidence)

I Liquidity and risk spread significantly negative in the mediumrun only (weak credit and confidence channel)

Bluwstein, Canova Beggar-thy-Neighbor? 18/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Summary of results for conventional and news shock

I With conventional monetary policy disturbances outputresponses significant and persistent - peak effect after 8 -10weeks

I Risk perceptions persistently decrease; stock prices increase

I UMP announcement surprises have little effect on aggregatedmacro variables

I The responses of stock prices and risk spread similar to thoseof a conventional policy disturbances (Szczerbowicz, 2015)

I Possible underestimation because of averaging of daily data(see Ghysels et al., 2013; Rogers et al., 2014)

Bluwstein, Canova Beggar-thy-Neighbor? 19/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Research Questions

I What are the spillover effects of the ECB’s unconventionalmonetary policy (UMP) within the Euro Area?

IWhat are the spillover effects of the ECB’s

unconventional monetary policy on other countries?

IAre they beggar-thy-neighbor policies?

I Are there differences among countries and if so, why?

Bluwstein, Canova Beggar-thy-Neighbor? 20/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

International Transmission of UMP shock

I Responses in deviations from Euro area responses (theexchange rate is in level)

I Country groups:

Advanced: Sweden, Norway, Denmark, and Switzerland

CEE: Central Eastern European countries - Poland,and the Czech Republic

SEE: Southern Eastern European countries - Hungary,Romania, and Bulgaria

Bluwstein, Canova Beggar-thy-Neighbor? 21/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

2 4 6 8 10 12 14 16

-0.2

0

0.2

Advanced

Output

2 4 6 8 10 12 14 16

0

0.2

0.4

Inflation

2 4 6 8 10 12 14 16

-0.1-0.05

00.05

Exchange Rate

2 4 6 8 10 12 14 16

-0.2-0.10

0.1Stock Prices

2 4 6 8 10 12 14 16

-0.01

0

0.01

Liquidity

2 4 6 8 10 12 14 16

-0.50

0.51

1.5

Risk (CDS)

SE NO SW DK

2 4 6 8 10 12 14 16

-0.2

0

0.2

CEE

2 4 6 8 10 12 14 16-0.2

-0.1

0

0.1

2 4 6 8 10 12 14 16

-0.15

-0.1

-0.05

0

2 4 6 8 10 12 14 16

-0.2

-0.1

0

0.1

2 4 6 8 10 12 14 16

-0.03-0.02-0.01

00.01

2 4 6 8 10 12 14 16

-2

-1

0

CZ PO

2 4 6 8 10 12 14 16

-0.3

-0.2

-0.1

0SEE

2 4 6 8 10 12 14 16

-0.1

0

0.1

2 4 6 8 10 12 14 16-0.2

-0.1

0

2 4 6 8 10 12 14 16-0.2

0

0.2

2 4 6 8 10 12 14 16-0.06

-0.04

-0.02

0

2 4 6 8 10 12 14 16

-1-0.50

0.5

HU RO BG

Bluwstein, Canova Beggar-thy-Neighbor? 22/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Summary of International Transmission of UMP shocks

I Macro responses heterogeneous

I No generalized beggar-thy-neighbor effect!

Bluwstein, Canova Beggar-thy-Neighbor? 23/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

I The exchange rate, wealth, risk and portfolio re-balancingchannels spill Euro area UMP shocks to foreign countries

I Credit channel is weak

I The exchange rate channel is not responsible for heterogeneityin output responses

I Financial channels crucial for international transmission ofUMP disturbances (less so for conventional monetary shocks)

Bluwstein, Canova Beggar-thy-Neighbor? 24/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Research Questions

I What are the spillover effects of the ECB’s unconventionalmonetary policy (UMP) within the Euro Area?

I What are the spillover effects of the ECB’s unconventionalmonetary policy on other countries?

I Are they beggar-thy-neighbor policies?

IAre there differences among countries and if so, why?

Bluwstein, Canova Beggar-thy-Neighbor? 25/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Why are foreign macro responses heterogeneous?

I Different exchange rate regimes?

I Other exogenous shocks, e.g. oil shocks that occur at thesame time and proxy for UMP shocks?

I UMP shocks hit countries at different stages of their businessand financial cycle?

I Some small countries themselves conducted UMP, while othersdid not?

I Different domestic financial market structure?

Bluwstein, Canova Beggar-thy-Neighbor? 26/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Why are foreign macro responses heterogeneous?

I IMF (2013) states 70-90% of assets in CEE and SEE countriesheld by foreign banks (mostly from the Euro area)

I Cheap ECB liquidity may be invested into foreign financialmarkets rather than lent to foreign households and firms

I Increase in foreign asset prices and risk reductions

I No positive real spillovers - foreign loans unaffected by theadditional liquidity banks obtain

I In countries with a large share of foreign banks, global liquidityincreases should have the smallest real pass-through

Bluwstein, Canova Beggar-thy-Neighbor? 27/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

0 2 4 6 8 10 12 14 16-1

-0.5

0

0.5

1Industrial Production

0 2 4 6 8 10 12 14 16-0.4

-0.2

0

0.2

0.4Inflation

0 2 4 6 8 10 12 14 16-0.15

-0.1

-0.05

0

0.05

0.1Real Exchange Rate

0 2 4 6 8 10 12 14 16-0.2

-0.1

0

0.1

0.2Stock Prices

0 2 4 6 8 10 12 14 16-0.04

-0.02

0

0.02

0.04Liquidity Spread

0 2 4 6 8 10 12 14 16-0.6

-0.4

-0.2

0

0.2

0.4

0.6Risk (CDS)

low Foreign Bank Share high Foreign Bank Share

Bluwstein, Canova Beggar-thy-Neighbor? 28/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Heterogeneity due to foreign bank share?

I Stark difference in the response of output, inflation and risk

I Countries with high share of foreign bank ownership experiencedecrease in output, an increase in inflation and reduction inrisk relative to the Euro area

I Similar conclusions if we group countries according to the levelof financial development or the credit-to-GDP ratio

I Result in line with macro studies Aizenman (2015), Dedola(2015), and micro studies Ongena et al. (2015)

I Exchange rate and credit channel shows no significantdifference between groups

Bluwstein, Canova Beggar-thy-Neighbor? 29/32

IntroductionEstimation

ResultsConclusion

UMP Shock: DomesticUMP Shock: InternationalHeterogeneityRobustness

Robustness

I VIX instead of CDS for countries available

I Excess liquidity as UMP measure

I Splitting of liquidity and sovereign bond policies: sovereigndebt policies produce positive real activity and negativeinflation response

I Identification Scheme

I R1-R3: Reordering of financial block

I R4: Sign and zero restrictions (liquidity spread non-positive forat least one period after UMP shock)

I R5: Heteroskedasticity switches before/ after Draghi"Whatever-it- takes" speech

I ! qualitative results fairly robustBluwstein, Canova Beggar-thy-Neighbor? 30/32

IntroductionEstimation

ResultsConclusion

Conclusion

I ECB UMP shocks have important domestic effects, especiallyon inflation and stock prices

I ECB UMP shocks have international real and financialspillover effects

I No generalized beggar-thy-neighbor effects

I Heterogeneous international macro effectsI Heterogeneity possible due to share of foreign banks in

domestic financial markets

I International transmission occurs through both trade andfinancial channels

I But: financial channels dominate

Bluwstein, Canova Beggar-thy-Neighbor? 31/32

IntroductionEstimation

ResultsConclusion

Thank you for your attention!

Bluwstein, Canova Beggar-thy-Neighbor? 32/32