BALL-CHATHAM COMMUNITY UNIT SCHOOL … District/IL Ball-Chatham Cusd 5 2017.pdf · INDEPENDENT...

89

Prepared by: Mack & Associates, P.C. Certified Public Accountants 116 E. Washington Street, Suite One Morris, IL 60450 Telephone: (815) 942-3306 CERTIFIED PUBLIC ACCOUNTANTS BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5 CHATHAM, ILLINOIS ANNUAL FINANCIAL REPORT JUNE 30, 2017

Transcript of BALL-CHATHAM COMMUNITY UNIT SCHOOL … District/IL Ball-Chatham Cusd 5 2017.pdf · INDEPENDENT...

Prepared by:

Mack & Associates, P.C. Certified Public Accountants

116 E. Washington Street, Suite One

Morris, IL 60450 Telephone: (815) 942-3306

CERTIFIED PUBLIC ACCOUNTANTS

BALL-CHATHAM COMMUNITY UNIT SCHOOL

DISTRICT #5

CHATHAM, ILLINOIS

ANNUAL FINANCIAL REPORT

JUNE 30, 2017

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5 Table of Contents

PAGE INDEPENDENT AUDITORS' REPORT ................................................................................................ 1-2 FINANCIAL STATEMENTS Statement of Assets, Liabilities, and Fund Balances Arising from Cash Transactions - All Funds and Account Groups (Statement A) ...................................... 3-4 Statement of Revenues Received, Expenditures Disbursed, Other Financing Sources (Uses) and Changes in Fund Balances – All Funds (Statement B) ......................... 5-6 Statement of Revenues Received – All Funds (Statement C) ..................................................... 7-10 Statement of Expenditures Disbursed – Budget and Actual Educational Fund (Statement D) .......................................................................................... 11-18 Operations and Maintenance Fund (Statement E) ..................................................................19 Debt Service Fund (Statement F) ............................................................................................20 Transportation Fund (Statement G) ........................................................................................21 Municipal Retirement / Social Security Fund (Statement H) ....................................................22 Capital Projects Fund (Statement I) ........................................................................................23 Fire Prevention and Safety Fund (Statement J) ......................................................................24 NOTES TO FINANCIAL STATEMENTS ............................................................................................. 25-59 OTHER INFORMATION Illinois Municipal Retirement Fund: Schedule of Changes in Net Pension Liability and Related Ratios (Schedule A-1) ................60 Schedule of Contributions (Schedule A-2) ..............................................................................61 Teachers’ Retirement System of the State of Illinois: Schedule of District’s Share of the Net Pension Liability (Schedule A-3) ................................62 Schedule of Contributions (Schedule A-4) ..............................................................................62 NOTES TO OTHER INFORMATION .....................................................................................................63 SUPPLEMENTARY INFORMATION Trust & Agency Funds: Statement of Changes in Assets and Liabilities (Schedule B) .............................................. 64-67 Assessed Valuations, Tax Rates, Tax Extensions and Tax Collections (Schedule C) .........................................................................68

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5 Table of Contents

PAGE OTHER REPORTS Independent Auditors’ Report on Internal Control Over Financial Reporting and On Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards ........................................................... 69-70 SINGLE AUDIT SECTION:

Independent Auditors’ Report on Compliance for Each Major Program and on Internal Control Over Compliance Required by the Uniform Guidance ................................................................... 71-72 Schedule of Expenditures of Federal Awards ......................................................................... 73-74 Notes to the Schedule of Expenditures of Federal Awards ........................................................75 Schedule of Findings and Questioned Costs .............................................................................76 Summary Schedule of Prior Year Audit Findings .................................................................... 77-78

CERTIFIED PUBLIC ACCOUNTANTS

116 E. Washington Street Suite One Morris, Illinois 60450 Phone: (815) 942-3306 Fax: (815) 942-9430 www.mackcpas.com

TAWNYA R. MACK, CPALAURI POPE, CPA

ERICA BLUMBERG, CPATREVOR DEBELAK, CPA

MATT MELVINCHRIS CHRISTENSENSTEPHANIE HEISNER

1

Independent Auditors’ Report

To the Board of Education Ball-Chatham Community Unit School School District #5 Chatham, Illinois

We have audited the accompanying financial statements of Ball-Chatham Community Unit School District #5, as of and for the year ended June 30, 2017, and the related notes to the financial statements, which collectively comprise the District’s financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with the financial reporting provisions of the Illinois State Board of Education. Management is also responsible for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to error or fraud.

Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Basis for Adverse Opinion on U.S. Generally Accepted Accounting Principles As described in Note 1, the financial statements are prepared by Ball-Chatham Community Unit School District #5 on the basis of the financial reporting provisions of the Illinois State Board of Education, which is a basis of accounting other than accounting principles generally accepted in the United States of America, to comply with the requirements of the Illinois State Board of Education. The effects on the financial statements of the variances between the regulatory basis of accounting described in Note 1 and accounting principles generally accepted in the United States of America, although not reasonably determinable, are presumed to be material.

2

Adverse Opinion on U.S. Generally Accepted Accounting Principles

In our opinion, because of the significance of the matter discussed in the “Basis for Adverse Opinion on U.S. Generally Accepted Accounting Principles” paragraph, the financial statements referred to in the first paragraph do not present fairly, in accordance with accounting principles generally accepted in the United States of America, the financial position of Ball-Chatham Community Unit School District #5, as of June 30, 2017, the changes in its financial position for the year then ended.

Unmodified Opinion on Regulatory Basis of Accounting In our opinion, the financial statements referred to in the first paragraph present fairly, in all material respects, the assets, liabilities, and fund balances arising from cash transactions of each fund of Ball-Chatham Community Unit School District #5 as of June 30, 2017, and their respective cash receipts and disbursements, and budgetary results for the year then ended, on the basis of the financial reporting provisions of the Illinois State Board of Education.

Basis of Accounting We draw attention to Note 1 of the financial statements, which describes the basis of accounting. The financial statements are prepared on the modified cash basis of accounting, which is a basis of accounting other than accounting principles generally accepted in the United States of America. Our opinion is not modified with respect to that matter.

Other Matters Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise Ball-Chatham Community Unit School District #5’s financial statements. The other information, including notes to other information, on pages 60-63, and the supplementary information on pages 64-68 are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The schedules identified above have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Comparative Information

Other auditors previously audited, in accordance with auditing standards generally accepted in the United States of America, the financial statements of Ball-Chatham Community Unit School District #5 for the year ended June 30, 2016, which are presented in summary for comparison purposes with the accompanying financial statements. In their report dated October 24, 2016, they expressed a qualified opinion on the financial statements due to omitted disclosures required by GASB Statement No. 45.

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated September 26, 2017, on our consideration of Ball-Chatham Community Unit School District #5’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Ball-Chatham Community Unit School District #5’s internal control over financial reporting and compliance.

Mack & Associates, P.C. Certified Public Accountants Morris, Illinois September 26, 2017

Mack & Associates, P.C.

FINANCIAL STATEMENTS

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Statement of Assets, Liabilities, and Fund Balances Arising from Cash TransactionsAll Funds and Account GroupsAs of June 30, 2017

MunicipalOperations & Retirement/

Educational Maintenance Debt Service Transportation SocialFund Fund Fund Fund Security Fund

Assets

Cash 7,484,584$ 2,467,743 2,693,266 1,569,791 860,950 Other Current Assets - 1,508 - - -

Total Current Assets 7,484,584 2,469,251 2,693,266 1,569,791 860,950

Capital Assets:Land - - - - - Building - - - - - Other Improvements - - - - - Capitalized Equipment - - - - - Construction in Progress - - - - -

Amount Available in DebtService Fund - - - - -

Amount to be provided forPayment of Bonds - - - - -

Total Assets 7,484,584$ 2,469,251 2,693,266 1,569,791 860,950

Liabilities and Fund Balance

Liabilities:Current Liabilities:

Payroll Deductions & Withholdings 16,428$ - - 128 3,130 Due to Student Organizations - - - - -

Total Current Liabilities: 16,428 - - 128 3,130

Long-Term Liabilities:Long-Term Debt Payable - - - - -

Total Long-Term Liabilities: - - - - -

Total Liabilities 16,428 - - 128 3,130

Fund Equity:Unreserved Fund Balance (deficit) 5,689,890 2,469,251 2,693,266 1,569,663 411,572 Reserved Fund Balance 1,778,266 - - - 446,248 Investment in General Fixed Assets - - - - -

Total Fund Balance 7,468,156 2,469,251 2,693,266 1,569,663 857,820

Total Liabilities and Fund Balance 7,484,584$ 2,469,251 2,693,266 1,569,791 860,950

The Notes to Financial Statements are an integral part of this statement.3

Statement A

TotalFire Account Groups (Memorandum

Capital Working Tort Prevention General General Only)Projects Cash Immunity and Safety Agency Fixed Long-Term Year Ended

Fund Fund Fund Fund Fund Assets Debt June 30, 2017

4,617,586 2,141,886 - 973,337 577,631 - - 23,386,774 - - - - - - 1,508

4,617,586 2,141,886 - 973,337 577,631 - - 23,388,282

- - - - - 4,426,429 - 4,426,429 - - - - - 111,041,262 - 111,041,262 - - - - - 8,341,565 - 8,341,565 - - - - - 14,761,906 - 14,761,906 - - - - - 73,683 - 73,683

- - - - - - 2,693,266 2,693,266

- - - - - - 49,391,734 49,391,734

4,617,586 2,141,886 - 973,337 577,631 138,644,845 52,085,000 214,118,127

- - - - - - - 19,686 - - - - 577,631 - - 577,631

- - - - 577,631 - - 597,317

- - - - - - 52,085,000 52,085,000

- - - - - - 52,085,000 52,085,000

- - - - 577,631 - 52,085,000 52,682,317

4,617,586 2,141,886 - 766,337 - - - 20,359,451 - - - 207,000 - - - 2,431,514 - - - - - 138,644,845 - 138,644,845

4,617,586 2,141,886 - 973,337 - 138,644,845 - 161,435,810

4,617,586 2,141,886 - 973,337 577,631 138,644,845 52,085,000 214,118,127

The Notes to Financial Statements are an integral part of this statement.4

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Statement of Revenues Received, Expenditures Disbursed, Other Financing Sources (Uses),and Changes in Fund Balances - All FundsFor the Year Ended June 30, 2017

OperationsEducational & Maintenance Debt Service Transportation

Fund Fund Fund Fund

Receipts:Local Sources 23,546,309$ 3,985,703 4,952,006 1,520,149 State Sources 7,775,075 - - 602,668 Federal Sources 2,241,603 - - 1,849

Total Direct Receipts 33,562,987 3,985,703 4,952,006 2,124,666

Receipts for "On Behalf" Payments 7,366,806 - - -

Total Receipts 40,929,793 3,985,703 4,952,006 2,124,666

Disbursements:Instruction 21,468,999 - - - Support Services 9,847,468 3,502,462 - 1,846,650 Community Services 12,573 - - - Payments to Other Districts & Governmental Units 397,677 - - - Debt Service 2,586 - 4,976,708 -

Total Direct Disbursements 31,729,303 3,502,462 4,976,708 1,846,650

Disbursements for "On Behalf" Payments 7,366,806 - - -

Total Expenditures Disbursed 39,096,109 3,502,462 4,976,708 1,846,650

Excess of Direct Receipts Over (Under) DirectDisbursements 1,833,684 483,241 (24,702) 278,016

Fund Balance, Beginning of Year 5,634,472 1,986,010 2,717,968 1,291,647

Fund Balance, End of Year 7,468,156$ 2,469,251 2,693,266 1,569,663

The Notes to Financial Statements are an integral part of this statement.5

Statement B

Municipal Fire TotalRetirement/ Capital Working Tort Prevention (Memorandum Only)

Social Projects Cash Immunity and Safety Year EndedSecurity Fund Fund Fund Fund Fund June 30, 2017

1,569,237 23,321 131,188 - 106,897 35,834,810 - - - - - 8,377,743 - - - - - 2,243,452

1,569,237 23,321 131,188 - 106,897 46,456,005

- - - - - 7,366,806

1,569,237 23,321 131,188 - 106,897 53,822,811

421,591 - - - - 21,890,590 1,032,999 523,279 - - 109,422 16,862,280

- - - - - 12,573 - - - - - 397,677 - - - - - 4,979,294

1,454,590 523,279 - - 109,422 44,142,414

- - - - - 7,366,806

1,454,590 523,279 - - 109,422 51,509,220

114,647 (499,958) 131,188 - (2,525) 2,313,591

743,173 5,117,544 2,010,698 - 975,862 20,477,374

857,820 4,617,586 2,141,886 - 973,337 22,790,965

The Notes to Financial Statements are an integral part of this statement.6

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Statement of Revenues ReceivedAll FundsFor the Year Ended June 30, 2017

OperationsEducational & Maintenance Debt Service Transportation

Fund Fund Fund FundReceipts:

Local Sources:Property Taxes:

Designated Purposes Taxes 20,168,128$ 3,793,979 4,951,855 1,252,576 Leasing Purposes Taxes 143,259 - - - Special Education Taxes 143,259 - - - FICA and Medicare Taxes - - - -

Corporate Personal Property Replacement Taxes - - - 216,751 Summer School Tuition from Pupils or Parents 6,520 - - - Interest on Investments 47,231 114 151 40 Food Services

Sales to Pupils - Lunch 505,947 - - - Sales to Pupils - Breakfast 32,443 - - - Sales to Pupils - A la Carte 1,046,691 - - - Sales to Adults 37,061 - - -

District Activity IncomeAdmissions - Athletic 73,982 - - - Fees 138,443 - - - Other 94,895 - - -

Textbook IncomeRentals 582,814 - - - Other 8,415 - - -

Other Local IncomeRentals - 94,323 - - Contributions and Donations from Private Sources 13,288 4,815 - - Services Provided to Other Districts - - - 14,833 Refund of Prior Year Expenditures 254,923 90,720 - 300 Payments of Surplus Moneys from TIF Districts 165,910 - - - Drivers' Education Fees 54,055 - - - Other Local Income 29,045 1,752 - 35,649

Total Receipts from Local Sources 23,546,309 3,985,703 4,952,006 1,520,149

State Sources:General State Aid 6,140,076 - - 100,000 Special Education

Private Facility Tuition 351,826 - - - Funding for Children Requiring Sp Ed Services 425,339 - - - Personnel 451,752 - - - Orphanage - Individual 202,862 - - -

State Free Lunch & Breakfast 1,835 - - - Driver Education 49,189 - - - Transportation Aid

Regular - - - 270,175 Special Education - - - 208,493

Early Childhood - Block Grant 152,196 - - 24,000

Total Receipts from State Sources 7,775,075 - - 602,668

The Notes to Financial Statements are an integral part of this statement.7

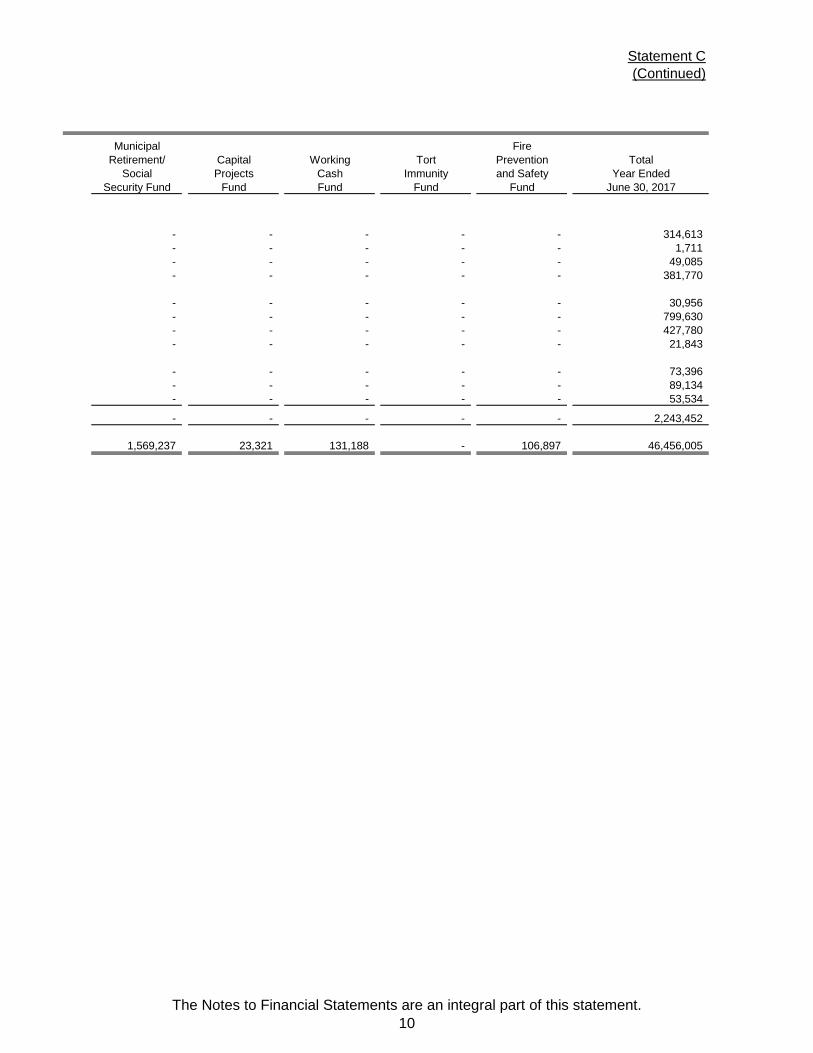

Statement C

Municipal FireRetirement/ Capital Working Tort Prevention Total

Social Projects Cash Immunity and Safety Year EndedSecurity Fund Fund Fund Fund Fund June 30, 2017

706,756 - 131,184 - 106,892 31,111,370 - - - - - 143,259 - - - - - 143,259

820,470 - - - - 820,470 41,965 - - - - 258,716

- - - - - 6,520 46 23,321 4 - 5 70,912

- - - - - 505,947 - - - - - 32,443 - - - - - 1,046,691 - - - - - 37,061

- - - - - 73,982 - - - - - 138,443 - - - - - 94,895

- - - - - 582,814 - - - - - 8,415

- - - - - 94,323 - - - - - 18,103 - - - - - 14,833 - - - - - 345,943 - - - - - 165,910 - - - - - 54,055 - - - - - 66,446

1,569,237 23,321 131,188 - 106,897 35,834,810

- - - - - 6,240,076

- - - - - 351,826 - - - - - 425,339 - - - - - 451,752 - - - - - 202,862 - - - - - 1,835 - - - - - 49,189

- - - - - 270,175 - - - - - 208,493 - - - - - 176,196

- - - - - 8,377,743

The Notes to Financial Statements are an integral part of this statement.8

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Statement of Revenues Received - All FundsFor the Year Ended June 30, 2017

OperationsEducational & Maintenance Debt Service Transportation

Fund Fund Fund FundReceipts (Continued):

Federal Sources:National School Lunch Program 314,613 - - - Special Milk Program 1,711 - - - School Breakfast Program 49,085 - - - Title I - Low Income 381,770 - - - Special Education:

Preschool - Flow-Through 30,956 - - - IDEA - Flow-Through 797,781 - - 1,849 IDEA Room & Board 427,780 - - -

Title II - Teacher Quality 21,843 - - - Medicaid Matching Funds:

Administrative Outreach 73,396 - - - Fee for Service 89,134 - - -

Other Federal Revenues - STEP Grant 53,534 - - -

Total Receipts from Federal Sources 2,241,603 - - 1,849

Total Direct Receipts 33,562,987$ 3,985,703 4,952,006 2,124,666

The Notes to Financial Statements are an integral part of this statement.9

Statement C(Continued)

Municipal FireRetirement/ Capital Working Tort Prevention Total

Social Projects Cash Immunity and Safety Year EndedSecurity Fund Fund Fund Fund Fund June 30, 2017

- - - - - 314,613 - - - - - 1,711 - - - - - 49,085 - - - - - 381,770

- - - - - 30,956 - - - - - 799,630 - - - - - 427,780 - - - - - 21,843

- - - - - 73,396 - - - - - 89,134 - - - - - 53,534

- - - - - 2,243,452

1,569,237 23,321 131,188 - 106,897 46,456,005

The Notes to Financial Statements are an integral part of this statement.10

Statement DBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Instruction:

Regular Programs:Salaries 11,602,474$ 11,419,436 11,371,501 47,935 10,942,217 Employee Benefits 2,544,826 2,562,338 2,706,433 (144,095) 2,727,420 Purchased Services 459,343 475,323 456,342 18,981 460,072 Supplies and Materials 587,308 606,926 535,436 71,490 268,002 Capital Outlay - - - - - Other Objects 8,460 8,460 3,718 4,742 5,084 Non-Capitalized Equipment - - 550 (550) 1,600

Total Regular Programs 15,202,411 15,072,483 15,073,980 (1,497) 14,404,395 .

Tuition Payments to Charter Schools:Purchased Services 5,390 5,390 - 5,390 -

Total Tuition Payments toCharter Schools 5,390 5,390 - 5,390 -

Pre-K Programs:Salaries 151,703 198,556 194,892 3,664 148,056 Employee Benefits 52,191 72,034 70,740 1,294 51,629 Purchased Services - 2,618 2,617 1 - Supplies and Materials 10,309 21,817 21,347 470 5,972

Total Pre-K Programs 214,203 295,025 289,596 5,429 205,657

Special Education Programs:Salaries 2,486,548 2,476,548 2,464,335 12,213 2,437,929 Employee Benefits 556,361 705,804 678,090 27,714 696,830 Purchased Services 27,930 31,230 25,144 6,086 23,144 Supplies and Materials 20,080 30,420 15,638 14,782 27,721 Capital Outlay - - - - 752

Total Special Education Programs 3,090,919 3,244,002 3,183,207 60,795 3,186,376

Special Education Programs Pre-K:Salaries 61,214 76,214 50,254 25,960 64,787 Employee Benefits 15,997 16,002 6,869 9,133 15,304 Supplies and Materials 1,234 1,734 1,097 637 7,517

Total Special EducationPrograms Pre-K 78,445 93,950 58,220 35,730 87,608

Adult/Continuing Education Programs:Salaries 37,815 37,815 37,893 (78) 36,903 Employee Benefits 7,800 7,676 7,389 287 7,381 Purchased Services - - 336 (336) -

Total Adult / ContinuingEducation Programs 45,615 45,491 45,618 (127) 44,284

The Notes to Financial Statements are an integral part of this statement.11

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Instruction (continued):

CTE Programs:Salaries 360,754$ 364,956 363,641 1,315 350,246 Employee Benefits 79,982 89,313 77,377 11,936 76,977 Purchased Services 4,100 4,100 2,006 2,094 1,972 Supplies and Materials 22,690 22,690 17,495 5,195 17,428

Total CTE Programs 467,526 481,059 460,519 20,540 446,623

Interscholastic Programs:Salaries 593,345 563,345 532,498 30,847 487,958 Employee Benefits 44,968 82,663 57,203 25,460 5,614 Purchased Services 95,960 95,110 76,050 19,060 83,966 Supplies and Materials 66,000 66,000 55,088 10,912 61,062 Capital Outlay 12,000 12,000 - 12,000 - Other Objects 23,270 23,270 24,693 (1,423) 26,707 Non-Capitalized Equipment 12,000 12,000 10,964 1,036 -

Total Interscholastic Programs 847,543 854,388 756,496 97,892 665,307

Summer School Programs:Salaries 23,371 35,853 37,363 (1,510) 22,818 Employee Benefits 305 305 622 (317) 315

Total Summer School Programs 23,676 36,158 37,985 (1,827) 23,133

Driver's Education Programs:Salaries 158,680 148,680 151,631 (2,951) 154,058 Employee Benefits 40,482 39,909 38,602 1,307 38,752 Purchased Services 2,000 2,000 3,207 (1,207) 1,455 Supplies and Materials 8,600 8,600 50 8,550 181 Other Objects 30 30 - 30 30

Total Driver's Education Programs 209,792 199,219 193,490 5,729 194,476

Special Education ProgramsK-12 Private Tuition:

Other Objects 1,196,750 1,196,750 1,369,888 (173,138) 1,335,243

Total Special Education ProgramsK-12 Private Tuition 1,196,750 1,196,750 1,369,888 (173,138) 1,335,243

Total Instruction 21,382,270 21,523,915 21,468,999 54,916 20,593,102

The Notes to Financial Statements are an integral part of this statement.12

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

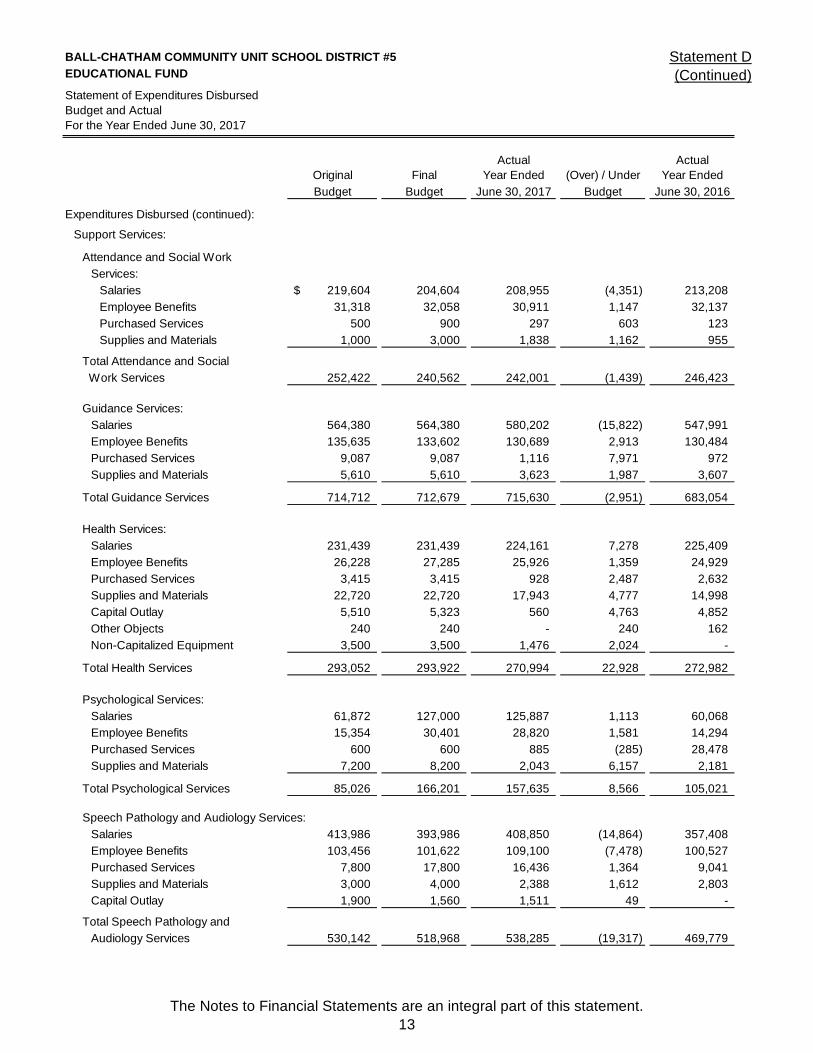

Support Services:

Attendance and Social Work Services:

Salaries 219,604$ 204,604 208,955 (4,351) 213,208 Employee Benefits 31,318 32,058 30,911 1,147 32,137 Purchased Services 500 900 297 603 123 Supplies and Materials 1,000 3,000 1,838 1,162 955

Total Attendance and Social Work Services 252,422 240,562 242,001 (1,439) 246,423

Guidance Services:Salaries 564,380 564,380 580,202 (15,822) 547,991 Employee Benefits 135,635 133,602 130,689 2,913 130,484 Purchased Services 9,087 9,087 1,116 7,971 972 Supplies and Materials 5,610 5,610 3,623 1,987 3,607

Total Guidance Services 714,712 712,679 715,630 (2,951) 683,054

Health Services:Salaries 231,439 231,439 224,161 7,278 225,409 Employee Benefits 26,228 27,285 25,926 1,359 24,929 Purchased Services 3,415 3,415 928 2,487 2,632 Supplies and Materials 22,720 22,720 17,943 4,777 14,998 Capital Outlay 5,510 5,323 560 4,763 4,852 Other Objects 240 240 - 240 162 Non-Capitalized Equipment 3,500 3,500 1,476 2,024 -

Total Health Services 293,052 293,922 270,994 22,928 272,982

Psychological Services:Salaries 61,872 127,000 125,887 1,113 60,068 Employee Benefits 15,354 30,401 28,820 1,581 14,294 Purchased Services 600 600 885 (285) 28,478 Supplies and Materials 7,200 8,200 2,043 6,157 2,181

Total Psychological Services 85,026 166,201 157,635 8,566 105,021

Speech Pathology and Audiology Services:Salaries 413,986 393,986 408,850 (14,864) 357,408 Employee Benefits 103,456 101,622 109,100 (7,478) 100,527 Purchased Services 7,800 17,800 16,436 1,364 9,041 Supplies and Materials 3,000 4,000 2,388 1,612 2,803 Capital Outlay 1,900 1,560 1,511 49 -

Total Speech Pathology andAudiology Services 530,142 518,968 538,285 (19,317) 469,779

The Notes to Financial Statements are an integral part of this statement.13

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Support Services (continued):

Other Support Services - Pupils:Salaries 342,109$ 360,109 365,840 (5,731) 343,054 Employee Benefits 24,043 39,054 37,999 1,055 45,631 Purchased Services 2,450 2,450 1,759 691 1,863 Supplies and Materials 2,430 2,430 - 2,430 2,127

Total Other Support Services - Pupils 371,032 404,043 405,598 (1,555) 392,675

Improvement of Instruction Services:Salaries 175,071 155,071 153,942 1,129 174,252 Employee Benefits 37,634 44,205 31,949 12,256 38,361 Purchased Services 93,632 164,744 70,130 94,614 65,035 Supplies and Materials 3,500 6,101 2,520 3,581 7,931 Other Objects 3,654 4,249 289 3,960 731

Total Improvement of Instruction Services 313,491 374,370 258,830 115,540 286,310

Educational Media Services:Salaries 233,929 177,929 170,552 7,377 227,114 Employee Benefits 62,277 64,442 43,921 20,521 59,202 Purchased Services 20,550 20,050 5,242 14,808 17,009 Supplies and Materials 26,225 26,225 36,203 (9,978) 23,985

Total Educational Media Services 342,981 288,646 255,918 32,728 327,310

Assessment and Testing:Purchased Services 5,000 5,000 425 4,575 630 Supplies and Materials 1,800 1,800 1,593 207 1,590

Total Assessment and Testing 6,800 6,800 2,018 4,782 2,220

Board of Education Services:Salaries 87,374 92,378 58,923 33,455 4,622 Employee Benefits 4,300 4,300 20,873 (16,573) 4,403 Purchased Services 818,600 818,600 743,561 75,039 778,033 Supplies and Materials 15,000 15,000 13,155 1,845 16,354 Other Objects 14,000 14,000 12,307 1,693 12,592

Total Board of Education Services 939,274 944,278 848,819 95,459 816,004

The Notes to Financial Statements are an integral part of this statement.14

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Support Services (continued):

Executive Administration Services:Salaries 292,780$ 292,780 303,660 (10,880) 251,408 Employee Benefits 60,398 65,161 74,115 (8,954) 33,521 Purchased Services 9,750 9,750 9,547 203 29,487 Supplies and Materials 5,350 5,350 360 4,990 6,638 Other Objects 2,800 2,800 3,815 (1,015) 2,776

Total Executive AdministrationServices 371,078 375,841 391,497 (15,656) 323,830

Special Area Administration Services:Salaries 317,100 237,100 241,908 (4,808) 356,998 Employee Benefits 38,130 58,234 51,412 6,822 38,370 Purchased Services - 2,100 6,570 (4,470) 6,772 Supplies and Materials - - - - 658 Other Objects - - 520 (520) 670

Total Special Area AdministrationServices 355,230 297,434 300,410 (2,976) 403,468

Office of the Principal Services:Salaries 1,705,791 1,449,433 1,457,179 (7,746) 1,691,036 Employee Benefits 208,880 331,775 304,736 27,039 198,667 Purchased Services 28,300 28,300 10,750 17,550 24,024 Supplies 62,819 62,819 35,452 27,367 45,692 Capital Outlay 600 600 - 600 - Other Objects 10,125 10,125 8,828 1,297 7,968 Non-Capitalized Equipment - - - - 2,395

Total Office of the PrincipalServices 2,016,515 1,883,052 1,816,945 66,107 1,969,782

School Administration Services:Salaries 119,400 119,400 122,424 (3,024) 96,685 Employee Benefits 5,470 13,200 13,323 (123) 5,505 Purchased Services 2,350 8,350 8,049 301 - Supplies and Materials 500 500 1,995 (1,495) 27 Other Objects 275 275 199 76 -

Total School AdministrationServices 127,995 141,725 145,990 (4,265) 102,217

The Notes to Financial Statements are an integral part of this statement.15

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Support Services (continued):

Direction of Business Support Services:Salaries 99,450$ 99,450 105,050 (5,600) 86,742 Employee Benefits 3,800 6,700 4,956 1,744 910 Purchased Services 2,100 3,500 4,215 (715) 1,400 Supplies and Materials 500 500 655 (155) - Capital Outlay 500 500 - 500 - Other Objects 1,000 1,000 710 290 325

Total Direction of Business Support Services 107,350 111,650 115,586 (3,936) 89,377

Fiscal Services:Salaries 128,000 128,000 126,292 1,708 77,158 Employee Benefits 23,490 21,852 21,584 268 14,744 Purchased Services 3,000 3,000 68,238 (65,238) - Supplies and Materials - 1,400 1,352 48 -

Total Fiscal Services 154,490 154,252 217,466 (63,214) 91,902

Operation & Maintenance of Plant Services:Salaries 332,112 216,970 216,049 921 205,668 Employee Benefits 4,809 8,137 2,694 5,443 4,551

Total Operation & Maintenanceof Plant Services 336,921 225,107 218,743 6,364 210,219

Pupil Transportation Services:Supplies and Materials - - - - 24,490

Total Pupil Transportation Services - - - - 24,490

Food Services:Salaries 792,464 732,464 748,681 (16,217) 774,400 Employee Benefits 161,678 156,311 139,018 17,293 152,958 Purchased Services 33,150 33,150 16,555 16,595 82,164 Supplies and Materials 972,245 911,245 1,020,576 (109,331) 1,023,207 Other Objects 750 750 529 221 701 Non-Capitalized Equipment 700 700 - 700 -

Total Food Services 1,960,987 1,834,620 1,925,359 (90,739) 2,033,430

Information Services:Salaries 64,454 64,454 67,004 (2,550) 64,686 Employee Benefits 1,370 1,111 996 115 2,262 Purchased Services 1,950 1,950 1,200 750 175 Other Objects 300 300 90 210 275

Total Information Services 68,074 67,815 69,290 (1,475) 67,398

The Notes to Financial Statements are an integral part of this statement.16

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Support Services (continued):

Staff Services:Salaries 37,258$ 41,272 45,819 (4,547) 105,679 Employee Benefits 22,618 28,625 13,577 15,048 25,688 Purchased Services 4,200 4,200 6,910 (2,710) 4,400 Supplies and Materials 500 500 - 500 -

Total Staff Services 64,576 74,597 66,306 8,291 135,767

Data Processing Services:Salaries 290,092 280,092 277,041 3,051 293,935 Employee Benefits 51,020 51,315 45,876 5,439 53,175 Purchased Services 336,200 269,200 245,516 23,684 233,579 Supplies and Materials 172,000 245,000 232,352 12,648 214,332 Capital Outlay - 50,000 76,356 (26,356) - Other Objects 9,730 9,730 - 9,730 10,267 Non-Capitalized Equipment 420,000 367,000 5,760 361,240 42,730

Total Data Processing Services 1,279,042 1,272,337 882,901 389,436 848,018

Other Support Services:Purchased Services 3,100 3,100 1,050 2,050 1,800 Supplies and Materials 2,300 2,300 197 2,103 -

Total Other Support Services 5,400 5,400 1,247 4,153 1,800

Total Support Services 10,696,590 10,394,299 9,847,468 546,831 9,903,476

Community Services:Salaries 9,555 9,555 9,485 70 7,926 Employee Benefits - 1,029 1,161 (132) - Purchased Services 350 350 250 100 234 Supplies and Materials 6,994 3,694 1,677 2,017 3,530

Total Community Services 16,899 14,628 12,573 2,055 11,690

Payments to Other Governmental Units:Payments to Other Governmental Units - In State:

Regular Programs 1,500 1,500 19,981 (18,481) 22,384 Special Education Programs 36,000 41,000 - 41,000 - CTE Programs - 2,800 2,796 4 3,034 Other Payments - - 13,767 (13,767) 400

Tuition Payments:Special Education Programs 54,000 72,000 66,452 5,548 42,932 CTE Programs 252,000 295,000 294,681 319 271,131

Total Payments to OtherGovernmental Units 343,500 412,300 397,677 14,623 339,881

The Notes to Financial Statements are an integral part of this statement.17

Statement D(Continued)

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5EDUCATIONAL FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed (continued):

Interest on Short-Term Debt -$ - 2,586 (2,586) 4,087

Provision for Contingencies 2,000 2,000 - 2,000 -

Total Expenditures Disbursed 32,441,259$ 32,347,142 31,729,303 617,839 30,852,236

The Notes to Financial Statements are an integral part of this statement.18

Statement EBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5OPERATIONS AND MAINTENANCE FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Support Services:

Operation & Maintenance of Plant Services:

Salaries 1,794,580$ 1,634,580 1,678,899 (44,319) 1,658,519 Employee Benefits 324,160 317,713 290,087 27,626 308,865 Purchased Services 463,667 463,667 407,628 56,039 424,340 Supplies and Materials 1,252,122 1,252,122 1,101,927 150,195 1,231,211 Capital Outlay 15,900 15,900 3,050 12,850 22,436 Other Objects 6,217 6,217 5,929 288 5,477 Non-Capitalized Equipment 16,143 16,143 14,942 1,201 1,277

Total Operation & Maintenanceof Plant Services 3,872,789 3,706,342 3,502,462 203,880 3,652,125

Total Support Services 3,872,789 3,706,342 3,502,462 203,880 3,652,125

Total Expenditures Disbursed 3,872,789$ 3,706,342 3,502,462 203,880 3,652,125

The Notes to Financial Statements are an integral part of this statement.19

Statement FBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5DEBT SERVICE FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Debt Service:Interest on Long-Term Debt 2,128,860$ 2,128,860 2,098,858 30,002 12,918,533 Principal on Long-Term Debt 2,860,000 2,860,000 2,860,000 - 2,482,215 Other - - 17,850 (17,850) 151,888

Total Expenditures Disbursed 4,988,860$ 4,988,860 4,976,708 12,152 15,552,636

The Notes to Financial Statements are an integral part of this statement.20

Statement GBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5TRANSPORTATION FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Support Services:

Pupil Transportation Services:Salaries 1,410,405 1,340,646 1,322,540 18,106 1,371,412 Employee Benefits 152,003 147,605 146,979 626 147,957 Purchased Services 100,550 100,550 76,233 24,317 106,467 Supplies and Materials 316,500 311,350 300,898 10,452 286,016

Total Pupil Transportation Services 1,979,458 1,900,151 1,846,650 53,501 1,911,852

Total Support Services 1,979,458 1,900,151 1,846,650 53,501 1,911,852

Total Expenditures Disbursed 1,979,458$ 1,900,151 1,846,650 53,501 1,911,852

The Notes to Financial Statements are an integral part of this statement.21

Statement HBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5MUNICIPAL RETIREMENT / SOCIAL SECURITY FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Instruction:

Employee Benefits:Regular Programs 141,942$ 134,840 192,360 (57,520) 195,005 Pre-K Programs 64,996 64,996 3,153 61,843 3,303 Special Education Programs 102,070 189,922 183,810 6,112 188,174 Special Education Pre-K 662 5,474 4,782 692 3,783 Adult/Continuing Education 6,932 6,932 6,758 174 6,733 CTE Programs 5,270 5,270 5,495 (225) 5,579 Interscholastic Programs 25,116 25,116 22,592 2,524 22,596 Summer School Programs 342 342 536 (194) 337 Driver's Education Programs 2,188 2,188 2,105 83 2,124

Total Instruction 349,518 435,080 421,591 13,489 427,634

Support Services:

Employee Benefits:Attendance and Social Work 3,228 3,228 3,023 205 3,134 Guidance Services 13,655 13,655 13,620 35 13,265 Health Services 48,680 44,533 40,135 4,398 41,222 Psychological Services 1,149 2,492 1,794 698 1,107 Speech Pathology & Audiology 6,003 6,003 5,693 310 5,063 Other Support Services - Pupils 54,751 55,216 54,137 1,079 49,850 Improvement of Instruction 2,582 2,582 2,212 370 2,447 Educational Media Services 23,156 21,433 21,998 (565) 22,567 Board of Education Services 10,615 10,615 1,061 9,554 343 Executive Administration 4,318 4,318 15,165 (10,847) 13,870 Special Area Administration 11,100 9,104 8,968 136 11,019 Office of the Principal Services 93,927 72,026 69,927 2,099 80,400

School Administration Services 21,886 21,400 22,237 (837) 17,259 Direction of Business 18,229 18,229 18,513 (284) 2,804 Fiscal Services 23,462 22,736 22,804 (68) 14,063 Operation and Maintenance of

Plant 400,269 324,380 328,264 (3,884) 342,517 Pupil Transportation Services 268,109 203,508 223,825 (20,317) 220,090 Food Services 129,496 112,893 113,673 (780) 112,685 Information Services 12,339 12,339 12,151 188 12,023 Staff Services 17,506 5,619 4,817 802 16,995 Data Processing Services 50,948 47,552 48,982 (1,430) 48,382 Other Support Services 617 - - - -

Total Support Services 1,216,025 1,013,861 1,032,999 (19,138) 1,031,105

Community Services: - 617 - 617 606

Total Expenditures Disbursed 1,565,543$ 1,449,558 1,454,590 (5,032) 1,459,345

The Notes to Financial Statements are an integral part of this statement.22

Statement IBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5CAPITAL PROJECTS FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Support:

Facilities Acquisition and Construction:Supplies and Materials -$ - - - 4,051 Capital Outlay 4,584,700 810,000 523,279 286,721 4,944,012

Total Facilities Acquisitionand Construction 4,584,700 810,000 523,279 286,721 4,948,063

Total Expenditures Disbursed 4,584,700$ 810,000 523,279 286,721 4,948,063

The Notes to Financial Statements are an integral part of this statement.23

Statement JBALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5FIRE PREVENTION AND SAFETY FUND

Statement of Expenditures DisbursedBudget and ActualFor the Year Ended June 30, 2017

Actual ActualOriginal Final Year Ended (Over) / Under Year EndedBudget Budget June 30, 2017 Budget June 30, 2016

Expenditures Disbursed:

Support:

Operation & Maintenance of Plant Services:

Supplies and Materials -$ - 3,780 (3,780) - Capital Outlay 1,000,000 130,000 105,642 24,358 178,248

Total Support 1,000,000 130,000 109,422 20,578 178,248

Total Expenditures Disbursed 1,000,000$ 130,000 109,422 20,578 178,248

The Notes to Financial Statements are an integral part of this statement.24

NOTES TO FINANCIAL STATEMENTS

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

25

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies of the Ball-Chatham Community Unit School District #5 conform to the modified cash basis of accounting as defined by the Illinois State Board of Education Audit Guide and comply with regulatory provisions prescribed by the Illinois State Board of Education. The following is a summary of the significant policies.

A. Reporting Entity

The District’s reporting entity includes the District’s governing board and all related organizations for which the District exercises oversight responsibility. The District has developed criteria to determine whether outside agencies with activities, which benefit the citizens of the District, including joint agreements, which serve pupils from numerous districts, should be included within its financial reporting entity. The criteria include, but are not limited to, oversight responsibility (including financial interdependency, selection of governing authority, designation of management, ability to significantly influence operations, and accountability for fiscal matters), scope of public service, and special financing relationships. There are no component units as defined above that are included in the districts reporting entity, also the District is not included in any other governmental “reporting entity.”

B. Fund Accounting

The accounts of the District are organized on the basis of funds or account groups, each of which is considered a separate accounting entity. The operations of each fund are summarized by providing a separate set of self-balancing accounts which includes its assets, liabilities, fund equity, revenue, and expenditures. The District maintains individual funds required by the State of Illinois. These funds are grouped as required for reports filed with the Illinois State Board of Education. District resources are allocated to and accounted for in individual funds based upon the purpose for which they are to be spent and the means by which spending activities are controlled. The District uses eight funds and two account groups as follows: Governmental Funds Governmental Funds are those through which most governmental functions of the District are financed. The acquisition, use and balance of the District’s expendable financial resources and the related liabilities (arising from cash transactions) are accounted for through governmental funds. The Educational Fund and the Operations and Maintenance Fund are the general operating funds of the District. They are used to account for all financial resources except those required to be accounted for in another fund. The Special Education levy and Leasing levy are included in the Educational Fund.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

26

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

B. Fund Accounting – (Continued)

Governmental Funds – (Continued) The Transportation Fund and the Municipal Retirement/Social Security Fund are used to account for the proceeds of specific revenue sources that are legally restricted to cash disbursements for specific purposes. The Capital Projects Fund and Fire Prevention and Safety Fund are used to account for financial resources to be used for the acquisition or construction of major capital facilities. The Working Cash Fund is used to account for financial resources held by the District to be used for temporary interfund loans to other funds. The Debt Service Fund accounts for the accumulation of resources for, and the payment of, general long-term debt principal, interest and related costs. Fiduciary Funds Fiduciary Funds are used to account for assets held by the District in a trustee capacity or as an agent for individuals, private organizations, other governments or other funds. The Agency Funds (Activity Funds) include both Student Activity Funds and Convenience Accounts. They account for assets held by the District as an agent for the students and teachers. These funds are custodial in nature and do not involve the measurement of the results of operations. The amounts due to the activity fund organizations are equal to the assets. Account Groups The accounting and reporting treatment applied to the fixed assets and long-term liabilities associated with a fund are determined by its measurement focus. The two account groups described below are not “funds.” They are concerned only with the measurement of financial position. They are not involved with measurement of results of operations.

General Fixed Assets Account Group – This account group is used to account for all capital assets used in governmental operations. General Long-Term Debt Account Group – This account group is established to account for all long-term liabilities expected to be financed from governmental funds.

The accompanying financial statements include Memorandum Only totals columns, which present total assets, liabilities, fund balances, revenues and expenditures for all of the District’s funds and account groups.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

27

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

C. Measurement Focus The financial statements of all governmental funds focus on the measurement of spending or “financial flow” and the determination of changes in financial position, rather than upon net income determination. This means that only current assets and current liabilities are generally included on their statement of assets and liabilities. Their reported fund balance (net current assets) is considered a measure of “available spendable resources.” Governmental fund operating statements present increases (cash receipts and other financial sources) and decreases (cash disbursements and other financing uses) in net current assets. Accordingly, they are said to present a summary of sources and uses of “available spendable resources” during a period.

D. Basis of Accounting Basis of accounting refers to when revenues and expenditures or expenses are recognized in the accounts and reported in the financial statements. The District maintains its accounting records for all funds and account groups on the modified cash basis of accounting under guidelines prescribed by the Illinois State Board of Education. Revenues are recognized when cash is received. Expenditures are recognized when cash is disbursed. Assets of a fund are only recorded when a right to receive cash exists which arises from previous cash transactions. Liabilities of a fund, similarly, result from previous cash transactions. Modified cash basis financial statements omit recognition of receivables and payables and other accrued and deferred items that do not arise from previous cash transactions. Proceeds from sales of bonds are included as other financing sources in the appropriate fund on the date received. Related bond principal payable in the future is recorded at the same time in the General Long-Term Debt Account Group.

E. Budgets and Budgetary Accounting The budget for all governmental funds is prepared on the modified cash basis of accounting, which is the same basis that is used in financial reporting. This allows for comparability between budget and actual amounts. This is an acceptable method in accordance with Chapter 122, Paragraph 17.1 of the Illinois Revised Statutes. The budget was passed on September 26, 2016 and was amended on June 20, 2017. For each fund, total expenditures disbursed may not legally exceed the budgeted amounts. The budget lapses at the end of the fiscal year.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

28

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

E. Budgets and Budgetary Accounting – (Continued) The District follows these procedures in establishing the budgetary data reflected in the financial statements:

1. Prior to July 1, the Superintendent submits to the Board of Education a proposed operating budget for the fiscal year commencing on that date. The operating budget includes proposed expenditures and the means of financing them.

2. The proposed budget is placed on file and a public hearing is held to obtain taxpayer comments.

3. Prior to October 1, the budget is legally adopted by the Board of Education through

passage of a resolution. 4. Formal budgetary integration is employed as a management control device at the

functional/objective level during the year. 5. The Board of Education may make transfers between the various items in any fund

not exceeding in the aggregate 10% of the total of such fund as set forth in the budget.

6. The Board of Education may amend the budget (in other ways) by the same

procedures required of its original adoption.

F. Investments Investments are recorded in accordance with GASB Statement No. 72, Fair Value Measurement and Application. Accordingly, the change in fair value of investments is recognized as an increase or decrease to investment assets and investment income. Gains or losses on the sale of investments are recognized upon realization. The District has adopted a formal written investment policy. The institutions in which investments are made must be approved by the Board of Education. The District’s investments consist of demand deposits and investments in an external investment pool, which are exempt from GASB Statement No. 72 fair value measurements.

G. General Fixed Assets Fixed assets have been acquired for general governmental purposes. At the time of purchase, assets are recorded as expenditures disbursed in the Governmental Funds and capitalized at cost in the General Fixed Assets Account Group. Donated general fixed assets are stated at estimated fair market value as of the date of acquisition. The capitalization threshold for all assets is $1,000. Depreciation accounting is not considered applicable (except to determine the per capita tuition charge). Depreciation was calculated on the straight-line basis for the per capita tuition charge and was $1,891,931, including $3,369 of depreciation on non-capitalized equipment, for the year ended June 30, 2017.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

29

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) G. General Fixed Assets – (Continued)

The estimated useful lives for fixed assets are as follows:

Property Type

Estimated Useful Life

(Years)Depreciable Land 50Buildings:

Permanent 50Temporary 20

Infrastructure other than Buildings 20Capitalized Equipment 3-10

H. Pensions

For purposes of measuring the net pension liability, information about the fiduciary net position of TRS and IMRF and additions to/deductions from the TRS and IMRF fiduciary net position have been determined on the same basis as they are reported by TRS and IMRF.

I. Reclassifications Certain prior year balances may have been reclassified to conform to the current year presentation.

J. Restricted Resources If both restricted and unrestricted resources are to be used for the same purpose, expenditures will first be made from restricted resources.

K. Use of Estimates The preparation of financial statements in conformity with the modified cash basis of accounting requires the District to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amount of revenues received and expenditures disbursed during the reported period. Actual results could differ from these estimates. The most significant estimate is depreciation used in calculating the per capita tuition charge.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

30

NOTE 2: CASH AND INVESTMENTS Cash and investments (excluding fiduciary funds) as of June 30, 2017 consist of the following:

Cash on Hand 539$ Deposits with Financial Institutions 18,674,552 Investments in External Investment Pool 4,134,052

Total Cash and Investments 22,809,143$

Investments Authorized by Illinois Compiled Statutes and the District’s Investment Policy The District is allowed to invest in securities as authorized by 30 ILCS 235/2 and 235/6 and 105 ILCS 5/8-7 of the Illinois Compiled Statutes. The District’s investment policy is consistent with Illinois Compiled Statues. Disclosures Relating to Interest Rate Risk Interest rate risk is the risk that changes in market interest rates will adversely affect the fair value of an investment. Generally, the longer the maturity of an investment, the greater the sensitivity of its fair value to changes in market interest rates. The District’s investment policy does not specifically address interest rate risk; however, one of the ways that the District manages its exposure to interest rate risk is by limiting its purchases of long term investments. At June 30, 2017, the District’s investments were deposits in financial institutions and investments in external investment pools. The activity fund’s and the expendable trust fund’s investments, are all demand deposits. None of the District’s investments are highly sensitive to interest rate fluctuations. Disclosures Relating to Credit Risk Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment. This is measured by the assignment of a rating by a nationally recognized statistical rating organization. The District’s investment policy requires a rating at the time of purchase at one of the three highest classifications established by at least two standard rating agencies. The District’s deposits with financial institutions are not subject to credit risk rating. The external investment pool has been rated AAAm. Concentration of Credit Risk The investment policy of the District contains no limitation on the amount that can be invested in any one issuer. Deposits with financial institutions and investments in external investment pools are exempt from the 5% investment in any one issuer disclosure.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

31

NOTE 2: CASH AND INVESTMENTS – (Continued) Custodial Credit Risk Custodial credit risk for deposits is the risk that in the event of a bank failure, the District’s deposits may not be returned or the District will not be able to recover collateral securities in the possession of an outside party. Illinois Compiled Statutes do not contain requirements that would limit the exposure to custodial credit risk for deposits. However, the District’s investment policy requires that all amounts deposited or invested with financial institutions in excess of any insurance limit to be collateralized. As of June 30, 2017, $22,291,602 of the District’s deposits with financial institutions in excess of federal depository insurance limits were collateralized by securities held by the pledging financial institution. Investment in External Investment Pool Illinois School Liquid Asset Fund Plus The District is a voluntary participant in the Illinois School Liquid Asset Fund Plus (ISDLAF+). ISDLAF+ is an Illinois common law trust organized to permit Illinois School Districts, community colleges, and educational services regions to pool their investment funds. The fund is overseen by a Board of Trustees. ISDLAF+ invests in high-quality, short-term debt instruments guaranteed by the full faith and credit of the United States, certain U.S. government agency obligations, commercial paper, bank obligations and other obligations permitted by Illinois law. The investment is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental or private agency. ISDLAF+ Fund is rated AAAm by Standard and Poors. The value of the District’s investment in the pool is reported at cost, which approximates market. Investors are not required to maintain minimum account balances. Foreign Currency Risk Foreign currency risk is the risk that changes in foreign exchange rates will adversely affect the fair values of an investment or deposit. None of the District’s investments are directly subject to foreign currency risk. The District’s investment policy does not address foreign currency risk.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

32

NOTE 3: PROPERTY TAXES The District’s property taxes are levied each year on all taxable real property located in the District on or before the last Tuesday in December. Taxes are levied in Sangamon County. The most recent levy was passed by the board on December 19, 2016. Property taxes attach as an enforceable lein on property as of January 1 and are payable in two installments in June and September. The District receives significant distributions of tax receipts approximately one month after these due dates. The Property Tax Extension Limitation Law of the State of Illinois, as amended (PTELL), limits the amount of annual increase in property taxes to be extended for certain Illinois non-home rule units of government, including this District. In general, PTELL restricts the amount of a property tax extension increase to the lesser of 5% or the percentage increase in the Consumer Price Index for Urban Consumers during the preceding calendar year. Tax levies may also be increased due to assessed valuation increases from new construction, referendum approval, and consolidation of local governmental units. The effect of the PTELL is to limit the growth of the amount of property taxes that can be extended for a taxing body. The PTELL was effective for Sangamon County on January 1, 1997. Tax proceeds from the 2016, 2015 and prior levies are reported as receipts from local sources in the June 30, 2017 financial statements. The remainder of the 2016 tax levy will be received in the subsequent year. The District receives the following levies that could result in restricted fund balances in the Educational Fund: Special Education - Cash receipts and the related cash disbursements of this restricted tax levy are accounted for in the Educational Fund. A total of $143,259 was collected and all was spent, resulting in no restricted fund balance. Leasing - Cash receipts and the related cash disbursements of this restricted tax levy are accounted for in the Educational Fund. A total of $143,259 was collected and all was spent, resulting in no restricted fund balance.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

33

NOTE 4: GENERAL FIXED ASSETS

BalanceJuly 1, 2016 Additions Deletions

BalanceJune 30, 2017

Capital Assets not Being Depreciated:Land 4,426,429$ - - 4,426,429 Construction in Progress 5,172,327 73,683 5,172,327 73,683

Total Capital Assets not being Depreciated 9,598,756 73,683 5,172,327 4,500,112

Depreciable Capital Assets:Buildings and Building Improvements 106,047,183 4,994,079 - 111,041,262 Site Improvements and Infrastructure 8,331,565 10,000 - 8,341,565 Capitalized Equipment 14,326,863 435,043 - 14,761,906

Total Depreciable Capital Assets 128,705,611 5,439,122 - 134,144,733

Total Capital Assets 138,304,367 5,512,805 5,172,327 138,644,845

Accumulated Depreciation:

Buildings and Building Improvements 3,535,645 1,045,399 - 4,581,044 Site Improvements and Infrastructure 486,178 164,264 - 650,442 Capitalized Equipment 3,191,275 682,268 - 3,873,543

Total Accumulated Depreciation 7,213,098 1,891,931 - 9,105,029

Capital Assets, Net 131,091,269$ 3,620,874 5,172,327 129,539,816

As explained in Note 1, depreciation is calculated to determine the District’s per capita tuition charge. Significant capital additions during the year ended June 30, 2017, included completion of the Glenview High School addition ($4,994,079) and completion of the camera security system ($283,890), which were reported as construction in progress at June 30, 2016. At June 30, 2017, construction in progress includes construction of a new security office entrance, which is expected to be completed during the year ended June 30, 2018.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

34

NOTE 5: LONG-TERM OBLIGATIONS The following is a summary of the District’s general long-term obligations for the year ended June 30, 2017:

Principal Principal AmountOutstanding Outstanding Due in6/30/2016 Increases Decreases 6/30/2017 One Year

General Obligation Bonds:Refunding Bonds (2005) 360,000$ - 360,000 - - Fire Prevention and Safety Bonds (2010A) 3,685,000 - 645,000 3,040,000 - Refunding Bonds (2010B) 1,900,000 - 600,000 1,300,000 625,000 Building Bonds (2012) 9,310,000 - - 9,310,000 - Building Bonds (2013) 8,695,000 - - 8,695,000 - Refunding Bonds(2014A) 1,230,000 - - 1,230,000 - Building Bonds (2014B) 6,610,000 - - 6,610,000 - Refunding Bonds (2014C) 2,705,000 - - 2,705,000 635,000 Working Cash Bonds (2015A) 1,700,000 - 10,000 1,690,000 40,000 Building Bonds (2015B) 9,470,000 - - 9,470,000 - Refunding Bonds (2015C) 140,000 - - 140,000 - Refunding Bonds (2016) 9,140,000 - 1,245,000 7,895,000 1,795,000

Total General Long Term Debt 54,945,000$ - 2,860,000 52,085,000 3,095,000

Refunding Bonds (2005) Original issue $21,955,000 dated July 6, 2005, provides for serial retirement of principal on January 1 and interest payable on January 1 and July 1 of each year as stated interest rates ranging from 3.00% to 5.00%. This issue advance refunded $22,595,000 of outstanding 1999 Refunding/Building Bonds. The net proceeds were used to purchase U.S. government securities. Those securities were deposited in an irrevocable trust with an escrow agent to provide for future debt service payments on 1999 Refunding/Building Bonds. As a result, $22,595,000 of the 1999 Refunding/Building Bonds is considered to be defeased and the liability of those bonds has been removed from the general long-term debt account group. The Series 2014A Refunding Bonds advanced refunded $1,100,000 of these bonds. As a result, $1,100,000 of principal is considered to be defeased. The Series 2015C Refunding Bonds advanced refunded $120,000 of these bonds. As a result, $120,000 of principal is considered to be defeased. The Series 2016 Refunding Bonds currently refunded $9,635,000 of these bonds. As a result, $9,635,000 of principal is considered to be defeased. As of June 30, 2017, the bonds have been paid in full.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

35

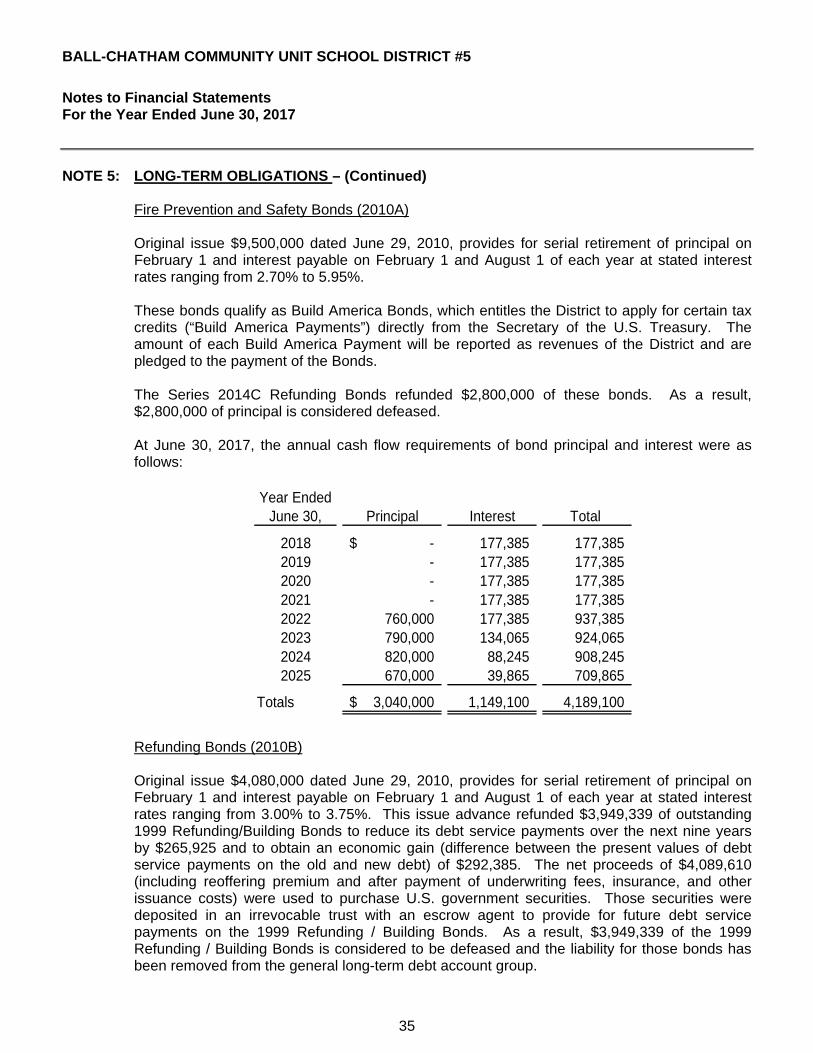

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Fire Prevention and Safety Bonds (2010A) Original issue $9,500,000 dated June 29, 2010, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at stated interest rates ranging from 2.70% to 5.95%. These bonds qualify as Build America Bonds, which entitles the District to apply for certain tax credits (“Build America Payments”) directly from the Secretary of the U.S. Treasury. The amount of each Build America Payment will be reported as revenues of the District and are pledged to the payment of the Bonds. The Series 2014C Refunding Bonds refunded $2,800,000 of these bonds. As a result, $2,800,000 of principal is considered defeased. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 177,385 177,385 2019 - 177,385 177,385 2020 - 177,385 177,385 2021 - 177,385 177,385 2022 760,000 177,385 937,385 2023 790,000 134,065 924,065 2024 820,000 88,245 908,245 2025 670,000 39,865 709,865

Totals 3,040,000$ 1,149,100 4,189,100

Refunding Bonds (2010B) Original issue $4,080,000 dated June 29, 2010, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at stated interest rates ranging from 3.00% to 3.75%. This issue advance refunded $3,949,339 of outstanding 1999 Refunding/Building Bonds to reduce its debt service payments over the next nine years by $265,925 and to obtain an economic gain (difference between the present values of debt service payments on the old and new debt) of $292,385. The net proceeds of $4,089,610 (including reoffering premium and after payment of underwriting fees, insurance, and other issuance costs) were used to purchase U.S. government securities. Those securities were deposited in an irrevocable trust with an escrow agent to provide for future debt service payments on the 1999 Refunding / Building Bonds. As a result, $3,949,339 of the 1999 Refunding / Building Bonds is considered to be defeased and the liability for those bonds has been removed from the general long-term debt account group.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

36

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Refunding Bonds (2010B) – (Continued) At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 625,000$ 47,187 672,187 2019 675,000 25,313 700,313

Totals 1,300,000$ 72,500 1,372,500

Building Bonds (2012) Original issue $9,310,000 dated December 27, 2012, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at stated interest rates ranging from 2.50% to 4.00%. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 322,750 322,750 2019 - 322,750 322,750 2020 - 322,750 322,750 2021 - 322,750 322,750 2022 - 322,750 322,750 2023 2,000,000 322,750 2,322,750 2024 2,000,000 242,750 2,242,750 2025 2,000,000 162,750 2,162,750 2026 1,010,000 82,750 1,092,750 2027 1,000,000 57,500 1,057,500 2028 1,300,000 32,500 1,332,500

Totals 9,310,000$ 2,514,750 11,824,750

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

37

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Building Bonds (2013) Original issue $8,695,000 dated February 5, 2013, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at stated interest rates ranging from 2.50% to 2.625%. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 219,437 219,437 2019 - 219,437 219,437 2020 - 219,437 219,437 2021 - 219,437 219,437 2022 - 219,437 219,437 2023 - 219,437 219,437 2024 - 219,437 219,437 2025 700,000 219,437 919,437 2026 2,845,000 201,938 3,046,938 2027 3,500,000 130,813 3,630,813 2028 1,650,000 43,313 1,693,313

Totals 8,695,000$ 2,131,560 10,826,560

Refunding Bonds (2014A) Original issue $1,230,000 dated April 2, 2014, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at a stated interest rate of 2.75%. This issue advance refunded $1,110,000 of outstanding 2005 Refunding Bonds. The net proceeds of $1,196,104 (including reoffering premium and after payment of underwriting fees, insurance, and other issuance costs) were used to purchase U.S. government securities. Those securities were deposited in an irrevocable trust with an escrow agent to provide for future debt service payments on the 2005 Refunding Bonds. As a result, $1,100,000 of the 2005 Refunding Bonds is considered to be defeased and the liability for those bonds has been removed from the general long-term debt account group. The partial refunding of both the 2005 Refunding Bonds and 2010A Fire Prevention and Safety Bonds resulted in a net present value savings of $128,764 to the District.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

38

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Refunding Bonds (2014A) – (Continued) At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 33,825 33,825 2019 - 33,825 33,825 2020 1,230,000 33,825 1,263,825

Totals 1,230,000$ 101,475 1,331,475

Building Bonds (2014B) Original issue $6,610,000 dated April 2, 2014, provides for serial retirement of principal on February 1 and interest payable February 1 and August 1 of each year at stated interest rates ranging from 4.00% to 4.50%. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ending June 30, Principal Interest Total

2018 -$ 288,944 288,944 2019 - 288,944 288,944 2020 - 288,944 288,944 2021 - 288,944 288,944 2022 - 288,944 288,944 2023 - 288,944 288,944 2024 - 288,944 288,944 2025 370,000 288,944 658,944 2026 1,775,000 274,144 2,049,144 2027 1,470,000 200,925 1,670,925 2028 2,745,000 134,775 2,879,775 2029 250,000 11,250 261,250

Totals 6,610,000$ 2,932,646 9,542,646

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

39

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Refunding Bonds (2014C) Original issue $2,705,000 dated April 2, 2014, provides for serial retirement of principal on February 1 and interest payable on February 1 and August 1 of each year at stated interest rates ranging from 3.00% to 4.00%. This issue currently refunded $2,800,000 of outstanding 2010A Fire Prevention and Safety Bonds. The net proceeds of $2,887,293 (including reoffering premium and after payment of underwriting fees, insurance, and other issuance costs) were used to pay principal and interest. As a result, $2,800,000 of the 2010A Fire Prevention and Safety Bonds is considered to be defeased and the liability for those bonds has been removed from the general long-term debt account group. The partial refunding of both the 2005 Refunding Bonds and the 2010A Fire Prevention and Safety Bonds resulted in a net present value savings of $128,764 to the District. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ending June 30, Principal Interest Total

2018 635,000$ 101,050 736,050 2019 665,000 75,650 740,650 2020 690,000 49,050 739,050 2021 715,000 21,450 736,450

Totals 2,705,000$ 247,200 2,952,200

Working Cash Bonds (2015A) Original issue $1,700,000 dated March 2, 2015, provides for serial retirement of principal on January 1 and interest payable on January 1 and July 1 of each year at stated interest rates ranging from 0.95% to 4.10%.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

40

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Working Cash Bonds (2015A) – (Continued) At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ending June 30, Principal Interest Total

2018 40,000$ 62,480 102,480 2019 35,000 61,950 96,950 2020 40,000 61,290 101,290 2021 45,000 60,415 105,415 2022 20,000 59,670 79,670 2023 20,000 59,140 79,140 2024 20,000 58,550 78,550 2025 200,000 54,840 254,840 2026 - 51,440 51,440 2027 - 51,440 51,440 2028 630,000 38,840 668,840 2029 640,000 13,120 653,120

Totals 1,690,000$ 633,175 2,323,175

Building Bonds (2015B) Original issue $9,470,000 dated March 2, 2015, provides for serial retirement of principal on January 1 and interest payable on January 1 and July 1 each year at stated interest rates ranging from 4.498% to 5.00%. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 453,975 453,975 2019 - 453,975 453,975 2020 1,445,000 417,850 1,862,850 2021 3,050,000 305,475 3,355,475 2022 3,385,000 150,375 3,535,375 2023 1,590,000 35,763 1,625,763

Totals 9,470,000$ 1,817,413 11,287,413

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

41

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Refunding Bonds (2015C) Original issue $140,000 dated March 2, 2015, provides for serial retirement of principal on January 1 and interest payable on January 1 and July 1 each year at stated interest rate of 1.90%. This issue advanced refunded $120,000 of outstanding 2005 Refunding Bonds. The net proceeds of $125,867 (including reoffering premium and after payment and underwriting fees, insurance, and other issuance costs) were used to purchase U.S. government securities. Those securities were deposited in an irrevocable trust with an escrow agent to provide for future debt service payments on the 2005 Refunding Bonds. As a result, $120,000 of the 2005 Refunding Bonds is considered to be defeased and the liability for those bonds has been removed from the general long-term debt account group. The partial refunding of the 2005 Refunding Bonds resulted in a net present value loss of $6,129 to the District. At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total

2018 -$ 2,660 2,660 2019 - 2,660 2,660 2020 140,000 1,330 141,330

Totals 140,000$ 6,650 146,650

Refunding Bonds (2016) Original issue $9,140,000 dated January 5, 2016, provides for serial retirement of principal on January 1 and interest payable on January 1 and July 1 of each year at stated interest rates ranging from 3.00% to 4.00%. This issue currently refunded $9,635,000 of outstanding 2005 Refunding Bonds. The net proceeds of $9,653,735 (including reoffering premium and after payment of underwriting fees, insurance, and other issuance costs) were used to pay principal and interest. As a result, $9,635,000 of the 2005 Refunding Bonds is considered to be defeased and the liability for those bonds has been removed from the general long-term debt account group. The partial refunding of the 2005 Refunding Bonds resulted in a net present value savings of $451,976 to the District.

BALL-CHATHAM COMMUNITY UNIT SCHOOL DISTRICT #5

Notes to Financial Statements For the Year Ended June 30, 2017

42

NOTE 5: LONG-TERM OBLIGATIONS – (Continued) Refunding Bonds (2016) – (Continued) At June 30, 2017, the annual cash flow requirements of bond principal and interest were as follows:

Year Ended June 30, Principal Interest Total