Avramov Doron Financial Econometrics

554

Lecture Notes Financial Econometrics Professor Doron E. Avramov Hebrew University of Jerusalem ' Prof . Doron Avramov Financial Econometrics 1

-

Upload

alvaro-mamani-machaca -

Category

Documents

-

view

267 -

download

8

Transcript of Avramov Doron Financial Econometrics

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 1/553

Lecture Notes

Financial Econometrics

Professor Doron E. Avramov

Hebrew University of Jerusalem

'Prof. Doron Avramov

Financial Econometrics1

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 2/553

Syllabus: Motivation• Why do we need a course in financial

econometrics?

• The past few decades have been characterized

by an extraordinary growth in the use of

quantitative methods in financial markets inanalyzing various asset classes; be it equities,

fixed income instruments, commodities, or

derivative securities.

'Prof. Doron Avramov

Financial Econometrics2

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 3/553

Syllabus: MotivationFinancial market participants, both academics

and practitioners, have been routinely using

advanced econometric techniques in a host of

applications including portfolio management,

risk management, modeling volatility,understanding pivotal issues in corporate

finance, asset pricing, interest rate modeling, as

well as regulatory purposes.

'Prof. Doron Avramov

Financial Econometrics3

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 4/553

Syllabus: Objectives• This course attempts to provide a fairly deep

understanding of topical issues in asset pricing

and deliver econometric methods in which to

develop research agenda in financial economics.

•The course targets advanced master level and

PhD level students in finance and economics.

'Prof. Doron Avramov

Financial Econometrics4

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 5/553

Syllabus: Prerequisite• I will assume some prior exposure to matrix

algebra, distribution theory, Ordinary Least

Squares, and Maximum Likelihood

Estimation.

• I will also assume you have some skills in

computer programing beyond Excel.

Suggested packages include MATLAB,STATA, SAS, R, etc.

'Prof. Doron Avramov

Financial Econometrics5

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 6/553

Syllabus: Topics to be CoveredOverview:

Matrix algebra

Regression analysisLaw of iterated expectations

Variance decomposition

Taylor approximationDistribution theory

Hypothesis testing

OLS

MLE

'Prof. Doron Avramov

Financial Econometrics6

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 7/553

Syllabus: Topics to be CoveredTesting asset pricing models including the CAPM

and multi factor models: Time series analysis.

The econometrics of the mean variance frontier

Estimating expected returns

Estimating the covariance matrix of stock returns.

Forming mean variance efficient portfolio, the

Global Minimum Volatility Portfolio, and the

minimum Tracking Error Volatility Portfolio.'Prof. Doron Avramov

Financial Econometrics7

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 8/553

Syllabus: Topics to be CoveredThe Sharpe ratio: estimation and distribution

The Delta method

The Black-Litterman approach for estimating expected

returns.

Principal component analysis.

'Prof. Doron Avramov

Financial Econometrics8

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 9/553

Syllabus: Topics to be CoveredRisk management and the downside risk measures:

value at risk, shortfall probability, expectedshortfall, target semi-variance, downside beta, and

drawdown.

Option pricing: testing the validity of the B&S

formula

Model verification based on failure rates

'Prof. Doron Avramov

Financial Econometrics9

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 10/553

Syllabus: Topics to beCoveredVariance ratio tests

Predicting asset returns using time series regressions

The econometrics of back-testing

Understanding time varying volatility models

including ARCH, GARCH, EGARCH, stochastic

volatility, implied volatility, and realized volatility

'Prof. Doron Avramov

Financial Econometrics10

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 11/553

Syllabus: Grade Components• Assignments (35%): there will be three problem sets

during the term. You can form study groups to prepare

the assignments with up to four students per group.

•Class Participation (15%) - Attending AT LEAST 80%

of the sessions is mandatory.•Take-home final exam (50%): based on class material,

handouts, assignments, and readings.

'Prof. Doron Avramov

Financial Econometrics11

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 12/553

Let us StartThis session is mostly an overview. Major contents:

• Why do we need a course in financial econometrics?• Normal, Bivariate normal, and multivariate normal

densities

• The Chi-squared, F, and Student t distributions

• Regression analysis

• Basic rules and operations applied to matrices

• Iterated expectations and variance decomposition'Prof. Doron Avramov

Financial Econometrics12

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 13/553

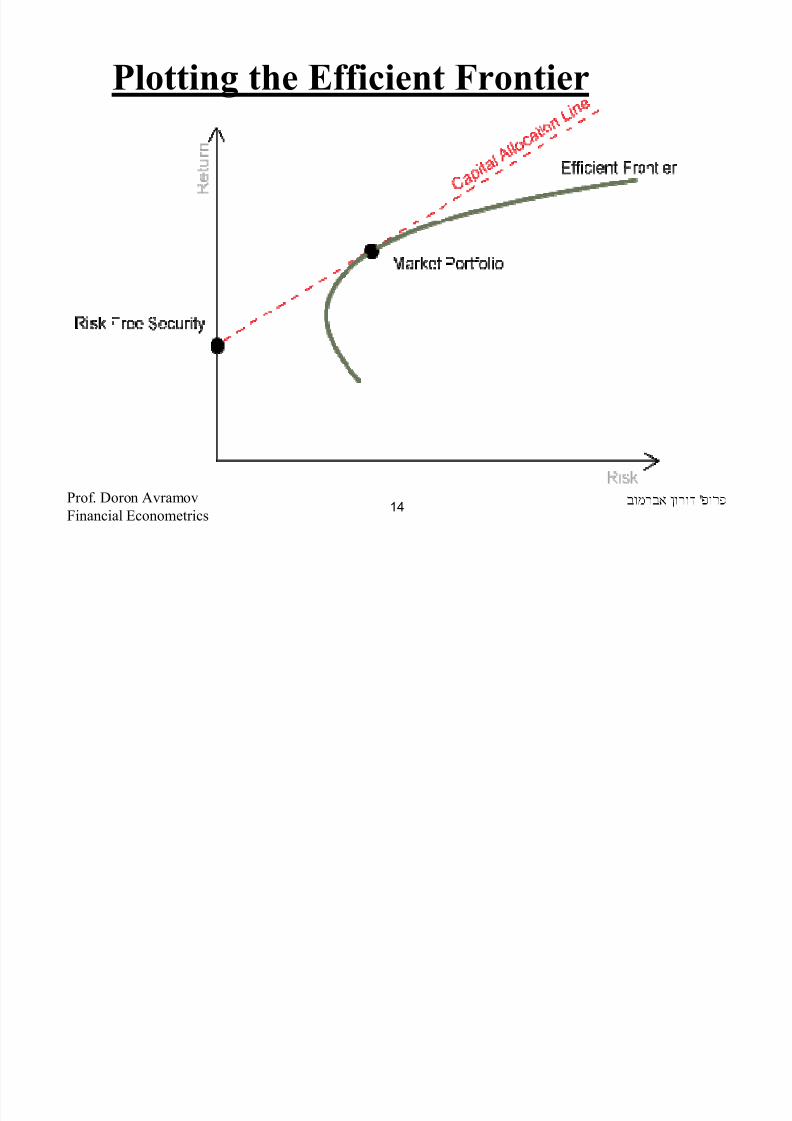

Financial EconometricsIn previous courses in finance and economics you

mastered the concept of the efficient frontier.

A portfolio lying on the frontier is the highest

expected return portfolio for a given volatility target.

Or it is the lowest volatility portfolio for a given

expected return target.

'Prof. Doron Avramov

Financial Econometrics13

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 14/553

Plotting the Efficient Frontier

'Prof. Doron Avramov

Financial Econometrics14

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 15/553

However, how could you Practically Form

an Efficient Portfolio?

• Problem: there are TOO many parameters to estimate.

For instance, investing in ten assets requires:

which is about ten estimates for expected return, ten for volatility, and 45 for covariances/correlations.

Overall, 65 estimates are required. That is a lot!!!

10

2

1

.

.

µ

µ

µ

2

1010,1

2

22,1

10,1

2

,

1

σ σ

σ σ

σ σ

KKKKK

KKKKKKKK

KKKKK

KKKKK

'Prof. Doron Avramov

Financial Econometrics15

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 16/553

More generally, if there are N investable assets, you need:

• N estimates for the means,

• N estimates for the volatilities,

• 0.5N(N-1) estimates for correlations.

Overall: 2N+0.5N(N-1) estimates are required!

Mean, volatility, and correlation estimates are noisy

as reflected through their standard errors.

'Prof. Doron Avramov

Financial Econometrics16

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 17/553

• The volatility estimate is less noisy than the mean.

• I will later show that the standard error of the volatilityestimate is lower than that of mean return.

• We have T asset return observations:

•The sample mean and volatility are given by

T R R R R KKK321 ,,

( )

1

ˆ

2

1

−

−= ∑=

T

R RT

t t σ Less noisy

'Prof. Doron Avramov

Financial Econometrics17

T

R R

T

t t ∑ == 1

Sample Mean and Volatility

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 18/553

Estimation Methods

• One of the ideas here is to introduce robust methods

in which to estimate the comprehensive set of

parameters.

• We will discuss asset pricing models and the Black

Litterman approach for estimating expected returns.• We will further introduce several methods for

estimating the large-scale covariance matrix of asset

returns.

'Prof. Doron Avramov

Financial Econometrics18

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 19/553

Mean-Variance vs. Down

Side Risk

•We will comprehensively cover topics in meanvariance analysis.

•We will also depart from the mean variance

paradigm and consider down side risk measuresto form as well as evaluate investment strategies.

• Why do we need to resort to down side risk?

'Prof. Doron Avramov

Financial Econometrics19

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 20/553

Down Side Risk

• For one, investors often care more about the

down side of investment payoffs than the upside

potential.

•The practice of risk management as well as

regulations of financial institutions are typicallyabout downside risk – such as targeting VaR,

shortfall probability, and expected shortfall.

•Moreover, there is a major weakness embedded

in the mean variance paradigm.

'Prof. Doron AvramovFinancial Econometrics

20

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 21/553

Drawback in the Mean-Variance Setup

• To illustrate, consider two stocks, A and B, with

correlation coefficient smaller than unity.

•There are five states of nature in the economy.

•Returns in the various states are described on the

next page.

'Prof. Doron AvramovFinancial Econometrics

21

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 22/553

• Stock A dominates stock B in every state of nature.

• Nevertheless, a mean-variance investor may consider

stock B because it can reduce the portfolio’s volatility.

• Investment criteria based on down size risk measurescould get around this weakness.

S5S4S3S2S1

20.05%10.50%15.00%8.25%5.00%A3.01%3.10%2.95%2.90%3.05%B

'Prof. Doron AvramovFinancial Econometrics

22

Drawback in Mean-Variance

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 23/553

The Normal Distribution• In various applications in finance and economics, a

common assumption is that quantities of interests, such

as asset returns, economic growth, dividend growth,

interest rates, etc., are normally (or log-normally)

distributed.

• The normality assumption is primarily done for

analytical tractability.

• The normal distribution is symmetric.

• It is characterized by the mean and the variance.

'Prof. Doron AvramovFinancial Econometrics

23

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 24/553

Confidence Level Normality suggests that deviation of 2 SD away from

the mean creates an 80% range (from -32% to 48%) for

the realized return with 95% confidence level.

'Prof. Doron AvramovFinancial Econometrics

24

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 25/553

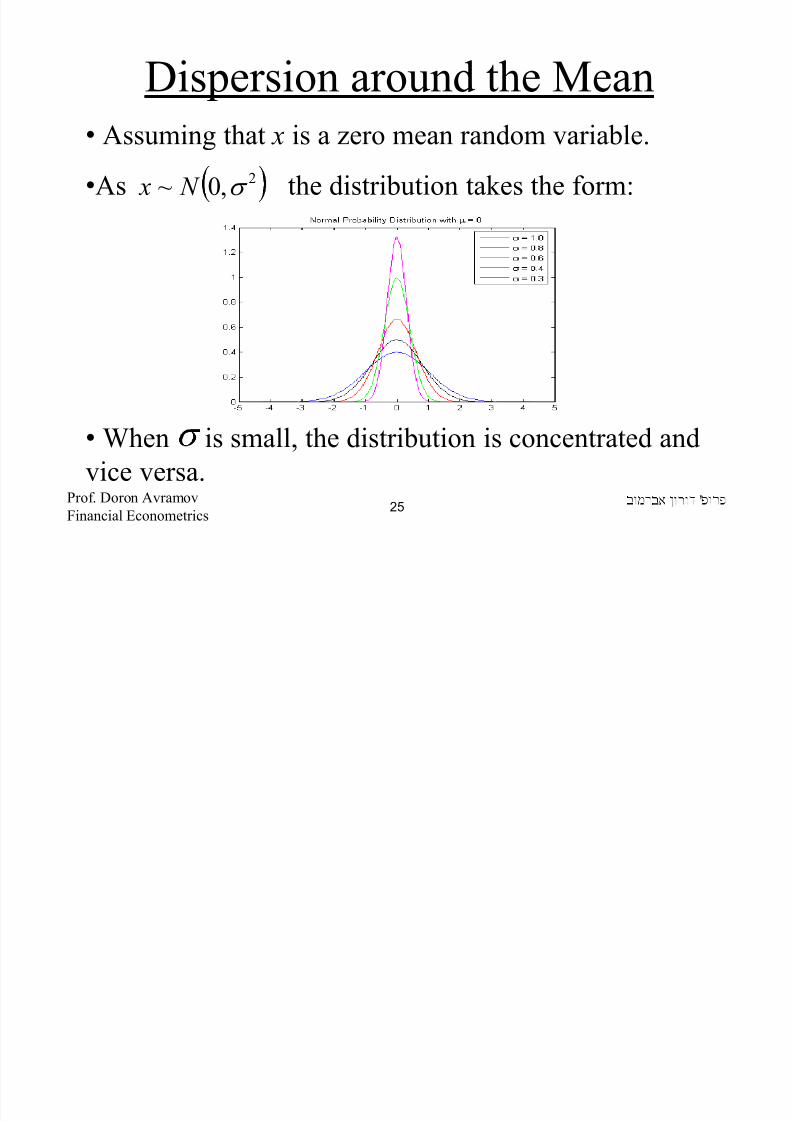

Dispersion around the Mean

• Assuming that x is a zero mean random variable.

•As the distribution takes the form:

• When is small, the distribution is concentrated and

vice versa.

2,0~ σ N x

'Prof. Doron AvramovFinancial Econometrics

25

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 26/553

Probability Distribution Function

• The Probability Density Function (pdf) of the normal

distribution is:

• If then:

• The Cumulative Density Function (CDF), which is the

integral of the pdf, is 50% at that point.

( )

−−=2

2

2 2

1exp

2

1)(

σ

µ

πσ

r r pdf

==

r µ

σ 1

π 2

1)( =r pdf

'Prof. Doron AvramovFinancial Econometrics

26

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 27/553

Normally Distributed Return•Assume that the US excess rate of return on the

market portfolio is normally distributed with annual

mean (equity premium) and volatility given by 8% and20%, respectively.

•That is to say that with a nontrivial probability theactual excess annual market return can be negative.

See figures on the next page.

'Prof. Doron AvramovFinancial Econometrics

27

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 28/553

Confidence Intervals for Annual Excess

Return on the Market

The probability that the realization is negative

%99)2.0308.02.0308.0(Pr

%95)2.0208.02.0208.0(Pr

%68)2.008.02.008.0(Pr

=×+<<×−

=×+<<×−

=+<<−

Rob

Rob

Rob

'Prof. Doron AvramovFinancial Econometrics

28

%4.34)4.0(Pr

2.0

08.00

2.0

08.0Pr )0(Pr

=−<=

−<

−=<

z ob

Rob Rob

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 29/553

Higher Moments• Skewness – the third moment - is zero.

• Kurtosis – the fourth moment – is three.

• Odd moments are all zero.

• Even moments are (often complex) functions of themean and the variance.

•In the next slides, skewness and kurtosis are presented

for other distribution functions.

'Prof. Doron AvramovFinancial Econometrics

29

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 30/553

Skewness• The skewness can be negative (left tail) or

positive (right tail).

'Prof. Doron AvramovFinancial Econometrics

30

Kurtosis

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 31/553

Kurtosis

'Prof. Doron AvramovFinancial Econometrics

31

• Mesokurtic - A term used in a statistical context where the

kurtosis of a distribution is similar, or identical, to the

kurtosis of a normally distributed data set.

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 32/553

•

•Positive skewness means non-zero probability for large payoffs.

• Kurtosis is a measure for how tick the distribution’s tails are.

• When is the skewness zero? In symmetric distributions.

'Prof. Doron AvramovFinancial Econometrics

32

The Essence of Skewness and

Kurtosis

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 33/553

Bivariate Normal Distribution

• Bivariate normal:

• The marginal densities of x and y are

• What is the distribution of y if x is known?

22

2

,

,,~

y xy

xy x

y

x N

y

x

σ σ

σ σ

µ

µ

(( )[ ]2

2

,~

,~

y y

x x

N y

N x

σ µ

σ µ

'Prof. Doron AvramovFinancial Econometrics

33

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 34/553

Conditional Distribution

• Conditional distribution:

always non-negative• When the correlation between x and y is positive

and - then the conditional expectation ishigher than the unconditional one.

( )

−−+ 2

2

22

,~ x

xy y x

x

xy y x N x y

σ σ σ µ

σ σ µ

x x µ >

'Prof. Doron AvramovFinancial Econometrics

34

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 35/553

Conditional Moments• If we have no information about x, or if x and y are

uncorrelated, then the conditional and unconditional

expected return of y are identical.• Otherwise, the expected return of y is .

• If , then:

Here, the realization of x does not say anything about y.

0= xyσ

x yµ

y

x

xy

y x y σ σ

σ σ σ =−=

2

2

2

'Prof. Doron AvramovFinancial Econometrics

35

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 36/553

Conditional Standard Deviation

• Developing the conditional standard deviation further:

• When goodness of fit is higher the conditional standarddeviation is lower.

( )2

22

2

2

2

2

2 11 R y

y x

xy

y

x

xy

y x y −=

⋅

−=−= σ

σ σ

σ σ

σ

σ σ σ

'Prof. Doron AvramovFinancial Econometrics

36

M lti i t N l

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 37/553

• Define Z=AX+B.

( )mmm

m

m N

x

x

x

X ××× ∑

= ,~

.

. 1

2

1

1 µ

'Prof. Doron AvramovFinancial Econometrics

37

Multivariate Normal

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 38/553

• Let us make some transformations to end up with

N (0,I):

( )

( )( ) ),0(~

),0(~

),(~

11

2

1'

'11

'

1111

I N B A Z A A

A A N B A Z

A A B A N B X A Z

nmmnnmmmmn

nmmmmnnmmn

nmmmmnnmmnnmmn

×××

−

×××

×××⋅××

×××××××××

−−∑

∑+−

∑++⋅=

µ

µ

µ

'Prof. Doron AvramovFinancial Econometrics

38

Multivariate Normal

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 39/553

Multivariate Normal

• Consider an N -vector or returns which is normally

distributed:

• Then:

• What does mean? A few rules:

( ) N N N N N R ××× ∑,~ 11 µ

( )

( ) ( ) I N R

N R

,0~

,0~

2

1

µ

µ

−∑

∑−

−

2

1−

∑

I =∑⋅∑

∑=∑⋅∑

∑=∑⋅∑

−

−−−

2

1

2

1

2

1

2

1

12

1

2

1

'Prof. Doron AvramovFinancial Econometrics

39

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 40/553

• If X 1~N(0,1) then

• If X 1~N(0,1), X 2~N (0,1) & then:

( )2~ 222

21 χ X X +

21 X X ⊥

'Prof. Doron AvramovFinancial Econometrics

40

The Chi-Squared Distribution

( )1~ 22

1 χ X

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 41/553

• Moreover if

then

( )

( )

21

2

2

2

1

~

~

X X

n X

m X

⊥

χ

χ

( )nm X X ++ 221 ~ χ

'Prof. Doron AvramovFinancial Econometrics

41

More about the Chi-Squared

The F Distribution

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 42/553

•Gibbons, Ross & Shanken (GRS) designated a finite

sample asset pricing test that has the F - Distribution.

•If

•Then

),(~2

1

nm F

n X m

X

A =

( )( )

21

2

2

21

~

~

X X

n X

m X

⊥

χ

χ

'Prof. Doron AvramovFinancial Econometrics

42

The F Distribution

The Student’s t Distribution

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 43/553

The Student s t Distribution

'Prof. Doron AvramovFinancial Econometrics

43

The t Distribution

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 44/553

• The pdf of student-t is given by:

• Where is beta function and is a number of

degrees of freedom

The t Distribution

'Prof. Doron AvramovFinancial Econometrics

44

( )( )

2

12

121,2

1,

+−

+⋅

⋅=

v

v x

v Bvv x f

( )ba B , 1≥v

The t Distribution

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 45/553

• As noted earlier, is a sample of length T of

stock returns which are normally distributed.

• The sample mean and variance are

• The resulting t -value which has the t distribution with T-1

d.o.f is

The t Distribution

'Prof. Doron AvramovFinancial Econometrics

45

T r r r ,,, 21 K

T

r r

r

T K+

=

1

and ( )∑= −−=

T

t t r r T s 1

22

1

1

1−−=T

sr t µ

The t Distribution

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 46/553

• The t -distribution is the sampling distribution of the t -value

when the sample consist of independent and identically

distributed observations from a normally distributed population.

• It is obtained by dividing a normally distributed random variable

by a square root of a Chi-squared distributed random variable

when both random variables are independent.

• Indeed, later we will show that when returns are normally

distributed the sample mean and variance are independent.

The t Distribution

'Prof. Doron AvramovFinancial Econometrics

46

R i A l i

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 47/553

Regression Analysis• Various applications in corporate finance and asset

pricing require the implementation of a regression

analysis.• We will estimate regressions using matrix notation.

• For instance, consider the time series regression

t t t t Z Z R ε β β α +++= 2211 T ,2,1, KK=∀

'Prof. Doron AvramovFinancial Econometrics

47

R iti th t i t i f

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 48/553

• Rewriting the system in a matrix form:

yields

• We will derive regression coefficients and their standard

errors using OLS, MLE, and Method of Moments.

=×

21

2221

1211

3

,,1

.

.

,,1

,,1

T T

T

Z Z

Z Z

Z Z

X

=×

2

113

β β

α

γ

11331 ×××× += T T T X R ε γ

=×

T

T

ε

ε

ε

ε ..

2

1

1

'Prof. Doron AvramovFinancial Econometrics

48

=×

T

T

R

R

R

R..

2

1

1

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 49/553

Vectors and Matrices: some Rules

• If A is a row vector:

• Then the transpose of A is a column vector:

• The identity matrix satisfies

[ ]t t aaa A 112,111 ,K=×

=×

1

21

11

1

.

.'

t

t

a

a

a

A

B I B B I =⋅=⋅

'Prof. Doron AvramovFinancial Econometrics

49

M l i li i f M i

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 50/553

Multiplication of Matrices:

,

The inverse of the matrix A is A-1 which satisfies:

=×

22,21

12,11

22aa

aa A

=×

22,12

21,11

22'aa

aa A

=×

22,21

12,11

22bb

bb B

++

++=××

22221221,21221121

22121211,21121111

2222babababa

babababa B A

==−

×× 1,0

0,11

2222 I A A

111)(

'')'(

−−− =

=

A B AB

A B AB

'Prof. Doron AvramovFinancial Econometrics

50

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 51/553

Solving Large Scale Linear Equations:

• Of course, A has to be a square invertible matrix.

b

b X A mmmm

1

11

−

×××

=

=

'Prof. Doron AvramovFinancial Econometrics

51

Linear Independence and Norm

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 52/553

Linear Independence and Norm

• The vectors are linearly independent if there

does not exists scalars such that

• The norm of a vector V is

'Prof. Doron AvramovFinancial Econometrics

52

N V V ,,1 K

N cc ,,1 K

unless

V cV cV c N N 02211 =+++ K

021 === N ccc K

V V V '=

A Positive Definite Matrix

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 53/553

A Positive Definite Matrix

• An matrix is called positive definite if

for any nonzero vector V.

• A non positive definite matrix cannot be inverted and

its determinant is zero.

'Prof. Doron AvramovFinancial Econometrics

53

N N × ∑

0' 11 >⋅∑⋅ ××× N N N N V V

The Trace of a Matrix

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 54/553

The Trace of a Matrix

• Let

• Then

• Trace is the sum of diagonal elements.

'Prof. Doron AvramovFinancial Econometrics

54

( ) ( )[ ]111

2

,1,

2

22,1

,1

2

,,,

1

××× =

=∑ N

N

N

N N

N

N N σ σ

σ σ

σ σ

σ σ

K

KKKKK

KKKKKKKK

KKKKK

KKKKK

( )

22

2

2

1 N tr σ σ σ +++=∑K

Matrix Vectorization

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 55/553

Matrix Vectorization

This is the vectorization operator –

it works for both square as well

as non square matrices.

'Prof. Doron AvramovFinancial Econometrics

55

( )

( )

( )

( )

=∑×

N

N Vec

σ

σ

σ

M

2

1

12

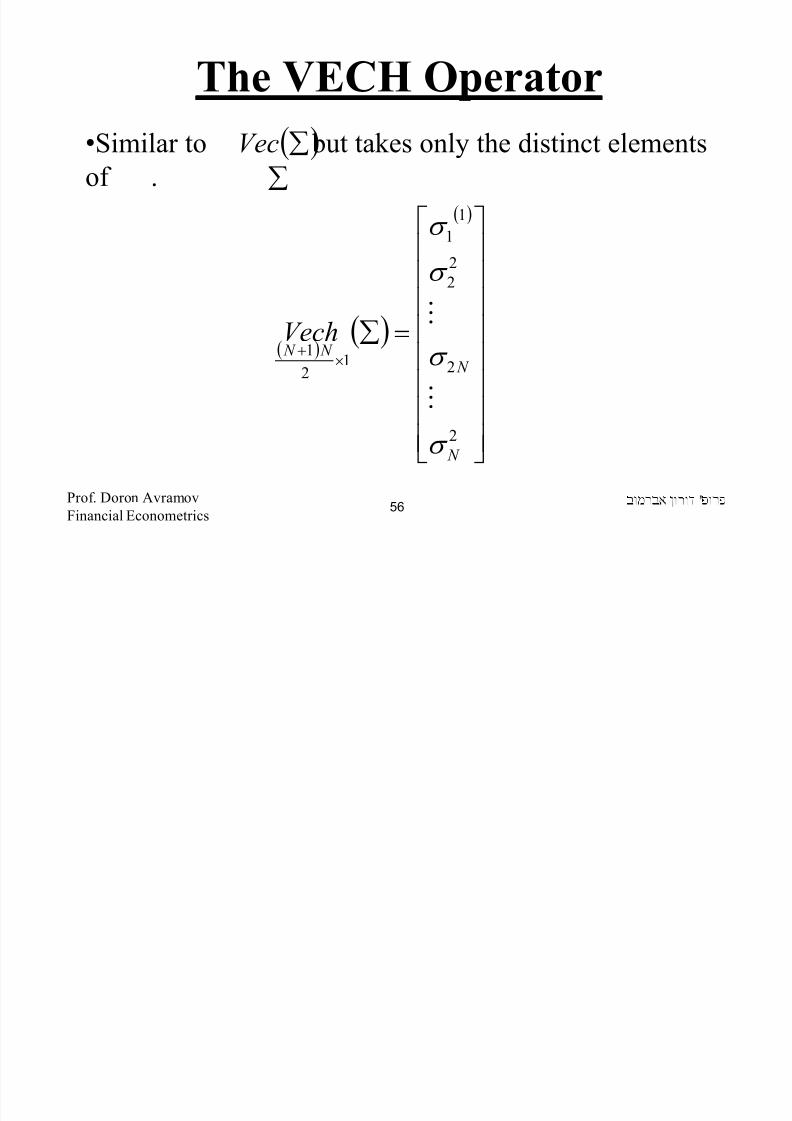

The VECH Operator

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 56/553

The VECH Operator

•Similar to but takes only the distinct elements

of .

'Prof. Doron AvramovFinancial Econometrics

56

( )( )

( )

=∑×

+

2

2

2

2

1

1

12

1

N

N N N

Vech

σ

σ

σ

σ

M

M

( )∑Vec

∑

Partitioned Matrices

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 57/553

•A, a square nonsingular matrix, is partitioned as

•Then the inverse of A is given by

•Check that

'Prof. Doron AvramovFinancial Econometrics

57

=

××

××

2212

2111

2221

1211

,

,

mmmm

mmmm

A A

A A

A

( ) ( )

( )

−−−

−−−=

−−−

−−−−

12

1

112122

1

2122121121

1

22

22

1

12

1

21221211

1

212212111

,

,

A A A A A A A A A A

A A A A A A A A A A A

( )21

1

mm I A A +− =⋅

Matrix Differentiation

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 58/553

• Y is an M -vector. X is an N -vector. Then

• Let

'Prof. Doron AvramovFinancial Econometrics

58

∂∂

∂∂

∂∂

∂∂

∂∂

∂∂

=∂∂

×

N

M M M

N

N M

X

Y

X

Y

X

Y

X

Y

X

Y

X

Y

X

Y

,,,

,,,

21

1

2

1

1

1

K

M

K

A X

Y =

∂∂

11 ×××=

N N M M X AY

Matrix Differentiation

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 59/553

Matrix Differentiation

• Let

'Prof. Doron AvramovFinancial Econometrics

59

''

'

A X Y

Z

AY X

Z

=∂∂

=∂∂

11'

×××=

N N M M X AY Z

Matrix Differentiation

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 60/553

Matrix Differentiation

• Let

• If C is symmetric, then

'Prof. Doron AvramovFinancial Econometrics

60

( )'' C C X

X

+=

∂

∂θ

11'

×××=

N N N N X C X θ

C X X

'2=∂∂θ

Kronecker Product:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 61/553

•It is given by

g pmnmg np B AC ××× ⊗=

=×

Ba Ba

Ba BaC

nmn

m

mg np

,

,

1

111

KKKKK

KKKKKKKKK

KKKKK

'Prof. Doron AvramovFinancial Econometrics

61

Kronecker Product:

Kronecker Product:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 62/553

For A,B square matrices, it follows that

'Prof. Doron AvramovFinancial Econometrics62

( )

( )( ) ( ) BD AC DC B A

B A B A

B A B A N M

N N M M

⊗=⊗⊗

=⊗⊗=⊗

××

−−− 111

Operations on Matrices

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 63/553

Operations on Matrices

'Prof. Doron AvramovFinancial Econometrics63

[ ][ ] [ ]

)')((),(

)(')'()'(

)'()'(

)()''()()()()(

)()()(

)()()(

µ µ µ

µ µ

−−=Σ=

Σ+===

=

= +=+

+=+=⊗

X X E X E

where

Atr A A XX E tr A XX tr E

AX X tr E AX X E

Avec Bvec ABtr Bvech Avech B Avech

Bvec Avec B Avec

Btr Atr B Atr

Using Matrix Notation in a Portfolio

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 64/553

The expectation and the variance of a portfolio’s rate of

return in the presence of three stocks are formulated as

ω ω

ρ σ σ ω ω ρ σ σ ω ω ρ σ σ ω ω

σ ω σ ω σ ω σ

µ ω µ ω µ ω µ ω µ

∑=

+++++=

=++=

'

222

'

233232133131122121

23

23

22

22

21

21

2

332211

p

p

'Prof. Doron AvramovFinancial Econometrics64

Choice Context

Using Matrix Notation in a Portfolio

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 65/553

where

=×

3

2

1

13

ω

ω

ω

ω

=∑×

2

33231

23

2

221

1312

2

1

33

,,

,,

,,

σ σ σ

σ σ σ

σ σ σ

=×

3

2

1

13

µ

µ

µ

µ

'Prof. Doron AvramovFinancial Econometrics 65

Choice Context

The Expectation, Variance, and

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 66/553

Covariance of Sum of RandomVariables

)()()()( z cE ybE xaE cz byax E ++=++

'Prof. Doron AvramovFinancial Econometrics 66

),(2),(2),(2

)()()()( 222

z ybcCov z xacCov y xabCov

z Var c yVar b xVar acz byaxVar

+++

++=++

),(),(),(),(),(

w ybdCov z ybcCovw xadCov z xacCovdwcz byaxCov

+++=++

Law of Iterated Expectations (LIE)

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 67/553

Law of Iterated Expectations (LIE)

• The LIE relates the unconditional expectation of a

random variable to its conditional expectation via the

formulation

• Paul Samuelson shows the relation between the LIE andthe notion of market efficiency – which loosely speaking

asserts that the change in asset prices cannot be predicted

using current information.

Prof. Doron AvramovFinancial Econometrics

[ ] [ ] X Y E E Y E x |=

'67

LIE and Market Efficiency

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 68/553

LIE and Market Efficiency

• Under rational expectations, the time t security

price can be written as the rational expectation of

some fundamental value, conditional on informationavailable at time t :

• Similarly,• The conditional expectation of the price change is

• The quantity does not depend on the information.

][| ** P E I P E P t t t ==

Prof. Doron AvramovFinancial Econometrics

][|

*

11

*

1 P E I P E P t t t +++ ==

0][][]|[**

11 =−=− ++ P E P E E I P P E t t t t t t

'68

Variance Decomposition (VD)

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 69/553

Variance Decomposition (VD)

• Let us decompose :

• Shiller (1981) documents excess volatility in the

equity market. We can use VD to prove it:

• The theoretical stock price:

based on actual future dividends

• The actual stock price:

[ ] yVar

[ ] ( )[ ] ( )[ ] x yVar E x y E Var yVar x x || +=

t t t I P E P *=

( )LL

2

21*

11 r

D

r

D P t t

t +

++

= ++

'Prof. Doron AvramovFinancial Econometrics 69

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 70/553

Variance Decomposition

What do we observe in the data? The opposite!!

t t t t t I P Var E I P E Var P Var *** +=

[ ] positive P Var P Var t t +=* positive

[ ]t t P Var P Var >*

'Prof. Doron AvramovFinancial Econometrics 70

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 71/553

Lecture Notes in Financial

Econometrics

Taylor Approximations inFinancial Economics

'Prof. Doron Avramov

Financial Econometrics 71

TA in Finance

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 72/553

• Several major applications in finance require the use of

Taylor series approximation.

• See three applications in the following table.

• We will also derive a test statistic for the Sharpe ratio –

the price of risk – which is based on the delta method,

which in turn is using the first order Taylor

approximation.

'Prof. Doron Avramov

Financial Econometrics 72

TA in Finance: Major

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 73/553

Applications

'Prof. Doron Avramov

Financial Econometrics 73

Expected Utility Bond Pricing Option Pricing

First Oder Mean Duration Delta

Second Order Volatility Convexity Gamma

Third Order Skewness

Fourth Order Kurtosis

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 74/553

Taylor Approximation• Taylor series is a representation of a function as

an infinite sum of terms that are calculated from

the values of the function's derivatives at a single

point.

• Taylor approximation is written as:

• It can also be written with notation:

....))((!3

1))((

!2

1))((

!1

1)()( 3

00

'''2

00

''

00

'

0 +−+−+−+= x x x f x x x f x x x f x f x f

( )∑∞

=−=

0 00

!

)()(

n

nn

x xn

x f x f

∑

'Prof. Doron Avramov

Financial Econometrics 74

Maximizing Expected Utility of

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 75/553

Terminal Wealth

).1)......(1)(1(1

)1(

21 K T T T

T K T

R R R Rwhere

RW W

+++

+

+++=+

+=

The invested wealth is

The investment horizon is K periods.

The terminal wealth, the wealth in the end of the investment

horizon, is

T W

'Prof. Doron Avramov

Financial Econometrics 75

Transforming to Log Returns

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 76/553

)1ln(

.....

)1ln(

)1ln(

22

11

K T K T

T T

T T

Rr

Rr

Rr

++

++

++

+=

+=

+=

'Prof. Doron Avramov

Financial Econometrics 76

Power utility as a Function of

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 77/553

• Assume that the investor has the power utility function

of the from

• The cumulative log return (CLR) over the investment

horizon is:

• The terminal wealth as a function of CLR is

'Prof. Doron Avramov

Financial Econometrics 77

K T K T W W u ++ =γ

γ

1)(

K T T T r r r r +++ +++= ...21

)exp()1( r W RW W T T K T =+=+

Log Return

Power utility as a Function of

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 78/553

• Then the utility function of terminal wealth can be

expressed as a function of CLR

• We can use the TA to express the utility as a function

of the moments of CLR.

• That is, we will approximate around

'Prof. Doron Avramov

Financial Econometrics 78

)exp(11

)( r W W W u T k T K T γ γ γ

γ γ == ++

)( K T W u + )(r E =µ

Log Return

The Utility Function

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 79/553

'Prof. Doron Avramov

Financial Econometrics 79

])(24

1)(

6

1

)(2

11)[exp()]([

....))(exp(24

1

))(exp(6

1))(exp(

2

1

))(exp()exp()(

43

2

44

3322

γ γ

γ µγ γ

γ µ µγ

γ µ µγ γ µ µγ

γ µ µγ γ

µγ γ

γ

γ γ

r Kur r Ske

r Var W

W u E

r

r r

r W W

W u

T K T

T T K T

+

++≈

+−+

−+−+

−+=

+

+

Approximation

Expected Utility

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 80/553

Let us assume that log return is normally distributed:

The exact solution under normality is

[ ]

++≈⋅

== →

4422

42

821)exp(:

3,0),(~

σ γ σ γ γµ γ

σ σ µ

γ T W E Then

Kur Ske N r

'Prof. Doron Avramov

Financial Econometrics 80

[ ]

+=⋅ 2

2

2

exp σ γ

γµ

γ

γ

T W E

Taylor Approximation – Bond Pricing

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 81/553

• Taylor approximation is also used in bond pricing.

• The bond price is:

where y0 is the yield to maturity.

• Assume that y0 changes to y1

• The delta (the change) of the yield to maturity is written

as:

( )∑ =

+

=n

i i

i

y

CF y P

1

0

0

1

)(

01 y y y −=∆

'Prof. Doron Avramov

Financial Econometrics 81

Changes in Yields and Bond

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 82/553

Pricing• Using Taylor approximation we get

2

010

''

010

'

01

))((!2

1))((

!1

1)()( y y y P y y y P y P y P −+−+≈

2

010

''

010

'

01 ))((!2

1))((!11)()( y y y P y y y P y P y P −+−≈−⇒

'Prof. Doron Avramov

Financial Econometrics 82

Duration and Convexity

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 83/553

• Dividing by P(y0 ) yields

•Instead of: we can write “-MD”

(Modified Duration).

•Instead of: we can write “Con”(Convexity).

)(2

)(

)(

)(

0

2

0

''

0

0

'

y P

y y P

y P

y y P

P

P ∆⋅+

∆⋅≈

∆

)(

)(

0

0

'

y P

y P

)()(

0

0

''

y P y P

'Prof. Doron Avramov

Financial Econometrics 83

The Approximated Bond Price

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 84/553

Change• It is given by

• What if the yield to maturity falls?

2

2 yCon y MD

P

P ∆⋅+∆⋅−≈

∆

'Prof. Doron Avramov

Financial Econometrics 84

The Bond Price Change when

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 85/553

• The change of the bond price is:

• According to duration - bond price should increase.

• According to convexity - bond price should also

increase.• Indeed, the bond price rises.

2

2 yCon y MD

P

P ∆⋅+∆⋅−=∆

'Prof. Doron Avramov

Financial Econometrics 85

Yields Fall

The Bond Price Change when

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 86/553

• And what if the yield to maturity increases?

• Again, the change of the bond price is:

• According to duration – the bond price should

decrease.

2

2 yCon y MD

P

P ∆⋅+∆⋅−=

∆

'Prof. Doron Avramov

Financial Econometrics 86

Yields Increase

The Bond Price Change when

Yi ld I

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 87/553

• According to convexity - bond price should increase.

• So what is the overall effect?

• Notice: the influence of duration is always stronger

than that of convexity as the duration is a first order effect while the convexity is second order.

'Prof. Doron Avramov

Financial Econometrics 87

Yields Increase

Option Pricing

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 88/553

• A call price is a function of the underlying asset price

• What is the change in the call price when the

underlying asset pricing changes?

• Focusing on the first order term – this establishes the

delta neutral trading strategy.

( ) ( )

( ) ( )2

2

2

2

2

1)(

2

1

)()(

t st st

t st st s

P P P P P C

P P P

C

P P P

C

P C P C

−Γ+−∆+≈

−∂

∂

+−∂

∂

+≈

'Prof. Doron Avramov

Financial Econometrics 88

Delta Neutral Strategy

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 89/553

Suppose that the underlying asset volatility increases.

Suppose further the implied volatility lags behind.

The call option is then underpriced – buy the call.

However, you take the risk of fluctuations in the price

of the underlying asset.

To hedge that risk you sell Delta units of theunderlying asset.

'Prof. Doron Avramov

Financial Econometrics 89

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 90/553

Lecture Notes in Financial

Econometrics

OLS, MLE, MOM

'Prof. Doron Avramov

Financial Econometrics 90

Ordinary Least Squares (OLS)

h l i i h i

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 91/553

• The goal is to estimate the regression parameters.

• Using optimization can help us reach the goal.

• Consider the regression:

, ,

∑=

=

−=

+=

T

T

t

t t t

t t t

f

x y

x y

1

2

)( ε

β ε

ε β

β

=

T y

y

Y .

1

=

KT T

K

x x

x x

X

,,,1

,,,1

1

111

K

KKKKK

K

=

T

E

ε

ε

.

1

'Prof. Doron Avramov

Financial Econometrics 91

• First Order Conditions

L t d i th f ti ith t t b t d

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 92/553

• Let us derive the function with respect to beta and

make the derivative equal to zero

• Recall: X and Y are observations based on real data.

• Could we choose other to obtain smaller

Y X X X

Y X X X f

'1'

'')(

)(ˆ

02)(2

−=

=−=∂

∂

β

β β β

β ∑=

=T

T

t E E 1

2' ε

'Prof. Doron Avramov

Financial Econometrics 92

• o! Because the optimization minimizes the quantity

The OLS Estimator

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 93/553

.

• We know:

• Is the estimator unbiased for ?

, So – it is indeed unbiased.

E X X X

E X X X X X X X E X X X X E X Y

'1'

'1''1'

'1'

)(ˆ

)()(ˆ)()(

ˆ

−

−−

−

+=

+=+=→+=

β β

β β β β β

β β

[ ][ ] 0)(

)(

ˆ

'1'

'1'

==

=

−

−

−

E E X X X

E X X X E

E β β

E '

'Prof. Doron Avramov

Financial Econometrics 93

• What about the Standard Error of ?β

The Standard Errors of the OLS Estimates

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 94/553

• What about the Standard Error of ?

• Reminder:

β

( ) ( )

−⋅−=

'ˆˆ)ˆ( β β β β β E VAR

( ) 1'''

'1'

)(ˆ

)(ˆ

−

−

=−

=−

X X X E

E X X X

β β

β β

'Prof. Doron Avramov

Financial Econometrics 94

Continuing:

The Standard Errors of the OLS Estimates

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 95/553

where K is the number of explanatory variables in

the regression specification.

[ ]

E E K T

X X X X X X X EE E X X X

X X X EE X X X E

ˆˆ1

1ˆ

ˆ)(ˆ

ˆ)()()(

)()(

'2

21'

21'1'''1'

1'''1'

−−=

=∑=

=

−

−−−

−−

ε

ε β

ε

σ

σ σ

'Prof. Doron Avramov

Financial Econometrics 95

MLE

• We next turn to resorting to Maximum Likelihood as a

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 96/553

• We next turn to resorting to Maximum Likelihood as a

powerful tool for both estimating regression parameters

as well as testing models.

• The MLE is an asymptotic procedure and it a

parametric approach in that the distribution of the

regression residual must be specified explicitly.

'Prof. Doron Avramov

Financial Econometrics 96

Implementing MLE

A h ( )2N

iid

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 97/553

• Assume that

• Let us estimate and using MLE; then derive

the joint distribution of these estimates.

• Under normality, the probability distribution

function ( pdf ) of the rate of return takes the form

( )2,~ σ µ N r t

µ 2σ

( )

−−=

2

2

2 2

1exp

2

1)(

σ

µ

πσ

t t

r r pdf

'Prof. Doron Avramov

Financial Econometrics 97

The Joint Likelihood

( ) ( ) ( ) ( )rpdfrrrpdfrrrpdfrrrpdfL ×××== 322121

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 98/553

• Since stock returns are assumed iid - it follows that

• Now take the natural log of the joint likelihood:

( ) ( ) ( )

( )

−

−=

×××=

∑=

−T

T

t T

T

r L

r pdf r pdf r pdf L

1

2

22

21

2

1exp2

σ

µ πσ

K

( ) ( ) ∑=

−−−−=

T

t

t r T T L1

2

2

21ln

22ln

2ln

σ µ σ π

( ) ( ) ( ) ( )T T T T r pdf r r r pdf r r r pdf r r r pdf L ×××== KKKK 322121 ,,,

'Prof. Doron Avramov

Financial Econometrics 98

MLE: Sample Estimates

• Derive the first order conditions

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 99/553

• Derive the first order conditions

Since - the variance estimator is not

unbiased.

( )( )∑ ∑

∑∑

= =

==

−=→=−

+−=

∂

∂

=→=

−

=∂

∂

T

t

T

t

t t

T

t t

T

t

t

r

T

r T L

r T

r L

1 1

22

4

2

22

112

ˆ1

ˆ0

2

ln

1

ˆ0

ln

µ σ

σ

µ

σ σ

µ σ

µ

µ

22ˆ σ σ ≠ E

'Prof. Doron Avramov

Financial Econometrics 99

MLE: The Information Matrix

• Take second derivatives:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 100/553

• Take second derivatives:

( )

( )

( )

∑

∑

∑

=

=

=

−=

∂

∂→

−−=

∂

∂

=

∂∂

∂→

−−=

∂∂

∂

−=

∂

∂

→−=−=∂

∂

T

t

t

T

t

t

T

t

T L E

r T L

L E

r L

T L

E

T L

1422

2

4

2

422

2

1

2

2

42

2

21

2

2

222

2

2

ln

2

ln

0lnln

ln1ln

σ σ

σ

µ

σ σ

σ µ σ

µ

σ µ

σ µ σ σ µ

'Prof. Doron Avramov

Financial Econometrics 100

MLE: The Covariance Matrix

• Set the information matrix ∂= ln)(2

θ LEI

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 101/553

• Set the information matrix

• Then the asy. distribution of the parameters is

In our context, the information matrix is derived as

∂∂∂−=

'ln)(θ θ

θ L E I

→

→

−

−−

T

T

T

T

T

T INVERSE MULTIPLY

4

2

4

2"1"

4

2

2,0

0,

2,0

0,

2,0

0,

σ

σ

σ

σ

σ

σ

( )1)(,0~

−∧

− θ θ θ I N T

'Prof. Doron Avramov

Financial Econometrics 101

To Summarize

•The asy distribution of the parameters is

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 102/553

The asy. distribution of the parameters is

In our context, the joint distribution of the sample

mean and variance assuming IID normal is

( )1)(,0~

−∧

− θ θ θ I N T

−−

−

∑∑

∑

==

=

4

2

2

11

2

1

2,0

0,,

0

0~

)1(1

1

σ

σ

σ

µ

N

r T

r T

r T

T T

t

t

T

t

t

T

t

t

'Prof. Doron Avramov

Financial Econometrics 102

The Sample Mean and Variance

• Notice that when returns are normally distributed –

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 103/553

Notice that when returns are normally distributed

the sample mean and variance are independent.

• That would not be the case otherwise.

• Departing from normality, the covariance between the

sample mean and variance is the skewness (see below).• Notice also that the ratio obtained by dividing the

variance of the variance by the variance of the mean is

smaller than one as long as volatility is below 70%.

• Clearly, the mean return estimate is more noisy.'Prof. Doron Avramov

Financial Econometrics 103

Departing from Normality:

Setting Moment Conditions

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 104/553

Setting Moment Conditions• We know:

• If:

•Then:

• That is, we set two momentum conditions.

( )

( )22

σ µ

µ

=−

=

t

t

r E

r E

( )( )

−−

−=

22σ µ

µ θ

t

t

t r

r g

( )

=

0

0t g E

'Prof. Doron Avramov

Financial Econometrics 104

Method of Moments (MOM)

• There are two parameters: 2σµ

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 105/553

There are two parameters:

• Stage 1: Moment Conditions

• Stage 2: estimation

,σ µ

( )

−−−=

22σ µ

µ

t

t

t r

r g

01

1

^

=∑=

T

t

t g T

'Prof. Doron Avramov

Financial Econometrics 105

Method of Moments

• Continue estimation:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 106/553

Continue estimation:

( )

( )[ ]

( )∑

∑

∑

∑

=

=

=

−=

=−−

=

=−

T

t

t

T

t

t

T

t

t

t

r

T

r T

r T

r

T

1

22

1

22

1

ˆ1

ˆ

0ˆˆ1

1ˆ

0ˆ1

µ σ

σ µ

µ

µ

'Prof. Doron Avramov

Financial Econometrics106

T t ,,1 K=

MOM: Stage 3

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 107/553

)'

t t g g E S =

− 4

43

3

2

,

,

σ µ µ

µ σ

( ) ( ) ( )( ) ( ) ( ) ( )

+−−−−−−

−−−−=

422423

232

2,

,

σ µ σ µ µ σ µ

µ σ µ µ

t t t t

t t t

r r r r

r r r E S

'Prof. Doron Avramov

Financial Econometrics107

MOM: stage 4

M

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 108/553

• Memo:

• Stage 4: derive wrt and take the expected

value

( )( )

−−

−=

22σ µ

µ θ

t

t

t r

r g

( )θ t g θ

( )( )

−

−=

−−−

−=

∂∂=

1,0

0,1

1,2

0,1

µ θ

θ

t

t

r E

g E D

'Prof. Doron Avramov

Financial Econometrics108

MOM: The Covariance Matrix

Stage 5:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 109/553

g

( )S

DS D

=∑

=∑−−

θ

θ

11'

'Prof. Doron Avramov

Financial Econometrics109

The Covariance Matrices

=∑21 0,σ

θ =∑ 322 ,µ σ θ

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 110/553

∑42,0 σ

θ

−

∑4

43, σ µ µ θ

• Sample estimates of the Skewness and Kurtosis are

3

3 σ µ ×== sk SK

( )∑=

−=T

t

t r r T 1

3

3

1µ ( )∑

=

−=T

t

t r r T 1

4

4

1µ

sk is the skewness of the standardized

return

kr is the kurtosis of the standardizedreturn

4

4 σ µ ×== kr KR

110

Under Normality the MOM Covariance

Matrix Boils Down to

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 111/553

1

44

43

32

2

2,0

0,θ θ

σ σ µ µ

µ σ Σ=

=−===∑

'Prof. Doron Avramov

Financial Econometrics111

MOM: Estimating Regression Parameters

• Let us run the time series regression

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 112/553

• There are two moment conditions:

t mt t r r ε α +⋅+=

( )

( ) 0

0

=

=

t mt

t

r E

E

ε

ε

( )( )[ ]

[ ][ ]',',1

'

β α θ

θ

β α

β α

==

−=

⋅−−

⋅−−=

mt t

t t t

mt mt t

mt t

t

r x

xr x

r r r

r r g

'Prof. Doron Avramov

Financial Econometrics112

MOM: Estimating Regression Parameters

• Estimation:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 113/553

( )

=

=

=

=−

×

−

=

−

=

==

∑∑∑∑

mT

m

T

T

t

t t

T

t

t t

T

t

t t

T

t

t t

r

r

X

R X X X r x x x

x xT

r xT

,1

,1

011

1

2

'1'

1

1

1

'^

1

^'

1

KK

θ

θ

=

T r

r

R K

1

'Prof. Doron Avramov

Financial Econometrics113

MOM: Estimating Standard Errors

• Estimation of the covariance matrix

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 114/553

T

X X

x xT

g

T D

x xT g g T S

t

T

t t

T

t

t

T

t t

T

t

t t

T

t

t T

'

)'(

1)(1

ˆ)'(

1

)'()(

1

11^

^

2

1

^

1

^

−=−=∂

∂

=

==

∑∑

∑∑

==

==

θ

θ

ε θ θ

'Prof. Doron Avramov

Financial Econometrics114

MOM: Estimating Standard Errors

• The covariance matrix estimate is thus

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 115/553

•Then, asymptotically we get

1

1

21

11

)'(ˆ)'()'(

)'(

−

=

−

−−

=Σ

=Σ

∑ X X x x X X T

DS DT

t

t t t

T T T

ε θ

θ

'Prof. Doron Avramov

Financial Econometrics115

),0(~)(^

θ θ θ Σ− N T

Lecture Notes in Financial

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 116/553

Lecture Notes in Financial

Econometrics

Hypothesis Testing

'Prof. Doron Avramov

Financial Econometrics116

Overview

A short brief of the major contents for today’s class:

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 117/553

• Hypothesis testing

• TESTS: Skewness, Kurtosis, Bera-Jarque

• A first step to testing asset pricing models

• Deriving test statistic for the Sharpe ratio

'Prof. Doron Avramov

Financial Econometrics117

Hypothesis Testing

• Let us assume that a mutual fund invests in value

t k ( t k ith hi h ti f b k t k t)

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 118/553

stocks (e.g., stocks with high ratios of book-to-market).

• Performance evaluation is mostly about running theregression of excess fund returns on the market premium

• The hypothesis testing for examining performance is

H0

: means no performanceH1: Otherwise

it

e

mt ii

e

it R R ε β α ++=

=iα

'Prof. Doron Avramov

Financial Econometrics118

Hypothesis Testing

• Errors emerge if we reject H 0 while it is true, or whend t j t H h it i

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 119/553

we do not reject H 0 when it is wrong:

Reject H0Don’t

reject H0

Type 1

error

Good

decisionH0

Good

decision

Type 2 error H1

α True state

of world

'Prof. Doron Avramov

Financial Econometrics119

Hypothesis Testing - Errors

• is the first type error (size), while is the secondtype error (related to power)

α β

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 120/553

type error (related to power).

• The power of the test is equal to 1- .

• We would prefer both and to be as small as

possible, but there is always a trade-off.

• When decreases increases and vice versa.

•The implementation of hypothesis testing requires the

knowledge of distribution theory.

β

α

α β

'Prof. Doron Avramov

Financial Econometrics120

Skewness, Kurtosis & Bera

Jarque Test Statistics

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 121/553

q

• We aim to test normality of stock returns.

• We use three distinct tests to examine normality.

'Prof. Doron Avramov

Financial Econometrics121

• TEST 1 - Skewness (third moment)

Test I – Skewness

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 122/553

• The setup for testing normality of stock return:

H0:

H1: otherwise

• Sample Skewness is

( 2,~ σ µ N Rt

∑=

−=

T

t

H t

T N

R

T S

1

36

,0~ˆ

ˆ1 0

σ

µ

'Prof. Doron Avramov

Financial Econometrics

122

• Multiplying S by we get ( )10~ NST T

Test I – Skewness

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 123/553

• Multiplying S by , we get

• If the statistic value is higher (absolute value) than thecritical value e.g., the statistic is equal to -2.31, then

reject H 0, otherwise do not reject the null of nomrality.

( )1,0~6

N S 6

'Prof. Doron Avramov

Financial Econometrics

123

TEST 2 - Kurtosis

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 124/553

• Kurtosis estimate is:

• After transformation:

∑=

−=

T

t

H t

T N R

T K 1

424

,3~ˆ

ˆ1 0

σ

µ

( ) ( )1,0~324

0

N K T

H

−

'Prof. Doron Avramov

Financial Econometrics

124

• The statistic is: ( ) ( )2~3 222 χ−+= KT

ST

BJ

TEST 3 - Bera-Jarqua Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 125/553

The statistic is:

• Why ?

( ) ( )23246

χ + K S BJ

)2(2 χ

'Prof. Doron Avramov

Financial Econometrics

125

• If X1~N(0,1) , X2~N (0,1) & then:21 XX ⊥

TEST 3 - Bera-Jarqua Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 126/553

If X 1 N(0,1) , X 2 N (0,1) & then:

• and are both standard normal and

they are independent random varaibles.

( )2~22

2

2

1 χ X X +

21 X X ⊥

S T 6 ( )324 − K

T

'Prof. Doron Avramov

Financial Econometrics

126

Chi Squared Test

• In financial economics, the Chi square test is

implemented quite frequently in hypothesis testing

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 127/553

implemented quite frequently in hypothesis testing.

• Let us derive it.

• Suppose that:

Then:

( ) ( )

( ) ( ) ( ) N R R y y

I N R y

21''

2

1

~

,0~

χ µ µ

µ

−∑−=

−∑=−

−

'Prof. Doron Avramov

Financial Econometrics

127

Testing the CAPM

• For one the chi squared is used to test the CAPM

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 128/553

• For one, the chi squared is used to test the CAPM

• There are a few tests based on time series and crosssection specifications. Let us start with the time series.

• The CAPM says that:• Thus, we first run the time-series market regressions:

)()(

e

mi

e

i R E R E β =

N

e

m N N

e

N

e

m

e

R R

R R

ε β α

ε β α

++=

++=

KKKKKKKK

1111

'Prof. Doron Avramov

Financial Econometrics

128

• The expected excess return for asset i is given by:

)()( emii

ei R E R E β α +=

Testing the CAPM

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 129/553

• According to the CAPM, the intercept i is restricted

to be zero for every test asset.

• So, the joint hypothesis test is:

• While doing the estimation, we will never get .

• Rather, we examine whether the estimate is equal to

zero statistically. For example, the sample estimate could be -- nevertheless this estimate could be

insignificant, or it is statistically equal to zero.

)(α

otherwise H

H N

:

0:

1

210 === α α α K

005.0ˆ =α

'Prof. Doron Avramov

Financial Econometrics

129

0ˆ =α

The Test Statistic

• Estimate :

=α

α .ˆ

ˆ1

α

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 130/553

• If:

and

• We get:

• Later we will develop the exact analytics of this test.

N α ˆ

( ) ( )

( )α

α

α

α α µ

∑

∑→∑

,0~ˆ

,~ˆ,~

0

N

N N R

H

( ) N

H 21'

0

~ˆˆ χ α α α

−

∑

'Prof. Doron Avramov

Financial Econometrics

130

Joint Hypothesis Test

• Y th ti i i

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 131/553

• You run the time series regression:

,22110 t t t t

x x y ε β β β +++= T t ,,2,1 K=

'Prof. Doron Avramov

Financial Econometrics

131

Joint Hypothesis Test

• We have three orthogonal conditions:( ) 0=t E ε

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 132/553

• We have three orthogonal conditions:

• Using matrix notation:

( )

( ) 0

0

2

1

=

=

t t

t t

x E

x E

ε

ε

=×

T

T

y

y

Y ..

1

1

=×

T T

T

x x

x x

x x

X

21

2212

2111

3

,,1

,,1

,,1

KKKK[ ]'32113 ,, β β β β = x

11331 ×××× += T T T E X Y

=×

T

T E

ε

ε

.

.

1

1

'Prof. Doron Avramov

Financial Econometrics

132

• Let us assume that: , are iid (2

,0~ ε σ ε N t T ε ε ε ε K

321 ,,

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 133/553

• Joint hypothesis testing:

( )( ) Y X X X

X X N '1'

21'

ˆ

,~ˆ−

−

= β

σ β β ε

otherwise H

H

:

0,1:

1

200 == β β

'Prof. Doron Avramov

Financial Econometrics

133

• Define: ,

= 1,0,0

0,0,1 R

= 0

1

q

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 134/553

• The joint test becomes:

otherwise H

q R H

H

:

0

1

1,0,0

0,0,1

:

1

2

0

2

1

0

0

0

=

=

×

=

β

β

β

β β

β

'Prof. Doron Avramov

Financial Econometrics

134

q

• Returning to the testing:

otherwise H

q R H

:

0:

1

0 =− β

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 135/553

• Under H0:

• Chi squared:

test statistic

( )',~ˆ R Rq R N q R

β β β ∑−−

( )',0~ˆ0

R R N q R H

β β ∑−

( ) ( ) ( ) ( )2~ˆˆ 21''

χ β β β q R R Rq R −∑−−

'Prof. Doron Avramov

Financial Econometrics

135

•Yet, another example:

t t t t t t t x x x x x y ε β β ++++++= 55443322110

Tt 321=

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 136/553

, ,

=×

T

T

y

y

Y .

1

1

=×

T T

T

x x

x x

X

51

5111

6

,,,1

.

.

,,,1

K

K [ ]',, 61016 β β β β K=×

=×

T

T

ε

ε

ε .

1

1

T t ,,3,2,1 K=

E X Y += β

'Prof. Doron Avramov

Financial Econometrics

136

• Joint hypothesis test:

H 7,4

1,

3

1,

2

1,1: 532100 ===== β β β β β

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 137/553

• Here is a receipt:1.

2.

3.

4.

otherwise H :

432

1

( )

( )( ) β ε

ε

σ β β

σ

β

β

∑=

⋅

−

=

−=

=

−

−

21'

'2

'1'

,~ˆ

ˆˆ

6

1ˆ

ˆˆ

ˆ

X X N

E E

T

X Y E

Y X X X

'Prof. Doron Avramov

Financial Econometrics

137

5.

=

=1

2

1

1

000100

0,0,0,0,1,00,0,0,0,0,1

qR

Joint Hypothesis Test

8/22/2019 Avramov Doron Financial Econometrics

http://slidepdf.com/reader/full/avramov-doron-financial-econometrics 138/553

5.

6.

7.

8.

9.

=

=

7

4

1

3,

1,0,0,0,0,00,0,1,0,0,0

0,0,0,1,0,0 q R

( )( )

( )( ) ( ) ( )5~ˆˆ

,0~ˆ

,~ˆ

0:

21''

'

'

0

0

0

χ β β

β

β β

β

β

β

H