August 2015! Brexit - unibocconi.itdidattica.unibocconi.it/mypage/dwload.php?nomefile=Bocconi... ·...

28

Asset Allocation in a distorted environment Only for academic purposes Pictet Asset Management EXPECTED VOLATILITY 33 Implied Volatility (Index Options) Source: Pictet Asset Management, Bloomberg August 2015! Uncertainty reduced by ‘endogenous’ Fed (unemployment doesn’t decrease, QE) and BCE’s OMT/QE Brexit

Transcript of August 2015! Brexit - unibocconi.itdidattica.unibocconi.it/mypage/dwload.php?nomefile=Bocconi... ·...

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

EXPECTED VOLATILITY

33

Implied Volatility (Index Options)

Source: Pictet Asset Management, Bloomberg

August 2015!

Uncertainty reduced by ‘endogenous’ Fed (unemployment doesn’t decrease, QE) and BCE’s OMT/QE

Brexit

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

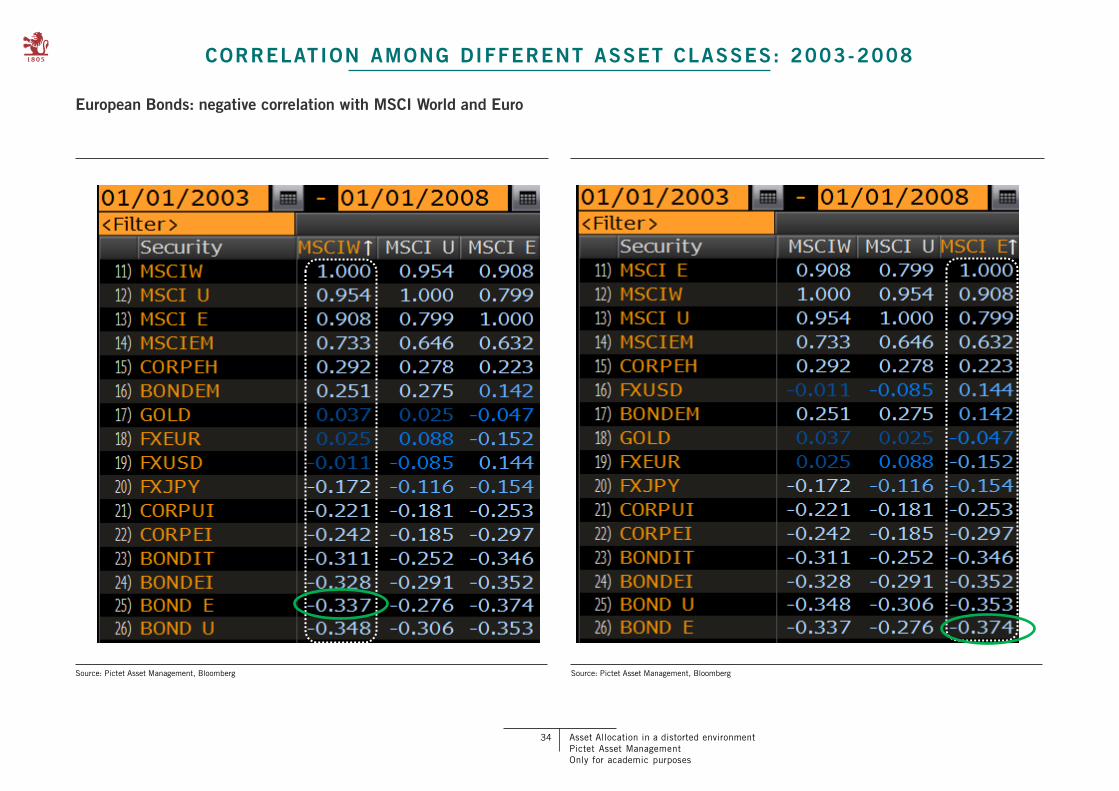

CORRELATION AMONG DIFFERENT ASSET CLASSES: 2003-2008

34

Source: Pictet Asset Management, Bloomberg Source: Pictet Asset Management, Bloomberg

European Bonds: negative correlation with MSCI World and Euro

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

CORRELATION AMONG DIFFERENT ASSET CLASSES: 2009-2012

35

Source: Pictet Asset Management, Bloomberg Source: Pictet Asset Management, Bloomberg

European Bonds: positive correlation with MSCI World and Euro

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

CORRELATION ANALYSIS

36

Weekly Correlations (on a rolling 12M window) between US TSY and MSCI US (lhs); EMU Bonds and MSCI EMU (rhs)

Source: Pictet Asset Management, Bloomberg

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

HOW TO FACE FINANCIAL REPRESSION REGIME AND TRANSITION TO NORMAL ITY?

38

Expected Risk & Return map of main financial assets (Yield to Maturity for bonds & Earing Yields for equities)

Source: Pictet Asset Management, Bloomberg, data as at 11.11.2016

Reference indices: MSCI World in USD (World Equities), Euro Stoxx in EUR (European Equities), S&P500 in USD (US Equities), MSCI Emerging Markets in USD (Emerging Equities), Euribor 3 months in EUR, BofA ML EUR Corporate Bonds in EUR (EUR Corporate Bonds), BofA

ML EUR High Yield in EUR (EUR High Yield), BofA ML Global Government Index in USD (World Government Bonds), JPM EMBI Global Diversified Composite in USD (USD Emerging Debt), German 10Y Government Bond in EUR

* The ‘Static Portfolio’ is a linear combination (ie assumes perfect correlation) based on 70% 3-5y Bond Index Barclays Euro Aggregate and 30% MSCI World in €

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

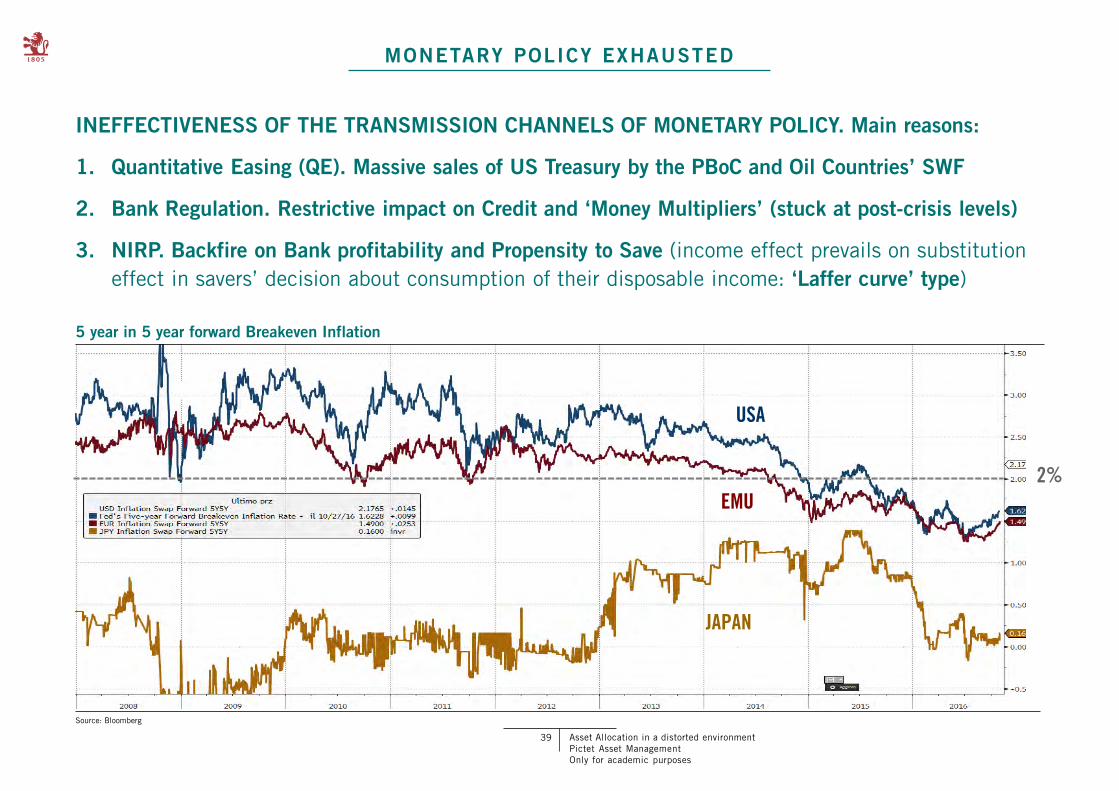

MONETARY POLICY EXHAUSTED

39

INEFFECTIVENESS OF THE TRANSMISSION CHANNELS OF MONETARY POLICY. Main reasons:

1. Quantitative Easing (QE). Massive sales of US Treasury by the PBoC and Oil Countries’ SWF

2. Bank Regulation. Restrictive impact on Credit and ‘Money Multipliers’ (stuck at post-crisis levels)

3. NIRP. Backfire on Bank profitability and Propensity to Save (income effect prevails on substitution

effect in savers’ decision about consumption of their disposable income: ‘Laffer curve’ type)

5 year in 5 year forward Breakeven Inflation

Source: Bloomberg

USA

EMU

JAPAN

2%

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

FINANCIAL REPRESSION POSES A DILEMMA TO INVESTORS

Yields to Maturity (BY) of 10 US

year government bonds are

around 2%, a low level compared

with the last 30 years of history

On the contrary, Equity

valuations, i.e. Earnings Yields

(EY) are close to historical

average

Yield compression has created a

dilemma for investors – forcing

them to choose between giving up

potential returns or increasing

their risk budget

40

US: Equities Earnings Yields at historical average; Bond Yields and MM rates much lower

Source: IBES, DATASTREAM, Bloomberg, Pictet Asset Management, as at 31.10.2016

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

JAN-99 JAN-01 JAN-03 JAN-05 JAN-07 JAN-09 JAN-11 JAN-13 JAN-15

EUR CASH EUR BONDS MSCI WORLD

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

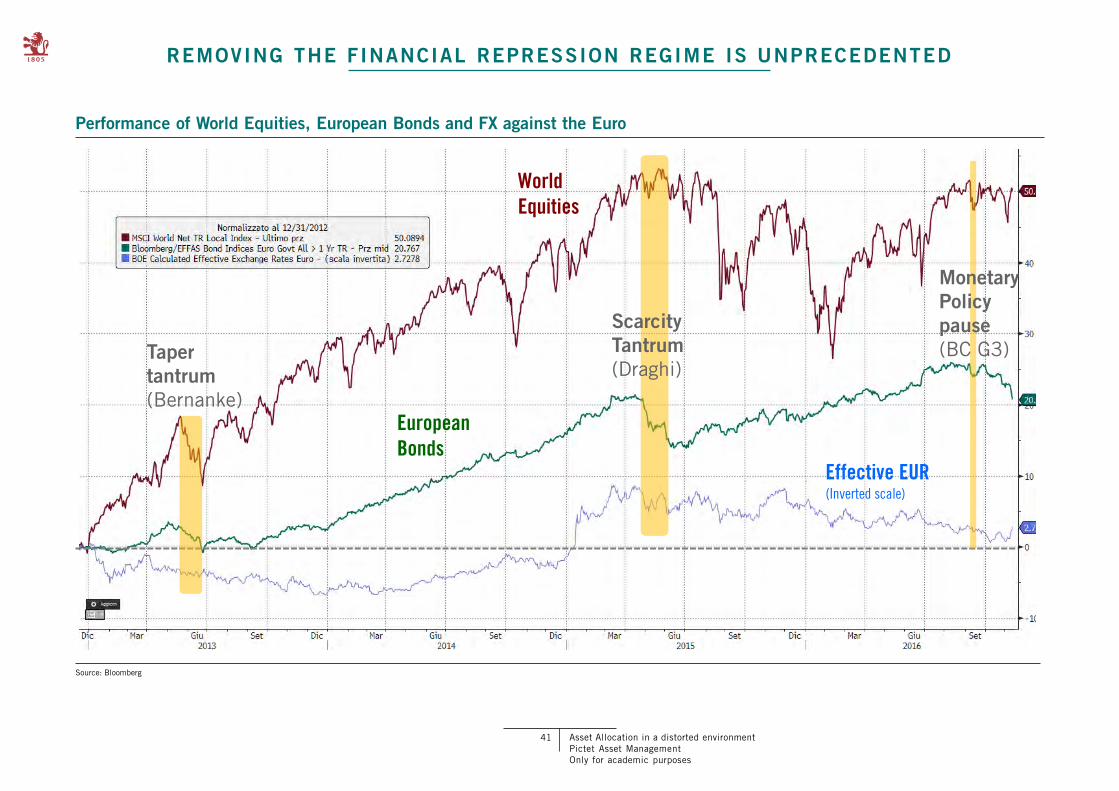

REMOVING THE FINANCIAL REPRESSION REGIME IS UNPRECEDENTED

41

Performance of World Equities, European Bonds and FX against the Euro

Source: Bloomberg

World Equities

European Bonds

Effective EUR (Inverted scale)

Taper tantrum (Bernanke)

Scarcity Tantrum (Draghi)

Monetary Policy pause (BC G3)

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

IF BONDS SUFFER FOR ‘WRONG ’ REASONS, CONTAGION AFFECTS RISKY ASSETS TOO

42

Performance of World Equities, European Bonds and FX against the Euro

Source: Bloomberg

Brexit

ECB

Trump World Equities

European Bonds

Effective EUR (Inverted scale)

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

DURATION MAGO

43

Dentsitivity of the portfolio to a rise in interest rates

Source: Pictet Asset Management, as at 11.11.2016

* Calculated assuming the actual overall duration of the portfolio (teal-colored line) was rebased on 70% of the portfolio

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

HOW TO FACE FINANCIAL REPRESSION REGIME AND TRANSITION TO NORMAL ITY?

44

Expected Risk & Return map of main financial assets (Yield to Maturity for bonds & Earing Yields for equities)

Source: Pictet Asset Management, Bloomberg, data as at 11.11.2016

Reference indices: MSCI World in USD (World Equities), Euro Stoxx in EUR (European Equities), S&P500 in USD (US Equities), MSCI Emerging Markets in USD (Emerging Equities), Euribor 3 months in EUR, BofA ML EUR Corporate Bonds in EUR (EUR Corporate Bonds), BofA

ML EUR High Yield in EUR (EUR High Yield), BofA ML Global Government Index in USD (World Government Bonds), JPM EMBI Global Diversified Composite in USD (USD Emerging Debt), German 10Y Government Bond in EUR

* The ‘Static Portfolio’ is a linear combination (ie assumes perfect correlation) based on 70% 3-5y Bond Index Barclays Euro Aggregate and 30% MSCI World in €

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

EX-ANTE VOLATILITY OF PICTET MULTI ASSET GLOBAL OPPORTUNITIES (MAGO )

45

Risk Management in Portfolio Construction

Source: Pictet Asset Management

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

5,00%

5,50%

6,00%

6,50%

SEP-13 DEC-13 MAR-14 JUN-14 SEP-14 DEC-14 MAR-15 JUN-15 SEP-15 DEC-15 MAR-16 JUN-16 SEP-16

4,18%

A sset C lass C o ntributio n to Vo lat ility (bps)

Bonds 27

Cash 26

Equities 351

Alternative 5

Commodities 9

TOTAL 418

VOLATILITY BUDGET

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

MAGO VS PEERS (3 YEARS)

46

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

Macro and Market Scenario Analysis 5.

47

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

MONETARY POLICY EXHAUSTED

48

INEFFECTIVENESS OF THE TRANSMISSION CHANNELS OF MONETARY POLICY. Main reasons:

1. Quantitative Easing (QE). Massive sales of US Treasury by the PBoC and Oil Countries’ SWF

2. Bank Regulation. Restrictive impact on Credit and ‘Money Multipliers’ (stuck at post-crisis levels)

3. NIRP. Backfire on Bank profitability and Propensity to Save (income effect prevails on substitution

effect in savers’ decision about consumption of their disposable income: ‘Laffer curve’ type)

5 year in 5 year forward Breakeven Inflation

Source: Bloomberg

USA

EMU

JAPAN

2%

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Fed Fund rate Tgt

FF avg [OIS 10Y]

Zero Curve 10Y

TP = (Zero - CDS) 10Y - FF avg [OIS 10Y]

SINCE THE CHINESE CRISIS OF 2015 TERM PREMIUMS HAVE NORMALISED

49

Term premium on T-Notes: yield to maturity - CDS - average interest rate on Fed funds for the next 10 years

Source: Pictet Asset Management, Bloomberg

Term Premium: 30bp (by difference)

T-Note: 2,35%

Expected FF: 1,65% (Estimated w FF Futures

etc.)

CDS10 on T-Note: 40bp

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

ONLY NOW, AFTER QE IS OVER ½ OF THE MOVE DUE TO THE TERM PREMIUM !

50

The Fed has contributed to the confusion with ambiguous interventions, the market has misunderstood

MONETARY

INTEREST RATES

(forward)

TERM PREMIUM

YIELD TO MATURITY Net of Credit Risk

19 April 2013 11 November 2016 change

1,62% 1,65% +3bp

-0,36% 0,30% 66bp

1,26% 1,95% 69bp

QE

Guidance*

* In December 2012 became quantitative: rate hikes were conditional

upon macro-economic objectives (Unemployment < 6,5%; inflation >

2,5%); since March 2014 Fed’s guidance is again qualitative.

TOTAL

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

MONETARY IMPULSE TRANSMISSION

Large Scale Asset Purchases (QE) extremely expansive, restrictive regulation and decreasing yields alter the relation between these values

• The traditional stable relation between monetary aggregates sharply modifies after 2008, and money (or

credit) multiplier becomes unstable. How does transmission mechanism changes? From deleverage to

restrictive regulation?

• The traditional stable relation between money and economic activity loosens: since 15 years ago velocity

of money is falling. May the preference for liquidity (even corporate) and negative rates explain the effect?

Multipliers and Speed of money circulation

Monetary Base Monetary Aggregates Nominal GDP Monetary multiplier

Velocity of money

51

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

STRUCK MULTIPLIER? QE COMPENSATED DELEVERAGE OF THE SYSTEM

Multiplier of money USA (M2/H quotient between money created by banking system via credit granted and monetary basis)

Multiplier is 1/3 of pre subprime crisis level. How much of this decrease is structural?

M2: Money created by the intermediaries’ system

H: Monetary base

m: Money multiplier

Source: Bloomberg 52

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

REGULATORY RESTRICTIONS AND MACRO-PRUDENTIAL POLICIES

Source: JP Morgan – Q2 2014

53

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

INEQUALITY, ‘LAFFER ’ EFFECT BEHIND THE RISING SAVINGS RATE IN G3

54

G3 Savings Rate (% disposable income)

Source: Pictet Asset Management, Penn World Table, CEIC, Datastream

G3 Savings Rate (% disposable income) – 3y average

Source: Pictet Asset Management, CEIC, Datastream

23

24

24

25

25

26

26

27

27

28

28

29

0

2

4

6

8

10

12

14

16

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

% d

ispo

sabl

e in

com

e

% d

ispo

sabl

e in

com

e

U.S.EURO AREAJAPAN

G5Households saving ratio (%

disposable income, 5-year average)

U.S. 6.0

Euro area 12.5

Japan 26.0Working age polulation

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

SAVING RATIOS FOR WEALTH CLASSES -> HIGHER AVERAGE SAVING RATIO ?

Source: Saez, Zucman, NBER 2014

55

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

MONETARY POLICY EXHAUSTED

56

Interest rate

GDP

LM

LM’

LM’’

IS

i

i’

i’’

Traditionally expansionary impact

Monetary Policy effectiveness is reduced…

Could fade completely with Z/NIRP

y y’ y’’

LM’’’

i’’’ y’’’

…as a Liquidity Trap unfolds

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

FISCAL POLICY

57

Interest rate

GDP

LM

IS

i

IS’

y y’

i’

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

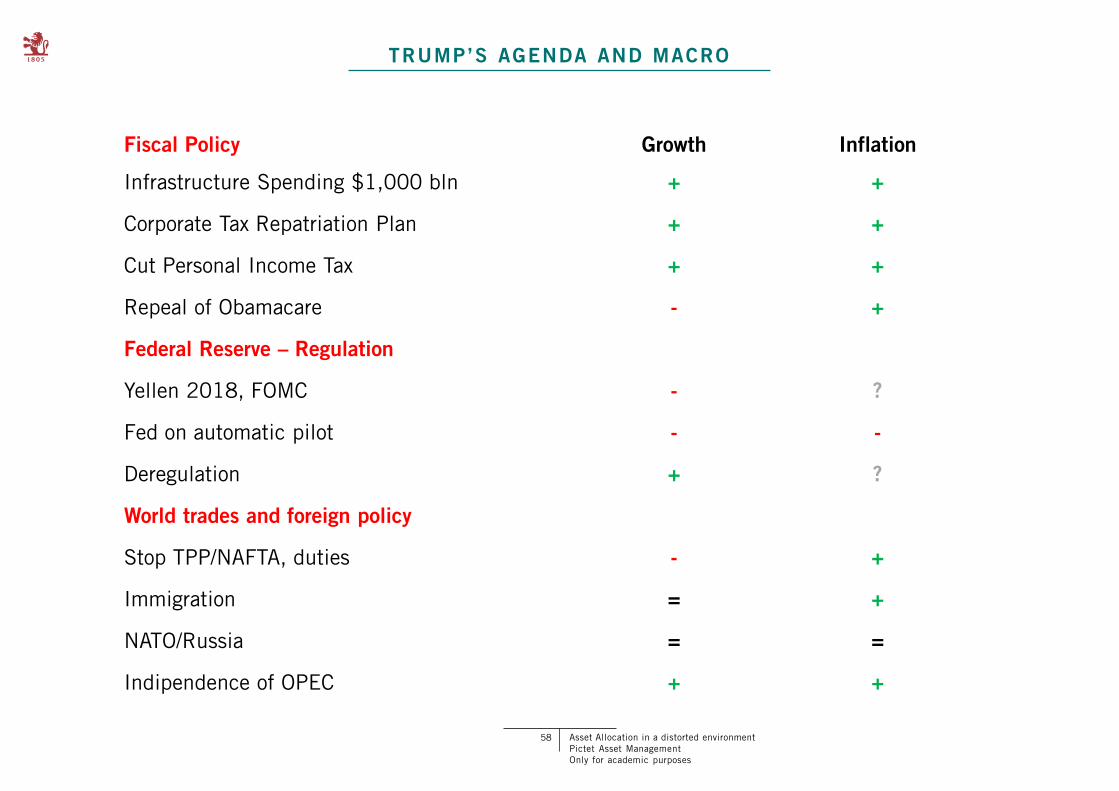

TRUMP’S AGENDA AND MACRO

58

Fiscal Policy Growth Inflation

Infrastructure Spending $1,000 bln + +

Corporate Tax Repatriation Plan + +

Cut Personal Income Tax + +

Repeal of Obamacare - +

Federal Reserve – Regulation

Yellen 2018, FOMC - ?

Fed on automatic pilot - -

Deregulation + ?

World trades and foreign policy

Stop TPP/NAFTA, duties - +

Immigration = +

NATO/Russia = =

Indipendence of OPEC + +

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

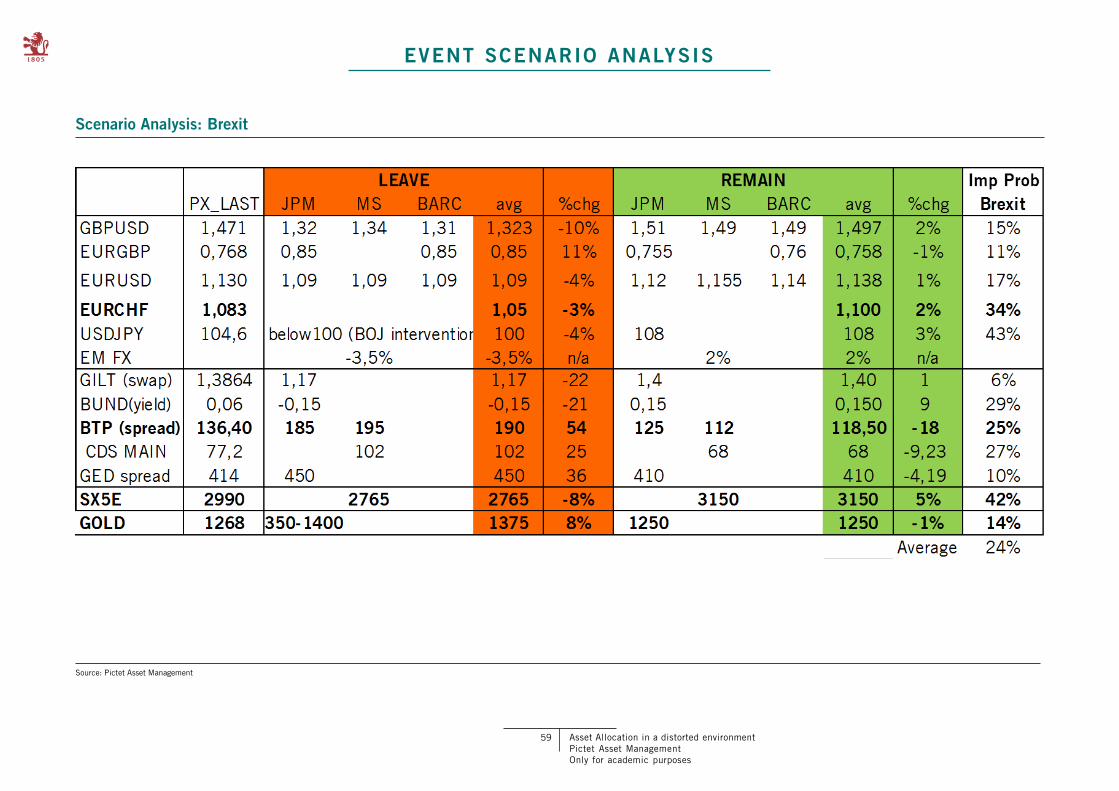

EVENT SCENARIO ANALYSIS

59

Scenario Analysis: Brexit

Source: Pictet Asset Management

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

CONCLUSIONS

60

• The benefits coming from diversification are directly proportional to the degree

of decorrelation among the investment portfolio’s assets.

• Since the subprime crisis of 2008, correlations remained relatively high

(typical during financial turmoil). On the contrary, the volatilities have

experienced a normalization.

• One of the causes of the correlations behavior is the standardization of the

investors’ behavior, affecting in particular intra-assets correlations. The

correlation between equities and bonds has been affected by the European Debt

Crisis and by the behavior of the Fed in the USA, and later many other Central

Banks adopting Quantitative Easing, that favor (at least a temporary) inversion of

the correlation sign from negative to positive.

• When there is uncertainty on the economic growth, the correlation between

equities and bonds should be ‘normal’ (negative): this could encourage holding a

longer duration.

• Because of the paucity of decorrelations, there are now less opportunities than

before. How to face this new world? Two solutions: i) Reduce your Total Return

objectives; ii) become more «aggressive» in order to reach ‘sub-optimal’ but

higher gains. Either way, we are induced to diversify through additional presence

of risky assets (equities).

In this last case, using a max Diversification portfolio (or based on Risk Parity), instead of a max Sharpe one, may hold better in the face of uncertain/unstable

correlations.

Asset Allocation in a distorted environment

Only for academic purposes

Pictet Asset Management

For more information please contact your client relationship manager.

This marketing material is

issued by Pictet Funds (Europe)

S.A. It is neither directed to,

nor intended for distribution or

use by, any person or entity

who is a citizen or resident of,

or domiciled or located in, any

locality, state, country or

jurisdiction where such

distribution, publication,

availability or use would be

contrary to law or regulation.

Only the latest version of the

fund’s prospectus, regulations,

annual and semi-annual reports

may be relied upon as the basis

for investment decisions. These

documents are available on

www.pictetfunds.com or at

Pictet Funds (Europe) S.A., 15,

avenue J. F. Kennedy L-1855

Luxembourg.

The information and data

presented in this document are

not to be considered as an offer

or solicitation to buy, sell or

subscribe to any securities or

financial instruments.

Information, opinions and

estimates contained in this

document reflect a judgment at

the original date of publication

and are subject to change

without notice. Pictet Funds

(Europe) S.A. has not taken any

steps to ensure that the

securities referred to in this

document are suitable for any

particular investor and this

document is not to be relied

upon in substitution for the

exercise of independent

judgment. Tax treatment

depends on the individual

circumstances of each investor

and may be subject to change

in the future. Before making

any investment decision,

investors are recommended to

ascertain if this investment is

suitable for them in light of

their financial knowledge and

experience, investment goals

and financial situation, or to

obtain specific advice from an

industry professional.

The value and income of any of

the securities or financial

instruments mentioned in this

document may fall as well as

rise and, as a consequence,

investors may receive back less

than originally invested. Risk

factors are listed in the fund’s

prospectus and are not

intended to be reproduced in

full in this document.

Past performance is not a

guarantee or a reliable indicator

of future performance.

Performance data does not

include the commissions and

fees charged at the time of

subscribing for or redeeming

shares. This marketing material

is not intended to be a

substitute for the fund’s full

documentation or any

information which investors

should obtain from their

financial intermediaries acting

in relation to their investment

in the fund or funds mentioned

in this document.

PICTET ASSET MANAGEMENT

60, route des Acacias

1211 Geneva 73 - Switzerland

group.pictet

61