ATWOOD OCEANICS, INC. - AnnualReports.com€¦ · THE COMPANY This Annual Report is for Atwood...

47

ATWOOD OCEANICS, INC. 2006 ANNUAL REPORT

Transcript of ATWOOD OCEANICS, INC. - AnnualReports.com€¦ · THE COMPANY This Annual Report is for Atwood...

ATWOOD OCEANICS, INC.

2006 ANNUAL REPORT

2006 ANNUAL REPORT TO SHAREHOLDERSTHE COMPANY

This Annual Report is for Atwood Oceanics, Inc. and its subsidiaries, which

are collectively referred to as “we”, “our”, or the “Company” except where stated

otherwise. We are engaged in the international offshore drilling and completion of

exploratory and developmental oil and gas wells and related support, manage-

ment and consulting services. Presently, we own and operate a premium, modern

fleet of eight mobile offshore drilling units and manage the operations of two

operator-owned platform drilling units currently located in Northwest Australia.

Since fiscal year 1997, we invested approximately $510 million in upgrading

seven mobile offshore drilling units and constructing an ultra-premium jack-up

unit, the ATWOOD BEACON. Upon its expected delivery on or before September

2008, the ATWOOD AURORA will be our ninth active mobile offshore drilling unit.

We support our operations from our Houston headquarters and offices currently

located in Australia, Malaysia, Malta, Egypt, Indonesia, Singapore and the United

Kingdom.

FINANCIAL HIGHLIGHTS

2006 2005

(In Thousands)

FOR THE YEAR ENDED SEPTEMBER 30:

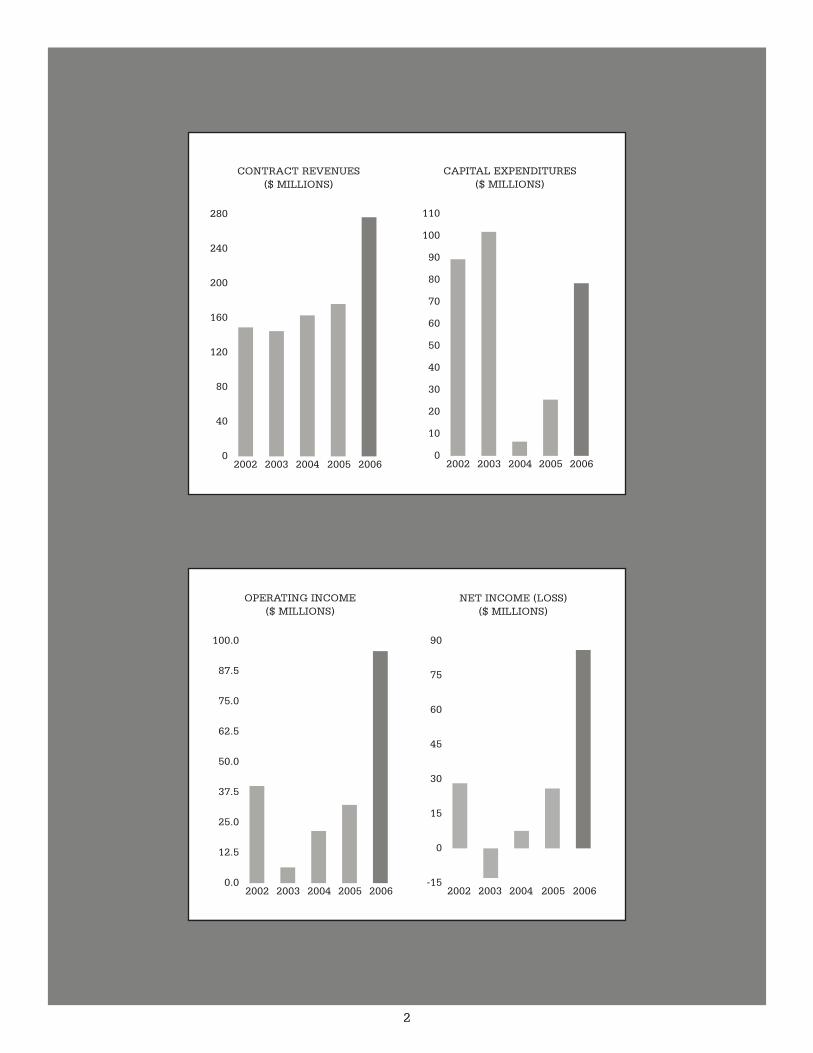

REVENUES $276,625 $176,156

NET INCOME 86,122 26,011

CAPITAL EXPENDITURES 78,464 25,563

AT SEPTEMBER 30:

NET PROPERTY AND EQUIPMENT $436,166 $390,778

TOTAL ASSETS 593,829 495,694

TOTAL SHAREHOLDERS’ EQUITY 458,894 362,137

%%TRANSMSG*** Transmitting Job: H41700 PCN: 001000000 ***%%PCMSG| |00004|Yes|No|12/19/2006 02:47|0|0|Page is valid, no graphics -- Color: D|

2

0

40

80

120

160

200

240

280

2004 2005 200620032002

0.0

12.5

25.0

37.5

50.0

62.5

75.0

87.5

100.0

2004 200520032002 2006-15

0

15

30

45

60

75

90

2004 200520032002 2006

0

10

20

30

40

50

60

70

80

90

100

110

2004 200520032002 2006

CONTRACT REVENUES($ MILLIONS)

NET INCOME (LOSS)($ MILLIONS)

CAPITAL EXPENDITURES($ MILLIONS)

OPERATING INCOME($ MILLIONS)

PRESIDENTS MESSAGE

TO OUR SHAREHOLDERS AND EMPLOYEES:

We are pleased to report revenues, operating cash flows and net income for fiscal year 2006 were thehighest in our thirty-nine year history. Our net income of $86 million, or $2.74 per diluted share, was morethan twice our previous record net income in fiscal year 1998.

Fiscal year 2006 ends with the Company in a strong position for the future. Our fleet utilization for thefiscal year was 100% and there were a number of accomplishments during the fiscal year in other key areas.Our contract backlog in terms of available rig days for our eight units, all contracted at historically highdayrates, is approximately 95% for fiscal year 2007, 80% for fiscal year 2008 and 40% for fiscal year 2009. Thiscontract backlog provides strong upside visibility for fiscal year 2007 and further upside potential beyondfiscal year 2007, particularly with our deepwater and international jack-up leverage and with the ATWOODHUNTER, ATWOOD SOUTHERN CROSS and RICHMOND contracts repricing in fiscal year 2008. Also,this year, our future visibility is enhanced with the change from well or well-to-well contracts to termcontracts on the VICKSBURG, ATWOOD HUNTER, ATWOOD FALCON, SEAHAWK and ATWOODBEACON. The ATWOOD SOUTHERN CROSS has a contract that continues into fiscal year 2008, and theATWOOD EAGLE has a two-year contract at a high dayrate, currently estimated to commence in the firstquarter of fiscal year 2009. Our new, ultra-premium jack-up, the ATWOOD AURORA, scheduled for deliveryon or before September 2008, will offer growth potential when it commences operation as our ninth ownedoffshore drilling unit. Our remaining unit, the RICHMOND, is operating in the U.S. Gulf of Mexico. TheRICHMOND has operated profitably in the Gulf of Mexico for many years.

We continue to focus daily on safe, high standards of performance, our people and the continuingdevelopment of our organization for the future. Our safety and operational performance this fiscal year hasbeen recognized by many of our clients.

The Company also continued its fleet upgrade, enhancement and new construction program during theyear with the successful completion of three shipyard update projects (the ATWOOD SOUTHERN CROSS,SEAHAWK and ATWOOD FALCON). Total expenditures of approximately $50 million for these projectsbrought our total project expenditures, since 1997, for fleet upgrade, renewal and construction completed, toover $500 million. Construction of our new, ultra-premium jack-up, the ATWOOD AURORA, also com-menced this year.

We are pleased with the Company’s current position: a strong balance sheet with a current debt to totalcapitalization ratio of approximately 12% and a continuing trend for improvements in cash flows and financialresults at historic levels. The demand by our clients for the services and equipment that our Companyprovides continues at a high level. Our strategy of focusing on safe, quality operations, premium equipment,long-standing client relationships, and being leveraged to attractive international markets has served uswell — and we believe will serve us well in the future.

We are in a position to be opportunistic, when the time is right, and, accordingly, continue to pursueand explore other future opportunities, as well as evaluating the best use of future cash flow balances.

As always, we thank our shareholders for their confidence and our employees for their many contribu-tions and achievements during fiscal year 2006, and we look forward to fiscal year 2007.

JOHN R. IRWIN

3

%%TRANSMSG*** Transmitting Job: H41700 PCN: 002000000 ***%%PCMSG|3 |00004|Yes|No|12/14/2006 11:28|0|0|Page/graphics valid 12/14/2006 11:29 -- Color: D|

4

RICHMOND

SEAHAWK

ATWOOD SOUTHERN CRO

ATWOOD HUNTER

Corporate Headquarters

Office / Shorebase

Rig

Legend

C

Malta

Great

WORLD WIDE

* Rig locations are as of December 12, 2006.

**The rig is being mobilized to India with estimated arrival before the end of December 2006.

5

ATWOOD EAGLE

VICKSBURG

ATWOOD FALCON

SS

ATWOOD BEACON**

Jakarta

Kuala Lumpur

Singapore

Perth

NORTH RANKIN ‘A’

GOODWYN ‘A’

Cairo

t Yarmouth

OPERATIONS*

6

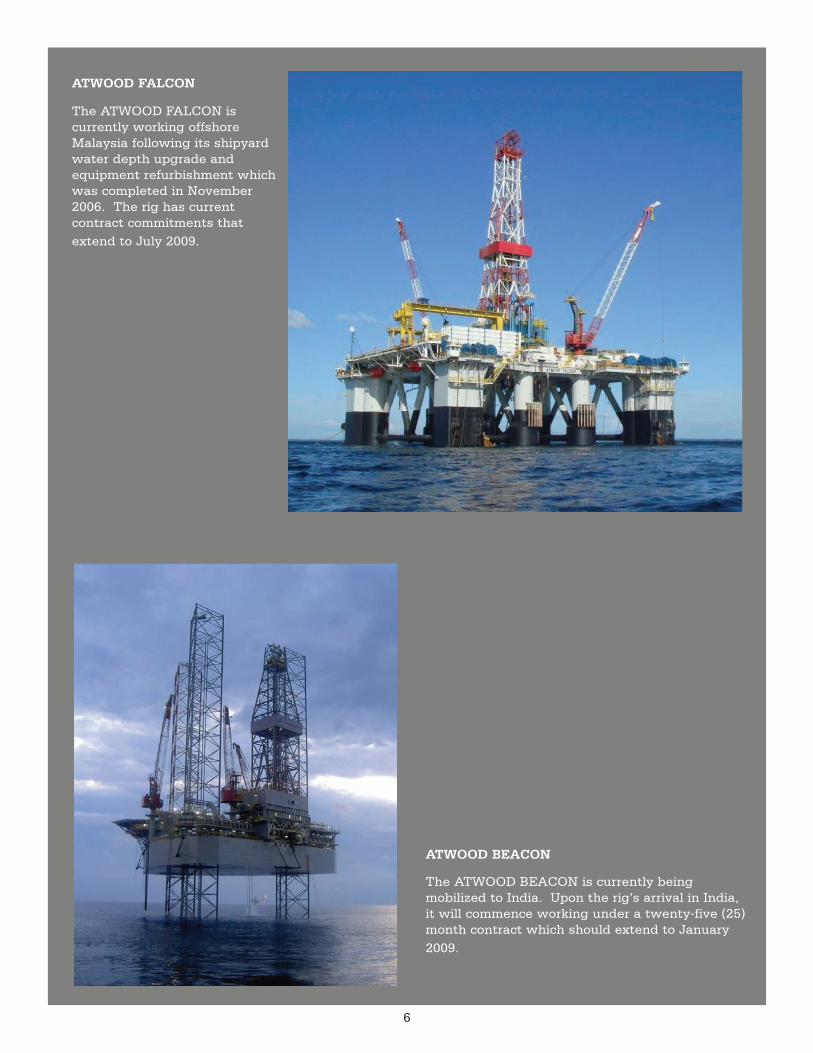

ATWOOD BEACON

The ATWOOD BEACON is currently beingmobilized to India. Upon the rig’s arrival in India,it will commence working under a twenty-five (25)month contract which should extend to January2009.

ATWOOD FALCON

The ATWOOD FALCON iscurrently working offshoreMalaysia following its shipyardwater depth upgrade andequipment refurbishment whichwas completed in November2006. The rig has currentcontract commitments thatextend to July 2009.

7

ATWOOD SEAHAWK

The SEAHAWK is currently working offshore Equatorial Guinea following its shipyard upgrade andrelocation from Southeast Asia. The rig has a current contract commitment that extends through fiscal

year 2008 and, if all options are exercised, could extend through fiscal year 2010.

Atwood Oceanics, Inc. and Subsidiaries

FIVE YEAR FINANCIAL REVIEW

(In thousands, except per share amounts, fleetdata and ratios) 2006 2005 2004 2003 2002

At or For the Years Ended September 30,

STATEMENTS OF OPERATIONS DATA:Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 276,625 $ 176,156 $163,454 $144,765 $149,157Contract drilling costs . . . . . . . . . . . . . . . . . . (144,366) (102,849) (98,936) (98,500) (75,088)Depreciation. . . . . . . . . . . . . . . . . . . . . . . . . . (26,401) (26,735) (31,582) (25,758) (23,882)General and administrative expenses . . . . . . (20,630) (14,245) (11,389) (14,015) (10,080)Gain on sale of equipment . . . . . . . . . . . . . . 10,548 — — — —

OPERATING INCOME . . . . . . . . . . . . . . . . . . 95,776 32,327 21,547 6,492 40,107Other expense . . . . . . . . . . . . . . . . . . . . . . . . (3,940) (6,719) (9,145) (4,856) (1,330)Tax (provision) benefit . . . . . . . . . . . . . . . . . . (5,714) 403 (4,815) (14,438) (10,492)

NET INCOME (LOSS). . . . . . . . . . . . . . . $ 86,122 $ 26,011 $ 7,587 $ (12,802) $ 28,285

PER SHARE DATA(1):Earnings (loss) per common share:

Basic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2.78 $ 0.86 $ 0.27 $ (0.46) $ 1.02Diluted . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2.74 $ 0.83 $ 0.27 $ (0.46) $ 1.01

Average common shares outstanding:Basic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30,936 30,412 27,718 27,692 27,678Diluted . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31,442 31,220 28,064 27,692 27,988

FLEET DATA:Number of rigs owned or managed, at end

of period . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 11 11 11 10Utilization rate for in-service rigs(2) . . . . . . . 100% 98% 93% 92% 86%

BALANCE SHEET DATA:Cash and cash equivalents . . . . . . . . . . . . . . $ 32,276 $ 18,982 $ 16,416 $ 21,551 $ 27,655Working capital . . . . . . . . . . . . . . . . . . . . . . . 86,308 35,894 32,913 26,063 43,735Net property and equipment . . . . . . . . . . . . . 436,166 390,778 401,141 443,102 368,397Total assets . . . . . . . . . . . . . . . . . . . . . . . . . . 593,829 495,694 498,936 522,674 445,238Total long-term debt (including current

portion) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64,000 90,000 181,000 205,000 115,000Shareholders’ equity(3)(4) . . . . . . . . . . . . . . . 458,894 362,137 271,589 263,467 276,133Ratio of current assets to current

liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.41 1.64 1.55 1.52 2.44

Notes —(1) Fiscal years 2005, 2004, 2003 and 2002 have been restated to reflect a two-for-one stock

split effected on March 2, 2006. See Note 7 to the consolidated financial statements forfurther discussion.

(2) Excludes managed rigs, the SEASCOUT (sold in fiscal year 2006), and contractual downtimeon rigs upgraded.

(3) We have never paid any cash dividends on our common stock.

(4) In October 2004, we sold 2,350,000 shares of common stock in a public offering.

8

%%TRANSMSG*** Transmitting Job: H41700 PCN: 003000000 ***%%PCMSG|8 |00004|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

OFF

SHO

RE

DR

ILLI

NG

OPE

RA

TIO

NS

Rig

Nam

eY

ear

Up

gra

ded

Max

imu

mW

ater

Dep

th

Per

cen

tag

eof

FY

2006

Rev

enu

es

Loc

atio

nat

Dec

emb

er12

,20

06C

ust

omer

Con

trac

tS

tatu

sat

Dec

emb

er12

,20

06

SE

MIS

UB

ME

RS

IBL

ES

—A

TW

OO

DE

AG

LE20

00/2

002

5,00

0Ft

.17

%O

ffsho

reA

ustr

alia

BH

PB

ILLI

TO

NPE

TR

OLE

UM

PTY

(‘‘B

HPB

”)

The

rig

iscu

rren

tlyw

orki

ngun

der

adr

illin

gpr

ogra

mfo

rB

HPB

whi

chco

uld

exte

nd,i

fal

lopt

ion

wel

lsar

edr

illed

,to

Nov

embe

r20

07.

Upo

nco

mpl

etio

nof

this

drill

ing

com

mit

men

t,th

eri

gha

sa

one

(1)

wel

lcon

trac

tco

mm

itm

ent

wit

hE

NI

Aus

tral

iaB

V,fo

llow

edby

atw

o(2

)ye

arco

ntra

ctco

mm

itm

ent

wit

hW

oods

ide

Ene

rgy,

Ltd.

Itsh

ould

take

unti

lDec

embe

r20

09be

fore

thes

edr

illin

gco

mm

itm

ents

are

com

plet

ed.

AT

WO

OD

HU

NT

ER

1997

/200

15,

000

Ft.

23%

Offs

hore

Mau

rita

nia

WO

OD

SID

EE

NE

RG

Y,LT

D.

(‘‘W

OO

DSI

DE

”)

The

rig

iscu

rren

tlyw

orki

ngun

der

adr

illin

gpr

ogra

mfo

rW

oods

ide

whi

chex

tend

sto

Apr

il20

08.

AT

WO

OD

FALC

ON

1998

/200

65,

000

Ft.

11%

Offs

hore

Mal

aysi

aSA

RA

WA

KSH

ELL

BE

RH

AD

(‘‘SH

ELL

”)

The

rig

iscu

rren

tlyw

orki

ngun

der

alo

ng-t

erm

drill

ing

com

mit

men

tw

ith

Shel

lwhi

chex

tend

sto

July

2009

.

AT

WO

OD

SOU

TH

ER

NC

RO

SS19

97/2

006

2,00

0Ft

.11

%O

ffsho

reTu

rkey

TO

RE

AD

OR

TU

RK

EY

LIM

ITE

D(‘‘

TO

RE

AD

OR

”)A

ND

ME

LRO

SER

ESO

UR

CE

S(‘‘

ME

LRO

SE”)

The

rig

iscu

rren

tlyw

orki

ngun

der

drill

ing

com

mit

men

tsfo

rsi

x(6

)w

ells

plus

two

(2)

opti

ons

for

Tore

ador

and

Mel

rose

whi

chco

uld

take

unti

lJul

y20

07to

com

plet

e.Fo

llow

ing

com

plet

ion

ofth

ese

com

mit

men

ts,

the

rig

has

drill

ing

com

mit

men

tsin

the

Bla

ckSe

afo

rTu

rkiy

ePe

trol

leri

A.O

.and

Van

cow

hich

coul

dex

tend

toA

pril

2008

.

CA

NT

ILE

VE

RJA

CK

-UP

S—

AT

WO

OD

BE

AC

ON

Con

stru

cted

in20

0340

0Ft

.12

%M

obili

zing

toIn

dia

GU

JAR

AT

STA

TE

PET

RO

LEU

MC

OR

POR

AT

ION

LTD

.(‘‘

GSP

C”)

The

rig

iscu

rren

tlybe

ing

mob

ilize

dto

Indi

ato

com

men

cea

twen

ty-f

ive

(25)

mon

thco

ntra

ctfo

rG

SPC

.

VIC

KSB

UR

G19

9830

0Ft

.11

%O

ffsho

reT

haila

ndC

HE

VR

ON

OV

ER

SEA

SPE

TR

OLE

UM

(‘‘C

HE

VR

ON

”)

The

rig

iscu

rren

tlyw

orki

ngun

der

alo

ng-t

erm

drill

ing

com

mit

men

tfo

rC

hevr

onw

hich

will

exte

ndto

June

2009

.

AT

WO

OD

AU

RO

RA

Und

erC

onst

ruct

ion

400

Ft.

0%N

/AN

/AT

heri

gis

unde

rco

nstr

ucti

onin

Bro

wns

ville

,Te

xas

wit

hex

pect

edco

mpl

etio

non

orbe

fore

Sept

embe

r20

08.

SU

BM

ER

SIB

LE

—R

ICH

MO

ND

2000

/200

270

Ft.

7%U

.S.

Gul

fof

Mex

ico

HE

LIS

OIL

&G

AS

(‘‘H

ELI

S”)

The

rig

iscu

rren

tlyw

orki

ngfo

rH

elis

unde

ra

cont

ract

whi

chco

uld

exte

ndto

May

/Jun

e20

07.

9

%%TRANSMSG*** Transmitting Job: H41700 PCN: 004000000 ***%%PCMSG|9 |00010|Yes|No|12/19/2006 21:48|0|0|Page is valid, no graphics -- Color: D|

Rig

Nam

eY

ear

Up

gra

ded

Max

imu

mW

ater

Dep

th

Per

cen

tag

eof

FY

2006

Rev

enu

es

Loc

atio

nat

Dec

emb

er12

,20

06C

ust

omer

Con

trac

tS

tatu

sat

Dec

emb

er12

,20

06

SE

MIS

UB

ME

RS

IBL

ET

EN

DE

RA

SS

IST

UN

IT—

SEA

HA

WK

1992

/199

9/20

0660

0Ft

.4%

Offs

hore

Equ

ator

ial

Gui

nea

AM

ER

AD

AH

ESS

EQ

UA

TO

RIA

LG

UIN

EA

,IN

C.

(‘‘H

ESS

”)

The

rig

iscu

rren

tlyw

orki

ngun

der

atw

o-ye

arco

ntra

ctua

lco

mm

itm

ent

wit

hH

ess

whi

chex

tend

sto

Sept

embe

r20

08.

Hes

sal

soha

sfo

ur(4

)si

x-m

onth

opti

ons.

MO

DU

LA

RP

LA

TF

OR

MS

—

MA

NA

GE

ME

NT

CO

NT

RA

CT

GO

OD

WY

N‘A

’an

dN

OR

TH

RA

NK

IN‘A

’N

/A4%

*A

ustr

alia

WO

OD

SID

EB

oth

the

GO

OD

WY

N‘A

’an

dN

OR

TH

RA

NK

IN‘A

’ar

eid

lew

ith

plan

ned

brea

ksin

drill

ing

acti

vity

.We

are

curr

ently

prov

idin

gri

gm

aint

enan

cese

rvic

esto

thes

eri

gs.

*F

orb

oth

un

its,

coll

ecti

vel

y.

10

%%TRANSMSG*** Transmitting Job: H41700 PCN: 005000000 ***%%PCMSG|10 |00007|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

SECURITIES LITIGATION SAFE HARBOR STATEMENT

Statements included in this report which arenot historical facts (including any statementsconcerning plans and objectives of managementfor future operations or economic performance, orassumptions related thereto) are “forward-lookingstatements” within the meaning of the PrivateSecurities Litigation Reform Act of 1995. In addi-tion, we and our representatives may from totime to time make other oral or written state-ments which are also forward-looking statements.

These forward-looking statements are madebased upon management’s current plans, expec-tations, estimates, assumptions and beliefs con-cerning future events impacting us and thereforeinvolve a number of risks and uncertainties. Wecaution that forward-looking statements are notguarantees and that actual results could differmaterially from those expressed or implied in theforward-looking statements.

Important factors that could cause our actualresults of operations or our actual financial condi-tions to differ include, but are not necessarilylimited to:

• our dependence on the oil and gasindustry;

• the operational risks involved in drilling foroil and gas;

• changes in rig utilization and dayrates inresponse to the level of activity in the oiland gas industry, which is significantlyaffected by indications and expectationsregarding the level and volatility of oil andgas prices, which in turn are affected bysuch things as political, economic andweather conditions affecting or potentiallyaffecting regional or worldwide demandfor oil and gas, actions or anticipatedactions by OPEC, inventory levels, deliver-ability constraints, and future marketactivity;

• the extent to which customers and poten-tial customers continue to pursue deepwa-ter drilling;

• exploration success or lack of explorationsuccess by our customers and potentialcustomers;

• the highly competitive and cyclical natureof our business, with periods of lowdemand and excess rig availability;

• the impact of the war with Iraq or othermilitary operations, terrorist acts or embar-goes elsewhere;

• our ability to enter into and the terms offuture drilling contracts;

• the availability of qualified personnel;

• our failure to retain the business of one ormore significant customers;

• the termination or renegotiation of con-tracts by customers;

• the availability of adequate insurance at areasonable cost;

• the occurrence of an uninsured loss;

• the risks of international operations,including possible economic, political,social or monetary instability, and compli-ance with foreign laws;

• the effect public health concerns couldhave on our international operations andfinancial results;

• compliance with or breach of environmen-tal laws;

• the incurrence of secured debt or addi-tional unsecured indebtedness or otherobligations by us or our subsidiaries;

• the adequacy of sources of liquidity;

• currently unknown rig repair needs and/oradditional opportunities to accelerateplanned maintenance expenditures due topresently unanticipated rig downtime;

• higher than anticipated accruals for perfor-mance-based compensation due to betterthan anticipated performance by us,higher than anticipated severance

11

%%TRANSMSG*** Transmitting Job: H41700 PCN: 006000000 ***%%PCMSG|11 |00003|Yes|No|12/14/2006 11:28|0|0|Page is valid, no graphics -- Color: D|

expenses due to unanticipated employeeterminations, higher than anticipated legaland accounting fees due to unanticipatedfinancing or other corporate transactions,and other factors that could increase gen-eral and administrative expenses;

• the actions of our competitors in the off-shore drilling industry, which could signif-icantly influence rig dayrates andutilization;

• changes in the geographic areas in whichour customers plan to operate, which inturn could change our expected effectivetax rate;

• changes in oil and gas drilling technologyor in our competitors’ drilling rig fleetsthat could make our drilling rigs less com-petitive or require major capital invest-ments to keep them competitive;

• rig availability;

• the effects and uncertainties of legal andadministrative proceedings and othercontingencies;

• the impact of governmental laws and reg-ulations and the uncertainties involved intheir administration, particularly in someforeign jurisdictions;

• changes in accepted interpretations ofaccounting guidelines and other account-ing pronouncements and tax laws;

• the risks involved in the construction,upgrade, and repair of our drillingunits; and

• such other factors as may be discussed inour reports filed with the Securities andExchange Commission, or SEC.

These factors are not necessarily all of theimportant factors that could cause actual resultsto differ materially from those expressed in any ofour forward-looking statements. Other unknownor unpredictable factors could also have materialadverse effects on future results. The words“believe,” “impact,” “intend,” “estimate,” “antici-pate,” “plan” and similar expressions identify for-ward-looking statements. These forward-lookingstatements are found at various places through-out this report. When considering any forward-looking statement, you should also keep in mindthe risk factors described in our Form 10-K forthe year ended September 30, 2006, particularlyin Item 1A Risk Factors, to which this AnnualReport is an exhibit, and in other reports orfilings we make with the SEC from time to time.Undue reliance should not be placed on theseforward-looking statements, which are applicableonly on the date hereof. Neither we nor ourrepresentatives have a general obligation torevise or update these forward-looking state-ments to reflect events or circumstances thatarise after the date hereof or to reflect the occur-rence of unanticipated events.

12

%%TRANSMSG*** Transmitting Job: H41700 PCN: 007000000 ***%%PCMSG|12 |00006|Yes|No|12/14/2006 08:59|0|0|Page is valid, no graphics -- Color: D|

MANAGEMENT’S DISCUSSION AND ANALYSISOF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OUTLOOK

Revenues, operating cash flows and netincome for fiscal year 2006 were the highest inour thirty-nine year history. All of our eight drill-ing units have contractual dayrate commitmentsthat are the highest in their respective histories.Currently, we have approximately 95% and 80%of our available rig days contracted for fiscalyears 2007 and 2008, respectively. A comparisonof the average per day revenues for fiscal years2006 and 2005 for each of our eight drilling unitsto their highest currently contracted dayratecommitment is as follows:

AveragePer Day

Revenuesfor FiscalYear 2005

AveragePer Day

Revenuesfor FiscalYear 2006

HighestCurrently

ContractedDayrate

Commitment

PercentageChange

FromFiscal Year

2006

ATWOOD EAGLE . . . . $95,000 $129,000 $405,000 214%ATWOOD HUNTER. . . $61,000 172,000 245,000 42%ATWOOD FALCON . . . $82,000 83,000 200,000 141%ATWOOD SOUTHERN

CROSS . . . . . . . . . $30,000 82,000 305,000 272%ATWOOD BEACON . . $66,000 88,000 133,500 52%VICKSBURG . . . . . . . $65,000 82,000 154,000 88%SEAHAWK . . . . . . . . $38,000 32,000 68,430 114%RICHMOND . . . . . . . $33,000 55,000 80,000 45%

The ATWOOD EAGLE is currently workingunder a contractual commitment offshore Austra-lia at dayrates ranging from $150,000 to approxi-mately $170,000 which should extend toNovember 2007. Following completion of thiscontract commitment, the rig will drill one (1) wellat a dayrate of $360,000 and then commence atwo-year contract commitment at a dayrate of$405,000 which should extend to December 2009.The ATWOOD HUNTER is currently working off-shore Africa at dayrates ranging from $240,000 to$245,000 under a long-term contract commitmentwhich should extend to April 2008. The ATWOODFALCON has a contractual commitment offshoreMalaysia at dayrates ranging from $93,000 to$200,000 which should extend into July 2009.Under this contractual commitment, during theperiod August 2006 to early November 2006 the

rig incurred a $30 million water depth upgradealong with certain equipment refurbishments ofwhich the customer will pay $24 million of suchcosts along with payment of a $90,000 dayrateduring this shipyard period. The $24 million willbe amortized into income on a straight-line basisover the term of the contract through July 2009.The ATWOOD SOUTHERN CROSS is currentlyworking in the Black Sea and has several drillingcommitments at dayrates ranging from $125,000to $305,000 that should extend through the firsthalf of fiscal year 2008. Currently, the ATWOODBEACON is being relocated to India to com-mence a 25-month contract at dayrates rangingfrom $113,000 to $133,500. The VICKSBURG hascontract commitments offshore Thailand at day-rates ranging from $94,500 to $154,000 thatshould extend to June 2009. The SEAHAWK iscurrently working offshore West Africa under along-term drilling program that should extend toSeptember 2008. This drilling contract providesfor four six month options with a dayrate for thefirm and option periods of $68,430. After the firstyear, the stated dayrate of $68,430 will increasebased upon certain cost escalations. Our only rigin the U.S. Gulf of Mexico, the RICHMOND, has acurrent contract commitment at a dayrate of$80,000 which could extend to May/June 2007.The ATWOOD AURORA, an ultra premiumjack-up to become our ninth owned offshore drill-ing unit upon its delivery, is under constructionat Brownsville, Texas. The construction of this rigis currently expected to be completed on orbefore September 2008 at a total cost (includingcapitalized interest) of $160 million.

The current strong market environment isnot only supporting high equipment utilizationwith historical high dayrate environments, butalso has resulted in a significant increase in ouroperating costs. Over the next few months, weexpect daily operating costs for the ATWOODEAGLE to average between $80,000 and $85,000.The ATWOOD HUNTER, during the time it works

13

%%TRANSMSG*** Transmitting Job: H41700 PCN: 008000000 ***%%PCMSG|13 |00010|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

offshore Mauritania and Libya, is expected toincur daily operating costs between $55,000 and$60,000; however, costs could be higher duringany relocation period or during any period whenthe rig is undergoing required inspections. TheATWOOD HUNTER is expected to be off dayratefor ten to fourteen days in December 2006 forrequired regulatory inspections and maintenance.Operating costs during this period could averagebetween $60,000 and $65,000 per day. We expectthat the ATWOOD FALCON will incur averagedaily operating costs between $45,000 and$50,000 while working offshore Malaysia; how-ever, costs will be significantly higher during thefirst quarter of fiscal year 2007 ($85,000 to$95,000 per day) due to expensing certain costsincurred during the period the rig was in theshipyard undergoing its water depth upgrade.The ATWOOD SOUTHERN CROSS is alsoexpected to have average daily operating costs inthe Black Sea between $45,000 and $50,000; how-ever, during the rig’s relocation to the Black Seaduring October 2006, operating costs wereexpected to average around $60,000 per day.Operating costs for our bottom supported drillingunits (ATWOOD BEACON, VICKSBURG, andRICHMOND) should average between $30,000and $35,000 per day. The SEAHAWK is expectedto incur operating costs between $60,000 and$65,000 per day while working offshore EquatorialGuinea; however, these figures include anapproximate $16,000 per day amortization of cer-tain deferred costs on a straight-line basis overthe life of the applicable drilling contract whichwill be more than offset by the amortization ofrelated deferred fees of approximately $19,000 perday which are also recognized and earned on astraight-line basis over the life of the contract.Operating costs will vary for all rigs dependingupon each rig’s specific operating activities. Forexample, cost may increase when a rig is beingrelocated to a new drilling location, when a rig isundergoing required inspection or when a rig isundergoing extraordinary maintenance or equip-ment replacement.

Despite the increase in operating costs forfiscal year 2006, our operating results signifi-cantly increased for fiscal year 2006 compared tofiscal year 2005. Although we anticipate a con-tinuing trend for increases in operating costsduring the next fiscal year, with our backlog ofcontracted days providing increasing revenueexpectations, we anticipate that revenues, oper-ating cash flows and earnings for fiscal years2007 and 2008 will reflect a significant improve-ment over fiscal year 2006 operating results andare expected to be the highest in our history.

RESULTS OF OPERATIONS

Fiscal Year 2006 Versus Fiscal Year 2005

Revenues for fiscal year 2006 increased 57%compared to the prior fiscal year. A comparativeanalysis of revenues by rig for fiscal years 2006and 2005 is as follows:

Fiscal2006

Fiscal2005 Variance

REVENUES(In millions)

ATWOOD HUNTER. . . . . . . . . $ 62.8 $ 22.1 $ 40.7ATWOOD SOUTHERN

CROSS . . . . . . . . . . . . . . . . 29.9 10.8 19.1ATWOOD EAGLE . . . . . . . . . . 47.0 34.6 12.4RICHMOND . . . . . . . . . . . . . . 20.2 11.9 8.3ATWOOD BEACON . . . . . . . . 32.1 24.2 7.9AUSTRALIA MANAGEMENT

CONTRACTS . . . . . . . . . . . 12.9 5.2 7.7VICKSBURG . . . . . . . . . . . . . . 30.0 23.6 6.4ATWOOD FALCON . . . . . . . . . 30.1 29.8 0.3SEAHAWK . . . . . . . . . . . . . . . 11.6 13.9 (2.3)

$276.6 $176.1 $100.5

The increase in fleetwide revenues is prima-rily attributable to the increase in average day-rates due to improving market conditions andstrong demand for offshore drilling equipment asnoted in Market Outlook. Thus, unless otherwisenoted below, the increase in revenues for eachrig is due to the increases in contractual dayratesin fiscal year 2006 compared to fiscal year 2005.

During the last quarter of fiscal year 2005,the ATWOOD SOUTHERN CROSS was relocated

14

%%TRANSMSG*** Transmitting Job: H41700 PCN: 009000000 ***%%PCMSG|14 |00010|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

from Southeast Asia to the Mediterranean Seawith no revenues being realized during this relo-cation period. This relocation resulted in earnedmobilization fees for the ATWOOD SOUTHERNCROSS increasing from $0.8 million in fiscal year2005 to $8.1 million in fiscal year 2006, which,along with increases in contracted dayratesaccounts for its increase in revenues. Increasesin revenues for the ATWOOD HUNTER,ATWOOD EAGLE, VICKSBURG, ATWOOD BEA-CON, ATWOOD FALCON and the RICHMONDwere related to each of these drilling units work-ing under higher dayrate contracts in fiscal year2006 compared to fiscal year 2005. The increasein revenues from the AUSTRALIA MANAGE-MENT CONTRACTS was due to one of thesemanaged rigs returning to active drilling. Thedecline in revenues for the SEAHAWK was dueto the unit being upgraded in fiscal year 2006,with no revenues being realized during thisupgrade period.

Contract drilling costs for fiscal year 2006increased 40% compared to the prior fiscal year.A comparative analysis of contract drilling costsby rig for fiscal years 2006 and 2005 is as follows:

Fiscal2006

Fiscal2005 Variance

(In millions)

CONTRACT DRILLINGCOSTS

ATWOOD SOUTHERNCROSS . . . . . . . . . . . . . . . . $ 24.2 $ 9.1 $15.1

ATWOOD HUNTER. . . . . . . . . 18.8 11.9 6.9AUSTRALIA MANAGEMENT

CONTRACTS . . . . . . . . . . . 10.8 4.7 6.1ATWOOD EAGLE . . . . . . . . . . 26.8 21.9 4.9VICKSBURG . . . . . . . . . . . . . . 11.9 8.8 3.1ATWOOD BEACON . . . . . . . . 10.4 8.5 1.9ATWOOD FALCON . . . . . . . . . 16.5 14.6 1.9RICHMOND . . . . . . . . . . . . . . 10.4 8.9 1.5SEAHAWK . . . . . . . . . . . . . . . 8.4 9.9 (1.5)OTHER. . . . . . . . . . . . . . . . . . 6.2 4.5 1.7

$144.4 $102.8 $41.6

The increase in fleetwide drilling costs wasprimarily attributable to four areas: rising person-nel costs due to wage increases, increasedrepairs and maintenance expenses and freight

costs due to the amount and timing of variousrepairs and maintenance projects and equipmentenhancements and rising insurance costs due toincreased premiums. Thus, unless otherwisenoted below, the increase in drilling costs foreach rig is primarily due to the four areas men-tioned above.

Besides the four areas discussed above, theincrease in drilling costs for the ATWOODSOUTHERN CROSS is also due to $8.6 million ofmobilization expense amortization during the fis-cal year 2006, compared to $0.8 million ofdeferred mobilization expense during fiscal year2005 as the rig relocated from Southeast Asia tothe Mediterranean during the fourth quarter offiscal year 2005. The increase in drilling costs forthe ATWOOD HUNTER also includes higheragent commissions due to increased revenueswhen compared to the prior fiscal year and dueto its relocation from Egypt to Mauritania whereoperating costs are higher. As previously men-tioned, one of our managed platform rigs in Aus-tralia commenced a new drilling program duringthe current fiscal year, and thus, service activitiesfor our AUSTRALIA MANAGEMENT CON-TRACTS for fiscal year 2006 have increasedaccordingly when compared to fiscal year 2005.The decrease in drilling costs for the SEAHAWKis due to $4.0 million of deferred mobilizationcosts for fiscal year 2006 due to the relocation ofthe rig from Southeast Asia to West Africa com-pared to no deferred mobilization costs in theprior fiscal year. Other drilling costs for fiscal year2006 have increased primarily due to the record-ing of stock option compensation expense (result-ing from adoption of Statement of FinancialAccounting Standards No. 123(R), “Share-BasedPayment”, or SFAS 123(R) on October 1, 2005) forfield personnel.

Depreciation expense for fiscal year 2006decreased 1% as compared to the prior fiscalyear. A comparative analysis of depreciation

15

%%TRANSMSG*** Transmitting Job: H41700 PCN: 010000000 ***%%PCMSG|15 |00014|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

expense by rig for fiscal years 2006 and 2005 isas follows:

Fiscal2006

Fiscal2005 Variance

(In millions)

DEPRECIATIONEXPENSE

SEAHAWK . . . . . . . . . . . . . . . . . $ 1.6 $ 0.5 $ 1.1ATWOOD HUNTER . . . . . . . . . . 5.4 5.3 0.1VICKSBURG. . . . . . . . . . . . . . . . 2.8 2.7 0.1ATWOOD BEACON . . . . . . . . . . 5.3 5.2 0.1RICHMOND . . . . . . . . . . . . . . . . 0.9 0.9 —ATWOOD FALCON . . . . . . . . . . 2.8 2.8 —ATWOOD EAGLE . . . . . . . . . . . 4.6 4.7 (0.1)ATWOOD SOUTHERN CROSS . . 2.9 4.5 (1.6)OTHER . . . . . . . . . . . . . . . . . . . 0.1 0.1 —

$26.4 $26.7 $(0.3)

The increase in depreciation expense for theSEAHAWK was due to the completion of a$16 million life enhancing upgrade during thefourth quarter of the current fiscal year. Duringthe first quarter of the current fiscal year, theATWOOD SOUTHERN CROSS underwent a lifeenhancing upgrade whereby the useful life of therig was extended from approximately two to fiveyears. Depreciation expense for our other unitswas relatively unchanged in fiscal year 2006 ascompared to fiscal year 2005.

In October 2005, we sold our semisubmersi-ble hull, SEASCOUT, for $10 million (net aftercertain expenses) and our spare 15,000 P.S.I. BOPStack for approximately $15 million. For the 2006fiscal year period, gains on the sales of these twoassets and other excess equipment totaledapproximately $10.5 million in the aggregate. Wehad no operations or revenues associated withthese assets prior to their sale.

General and administrative expenses for fis-cal year 2006 have increased 45% compared tothe prior fiscal year due primarily to the follow-ing: $3.7 million of stock option compensationexpense (resulting from adoption of SFAS 123(R)on October 1, 2005), a $1.5 million increase inprofessional fees primarily related to higher Sar-banes-Oxley compliance costs, and a $0.6 million

increase in annual bonus compensation. Interestexpense has decreased primarily due to thereduction of our outstanding debt while interestincome has increased when compared to theprior fiscal year due to higher interest ratesearned on higher cash balances.

Virtually all of our tax provision for fiscal year2006 relates to taxes in foreign jurisdictions. As aresult of working in foreign jurisdictions, weearned a high level of operating income in certainnontaxable and deemed profit tax jurisdictionswhich significantly reduced our effective tax ratefor the current fiscal year when compared to theUnited States statutory rate. In addition, wereversed a $1.8 million tax contingent liabilitydue to the expiration of the statute of limitationsin a foreign jurisdiction. Also, we were advisedby a foreign tax authority that it had approvedacceptance of certain amended prior year taxreturns. The acceptance of these amended taxreturns, along with the fiscal year 2005 tax returnin this foreign jurisdiction, resulted in the recog-nition of a $4.6 million tax benefit in the thirdquarter. Including the two previously mentioneddiscrete items, which reduced our rate by 7%,our effective tax rate for fiscal year 2006 wasapproximately 6%.

Excluding any discrete items that may occur,we expect our effective tax rate to be approxi-mately 15-20% for fiscal year 2007 due toincreased earnings in foreign jurisdictions withhigh statutory tax rates.

Fiscal Year 2005 Versus Fiscal Year 2004

Revenues for fiscal year 2005 increased 8%compared to the fiscal year 2004. A comparative

16

%%TRANSMSG*** Transmitting Job: H41700 PCN: 011000000 ***%%PCMSG|16 |00012|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

analysis of revenues by rig for fiscal years 2005and 2004 is as follows:

Fiscal2005

Fiscal2004 Variance

(In millions)REVENUES

ATWOOD EAGLE . . . . . . . . . . $ 34.6 $ 30.4 $ 4.2ATWOOD FALCON . . . . . . . . . 29.8 26.0 3.8ATWOOD BEACON . . . . . . . . 24.2 20.7 3.5AUSTRALIA MANAGEMENT

CONTRACTS . . . . . . . . . . . 5.2 2.0 3.2ATWOOD HUNTER. . . . . . . . . 22.1 19.4 2.7RICHMOND . . . . . . . . . . . . . . 11.9 9.6 2.3VICKSBURG . . . . . . . . . . . . . . 23.6 24.3 (0.7)ATWOOD SOUTHERN

CROSS . . . . . . . . . . . . . . . . 10.8 12.5 (1.7)SEAHAWK . . . . . . . . . . . . . . . 13.9 18.6 (4.7)

$176.1 $163.5 $12.6

During fiscal year 2005, the ATWOODEAGLE was fully utilized at dayrates rangingfrom $89,000 to $109,000 compared to approxi-mately 90% utilization at the same dayrates dur-ing fiscal year 2004. The increase in revenues forthe ATWOOD FALCON was due to the rig beingfully utilized during fiscal year 2005 at an averagedayrate of $82,000 compared to 90% utilization atan average dayrate of $78,000 during fiscal year2004. The ATWOOD BEACON had average perday revenues during fiscal year 2005 of $66,000(which includes 100 days of business interruptionproceeds) compared to average per day revenuesduring fiscal year 2004 of $62,000 (which includes35 days of business interruption proceeds and30 days of zero rate downtime immediately fol-lowing its July 2004 incident which damaged itslegs and derrick). Refer to Note 4 to the consoli-dated financial statements for further discussionof the Atwood Beacon incident. Since the end offiscal year 2001, there has been a planned breakin drilling activities on the GOODWYN ‘A’ andNORTH RANKIN ‘A’ platform rigs during whichwe have provided a limited amount of mainte-nance services to these platform rigs. However,during fiscal year 2005, service activities forNORTH RANKIN ‘A’ increased due to a planneddrilling program to commence during fiscal year

2006. The ATWOOD HUNTER was fully utilizedduring fiscal year 2005 at an average dayrate of$61,000 compared to 95% utilization during fiscalyear 2004 at an average dayrate of $55,000. Theincrease in revenue for the RICHMOND was dueto an increase in the average dayrate from$26,000 during fiscal year 2004 to $33,000 duringfiscal year 2005. Revenues for the VICKSBURGwere relatively consistent for fiscal years 2004and 2005 while revenues for the ATWOODSOUTHERN CROSS declined due to a decreasein the amount of earned mobilization revenuefrom $4.1 million in fiscal year 2004 to $0.8 millionin fiscal year 2005 as the rig relocated twiceduring fiscal year 2004 and only once duringfiscal year 2005. This decrease was partially off-set by an increase in dayrates ranging from$35,000 to $40,000 during fiscal year 2005 com-pared to $30,000 to $35,000 during fiscal year2004. The SEAHAWK was fully utilized duringthe fiscal year 2004 at an average dayrate of$50,000 compared to 85% utilization during fiscalyear 2005 at an average dayrate of $45,000.

Contract drilling costs for fiscal year 2005increased 4% compared to fiscal year 2004. Acomparative analysis of contract drilling costs byrig for fiscal years 2005 and 2004 is as follows:

Fiscal2005

Fiscal2004 Variance

(In millions)

CONTRACT DRILLINGCOSTS

AUSTRALIA MANAGEMENTCONTRACTS . . . . . . . . . . . . $ 4.7 $ 2.1 $ 2.6

ATWOOD EAGLE . . . . . . . . . . . 21.9 20.7 1.2RICHMOND . . . . . . . . . . . . . . . 8.9 7.9 1.0SEAHAWK . . . . . . . . . . . . . . . . 9.9 9.0 0.9VICKSBURG . . . . . . . . . . . . . . . 8.8 8.3 0.5ATWOOD HUNTER . . . . . . . . . 11.9 12.0 (0.1)ATWOOD FALCON. . . . . . . . . . 14.6 15.1 (0.5)ATWOOD BEACON . . . . . . . . . 8.5 10.2 (1.7)ATWOOD SOUTHERN

CROSS . . . . . . . . . . . . . . . . . 9.1 12.3 (3.2)OTHER . . . . . . . . . . . . . . . . . . 4.5 1.3 3.2

$102.8 $98.9 $ 3.9

17

%%TRANSMSG*** Transmitting Job: H41700 PCN: 012000000 ***%%PCMSG|17 |00008|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

With the increase in service activities forNORTH RANKIN ‘A’ during fiscal year 2005 dueto a planned drilling program to commence dur-ing fiscal year 2006, drilling costs as well asrevenues increased from our management of thisplatform rig. The increase in drilling costs for theATWOOD EAGLE was due to higher labor costsdue to local operating requirements offshore Aus-tralia, its location for all of the fiscal year 2005.The increase in drilling costs for the RICHMONDand SEAHAWK were primarily due to higherrepair and maintenance expenses incurred on therigs during the fiscal year ended September 30,2005 compared to the fiscal year ended Septem-ber 30, 2004. Drilling costs for the VICKSBURG,ATWOOD HUNTER, and ATWOOD FALCONremained relatively consistent for fiscal year 2005compared to fiscal year 2004. The decline indrilling costs for the ATWOOD BEACON was dueto a decrease in repair and maintenanceexpenses primarily resulting from the recordingof a $1.0 million insurance deductible duringfiscal year 2004 related to damage incurred dur-ing the rig’s July 2004 incident. During most ofthe fourth quarter of fiscal year 2005, theATWOOD SOUTHERN CROSS was being mobi-lized from Southeast Asia to the Mediterranean.Virtually all costs incurred during a mobilizationperiod are deferred and amortized as an expenseover the term of the new contract. Havingdeferred mobilization costs at the end of fiscalyear 2005 compared to having no such deferredcosts at the end of fiscal year 2004 accounts forits decline in drilling costs. The increase of otherdrilling costs during fiscal year 2005 was due to a$1.0 million reduction in the amount of insurancepremium refunds received during fiscal year 2005when compared to fiscal year 2004 and also dueto fiscal year 2004 including the settlement of adispute with a client which resulted in a reduc-tion of operation costs of $0.6 million along withvarious other increases of non-drilling unit spe-cific costs.

Depreciation expense for fiscal year 2005decreased 16% as compared to fiscal year 2004.

A comparative analysis of depreciation expenseby rig for fiscal years 2005 and 2004 is as follows:

Fiscal2005

Fiscal2004 Variance

(In millions)

DEPRECIATIONEXPENSE

ATWOOD SOUTHERN CROSS . . $ 4.5 $ 4.2 $ 0.3VICKSBURG. . . . . . . . . . . . . . . . 2.7 2.6 0.1ATWOOD FALCON . . . . . . . . . . 2.8 2.7 0.1ATWOOD BEACON . . . . . . . . . . 5.2 5.2 —RICHMOND . . . . . . . . . . . . . . . . 0.9 0.9 —ATWOOD EAGLE . . . . . . . . . . . 4.7 4.8 (0.1)ATWOOD HUNTER . . . . . . . . . . 5.3 5.4 (0.1)SEAHAWK . . . . . . . . . . . . . . . . . 0.5 5.1 (4.6)OTHER . . . . . . . . . . . . . . . . . . . 0.1 0.7 (0.6)

$26.7 $31.6 $(4.9)

Effective October 1, 2004, we extended theremaining depreciable life of the SEAHAWK from2 months to 5 years. The depreciable life of thisrig was extended based upon entry into a con-tract that extended the rig’s commercial viabilityfor up to 5 years, coupled with our intent tocontinue marketing and operating the rig beyond2 months. The decrease in other depreciation isdue to certain non-rig assets becoming fullydepreciated during the last quarter of fiscal year2004 and the first quarter of fiscal year 2005.Depreciation expense for our other units wasrelatively unchanged in fiscal year 2005 as com-pared to fiscal year 2004.

General and administrative expenses for fis-cal year 2005 increased 25% compared to fiscalyear 2004 due to significantly increased profes-sional fees primarily resulting from compliancerequirements of the Sarbanes-Oxley Act and dueto $0.7 million of bonuses paid during fiscal year2005, compared with no bonus payments duringfiscal year 2004. Although the level of our out-standing debt has been reduced significantlyfrom fiscal year 2004, the reduction of interestexpense was partially offset by rising interestrates during fiscal year 2005. Interest income hasincreased when compared to fiscal year 2004 dueto higher interest rates earned on cash balances

18

%%TRANSMSG*** Transmitting Job: H41700 PCN: 013000000 ***%%PCMSG|18 |00011|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

and interest income earned on income taxrefunds.

Virtually all of our tax provision for fiscalyears 2005 and 2004 related to taxes in foreignjurisdictions, with fiscal year 2005 also impactedby a $3.3 million United States tax benefit recog-nized. During fiscal year 2005 our provision wasalso offset by two other foreign discrete items.During the first quarter of fiscal year 2005, wereceived a $1.7 million tax refund in Malaysiarelated to a previously reserved tax receivable. Inaddition, a $1.0 million deferred tax benefit wasrecognized in June 2005 due to the filing andsubsequent acceptance by the local tax authority,of amended prior year tax returns. On Decem-ber 1, 2005, we received notification from theUnited States Department of Treasury that a pre-viously reserved United States income tax refundwe had been pursuing for over two years hadbeen approved for payment. Based upon thisapproval, we reduced our income tax provisionby the refund amount of $3.3 million for the yearended September 30, 2005. Furthermore, duringfiscal year 2005, operating income earned in cer-tain nontaxable and deemed profit tax jurisdic-tions was higher when compared to fiscal year2004, including business interruption proceedsearned by the ATWOOD BEACON in a zero taxjurisdiction for approximately three and a halfmonths, which contributed to our lower effectivetax rate. As a result of these items, our effectivetax rate for fiscal year 2005 was significantly lesswhen compared to fiscal year 2004 and theUnited States statutory rate.

LIQUIDITY AND CAPITAL RESOURCES

Since we operate in a very cyclical industry,maintaining high equipment utilization in up, aswell as down, cycles is a key factor in generatingcash to satisfy current and future obligations. Forfiscal years 2001 through 2005, net cash providedby operating activities ranged from a low ofapproximately $13.7 million in fiscal year 2003 toa high of approximately $62.3 million in fiscal

year 2001 compared to net cash provided byoperating activities of approximately $85.5 millionfor fiscal year 2006. Our operating cash flows areprimarily driven by our operating income, whichreflects dayrates and rig utilization. The low levelof net cash provided by operating activities infiscal year 2003 was due to a downturn in marketconditions during which we pursued short-termcontract opportunities in high operating costareas in order to maintain high utilization of ourfleet. Operating results in fiscal years 2004, 2005and 2006 reflected continuing improvements inmarket conditions which enabled us to havehigher cash flows and earnings in these yearscompared to fiscal year 2003. Due to the signifi-cant increase in future dayrate commitments athistorically high levels, we have pursued longer-term contract opportunities for some of our drill-ing units. We currently have approximately 95%and 80% of our available operating rig days com-mitted for fiscal years 2007 and 2008, respec-tively. With the current historically high dayratecommitments on all eight of our actively owneddrilling units, we anticipate significant improve-ment in cash flows and earnings during fiscalyears 2007 and 2008. Other than our expectedcapital expenditures of $110 million to $115 mil-lion for fiscal year 2007, the only additional cashcommitment for fiscal year 2007, outside of fund-ing current rig operations, is our required quar-terly repayments under the term portion of oursenior secured credit facility which will total$36 million for fiscal year 2007. We expect togenerate more than sufficient cash flows fromoperations to satisfy all of these obligations.

In October 2004, we sold in a public offering2,350,000 shares of our common stock at aneffective net price (before expenses) of $22.92 fornet proceeds of approximately $53.6 million. Weused these proceeds and cash on hand to repaythe $55 million outstanding under the revolvingportion of our credit facility. As of September 30,2006, we only had $54 million outstanding underthe term portion of our credit facility, with$10 million (repaid in October 2006) outstanding

19

%%TRANSMSG*** Transmitting Job: H41700 PCN: 014000000 ***%%PCMSG|19 |00006|Yes|No|12/14/2006 11:34|0|0|Page is valid, no graphics -- Color: D|

under the revolving portion of our credit facility.Our total debt to capitalization ratio (debt/(debt +equity)) is 12% as of September 30, 2006. Thisratio will continue to decline unless we identifyan acceptable growth opportunity. However, wewill continue to explore opportunities for valueenhancing growth as they arise.

We are in compliance with all financial cove-nants at September 30, 2006 and expect toremain in compliance with all financial covenantsduring fiscal year 2007. Further, at all times dur-ing fiscal year 2004, 2005 and 2006 when wewere required to determine compliance with ourfinancial covenants, we were in compliance withthose covenants. Aside from the financial cove-nants, no other provisions exist in the creditfacility that could result in acceleration of theApril 1, 2008 maturity date.

At September 30, 2006, the collateral for ourcredit facility consists primarily of preferred mort-gages on all eight of our active drilling units(with an aggregate net book value at Septem-ber 30, 2006 totaling approximately $397 million).We are not required to maintain compensatingbalances; however, we are required to pay a feeof approximately 0.60% per annum on the unusedrevolving portion of our credit facility and certainother administrative costs.

In October 2005, we sold our semisubmersi-ble hull, SEASCOUT, for $10 million (net aftercertain expenses) and our spare 15,000 P.S.I. BOPStack for approximately $15 million. For the 2006fiscal year period, gains on the sales of these twoassets and other excess equipment totaledapproximately $10.5 million in the aggregate. Theapproximate $26 million in cash received fromthe sales of excess equipment, plus borrowingsunder the revolving portion of our credit facility($10 million outstanding at September 30,2006) along with our operating cash flows, hasallowed us to expend approximately $30 milliontoward the construction of the ATWOODAURORA, approximately $16 million on upgrad-ing the SEAHAWK, approximately $5 million in

completing the ATWOOD SOUTHERN CROSSupgrade, approximately $16 million toward theATWOOD FALCON upgrade and approximately$11 million in other capital expenditures duringfiscal year 2006 and have cash and cash equiva-lents remaining on hand at September 30, 2006of approximately $32 million.

Our accounts receivable have increased by$40.4 million since September 30, 2005, primarilydue to our increased rig utilization and higherdayrates. Our portfolio of accounts receivable iscomprised of major international corporate enti-ties with stable payment experience. Historically,we have not encountered significant difficulty incollecting receivables and typically do not requirecollateral for our receivables; however, we have a$0.8 million allowance for doubtful accounts atSeptember 30, 2006. The insurance receivable of$0.6 million at September 30, 2005 and Septem-ber 30, 2006, relates to repairs to be made to theATWOOD BEACON. Final repairs on this rigwere completed in November 2006, and weexpect to collect the remaining $0.6 million insur-ance receivable associated therewith in fiscalyear 2007.

Long-term deferred credits have increasedby $22.3 million since September 30, 2005, prima-rily due to deferred fees associated with thecurrent fiscal year upgrades and mobilizations ofthe ATWOOD FALCON and SEAHAWK.

Commitments

The following table summarizes our obliga-tions and commitments (in thousands) at Sep-tember 30, 2006:

Fiscal2007

Fiscal2008

Fiscal2009

Fiscal2010

Fiscal2011 andthereafter

Long-Term Debt(1) . . . . . $36,000 $28,000 $ — $ — $ —Purchase

Commitments(2) . . . . . 61,854 28,282 — — —Operating Leases . . . . . . 1,916 1,102 978 845 3,570

$99,770 $57,384 $978 $845 $3,570

20

%%TRANSMSG*** Transmitting Job: H41700 PCN: 015000000 ***%%PCMSG|20 |00009|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

(1) Excluded from the above table is interest associ-ated with borrowings under our credit facilitybecause the applicable interest rate is variable.The principal amount outstanding under ourcredit facility included in the above table is$64 million which currently bears interest at arate of approximately 7%.

(2) Rig construction and upgrade commitments forthe ATWOOD AURORA and the ATWOOD FAL-CON, respectively.

CRITICAL ACCOUNTING POLICIES

Significant accounting policies are includedin Note 2 to our consolidated financial statementsfor the year ended September 30, 2006. Thesepolicies, along with the underlying assumptionsand judgments made by management in theirapplication, have a significant impact on ourconsolidated financial statements. We identifyour most critical accounting policies as thosethat are the most pervasive and important to theportrayal of our financial position and results ofoperations, and that require the most difficult,subjective and/or complex judgments by manage-ment regarding estimates about matters that areinherently uncertain. Our most critical account-ing policies are those related to revenue recogni-tion, property and equipment, impairment ofassets, income taxes, and employee stock-basedcompensation.

We account for the drilling and managementcontract revenue in accordance with the terms ofthe underlying drilling or management contract.These contracts generally provide that revenue isearned and recognized on a daily rate (i.e. “day-rate”) basis and dayrates are typically earned fora particular level of service over the life of acontract. Dayrate contracts can be for a specifiedperiod of time or the time required to drill aspecified well or number of wells. Revenues fromdayrate drilling operations, which are classifiedunder contract drilling services, are recognizedon a per day basis as the work progresses. Inaddition, lump-sum fees received at

commencement of the drilling contract as com-pensation for the cost of relocating drilling rigsfrom one major operating area to another, as wellas equipment and upgrade costs reimbursed bythe customer are recognized as earned on astraight-line method over the term of the relateddrilling contract, as are the dayrates associatedwith such contract. However, lump-sum feesreceived upon termination of a drilling contractare recognized as earned during the period termi-nation occurs. In addition, we defer the mobiliza-tion costs relating to moving a drilling rig to anew area and customer requested equipmentpurchases that will revert to the customer at theend of the applicable drilling contract. We amor-tize such costs on a straight-line basis over thelife of the applicable drilling contract.

We currently operate eight active offshoredrilling units. These assets are premium equip-ment and should provide many years of qualityservice. At September 30, 2006, the carryingvalue of our property and equipment totaled$436.2 million, which represents 73% of our totalassets. This carrying value reflects the applica-tion of our property and equipment accountingpolicies, which incorporate estimates, assump-tions and judgments by management relative tothe useful lives and salvage values of our units.Once a rig is placed in service, it is depreciatedon the straight-line method over its estimateduseful life, with depreciation discontinued onlyduring the period when a drilling unit is out ofservice while undergoing a significant upgradethat extends its useful life. The estimated usefullives of our drilling units and related equipmentrange from 3 years to 25 years and our salvagevalues are generally based on 5% of capitalizedcosts. Any future increases in our estimates ofuseful lives or salvage values will have the effectof decreasing future depreciation expense infuture years and spreading the expense to lateryears. Any future decreases in our useful lives orsalvage values will have the effect of acceleratingfuture depreciation expense.

21

%%TRANSMSG*** Transmitting Job: H41700 PCN: 016000000 ***%%PCMSG|21 |00006|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

We evaluate the carrying value of our prop-erty and equipment when events or changes incircumstances indicate that the carrying value ofsuch assets may be impaired. Asset impairmentevaluations are, by nature, highly subjective.Operations of our drilling equipment are subjectto the offshore drilling requirements of oil andgas exploration and production companies andagencies of foreign governments. These require-ments are, in turn, subject to fluctuations ingovernment policies, world demand and price forpetroleum products, proved reserves in relation tosuch demand and the extent to which suchdemand can be met from onshore sources. Thecritical estimates which result from these dynam-ics include projected utilization, dayrates, andoperating expenses, each of which impact ourestimated future cash flows. Over the last tenyears, our equipment utilization rate has aver-aged approximately 90%; however, if a drillingunit incurs significant idle time or receives day-rates below operating costs, its carrying valuecould become impaired. The estimates, assump-tions and judgments used by management in theapplication of our property and equipment andasset impairment policies reflect both historicalexperience and expectations regarding futureindustry conditions and operations. The use ofdifferent estimates, assumptions and judgments,especially those involving the useful lives of ourrigs and vessels and expectations regardingfuture industry conditions and operations, wouldlikely result in materially different carrying valuesof assets and results of operations.

We conduct operations and earn income innumerous foreign countries and are subject tothe laws of taxing jurisdictions within thosecountries, as well as United States federal andstate tax laws. At September 30, 2006, we have a$16.0 million net deferred income tax liability.This balance reflects the application of ourincome tax accounting policies in accordancewith statement of Financial Accounting Stan-dards No. 109, “Accounting for Income Taxes”.Such accounting policies incorporate estimates,

assumptions and judgments by management rel-ative to the interpretation of applicable tax laws,the application of accounting standards, andfuture levels of taxable income. The estimates,assumptions and judgments used by manage-ment in connection with accounting for incometaxes reflect both historical experience andexpectations regarding future industry conditionsand operations. Changes in these estimates,assumptions and judgments could result in mate-rially different provisions for deferred and currentincome taxes.

Effective October 1, 2005, we adopted State-ment of Financial Accounting StandardsNo. 123(R), “Share-Based Payment”, orSFAS 123(R), using the modified prospectiveapplication transition method. Under this method,stock-based compensation cost is measured atthe grant date, based on the calculated fair valueof the award, and is recognized as an expenseover the requisite service period (generally thevesting period of the equity grant). In addition,stock-based compensation cost recognizedincludes compensation cost for unvested stock-based awards as of October 1, 2005. Prior toOctober 1, 2005, we accounted for share-basedcompensation in accordance with AccountingPrinciples Board Opinion No. 25, “Accounting forStock Issued to Employees”, or APB No. 25. Noshare-based employee compensation cost hasbeen reflected in net income prior to October 1,2005. Before that date, we reported the entire taxbenefit related to the exercise of stock options asan operating cash flow. SFAS 123(R) requires usto report the tax benefit from the tax deductionthat is in excess of recognized compensationcosts (excess tax benefits) as a financing cashflow rather than as an operating cash flow. Thecumulative effect of the change in accountingprinciple from APB No. 25 to FAS 123(R) was notmaterial.

22

%%TRANSMSG*** Transmitting Job: H41700 PCN: 017000000 ***%%PCMSG|22 |00006|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

RECENTLY ISSUED ACCOUNTINGPRONOUNCEMENTS

In June 2006, the FASB issued FIN 48,“Accounting for Uncertainty in Income Taxes —an Interpretation of FASB Statement 109.” FIN 48prescribes a comprehensive model for recogniz-ing, measuring, presenting, and disclosing uncer-tain tax positions within the financial statements.The provisions of FIN 48 are effective for fiscalyears beginning after December 15, 2006. We arecurrently evaluating the impact of the adoption ofFIN 48 on our consolidated financial position,results of operations and cash flows.

In September 2006, the FASB issuedSFAS No. 157, “Fair Value Measurements”, orSFAS No. 157, which defines fair value, estab-lishes methods used to measure fair value andexpands disclosure requirements about fair valuemeasurements. SFAS No. 157 is effective forfinancial statements issued for fiscal year begin-ning after November 15, 2007, and interim peri-ods within those fiscal periods. We are currentlyanalyzing the provisions of SFAS No. 157 anddetermining how it will affect accounting policiesand procedures, but we have not yet made adetermination of the impact the adoption willhave on our consolidated financial position,results of operations and cash flows.

In September 2006, the SEC issued StaffAccounting Bulletin No. 108, “Considering theEffects of Prior Year Misstatements when Quanti-fying Misstatements in Current Year FinancialStatements”, or SAB 108, which provides guid-ance on the consideration of the effects of prioryear misstatements in quantifying current yearmisstatements for the purpose of a materialityassessment. SAB 108 requires that the material-ity of the effect of a misstated amount be evalu-ated on each financial statement and the relatedfinancial statement disclosures, and that materi-ality evaluation be based on quantitative andqualitative factors. SAB 108 is effective for fiscal

years beginning after November 15, 2006. We donot believe this guidance will have a materialimpact on our financial position, results of opera-tions or cash flows.

DISCLOSURES ABOUT MARKET RISK

We are exposed to market risk, includingadverse changes in interest rates and foreigncurrency exchange rates as discussed below.

Interest Rate Risk

All of the $64 million of long-term debt out-standing at September 30, 2006, was floating ratedebt. As a result, our annual interest costs infiscal year 2006 will fluctuate based on interestrate changes. Because the interest rate on ourlong-term debt is a floating rate and due to ourdebt maturing in 2008, the fair value of our long-term debt approximated carrying value as of Sep-tember 30, 2006. The impact on annual cash flowof a 10% change in the floating rate (approxi-mately 70 basis points) would be approximately$0.4 million, which we believe to be immaterial.We did not have any open derivative contractsrelating to our floating rate debt at September 30,2006.

Foreign Currency Risk

Certain of our subsidiaries have monetaryassets and liabilities that are denominated in acurrency other than their functional currencies.Based on September 30, 2006 amounts, adecrease in the value of 10% in the foreigncurrencies relative to the United States dollarfrom the year-end exchange rates would result ina foreign currency transaction gain of approxi-mately $0.2 million. Thus, we consider our cur-rent risk exposure to foreign currency exchangerate movements, based on net cash flows, to beimmaterial. We did not have any open derivativecontracts relating to foreign currencies at Sep-tember 30, 2006.

23

%%TRANSMSG*** Transmitting Job: H41700 PCN: 018000000 ***%%PCMSG|23 |00008|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

MANAGEMENT’S REPORT ON INTERNAL CONTROLOVER FINANCIAL REPORTING

Company management is responsible for establishing and maintaining adequate internal controlover financial reporting as defined in Rules 13a-15(f) and 15d-15(f) under the Securities Exchange Act of1934. Our internal control over financial reporting was designed by management, under the supervisionof the Chief Executive Officer and Chief Financial Officer, to provide reasonable assurance regarding thereliability of financial reporting and the preparation of financial statements for external purposes inaccordance with accounting principles generally accepted in the United States, and includes thosepolicies and procedures that:

(i) pertain to the maintenance of records that in reasonable detail accurately and fairly reflectthe transactions and dispositions of the assets of the Company;

(ii) provide reasonable assurance that transactions are recorded as necessary to permit prepa-ration of financial statements in accordance with accounting principles generally accepted in theUnited States, and that receipts and expenditures of the Company are being made only inaccordance with authorizations of management and directors of the Company; and

(iii) provide reasonable assurance regarding prevention or timely detection of unauthorizedacquisition, use or disposition of the Company’s assets that could have a material effect on thefinancial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent ordetect misstatements. Also, projections of any evaluation of effectiveness to future periods are subjectto the risk that controls may become inadequate because of changes in conditions, or that the degree ofcompliance with the policies and procedures may deteriorate.

Management assessed the effectiveness of the Company’s internal control over financial reportingas of September 30, 2006. In making this assessment, management used the criteria set forth by theCommittee of Sponsoring Organizations of the Treadway Commission (COSO) in Internal Control-Integrated Framework.

Based on our evaluation under the framework in Internal Control — Integrated Framework, manage-ment has concluded that the Company maintained effective internal control over financial reporting asof September 30, 2006. PricewaterhouseCoopers LLP, our independent registered public accounting firm,has audited our assessment of the effectiveness of the Company’s internal control over financialreporting as of September 30, 2006, as stated in their report, which appears on the following page.

ATWOOD OCEANICS, INC.

by

John R. IrwinDirector, Presidentand Chief Executive Officer

James M. HollandSenior Vice President andChief Financial Officer

December 12, 2006

24

%%TRANSMSG*** Transmitting Job: H41700 PCN: 019000000 ***%%PCMSG|24 |00008|Yes|No|12/18/2006 18:47|0|0|Page/graphics valid 12/18/2006 18:47 -- Color: D|

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors and Shareholders of Atwood Oceanics, Inc.

We have completed integrated audits of Atwood Oceanics, Inc.’s 2006 and 2005 consolidatedfinancial statements and of its internal control over financial reporting as of September 30, 2006 and anaudit of its 2004 consolidated financial statements in accordance with the standards of the PublicCompany Accounting Oversight Board (United States). Our opinions, based on our audits, are presentedbelow.

Consolidated financial statements

In our opinion, the accompanying consolidated balance sheets and the related consolidatedstatements of operations, of cash flows and of changes in shareholders’ equity present fairly, in allmaterial respects, the financial position of the Company at September 30, 2006 and 2005, and the resultsof their operations and their cash flows for each of the three years in the period ended September 30,2006 in conformity with accounting principles generally accepted in the United States of America.These financial statements are the responsibility of the Company’s management. Our responsibility is toexpress an opinion on these financial statements based on our audits. We conducted our audits of thesestatements in accordance with the standards of the Public Company Accounting Oversight Board(United States). Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit offinancial statements includes examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements, assessing the accounting principles used and significantestimates made by management, and evaluating the overall financial statement presentation. We believethat our audits provide a reasonable basis for our opinion.

As discussed in Note 3 to the consolidated financial statements, in 2006 the Company changed itsmethod of accounting for share-based compensation as a result of adopting the provisions of Statementof Financial Accounting Standards No. 123(R), “Share-Based Payment.”

Internal control over financial reporting

Also, in our opinion, management’s assessment, included in the accompanying Management’sReport on Internal Control Over Financial Reporting, which appears on the preceding page, that theCompany maintained effective internal control over financial reporting as of September 30, 2006 basedon criteria established in Internal Control — Integrated Framework issued by the Committee of Sponsor-ing Organizations of the Treadway Commission (COSO), is fairly stated, in all material respects, basedon those criteria. Furthermore, in our opinion, the Company maintained, in all material respects,effective internal control over financial reporting as of September 30, 2006, based on criteria establishedin Internal Control — Integrated Framework issued by the COSO. The Company’s management isresponsible for maintaining effective internal control over financial reporting and for its assessment ofthe effectiveness of internal control over financial reporting. Our responsibility is to express opinions onmanagement’s assessment and on the effectiveness of the Company’s internal control over financialreporting based on our audit. We conducted our audit of internal control over financial reporting inaccordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance aboutwhether effective internal control over financial reporting was maintained in all material respects. Anaudit of internal control over financial reporting includes obtaining an understanding of internal controlover financial reporting, evaluating management’s assessment, testing and evaluating the design and

25

%%TRANSMSG*** Transmitting Job: H41700 PCN: 020000000 ***%%PCMSG|25 |00008|Yes|No|12/18/2006 18:47|0|0|Page is valid, no graphics -- Color: D|

operating effectiveness of internal control, and performing such other procedures as we considernecessary in the circumstances. We believe that our audit provides a reasonable basis for our opinions.

A company’s internal control over financial reporting is a process designed to provide reasonableassurance regarding the reliability of financial reporting and the preparation of financial statements forexternal purposes in accordance with generally accepted accounting principles. A company’s internalcontrol over financial reporting includes those policies and procedures that (i) pertain to the mainte-nance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositionsof the assets of the company; (ii) provide reasonable assurance that transactions are recorded asnecessary to permit preparation of financial statements in accordance with generally accepted account-ing principles, and that receipts and expenditures of the company are being made only in accordancewith authorizations of management and directors of the company; and (iii) provide reasonable assuranceregarding prevention or timely detection of unauthorized acquisition, use, or disposition of thecompany’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent ordetect misstatements. Also, projections of any evaluation of effectiveness to future periods are subjectto the risk that controls may become inadequate because of changes in conditions, or that the degree ofcompliance with the policies or procedures may deteriorate.

PricewaterhouseCoopers LLP

Houston, TexasDecember 12, 2006

26

%%TRANSMSG*** Transmitting Job: H41700 PCN: 021000000 ***%%PCMSG|26 |00006|Yes|No|12/14/2006 11:34|0|0|Page/graphics valid 12/19/2006 22:40 -- Color: D|

Atwood Oceanics, Inc. and Subsidiaries

CONSOLIDATED BALANCE SHEETS

(In thousands) 2006 2005

September 30,

ASSETSCURRENT ASSETS:

Cash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 32,276 $ 18,982Accounts receivable, net of an allowance of $750 and $189 at September 30,