AttrActiveness of BrAzil As An internAtionAl investment And Business...

152

ATTRACTIVENESS OF BRAZIL AS AN INTERNATIONAL INVESTMENT AND BUSINESS HUB 2012 /# 2

-

Upload

duongkhanh -

Category

Documents

-

view

216 -

download

2

Transcript of AttrActiveness of BrAzil As An internAtionAl investment And Business...

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 2012 /# 2

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 2012 /# 2

4 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

Brazil’s rise as a global economic power is undeniable. in recent decades the country finally left behind the old promise of “country of the future”; however, complete ful-fillment requires capturing international recognition of Brazil’s transformation into an investment and business hub.

this document is the second edition of our report entitled Attractiveness of Brazil as an international investment and business hub, published by BrAin for the first time in 2011. this report attempts to shed new light on the attractiveness of an investment and business hub, identifying initiatives that will make the country even more at-tractive to investors and business executives, as well as to all other players involved. this version brings an updated view of Brazil’s performance compared to a number of selected nations along a set of seven pillars, considered to be essential for the at-tractiveness of an investment and business hub.

in preparing this material BrAin conducted extensive research and analysis, with the support of the Boston consulting Group. this document is a result of this effort and describes in detail the attractiveness of Brazil as a latin American investment and business hub. it also defines a number of indicators that can be used to dynamically track the position of the country, and lists next steps and initiatives that will further this position.

Created in 2010, BRAiN’s mission is to ensure the creation of a multi-sector vision of Latin America as a strongly interconnected regional business hub, within which Brazil should be one of the preeminent hubs.

Additional information about BRAiN and its vision is available at www.brainbrasil.org.

PrefAce

6 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

01

02

03

04

05

06

07

executive summary 08

dashboard of Brazil’s attractiveness 16

macroeconomic environment 26

institutional environment 40

talent and human capital 54

Physical infrastructure 70

financial infrastructure 86

connectivity 102

image of the country 124

Appendix: details of the indicators used 140

contents

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 7

8 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

the attractiveness of Brazil as an investment and business destination is a recurring and very important theme. As part of its activities to articulate and catalyze the crea-tion of an international hub in Brazil, BrAin - Brasil investimentos & negócios (Brazil investments & Business) is issuing this second edition of its Attractiveness of Brazil as an international investment and business hub report, first published in 2011. this new study, supported by extensive research and data analysis, re-examines the seven pillars that constitute BrAin’s vision of the fundamental prerequisites for the creation and excellence of an attractive investment and business hub: macroeconomic envi-ronment, institutional environment, talent and human capital, physical infrastructure, financial infrastructure, connectivity and image of the country.

Brazil has numerous characteristics that make it suitable for the international invest-ment and business hub status, such as the strength of the economy and its importance within its region, its financial infrastructure as well as political and institutional stability.

however, its prominence in the international scenario still faces numerous challenges that the country must address, such as the quality of the education, an irrational tax system and poor transport infrastructure. these challenges represent ultimately ad-ditional costs for investing and doing business in the country. however, given the advances of the past decade, including the country’s resilience to recent crises, the outlook is far more positive for Brazil.

Below are the main elements of each of the pillars analyzed:

1) Macroeconomic environment: Brazil is currently a strong economy with global relevance. in 2011 it became the world’s sixth largest economy in terms of nominal GdP. it is also a stable economy, having kept inflation in single digits since 2002, with an average consumer price index (iPcA1) of 5.8% a year between 2003 and 2011. in addition, exchange volatility has been low over the past five years. the nation also proved quite resilient to the effects of the global economic crisis, growing at an annual rate of 4.4% between 2006 and 2010. however, growth slowed to 2.7% in 2011, a clear indication that there are challenges ahead if Brazil is to keep growing with no increase in inflation. in particular, a new model for growth should be pursued, one that is not so much dependent on consumer spending as it has been recently.

executive summAry

1 Ample consumer Price index (iPcA), the official index the Brazilian Govern-ment has used to measure inflation since 1999

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 9

in order to keep on this positive path for growth, it is essential that Brazil increases its investment capacity. Between 2002 and 2011, investment in Brazil averaged 17.3% of the GdP, well below countries such as china and india, and even other latin Ameri-can countries such as chile and mexico. investment as a percentage of GdP in these countries was 41.5%, 29.9%, 21.5% and 20.6% respectively over this same period. increasing the rate of investment is particularly critical in light of the low average rate of internal savings in Brazil, which was only 19% from 2008 to 2011. this means that attracting foreign investment is key for future growth.

continued reduction in the nominal public deficit, which decreased from 4.5% of the GdP in 2002 to 2.6% in 2011 as well as continued fiscal discipline are the basis for continued economic stability and thus attracting foreign capital, and essential for increasing the investment rate and consequently the country’s growth over the coming years.

2) Institutional environment: Brazil has reached important milestones in its political and institutional systems. it has consolidated its position as a democracy, with regular, direct and multi-party elections, and there is no sign of any internal or external conflict.

however, it faces important challenges in institutional aspects related to the economy, in particular those related to its complex tax system and bureaucracy. regarding the former, it must be mentioned how difficult and complex it is for companies to calculate and pay taxes such as icms, iss, Pis and cofins. regarding the latter, bureaucracy is a clear hurdle for business activities, and according to an imd survey2, Brazil is more bureaucratic than china or mexico, and very far from the main international invest-ment and business hubs such as the united Kingdom and the united states of America. merely as an example, one could mention the process of opening a business, which is complex and decentralized, with numerous steps at the municipal, state and federal levels, taking an average of 119 days in são Paulo, Brazil’s main business city.

2 the 2012 World competitiveness year-book, an annual global survey of middle

and senior managers in 59 countries

10 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

however, progress has been made and further progress is expected in the future, such as the government of minas Gerais’ initiative to optimize the process to open a busi-ness, which has already proven a successful model and may be implemented in other eight states in 2012. in addition to rationalizing bureaucracy, the Brazilian state took an additional step in institutional matters, making government data more transparent with the signing of the law # 12,527 in november 2011 that requires the disclosure of public information, including civil servants’ salaries.

3) Talent and human capital: Brazil has a solid and positive demographic base, and it is the world’s largest economy with an economically active base growing fast enough to supply the expected increase in the demand for labor in the coming years.

however, if it is to leverage this advantage and become more attractive, Brazil must improve significantly the training and qualification of its workforce. net enrollment rates of 87% in primary school (grades 1 - 5) and 69% in secondary school (grade 6 to the end of secondary school) are close to world averages. however, this does not mean that the quality of the education is good. to illustrate the problem, in 2009 the average score for Brazilian students in the international PisA3 test was 401, well below the average of 497 for the oecd countries and 468 for all countries evaluated. the performance of secondary school students is also unsatisfactory, scoring below the expected in the 2011 Prova Brasil, with essentially no change compared to 2009.

in terms of higher education, net enrollment in Brazil is 27%, below the world aver-age of 40%, and has the same quality problems as primary and secondary education. regarding the alignment between higher education and market needs, an imd survey4 reveals that Brazil is the worst of the 13 nations compared. in addition to this, only 9% of the programs analyzed were rated as good in the 2010 General course index, Brazil’s ministry of education’s assessment of the quality of higher education5.

changes are underway and the Brazilian Government is making an effort to grant scholarships and invest in technical education, with programs such as Prouni, which granted 195 thousand scholarships for higher education in the first half of 2012, and PronAtec, created in late 2011 to promote technical education. Additionally, the pri-vate sector has numerous initiatives to give people the training and knowledge nec-essary for their activities. however, taking benefit from the country’s demographic advantage requires a continuous effort in training the population in order to meet market needs, with long-term impacts.

3 Programme for international student Assessment: a test ap-plied from time to time by the oecd to 15-year- old students (equivalent to the 9th grade) in 65 countries

4 the 2012 World competitiveness yearbook, an annual global survey of middle and senior managers in 59 countries

5 schools scoring 4 or 5 on a scale of 1 to 5, with the higher scores being better

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 11

12 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

4) Physical infrastructure: the availability of basic services within Brazil’s urban cent-ers is adequate, with 99% and 85% of the urban population having access to clean water and basic sanitation, respectively. in this regard, Brazil performs better than other Brics, and it is close to the level of developed nations.

however, its performance along other dimensions is still quite poor. in transportation there are clear infrastructure bottlenecks, resulting from a slowdown in investments in this sector dating back to more than three decades - in the seventies the country invested 5.4% of its GdP in infrastructure, but by the two thousands was investing only 2.1%. this puts Brazil at a disadvantage compared to developed nations with established infrastructure and emerging nations such as china, which in 2010 spent 11% of its GdP on infrastructure, and india, which invested 5.1% between 2004 and 2008. And the latter plans to invest 7.6% of its GdP a year between 2008 and 2012.

Addressing this challenge is part of the Brazilian Government’s current agenda, which includes greater involvement of the private sector. concessions for the private opera-tion of three airports - cumbica (sP), viracopos (sP) and Juscelino Kubitschek (df), awarded in the first half of 2012, are illustrations of the Government’s greater willing-ness to allow private participation in physical infrastructure investments. Additional concessions and PPPs (public-private partnerships) are planned for the coming years. the investment in logistics Program announced in August 2012 points to clear oppor-tunities in the road, railway, port and airport sectors. in addition to attracting invest-ments and creating jobs, these works will also make the country more competitive as an investment and business hub.

5) Financial infrastructure: Brazil has solid financial regulations, for which it is recog-nized worldwide. its rules of prudence, for example, make fraudulent market schemes, such as the madoff affair, more difficult to happen in the country. this is probably the pillar in which Brazil stands out the most compared to other investment and business hubs. it was largely due to the solidity of its banking infrastructure that Brazil weath-ered the 2008 financial crisis so well.

In transportatIon there are clear Infrastructure bottlenecks, resultIng from a

slowdown In Investments In thIs sector datIng back to more than three decades

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 13

in terms of funding for businesses, in recent years the number of bank loans has in-creased, and companies have diversified their sources of funds, in particular using the stock market. nevertheless, there remain opportunities for greater diversification of the instruments used.

it is hoped that falling real interest rates will foster the debentures market, for in-stance. the use of this financing instrument in Brazil is rather limited in comparison to other countries: it represents less than 1% of the GdP, compared to 36% in south Ko-rea. Also, its growth in real terms in Brazil, about 4% a year between 2004 and 2011, was quite low compared to the 15% annual increase in bank credit during the same period. When it sought to replicate the success of the novo mercado6 self-regulation initiative to private-debt issues, the market organized and created added incentives for businesses to use this type of financing.

6) Connectivity: Brazil captures a major share of latin America’s inward foreign direct investment (fdi). in 2011, 41.1% of the total fdi in latin America went to Brazil, and it is the major destination of large north American, european and Asian companies.

however, there’s room for growth, as Brazil attracts proportionally less fdi than its share of regional GdP – the country has an fdi to GdP ratio of 0.957, while chile has 3.13.

exports of goods and services increased 12.4% and 12.5% a year respectively be-tween 2007 and 20118, a rate that is larger than those experienced by the rest of latin America and the world at large. however, Brazil’s share of global trade is small, something around 1% of the total.

in order to bolster both the flows of capital and goods and services, Brazil could pro-mote further integration with other countries in the form of international trade agree-ments as a means to soften still-existing protectionist policies.

6 Bm&fBovesPA rules for listing that de-mand corporate governance standards

above those required by law

7 Average between 2009 and 2011

8 imports of goods and services in-creased 16.7% and 19.7% respectively

over the same period

14 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

7) Image of the country: Brazil has a positive image as a tourist destination, accord-ing to the Anholt-GfK roper nation Brands index, and cities such as são Paulo and rio de Janeiro are recognized as some of the best places to do business in latin America, as shown in the ranking published by the Américaeconomía magazine.

in terms of image as a place to do business, Brazil could increase its efforts to promote itself within a broader context, which are still quite limited. here one could mention the Best BrAzil initiative, which presents Brazil’s financial and capital markets to for-eign investors, and APex, whose goal is to promote the country’s foreign trade.

Brazil has a unique opportunity to promote itself abroad over the next few years, given the exposure it will get for hosting the 2014 fifA World cup and the 2016 olympic Games, which should attract some 600 thousand visitors in 2014, and 380 thousand in 2016. if Brazil successfully exports its image during these sports events, the current flow of tourists, which in 2011 was 5.4 million, could reach a higher level and offer the country an opportunity to improve its image abroad as a destination for tourism and, more importantly, for business.

in the next section, we present a dashboard of indicators with a comparative analysis of Brazil. the country is compared to 13 selected countries in each of the 57 dimensions of the 7 pillars of attractiveness. in the sections ahead, we discuss Brazil’s position as an investment and business hub in each of these dimensions and pillars in greater depth.

brazIl has a unIque opportunIty to promote

Itself abroad over the next few years, gIven the

exposure It wIll get for hostIng the fIfa world cup

and the olympIc games

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 15

16 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

A dAshBoArd of BrAzil's AttrActiveness

to analyze the attractiveness of a hub we considered two main streams: the country’s intrinsic characteristics and its connectivity. intrinsic characteristics are those that defi-ne a country as attractive in itself: a strong economy, its physical, financial, legal and regulatory infrastructure, and a trained and qualified population. connectivity, meaning flows, defines the attractiveness of the network to which the country belongs, reflec-tion of the number and quality of its intra-regional connections, and its connections to other relevant hubs around the world. these streams make up a country’s attractive-ness as a hub and allow a nation to compete with other global hubs for resources for itself and for its region of influence.

these characteristics are detailed in seven pillars that constitute BrAin’s vision of the fundamental prerequisites for the creation and excellence of an attractive investment and business hub: macroeconomic environment, institutional environment, talent and human capital, physical infrastructure, financial infrastructure, connectivity and image of the country (see Exhibit 1).

from this starting point, separate dashboards were created for each pillar to enable easy comparison of how Brazil is doing in relation to a list of 13 countries. these dash-boards contain 57 dimensions, representing the main elements analyzed in this report. the objective is to track Brazil’s progress over the years so as to enable mapping the next steps required to enhance Brazil’s attractiveness as an investment and business hub. these metrics take into consideration the quality of the source, the availability of data for different countries, and the possibility of continuous monitoring over time.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 17

exhiBit 1the seven pillars that underlie the fundamental requirements for creating and excelling as an investment and business hub

MACRoeCoNoMIC eNvIRoNMeNT

TALeNT AND HUMAN CAPITAL

FINANCIAL INFRAsTRUCTURe

INsTITUTIoNAL eNvIRoNMeNT

PHysICAL INFRAsTRUCTURe

CoNNeCTIvITy

IMAge oF THe CoUNTRy

steady economic growth and little uncertainty regarding interest and the exchange rate are examples of the underlying conditions required for creating an international investment and business hub in any country

An adequate supply of talents, not only in terms of numbers but also in terms of their qualification and training, which must be aligned with what the job market is looking for, along with possibility of attracting and bringing in experts from outside the country are also requirements that any location that aspires to be an international hub must fulfill

the existence of capable financial intermediaries, continuous access to several sources of funding and tools to mitigate risk all directly support the development of an investment and business hub

A solid state of law, enabling economic agents to fully meet their obligations and transparent and efficient administrative processes are key elements when it comes to qualifying a country as a hub, in particular compared to other potential hubs

multimodal shipping options that enable flows into, out of and within the hub, along with access to a communications network that is competitive in terms of both cost and performance are clearly some of the factors of success for any business hub

intense trade in goods and services, capital and people flows are vital to continuously nurture an investment and business hub

A positive perception of what a country as a whole has to offer is an important asset to consolidate the position of any hub, and in particular for attracting companies and talents

18 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

P: INDICAToR BAseD oN PRojeCTeD DATA

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

mAcroeconomic environment

critical needs improvement good excellent

jPN

DeU

FRA HKg

sgPgBR UsA RUs

MeX

CHNCHLKoR

INDeCoNoMIC gRowTHP1.

BRA

eCoNoMIC voLATILITy5.jPNDeU KoRHKg UsA sgPgBR CHNRUsCHL MeX IND

FRA

BRA

FIsCAL soLIDITyP3.jPN

gBR

FRA DeU KoRUsA sgP HKgMeX CHN

CHL

RUsBRA

IND

INCoMe DIsTRIBUTIoN7.

BRAHKgCHL MeX

sgP

UsARUs

CHN

jPN

IND FRA

DeUgBR KoR

jPNHKg FRAUsA

sgPgBR

RUsIND MeX

DeUCHLCHN

KoRMoNeTARy sTABILITyP2.

BRA

HUMAN DeveLoPMeNT6.DeUFRA

KoR

HKg

UsA

sgP

gBR

IND CHN RUs MeX CHL

jPN

BRA

eXTeRNAL vULNeRABILITy4.KoR sgPHKg CHNCHL MeX RUsIND

BRA

the basket of countries for comparison was made up by looking for examples of coun-tries that are recognized as investment and business hubs: the united states, the uni-ted Kingdom, hong Kong and singapore; developed nations: france, Germany, Japan and south Korea; and countries that, like Brazil, are considered emerging: russia, india, china, chile and mexico.

in order to assign countries to positions along each indicator scale, and to classify them as “excellent”, “good”, “needs improvement” and “critical”, one of two rationales was used: (1) where available, a publicly established social, political or economic consen-sus, (2) where no such consensus exists, a statistical rationale where the population average is the divider between the “good” and “needs development” levers, and a standard deviation added to or subtracted from the average and used as the divider between the “excellent” and “critical” levels respectively.

details regarding indicator sources and the criteria for allocating countries along each scale are available in the Appendix of this report.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 19

1. DATA CANNoT Be UPDATeD FRoM THe 2011 ATTRACTIveNess RePoRT

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

institutionAl environmentcritical needs improvement good excellent

jPN UsA HKggBR

sgP

RUs CHN

CHL

MeX FRA DeU

IND KoRQUALITy oF RegULATIoNs

BRA

2.

LegAL seCURITyjPN

KoR

HKg

sgP

gBR

CHLMeX INDRUs FRA

DeU

UsACHN

BRA

3.

LABoR MARKeT FLeXIBILITy1FRA KoR jPNDeU UsA sgPgBRCHLCHN

MeX HKgINDRUs

BRA

4.

jPN sgPgBR

HKgUsA

FRA

RUs

KoR

IND CHL

MeX

CHNPoLITICAL sTABILITy

DeUBRA

1.

eAse oF oPeNINg A BUsINess1

jPNKoR

UsA

sgP gBR

MeX

CHN INDRUs

CHL FRA

BRA

5.

How eAsy IT Is FoR BUsINesses To PAy TAXes DeU FRA

HKgUsAKoR gBR

sgPCHN CHL

RUsjPNMeX INDBRA

6.

20 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

tAlent And humAn cAPitAlcritical needs improvement good excellent

FRA DeUgBRHKg sgPRUsCHL CHNINTeNsITy oF ReseARCH AND DeveLoPMeNT8.

BRAIND

KoR

jPN

DeU CHL RUsgBRDIAsPoRA MANAgeMeNT11.

BRA

sgP HKg IND

FRA

sgP HKg

RUs

CHLCHNAvAILABILITy oF QUALIFIeD MANAgeRs AND eNgINeeRs7.

BRA

UsA

KoR INDDeU gBRjPN

KoR

jPN

gBRDeU FRA

RUs

IND MeXCHNDeMogRAPHIC CoNTINgeNTP1.

BRAUsA

DeU

gBR jPNRUs

IND

MeX

CHLCHNQUANTITy oF PRIMARy AND seCoNDARy eDUCATIoN2.

BRAHKg UsA sgP FRA

KoR

FRA DeU HKgKoRjPNRUsMeX CHL CHNQUALITy oF PRIMARy AND seCoNDARy eDUCATIoN13.

BRA

sgPUsA gBR

FRADeU HKg

gBR

KoRjPN RUsIND MeXCHN

CHLQUANTITy oF HIgHeR eDUCATIoN4.

BRAsgP UsA

FRA DeUUsA sgPKoR

RUs

IND

MeX

CHN CHLALIgNMeNT BeTweeN HIgHeR eDUCATIoN AND THe MARKeT5.

BRAgBR HKgjPN

FRA DeUgBR HKgsgPjPN KoR

RUs

INDCHLCHNINTeRNATIoNALIzATIoN oF THe CoUNTRy’s eDUCATIoN (FoReIgN LANgUAges AND eXPeRIeNCe)

6.

BRAUsA

MeX

KoR DeUFRA

gBR sgP

RUs

IND

CHN CHLCoUNTRy ATTRACTIveNess To INTeRNATIoNAL TALeNT9.

BRAMeXjPN

HKg

UsA

KoR FRA

HKg

CHLjPN CHN MeXRUs sgPTALeNT IMMIgRATIoN CoMPLeXITy10.

BRA

UsA

gBRINDDeU

P: INDICAToR BAseD oN PRojeCTeD DATA 1. DATA CANNoT Be UPDATeD FRoM THe 2011 ATTRACTIveNess RePoRT

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 21

PhysicAl infrAstructurecritical needs improvement good excellent

PoweR AvAILABILITyKoR jPN DeU FRAgBR

HKg

sgPCHNMeX CHL UsAIND

RUs

BRA

4.

BAsIC seRvICes AvAILABLe To THe URBAN PoPULATIoN1

CHN gBRsgP

FRAjPN

KoRUsA

DeU

MeXIND RUs CHLBRA

5.

FRA DeU gBRRUsIND

MeX

CHNURBAN MoBILITy1

BRAUsA

1.

jPN KoR FRA DeU

gBRUsA HKg

RUs CHN

IND

CHLMeXQUALITy oF AIR TRANsPoRT

sgPBRA

2.

QUALITy AND CosT oF TeLeCoMMUNICATIoNs

jPN DeUFRA KoRsgPgBRCHNMeX INDRUs

HKg

UsACHL

BRA

3.

1. DATA CANNoT Be UPDATeD FRoM THe 2011 ATTRACTIveNess RePoRT

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

22 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

finAnciAl infrAstructurecritical needs improvement good excellent

Use

oF

FIN

AN

CIA

L Re

soUR

Ces

sHARe oF RegIoNAL AND INTeRNATIoNAL CoMPANIes IN THe sToCK eXCHANge

jPN UsA gBR

CHN

INDRUs CHL MeX

BRAKoR sgP HKgFRA

5.

AvAILABILITy oF FINANCIAL seRvICes

KoR jPN FRA

DeU

gBRRUs

CHN

IND CHLMeXBRA

sgP

HKgUsA6.

PRojeCTIoN As AN IFCKoR DeUjPN HKg gBRFRAIND RUs MeX CHN

BRA

sgP UsA8.

KoR

FRA

jPN

gBRRUs IND CHLMeXCHN DeUeFFeCTIveNess oF FINANCIAL RegULATIoNs

BRAUsA

HKg

sgP1.

DeBeNTUResjPN

DeU

FRA KoRsgP

gBR

HKg UsACHN CHLIND MeX

BRA

3.

jPNIND

FRA

UsA gBR sgP HKg

RUs

CHN CHL

MeXsToCK eXCHANge

DeU KoRBRA

2.

CoRPoRATe CReDIT

KoR FRA

gBR

UsA CHNsgP

IND

DeUBRA

4.

sToCK eXCHANge LIQUIDITy

FRA jPN HKggBR

DeU

KoRINDCHL RUs

CHN

MeX

BRA

sgP

UsA7.

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 23

connectivity

critical needs improvement good excellent

TRA

De

CAPI

TAL

BUsI

Nes

ses

Peo

PLe

jPN KoR sgPDeUgBRUsA RUs CHNIND MeXTRADe IN gooDs

FRA

HKgCHL2.

BRA

KoR jPN DeU UsARUs CHN CHLINDMeX

sgP FRAgBR

INTeRNATIoNAL oPeNNess FoR TRADe IN gooDs1

1.

BRAHKg

PeoPLe MoBILITyCHL IND CHN RUsMeX HKg

gBRjPN

FRA11.

BRAUsAsgP

KoRDeU

CHN

IND RUsUsA

MeX

CHLjPN

KoR

HKgsgPgBRDeU FRA5.

BRA

CAPITAL FLows

INTeRNATIoNAL oPeNNess FoR TRADe IN seRvICes1

3.jPNDeU

FRAKoRsgP CHNIND MeX gBR

HKg

CHL

BRAUsA

TRADe IN seRvICesFRA KoR

sgP

gBRCHN CHL INDMeX jPN

RUs

UsA DeU HKg4.

BRA

CHNCHLMeX FRAjPN

gBR

sgP DeUKoR6.

BRA

HKg

INTeRNATIoNAL AgRe-eMeNTs ALLowINg CAPITAL FLows1 INDRUs

UsA

CHN RUs CHL

IND

MeX gBR HKgUsA jPNKoR7.

BRA

DeU

sgPFRANATIoNAL RegULA-TIoNs sUPPoRTINg INTeRNATIoNAL CAPITAL FLows1

eXPANsIoN oF THe CoUNTRy’s MULTINATIoNALs IND

RUs MeX CHNCHL HKg gBR UsAjPN DeU FRA

KoR8.

BRAsgP

eAse oF eNTRy FoR FoReIgN MULTINATIoNALs1

IND

CHL

MeX RUsCHN UsAKoR FRA9.

gBR

sgP jPN

oPeNNess To IMMIgRANTs1

IND RUsCHN MeX CHL gBR HKgKoR jPN DeU10.

BRA

UsA sgPFRA

BRA

1. DATA CANNoT Be UPDATeD FRoM THe 2011 ATTRACTIveNess RePoRT

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

24 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

imAGe of the country

critical needs improvement good excellent

FRA DeU CHLgBR

UsA

sgP HKgjPN KoRRUs IND

MeX

CHNCULTURAL oPeNNess6.

BRA

HKg sgP

UsA

DeU

RUs

CHL

FRA

KoR INDFoReIgN INTeResT IN THe CoUNTRy’s INvesTMeNT AND BUsINess

2.

BRA

jPN

MeX CHN gBR

KoR

CHN FRAHKg

MeX

RUsCHLQUANTITy oF vIsIToRs9.

BRAIND jPN

DeU gBR UsA

sgP

CHL sgP

RUs

UsAgBRCHN

MeX

IMAge As A PLACe To Do BUsINess1.

BRA

IND FRA jPN

KoR

DeU

gBR

DeUHKg sgP

KoR CHN

RUs IND MeXCHL jPNATTRACTIveNess FoR INTeRNATIoNAL eveNTs3.

BRAUsAFRA

FRA

DeU gBRKoR jPNCHLMeXIND RUsCHNsUsTAINABILITy4.

BRAsgP

UsA

KoR gBR

FRA

UsA sgPIND DeU

RUs

CHN CHL jPNQUALITy oF LIFe5.

BRAHKg

MeX

CHLKoR

jPN

gBR sgP

HKg

UsARUs

CHN

INDPeRsoNAL sAFeTy AND AsseT seCURITy7.

BRAMeX FRA DeU

jPN DeU

FRA

sgP RUsCHL CHNIMAge FoR ToURIsM AND LeIsURe8.

BRA

INDKoR

MeX UsA

gBR

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 25

26 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

01MacroeconoMic environMent

to assess the attractiveness of an investment and business hub it is essential to look at the country’s macroeconomic scenario. stable economies that are growing sustainably and that offer suitable financing terms are able to leverage the strength of their local businesses and create a virtuous economic circle.

in this chapter we analyze the performance of Brazil’s macroeconomic environment along three dimensions - growth, predictability and financing terms.

growthBrazil continues to stand out in the global context, following a trend that has consoli-dated over recent years. Brazil passed the uK in nominal GdP in 2011, thus becoming the world’s sixth largest economy. Although its growth in 2011 was only 2.7%, below the 4.4% average for the period between 2006 and 2010, the outlook remains good for Brazil, and by 2020 the country should go up one more point in the ranking of the world’s largest economies (see Exhibit 2).

main aspects of the macroeconomic environment pillar

growth: the size of a country’s economy and conditions to ensure long term growth are essential for business expansion and to improve the quality of life of the popula-tion as a whole.

Predictability: Predictability is critical to generate trust and facilitate business opera-tions, in this way increasing the likelihood that economic agents invest in the country.

Financing terms: the financial capability of a nation is extremely important for main-taining a healthy macroeconomic environment.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 27

9 this index ranges from 0 to 1. higher scores indicate greater social inequality

10 source: de volta ao país do futuro: crise europeia, projeções e a nova

classe média (Back to the country of the future: european crisis, projections and

the new middle class), 2012, fundação Getúlio vargas center for social Policies

With the increase in GdP, income distribution as measured by the Gini index9 also improved. in 2002 the Gini index for Brazil was 0.59, and in 2012 should reach 0.5210. nevertheless, social inequality is still large compared to developed nations such as Germany or france, or even some emerging nations such as india and china, with much lower scores: 0.28, 0.33, 0.37 and 0.42 respectively.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

1980 1990 2000 2010 2011 2020 2030

exhiBit 2a solid macroeconomic environment is key for a favorable business environment

World ranking of countries by GDP (US$)1Selected country growths 1996-2011

1. Based on the nominal GDP of the countries in US dollars using the average US$ exchange rate for the yearNote: According to the most recent data from EIU in May 2012 / Source: EIU Country Data; BCG analysis

In 2011, brazil overtook the uk to become the world’s 6th largest economy

furthermore, it continues grows at satisfactory rates, despite a recent slowdown

cAGr by period (%)15

10

5

0

1996-2000

BRA BRABRA BRACHN CHNCHN CHNUSA USAUSA USA2001-2005

Brazil’s growth is stable: variation between

2006 and 2010Brazil: 0.71 china: 0.19

usA: 3.73

2006-2010 2010-2011

2.02

2.78

9.76

2.39

4.45

11.20

0.73

2.74

9.20

1.74

8.63

4.30

28 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 29

income distribution is also reflected in the growth of the middle class11, which in 2011 made up 55% of Brazil’s population, compared to 38.6% in 200212. According to the international labor organization13, a favorable economy, formal jobs14 and a real in-crease in the minimum wage15 all contributed to better income distribution.

despite better income distribution, Brazil still has a lot of room to improve in terms of its human development index. calculated based on criteria such as income, education and life expectancy, this index is measured on a scale of 0 to 1, with higher scores being better. Brazil has made progress, going from 0.665 in 2000 to 0.718 in 2011, but is still only 84th out of the 187 nations surveyed16.

the last decade has provided clear evidence of a positive cycle of growth for Bra-zil. however, the 2.7% growth the country recorded in 2011 shows that challenges remain, in particular in terms of its investment capacity, translated into Gross fixed capital formation. estimates show that Brazil would need an investment rate of around 22% of its GdP to sustain 4% annual growth. Between 2002 and 2011 Brazil averaged a rate of 17.4%, while in china the investment rate was 41.5% and in india 29.9%. even compared to other latin American countries Brazil fares poorly, as in chile the investment rate is 21.4% of the GdP, and in mexico 20.6%. thus it is critical that Brazil adjust its investment rate to ensure higher and sustained growth in future.

furthermore, one of Brazil’s greatest macroeconomic challenges in the coming years will be how to solve the paradigm of growth based on consumption. While it is undeni-able that consumer spending helped the country go through the 2008 crisis, continued use of this model could have undesirable results. unemployment at an all-time low rate - under 6% - should serve as a warning to the continued policy of economic ex-pansion based on consumer spending. the low productivity17 of the workers that are being hired is in stark contrast with the high wages offered by a heated economy. the result are products that are expensive and non competitive, but that find a market within the country because they are protected by import tariffs. continued use of a model that stimulates demand will require more expensive resources and, at the limit, could drive up inflation.

the solution for this situation could encompass three actions: the first is to adjust credit expansion and consumption, with more restrictive fiscal policies designed not to overly accelerate demand and pressure inflation; the second is improving pro-ductivity of the Brazilian workforce, investing in education and making it easier for workers who are qualified in sectors where there is a labor shortage to enter the country (this is further discussed in the talent and human capital chapter); the third action, which we will also further address along this report, are policies to increase savings and investments in the country.

11 families making be-tween r$ 1,200.00 and

r$ 5,174.00 a month, 2011 prices

12 source: A nova classe média: o lado brilhante

da base da pirâmide (the new middle class:

the bright side of the base of the pyramid),

2011, fundação Getúlio vargas center for social

Policies

13 source: Perfil do tra-balho decente no Brasil:

um olhar sobre as unidades da federação (Profile of decent work in Brazil: a look at the different states), 2012

14 Between 2003 and 2010 the number of

people holding formal jobs increased 53.6%

15 Between April 2003 and January 2010 the accumulated real in-

crease in the minimum wage was 53.7%

16 in 2000 Brazil was 71st out of 153. source:

united nations develop-ment Program - human

development report

17 Within latin America Brazil is ranked 15th in productivity, and 75th

worldwide. source: the conference Board

30 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

Predictability

inflation is one of the main factors that influence the predictability of an economy. following the hyperinflation Brazil experienced in the 1980s, important reforms in the nineties were able to contain an inertial inflation process. in addition, the formal implementation of inflation targets in 1999, which increased predictability and aligned the expectations of economic agents, was a major institutional milestone and remains a fundamental pillar of the country’s macroeconomic policy. As a result, between 2002 and 2011 the iPcA18 averaged 5.8%. Between 2012 and 2016, inflation is expected to reach 5.0% annually, which although high compared to developed nations, puts Brazil in advantage compared to india and russia. these two countries expect inflation rates of 7.7% and 5.3%, respectively.

Another important element for economic predictability is the exchange rate, as it re-duces market asymmetries and gives businesses the stability required to assess inter-national trade. even with the floating exchange system, the exchange rate fluctuation diminished over the past five years, with the us dollar remaining at between r$ 1.50 and r$ 2.40. in the early 2000s, the dollar had reached levels close to r$ 4.00.

Financing terms

the state of a country’s public finance has a major influence on its financing terms. net public sector debt as a percentage of GdP is dropping in Brazil, going from 60.4% in 2002 to 36.4% in 2011. regarding its foreign debt, in 2006 Brazil went from debtor to creditor. furthermore, the public deficit has been dropping in recent years, reaching 2.6% of the GdP in 2011 (see Exhibit 3).

the nation’s gross public debt also dropped, from a high in 2002, when it reached 70.9% of the GdP, to 66.2% in 2011. over the coming years Brazil is expected to re-main on this positive path, and by 2016 gross public debt is expected to be only 58% of the GdP19. therefore, Brazil is moving in the opposite direction of developed coun-tries such as the uK, france and singapore, whose debts are expected to keep growing and be around 90% of the GdP, and the us, with a projected debt of 113% of the GdP.

the formal ImplementatIon of InflatIon targets In 1999 was a major InstItutIonal

mIlestone and remaIns a fundamental pIllar of the country's macroeconomIc polIcy

18 Ample consumer Price index (iPcA), the official index the Government has used to measure inflation since 1999

19 source: international monetary fund (imf)

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 31

over the course of the past years the public debt has dropped to a new level...

…the same is true for the deficit

exhiBit 3financing terms in Brazil have evolved positively

Public Deficit

4.5

3.0

0

5.5% GdP

external/total (%)

26 20 16 7 -2 -16 -28 -21 -24 -36

1. Position at year end. Equivalent to the net balance of the non financial public sector and the Central Bank debt with the financial system (public and private), the non financial private sector and the other countries / Source: Brazilian Central Bank

Net Public Sector Debt

47.3

-10

0

10

20

50

40

30

60

% GdP1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

36.4

internal external total

60.4

2.9

5.2

3.6

2.0

3.3

2.6

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

32 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

in that sense, an important institutional step that contributed to this was the signing in 2000 of the complementary law #101, also known as the fiscal responsibility law, which rationalized and set limits for public spending (see Box A).

Another critical factor for a country’s financing terms is the interest rate. interest rates have been dropping in Brazil since 2006, and dropping faster in 2012, when the central Bank set its target base interest rate to the lowest level since 1986, the first year such records were kept. the Brazilian Government expects the real base interest rate to be around 2% a year by 2014 - in 2006 it was 11.7%. All of this stimulates economic activity and reduces the spread to be paid by the Government. changes in legislation governing how savings accounts are remunerated, formerly set at 6.2% a year + the tr (the Brazilian central Bank reference rate), posing a barrier to any further drop in interest rates, and the Government’s policy to cut interest rates have paved the way for cheaper financing terms, aligning Brazil with countries such as china and russia (see Exhibit 4).

Box Acontributions of the fiscal responsibility law to Brazil’s financial health

the fiscal responsibility law, enacted on may 4th, 2002, sets limits on state and municipal public spending, forcing them to stay within their budget (literally their ability to collect taxes). supported on four principles (planning, transparency, con-trol and accountability), the frl defined the parameters for fiscal organization in Brazil. the law was designed to make public finance more transparent, and make it impossible for public managers to run up large debts at the end of their mandates, that their successors then had to tackle.

Brazil was the world’s first emerging nation to approve a fiscal responsibility law, and significantly increased this nation’s maturity regarding this theme. continuing along this path requires taking a number of additional steps, such as creating the fiscal management Board and setting limits on the federal public debt.

in addition, the law could be perfected so as to provide sufficient incentives to keep the short-term fiscal balance and not compromising the long-term investments Brazil needs, such as spending on infrastructure.

source: fiscal responsibility law; Brazilian federal revenue; fGv Projetos

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 33

interest rates have dropped steadily over the years

Brazil reaches the same level as countries such as russia and china3

exhiBit 4the trend is for lower interest rates going forward

1. Average rate over the period and actual rate deflated using the IPCA 2. Estimate based on an IPCA of 5.2% and interest rate of 8% 3. Estimates for 2012 based on the median on the data collected from Bloomberg in June, 2012 / Source: Tendências Consultoria, Brazilian Central Bank, Bloomberg

12.4

10.1 9.8

11.7

interest rate1 (%) Actual interest rate %

8.0

Actual rate nominal rate

15.3

11.7

7.2

6.15.5

3.7

4.8

2.7 BRAz

il

2.7

CHiN

A

2.6

RUSS

iA

2.5

CHil

E

1.6

mEx

iCo

0.7

USA

-1.9

UNit

Ed k

iNgd

om

-2.3

emerging nations

developed nations

Brazil

in looking at financing mechanisms, it is clear that the domestic savings rate in Brazil is lower than in other countries (see Exhibit 5). Between 2008 and 2010 domestic savings in Brazil was 19%, while in china, india, chile and mexico it was 52%, 31%, 28% and 23% respectively. the low savings rate limits the country’s ability to fund any increase in investment and demands that it attract foreign sources.

Brazil is now in a more favorable position to attract foreign investment than it was in the past. in 2008 the rating agencies upped it to “investment grade”, and the country risk measured by the emBi+20 has been around 200 points since 2011, compared to more than 2,000 in 2002.

in short, financing terms in Brazil have been on a positive path in recent years, both in terms of the performance of its public accounts, and the drop in interest rates. nev-ertheless, the country must increase the domestic savings rates if it is to ensure good financing terms in future.

20 emerging markets Bond index Plus

12.0

34 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

the savings rate in Brazil is low compared to selected countries

Indicators

the dimensions selected for continuous tracking of the macroeconomic environment pillar are:

• Economic growth: the faster a country’s economy is expected to grow, the more attractive it will be for international agents. it is extremely difficult for a hub to attract investments and business if it does not rank better than other hubs competing with it for capital;

• Monetary stability: monetary stability contributes to predictable economics of a hub’s investments and business. countries where there is the expectation of high inflation are less attractive, as international agents are concerned lest the value of their investments and companies erode together with the value of the local currency;

• Fiscal solidity: if a country’s fiscal policies are inadequate, the cost of funding in gen-eral will go up, thus increasing operating costs in the economy as a whole. therefore, the more fiscally solid a country, the more attractive it will be;

12%

exhiBit 5the savings rate in Brazil is among the lowest in the world

CHiN

A

SiNg

APoR

E

iNdi

A

RUSS

iA

SoUt

H ko

REA

HoNg

koN

g

CHil

E

mEx

iCo

gERm

ANY

JAPA

N

BRAz

il

FRAN

CE

UNit

Ed k

iNgd

om USA

52% 51%

31% 31%28%

21%

18%

13%

Gross domestic savings/GDP (%)1

1. Average for 2008-2009 / Note: 2010 is the last year data is available for all of the countries in the com-parison. In 2011, gross domestic savings in Brazil amounted to 19% of the GDP / Source: World Bank

31%30%

23% 23%

19%

emerging nations

developed nations

Brazil

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 35

36 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 37

P: INDICAToR BAseD oN PRojeCTeD DATA

MAIN INTeRNATIoNAL HUBs oTHeR DeveLoPeD NATIoNseMeRgINg NATIoNs

mAcroeconomic environment

critical needs improvement good excellent

jPN

DeU

FRA HKg

sgPgBR UsA RUs

MeX

CHNCHLKoR

INDeCoNoMIC gRowTHP1.

BRA

eCoNoMIC voLATILITy5.jPNDeU KoRHKg UsA sgPgBR CHNRUsCHL MeX IND

FRA

BRA

FIsCAL soLIDITyP3.jPN

gBR

FRA DeU KoRUsA sgP HKgMeX CHN

CHL

RUsBRA

IND

INCoMe DIsTRIBUTIoN7.

BRAHKgCHL MeX

sgP

UsARUs

CHN

jPN

IND FRA

DeUgBR KoR

jPNHKg FRAUsA

sgPgBR

RUsIND MeX

DeUCHLCHN

KoRMoNeTARy sTABILITyP2.

BRA

HUMAN DeveLoPMeNT6.DeUFRA

KoR

HKg

UsA

sgP

gBR

IND CHN RUs MeX CHL

jPN

BRA

eXTeRNAL vULNeRABILITy4.KoR sgPHKg CHNCHL MeX RUsIND

BRA

• External vulnerability: the availability of reserves to honor its foreign commitments is a measure of a country’s autonomy to ensure its global financial credibility and of its dependence on foreign funds;

• Economic volatility: short term interest rates on government bonds are a good indicator of the volatility of a country’s economy and the frequency with which it must make adjustments. less volatile economies offer a more secure planning horizon for both companies and families, fostering high levels of investment and growth;

• Human development: the higher the human development index the more attrac-tive a country will be as a hub, since greater development means more talents, a larger domestic consumer market and better quality of life for its citizens;

• Income distribution: income distribution influences factors that are key for devel-oping a hub, such as the availability of talents, the size and profile of the consumer market, the country’s level of innovation and its quality of life. if the income is better distributed, these aspects will be more positive for the business hub.

the following exhibit shows how Brazil compares to other countries along the dimen-sions of the macroeconomic environment pillar:

38 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

In the fIscal solIdIty IndIcator the country proved better, but stIll requIres Improvement, especIally In lIght of hIgh levels of publIc spendIng that could be revIewed and balanced

in general Brazil is well positioned in this pillar, in particular in the future economic growth dimension. in the fiscal solidity indicator the country proved better, but still requires improvement, especially in light of high levels of public spending that could be reviewed and balanced.

it comes as no surprise that in the human development and income distribution indica-tors Brazil is at a disadvantage compared to other countries, despite the advances of the last decade.

Conclusion

Brazil clearly stands out in the world, combining growth with income distribution and economic stability. in addition, in 2011 it had the world’s sixth largest nominal GdP, and in 2012 the real interest rate reached the lowest level ever, reducing the interest on the public debt and driving a more vibrant economy.

even so, it is important to make sure the current macroeconomic policy is followed, in particular when it comes to fiscal issues and the public deficit, and that the model for growth that is primarily based on consumer spending be reviewed. in addition, the in-terest and savings rates must be addressed to ensure sustained growth at rates similar to the previous decade and continued advances in income distribution.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 39

40 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

confidence in the effectiveness of a country’s laws, translated into political stability and legal security, is an essential condition for business, and consequently for the attractiveness of a hub. A solid institutional environment that is quick and efficient, with enhanced public controls, is also a catalyst of investment and business, making negotiations safer and business operations more agile and less costly.

this chapter analyzes the current situation and the coming challenges Brazil will face in terms of the political system, the stability and clarity of its laws, legal security, and bureaucracy and business operations.

02 institutional environMent

main aspects of the institutional environment pillar

Political system: this is the foundation upon which all of a country’s operating rules rest, and safeguards the nation’s core framework from sudden change.

stable and clear laws: the more consolidated, predictable and clear are the laws of a country, the more agents will be willing to invest and do business there.

Legal security: environments that are more secure reduce the risks associated with legal disputes and contract interpretation, which translate into lower costs for economic agents.

Bureaucracy and business operations: more efficient government and limited bureaucratic hurdles act as catalysts of economic development, making business operations more efficient and agile, and less costly.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 41

Political system

Brazil has had a stable, democratic, multi-party regime for over two entire decades. elec-tions are direct, regular and cast via electronic ballot, a safe, modern and quick system that has become a global reference. in addition, there are no signs of existing or potential conflicts between Brazil and its neighbors, ensuring an environment of international peace and political and economic collaboration. As a consequence, the perception of po-litical stability in Brazil, as published by the World Bank, is equivalent to that of the united states and Great Britain21, both with longstanding traditions of democracy.

the system can and should continue to improve. As an example of an important step, in november 2011 Brazil signed a law ensuring the right to access government data (freedom of information)22, in line with common practices in countries such as sweden, the us and france, as well as latin American countries such as colombia, Peru, chile and mexico23. this law requires that all spheres of government actively disclose information such as financial records, bid and tender procedures, and data on monitoring govern-ment agencies. in addition, any interested party may ask to see information produced by government bodies that is of public interest, with deadlines and penalties for non fulfill-ment of such requests. this measure opens the way to a more transparent public sector.

this positive agenda must continue to advance, especially the separation between mat-ters of state and the political interests of governments. examples of improvement might include topics such as the financial independence of regulatory agencies and the inde-pendence of mandates of the President of the Brazilian central Bank. regarding the for-mer, although there are legal provisions for this24, in practice budgets are determined by the respective ministry. the development of formal funding mechanisms would benefit regulatory activities, making regulators more independent of politics and their resources more stable and predictable25. regarding the latter, formalized fixed mandates that do not coincide to those of the nation’s president, as is the case in the us and the uK, would strengthen the central Bank’s autonomy to conduct monetary policy.

21 indicator: Political stability and absence of [political] violence, from 0 to 100. score: Brazil: 51; Great Britain:

58; united states: 56. source: World Governance indicators – World Bank

22 law 12,527/11

23 source: freedom of information - unesco

24 law that created each of the ten regulatory agencies in the country

25 source: Judgement #2,261/2011 of the Brazilian Audit court, in response to

a request of the Brazilian senate

42 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

stable and clear laws

Brazil still faces challenges in the area of stable and clear laws. for instance, be-tween the time the federal constitution was issued in 1988, and 2011, an average of 19 federal laws26 has been issued each day. in 2011 alone, 1,781 new federal laws were signed27. this clearly makes it hard to keep up with applicable laws and standards, thus increasing the level of legal insecurity and the cost of investing and going business in the country.

there are other impediments related to the clarity of laws in Brazil. the technical quality of the wording of laws and standards must be improved, as well as enhanced control of their legality. for instance a 2009 study by fGv28 shows that 194 of the 218 articles of the Brazilian tax code - the main federal law governing the tax system - have been challenged in the superior court of Justice.

in addition to the legislative instability mentioned above, the frequent use of Provi-sional measures by the Brazilian executive Power as a legislative tool, and of so-called terminative decisions (a decision taken by a commission that counts as if voted in the senate Plenary) that result in some laws being approved without being submitted to the plenary, confer an undesired element of legislative uncertainty.

• Legal Security

the higher the degree of legal security, the fewer the uncertainties arising from court cases and contract interpretation, and consequently the lower the investment and business risk. it is important that Brazil stresses as a fundamental right29 the protec-tion of acquired rights, meaning that such rights persist even if the law granting them is no longer in effect. Another principle that is being included in the Brazilian legal framework that also has a positive influence on legal safety is the non retroactivity of a law, meaning that a law cannot influence situations that preceded it, unless it will benefit society.

the new Bankruptcy law, signed in 200530, is a good example of how legislative changes can improve legal security and benefit the investment and business environ-ment. the new law introduced the concept of judicial recovery in place of concordata (creditor protection), reducing the uncertainty regarding the assets at risk of liquida-tion, and the treatment of guarantees. consequently, the number of actual bankrupt-cies in Brazil dropped significantly. in 2005, before the new law was passed, 9.5 thou-sand bankruptcy requests were filed in Brazil, after the new law the annual average went down to 2.5 thousand (see Exhibit 6), and in 2011 was only 1.7 thousand, the smallest number in the past 12 years.

26 number of constitutional amendments, supplemental and ordinary laws, provisional measures, decrees and normative acts such as, for example, directives, opinions and instructions. source: instituto Brasileiro de Planejamento tributário (Brazilian tax Planning institute)

27 laws signed between october 2010 and october 2011 source: instituto Brasileiro de Planejamento tributário (Brazilian tax Planning institute)

28 source: valor econômico

29 fundamental guarantees described in the Brazilian constitution are considered “cláusulas pétreas” (in english, fixed clauses), meaning that they cannot be subsequently changed

30 law 11,101

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 43

even with this good example, it remains important to reduce the long time it takes to resolve disputes and enforce court rulings. to invest and conduct business in a country it is not enough to have a legal framework that has legal security as a principle, it is also necessary that the defense of one’s rights not be a slow, lengthy process as this in itself penalizes the party whose rights have been violated.

A 2012 study by the World Bank ranks Brazil among the worst countries in the world when it comes to the time it takes to resolve a business dispute: 731 days, while in singapore an equivalent dispute would be resolved in 150 days (see Exhibit 7). the main reasons for this have to do with the different systems adopted by each country. in Brazil, the delay is primarily the result of the rules that govern the civil and penal process codes, which allow a large number of appeals, and the overly detailed consti-tution, which enables many cases to be submitted to the supreme court.

in recent years there have been important reforms, in attempts to resolve this prob-lem, both to reduce the volume of lawsuits as well as to facilitate the operation of the Judiciary system. regarding the first initiative, one could mention the introduction of binding precedents31 and the principle of general repercussion32 in 2006, and the limits imposed on repetitive special appeals33 in 2008. the creation of so-called special courts34 and Arbitration chambers35 has contributed to the reform of the Judiciary sys-tem. Another important step was the implementation in 2011 of goals for the Judiciary system, such as judging a larger number of cases in a year than were filed in order to reduce the backlog.

exhiBit 6ultimately, institutional reforms impact the population in a positive manner

1. Law 11,101/2005 / Source: Serasa Experian, BCG analysis

More coMpanies operating could Mean More jobs and increased value creation for society as a whole

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110

5

2,5

10

15

20

25

with the new law created in 2005, the average number of bankruptcies each year dropped to 2.5 thousand

Average = 2.5 thousand (2006-2011)

13.9

11.6

19.920.7

13.9

9.5

4.2

2.7 2.2 2.4 1.9 1.7

Number of bankruptcy filings per year (thousand)

the new Bankruptcy law1 helped reduce the number of companies closing their doors in Brazil

-5.4

31 law 11,417

32 law 11,418

33 law 11,672

34 law 9,099 signed in 1995

35 law 9,307 signed in 1996

44 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

exhiBit 7the time it takes to for rulings adds uncertainty to the operation of the Justice system

ruling: 480 dayssentence enforcement: 210 days

other: 41 days

SgP Hkg USA FRA JPN dEU AUS Uk CHN mEx CHl CAN BRA iNd

150

280 300 331 360 394 395 399 406 415480

570

731

1,420Number of days to resolve a commercial dispute

Note: The standard dispute used for this study is a transaction between two companies (the buyer and the seller) in which the buyer fails to pay for some of the goods claiming that the quality of the goods did not meet the agreed quality standards. The seller then files a lawsuit to collect the amount owed for the goods it sold / Source: Doing Business Report – World Bank – 2012

Brazil has one of the longest conflict resolution terms of any international center

the enforcement of guarantees is another important element of legal security. loans at lower interest rates are possible if there are no rules making it difficult for the credi-tor to recover an asset, as the associated risk is smaller. in Brazil, there are a number of hurdles for creating and enforcing guarantees, typically related to the rigidity of traditional guarantees, difficulty constituting guarantees and a slow judiciary. regard-ing the first point, the effectiveness of guarantees is diminished since in the judicial recovery of companies and bankruptcies both labor and tax creditors have preference over creditors with real guarantee rights such as mortgages and pledges, reducing the effectiveness of these instruments. furthermore, formally registering secured credi-tor agreements is a complex and costly process. As there is no standardization of the documents required for such agreements, the procedure is subject to the specificities and demands of each notary office.

to eliminate the existing hurdles, efforts are being made to make processes more flexible and diversify the instruments available, such as the expansion of the concept of fiduciary property, where goods and rights do not become a part of the borrower’s assets until they have been paid for in full. thus, the guarantee posted is not part of the judicial recovery process and, unless otherwise determined, there is no competi-tion with the other types of creditors. there are also advantages in enforcement, which no longer requires that the case go through ordinary proceedings, which reduces the steps in the procedure and thus the time it takes for creditors to recover their assets.

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 45

Another theme that embodies legal security is respect for property, including intel-lectual property rights. A survey conducted by the World economic forum in 2012 puts Brazil in 51st place out of a list of 144 countries36. the reasons for this poor placing have to do both with the lengthy and costly patent application process, as well as the widespread practice of purchasing counterfeit (pirate) goods. in these two points there has been improvement. in 2011, Brazil was removed from the us list of “notorious piracy and contraband markets”37, and in fact is the only Bric not on that list, and the time it takes to get a patent has dropped to five years in 2011, compared to eight just one year previously38.

Bureaucracy and business operations

even if it does not actually impede business operations, it is generally believed that excessive bureaucracy greatly increases the cost of investing and doing business in a country. Brazil is the worst-ranked country in an indicator39 that reveals the impact of bureaucracy on business operations, behind other business hubs surveyed and behind other emerging nations such as mexico, china and chile (see Exhibit 8).

36 rank calculated from a score based on over 14 thousand interviews with executives. the question asked was:

“how would you rate the protection of property rights in your country, including

financial assets? [1 = very poor; 7 = very strong]. Brazil scored 4.7. source:

World economic forum – Global compe-titiveness report, 2012-2013

37 united states trade representation (ustr)

38 source: inPi

39 source: the 2012 World competi-tiveness yearbook, an annual global

survey of middle and senior managers in 59 countries

exhiBit 8the high cost of bureaucracy impacts business

in terms of the impact of bureaucracy on business, Brazil is the lowest ranked country

BRA CHN FRA mEx Uk JPN USA CHl Hkg SgP

8.6

7.97.3

7.0

6.1 6.0 5.9

4.2

3.22.9

The impact of bureaucracy on business / Score (0-10)

Note: An annual global survey of middle and senior managers in 59 countriesSource: World Competitiveness Yearbook 2012 - IMD; BCG analysis

46 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

one consequence of excessive bureaucracy is that it creates opportunities for corrup-tion, as lengthier, more complex and costlier transactions create more room for the payment of favors for speedier resolution. reducing corruption is thus an additional advantage of reducing excessive bureaucracy in an investment and business hub.

one example of a long, slow process is the time it takes to open a business, which in several of Brazil’s state capitals requires a large number of steps and a very long time. the average time it takes in são Paulo, for instance, is around 119 days40. decentral-izing procedures is one of the issues most often mentioned to justify this situation, and the number of entities involved confirms this perception (see Exhibit 9).

in addition, according to the 2012 doing Business report, it takes an average of 469 days to get approval for a real estate development41 in the city of são Paulo, com-pared to an average of 221 days in other latin American and caribbean nations. in são Paulo there is currently a proposal to create a Balcão Único law, something akin to a “one-stop-shop” to centralize the analysis and instruction of applications made to the different municipal bodies. this would pave the way to reduce bureaucracy and thus enable investments and business to proceed more swiftly.

Although this is a problem in most Brazilian cities, numerous initiatives have dem-onstrated there is room for improvement and the entire process of opening a new business can be made more agile. in the state of minas Gerais, a joint effort by the state government and the boards of trade, known as the minas fácil program, has made great strides in simplifying the process to open a new business, which cur-rently takes eight days42. in addition, the integrar project is an initiative that seeks to

40 Based on the time it takes to open a 50 employee company with share capital equal to ten times the per capita GdP, constituted as a limited company. source: World economic forum’s 2012 doing Business report

41 the construction of an industrial warehouse was used as the basis for the study

42 source: minas fácil

exhiBit 9opening a business involves numerous agencies

decentralized proceedings is one of the problems most often mentioned as the reason for this

1. Foreign capital only 2. Applies only to businesses whose activities might impact the environment / Source: Doing Business 2012 - World Bank; RFOR Advogados; BCG analysis

Entities involved in opening a new business in Brazil

city

Applies to All

depending on the type of

business

state federal other

municipal Bureau of the treasury

municipal Government

Bureau of the state treasury BureauBoard of trade

caixa econômica federalfederal revenueministry of labor and employment

inss (social security)

industry Associations employee unions

Bureau of the environmentWorks inspector

fire Bureau

Bureau of the environment

central Bank1

iBAmA2 funAi2

AnvisA

industry Associations

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 47

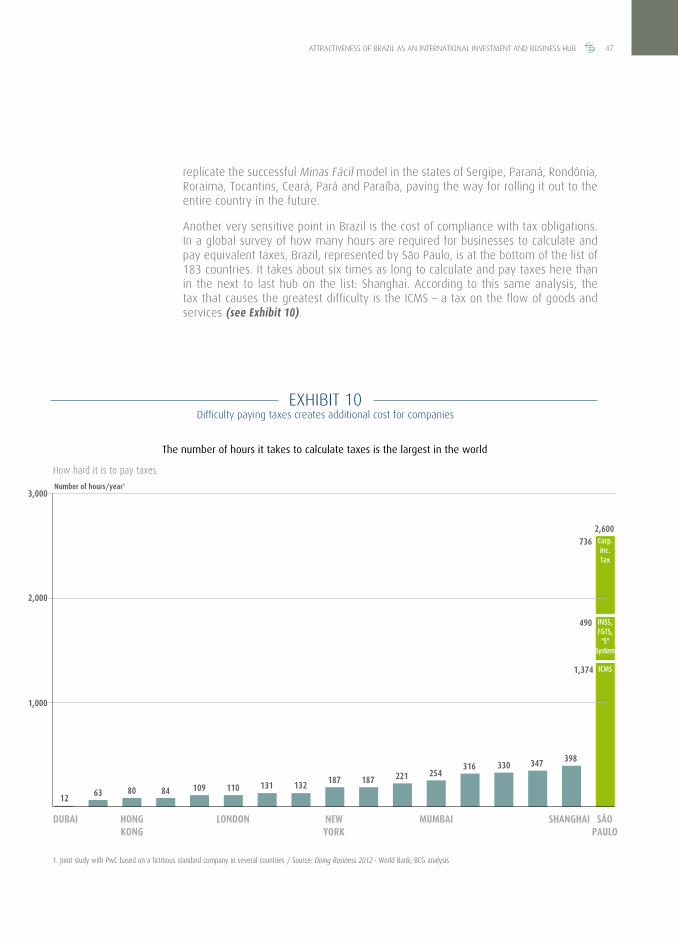

replicate the successful minas fácil model in the states of sergipe, Paraná, rondônia, roraima, tocantins, ceará, Pará and Paraíba, paving the way for rolling it out to the entire country in the future.

Another very sensitive point in Brazil is the cost of compliance with tax obligations. in a global survey of how many hours are required for businesses to calculate and pay equivalent taxes, Brazil, represented by são Paulo, is at the bottom of the list of 183 countries. it takes about six times as long to calculate and pay taxes here than in the next to last hub on the list: shanghai. According to this same analysis, the tax that causes the greatest difficulty is the icms – a tax on the flow of goods and services (see Exhibit 10).

SÃo PAUlo

mUmBAi SHANgHAiNEW YoRk

dUBAi HoNg koNg

loNdoN

the number of hours it takes to calculate taxes is the largest in the world

1. Joint study with PwC based on a fictitious standard company in several countries / Source: Doing Business 2012 - World Bank; BCG analysis

exhiBit 10difficulty paying taxes creates additional cost for companies

2,600

1,000

2,000

3,000Number of hours/year1

1263 80 84 109 110 131 132

187 187 221 254316 330 347 398

icMs

inss, fgts, "s"

system

corp. inc. tax

1,374

490

736

How hard it is to pay taxes

48 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

the main factors influencing this poor position are the excessive number of taxes, changing laws and complexity in complying with the ancillary obligations required to pay taxes. According to the World Bank doing Business report, businesses in Brazil must pay a total of nine taxes, where as in other business hubs such as singapore and hong Kong this number is five and three43 respectively.

the issue of the large number of laws passed also applies to the tax system. As mentioned, this makes it hard to keep track of which federal laws are applicable, making it more likely for there to be gray areas that not only increase bureaucracy, but also contribute to greater uncertainty in the payment of taxes. in the case of non financial service providers, the requirements for calculating taxes such as the icms are even more complex. for financial institutions, the hardest taxes to calculate are iss, Pis and cofins.

it is worth mentioning that in the case of investments in funds, debentures or fixed yield instruments, the financial institution managing the investment is responsible for paying the tax, and the investor receives its investment net of taxes.

finally, another very important element to doing business in a country is the flexibility of its labor market. When it comes to matters specific to hiring employees, Brazil is among the least flexible nations, behind chile and the united states, for example. on the other hand, when it comes to dismissal process, Brazil does not do badly (see Ex-hibit 11). care should be taken, however, lest this position be weakened (for example the possibility that ilo convention 15844 may be adopted), so as to continue to be able to efficiently allocate people and pursue business.

even though Brazil faces a challenging situation in terms of bureaucracy, it is important to understand that efforts have and are being made, such as the creation of enAP, the national school of Public management, whose purpose is to develop competences in civil servants and improve the quality of government services, PnAfe, the national Program to support fiscal Administration in Brazilian states, which focuses on improv-ing tax issues, and mBc, the competitive Brazil movement, an entity that, among other responsibilities, has programs to modernize government administration. in addition to these initiatives, increased use of digital technologies has contributed to speedier interaction between the government and the private sector. An example of it would be the sPed – the Government system of digital Bookkeeping.

43 doing Business database, completed in december 2010

44 international labor organization convention 158 makes the termination process far more rigid and bureaucratic. if adopted its requirements include writ-ten justification as to why the employee is being let go submitted to the relevant authorities, the right to appeal against the decision, the inclusion of unions in individual termination decisions and lawsuits in the event of disagreements. only 35 of the 183 ilo member states have ratified the convention and only six of them are developed nations (Aus-tralia, finland, luxembourg, Portugal and spain). source: ilo

when It comes to matters specIfIc to hIrIng

employees, brazIl Is among the least flexIble natIons

AttrActiveness of BrAzil As An internAtionAl investment And Business huB 49

furthermore, models used in other countries could serve as an inspiration and be adapted to the situation in Brazil, such as the uK’s Better regulation executive, which improves the distribution of information to public agencies, reduces the number of registrations required and engages civil servants in understanding public services and processes to disseminate best practices.

exhiBit 11Brazil is not well positioned when it comes to flexibility of its labor market

Labor market flexibility (% countries in each situation)1

Termination notice (months) 2: 25% 1: 63% 0: 13%

Termination costs (weeks of work)3 0: 19%1 to 6: 25%8 to 11: 31%20 or more: 25%

Existence of reemployment rules yes: 31% no: 69%

Obligation to retrain or place before termination yes: 38% no: 63%

Need for third party approval yes: 13% no: 88%

Annual paid vacation (days) 21 to 30: 31% 11 to 20: 44% 10 or fewer: 25%

Overtime cost to the company (% over standard

cost per hour)100: 13% 02: 13%50: 56% 25 to 40: 19%

Maximum allowed duration of temporary

contracts (months)up to 24: 31%

60 or fewerunlimited: 63%6%

Temporary contracts are allowed for per-

manent activitiesno: 25% yes: 75%

1. Countries included in the assessment: BRA, MEX, CHL, USA, GBR, FRA, GER, SGP, HGK, CHN, JPN, IND, RUS, KOR, AUS, CAN 2. Not defined by law 3. Average based on employees with 5 years tenure in the different countries analyzed / Source: Doing Business 2012 – World Bank; BCG analysis

HiRi

NgEm

PloY

mEN

ttE

RmiN

Atio

N

degree of flexibility

- +

50 AttrActiveness of BrAzil As An internAtionAl investment And Business huB

Indicators

the dimensions selected for continuous tracking of the institutional environment pillar are:

• Political stability: normally the political situation has a major impact on the at-tractiveness of a country. thus a country that is more stable and democratic, free of political violence, will be more attractive;

• Quality of regulations: this indicator measures how clear a country’s regulations are and if there are clearly defined and understood roles for the regulators, with delega-tion of powers as necessary;