Pricing Methods Pricing chart Pricing Methods Pricing chart Pricing software.

date post

21-Dec-2015Category

view

220download

1

Asset Pricing Theory in One Lecture

Eric Falkenstein

1Finding Alpha

Capital Asset Pricing Model (CAPM)Arbitrage Pricing Model (APT)Stochastic Discount Factor Model (SDF)General Equilibrium Theory

2Finding Alpha

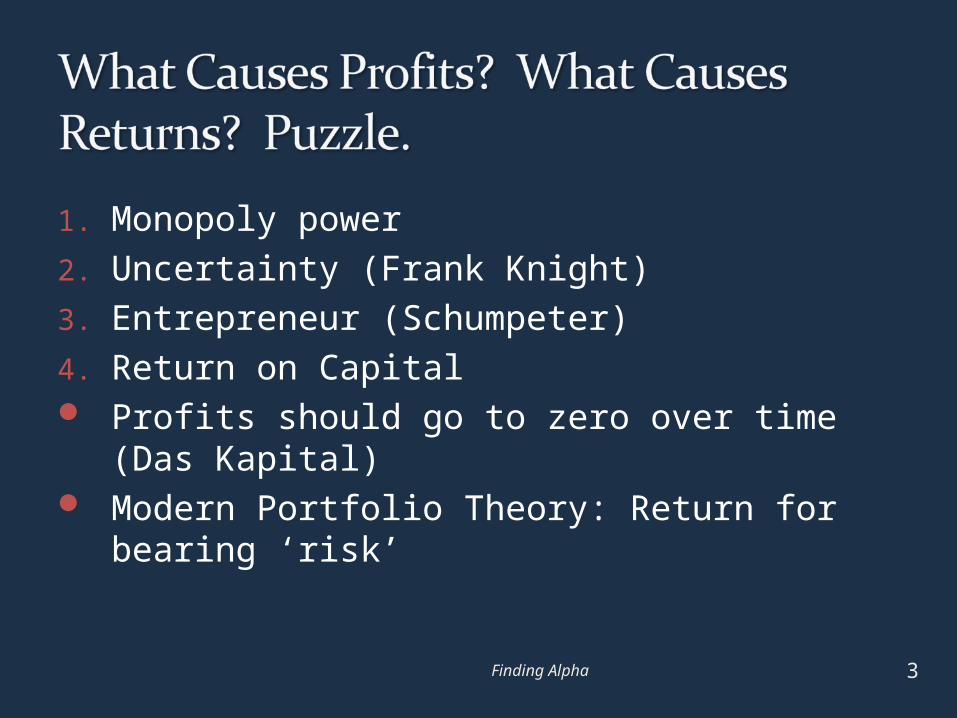

1. Monopoly power2. Uncertainty (Frank Knight)3. Entrepreneur (Schumpeter)4. Return on Capital Profits should go to zero over time (Das

Kapital) Modern Portfolio Theory: Return for bearing

‘risk’

3Finding Alpha

Diversification, Diminishing Marginal Utility

Processes:Arbitrage Equilibrium

4Finding Alpha

E[Reti]=+Eif

DiversificationDecreasing marginal utility

Util

ity

Consumption

Portf

olio

Vol

# assets

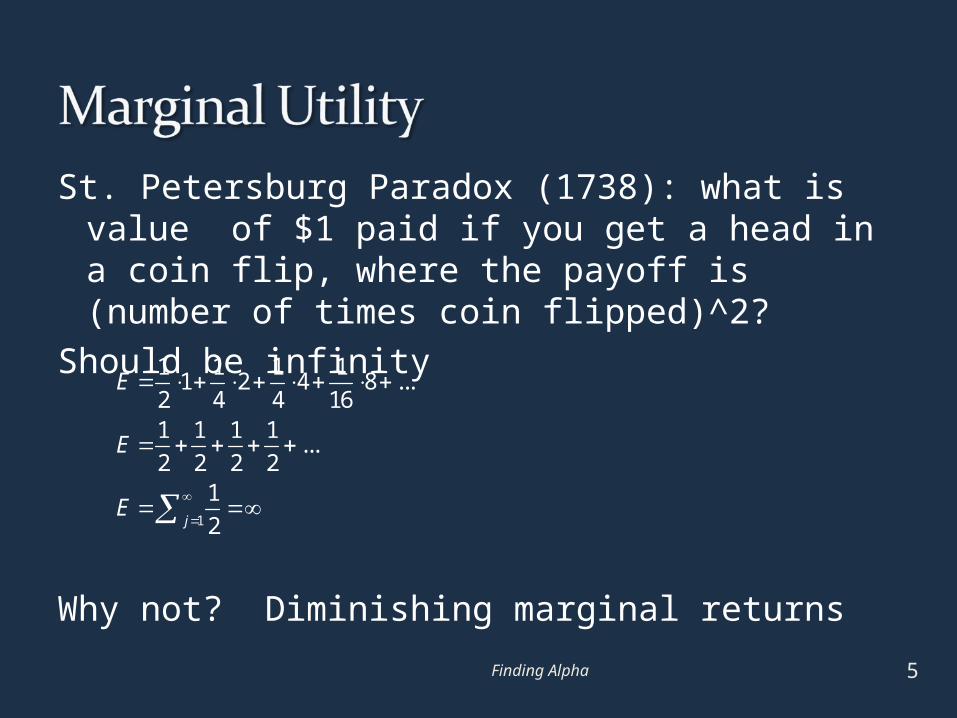

St. Petersburg Paradox (1738): what is value of $1 paid if you get a head in a coin flip, where the payoff is (number of times coin flipped)^2?

Should be infinity

Why not? Diminishing marginal returns

5Finding Alpha

1

1 1 1 11 2 4 8 ...

2 4 4 161 1 1 1

...2 2 2 2

1

2j

E

E

E

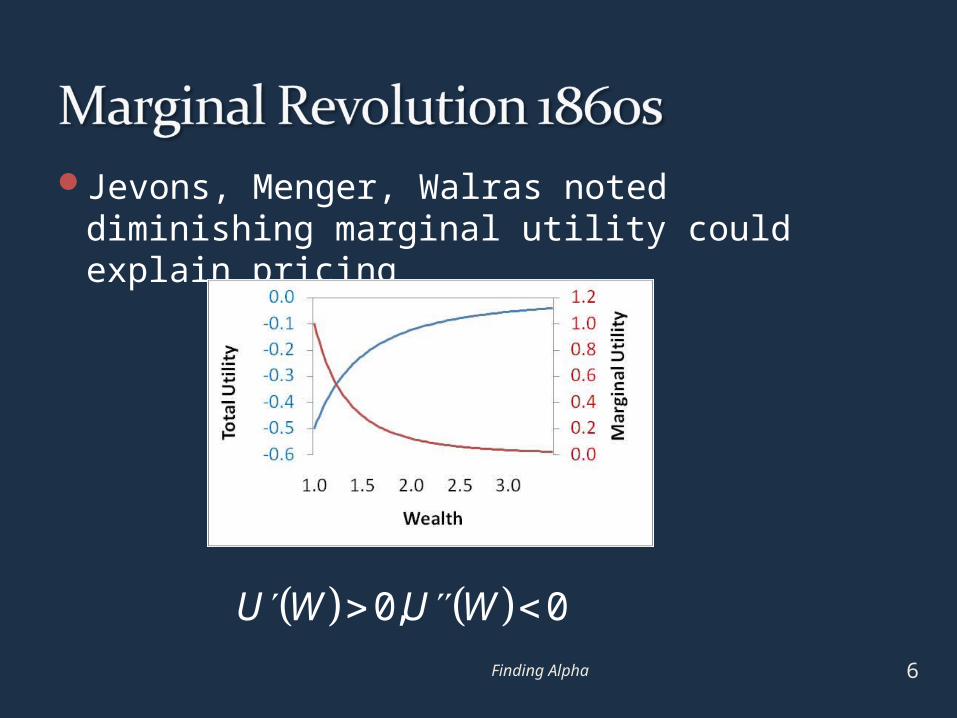

Jevons, Menger, Walras noted diminishing marginal utility could explain pricing

6Finding Alpha

0, 0U W U W

7Finding Alpha

Johnny Von Neumann and Oscar Mortgenstern 1941 Theory of GamesMilton Friedman and Savage 1947

Why not put all your wealth in one stock?

“To suppose that safety-first consists in having a small gamble in a large number of

different [companies] … strikes me as a travesty of investment policy.”

Keynes

8Finding Alpha

9Finding Alpha

2

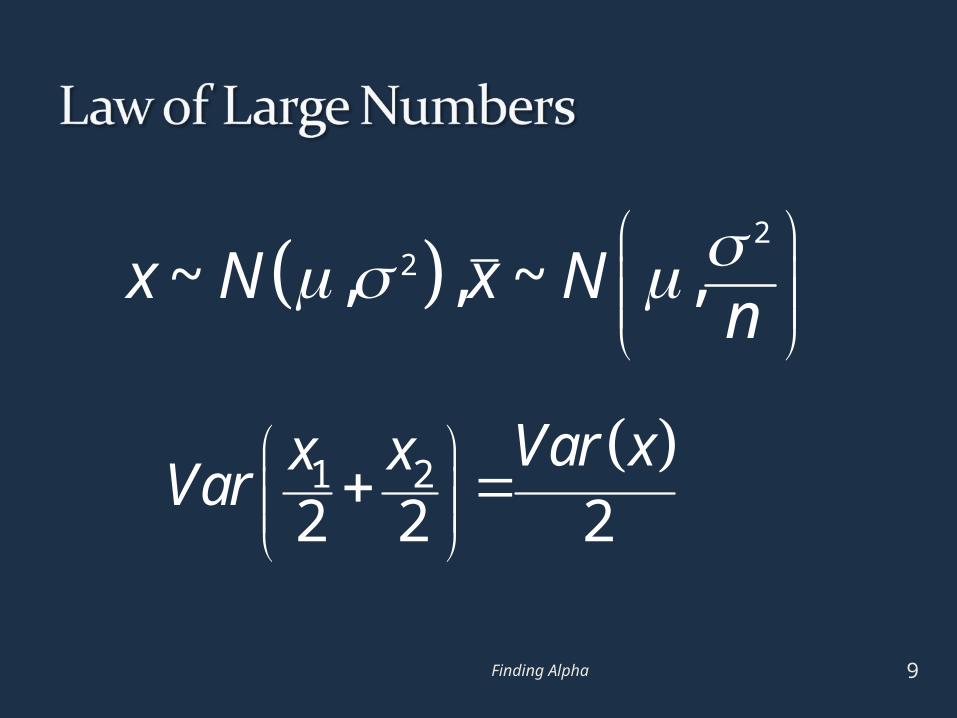

2~ , , ~ ,x N x Nn

1 2

2 2 2Var xx x

Var

Finding Alpha 10

22 2 21 1 1BA ABvol xA x B x x x x

2 2 2BA ABVar A B

Finding Alpha 11

Systematic Risk

Idiosyncratic Risk

n

Total risk; U

ip

2 21 11p i ipN N

2 lim p ipN

12Finding Alpha

‘risk’ is ‘variance of return’

Finding Alpha 13

aW

aW

U e

EU E e

2

2

2

~ ,

aa

if W N

EU e

Finding Alpha 14

2U E r a

Finding Alpha 15

Standard Deviation

Expected Return

100% investment in security with highest E(R)

100% investment in minimum variance portfolio

No points plot above the red line

All portfolios on the red line are efficient

Why we like efficient portfolios

Portfolio Selection: Efficient Diversification of Investments (1959)

Markowitz preferred ‘semi-variance’ in bookAlso examines:

standard deviation, expected value of loss, expected absolute deviation, probability of loss, maximum loss

‘Prospect Theory’ in 1952

16Finding Alpha

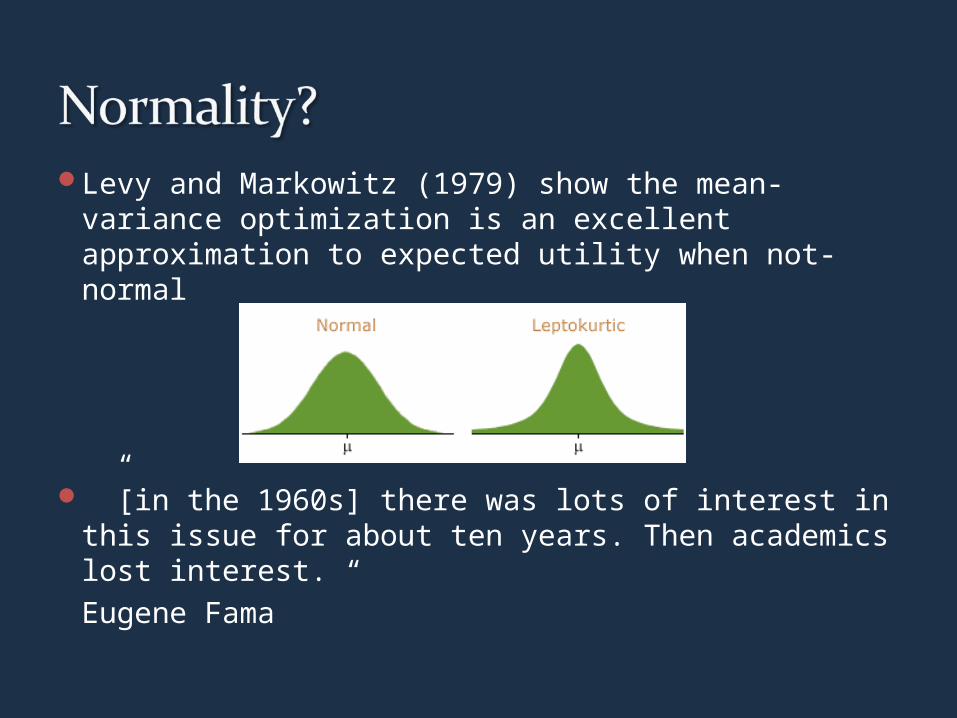

Levy and Markowitz (1979) show the mean-variance optimization is an excellent approximation to expected utility when not-normal

”[in the 1960s] there was lots of interest in this issue for about ten years. Then academics lost interest. “

Eugene Fama

Finding Alpha 18

ExpReturn

Volatility

U1

U2

U3

Port-1

Port-2

Port-3

U4

Finding Alpha 19

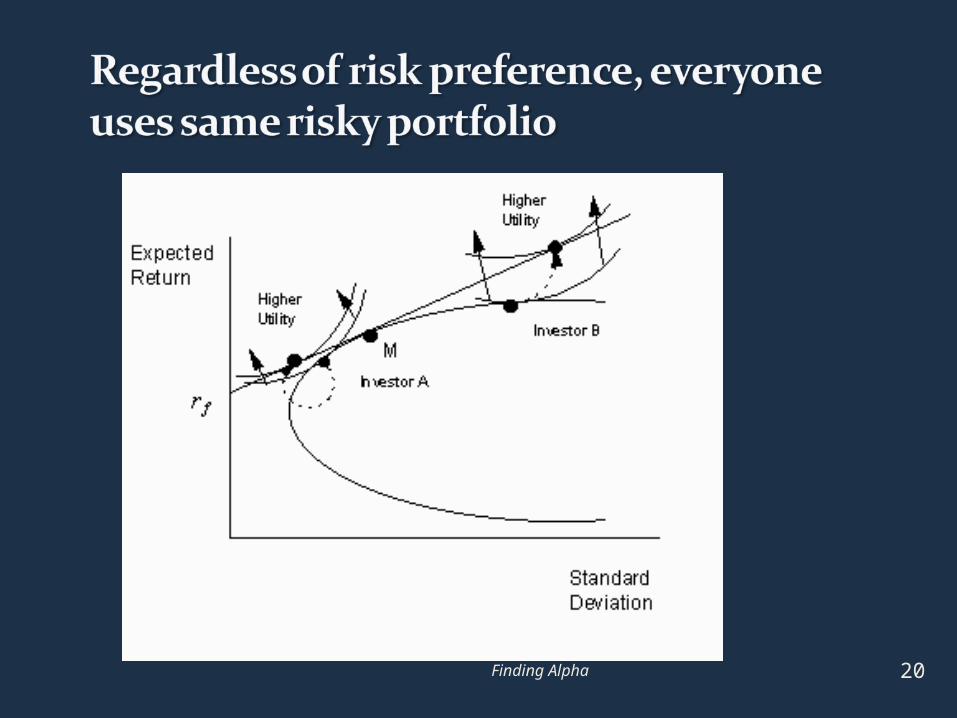

Finding Alpha 20

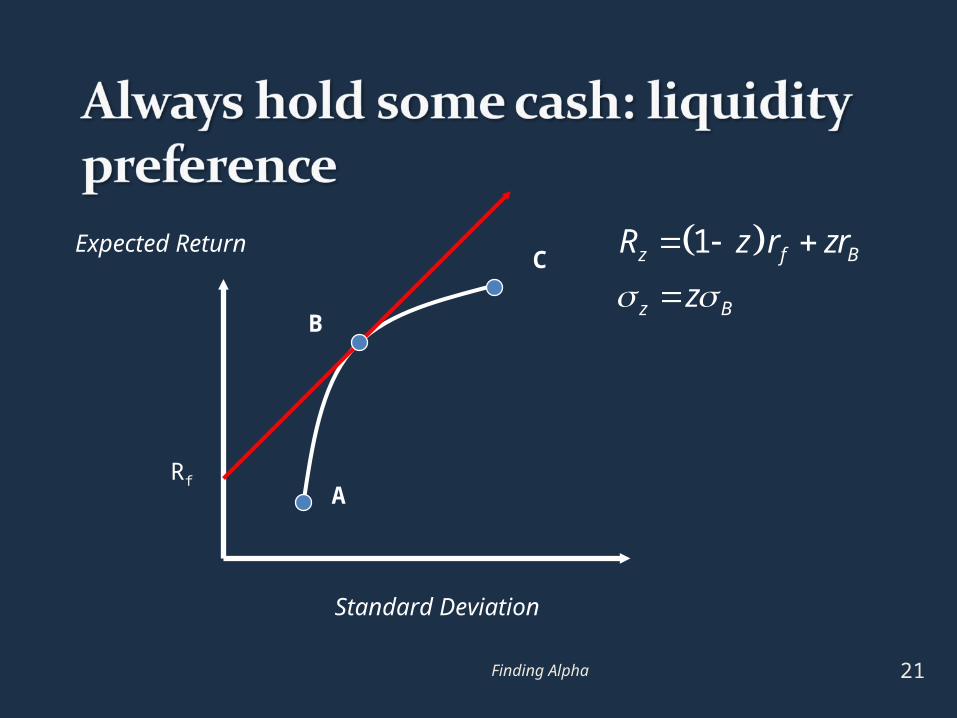

Finding Alpha 21

Standard Deviation

Expected Return

RfA

B

C 1z f B

z B

R z r zr

z

22Finding Alpha

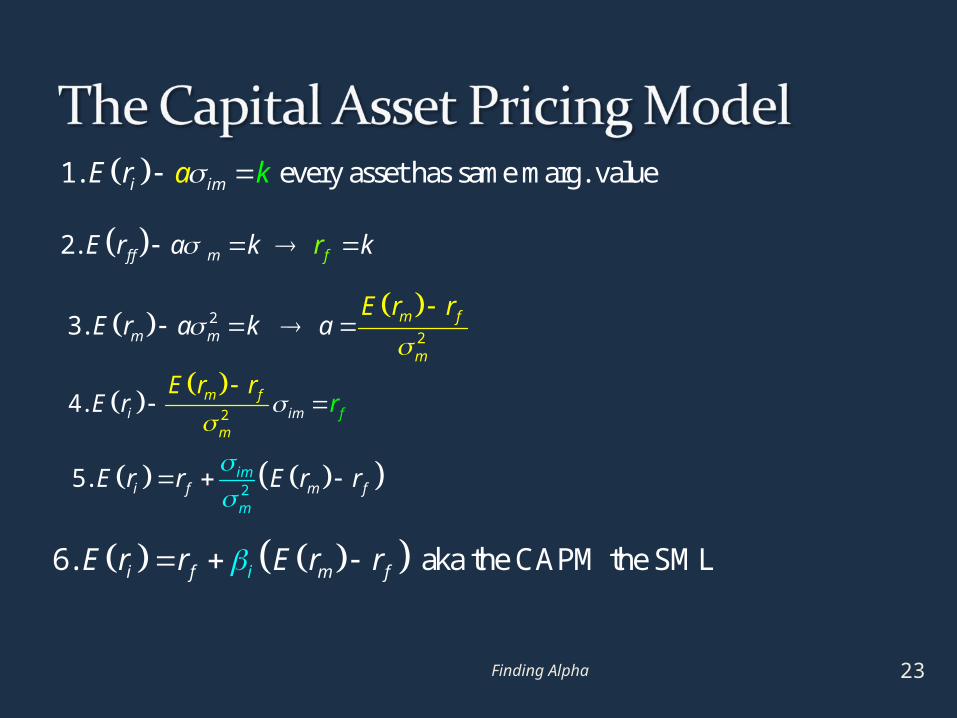

23Finding Alpha

1. every asset has same marg. valuei imaE r k

2. f fm fE r a k kr

22

3. m f

mm mE r a k a

E r r

2

4. i im

fm f

m

E r rrE r

25. im

f m fm

iE r r E r r

6. aka the CAPM the SMLi f m fiE r r E r r

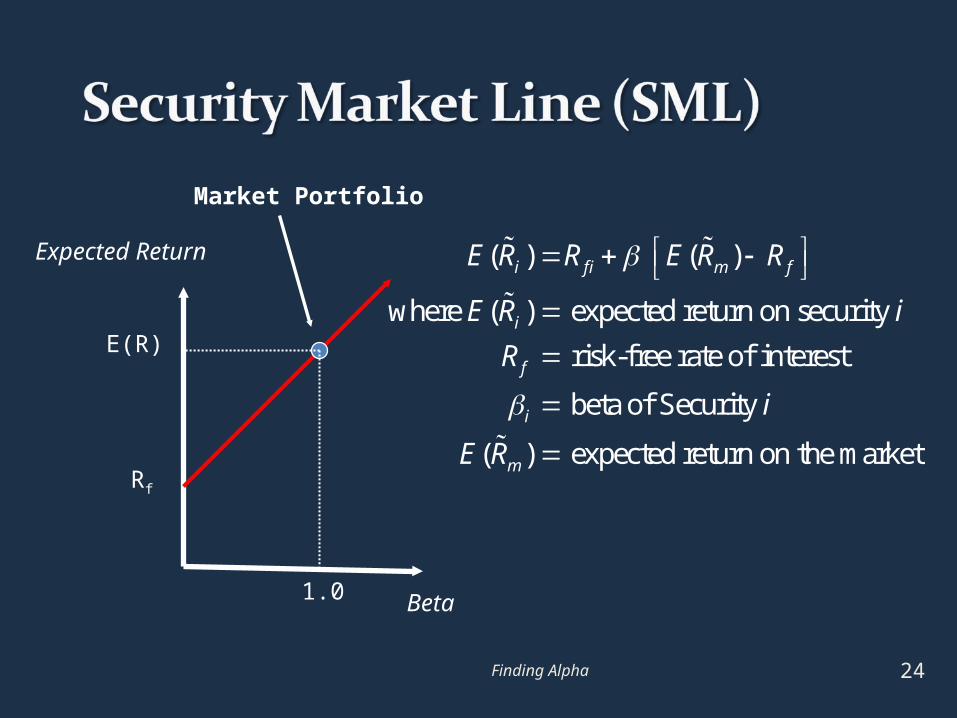

Finding Alpha 24

Beta

Expected Return

Rf

Market Portfolio

1.0

E(R)

( ) ( )

where ( ) expected return on security

risk-free rate of interest

beta of Security

( ) expected return on the market

i f i m f

i

f

i

m

E R R E R R

E R i

R

i

E R

Finding Alpha 25

'

' ' 10 1 '

0

U1. U U 1 1 1

UE r E r

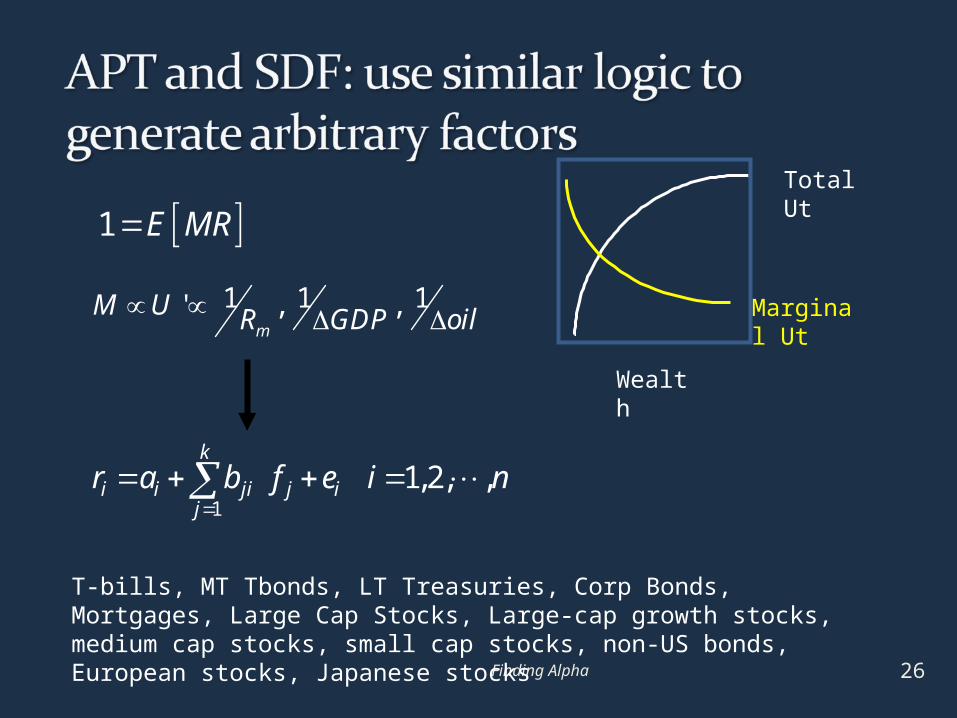

3. [ ] [ ] [ ] cov( , ) 1E MR E M E R M R

1

[ ]

c4.

ov( , ]

[ ][

)E

M

M

E

R

E MR

15. [ ]

[ ]ff RE RE M

'1' '0 0

'0

-U6.

U U

1 cov( , )

' cov( , )

m

m

i mR

RM

U M RR

UR

'0' '

01

cov( ,7.

)[ ] i m

fEU

RR R

U UR

'1'0

2. 1 givU

Uen M=E MR

'1

cov( , )8. [ ] i m

f

R RE R R

U

cov( , )11. [ ] [ ]

var( )i m

i f m fm

R RE R R E R R

R

12. [ ] [ ]i f m fE R R E R R

'1

var( )9. letting R =R

[ ]m

i mm f

RU

E R R

cov( , )10. [ ]

var( )

[ ]

i mf

m

m f

R RE R R

R

E R R

26Finding Alpha

1 E MR

1 1,2, ,

k

i i ji j ij

r a b f e i n

1 1 1' , , m

M U R GDP oil

Total Ut

Marginal Ut

Wealth

T-bills, MT Tbonds, LT Treasuries, Corp Bonds, Mortgages, Large Cap Stocks, Large-cap growth stocks, medium cap stocks, small cap stocks, non-US bonds, European stocks, Japanese stocks

If f is a risk factor, it must have a linear price to prevent arbitrage

Can of beer: $16-pack of beer: $6Case of beer (24 pack): $24Price of beer linear in units, else arbitrage

27Finding Alpha

1 1 2 2

Random'price of risk''how much'

,

0

1,2, ,

~

f i

j j j

j

i iibr r f b f e i n

f N

Finding Alpha 28

For k number factors

How many factors? 3? 5? 12?What are the factors? Empirical issue.Could be estimated just like a ‘bias’Total Portfolio Volatility no longer the issue

1 1,2, ,

k

i i ji j ij

r a b f e i n

f m m f size small big value value growth mo up downi r r r r r r r r rr

Markowitz. Normative model: people should invest in efficient portfoliosNo residual aka idiosyncratic aka unsystematic,

volatilityTobin: Efficient portfolio always combination

of a single risky portfolio and the non-risky asset

Sharpe : Given Tobin, covariance with the market dictate expected return

Ross: add factors like Rm-Rf , whatever matters to people, linear pricing in factors

29Finding Alpha

linear in risk factorsnot include residual riskinclude something very like the stock market

as one of the prominent factors

30Finding Alpha