Software Asset Management: Software Asset Management: Playing ...

April 2016

CEE – Europe’s roaring workshop

Karoll Financial Group Mission

“Our goal is to create top-notch vehicles, tools and processes in helping international investors harness the exciting potential of Emerging Europe.”

Stanimir Karolev

Founder and Chairman,

Karoll Financial Group

2

Karoll Financial Group Product Offering

Bulgarian Capital Market

International Capital Markets

Brokerage

Wealth Management

• Advance Invest

• Advance Eastern Europe

• Advance Emerging Europe Opportunities

• Advance Global Trends

• Advance Conservative Fund

• Discretionary accounts

Institutional Mandates

• Eastern Europe

• Central Europe

• Balkan

• Thematic equity

• Mixed

Asset Management

IPO & SPO Activities

M&A Restructuring

Investment Banking

Real Estate

ADVANCE TerraFund

REIT

Private Equity

ADVANCE Equity Holding

3

Karoll Financial Group

Karoll Brokerage

Karoll Capital Management

Advance Terrafund

Advance Equity

Karoll Investment

Leader in number of transactions on BSE for 13 consecutive years 30% market share of of all transactions

Pioneered the first mutual fund in Bulgaria Strategic partner of Schroders for the local markets

Largest farm land REIT in the country IFC (World Bank) - key stakeholder

First Private Equity fund in the country

Executed the first IPO in Bulgaria (2004); Successfully raised capital through the stock exchange (BGN 160 mln)

23 EXCITING YEARS OF SUCCESS | TEAM OF 200 EXPERTS

Karoll Capital Management Overview

Unique heritage in CEE

Founded in Sofia in 2003, our roots are truly in Emerging Europe

Independent and skilled Eastern Europe-based team

Part of Karoll Financial Group with support of 200 professionals + 70 local offices

Steady business growth on solid reputation

AUM over EUR 200 mln.

Assets split in various mutual funds, real estate investment trusts, wealth mgt & mandates

Manages 5 UCITS funds and multiple private accounts

Crisp focus on Emerging Europe

Helping clients harness the potential of emerging Europe

Deep understanding of the cultures and dynamics of our markets

On-the-ground research coverage of strategically important holdings

Partnership with top international names

Local representative of Schroder Investment Management, UK

Partners with IFC (World Bank), European institutions and global players

International road-shows and conferences

5

Our Unique Value Proposition

“Emerging Europe offers a unique asset class with strong upside potential and low correlation to the developed world. It is a truly overlooked opportunity.

We pick out high-growth sectors in a high-growth region.

We generate alpha in the region while helping global investors overcome local barriers.”

Daniel Ganev

Managing Director,

Karoll Capital Management

Independent

Flexible

Entrepreneurial

Deep understanding

of local markets

6

Karoll Capital’s Investment Committee

Seasoned investment team with unique combination of skills >>>

Daniel Ganev, Managing Director

15+ yrs of experience in in fund management, financial products development and marketing, business development in emerging markets

Nadia Nedelcheva, CFA, Head of Portfolio Management

15+ yrs of experience in portfolio management, research, valuations and modeling in Central & Eastern Europe

Alexander Nikolov, Portfolio Manager

18+ yrs of experience in portfolio management, financial analysis, technical analysis on the US, European and CEE markets

Katerina Atanassova, Portfolio Manager

15+ yrs of experience in portfolio management, technical analysis and trading on the global developed and emerging markets

Georgi Georgiev, Portfolio Manager

13+ yrs of experience in research, fundamental analysis, valuations, portfolio management and trading in the global emerging markets and USA

Dimitrios Latitaris, Investment Analyst

4+ yrs of experience in research, investment banking, fundamental analysis, valuations in Central & Eastern Europe

Georgi Raykov, Investment Analyst

3+ yrs of experience in research, fundamental analysis, valuations in Central & Eastern Europe

Investment Process – the 4 S’s

Screen

The process starts with our on-the-ground analyst team screening the landscape in search of investment opportunities in Emerging Europe. We apply filters in terms of liquidity (time needed to enter/exit investment), market cap, transparency, corporate governance, etc. As a result, our investment universe comprises around 500 stocks out of some 3 000 listed companies in CEE. Our major advantage is the freedom to deviate from local indices based on our views. This gives us flexibility in our investment choice, regularly leading to superior results and outperformance of benchmarks and peers. Using proprietary analytical tools and exchange with local contacts, we seek to pinpoint stocks that are trading at a discount or that are in a position to undergo some fundamental change. Examples of such events are turnaround situations, management changes, financial results surprises, etc.

Study

The generation of investment ideas leads to the next step -- a thorough in-depth analysis conducted in house. Because of market inefficiencies we believe Emerging Europe is abundant with mispriced assets. In estimating the true value of a stock we study the firm’s business model and its ability to realize returns greater than the cost of capital, the shareholder structure and management capabilities, sector dynamics and overall market position. We strive to find companies with improving profitability margins and low debt levels that are traded at a discount to peers. On-site visits and regular contact with company representatives are a key part of research as well. In addition to employing valuation methods, we also consider investor psychology, liquidity and order flows. The outcome of the investment assessment is the analyst proposal to the investment committee, which summarizes the case, the rationale behind it, potential upside and associated triggers, as well as the risks involved.

Shape

Karoll Capital’s 4-member investment committee, supported by the analyst team, examines the selected investment proposals in view of portfolio construction. At the asset allocation level (asset class and geographic splits), we normally apply the Black Litterman model, which takes into account the market size, volatility, correlations and our convictions. The committee then debates whether a stock deserves to be included in the portfolio, when and what weight to be assigned to it. In the case of Karoll’s mutual funds the Portfolio Manager has the final say with regard to stock selection, while in the case of managed accounts / mandates the decision is collective. Likewise, the committee / PM decides on position weight changes and/or liquidations. At each stage, compliance with regulatory guidelines and client-tailored requirements are factored in.

Scrutinize

Finally, the investment portfolio is monitored with all different positions being systematically scrutinized. The investment team applies in-house processes and practices enabling it to adequately react to the different triggers causing distortions to the investment case. As part of the process our analysts and portfolio managers follow up with the companies’ management, screen the sector competitors and general business/political environment. Conducting attribution and risk management analysis on the portfolio holdings is essential. Any resulting concerns related to the investment case prompt reviews of the rationale behind the decision to add / hold/ reduce the stock as a portfolio component.

8

Our Investment Universe

3,000+ listed companies in CEE

Investment Universe – 1,500

750

500

250

Survivors

150

Selection Filters:

Sector Outlook & Company Competitiveness

Mkt cap & Liquidity

Corp Governance & Transparency

Financial Strength

In-house Valuation

Investment Capabilities & Results

4 main strategies offered to institutional investors:

Eastern Europe, Central Europe, Balkan, and Thematic, as well as mixed strategies

based on specific mandate

Karoll Capital’s Investment Committee aims to construct for our institutional clients

Managed Accounts / Mandates portfolios designed to take advantage of the L.T. trends

as well as hot opportunities in the market

We have identified a compelling theme as an excellent opportunity for our institutional clients:

“CEE – Europe’s roaring workshop”, comprising companies from the industrial, outsourcing

and ICT sectors with excellent upside potential

Model portfolios vs. benchmark, as of 15.04.2016 YTD 1 year 3 years,

annualized Volatility Beta Alpha

MSCI EFM Europe +CIS 9.44% -17.50% -9.32% 16.69%

MSCI EFM Europe +CIS ex RU 6.68% -17.65% -10.16% 14.40%

Balkan strategy -7.53% -13.96% 0.65% 10.77% 0.38 10.81%

Eastern Europe strategy 1.19% -9.95% 0.28% 8.90% 0.29 9.60%

Central Europe strategy 0.40% -8.52% -5.25% 10.42% 0.29 4.91%

Thematic strategy 6.20% 4.30% 12.80% 15.70% 0.25 22.12%

Emerging Europe thematic model portfolio “CEE – Europe’s roaring workshop”, comprising companies from the industrial, outsourcing

and ICT sectors with excellent upside potential

Ukraine

2%

Bulgaria 3%

Czech Republic

3% Hungary 4%

Romania 8%

Russia 19%

Turkey 27%

Poland 34%

Geographic breakdown Sector breakdown

Top 5 positions % of portfolio Country Sector

Tofas Turk Otomobil Fabrikasi AS 5.81% Turkey Automobiles & Multi Utility Vehicles

Arcelik AS 5.66% Turkey Household appliances

GMK Noril'skiy nikel' PAO 5.48% Russia Basic materials

Uniwheels AG 5.35% Poland Automotive supplies

Asseco Poland SA 5.10% Poland IT services and consulting

Model portfolio vs. benchmark, as of 15.04.2016 YTD 1 year 3 years,

annualized Volatility Beta Alpha

MSCI EFM Europe +CIS 9.44% -17.50% -9.32% 16.69%

Thematic strategy 6.20% 4.30% 12.80% 15.70% 0.25 22.12%

Agriculture 2%

Pharmaceutical 8%

Wood products/Furnit

ure 9%

Household appliances

11%

Machinery 11%

Chemical 12% IT services and

consulting 14%

Basic materials 16%

Automotive 17%

Accessing investment opportunities in Emerging Europe is often obstructed by various challenges related

to language barriers, cultural differences and transparency issues.

To help our institutional clients make the most of what the region has to offer we provide a number of

analytical tools:

quarterly strategy report & flash reports

individual sector and stock reports upon request

monthly performance statements, attribution analyses

conference calls and discussions with investment committee members

on-site client visits upon request

Analytical Support for Institutional Clients

12

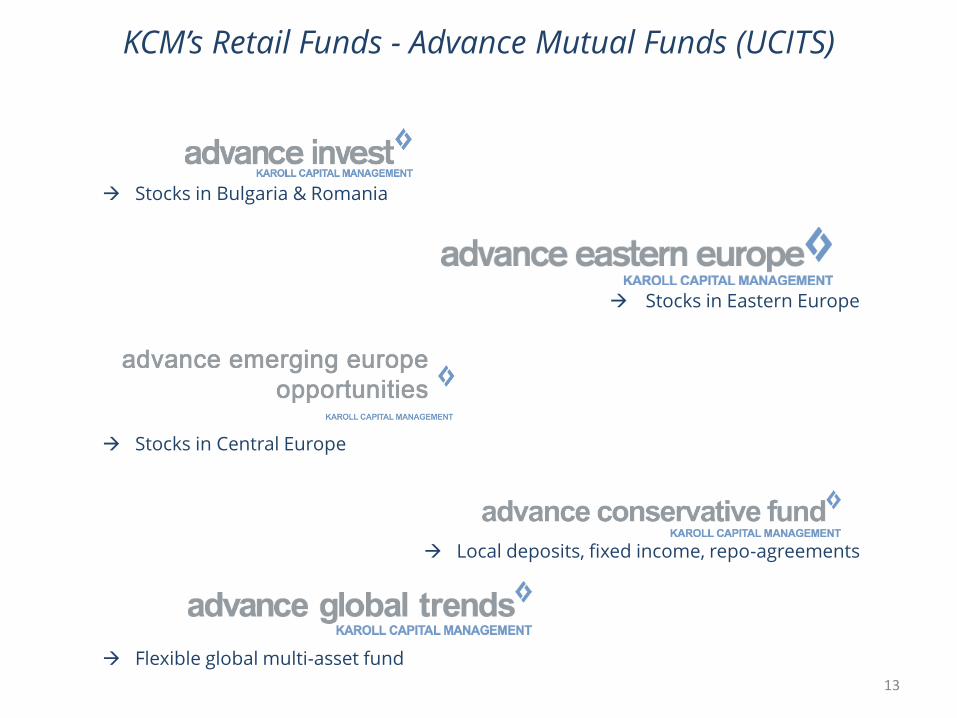

KCM’s Retail Funds - Advance Mutual Funds (UCITS)

Stocks in Bulgaria & Romania

Stocks in Eastern Europe

Stocks in Central Europe

Local deposits, fixed income, repo-agreements

Flexible global multi-asset fund

13

Emerging Europe – the Overlooked Opportunity

14

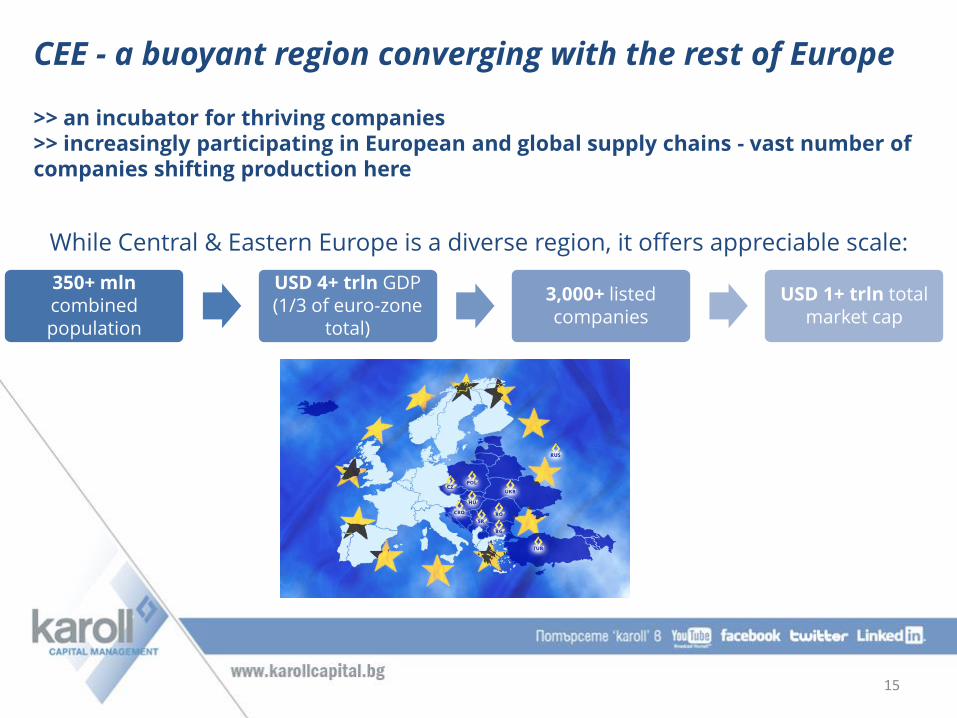

CEE - a buoyant region converging with the rest of Europe >> an incubator for thriving companies >> increasingly participating in European and global supply chains - vast number of companies shifting production here

While Central & Eastern Europe is a diverse region, it offers appreciable scale:

350+ mln combined population

USD 4+ trln GDP (1/3 of euro-zone

total)

3,000+ listed companies

USD 1+ trln total market cap

15

CEE now a major production & services hub for Western Europe

CEE countries have become major automotive producers 26% of motor vehicles in Europe are produced here Local suppliers steadily moving up the value chain CEE is Europe’s Silicon Valley IT sector rapidly increasing its share of GDP with fast growing number of employees Booming outsourcing sector CEE countries in top 20 ranking for Business Process Outsourcing

16

CEE growing much faster than developed Europe

GDP growth (%)

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%2

00

5

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

e

20

16

f

20

17

f

Euro area

Emerging and

developing

Europe

Source: IMF April 2016 outlook

Emerging Europe growing at a much faster pace vs. developed Europe: +3.5% on average b/n 2005 and 2015 vs. +0.8% for euro-area Trend expected to persist in the following years

GDP growth (%)

17

Low levels of GDP p.c. suggest solid catch-up potential

0 5 000 10 000 15 000 20 000 25 000 30 000 35 000

Euro area

Czech Republic

Estonia

Lithuania

Hungary

Poland

Latvia

Croatia

Russia

Turkey

Romania

Bulgaria

Serbia

Ukraine

GDP per capita (EUR)

Source: Eurostat

Rising but still very low levels of GDP per capita –b/n and 8 and 53% of euro-zone average

18

Compelling opportunities

Strategic location of the region ideally situated for building trade links between Western Europe, Middle East and Asia. Infrastructure has significantly improved in the past years with major investments planned in the mid term -> the region now deeply integrated with pan-European transport corridors

Most countries are current or future members of EU, OECD and NATO resulting in major changes in their economies and business environment. Some have already adopted the Euro. Legal, regulatory and business conditions have marked solid improvement; regulatory framework synchronized following EU accession.

CEE boasts well-educated and relatively inexpensive workforce labor force with tertiary education has been steadily increasing. Wages have been on the rise, but still far below EU average.

Favorable tax regimes significantly lower tax rates (e.g. 10% corporate income tax in Bulgaria)

19

Stable economies with low level of government debt

94%

92%

85%

76%

76%

50%

43%

41%

41%

40%

33%

27%

18%

10%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Ukraine

Euro zone average

Croatia

Serbia

Hungary

Poland

Czech Republic

Lithuania

Latvia

Romania

Turkey

Bulgaria

Russia

Estonia

Government debt/GDP, 2014

Source: Eurostat, IMF

Government debt in CEE at comparatively low levels: below 50% of GDP for the region vs. 90 % for euro-zone

20

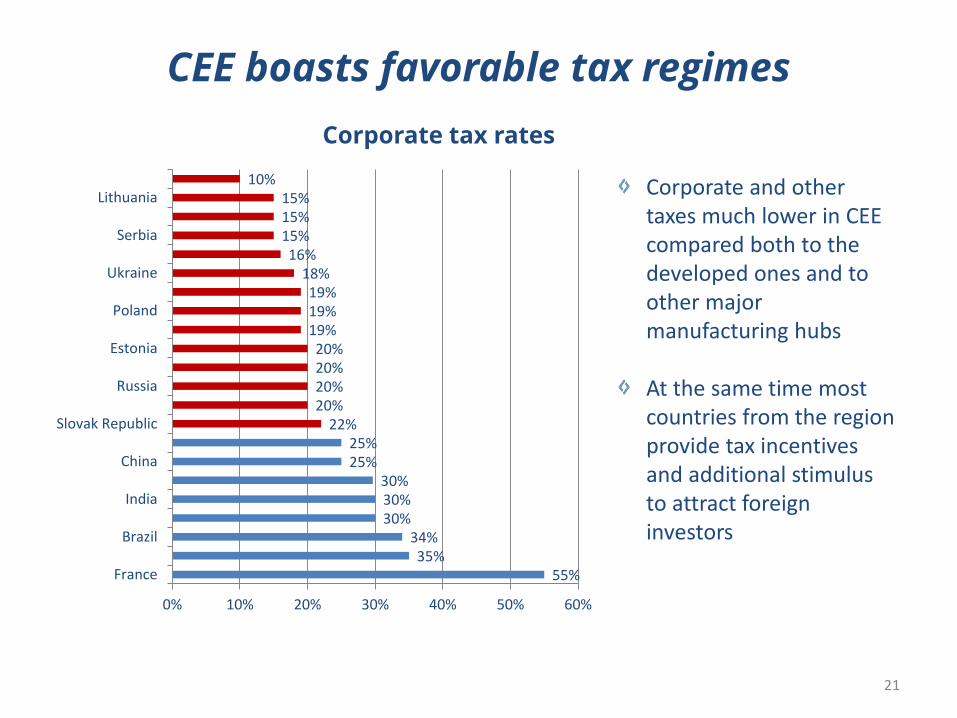

CEE boasts favorable tax regimes

Corporate tax rates

55% 35%

34% 30% 30% 30%

25% 25%

22% 20% 20% 20% 20%

19% 19% 19%

18% 16%

15% 15% 15%

10%

0% 10% 20% 30% 40% 50% 60%

France

Brazil

India

China

Slovak Republic

Russia

Estonia

Poland

Ukraine

Serbia

Lithuania Corporate and other taxes much lower in CEE compared both to the developed ones and to other major manufacturing hubs At the same time most countries from the region provide tax incentives and additional stimulus to attract foreign investors

21

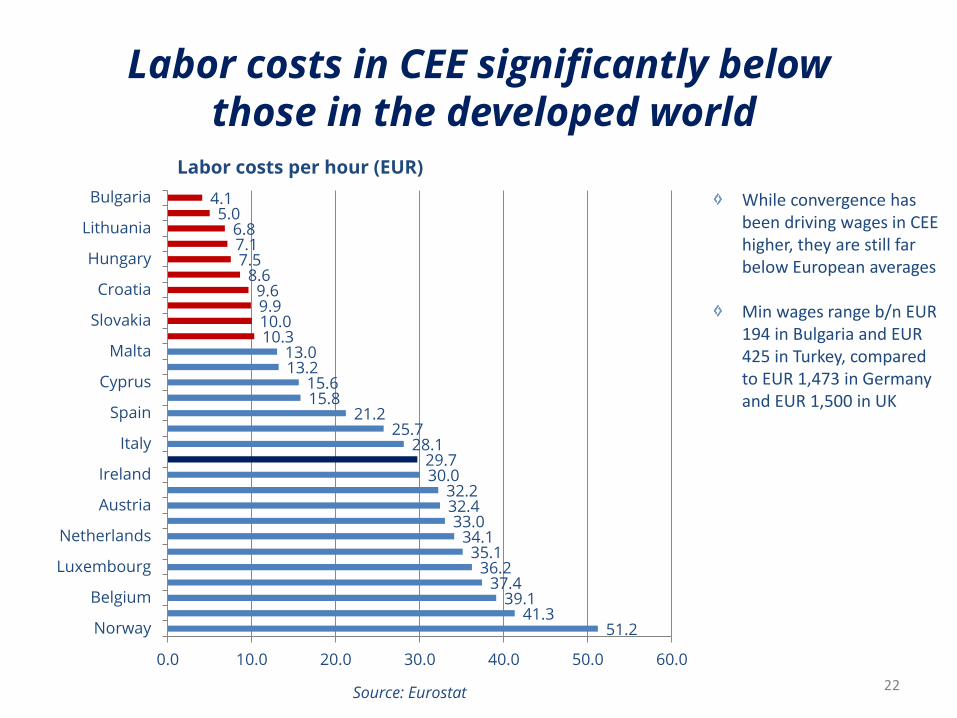

Labor costs in CEE significantly below those in the developed world

51.2 41.3

39.1 37.4

36.2 35.1

34.1 33.0

32.4 32.2

30.0 29.7

28.1 25.7

21.2 15.8 15.6

13.2 13.0

10.3 10.0 9.9 9.6

8.6 7.5 7.1 6.8

5.0 4.1

0.0 10.0 20.0 30.0 40.0 50.0 60.0

Norway

Belgium

Luxembourg

Netherlands

Austria

Ireland

Italy

Spain

Cyprus

Malta

Slovakia

Croatia

Hungary

Lithuania

Bulgaria

Labor costs per hour (EUR)

While convergence has been driving wages in CEE higher, they are still far below European averages Min wages range b/n EUR 194 in Bulgaria and EUR 425 in Turkey, compared to EUR 1,473 in Germany and EUR 1,500 in UK

Source: Eurostat 22

CEE boasts well educated and qualified workforce

17.1

24.1

35.3

15.1

9.2

15.1

11.7 9.5

7.5

26.5

33.1 32.7

27.8

24.3 23.9

20.9 19.7 18.6

14.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2000

2015

People with tertiary education (% of population)

Share of people with tertiary education in CEE steadily on the rise

Source: Eurostat

23

Steady growth of employment in science and tech

37

42

35

31 28

33 32 31

28 29

21

45

50 47

41 40 38

36 36 35 33

26

0

10

20

30

40

50

60

2004

2014

Human resources in science and technology (% of population)

Science and technology play an increasing role in CEE economies with R&D expenditures rising fast The Czech Republic, Estonia, Hungary, Lithuania now spending over 1% of GDP on R&D while the figure still low compared to EU average of 2%, it is rapidly rising Source: Eurostat

24

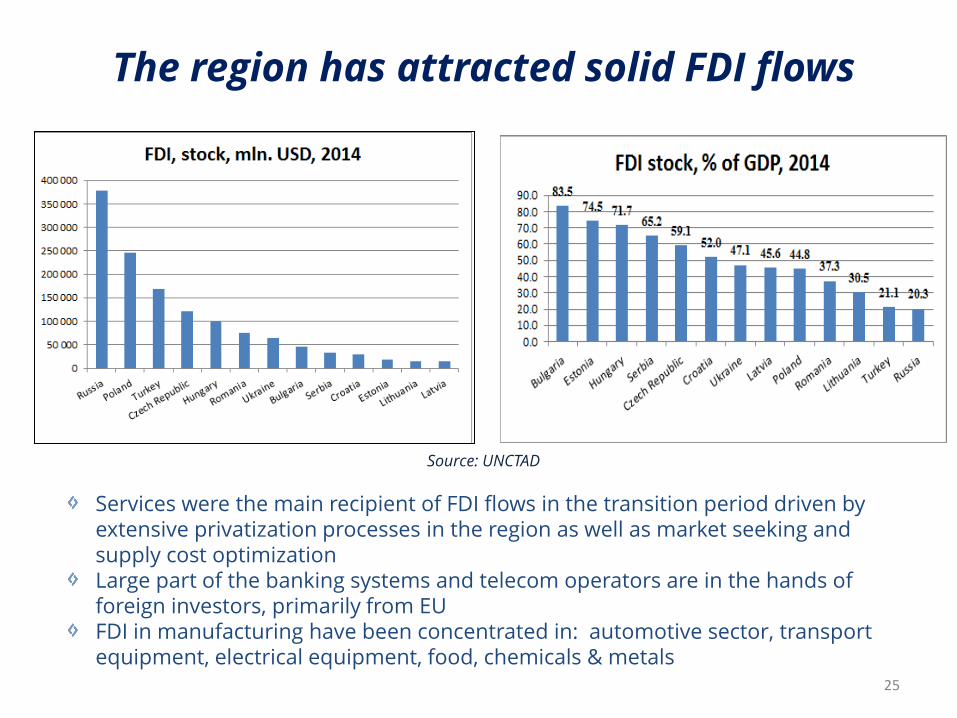

The region has attracted solid FDI flows

Services were the main recipient of FDI flows in the transition period driven by extensive privatization processes in the region as well as market seeking and supply cost optimization Large part of the banking systems and telecom operators are in the hands of foreign investors, primarily from EU FDI in manufacturing have been concentrated in: automotive sector, transport equipment, electrical equipment, food, chemicals & metals

Source: UNCTAD

25

EU accession provided abundant resources to CEE

Since the CEE countries became EU members, EU co-financing has become an essential factor for their development EU Structural and Cohesion Funds (SCF) accounted for 11.3 - 25% of annual GDP in 2007-2013 programming period, fostering regional cohesion

Large part of EU SCF financed major infrastructure projects, but also environment projects, renewable energy, SMEs, education & health, information society, increasing the adaptability of workers and enterprises, strengthening of institutional capacity, etc.

Poland Czech Republic Hungary Romania Slovakia Lithuania Bulgaria Latvia Slovenia Estonia Croatia*

EU funds, 2007-2013 (EUR, bln.) 67.19 26.3 24.92 19.18 11.65 6.77 6.67 4.54 4.1 3.4 1

EU funds/GDP (%) 17.2% 17.6% 25.4% 13.4% 16.2% 19.6% 16.7% 19.4% 11.6% 18.5% 2.3%

Total: EUR 175.7 bln = 16.2% of GDP on average

*Croatia joined the EU in July 2013 26

EU cohesion policy 2014-2020 to provide further boost to regional competitiveness

0

10

20

30

40

50

60

70

8077.6

32.8 28.6

23 22 21.9 21.5 19.2

15.9 15.5 14 11.8 8.6

7.6 6.8 4.5 3.6 3.1 2.3 2.1 1.5 1.4 1.2 1.2 0.7 0.7 0.6 0.1

EU cohesion policy 2014-2020, allocation by country (EUR bln)

CEE to receive over 50% of EU 2014-2020 Cohesion Policy = more than EUR 190 bln EU 2014-2020 Cohesion Policy targets: R&D, ICT sector, sustainable transport, SMEs, renewable energy & energy efficiency, environment, employment and education

27

Competitiveness of local economies steadily on the rise

Country Rank, 2006

Rank, 2016

Change of position

Estonia 18 16 2

Lithuania 22 20 2

Poland 56 25 31

Slovenia 42 29 13

Slovakia 32 29 3

Czech Republic 59 36 23

Romania 62 37 25

Mexico 58 38 20

Bulgaria 48 38 10

Hungary 46 42 4

Thailand 23 49 -26

Russia 95 51 44

Turkey 60 55 5

Croatia 115 65 50

Vietnam 75 78 -3

China 89 90 -1

Serbia 78 91 -13

Indonesia 114 114 0

India 116 130 -14

Competitiveness of local economies has registered solid advance as measured by the Ease of Doing Business Ranking by the World Bank Most CEE countries are in top 50 5 countries hold a position in top 30

28

CEE increasing role in European value chains

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

56.7

114.0

54.0

41.6 36.2

15.8

5.7 6.2 8.7 4.8 1.2 4.5 3.2

141.6 135.7

119.1

72.4

61.6

40.2

14.9 14.1 12.8 8.7 7.9 7.7 7.5

2005

2015

Export of CEE countries to EU (EUR bln)

Export of CEE countries to EU have jumped by more than 80% b/n 2005 and 2015 Share in total EU imports now above 37% (2005: 29.8%) and significantly lower before that Most countries export over 50% of production to EU

2015

Czech Republic 83.4%

Hungary 81.4%

Poland 79.2%

Estonia 75.2%

Romania 73.7%

Latvia 69.5%

Croatia 65.9%

Bulgaria 64.2%

Serbia 63.7%

Lithuania 61.3%

Turkey 44.5%

Russia 44.4%

Ukraine 24.2%

Share of export to the EU in total export (2015)

Source: Eurostat, KCM calculations

Eastern Europe becoming a major manufacturing

hub for multinationals In the past 15 years the regions has

seen massive inflows of foreign investors

The crisis has affected flows to the region, but now there is a clear trend of Eastern Europe establishing itself as a major manufacturing hub

Much lower total production costs – labor, office rentals, electricity, taxes, tax and other incentives many multinational corporations shifting production to Eastern Europe

Location becoming more important – proximity, both in geographical and cultural terms, favors Eastern Europe over other manufacturing hubs like Asia and Latin America

EU membership and accession make trading much easier

NEARSHORING becoming more and more popular

30

Eastern Europe vs. Asia

Eastern Europe is increasingly recognizing the importance of quality as a differentiator to low-cost Asian producers Wages have been growing robustly in Asia in the past years with wage gap between Eastern Europe and Asia narrowing; wages in China have more than tripled in the past decade Realizing the trend of nearshoring, even Asian companies are investing in the region Eastern Europe now moving up the value chain from low-cost manufacturing centers, regional economies now facing the challenge to become innovative knowledge-based economies

Rather than viewing the CEE region as a cheap production base, multinationals increasingly consider it to be a source of expertise. The trend will continue and a deep supplier base will emerge here as local companies become integrated into global supply chains. Production gains in CEE have come from better management rather than from growing population and capital investment (the Asian case).

31

Automotive sector in CEE

• Assessing the potential of the region, Western European and Asian companies invested in local automakers and established new companies. Fiat acquired Poland’s FSM in 1992; Volkswagen took over Škoda in the Czech Republic in 1991; and Renault bought Dacia in Romania in 1998. Audi, Opel, and Suzuki all opened plants in Hungary; Peugeot, Toyota, and Hyundai established operations in the Czech Republic; and Peugeot Citroën invested in Slovakia. Renault, Toyota, Hyundai, Honda, Ford and Fiat all have production facilities in Turkey. Russia is the top producer in the whole CEE region with sizable production by Hyundai, Renault, Volkswagen, Nissan, General Motors and others.

• Along with the automakers came automotive parts suppliers, creating automotive clusters across the region. The factory of Audi in Hungary is now the biggest car engines producer in the world.

• Nearly 2/3 of automotive exports go to EU-15 markets, and 60% of sales are concentrated in Germany, the UK, and France 32

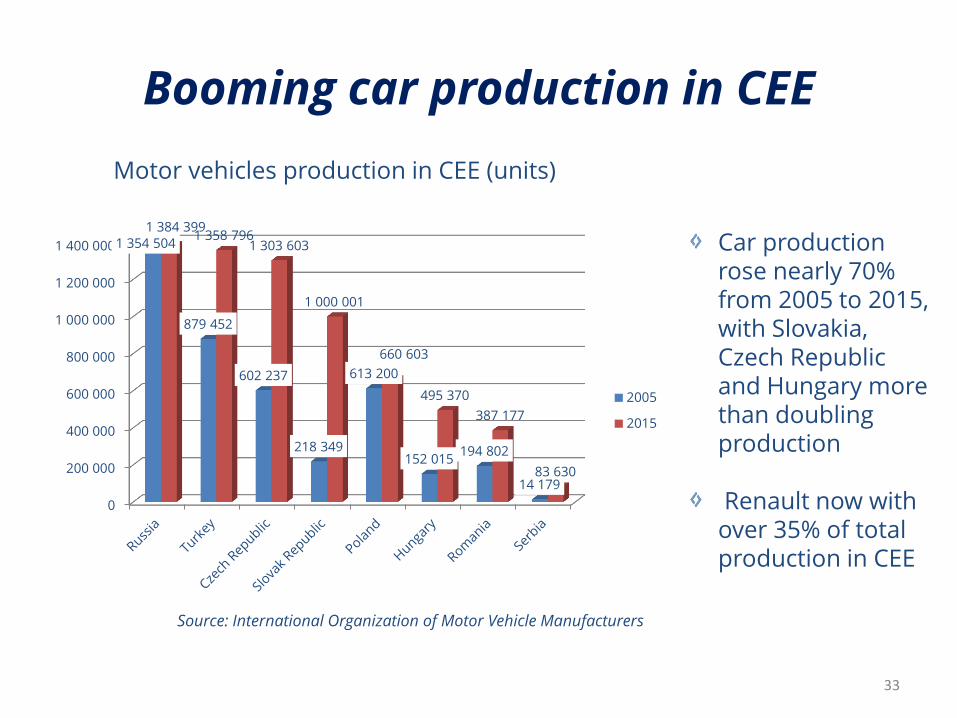

Booming car production in CEE

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 0001 354 504

879 452

602 237

218 349

613 200

152 015 194 802

14 179

1 384 399 1 358 796

1 303 603

1 000 001

660 603

495 370

387 177

83 630

2005

2015

Motor vehicles production in CEE (units)

Car production rose nearly 70% from 2005 to 2015, with Slovakia, Czech Republic and Hungary more than doubling production Renault now with over 35% of total production in CEE

Source: International Organization of Motor Vehicle Manufacturers

33

Eastern Europe – the new Silicon Valley

The human assets of the region make it a major player in technological innovation Forbes consistently ranks CEE at the top of the world in educational achievement in math, science & technology.

In 2013, 16 out of the 24 finalists of Google's annual Code Jam programming competition were from Central and Eastern Europe

Solid growth of number of employees in ICT sector (Estonia: +128% in the past 10 years, Romania: +120%, Bulgaria: +84%).

Many significant tech businesses have started in CEE:

- Skype founded by Estonians, acquired by Microsoft for $8.5 bln

- Whatsapp founded by Ukrainian, acquired by Facebook for $19 bln

- Prezi launched in Hungary as online tool for creating presentations

- Major cyber security companies - AVG Technologies, Avast and ESET, in the Czech Republic and Slovakia

Abundant EU funding supports start-ups from the tech sector

34

Pronounced success in outsourcing

Country European Ranking

Global ranking

Poland 1 10

Bulgaria 2 12

Romania 3 13

Russia 4 17

Latvia 5 18

Turkey 6 21

Ukraine 7 24

Czech Republic

8 26

A.T. Kearney’s Global Services Location Index. 2016

CEE countries climbing up the global rankings for Business Process Outsourcing (A.T. Kearney’s

Global Services Location Index includes the

top 55 countries for BPO) While low cost of well-qualified employees, with multi-language skills used to be main driver for outsourcing, now many CEE firms have grown into solid centers of competence, equal tech partners and value-added developers shift from outsourcing to outsharing CEE outsourcing industry projected to grow at CAGR of 10% and reach USD 1.6 trln by 2020

35

CEE stock markets lagging behind

Performance of MSCI EFM Europe+CIS

3M 11.56%

YTD 8.54%

1Y -20.14%

3Y, annualized

-10.88%

5Y, annualized

-10.06%

10Y, annualized

-6.59%

Change since 2007 peak

-56.1% 0.000

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

2004 2006 2008 2010 2012 2014

MSCI ACWI

MSCI EFM EUROPE + CIS

(E+C)

MSCI EM ASIA

MSCI EM LATIN

AMERICA

MSCI EUROPE

MSCI NORTH AMERICA

Lagging performance, high catch-up potential

Attractive valuation ratios across CEE

0

5

10

15

20

10.24

19.51

14.33 16.00 15.93 15.30

17.99

11.44

P/E, ttm

0.00%

1.00%

2.00%

3.00%

4.00%

5.00% 4.01%

2.53% 3.11%

4.45%

1.92% 1.71% 1.57%

3.71%

Dividend yield, %

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

0.93

2.60

1.54 1.64 1.50

2.80 3.13

1.30

P/B, mrq

Source: Reuters, KCM calculations 37

Compelling reasons to invest in CEE

-CEE turning into major manufacturing hub -> rising role in global value chains (over 50% of exports to EU) -Major global companies shift production here -> solid FDIs in automotive sector, transport equipment,

electrical equipment, food, chemicals & metals -CEE turning into the new Silicon Valley due to highly qualified IT specialists

-Booming outsourcing sector -> CEE countries in top 20 for Business Process Outsourcing.

-Buoyant region with appreciable scale converging with the West -Growing much faster than developed Europe

-Among lowest taxes in the world -Low labor costs –> 27% of euro-zone average -Well-educated & highly qualified workforce

-Abundant EU funding boosts competitiveness -Geographic & cultural proximity to the West

-Greater focus on quality vs. low cost Asian producers

Why invest in Emerging Europe now

Solid catch-up potential based on lagging performance in past years

Based on bright macroeconomic outlook and compelling data, the region is considered a safe haven.

Improving sentiment towards emerging markets as a whole to spark uptrend

Attractive valuation ratios with multiples lower than peers and historic averages

Low market penetration -> solid catch-up potential

Improving liquidity

39

Disclaimer This presentation is for information purposes only and does not represent a proposal for buying of selling securities. While reasonable care has been taken to ensure that the information contained herein is not untrue or misleading at the time of publication, Karoll Financial Group makes no representation that it is accurate or complete. The information contained herein is subject to change without notice. Karoll Financial Group makes no representations or warranties whatsoever as to the data and information provided in any third party referenced website and shall have no liability or responsibility arising out of or in connection with any such referenced website. Karoll Financial Group does not maintain a predetermined schedule for publication of research and will not necessarily update this presentation. Karoll Financial Group and any of its officers, employees, related and discretionary accounts may, to the extent not disclosed above and to the extent permitted by law, have long or short positions or may be otherwise interested in the investments or securities referred to in this document, or in options on such investments or securities, or in related investments (including other securities of the same issuer). Karoll, or its clients or customers, may trade as market maker in the investments or securities that are the subject of this document, or in related investments, and may have acted upon, bought for their own account or used the information contained in this document, before its publication. In addition, Karoll Financial Group may provide banking, insurance or asset management services for, or solicit such business from, any company referred to in this presentation. Any investments referred to herein may involve significant risk, may be illiquid and may not be suitable for all investors. Investors should note that income from such investments or other securities, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investment mentioned in this presentation. This presentation should not be regarded by recipients as a substitute for the exercise of their own judgment. Investors should make their own investigations and investment decisions without relying on this presentation. Only investors with sufficient knowledge and experience in financial matters to evaluate the merits and risks should consider an investment in any issuer or market discussed herein and other persons should not take any action on the basis of this presentation. Before entering into any transaction, investors should consult their advisors and understand the risks involved in these transactions. Investors should make themselves aware of any local laws governing such securities or investments.

40

Contacts:

Daniel Ganev Managing Director, Karoll Capital Management

E-mail: [email protected] Tel: +359 2 400 8 382

Nadia Nedelcheva, CFA Head of Portfolio Management, Karoll Capital Management

E-mail: [email protected] Tel: +359 2 400 8 386

Headquarters Sofia 1 Zlatovrah Str., Sofia 1164, Bulgaria | (+359 2) / 4008 382 | [email protected] www.karollcapital.bg