ars.els-cdn.com · Web viewThe natural gas price trajectories from the Capped Price and Rising...

20

DRAFT Supplementary Material S1. Modeling Assumptions Figure S1 shows the assumed carbon price trajectories for the Capped Price Case (blue) and the Rising Price Case (red) as discussed in the main text. The carbon price is specified through 2080, but shown here through 2050 for convenience (to preserve the scale). Figure S1. Carbon prices in the cases developed in this study. As discussed in the main text and below, carbon prices were chosen in this study such that the Capped Price Case would yield emissions outcomes consistent with a known, publicly available benchmark, namely the AEO 2017 Reference Case, which includes a stylized representation of the CPP (EIA 2017). 1

Transcript of ars.els-cdn.com · Web viewThe natural gas price trajectories from the Capped Price and Rising...

DRAFT

Supplementary Material

S1. Modeling Assumptions

Figure S1 shows the assumed carbon price trajectories for the Capped Price Case (blue) and the Rising

Price Case (red) as discussed in the main text. The carbon price is specified through 2080, but shown

here through 2050 for convenience (to preserve the scale).

Figure S1. Carbon prices in the cases developed in this study. As discussed in the main text and below, carbon

prices were chosen in this study such that the Capped Price Case would yield emissions outcomes consistent with a

known, publicly available benchmark, namely the AEO 2017 Reference Case, which includes a stylized

representation of the CPP (EIA 2017).

Figure S2 shows the power sector CO2 emissions trajectories that follow from the carbon prices

shown in Figure S1. The Capped Price Case yields an emissions trajectory (blue line) that closely matches

the emissions associated with the CPP (orange line), as represented by EIA in the AEO 2017 Reference

Case (EIA 2017). Although the carbon price in the Rising Price Case is the same as the carbon price in the

Capped Price Case prior to 2030, the emissions are lower (red line) during this period due to anticipation

1

DRAFT

of higher prices (the effect of foresight). The Reference Case, which is otherwise identical to the carbon

price cases but does not include a carbon price (black line) is shown for comparison.

Figure S2. Emissions trajectories in the cases developed in this study. The orange line indicates the emissions

associated with the CPP as projected by EIA in the AEO 2017 Reference Case (EIA 2017).

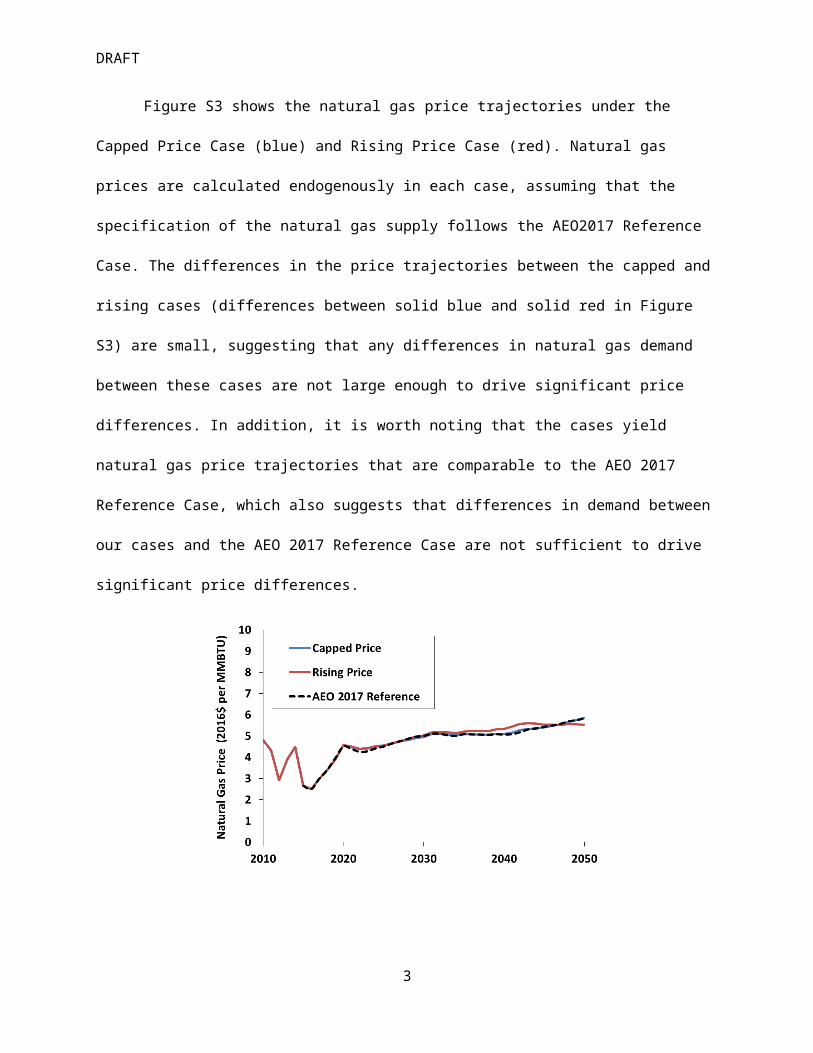

Figure S3 shows the natural gas price trajectories under the Capped Price Case (blue) and Rising

Price Case (red). Natural gas prices are calculated endogenously in each case, assuming that the

specification of the natural gas supply follows the AEO2017 Reference Case. The differences in the price

trajectories between the capped and rising cases (differences between solid blue and solid red in Figure

S3) are small, suggesting that any differences in natural gas demand between these cases are not large

enough to drive significant price differences. In addition, it is worth noting that the cases yield natural

gas price trajectories that are comparable to the AEO 2017 Reference Case, which also suggests that

differences in demand between our cases and the AEO 2017 Reference Case are not sufficient to drive

significant price differences.

2

DRAFT

Figure S3. Natural gas prices at Henry Hub in the cases developed in this study. The natural gas price trajectories

from the Capped Price and Rising Price Cases closely track the natural gas price trajectory from the AEO 2017

Reference Case (EIA 2017), from which the underlying resource assumptions were adopted.

Table S1 compares initial capital cost assumptions for several major technologies in AEO 2017

and Table S2 provides values for fixed O&M, variable O&M, and heat rates for relevant technologies.

Capital costs decline over time as a function of cumulative deployment, so the trajectories of capital

costs are case-specific, although the variability among cases considered in this study is relatively small.

For many mature technologies, the overall cost decline is also small, although for some technologies it

can be significant. For example, in the Capped Price Case, the capital cost for solar PV declines from its

initial value of $2,161 to $1,682 per KW in 2030. These cost trajectories fall within the range of other

recent estimates. For example, in most years this trajectory is between the “Mid” and “High” estimates

provided in the National Renewable Energy Laboratory’s 2016 Annual Technology Baseline.1

1 See NREL (National Renewable Energy Laboratory), 2016 Annual Technology Baseline. Available at: http://nreldev.nrel.gov/analysis/pdfs/2016-ATB-Summary-Final.pdf.

3

DRAFT

Table S1. Initial total overnight capital costs in AEO 2017, which are the costs used in this study. The year

associated with each cost may vary by technology since the first year in which the technology can be deployed

varies due to differences in construction times. Total overnight capital costs include contingency factors (project

contingency factors and technology optimism factors), which are applied to the base overnight capital costs, as

well as learning realized prior to the first year in which endogenous installations are possible. However, the costs

reported here do not include any regional or ambient technology multipliers or the ITC for eligible technologies.

TechnologyTotal Overnight Capital Cost

(AEO 2017 and this study)

(2016 $ per KW)

Coal with CCS 5,511

Advanced NGCC 1,092

Advanced NGCC with CCS 2,136

Advanced Nuclear 5,360

Wind (onshore) 1,860

Solar PV 2,161

Table S2. Fixed O&M, variable O&M and heat rates for selected technologies, following AEO 2017 assumptions.

Technology Fixed O&M Costs Variable O&M Costs Heat Rates (nth of a kind)

(2016 $ per KW per year) (2016 $ per MWh) BTU per KWh

Coal with CCS 80.8 9.5 9,257

Advanced NGCC 9.9 2.0 6,200

Advanced NGCC with CCS 33.2 7.1 7,493

Advanced Nuclear 99.7 2.3 -

Wind (onshore) 46.7 - -

Solar PV 21.7 - -

4

DRAFT

Whereas the capacity factors for solar (for a given region) do not change over time, the capacity

factors for wind (for a given resource class and region) increase as a function of cumulative deployment.

In addition, four wind classes (representing differences in resource quality) are included. When weighted

by deployment, the national average annual capacity factors for new wind and solar PV capacity are

approximately 41 percent and 24 percent, respectively. The equivalent national average capacity values

on peak for wind and solar PV (calculated endogenously by the model) are 12 percent and 48 percent,

respectively, although they vary over time with cumulative deployment and shifts in load patterns.

Regional variability in both quantities for both wind and solar PV is significant.

Deployment of wind is further affected by the way that wind cost heterogeneity is represented.

In addition to representing different wind classes explicitly, each wind class is characterized by a supply

curve that accounts for other differences in natural resource quality (e.g., terrain slope and accessibility),

costs of upgrading distribution and transmission to accommodate resources that may not be near

existing transmission, and other market factors. The capital costs reported in Table S1 indicate the costs

associated with the first step on this supply curve. Additional steps on the curve increase the capital cost

by 10%, 25%, 50% an 100%, respectively. Deployment of wind and solar PV may be further affected by

the costs of transmission, since there is an additional cost imposed whenever new transmission is added

to exchange generation or capacity between adjacent regions (the magnitude of that cost depends on

which regions are being connected). While this transmission cost is not associated with particular

technologies, wind and solar PV are more likely to be built far away from the load that they serve and

thus more likely to motivate the need for additional transmission capacity.

Finally, Table S3 shows the tax credits for wind and solar PV, assuming wind takes the PTC and

solar PV takes the ITC. The tax credits expire in 2020 for wind and revert to 10 percent in the case of

solar PV in 2020, with projects eligible provided that they begin construction by this time. The years in

Table S3 reflect online years, and because projects take several years to build, the credits are assumed

5

DRAFT

to apply to projects that come online several years after 2020. Although this study does not report

results at a regional level, a map of the EMM regions is also provided below in order to provide a sense

of the resolution of the model used in this study.

Table S3. Schedule of tax credits for wind and solar PV, following AEO 2017 Reference Case assumptions.

Online Year Wind (onshore) PTC Solar PV ITC

2016 $ per MWh % of initial capital cost

2018 22.53 30%

2019 22.53 30%

2020 22.53 30%

2021 18.03 30%

2022 13.52 26%

2023 9.01 22%

2024 and thereafter 0 10%

6

DRAFT

Figure S4. Map of EMM regions in NEMS from EIA (EIA 2015).2

2 See http://www.eia.gov/outlooks/archive/aeo15/pdf/0383(2015).pdf.

7

DRAFT

S2. Comparison of Rolling Foresight and Perfect Foresight Approaches

As discussed in the main text, the EMM uses a rolling foresight approach to account for future

expectations when solving for investment in the following year. In this approach, future information in

year t is only used to solve for investment in year t+1, at which point the process repeats. This approach

can be contrasted with a perfect foresight approach, in which the time path of investment is the

outcome of a single inter-temporal optimization. In this approach, all information about future

technology, demand and policy is assumed to be known, and the time path of investment (and other

quantities) is the one that minimizes the net present value (NPV) of all future costs. While perfect

foresight is an idealized assumption about the real world, the approach is often considered appropriate

for normative analysis in which optimality is a desirable benchmark. For this reason, it is useful to know

whether and to what extent the rolling foresight approach approximates perfect foresight.

To examine this question quantitatively, we consider simplified representations of the two

approaches. In both approaches, we assume technology costs and fuel prices are exogenous. We further

assume that the perfect foresight model is discretized into several time periods: 2020, 2025, 2030, 2035,

2040, 2045 and 2050. These time periods are the only ones considered by the perfect foresight model.

In contrast, in the rolling foresight model (with a 30-year rolling foresight window comparable to the

EMM), the set of time periods gets updated as the model propagates forward. As an example, when

solving for investment in 2030, the time periods would be: 2025, 2030, 2035, 2040, 2045, 2050, 2055. In

this example, 2025 is the current period (t), and 2030 is the period from which output is recorded (t+1).

In both of these approaches, one may define Ci as the cost difference between the two most

competitive technologies, where i indexes the absolute year (let i=1 in 2025, i=2 in 2030, etc). Ci could be

either positive or negative. Further assume that one of the technologies is NGCC, and that NGCC is

cheaper than the alternative until 2040, after which it is more expensive. So, the vector of cost

8

DRAFT

differences might be: C1, C2, C3 < 0; C4=0, C5, C6, C7 > 0. A negative value means that NGCC is less costly

than the alternative.3

One may also define Dj as the discount factor for period j, where j is defined from the start of

the respective model for a given approach. So in the perfect foresight model, D1 would be the discount

term applied in year 2025, while under the rolling foresight model solving for investment in 2030, D1

would be the discount term in year 2030. D1 is related to the discount rate (r) by: D1 = 1/(1+r)5, D2 =1/

(1+r)10, D3 = 1/(1+r)15 etc. Note that D3 = D2*D1 and generally Dj+1 = Dj*D1.

With the information above, one may compare the outcomes of the two approaches. Under the

perfect foresight approach, NGCC would be built in 2030 if C2*D2 + C3*D3 + C4*D4 + C5*D5 + C6*D6 < 0. This

condition says that, starting in 2030, the NPV of the cost of NGCC must be less than the NPV cost of its

nearest competitor, where all costs are discounted back to the start of the model in 2020.

Under the rolling foresight approach, NGCC would be built in 2030 if C2*D1 + C3*D2 + C4*D3 +

C5*D4 + C6*D5 + C7*D6 < 0. In this framework, the model makes a decision in 2025 about what gets built

in the next period (in this case 2030), taking into account information through 2055. All costs are

discounted back to the start year, which in this case is 2025. Note that the expression above for perfect

foresight could be re-written as D1*(C2*D1 + C3*D2 + C4*D3 + C5*D4 + C6*D5) < 0. Thus the conditions for

NGCC expansion are equivalent in the two approaches, except for the final term in the rolling foresight

approach (C7*D6).

The inclusion of discounting implies that this final term is likely to be small relative to the total

NPV cost. In addition, this term is positive under the assumptions above, making the rolling foresight

approach less likely to expand NGCC than the perfect foresight approach. Put differently, rolling

foresight, under the assumptions above, yields a more restrictive condition on the expansion of NGCC

3 As discussed earlier, R-NEMS does not include foresight about the evolution of technology capital costs, which could lead to differences with a perfect foresight approach.

9

DRAFT

than perfect foresight. This result makes sense intuitively, because a perfect foresight model that runs

only until 2050 does not account for the world after 2050 when making decisions about 2030, whereas a

rolling foresight model with a 30-year foresight window accounts for the world through 2055 when

making decisions about 2030.4 Under a rapidly escalating carbon price, this additional increment of

foresight in the rolling approach slightly discourages early expansion of NGCC relative to the perfect

foresight approach. Nonetheless, such a conceptual comparison between the approaches suggests that

the rolling foresight approach in the EMM can be viewed as a reasonable approximation to perfect

foresight.

S3. Analytic Model of Anticipation

The role of foresight in the scenarios discussed in this paper can be further illustrated using a stylized

analytic model of the competition between two technologies. In Figure S6, the red line represents an

illustrative emissions-free technology (such as wind or solar PV), with a levelized cost of cef. That is, if the

technology is installed at t=0, then the cost to produce power in each year (accounting for capital and

operating costs) is cef until t=T. In this example, T represents the time at which capital is fully

depreciated, after which the cost is much lower, and therefore negligible in an NPV sense. When

choosing whether to install this technology at t=0, a model (or market actor) with foresight will examine

the NPV cost of the technology

Cost ef=∫0

T

cef ∙ e−rt dt (S1)

In Eq. S1, r is the discount rate, which, in this context, reflects the opportunity cost of capital.

4 Of course, the time periods considered in these two frameworks are illustrative. It is possible for a perfect foresight model to consider a larger or smaller time horizon, and similarly, it is possible for a rolling foresight model to look ahead by more or fewer years.

10

DRAFT

Figure S5. Illustration of cost trajectories for two competing technologies. The red line represents an illustrative

emissions-free technology, whereas the blue curve represents an illustrative emitting technology whose cost

increases with time due to an assumed rising carbon price.

In Figure S5, the blue curve represents an illustrative emitting technology (such as NGCC without

CCS). The time dependence of the cost reflects an assumption that the carbon penalty associated with

producing power from this technology increases due to an increasing carbon price. While the carbon

price might be assumed to increase rapidly (such as at 8 percent annually, as in the scenarios discussed

in this paper), the growth rate of the total cost of this technology (g) would be expected to increase

more gradually, perhaps at 1-2 percent annually. An additional assumption is that at some future time,

t*, the annual costs of producing power from these two technologies cross. Given the time at which

they cross, and the growth rate of the cost of the emitting technology, it is possible to show that the

initial cost of the emitting technology is cef e−g t∗¿¿. In that case, the NPV cost of the emitting technology

at time t=0 is

11

DRAFT

Cost em=∫0

T

cef e−¿∗¿ e¿ ∙e−rt dt¿ (S2)

Given this information about the NPV cost of each technology, it is possible to solve for the value of t*

that equates the NPV costs of the two technologies. The resulting value of t* indicates the number of

years prior to the actual crossover year that a hypothetical actor with foresight would switch from

preferring the carbon emitting technology (which has an initially lower cost) to the emissions-free

technology. In effect, the value of t* indicates the extent to which investment choices are affected by

foresight. In a world without foresight, investment would switch from one technology to the other at

the crossover year and not before.

Setting Eq. S1 equal to Eq. S2 and solving for t* yields the following expression

t ¿= 1gln [( r

r−g )( e−(r−g )T−1e−rT−1 )] (S3)

One can evaluate Eq. S3 for different choices of the parameters, T, g and r. T is the period over which

capital is amortized. We assume this period is 30 years, which is consistent with the assumptions used in

the scenarios discussed in this paper. We assume that g is 1.5 percent, which is consistent with the

growth rate of the cost of NGCC between 2020 and 2040 in the Rising Price Case. We assume that r is 7

percent, which is consistent with typical values assumed for the opportunity cost of capital as well as

with assumptions used in the scenarios discussed in this paper. Using these parameters, we find that t*

is approximately 10 years. This implies that, in our scenarios, and in other scenarios with foresight and

comparable assumptions about other parameters, actors with foresight would be expected to anticipate

the crossover in technology costs by about a decade.

The applicability of this simplified conceptual framework to R-NEMS can be assessed by

examining the deployment of new NGCC capacity and the retirement of existing coal capacity as a

12

DRAFT

function of carbon price in the two scenarios. In panel (a) of Figure S6, it is clear that for any given

carbon price, the number of coal retirements is higher in the Rising Price Case than in the Capped Price

Case. This difference is driven by foresight – for any given instantaneous carbon price, the effective

carbon price used in making decisions about capacity is higher in the Rising Price Case than in the

Capped Price case, because the effective price captures information about the instantaneous price in

future years.

When coal retirements are plotted as a function of the carbon price achieved ten years in the

future (panel c), then the outcomes align more closely across the cases. This result is consistent with the

theoretical framework discussed above, which suggests that the inclusion of foresight allows the model

to anticipate future conditions by approximately ten years. The same observations can be applied to

NGCC capacity additions. In panel (b), the same instantaneous carbon price yields different amounts of

NGCC additions across the two cases, but in panel (d), when additions are plotted as a function of the

effective carbon price (i.e., the instantaneous carbon price ten years in the future), then the results align

more closely.

13

DRAFT

Coal Retirements NGCC Additions

Figure S6. Cumulative coal retirements (panels a and c) and cumulative NGCC capacity (panels b and d) as a

function of either the instantaneous carbon price (panels a and b) or the carbon price ten years in the future

(panels c and d) for the cases developed in this study. In each of the panels, outcomes from the Capped Price Case

are shown as blue circles and outcomes from the Rising Price Case are shown as red squares. In all panels,

cumulative additions or retirements are shown as the difference from a particular carbon price case and an

identical case without a carbon price in order to isolate the effect of the carbon price (i.e., control for additions or

retirements that occur due to load growth or other factors unrelated to the carbon price).

14