APPRAISAL REPORT - images.bizbuysell.com

223

APPRAISAL REPORT APPRAISAL OF A 2,400-Square-Foot Industrial Building Located at 1961 Whitney Mesa Drive Henderson, Nevada 89014 Owner of Record: County Funeral Services, LLC APN: 161-32-712-013 PREPARED FOR Clark County Credit Union c/o Mr. John Gentile 87 E. Lake Mead Parkway Henderson, Nevada 89015 PREPARED BY Luke J. Adamo, MAI Britton-Adamo Group/ROI Appraisal 55 Gibson Road, Suite 104 Henderson, Nevada 89012 Phone: 702-558-2144 Fax: 702-558-9933 File # 20-089 DATE OF “AS IS” VALUATION September 25, 2020

Transcript of APPRAISAL REPORT - images.bizbuysell.com

APPRAISAL REPORT

APPRAISAL OF

A 2,400-Square-Foot Industrial Building

Located at 1961 Whitney Mesa Drive

Henderson, Nevada 89014

Owner of Record: County Funeral Services, LLC

APN: 161-32-712-013

PREPARED FOR

Clark County Credit Union

c/o Mr. John Gentile

87 E. Lake Mead Parkway

Henderson, Nevada 89015

PREPARED BY

Luke J. Adamo, MAI

Britton-Adamo Group/ROI Appraisal

55 Gibson Road, Suite 104

Henderson, Nevada 89012 Phone: 702-558-2144 Fax: 702-558-9933

File # 20-089

DATE OF “AS IS” VALUATION

September 25, 2020

ROI Appraisal BBRRIITTTTOONN--AADDAAMMOO GGRROOUUPP

RR EE AA LL EE SS TT AA TT EE AA PP PP RR AA II SS EE RR SS && CC OO NN SS UU LL TT AA NN TT SS

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558.2144 • Fax 702.558.9933

September 29, 2020

Clark County Credit Union

c/o Mr. John Gentile

87 E. Lake Mead Parkway

Henderson, Nevada 89015

RE: A 2,400-square-foot industrial building located at 1961 Whitney Mesa Drive, Henderson,

Nevada 89014

Owner of Record: County Funeral Services, LLC

APN: 161-32-712-013

To Whom It May Concern:

As you requested, I have completed an appraisal of the above referenced property. The subject

property consists of a single-tenant, industrial building, located at 1961 Whitney Mesa Drive,

Henderson, Nevada 89014. The subject improvements consist of 2,400 square feet of total

building area, containing approximately 480 square feet of one-story office space and 1,920

square feet of warehouse space, indicating an office space ratio of roughly 20%. The subject is

situated on a 0.16-acre site located within the interior of the Green Valley Industrial Park, along the

south side of Whitney Mesa Drive, east of Mountain Vista Street, in the southeast portion of the

Las Vegas Valley, in the City of Henderson, Clark County, Nevada. The subject was constructed

in 2006 and is in an overall good condition for its age.

The subject is currently being operated as a crematorium and includes specific built-in

equipment for the business operation. The equipment is separately identified and valued within

the appraisal. The property is fully described in the attached report, which contains the data and

analysis from which the value estimates were formed.

The purpose of this appraisal is to estimate the market value of the subject property based upon the

following valuation scenario:

• Market Value of the Real Estate – “As Is” – fee simple interest

• Fair Market Value in Continued Use of the Equipment – “As Is” – fee simple interest

The client of this appraisal is Clark County Credit Union. The intended user of this appraisal is

Clark County Credit Union, the Small Business Administration and Nevada State Development

Corporation. The intended use of this appraisal is for loan underwriting and/or credit decisions.

The use of the appraisal, or any information contained herein, by any other party other than the

stated client, or for any other use than the stated intended use, is considered unauthorized and is

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558 .2144 • Fax 702.558.9933

prohibited. The appraisers and the appraisal firm will assume no responsibility for the results

from the unauthorized use of this report or the contents herein.

This appraisal has been prepared to comply with the Financial Institutions Reform, Recovery and

Enforcement Act of 1989 (FIRREA), the Uniform Standards of Professional Appraisal Practice

(USPAP), as promulgated by the Appraisal Standards Board and the Office of the Comptroller of

Currency, and Clark County Credit Union appraisal requirements. This report has been prepared

in an Appraisal Report format, as set forth under Standards Rule 2-2(a) of USPAP. The depth of

discussion contained in the report is specific to the needs of the client and for the intended use

stated herein.

After considering all of the available facts and subject to the underlying assumptions and limiting

conditions contained herein, it is our opinion that the market values in the subject, as of

September 25, 2020 are:

Component Market Value

Real Estate – “As Is” – fee simple interest $430,000

Continued Use of the Equipment – “As Is” – fee simple interest $100,000

To determine actual mechanical condition of the equipment is outside of our expertise and the

scope of this assignment. The equipment appeared to be in functional and good condition. If it is

the client’s desire to verify the physical condition and/or needed repairs of the subject

equipment, the client should consult a qualified mechanic/technician.

The equipment value is for business personal property only and exclude consideration of real

estate or goodwill, and it is assumed there are no hidden defects which are not discernible from a

visual inspection and which could affect value. The owner is further assumed to have fee simple

ownership of the various appraised items, which are appraised assuming a clear and marketable

title.

The exposure time associated with the value conclusion is estimated at 12 months. The

estimated marketing time for the subject, as of the date of value, is 12 months.

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558 .2144 • Fax 702.558.9933

Thank you for giving us the opportunity to be of service to you in this important matter. If you

have any questions regarding the attached appraisal report, or require further assistance, please

do not hesitate to call our office at 702-558-2144.

Sincerely,

Luke J. Adamo, MAI

Certified General Appraiser #07352

State of Nevada

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558 .2144 • Fax 702.558.9933

COVID-19 Disclaimer

As of the date of this appraisal, the world is being significantly affected by COVID-19, also

known as the coronavirus. Reports are that this virus has obviously affected all aspects of the

real estate market. Specifically, there are less sales as potential buyers and brokers cannot

inspect properties and the majority of real estate professionals are working remotely from their

homes. According to CoStar as of March 15, 2020, “Early signs are emerging of a potential

slowdown in U.S. commercial real estate sales from the impact of the coronavirus pandemic. For

the three-week period following Feb. 21, when stock markets first began retreating from historic

highs, the pace of commercial property sales was about half what it was same three weeks a year

ago, according to CoStar data. Multifamily property sales were down about 58%. Industrial sales

sank 63%, retail declined 61% and hospitality showed a 37% drop. The one relative bright spot

was office property sales, which were only off slightly by 4.4%.”

This is obviously one of the most significant economic events in history and the fall out is

difficult to measure for the next few months. Never before has the Governor of the State of

Nevada ordered all casinos and non-essential businesses to close. These closures started on

March 18, 2020. Although phased reopening has begun, this has already lead to significant

layoffs, which will undoubtedly result in missed mortgage payments and other financial damage

to the local economy. Based on the current market data and the recent historical operation of the

subject, the opinion of the market value in this appraisal is valid. However, this pandemic could

cause this opinion of value to change once the effects of the market conditions are more known,

which could be at any time.

The positive aspect of this crisis is that interest rates have been significantly lowered which is

leading to an increase in the refinancing of real estate. In the first week of March, Treasury

yields on some bonds fell to their lowest level since 2001 and the Federal Reserve took the rare

action of making an emergency cut to interest rates to support the market. When Treasury yields

fall, banks charge lower interest rates for mortgages. These rates have really fallen since the first

of March 2020. On top of collapsing Treasury yields, the Federal Reserve announced a rare

emergency rate cut in response to concern over the effect of the rapidly spreading coronavirus on

global growth. They announced a 50-basis point reduction in the target rate on March 3, 2020.

According to the Mortgage Bankers Association (MBA), their Refinance Index increased 26%

on the second week of March from the previous week before much of the capital markets’

turmoil. “The 30-year fixed rate mortgage dropped to its lowest level in more than seven years

last week, amidst increasing concerns regarding the economic impact from the spread of the

coronavirus, as well as the tremendous financial market volatility,” Mike Fratantoni, MBA's

senior vice president and chief economist, said in a statement. “Given the further drop in

Treasury rates this week, we expect refinance activity will increase even more until fears subside

and rates stabilize.” Although these refinance statistics are more reflective of the residential

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558 .2144 • Fax 702.558.9933

mortgage industry, the lower interest rates will also lead to the refinancing of commercial real

estate mortgages.

A historical analysis or real estate prices due to catastrophic economic events indicates prices

will likely decrease. The great recession caused by the sub-prime lending crises that took hold in

2008 and continued into 2011. The charts below illustrate industrial building prices for the Las

Vegas area.

The price decline in 2008 at the start of the great recession was far greater, dropping over 70%

from 3rd Quarter 2007 to 3rd Quarter 2010, and remaining stagnant through 2013. As indicated in

the table above, according to CoStar Analytics, the anticipation is for declines in property values

of nearly 20% over the next year with an equivalent recovery over the following year.

There is great debate about how the Covid-19 Pandemic will impact commercial real estate

prices. To date there has been nominal data to indicate whether prices are decreasing, as many

sellers have pulled their listings off the market and most buyers remain sidelined to determine

the fallout from lost employment and shuttered small businesses.

A number of brokers in the Las Vegas market area were consulted over the previous month in

regard to the impact of the current market conditions with consideration given to COVID-19.

Although there is limited comparable data to develop a specific adjustment, there is a generally

consensus of some negative impacts to commercial real estate. We are aware of transactions that

have been renegotiated a slightly lower rates of 5%-10%, rate reductions by property managers

55 South G ibson Road • Su i te 104 • Henderson, NV 89012

Phone 702.558 .2144 • Fax 702.558.9933

as a concession to existing tenants of 5%, and deferred rent payments. These factors were

considered in various components within the valuation.

While this appraisal reports an exposure time opinion, marketing times may increase due to the

overall uncertainty in the market at this time due to market participants putting buying/selling

plans on hold until a more clear picture of the extent of the impacts of the virus is determined.

The few transactions that have closed, have yet to show any clear impact. A recent article

published in Market Watch reports delinquencies on commercial mortgage-backed securities

(CMBS), which are loans on malls, skyscrapers, apartments, offices and other property types

packaged into bond deals, stood at 2.57% in March, far lower than their 10.06% peak in July

2012 in the wake of the global financial crisis, according to Moody’s Investors Service’s latest

tally.

But those figures also don’t fully capture the economic disruptions caused by the coronavirus

pandemic, Moody’s analysts warned, adding that property-level “cash-flow stress, particularly

across hotels and retail properties,” will trigger more defaults. Much, naturally, will hinge on

how many borrowers struggle to stay current on their debts in the coming months, if property

loan defaults spike and whether financing conditions start to thaw after freezing up last month.

Even recent positive developments, including talk of daily life eventually resuming, come with

the caveat that the pandemic will leave scars. There are relief efforts for commercial property

owners, which could benefit from some of the Federal Reserve’s up-to-$2.3 trillion in emergency

facilities to keep credit flowing in financial markets. In April 2020, the Fed expanded its reach

to include older commercial mortgage-backed securities, which provided a boost to secondary

trading after liquidity dried up in March. But unlike the Fed’s broad backstop of corporate debt,

new CMBS issuance remains outside of its reach, casting a shadow over the more-than-$60

billion of debt that borrowers will need to refinance through 2022, per Cantor Fitzgerald

estimates.

In conclusion, it is probable property values will decrease in the short term while the economy

re-opens. To date, current data available is not showing any clear downward pressure with

limited inventory in the subject’s property type; however, market fundamentals (increased

unemployment, business closures, loan defaults), will eventually take hold and negatively impact

property values.

Britton-Adamo Group/ROI Appraisal

File Number 20-089

T A B L E O F C O N T E N T S

EXECUTIVE SUMMARY .......................................................................................................... 1

SUBJECT PHOTOGRAPHS ...................................................................................................... 4

INTRODUCTION......................................................................................................................... 8

N E I G H B O R H O O D D E S C R I P T I O N ........................................................................ 14

INDUSTRIAL MARKET OVERVIEW ................................................................................... 29

PROPERTY TAXES AND ASSESSOR’S VALUES .............................................................. 39

SITE DESCRIPTION ................................................................................................................. 42

DESCRIPTION OF IMPROVEMENTS .................................................................................. 45

HIGHEST AND BEST USE ANALYSIS ................................................................................. 48

METHOD OF VALUATION .................................................................................................... 56

SALES COMPARISON APPROACH ..................................................................................... 57

INCOME CAPITALIZATION APPROACH .......................................................................... 74

RECONCILIATION .................................................................................................................. 88

INSURABLE VALUE ................................................................................................................ 91

VALUATION OF EQUIPMENT .............................................................................................. 92

VALUATION ANALYSIS ....................................................................................................... 100

ASSUMPTIONS AND LIMITING CONDITIONS .............................................................. 102

CERTIFICATION .................................................................................................................... 107

ADDENDA

Engagement Letter

Subject Property Information

CoStar Analytics

Definitions

Qualifications of the Appraiser

Britton-Adamo Group/ROI Appraisal

File Number 20-086 1

E X E C U T I V E S U M M A R Y

Real Estate

Property Identification: A single-tenant, free standing industrial building located at 1961

Whitney Mesa Drive, Henderson, Nevada 89014

Assessor Parcel Number: 161-32-712-013

Site Size: 0.16 acres; 7,000 square feet

Building Area: Office – 480 sf

Warehouse – 1,920 sf

Total - 2,400 sf

Office Build-Out: 20%

Number of Units: 1

Occupancy 100% Owner-Occupied

Year Built: 2006

Remaining Economic Life: 35 years

Census Tract: 5101

Zoning: IL, Limited Industry District (Henderson)

Land Use Designation: Commercial (Henderson)

Flood Zone: Zone X; FEMA Flood Insurance Rate Map 32003C 2580F

Highest & Best Use “As Vacant Land”: Hold for industrial development

Highest & Best Use “As Is”: Continued use as industrial building

Probable Buyer: Owner-user

Real Estate Market Value “As Is”: $430,000

Extraordinary Assumptions: None

Hypothetical Condition: None

Insurable Value $195,000

Britton-Adamo Group/ROI Appraisal

File Number 20-086 2

Equipment

General Description: The subject is currently being operated as a crematorium and

includes specific built-in equipment for the business operation.

The primary components of the equipment include:

• Human cremator retort

• Cremains processing station

• 2 walk-in coolers

• Hydraulic lift table

• Mortuary freezer

Assumption/Condition: To determine actual mechanical condition is outside of our

expertise and the scope of this assignment. The equipment

appeared to be in functional and good condition. If it is the

client’s desire to verify the physical condition and/or needed

repairs of the subject equipment, the client should consult a

qualified mechanic/technician.

The equipment values is for business personal property only

and exclude consideration of real estate or goodwill, and it is

assumed there are no hidden defects which are not discernible

from a visual inspection and which could affect value. The

owner is further assumed to have fee simple ownership of the

various appraised items, which are appraised assuming a clear

and marketable title.

Title of Appraised Property: All appraised items are presumably owned by County Funeral

Services, LLC; owner of the aforementioned real property

Highest & Best Use “As Is”: Continued use as crematory

Fair Market Value: $100,000

Sale History of Appraised Items: Other than the acquisition by the current owner, we are

unaware of any prior sales of the appraised items. To our

knowledge, none of the items are currently listed for sale.

Class of Property: Crematory equipment

Use on Effective Date: Crematory equipment

Use on Report Date: Crematory equipment

Measurable Marketplace: Similar businesses that provide comparable products and

services throughout Nevada

Exposure/Marketing Time: 0-6 months

Britton-Adamo Group/ROI Appraisal

File Number 20-086 3

General

Dates of Value: September 25, 2020

Interest Appraised: Fee simple

Date of Report: September 29, 2020

Client Clark County Credit Union

Intended User Clark County Credit Union, the Small Business Administration

and Nevada State Development Corporation

Intended Use: The intended use of this appraisal is for loan underwriting

and/or credit decisions.

Exposure/Marketing Period: 12 months

Britton-Adamo Group/ROI Appraisal

File Number 20-086 4

S U B J E C T P H O T O G R A P H S

Aerial Photograph

SUBJECT

SUBJECT

Britton-Adamo Group/ROI Appraisal

File Number 20-086 5

View to the southwest facing the subject property

South

Yard entrance

Primary access to office

Office

Britton-Adamo Group/ROI Appraisal

File Number 20-086 6

Restroom

Mezzanine

Warehouse

Yard

Britton-Adamo Group/ROI Appraisal

File Number 20-086 7

Equipment

Human cremator retort

2 walk-in coolers

4-person mortuary freezer

Cremains processing station

Hydraulic lift

Britton-Adamo Group/ROI Appraisal

File Number 20-086 8

I N T R O D U C T I O N

Subject Identification

The subject property consists of a single-tenant, industrial building, located at 1961 Whitney

Mesa Drive, Henderson, Nevada 89014. The subject improvements consist of 2,400 square feet

of total building area, containing approximately 480 square feet of one-story office space and

1,920 square feet of warehouse space, indicating an office space ratio of roughly 20%. The

subject is situated on a 0.16-acre site located within the interior of the Green Valley Industrial

Park, along the south side of Whitney Mesa Drive, east of Mountain Vista Street, in the southeast

portion of the Las Vegas Valley, in the City of Henderson, Clark County, Nevada. The subject

was constructed in 2006 and is in an overall good condition for its age.

The subject is currently being operated as a crematorium and includes specific built-in

equipment for the business operation. The equipment is separately identified and valued within

the appraisal. The remaining discussion and analysis of the equipment is provided following the

conclusion of the real property.

The subject property is also identified as Clark County assessor’s parcel number 161-32-712-

013.

Property Ownership and History

The subject is currently under the ownership of County Funeral Services, LLC. The subject

recently transferred to the current owner in July of 2020 via bankruptcy sale at a recorded price

of $215,000 (Document #: 20200717:02663). The current owner operates within the mortuary

industry and was familiar with the distressed nature of the sale. The difference between the

current market value and the recent sale price is primarily attributed to the conditions of sale.

There have been no other transfers involving the subject property in the prior three-year period.

Legal Description

A legal description is provided within the title report as follows:

Britton-Adamo Group/ROI Appraisal

File Number 20-086 9

The subject property is also described by its Clark County assessor’s parcel number 161-32-712-

013 or by its common street address of 1961 Whitney Mesa Drive, Henderson, Nevada 89014.

The property is further described by the maps and exhibits contained within this report.

Census Tract

The subject property is located in Census Tract 5101.

Purpose of the Appraisal

The purpose of this appraisal is to estimate the market values of the subject property based upon the

following valuation scenarios:

• Market Value of the Real Estate – “As Is” – fee simple interest

• Fair Market Value in Continued Use of the Equipment – “As Is” – fee simple interest

Property Rights Appraised

The interest that is the subject of this valuation is the fee simple estate, defined below.

Fee Simple Estate

“Absolute ownership unencumbered by any other interest or estate, subject only to the

limitations imposed by the governmental powers of taxation, eminent domain, police

power, and escheat.”

Source: Appraisal Institute, The Dictionary of Real Estate Appraisal, 6th ed. (Chicago: Appraisal Institute, 2015)

Client of the Appraisal

The client of this appraisal is Clark County Credit Union.

Intended User of the Appraisal

The intended user of this appraisal is Clark County Credit Union, the Small Business

Administration and Nevada State Development Corporation.

Intended Use

The intended use of this appraisal is for loan underwriting and/or credit decisions. The

conclusions and opinions in this appraisal are not to be relied upon for purposes other than the

above stated intended use. The appraisers and the appraisal firm assume no responsibility for

results from the reliance on all or part of the appraisal for any other use other than the specified

intended use.

Effective Date of Valuation/Inspection Date

The effective date of the “as is” market value, as well as the inspection date of the property is

September 25, 2020.

Date of Report

The date of this report is September 29, 2020.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 10

Market Value Defined

Market Value means the most probable price which a property should bring in a competitive and

open market under all conditions requisite to a fair sale, the buyer and seller each acting

prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit

in this definition is the consummation of a sale as of a specified date and the passing of title from

seller to buyer under conditions whereby:

(1) Buyer and seller are typically motivated;

(2) Both parties are well informed or well advised, and acting in what they consider

their own best interests;

(3) A reasonable time is allowed for exposure in the open market;

(4) Payment is made in terms of cash in U.S. dollars or in terms of financial

arrangements comparable thereto; and

(5) The price represents the normal consideration for the property sold unaffected by

special or creative financing or sales concessions granted by anyone associated

with the sale. (Source: Office of the Comptroller of the Currency under 12 CFR, Part 34, Subpart C- Appraisals, 34.42 Definitions [f].)

Competency Provision

The signers of this report have the knowledge and experience to complete this appraisal

assignment in a competent manner. They have performed a number of appraisal assignments

recently for this property classification in the market area. Included in the Addenda are the

appraisers’ qualifications and the reader is referred to this section for additional information.

Appraisal Development and Reporting Process

This appraisal has been presented as an Appraisal Report as defined by the Uniform Standards of

Professional Appraisal Practice (USPAP), promulgated by the Appraisal Standards Board of

The Appraisal Foundation, and Clark County Credit Union appraisal requirements. The

reporting guidelines for an Appraisal Report are set forth under Standards Rule 2-2(a) of

USPAP and relate to the content and level of information provided in the report. This reporting

format requires all the necessary research and analysis to be performed however, some of the

information presented can be in an abbreviated format.

This appraisal is also intended to comply with the appraisal standards required by 12 CFR Part

34, dated June 7, 1994 of FIRREA (Federal Financial Institutions Reform, Recovery and

Enforcement Act), and to comply with the 2020-2021 Edition of USPAP, as published by the

Appraisal Foundation, and the appraisal standards of the client.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 11

Scope of the Appraisal

The scope of the appraisal required investigating sufficient data relative to the subject property to

derive an opinion of value. The depth of the analysis was intended to be appropriate in relation

to the significance of the appraisal problem. In preparing this appraisal, the appraisers solely

inspected the exterior of the subject and researched specific subject property information deemed

relevant to this appraisal. This included information relating to ownership, zoning and planning,

flood hazard potential, tax assessment information, as well as other property information that may

affect the highest and best use of the subject. The appraisers also examined the subject's market

area for information on comparable sales, pending sales and listings of similar properties, as well

as general real estate and economic statistics and trends that are applicable to the subject’s

valuation. The market area was also examined to determine the demand and marketability of

properties with the subject's classification.

• Information provided for this appraisal included a brief description of the subject, bankruptcy

purchase agreement, summary of equipment and an engagement letter.

The opinions of the appraisers, and the analyses used to arrive at a conclusion(s) of value, is

based upon the market data available, together with the appraisers’ sole education, experience

and knowledge concerning the type of property being appraised. The appraisers are not

responsible for any items of fact in public records databases, subscription (fee) information

providers, or any other sources deemed reliable, that are incorrect.

Limitations of Scope

None

Environmental Hazards & Conditions

An environmental assessment report for the subject was not provided for review and

environmental issues are beyond my scope of expertise. During the course of this assignment,

there were no obvious signs of adverse environmental conditions or hazardous materials on or

near the property. Therefore, it is assumed that the subject is not adversely affected by

environmental hazards or conditions.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 12

AREA MAP

SUBJECT

Britton-Adamo Group/ROI Appraisal

File Number 20-086 13

NEIGHBORHOOD MAP

Britton-Adamo Group/ROI Appraisal

File Number 20-086 14

N E I G H B O R H O O D D E S C R I P T I O N

The Dictionary of Real Estate Appraisal, (Sixth Edition, 2015, page 156) defines a neighborhood

as “a group of complementary land uses; a congruous grouping of inhabitants, buildings, or

business enterprises.” Neighborhoods are defined by both physical and social boundaries to

delineate areas in which social, economic, governmental and environmental influences work in a

complementary fashion to affect the use and value of real estate. A neighborhood may be an

urban or suburban development, which may include residential, commercial, industrial or other

land uses that are generally characterized as being homogeneous in some respects, and includes a

unified area with some definite boundaries. Neighborhood boundaries may consist of well-

defined natural or man-made barriers or they may be defined by a distinct change in land use or

in the character of the inhabitants.

The purpose of a neighborhood analysis is to provide a bridge between the study of general

influences on all property values and the more detailed influencing characteristics of a localized

neighborhood. Neighborhood analysis is important in that it is concerned with the relationship

of the immediate surrounding urban environment to a particular parcel in its current or proposed

use. This evaluation is a necessary link of the property under study to the general market supply

and demand situation.

Location

The subject neighborhood is located approximately 10 miles south and southeast of downtown

Las Vegas, and is generally delineated by the following boundaries:

North: Russell Road

East: Lake Mead National Recreation Area

South: Black Mountain Range

West: Interstate 15

The majority of the neighborhood is within the City of Henderson boundaries, but also includes

unincorporated portions of Clark County and a section of Paradise Valley Township. Henderson

comprises the majority of the southeast Las Vegas Valley and includes the majority of the

population in the area. Most of the developments that have an impact on the area are within the

city limits of Henderson, including large well-established master-planned communities.

Statistical data for the city of Henderson is primarily presented as it provides the best indications

of the trends seen in the neighborhood.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 15

HENDERSON MAP

Demographics

The following map and table delineates the neighborhood zip codes.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 16

Information on population, housing and income for the City of Henderson are presented in the

following tables:

CITY OF HENDERSON POPULATION BY ZIP CODE

The population in the City of Henderson has had significant growth in recent years with a total

increase of nearly 55% from 2000 to 2015, indicating an annual growth rate of near 3%.

Between 2000 and 2006, Henderson was the fastest growing city in the country in terms of

percentage growth in the United States. The population has grown to over 300,000. The current

population projections indicate growth to nearly 364,000 over the next 5 years with an average

growth rate of nearly 2% per year over the next 10 years.

CITY OF HENDERSON - Housing Estimates by Zip Code

Britton-Adamo Group/ROI Appraisal

File Number 20-086 17

Business/Employment

The City is actively trying to attract new businesses to Henderson and there has been steady

growth in the number of businesses and employment. There are many incentives that attract new

business, as is shown in the list below.

A summary of the Henderson Employment figures are below:

Henderson has a higher median household income than Las Vegas, North Las Vegas and

unincorporated Clark County, and is approximately 23% above the income in all of Clark

County, Nevada.

The business climate is strong due to the many programs to lower various costs of doing

business. The following table provides Henderson’s largest private employers, ranked by the

number of employees.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 18

Henderson Largest Private Employers

Source: City of Henderson – http://hendersondata.com/industrial-structure

The following tables provide information on employment and wages by industry for Clark

County, Nevada.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 19

Source: City of Henderson – http://hendersondata.com/labor-force

Land Use/Development

The city is comprised of a variety of land uses, from low density residential to industrial and

commercial. Land within Henderson and in other local jurisdictions, by land usage is shown in

the following tables.

Land Area (Acres)

Source: http://hendersondata.com/jurisdictional-comparison

% of Land Area

Source: http://hendersondata.com/jurisdictional-comparison

Britton-Adamo Group/ROI Appraisal

File Number 20-086 20

The total land value of each property type for Henderson and other local jurisdictions, is

summarized in the table below.

Total Value By Land Use (2018)

Source: http://hendersondata.com/jurisdictional-comparison

The assessed value per acre for each of the various land uses in Henderson and other local

jurisdictions is summarized in the following table.

Value per Acre (2018)

Source: http://hendersondata.com/jurisdictional-comparison

Single family residential land in Henderson has an assessed value of approximately $676,000 per

acre, higher than Las Vegas, North Las Vegas and unincorporated Clark County, and nearly 25%

above the value per acre for all of Clark County.

Since the turn of the century, Henderson has experienced a tremendous amount of commercial

and residential development. Significant commercial development has occurred to support the

population base including the relocation of numerous businesses to the area. Retail and office

development are primarily located along the major roadways and much of the new construction

has been in the southwest portion of the city along St. Rose Parkway and Eastern Avenue. New

commercial projects not only provide an amenity to the area residents, but also add to the

employment base. Large developments include the Galleria Regional Mall, Green Valley Ranch

District, Sunset Station Hotel/Casino and the Green Valley Auto Center, all of which have been

well received and added to the employment opportunities in Henderson. The Galleria Mall is a

major regional mall with Robinson’s-May, Dillard’s and JC Penney as anchor tenants. The

District is an open-air village retail center adjacent to the Green Valley Ranch Resort with

upscale stores and restaurants at ground level and condominium units above.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 21

Industrial development has primarily been along the U.S. 95 corridor, generally between Sunset

Road on the north and Lake Mead Drive on the south. Industrial parks such as Black Mountain

Business Park, Gibson Business Park, Green Valley Business Park and Whitney Mesa have

attracted new businesses, many relocating to the Las Vegas area. Over the previous year, there

has been an influx of new industrial development in the West Henderson area of the submarket,

with large distribution centers and warehousing.

With an increasing population base, supporting commercial facilities have increased in demand.

Office buildings had been generally well received by the market, as have most retail centers.

These facilities are generally located along the major thoroughfares, with secondary locations

being built-out with residential product. An indirect influence of the subject neighborhood is the

City of Henderson downtown core. This older section of Henderson is undergoing revitalization

supported by the Redevelopment Agency and is evidenced by several new retail, residential, and

office projects.

The following summarizes the commercial market segments in Henderson as of the 4th Quarter

of 2019.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 22

Taxable Retail Sales

The following table reflects the year over year retail sales trends and categories.

.

Master Planned Communities

The development of master planned communities in Henderson has accounted for much of the

population growth in the city over the past 20 years. The larger communities include a variety of

single family and multi-family residential products, supporting commercial uses and significant

parks and public recreation and cultural facilities. As of 2017, these communities are in various

stages of development, with most of the anticipated growth in the coming years expected to

occur in the Inspirada and Cadence development, which combined are planned to add over

25,000 units to the city. The major master planned communities in Henderson are presented on

the following page.

HENDERSON MASTER PLANNED COMMUNITIES

Britton-Adamo Group/ROI Appraisal

File Number 20-086 23

Lake Las Vegas is a large master-planned residential and resort community surrounding a 320

acre lake with more than ten miles of shoreline established in 1984. This community (roughly

half of which is gated) has the additional following amenities: waterfalls, wildlife, high-end

resorts and hotels, a yacht and beach club, a fitness center, three golf courses dispersed

throughout the community, smaller ponds also dispersed throughout the community and

incredible views. There are 19 distinct neighborhoods including custom home sites, courtyard

villas, waterfront & golf villas, resort condominiums, luxury executive homes and courtyard

town homes. Hyatt opened a hotel/casino at Lake Las Vegas in 1999, and the 350-room Ritz-

Carlton hotel/casino was completed in 2003. The community has had ongoing financial

problems and changes in ownership beginning about 2007 when the past developers pushed the

project into bankruptcy. The project emerged from bankruptcy in 2010 under the control of

Credit Suisse and Highland Capital. There have been some positive signs of improvement, with

rising home prices, hotel occupancy improving and sales of vacant sites to developers and

homebuilders. The Falls golf course and the Reflection Bay Golf Club both closed in 2009

however, reopened in 2014. The Casino MonteLago was completed in 2003 and has closed

multiple times, most recently in 2013 and has yet to reopen.

MacDonald Highlands is within the MacDonald Ranch development, a 3,200-acre development

with 4 villages including Del Webb's Sun City MacDonald Ranch, in the city of Henderson,

Nevada. MacDonald Highlands, formerly known as The Foothills at MacDonald Ranch, is a

private gated golf course community in the foothills of the McCullough Mountains south of

Horizon Ridge Parkway, and is planned for 500+ homes on semi-custom and custom home lots.

It features an 18-hole golf course designed by Jay Morrish and David Druzisky, completed in

2001. This 18-hole private course has an open guest policy and is surrounded by custom homes

and custom home lots ranging from about one-third of an acre to over 2 acres.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 24

Features of this community include a 27,000-square-foot clubhouse, planned to be completed in

2003, which will offer a golf shop, exercise facility, swimming pool, tennis courts and dining, as

well as various community parks and hiking trails. Additional community amenities will include

three parks encompassing 10 acres, featuring tennis, basketball and volleyball courts; play areas;

and picnic facilities. Five miles of fitness trails are also planned in the foothills of Black

Mountain.

Seven Hills is located a mile south of Lake Mead Drive at Eastern Avenue. This 1,300 acre

master-planned community has been developed in two villages, with one oriented to an 18-hole

golf course. The community, upon final build-out, will have 3,600 units, with 735 units in the

golf-oriented portion. The residential projects include rental apartments, detached units, and

custom home sites. Amenities include a golf course, 26 neighborhoods, parks, and discovery

trails. The focal point of this community is Rio Secco, a 72-par championship golf course. One-

third of the total area has been allocated to open area, which includes golf, trails and common

areas.

Anthem is an approximate 5,000 acre community located in southern Henderson, southeast of

Seven Hills and features Sun City Anthem (age-restricted 55 and up), and Solera, a moderately-

priced community within Sun City Anthem, Anthem Country Club (a gated golf course

community), as well as Anthem Highlands, a traditional "family" community with a variety of

single-family homes covering a spectrum of product and prices.

Serving the Sun City residents is the 77,000 square foot Anthem Center clubhouse located at the

high point of the area with commanding views of the Las Vegas Valley. This facility provides a

high-quality environment for a large variety of activities and amenities. Included within the

Anthem Center are: restaurant, a fitness/exercise/wellness center, indoor walking track, indoor

and outdoor pools and spas (handicap accessible), tennis center, ballroom/meeting rooms, studios

for various crafts and activities, bocce ball, billiards, and a library, among others. In 2005,

Independence Center, housing the 300-seat Freedom Hall Theater and SCA-TV studios was

completed at the corner of Anthem Parkway and Hampton Road. Sun City also features The

Revere Gold Club, which offers 2 professional 18-hole golf courses; the Lexington and the

Concord.

The Anthem Country Club community features a gated entry, a Hale Irwin/Keith Foster-

designed golf course and a 33,000 square foot clubhouse housing a dining room, the Club Grille

& Sports Bar and a pro shop, among other features. Anthem Country Club also has a 13,700

square foot athletic club with tennis courts, a six-lane lap pool, resort and wading pools, spa,

volleyball and a poolside cafe. This is an exclusive guard gated private golf neighborhood of

upper end production homes and custom home lots.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 25

Anthem Highlands and Madeira Canyon are more recent developments at the southern end of

Anthem. These communities offer a variety of single family homes, including the Club at

Madeira, a guard gated community with over 500 homes of 2,500 to 4,800 square feet and prices

averaging over $500,000. Amenities include a clubhouse, swimming pool, tennis courts and

recreational facilities.

Inspirada is a 1,950-acre master planned community located south of the Henderson Executive

Airport and west of Sun City Anthem and Anthem Highlands planned for approximately 15,500

residential units. This development was envisioned as a New Urbanist community which was

designed to capture an “old town” feeling where residents can walk to work, schools, churches

and parks. The development is planned for residential, commercial, mixed-use, and casino

components, and there has been many new residential communities under construction, as well

as roadways and recreation centers with community centers, pools and sports fields.

Residential Market

Recent single family residential market statistics for Henderson and the Las Vegas area are

presented below.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 26

Accessibility

Accessibility is considered good to most portions of the neighborhood. The US 95 Freeway,

Lake Mead Drive, Boulder Highway, and the I-215/Las Vegas Beltway are the major traffic

thoroughfares for this area and provide good accessibility in and around the market area. The

Las Vegas Beltway “flyover” interchange with US 95 at Lake Mead Parkway provides

uninterrupted traffic flow between the two freeways. The extension of the I-215/Las Vegas

Beltway along Lake Mead Parkway and the interchange with US 95 greatly improves access

throughout Henderson and has helped increase the development in the neighborhood. In

addition, the interchange at St. Rose Parkway and Interstate 15, which opened in 2008, and the

widening of St. Rose Parkway to eight lanes of traffic should satisfy the anticipated growth of

the area over the foreseeable future.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 27

Public Services

With the expansion of the residential base, schools, fire stations, and similar services have been

completed and/or are proposed in the neighborhood. Henderson has been approved for several

new schools, which will likely be located in the southern portion of the neighborhood where the

majority of the residential development is occurring.

Public utilities, police protection and other public services are available to meet the needs of the

neighborhood. As the residential base expands, additional services will be made available.

Conclusion

The City of Henderson has seen substantial growth in the past two decades and continues to

grow, albeit not at the rate seen in the 1990s and early 2000s. During that time Henderson was

the fastest growing city over 100,000 residents in the United States from 1990 to 1996.

Development has been primarily centered in the more than 25 master planned communities

which are predominantly residential with some associated commercial and service uses.

Residential uses include all types of product from entry level condominiums to high-end custom

homes. Commercial development and community services and roadways have been expanded

throughout the area and have for the most part, kept up with the expanding population and

employment base. The future outlook is considered positive with new development occurring

throughout the city, although primarily in the west and east portions where there is still available

vacant land.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 28

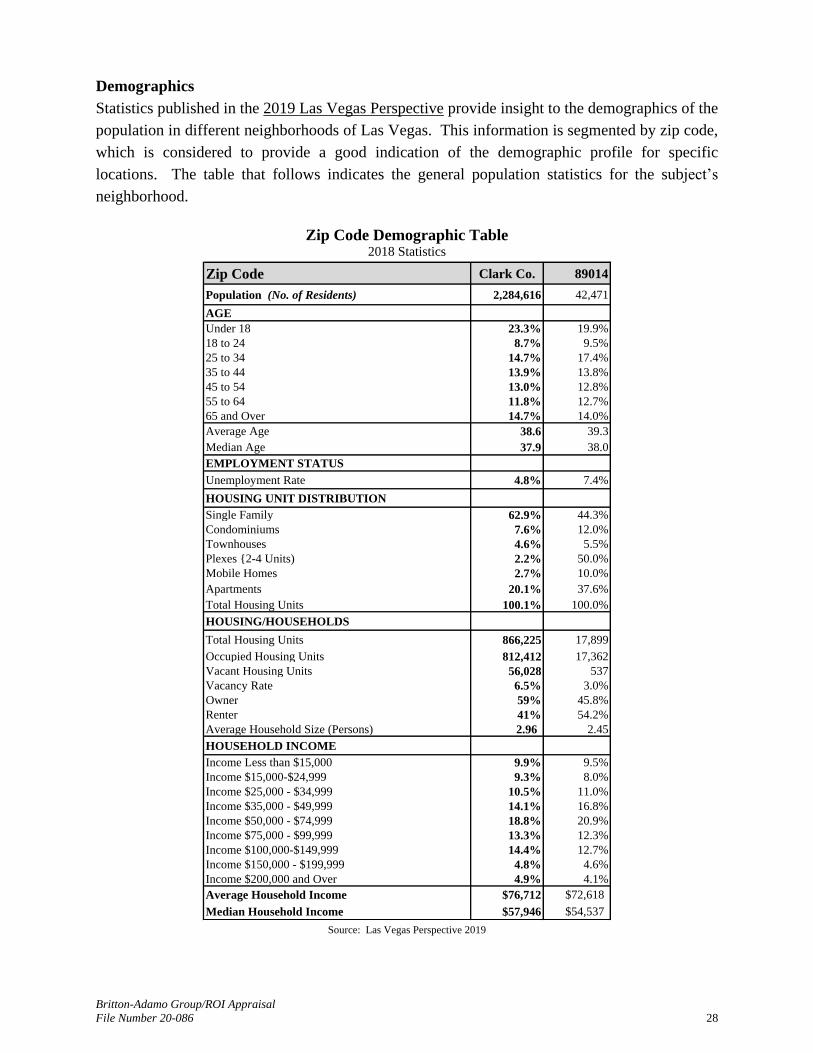

Demographics

Statistics published in the 2019 Las Vegas Perspective provide insight to the demographics of the

population in different neighborhoods of Las Vegas. This information is segmented by zip code,

which is considered to provide a good indication of the demographic profile for specific

locations. The table that follows indicates the general population statistics for the subject’s

neighborhood.

Zip Code Demographic Table

2018 Statistics

Zip Code Clark Co. 89014

Population (No. of Residents) 2,284,616 42,471

AGE

Under 18 23.3% 19.9%

18 to 24 8.7% 9.5%

25 to 34 14.7% 17.4%

35 to 44 13.9% 13.8%

45 to 54 13.0% 12.8%

55 to 64 11.8% 12.7%

65 and Over 14.7% 14.0%

Average Age 38.6 39.3

Median Age 37.9 38.0

EMPLOYMENT STATUS

Unemployment Rate 4.8% 7.4%

HOUSING UNIT DISTRIBUTION

Single Family 62.9% 44.3%

Condominiums 7.6% 12.0%

Townhouses 4.6% 5.5%

Plexes {2-4 Units) 2.2% 50.0%

Mobile Homes 2.7% 10.0%

Apartments 20.1% 37.6%

Total Housing Units 100.1% 100.0%

HOUSING/HOUSEHOLDS

Total Housing Units 866,225 17,899

Occupied Housing Units 812,412 17,362

Vacant Housing Units 56,028 537

Vacancy Rate 6.5% 3.0%

Owner 59% 45.8%

Renter 41% 54.2%

Average Household Size (Persons) 2.96 2.45

HOUSEHOLD INCOME

Income Less than $15,000 9.9% 9.5%

Income $15,000-$24,999 9.3% 8.0%

Income $25,000 - $34,999 10.5% 11.0%

Income $35,000 - $49,999 14.1% 16.8%

Income $50,000 - $74,999 18.8% 20.9%

Income $75,000 - $99,999 13.3% 12.3%

Income $100,000-$149,999 14.4% 12.7%

Income $150,000 - $199,999 4.8% 4.6%

Income $200,000 and Over 4.9% 4.1%

Average Household Income $76,712 $72,618

Median Household Income $57,946 $54,537 Source: Las Vegas Perspective 2019

Britton-Adamo Group/ROI Appraisal

File Number 20-086 29

I N D U S T R I A L M A R K E T O V E R V I E W

The market overview addresses historic and current trends in the industrial real estate segment

within the Las Vegas metropolitan area. Various sources of market statistics were utilized in this

analysis, including Applied Analysis, Voit Real Estate Services, Colliers International, Restrepo

Consulting Group and Grubb & Ellis. The industrial market statistics presented in the tables

includes speculative and non-speculative incubator, flex, midbay, distribution, freestanding and

other.

The six types of industrial buildings categorized in the Voit Industrial Market Report - Quarterly

Market Survey, are briefly described as follows:

Incubator: 500 - 1,500 sf divisibility, minimal office, one roll-up door

Flex: 1,500 - 3,000 sf divisibility, 40% or more office build-out, one roll-up door, high visibility

Midbay: 5,000 - 15,000 sf divisibility, 10%-15% office build-out, dock high and grade level loading

Distribution: over 15,000 sf divisibility, 3%-5% office build-out, multiple docks and grade level loading

Free standing: single or dual user(s)

Other: tenant improvements to a non-conventional build-out

The Las Vegas market is segmented into submarkets which have the same general location

characteristics, including access, proximity to employment centers, municipal boundaries and

surrounding land uses. The segmentation of the building type and submarket provides the

opportunity to analyze specific segments of the industrial market.

Las Vegas Industrial Market Trends

The following table provides a summary of the primary statistics for the Las Vegas industrial

market in recent years.

Source: Colliers International

The Las Vegas industrial market has consistently gown over the previous 10 years. Lease rates

have also significantly increased over the previous 5 years.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 30

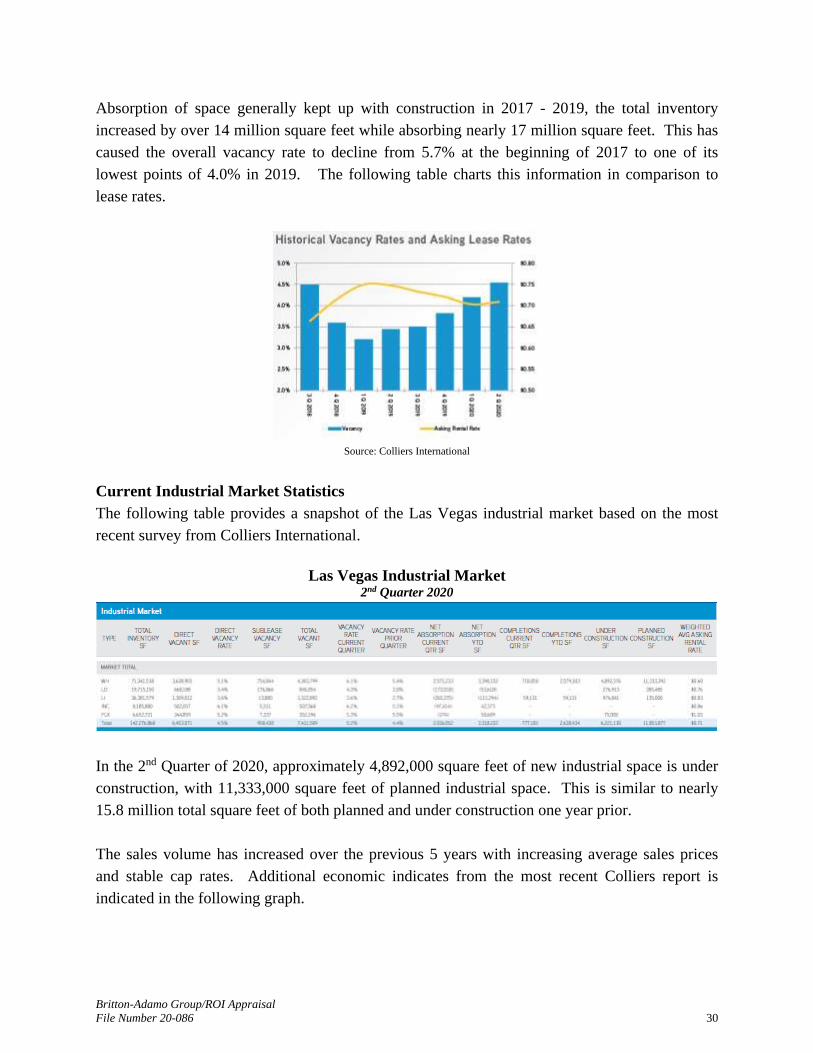

Absorption of space generally kept up with construction in 2017 - 2019, the total inventory

increased by over 14 million square feet while absorbing nearly 17 million square feet. This has

caused the overall vacancy rate to decline from 5.7% at the beginning of 2017 to one of its

lowest points of 4.0% in 2019. The following table charts this information in comparison to

lease rates.

Source: Colliers International

Current Industrial Market Statistics

The following table provides a snapshot of the Las Vegas industrial market based on the most

recent survey from Colliers International.

Las Vegas Industrial Market 2nd Quarter 2020

In the 2nd Quarter of 2020, approximately 4,892,000 square feet of new industrial space is under

construction, with 11,333,000 square feet of planned industrial space. This is similar to nearly

15.8 million total square feet of both planned and under construction one year prior.

The sales volume has increased over the previous 5 years with increasing average sales prices

and stable cap rates. Additional economic indicates from the most recent Colliers report is

indicated in the following graph.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 31

Britton-Adamo Group/ROI Appraisal

File Number 20-086 32

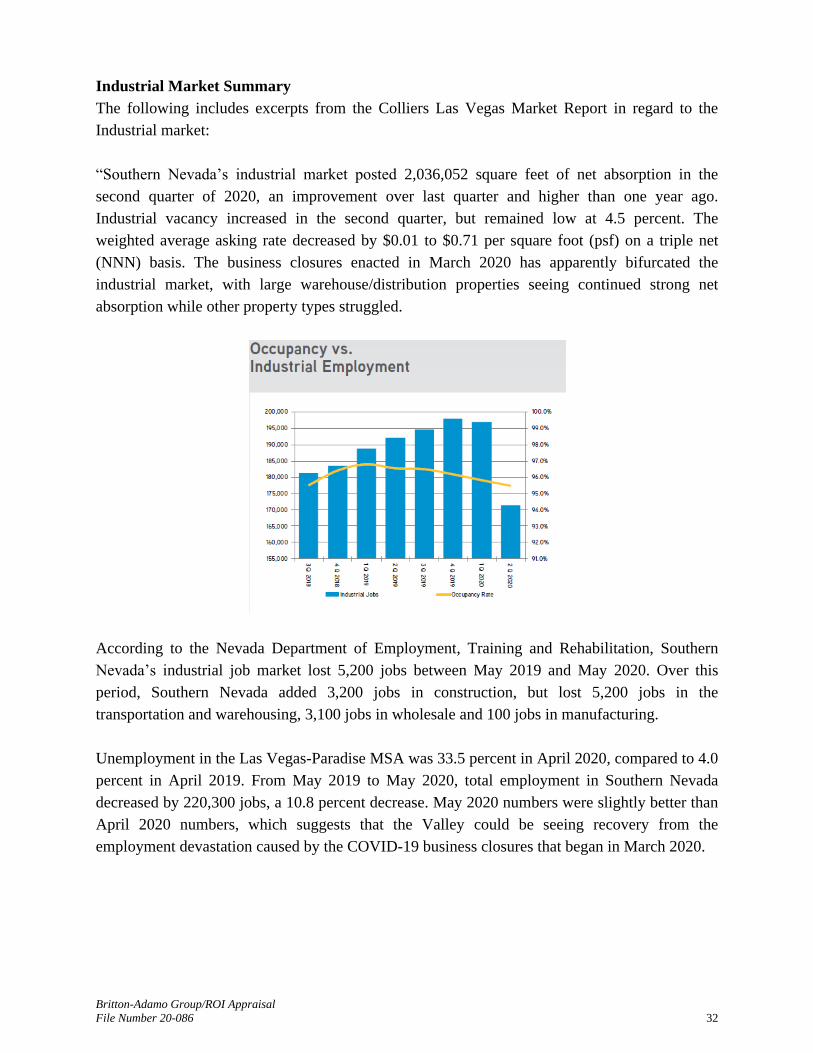

Industrial Market Summary

The following includes excerpts from the Colliers Las Vegas Market Report in regard to the

Industrial market:

“Southern Nevada’s industrial market posted 2,036,052 square feet of net absorption in the

second quarter of 2020, an improvement over last quarter and higher than one year ago.

Industrial vacancy increased in the second quarter, but remained low at 4.5 percent. The

weighted average asking rate decreased by $0.01 to $0.71 per square foot (psf) on a triple net

(NNN) basis. The business closures enacted in March 2020 has apparently bifurcated the

industrial market, with large warehouse/distribution properties seeing continued strong net

absorption while other property types struggled.

According to the Nevada Department of Employment, Training and Rehabilitation, Southern

Nevada’s industrial job market lost 5,200 jobs between May 2019 and May 2020. Over this

period, Southern Nevada added 3,200 jobs in construction, but lost 5,200 jobs in the

transportation and warehousing, 3,100 jobs in wholesale and 100 jobs in manufacturing.

Unemployment in the Las Vegas-Paradise MSA was 33.5 percent in April 2020, compared to 4.0

percent in April 2019. From May 2019 to May 2020, total employment in Southern Nevada

decreased by 220,300 jobs, a 10.8 percent decrease. May 2020 numbers were slightly better than

April 2020 numbers, which suggests that the Valley could be seeing recovery from the

employment devastation caused by the COVID-19 business closures that began in March 2020.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 33

New completions of industrial space in the second quarter of 2020 totaled 777,181 square feet.

The majority of the industrial space completed this quarter was warehouse/distribution space

located in North Las Vegas. Approximately 64 percent of this space was preleased at completion.

An additional 2.8 million square feet of industrial space is scheduled for completion in the third

quarter of 2020, with approximately 33 percent of this space preleased.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 34

Industrial net absorption was 2,036,052 square feet in the second quarter of 2020, an increase

from one year ago when net absorption was 1,831,220 square feet. The Valley’s highest net

absorption this quarter was in North Las Vegas, at 2,343,153 square feet, followed by the West

Henderson submarket at 154,291 square feet. Net absorption was negative in most other

submarkets, with Southwest experiencing the lowest net absorption, negative 186,568 square

feet. Net absorption was 2,571,233 square feet in warehouse/distribution, negative 172,018

square feet in light distribution, negative 265,375 square feet in light industrial, negative 97,414

square feet in incubator and negative 374 square feet in flex properties.

Southern Nevada’s industrial vacancy rate increased to 4.5 percent in the second quarter of 2020.

The Valley’s lowest vacancy rate was 1.7 percent in the Henderson submarket. The Valley’s

highest vacancy rate was 8.2 percent in rapidly expanding West Henderson, followed by 6.3

percent in North Las Vegas. Among product types, vacancy was lowest in light distribution

properties at 3.4 percent, followed by light industrial at 3.6 percent, 5.1 percent in

warehouse/distribution, 5.2 percent in flex and 6.1 percent in incubator properties.

The industries most active in occupying space in the second quarter of 2020 were involved in

manufacturing (36.3 percent), wholesale (22.4 percent) and transportation and warehousing (12.6

percent). Local companies took 31.5 percent of the leased square footage we tracked in the

second quarter of 2020. Companies headquartered in the Midwest took 29.7 percent of the space

occupied, followed by the Northeast U.S. at 20.3 percent and Southwest U.S. 15 percent.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 35

The weighted average asking rate for industrial product in Southern Nevada decreased in the

second quarter of 2020. The weighted average asking rate was $0.71 psf, a $0.01 increase from

one quarter ago, and a $0.04 decrease from one year ago. Asking rates increased by $0.03 psf in

flex properties, $0.02 psf in light industrial properties and remained flat in

warehouse/distribution properties. Asking rates decreased by $0.09 psf in incubator and $0.05

psf in light distribution properties.

Industrial investment sales in the second quarter of 2020 showed an improvement over 2019, and

were on par to match the recent high point in investment sales in 2018. Sales volume was $447.1

million in 39 sales totaling 3,343,000 square feet at an average sales price of $130.19 psf. The

average cap rate increased to 7.7 percent from last year’s 6.3 percent, and the average size of a

sold property increased to 88,000 square feet.

The second quarter of 2020 managed to produce over 2 million square feet of industrial net

absorption despite the business closures that began in March 2020. The business closures took a

serious toll on the local economy, with Southern Nevada losing more than 220,000 jobs since

May 2019. The loss of jobs, and the loss of occupied industrial space, was not felt evenly in the

market. Warehouse/distribution product posted all of the Valley’s positive net absorption in the

second quarter of 2020. Other industrial product types, which rely more heavily on small

businesses, suffered negative net absorption. While it is likely that warehouse/distribution

demand will remain relatively strong through the remainder of 2020, it is unknown how quickly

Britton-Adamo Group/ROI Appraisal

File Number 20-086 36

small businesses will recover. By the end of 2020, we may see an overall positive industrial

picture that nevertheless obscures the challenges faced by many landlords of non-

warehouse/distribution properties in the Valley.

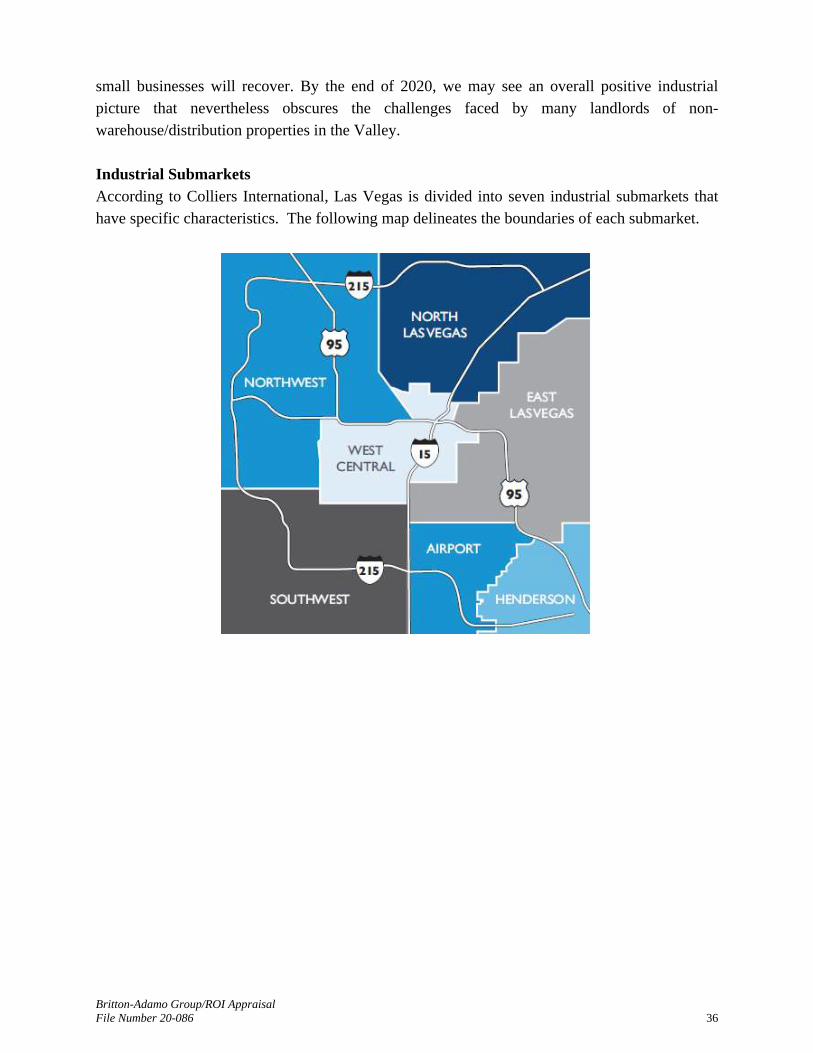

Industrial Submarkets

According to Colliers International, Las Vegas is divided into seven industrial submarkets that

have specific characteristics. The following map delineates the boundaries of each submarket.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 37

The following table delineates the characteristics of the individual submarkets throughout the

Las Vegas Valley.

Las Vegas Industrial Submarkets 2nd Quarter 2020

Britton-Adamo Group/ROI Appraisal

File Number 20-086 38

Conclusion

The Las Vegas industrial market has improved over the past 5 years, with vacancy decreasing

below 5%. We have been in complete recovery from the recessions in 2007. As indicated in the

following tables, capitalization rates in the Las Vegas market as well national rates have

continued to improvement with signs of stabilization, after a period improving rates over recent

years.

PwC Real Estate Investor Survey

The occupancy levels for this product type has been relatively consistent in recent years, a trend

that will likely extend to second-tier markets such as Las Vegas over the next few years,

assuming a short-term affect from COVID-19.

Overall based on the provided market data, the industrial market is toward the end of the period

of recovery from the previous recession with positive signs of improvements.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 39

P R O P E R T Y T A X E S A N D A S S E S S O R ’ S V A L U E S

The State of Nevada employs a millage structure for real estate taxation. Nevada Revised

Statutes require that all property be valued every five years based on a "Replacement Cost"

approach. The Assessor's Office determines the cost necessary to replace an improvement, less

depreciation. The land value is also included, based upon market sales.

During non-reevaluation years, the values are updated every year by an Index computed by the

State Department of Taxation. Current Nevada law requires that all property be factored each

year to reflect the increased cost of construction. This factor varies by location and type of

property. The assessment ratio is 35% as defined in NRS 361.225. In addition, each property

also has a "Computed Taxable" value that cannot exceed the full cash value.

The State of Nevada operates on a fiscal basis with a fiscal year which begins on July 1st and

ends on June 30th of the following calendar year. In Clark County there are a number of tax

districts. The tax rates for each of these districts are based on the amount of monies budgeted to

them for the necessary maintenance and improvements of their facilities and services. The

monies collected must pay for schools, roads, police, and fire protection, along with the other

services that a taxpayer expects from the local government. The tax rates vary depending on the

type of services provided to a particular area.

A comparison of cities of comparable size to those in the Las Vegas Valley shows that Las

Vegas and Clark County have some of the lowest property tax burdens in the western United

States. This helps attract new residents and businesses to the area.

The subject property consists of a legal parcel located in tax area 505 (Henderson), which has a

tax rate for fiscal year 2020/2021 of 2.9291%. The subject’s current assessment and estimated

tax obligation is indicated in the table below.

Clark County Assessment and Cap Reduction Information

APN Land Improvements Total Taxes as

Assessed

Less Cap

Reduction Net Taxes

161-32-712-013 $18,784 $42,860 $61,644 $1,805.61 $355.73 $1,449.88

The Nevada Legislature passed a property tax relief measure in the Spring of 2005 to curb the

impact of rapidly escalating property values. The law limits the amount that taxes can increase

from one year to the next. The tax increases are capped at 3% for owner/occupied homes and a

6.7% cap on most other properties, including the subject. The subject property’s tax liability has

been reduced in the current tax year.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 40

According to the Clark County Treasurer’s office, as of September 25, 2020, the subject does not

have delinquent taxes. The value conclusion in this appraisal assumes that the taxes have been

paid in full, and there are no outstanding taxes due.

Additional Clark County assessor’s and treasurer’s information for the subject property is located

in the Addenda to this report.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 41

ASSESSOR’S PARCEL MAP

SUBJECT

SUBJECT

Britton-Adamo Group/ROI Appraisal

File Number 20-086 42

S I T E D E S C R I P T I O N

Configuration and Size

The subject site includes a 0.16-acre parcel located within the interior of the Green Valley

Industrial Park, along the south side of Whitney Mesa Drive, east of Mountain Vista Street. The

site is near rectangular in shape with roughly 109 feet in a north/south direction and 66 feet in an

east/west direction.

Topography and Flood Hazard

The subject property is generally flat and level with the surrounding properties and adjacent

roadways. According to the FEMA Flood Insurance Rate Map (FIRM) 32003C 2580F, the

subject property is in Zone X, an area determined to be outside the 0.2% annual chance

floodplain. There were no obvious signs of any significant flood hazards that affect the subject

property and none were reported to us during the course of this assignment. It is an assumption

of this report that the subject is not affected by any atypical flood hazards or conditions which

would adversely affect the market value or development potential of the property. A copy of the

flood map is located in the Addenda to this report.

This parcel IS NOT in a 100-year flood zone.

Parcel 16132712013

Owner LEE PROPERTIES NEVADA INC

Address 1961 WHITNEY MESA

Entity Henderson

Contact 702-267-3058

Flood Zone This parcel IS NOT in a 100-year flood zone.

FIRM Panel View FIRM Panel (2580)

LOMR This parcel is not affected by a LOMR

SUBJECT

Britton-Adamo Group/ROI Appraisal

File Number 20-086 43

Soils and Subsoil

A soil report for the property was not provided to us during the course of this assignment. Based

upon a physical inspection of the property, as well as a review of various maps and site plans,

there are no obvious signs of any significant adverse soil conditions on the subject property. In

addition, no adverse soil conditions were reported to us during the course of this assignment.

Overall, there is no evidence of any adverse soil conditions that would affect the market value or

development potential of the subject property. However, we are not qualified professionals in

this field, and therefore; cannot provide a valid determination of the soil conditions. It is

assumed the soils are capable of supporting a variety of utilizations and developments.

Easements and Encroachments

A title report was not provided for our review and no adverse easements or encroachments were

noted. Based upon a physical inspection of the subject property, the subject is encumbered by

various utility easements, which are typical for industrial buildings in the area. The existing

easements are common to the neighborhood and do not adversely affect the value of the

property. The following describes the easement derived from the deed.

The easements that exist on the subject property are typical for the area and do not significantly

affect the development potential or highest and best use of the property.

Environmental Conditions

A Phase I Environmental Site Assessment was not provided to us. Based upon a physical

inspection of the subject property, there does not appear to be any significant adverse

environmental conditions that are obvious and would affect the market value of the property. In

addition, there were no reported adverse conditions on the subject site, or any adjacent sites.

However, we are not professionals in this field and are not qualified to determine environmental

hazards or conditions. Therefore, we take no responsibility to the existence of any known or

unknown environmental hazards or conditions that may exist on the subject property (see

Assumptions and Limiting Conditions #8).

Seismic Hazard

The Nevada Bureau of Mines and Geology has published a map of known faults and fissures in

the area. Fault scarps are common in the Las Vegas Valley; yet, horizontal or vertical land

movement is generally low. According to consulting geologist Dr. Burton Slemmons, in “Land

Subsidence in Las Vegas”, faults of Las Vegas Valley have low rates of activity with recurrence

intervals of about 10,000 years or more; greatly lower than the 150-300 years for the San

Andreas, Hayward, and Calaveras faults of California.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 44

Nevada has no regulations for determining earthquake hazard/risk for a specific site, although

Clark County has adopted Uniform Building Code (Zone 2B) requirements, which include

foundation-wall-roof anchoring and steel reinforcement provisions.

Utilities

All public utilities are available and at adequate capacity to accommodate a wide variety of

potential developments, including the existing building improvements. They are provided by the

following:

Electricity: NV Energy

Natural Gas: Southwest Gas Company

Water: Las Vegas Valley Water District

Sewer: Clark County Sanitation District

Telephone: CenturyLink Communications

Disposal: Republic Services

Street Improvements and Access

The subject property is located within the interior of the Green Valley Industrial Park, along the

south side of Whitney Mesa Drive, east of Mountain Vista Street. Access to the subject is

provided from reciprocal access agreements within the development. The development is

accessed by two sets of curb cuts located along Whitney Mesa Drive. Whitney Mesa Drive is a

two lane 60-foot wide roadway, which has a signalized intersection with Mountain Vista Street,

roughly one-quarter mile to the west. Mountain Vista Street is secondary neighborhood arterial,

which intersects with Russell Road roughly one mile to the north and continues throughout

residential communities also intersecting with Tropicana Avenue and Flamingo Road. Mountain

Vista Street turns into and intersects with Sunset Road roughly one-half mile to the south, which

traverses the southern portion of the Las Vegas Valley. The nearest freeway interchanges are at

US Highway 95 via Tropicana Avenue roughly 2 miles to the northwest and via Russell Road

roughly 2 miles to the east. Overall, access to the subject property is considered to be average.

Zoning

The subject property is currently zoned IL, Limited Industry District with the City of Henderson.

The IL district is established to provide areas appropriate for low-intensity industrial uses

including light manufacturing, warehousing and distribution, research and development, and

commercial services, and to protect these areas, to the extent feasible, from the disruption and

competition for space from unrelated retail uses, primary office uses, and general industrial uses.

Conversion of buildings and sites to general office use is permitted only as expressly stated in

this Development Code. Secondary accessory office uses on the site are allowed.

Additional information on this zoning designation is located in the Addenda to this report.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 45

D E S C R I P T I O N O F I M P R O V E M E N T S

The subject is an existing single-tenant industrial building built with 2,400 square feet of

building area. The building includes roughly 480 square feet of office space, which is generally

and open space, and a 2-fixture restroom. The public entrance to the building is situated at the

north side of the building structure via a single glass doorway. There is a grade level doorway

along the west side of the building providing access to the warehouse area from the enclosed

storage yard, and one additional grade level door along the north side of the building. The yard

area includes nearly 2,000 square feet.

In addition, the warehouse also includes roughly 400 square feet of open mezzanine storage

space above the office. The mezzanine is accessed via an interior stairwell in the warehouse.

Due to the quality of the space, it is not considered as part of the total building area is a

beneficial characteristic. The improvements were constructed in 2006 and are in an overall good

condition.

A complete set of building plans as well as a detailed list of the interior improvements were not

provided.

Type of Improvement Office/warehouse building

Number of Buildings One

Number of Stories One

Number of Units One

Year Built 2006

Building Size Office – 480 sf

Warehouse – 1,920 sf

Total - 2,400 sf

Percent Office 20% (480 SF/2,400 SF)

Site Coverage Ratio 34% (2,400 SF/7,000 SF)

Floor Area Ratio 34% (2,400 SF/7,000 SF)

Britton-Adamo Group/ROI Appraisal

File Number 20-086 46

Construction Components

Foundation Reinforced concrete slab

Structural System: Concrete block (CMU)

Roof: A flat built-up commercial roof.

Exterior Walls: Painted concrete

Interior Walls: The interior walls are wood-frame with painted, textured

and taped drywall in office and smooth concrete in

warehouse.

Building Height: 18’ (16’ clear height)

Floor Finish: Ceramic tile throughout the office and smooth concrete in the

warehouse

Plumbing: There is one 2-fixture restroom.

Sprinklers: Yes

Electricity: Commercial grade that is assumed to meet code.

Ceilings & Lighting: Taped and textured drywall with fluorescent light fixtures

in office. Warehouse includes open beam with skylights

and hung metal halide bay light fixtures.

Interior & Exterior Doors: The entryway to the office area consist of glass in an

aluminum frame. The majority of the interior doorways are

wood in wood frames. The warehouse is served by two

external grade level doors.

Heating & A/C: Roof mounted package HVAC unit assumed to maintain

adequate year-round temperatures in office with swap

coolers in the warehouse areas.

Glass: There are storefront glass storefront windows along the

main building façade.

Parking: The subject property has 3 front parking stalls with

additional potential parking in the yard. The parking is

considered to satisfy the current development restrictions.

Britton-Adamo Group/ROI Appraisal

File Number 20-086 47

Yard Improvements: There is minimal landscaping along the perimeter of the

development. The subject includes an enclosed storage

yard with a manual gate along the west side of the building.

Americans with Disabilities Act (ADA) Compliance

The Americans with Disabilities Act (ADA) became effective January 26, 1992. The appraisers

have not made a specific compliance survey and analysis of this property to determine whether

or not it is in conformity with the various detailed requirements of the ADA. It is possible that a

compliance survey of the property together with a detailed analysis of the requirements of the

ADA could reveal that the property is not in compliance with one or more of the requirements of

the act. If so, this fact could have a negative effect upon the value of the property. Since the

appraisers have no direct evidence relating to these issues, the appraisers did not consider

possible non-compliance with the requirements of ADA in estimating the value of the property.

Hazardous Materials

We are not aware of any potentially hazardous materials (such as formaldehyde foam insulation,

asbestos insulation, radon gas emitting materials, or other potentially hazardous materials) which

will be used in the construction of the improvements. However, we are not qualified to detect

such materials and urge the client to employ an expert in the field to determine if such hazardous

materials exist.

Construction Class/Economic Life

According to the Marshall Valuation Cost reference manual, the subject improvements are

classified as a good quality Class "C" Light Industrial/Warehouse Shell Building, with average

quality Industrial, Interior Office Space (Section 14, Page 35). The life expectancy tables in the