Appraisal of the ,ga Uay Yugoslavia Oil Pipeline - … · Appraisal of the ,ga Uay Yugoslavia Oil...

79

ReportNo. 886-YU Appraisal of the ,gaUay Yugoslavia Oil Pipeline (Yugoslavenski Naftovod Poduzece za Transport Nafte U Osnivanju) October 7, 1975 Regional Projects Department Europe, Middle East, and North Africa Regional Office Not for PublicUse Document of the World Bank Thisdocument hasa restricteddistribution and may be usedby recipients only in the performance of their official duties. Its contentsmay not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Appraisal of the ,ga Uay Yugoslavia Oil Pipeline - … · Appraisal of the ,ga Uay Yugoslavia Oil...

Report No. 886-YU

Appraisal of the ,ga UayYugoslaviaOil Pipeline(Yugoslavenski Naftovod Poduzece za Transport Nafte U Osnivanju)

October 7, 1975Regional Projects DepartmentEurope, Middle East, and North Africa Regional Office

Not for Public Use

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUrJAIJ.iTS

Currency Unit -- +aosiaviga Dinar (Din,)Din. 1 u us$oo059US$1 - Di]t, J7W)

WEIGHTS AND MASA-RES

1 inch (in) - 2,54 CentImeters1 meter (m) = 3.28 feet (ft)1 kilometer (km) = O.6214 miles (mi)1 square kilometer (km2) = 02386 s.-are mile 1 cubic meter (m3 ) = 6.28-3 baxrels

= 0.80 to 095 metric tons of crude oil1 barrell (bbl) =42 'S gallons (gal)1 kilocalorie (kcal) - 3,968 British thermal units (Btu)

0 0,001,6 kilowatt hours (kWh)1 horsepower - 07)46l kilo-watt (kW)1 Megawatt (MW) = 1,000 kilowatts (16-kkW)1 Gigawatt hour (GWh) 1 mil lion kilDwatt hours (106kWh)1 long ton (lg ton)1/ 2,21iO pouids (lbs)1metric ton (ton) - 2,205 pounds (lbs)1 short ton (sh ton) - 20G0O pounds (lbs)Tons oil equivalent (Toe) - 10 million kilocalories (kcal)

GLOSSARY OF ABBREVILATIONS

ANSI - American National Stand&us Inst:ituteAPI - American Petroleum InstituteCCITT - Comite Consultatif International Telegrafique et

TelephorniqueCCIR - Comite Consultatif InternatLonal des Radiocommunicationsdwt - Deadweight tons, oil carrying capacity of tanker in lg tonsFCEI - Federal Committee on Energy and IndustryIEC - International Electric CodeJUGEL - Union of Yugoslav Electric Power IndustryMATREZ - Federal Directorate for Reseries of Foodstuffs and Strategic

StocksNEC - National (US) Electric CodeSAS - Social Accounting Service

JUGOSLAVENSKI NAF2C'OYGDFISCAL YEAR

January 1 - December 31

1/ Used throughout the report when referrLig t.o c;rude oil and pipe

APPRAISAL OF

THE YUGOSLAVIA OIL PIPELINE

(Jugoslavenski Naftovod Poduzeceza Transport Nafte U Osnivanju)

CONTENTS

Page No.

SUMMARY ........................................... i

I. INTRODUCTION ..................... .................

II. BACKGROUND ........................................ 2

A. The Country and the Economy .... .............. 2B. Energy Resources ............................. 3C. Energy Sector Policy and Organization ........ 3D. The Oil and Gas Sector .... .................... 4E. Past Developments in Energy Supply and Demand. 5F. Present Situation and Future Prospects ....... 6

III. THE BORROWER ...................................... 7

A. Background ....... ........................... . 7B. Organization and Management ............... .. . 7C. Recruitment and Training ................. .... 7D. Line Fill ................................... . 8E. Insurance ....... ........................... . 8F. Operations and Maintenance ............... .... 8G. Operational Arrangements with Clients and

Others . ..................................... 9H. Investment Plan ...... ....................... . 9

IV. THE PROJECT ....................................... 10

A. Objectives ................... ................ 10B. Description ...... ............ ................ 10C. Status of Engineering ........... .. ........... 12D. Cost Estimate ............... .. ............... 12E. Financing Plan .......... .. ................... 14F. Implementation ............... .. .............. 15G. Disbursements ............... .. ............... 17H. Ecology and Safety .......................... 17

TABLE OF CONTENTS (Continued)

Page No.

V. FINANCIAL EVALUATION ............................... 18

A. Financial Forecasts ............ .. ............ 18B. Tariffs ...................... . ................ 19C. Cash Flow ...... ............. ................. 20D. Audit ....... .............. ................... 20E. Special Loan Repayment Guarantees .... ........ 20

VI. ECONOMIC EVALUATION ................................ 21

A. General ...................................... 21B. Demand Projections ........ ;: ................. 21C. Size of the Proposed Facilities .... .......... 22D. Alternatives to the Proposed System .... ...... 22E. Project Benefits ..................... 23F. Sensitivity to Changes in Traffic Growth ..... 23G. Beneficiaries and Employment .... ............. 23H. Impact on Alternative Means of Transport 24

VII. AGREEMENTS REACHED AND RECOMMENDATIONS .... ........ 24

ANNEXES

1. The Energy Sector ir. Yugoslavia2. Tanker Terminal3. Duties of The Foreign Consultants4. Detailed Project Cost Estimate5. Estimated Schedule of Disbursements6. Budget and Accounting Procedures7. Bases and Assumptions Used in Financial Ana:Lysis8. Revenue Accounts9. Balance Sheet10. Cash Flow11. Resume of Transport Agreements12. Background and Assumptions Used in the Justification of the Project13. Design Codes and Standards

CHARTS

1. Organization Chart (World Bank 9761)2. Schematic Diagram of the Pipeline System (World Bank 9754)3. Project Schedule (World Bank 15172)

>APS

1. Location of The Pipeline System (IBRD 11536)2. Location of Hydrocarbons and Coal (IBRD 11617)

APPRAISAL OF

THE YUGOSLAVIA OIL PIPFLINE

(Jugoslavenksi Naftovod Poduzeceza Transport Nafte U Osnivanju)

SUMMARY

i. Yugoslavia's energy resources are lignite and coal (97%), hydrocar-bons (oil and gas 3%) and hydropower. At the 1975-1990 forecast level ofconsumption, lignite and coal will last some 260 years. Despite the largecoal reserves and hydroelectric potential, Yugoslavia is not self-sufficientin energy; the low quality of the coal makes long distance haul uneconomic andlimits its use to power and steam generation while development of the hydro-electric potential has been hampered by administrative considerations.

ii. Energy producers, consumers and the authorities are in the processof negotiating social agreements which will define the interrelationship ofall parties. The Government created a Federal Committee on Energy and Indus-try (FCEI) to study long-term energy policy; the Committee's findings arethat: (a) Yugoslavia should limit its dependence on imported fuels by substi-tuting coal and hydropower for the former wherever feasible; (b) conservationmeasures should be adopted where appropriate but not at the expense of econo-mic development and (c) pricing policies should be revised to support anational energy policy. The Government has agreed to discuss these findingswith a Bank mission scheduled to visit Yugoslavia in the fall of 1975.

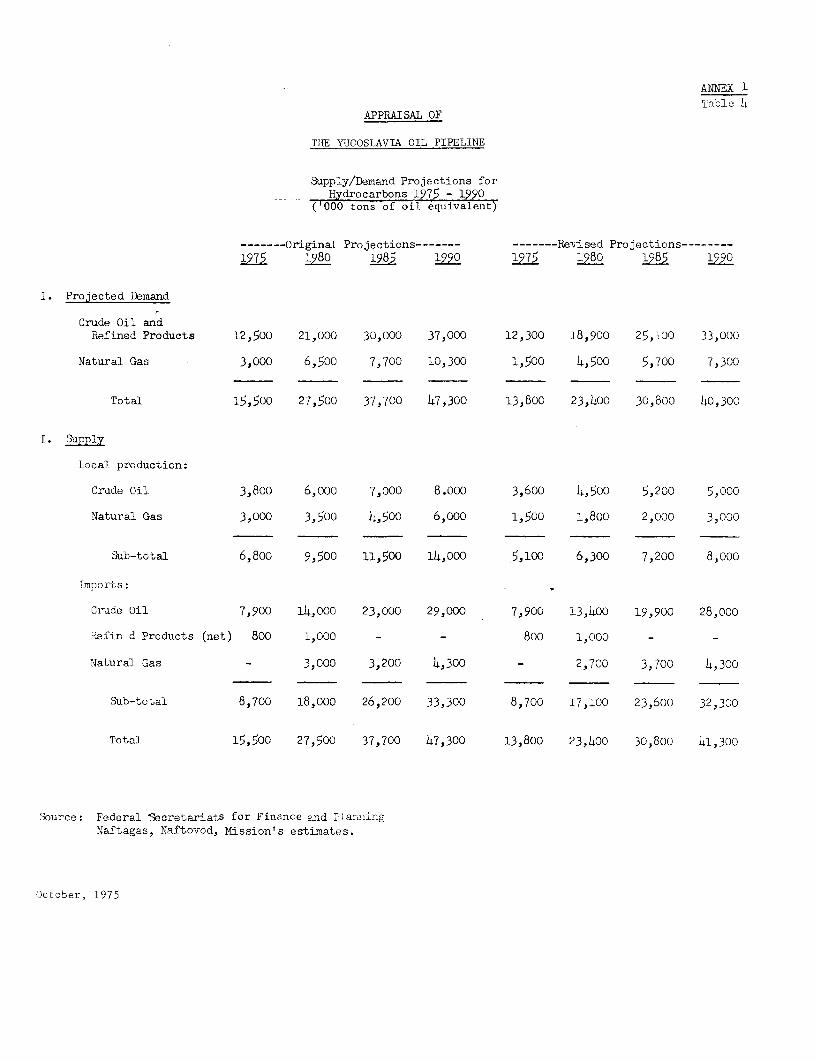

iii. These measures should provide a logical framework for energy devel-opment in Yugoslavia. The Government's energy demand forecasts which werelowered after the oil crisis show total energy demand to increase three timesbetween 1975 and 1990. Hydrocarbons demand will increase at the same paceas total energy and imports of crude oil are expected to increase from 7.9million in 1975 to 28 million tons in 1990. Considering Yugoslavia's currentlow per capita energy consumption, these projections are reasonable.

iv. To handle the increased volumes of oil imports three oil and gasenterprises decided to build the necessary facilities and the Government hasasked the Bank for assistance in financing the facilities for the projectwhich will provide an oil port and overland transport of crude oil by pipe-line to five inland refineries and to Hungary and Czechoslovakia. The crudeoil will be imported through the Adriatic Port of Omisalj. Besides the oilport, the project will comprise seven pump stations, five oil storage tankfarms, a control system and 736 km of pipelines. The project will lower thecost of inland transport of oil in Yugoslavia.

v. The project costs, net of duties and other local taxes, are estimatedat Din. 6,532.2 million (US$384.2 million) of which Din. 3,675 million(USS216.2 million) would be foreign exchange and Din. 2,857.2 million(US$168.0 million) represent the local currency expenditure.

- ii -

vi. This would be the second loan to Yugoslavia in the pipeline sub-sector. The first loan (Loan 916-YU, June 1973) was made for the NaftagasPipeline Project to transport and distribute natural gas to industrial con-sumers in Serbia and Vojvodina and contemplated future expansion into Kosovo,a less-developed area. Due to a tripling of the price of pipe, this projectis facing a large cost overrun which the Borrower and the local guarantorbank is unable to finance. The restructuring of the project and a revised.financing plan are now being considered.

vii. The project would be financed by the Bank loan (US$49 million) at8.5% repayable in 18 years including a grace period of four years; other for-eign loans will be from Kuwait (US$125 million), Libya (USS70 million),Hungary (US$25 million) and Czechoslovakia (US$25 million). The local loanswill be for US$26.5 million, US$59.0 million and US$20.5 million respectivelyfrom three oil and gas enterprises, the Federal Petroleum Fund and two banks.The proceeds of all loans total US$400 million and will cover the projectcosts including taxes and interest during construction on the Kuwait and Bankloans. Bank financing would be parallel with that of other foreign lenders.

viii. The Borrower would be Jugoslavenski Naftovod Poduzece za TransportNafte U Osnivanju (Naftovod), an enterprise established by three oil and gasenterprises in Yugoslavia, INA, Naftagas, and Energoinvest. Naftovod wouldbe responsible for project implementation and for oPeration of the facilitiesexcept the port. Consultants have been employed to carry out design andconstruction supervision.

ix. The foreign exchange costs of consultants, construction, two tugsand oil loading arms would be financed under the Bank loan and would be pro-cured under international competitive bidding except for the services offoreign consultants. The Kuwaiti loan will comprise cash and the supply ofpipe, and the Czechoslovakian loan comprises pipe and construction servicesfor the Sisak-Hungary section of the pipeline.

x. The construction period would start in March or April 1976; Stage I(16 million tons annual capacity) would be completed in May 1978, and StageII (20 million tons) would be finished in 'May 1979.

xi. The project will start earning revenue from 1978 at the completionof Stage 1. The financial forecasts indicate that it will earn sufficientrevenue to meet all liabilities and generate funds for financial reserves.

xii. The pr,ject will provide economical transport of crude oil to fiveYugoslav refineries. When compared to expanding the existing means of oiltransport, railways and barges, the rate of discount at which both coststreams are equalized is 50% after taking account of foreign transit revenues.

xiii. In view of the problems with recent cost overrtns in Yugoslavia,special overrun guarantees have been provided. To cope with unforeseenemergencies, which might create temporary liquidity problems, special debtservice guarantees have also been provided. In view of the very tight proj-ect schedule, contingency planning will be provided to help ensure that thefacilities required for the foreign transit are completed in time.

- iii -

xiv. Subject to agreement on the issues set forth in this report, theproject is suitable for a Bank loan of US$49 million to Jugoslavenski NaftovodPoduzece za Transport Nafte U Osnivanju. A reasonable term for the loan is18 years including four years of grace.

APPRAISAL OF

THE YUGOSLAVIA OIL PIPELINE

(Jugoslavenski Naftovod Poduzeceza Transport Nafte U Osnivanju)

I. INTRODUCTION

1.01 The Socialist Federal Republic of Yugoslavia and INA, Naftagas,and Energoinvest (the Founders) have asked the Bank to help finance a pipe-line project to transport imported crude oil from an Adriatic port to fiveinland refineries and Hungary and Czechoslovakia. Jugoslavenski NaftovodPoduzece za Transport Nafte U Osnivanju (Naftovod, the Borrower) was createdto implement the project and operate the facilities. The project was pre-pared by the Borrower with the assistance of consultants.

1.02 The concept of pipeline transport of imported oil dates back to1969 when the Founders proposed rival pipeline schemes. In 1973 the Founderspooled their activities and the project was selected as being the most econom-ical scheme. The Bank was asked to participate in financing the projectwith the principal aim of attracting other foreign loans on reasonable terms.To enable the Bank to influence project execution, a loan of US$49 million isrecommended. The proposed facilities will transport "transit" oil to Hungaryand Czechoslovakia at a profit and will provide economical oil transport tothe inland refineries. The project comprises an oil-receiving port in OmisaljBay, five oil storage tank farms, seven pump stations, 736 kilometers (km) ofvarious sizes of pipelines, and the services of foreign engineering consult-ants.

1.03 The project is estimated to cost Din. 6,409.4 million (IJS$377 mil-lion) including all contingencies and local taxes. The foreign exchange com-ponent is estimated at Din. 3,284.4 million (US$193.2 million) or 51% of thetotal.*

1.04 Including the Bank a total of five foreign lenders are contributingUS$294 million, while local financing in the amount of US$106 million is be-ing contributed by six Yugoslav lenders. The financing plan includes inter-est during construction of Din. 390.6 million (US$23 million).

1.05 This report is the result of an identification mission in December,1973, and pre-appraisal and appraisal missions in Septerber, 1974, andJanuary, 1975, respectively. The appraisal. mission consisted of Messrs.P. Bourcier (Economist), A. Krishnan (Financial Analyst), J. Ristorcelli(Engineer), and H. Harries (consultant).

* Net of duties and other local taxes but including interest during con-struction, the project is estimated to cost Din. 6,532.2 million(US$384.2 million).

- 2 -

II. BACKGROUND

A. The Country and The Eoomy

2.01 Yugoslavia is a federation of six republics and two autonomousprovinces. It has an area of 255,804 km2 and a population of 21 milliongrowing at 1% per annum. It has a socialist market economy, in which mostof the means of production are owned by society as a whole, but are entrusted,through a system of self-management, to the control of the workers that usethem. There is a private sector, accounting for only 15% of GDP, which ismade up of small farms and small commercial enterprises 1-rincipally in theretail and service trades.

2.02 In the social sector decisions are decentralized and largely out-side the scope of government at any level, although there are policies formandatory coordination in certain instances. The basic principle for alleconomic decision-making is self-management by the workers. The basicdecision-making units are called Basic Organizations of Associated Labor(BOAL) which are technically identifiable units which could, at least inprinciple, function independently. In most instances, several BOALs areintegrated into Work Organizations of Associated Labor through revocablecontracts knonm as Self-Management Agreements. The affairs of BOALs andwork organizations are governed by councils elected by all the workers.

2.03 When the economic activities of workers are of concern to others,such as in public utilities and public services, Self-Managing Conmunities ofInterest are established by the organizations of associated labor in thesefields and the beneficiaries of their products or services. The Communitiesof Interest provide the framework for developing, financing, and regalatingthe activity concerned. They are a recent development and many of them arestill in the process of being established.

2.04 The economy has grown at the high rate of 5.5% per annum over thelast two decades, and GDP per capita, measured in real terms, at 4.5% perannum. Wide disparities exist between regions; compared with the nationalaverage of about US$900 (1973), per capita GDP is one-third in Kosovo andnearly double in Slovenia. Industry, which now accounts for 40% of GDP, hasgrown about 9% per annum. Agriculture now accounts for 20% of GDP, and itsgrowth rate has been about 2.5% per annum. The projected trend of economicgrowth implies continuation of the past high-growth rate in overall energydemand, and, more particularly, electricity, oil, and natural gas (para.2.19).

-3-

B. Energy Resources

2.05 Yugoslavia's main energy resources are lignite, coal, and hydro-power (Map 2). Total fossil fuel reserves are estimated at 4,100 milliontons of oil equivalent (Toe) with low-grade coal and lignite accounting for97% and hydrocarbons for 3%. Reserves of coal and lignite are located inKosovo (70%) and Bosnia-Herzegovina (20%). Reserves of oil and gas arelocated in Vojvodina (40%) and Croatia (60%). Hydro resources represent about60,000 million kWh/year and 70% df it is located in Croatia, Serbia, andBosnia-Herzegovina.

2.06 Despite large coal reserves, Yugoslavia is not self-sufficient inenergy and has to rely on imports of hydrocarbons and coking coal to satisfyinternal demand. This is principally due to the low quality of lignite andbrown coal which prohibits transport over long distances and limits its useto power and steam generation. Annex 1 gives a detailed description of energyreserves.

C. Energy Sector Policy and Sector Organization

2.07 National energy policy is based on restraining dependence on im-ported fuels, particularly oil, through greater development and utilizationof indigenous sources, and this has been accounted for in the preparationof the project (Annex 1, para. 24). Until recently the role of the FederalGovernment was limited to pricing and foreign borrowing. The functions ofplanning and policy-making in the energy sector and the coordination of theenergy programs of the Republics were assigned to a Federal Committee onEnergy and Industry (FCEI) created in 1974. It consists of representativesof local governments and energy and industry sectors.

2.08 Responsibility for implementing energy policy lies, as in mostother sectors, with the energy enterprises which are the principal agents inthe development of energy. They draw up their development and investmentplans and arrange financing. A large number of enterprises are members ofprofessional associations which represent them within the Federal Chamber ofEconomy. Power enterprises belong to the Union of Yugoslav Electric PowerIndustry (JUGEL) and coal producers to the Association of Yugoslav Coal Pro-ducers. These V-dies have no executive power and cannot coordinate adequate-ly the development of the energy sector. There is not, so far, a similarbody in the oil and gas industry.

2.09 Since 1965 coordination between various subsectors (electricity,coal, and hydrocarbons) has been weak particularly in resource allocations.Investment decisions were made on a local basis without due attention tocountry and sector development. This was particularly true in the powersector and together with lack of adequate funds it resulted in severe powershortages in 1973. This situation is not expected to improve until 1977/78.

-4-

2.10 The recent constitutional changes and the increase in the worldprice of energy, particularly oil, have brought about two major changes:

(i) relations between energy enterprises, users, and local andFederal Authorities are now regulated by "social agreements"which will form the framework of the future development ofthe sector for a period of five years, and

(ii) through FCEI the Federal Government is now playing a moresignificant role in the formulation and implementation oflong-term energy policies (para. 2.07),. and a statement onenergy policy by the Federal Executive Council recently ap-peared in the document entitled "The Basis of Common Policyfor the Long-Term Development of Yugoslavia."

2.11 Social agreements in the power and coal. industries are in the finalstage of negotiations; the oil industry was expected to complete its dis-cussions and sign the agreements by the end of 19,75. These agreements willdefine, inter alia, the quantitative objectives to be achieved for a partic-ular branch, the investment program and financing plan of that branch for thenext five years and the pricing policy. Since these agreements involve pro-ducers, users, and local and Federal Authorities, it is expected that theywill improve coordination within and among branches. Some positive resultshave already been achieved by eliminating duplication among individual devel-opment plans. There is, however, room for improvement in the definition ofsector priorities and in project preparation and implemertation.

2.12 The studies sponsored by FCEI should provide a rational frameworkfor the selection of priorities and the formulation of adequate developmentstrategy. It has initiated studies covering the immediate, medium, and long-term future (1985-1990) with the objective of submitting proposals to theFederal Govermnent by mid-1975. Preliminary results of these studies werediscussed by the mission and were found to be a substantial improvement onpast performance. Although it is too early to ma.ke a final judgment as to theeventual efficiency of the new procedures, Yugoslavia has now an adequatetool to deal with energy problems, and positive results should materializesoon. In agreement with Federal Authorities, the Bank has scheduled a mis-sion to review the findings and recommendations of FCEI.

D. The Oil and Gas Sector

2.13 The oil and gas sector consists primarily of two large integrateddomestic enterprises, INA and Naftagas, which cover all activities in the oiland gas industry from exploration to distribution. of final products. Inaddition there is one enterprise dealing with oil refining (Energoinvest)and several enterprises dealing with the distribu.tion of refined products.All these enterprises are independent and to a large extent competitive;however, they are linked together by market agreements regarding the purchas-ing of crude oil and the distribution of products. They also cooperate

-5-

closely in the preparation of tariffs for approval by the Federal Governmentwhich coordinates the imports of oil. By year-end 1975 Yugoslavia expectsto sign long-term oil supply contracts covering 80% of the country require-ments over the five years ending in 1980.

2.14 Coordination between these enterprises in the past has been in-adequate; in many instances they could not agree on common development pro-grams and some projects have been delayed considerably by conflicting re-gional interests. This is the case for the proposed project which was firstinitiated in 1969, and for which agreement was not reached until the end of1973. The situation, however, is improving considerably, partly as a resultof the efforts of FCEI, and partly as a result of the proposed project whichled to intensive discussions on long-term supply and demand projections,pricing policies, and development of domestic refining capacity. Within thisframework, the oil and gas enterprises have agreed on common supply/demandfigures until 1985-1990 (Annex 1, para. 27) and have also agreed to lowerrefining capacity expansion to satisfy the projected demand. These will befinalized in the social agreement presently under negotiation (para. 2.11)and have been used as the basis for the project.

E. Past Developments in Energy Supply and Demand

2.15 After a period of relative stagnation, overall energy consumptionincreased rapidly from 1967 to 1973 at an average rate of 8.2% per annum com-pared with an average GNP increase of 6.4% per annum. During the same periodthe structure of demand changed considerably and coal whiLch had been tradi-tionally the predominant fuel in Yugoslavia was surpassed by oil. This wasdue primarily to the development of a modern industrial sector (40% of GDP)and to the rapid growth of road transportation. In 1973 total oil consump-tion accounted for over 40% of the total demand compared to 28% in 1967. Oilis used mainly in the industrial and transportation sectors, which accountfor 84% of total demand for main oil products; oil and gas consumption inpower generation has always been and will remain margi;ial, as most of the in-crease will be based on the use of domestic coal.

2.16 Domestic oil production has not kept pace with demand and Yugo-slavia has to rely increasingly on imports to supply its six domestic refin-eries (Rijeka, Sisak, Bosanski-Brod, Novi Sad, Pancevo, and Lendava). In 1973oil imports accounted for 70% of total internal demand for refined products.Traditionally, the USSR has been the main foreign supplier of oil; however,in recent years Yugoslavia has been importing increasingly from the MiddleEast (Iraq, Iran). Russian crude is imported through the Danube by barge,while Middle East crude is imported through Adriatic ports and transportedby rail to the refineries of Sisak and Bosanski Brod; in 1974 oil and oilproducts transport on the Yugoslav railways accounted for about 7% of totalfreight traffic, and the cost of oil imports represented about 12% of allimports.

- 6 -

F. Present Situation and Future Prospects

2.17 Since Yugoslavia is a large importer of crude oil, it was seriouslyaffected by the oil crisis; the problem, however, wa- more one of prices thanof availability. Because of the poor quality of domestic coal, possible sub-stitution of coal for oil is limited and only minor adjustments could be madein the short run to reduce the country's dependence on foreign oil. The mainsteps taken were increases in the price of refined oil products and the crea-tion of an equalization fund to align the price of domestic crude with worldmarket prices; as a result, consumption growth slowed down to 6% per annumin 1974 compared to 7.7% in 1973.

2.18 Before the oil crisis it was expected that total energy demandwould continue to grow rapidly and would increase 3.5 times between 1973 and1990. Oil demand would continue to grow faster than overall demand and wouldbe primarily satisfied by imports, since domestic production was not expectedto meet more than 9% of the total energy demand.. Natural gas would also bedeveloped based on exploitation of domestic resources and on imports from theUSSR and North Africa and by 1990 hydrocarbons would account for more than51% of total energy demand.

2.19 Following the oil crisis these projections were lowered and thepreliminary results of studies sponsored by FCEI] show that total energy con-sumption will increase 3 times over the next 15 years reaching about 83 mil-lion Toe by 1990. Hydrocarbon demand will grow at the same pace as totaldemand; however, the volumes of oil imports in 1990 will be almost identicalto those projected previously because:

(i) previous projections were based on fast growth in the useof natural gas which is not likely to materialize. Recent -evaluations of domestic fields have been somewhat disap-pointing and import possibilities at competitive prices arelimited; and

(ii) previous projections for domestic oil production were over-optimistic. It is now estimated that domestic productionwould start declining after 1985 to reach 5 million tonsin 1990 instead of 8 million previously considered.

2.20 Based on these projections it is now considered that import ofcrude oil will increase from about 7.9 million tons in 1975 to 28 milliontons in 1990, at average rates per annum declining from 11% between 1975 and1980, to 8% and 7% between 1980 and 1985, and 1985 and 1990, respectively.Host of this oil would be imported from the Middle East through Adriatic portsand would have to be transported to the inland refineries. Conventionaltransport of such volumes of oil by rail is not economical and it was, there-fore, decided to build the pipeline.

III. THE BORROWER

A. Background

3.01 The three principal oil and gas enterprises of Yugoslavia, INA ofCroatia, Energoinvest of Bosnia-Herzegovina, and Naftagas of Serbia (theFounders), have jointly established a new enterprise, JUGOSLAVENSKI NAFTOVOD(Naftovod) to design, build and operate port and pipeline facilities forthe transport of imported crude oil to five local refineries and for transitto Hungary and Czechoslavakia. The new Enterprise has been registered in theDistrict Commercial Court in Rijeka; its headquarters will be in Rijeka withoffices in Zagreb and Belgrade. Naftovod will be the Borrower. The Enter-prise will charge the foreign offtakers at agreed commercial rates and localrefineries at cost, both arrangements being covered by take or pay clausesin the transport contracts.

B. Organization and Management

3.02 Currently and until completion of construction, Naftovod is an"enterprise under foundation" and a Council of 12 members, six appointed bythe Founders and six by Naftovod, which will be the governing body responsibleall policy decisions. The General Manager, guided by a Coordinating Commit-tee of six members (two from each Founder) will execute the Project in accord-ance with the Council's decisions. During this phase Naftovod, assisted bylocal and foreign consultants (para. 4.04), will be responsible for projectexecution. It will employ over 100 staff, 40 of whom have already been ap-pointed; no difficulties are envisaged in recruiting the balance. -

3.03 At the start of commercial operations, the Council will be substi-tuted by a Workers' Council and the Coordinating Committee will look afterthe interests of the Founders. The Enterprise will then consist of fivedepartments, namely: (1) Technical, (2) Economic and Financial, (3) Legaland Personnel, (4) Commercial, and (5) Operations, comprising a total of 350staff (Chart 1). The proposed organization appears suitable, and the manage-ment staff thus far appointed are capable and diligent.

C. Recruitment and Training

3.04 No difficulties are anticipated in the recruitment of the majorityof the skilled personnel, as experienced staff are available in the variousrefineries which employ thousands of skilled workers. Most of them will re-quire only familiarization with the new facilities and the pipeline's operat-ing procedures. However, Naftovod will have to train staff in some specialskills, such as electronics, instrumentation, and oil dispatching and schedul-ing. A program of training has yet to be worked out; this will be done by

-8-

the foreign consultants (Annex 3). The specialized training will very likelyinvolve less than 40 individuals, and it will be carried out partly on thejob in Yugoslavia, partly in foreign suppliers' plants, and in part in simi-lar European facilities. The Bank has Naftovod's agreement to begin implement-ing the specialized training program no later than May 31, 1977.

D. Line Fill

3.05 The initial supply of crude oil to fill the pipeline and the storagetanks, the line fill, would amount to about US$30 million. In the case ofpipeline companies who are common carriers, the line fill is either providedby them as part of their capital investment and tariffs charged accordinglyor supplied by the users and treated by them as their "sailing stock." Thislatter procedure is common in Europe. In the case of Naftovod, the line fillwill be provided free of cost by the Federal Directorate for Reserves of FoodStuffs and Strategic Stocks (MATREZ), who will have first call on the linefill in case of a national emergency.

E. Insurance

3.06 Adequate insurance coverage for all assets and third-party risks,including possible damage from oil spills, will be provided; adequate pro-vision for insurance has been made in the revenue accounts.

F. Operations and Maintenance

3.07 The local refineries, under the coordination of the Federal Govern-ment, and Hungary and Czechoslovakia will be responsible for arranging de-livery of the crude oil to Naftovod at the oil port.

3.08 Handling the tankers and operating the port facilities will be theresponsibility of the Port of Rijeka (para. 3.12 b(i)).

3.09 Naftovod will be responsible for receiving the crude and deliveringit to the offtakers. Basic transport agreements have been signed betweenNaftovo.d on one hand and Hungary, Czechoslovakia, and the Founders on theother; detailed operational arrangements have yet to be agreed (para. 3.12(a)).

3.10 Electric power for the operation of the system will be provided bylocal enterprises. Naftovod will install telecontrol systems to serve thepipeline in areas where the Federal Communications Authority has no such in-stallations. In other areas, largely from Sisak eastward, Naftovod will leasecable facilities from the appropriate communications authorities (para. 3.12r) (ii) ).

- 9 -

3.11 The principal maintenance depot will be located in Sisak and asmaller one in Omisalj. The maintenance crews of the various refineries willbe available to Naftovod during emergencies. The project estimate includesDin. 44.2 million (US$2.6 million) for warehouses, shops, and maintenanceequipment; this is adequate.

G. Operational Arrangements with Clients and Others

3.12 The Bank has Naftovod's agreement that it will sign: (a) by Novem-ber 15, 1975, operating agreements with the seven offtakers covering technicaland operational matters, such as batching procedures, metering and custodytransfer, types of crude, including physical and chemical properties, sche-duling of oil receipts and shipments, etc., (para. 3.09), and (b) by May 31,1977, the following agreements:

(i) a port operations agreement with the Port of Rijeka forproviding normal port facilities and services, whichwill ensure that Naftovod will receive suitable compensa-tion for the port facilities financed by the project andturned over to the port authority (para. 3.08 and Annex 2,para. 11), and

(ii) a telecommunications and power supply agreement with theappropriate authorities for the lease of communicationsfacilities and the supply of power (para. 3.10),

and that prior to such signature it will submit the draft agreements to theforeign consultants for their advice and thereafter the draft agreementunder b(i) to the Bank for its review and approval.

H. Investment Plan

3.13 The proposed project is the first and major part of a series inNaftovod's investment plan which provides for the project and for increasesin capacity to handle the traffic to 1990. The investment program totalsDin. 8,315 million during the period 1975-1990; this includes Din. 6,800million for the project and Din. 1,515 million, for expansion to ultimatecapacity (para. 4.01). The mission found that refineries' demand forecastswere high because they overlapped due to a lack of coordination (paras. 2.11and 2.14) and this led to inflated projections which were corrected after somediscussion. To help ensure proper coordination in preparing future demandprojections, the Bank has Naftovod's agreement not to undertake capacity ex-pansion programs without prior consultation with the Bank.

- 10 -

IV. THE PROJECT

A. Objectives

4.01 Stage I of the project will be completed in 1978 and comprises thefacilities to transport 16 million tons of petroleum per year; Stage II willbe completed in 1979 and will increase the capacity to 20 million tons annual-ly. The facilities are capable df being expanded to 34 million tons yearly,the throughput in 1990. The project will provide substantial earnings toYugoslavia from the transit of foreign oil and economical transport of crudeto the Yugoslav refineries.

B. Description

4.02 The project is the least cost solution tCo oil transport and it com-prises (Chart 2 and Map 1) an oil port, five oil storage tank farms, sevenpump stations, 736 km of pipelines, a control system and engineering services.The project will be designed to the codes and standards listed in Annex 13and will consist of:

(a) the procurement of two tugs of about 2,000 horsepower each andseveral launches, to assist the tankers to and from the berths;

(b) the procurement and installation of two marine berths in OmisaljBay capable of handling tankers from 30,000 dwt to 350,000 dwt,including mooring dolphins, power, bunkering, fire-fighting andwater-supply facilities, and navigational aids at the approachesto the port.

(c) the procurement and installation of an oil storage tank farmwith a capacity of approximately 720,000 m3 (about 612,000tons), including piping, utilities, and a fire-fighting system;

(d) the procurement and installation of:

(i) approximately 173 km of 36-in pipeline between Omisaljand Sisak with a short lateral pipeline to the Sisakrefinery;

(ii) two pump stations (Omisalj and Melnice) totalling ap-proximately 17,500 kW;

(iii) a maintenance depot at Omisalj housing specialized equip-ment and personnel;

(iv) a pressure-reducing station between Melnice and Sisak;

- 11 -

(v) a buffer oil storage tank farm at Sisak with a capacityof about 70,000 m3 (approximately 60,000 tons);

(e) the procurement and installation of:

(i) approximately 105 km of 28-in pipeline from Sisak toVirje and Gola 1/ (Hungarian border);

(ii) a 7,500 kW pump station and a maintenance depot atSisak;

(iii) a buffer oil storage tank farm of about 30,000 m3

(approxlmately 25,500 tons) capacity at Virje;

(iv) a pump station at Virje of about 600 kW, and

(v) a 67 km long 12-in pipeline between Virje and theLendava refinery;

(f) the procurement and installation of:

(i) approximately 138 km of 28-in pipeline between Sisakand Slobodnica with a 4.5 km lateral pipeline betweenSlobodnica and the Bosanski Brod refinery;

(ii) two additional pumps at Sisak with a total power of3,200 kW, and

(iii) a buffer oil storage tank with a capacity of 40,000 m3

(approximately 34,000 tons) at Slobodnica;

(g) the procurement and installation of:

(i) a 16-in pipeline about 85 km long between Slobodnicaand Negoslavci;

(ii) a 4,100 kW pump station at Slobodnica;

(iii) a 22-in 78 km long pipeline between Negoslavci andNovi Sad with a short lateral pipeline between NoviSad and the Novi Sad refinery;

(iv) a 2,300 kW pump station at Negoslavci,

1/ At Gola a connection will be made with the Hungarian pipeline which willbe built to transport the crude oil into Hungary and to Ctechoslovakia.

- 12 -

(v) a buffer oil storage tank farm of 40,000 m3 (approxi-mately 34,000 tons) at Novi Sad;

(vi) a 2,600 kW pump station at Novi Sad,, and

(vii) a 86 km 18-in pipeline between Novi Sad and thePancevo refinery;

(h) the incorporation into the system of an existing 16-in pipelinebetween Slobodnica and Negoslavci;

(i) the procurement and installation of a supervisory controlsystem including telecommunications, telemetering and tele-control;

(j) the services of pipelines engineering consultants to do thebasic designs, tendering and project plarnning and to provideoverall supervision during implementation.

C. Status of Engineering

4.03 The project is based on a feasibility study by INA Engineering(Zagreb) and INEG Consultants (UK) and optimization studies by Industropro-jekt, Zagreb consultants. Although final designs have not yet been started,sufficient preparatory work has been done to define! the project and makerealistic cost estimates. Slight reductions in the size of the facilitiesmay be indicated upon completion of final designs.

4.04 Naftovod has assigned overall design responsibility to Industro-projekt of Zagreb, assisted by Omniam Technique des Transports par Pipelines(OTP, a French firm) who will be responsible for designs, tender preparation,project coordination, and some of the duties outlined in Annex 3. Industro-projekt may, at its discretion, subcontract further work to other competentlocal firms on terms and conditions acceptable to Naftovod and the Bank.Naftovod informed the Bank that it will assign overall responsibility forconstruction supervision also to Industroprojekt assisted by OTP, who willcarry out the remaining duties in Annex 3. These arrangements are satis-factory.

D. Cost Estimate

4.05 The project is estimated to cost Din. 6,409.4 million (US$377 mil-lion) including all contingencies and local taxes plus interest during con-struction of Din. 390.6 million (US$23 million) on the proposed Kuwaiti andBank loans. The foreign exchange component is estimated at Din. 3,675 million(US$216.2 million) or 54% of the total. Customs duties and other local taxesare estimated at Din. 267.8 million (US$15.7 million).

- 13 -

4.06 The basic components of the project and their estimated costs(rounded) are shown below; further details are shown in Annex 4.

% of Basic---- Din Million ------ -----US$ Million----- ProjectLocal Foreign Total Local Foreign Total Cost

A. Port Facilities 224.7 202.6 427.3 13.22 11.92 25.14 9.3

B. Terminals, Tanksand Pump Stations 580.0 607.5 1,187.5 34.12 35.74 69.86 25.9

C. Pipelines 958.2 1,488.0 2,446.2 56.35 87.52 143.87 53.3

D. Telecommunication& Control 21.1 124.3 145.4 1.24 7.31 8.55 3.2

E. Owners supervision,training & consult-ants 312.8 69.4 382.2 18.40 4.08 22.48 8.3

Basic project cost 2,096.8 2,491.8 4,588.6 123.33 146.57 269.90 100.0

F. Contingencyallowances

1. Physical 285.1 231.7 516.8 16.77 13.63 30.40 11.32. Price 743.1 560.9 1,304.0 43.70 23.00 76.70 28.4

Subtotal F 1,028.2 792.6 1,820.8 60.47 46.63 107.10 39.7

G. Total projectcost 3,125.0 3,284.4 6,409.4 183.80 193.20 377.00 139.7

4.07 The estimate was prepared by Naftovod and the consultants; it wasreviewed by the Bank and found adequate. Although it is not anticipated thatforeign contractors alone will win many bids due to the advanced state ofthe contracting industry in Yugoslavia, some participation by foreign con-tractors is expected. The above estimate reflects Naftovod's and the Bank'sjudgment of the most likely degree of participation by foreign contractors(para. 4.15). The foreign exchange costs of the project could increase toUS$213:2 million or decrease to US$179.2 million based, respectively, onmaximum and minimum awards to and participation by foreign contractors. Theestimate provides an overall physical contingency of 11.3% which is ample.Price contingencies of 15% and 12% were applied to local costs for 1975 andthereafter, respectively; foreign costs were escalated at 11% and 8%, respect-ively, in 1975 and thereafter. These escalation factors are in accordancewith current Bank guidelines.

- 14 -

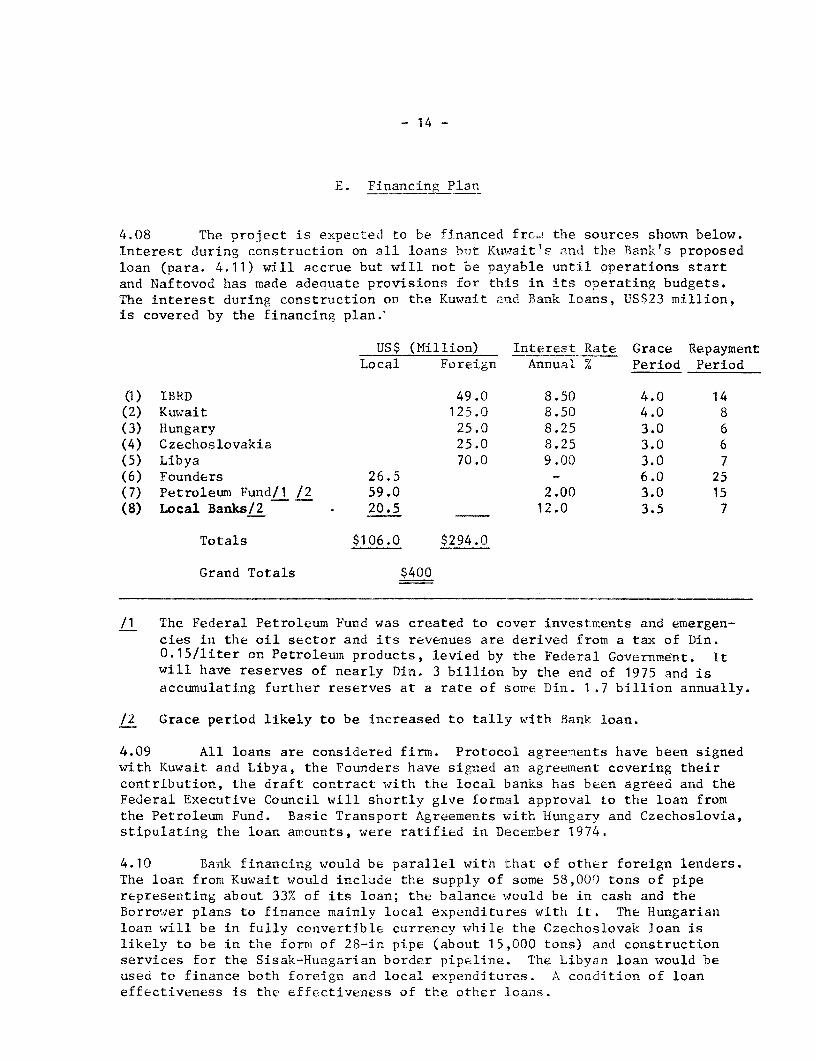

E. Financing Plar

4.08 The project is expected to be financed frc, the sources shomn below.Interest during construction on all loans biit Kuwait's and the Bank's proposedloan (para. 4.11) will accrue but will not be payable until operations startand Naftovod has made adequate provisions for this in its operating budgets.The interest during construction on the Kuwait and Bank loans, US$23 million,is covered by the financing plan.'

US$ (Million) Interest Rate Grace RepaymentLocal Foreign Annual % Period Period

(1) IBRD 49.0 8.50 4.0 14(2) Kuwait 125.0 8.50 4.0 8(3) Hungary 25.0 8.25 3.0 6(4) Czechoslovakia 25.0 8.25 3.0 6(5) Libya 70.0 9.00 3.0 7(6) Founders 26.5 - 6.0 25(7) Petroleum Fund/i /2 59.0 2.00 3.0 15(8) Local Banks/2 * 20.5 12.0 3.5 7

Totals $106.0 $294.0

Grand Totals $400

/1 The Federal Petroleum Fund was created to cover investments and emergen-cies in the oil sector and its revenues are derived from a tax of Din.0.15/liter on Petroleum products, levied by the Federal Government. Itwill have reserves of nearly Din. 3 billion by the end of 1975 and is

accumulating further reserves at a rate of some Din. 1.7 billion annually.

/z Grace period likely to be increased to tally with Bank loan.

4.09 All loans are considered firm. Protocol agreements have been signedwith Kuwait and Libya, the Founders have signed an agreement covering theircontribution, the draft contract with the local banks has been agreed and theFederal Executive Council will shortly give formal approval to the loan fromthe Petroleuml Fund. Basic Transport Agreements with Hungary and Czechoslovia,stipulating the loan amounts, were ratified in December 1974.

4.10 Bank financing would be parallel with that of other foreign lenders.The loan from Kuwait would include the supply of some 58,000 tons of piperepresenting about 33% of its loan; the balance would be in cash and theBorrower plans to finance mainly local expenditures with it. The Hungarianloan will be in fully convertible currency while the Czechoslovak loan islikely to be in the forrmi of 28-in pipe (about 15,000 tons) and constructionservices for the Sisak-Hungarian border pipeline. The Libyan loan would beused to finance both foreign and local expenditures. A condition of loaneffectiveness is the effectiveness of the other loans.

- 15 -

The Loan

4.11 The project is suitable for a Bank loan of US$49 million with repay-ment in 18 years, including a grace period of four years which corresponds withthe construction period. The proposed Bank loan would cover the foreign ex-change costs of consultants, construction services (para. 4.14) and procure-ment of two tugs and oil loading arms. These elements would be disbursed inrhythm with construction or late in the procurement cycle, and this wouldprovide the Bank with an effective means of influencing project execution(paras. 4.15 and 4.16). Retroactive financing of foreign consultants' ser-vices to May 1975 in an amount not to exceed US$0.5 million is provided.

Cost Overrun Guarantees

4.12 Loan proposals did not provide cost overrun guarantees with the ex-ception of the local banks who had agreed to guarantee overruns in propor-tion to their contribution to the project, 50; this is inadequate. Duringappraisal the Bank asked the Federal Authorities and Naftovod to considercovering cost overruns with guarantees from: (a) the Petroleum Fund; or (b)the Founders; or (c) the five refineries. The Bank has now obtained confirma-tion that the Founders will provide this guarantee and a condition of loaneffectiveness is that the Founders Agreement will be suitably amended.

F. Implementation

Land Acquisition

4.13 According to Yugoslav regulations many formalities have to-be com-pleted before the land required for the project can be acquired and construc-tion work can commence. These involve obtaining approvals in principle (thishas been done), based on preliminary studies and then construction permitsbased on final designs and estimates; the approvals and permits are grantedby many committees in each Republic. Although no serious impediments are anti-cipated, the complex procedures involved could delay the project. It hasbeen agreed that Naftovod shall promptly take all such action as shall benecessary and shall supply evidence satisfactory to the Bank that it has ob-tained all construction permits and acquired all the land and right-of-waypermits require I for the project.

Procurement

4.14 Procurement under the loan would be by international competitivebidding in accordance with the Bank Group's "Guidelines for Procurement."(For construction contracts the loan would cover foreign exchange costs ofthese contracts whose total value is estimated at US$160 million excludingproject materials and pipe and the laying of the Sisak-Gola pipeline whichwould be financed by other loans and with the exceptions noted below). Ex-ceptions would be: (a) construction contracts estimated not to exceed

- 16 -

US$100,000 (provided that in the aggregate they do not exceed US$1,000,000)which would be procured by local shopping, and (b) construction contractsestimated not to exceed US$500,000 (provided that in total they do not exceedUSS9,000,000) which would be procured by local competitive bidding. Localshopping and competitive bidding in accordance with local procedures areappropriate for the above contracts because they are geographically dispersedand the amounts involved are such that foreign firms would not be interested.Moreover, these contracts would cover mostly preparatory works such as sitepreparation and construction of materials yards wrhich should be awarded earlyin view of the tight schedule, and international competitive bidding wouldinvolve delays. Bank staff has reviewed the local procedures and they areacceptable since they ensure adequate competition. The construction coststo be financed by the loan would exclude project materials since these wouldbe financed by other foreign loans. Yugoslavia has no preference treaties,and bids for the tugs and loading arms included in the Bank loan will be com-pared on a CIF basis net of customs duties; a preference of 15% of the CIFprice or the actual customs duties, whichever is the lower, will be given tolocal manufacturers who qualify as preferred bidders.

4.15 In view of the specialized nature of the work and of the tight proj-ect schedule (para. 4.17), the Bank has Naftovod's agreement to prequalifyconstruction contractors under the Bank's Guidelines for Procurement; it wouldthus assist Naftovod in screening contractors, particularly local ones, whomight be fully occupied in the many oil and gas projects being undertaken inYugoslavia and who might require the cooperation of international contractors.Local contractors are competent to construct the port facilities, pump sta-tions, tanks and most of the pipelines and depending on their commitments arelikely to bid for these contracts. The most probable outCome will be a mixof local contractors and joint ventures of foreign and local firms, and thisis the basis for the project estimate.

4.16 As stated in para. 4.10, the Kuwait and Czechoslovak loans involvethe supply of some 73,000 tons of pipe. It is important that the pipe be madeaccording to internationally recognized standards, reasonably priced and sup-plied in accordance with the project schedule. The Borrower provided the Bankwith an engineering report on the capabilities of the Kuwait Metal Pipe In-dustries Mill. The report states that the qualit:y of the pipe produced bythe Mill is good, but it casts some concern as to the ability of the Millto supply the pipe in time to meet the construction schedule. Any delay inthe delivery schedule will, however, be detected in time for Naftovod to ob-tain supplies from alternative sources. The Bank has Naftovod's agreementto select and hire competent inspection agencies to inspect all pipe at theMills.

Project Schedule

4.17 The schedule for the project is very tight (Chart 3) since Stage Iis to be completed and operating by May 31, 1978 and Stage II one year later.Failure to start delivering oil to all offtakers by May 31, 1978 could subjectNaftovod to penalties and to avoid this, extremely careful planning is needed.

- 17 -

This will require that Naftovod place orders for pipe and long lead materi-als for Stage I in late 1975 at the latest and follow the progress of theseorders with extreme care. In some cases, premiums for early deliverieswill be required, but they will be well within the contingency allowance.Since the Omisalj tank farm and the pipelines lie on the critical path, thiswill require starting site clearing, grading and blasting in 1misalj this fallor very early in 1976 and pipeline construction soon thereafter; moreover, atleast two construction crews each for the pipelines, tank farms and pump sta-tions will be required. Valuable time has been lost in obtaining financingbut with proper controls and good planning, Naftovod should be able to meetthe target completion date for Stage I. If construction slips and timelycompletion is threatened, contingency plans would give priority to the facil-ities required to deliver oil to the foreign offtakers, and the Bank hasNaftovod's agreement to assign such priority and to seek the refineries' agree-ment not to impose penalties on Naftovod for failure to deliver oil accordingto schedule. The timely completion of Stage II does not pose serious problems.

G. Disbursements

4.18 Loan disbursements would cover: (a) the foreign exchange costs ofthe foreign consultants (b) the foreign exchange costs of construction con-tracts - the Bank would disburse against the foreign exchange costs, estimatedat 38% of total costs for foreign firms and 25% for local firms or jointventures - and (c) the costs of two tugs and loading arms for two berths ifprocured abroad or 75% of their total costs if procured locally, up to US$4million. Disbursements are expected to take place over four years from thefourth quarter of 1975 to the fourth quarter of 1979. The estimated scheduleof disbursements is given in Annex 5. Since this is a self-contained project,any surplus loan amounts on completion of the project should be cancelled.

H. Ecology and Safety

4.19 Environmental impact studies and related recommendations will bemade by four Yugoslav agencies 1/ and the UNDP Study Group for "Protectionof Human Environment in the Yugoslav Adriatic Region." These organizationswill also monitor the project during construction.

1/ Institute Ruder Boskovic (Zagreb), the Hydrographic Institute of theNavy (Split), the Institute for Oceanography and Fishing (Split), theBiological Institute of the Yugoslavian Academy of Arts and Sciencies(Dubrovnik).

- 18 -

4.20 The following are some of the environmental protection measuresrecommended in the feasibility study: (a) a floating boom and skimmer (Annex2) to contain any oil spills inside the harbor and to remove any spilled oil;(b) a 15,000 ton capacity tank and API separator to receive slops from thetankers with backwash filtration of the settled water from the separator andof storm water from oil operating areas, and biological percolation of these,as well as sewerage, so that the oil content of the processed water will beless than 5 parts per million, and (c) oil storage tanks to be surrounded bydikes of such a height that the enclosed area will be able to contain one-and-a-half times the tank volume as safety in the event of tank leaks. TheBank has (a) Naftovod's agreement that these or similarly effective measures,such as purifying all effluents from the installations, monitoring for pipe-line leaks and air pollution, etc., will be taken, as well as any reasonablemeasures recommended by the environmental study agencies, and (b) the FederalGovernment's assurance that it will take such action, within its constitution-al powers, as necessary to ensure the expeditious and effective institutionand implementation of such measures.

4.21 Installation of the pipelines will pose no threat to the environ-ment. They will be buried at sufficient depth to avoid interference withland cultivation, highways, railways, natural drainage, and animal migration.At water crossings, they will be either suspended by a structure sufficientlyhigh to avoid interference with shipping or buried deep under the river beds.They will be a silent, nearly invisible, and clean means of overland trans-port. The only visible signs of the pipeline system will be its storage tankfarms and pump stations, and the former are required, in any case, by railsand barges, while the latter will be noiseless, clean, and unobtrusive.

V. FINANCIAL EVALUATION

A. Financial Forecasts

5.01 In 1978, the traffic handled will be 8.3 million tons increasingto 16.7 and 19.8 million tons, respectively, in 1979 and 1980. Revenue Ac-counts and Balance Sheets were prepared by Naftovod staff on the standardYugoslav pattern. These have been modified where necessary for the finan-cial analysis. A description of the budget and accounting procedures isgiven in Annex 6. Bases and assumptions used in the financial analysis aregiven in Annex 7, Revenue Accounts to 1988 in Annex 8, Cash Flow Statementin Annex 10 and Balance Sheet in Annex 9. Represeintative Revenue Accountsfor 1978, 1979 and 1980 are shown below:

- 19 -

1978 1979 1980--------Din. Million------

Operating Revenue 760 1,486 1,554Operating Expenses 88 193 239Depreciation 178 315 315Surplus 494 978 1,000Interest Charges 277 606 586Repayment of Loan 185 415 454Operating Ratio 35 34 36Interest Coverage 1.7x 1.6x 1.7xDebt Service Coverage /1 1.4x 1.3x 1.3x

/1 Surplus + depreciation , interest and loan repayment.

5.02 Naftovod is protected by the take or pay clause in the transportagreements. The Revenue Accounts (Annex 8) show that under the existingtransport arrangements sufficient surplus is generated to meet all expendi-tures including debt service, and, therefore, the Enterprise is financiallysound. To ensure the continuance of this, the Bank has Naftovod's agreementthat it will not, without prior consultation with the Bank, consent to anymodification of the contracts which would affect the agreed quantities ofcrude oil to be transported and the basis of charges therefor.

B. Tariffs

5.03 The agreements with the Founders provide for the annual revisionof the tariffs payable by them on the basis of the actual expenditures in-curred by Naftovod, plus a surplus limited to 25% of the gross salarie's andwages. Under this arrangement, Naftovod would normally not incur a loss.As to Hungary and Czechoslovakia, the tariffs payable by them are laid downin the respective agreements, which provide for annual revisions accordingto price indices for steel, labor and electricity. Without providing forany changes in the price of steel 1/ but, allowing for inflation in wagesand electricity (para. 1, Annex 7), Naftovod is expected to make a substan-tial profit from transit oil beginning with Din. 118 million (US$7 million)in 1978 and totalling up to Din. 1,439 million (US$85 million) by 1988. Ifallowance is made for an increase in the price of steel, the profit is likelyto be even more. The yearly profit has been shown separately in the RevenueAccounts as "Profit from Transit." According to existing agreements, thisprofit is to be passed on to the refineries. A resume of the provisions inthe transport agreements is given in Annex 11.

1/ At the end of November 1974, the average price increase of the steelscited in the agreements was 34% over the base price of November 1973.

- 20 -

C. Cash Flow

5.04 The Cash Flow (Annex 10) shows that the surplus funds available toNafto,cd increase from Din. 2.3 million (US$0.13 million) in 1978 to Din.214.8 million (US$12.6 million) in 1988. The initial working capital willbe provided by the Founders.

D. Audit

5.05 The annual financial statements of Naftovod will be checked by theSocial Acrounting Service (SAS), a separate statutory organization responsiblefor such work (para. 3, Annex 6). The staff of SAE; is being trained to enableit to carry out audits in accordance with standards, acceptable to the Bank(para. 5, Annex 6) and it is expected that staff will be suitably trained by1979. The Bank has Naftovod's agreement to have its annual financial state-ments audited in a manner acceptable to the Bank anid to submit them withinsix months of the end of each year.

E. Special Debt Service Guarantees

5.06 The foreign offtakers have signed transport agreements with Nafto-vod containing take or pay clauses which provide that the offtakers will payNaftovod 80% of the tariff for any amount of allocated capacity not utilizedby them; likewise Naftovod will pay the offtakers 80% of the tariff for anyagreed amount of oil that it fails to deliver. The take or pay clause isvoided by events of force majeure. Naftovod and the Founders have signeda sf,ilar agreement except that only events of force majeure lasting morethan six months would void the take or pay commitment.

5.07 A total shutdown of the pipeline for periods exceeding a few daysis extremely unlikely and as mentioned in para. 5.02, Naftovod is expected toearn sufficient revenue to cover all expenditures. A severe fire or an ex-tensive landslide could shut down the pipeline for 2 to 3 months and the six-months clause mentioned in para. 5.06 could pose a financial threat to Nafto-vod, because, in such an event, it would not only lose its revenue from allseven offtakers, thus causing it tc be unable to meet debt service, but itwould also have to pay t. the local refineries an amount that would approachits lost revenues. The same situation would arise if project completion weredelayed or if unusual problems were to be met during commissioning and _tiartup of facilities. Naftovod has obtained guarantees from the local banks tomeet these financial commitments in case of need, other than the debt serviceobligations with regard to the Bank loan, which is; guaranteed by the FederalGovernment. In the event of a shutdown of the pipeline for a short period,the estimated operating surplus available at the end of the year would be.-ore than sufficient to cover the annual debt service of the Bank loar.

- 21 -

VI. ECONOMIC EVALUATION

A. General

6.01 According to recent projections for energy supply and demand inYugoslavia, it is expected that internal demand for hydrocarbons (oil and gas)will increase from 13 million Toe in 1974 to about 40 million Toe in 1990.A large part of the incremental demand will have to be imported from easternEurope, North Africa and the Middle East, and transported from the ports ofentry to the main oil processing and gas consumption centers. While there ispresently no economic alternative to pipelines for overland transport of gas,oil can be transported by a variety of means (road and rail tankers, barges,pipelines). Therefore, the economic feasibility of the proposed crude oilpipeline system was evaluated by comparing the cost of transporting oilthrough the pipeline with the cost of conventional transport.

B. Demand Projections

6.02 Annex 1 gives details of future energy supply and demand. Demandprojections used to size the project were derived from studies sponsored byFCEI after the oil crisis of 1973-1974 and are considered reasonable. Theyare lower than pre-crisis projections and reflect efforts being made undergovernment coordination to conserve energy and to substitute domestic fuels(mostly coal) for expensive foreign oil. Current energy demand projectionsfor Yuigoslavia are 15% and 18% lower than pre-crisis projections in 1980 and1985 respectively. This is comparable with the expected decrease in totalenergy demand in the European Economic Community (EEC) for the same period,according to a recent study 1/ by the Organization for Economic Cooperationand Development (OECD). However, the increase in demand for hydrocarbonswould be larger in Yugoslavia (3.0 times between 1972 and 1985) than it wouldbe in the EEC (1.8 times). This is due mainly to the limited scope forenergy conservation in a country which has low per capita consumption and lowquality coal, which in most instances cannot now be substituted economicallyfor hydrocarbons. 2/ However, the sensitivity of the feasiblity of the pro-posed project was tested against lower demand figures (para. 6.08).

6.03 Since domestic production is not expected to increase substantially,(para. 2.19) net oil imports in Yugoslavia should increase from 8.7 million

1/ Energy Prospects to 1985, OECD Paris 1974.

2/ Coal gasification and liquefaction on a commercial scale in Yugoslaviaare not expected to occur before 1985 to 1990 and would, therefore, notthreaten the viability of the project.

- 22 -

tons in 1975 to 11.7 million tons in 1978, the first year of operation of theproposed pipeline and to about 20 and 28 million tons in 1985 and 1990 re-spectively. These figures do not account for any substantial discovery of oilin Yugoslavia or off-shore; if commercial discoveries should take place, thenew fields could be connected to the pipeline which crosses the main potentialareas (Map 2) and the flow of oil could even be reversed in some sections ofthe pipeline. A discovery off shore would imply that oil would be lifted bytanker from the drilling site and unloaded at the Omisalj terminal in much thesame fashion as imported oil. It is therefore not expected that new domesticdiscoveries would threaten the economic feasibility of the pipeline.

C. Size of the Proposed Facilities

6.04 The pipeline system and the terminal facilities were sized to handleabout 34 million tons of oil annually by 1990 (24 million tons for the Yugoslavinternal market and 10 million tons in transit for Hungary and Czechoslovakia).Naftovod used computer simulation models to optimize the size of the pipelineand tanker terminal. The methodology used was satisfactory and led to reduc-tion in the diameter of the Sisak-Slobodnica section of the line and in tank-age capacity. Naftovod, however, has decided to maintain the diameter of thefirst section (Omisalj-Sisak) at 36" for which the study shows the optimumsize to be 34". The main reason behind this decision is that transit trafficmight increase in the future (discussions have talcen place with Austria), andthat it would be difficult to increase the capacity of the first section ofthe line to satisfy additional transit requirements, since it crosses diffi-cult mountainous terrain. In the light of the comparatively small differencein initial investment costs (less than US$3 million, i.e. 0.75% of the totalproject cost) this decision is acceptable. The project was compared withother pipeline alternatives, in particular to one linking the port of.Plocewith the inland refineries, and was found to be the least cost solution.

D. Alternatives to the Proposed System

6.05 Since most oil imports are expected to come from the Middle Eastand North Africa, the next best alternative to the pipeline system is a com-bination of rail and inland water transport. Such an alternative would re-quire substantial investments in ports and railway facilities and the acqui-sition of railroad tank cars and barges. Since it would require frequentcrude oil transfers from one mode to another, it would increase the risk ofpollution, particularly in the main waterways. Estimates prepared by Nafto-vod, with the assistance of consultants, show that total investments of aboutUS$300 million would be required to expand existing and create new port andrailway facilities at Koper, Bakar, Bar, Pancevo, Novi Sad, Bosanski-Brod,Sisak and Lendava. In addition, the transport of 34 million tons of oilwould require the acquisition of some 12,500 rail tank cars and 750 locomo-tives and of barges and pusher tugs at a cost estimated at about US$460million.

- 23 -

E. Project Benefits

6.06 The total project cost, including the cost of expansion to ultimatecapacity, is estimated at Din. 5,940 million (US$350 million) excluding taxes,customs duties, interest during construction, and price contingencies. Noadjustment was made for shadow labor costs or rate of exchange. The value ofthe land used by the pipeline proper was not included, since it will be re-stored to its normal use after construction; however, project costs includecompensation for crop and property damage along the pipeline and land valuesfor pump stations and tank farms.

6.07 The comparison of the project cost and of the next best alternativeshows that the rate of discount which equalizes both cost streams over 20years is 50%. This high rate indicates that the facilities should have beenbuilt sooner. Assumptions and details of the calculation are in Annex 12.

F. Sensitivity to Changes in Traffic Growth

6.08 If oil import demand should be lower so that the traffic in 1990 isonly 85% of the projections (a conservative assumption), the pipeline wouldstill be the least cost solution for the transport of oil, and the rate ofdiscount which equalizes both cost streams over 20 years being in excess of43%.

G. Beneficiaries and Employment

6.09 The benefits derived from the project would be savings in transporta-tion costs which are estimated at slightly over 1% of the average sales priceof oil products because oil is an expensive commodity. These marginal savingscan be passed on to the consumer without significantly increasing demand, thusthe beneficiary would be the public at large.

6.10 During construction, the pipeline will provide employment to some2,000 persons while during operations some 350 staff will be employed. Theincrease in the transport of oil products and other cargo resulting from nor-mal growth of the economy will, in a short time, make up any temporary slackcreated by the pipeline in the railways and the few local waterways carriersinvolved (paras. 6.11 and 6.12).

- 24 -

H. Impact on Alternative Means of Transport

6.11 The present requirement of about 12 million tons of crude oil perannum "or all the refineries in Yugoslavia is transported from overseas bytank'.ers and by rail and barges inside Yugoslavia. About 4 million tons arereceaivd in Rijeka by tankers for the Rijeka refinery. Of the remaining8 million tons, about 5.4 million tons are transported by rail from otherports in the Adriatic and from domestic oil fields and the remainder, about2.6 million tons, by barges on the Sava and Danube Rivers.

5,12 The construction of the pipeline will divert crude oil traffic fromthe railways and barges. However, this should not be a problem because railand river traffic is already congested. Since most of the oil moving in theInland waterways is transported in barges of foreign flags the impact of thisdiversion on the local carriers will be minimal. Many of the railway wagonsare fairly old and not likely to be in use very long, while others are onhire from foreign countries and can be returned when no longer required.Although oil and oil products account for only 7% of total rail traffic, therailway authorities are aware of the pipeline project and have taken it into-ccount in their projections of future rail traffic and investment programs.Because of the increase in the anticipated consumption of oil products inthe country, the railways and local water transport enterprises will profitfrom the increased transport of refined products.

VII. AGREEMENTS REACHED AND RECOMMENDATIONS

7.01 Agreement has been reached on the main :issues referred to in thepreceding chapters and more particularly on cost overruns (para. 4.12), proj-ect schedule (para. 4.17) and Debt Service Guarantee (para. 5.07). Subject tothe conditions of effectiveness referred to in paras. 4.10 and 4.12, the pro-posed project is suitable for a Bank loan of US$49 million to Naftovod for aterm of 18 years including four years of grace corresponding to the period ofconstruction.

ANNEX 1Page 1

APPRAISAL OF

THE YUGOSLAVIA OIL PIPELINE(Jugoslavenski Naftovod)

The Energy Sector in Yugoslavia

A. Background

1. The main part of Yugoslav proven energy reserves consists of low-grade coal (brown coal and lignite) located in Kosovo and Serbia, and of asizeable hydro power potential in Croatia, Bosnia-Herzegovina and Serbia.Known hydrocarbon reserves (oil and natural gas) located mainly in Serbiaand Croatia are relatively small. Other potential sources exist (nuclear,geothermal and oil shales) but have not yet been investigated in sufficientdetail to be evaluated accurately. A description of the reserves is givenin Table 1, and their location is shown on Map 2.

Coal

2. Coal reserves amount to about 4,000 million tons of oil equivalent(Toe) or about 260 years at average 1975-90 consumption. The largest partof the reserves (83%) consists of coal with an average heating value of about1,900 kcal/kg (7,520 Btu/kg) and high water and ash contents. The size andlocation of the deposits makes them suitable for open pit, mining each with anaverage annual production of about 12 to 15 million tons (2.50 to 3.00 mil-lion Toe). Brown coal reserves account for about 15% of total coal reserves;individual deposits are generally small and scattered and most of them arenot suitable for open pit mining because of the depth of the layer (150 to 500m). The average calorific value of Brown coal is about 3,500 kcal/kg (13,860Btu/kg). Hard coal accounts for 2% of the total coal reserves. MIost depo-sits have highly complex features and steeply dipping strata; the layers arethin and irregular and normally occur at considerable depth, limiting theuse of modern mechanical equipment. The use of domestically produced housecoal is limited because of its high sulphur content (1 to 9%); the averagecalorific value is about 6,420 kcal/kg (25,400 Btu/kg).

Hydroelectricity

4. Total economicallv exploitable hydropower generation potential inYugoslavia is evaluated at about 60,000 million kWh p.a. At the end of 1973only 30% of this potential was developed with an average production capabilityof 18,000 million kWh. The underdeveloped potential is spread rather evenlyover the country. While it is recognized that further development would bejustified, this has been delayed by lack of appropriate resources and admin-istrative considerations.

PaNNEX 1Page 2

Hydrocarbons

5. Total proven recoverable oil and natural gas reserves are estimatedat about 100 million Toe and they account for 2.5% of total Yugoslav energyreserves (about 16 years and 13 years at average 197j-19 90 oil and gasconsumption respectively). Known reserves evaluated at -15 million Toe arelocated in the Pannonian Basin (north and northeastern part of Yugoslavia)and are producing an average of 3 million tons of oil and 1,000 million m3 ofgas annually. Exploration has recently started in the Dinaric Basin offshorethe Adriatic coast where potential oil and gas-bearing structures exist. Sofar three gas-producing wells have been drilled but no commercial exploita-tion has started. Probable recoverable reserves in the Dinaric Basin areestimated at 200 million tons of oil and 37 million Toe of natural gas.

6. Local production of oil, supplemented by irports (para. 12) isprocessed in six refineries (Rijeka, Sisak, Bosanski-Brod, Pancevo, NoviSad and Lendava) with a total annual refining capacity of about 12 milliontons (Map 1).

Nuclear Fuel and Other Non-Conventional Fuels

7. Potential uranium bearing areas cover some 170,000 km2 of which65,000 km2 have been explored. Preliminary estimates show that some 36,500tons of uranium concentrate (U308) could be recovered. Further investigationsare being carried out to refine these estimates and to prepare the develop-ment of the most promising deposits which are in Slovenia.

B. Past Supply and Demand for Energy

8. Per capita consumption in Yugoslavia is 15% below the world averageand about 40% of the West European average. There are, however, considerablevariations in the level of consumption among the various Republics and Prov-inces. The highest levels are reached in Croatia and Serbia which are fairlydeveloped, and the lowest in elontenegro and Kosovo. From 1965 to 1973 annualper capita consumption grew from about 8.5 million keal to 12.6 million kcal,an average rate of 5% p.a.

9. Until the mid-sixties coal had been the predom½-nant fuel and Yugos-lavia was almost self-sufficient in energy except in oil production, whichhad to be supplemented by imports. After a period of relative stagnationfollowing the economic reforms of 1965, overall energy consumption increasedrapidly from 1967 to 1973 at a rate of 8.2% p.a. compared with an averageGDP increase of 6.4% per year. During the same period the structure of con-sumption changed considerably and coal was surpassed by hydrocarbons, prin-cipally oil. The share of hydroelectricity stayed almost constant while theuse of natural gas remained marginal. This was due mainly to the rapiddevelopment of modern industrial sectors (31% of GDP) based on heavy industry

ANTNEX 1

Page 3

(mining and metallurgy) which are energy-intensive and require high-gradecoal or liquid fuels, and to the rapid growth of road transport (Table 2 and3).

10. Most of the coal is used near the mining site, mostly in power andsteam generation which account for 70% and 30% of the total consumptionrespectively. The relatively small volumes of hard coal produced locally areused in the residential sector and by light industry. Coking coal for ironand steel industry is imported. 'In 1973 total coal consumption accounted for39.5% of the total internal demand compared to 64.3 in 1965.

11. About 84% of the demand for oil products is accounted for by thetransportation and industrial sector, the remainder being divided betweenagriculture (6%) and residential and commercial usage (10%). At present,demand for petrochemicals is low but is expected to grow in the future asfeedstock requirements for fertilizers and plastics increase. The use offuel oil for power generation has traditionally been limited; in 1973 thefirst oil-fired plant was commissioned, while four more were under construc-tion. Following the oil crisis, steps were taken to restrict further construc-tion of such plants (paras. 25 and 26).

CONSUMPTION OF MAIN REFINED PRODUCTS BY SECTOR IN 1973/1(000 Tons)

Gasoline Diesel Oil Fuel Oil Total % of Total

Agriculture 30 350 100 480 5.6Transportation 1,350 1,700 520 3,570 41.8Industry 315 520 2,280 3,115 36.3Power Generation 10 150 380 540 -6.3Others 35 500 320 855 10.0

Total 1,740 3,220 3,600 8,560 100.0

/1 Source: Federal Chamber of Economy_ excludes kerosene and aviation andbunker fuels.