Applying Long-Term Thinking in a Short-Term Market · Applying Long-Term Thinking in a Short-Term...

6

Applying Long-Term Thinking in a Short-Term Market UPDATE As part of the Pitcairn Family Wealth & Investment Forum, Chief Investment Officer Rick Pitcairn moderated an investment roundtable of leading financial thinkers. Rick offered Pitcairn’s perspectives on the current market environment and reflected on themes for the coming decade. He then introduced the Investment Roundtable speakers for a whirlwind tour of global politics and a closer look at our own country with insight into Federal Reserve policy, the US economy, and the equity markets. For the last few years, equities have given people plenty of excuses to get out of the market. But if you know me, you know my philosophy is that people should stay in the market. That recommendation has not changed despite recent choppiness. I believe investors will always be rewarded for maintaining a long-term view in the face of short-term volatility. For Pitcairn clients, it may seem that our investment portfolios are static because at the highest levels, allocation strategy doesn’t often change. At the tactical level, however, adjustments are common. For example, in the third quarter, a commodities manager shifted from active holdings to cash, thereby beating the benchmark, and an international manager sold holdings in China, avoiding some of the poor performance in that market. As Pitcairn CIO, I lead a team that is responsible for many tasks, most of which fall under three categories: 1. Macro-economic assessment. It’s important to have accurate forecasts for macro-economic developments so we make effective allocations. Studies show that asset allocation is the most significant driver of a portfolio’s total return. the market. Compared to today, there wasn’t much to watch – US common stocks and US bonds were all that was available to most investors. Few mutual funds, no international investing, no hedge funds, and just a smattering of private equity for a privileged few. Since then, investment vehicles and structures have evolved dramatically and continue to do so. Our team knows how important it is to educate ourselves on the available tools. We focus significant effort on evaluating new structures to determine whether they would benefit your portfolio and how they may affect broader market performance. Examples of concepts currently on our radar are exchange- traded funds, developments in alternative investing, and impact investing, which aims to deliver market-comparable returns while achieving a social or philanthropic mission. Take for example, exchange-traded funds. Their impact on stock performance during the August turmoil underlines why it is critical for us to understand how they affect market dynamics and how can we use these pools of risk and return to achieve desired results in your portfolio. We are constantly evaluating new structures, new investment ideas, and new managers to be sure we are putting the best opportunities to work for you. Turning to the global investment environment, our bumpy summer raised 2. Manager selection. Our job is to identify the best investment managers in the world in each asset class. Over the last few years, market performance has spurred debate about whether active investing adds value over passive investing. We believe the interplay between active and passive is cyclical and that a smart combination of the two is the right approach. (See Chart A: Active Passive Interplay Is Cyclical.) 3. Construct investment solutions. In 1972, when I was a 12 year-old in Texas, I convinced my parents, teachers, and the local Merrill Lynch office to let me skip a week of school and watch

Transcript of Applying Long-Term Thinking in a Short-Term Market · Applying Long-Term Thinking in a Short-Term...

Applying Long-Term Thinking in a Short-Term Market

update As part of the Pitcairn Family Wealth & Investment Forum, Chief Investment Officer Rick Pitcairn moderated an investment roundtable of leading financial thinkers. Rick offered Pitcairn’s perspectives on the current market environment and reflected on themes for the coming decade. He then introduced the Investment Roundtable speakers for a whirlwind tour of global politics and a closer look at our own country with insight into Federal Reserve policy, the US economy, and the equity markets.

For the last few years, equities have given people plenty of excuses to get out of the market. But if you know me, you know my philosophy is that people should stay in the market. That recommendation has not changed despite recent choppiness. I believe investors will always be rewarded for maintaining a long-term view in the face of short-term volatility.

For Pitcairn clients, it may seem that our investment portfolios are static because at the highest levels, allocation strategy doesn’t often change. At the tactical level, however, adjustments are common. For example, in the third quarter, a commodities manager shifted from active holdings to cash, thereby beating the benchmark, and an international manager sold holdings in China, avoiding some of the poor performance in that market.

As Pitcairn CIO, I lead a team that is responsible for many tasks, most of which fall under three categories:

1. Macro-economic assessment. It’s important to have accurate forecasts for macro-economic developments so we make effective allocations. Studies show that asset allocation is the most significant driver of a portfolio’s total return.

the market. Compared to today, there wasn’t much to watch – US common stocks and US bonds were all that was available to most investors. Few mutual funds, no international investing, no hedge funds, and just a smattering of private equity for a privileged few. Since then, investment vehicles and structures have evolved dramatically and continue to do so. Our team knows how important it is to educate ourselves on the available tools.

We focus significant effort on evaluating new structures to determine whether they would benefit your portfolio and how they may affect broader market performance. Examples of concepts currently on our radar are exchange-traded funds, developments in alternative investing, and impact investing, which aims to deliver market-comparable returns while achieving a social or philanthropic mission. Take for example, exchange-traded funds. Their impact on stock performance during the August turmoil underlines why it is critical for us to understand how they affect market dynamics and how can we use these pools of risk and return to achieve desired results in your portfolio. We are constantly evaluating new structures, new investment ideas, and new managers to be sure we are putting the best opportunities to work for you.

Turning to the global investment environment, our bumpy summer raised

2. Manager selection. Our job is to identify the best investment managers in the world in each asset class. Over the last few years, market performance has spurred debate about whether active investing adds value over passive investing. We believe the interplay between active and passive is cyclical and that a smart combination of the two is the right approach. (See Chart A: Active Passive Interplay Is Cyclical.)

3. Construct investment solutions. In 1972, when I was a 12 year-old in Texas, I convinced my parents, teachers, and the local Merrill Lynch office to let me skip a week of school and watch

Any other time, people would be near the doors, ready to get out. But this market has been slowly evolving and though many people thought they could outsmart the market over the last seven years, those who took a long-term strategic mindset are the ones who did well.

We encourage all Pitcairn families to measure success in the capital markets over years and decades, not weeks and quarters. Over the last 10 years, a pervasive fear kept many people out of equities at the same time that central banks engineered a period of extraordinary capital market resilience. I can guarantee the next 10 years will not be a repeat of the last 10, and I am also sure there will be abundant opportunities. Our job is to anticipate key themes of the next 10 years. Ideas at the forefront of our thinking include:

1. Technological innovation. At a recent Wigmore Association meeting in Silicon Valley, we were awed by the level of innovation. Many companies are quite literally changing the world with things like nanotechnology, robotics, DNA mapping, and biomedical engineering.

2. Global interconnectedness. Innovation plays out in global relationships, fostering commerce across borders, which is why we continue to recommend global portfolios for all our families.

3. The rise of global consumers. Interconnectedness has in turn given

some legitimate questions – Are we nearing the end of the road for this bull market? Will weaker performance be temporary or prolonged? In August, we wrote that we thought markets would come back in the fall and they did, even more quickly than we expected. However, the underlying question looms, when does this bull market end?

As investment thinkers, we at Pitcairn pride ourselves on applying long-term thought in a short-term world. Since we have been persistently bullish over the last few years, it’s important to ask ourselves, what would change our minds? Three developments that would make us more cautious are:

1. Euphoria at the average investor level. Euphoria like the 1960s or 1990s would raise concerns for us, but markets are still characterized more by fear than confidence.

2. Excessive valuations. People argue whether valuations are stretched too high or still seem fair, but compared to long-term historical averages, valuations don’t seem excessive to us.

3. Onset of a recession. Of the three, this is the one we are currently most alert to, but at this time, we do not see the kind of environment that would lead the US or the world into a recession.

This economic cycle has been a long one, seven years without a slowdown.

rise to the global consumer, which will be tremendously positive for capitalism and should overshadow concerns about short-term cycles of China and other individual countries.

4. Rising interest rates. As the Fed shifts its monetary policy, missteps are possible. We believe the best positioning for that environment is a diverse, strategic portfolio.

There’s an old saying that you don’t really have a diverse portfolio if there’s not something in there that you currently hate. In 2011, having a diverse portfolio felt great because everything went up. In 2015, a diverse portfolio is still the right strategy; it just doesn’t feel good because some things aren’t performing as well. But even when a diverse portfolio doesn’t feel great, it’s doing its job of moving you toward your long-term goals.

Though the world is changing very quickly, our investment portfolios have remained stable at the allocation level because we believe that what has worked for the last three to four years will probably work for the next three to four years. Pitcairn has been ahead of the curve and you can rest assured that we are committed to staying ahead of the curve even as both tools and opportunities change.

Active Management Winning

Active Opportunity Building

ActiveOutperforming

PassiveOutperforming

Post-TMT Bubble

Post-Banking CrisisPost-Safety Bubble

S&P

500

Rank

100

75

50

25

01997 2003 2009 20141985 1991

Source: Bernstein, Data as of 12/31/2014.

Chart A: Active Passive Interplay Is Cyclical Harold F. “Rick” Pitcairn, II, CFA is Chief Investment Officer of Pitcairn. One of the chief architects behind Pitcairn’s open architecture investment

platform, he is a leading authority on the use of tax overlay and Unified Managed Accounts (UMA) in trust structures and for the ultra high net worth investor. In addition, Rick is a founding member and past chairman of the Wigmore Association, a global collaboration of chief investment officers from eight family offices from across North America, Europe, Australia, and South America. Rick is a frequent speaker and author on investment topics including long-term investing for families, due diligence, tax overlay, and global asset allocation.

P©2016 Pitcairn

We live in a volatile world. If you have any doubt of that, consider the events we have witnessed since 2008: severe global recession, doubts about the European Union’s survival, a wave of unrest in North Africa and the Middle East, Syrian civil war, a global refugee crisis, the rise of ISIS, Russia and Ukraine at war, and oil at $40 a barrel. If I had predicted these things in 2008, no one would have believed me. I wouldn’t have believed it either.

This litany of global crises is not a doomsday scenario, but a sign of how quickly things change. We are transitioning from a world that was politically, culturally, and economically dominated by the US toward a world that is still undefined. I don’t believe the US is in decline. Our economy continues to change the game, particularly in energy markets. However, our global influence is lessening. Why? Because emerging powers now have a much greater say about what goes on in their regions.

Let’s take a quick trip around the globe, focusing on countries and events that may shape 2016.

Europe

• We see low probability of a hard economic landing, but it may take time for the region’s economy to recover. Potential obstacles include the possibility – however unlikely – that Greece or the UK will withdraw from the European Union, security issues as highlighted by recent terrorist attacks, and Russia pressuring Europe at the margins.

• Open borders are good for Europe’s economy, but if temporary border limits stemming from the refugee situation become more permanent, that would hamper economic recovery.

• German chancellor Angela Merkel, Europe’s most important and most popular leader, has played a role in solving many problems. If her

welcome for hundreds of thousands of migrants puts her in a weaker political position, that would affect our outlook for Europe.

Middle East

• Rivalry between Iran and Saudi Arabia has long defined the Middle East’s political and economic stability. A power shift is now underway due to Iran’s international sanctions ending and Saudi Arabia becoming more isolated.

• In the past, the Saudis have managed the Iran conflict by keeping oil prices high enough to ensure stability, but not high enough to help Iran. However, Saudi Arabia now has less influence over oil prices due to North American production.

Russia. That’s also why he went into Syria. If Russia can help stabilize Syria, Europe will likely ease sanctions.

• In general, we expect Russia to play a less noisy role in international politics in the coming year because there aren’t as many opportunities for Mr. Putin to intervene, though he will never ignore what he sees as provocations.

China

• Despite its size, China’s economy is still immature, developing, and volatile. Currently, China’s government is trying to shift its economic model from export-driven to consumer-driven growth, which means transferring wealth from powerful people in the state sector to individual consumers.

Investment Roundtable from left to right: Willis Sparks, Rick Pitcairn, Dorothy Weaver, and Nick Bohnsack.

• ISIS is not a threat to oil because it does not control Iraq’s oil producing region.

• Our forecast is for oil prices to stay pretty much where they are now for the next 6-12 months.

Russia

• Vladimir Putin has been a wild card. However, low oil prices are bad for Russia and the country’s worsening economic conditions may force him to become more cautious.

• Currently, Mr. Putin is keeping Ukraine out of the headlines as he tries to get Europe to drop its sanctions against

• Evidence suggests President Xi Jinping is fully in charge and that China’s vulnerability to an economic hard landing is overstated. We don’t take China’s economic statistics at face value, but we believe its own leaders know the real results and are moving forward with reform.

• Due to investment in foreign infrastructure, China’s commodity demand won’t fall through the floor, a consolation for its commodity-dependent trading partners.

• We think the risk of a major crisis is small at this time. However, we

Around the World with Willis Sparks

Willis Sparks is director of global macro at Eurasia Group. Mr. Sparks focuses on global political risks as well as US politics and elections, and regularly

gives speeches on market-moving trends in international politics.

expect more events like August where something happening in China sets off a round of jitters in the capital markets.

US

• It’s unlikely the next president will change much from President Obama’s Middle East strategy. There are no clear solutions for the complicated issues, the situation is not affecting oil prices, and there is no public support or a clear objective for US involvement in Syria.

As you would expect, I am frequently asked about the Federal Reserve’s plans for interest rates. The reality is that when the Fed raises rates and by how much probably doesn’t make that much difference. (Note: the Federal Reserve raised the Fed funds rate 0.25% in December.) It matters because people think it’s important. In terms of the long anticipated shift in Fed policy, we need to remember that the strength of the Fed is the message. The market wants to feel the Fed is in control.

Before its September meeting, I thought the Fed should just end the suspense and raise the Fed funds rate. Instead the Fed considered the environment at the time – China throwing global markets into turmoil and the US Congress continuing its dysfunction – and tried to send a message that there was still an adult in the room and everyone should just take a breath. The Fed was shocked that its message caused markets to hyperventilate. Markets have always watched the Fed, but now the Fed is watching the markets, which is not its mandate and certainly complicates its decision making.

After the Fed held steady in September, some very strong economic data allayed

fears that the Fed would miss its window to raise interest rates in December. Most notably, average payroll rose 2.5%. The Fed was looking for a payroll increase, with its corresponding impact on inflation, because the Fed is most worried about deflation, something it has no tools to fight. Though inflation can be painful, the Fed has tools to manage it.

The massive liquidity pumped into the system here and abroad since the 2008 financial crisis has taken money from the elderly, the savers, and the responsible people doing what they are supposed to do and added to the balance sheets of banks that aren’t lending. Starved for return, people have been pushed out on the risk spectrum – accepting lower credit quality or longer durations and still getting paid very little. Many people don’t realize how risky their fixed income allocation has become. It’s a mathematical fact that if interest rates go up, bond prices will go down.

The past several years have not been a good environment for active managers or hedge fund managers as most investments moved in lock step – the good, the bad, and the ugly. That appears to be changing.

What Can We Expect from the Federal Reserve?

Dorothy Weaver is Chair and CEO of Collins Capital. As former chair of the Federal Reserve Bank of Miami, Ms.Weaver has useful insight into the inner workings of the Federal Reserve.

It looks like we are entering a period more favorable to active investing and alternative investing. Some companies are going to benefit from low oil prices and some are going to be crushed. Some countries will be winners and others will be scrambling. Doing your homework – on both the credit side and the equity side – is going to matter again.

My recommendation is not to fixate on Federal Reserve policy. Broaden your thinking to consider opportunities related to liquidity and global interconnectedness. We are not seeing pricing power or topline revenue growth in most of corporate America. As we enter 2016, it will be increasingly important to identify active managers and alternative managers who can identify the winners and the losers and can navigate and even benefit from a much more volatile environment.

• The next president will likely focus on Asia, particularly relations with China, and on a trade agreement with Europe.

Equities have proven resilient despite geopolitical volatility, and we think they will remain resilient. We do think it is more important than ever to understand which countries are better governed and more resilient than others, and that diversification is needed in your portfolio to ride through volatile times. P

P©2016 Pitcairn

©2016 Pitcairn

Nicholas Bohnsack is founding Partner and Head of Quantitative Research at Strategas. He directs Strategas’ equity sector strategy and global asset allocation research.

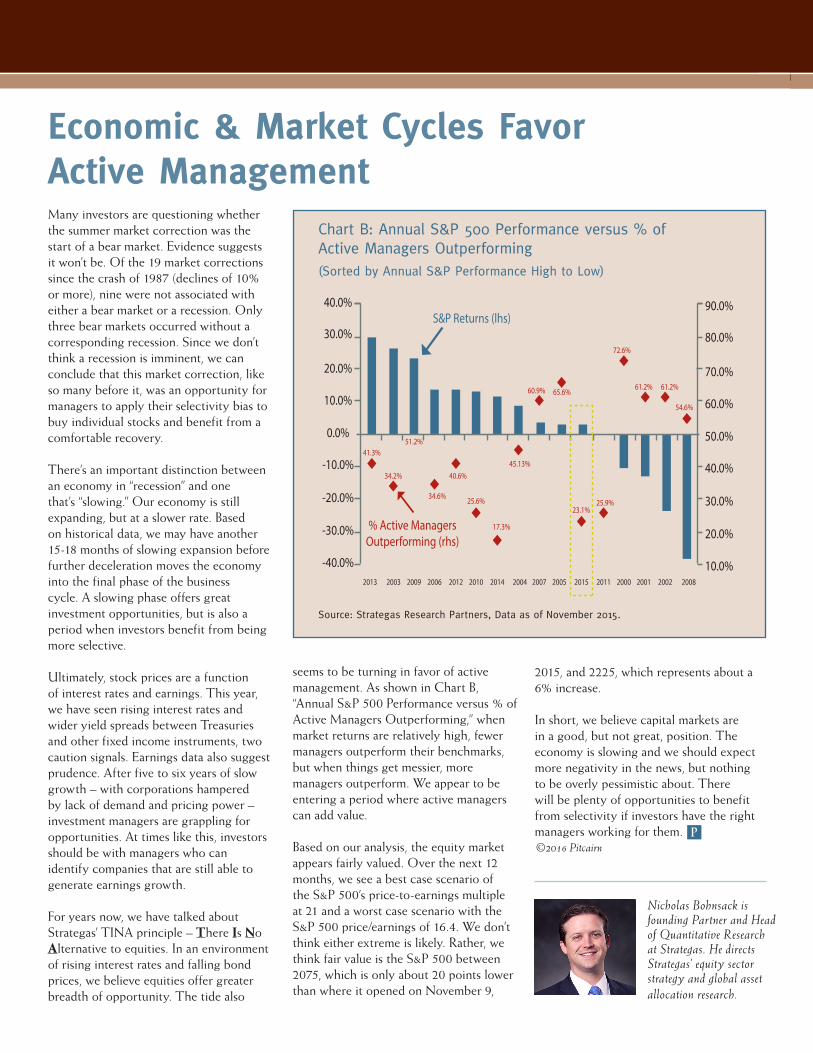

Many investors are questioning whether the summer market correction was the start of a bear market. Evidence suggests it won’t be. Of the 19 market corrections since the crash of 1987 (declines of 10% or more), nine were not associated with either a bear market or a recession. Only three bear markets occurred without a corresponding recession. Since we don’t think a recession is imminent, we can conclude that this market correction, like so many before it, was an opportunity for managers to apply their selectivity bias to buy individual stocks and benefit from a comfortable recovery.

There’s an important distinction between an economy in “recession” and one that’s “slowing.” Our economy is still expanding, but at a slower rate. Based on historical data, we may have another 15-18 months of slowing expansion before further deceleration moves the economy into the final phase of the business cycle. A slowing phase offers great investment opportunities, but is also a period when investors benefit from being more selective.

Ultimately, stock prices are a function of interest rates and earnings. This year, we have seen rising interest rates and wider yield spreads between Treasuries and other fixed income instruments, two caution signals. Earnings data also suggest prudence. After five to six years of slow growth – with corporations hampered by lack of demand and pricing power – investment managers are grappling for opportunities. At times like this, investors should be with managers who can identify companies that are still able to generate earnings growth.

For years now, we have talked about Strategas’ TINA principle – There Is No Alternative to equities. In an environment of rising interest rates and falling bond prices, we believe equities offer greater breadth of opportunity. The tide also

seems to be turning in favor of active management. As shown in Chart B, “Annual S&P 500 Performance versus % of Active Managers Outperforming,” when market returns are relatively high, fewer managers outperform their benchmarks, but when things get messier, more managers outperform. We appear to be entering a period where active managers can add value.

Based on our analysis, the equity market appears fairly valued. Over the next 12 months, we see a best case scenario of the S&P 500’s price-to-earnings multiple at 21 and a worst case scenario with the S&P 500 price/earnings of 16.4. We don’t think either extreme is likely. Rather, we think fair value is the S&P 500 between 2075, which is only about 20 points lower than where it opened on November 9,

Economic & Market Cycles Favor Active Management

Source: Strategas Research Partners, Data as of November 2015.

Chart B: Annual S&P 500 Performance versus % of Active Managers Outperforming (Sorted by Annual S&P Performance High to Low)

90.0%

80.0%

70.0%

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

40.0%

30.0%

20.0%

10.0%

0.0%

-10.0%

-20.0%

-30.0%

-40.0%2013 2003 2009 2006 2012 2010 2014 2004 2007 2005 2015 2011 2000 2001 2002 2008

41.3%51.2%

34.2%

34.6%

40.6%

25.6%

17.3%

45.13%

60.9% 65.6%

72.6%

61.2% 61.2%

54.6%

25.9%23.1%

% Active ManagersOutperforming (rhs)

S&P Returns (lhs)

©2016 PitcairnP

2015, and 2225, which represents about a 6% increase.

In short, we believe capital markets are in a good, but not great, position. The economy is slowing and we should expect more negativity in the news, but nothing to be overly pessimistic about. There will be plenty of opportunities to benefit from selectivity if investors have the right managers working for them.

Pitcairn Update is a publication prepared by Pitcairn for the exclusive use of its clients. The information provided should not be construed as imparting legal, tax, or financial advice on any specific matter. For more information, please call us at 1-800-211-1745 or visit us on the web at www.pitcairn.com.

One Pitcairn Place Suite 3000 165 Township Line Road Jenkintown, PA 19046-3593

Representative Office99 Park AvenueSuite 320New York, NY10016-1501

Tysons IISuite 2201750 Tysons BoulevardMcLean, VA 22102-4228

About PitcairnPitcairn is one of the world’s leading family offices. We are dedicated to helping families sustain and grow their substantial, often complex financial assets and supporting the unique heritage of our clients across multiple generations. Pitcairn works with families and single family offices filling one need or providing comprehensive solutions. Since our founding as a family office in 1923, we have successfully transitioned wealth across generations of families through a combination of effective planning, strong investment results, thoughtful governance, and a commitment to education. Headquartered in Philadelphia, Pitcairn also has offices in New York and Washington, DC as well as a network of resources around the world. You can learn more about our family office services as well as find additional articles, news, and events on our website at www.pitcairn.com.