Antares presentation -_january_2014

22

32 nd Annual J.P. Morgan Healthcare Conference January 16, 2014 Paul K. Wotton, Ph.D. President and Chief Executive Officer NASDAQ:ATRS Paul

Transcript of Antares presentation -_january_2014

32nd Annual J.P. Morgan Healthcare Conference January 16, 2014

Paul K. Wotton, Ph.D.

President and Chief Executive Officer

NASDAQ:ATRS

Paul

This presentation may contain forward-looking statements which are made pursuant to the safe harbor provisions of Section 21E of the Securities Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995. Investors are cautioned that statements which are not strictly historical statements, including, without limitation, statements regarding the plans, objectives and future financial performance of Antares Pharma, constitute forward-looking statements which involve risks and uncertainties. The Company’s actual results may differ materially from those anticipated in these forward-looking statements based upon a number of factors, including anticipated operating losses, uncertainties associated with research, development, testing and related regulatory approvals, unproven markets, future capital needs and uncertainty of additional financing, competition, uncertainties associated with intellectual property, complex manufacturing, high quality requirements, dependence on third-party manufacturers, suppliers and collaborators, lack of sales and marketing experience, loss of key personnel, uncertainties associated with market acceptance and adequacy of reimbursement, technological change, and government regulation. For a more detailed description of the risk factors associated with the Company, please refer to the Company’s periodic reports filed with the U.S. Securities and Exchange Commission from time to time, including its Annual Report on Form 10-K for the year ended December 31, 2012. Undue reliance should not be placed on any forward-looking statements, which speak only as of the date of this presentation. The Company undertakes no obligation to update any forward-looking information contained in this presentation.

Safe Harbor Statement

2

Overview of Q313 and Recent Events

3

RESEARCH AND DEVELOPMENT

• Received approval from the U.S. Food and Drug Administration (FDA) for OTREXUP™ for the treatment of RA,

Psoriasis and JRA.

• Initiated a clinical study evaluating testosterone enanthate administered weekly by subcutaneous injection and

dosed the first testosterone deficient adult males using the VIBEX® Quick Shot™ auto injector device. Enrolment

was completed 11/12/13, audited results due in late February.

BUSINESS DEVELOPMENT

• Entered into an exclusive U.S. collaboration agreement with LEO Pharma for OTREXUP™ in Dermatology.

CORPORATE

• Elected Robert P Roche Jr. to the Board of Directors. Mr. Roche brings to Antares extensive commercial and

product launch experience.

• Appointed Dr. Bruce Freundlich as Senior Vice President, Medical. Dr. Freundlich’s experience both in industry and

academia as a practicing and highly regarded rheumatologist will be valuable as we commercialize OTREXUP™.

• Appointed David H. Bergstrom Ph.D. Senior Vice President Pharmaceutical Development. Dr. Bergstrom has

worked on multiple FDA approved products including 505B2 drug/device combination programs.

• Finalizing OTREXUP™ launch plan – Supply Chain, Reimbursement, Sales Force Training, and Launch Meeting all

in place.

• Ended the quarter with $70.0 million in cash and investments and no debt.

4

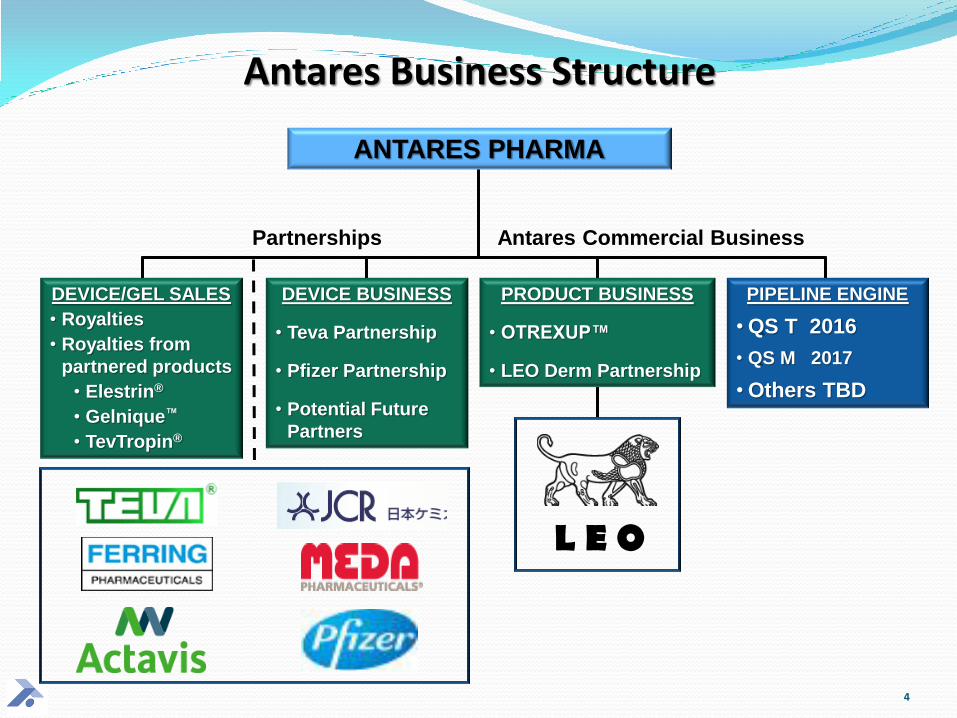

ANTARES PHARMA

DEVICE/GEL SALES

• Royalties

• Royalties from

partnered products

• Elestrin®

• Gelnique™

• TevTropin®

DEVICE BUSINESS

• Teva Partnership

• Pfizer Partnership

• Potential Future

Partners

PRODUCT BUSINESS

• OTREXUP™

• LEO Derm Partnership

PIPELINE ENGINE

• QS T 2016

• QS M 2017

• Others TBD

Antares Business Structure

Partnerships Antares Commercial Business

L E O

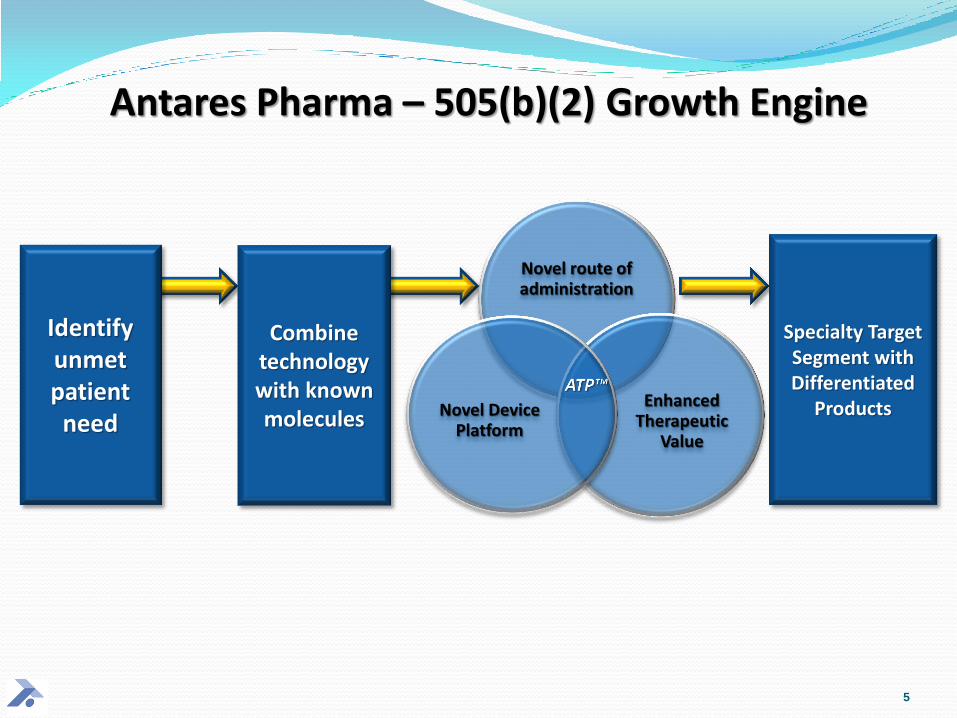

Antares Pharma – 505(b)(2) Growth Engine

Novel route of administration

Enhanced Therapeutic

Value

Novel Device Platform

Identify unmet patient

need

Combine technology with known molecules

Specialty Target Segment with Differentiated

Products

5

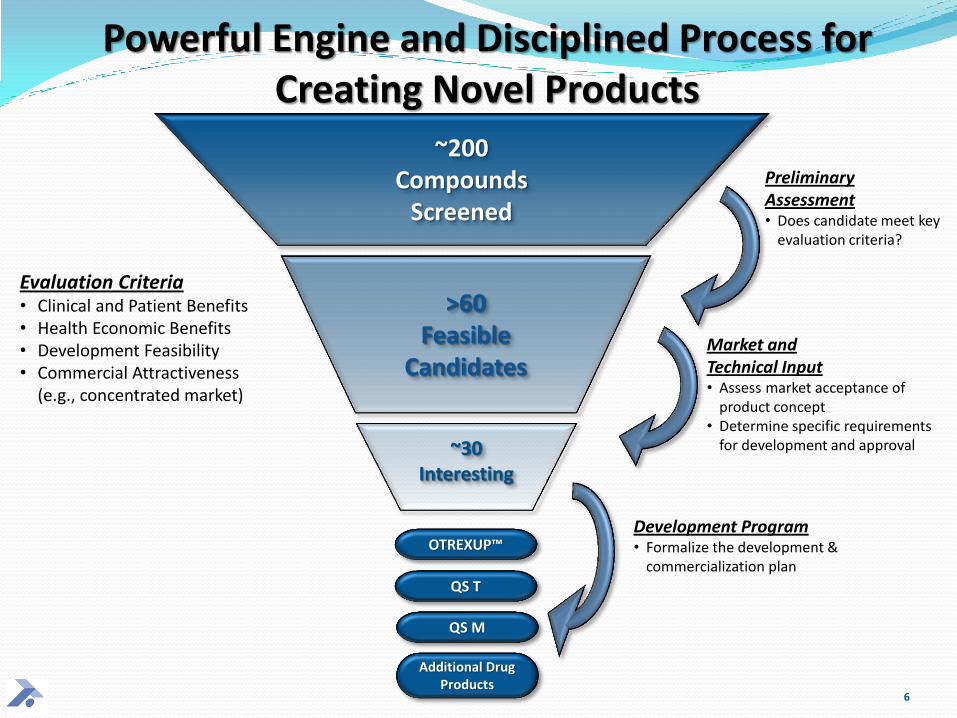

Powerful Engine and Disciplined Process for Creating Novel Products

~200 Compounds

Screened

>60 Feasible

Candidates

OTREXUP™

~30 Interesting

Evaluation Criteria • Clinical and Patient Benefits • Health Economic Benefits • Development Feasibility • Commercial Attractiveness

(e.g., concentrated market)

Preliminary Assessment • Does candidate meet key

evaluation criteria?

Market and Technical Input • Assess market acceptance of

product concept • Determine specific requirements

for development and approval

Development Program • Formalize the development &

commercialization plan

QS T

QS M

Additional Drug Products

6

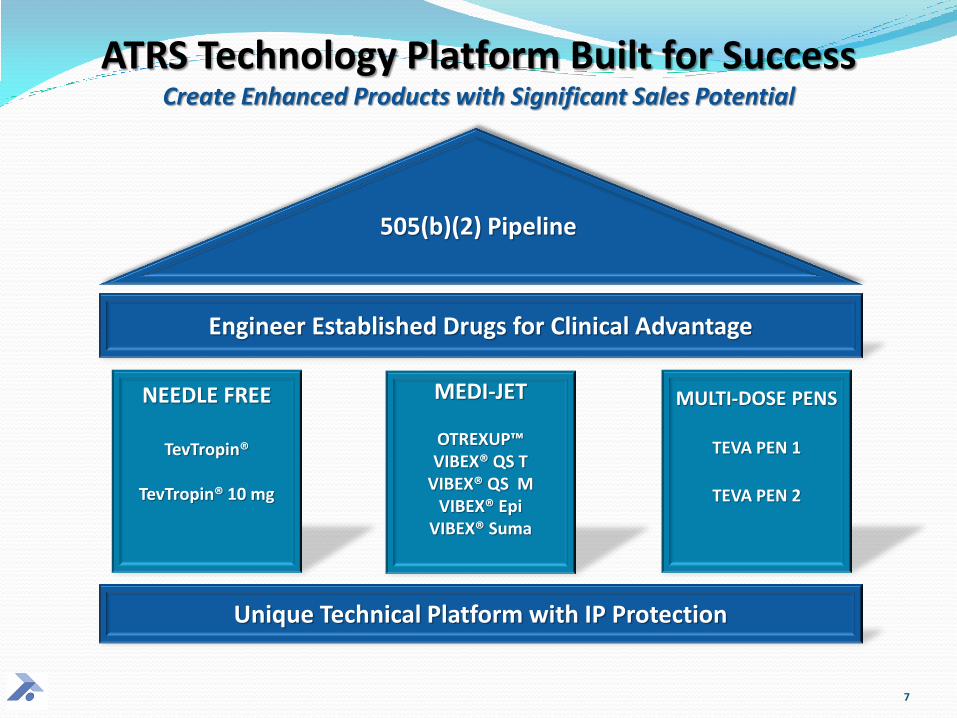

ATRS Technology Platform Built for Success Create Enhanced Products with Significant Sales Potential

Engineer Established Drugs for Clinical Advantage

Unique Technical Platform with IP Protection

NEEDLE FREE

TevTropin®

TevTropin® 10 mg

MULTI-DOSE PENS

TEVA PEN 1

TEVA PEN 2

MEDI-JET

OTREXUP™ VIBEX® QS T

VIBEX® QS M VIBEX® Epi

VIBEX® Suma

505(b)(2) Pipeline

7

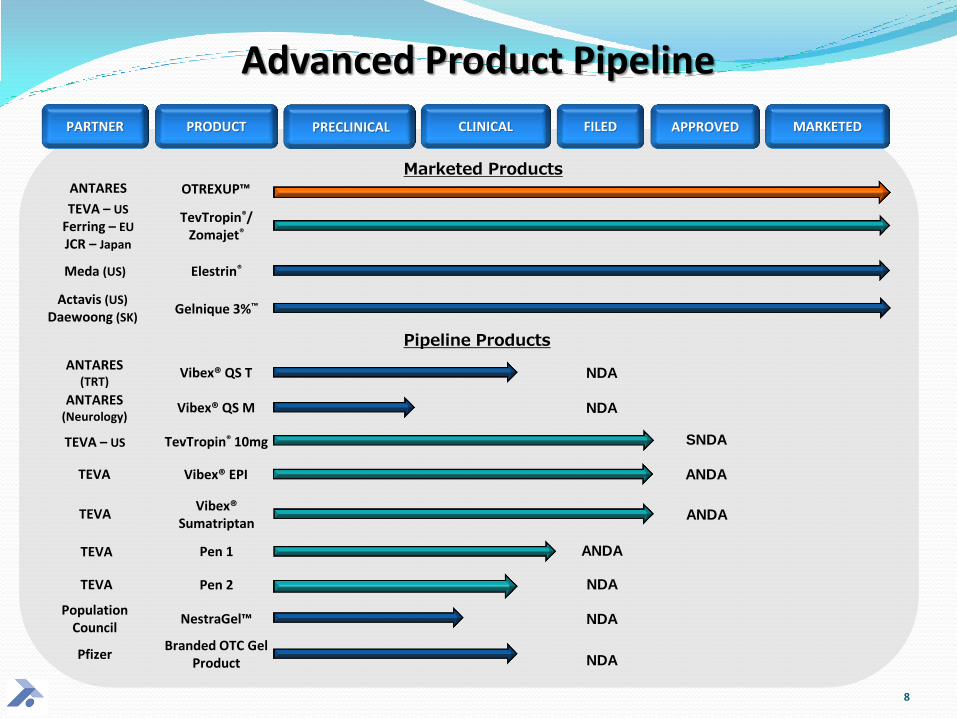

Advanced Product Pipeline

PRODUCT PRECLINICAL CLINICAL FILED MARKETED PARTNER APPROVED

TEVA – US

Ferring – EU

JCR – Japan

TevTropin®/ Zomajet®

Meda (US) Elestrin®

Actavis (US)

Daewoong (SK) Gelnique 3%™

TEVA Vibex® EPI ANDA

TEVA Vibex®

Sumatriptan ANDA

TEVA Pen 1 ANDA

ANTARES OTREXUP™

TEVA Pen 2 NDA

Population Council

NestraGel™ NDA

Pfizer Branded OTC Gel

Product NDA

ANTARES (TRT)

Vibex® QS T NDA

TevTropin® 10mg TEVA – US SNDA

ANTARES (Neurology)

Vibex® QS M NDA

Marketed Products

Pipeline Products

8

9

A Compelling Opportunity

First and only FDA approved SC MTX product for

self administration now available to patients

Single use, once weekly disposable device

Dosages: 10, 15, 20 and 25mg

Oral MTX may not always provide an adequate response due to lack of efficacy or poor tolerability and has GI absorption limitations

OTREXUP™ (SC MTX) delivers greater bioavailability than oral MTX – systemic exposure of MTX from OTREXUP™ at all doses (10, 15, 20, and 25mg) was higher than that of oral MTX

Convenience – easy to use even for RA patients with moderate to severe hand impairment

Safety – avoid dosing errors and inadvertent exposure to cytotoxic agent through accidental needle sticks

OTREXUP™ addresses a large and growing RA and Psoriasis market

Switching to OTREXUP™ may extend the use of MTX as well as potentially reduce overall cost of the RA treatment continuum

Seven Orange Book listed patents with coverage ranging from 2019 - 2030

10

OTREXUP™ Overview

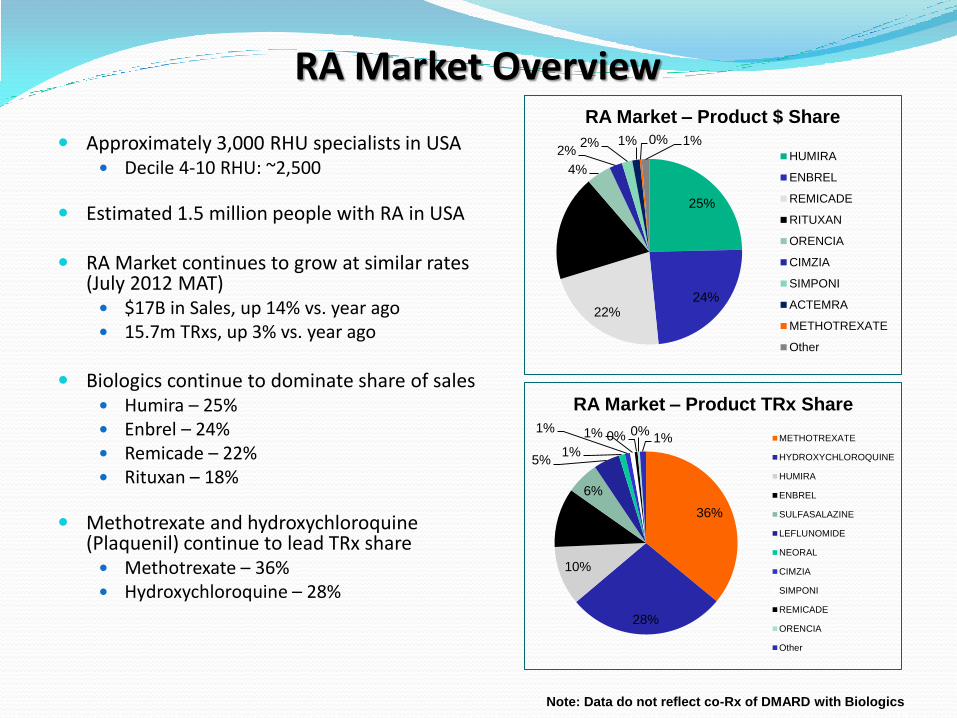

RA Market Overview

Approximately 3,000 RHU specialists in USA Decile 4-10 RHU: ~2,500

Estimated 1.5 million people with RA in USA

RA Market continues to grow at similar rates (July 2012 MAT) $17B in Sales, up 14% vs. year ago 15.7m TRxs, up 3% vs. year ago

Biologics continue to dominate share of sales Humira – 25% Enbrel – 24% Remicade – 22% Rituxan – 18%

Methotrexate and hydroxychloroquine (Plaquenil) continue to lead TRx share Methotrexate – 36% Hydroxychloroquine – 28%

25%

24% 22%

18%

4%

2% 2% 1% 0% 1%

RA Market – Product $ Share

HUMIRA

ENBREL

REMICADE

RITUXAN

ORENCIA

CIMZIA

SIMPONI

ACTEMRA

METHOTREXATE

Other

36%

28%

10%

10%

6%

5% 1%

1% 1% 0% 0% 1%

RA Market – Product TRx Share

METHOTREXATE

HYDROXYCHLOROQUINE

HUMIRA

ENBREL

SULFASALAZINE

LEFLUNOMIDE

NEORAL

CIMZIA

SIMPONI

REMICADE

ORENCIA

Other

11 Note: Data do not reflect co-Rx of DMARD with Biologics

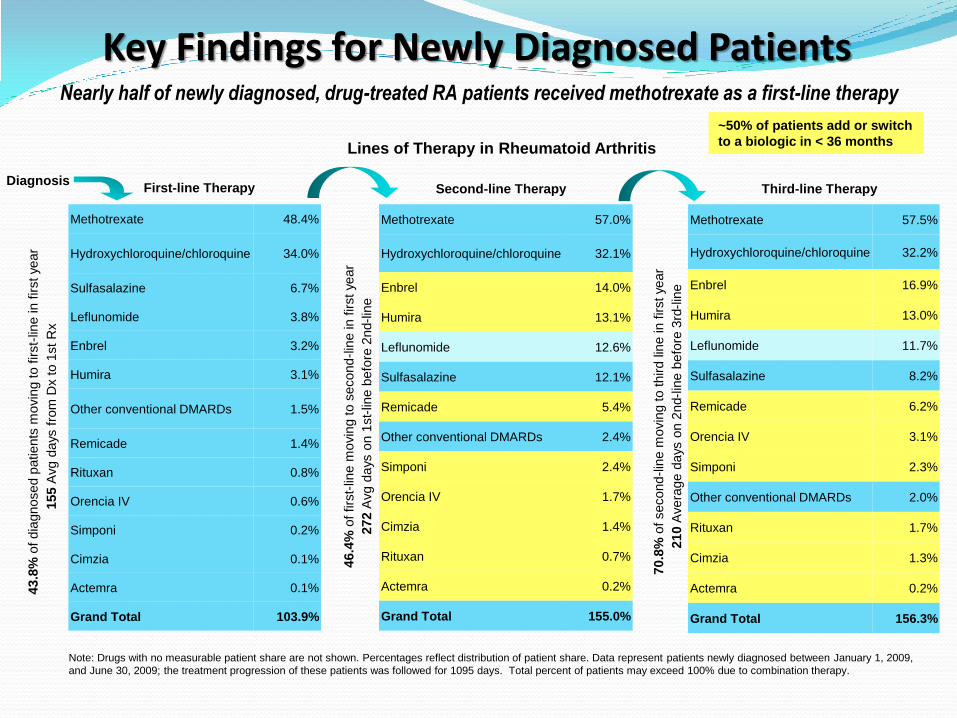

First-line Therapy Second-line Therapy Third-line Therapy Diagnosis

Key Findings for Newly Diagnosed Patients

Lines of Therapy in Rheumatoid Arthritis

43.8

% o

f dia

gnosed p

atients

movin

g to f

irst-

line in f

irst year

155 A

vg d

ays f

rom

Dx to 1

st R

x

46.4

% o

f firs

t-lin

e m

ovin

g to s

econd

-lin

e in f

irst ye

ar

27

2 A

vg d

ays o

n 1

st-

line b

efo

re 2

nd-l

ine

70.8

% o

f second

-lin

e m

ovin

g to third lin

e in f

irst year

21

0 A

vera

ge d

ays o

n 2

nd-l

ine b

efo

re 3

rd-l

ine

Methotrexate 48.4%

Hydroxychloroquine/chloroquine 34.0%

Sulfasalazine 6.7%

Leflunomide 3.8%

Enbrel 3.2%

Humira 3.1%

Other conventional DMARDs 1.5%

Remicade 1.4%

Rituxan 0.8%

Orencia IV 0.6%

Simponi 0.2%

Cimzia 0.1%

Actemra 0.1%

Grand Total 103.9%

Methotrexate 57.0%

Hydroxychloroquine/chloroquine 32.1%

Enbrel 14.0%

Humira 13.1%

Leflunomide 12.6%

Sulfasalazine 12.1%

Remicade 5.4%

Other conventional DMARDs 2.4%

Simponi 2.4%

Orencia IV 1.7%

Cimzia 1.4%

Rituxan 0.7%

Actemra 0.2%

Grand Total 155.0%

Methotrexate 57.5%

Hydroxychloroquine/chloroquine 32.2%

Enbrel 16.9%

Humira 13.0%

Leflunomide 11.7%

Sulfasalazine 8.2%

Remicade 6.2%

Orencia IV 3.1%

Simponi 2.3%

Other conventional DMARDs 2.0%

Rituxan 1.7%

Cimzia 1.3%

Actemra 0.2%

Grand Total 156.3%

Nearly half of newly diagnosed, drug-treated RA patients received methotrexate as a first-line therapy

Note: Drugs with no measurable patient share are not shown. Percentages reflect distribution of patient share. Data represent patients newly diagnosed between January 1, 2009,

and June 30, 2009; the treatment progression of these patients was followed for 1095 days. Total percent of patients may exceed 100% due to combination therapy.

~50% of patients add or switch

to a biologic in < 36 months

OTREXUP™ In Dermatology – LEO Pharma

Exclusive U.S. collaboration agreement with LEO Pharma for OTREXUP™ in dermatology

LEO is a global leader in dermatology and topical treatments for psoriasis

Antares to receive up to $20 million in milestone payments including an upfront payment of $5 million

Antares will record all dermatology related product revenues

LEO will be responsible for promotion and marketing activities in dermatology supported by a sales force of 75 representatives

LEO has proven capabilities within life-cycle management focusing on innovative patient solutions in dermatology

13

OTREXUP™Polyarticular Juvenile Arthritis

Polyarticular Juvenile Arthritis refers to a form of juvenile arthritis that causes joint inflammation and stiffness for more than six weeks in children under 16

About 30% of all children with juvenile arthritis have polyarticular disease and girls are two times more likely to have the disease than boys

Children with polyarticular juvenile arthritis are unlikely to outgrow the disease, therefore initial drug therapy should be aggressive in order to control the inflammatory process and relieve symptoms as quickly as possible

It is rare for NSAIDS alone to control the inflammatory process of polyarticular disease – methotrexate has been recognized as the standard therapy for children with this form of juvenile arthritis

OTREXUP™ label includes Juvenile Indication – 80% of prescriptions in this area written by same physicians as for Adult RA

14

OTREXUP™ Launch Plan

OTREXUP™ NDA approved October 14 – launched!

OTREXUP™ Commercial Team – Broad Rheumatology expertise with over

100 years of combined commercial experience

DMs, Sales Representatives and NAMs possess extensive experience in

marketing rheumatoid arthritis drugs and will be Quintiles employees

dedicated solely to the marketing of OTREXUP™

Six MSL’s providing value proposition to Key Opinion Leaders in RA

Feedback from AMCP validates pricing strategy – $548 per Rx (4 weeks)

Discussions with pharmacy and medical directors suggest initial tier 3

access with several plans already mentioning the possibility of tier 2 access

Leo will launch to dermatologists in February with 75 Representatives

bringing total number of OTREXUP™ sales personnel to over 100

15

OTREXUP™ Launch Success Factors

Enthusiasm by Rheumatologists and Dermatologists

Market Access Through Managed Care

Understanding the value proposition of OTREXUP™

ATRS Managed Markets Group working since June

Initial Tier 3 coverage with potential for Tier 2

coverage

Risk Mitigation With LEO Partnership

“First Impressions” Program educating Physicians,

Nurses and Patients

16

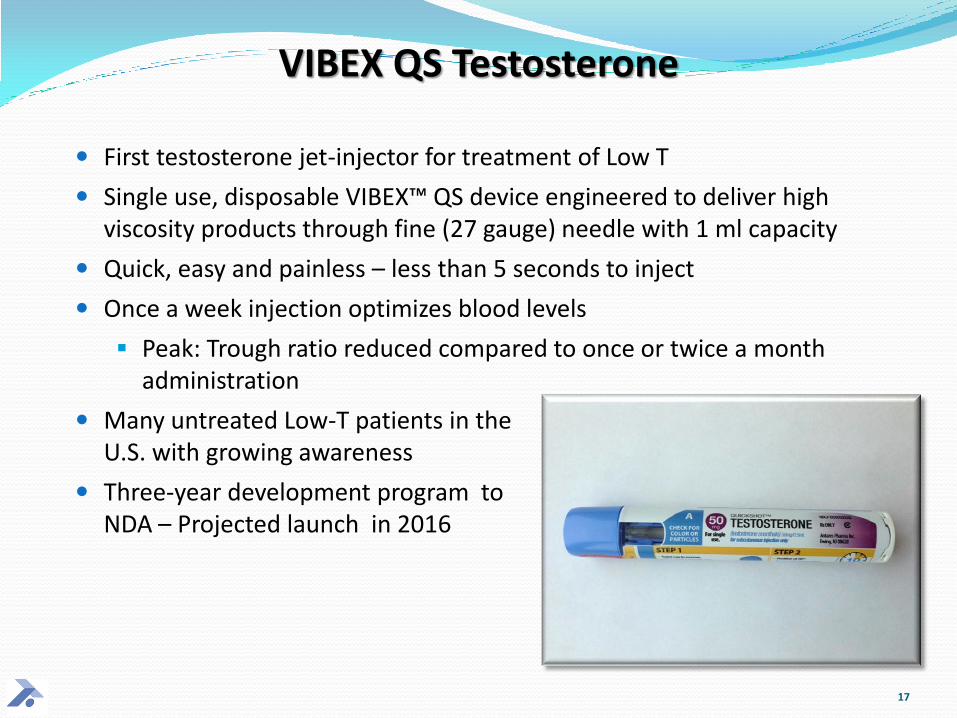

VIBEX QS Testosterone

First testosterone jet-injector for treatment of Low T

Single use, disposable VIBEX™ QS device engineered to deliver high viscosity products through fine (27 gauge) needle with 1 ml capacity

Quick, easy and painless – less than 5 seconds to inject

Once a week injection optimizes blood levels

Peak: Trough ratio reduced compared to once or twice a month administration

Many untreated Low-T patients in the U.S. with growing awareness

Three-year development program to NDA – Projected launch in 2016

17

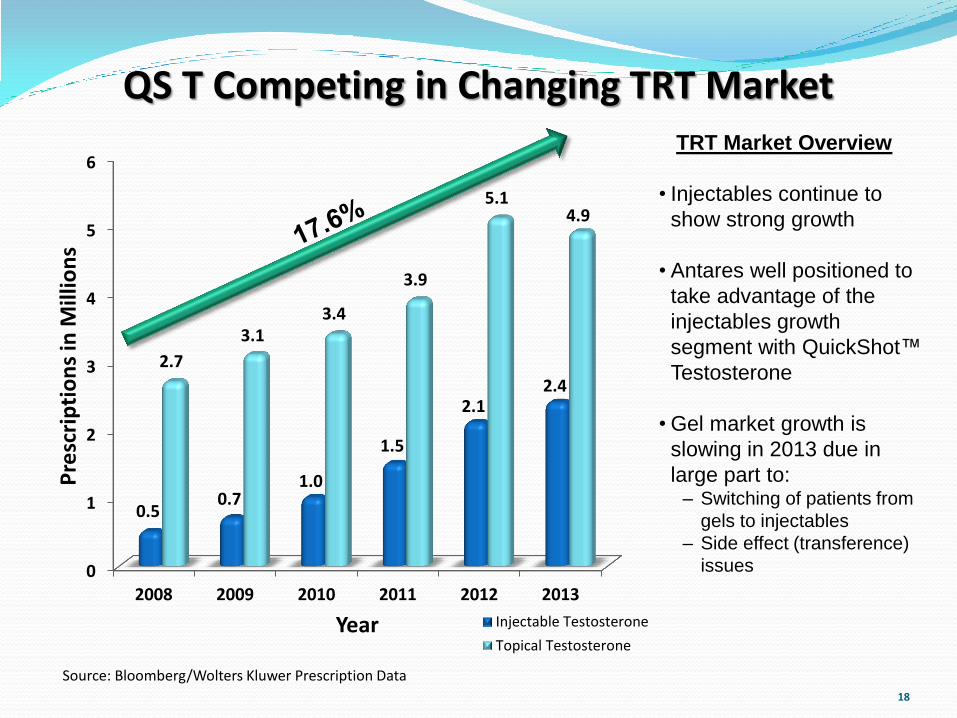

QS T Competing in Changing TRT Market

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013

0.5 0.7

1.0

1.5

2.1 2.4

2.7

3.1 3.4

3.9

5.1 4.9

Pre

scri

pti

on

s in

Mill

ion

s

Year Injectable Testosterone

Topical Testosterone

Source: Bloomberg/Wolters Kluwer Prescription Data

18

TRT Market Overview

• Injectables continue to

show strong growth

• Antares well positioned to

take advantage of the

injectables growth

segment with QuickShot™

Testosterone

• Gel market growth is

slowing in 2013 due in

large part to: – Switching of patients from

gels to injectables

– Side effect (transference)

issues

VIBEX QS T – Testosterone Replacement Therapy (TRT)

U.S. sales of testosterone replacement therapies exceeded $2.7 billion* in 2013 – 7.3 million Rx’s, growing at ~18% annually and projected to exceed $5 Billion in 2017**

Studies have shown that gel patients do not achieve adequate absorption or therapeutic response, injection patients bear the cost and inconvenience of in-office deep intramuscular injections every 2 to 4 weeks

Physicians surveyed believe weekly self-injection will improve patient compliance and deliver optimized serum testosterone levels

Self contained Auto-injector avoids the transference issues seen with Gels (Black Box)

Pre-IND meeting held with FDA on 12/5/12 – clinical path forward agreed upon with agency

First patients dosed 9/16/13 – 2015 NDA filing on track

Expected to go to market in 2016

19 Sources: *Bloomberg **Global Industry Analysts

Financial Overview

Cash Position

As of September 30th 2013 cash and investments of $70 million

Growing Revenue Base

2008 total revenues $4.6 million

2009 total revenues $8.3 million (47% over 2008)

2010 total revenues $12.8 million (54% over 2009)

2011 total revenues $16.5 million (28% over 2010)

2012 total revenues $22.6 million (37% over 2011)

20

Priority Goals for Next 12-18 Months

OTREXUP™ partnership – Completed

OTREXUP™ launched in Q1 2014 for RA and Psoriasis (LEO)

• VIBEX™ QS T (testosterone) will complete clinical studies

• VIBEX™ QS M to begin clinical studies

• Teva programs – two multi-dose pen products filed

• TevTropin® 10 mg approval and launch

21

Antares Pharma, Inc. Princeton South Corporate Center

100 Princeton South, Suite 300 Ewing, NJ 08628 NASDAQ: ATRS

22